Today I wanted to tell you about a smartphone app called DreamLab. You can download this free to your smartphone or tablet, to add its computing power to a massive cancer research project. Versions are available for both Android and Apple iOS.

DreamLab was developed by Vodafone Australia and the Garvan Insitute of Medical Research. While your smartphone is charging (typically overnight; hence the name), the app automatically downloads genetic sequencing profiles provided by the Garvan Institute. This information is then processed using your smartphone’s CPU and sent back to the Institute to be used in cancer research.

There are currently two projects you can support. The first one, Project Decode, aims to decode breast, ovarian, prostate and pancreatic cancers. The second, which launched recently, is Project Genetic Profile. This aims to decode brain, lung, melanoma and sarcoma cancers.

As well as the project you wish to support, you can select how much mobile data (if any) the app uses every month. Personally I only use DreamLab with my wifi, so I have the monthly data allowance set to zero. You might, though, like to know that if VodaFone is your service provider, any data used for DreamLab processing is free of charge.

The app keeps track of how many hours of computing time you have donated to the project and the number of sequencing problems your device has solved. You can also see what proportion of the overall project has been completed. In the case of Project Decode – which I am supporting – the figure is currently 69 percent. So while the project is well past the half-way mark, there is still a fair way to go.

DreamLab is a distributed computing project, which relies on volunteers donating spare processing capacity on their computers and mobile devices to a specific cause. One of the best-known such projects is SETI (Search for Extra-Terrestrial Intelligence), which uses this method to search for extra-terrestrial life by analyzing radio waves emanating from space. You can read more about this and other distributed computing projects (including DreamLab) on this Wikipedia page.

Today I thought I would discuss the state pension. This is a subject that concerns everyone, but may be of particular interest to readers of this blog who are approaching retirement age.

Of course, many people have one or more workplace or private pensions. However, the state pension is still a very important component of most people’s income in later life.

And unlike many workplace/private pensions, it rises automatically every year at the rate of inflation or above (under the current triple lock guarantee). That makes it increasingly valuable as you get older.

In this article I’ll be revealing how to check how much state pension you are due and when. But I’ll start with a look at the various changes to the state pension in the last few years and how they affect anyone coming up to pensionable age now.

Speaking of which, let’s start with one of the biggest changes…

Your State Pension Age

It’s unlikely to have escaped your notice that the pension age is rising. At present men can access their state pension at 65 while women get it at around 64. The age for women is in transition at the moment as it rises to equalize with men in 2018.

By 2020, the pension age for both men and women will go up to 66. Between 2026 and 2028 it is due to rise again to 67, and under current government plans it will go up again to 68 in 2037.

You can check when exactly you can start to claim the state pension by entering your date of birth and gender at this government website.

The New Flat Rate Pension

This is the other major change to the state pension in recent years.

Prior to April 2016 everyone received a basic pension (currently £122.30 a week). This was (and still is) topped up by additional state pension elements (S2P and Serps) which you accrued during your working life.

Anyone retiring from April 2016 onwards now receives a ‘flat rate’ pension currently worth £159.55 a week. If, however, you ‘contracted out’ of S2P and Serps at some point in your working life, you may get less than this. The presumption is that your contracted-out pension will provide another source of income for you, so you don’t need (or qualify for) the full flat-rate pension.

A further complication is that the government doesn’t want people who accrued large state pension entitlements under the old scheme (basic pension plus S2P and SERPS) to miss out. So when you reach pension age your entitlement under both the old and new methods of calculation will be worked out and you will receive the larger of the two. That means some people could actually qualify for more than the new flat-rate pension (£159.55 currently). If this is the case, it will be shown separately as a ‘protected payment’ on your state pension statement.

Also, to get the maximum new flat-rate pension you need to have at least 35 years of qualifying National Insurance contributions at the full (non-contracted-out) rate. If you have less than that you will get a reduced pension; and if less than 10 years, nothing at all.

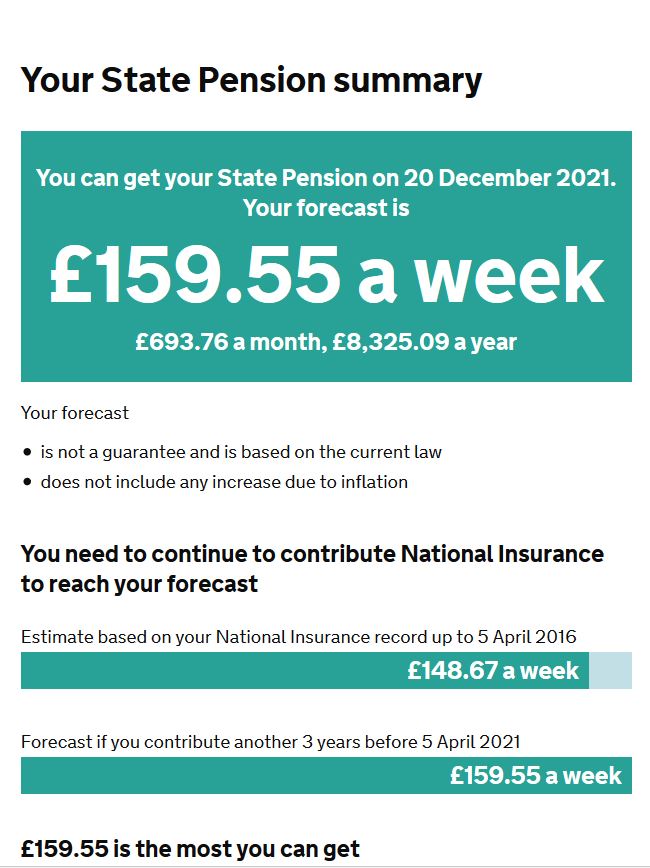

In some circumstances – which I’ll discuss shortly – you may be able to pay a lump sum to fill in gaps in your record. Even if you do have 35 years or more of contributions, though, it may not entitle you to a full pension. The government website (see below) tells me I have 37 years of contributions, but because I was contracted-out for some of these years and so paying a lower rate of National Insurance I still have to contribute for another three years to get the full flat-rate pension. Here’s a screen capture of my actual statement:

If you’re confused by all this, I’m not surprised. The rules are complicated and still being tweaked. So to avoid any nasty surprises it’s important to check what you are due to receive as well as when you are due to do so. There is now an official website where you can access all this information in one place.

Checking Your State Pension

Anyone aged 55 or over who has lived and worked in the UK for 10 years or more (even if they are not British citizens) can now visit https://www.gov.uk/check-state-pension to get an estimate of how much state pension they will receive when they retire.

Doing this is a bit more involved than just checking your start date on the pension age site mentioned earlier. You have to sign in with proof of identity, so allow a bit of time for this. If you already have an HMRC online tax account, the good news is you can use this to log in.

Once you’ve done so, you will see a forecast of how much state pension you will get once you’re eligible to start receiving it. This is based on current figures, so if you won’t reach retirement age for a few years yet, it will of course have risen by that time.

Boosting Your State Pension

If you’re disappointed by the amount forecast, one thing you can do to boost your state pension is defer taking it. Under the new rules you will receive an extra 1% for every 9 weeks you put off claiming.

Obviously, to benefit from this overall you should be in good health. For women especially, as their life expectancy tends to be a few years longer than men, deferring your pension (if you can afford to do so) could well be a profitable option. In a way this is a form of investment, underwritten by the government.

No special action is required to defer taking your pension. You just delay claiming and it will be assumed that you wish to defer it.

Another thing you may be able to do to boost your state pension is buy extra voluntary contributions to fill in any gaps in your record. Buying a year of extra contributions (normally Class 3 National Insurance) costs around £733 and will boost your pension by around £230 or £4600 over a 20-year retirement. This can be well worth doing if, for example, you were contracted out for several years.

There are some restrictions, however. In particular, as a general rule it must be done within six years of the end of the tax year concerned. So if the gaps in your record go back further than this, it’s unlikely you will be allowed to make up the whole shortfall in this way.

There’s also the question whether paying voluntary contributions to fill gaps in your record will be cost-effective for you. There is no easy way of calculating this, and I highly recommend getting advice from an independent financial adviser specializing in pensions if you are thinking of going down this route. It’s also a good idea to contact the government’s Future Pension Centre to find out what your options are.

Finally , it should be said that while the state pension provides a baseline income (currently equivalent to around £8,300 a year), on its own it won’t stretch to many (or any) luxuries. Most people will have private or workplace pensions and perhaps other investments as well, and this will be very important if you hope to enjoy your retirement rather than merely survive it. I will look at these in more detail in future posts.

As ever, if you have any comments or questions on this post, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

Today I have a guest post for you from my fellow money blogger Lewys Lew, who blogs at The Frugal Student.

Lewys has a particular interest in dividend investment. As I know this is a subject of interest to many readers of this blog, I asked him to write about it here.

Over to Lewys, then…

I watched the Conservative party conference in despair!

Not because I’m a Conservative but because once again the vultures circle Theresa May and Brexit seems to be going backwards.

Not that I voted to leave, but this constant uncertainty unsettles me and the market.

To add a cherry on top of bad news, productivity in the UK has begun shrinking and we’re no better off than we were in 2007.

What this means for you and me is that the economy continues to struggle and along with that interest rates remain dire.

Sure, for those of us who save a few pounds a month there are some decent bank accounts out there that offer 2%+ interest but these usually come straddled with a set of conditions and maximum deposits.

For those with large sums lying dormant in bank accounts the deals on offer are pitiful. With the current rate of inflation, your cash-pile may even be worth less.

In this post, I’m going to share with you how you could earn 5% in interest yearly.

Before we begin, there are a few things to note:

If you use this method your money is at risk.

To reduce risk, you should be prepared to lock your money up for 5+ years.

This method may not be suitable if you’ll need to use this money in an emergency

(remember to always keep six months’ worth of expenditure in an easy-access account)

Here’s some key terminology before we start:

Dividend = Money a company pays to you as a reward for being a share-holder.

Dividend Yield/Yield = A dividend as a percentage of a current share price, as so:

Dividend per share/Price per share.

Right, let’s get stuck in!

Dividend investing is a vast field. Myself, I’m a dividend growth investor. At 24 years old, I seek to buy stakes in companies who are growing their dividend at a rapid pace. Over time these types of stocks often increase their dividends at higher rates than companies who already pay a dividend at a higher yield.

But for those who maybe don’t have the benefit of a 30-year investment horizon, dividend yield investing may be a better choice for you. Frankly, getting just 1% of invested monies back as a dividend each year isn’t going to satisfy you if you’re close to retirement or retired.

The good news is that there’s an alternative dividend investing method that could see you getting 5% of your invested monies back each year, along with some capital gains along the way.

I’ll illustrate dividend yield investing with this example…

National Grid is a very boring, steadily performing utility company. It owns and manages the UK’s grid structure along with some bits in the United States and in return is allowed to make a modest profit from its operations. It’s a monopoly, meaning that we don’t need to worry about competition or anything of that sort.

As we can see from the graphic below (from the Hargeaves Lansdown website), National Grid pays a 5.15% dividend. This effectively means that for every £100 you invest, you’ll get £5.15 back every year.

The good news is that National Grid buys back its own shares, pushing up the capital value of your holding and reducing the possibility of capital loss over the long term (5+ years).

Dividend investing can be especially powerful if you use your dividends to buy more shares.

£1,000 worth of National Grid shares would let you buy around 5 additional shares with the dividend after one year. Compound this over the years and you could really start building a decent stream of dividend income.

Pros and Cons of High Yield Investing

Cons

When dividend yields go over 6%, this can be an indication that the stock is risky, as investors are fleeing the stock, thus reducing the share price and increasing the dividend yield (as this is relative to the price).

Stock prices could fall below your original purchase price and dividend income combined, leading to a net loss.

A large capital deposit is needed to make this method really effective; small amounts won’t really go a long way.

You have to pay to buy/sell stocks.

Identifying safe higher yield stocks can be difficult and time-consuming.

Pros

A 5+% dividend yield smashes any bank account out there.

The combination of steady stock price rises and dividend income can really boost your savings.

Large and ‘boring’ companies such as National Grid are very resilient and it’s relatively unlikely that you’d find yourself at a capital loss if you held such stocks over five years.

Remember that other investments can carry large risks and costs too. One such example is buying a rental property, where bad tenants, maintenance costs and the hassle can eat away at returns. By investing in a large company you won’t need to do anything else. Just sit back and soak up the dividends!

How Do I Buy Shares?

If you’re interested in building yourself a dividend income later on in life (40+) then I would certainly recommend chasing higher yields from boring large companies such as National Grid.

In order to buy shares you’ll have to sign up with a broker.

The most popular in the UK is Hargreaves Lansdown, but this platform charges a management fee of 0.45% annually, in the case of National Grid lowering your net income from 5.15% to 4.7%. They also charge £11.95 for share repurchases and 1% for dividend reinvestment.

To really reap the benefits of this strategy, I’d recommend signing up with online brokers De Giro, who only charge £1.75 a trade with no management fee.

If you like the idea of dividend yield investing but the risk is a little too high for you, I recommend you take a look at my Nutmeg Investment Review for a platform that manages your portfolio for you.

Many thanks to Lewys (pictured, right) for an eye-opening article.

Personally I have tended to stick with self-selected funds and ready-made portfolios (including Nutmeg) for my core investments, but I can certainly see the attraction of high-yield share dividend investing for part of my portfolio – especially as (being semi-retired) I am now looking to generate an income from my savings.

Another thing in favour of dividend yield investing is that there is a generous annual tax-free dividend allowance (which most people don’t make use of). Currently you can earn up to £5000 a year in dividends before any tax is due. The government has threatened to reduce this to £2000, but even if that happens the allowance is still well worth taking advantage of, as it comes in addition to other tax-free saving and investment opportunities such as ISAs.

If you have any comments or questions about this post, as always, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

A quickie today to let you know about a special promotion that is currently being run by the online payment platform Circle.

Anyone is welcome to enter their Education or Every Nation promo, whether or not they have an account with Circle already (if you don’t, you will need to sign up for free).

Everyone entering goes into a draw for a prize of a round-the-world trip or getting their university fees paid off – your choice. Luckily for me, I went to uni in the days students got grants rather than loans, so I asked for the world trip 🙂

But in addition, you get a guaranteed mystery cash prize of anywhere from 50p to £50 credited to your account. I got £0.61, but a colleague received £2.67. You can also introduce friends and relatives to this promotion (once you have entered yourself). For each one who signs up via your referral link – which is provided once you enter – you will get an extra prize draw entry and another mystery cash prize.

If you are a member of Prolific Academic – one of my favourite sideline earning opportunities – you may well have a Circle account already. It is a bit like PayPal, except the fees are lower!

Finally, please note that this is a limited-term promotion. I will aim to update this post as soon I know that it has closed, but to avoid disappointment I recommend entering as soon as possible.

Today I want to share a sideline-earning opportunity that may be of interest if you have a bit of time available during the week or at weekends.

A company called Viewber is recruiting people to conduct property viewings on behalf of local estate agents who don’t have any staff free to do it themselves.

As a Viewber (the name is also used by the company to describe its viewing agents) you will be asked to attend a property at a specified date and time to show a potential buyer or tenant round.

You will therefore need to obtain the key beforehand (or get it from a key safe), welcome viewers when they arrive, and let them in. You then follow at a discreet distance while they look round, answer any questions they may have (or refer them to the estate agent), show them out, and secure the property again.

You are also asked to report in writing to the estate agent afterwards with any information you have gleaned about the viewers that might be useful to them, e.g. if they are cash buyers or have looked at a lot of other properties already.

Who Can Do It?

In principle anyone can be a Viewber. You need to be reasonably smart and professional looking (as with estate agents generally). And, of course, you will need a polite and friendly manner and good communication skills.

The job is popular with retired and semi-retired individuals (like many readers of this blog) who are looking to supplement their income. It also attracts quite a few people who are ex-military or police, as well as former teachers, estate agents and other professionals. But any experience working with the public will be relevant and should assist your application.

Having your own transport is clearly desirable (though you can specify how far from home you are willing to travel). You will also need a mobile phone to contact the estate agents when required.

Although this asks about experience and qualifications in the property field, this is definitely not a requirement (I had neither but was accepted without quibble).

You are also required to upload a photograph of yourself so that the company can see you don’t look like an escaped convict.

You can expect to receive a reply to your application within a few days. Mine came by email. I was accepted on the basis of my application and photo, without any need for an interview.

You will then have to go through the company’s vetting procedure. This involves providing a copy of your driving licence or passport and a recent utility bill or bank statement showing your name and address. You will also need to provide bank details, so they can pay you.

Once you’re fully approved, you will be able to log in to your personal dashboard on the Viewber website. Here you will be able to view a range of information, including details of any jobs you have completed so far. You can also enter on a calendar any periods you are unavailable (e.g. on holiday).

Then it’s simply a matter of waiting for invitations to arrive by email. You aren’t under any obligation to accept these if you’re otherwise engaged – but if you do want to accept, you will need to do so quickly, before the job gets taken by someone else.

What It Pays

The basic pay is £20 for a single viewing of up to 30 minutes. Additionally if you have to travel by car there is a mileage allowance of 25p a mile, or £4 travel allowance in London.

If you are conducting multiple viewings at the same time or an ‘open house’ you will be paid more, up to £135 for a full day.

Additional fees are payable for taking (non-professional) photos of the property if requested and other services such as performing a property inspection.

Top Tips

Here are a few more tips on making the most of this opportunity.

Both viewers and agents can rate Viewbers, and this can affect the type and number of opportunities you are offered. It’s important to provide the best service you possibly can, therefore.

You will be sent information about the property concerned beforehand, so read this carefully and make a note of any particular things a viewer might want to know about.

There is also an online manual for Viewbers, so again read this carefully. It’s only a few pages long but covers most of the things you need to be aware of.

Greet viewers by name and be prepared to answer any general questions they may have, e.g. about the area if you’re familiar with it. For more detailed questions about the property, though, refer them to the estate agent. If possible, phone the agent there and then on the number provided.

Viewber is still new, which means there are currently more opportunities in some areas than in others. However, that does mean now is a great time to apply and start gaining experience, with the prospect of more work in the coming months as the service gains traction among estate agents.

In my view, if you want an interesting and varied sideline income stream – and enjoy meeting people and looking round houses – applying to be a Viewber has a lot to recommend it!

Many thanks to Lewys (pictured, right) for an eye-opening article.

Many thanks to Lewys (pictured, right) for an eye-opening article.