Long-time readers of Pounds and Sense will know that at one time I made a steady sideline income from matched betting.

Unfortunately the pandemic led to almost all sporting events stopping. And though they have now returned, for reasons discussed in this blog post, matched betting is no longer as lucrative as it once was. If you’ve never done it before, however, I do still recommend it as a risk-free way to generate some extra (tax-free) cash.

As any matched bettor will tell you, an occupational hazard with matched betting is being ‘gubbed’. This happens when the bookies get fed up with you taking advantage of their offers (which is basically what matched betting is) and bar you from taking part in any from then on. Once you have been gubbed by multiple bookmakers, clearly the returns you can make from matched betting diminish rapidly.

So what can you do? Enter my friends Gavin and Andy, who run a service/website called Gubbed. Some of you may remember Gavin’s earlier venture, which enabled anyone to profit from matched betting with no financial outlay and no need to place any bets themselves. Members received a share of the profits generated every month. Several PAS readers – including my sister Annie – signed up for this and made good money from it. Nobody lost any money, for the good reason that nobody was ever asked to pay anything. That service only closed because of the growing difficulty of making matched betting sufficiently profitable.

As the name indicates, the new Gubbed service is aimed especially at former matched bettors who have been gubbed (though anyone is welcome to sign up including those who have never done any betting before). Gubbed is emphatically not just a matched betting service. Andy and Gavin are sports betting specialists, as well as being expert programmers. They have developed AI bots and algorithms that – while they might not win every time – over a period deliver steady profits from betting. This video explains in a bit more detail how it works:

As you will gather, nobody is ever asked to pay any money to Gubbed. Even your starting capital is supplied by Gubbed themselves from syndicate winnings.

There is a certain amount of work initially uploading details of your betting accounts and/or creating new ones. And you will also need to set up a new, dedicated bank account solely for betting use. But once all that is done, you can sit back and let the bots do their thing. All the support you need is available any time from the dedicated Gubbed team.

Obviously in time the bookies WILL ban you or restrict your stakes to such an extent that no more worthwhile profits can be made. But in the time leading up to that, Gubbed guarantee that you will receive a minimum of £1,000 in winnings. To date, the highest amount paid out to a Gubbed member s £6,366.25 (to a lady named Sophie, as it happens).

One other thing I should mention is that to take part in the Gubbed programme, you need to be honest and trustworthy. That is because all the risk with the programme is taken by Gubbed themselves. They provide the capital needed to run the betting bots and in theory you could withdraw this yourself as it is (nominally anyway) your money. Of course, if you do this you will be immediately removed from the programme and forfeit the potentially much larger profits to be made during your membership. In addition, Gavin and Andy require all new members to take part in a short video call with them to assure themselves you are genuine. Of course, this is also your opportunity to ask them any questions face to face.

I have been working with Gavin and Andy for several years now and am happy to vouch that they are honest and trustworthy (Andy is a long-time PAS reader and actually made contact with Gavin after reading about his earlier betting service on the blog). I also made money from their previous service (as did my sister). If you’re willing to put in a little bit of work initially, you should pocket a tidy tax-free sum from Gubbed – though obviously I can’t guarantee that your payout will be as big as Sophie’s!

Please do check out the Gubbed website for more info. You can also contact the small and friendly Gubbed team via this web page.

Good luck, and if you join please do return here in due course and let me know how much you made!

Disclosure: I am an affiliate for Gubbed and will receive a referral fee if you sign up (free) with them after clicking through one of the links in this article. This will not affect in any way the service you receive or the returns generated by the programme. Please be aware that this is a collaborative no-risk money-making opportunity and you will never be asked for any money yourself. It is not gambling, and neither I nor the team at Gubbed advocate gambling in any shape or form.

If you enjoyed this post, please link to it on your own blog or social media:

I was recently offered the chance to review the Simba Hybrid Mattress Topper (see cover photo). This is a premium mattress topper from the well-known Simba sleep brand.

I must admit, incidentally, I hadn’t realised the variety of sleep products Simba offer. I knew about their mattresses, of course, but wasn’t aware they also sell quilts, pillows, mattress toppers, and so on.

I currently sleep on a Slumberland king-sized mattress which – despite being barely three years old – is starting to sag. My sleep quality had deteriorated and I was waking up with an aching back and hips. Not good at all 🙁 So when I got the opportunity to test out Simba’s hybrid mattress topper, naturally I leapt at it.

I have tried mattress toppers before, and in fact got a cheap one from Amazon prior to receiving the Simba product. It helped a little but clearly wasn’t going to be the solution for me.

The Simba hybrid mattress topper takes sleep comfort to a whole new level. For starters, it’s deeper and heavier than my previous mattress topper. It came rolled up in a (very) large cardboard box. I wrestled it upstairs and opened it without any help (nobody else being around at the time) but ideally I’d say this is a two-person job.

The mattress topper comes tightly wrapped in a clear plastic bag. Once I removed it from this, it lay flat on the bed without curling. Unlike some sleep products I have ordered in the past, you don’t have to wait for it to expand to its full depth.

From the first night onward I was hugely impressed with the Simba hybrid mattress topper. It is no exaggeration to say that it felt as though I was sleeping on a brand new mattress. It is smooth, cool and comfortable to lie on and (for me anyway) offers just the right medium-to-firm level of support. I am sleeping deeper and longer before waking, and the aches and pains in my back and hips are a thing of the past.

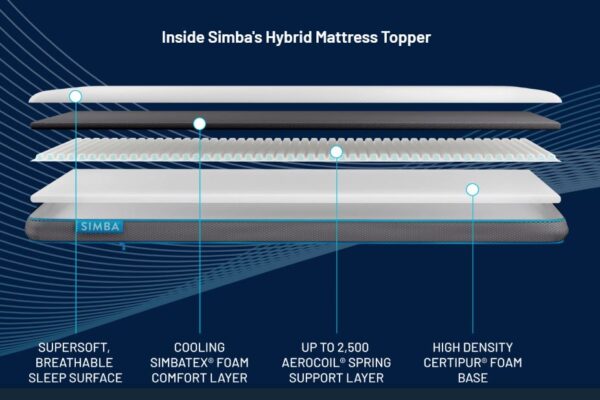

I thought it might be useful to reproduce here the diagram from the Simba web page showing how their hybrid mattress topper is constructed and the different layers it contains…

As you can see, the Simba hybrid mattress topper includes a number of different layers (hence the ‘hybrid’ in the name, I assume). You can read more about this on the Simba web page, but briefly at the top there is a soft, breathable sleep surface, with a foam comfort layer under that. In the middle is a spring support layer (just like in a mattress), with a high-density foam base below that. This is very different from most cheap mattress toppers, which are basically just quilts with a cotton/polyester filling.

Obviously because of its layered structure, you can’t turn the Simba hybrid mattress topper over. You can rotate it from end to end though, and it’s probably a good idea to do so occasionally to even out wear. No instructions are provided about this, however, so that’s purely a suggestion, based on my previous experience with mattresses.

Are there any drawbacks to the Simba hybrid mattress topper? Well, I did notice a slight ‘chemical’ smell which took a few days to disperse. It didn’t bother me, but ideally you might want to let your new mattress topper air for a day or two before starting to use it. I’m afraid I was too impatient to wait, though!

In addition, as this mattress topper contains springs, I wouldn’t recommend trying to wash it (it wouldn’t fit in a standard washing machine anyway!). It does though come with a removable, washable cover. Essentially, you need to treat this product as if it was a mini-mattress in its own right. That isn’t really a drawback to the Simba hybrid mattress topper, just a feature of it.

Overall, I am happy to give the Simba hybrid mattress topper my highest personal recommendation. If – like me – you have an old mattress that is starting to sag, it should prolong its useful life. Also, if you have a mattress that is too hard, it should make it softer and more comfortable for you. It’s not cheap (at the time of writing £219 for the single version or £329 for the king-size I received) – but, as so often in life, you get what you pay for. Easy payment by interest-free instalments (up to 12 months) is also available subject to status.

I should add as well that delivery is free and fast: next working day if you order before 2 pm or two working days if you order after 2 pm. There is also a range of options for buying a Simba double topper.

Many thanks again to my friends at Simba for allowing me to try out their hybrid mattress topper. If you have any comments or questions about this post, as ever, please do post them below as usual.

Disclosure: This is a sponsored post (gifted product).

If you enjoyed this post, please link to it on your own blog or social media:

Today I have another guest post for you on the subject of saving money and getting freebies 🙂

My friends at Hot Free Stuff have put together this list of seven top money-saving websites where you can get freebies, discount codes, downloadable coupons, and more. Check them out, and don’t forget to sign up for free emails from Hot Free Stuff to get all the latest free offers daily!

Are you a stressed-out mum (or dad) trying to make the family budget work?

It takes juggling to make the household budget balance without the need for taking a calculator on every shopping trip. That is because just a click of your mouse or a swipe of your tablet can reel in huge savings on credit card bills, home goods, fashion, electricity, and fun-filled family activities!

We have done the work of trawling the Internet to find you seven of the best money-saving websites around. We’ll help you get freebies, codes, downloadable coupons and more, so that you can do more with your budget every week. Here is our point-and-click guide to savings…

HotFreeStuff.co.uk

This site gets you access to lots of free samples you can really use, from lotions to perfumes. Save money using this site on lots of household goods and get a chance to try new products for free as soon as they are available.

Gumtree

At this so-called ‘classified community’ you can snap up lots of great deals on pets to property. There are many listings for rentals and jobs throughout the UK and Ireland. You will enjoy the deals, but you can also get free items via the freebies section. Just scroll beyond the ads and sponsor links to find many free listings for household items and furniture. At the time of writing there were listings on the London site for free sofas and mattresses, a working Hotpoint fridge-freezer, and free haircuts. Just a word of caution – we suggest for any classified site that you take someone along with you to collect any items, and be careful about giving away too much personal info when responding to ads.

HotUKDeals

This site has been around for well over a decade and is the most reputable place for people to share information on the freebies and discounts they have picked up on their website travels. It is free to register and features include ‘Top 10 Hottest Offers’, requests for offers, and fun, free competitions to enter.

My Voucher Codes

Get over 2000 discount codes at Britain’s biggest voucher website. Tabs include top listings as well as categories, together with the ability to print out vouchers.

Groupon

Never underestimate the power of Groupon! Many times it can seem like a venue for free or cut-price beauty treatments. There are, however, great deals on family attractions, meals and holiday getaways as well.

Moneysaving Expert (MSE)

This massive site set up by financial journalist Martin Lewis has saved the UK millions. It is clearly written, easy to understand, and has lots of information on getting deals on everything from home and car insurance to broadband and mortgages.

Travel Supermarket

This is the best site to find travel deals and compare flights and hotel offers in one easy-to-navigate resource.

Many thanks to Hot Free Stuff for sharing their advice and information. If you have any comments or questions – or other tips and resources for saving money – please do share them below as usual.

Disclosure: this is a sponsored post.

If you enjoyed this post, please link to it on your own blog or social media:

Today I have a guest post for you on a subject I’m sure will resonate with many Pounds and Sense readers.

We all love a freebie, but how do you ensure that by providing your details you aren’t opening the floodgates to a torrent of spam? Read and follow the tips below from my friends at All Free Stuff. And don’t forget to sign up for their free email newsletter to get details of all the latest free offers daily!

It’s completely possible for you to get free stuff. There are plenty of opportunities out there.

That said, for every legitimately free thing you can get, there are two complete scams set up to get your personal information at the cost of a few free samples. If you want to get free stuff without dealing with scams, try the following steps.

1. Set up a ‘spam catcher’ e-mail. This e-mail account is one you have no plans on using for normal correspondence, but rather the address you give out for giveaways and promotions. You can also use it when you register with a company that wants your e-mail address in exchange for free gifts. If you give the company your primary e-mail address, you’ll be swamped with a mass of promotional e-mails. It won’t take long for you to abandon your e-mail account in despair if this starts to happen.

2. Avoid giving personal information. You should never give out more than your name, e-mail address, physical address, and birthday. And you should be careful about giving away all of those, as well. If you can, try using a fake name or a PO Box. The more personal information you give out, the easier it will be for other companies to get that information. In addition, some websites ask for your credit card number ‘just to ensure you’re a real person’. Once they have your credit card information, you can’t make them forget it.

3. Be realistic about what you expect. If the deal seems too good to be true, it almost certainly is. It’s certainly possible the giveaway is legitimate, and if that’s the case then they should have company contact information readily available. You should also check the internet to see if you can find information. If the offer is that great, then plenty of people will be talking about it. Of course, if it’s a scam you’re liable to find discussion about that, too.

4. Visit only legitimate websites for samples. Manufacturers’ sites are generally trustworthy, whereas some retail-specific sites are not.

5. Write to the manufacturers of products you enjoy using. Companies are always happy to give a few freebies to customers willing to go out of their way to make their voice heard. It builds goodwill and often garners more customers. And all for the cost of a few free samples.

6. Learn to use coupons properly. It can take a huge amount of patience to learn to coupon well. That said, good couponing can save you so much you may even get free groceries. Couponing is a fairly big deal, so you can find plenty of websites that can help you learn. There are also many grocery stores or manufacturer sites that will keep you informed of what great deals and amazing coupons are available.

These are some of the best ways to get free stuff without dealing with scams. Do you have any other tips yourself? Please do leave them below!

Disclosure: This is a sponsored post.

If you enjoyed this post, please link to it on your own blog or social media:

As from 6 April 2024, UK investors have a fresh chance to supercharge their savings and investments with a new £20,000 Individual Savings Account (ISA) allowance.

To maximize the benefits of the new 2024/25 allowance, there’s a strong case for acting swiftly and using at least part of your £20,000 ISA allowance sooner rather than later. This is due to the power of compounding. By investing early, you give your money more time to grow, benefiting from the potential snowball effect of returns generating further returns. So the sooner you invest that £20,000 (assuming you are fortunate enough to have it) the more opportunity it has to multiply over time.

But the good news doesn’t end there. In addition to the ISA allowance remaining at a relatively generous £20,000, the rules surrounding ISAs have undergone a welcome relaxation from this tax year onward. One of the most significant changes is the ability to open more than one ISA of the same type (e.g. a stocks and shares ISA) with different providers in the same tax year. This means investors are no longer limited to a single provider for each type of ISA, giving them greater flexibility and choice in managing their investments.

Previously, investors were restricted to opening one cash ISA, one stocks and shares ISA and one innovative finance ISA (IFISA) per tax year. This restriction could prove frustrating for those seeking to diversify their investments or take advantage of new opportunities as the tax year progressed. Now, with the freedom to open multiple ISAs of the same type, investors can shop around for the best rates, terms, and investment options without being limited to a single provider for each ISA type. They can also move some or all of their money from one provider to another without jeopardising its tax-free status.

It’s important to note, however, that while the rules have been relaxed, the overall annual ISA allowance remains fixed at £20,000. This means that any contributions made across multiple ISAs of any type will count towards your total allowance for the tax year. You should still therefore take care not to exceed the annual limit to avoid any potential tax charges.

Cash ISAs offer a secure and accessible way to save, providing a tax-free environment for your savings with the added benefit of easy access to your funds when needed. Meanwhile, stocks and shares ISAs open the door to potential higher returns by investing in a wide range of assets such as equities, bonds, and funds, albeit with a higher level of risk. With a stocks and shares ISA you will never incur any liability for dividend tax, capital gains tax or income tax, even if your investments perform exceptionally well. Of course, there is no guarantee this will happen, but over a longer period stock market investments have typically outperformed cash savings, often by a substantial margin. IFISAs (e.g. from Assetz Exchange) allow you to invest is property crowdfunding and other forms of peer-to-peer finance. They are more specialized, but may appeal to some investors looking to further diversify their portfolios.

In recent years I have invested much of my own annual ISA allowance in a stocks and shares ISA with Nutmeg, a robo-manager platform that has produced good returns for me. You can read my in-depth review of Nutmeg here if you wish.

Closing Thoughts

In light of the new 2024/25 ISA allowance and relaxation of the rules surrounding them, now is the perfect time for UK investors to review their savings and investment strategies. Whether you’re looking to kickstart a new ISA or maximize your contributions to existing accounts, taking action early can set you on the path to optimizing your returns from this important tax-saving opportunity. By investing sooner rather than later and taking advantage of the increased flexibility in ISA provider options, savers can make the most of their money while minimizing their tax liabilities. So seize this opportunity to build your wealth and protect it from the taxman today!

As always, if you have any comments or questions about this post, please do leave them below.

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Cartoon image by courtesy of Bing AI.

If you enjoyed this post, please link to it on your own blog or social media:

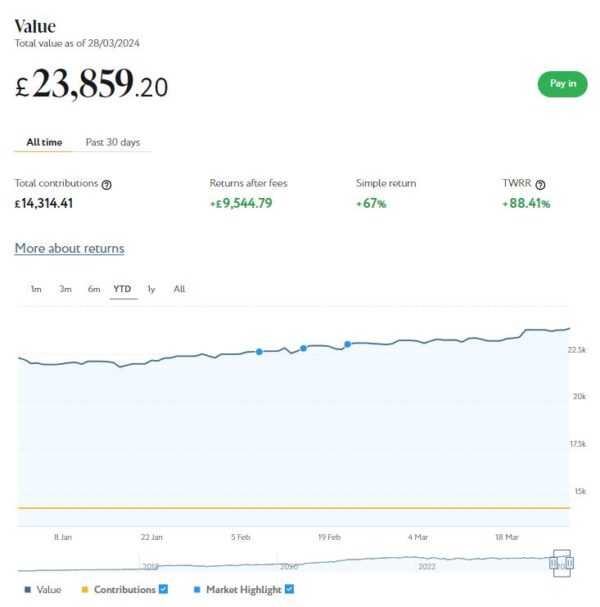

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

As the screenshot below for the year to date shows, my main Nutmeg portfolio is currently valued at £23,859. Last month it stood at £22,994 so that is a welcome increase of £865.

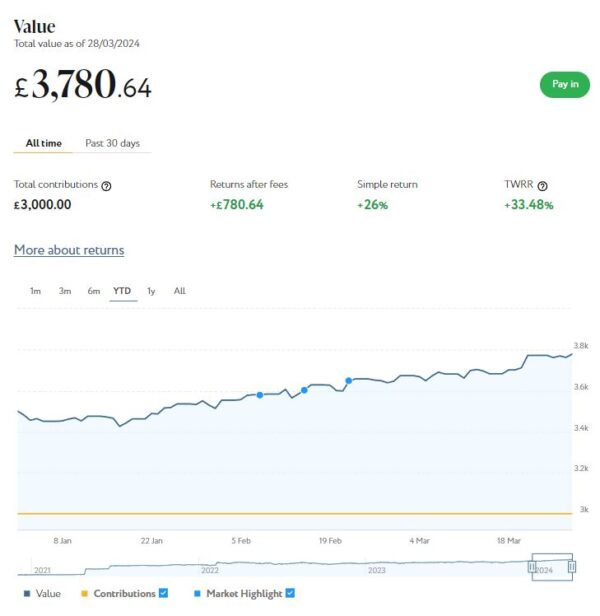

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £3,781 compared with £3,640 a month ago, a rise of £141. Here is a screen capture showing performance over the year to date.

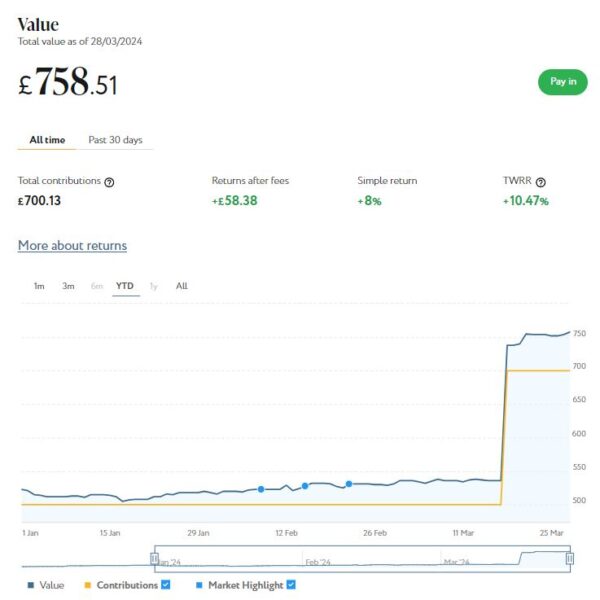

Finally, at the start of December 2023 I invested £500 in one of Nutmeg’s new thematic portfolios (Resource Transformation). As you can see from the screen capture below, this is now worth £759 compared with £530 last month, an increase of £229 since last month.

I should though say that £200 of this is ‘new money’. This came from a ‘Refer a Friend’ bonus, which I decided to pay into this pot rather than withdrawing. So if you disregard that, this portfolio has actually risen in value by £29 since last month.

March was obviously another good month for my Nutmeg investments. Overall – and disregarding the £200 RAF bonus – I was up £1,035 or 3.55%. And since the start of the year (again disregarding the £200 RAF bonus in March) I am up by £1,882 or 7.15%. In these turbulent times I am more than happy with that.

You can read my full Nutmeg review here (including a special offer at the end for PAS readers). If you are looking for a home for your annual ISA allowance, based on my overall experience over the last eight years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs), Lifetime ISAs and Junior ISAs as well.

Don’t forget, the current tax year ends on 5 April 2024 and after that the 2023/24 tax-free ISA allowance of £20,000 will be gone forever. But the good news is that you will then have a whole new £20,000 ISA allowance for 2024/25!

I also have investments with the property crowdlending platform Kuflink. They continue to do well, with new projects launching every week. I currently have around £1,570 invested with them in 10 different projects paying interest rates averaging around 7%. I also have £14 in my Kuflink cash account.

To date I have never lost any money with Kuflink, though some loan terms have been extended once or twice. On the plus side, when this happens additional interest is paid for the period in question.

There is now an initial minimum investment of £1,000 and a minimum investment per project of £500. Kuflink say they are doing this to streamline their operation and minimize costs. I can understand that, though it does mean that the option to test the water with a small first investment has been removed. It also makes it harder for small investors (like myself) to build a well-diversified portfolio on a limited budget.

One possible way around this is to invest using Kuflink’s Auto/IFISA facility. Your money here is automatically invested across a basket of loans over a period from one to five years. Interest rates range from 7% to around 10%, depending on the length of term you choose. Full up-to-date details can be found on the Kuflink website.

You can invest tax-free in a Kuflink Auto IFISA. Or if you have already used your annual iFISA allowance elsewhere, you can invest via a taxable Auto account. You can read my full Kuflink review here if you wish.

Moving on, my Assetz Exchange investments continue to generate steady returns. Regular readers will know that this is a P2P property investment platform focusing on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my AE portfolio has generated a respectable £173.90 in revenue from rental income. As I said in last month’s update, capital growth has slowed, though, in line with UK property values generally.

At the time of writing, 8 of ‘my’ properties are showing gains, 7 are breaking even, and the remaining 14 are showing losses. My portfolio is currently showing a net decrease in value of £35.05, meaning that overall (rental income minus capital value decrease) I am up by £138.85. That’s still a decent return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Assetz Exchange most projects are socially beneficial as well.

The overall fall in capital value of my AE investments is obviously a little disappointing. But it’s important to remember that until/unless I choose to sell the investments in question, it is largely theoretical, based on the most recent price at which shares in the property concerned have changed hands. The rental income, on the other hand, is real money (which in my case I’ve reinvested in other AE projects to further diversify my portfolio).

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of AE as far as i am concerned (especially now that Kuflink have raised their minimum investment per project to £500). You can actually invest from as little as 80p per property if you really want to proceed cautiously.

As I noted in this recent post, Assetz Exchange is particularly good if you want to compound your returns by reinvesting rental income. This effectively boosts the interest rate you are receiving. Personally, once I have accrued a minimum of £10 in rental payments, I reinvest this money in either a new AE project or one I have already invested in (thus increasing my holding). Over time, even if I don’t invest any more capital, this will ensure my investment with AE grows at an accelerating rate and becomes more diversified as well.

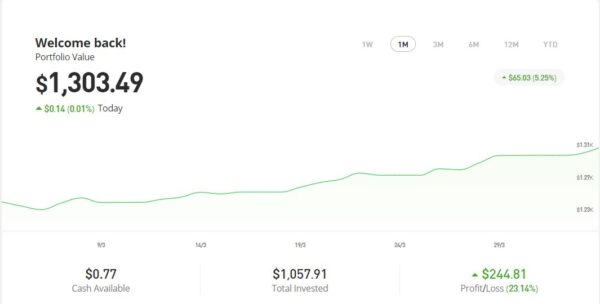

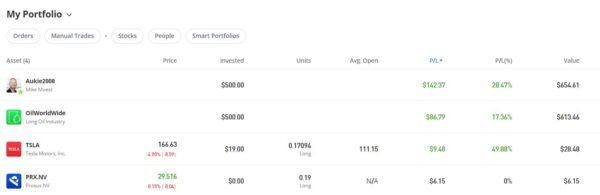

In 2022 I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios, Oil Worldwide. I also invested a small amount I had left over in Tesla shares.

As you can see from the screen captures below, my original investment totalling $1,022.26 is today worth $1,303.49, an overall increase of $281.23 or 27.51%.

eToro also offer the free eToro Money app. This allows you to deposit money to your eToro account without paying any currency conversion fees, saving you up to £5 for every £1,000 you deposit. You can also use the app to withdraw funds from your eToro account instantly to your bank account. I tried this myself and was impressed with how quickly and seamlessly it worked. You can read my blog post about eToro Money here. Note that it can also serve as a cryptocurrency wallet, allowing you to send and receive crypto from any other wallet address in the world.

I had two more articles published in March on the excellent Mouthy Money website. The first is Saving versus Investing – What’s the Difference and Why You Should Do Both. People often get confused between saving and investing, and it doesn’t help that the words are sometimes used loosely and interchangeably. In reality, though, there is a clear difference between them. In this article I explain why saving should always be your first priority, but ideally you should do both.

Also in March Mouthy Money published my article Are Solar Panels Still Worthwhile? As you probably know, solar PV panels generate electricity from sunlight. Growing numbers of homeowners (me included) have them on their roofs. At one time solar panels came with generous payment tariffs known as FiTs (feed-in tariffs), but those days are long gone. So in this article I examine what incentives exist today for installing panels and whether the sums still add up. I also look at the other pros and cons of solar panels.

As I’ve said before, Mouthy Money is a great resource for anyone interested in money-making and money-saving. I am a particular fan of my fellow MM contributor and money blogger Shoestring Jane. She writes mainly about money saving and frugal living. Her latest article Save Money on Gifts Throughout the Year sets out some top tips for saving money on gifts without (of course!) being a skinflint. You can see all of Jane’s articles for Mouthy Money via this web page.

I also published several posts on Pounds and Sense in March. I won’t bother mentioning those that are no longer relevant now, but the others are listed below.

One was a reminder that the Trading 212 welcome offer has reopened. If you haven’t done this before, you can get a free share worth up to £100. As I said in the article, my free share in AMD is now worth £151.88! This offer closes on 16 April 2024.

Also in March I published Don’t Miss Out! Use Your £20,000 ISA Allowance Before It’s Too Late. This was a reminder to use your 2023/24 allowance before it vanishes on 6th April 2024. Obviously you will need to move very smartly if you are going to do this now. But (as I said earlier) the good news is that everyone will have a fresh £20,000 allowance from that date.

One other bit of news this month is that I finally got around to buying a home storage battery to connect to my solar panels (see my recent MM article about panels). I used a local (Staffordshire) company called The Energy Box for this, and am very happy to recommend them.

I’ve had my battery for just over a fortnight now and it’s been quite eye-opening. Using the battery app I can see how much electricity my solar panels are generating at any time and how much I am using in my home. I can also check the battery charge level and whether it’s charging or discharging. Even at this time of year, if there’s a bit of sunshine I am generating enough electricity in the day to cover my needs and charge the battery to a level where I’m running the house from it till well into the evening.

In the summer I’d expect to be generating enough to live off solar-generated power entirely, meaning there will only be the dreaded standing charge to pay. So I will actually be saving more money than I originally anticipated, though admittedly it will still be a number of years before the cost is covered.

It wasn’t just a financial decision, though. My other aim was to be able to continue as normal in the event of power cuts (which I expect to become more frequent in coming years as the UK transitions away from fossil fuels), and that should be the case too. The only issue might be a power cut in the depths of winter when the battery hasn’t charged up from the panels. Even so, if I know (or suspect) a cut is coming I can charge the battery in advance from the mains.

I’ve written an article going into more detail about home storage batteries (including my own) for my regular clients at Mouthy Money. This will be published in April, so keep an eye out for it!

Finally, a quick reminder that you can also follow Pounds and Sense on Facebook or Twitter/X. Twitter/X is my number one social media platform these days and I post regularly there. I share the latest news and information on financial (and other) matters, and other things that interest, amuse or concern me. So if you aren’t following my PAS account, you are definitely missing out!

That’s all for today. As always, if you have any comments or queries, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media:

As the end of the tax year on 5 April 2024 approaches, so too does the deadline to utilize the annual tax-free Individual Savings Account (ISA) allowance.

The clock is ticking, and unless you take action in the next couple of weeks, this opportunity to maximize your tax-free savings for the 2023/24 financial year will be gone forever.

ISAs are a popular choice for savers and investors alike, offering a tax-efficient way to grow your wealth. With a diverse range of options available, from cash ISAs to stocks and shares ISAs and innovative finance ISAs, individuals have the flexibility to tailor their savings strategy to suit their financial goals and risk appetite.

The current ISA allowance stands at £20,000, providing a significant opportunity to shield your savings and investments from tax. This allowance represents a generous sum that, if left unused, cannot be carried forward to future years. In essence, any portion of the £20,000 allowance that remains untapped by the upcoming deadline will be lost, representing a missed opportunity for tax-free growth.

For those who have yet to fully utilize their annual ISA allowance, now is the time to take action. Whether you’re looking to bolster your rainy-day fund with a cash ISA or seeking to invest in the stock market through a stocks and shares ISA, there’s no shortage of options available. But bear in mind that under current rules you can only invest in one of each type of ISA in any one tax year (though this rule is changing from 2024/25). So if you already invested in, say, a stocks and shares ISA this year, you are not allowed to invest in a S&S ISA with a different provider in the current tax year. You will only be able to top up your current S&S ISA to whatever remains of your total £20,000 allowance.

Cash ISAs offer a secure and accessible way to save, providing a tax-free environment for your savings with the added benefit of easy access to your funds when needed. Meanwhile, stocks and shares ISAs open the door to potential higher returns by investing in a wide range of assets such as equities, bonds, and funds, albeit with a higher level of risk. With a stocks and shares ISA you will never incur any liability for dividend tax, capital gains tax or income tax, even if your investments perform exceptionally well. Of course, there is no guarantee this will happen, but over a longer period stock market investments have typically outperformed cash savings, often by a substantial margin.

In recent years I have invested much of my own annual ISA allowance in a stocks and shares ISA with Nutmeg, a robo-manager platform that has produced good returns for me. You can read my in-depth review of Nutmeg here if you wish.

With just a few weeks left to take advantage of this valuable tax benefit, procrastination could prove costly. By acting now, you can ensure that your savings and investments are positioned to grow tax-free, setting yourself up for a better financial future.

In summary, the £20,000 annual ISA allowance for the 2023/24 tax year presents a golden opportunity for UK residents to maximize tax-free savings and investments. Time is of the essence, though, and unless you act before the impending deadline on 5th April 2024, this valuable allowance will be lost forever. If you have the money available, therefore, seize the opportunity now to help secure your financial future.

As always, if you have any comments or questions about this article, please feel free to leave them below.

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

If you enjoyed this post, please link to it on your own blog or social media:

Offer now closed – sorry! I will update this post when/if it reopens.

Today I’m featuring a way you can get a free share worth up to £100 by signing up with an online share trading platform called Trading 212.

Trading 212 is unusual in that it offers commission-free and fee-free share trading. As a special offer, until 16 April 2024 they are offering people new to the platform a free share just for signing up via a referral link (such as the links in this post). The share you will get is chosen at random, but could be worth up to £100. You can either keep this share or sell it.

Table of Contents

How to Sign Up

Signing up with Trading 212 is pretty straightforward. Just visit the Trading 212 website via any of the (referral) links in this post and follow the on-screen instructions to register. Note that you will be required to provide various items of information, including your date of birth, National Insurance number, annual income, employment status, and contact details. I understand that this is to meet their legal ‘Know Your Customer’ duty.

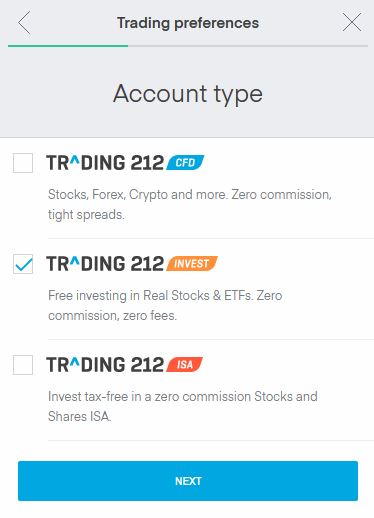

You will also need to indicate the type of account you want from the three options available (see screen capture below).

As you will see, the three account types on Trading 212 are CFD, Invest and ISA. You can apply for one, two or all three of these if you like.

CFD stands for Contract for Difference. CFDs are quite complex financial instruments, and unless you know what you’re doing I recommend giving them a miss. As you can see, you can also use this type of account for trading in Cryptocurrencies. Again this is pretty high risk and not something that appeals to me personally.

I would also recommend thinking carefully before you tick the ISA box. An ISA is, of course, a tax-exempt Individual Savings Account. Nothing wrong with that, except you can only invest in one of each type of ISA (Cash, Stocks and Shares, IFISA) in any one tax year (though this will change from April 2024).

Trading 212 are offering a Stocks and Shares ISA, so if you have already invested in one of these this year (e.g. with Nutmeg), you won’t be able to open another. Equally, once you invest in a Trading 212 ISA, you won’t then be able to open another Stocks and Shares ISA in this financial year. So you do need to be pretty sure that is how you want to use your 2023/24 Stocks and Shares ISA before doing this.

All you need to take advantage of the Trading 212 offer is a standard Invest account, so I recommend ticking this box only (as per the screen capture above).

Getting Your Free Share

There is one more step you will need to take in order to get your free share. You will need to deposit a minimum of £1 into your account. There are various ways you can do this, but i just used my debit card. There is no obligation to invest the £1 (or whatever you choose to deposit) and if you wish you can withdraw it once your free share has been credited.

The next business day you should receive an email confirming that a free share has been added to your account. As mentioned above, this is allotted at random. If you’re lucky you might get one worth up to £100. Even if you get a less valuable one, though, it’s still a share for free. If you choose to keep it, it may rise in value. There may also be dividends payable in future (and credited to your account).

Already have a Trading 212 account? You can also get a free ETF share worth up to £200 (and now guaranteed to be worth at least £10) with new DIY wealth-building app Wealthyhood. A minimum investment of £50 is required to get the free share (although if you’re not bothered about this you can start investing on the platform with as little as £20). Click through here for more info!

Selling Your Share

You can’t sell your share immediately. You have to wait three business days before doing so, but it is then just a matter of clicking the Sell button on your member’s dashboard.

The money will be credited to your Trading 212 account but you will have to wait 30 days before withdrawing it. So there may be a case for waiting to see if your share’s value goes up in that time. Of course, it could also go down!

In my case, I received a free share in the Ford Motor Company worth about £8 at the time. Obviously this wasn’t as exciting as I might have hoped, but it was still – in effect – free money for almost no time or effort 😀

How Safe Is Trading 212?

Trading 212 is registered in England and Wales and authorized and regulated by the Financial Conduct Authority. In addition, all clients’ funds are kept separately in segregated bank accounts which are covered by the Financial Services Compensation Scheme. So even if the company itself were to go broke, any cash in your account would be protected up to a value of £85,000.

Of course, the FSCS guarantee doesn’t apply to the value of your stocks and shares, which can go down as well as up. All investments carry a risk of loss, although in the case of your free share you can never lose any more than the original cost, which was of course zero!

Referral Scheme

Any Trading 212 member can also refer new members. In this case, both you and the person concerned will receive one free share worth up to £100. Obviously, the links in this blog post include my referral code – so if you register and get a free share, I will receive one also. Under the terms of the current offer you can get up to five free shares in this way. Five is the limit per person. Although you can still refer new members who will get a free share after this, as a referrer you won’t receive one as well.

Final Thoughts

I first heard about Trading 212 a while ago, but wasn’t initially sure whether it was legit and here for the long term. And I thought the free share offer was, frankly, too good to be true. However, my own experiences have been entirely positive. My original free share in the Ford Motor Company was credited the next business day as promised and I received an email notifying me about it.

I can log in to my Trading 212 account any time to see how my Ford share is doing. I have also collected a few other shares from referrals as well. These include a share in AMD (the semiconductor company), which is currently worth £151.51, and one in Nike, which is worth £88.33. I still have my original Ford Motor Company share and it has risen in value to £9.65. I also received an annual dividend payment from them a while ago. I haven’t sold any of my free shares yet but could of course do so any time I choose. I am not in any rush, as Trading 212 do not impose any platform or inactivity fees.

Although in this post I have focused on the free share offer, Trading 212 is worth considering as a share-dealing platform too. In particular, the fact that it’s fee-free and commission-free means it is well suited for people who are dipping a toe in stocks and shares investment for the first time. By contrast, the dealing fees and commissions charged by some other share-trading platforms can make small share purchases prohibitively expensive. This review by Money Savvy Daddy looks at the pros and cons of Trading 212 as a share-dealing platform in a bit more detail.

In conclusion, I hope this post has inspired you to consider registering with Trading 212 to claim your free share. If you do, I hope you get a valuable one! Please let me know what share you receive in a comment below. And, as always, any other comments or questions are very welcome too.

Don’t forget, the current free share offer ends on 16 April 2024.

Disclosure: The links in this post include my referral code. If you click through and register as described above, I will receive a free share (as will you). Please note also that I am not a qualified financial adviser and nothing in this post should be construed as individual financial advice. Everyone should do their own ‘due diligence’ before investing and seek advice from a qualified financial adviser if in any doubt how best to proceed. All investment carries a risk of loss (although not in the case of free shares, obviously).

This is an update of my original post about this special offer.

If you enjoyed this post, please link to it on your own blog or social media:

A quickie today to let you know that the price of stamps is rising (again!) on Tuesday 2nd April 2024.

Standard second-class stamps will be going up by 10p to 85p, while first-class stamps will also rise by 10p to £1.35.

A first-class stamp for a large letter will rise by 15p from £1.95 to £2.10. The price of a second-class stamp for a large letter will remain at £1.55.

Standard letters can weigh up to 100g and measure a maximum of 24cm x 16.5cm x 5mm. Large letters can measure 35.3cm x 25cm x 2.5cm but still have to weigh under 100g. If they weight over 100g, higher rates apply, and if they weigh over 750g they have to go at parcel rates.

Saving Money on Stamps

So is there anything you can do to mitigate the impact of the latest price rises?

Well, my number one recommendation is to stock up now while stamps are still at the old price. Standard and large-letter stamps don’t have values printed on them and will still be valid after the April price rise comes in.

If you can afford to buy (say) 100 standard first-class stamps and 100 second-class, that will save you an impressive £20 in total. If you’re anything like me, that will keep you going till Christmas 2024 and beyond!

The best bet for buying stamps is – of course – your local post office. If you don’t have one near at hand, however, you can also buy in bulk from various suppliers, including Viking Direct. They sell books of first and second class stamps at the current price, with postage free for orders of over £59. You can also buy stamps online from The Royal Mail Shop.

Amazon also sell postage stamps, though costs vary and when I checked some prices were significantly higher than at post offices. But they may be worth a look, especially if you are an Amazon Prime member.

Another option to consider is the online auction site eBay (search for “new UK stamps”). There can be good savings to be made here, but check reviews and ratings carefully and be wary of offers that are clearly too good to be true.

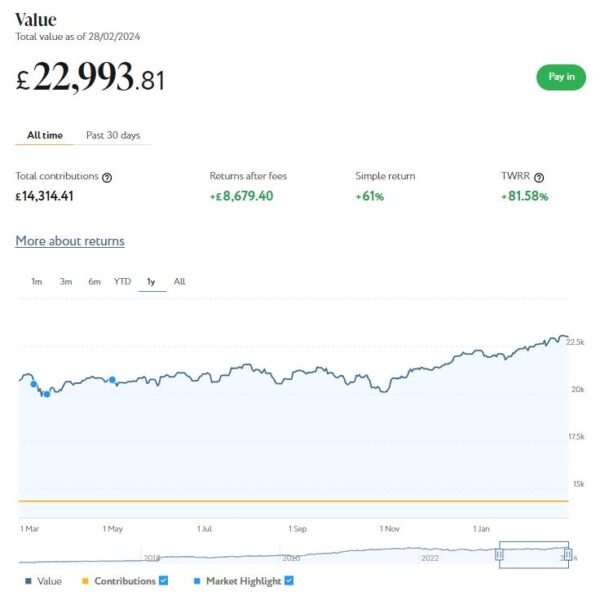

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

As the screenshot below for the last 12 months shows, my main Nutmeg portfolio is currently valued at £ £22,994. Last month it stood at £22,386 so that is a welcome increase of £608.

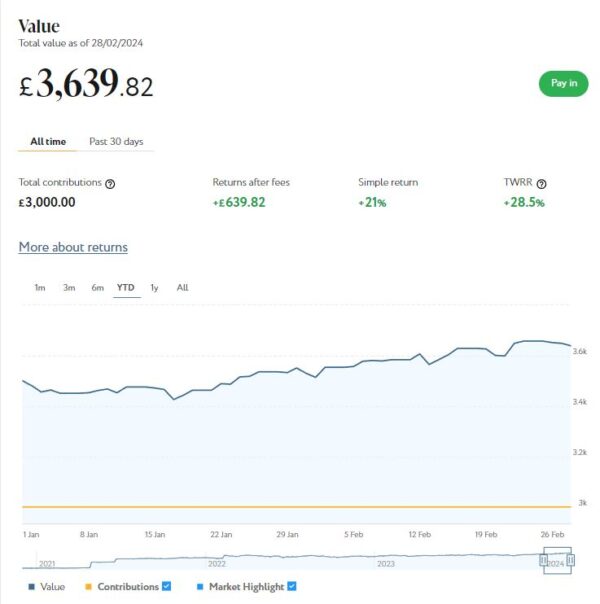

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £3,640 compared with £3,530 a month ago, a rise of £110. Here is a screen capture showing performance over the last 12 months.

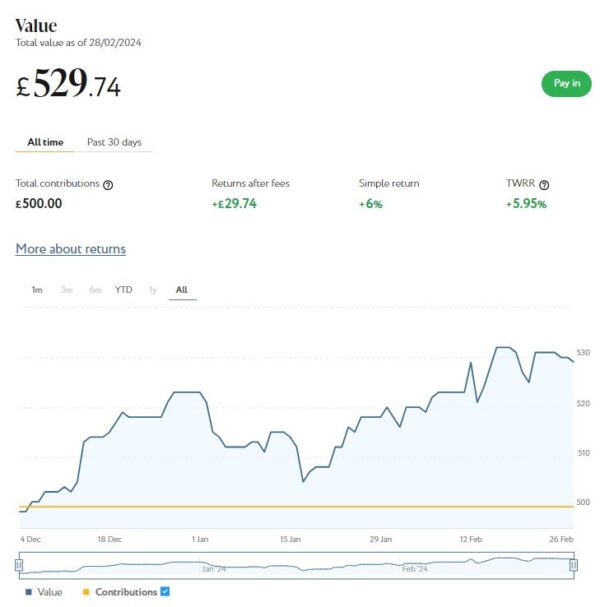

Finally, at the start of December 2023 I invested £500 in one of Nutmeg’s new thematic portfolios (Resource Transformation). As you can see from the screen capture below, this is now worth £530, an increase of £11 since last month and £30 or 6% over the three-month period since I first invested.

February was obviously a good month for my Nutmeg investments. Overall I was up £737 or 2.79%. In these turbulent times I am more than happy with that.

You can read my full Nutmeg review here (including a special offer at the end for PAS readers). If you are looking for a home for your annual ISA allowance, based on my overall experience over the last seven years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs), Lifetime ISAs and Junior ISAs as well.

Don’t forget, the current tax year ends on 5 April 2024 and after that the 2023/24 tax-free ISA allowance of £20,000 will be gone forever!

I also have investments with the property crowdlending platform Kuflink. They continue to do well, with new projects launching every week. I currently have around £1,570 invested with them in 10 different projects paying interest rates averaging around 7%. I also have £14 in my Kuflink cash account.

To date I have never lost any money with Kuflink, though some loan terms have been extended once or twice. On the plus side, when this happens additional interest is paid for the period in question.

There is now an initial minimum investment of £1,000 and a minimum investment per project of £500. Kuflink say they are doing this to streamline their operation and minimize costs. I can understand that, though it does mean that the option to test the water with a small first investment has been removed. It also makes it harder for small investors (like myself) to build a well-diversified portfolio on a limited budget.

One possible way around this is to invest using Kuflink’s Auto/IFISA facility. Your money here is automatically invested across a basket of loans over a period from one to five years. Interest rates range from 7% to around 10%, depending on the length of term you choose. Full up-to-date details can be found on the Kuflink website.

You can invest tax-free in a Kuflink Auto IFISA. Or if you have already used your annual iFISA allowance elsewhere, you can invest via a taxable Auto account. You can read my full Kuflink review here if you wish.

Moving on, my Assetz Exchange investments continue to generate steady returns. Regular readers will know that this is a P2P property investment platform focusing on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my AE portfolio has generated a respectable £168.53 in revenue from rental income. As I said in last month’s update, capital growth has slowed, though, in line with UK property values generally.

At the time of writing, 10 of ‘my’ properties are showing gains, 4 are breaking even, and the remaining 15 are showing losses. My portfolio is currently showing a net decrease in value of £40.01, meaning that overall (rental income minus capital value decrease) I am up by £128.52. That’s still a decent return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Assetz Exchange most projects are socially beneficial as well.

The overall fall in capital value of my AE investments is obviously a little disappointing. But it’s important to remember that until/unless I choose to sell the investments in question, it is largely theoretical, based on the most recent price at which shares in the property concerned have changed hands. The rental income, on the other hand, is real money (which in my case I’ve reinvested in other AE projects to further diversify my portfolio).

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of AE as far as i am concerned (especially now that Kuflink have raised their minimum investment per project to £500). You can actually invest from as little as 80p per property if you really want to proceed cautiously.

As I noted in this recent post, Assetz Exchange is particularly good if you want to compound your returns by reinvesting rental income. This effectively boosts the interest rate you are receiving. Personally, once I have accrued a minimum of £10 in rental payments, I reinvest this money in either a new AE project or one I have already invested in (thus increasing my holding). Over time, even if I don’t invest any more capital, this will ensure my investment with AE grows at an accelerating rate.

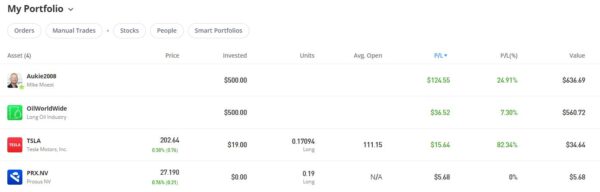

In 2022 I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios, Oil Worldwide. I also invested a small amount I had left over in Tesla shares.

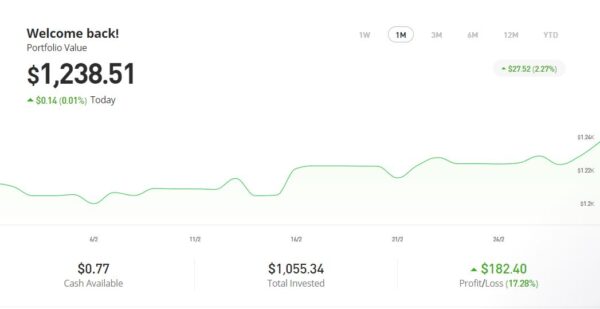

As you can see from the screen captures below, my original investment totalling $1,022.26 is today worth $1,238.51, an overall increase of $216.25 or 21.15%.

eToro also offer the free eToro Money app. This allows you to deposit money to your eToro account without paying any currency conversion fees, saving you up to £5 for every £1,000 you deposit. You can also use the app to withdraw funds from your eToro account instantly to your bank account. I tried this myself and was impressed with how quickly and seamlessly it worked. You can read my blog post about eToro Money here. Note that it can also serve as a cryptocurrency wallet, allowing you to send and receive crypto from any other wallet address in the world.

I had three more articles published in January on the excellent Mouthy Money website. The first is How to Save Money on Motoring. Like everything else in life the cost of motoring is going up and up, so in this article I set out a variety of ways – from ride-sharing to driving for fuel economy – you may be able to reduce it.

Also in February Mouthy Money published Are You Making the Most of Your Annual ISA Allowance?. As mentioned earlier, the 2023/24 tax year ends in just a few weeks’ time. And after that the £20,000 tax-free ISA allowance for that year will be gone forever. In this article I describe the different types of ISA – Cash ISA, Stocks and Shares ISA, Innovative Finance ISA (IFISA) and Lifetime ISA (LISA) – and explain how they work and the differences between them. I also provide some tips and advice for making the most of your annual ISA allowance.

My final article published on Mouthy Money last month was Can You Save Money on Your Shopping with JamDoughnut? Regular PAS readers will know that I am a fan of the JamDoughnut app, which enables you to save up to 20% on purchases with a growing range of retailers. The article also reveals how you can get a £2 head-start by using my referral code.

As I’ve said before, Mouthy Money is a great resource for anyone interested in money-making and money-saving. I am a particular fan of my fellow MM contributor and money blogger Shoestring Jane. She writes mainly about money saving and frugal living. Her latest article Frugal Skills to Save You Money sets out a selection of life skills that can save you money (and aren’t hard to learn). You can see all of Jane’s articles for Mouthy Money via this web page.

I also published several posts on Pounds and Sense in February. I won’t bother mentioning those that are no longer relevant now, but the others are listed below.

In Get Your Will Written Free of Charge in March I revealed how you can get your will written (or updated) free of charge during Free Wills Month. This regular event supports a range of leading charities. Obviously the hope is that you will include a bequest to charity in your will, but there is absolutely no obligation to do this. Free Wills Month is now up and running. If you want to take advantage and get your will written free, I recommend acting now as there are only limited spots available.

Also in March I published a guest post titled Building Your Own Home – It’s Not Just for the Super Rich! This post was written on behalf of Suffolk Building Society, who are trying to raise awareness of the self-build option in the UK. As they say in the article, they can provide mortgages to purchase land suitable for self-build projects. SBS emphasize that this option is suitable and available for ‘ordinary people’, not just the super-rich folk you see on TV shows like Grand Designs!

I also published Saving for a Rainy Day or a Stormy Breakup? The Surprising Facts About Secret Savings Accounts. This post is based on some eye-opening research from my friends at Smart Money People, which revealed (among other things) that one in ten people in a serious relationship, including marriage, civil partnerships, or cohabitation, maintain a secret savings account. Find out more in this post.

Also, from January this year I became a regular contributor to the new Over 60s Discounts website. You can read my latest article here: Who Cares for the Carers? This is about help available for unpaid carers in the UK, both financial and practical. I highly recommend registering at Over 60s Discounts, by the way – they list a growing range of discounts and bonuses for older people, including some that are unique to O60D.

One other thing is that this month I switched my Santander 123 Lite current account to a Santander Edge current account. I will try to find time to write a separate post about this soon. But briefly, my main reason was because having an Edge current account allows you to open an Edge savings account, which offers a market-leading 7% interest rate (AER) for amounts of up to £4,000 for one year (it then falls to 4.5% AER).

The Santander Edge account has slightly higher fees (£3 a month as opposed to £2) and the cashback on offer is slightly less. However, when I crunched the numbers, the value of having an Edge savings account easily outweighed this. Though I am fortunate in that I had £4,000 I could put into it immediately from another, lower-paying savings account. If I hadn’t had that, it wouldn’t have been worth switching to the Edge account.

Finally, a quick reminder that you can also follow Pounds and Sense on Facebook or Twitter/X. Twitter/X is my number one social media platform these days and I post regularly there. I share the latest news and information on financial (and other) matters, and other things that interest, amuse or concern me. So if you aren’t following my PAS account, you are definitely missing out!

That’s all for today. As always, if you have any comments or queries, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media: