As from 6 April 2024, UK investors have a fresh chance to supercharge their savings and investments with a new £20,000 Individual Savings Account (ISA) allowance.

To maximize the benefits of the new 2024/25 allowance, there’s a strong case for acting swiftly and using at least part of your £20,000 ISA allowance sooner rather than later. This is due to the power of compounding. By investing early, you give your money more time to grow, benefiting from the potential snowball effect of returns generating further returns. So the sooner you invest that £20,000 (assuming you are fortunate enough to have it) the more opportunity it has to multiply over time.

But the good news doesn’t end there. In addition to the ISA allowance remaining at a relatively generous £20,000, the rules surrounding ISAs have undergone a welcome relaxation from this tax year onward. One of the most significant changes is the ability to open more than one ISA of the same type (e.g. a stocks and shares ISA) with different providers in the same tax year. This means investors are no longer limited to a single provider for each type of ISA, giving them greater flexibility and choice in managing their investments.

Previously, investors were restricted to opening one cash ISA, one stocks and shares ISA and one innovative finance ISA (IFISA) per tax year. This restriction could prove frustrating for those seeking to diversify their investments or take advantage of new opportunities as the tax year progressed. Now, with the freedom to open multiple ISAs of the same type, investors can shop around for the best rates, terms, and investment options without being limited to a single provider for each ISA type. They can also move some or all of their money from one provider to another without jeopardising its tax-free status.

It’s important to note, however, that while the rules have been relaxed, the overall annual ISA allowance remains fixed at £20,000. This means that any contributions made across multiple ISAs of any type will count towards your total allowance for the tax year. You should still therefore take care not to exceed the annual limit to avoid any potential tax charges.

Cash ISAs offer a secure and accessible way to save, providing a tax-free environment for your savings with the added benefit of easy access to your funds when needed. Meanwhile, stocks and shares ISAs open the door to potential higher returns by investing in a wide range of assets such as equities, bonds, and funds, albeit with a higher level of risk. With a stocks and shares ISA you will never incur any liability for dividend tax, capital gains tax or income tax, even if your investments perform exceptionally well. Of course, there is no guarantee this will happen, but over a longer period stock market investments have typically outperformed cash savings, often by a substantial margin. IFISAs (e.g. from Assetz Exchange) allow you to invest is property crowdfunding and other forms of peer-to-peer finance. They are more specialized, but may appeal to some investors looking to further diversify their portfolios.

In recent years I have invested much of my own annual ISA allowance in a stocks and shares ISA with Nutmeg, a robo-manager platform that has produced good returns for me. You can read my in-depth review of Nutmeg here if you wish.

Closing Thoughts

In light of the new 2024/25 ISA allowance and relaxation of the rules surrounding them, now is the perfect time for UK investors to review their savings and investment strategies. Whether you’re looking to kickstart a new ISA or maximize your contributions to existing accounts, taking action early can set you on the path to optimizing your returns from this important tax-saving opportunity. By investing sooner rather than later and taking advantage of the increased flexibility in ISA provider options, savers can make the most of their money while minimizing their tax liabilities. So seize this opportunity to build your wealth and protect it from the taxman today!

As always, if you have any comments or questions about this post, please do leave them below.

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Cartoon image by courtesy of Bing AI.

If you enjoyed this post, please link to it on your own blog or social media:

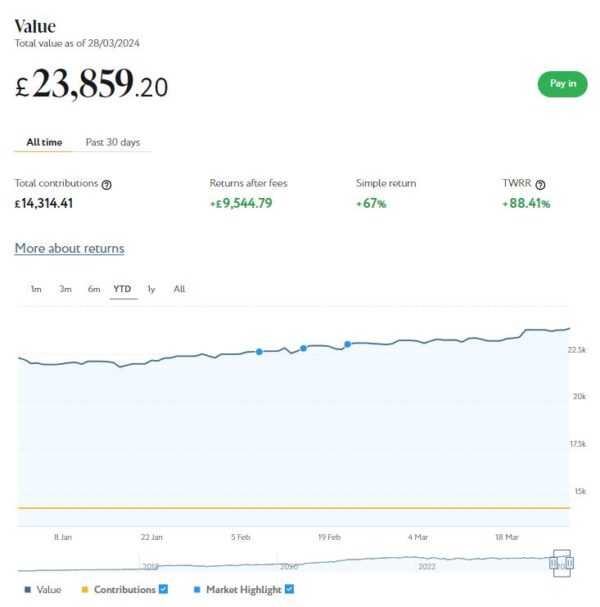

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

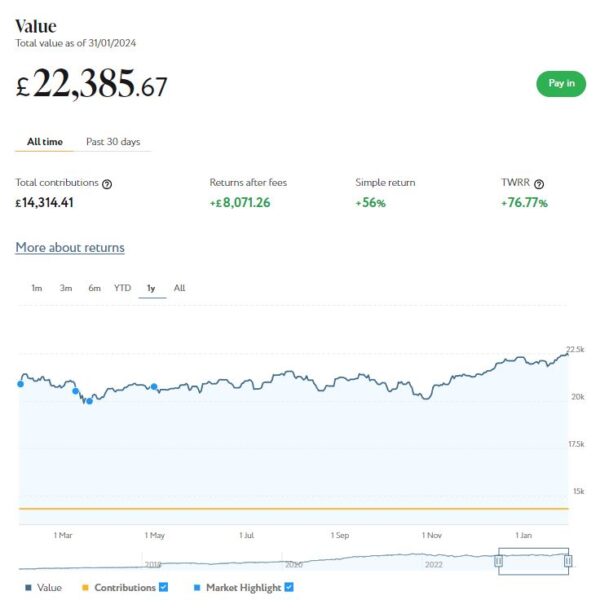

As the screenshot below for the year to date shows, my main Nutmeg portfolio is currently valued at £23,859. Last month it stood at £22,994 so that is a welcome increase of £865.

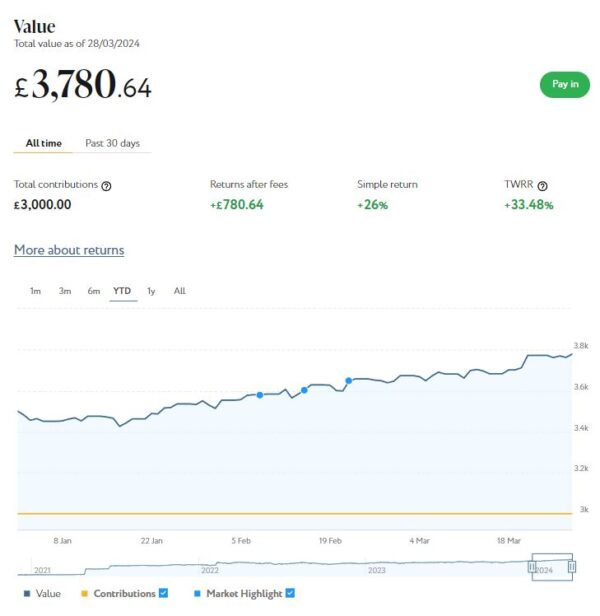

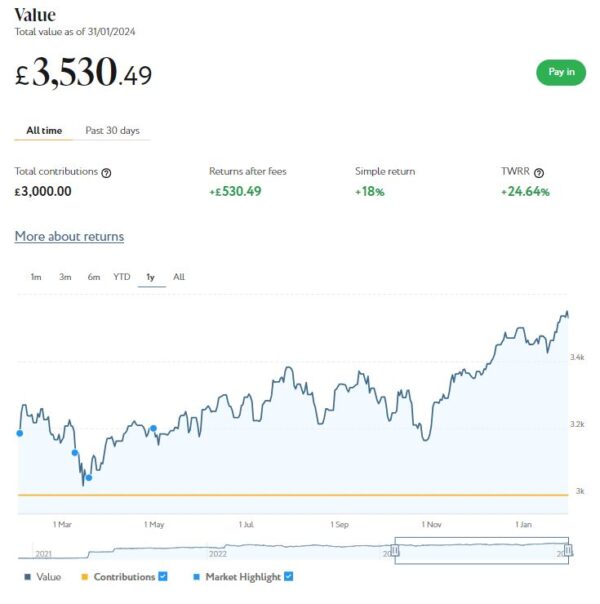

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £3,781 compared with £3,640 a month ago, a rise of £141. Here is a screen capture showing performance over the year to date.

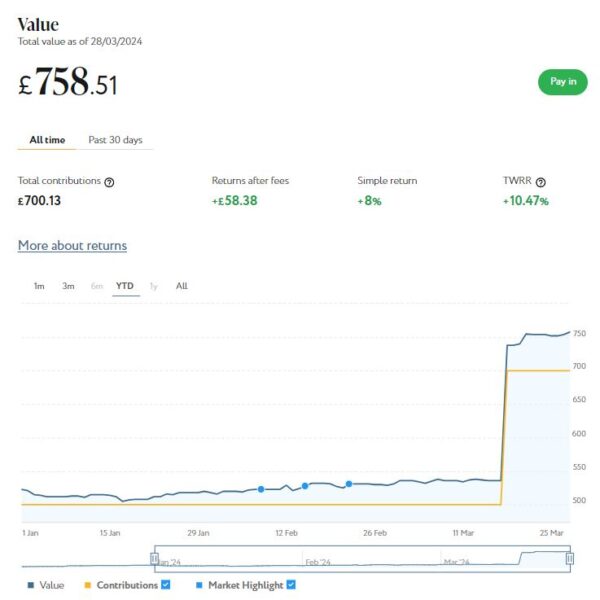

Finally, at the start of December 2023 I invested £500 in one of Nutmeg’s new thematic portfolios (Resource Transformation). As you can see from the screen capture below, this is now worth £759 compared with £530 last month, an increase of £229 since last month.

I should though say that £200 of this is ‘new money’. This came from a ‘Refer a Friend’ bonus, which I decided to pay into this pot rather than withdrawing. So if you disregard that, this portfolio has actually risen in value by £29 since last month.

March was obviously another good month for my Nutmeg investments. Overall – and disregarding the £200 RAF bonus – I was up £1,035 or 3.55%. And since the start of the year (again disregarding the £200 RAF bonus in March) I am up by £1,882 or 7.15%. In these turbulent times I am more than happy with that.

You can read my full Nutmeg review here (including a special offer at the end for PAS readers). If you are looking for a home for your annual ISA allowance, based on my overall experience over the last eight years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs), Lifetime ISAs and Junior ISAs as well.

Don’t forget, the current tax year ends on 5 April 2024 and after that the 2023/24 tax-free ISA allowance of £20,000 will be gone forever. But the good news is that you will then have a whole new £20,000 ISA allowance for 2024/25!

I also have investments with the property crowdlending platform Kuflink. They continue to do well, with new projects launching every week. I currently have around £1,570 invested with them in 10 different projects paying interest rates averaging around 7%. I also have £14 in my Kuflink cash account.

To date I have never lost any money with Kuflink, though some loan terms have been extended once or twice. On the plus side, when this happens additional interest is paid for the period in question.

There is now an initial minimum investment of £1,000 and a minimum investment per project of £500. Kuflink say they are doing this to streamline their operation and minimize costs. I can understand that, though it does mean that the option to test the water with a small first investment has been removed. It also makes it harder for small investors (like myself) to build a well-diversified portfolio on a limited budget.

One possible way around this is to invest using Kuflink’s Auto/IFISA facility. Your money here is automatically invested across a basket of loans over a period from one to five years. Interest rates range from 7% to around 10%, depending on the length of term you choose. Full up-to-date details can be found on the Kuflink website.

You can invest tax-free in a Kuflink Auto IFISA. Or if you have already used your annual iFISA allowance elsewhere, you can invest via a taxable Auto account. You can read my full Kuflink review here if you wish.

Moving on, my Assetz Exchange investments continue to generate steady returns. Regular readers will know that this is a P2P property investment platform focusing on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my AE portfolio has generated a respectable £173.90 in revenue from rental income. As I said in last month’s update, capital growth has slowed, though, in line with UK property values generally.

At the time of writing, 8 of ‘my’ properties are showing gains, 7 are breaking even, and the remaining 14 are showing losses. My portfolio is currently showing a net decrease in value of £35.05, meaning that overall (rental income minus capital value decrease) I am up by £138.85. That’s still a decent return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Assetz Exchange most projects are socially beneficial as well.

The overall fall in capital value of my AE investments is obviously a little disappointing. But it’s important to remember that until/unless I choose to sell the investments in question, it is largely theoretical, based on the most recent price at which shares in the property concerned have changed hands. The rental income, on the other hand, is real money (which in my case I’ve reinvested in other AE projects to further diversify my portfolio).

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of AE as far as i am concerned (especially now that Kuflink have raised their minimum investment per project to £500). You can actually invest from as little as 80p per property if you really want to proceed cautiously.

As I noted in this recent post, Assetz Exchange is particularly good if you want to compound your returns by reinvesting rental income. This effectively boosts the interest rate you are receiving. Personally, once I have accrued a minimum of £10 in rental payments, I reinvest this money in either a new AE project or one I have already invested in (thus increasing my holding). Over time, even if I don’t invest any more capital, this will ensure my investment with AE grows at an accelerating rate and becomes more diversified as well.

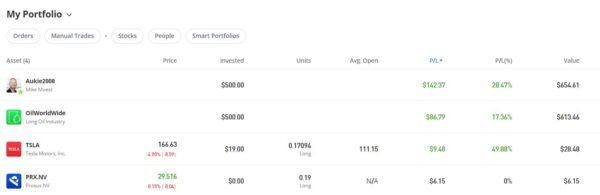

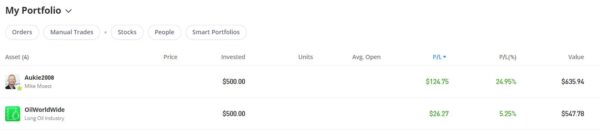

In 2022 I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios, Oil Worldwide. I also invested a small amount I had left over in Tesla shares.

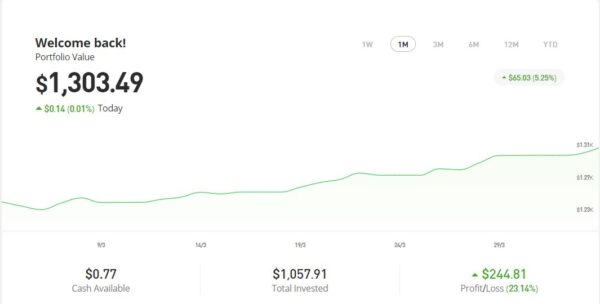

As you can see from the screen captures below, my original investment totalling $1,022.26 is today worth $1,303.49, an overall increase of $281.23 or 27.51%.

eToro also offer the free eToro Money app. This allows you to deposit money to your eToro account without paying any currency conversion fees, saving you up to £5 for every £1,000 you deposit. You can also use the app to withdraw funds from your eToro account instantly to your bank account. I tried this myself and was impressed with how quickly and seamlessly it worked. You can read my blog post about eToro Money here. Note that it can also serve as a cryptocurrency wallet, allowing you to send and receive crypto from any other wallet address in the world.

I had two more articles published in March on the excellent Mouthy Money website. The first is Saving versus Investing – What’s the Difference and Why You Should Do Both. People often get confused between saving and investing, and it doesn’t help that the words are sometimes used loosely and interchangeably. In reality, though, there is a clear difference between them. In this article I explain why saving should always be your first priority, but ideally you should do both.

Also in March Mouthy Money published my article Are Solar Panels Still Worthwhile? As you probably know, solar PV panels generate electricity from sunlight. Growing numbers of homeowners (me included) have them on their roofs. At one time solar panels came with generous payment tariffs known as FiTs (feed-in tariffs), but those days are long gone. So in this article I examine what incentives exist today for installing panels and whether the sums still add up. I also look at the other pros and cons of solar panels.

As I’ve said before, Mouthy Money is a great resource for anyone interested in money-making and money-saving. I am a particular fan of my fellow MM contributor and money blogger Shoestring Jane. She writes mainly about money saving and frugal living. Her latest article Save Money on Gifts Throughout the Year sets out some top tips for saving money on gifts without (of course!) being a skinflint. You can see all of Jane’s articles for Mouthy Money via this web page.

I also published several posts on Pounds and Sense in March. I won’t bother mentioning those that are no longer relevant now, but the others are listed below.

One was a reminder that the Trading 212 welcome offer has reopened. If you haven’t done this before, you can get a free share worth up to £100. As I said in the article, my free share in AMD is now worth £151.88! This offer closes on 16 April 2024.

Also in March I published Don’t Miss Out! Use Your £20,000 ISA Allowance Before It’s Too Late. This was a reminder to use your 2023/24 allowance before it vanishes on 6th April 2024. Obviously you will need to move very smartly if you are going to do this now. But (as I said earlier) the good news is that everyone will have a fresh £20,000 allowance from that date.

One other bit of news this month is that I finally got around to buying a home storage battery to connect to my solar panels (see my recent MM article about panels). I used a local (Staffordshire) company called The Energy Box for this, and am very happy to recommend them.

I’ve had my battery for just over a fortnight now and it’s been quite eye-opening. Using the battery app I can see how much electricity my solar panels are generating at any time and how much I am using in my home. I can also check the battery charge level and whether it’s charging or discharging. Even at this time of year, if there’s a bit of sunshine I am generating enough electricity in the day to cover my needs and charge the battery to a level where I’m running the house from it till well into the evening.

In the summer I’d expect to be generating enough to live off solar-generated power entirely, meaning there will only be the dreaded standing charge to pay. So I will actually be saving more money than I originally anticipated, though admittedly it will still be a number of years before the cost is covered.

It wasn’t just a financial decision, though. My other aim was to be able to continue as normal in the event of power cuts (which I expect to become more frequent in coming years as the UK transitions away from fossil fuels), and that should be the case too. The only issue might be a power cut in the depths of winter when the battery hasn’t charged up from the panels. Even so, if I know (or suspect) a cut is coming I can charge the battery in advance from the mains.

I’ve written an article going into more detail about home storage batteries (including my own) for my regular clients at Mouthy Money. This will be published in April, so keep an eye out for it!

Finally, a quick reminder that you can also follow Pounds and Sense on Facebook or Twitter/X. Twitter/X is my number one social media platform these days and I post regularly there. I share the latest news and information on financial (and other) matters, and other things that interest, amuse or concern me. So if you aren’t following my PAS account, you are definitely missing out!

That’s all for today. As always, if you have any comments or queries, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media:

As the end of the tax year on 5 April 2024 approaches, so too does the deadline to utilize the annual tax-free Individual Savings Account (ISA) allowance.

The clock is ticking, and unless you take action in the next couple of weeks, this opportunity to maximize your tax-free savings for the 2023/24 financial year will be gone forever.

ISAs are a popular choice for savers and investors alike, offering a tax-efficient way to grow your wealth. With a diverse range of options available, from cash ISAs to stocks and shares ISAs and innovative finance ISAs, individuals have the flexibility to tailor their savings strategy to suit their financial goals and risk appetite.

The current ISA allowance stands at £20,000, providing a significant opportunity to shield your savings and investments from tax. This allowance represents a generous sum that, if left unused, cannot be carried forward to future years. In essence, any portion of the £20,000 allowance that remains untapped by the upcoming deadline will be lost, representing a missed opportunity for tax-free growth.

For those who have yet to fully utilize their annual ISA allowance, now is the time to take action. Whether you’re looking to bolster your rainy-day fund with a cash ISA or seeking to invest in the stock market through a stocks and shares ISA, there’s no shortage of options available. But bear in mind that under current rules you can only invest in one of each type of ISA in any one tax year (though this rule is changing from 2024/25). So if you already invested in, say, a stocks and shares ISA this year, you are not allowed to invest in a S&S ISA with a different provider in the current tax year. You will only be able to top up your current S&S ISA to whatever remains of your total £20,000 allowance.

Cash ISAs offer a secure and accessible way to save, providing a tax-free environment for your savings with the added benefit of easy access to your funds when needed. Meanwhile, stocks and shares ISAs open the door to potential higher returns by investing in a wide range of assets such as equities, bonds, and funds, albeit with a higher level of risk. With a stocks and shares ISA you will never incur any liability for dividend tax, capital gains tax or income tax, even if your investments perform exceptionally well. Of course, there is no guarantee this will happen, but over a longer period stock market investments have typically outperformed cash savings, often by a substantial margin.

In recent years I have invested much of my own annual ISA allowance in a stocks and shares ISA with Nutmeg, a robo-manager platform that has produced good returns for me. You can read my in-depth review of Nutmeg here if you wish.

With just a few weeks left to take advantage of this valuable tax benefit, procrastination could prove costly. By acting now, you can ensure that your savings and investments are positioned to grow tax-free, setting yourself up for a better financial future.

In summary, the £20,000 annual ISA allowance for the 2023/24 tax year presents a golden opportunity for UK residents to maximize tax-free savings and investments. Time is of the essence, though, and unless you act before the impending deadline on 5th April 2024, this valuable allowance will be lost forever. If you have the money available, therefore, seize the opportunity now to help secure your financial future.

As always, if you have any comments or questions about this article, please feel free to leave them below.

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

If you enjoyed this post, please link to it on your own blog or social media:

Today I’m featuring a way you can get a free share worth up to £100 by signing up with an online share trading platform called Trading 212.

Trading 212 is unusual in that it offers commission-free and fee-free share trading. As a special offer, until 16 April 2024 they are offering people new to the platform a free share just for signing up via a referral link (such as the links in this post). The share you will get is chosen at random, but could be worth up to £100. You can either keep this share or sell it.

How to Sign Up

Signing up with Trading 212 is pretty straightforward. Just visit the Trading 212 website via any of the (referral) links in this post and follow the on-screen instructions to register. Note that you will be required to provide various items of information, including your date of birth, National Insurance number, annual income, employment status, and contact details. I understand that this is to meet their legal ‘Know Your Customer’ duty.

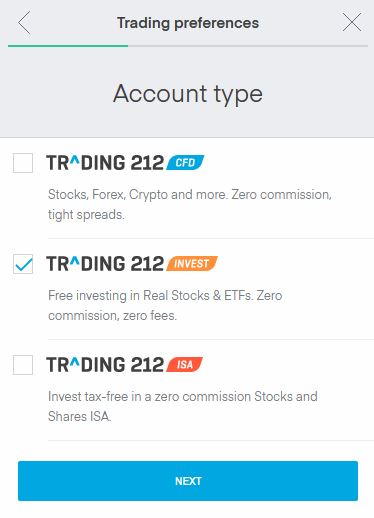

You will also need to indicate the type of account you want from the three options available (see screen capture below).

As you will see, the three account types on Trading 212 are CFD, Invest and ISA. You can apply for one, two or all three of these if you like.

CFD stands for Contract for Difference. CFDs are quite complex financial instruments, and unless you know what you’re doing I recommend giving them a miss. As you can see, you can also use this type of account for trading in Cryptocurrencies. Again this is pretty high risk and not something that appeals to me personally.

I would also recommend thinking carefully before you tick the ISA box. An ISA is, of course, a tax-exempt Individual Savings Account. Nothing wrong with that, except you can only invest in one of each type of ISA (Cash, Stocks and Shares, IFISA) in any one tax year (though this will change from April 2024).

Trading 212 are offering a Stocks and Shares ISA, so if you have already invested in one of these this year (e.g. with Nutmeg), you won’t be able to open another. Equally, once you invest in a Trading 212 ISA, you won’t then be able to open another Stocks and Shares ISA in this financial year. So you do need to be pretty sure that is how you want to use your 2023/24 Stocks and Shares ISA before doing this.

All you need to take advantage of the Trading 212 offer is a standard Invest account, so I recommend ticking this box only (as per the screen capture above).

Getting Your Free Share

There is one more step you will need to take in order to get your free share. You will need to deposit a minimum of £1 into your account. There are various ways you can do this, but i just used my debit card. There is no obligation to invest the £1 (or whatever you choose to deposit) and if you wish you can withdraw it once your free share has been credited.

The next business day you should receive an email confirming that a free share has been added to your account. As mentioned above, this is allotted at random. If you’re lucky you might get one worth up to £100. Even if you get a less valuable one, though, it’s still a share for free. If you choose to keep it, it may rise in value. There may also be dividends payable in future (and credited to your account).

Already have a Trading 212 account? You can also get a free ETF share worth up to £200 (and now guaranteed to be worth at least £10) with new DIY wealth-building app Wealthyhood. A minimum investment of £50 is required to get the free share (although if you’re not bothered about this you can start investing on the platform with as little as £20). Click through here for more info!

Selling Your Share

You can’t sell your share immediately. You have to wait three business days before doing so, but it is then just a matter of clicking the Sell button on your member’s dashboard.

The money will be credited to your Trading 212 account but you will have to wait 30 days before withdrawing it. So there may be a case for waiting to see if your share’s value goes up in that time. Of course, it could also go down!

In my case, I received a free share in the Ford Motor Company worth about £8 at the time. Obviously this wasn’t as exciting as I might have hoped, but it was still – in effect – free money for almost no time or effort 😀

How Safe Is Trading 212?

Trading 212 is registered in England and Wales and authorized and regulated by the Financial Conduct Authority. In addition, all clients’ funds are kept separately in segregated bank accounts which are covered by the Financial Services Compensation Scheme. So even if the company itself were to go broke, any cash in your account would be protected up to a value of £85,000.

Of course, the FSCS guarantee doesn’t apply to the value of your stocks and shares, which can go down as well as up. All investments carry a risk of loss, although in the case of your free share you can never lose any more than the original cost, which was of course zero!

Referral Scheme

Any Trading 212 member can also refer new members. In this case, both you and the person concerned will receive one free share worth up to £100. Obviously, the links in this blog post include my referral code – so if you register and get a free share, I will receive one also. Under the terms of the current offer you can get up to five free shares in this way. Five is the limit per person. Although you can still refer new members who will get a free share after this, as a referrer you won’t receive one as well.

Final Thoughts

I first heard about Trading 212 a while ago, but wasn’t initially sure whether it was legit and here for the long term. And I thought the free share offer was, frankly, too good to be true. However, my own experiences have been entirely positive. My original free share in the Ford Motor Company was credited the next business day as promised and I received an email notifying me about it.

I can log in to my Trading 212 account any time to see how my Ford share is doing. I have also collected a few other shares from referrals as well. These include a share in AMD (the semiconductor company), which is currently worth £151.51, and one in Nike, which is worth £88.33. I still have my original Ford Motor Company share and it has risen in value to £9.65. I also received an annual dividend payment from them a while ago. I haven’t sold any of my free shares yet but could of course do so any time I choose. I am not in any rush, as Trading 212 do not impose any platform or inactivity fees.

Although in this post I have focused on the free share offer, Trading 212 is worth considering as a share-dealing platform too. In particular, the fact that it’s fee-free and commission-free means it is well suited for people who are dipping a toe in stocks and shares investment for the first time. By contrast, the dealing fees and commissions charged by some other share-trading platforms can make small share purchases prohibitively expensive. This review by Money Savvy Daddy looks at the pros and cons of Trading 212 as a share-dealing platform in a bit more detail.

In conclusion, I hope this post has inspired you to consider registering with Trading 212 to claim your free share. If you do, I hope you get a valuable one! Please let me know what share you receive in a comment below. And, as always, any other comments or questions are very welcome too.

Don’t forget, the current free share offer ends on 16 April 2024.

Disclosure: The links in this post include my referral code. If you click through and register as described above, I will receive a free share (as will you). Please note also that I am not a qualified financial adviser and nothing in this post should be construed as individual financial advice. Everyone should do their own ‘due diligence’ before investing and seek advice from a qualified financial adviser if in any doubt how best to proceed. All investment carries a risk of loss (although not in the case of free shares, obviously).

This is an update of my original post about this special offer.

If you enjoyed this post, please link to it on your own blog or social media:

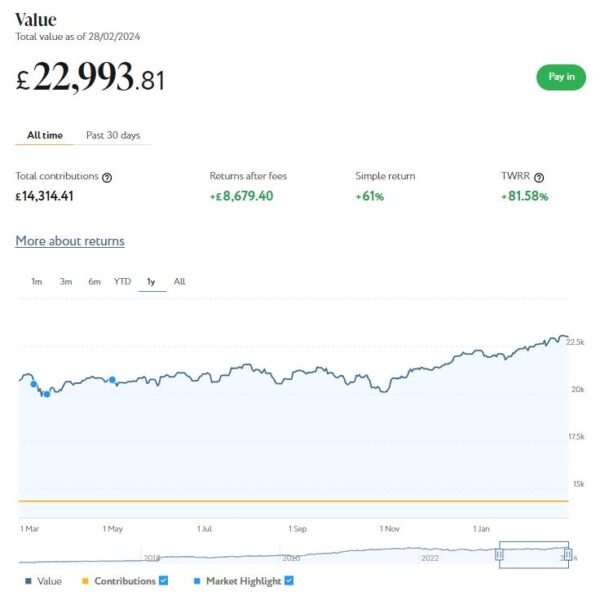

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

As the screenshot below for the last 12 months shows, my main Nutmeg portfolio is currently valued at £ £22,994. Last month it stood at £22,386 so that is a welcome increase of £608.

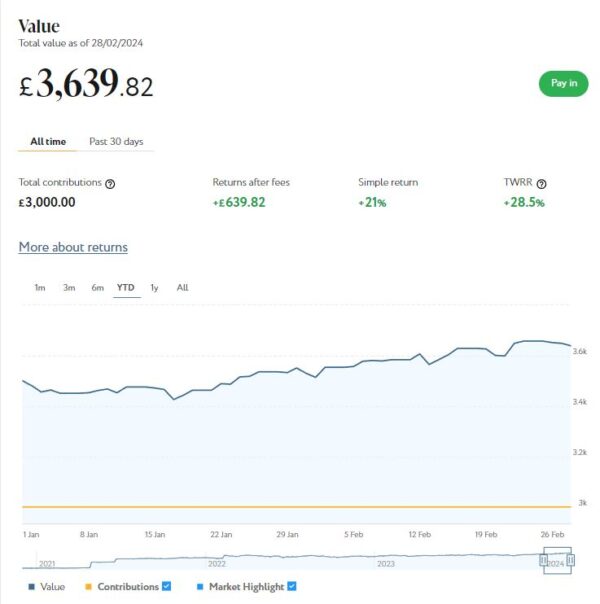

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £3,640 compared with £3,530 a month ago, a rise of £110. Here is a screen capture showing performance over the last 12 months.

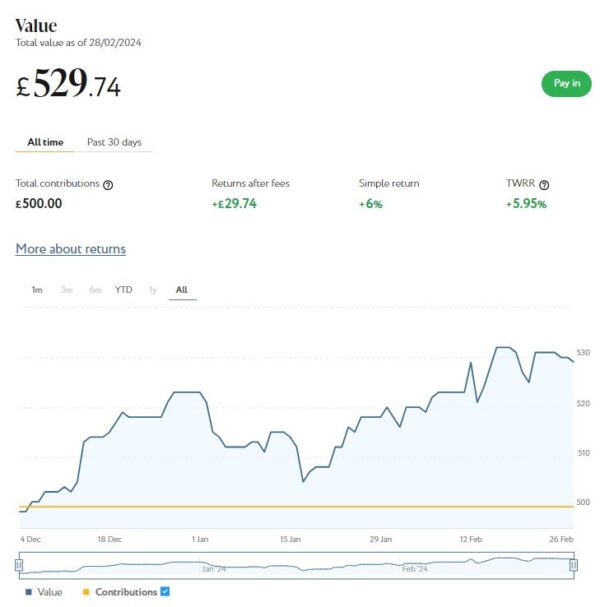

Finally, at the start of December 2023 I invested £500 in one of Nutmeg’s new thematic portfolios (Resource Transformation). As you can see from the screen capture below, this is now worth £530, an increase of £11 since last month and £30 or 6% over the three-month period since I first invested.

February was obviously a good month for my Nutmeg investments. Overall I was up £737 or 2.79%. In these turbulent times I am more than happy with that.

You can read my full Nutmeg review here (including a special offer at the end for PAS readers). If you are looking for a home for your annual ISA allowance, based on my overall experience over the last seven years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs), Lifetime ISAs and Junior ISAs as well.

Don’t forget, the current tax year ends on 5 April 2024 and after that the 2023/24 tax-free ISA allowance of £20,000 will be gone forever!

I also have investments with the property crowdlending platform Kuflink. They continue to do well, with new projects launching every week. I currently have around £1,570 invested with them in 10 different projects paying interest rates averaging around 7%. I also have £14 in my Kuflink cash account.

To date I have never lost any money with Kuflink, though some loan terms have been extended once or twice. On the plus side, when this happens additional interest is paid for the period in question.

There is now an initial minimum investment of £1,000 and a minimum investment per project of £500. Kuflink say they are doing this to streamline their operation and minimize costs. I can understand that, though it does mean that the option to test the water with a small first investment has been removed. It also makes it harder for small investors (like myself) to build a well-diversified portfolio on a limited budget.

One possible way around this is to invest using Kuflink’s Auto/IFISA facility. Your money here is automatically invested across a basket of loans over a period from one to five years. Interest rates range from 7% to around 10%, depending on the length of term you choose. Full up-to-date details can be found on the Kuflink website.

You can invest tax-free in a Kuflink Auto IFISA. Or if you have already used your annual iFISA allowance elsewhere, you can invest via a taxable Auto account. You can read my full Kuflink review here if you wish.

Moving on, my Assetz Exchange investments continue to generate steady returns. Regular readers will know that this is a P2P property investment platform focusing on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my AE portfolio has generated a respectable £168.53 in revenue from rental income. As I said in last month’s update, capital growth has slowed, though, in line with UK property values generally.

At the time of writing, 10 of ‘my’ properties are showing gains, 4 are breaking even, and the remaining 15 are showing losses. My portfolio is currently showing a net decrease in value of £40.01, meaning that overall (rental income minus capital value decrease) I am up by £128.52. That’s still a decent return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Assetz Exchange most projects are socially beneficial as well.

The overall fall in capital value of my AE investments is obviously a little disappointing. But it’s important to remember that until/unless I choose to sell the investments in question, it is largely theoretical, based on the most recent price at which shares in the property concerned have changed hands. The rental income, on the other hand, is real money (which in my case I’ve reinvested in other AE projects to further diversify my portfolio).

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of AE as far as i am concerned (especially now that Kuflink have raised their minimum investment per project to £500). You can actually invest from as little as 80p per property if you really want to proceed cautiously.

As I noted in this recent post, Assetz Exchange is particularly good if you want to compound your returns by reinvesting rental income. This effectively boosts the interest rate you are receiving. Personally, once I have accrued a minimum of £10 in rental payments, I reinvest this money in either a new AE project or one I have already invested in (thus increasing my holding). Over time, even if I don’t invest any more capital, this will ensure my investment with AE grows at an accelerating rate.

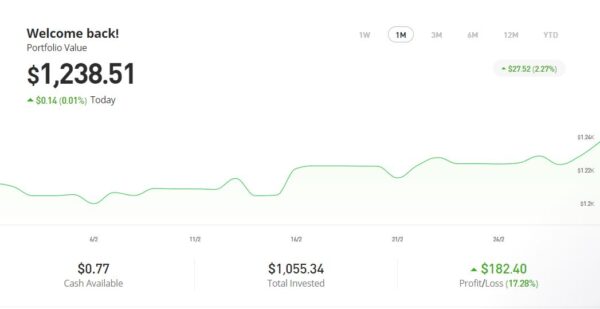

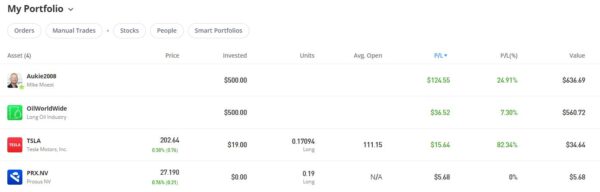

In 2022 I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios, Oil Worldwide. I also invested a small amount I had left over in Tesla shares.

As you can see from the screen captures below, my original investment totalling $1,022.26 is today worth $1,238.51, an overall increase of $216.25 or 21.15%.

eToro also offer the free eToro Money app. This allows you to deposit money to your eToro account without paying any currency conversion fees, saving you up to £5 for every £1,000 you deposit. You can also use the app to withdraw funds from your eToro account instantly to your bank account. I tried this myself and was impressed with how quickly and seamlessly it worked. You can read my blog post about eToro Money here. Note that it can also serve as a cryptocurrency wallet, allowing you to send and receive crypto from any other wallet address in the world.

I had three more articles published in January on the excellent Mouthy Money website. The first is How to Save Money on Motoring. Like everything else in life the cost of motoring is going up and up, so in this article I set out a variety of ways – from ride-sharing to driving for fuel economy – you may be able to reduce it.

Also in February Mouthy Money published Are You Making the Most of Your Annual ISA Allowance?. As mentioned earlier, the 2023/24 tax year ends in just a few weeks’ time. And after that the £20,000 tax-free ISA allowance for that year will be gone forever. In this article I describe the different types of ISA – Cash ISA, Stocks and Shares ISA, Innovative Finance ISA (IFISA) and Lifetime ISA (LISA) – and explain how they work and the differences between them. I also provide some tips and advice for making the most of your annual ISA allowance.

My final article published on Mouthy Money last month was Can You Save Money on Your Shopping with JamDoughnut? Regular PAS readers will know that I am a fan of the JamDoughnut app, which enables you to save up to 20% on purchases with a growing range of retailers. The article also reveals how you can get a £2 head-start by using my referral code.

As I’ve said before, Mouthy Money is a great resource for anyone interested in money-making and money-saving. I am a particular fan of my fellow MM contributor and money blogger Shoestring Jane. She writes mainly about money saving and frugal living. Her latest article Frugal Skills to Save You Money sets out a selection of life skills that can save you money (and aren’t hard to learn). You can see all of Jane’s articles for Mouthy Money via this web page.

I also published several posts on Pounds and Sense in February. I won’t bother mentioning those that are no longer relevant now, but the others are listed below.

In Get Your Will Written Free of Charge in March I revealed how you can get your will written (or updated) free of charge during Free Wills Month. This regular event supports a range of leading charities. Obviously the hope is that you will include a bequest to charity in your will, but there is absolutely no obligation to do this. Free Wills Month is now up and running. If you want to take advantage and get your will written free, I recommend acting now as there are only limited spots available.

Also in March I published a guest post titled Building Your Own Home – It’s Not Just for the Super Rich! This post was written on behalf of Suffolk Building Society, who are trying to raise awareness of the self-build option in the UK. As they say in the article, they can provide mortgages to purchase land suitable for self-build projects. SBS emphasize that this option is suitable and available for ‘ordinary people’, not just the super-rich folk you see on TV shows like Grand Designs!

I also published Saving for a Rainy Day or a Stormy Breakup? The Surprising Facts About Secret Savings Accounts. This post is based on some eye-opening research from my friends at Smart Money People, which revealed (among other things) that one in ten people in a serious relationship, including marriage, civil partnerships, or cohabitation, maintain a secret savings account. Find out more in this post.

Also, from January this year I became a regular contributor to the new Over 60s Discounts website. You can read my latest article here: Who Cares for the Carers? This is about help available for unpaid carers in the UK, both financial and practical. I highly recommend registering at Over 60s Discounts, by the way – they list a growing range of discounts and bonuses for older people, including some that are unique to O60D.

One other thing is that this month I switched my Santander 123 Lite current account to a Santander Edge current account. I will try to find time to write a separate post about this soon. But briefly, my main reason was because having an Edge current account allows you to open an Edge savings account, which offers a market-leading 7% interest rate (AER) for amounts of up to £4,000 for one year (it then falls to 4.5% AER).

The Santander Edge account has slightly higher fees (£3 a month as opposed to £2) and the cashback on offer is slightly less. However, when I crunched the numbers, the value of having an Edge savings account easily outweighed this. Though I am fortunate in that I had £4,000 I could put into it immediately from another, lower-paying savings account. If I hadn’t had that, it wouldn’t have been worth switching to the Edge account.

Finally, a quick reminder that you can also follow Pounds and Sense on Facebook or Twitter/X. Twitter/X is my number one social media platform these days and I post regularly there. I share the latest news and information on financial (and other) matters, and other things that interest, amuse or concern me. So if you aren’t following my PAS account, you are definitely missing out!

That’s all for today. As always, if you have any comments or queries, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media:

I recently posted about the importance of compounding to investors. In the article I pointed out that compounding, when combined with the magic of compound interest, is a powerful tool for building wealth and long-term financial success.

Compounding involves earning interest on both your initial investment and the accumulated interest from previous periods. In other words, it’s the process of generating earnings from an asset’s reinvested earnings. The more frequently your money is compounded, the faster it grows. And the longer your money remains invested, the more significant the compounding effect becomes.

A reader asked me if the effect of compounding is equivalent to getting a higher annual interest rate. The answer to that is yes, if interest is compounded more than once a year. The more times per year interest is compounded, the higher the effective annual rate becomes. The official term for this is AER, or annual equivalent rate.

In this article I thought I would explain AER in a bit more detail, as it is a very important concept for savers and investors to grasp.

What is AER?

Annual Equivalent Rate (AER) is a standardized way of expressing the interest rate on savings or investment products over a one-year period. It allows investors to compare the potential returns on different financial products on a like-for-like basis. AER takes into account the effect of compounding, providing a more accurate representation of the overall return on an investment.

Why is AER Important?

AER is crucial for investors as it helps them make more informed decisions when comparing different savings and investment options. While nominal interest rates may seem attractive at first glance, they can be misleading. AER provides a more accurate reflection of the actual return on an investment by factoring in the compounding of interest over time.

Example

Let’s consider two savings accounts:

Savings Account A offers a nominal interest rate of 7% per annum, compounded annually.

Savings Account B offers a nominal interest rate of 7% per annum, compounded quarterly.

To compare these accounts accurately, we can use the AER formula:

Where:

r is the nominal interest rate (as a decimal)

n is the number of compounding periods per year

For Account A:

For Account B:

In this example, even though both accounts have the same nominal interest rate, Account B has a higher AER due to the more frequent compounding.

Let’s now add a third savings account, Account C, again with a nominal annual interest rate of 7% but this time compounded monthly. We can calculate the AER for Account C using the formula as before:

As you can see, the AER is higher again due to the increased frequency of compounding. If compounding was even more frequent (e.g. daily) the difference would be even more pronounced. In addition, the longer the period over which you invest, the greater the difference frequency of compounding will make.

While AER is often considered with regard to savings accounts, it also applies to investments. As I said in my earlier post, with a property crowdlending platform like Assetz Exchange [referral link] which pays monthly dividends (and has low minimum investments), you can keep reinvesting the income you receive to boost the returns you make.

Understanding AER is crucial for UK savers and investors as it provides a standardized measure to compare the true potential returns of different financial products.

By taking into account the compounding effect, AER offers a more accurate picture of overall returns on investments. When evaluating savings or investment opportunities, always look beyond nominal interest rates and consider the AER to make informed decisions that align with your financial goals. And take any opportunity that arises to reinvest your returns to harness the power of compounding to grow your wealth faster.

As ever, if you have any comments or questions about this post, please do leave them below.

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

If you enjoyed this post, please link to it on your own blog or social media:

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

As the screenshot below for the last 12 months shows, my main Nutmeg portfolio is currently valued at £22,386. Last month it stood at £22,292 so that is a modest increase of £94.

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £3,530 compared with £3,501 a month ago, a rise of £29. Here is a screen capture showing performance over the last 12 months.

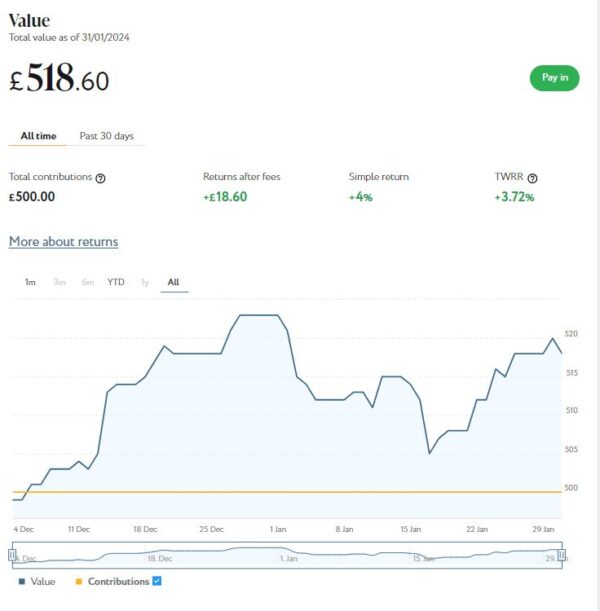

Finally, at the start of December 2023 I invested £500 in one of Nutmeg’s new thematic portfolios (Resource Transformation). As you can see from the screen capture below, after a storming start in December this fell back in January before recovering again to £519, a small drop of £4 or 0.76% month on month. It is still around 4% ahead since I invested at the start of December, though.

January was obviously a mixed month for my Nutmeg investments. Overall I was still £119 up, though. If you add this to the increase of £1,160 last month, that gives a total value increase over the last two months of £1,279 or 5.17%. In these turbulent times I am more than happy with that.

You can read my full Nutmeg review here (including a special offer at the end for PAS readers). If you are looking for a home for your annual ISA allowance, based on my overall experience over the last seven years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs), Lifetime ISAs and Junior ISAs as well.

I also have investments with the property crowdlending platform Kuflink. They continue to do well, with new projects launching every week. Last month I withdrew £350 from completed projects to help pay for a much-needed holiday in the spring. I currently have around £1,570 invested with them in 10 different projects paying interest rates averaging around 7%. I also have £14 in my Kuflink cash account.

To date I have never lost any money with Kuflink, though some loan terms have been extended once or twice. On the plus side, when this happens additional interest is paid for the period in question.

There is now an initial minimum investment of £1,000 and a minimum investment per project of £500. Kuflink say they are doing this to streamline their operation and minimize costs. I can understand that, though it does mean that the option to test the water with a small first investment has been removed. It also makes it harder for small investors (like myself) to build a well-diversified portfolio on a limited budget.

One possible way around this is to invest using Kuflink’s Auto/IFISA facility. Your money here is automatically invested across a basket of loans over a period from one to three years. Interest rates normally range from around 7% for one year to 9.83% gross for a three-year term.

As a special Valentine’s Day promotion, however, until 14 February 2024 they are offering enhanced rates of 9% for one year, 10.5% for two years and 12.25% gross for a three-year term. These figures are AER (annual equivalent rates) that incorporate reinvestment of interest paid at the end of each year. These are actually the highest rates I have ever seen Kuflink offering ❤

You can invest tax-free in a Kuflink Auto IFISA. Or if you have already used your annual iFISA allowance elsewhere, you can invest via a taxable Auto account. You can read my full Kuflink review here if you wish.

Moving on, my Assetz Exchange investments continue to generate steady returns. Regular readers will know that this is a P2P property investment platform focusing on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my AE portfolio has generated a respectable £161.85 in revenue from rental income. As I said in last month’s update, capital growth has slowed, though, in line with UK property values generally.

At the time of writing, 6 of ‘my’ properties are showing gains, 3 are breaking even, and the remaining 19 are showing losses. My portfolio is currently showing a net decrease in value of £40.87, meaning that overall (rental income minus capital value decrease) I am up by £120.98. That’s still a decent return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Assetz Exchange most projects are socially beneficial as well.

The overall fall in capital value of my AE investments is obviously a little disappointing. But it’s important to remember that until/unless I choose to sell the investments in question, it is largely theoretical, based on the most recent price at which shares in the property concerned have changed hands. The rental income, on the other hand, is real money (which in my case I’ve reinvested in other AE projects to further diversify my portfolio).

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of AE as far as i am concerned (especially now that Kuflink have raised their minimum investment per project to £500). You can actually invest from as little as 80p per property if you really want to proceed cautiously.

As I noted in this recent post, Assetz Exchange is particularly good if you want to compound your returns by reinvesting rental income. This effectively boosts the interest rate you are receiving. Personally, once I have accrued a minimum of £10 in rental payments, I reinvest this money in either a new AE project or one I have already invested in (thus increasing my holding). Over time, even if I don’t invest any more capital, this will ensure my investment with AE grows at an accelerating rate.

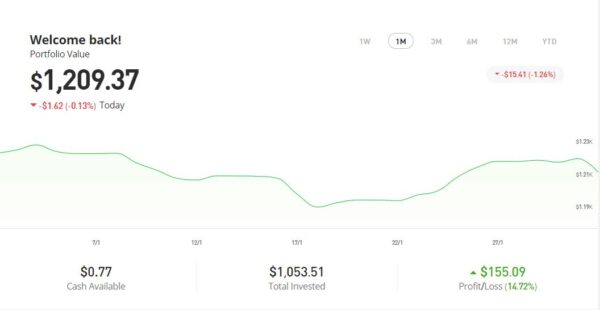

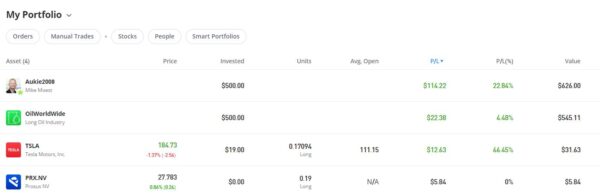

Last year I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios, Oil Worldwide. I also invested a small amount I had left over in Tesla shares.

As you can see from the screen captures below, my original investment totalling $1,022.26 is today worth $1,209.37, an overall increase of $187.11 or 18.30%.

eToro also recently introduced the eToro Money app. This allows you to deposit money to your eToro account without paying any currency conversion fees, saving you up to £5 for every £1,000 you deposit. You can also use the app to withdraw funds from your eToro account instantly to your bank account. I tried this myself and was impressed with how quickly and seamlessly it worked. You can read my blog post about eToro Money here.

I had three more articles published in January on the excellent Mouthy Money website. The first is How to Save Money on Your Water Bills. In Britain we’re lucky to have high-quality running water on tap whenever we need it. Like everything else in life it costs money, however. And in these times of rising prices and squeezed incomes, those costs can be a growing burden. So in this article I set out some ways you may be able to reduce your water bills.

Also in January Mouthy Money published How to Make Money With Classic Cars. In this article – written in association with my friends at the Car & Classic website – I described the surprising number of attractions to investing in classic cars, and provided a range of tips for those new to the field.

My final article published on Mouthy Money last month was Top Tips to Avoid Online Scams. This article set out my top ten tips for staying safe online and avoiding becoming a victim of the scammers. Do check it out!

As I’ve said before, Mouthy Money is a great resource for anyone interested in money-making and money-saving. I particularly like the ‘Deals of the Week’ feature compiled by Jordon Cox (‘Britain’s Coupon Kid’) which lists all the best current money-saving offers for savvy shoppers. Check out the latest edition here.

I am also a fan of my fellow MM contributor and money blogger Shoestring Jane. She writes mainly about money saving and frugal living. Her latest article How to Get Almost Everything More Cheaply has some great tips and ideas. You can see all of her articles for Mouthy Money via this web page.

I also published several posts on Pounds and Sense in January. I won’t bother mentioning those that are no longer relevant now, but the others are listed below.

In How to Start Copy Trading With eToro I discussed how to get started using the popular copy trading facility on eToro. This allows you to automatically copy successful traders on the platform – so when they make money, you make money too. As mentioned above, I have done this myself following Dutch professional investor Mike Moest and am currently around 23% in profit. You can read more in my post about copy trading on eToro and my experiences with it.

I also published HMRC Crackdown on Side Hustles – Truth and Fiction. As you may know, from January this year digital platforms like eBay, Etsy and Airbnb are required to collect additional information from sellers, including numbers of sales and amount of income generated. This data will be automatically shared with HMRC, who will compare it against their records to see if any tax may be due. This news has caused some consternation on social media, with many who have side hustles to help pay the bills worried they may be hit by an unexpected tax demand. In this post I explain what exactly is happening and set out to separate the truth from the fiction.

In Planning a UK Holiday This Year? Here Are Some Ideas For You! I set out a list of destinations in the UK I have visited myself, with links to my full reviews of the places concerned. They range from Bath to Barmouth, Lavenham to Llanbedrog. If you’re looking for ideas for a short break (or longer) in the UK this year, this could be a good source of inspiration for you 🙂

One Key Lesson About Investing I Learned From My Dad’s Big Mistake reveals an important lesson I learned from my late father about investing. It is a lesson I have tried to apply in all my investing myself. While it hasn’t stopped me making some mistakes along the way, it has certainly helped me avoid any disastrous losses. This article was first published in a slightly different form on Mouthy Money.

Finally in January I published How to Harness the Power of Compounding. In this article I discussed the power of compounding and compound interest. This is a wealth-building secret every saver and investor should embrace. I also revealed two particular types of investment where you can apply compounding to help boost your returns.

Also, from January I have become a regular contributor to the new Over 60s Discounts website. You can read my first article here: How to Cope With Loneliness in Later Life. As you may gather, as well as personal finance I will also be writing about ‘lifestyle’ matters for O60D.

On other things, the opportunity to get a free share worth up to £100 with Trading 212 has now closed. However, you can can also still Get a Free ETF Share Worth up to £200 with Wealthyhood. This DIY wealth-building app is aimed especially at people new to stock market investing. The minimum investment to qualify for the free share offer is £50 – but on the plus side, they now guarantee your free ETF share will be worth at least £10.

I am still using and getting good results from the cashback app JamDoughnut. You can see my review of JamDoughnut here, along with a referral code that will get you a £2 bonus when you sign up. To be honest I’m surprised more PAS readers haven’t taken advantage of this opportunity. Not only can you get discounts of up to 20% using the app, they also hold regular contests and promotions offering additional bonuses and discounts.

Finally, a quick reminder that you can also follow Pounds and Sense on Facebook or Twitter/X. Twitter/X is my number one social media platform these days and I post regularly there. I share the latest news and information on financial (and other) matters, and other things that interest, amuse or concern me. So if you aren’t following my PAS account, you are definitely missing out!

That’s all for today. As always, if you have any comments or queries, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media:

In the world of investing, there’s a powerful force that has the potential to turn small contributions into substantial wealth over time.

This force is known as compounding, and when combined with the magic of compound interest, it becomes a powerful tool for building wealth and long-term financial success.

For savers and investors, harnessing the power of compounding can be the key to achieving your financial goals.

The Basics of Compounding

Compounding is a simple yet highly effective concept that involves earning interest on both your initial investment and the accumulated interest from previous periods. In other words, it’s the process of generating earnings on an asset’s reinvested earnings. The longer your money remains invested, the more significant the compounding effect becomes.

Let’s consider a hypothetical scenario to illustrate the point. If you invest £1,000 with an annual interest rate of 5%, you would earn £50 in the first year. In the second year, however, you wouldn’t just earn interest on your initial £1,000, you would also earn interest on the £50 you earned in the first year (at 5% that would be another £2.50). Over time, this compounding effect can result in exponential growth.

The Magic of Compound Interest

Compound interest takes compounding to the next level. Unlike simple interest, where you only earn interest on the principal amount, compound interest allows you to earn interest on both the principal and the previously earned interest. This compounding occurs at regular intervals, such as annually, quarterly, or monthly, depending on the investment vehicle. In general, the more frequently compounding occurs, the faster your money will grow.

Compound interest can make a significant difference to the growth of your wealth. Whether you’re investing in stocks, bonds, or other financial instruments, the power of compound interest allows your money to work harder for you, potentially accelerating your journey towards financial freedom.

The Importance of Time in Wealth Building

A critical factor in maximizing the benefits of compounding and compound interest is time. The earlier you start investing, the longer your money has to grow, and the more substantial the compounding effect becomes. This is sometimes referred to as the ‘time value of money’.

For example, let’s compare two imaginary investors, Jane and Bob. Jane starts investing £1,000 per year at the age of 25 and continues until she’s 35, contributing a total of £11,000. Bob, on the other hand, starts investing the same amount at 35 and continues till he’s 65, contributing a total of £31,000.

Assuming an annual return of 7%, Jane’s investments will grow significantly more than Bob’s due to the extra years of compounding, despite the fact she invested £20,000 less than Bob in total. In this scenario, Jane’s investment would grow to over £193,000 by the time she is 65, while Bob’s would reach around £148,000. The difference is striking and emphasizes the importance of an early start in wealth building.

Key Steps for Investors

Start Early: The earlier you begin investing, the more time your money has to compound and grow. Even small amounts invested regularly can lead to substantial wealth over the long term.

Reinvest Earnings: Instead of cashing out your investment earnings, reinvest them to take full advantage of compounding. Reinvesting dividends and interest compounds your returns, accelerating wealth accumulation.

Diversify Your Portfolio: A diversified investment portfolio helps spread risk and enhances long-term returns. Consider a mix of stocks, bonds and other assets to optimize your investment strategy.

Stay Disciplined: Consistency is key when it comes to compounding. Stick to your investment plan, contribute regularly, and avoid unnecessary withdrawals to maximize the long-term benefits.

Practical Examples

Although compounding is often discussed in regard to cash savings, as indicated above the principle applies very much with stock-market-type investments as well.

To take one example from my own experience, regular readers will be aware that I have some money in the P2P property investment platform Assetz Exchange [referral link]. This platform specializes in relatively low-risk social housing projects where rents are typically paid by charities and housing associations or the government (e.g. asylum seeker hostels). Here is a link to my original review of Assetz Exchange.

With all my AE investments, I receive pro rata rental distributions every month. My investment is quite modest so these aren’t huge amounts in themselves. But once they have added up to a reasonable sum (say £10 or more) I reinvest them in another AE project or increase my holding in an existing one. From the following month I then start receiving distributions from these investments as well. That means my investment and monthly returns are building steadily, month by month, through the power of compounding.

Obviously that’s just one example. But Assetz Exchange works particularly well for this, as the minimum investment per project is so low (as little as 80p in some cases). So even if you are only investing relatively small amounts like me, you can still harness the power of compounding to grow your money.

That’s just one possible approach, of course. Another would be to invest in dividend-paying shares and reinvest the dividends when they arrive in more such shares. This approach to investment was discussed a while ago on PAS in a guest post by Lewys Lew.

Whatever your chosen investment vehicle, reinvesting your interest, income or dividends will help you grow it faster using the power of compounding.

Final Thoughts

As I hope I’ve shown in this post, the power of compounding and compound interest is a wealth-building secret every investor should embrace.

By understanding these concepts and implementing a disciplined and long-term investment strategy, you can harness the power of compounding to achieve your financial goals.

Start early, stay committed, and let compounding work its magic on your road to financial success 🙂

As always, if you have any comments or questions about this post, please do leave them below.

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

If you enjoyed this post, please link to it on your own blog or social media:

Let me tell you about my dad. He was a kind, thoughtful man and I learned many important things from him. But money was, sadly, never his strong point.

Here’s an example. Quite a few years ago a family member persuaded him to invest all his spare cash in a media services business a friend of a friend was setting up.

I didn’t hear about this till after the investment had been made. But even though I was much younger then, I could still see it was insanely risky.

It was a new business with no track record. And Dad knew nothing whatsoever about the media – he was a carpet-fitter turned hydraulic machinery salesman. And perhaps sensing that his wife (my stepmother) would disapprove, he didn’t actually bother to tell her about it.

For the next year or so, any time my partner Jayne and I went to visit, Dad would find an opportunity to take us aside at some point to give us an update. Inevitably this would begin with a conspiratorial, “Don’t tell Shirley, but…”

At first the news seemed encouraging, but soon it became clear the business was going south and Dad’s money was going with it. I’ll never know the full story, but it seemed to me he was badly advised (to put it kindly) by the relative concerned and quite probably cheated by the main shareholder, though it was all technically within the law.

Eventually he had to confess to my stepmother that he had lost most of their life savings. This inevitably caused a rift between them and had further ramifications that continued for the rest of their lives.

This whole incident was, of course, deeply traumatic for the whole family. The one good thing it taught me was the folly of putting all your eggs in one basket when investing.

I vowed I would never make that mistake with my own investments and have therefore always aimed to diversify as widely as possible. To date that principle has served me well.

How to Diversify

There is no one single recipe for successfully diversifying your investments, but here are some guidelines I have tried to follow myself.

Don’t even think about investing until you have paid off any interest-charging debts. You should also have at least three months’ of income in easily accessible form in case of sudden, unexpected emergencies. An instant access cash ISA (see below) might fit the bill.

Don’t invest more than a small proportion of your portfolio in single company shares. You will get much better diversification by investing in a fund that includes a broad range of shares and other investment products.

Aim to invest not only across different companies but different countries, sectors, industries, and so on. A well-diversified global fund can do this for you.

Make full use of your tax-free ISA allowance. This is currently a generous £20,000 a year. Investing via a reputable stocks and shares ISA can save you thousands of pounds in tax.

For further diversification you might also consider investing a small amount in an Innovative Finance ISA. IFISAs let you invest in peer-to-peer lending. While riskier than bank savings, the potential returns from this are also better. Each year you are allowed to invest in one IFISA as well as one stocks and shares ISA and one cash ISA, as long as you keep within the annual £20,000 limit. [Note: the rule about only investing in one of each type of ISA per year is being abolished from the start of the 2024/25 financial year.]

With a well-diversified portfolio, you greatly improve the chances that if one or more of your investments fails to perform, others will compensate. And whatever happens in the world, your overall investment pot will hopefully build over the years into a substantial sum.

Whatever you do, though, pleasedon’t make my dad’s mistake and put all your money into a single business (or other investment), especially if it’s one you don’t understand. That really is the fast track to a financial meltdown!

Disclaimer: I am not a qualified financial adviser and nothing in this post should be construed as personal financial advice. All investment carries a risk of loss. You should always do your own ‘due diligence’ before investing and consult a professional financial adviser if in any doubt how best to proceed.

This is an updated version of an article originally published on the Mouthy Money website.

If you enjoyed this post, please link to it on your own blog or social media:

In my post today I’m focusing on the trading and investment platform eToro. I originally reviewed eToro in this post.

eToro is a global fintech company with its HQ in Israel. The company has registered offices in Cyprus, the UK, the US and Australia. It is a hugely popular platform with 25 million customers from over 140 countries across the world. They offer a range of share trading and investment services.

eToro is regulated and authorised in the UK by the Financial Conduct Authority (FCA) and is covered by the Financial Services Compensation Scheme (FSCS). That means if eToro were to go bust any cash deposits with them up to £85,000 would be protected. Of course, the FSCS doesn’t protect you if you lose money simply due to your investments performing poorly.

What is Copy Trading?

Copy trading is a very popular feature of eToro. As mentioned, it allows you to automatically copy the trades of established eToro investors and benefit from the profits they (hopefully) make.

eToro has hundreds, probably thousands, of approved ‘popular investors’ whose trades you can copy automatically on the platform. They each have a profile page where you can find out more about them and their investment strategy.

On a trader’s profile page you can see various stats about them, including how many copiers they have and how many people are following them. You can also check their profits over various timeframes (though of course this is no guarantee of how successful they will be in the future).

eToro operates in US Dollars, though that isn’t an issue for UK investors (see tips, below). There’s a minimum investment of $200 (around £165) for copy trading. However, many approved traders recommend a higher minimum than this. That’s because, when you sign up to copy a trader, eToro automatically duplicates all of that person’s trades in proportion to the size of your investment.

eToro has a minimum investment size of $1 and if a trade would work out less than that pro rata it won’t be executed. It follows that traders whose strategies typically involve placing large numbers of relatively small trades generally recommend a higher minimum starting investment.

One of the biggest attractions of copy trading is that no charges are payable. The traders in question receive commission from eToro for the business they bring in for the company. So in effect you are getting privileged access to the skills and expertise of these people at no cost to yourself.

You are allowed to copy up to 100 different popular investors, though you can of course start with just one.

How to Copy a Trader

Before you can start copy trading, you will need to register for an account with eToro and deposit some funds with them. I talked about this in my original eToro review.

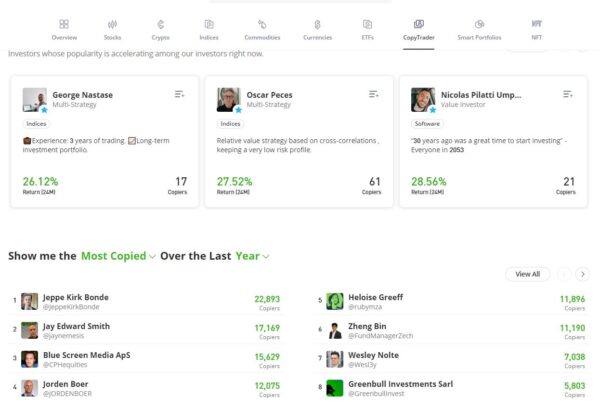

Once you have done this, you can check out popular investors on the platform by clicking on Discover in the left-hand menu of your dashboard when logged on, then clicking on CopyTrader near the top.

A new page will open showing the most popular copy traders and also those whose copier numbers are currently growing the fastest (probably due to good recent performance). Here’s a screen capture showing part of this page at the time of writing:

.

You can also use the search facility to search for popular investors according to where they are based, what they invest in, and how much profit they have made within a certain period.

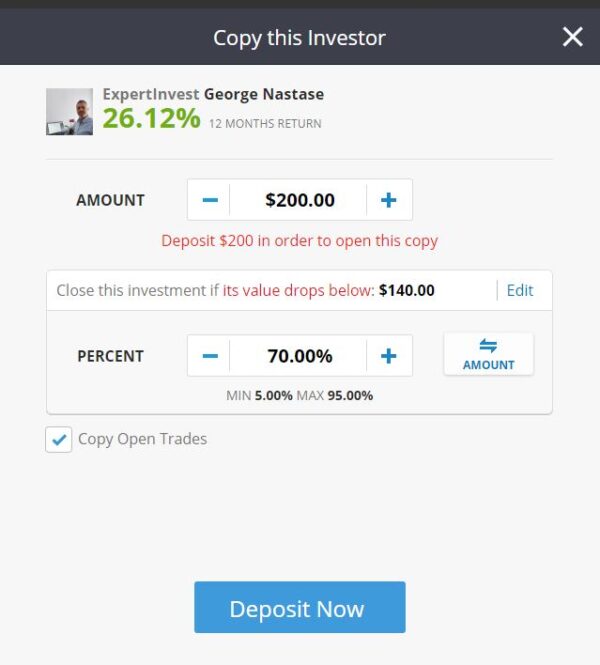

Once you’ve found an investor you want to copy, click on the green ‘Copy’ button on their profile page. A pop-up box such as the one below will then appear. Enter the total amount you want to invest at the top.

You also have to choose whether you want to copy all existing open positions as well as new ones. ‘Copy Open Trades’ is the default, and if you want to do this you should leave the box in question ticked. If you uncheck the box, only new trades opened after you start investing will be copied.

One drawback with copying all open positions is that you’ll be investing in these trades at the current price, whatever it is, instead of the price when the trader concerned opened their position. If the price has gone up since then, the profit potential may be less. On the other hand, if you opt only to copy new trades, it may be some time before your money is fully invested. There are pros and cons either way, but ultimately the longer you stay invested, the less difference this decision is likely to make.

Another choice to make here concerns the CopyTrader Stop Loss (CSL). If your copy value falls by that amount, the CSL will automatically terminate the copy relationship and return the remaining money to your eToro balance. You can set this figure anywhere between 5% and 95%. My advice is not to set it too high, as even a brief ‘wobble’ will then trigger the stop loss and crystallize your losses (see tips, below).

If any of the above sounds at all daunting, note that everyone on eToro also gets a $100,000 virtual portfolio to practise with. You can copy trade using this virtual money to see how the process works and what returns you make.

My Experience of Copy Trading

In June 2022 I invested $500 (then about £412) copying a Netherlands-based eToro trader called Aukie2008 (real name Mike Moest). I chose him for various reasons, including his eToro profit record and the number of followers he had already.

On his profile page he came across as a likeable, straight-talking individual, as well as being an experienced and knowledgeable trader. He posted regular updates on his strategies and on investing generally. I also liked the fact that he always took the trouble to answer questions posted by his followers. His recommended minimum starting investment was $500.

Unsurprisingly in these volatile times, my investment has been up and down, but it is currently (after 18 months) about $125 (25%) in profit. All things considered I am very happy with that.

In due course I may top up my copy trading investment with Aukie2008. I may also diversify my investments, either by following another approved trader or perhaps via another themed smart portfolio. As regular PAS readers will know, a few months ago I invested $500 in the Oil Worldwide smart portfolio. As the screen capture below shows, this has done okay, though not as well as my copy trading investment. It’s still early days, though.

Top Tips for Copy Traders

Here are some top tips to help you make the most of the copy trading facility on eToro. These are based partly on my own experiences, but also on other comments and advice I have seen.

As mentioned above, check the minimum recommended investment for any trader you are thinking of following and be sure to invest this amount of money or more.

Note also the risk score assigned by eToro. Each approved trader is allocated a score between 1 and 10, with 1 representing very low risk and 10 the highest. Scores are based on the number, size and type of trading activities they engage in. If you are just starting out you might prefer to begin with someone relatively low risk (say 5 or lower) and work up from there as you gain experience on the platform.

Other things being equal, when following a trader I recommend choosing ‘Copy Open Trades’. This will ensure all your money is put to work immediately. As mentioned above, it does mean some positions may not have the same profit potential as when they were opened, but the longer you remain invested, the less this will matter overall.

Also, as mentioned earlier, don’t set your CSL too high. Doing so will mean even a slight wobble may trigger your stop loss and crystallize your losses. Personally I wouldn’t set this figure any higher than 70%, but it’s your decision, of course, based on your tolerance for risk.

To keep currency conversion costs to a minimum, I strongly recommend opening a separate eToro Money account. This will allow you to deposit instantly to your eToro account without paying currency conversion fees or charges.

Remember one key principle of successful investing is diversification. You should therefore consider copying a number of traders with different investment strategies rather than just one. In addition, eToro offers a range of other investment opportunities as well, including individual company shares and themed portfolios.

Even though you’re following an approved trader, you should still monitor his/her results carefully and be prepared to switch if it seems they are losing their touch.

I recommend reading all the updates on the trader’s profile page too. Not only do these provide valuable background about their strategies, you can also learn a lot about the thought processes of professional traders.