My Investments Update – December 2021

As regular readers will know, I recently started posting monthly updates about my investments. These partly replace the ‘Coronavirus Crisis Updates’ I was posting from March 2020. You can read my November 2021 Investments Update here if you like

I’ll begin as usual with my Nutmeg Stocks and Shares ISA, as I know many of you like to hear what is happening with this.

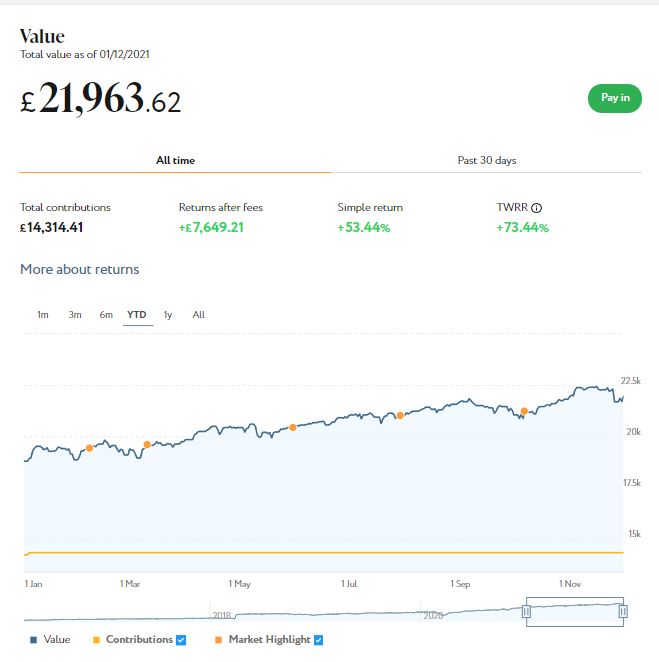

As the screenshot below shows, my main portfolio is currently valued at £21,963. Last month it stood at £21,940, so that is a modest rise of £23. Those figures don’t tell the whole story, though. In the early part of November, the value of this portfolio rose as high as £22,398. Unfortunately then news of the new Omicron variant spooked the markets and share prices fell dramatically. In the last few days there has been a modest recovery, resulting in the small month-on-month gain referred to above.

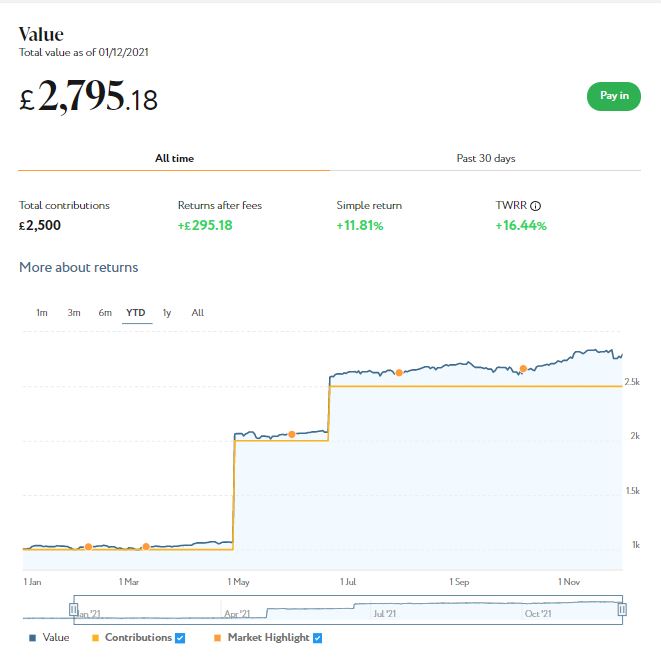

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This has followed a similar trajectory, though it has actually done a bit better than my main pot. It is now worth £2,795 compared with £2,756 last month, a net monthly increase of £39. Here is a year-to-date screen capture showing performance to the start of December 2021.

As I always say, you shouldn’t judge the performance of any equity-based investment on a month-by-month basis. But in these strange times I remain very happy with how my Nutmeg investments are doing. Hopefully the initial panic over Omicron may prove to have been excessive (it may help that there is growing evidence that this new variant typically causes only a mild illness). That being the case, I remain optimistic that the modest recovery in the markets over the last few days will continue.

You can read my full Nutmeg review here (including a special offer at the end for PAS readers). If you are still looking for a home for your 2021/22 ISA allowance, based on my experience they are certainly worth considering. If you haven’t yet seen it, check out also my blog post in which I looked at the performance of Nutmeg fully managed portfolios at every risk level from 1 to 10 (my main port is level 9). I was actually pretty amazed by the difference the risk level you choose makes. If you are investing for the long term (and you almost certainly should) in my view opting for a hyper-cautious low-risk strategy may not be the smartest thing to do.

As regular readers will know, this year I am using Assetz Exchange for my IFISA. This is a P2P property investment platform that focuses on lower-risk properties (e.g. sheltered housing on long leases). I have invested a total of around £1,000 in AE so far (I began with £100 in February 2021 and topped up twice).

Since I opened my account, my portfolio has generated £29.50 in revenue from rental and £45.86 in capital growth, for a total return of £75.36. I won’t bother publishing a statement on this occasion as it’s not massively different from last time. The bottom line is that I (still) have investments in 21 different projects with them and all are performing as expected, generating income and in most cases showing a profit on capital. So I am very happy with how this investment has been going.

- To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of AE as far as i am concerned. You can actually invest from as little as 80p per property if you really want to proceed cautiously.

As mentioned, my investment on Assetz Exchange is in the form of an IFISA so there won’t be any tax to pay on profits, dividends or capital gains. I’ve been impressed by my experiences with Assetz Exchange and the returns generated so far, and intend to continue investing with them. You can read my full review of Assetz Exchange here if you like. You can also sign up for an account on Assetz Exchange directly via this link [affiliate].

Another property platform I have some investments with is Kuflink [referral link]. They appear to be doing well, with new projects launching almost every day. I currently have just over £2,000 invested with them, quite a large proportion of which comes from reinvested profits. To date I have never lost any money with Kuflink, though some loan terms have been extended once or twice. On the plus side, where this happens additional interest is paid for the period in question.

My loans with Kuflink pay annual interest rates of 6 to 7.5 percent. As mentioned above, these days I invest no more than around £100 per loan (and often less). That is not because of any issues with Kuflink but more to do with losses of larger amounts on other P2P property platforms (such as this one). My days of putting four-figure sums into any single property investment are behind me now!

Nowadays I mainly opt to reinvest the monthly repayments I receive from Kuflink, which has the effect of boosting the percentage rate of return on the projects in question

You can read my full Kuflink review here. They offer a variety of investment options, including a tax-free IFISA paying up to 7% interest per year with built-in automatic diversification. Alternatively you can now build your own IFISA, with most loans on the platform being IFISA-eligible.

I’d also particularly draw your attention to their revised and more generous cashback offer for new investors. They are now paying cashback on new investments from as little as £500 (it used to be £1,000). And if you are looking to invest larger amounts, you can earn up to a maximum of £4,000 in cashback. That is one of the best cashback offers I have seen anywhere (though admittedly you will need to invest £100,000 or more to receive that!).

Kuflink has some similarities with Assetz Exchange (see above). However, it’s important to note that with Kuflink you are investing in loans secured by property, whereas with Assetz Exchange your money is going into actual bricks and mortar. Kuflink loans typically pay around 7% annual interest. With Assetz Exchange projected yields from rental are generally a bit lower at around 5%, but you do of course have the potential for capital appreciation as well. There is also an argument that investments on AE are more secure as properties are typically rented out to organizations such as housing associations which are publicly funded. But I should emphasize that over the years I have been investing with Kuflink I have never lost any money with them and I understand nobody else has either. That is of course no guarantee it couldn’t happen in the future, but personally I find it quite reassuring.

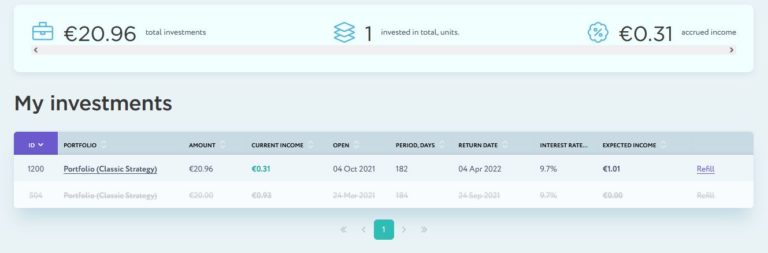

I haven’t mentioned my trial investment on European loan crowdfunding platform Nibble for a while, so thought I should remedy that this month. This has been proceeding without any issues. My initial test investment of 20 euros matured in September so I reinvested the entire sum at the same annual interest rate of 9.7 percent (see screen capture below).

I get weekly updates from Nibble confirming how much interest has been added to my account. Money has been a bit tight recently so I haven’t topped up my initial investment. Once I start getting my state pension (see below), however, I should have more available to invest, and Nibble is definitely on my list. My full review of Nibble can be found here.

Moving on, I have another article on the always-excellent Mouthy Money website. This is about how to save money on your motoring costs. I enjoyed researching this and learned some new and surprising things while doing so!

I’d also like to remind you that I am participating in not one but two pre-Christmas giveaways. One of these offers the chance to win a Hotel Chocolat Velvetiser kit worth around £150 in total. And the other giveaway has an amazing prize of cash and goods from homeware brand Arca valued at over £1,000 in total. Do check them both out (if you haven’t already) and get your entries in. It would be great if a Pounds and Sense reader were to win one (or both) of these great prizes 🙂

Finally, as I mentioned in this blog post, December 2021 marks a landmark for me, as I shall reach my 66th birthday and qualify for the new state pension. I am due to get my first payment on Christmas Eve. Tempting though it is, I probably won’t be blowing it all on a big party! 🎈🎈🎈

That’s all for now, so please stay safe (and warm) in these challenging times. And please don’t let scare stories in the mainstream media freak you out. At the time of writing hospitalizations and deaths from Covid in the UK have actually been falling steadily for weeks. So despite what the fear-mongers would have you believe, it really isn’t all bad news!

Have a lovely Christmas, enjoy socializing with friends and family, and I’ll be back again with another investments update at the start of 2022.

As always, if you have any comments or questions about this post, please do leave them below.