My Investments Update – December 2022

Here is my latest monthly update about my investments. You can read my November 2022 Investments Update here if you like

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension). I will discuss the latter a bit further down.

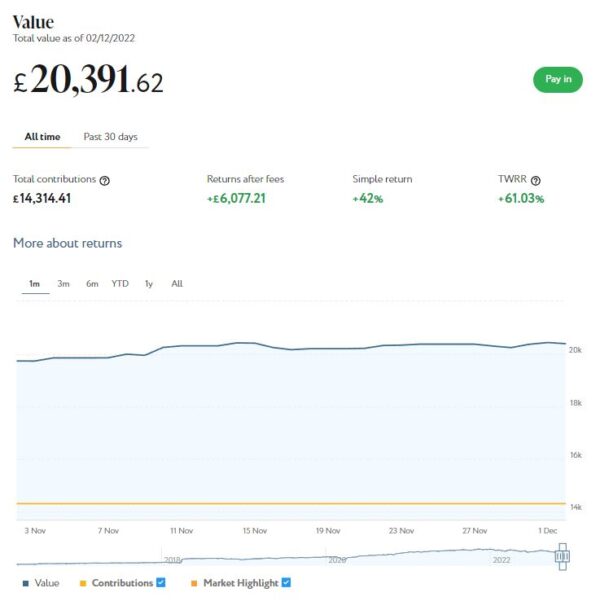

As the screenshot below of performance last month shows, my main Nutmeg portfolio is currently valued at £20,391. Last month it stood at £19,733 so that is a rise of £658.

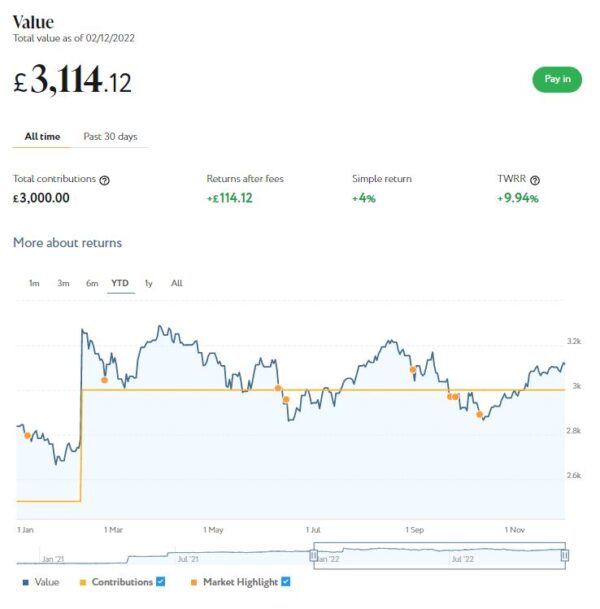

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £3,114 compared with £2,987 a month ago, an increase of £127.

Here is a screen capture showing performance since January 2022. As you can see, I topped up this account in February this year.

That is an overall month-on-month increase of £785. Furthermore since mid-October the total value of my Nutmeg investments has risen by £2,007 or around 8%. Anyone who was brave enough to invest in Nutmeg around the middle of October will therefore be looking at a substantial profit now. Of course, it’s always easy to spot an investment opportunity with 20/20 hindsight!

In my case, while the recent rises are very welcome, my Nutmeg investments are still down £1,607 or about 6.5% since the start of the year. To put this in context, though, in 2021 they rose by £3,552 (over 21%). And overall, I am still over £6,000 ahead since I started investing with Nutmeg in 2016. For my main portfolio that represents a return on capital of 42% or 51.03% time-weighted.

Of course, the real point of this is that investing is (or should be) a long-term endeavour. Over a period of years stock market investments such as those used by Nutmeg typically produce better returns than cash accounts, often by substantial margins. But there are never any guarantees, and in in the short to medium term at least, losses are always possible.

You can read my full Nutmeg review here (including a special offer at the end for PAS readers). If you are looking for a home for your annual ISA allowance, based on my experience over the last six years, they are certainly worth considering.

Moving on, my Assetz Exchange investments continue to perform well. Regular readers will know that this is a P2P property investment platform focusing on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my AE portfolio has generated £88.30 in revenue from rental and £17.59 in capital growth, a total of £105.89. That’s a decent rate of return on my £1,000 investment and does illustrate the value of P2P property investment for diversifying your portfolio when equity markets are volatile.

I now have investments in 23 different projects and all are performing as expected, generating rental income and in most cases showing a profit on capital as well. So I am very happy with how this investment has been doing. And it doesn’t hurt that most projects are socially beneficial as well.

- To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of AE as far as i am concerned. You can actually invest from as little as 80p per property if you really want to proceed cautiously.

My investment on Assetz Exchange is in the form of an IFISA so there won’t be any tax to pay on profits, dividends or capital gains. I’ve been impressed by my experiences with Assetz Exchange and the returns generated so far, and intend to continue investing with them. You can read my full review of Assetz Exchange here. You can also sign up for an account on Assetz Exchange directly via this link [affiliate].

Another property platform I have investments with is Kuflink. They continue to do well, with new projects launching almost every day. I currently have around £2,600 invested with them in 14 different projects. To date I have never lost any money with Kuflink, though some loan terms have been extended once or twice. On the plus side, when this happens additional interest is paid for the period in question. At present most of my Kuflink loans are performing to schedule, though two recently had their repayment dates put back by three months.

My loans with Kuflink pay annual interest rates of 6 to 7.5 percent. These days I invest no more than £200 per loan (and often less). That is not because of any issues with Kuflink but more to do with losses of larger amounts on other P2P property platforms in the past. My days of putting four-figure sums into any single property investment are behind me now!

- Nowadays I mainly opt to reinvest the monthly repayments I receive from Kuflink, which has the effect of boosting the percentage rate of return on the projects in question

Obviously a possible drawback with Kuflink and similar platforms is that your money is tied up in bricks and mortar, so not as easily accessible as cash savings or even (to some extent) shares. They do, however, have a secondary market on which you can offer any loan part for sale (as long as the loan in question is performing and not in arrears). Clearly that does depend on someone else wanting to buy it, but my experience has been that any loan parts offered are typically snapped up very quickly. So if an urgent need arises, withdrawing your money (or part of it) is unlikely to be an issue.

You can read my full Kuflink review here. They offer a variety of investment options, including a tax-free IFISA paying up to 7% interest per year with built-in automatic diversification. Alternatively you can now build your own IFISA, with most loans on the platform (including the one shown above) being IFISA-eligible.

My investment in European crowdlending platform Nibble continues to perform as advertised. My latest investment was in their Legal Strategy. These are loans that are in default and facing legal action. Nibble buy these loans at a heavily discounted rate and then seek to recover as much as possible of the money owed. The minimum investment is 10 euros and the minimum period is six months. I invested 100 euros for 12 months initially at a target annual interest rate of 12.5%.

The Legal Strategy comes with a deposit-back guarantee. This is a guarantee to return the full investment amount at the end of the investment period and a minimum yield of 9% per year. The actual yield depends on how successful recovery efforts prove, so in practice you may end up with a return of anywhere between 9% and 14.5%. All has gone to plan so far, but I will obviously continue to report on this in the months ahead.

- You can read my updated review of Nibble here if you like. You can also sign up directly on the Nibble website [affiliate link].

Earlier this year I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest). My investment has been up and down in the last few months, but it is currently $38 (about £31) in profit. In these turbulent times I am quite happy with that.

In any event, I’m looking on this as a long-term investment so won’t be judging it yet. I am also considering a further investment with eToro, possibly in one of their themed portfolios. You can read my full review of eToro here. You may also like to check out my recent more in-depth look at eToro copy trading.

Moving on, earlier I mentioned my Bestinvest SIPP (personal pension). This is now in drawdown, but regular readers will know that I suspended withdrawals from it in May this year to reduce the risk of pound-cost ravaging. I was able to do this because since December 2021 I have been receiving the state pension. And in association with my other income streams this has given me enough to live on (though by no means in luxury).

Anyway, with the cost of living crisis starting to bite, and energy bills shooting up at an alarming rate, I decided the time had come to resume taking payments from my SIPP. Plus, with the markets seemingly on an upward trajectory, the risk of pound-cost ravaging appeared to have receded.

I therefore asked Bestinvest to reinstate my payments from this month, though at a lower rate of £100 a month. One of the attractions of flexible drawdown pensions such as those from Bestinvest is that you can increase or decrease withdrawals at any time or even (as I did) suspend them completely. Obviously if you draw an excessive amount there is a risk of depleting your fund too quickly, so it runs out before you do. But Bestinvest sent me some reassuring projections that in any feasible scenario this was unlikely to happen in my case even if I live to the age of 99 (as I fully intend to 😀 ).

One other consideration I had with my SIPP is that withdrawals from it are taxable, whereas withdrawals from some of my other investments (e.g. Nutmeg ISA) are not. With the state pension also being taxable, this means withdrawing larger amounts from my SIPP would result in a portion of the money being grabbed by the taxman, which seems a waste. While I do of course accept that taxes have to be paid, I prefer to minimize my liability as much as possible (which we are all perfectly entitled to do).

I had two more articles published in November on the always-excellent Mouthy Money website. One of them was Win Fame and (Maybe) Fortune as a Quiz Show Contestant. This is something I have done myself in the past and enjoyed writing about again for MM. It can be a lot of fun, and any prizes you win are tax-free under UK law.

My other article was How to Cash in on Your Old Tech. Most of us have old technology we no longer use gathering dust in cupboards and drawers. This articles sets out ways you can make some much-needed cash out of this.

Obviously energy bills are a particular concern for many people at the moment, so I hope you are getting all the help you are entitled to. Everyone should be receiving a monthly rebate of £66 on their energy bill (going up to £67 in the new year). If you’re not, chase it up with your energy supplier.

I also recently updated my post about the Warm Home Discount, which this year is being increased from £140 to £150. The eligibility rules are changing somewhat, and I shall probably be one of the people who misses out, which is clearly disappointing. But on the plus side, most people won’t now have to apply for this benefit – if you are eligible, it should be applied automatically to your bill by your energy company.

- The government’s Help for Households website has a helpful summary of all the financial assistance currently available and is regularly updated.

Please do check out as well some of the other posts on Pounds and Sense for advice and resources, especially in the Making Money and Saving Money categories.

- Don’t forget, also, that there are currently two opportunities to claim a free share available. One is with Wealthyhood and the other with Trading 212 (the links will take you to the relevant blog posts). The current Trading 212 offer closes on 29 December 2022, so don’t delay if you want to take advantage of this one. As far as I know the Wealthyhood offer is open indefinitely, but that could always change, of course

That’s all for today. I hope you and your family are coping in these challenging times and wish you the happiest Christmas possible. I shall of course continue to update this blog over the coming weeks, and will return with a further update about my investments at the start of January.

As always, if you have any comments or queries, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

December 6, 2022 @ 4:31 pm

OOh well it is good to see some of your investments are on the up, which is better than the previous month, so here is hoping next month is even better!

December 7, 2022 @ 8:37 am

Thanks, Rachel. Yep, I am keeping my fingers crossed for a Santa rally 🎅 🙂

December 7, 2022 @ 12:06 pm

Such a difficult time at the minute. I am not able to invest as much as I would like, but I am hoping post Christmas I will have more disposable income.

December 7, 2022 @ 12:27 pm

Yep. The cost of living crisis is hitting everyone hard at the moment. But paradoxically now may be a good time to invest if you can find the money, while asset values remain depressed.