My Investments Update – October 2022

Here is my latest monthly update about my investments. You can read my September 2022 Investments Update here if you like

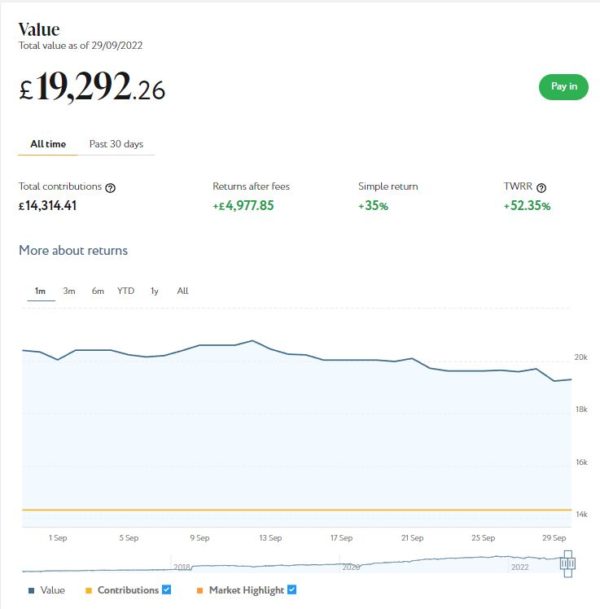

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension). Withdrawals from the latter are still on hold, incidentally, to avert the risk of pound-cost ravaging.

As the screenshot below of performance last month shows, my main portfolio is currently valued at £19,292. Last month it stood at £20,344 so that is a fall of £1,052.

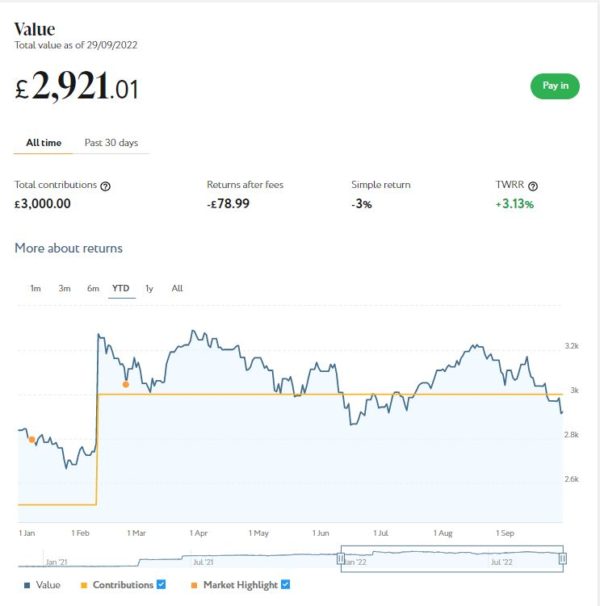

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £2,921 compared with £3,091 a month ago, another fall of £170.

Here is a screen capture showing performance since January 2022. As you can see, I topped up this account in February this year.

There is no denying that these falls are disappointing, especially with my Smart Alpha portfolio now worth less in total than I have contributed to it. As I’ve noted previously on PAS, however, you do have to expect ups and downs with equity-based investments. And this year there has been no lack of volatility, caused by rising inflation, the war in Ukraine and the aftermath of the pandemic (among other things).

About my only consolation is that things could have been even worse if – paradoxically – I’d opted for a lower-risk level with my investments. In their latest blog update, Nutmeg reveal that low and medium-risk portfolios actually performed worse overall last month than high-risk ones. I have copied below their explanation for this:

By design, Nutmeg’s low- and medium-risk portfolios have more exposure through ETFs to assets that are priced in sterling and with limited foreign currency exposure. As you will have seen in the headlines this week, the pound hit an all-time low against the dollar with markets initially placing little faith in the chancellor’s tax-cutting and pro-growth agenda.

This year it has been rewarding to hold foreign currency with sterling particularly weak versus the dollar. Some of our high-risk portfolios have benefited from currency moves, while low- and medium-risk portfolios have not. They haven’t lost money from having low foreign currency exposure, they just haven’t benefited from it.

Secondly, low- and medium-risk portfolios by design have more exposure – again through ETFs – to government bonds, which in ‘normal’ times are considered something of a safe haven and have much lower volatility than equities. After all, it is still highly unlikely that the UK government would default on its debts.

In a nutshell (no pun intended) low- and medium-risk Nutmeg portfolios hold a higher proportion of investments in pounds sterling and UK government bonds. These are normally regarded as lower risk, but last month both took a particular hammering. So in comparison nominally higher-risk portfolios like mine actually performed somewhat better.

This is one more reason I’m glad I opted for higher risk levels with my Nutmeg portfolios (9/10 for my main one and 5/5 for my Smart Alpha). If you haven’t yet seen it, you might also like to check out my blog post in which I looked at the performance over time of Nutmeg fully managed portfolios at every risk level from 1 to 10 . I was actually pretty amazed by the difference risk level makes, with higher-risk ports over almost any period of three or more years in the last ten generating significantly better overall returns. If you are investing for the long term (and you almost certainly should) opting for a hyper-cautious low-risk strategy may not be the smartest thing to do.

Since I started investing with Nutmeg in 2016 – and despite everything that has happened this year – I have still made a total net return on capital of £4,977 (35% or 52.35% time-weighted) on my main portfolio. So I can afford to be philosophical about the recent falls. Indeed, I am considering topping up my Nutmeg investments again now while asset values are depressed.

You can read my full Nutmeg review here (including a special offer at the end for PAS readers). If you are looking for a home for your annual ISA allowance, based on my experience over the last six years, they are certainly worth considering.

Moving on, my Assetz Exchange investments continue to perform well. Regular readers will know that this is a P2P property investment platform focusing on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my AE portfolio has generated £76.51 in revenue from rental and £63.58 in capital growth, a total of £140.09. That’s a decent rate of return on my £1,000 investment and does illustrate the value of P2P property investment for diversifying your portfolio when equity markets are volatile.

I now have investments in 23 different projects and all are performing as expected, generating rental income and in most cases showing a profit on capital as well. So I am very happy with how this investment has been doing. And it doesn’t hurt that most projects are socially beneficial as well.

- To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of AE as far as i am concerned. You can actually invest from as little as 80p per property if you really want to proceed cautiously.

My investment on Assetz Exchange is in the form of an IFISA so there won’t be any tax to pay on profits, dividends or capital gains. I’ve been impressed by my experiences with Assetz Exchange and the returns generated so far, and intend to continue investing with them. You can read my full review of Assetz Exchange here. You can also sign up for an account on Assetz Exchange directly via this link [affiliate].

Another property platform I have investments with is Kuflink. They continue to do well, with new projects launching almost every day. I currently have around £2,500 invested with them in 14 different projects. To date I have never lost any money with Kuflink, though some loan terms have been extended once or twice. On the plus side, when this happens additional interest is paid for the period in question. At present most of my Kuflink loans are performing to schedule, though two recently had their repayment dates put back by three months.

My loans with Kuflink pay annual interest rates of 6 to 7.5 percent. These days I invest no more than £200 per loan (and often less). That is not because of any issues with Kuflink but more to do with losses of larger amounts on other P2P property platforms in the past. My days of putting four-figure sums into any single property investment are behind me now!

- Nowadays I mainly opt to reinvest the monthly repayments I receive from Kuflink, which has the effect of boosting the percentage rate of return on the projects in question

Obviously a possible drawback with Kuflink and similar platforms is that your money is tied up in bricks and mortar, so not as easily accessible as cash savings or even (to some extent) shares. They do, however, have a secondary market on which you can offer any loan part for sale (as long as the loan in question is performing and not in arrears). Clearly that does depend on someone else wanting to buy it, but my experience has been that any loan parts offered are typically snapped up very quickly. So if an urgent need arises, withdrawing your money (or part of it) is unlikely to be an issue.

You can read my full Kuflink review here. They offer a variety of investment options, including a tax-free IFISA paying up to 7% interest per year with built-in automatic diversification. Alternatively you can now build your own IFISA, with most loans on the platform (including the one shown above) being IFISA-eligible.

My investment in European crowdlending platform Nibble continues to perform as advertised. My latest investment was in their Legal Strategy. These are loans that are in default and facing legal action. Nibble buy these loans at a heavily discounted rate and then seek to recover as much as possible of the money owed. The minimum investment is 10 euros and the minimum period is six months. I invested 100 euros for 12 months initially at a target annual interest rate of 12.5%.

The Legal Strategy comes with a deposit-back guarantee. This is a guarantee to return the full investment amount at the end of the investment period and a minimum yield of 9% per year. The actual yield depends on how successful recovery efforts prove, so in practice you may end up with a return of anywhere between 9% and 14.5%. All has gone to plan so far, but I will obviously continue to report on this in the months ahead.

- You can read my updated review of Nibble here if you like. You can also sign up directly on the Nibble website [affiliate link].

Moving on, I had another article published on the always-excellent Mouthy Money website. This one is entitled My Odd Smart Meter Story and Why Despite This I Still Recommend Them. In the article I discuss my rather strange experiences with a smart meter, which stopped working after I switched supplier and then rather mysteriously started again two years later! As per the article title, I do still recommend getting a smart meter, especially in these times of soaring energy bills.

Also in September I enjoyed a final (probably) short break of the year in Barmouth in Wales. I stayed at a Victorian Gothic hotel called Tyr Graig Castle. I was lucky with the weather, and enjoyed visiting nearby Harlech and Portmeirion (see cover image) as well as Barmouth itself.

I shall be publishing a full review of my short break in Barmouth soon. In the meantime, here is a photo of a rather splendid sunset taken from the hotel restaurant…

Finally, I know a lot of people are extremely anxious about the cost-of-living crisis. As I said last time, though, it’s important not to panic. I recommend a three pronged-approach of maximizing your income, minimizing your expenditure, and budgeting carefully (using your resources as effectively as possible, in other words).

Bear in mind, also, that a range of government support measures have been announced to mitigate the worst effects of the crisis. This government Help for Households website has a useful summary of all the help available and is regularly updated.

In the meantime, please do check out some of the other posts on Pounds and Sense for additional advice and resources, especially in the Making Money and Saving Money categories.

That’s all for today. As always, if you have any comments or queries, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

October 5, 2022 @ 8:57 am

It’s really interesting to read how your investments are coping with the fluctuating markets right now, fingers crossed for some financial stability soon.

October 5, 2022 @ 9:35 am

Thanks, Jenny. Yes, a bit more stability would be welcome. But there are undoubtedly good buying opportunities out there right now for those brave enough to take them!

October 5, 2022 @ 1:24 pm

Our shares on the portfolio we have at work had a slight tumble but one has picked back up and the other is still flat-lining at its lower yield, so that is the one we are watching.

October 5, 2022 @ 1:45 pm

Thanks, Rachel. These are certainly challenging times for investors.