Why Now Could Be the Ideal Time to Take Advantage of Your New Tax-Free ISA Allowance

As of 6 April 2025, UK investors have a fresh chance to supercharge their savings and investments with a new £20,000 Individual Savings Account (ISA) allowance.

ISAs represent a golden opportunity for investors to make their money work harder while shielding their returns from the taxman. With tax-free allowances for income frozen until April 2028 and tax-free thresholds for dividend tax and capital gains tax being slashed in the last few years, it’s more important than ever to protect your hard-earned savings and investments within an ISA wrapper.

To maximize the benefits of the new 2025/26 allowance, there’s a strong case for acting swiftly and using at least part of your £20,000 ISA allowance sooner rather than later. This is due to the power of compounding. By investing early, you give your money more time to grow, benefiting from the potential snowball effect of returns generating further returns. So the sooner you invest that £20,000 (assuming you are fortunate enough to have it) the more opportunity it has to multiply over time.

Another reason to use your ISA allowance sooner rather than later is that there are reports that Chancellor Rachel Reeves is considering slashing the tax-free allowance for cash ISAs in particular, potentially to as little as £4,000 a year. It’s probable there will be an announcement about this in the Autumn Budget. Any change is highly unlikely to be backdated, however – so taking advantage of the full allowance now could be a canny move.

In addition to the tax-free ISA allowance remaining at a relatively generous £20,000 (for now), the rules surrounding ISAs have recently undergone a welcome relaxation. One of the most significant changes is the ability to open more than one ISA of the same type (e.g. a stocks and shares ISA) with different providers in the same tax year. This means investors are no longer limited to a single provider for each type of ISA, giving them greater flexibility and choice in managing their investments.

Previously, investors were restricted to opening one cash ISA, one stocks and shares ISA and one innovative finance ISA (IFISA) per tax year. This restriction could prove frustrating for those seeking to diversify their investments or take advantage of new opportunities as the tax year progressed. Now, with the freedom to open multiple ISAs of the same type, investors can shop around for the best rates, terms and investment options without being limited to a single provider for each ISA type. They can also move some or all of their money from one provider to another without jeopardizing its tax-free status.

- It’s important to note, however, that while the rules have been relaxed, the overall annual ISA allowance remains fixed at £20,000. This means that any contributions made across multiple ISAs of any type will count towards your total allowance for the tax year. You should still therefore take care not to exceed the annual limit to avoid any potential tax charges.

Cash ISAs offer a secure and accessible way to save, providing a tax-free environment for your savings with the added benefit of easy access to your funds when needed. Meanwhile, stocks and shares ISAs open the door to potential higher returns by investing in a wide range of assets such as equities, bonds, and funds, albeit with a higher level of risk. With a stocks and shares ISA you will never incur any liability for dividend tax, capital gains tax or income tax, even if your investments perform exceptionally well. Of course, there is no guarantee this will happen, but over a longer period stock market investments have typically outperformed cash savings, often by a substantial margin. IFISAs (e.g. from Housemartin) allow you to invest is property crowdfunding and other forms of peer-to-peer finance. They are more specialized, but may appeal to some investors looking to further diversify their portfolios.

- In recent years I have invested much of my own annual ISA allowance in a stocks and shares ISA with Nutmeg, a robo-manager platform that has produced good returns for me. You can read my in-depth review of Nutmeg here if you wish.

Closing Thoughts

The start of a new financial year is a great time for UK investors to review their savings and investment strategies. Whether you’re looking to start a new ISA or maximize your contributions to existing accounts, taking action early can set you on the path to optimizing your returns from this important tax-saving opportunity.

By investing sooner rather than later and taking advantage of the increased flexibility in ISA provider options, savers and investors can make the most of their money while minimizing their tax liabilities. So seize this opportunity to build your wealth and protect it from the taxman today!

As always, if you have any comments or questions about this post, please do leave them below.

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

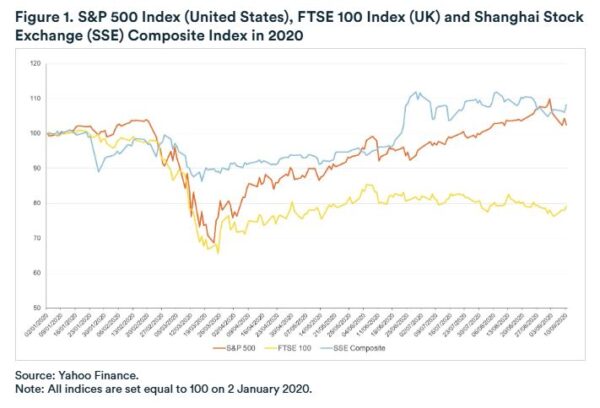

The recovery in stock market values continued through 2021. If you check out my in-depth

The recovery in stock market values continued through 2021. If you check out my in-depth

Bio: Sally Jenkins (pictured, right) currently writes uplifting and hopeful novels for the traditional publisher

Bio: Sally Jenkins (pictured, right) currently writes uplifting and hopeful novels for the traditional publisher