Today I have a guest post for you from my friends at Broadway Autocentres. As specialists in this field, they know exactly what it takes to get the most out of your car tyres.

Over to the experts, then…

When it comes to driving your own car, all the costs seem to mount up. If you’re not saving for the next service, you’re putting money aside for the MOT. And just when that is out of the way, you realise that you don’t know how old your tyres are or when they will need to be replaced.

There is no way to have your car use less fuel or oil, and skipping services is a bad idea – but if you can reduce the wear and tear on the vehicle whenever possible, so much the better for your purse or wallet.

Tyres are one of the biggest expenses you will face, so let us look at five ways to get the most out of your tyres before you bow to fate and replace them!

Buy Them in Twos

Buying a set of four tyres can seem impossible with a tight budget, so why not replace your tyres in twos instead? Depending on whether your car is front or back wheel drive, either the front set or back set will take the most punishment. It is the most worn tyres that should be replaced, with the more lightly worn set moving to take their place and the new tyres going where they will receive less wear. This system may seem inconsistent, but it will ensure that you stay safe while on the road without needing to spend a lot of money all at once.

Drive Sensibly

Drive according to the Highway Code at all times and resist the temptation to put your car through its paces. Maintain a safe speed, avoid rough or unsurfaced roads, and increase and decrease speed slowly whenever possible. All of these will help to keep your tyres in good condition for longer, so you can keep saving for their eventual replacements.

Buy the Best

While it may seem counter-intuitive, buying the best quality tyre you can afford is often more economical when taken over time. Budget tyres are sometimes made with flaws that can weaken the tyres more quickly, or with inferior rubber that begins to crumble and break apart. Better quality tyres will last better – sometimes twice as long as budget tyres, thereby comparatively halving their cost to you. You can book your tyres in Buckinghamshire at Broadway Autocentres (01494 680914).

Regular Checks

Get into the habit of checking your tyres often, looking for early signs of damage or weakness. In many cases, prompt corrective action or a swift repair can keep the tyre in place for some time, giving you the chance to continue getting out and about without suddenly needing to spend money on a new set or pair of tyres.

Proper Inflation

Modern tyres – no matter whether budget or premium – are designed to be used within a narrow recommended range of pressure, and will often perform poorly outside of this range. Keep your tyres inflated to within the range recommended by the manufacturer (this can be found online, sometimes on the tyre itself, or inside the car owner’s handbook) to ensure that not only do your tyres last as long as possible, but you are safer on the roads during this time. Correctly inflated tyres also aid fuel economy, saving you money that way as well.

Thanks again to my friends at Broadway Autocentres for their expert advice. As always, if you have any comments of questions about this post, please do leave them below.

This is a sponsored post.

If you enjoyed this post, please link to it on your own blog or social media:

Today I am looking at P2P property investment platform Kuflink.

I have been investing with Kuflink for five years now, so this is a fully updated repost of my original review.

What is Kuflink?

Kuflink is an online platform offering opportunities to invest in loans secured against property. These loans are typically made to developers who require short- to medium-term bridging finance, e.g. to complete a major property renovation project, before refinancing with a commercial mortgage.

Kuflink offer three types of investment, as follows:

Auto Invest and IFISAs both automatically invest your money across a number of loans and pay a fixed interest rate, typically between 7 and 9%. You can choose a 1-year, 2-year or 3-year term, and interest is paid annually (it is automatically reinvested at the end of each year with the two-year and three-year products). The Auto-Invest product is basically the same as the IFISA, but without the tax-free wrapper.

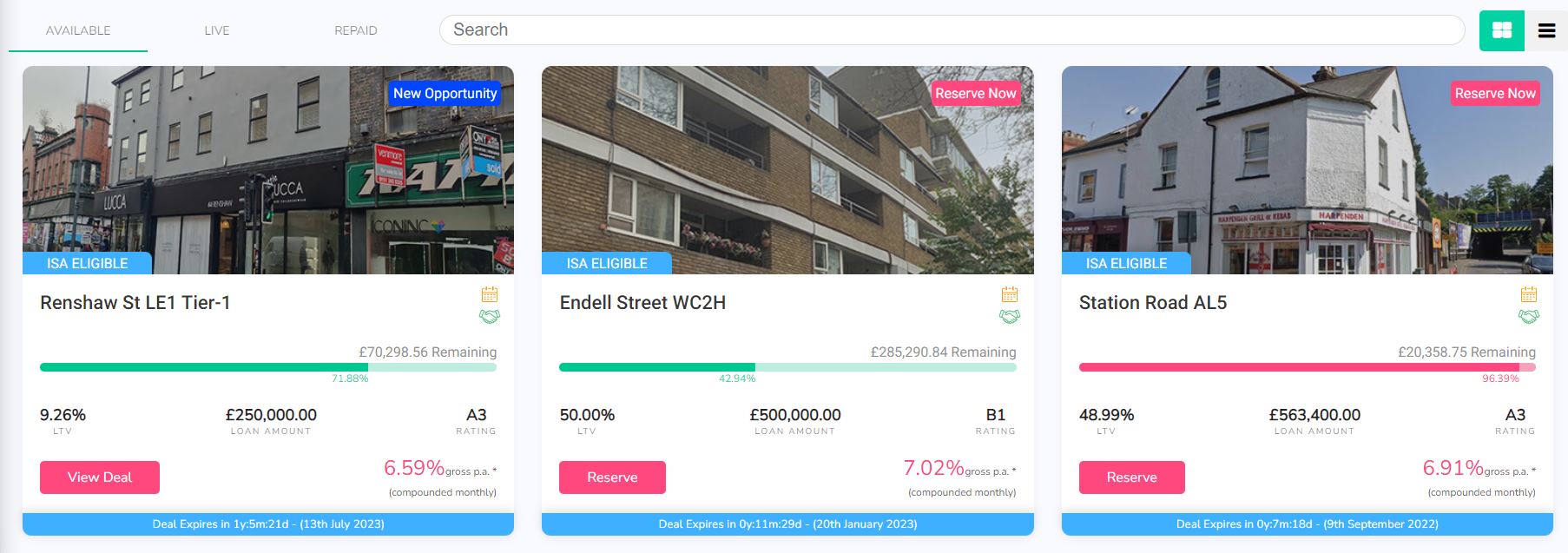

At one time only the Auto-Invest option was available for IFISAs, but nowadays you can choose your own investments if you prefer. The great majority of Self-Select loans on the Kuflink platform are IFISA-eligible. If you check out the Self-Select listings on the Kuflink website (see image below), this will tell you whether any particular loan is IFISA-eligible or not.

Individual Select-Invest loans pay interest rates varying between about 6 and 7.2%, depending largely on the LTV of the loan (loan to value, a measure of how secure the loan would be in the event of a default). The higher the LTV, the riskier the loan, and – other things being equal – the higher the interest rate paid in consequence. You can see a screen capture below of three Select-Invest loans available on the platform at the time of writing.

As a reasonably experienced P2P investor, I put my money into Select-Invest loans. These typically have a duration of six months to a year and (as mentioned above) pay interest from around 6 to 7.20 percent. That obviously isn’t as much as some P2P property platforms (e.g. BLEND), but I think it represents a fair balance between risk and reward. Kuflink also invest in every loan themselves up to 5% of the value of each loan – so, as the expression goes, they have skin in the game.

My Kuflink Review

I found signing up with Kuflink a quick and easy process. They do the obligatory money-laundering checks, but in my case anyway this was all done electronically behind the scenes. I uploaded a copy of my passport and was approved almost immediately. I started by depositing £500, but you can start with as little as £100 if you like.

Initially I put my money into a 12-month loan paying 7% annual interest. One good feature I didn’t grasp initially is that with Select-Invest loans interest is paid monthly. So once a month I receive interest payments on all the loans I am currently invested in. This is paid into a wallet, from which you can either withdraw to your bank account or reinvest.

Kuflink recently introduced an option to have monthly loan repayments automatically reinvested rather than paid into your account as cash. This effectively boosts your interest rate by the power of compounding, as you then receive interest on the reinvested payments as well. Currently this option is available for most, but not all, loans on the platform. You can see which of your loans compounding is available for via your Kuflink dashboard.

I have continued to invest in Kuflink, and have also reinvested in new loans when the original ones were paid off. Another good feature is that money invested in a loan but not yet released to the borrower attracts interest which is paid as cashback once the loan has gone live.

There have been no defaults so far on any of my loans, and Kuflink say on their website that to date nobody has lost a penny on their platform. I have experienced short delays with loans being repaid, but in such cases you continue to earn interest, of course.

Secondary Market

A new feature on Kuflink I like is the Marketplace (secondary market). Here you can buy loan parts from other investors who want to sell up early. You can also put up for sale any (or all) of your own loan parts.

The number of loan parts listed in the Marketplace went up in the early months of the pandemic, as many investors understandably wanted (or needed) to access their cash. This created short-term buying opportunities which I was happy to take advantage of. Loan parts offered via the Marketplace typically have only a few months to run, so you can expect to get your capital back quickly (and can then reinvest it if you wish). Only loans in good standing with monthly repayments up to date may be listed on the Marketplace, so that offers some reassurance against default – though of course it is by no means a guarantee.

In recent months the number of loan parts listed on the Marketplace has reduced considerably. And those that are tend to be snapped up quickly. As a would-be investor this is slightly disappointing, but it does indicate that people are keen to take advantage of the opportunities on offer. It also means that if you want (or need) to exit a loan early, accessing your money should be a quick and easy process.

Pros and Cons

Based on my experiences, here is my list of pros and cons for the Kuflink investment platform.

Pros

1. Easy sign-up process.

2. Low minimum investment.

3. All loans secured against property.

4. Choice of investments and approaches.

5. Manual and auto-invest options.

6. Kuflink invest in all loans themselves, so they have a strong incentive to ensure they are safe and secure.

7. They also cover the first 5% of losses on any loan before investors are affected (although this has never happened yet).

8. Money invested but not yet released to the borrower attracts interest which is paid as cashback once the loan has gone live.

9. In-depth information is provided on the website about all loans, so you can see exactly how your money will be used (and by whom).

10. There have been (according to Kuflink) no investor losses to date.

11. Customer service (in my experience anyway) is fast, friendly and helpful.

12. There is a 14-day cooling off period for new investors.

13. Marketplace (secondary market) for buying and selling loan parts.

14. No charges to investors lending on the primary market and only a 0.25% fee if you resell a loan part on the secondary market.

15. On most loans you can opt to reinvest monthly repayments to boost your net interest rate.

16. Tax-free IFISA option available.

Cons

1. Rates paid aren’t the highest in P2P lending.

2. Delays with some loans being repaid (although investors do earn extra interest if this happens).

3. No mobile app [UPDATE FEB 2023 – An app is now available.]

Conclusion

Overall, my experiences with Kuflink so far have been entirely positive and my investments have been generating the promised returns. I started cautiously with them, but have gradually built up the amount I have invested on the platform. Although – like all property P2P platforms – they were adversely affected by the pandemic, they appear to have come through it strongly, with new loans now being added almost daily.

As mentioned above, although Kuflink don’t pay the highest rates in P2P lending, I think the returns on offer are realistic and sustainable. The steady expansion of the platform seems to testify to this, as does the fact that they have received several industry awards. These include Best Alternative Business Funding Provider in the Business Moneyfacts Awards in both 2018 and 2019 and Best Service From an Alternative Funding Provider in 2020.

Kuflink are also highly rated on the independent TrustPilot website, with an average 4.6 out of 5 (‘Excellent’). At the time of writing 82% of reviewers award them the maximum five-star rating, which is among the highest figures I have seen for a financial services platform.

As with all P2P lending, your money does not enjoy the same level of protection as bank and building society accounts, which are covered (up to £85,000) by the Financial Services Compensation Scheme. Nonetheless, the rates of return on offer are significantly better than those from most financial institutions. And the fact that all loans are secured against bricks and mortar – and Kuflink themselves have cash invested in them – clearly offers some reassurance.

From my experience, Self-Select loans tend to fill up quickly. On the positive side, this shows investors have confidence in Kuflink and want to invest through the platform. On the minus side, it means there are typically no more than two or three new loans open for investment at any time.

Clearly, no-one should put all their spare cash into Kuflink (or any other P2P investment platform). Nonetheless, it is certainly worth considering as part of a diversified portfolio. Not only are the rates of return much higher than those offered by banks and building societies, they are relatively unaffected by ups and downs in the stock market. P2P loans aren’t a way of hedging your equity-based investments directly, but they do help spread the risk.

If you have any comments or questions about this review or Kuflink in general, as always, please do leave them below.

Disclosure: As stated above, I am an investor with Kuflink myself, and if you invest £500 or more via my link above I will receive a bonus for introducing you. Money is at risk. You should always do your own ‘due diligence’ before investing, and seek advice from a qualified financial adviser if in any doubt how best to proceed.

If you enjoyed this post, please link to it on your own blog or social media:

Today I’m spotlighting a new UK high-speed broadband service called Cuckoo.

They are aiming to shake up the world of broadband internet with great-value prices, first-rate customer service, and a social conscience too 🙂

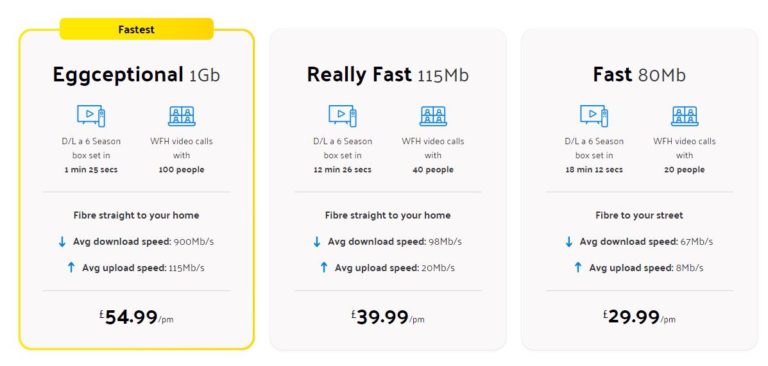

Cuckoo currently have three different customer offers based on speed. Briefly they are as follows:

Eggceptional (1 Gb) – £54.99 a month

Really Fast (115 Mb) – £39.99 a month

Fast (80 Mb) – £29.99 a month

You can see more detailed information from the Cuckoo website in the screen capture below.

Signing up is straightforward via the website and takes just a couple of minutes. Your router will then arrive in the post with full instructions for setting it up. If an engineer is needed (usually it isn’t) Cuckoo will arrange a convenient time for them to come. This is summed up in the graphic from the company website below.

As mentioned, Cuckoo is also a company with a social conscience. They take 1% of each bill and use it to help bring the Internet to places where it’s needed most. That includes conflict zones, natural disaster sites and developing communities. Customers get to choose which project they wish to to support under the Cuckoo Compass scheme.

Finally, Cuckoo aims to deliver top-notch customer service from their team of UK-based customer-support ‘Eggsperts’. Cuckoo have an impressive Trustpilot average rating of 4.6 (‘Excellent’), with 76% of people at the time of writing giving them a full five stars.

For much more information, please check out the Cuckoo website. And of course, if you have any comments or questions about this post, please feel free to leave them below as usual.

Disclosure: This sponsored post includes affiliate links. If you click through and end up making a purchase, I may receive a commission for introducing you. This will not affect the price you pay or the product or service you receive.

If you enjoyed this post, please link to it on your own blog or social media:

Today I am spotlighting BLEND, a peer-to-peer property platform that lends to established businesses (mostly experienced property developers). BLEND’s loan-based crowdfunding platform was founded by a team of former investment bankers with substantial experience in real estate and finance.

What Does BLEND Offer?

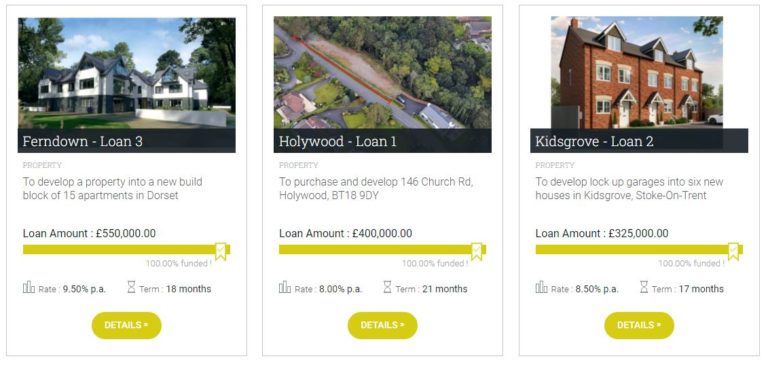

BLEND offers individuals the chance to invest in loans secured against property. They specialize in loans in geographical areas that banks and other lending platforms typically pay less attention to, e.g. Northern Ireland, though they fund projects across the whole of the UK. Loans are typically for small developments or building renovation/conversion projects. Some examples are shown in the screen capture below.

As mentioned above, all loans are secured against property. The LTV (loan-to-value ratio) is usually quite low, giving greater security for investors. Interest rates on offer range from 7 to 12 percent.

BLEND has some similarities with Kuflink, which I reviewed in this blog post a while ago (and invest in myself). Both offer the opportunity to invest in secured loans. Kuflink typically offers lower interest rates, however, between 5 and 7 percent. The risk level with Kuflink loans is (arguably) lower, but it should be said that BLEND so far has an unblemished record, with no loans in arrears or default.

The minimum investment on BLEND is £1,000, which means it is really aimed at high net worth and professional investors. It’s also worth noting that only a small number of new loans tends to be available at any given time and they typically sell out very quickly.

Using the AutoLend feature is recommended to ensure that you don’t miss out when a new loan comes on to the market.

Secondary Market

One drawback with any type of property investment is that it’s not as liquid as (say) equity-based investments. BLEND does offer a way around this with its secondary market, however.

Lenders who wish to liquidate early can sell their loan parts on the secondary market. Note that finding a buyer on the secondary market may take time and there is always a risk of no-one wanting to buy your loan part. You can start selling a loan in multiples of £1,000 on the secondary market as soon as funds have been released to the borrower.

Unlike the primary market, as a lender you will be charged a secondary market fee of 0.60% (or £6 for every £1,000 of capital) on capital outstanding. BLEND only charge this upon the successful resale of the loan portion you have listed in the secondary market. The secondary market is free for buyers.

Pros and Cons

A full list of Pros and Cons for BLEND is shown below.

Pros

1. Easy sign-up process

2. Well designed, user-friendly website

3. All loans secured against property

4. Low LTV ratios for added security

5. Manual and auto-invest options

6. In-depth info provided on the website about loans, so you can see exactly how your money will be used (and by whom)

7. No investor losses to date

8. Marketplace (secondary market) for buying and selling loan parts

9. No charges to investors lending on the primary market and only a 0.6% fee if you resell a loan part on the secondary market

10. Rates of return of up to 12% are at the upper end for P2P lending

11. Can invest via a SIPP or SSAS (private pension scheme)

Cons

1. Minimum investment of £1,000

2. Limited supply of new loans to invest in

3. No tax-free IFISA option

Final Thoughts

With a minimum investment of £1,000 (per project), BLEND obviously won’t be suitable for everyone. But if you have that sort of money available, the promised returns of up to 12 percent are undoubtedly enticing.

I like the fact that BLEND are very selective in the projects they back, even if that does mean the flow of new opportunities is limited. It’s also good that they perform in-depth ‘due diligence’ on every loan and publish full details about this on the website, including independent valuations. This means investors know exactly what the potential risks and rewards of a project are.

The absence of any charges to investors (apart from on the secondary market) is another big plus. And the presence of a secondary market offers the opportunity to exit loans early if your circumstances change (though, as noted above, you aren’t guaranteed to find a buyer).

BLEND is probably at the riskier end of the P2P property spectrum, but in my opinion the returns on offer fairly reflect this. Risks are also mitigated by generally low LTV ratios and the detailed research mentioned above. The fact that no loan has so far gone into default or even into arrears is impressive, though there is of course no guarantee this couldn’t happen in future. It does offer some reassurance though.

Finally, BLEND has an average Trustpilot rating of 4.6 (‘Excellent’), with 95% of people awarding them a maximum five stars rating. This is among the highest ratings I have seen for an investment platform on Trustpilot.

As always, if you have any questions or comments about this post or P2P property investment more generally, please do leave them below.

Disclaimer: I am not a qualified financial adviser and nothing in the article above should be construed as personal financial advice. You should always do your own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Please note also that this post includes affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect in any way the terms you are offered or the product/service you receive.

If you enjoyed this post, please link to it on your own blog or social media:

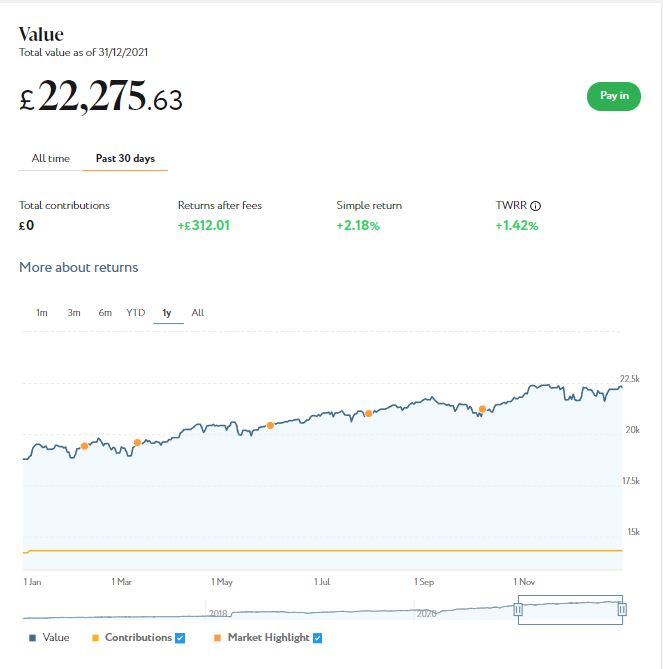

I’ll begin as usual with my Nutmeg Stocks and Shares ISA, as I know many of you like to hear what is happening with this.

As the screenshot below shows, my main portfolio is currently valued at £22,275. Last month it stood at £21,963, so that is a rise of £312. Obviously in these uncertain times I am very happy with that.

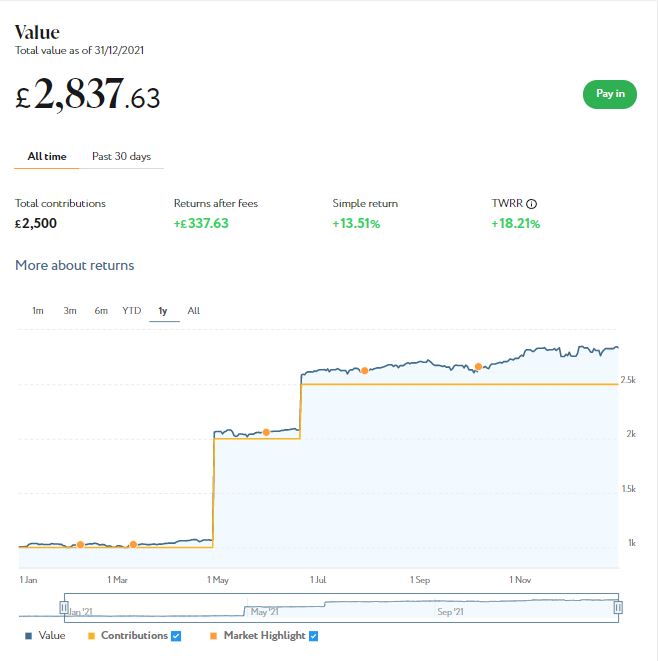

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £2,837 compared with £2,795 last month, a net monthly increase of £42. Again that’s a good result, pro rata slightly better than my main portfolio. Here is a screen capture showing performance over the last year.

You can read my full Nutmeg review here (including a special offer at the end for PAS readers). If you are still looking for a home for your 2021/22 ISA allowance, based on my experience they are certainly worth considering.

As regular readers will know, this year I am using Assetz Exchange for my IFISA. This is a P2P property investment platform that focuses on lower-risk properties (e.g. sheltered housing on long leases). I put an initial £100 into this in mid-February 2021 and another £400 in April. Everything went well, so in June 2021 I added another £500, bringing my total investment on the platform up to £1,000.

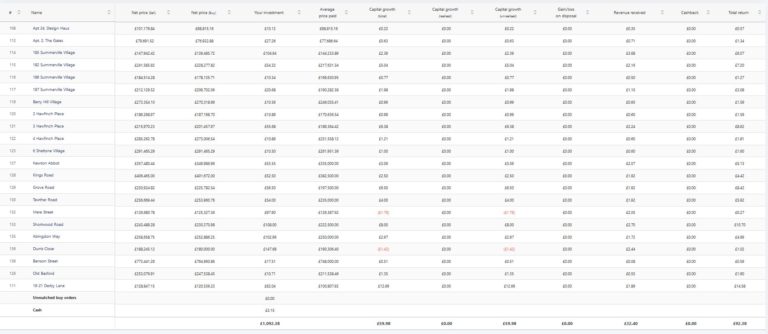

Since I opened my account, my portfolio has generated £32.40 in revenue from rental and £59.98 in capital growth, for a total return of £92.38. Here is my current statement:

To control risk with all my property crowdfunding investments nowadays, I am investing relatively modest amounts in individual projects. I don’t therefore put more than around £150 into any one project. As you can see, I have a well-diversified portfolio with Assetz Exchange comprising 21 different projects. This is a particular attraction of AE in my view. You can actually invest from as little as 80p per property if you really want to proceed cautiously.

As a matter of interest, I have also included a capture of my Assetz Exchange dashboard below. As you will see, this shows an average AER (Annual Equivalent Rate) yield of 5.38%. That is better than I could have got in interest from almost any savings account at the moment and doesn’t include capital growth either. Of course, money in Assetz Exchange is not protected by the Financial Services Compensation Scheme (FSCS), which covers all deposits with registered UK banks and building societies up to £85,000.

Another property platform I have investments with is Kuflink. They have been doing well recently, with new projects launching almost every day. I currently have just over £2,000 invested with them, quite a large proportion of which comes from reinvested profits. To date I have never lost any money with Kuflink, though some loan terms have been extended once or twice. On the plus side, when this happens additional interest is paid for the period in question.

My loans with Kuflink pay annual interest rates of 6 to 7.5 percent. As mentioned above, these days I invest no more than around £150 per loan (and often less). That is not because of any issues with Kuflink but more to do with losses of larger amounts on other P2P property platforms (such as this one). My days of putting four-figure sums into any single property investment are behind me now!

Nowadays I mainly opt to reinvest the monthly repayments I receive from Kuflink, which has the effect of boosting the percentage rate of return on the projects in question

You can read my full Kuflink review here. They offer a variety of investment options, including a tax-free IFISA paying up to 7% interest per year with built-in automatic diversification. Alternatively you can now build your own IFISA, with most loans on the platform being IFISA-eligible.

I’d also particularly draw your attention to their revised and more generous cashback offer for new investors [affiliate link]. They are now paying cashback on new investments from as little as £500 (it used to be £1,000). And if you are looking to invest larger amounts, you can earn up to a maximum of £4,000 in cashback. That is one of the best cashback offers I have seen anywhere (though admittedly you will need to invest £100,000 or more to receive that!).

I have also been investigating another P2P property investment platform called BLEND recently. Like Kuflink, they offer the opportunity to invest in secured loans to experienced property developers. They offer (on average) somewhat higher rates of return than Kuflink, though arguably with a bit more risk. Watch out for my in-depth blog post about them soon. You can also check out what they have to offer on their website [affiliate link].

Moving on, I have another article on the always-excellent Mouthy Money website. This is about how to save money on your water bills. I enjoyed researching this and some of the things I found out were quite eye-opening 🙂

That’s all for now, so please stay safe and warm in these challenging times. And as I said last time, don’t let scare stories in the mainstream media freak you out. It is now increasingly apparent that while the Omicron variant is more transmissible, it also tends to produce less severe illness. I am increasingly optimistic that as 2022 continues the virus will loom less large in our lives. But Covid will be with us forever, so we really do need to learn to live with it and start getting back to normal now.

As ever, if you have any questions or comments about this post, please do leave them below.

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that this post includes affiliate links (disclosed). If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered.

If you enjoyed this post, please link to it on your own blog or social media:

As mentioned,

As mentioned,