In this post in May 2020 I revealed why I was switching my Santander 123 account to a 123 Lite account.

At that time they were cutting their interest rate from 1.5 to 1 percent and I calculated it was no longer worth paying the £5 a month fee. So I switched to a 123 Lite account costing just £1 a month.

Admittedly with this account you don’t receive any interest, but you do still get cashback on your direct debits at the same rates. I worked out that overall I would be almost £30 a year better off with a 123 Lite account (obviously the exact figure would depend on the direct debits you have)..

Since then Santander has cut the interest rate paid on a standard 123 account again, to just 0.6% from August 2020. That made the decision to switch even more clear-cut for me.

October 2020 Changes

Santander have just announced further changes to their fees and cashback rates. These will apply from 27 October 2020.

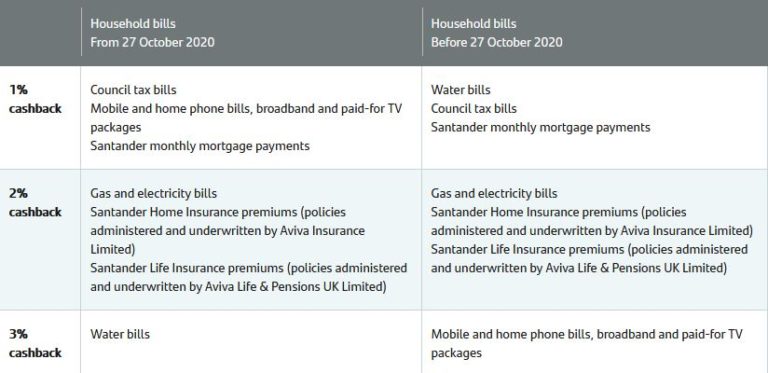

The main change is that the fee for a Santander 123 Lite account will be doubling from £1 to £2 a month. Cashback rates for direct debit payments will be changing as well. The main changes are as follows:

Water bill cashback will go up from one percent to three percent

Communications bill cashback (phones/broadband/TV packages) will be reduced from three percent to one percent.

Cashback paid on other household bills (such as gas, electricity, council tax, etc.) will remain unchanged.

The changes are detailed in the table below, which I have copied from the Santander website…

Effect of the Changes

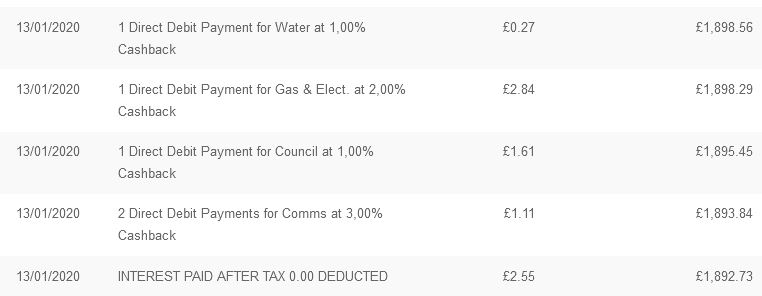

Below I have copied the list of monthly cashback payments from my post in May 2020. Obviously my finances are somewhat different now, but I thought it would be best to use this to provide a clear (and fair) comparison. At this time I still had an ordinary 123 account, so the screen capture below includes interest as well.

By my calculation, the cashback due to me under the new regime would be as follows:

Water – £0.81 (up £0.54)

Gas and Electricity – £2.84 (unchanged)

Council Tax – £1.61 (unchanged)

Comms (mobile phone and broadband) – £0.37 (down £0.74)

Overall, then, my monthly cashback will fall from £5.83 to £5.63 in October 2020. That’s a drop of 20p a month – disappointing but not exactly devastating.

If you deduct the new £2 a month fee, overall I will be making 5.63 – 2.00 = £3.63 a month or £43.56 a year. On my average £1,800 balance, that works out as a notional interest rate of 2.4%. That may not sound a lot, but it is still far better than most other instant access accounts. Of course, rather than interest the account pays cashback, but in money terms the effect is the same.

As a matter of interest, if I were to reduce the average balance in my Santander account to £900 while still earning the same cashback, that would effectively double the rate of return I receive. Perversely, with the Santander Lite account, the lower the average balance you can keep while still servicing your direct debits, the better the percentage return on your capital you will get 🙂

Obviously the numbers are likely to work out differently for you. I do, though, highly recommend taking a few moments to complete a calculation such as the one above using your own cashback figures. Most people are likely to earn less cashback under the new regime, as their water bills (with cashback rising) are likely to be lower than the cost of their phone, internet and TV packages (cashback falling). As in my case, though, it may not make a huge difference overall.

What If You Still Have a Standard 123 Account?

The monthly fee for a regular Santander 123 account will remain at £5 and it will continue to pay 0.6 percent interest, up to a maximum of £20,000.

The cashback terms will change along with 123 Lite accounts, however, meaning most people will receive a bit less cashback after October 27 2020.

Using myself as an example again, if I still had a regular 123 account I would be receiving £5.63 cashback and £0.90 interest per month on my average £1,800 balance (with the 0.6% interest rate that applies from August). That’s a total of £6.53 a month. Subtract the £5 fee from this, and my net returns from the account would be £1.53 a month or £18.36 a year. That’s less than half what I would get with a 123 Lite account, and works out as a return on capital of marginally over 1.00%

Again, if you have a regular 123 account I recommend completing a calculation such as the one above to see if you would be better off with a 123 Lite account. Unless you have a very high average balance (in which case you should probably be investing some and/or putting some in an interest-paying savings account) the 123 Lite account will almost certainly win.

To cover the £60 a year charges alone at the current interest rate of 0.6%, you would need to keep an average balance of £10,000 in the account.

If you want to switch from a regular 123 account to 123 Lite, as I mentioned in my earlier article, it is a very simple process. Just log in to your account and select the option to ‘upgrade’. You will have to answer a few quick questions and click to confirm. In a short time – next day in my case – you should receive an email confirming you are now the proud owner of a Santander 123 Lite account. The account will still have the same sort code and account number and the same PIN number, and you will be able to log in via the app or website just as before.

Conclusion

It is clearly disappointing that Santander are doing this, though they say that rising costs have left them with little option.

But even after the October changes, I still find that having a Santander 123 Lite current account makes sense for me and will continue to do so. I may, however, try to reduce the average balance I keep in the account by moving some money to an alternative, interest-paying savings account.

As always, if you have any comments or questions about this post, please do leave them below,.

If you enjoyed this post, please link to it on your own blog or social media:

In my last post I revealed how you can make money selling arts and crafts on Etsy, even if you don’t have any artistic skills or talents. I discussed how Etsy works and the types of product that are sold on it (and to whom). I also set out some suggestions for choosing products you could sell from an Etsy shop yourself.

Today I’m going to take you through the practicalities of setting up your shop on Etsy, listing your first item, taking photos, writing descriptions, promoting your shop to boost sales, and more.

Setting Up Your Shop

Before you can open an Etsy shop, you first have to join the site as a buyer. This is simple enough. Just click on the Register tab at the top of the Etsy homepage and enter the information required.

You have to provide a user name, and one tip here is to pick a name containing one or two of the keywords you want to target. This can help ensure that your shop is listed high in the search results for the keyword/s in question.

You can then set up your shop by clicking on Sell on Etsy. This is a simple, step-by-step process, and as mentioned last time no fee is charged. No coding is required either – it’s basically just a matter of providing some information and making a few choices.

Many new sellers agonize over their shop design, but it’s not worth wasting too much time on this. Most potential buyers will arrive via a search that takes them straight to a specific product listing, so this is where most of your effort should go.

Nonetheless, you do need to make some decisions about your shop’s overall look, so my advice would be to choose something simple but functional. You can always refine it later once you have made your first few sales.

One thing you should add at an early stage, however, is a banner or logo. This will be part of your branding, so it needs to be attractive and relevant to your product.

Unless you have skills in this area, it’s best to outsource logo design to someone who specializes in this. If you want to keep costs to a minimum, there are people on Fiverr.com who will create one for just $5 (about £4.00). At that price you could get a few done and choose the one you like best.

Your First Listing

My top tip here is to start small. Initially it is likely that only friends and family will see your shop, so there is no need to worry about offering a huge product range from day one.

In addition, if you spend hours making your products in a variety of sizes and colours and nobody wants to buy them, imagine how disappointed you will be. Much better to choose one particular product to start with, and make your listing for this the best it can be.

Product listings have two main components: the photo and the description. The photo is by far the most important, so let’s start by looking at that.

Taking Product Photos

The good news is you don’t need an expensive DSLR camera to take your product photos. A modern smartphone can produce more than acceptable results. Taking photos that sell well is an art, however, so here are some tips to get you started…

Keep backgrounds plain and simple. The product should always be the star of the show.

On the other hand, a strategically chosen prop (or props) can make even ordinary items look special.

Use natural light if possible. This nearly always looks better than artificial.

But if natural light isn’t available, use spotlights to ensure the product is brightly lit.

For small items, get as close as you can while ensuring the product remains in focus.

Use a tripod or stand to ensure your photos are as sharp as possible.

Look at the photos in successful Etsy shops and see what you can learn from them.

Try also searching on Pinterest for Etsy – this will produce image boards crammed with product photos from the site.

Take lots of photos and use only the best. Digital cameras and smartphones don’t use expensive film, so take full advantage of this!

Another benefit of digital photography is that you can easily edit photos, e.g. to sharpen or crop them. There are various free photo editing tools online, including Canva and (my personal favourite) PicMonkey. If you’re using a smartphone, there are many free and low-cost photo-editing apps you can download.

Finally, you can also do some basic editing when you upload photos to your Etsy shop. Your member’s page will show a preview of how the photo will look, with edit options allowing you to crop, rotate and add filters.

Once you have your photo looking exactly how you want, click to save it. All that is left then is…

Adding a Description

While it’s not as crucial as the photo, having a good description is important too.

There’s no need to write reams about your product – the image will do most of the talking for you – but you still need to answer any obvious questions a potential buyer might have.

One good tactic is to study how similar products are sold in other shops. A quick keyword search on Etsy should unearth plenty of such shops for you.

Obviously, you shouldn’t copy descriptions word for word, but they will help you see the sort of points you should be covering. The chances are that the sellers have included those details in their listings because their customers have asked about them.

Note down also any words your competitors use regularly, such as rustic, customized or handmade, and try to incorporate at least some in your own listings. It can also be good to suggest possible uses for your product, e.g. ‘These make great gifts for bridesmaids’ or whatever.

Check your work for spelling and grammatical mistakes, and ensure that the description sounds as enticing as possible. Once you’ve done all that, there is just one other matter you need to attend to…

Pricing

This is something many new Etsy sellers find challenging, but essentially it’s a simple process.

Start by working out what it will cost you to produce and sell an item. That means adding up the cost of materials and adding Etsy’s listing and transaction fees. Obviously you won’t know the exact transaction fee until you have worked out your final price, so use your best guess initially.

Next you need to decide how much you want to earn per hour. Time is money, so the cost of your item will need to reflect this. Let’s say you aim to make £12 an hour, and it takes you half an hour to create your product. That means to make £12 an hour, you will need to make 12/2 = £6 from each item you sell.

Finally, I recommend adding an extra amount – say 10 percent – for profit. All real world businesses budget to make a profit, and even if you’re working part-time from your kitchen table, you should do likewise. Profits can be set against overheads such as heating and lighting, and can also be invested in tools to make you more productive. Or you can simply take them as additional earnings, of course!

Once you’ve come up with a total, the final thing you should do is compare this with what others are charging for comparable products. Ideally you should aim to be selling for a slightly lower price, initially at least, to make your items more attractive to potential buyers. That may mean reducing your target earnings a little, or finding ways to produce items more quickly.

Like other aspects of your operation, such as photos and descriptions, it is important to test various price levels and see which produces the best returns overall.

Promoting Your Shop

If you have followed all the steps above, it shouldn’t be long before potential buyers start arriving at your Etsy shop. But there are plenty of things you can do to attract more visitors and get the sales flowing. Below I have listed a variety of methods, some free, some paid for.

Set up a Facebook fan page for your shop, with links to the items you are selling and other content that may interest potential buyers.

Set up a Pinterest board as well, with photos of your products linking to the sales pages in question. This can be a powerful marketing tool for products that are visually appealing.

You should also create an Instagram account on which to post photos of your arts and crafts products, again with a link back to your Etsy shop.

Consider investing some money in paid advertising. You could spend a few pounds boosting your Facebook fan page posts, for example, so they reach a much larger target audience.

Google Adwords is another advertising medium you could consider if your product is something people regularly search for using keywords. You won’t usually be able to show pictures using this method, of course.

Share links to your Etsy shop and individual product listings on Twitter. You may wish to set up a Twitter account specifically for your shop as well.

You can also pay to have your listings show up more prominently in search results on Etsy.

As sales start coming in, it’s important to keep in touch with your customers and answer any questions they ask promptly. This will help you get good reviews and ratings on Etsy, and may also turn some buyers into loyal customers who keep coming back for more. Plus the feedback you get can be invaluable for deciding what new products to offer in future. Etsy is in many ways a community of buyers and sellers, so grasp every opportunity to take advantage of this.

Final Thoughts

You won’t make a fortune from Etsy, but if you like arts and crafts, it can be a great way of earning money while doing something you enjoy.

It’s free to get started, and you can do it part-time or full-time. Etsy even lets you put up the virtual shutters on your shop for a week or two, if you want to go and spend some of your profits on a well-earned holiday. Check it out today, then take get out your scissors, your wire-cutters or your paintbrushes, and get crafting!

As always, if you have any comments or questions about this post, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

If you enjoy arts and crafts, did you know you could make money selling them on Etsy? In this two-part series, I’ll be revealing how you can do this to generate a second income or even a full-time living.

For anyone who may not know, Etsy is a website where anyone can set up an online store for handmade craft items. You can also sell ‘vintage’ items that are at least twenty years old, and art and craft supplies.

That means Etsy has a particular appeal to anyone with a creative talent. Even if you don’t, however, you can still sell items made by other people. You could even offer products sourced through online auctions, car boot sales, second-hand shops, and so on.

Right now, as you may imagine, there is a huge demand for attractive face masks and coverings. This could be a great product to offer on Etsy at the moment, although of course you will be facing some serious competition!

All About Etsy

Etsy started in New York in 2005 and has grown in leaps and bounds ever since. It is now a world-wide operation with offices round the globe.

One thing to note about Etsy is that a high proportion of users are women. Etsy doesn’t publish any figures itself, but an estimated 86% are female. One study reported that the typical Etsy customer was ‘an 18–34-year-old college-educated white female with no children, who makes less than $60,000 a year’.

Of course, that is a broad generalization, and in practice both buyers and sellers may be from other demographic groups as well. But it is still important to bear in mind that this is the typical profile of the potential buyers you will be targeting.

What Sells on Etsy?

Etsy is a marketplace for handmade craft items. Just a few examples include jewellery, tote bags, key chains, scarves, clothing, scented candles, duvet covers, sandals, mugs, soaps, cosmetics, phone cases, kitchen and garden accessories, and many more.

Many sellers offer buyers the opportunity to personalize their purchases. For example, they may be able to have their name and/or photograph incorporated in the design. Custom portraits (human or pets), usually created from photos, are also very popular.

Vintage items, especially clothing and jewellery, sell well too. And there are many people making good money on Etsy selling art and craft supplies, from beads to jewellery-making tools, yarns to knitting patterns.

How Does It Work?

Anyone can join Etsy and set up an online shop on the website. It’s easy to do, and no technical expertise is required.

Even better, there is no charge for creating a shop either. There are just a few fees you will have to pay once you’re up and running. One is a listing fee of 16p per item to have it displayed in your shop for four months. There is also a 5% transaction fee and a payment processing fee of 4% plus 20p.

Obviously these costs must be taken into account when pricing products (discussed next time). But they are still a lot less than the overheads you would have to pay if running a bricks-and-mortar store.

There are various ways you can collect payment in your shop, but the simplest (and most popular) is Direct Checkout. This will allow you to accept payments by credit or debit card, PayPal, Apple Pay, bank transfer, and more. If you use Direct Checkout, Etsy will accept payments on your behalf and transfer your earnings (less fees) to your bank on a fortnightly basis.

It is, of course, up to you to arrange shipping of purchases and you can charge what you like for this. You will also need to liaise with your customers and follow up any queries.

Other than that, all you have to do is make your products and count your profits!

Choosing What to Sell

This is clearly a crucial decision, and it isn’t something to rush. Spend some time browsing the Etsy website to see what the most successful shops are selling. You can get some idea how successful a shop is by noting how many reviews it has received and how many times it has been favourited.

Don’t make the mistake of choosing a product to sell simply because you like it. And, especially, don’t fall into the trap of thinking you need to offer something new or original.

On the contrary, there is much to be said for looking for products that are selling well on Etsy and offering something similar yourself. Remember that people will be actively searching for things such as tee-shirts, bracelets and handbags. By contrast, if you are selling a ‘pink thingumijig’ or some other unique item, nobody will be searching for that, so attracting potential buyers will be much harder.

Here are a few more tips for deciding what to sell…

Other things being equal, try to choose small items that are easy to pack. The lighter the better as well, as this will keep postal costs down.

But try to avoid choosing items that are delicate or fragile. We all know what can happen to them in the mail!

Consider whether products can be customized or (even better) personalized in some way. As already mentioned, such items are very popular on Etsy.

Choose something you like and enjoy making. If it sells well you’ll be making large numbers, so don’t pick something you will quickly get bored with.

Choose something that photographs well too, as people make buying decisions largely based on this. More about photography shortly.

Ensure that the supplies or raw materials you need are easy to obtain. You don’t want to have to close your shop because your only supplier has shut down.

Finally, think about the cost of your time. If making the product in question is very time-consuming, will you be able to charge buyers enough to make it worth your while?

Naturally, if you have a particular creative talent, you will want to sell products that capitalize on this.

Even so, it’s important to think carefully about the matters above, and see how you could channel your skills into making something that not only showcases your talents but will also sell well and make you a decent profit.

Of course, whatever decision you make now isn’t set in stone. If your first choice product doesn’t sell, you can always try again with something else. Your only costs will be the raw materials and Etsy’s (low) listing fees. Even once you are selling successfully, you should be constantly refining your product range and looking for new things you can offer your customers.

Next time I will take you through opening your Etsy shop, pricing products, taking photos, promoting your shop, and more.

If you enjoyed this post, please link to it on your own blog or social media:

Today I have a guest post for you from my old friend John Goss, who blogs at All the Goss.

John blogs about a range of subjects, including politics and media. In this post he writes about the government’s recent decision to make face masks in shops compulsory in England and why he believes this is a mistake. The post struck a chord with me, so I asked John for permission to republish it on PAS, which he kindly gave me. At the end of the post I will add a few thoughts of my own on the subject.

Over to John, then…

It is not for me to tell others how to behave. For myself, however, I am unable to wear a face mask because of a medical condition.

Maskaphobia is a lot more common than people may think. It can start in childhood, get further endorsed in the dentist’s chair, by horror movies and scary images – an example might be the image of an executioner or a “wild animal in a black mask” to quote one of my favourite poets, George Ivanov (1894-1958). The condition is serious.

It has been announced that the wearing of face masks in shops will be compulsory from 24 July. This will make it intolerable for maskaphobes. Other people wearing masks can only cause more stress for this growing sector of the population. Other illnesses as well as maskaphobia are made worse by the wearing of masks.

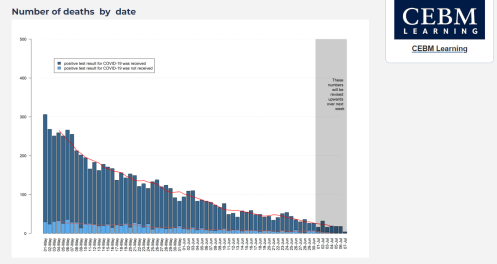

So is this directive from the government necessary? The graph below charts the falling number of deaths where Covid-19 has been reported from 1 May to 7 July. I think people can see for themselves that this sudden imposition of face masks is a simple test to see just how simple, gullible and pliable to government dictates the UK populace is.

People with disabilities, including deaf, blind and paranoid, may suffer adversely from mask apparel. Other medical conditions which are exacerbated by the wearing of masks include asthma and respiratory illnesses. People with high blood-pressure should not wear masks because added CO2 will increase their blood-pressure. Nearly everyone will have some condition which the wearing of face-masks will make worse.

Mine is not maskaphobia. Well not yet, though I do feel a strong aversion to masks, which is growing by the day. For me it is something else.

Medical conditions are private between you and your GP. You do not need to tell any third party what yours is. Explaining that you have one should be sufficient.

Many thanks again to John for allowing me to republish his post. You can read more of John’s work at https://johnplatinumgoss.com.

Regular readers of Pounds and Sense will know (e.g. from this post) that I am also opposed to the imposition of mandatory face coverings in shops and supermarkets. In my view any benefits they may confer are marginal at best. What’s more, if incorrectly used (as many do) they can actually increase the risk of transmission. On my last visit to my local Morrisons I saw several people fiddling with their masks and one actually hold it to his face and then touch items on the shelves with the same hand. If you were deliberately trying to transmit the virus, you could hardly do better than that.

I am also concerned that – contrary to what the government appears to believe – this measure will not encourage people to go out and shop. Indeed, the reverse is true. For example, a recent Twitter poll of over 43,000 people by Martin Lewis of Moneysavingexpert fame found that significantly more people said they would be less likely to go to the shops if masks are compulsory than those saying it would make this more likely.

Of course, PAS is aimed especially at older people and people with disabilities, and I am particularly concerned about the impact this measure will have on them. Here is one typical comment from Martin Lewis’s survey…

As someone who wouldn’t be wearing one on health grounds it makes me more anxious that I’d be subject to ridicule/online ‘calling out’ and abuse. So while it’s in force I won’t go to a shop unless life & death in a bid to look after my mh [mental health]

At a time when many of us are experiencing extreme stress and other mental health worries, it seems wrong to me that as a result of this measure many people feel they are being forced back into isolation.

I would like to close by endorsing again what John says in his article. If you have a medical or psychological condition that is exacerbated by wearing a mask, you do NOT have to wear one. Neither do you have to provide proof of the condition, or even explain to shop staff (or anyone else) what it is.

Although it’s not essential, if you would like a way of showing you are exempt from the requirement to wear a mask – for medical or psychological reasons – you can buy a badge/lanyard (see picture below) from.the Disability Horizons online shop. This has no official status (not that this is needed) but may reduce the likelihood of your being challenged.

As always, if you have any comments or questions about this post, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

As you may have heard, the BBC has now confirmed that from 1st August 2020 people over 75 in the UK will lose their automatic right to a free TV licence and have to pay the same £157.50 a year as everyone else. This was originally due to happen in June 2020, but it was postponed due to the coronavirus pandemic.

For many old people, TV is their main (or only) source of company. Suddenly having to find this quite large sum out of (in many cases) a very limited income may cause them financial difficulties or downright hardship. Some may even have to choose between watching television and paying their heating bills.

This parlous situation has arisen because the BBC say they have to make economies, and continuing to subsidise free licences for the elderly would force them to cut back drastically in other areas. Meanwhile the government, despite their pre-election promises, has shown no sign of stepping in to preserve free TV licences for over 75s (which they could perfectly well do). Although charities such as Age UK have been raising petitions and applying as much pressure as they can, it now seems certain that this change is going to happen.

So what can people in this situation – or their relatives/friends/carers – do? The BBC have allowed just one concession – the poorest over-75s can continue to receive a free TV licence if they claim and receive pension credit. So let’s look at this in a bit more detail…

Pension Credit

Pension credit is a state benefit for people above retirement age who are on a low income. It can be paid to single people or to couples. It is usually paid weekly, though you can also choose to have it paid fortnightly or monthly.

Along with attendance allowance – which I discussed in this recent post – pension credit is one of the most under-claimed benefits. According to the Department for Work and Pensions, around 40 percent of eligible people, or two in five, fail to claim it. That’s an estimated 1.5 million eligible households in the UK who are missing out.

Pension credit actually comes in two parts – guarantee credit and savings credit. Guarantee credit boosts your weekly income to £167.25 if you’re single or £255.25 if you’re a couple (all figures correct as of March 2020). You may be eligible for guarantee credit if you have reached state pension age and your total income is less than these amounts (even if you own your own home). If you have under £10,000 in savings and investments this will not be taken into consideration. If you have over £10,000, it will be assumed that you earn £1 a week per £500 of savings and investments (equivalent to an interest rate of 10.4% – if only!). This will be added to your total income when working out your eligibility.

Savings credit is meant to be a reward for those who have saved for their retirement. It’s worth up to £13.73 a week for a single person or £15.35 for couples. To qualify, you must have a minimum income of £144.38 a week if you’re single, and £229.67 a week if you’re in a couple. For every £1 by which your income exceeds this amount, you get 60p of savings credit – up to the £13.73/£15.35 maximum. If your income is less than the £144.38/£229.67 savings credit threshold, you won’t qualify. Savings Credit is only available to people who reached state pension age before 6 April 2016. Couples where only one partner reached state pension age before 6 April 2016 can also retain savings credit if the older partner had reached 65 and qualified for savings credit before that date AND they have remained continuously entitled to it ever since.

It’s worth adding that if you pay mortgage interest or have other housing costs, have caring responsibilities, are responsible for a child, or are severely disabled, you may be entitled to more pension credit. If you receive attendance allowance or carers credit, for example, this may boost the amount you’re entitled to. The rules surrounding all this are complicated, but the government has provided a free online calculator you can use to work out whether you qualify and how much you might get. This is for guidance only, however. You can’t apply via the calculator and there is no guarantee that you will receive the amount it shows you.

To actually apply you will need to phone the DWP’s Pension Credit helpline on 0800 991234. You will need your National Insurance number, information about your income, savings and investments and your bank account details. The person you speak to will then take you through the application process. This is a subject I discussed in more detail in this blog post, as I recently helped an older friend to do this successfully.

What Does Pension Credit Entitle You To?

As well as the money – which can amount to thousands of pounds a year – if you receive pension credit you will be entitled to a range of additional benefits. A free TV licence if you are over 75 is just one of them. You may also get:

reduced council tax (or free if you are awarded guarantee credit)

Even if you only receive a small amount of pension credit, you will be eligible for all of the above. So it really is well worth applying if there is any chance you may qualify. As mentioned above, you can check first using the free online calculator here and then apply by phoning the DWP’s Pension Credit helpline on 0800 991234.

Don’t delay, as there are now just seven weeks left before the free TV licence for all over-75s becomes a cherished memory.

Equity Release to Boost Your Income

If you’re still struggling to pay the bills even with pension credit, there are other methods to help boost your income. In particular, UK homeowners are fortunate to have opportunities to unlock their property value. An equity release loan could provide the security you desire if you require the means to pay for life’s simple pleasures or cover essential costs.

What’s more, homeowners can unlock up to 65% of their property value, with no compulsory payments required during their lifetime. There’s no limit on how you can use the tax-free cash you receive, so an income lifetime mortgage could be the ideal way to pay your bills and have a bit extra for luxuries as well.

Regular readers will know that I have been posting about my personal experience of the coronavirus crisis since lockdown started (you can read my June update here if you like).

In what I hope will be my final update, I thought I would discuss what has been happening with my finances and my life generally over the last few weeks. As previously, I will start with the money-related stuff…

Financial

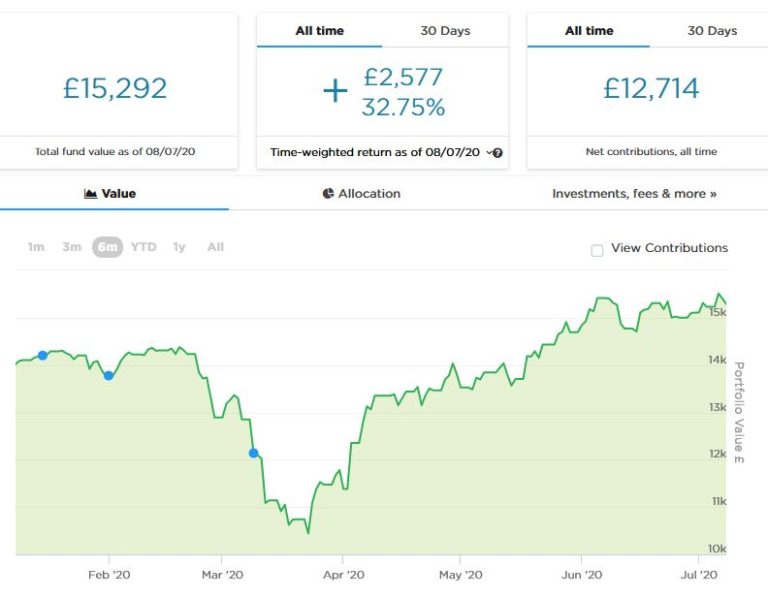

Overall things haven’t changed dramatically since my update last month. Here’s the latest chart showing how my Nutmeg stocks and shares ISA is faring…

As you can see, my ISA made a good recovery after losing over a third of its value in March (admittedly I helped things along by investing another £1,000 when the markets were near their lowest point). In the last few weeks things have plateaued somewhat, though the overall trend is still upward. Allowing for the extra £1,000 invested in March, my portfolio is now back at the level where it was before the crisis started.

Assuming there is no major second wave of the virus – and there has been little sign of that so far – I am hopeful the recovery will continue over the longer term. Of course, there are likely to be bumps along the way, and in the short term at least we face the likelihood of a recession. Even so, I am keeping my fingers crossed for a recovery over the next year or so, and am continuing to invest cautiously where I see value. I haven’t put any more money into my Nutmeg ISA yet but definitely plan to. I may, though, take the opportunity to reduce my risk level (which is easy to do from the Nutmeg dashboard). Do take a look at my in-depth Nutmeg review if you haven’t already.

My monthly payments from my two Buy2LetCars investments (totalling around £420) continue to appear in my bank account every month like clockwork. I was initially wary about this, as it is obviously a bit outside the usual range of investments. However, I have had no issues at all, and am glad also to be supporting key workers by providing reasonably priced transport for them.

Again, if you’d like to learn more, you can read my review of Buy2LetCars here and my more recent article about the company here. Obviously the minimum investment is £7,000 so this opportunity isn’t going to be for everyone – but if I had that sort of money burning a hole in my pocket right now, I wouldn’t hesitate to invest through them again. Each car generates a monthly income, with a large lump sum at the end of the three-year term. Interest rates range from 7 to 12 percent per year.

My other equity-based investments generally are doing about as well as could be expected in the circumstances and in some cases better. In particular, my Bestinvest SIPP hasn’t lost any significant value when you allow for the fact that it’s in drawdown and I am currently withdrawing £200 a month from it. I’m not claiming any special skills as a stock picker, but having a broad range of funds in my portfolio has undoubtedly served me well. Years ago, also, I decided to invest some of my pension money in specialist healthcare funds, and these have done better than average over the last few months 🙂

On the property crowdfunding side, the picture isn’t so rosy. A number of my property investments still seem to be stuck in limbo, though I did hear from The House Crowd that they had received an offer for a house in Liverpool in which I invested £1,000 six years ago (pictured below).

The offer was for slightly less than the original purchase amount, but nonetheless the investors (including me) voted by a clear majority to accept it. So I will get a bit less than my original £1,000 back, though when you add in the dividend payments (from rent) since I first invested, I should be slightly up overall. But that’s before you allow for inflation, of course!

I am hoping that the Stamp Duty holiday announced by chancellor Rishi Sunak this week will help get the housing market moving and maybe ‘unstick’ some of my other property crowdfunding investments that have been on hold for a while. In retrospect I probably let my enthusiasm for the property crowdfunding concept run away with me a bit in the past. Overall I have still made some money from these investments, but not as much as I hoped or expected. And I still have a fair-sized sum tied up in properties I really expected to be sold by now. I do still think property crowdfunding can merit a place in people’s portfolios, but would advise diversifying as much as possible across platforms and properties. And definitely don’t invest money you might need any time soon!

Finally on this subject, I would just say that I exclude property loan investment platform Kuflink from the criticisms above. All of my investments with them have been doing well. Although there was a short delay with one loan, it has now been repaid (with added interest). Kuflink are adding new investment opportunities to the platform most days and I have been investing modestly in them, along with loan portions that have just a few months left to run via the Kuflink Marketplace. See my Kuflink review here for more information. Their up-to-£4,000 cashback offer for new investors is still open, incidentally.

One other thing I have mentioned before is that I have a few invitations available for an unusual sideline-earning opportunity based on matched betting. I have been asked not to divulge too many details about it on the blog for very good reasons I will explain privately to anyone who may be interested (and no, it’s not illegal!). What I can say is that it doesn’t require any financial outlay, is entirely hands-off, and will provide an income of £50 a month. No knowledge of betting is required, and you won’t have to place any bets yourself. Just note that the opportunity is only open to people who haven’t done matched betting before and have no more than two accounts already with online bookmakers. For more info (and receive a no-obligation invitation) drop me a line including your email address via my Contact Me page 🙂

Personal

As I’ve said before, I live on my own since my partner, Jayne, passed away a few years ago. I am lucky to live in a fairly large house with a good-sized garden, so being mostly confined to home hasn’t been as big a challenge for me as I’m sure it has for some. Also, I am well used to working from home, having done this for the last 30 years or so.

Nonetheless, the ongoing nature of the crisis is undoubtedly taking its toll on me. Every day seems so similar it is starting to feel like Groundhog Day. And while that is one of my all-time favourite movies, I definitely don’t want to live in it myself. Mind you, I saw someone on Twitter compare their experience of lockdown at home with the Overlook Hotel in The Shining. At least I wouldn’t claim it’s as bad as that!

So far as work is concerned, as you may know I’m a semi-retired freelance writer and editor (age 64). I’ve had very little work since the lockdown started, and was duly grateful to receive some financial support from the government’s SEISS scheme. I have, though, been keeping myself busy (and sane) with this blog and – as you may have noticed – have enjoyed quite a productive period. I ran out of inspiration a bit this week, but hopefully that is just a temporary blip.

I am still available for freelance writing, editing or proofreading work, although I am not taking on book-length projects any more. Feel free to drop me a line if you think my services might be of interest to you 🙂

Life generally is changing now as – touch wood – the worst of the pandemic appears to be behind us. The experience of shopping is still evolving and I guess it will be many months before it is entirely back to normal. I haven’t yet been to any ‘non-essential’ shops, but at my local Morrisons supermarket it feels a bit more relaxed. I would say only about a quarter of people are wearing masks or other face coverings now. I was wearing a bandana over my nose and mouth but have mostly stopped that unless I find myself surrounded by other shoppers. Of course, in England face coverings are now compulsory on public transport, so I will be keeping my bandanas washed and ready for that.

UPDATE: Just heard that the government is considering making the wearing of face-masks in shops in England compulsory. I find that bizarre at a time when – apart from a few local outbreaks – the virus is waning rapidly. It also sends out a mixed message at a time when the government is encouraging people to eat out, obviously not wearing masks. And the evidence in favour of wearing masks in public is weak anyway. Personally I really hope.the government refrains from doing this.

Many pubs are open again now. I walked past my nearest, The Drill, on Sunday afternoon. It all looked quite continental, with people sitting at tables outside and waitresses going in and out with trays of beer and other drinks. There was a happy buzz of conversation and laughter. The only less cheerful note was struck by the manager standing by the door with a clipboard, presumably taking the contact details of people as they arrived for contact-tracing purposes. I wasn’t tempted to go in myself, though I don’t rule out going for a drink and a meal soon, maybe taking advantage of the government’s £10 off vouchers 🙂

I am still looking forward to my short break in Minehead in September, which I booked before this crisis happened. I am also mulling over whether to try to book a couple of days away in August. I worked out the other day that I have been to Wales every year for over 30 years, and it would be a shame to break that long run in 2020. Llandudno or Aberystwyth could both be contenders.

I am still working my way through my box sets of Deep Space Nine and Bergerac. With the latter, it’s quite interesting to see how mobile phones evolved as the series was made. In the earliest episodes I guess they didn’t exist at all, and Bergerac’s office generally seemed to know telepathically where he was and phoned him at his father-in-law’s or wherever. Later on car phones make an appearance, and then house-brick-sized mobiles with aerials sticking out of them. Ah, the nostalgia!

I am trying not to spend too much time on social media as I know it’s bad for my mental health. There are a few people I follow regularly on Twitter and and enjoy hearing from, though. Last time I mentioned Professor Karol Sikora, a well-respected cancer specialist with a doctorate in immunology. Many people, including me, have found him a beacon of hope amid all the negativity, with his generally positive and optimistic view (though still informed by science and statistics). He doesn’t have a political axe to grind and is willing to give the government credit for things they have done well and criticize things they have done badly. If you want one person to follow for unbiased news about the pandemic with a measure of hope for the future, I highly recommend checking out his Twitter page.

Lately I’ve also been enjoying reading the posts of Scottish blogger Effie Deans (who blogs as Lily of St Leonards). She is a Scottish academic who has a lot of interesting things to say about nationalism, education, culture, and more. You may or may not agree with all her views; but if you want an interesting and genuinely thought-provoking perspective on events from someone who isn’t afraid to challenge current orthodoxies, I highly recommend checking out her Twitter page and blog.

To end on a positive note, I am looking forward to having my hair cut for the first time in four months next week. I’ve actually quite enjoyed revisiting my long-haired student days, but enough is definitely enough! I am also looking forward to going swimming again after it was announced that outdoor pools can reopen from tomorrow and indoor pools a fortnight later. The David Lloyd Leisure club I belong to has both indoor and outdoor pools, so I am waiting to hear whether they will be opening the outdoor pool immediately or whether I will have to wait a bit longer till both pools can reopen. (UPDATE – Now heard I have to wait another fortnight 🙁 )

So that has been my experience of the coronavirus crisis to date. I do of course appreciate that I am in a fortunate position compared with many others, and hope you and your family are coping in these strange and worrying times. Here’s hoping that things continue to improve and we can all return in due course to something approximating normal life.

As ever, I’d love to hear your thoughts and experiences. If you have any comments or questions, as always, please do post them below.

Disclaimer: I am not a registered financial adviser and nothing in this post should be construed as personal financial advice. You should always do your own ‘due diligence’ before investing and seek advice from a qualified financial adviser/planner if in any doubt how best to proceed. All investments carry a risk of loss.

If you enjoyed this post, please link to it on your own blog or social media: