My Investments Update – July 2026

Here is my latest monthly update about my investments. You can read my June 2026 Investments Update here if you like.

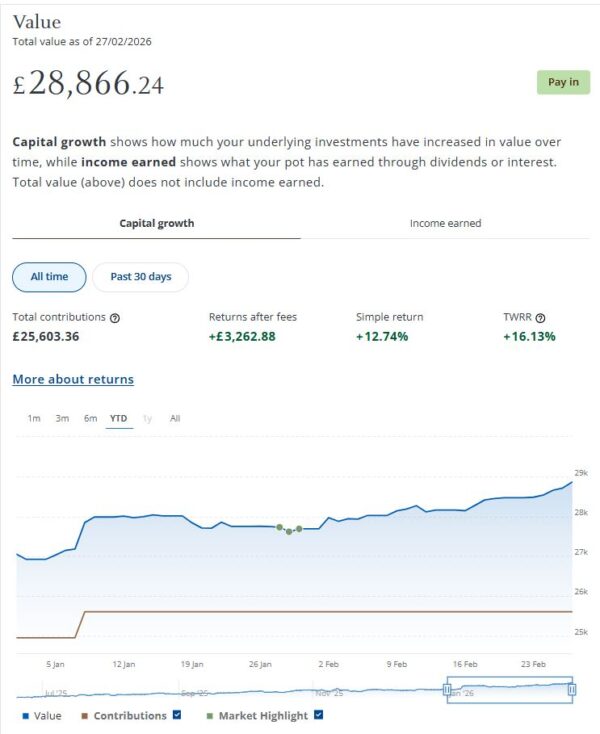

I’ll begin as usual with my JP Morgan Personal Investing (previously Nutmeg) Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

As regular readers will know, in June last year I transferred most of the money in my former Nutmeg Fully Managed portfolio (just under £25,000) to a new Nutmeg Income Portfolio. I discussed this in detail in this post, but basically money in this port is invested to generate an income from share dividends and other sources. This is then paid monthly. Capital appreciation is targeted as well, but these portfolios are aimed primarily at older people (and others) who want/need their investment to generate a regular cash income.

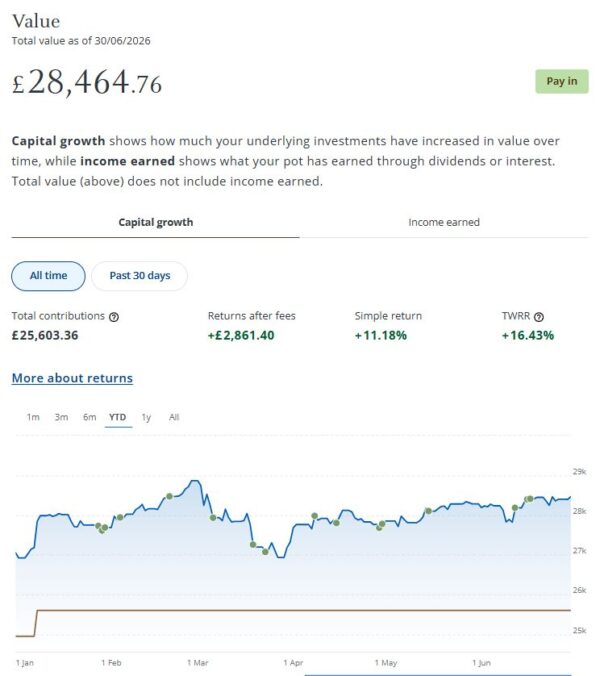

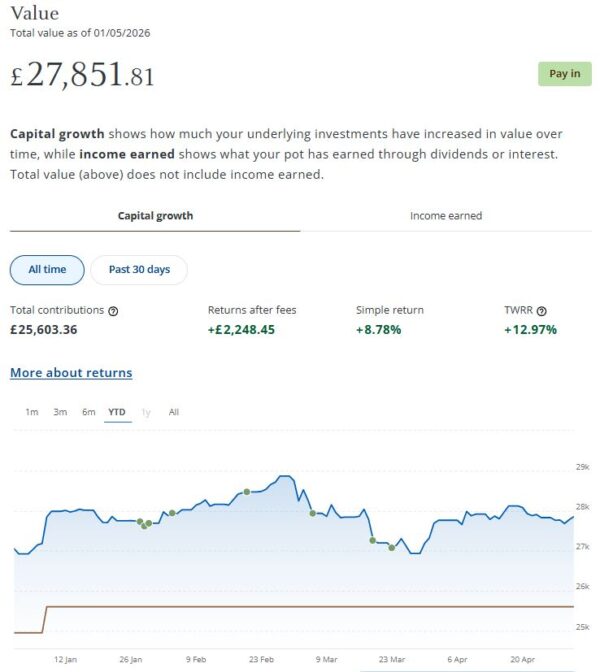

In June my JPM Investing income portfolio generated a respectable £222.45 of income, which was duly paid into my bank account on 24 June 2026. That means I have now received tax-free income of £647.83 in 2026 and a total of £1,119.29 since I opened the account in June last year. That’s a return on capital of a little over 4.48% to date. That is pretty much in line with JPM’s original projected annual return of just under 5% for income ports at my chosen risk level (five).

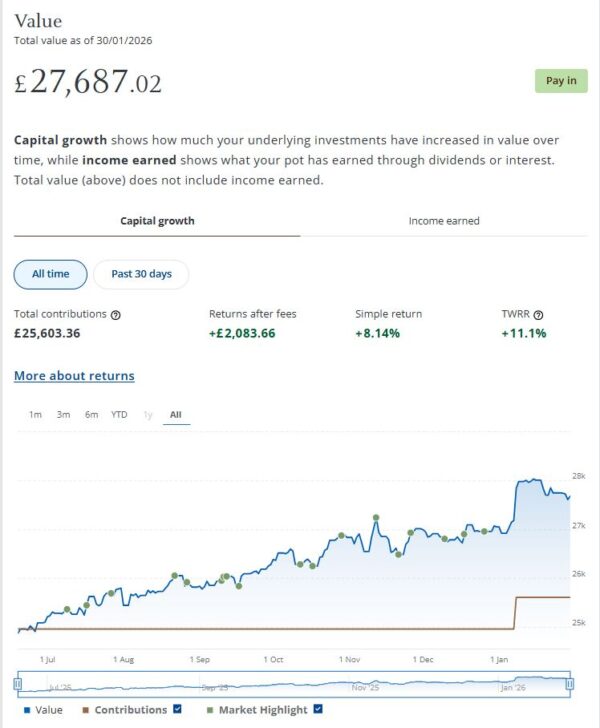

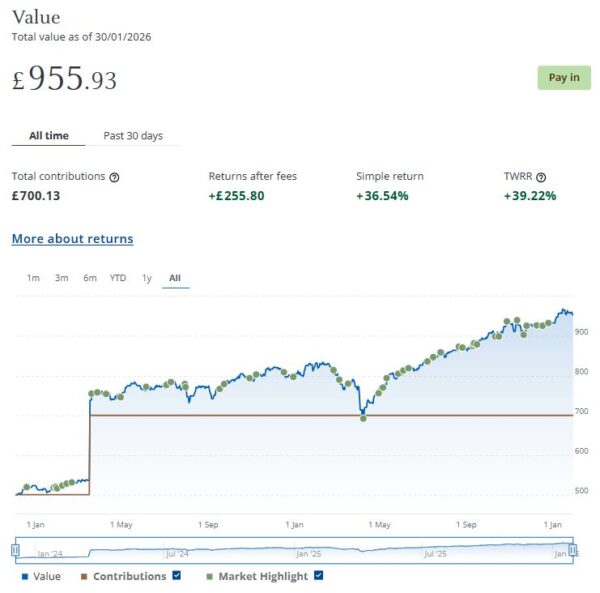

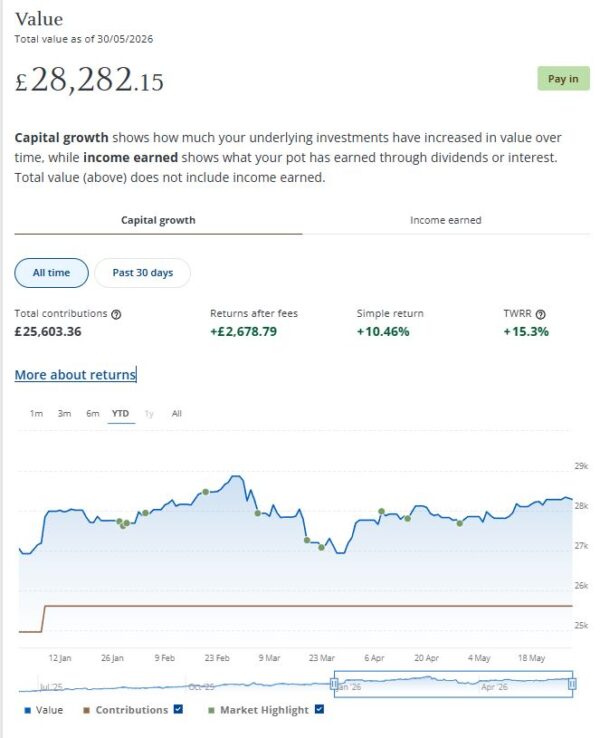

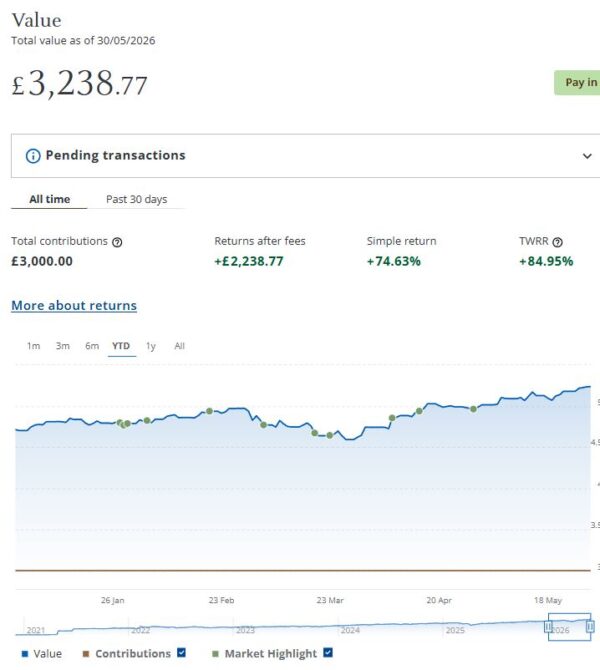

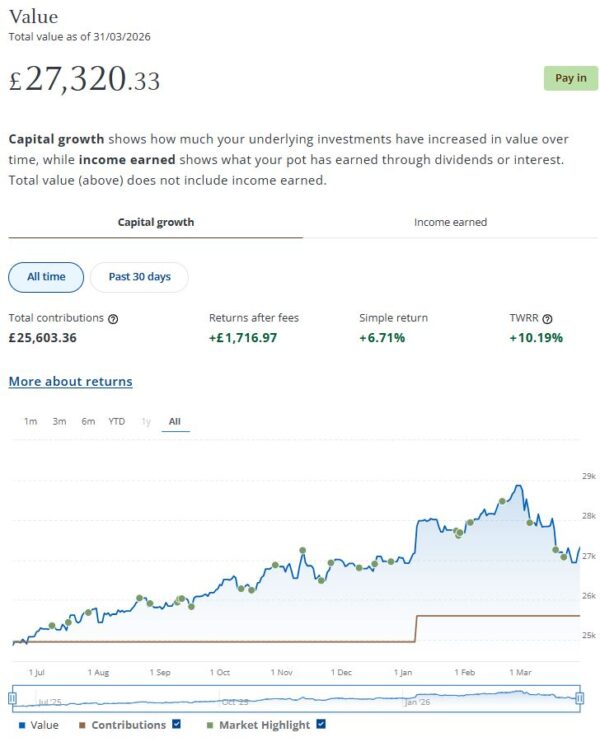

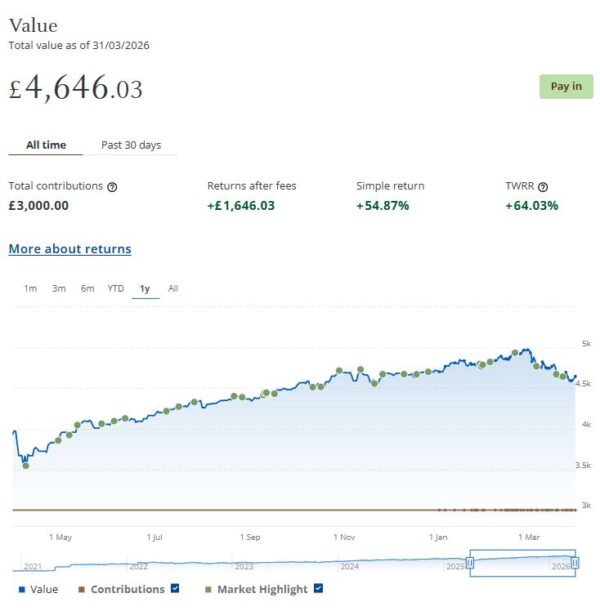

My income portfolio increased in value again in June. It’s now worth £28,465 (rounded up) compared with £28,282 at the start of June, a rise of £183. As the screen capture below shows, my income port is up by a respectable £2,861 (11.18%) after fees since I opened it last June (about a year ago).

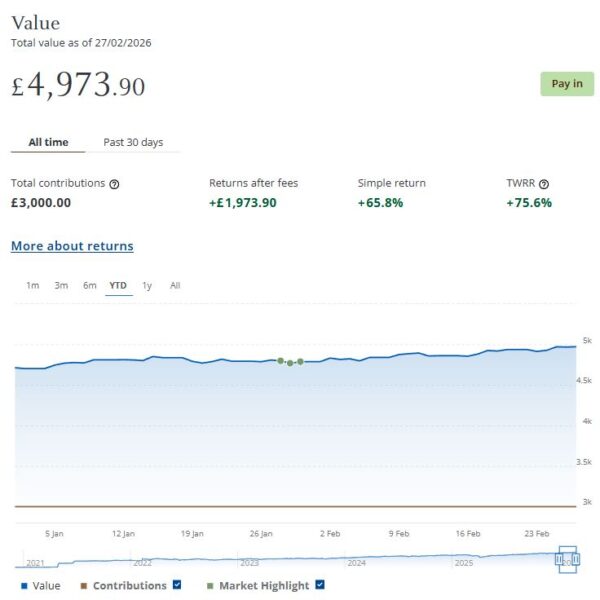

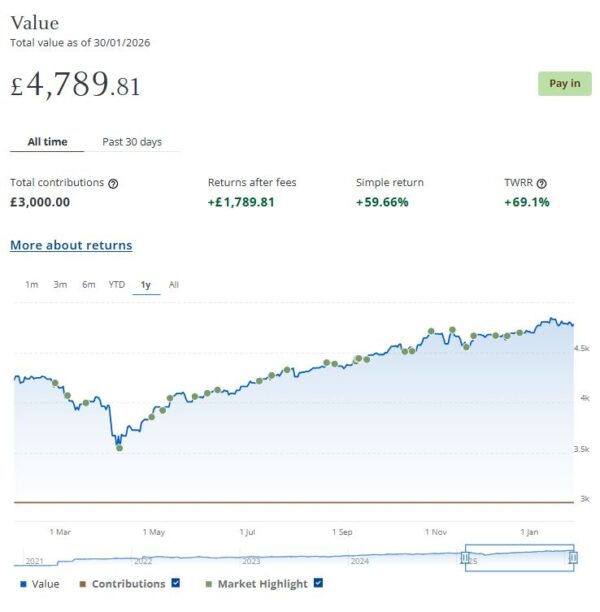

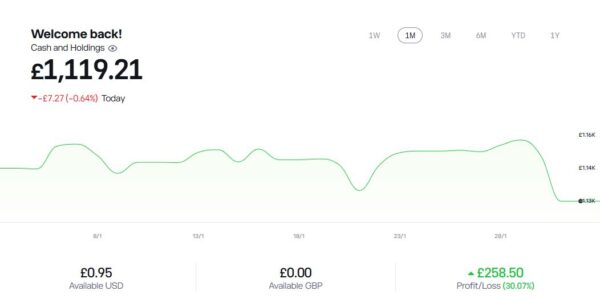

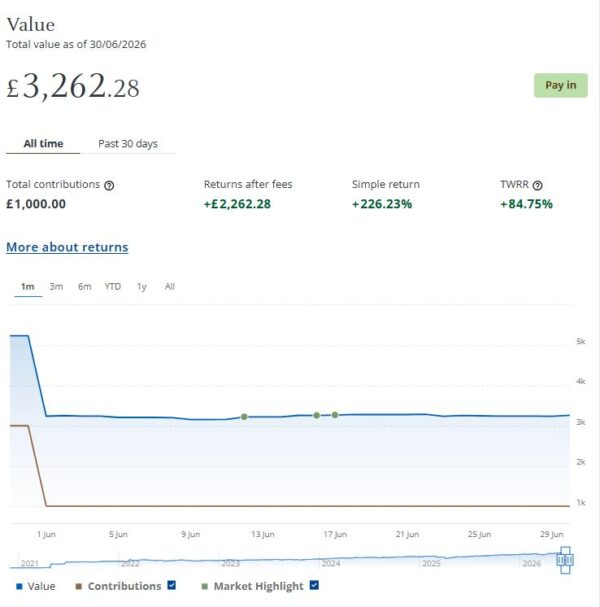

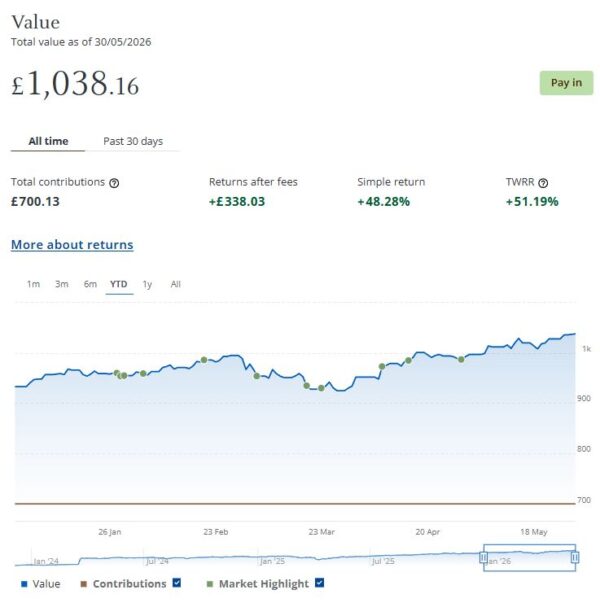

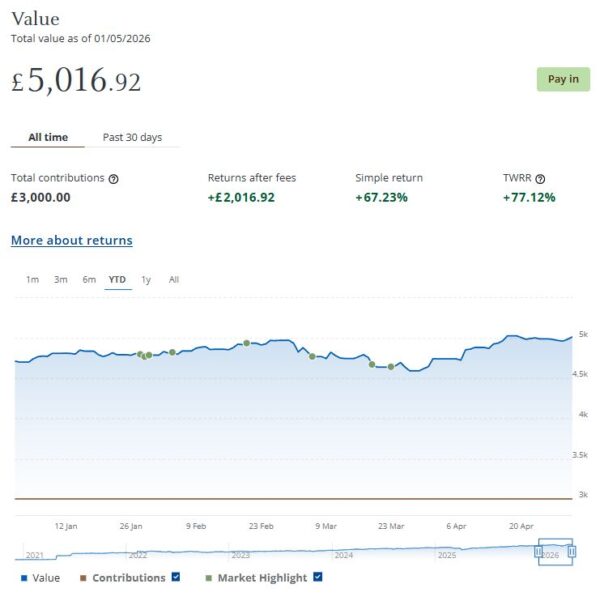

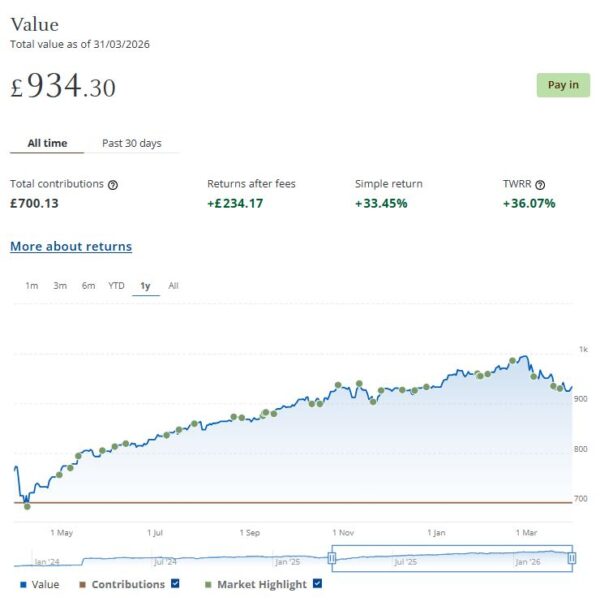

I still have a smaller, growth-oriented pot using JPM Investing’s Smart Alpha option. This is now worth £3,262 compared with £5,239 a month ago. As I mentioned last month, in early June I withdrew £2,000 from this portfolio to pay for some building work, so if you deduct this the value of the port has actually risen by £23. Here is a screen capture showing performance over the last month.

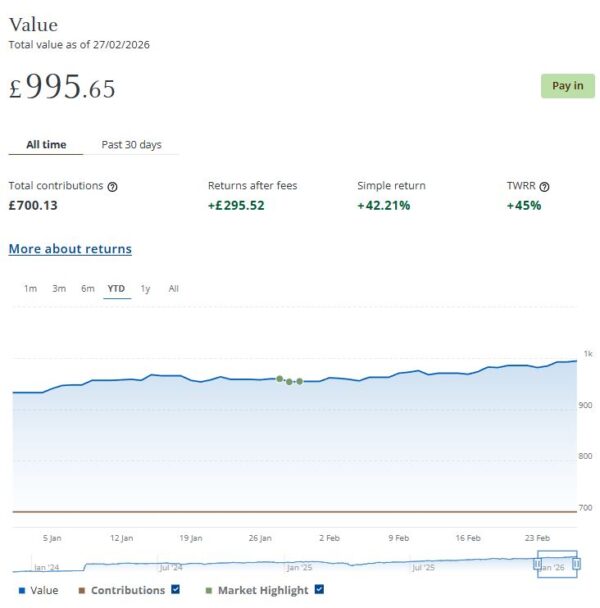

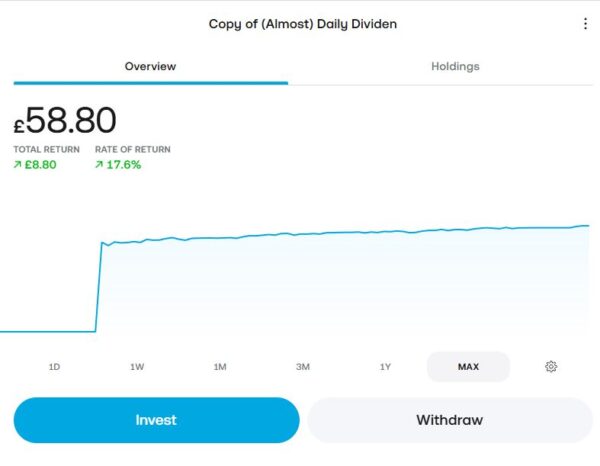

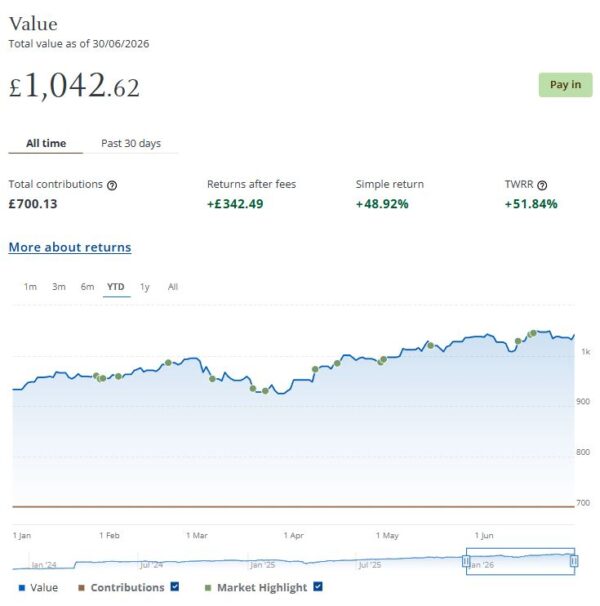

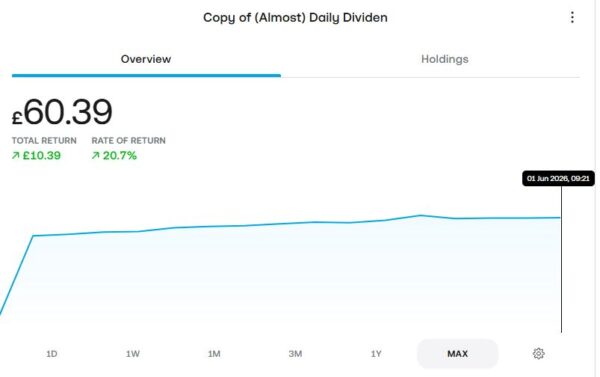

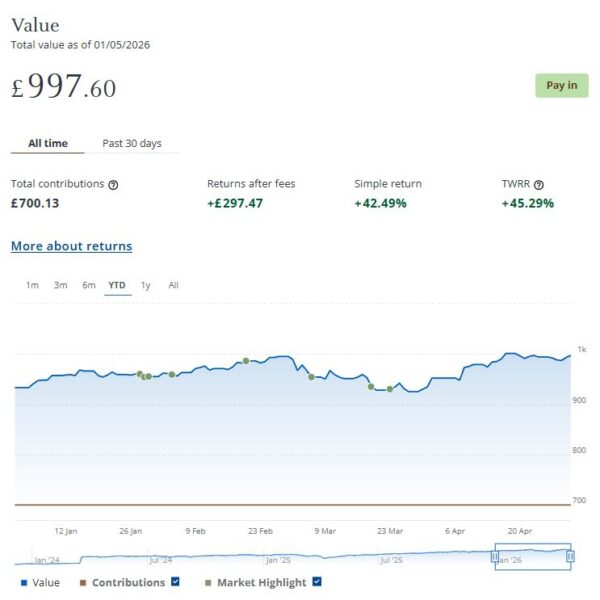

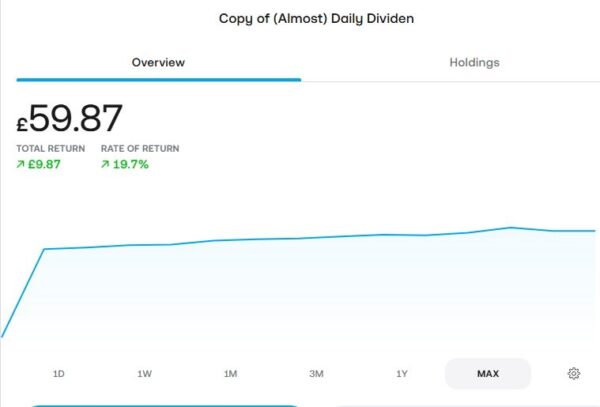

Finally, at the start of December 2023 I invested £500 in one of Nutmeg/JPM’s thematic portfolios (Resource Transformation). In March 2024 I also invested a further £200 from referral bonuses (something I no longer receive). As you can see from the YTD screen capture below, this portfolio is now worth £1,043 (rounded up) compared with £1,038 last month, a small rise of £5.

Overall in June (and allowing for the £2,000 I withdrew) the value of my JPM investments rose by £220 or 0.65%. In addition I did, of course, receive £222.45 in income from my income portfolio. In total, then, I am £442.45 up for the month.

Excluding income generated (and again allowing for the £2,000 withdrawal) the overall value of my JPM investments is up by £3,997 or 12.99% since the start of July 2025. If you add to this the £1,119.29 of income generated by my Income portfolio to date, that gives a total profit for the last 12 months of £5,272.84 – a pretty good return in these uncertain times.

Some volatility is always to be expected with stock market investments, but in the longer term they tend to even themselves out (and typically outperform bank savings accounts, although that is never guaranteed). In general the worst thing you can do is panic and sell up when downturns occur (as happened in March due to events in the Middle East). You are then crystallizing your losses rather than giving the markets time to recover. That is something I discussed last year in this blog post.

You can read my full original Nutmeg/JPM review here. If you are looking for a home for your annual ISA allowance, based on my overall experience over the last nine years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs), Lifetime ISAs and Junior ISAs as well.

- As mentioned, Nutmeg have rebranded as J.P. Morgan Personal Investing and their website is now at www.personalinvesting.

jpmorgan.com.

Moving on, I also have investments with P2P property investment platform Housemartin. As discussed in this post, the company rebranded last year from Assetz Exchange.

My investments with Housemartin continue to generate steady returns. Housemartin focuses on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my HM portfolio has generated a respectable £328.30 in revenue from rental income. I have made a small net loss of £17.60 on property disposals. Capital growth generally has slowed, in line with UK property values generally.

At the time of writing, 21 of ‘my’ properties are showing gains, 5 are breaking even, and the remaining 18 are showing losses. My portfolio of 44 properties is currently showing a net decrease in value of £64.57. That means that overall (rental income minus capital value decrease and loss on disposal) I am up by £246.13. That’s still a respectable return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Housemartin most projects are socially beneficial as well.

- A further consideration is that property investments on Housemartin are less likely to be affected by stock market downturns, as happened in March due to events in the Middle East. This again demonstrates the potential value of such investments for diversifying your portfolio during challenging times.

The net fall in capital value of my Housemartin investments is obviously a little disappointing. But it’s important to remember that until/unless I choose to sell the investments in question, it is largely theoretical, based on the latest price at which shares in the property concerned have changed hands. The rental income, on the other hand, is real money (which in my case I’ve reinvested in other HM projects to further diversify my portfolio).

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of Housemartin as far as i am concerned. You can actually invest from as little as £1 per property if you really want to proceed cautiously.

- As I noted in this blog post, Housemartin is particularly good if you want to compound your returns by reinvesting rental income. This effectively boosts the interest rate you are receiving. Personally, once I have accrued a minimum of £10 in rental payments, I usually reinvest this money in either a new HM project or one I have already invested in (thus increasing my holding). Over time, even if I don’t invest any more capital, this will ensure my investment with Housemartin grows at an accelerating rate and becomes more diversified as well.

My investment on Housemartin is in the form of an IFISA so there won’t be any tax to pay on profits, dividends or capital gains. I’ve been impressed by my experiences with Housemartin and the returns generated so far, and intend to continue investing with them. You can read my original review of Assetz Exchange/Housemartin here and my article about the rebranding to Housemartin here. You can also sign up for an account directly via this link [affiliate].

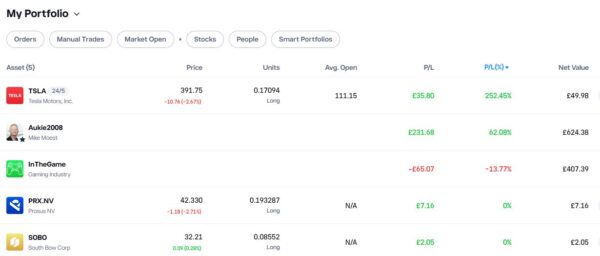

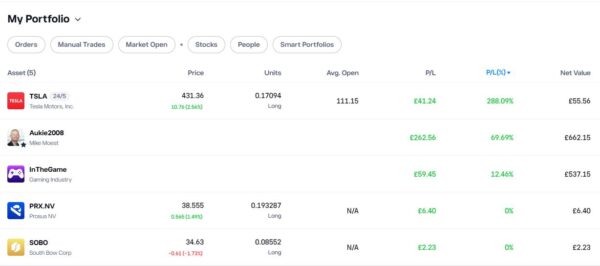

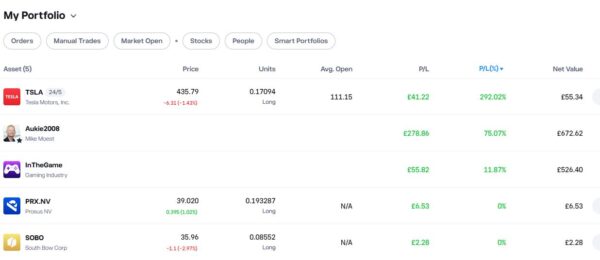

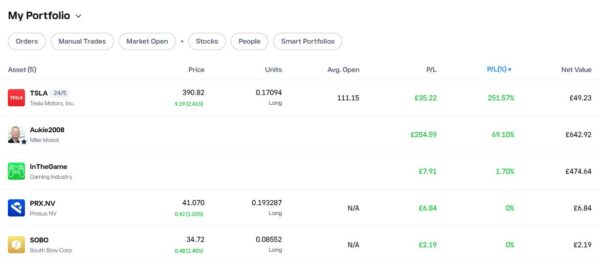

In 2022 I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios, Oil Worldwide. I also invested a small amount I had left over in Tesla shares.

In January this year, as Oil Worldwide hadn’t exactly been setting the world alight, I decided to switch my entire investment in this to another smart portfolio, InTheGame. This port, focusing on the computer gaming industry, had been the top performer for some time in my eToro virtual portfolio.

Unfortunately just as I switched away from Oil Worldwide, President Trump decided to invade Venezuela. This gave the oil industry a significant boost, which I would otherwise have benefited from. Meanwhile InTheGame went south, partly due to the war in the Middle East. At one point I was down by over 10% on this investment. Fortunately in the last three months InTheGame has made a good recovery and is now in profit by 12.45%.

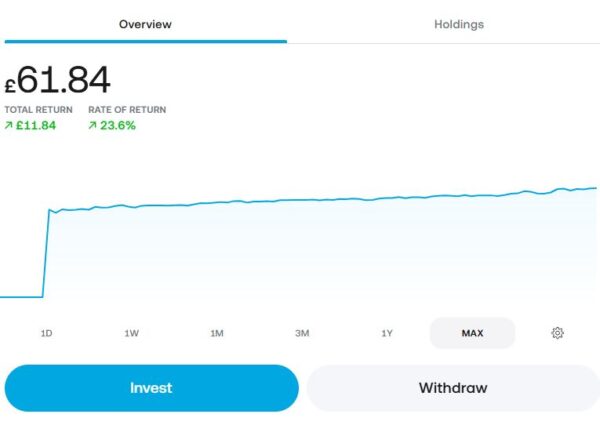

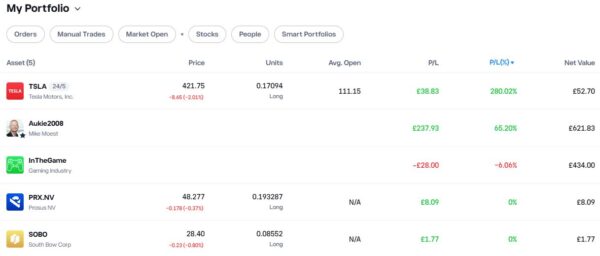

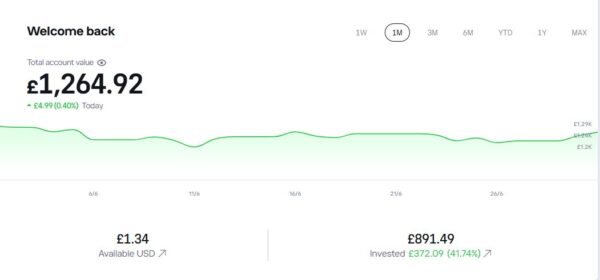

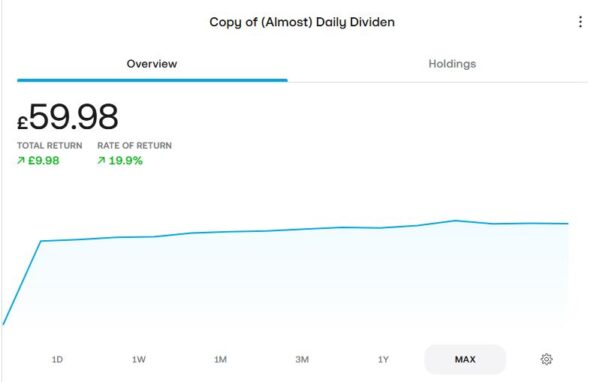

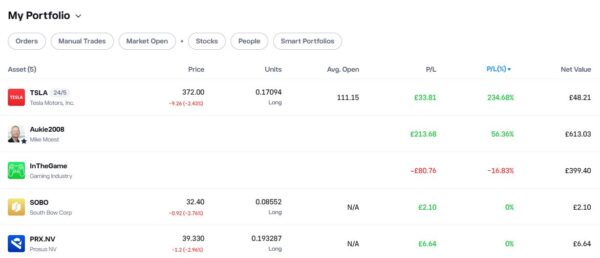

As you can see from the screen captures below, my original eToro investment (total value £888.36 in pounds sterling) is today worth £1,264.92, an overall increase of £376.56 or 42.39%.

- Note: eToro now displays the value of investments in your native currency, although you can change this if you wish.

You can read my full review of eToro here. You may also like to check out my more in-depth look at eToro copy trading. I also discussed thematic investing with eToro using Smart Portfolios in this post.

As mentioned above, my new investment in InTheGame is currently up by 12.45%. And my copy trading investment with Aukie2008 is showing an impressive overall profit of 69.49%. Of course, I have held this investment for quite a bit longer.

My Tesla shares, which I purchased as an afterthought with some spare cash I had in my account, are down marginally this month but still showing an overall profit of over 288% since I bought them. If only I had put a bit more money into this!

You might also notice that I have small holdings in Prosus NV, a Dutch internet group, and South Bow, a Canadian energy infrastructure company. To be honest I don’t understand how I acquired these, but I assume they are some sort of bonus I was awarded. In any event, I am happy to have them in my portfolio.

- If you would like more information about setting up an eToro account, please click on this no-obligation website link [affiliate]. Don’t forget that you also get a free $100,000 virtual portfolio, which you can use to experiment with trading and investing strategies. I have certainly earned a lot from mine.

Moving on, I published various posts on Pounds and Sense in June. I have listed below those that are still relevant.

In Get a Free Share Worth up to £100 With Trading 212, I revealed that this promotional offer had reopened. If you haven’t done it before, you can get a free share worth up to £100 just by signing up to this popular share trading platform. My own free share in AMD is now worth £361.04! This offer closes on 9th July 2026. Learn more and sign up via my blog post.

And in The Best Realistic Side Hustles for Over-50s, I set out some easy side hustles that can work well for people in their fifties, sixties and beyond. If you’re looking for some simple, flexible ways to supplement your pension, build up a holiday fund, help cover rising household bills, or just earn some extra spending money, you’ll find a range of realistic ideas here.

Finally, I should mention that EDF Energy have enhanced their switching offer. Until 13th July 2026 you can get a FREE £75 (increased from £50) credited to your energy account when you switch to EDF via my referral link. Terms and conditions apply.

I’ll close with my customary reminder that you can also follow Pounds and Sense on Facebook or Twitter (or X as it is now). Twitter/X is my number one social media platform and I post regularly there. I share the latest news and information on financial matters, and other things that interest, amuse or concern me. So if you aren’t following my PAS account on Twitter/X, you are definitely missing out!

- I am also on the BlueSky social media network under the username poundsandsense.bsky.social. Twitter/X remains my primary social media platform, but I also post details of my latest blog posts, third-party articles and other financial news and resources on BlueSky for those who prefer to follow me there.

As always, if you have any comments or questions, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts on PAS may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

The Advantages of Buying an Annuity

The Advantages of Buying an Annuity The Disadvantages

The Disadvantages