Today I’m sharing a sideline money-making opportunity that – if you’re in a position to do it – can bring in a steady income for very little effort.

The shortage of parking spaces in many towns and cities has created an opportunity for anyone who has a driveway (or garage) they aren’t using all the time.

One of the best-known operators in this field is JustPark. Through their website and mobile app, they put drivers in touch with home-owners and businesses who have parking spaces (and/or EV charging spaces) available near their destination. They say they help over 10 million drivers a year find parking spaces at over 45,000 UK locations.

Listing your space is free and you can set your own price based on how long the driver wishes to stay. JustPark will suggest an appropriate price based on your location and the facilities you are offering, but you aren’t obliged to accept this.

JustPark charges space-owners a 3% fee on one-off bookings (so if you charge £10 they will take 30p, meaning you receive £9.70). For longer term or rolling bookings over two months, they charge space-owners a higher fee of 20% for the first month, with the fee reverting to the standard 3% after that.

JustPark also make money from drivers, adding up to 25% of the space-owner’s asking price to the fee charged. They say, however, that charges to drivers are still typically 30% lower than ad hoc street parking (if you can find it), which makes the service attractive to motorists as well.

One big attraction of JustPark is that they handle all the admin on your behalf. All payments are made via the website, and space-owners can withdraw earnings via PayPal or direct to their bank account. JustPark also ensure you still get paid even if the booker doesn’t turn up.

JustPark say that the money you earn from renting out your parking space is included in the property trading income allowance introduced by the government in April 2017 – so you can make up to £1,000 per year completely tax-free (and no need to declare it to the taxman).

All drivers using the service have to register on the site, so you know exactly who will be using your space on any given day. There is also a rating system so you can see any comments other users of the service have made about them. Space-owners are also rated by drivers, incidentally.

You can offer spaces by the day, week or month, and set any restrictions you wish on when your space is available. Anyone is welcome to advertise spaces on JustPark, but the locations in most demand are those near airports, stations and stadiums, and in major cities. According to one recent article in the Daily Mail, people in such areas are making more than £4,000 a year doing this. Even if that doesn’t apply to you, though, you can still earn from a few hundred pounds a year to £1000 or more by this means.

Obviously the pandemic and working from home reduced demand for parking spaces. But with life returning to normal now, demand for parking spaces is steadily increasing again.

Of course, if you don’t have a suitable space to offer, you won’t be able to benefit from this opportunity. You could still use JustPark to save money on your own parking costs, though. Either way, the service is well worth checking out 🙂

Another option for cheaper parking is Your Parking Space. Over 60s can get an exclusive 10% discount on this service through my friends at Over 60s Discounts.

Disclosure: As well as being a registered user of JustParkI am an affiliate for them and will therefore receive a small commission if you click through any of my links and sign up. This will not affect the money you earn through the site and/or any savings you make if you use them to find parking spaces.

Cover image by courtesy of BingAI.

This is a fully revised and updated version of my original article on this subject.

If you enjoyed this post, please link to it on your own blog or social media:

A quickie today to remind you that you have just 10 days left to use or exchange any remaining non-barcoded stamps you may have. The stamps concerned are the plain ones with the late Queen’s head on (all stamps with the new King’s head are barcoded).

Christmas stamps and other ‘special’ stamps with pictures on will continue to be valid for the foreseeable future, but it would still be a good idea to use them up now (or give them to a collector in the family!).

If you can’t use the stamps before the end of July, you can exchange them free of charge using Royal Mail’s Swap Out scheme. You will need to complete a Stamp Swap Out form for stamps worth up to £200, or a Bulk Stamp Swap Out form for stamps worth more than £200. Forms are available from post offices, though note that you cannot exchange the stamps themselves there.

An image from the Royal Mail website showing which stamps can and can’t be swapped is shown below.

The deadline for using plain non-barcoded stamps is 31 July 2023. If you use them after that date, the recipient will have to pay a fee (to be announced) on delivery. That’s assuming they are delivered at all, of course.

As well as post offices, you can print Swap Out forms from the Royal Mail website, or phone their customer services on 03457 740740 to request one. There is currently no deadline for the Swap Out scheme and it will continue after 31 July 2023, though again it may be best to do this sooner rather than later.

Today I have a collaborative post for you in association with my friends at European crowdlending platform Mintos.

The article sets out some basic principles for anyone who may be considering investing for the first time.

Introduction

if you’re looking to build long-term wealth and create the financial means to achieve life-long goals, investing can be the key to doing this. To get you started, we’ve put together an overview of what investing is, what people invest in, how people invest, and what you might need to start your investment journey.

Key takeaways

Investing can be an effective way to build long-term wealth and unlock financial freedom.

When you invest, you can expect to earn a profit on the money you have invested, otherwise known as an investment return.

Investment returns compound (grow bigger and bigger) each time you reinvest them, helping you achieve financial goals faster.

Investments are referred to as assets; they are grouped into asset classes, e.g. cash, stocks, bonds, real estate, commodities, and alternatives.

Anyone can start investing, regardless of experience or financial situation. Even just a little money can go a long way.

What Is Investing?

Whether consciously or not, we invest our time and energy throughout our lives, whether it’s on getting a university degree or learning to cook a new recipe. Typically we do these things because we expect them to bring us value in future, e.g. landing our dream job after finishing university.

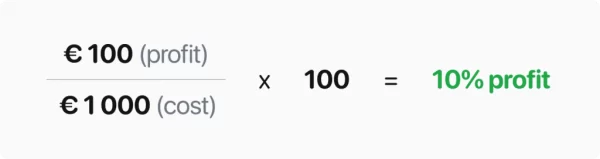

With investing money, the concept is similar – you put your money into something with the expectation that you’ll make a profit from this in the future.

The profit you earn from investments is commonly referred to as a return. This is often expressed as a percentage. For example, if you invest €1000 in something and at the end of the investment period, you get back €1100, then your profit would be €100, giving you a 10% return on your investment.

Why Do People Invest?

For many years people have used investing as a means to build their wealth. The reason long-term investing is so effective is because of compound growth. Investment returns compound (grow bigger and bigger) each time they are reinvested, helping you achieve your financial goals faster.

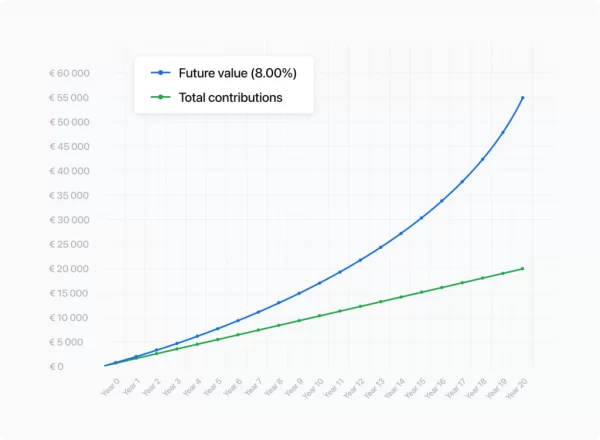

For example, if you invest €100 a month over the next 20 years at an 8% interest rate, each year your funds will grow at a faster pace (see chart below). The idea is that by the end of the investment period, you will have significantly more money than if you’d added the same amount to a savings account.

For many, investing provides the means to pay for education, home ownership, cars, travel, retirement, and so on. So people often look to investing because it can provide them with opportunities.

What Do People Usually Invest In?

When you own something of value that can be converted to money, it’s described as an asset. Assets can be liquid, meaning they can be quickly converted to money, or illiquid, where it’s more time-consuming and complex to turn them into money.

In the investment market, assets are categorized into asset classes. These are groups of assets with similar characteristics. Some examples of popular asset classes are:

Where to Start?

As you can see, there are many different ways of investing. How people choose often comes down to prior experience and financial objectives. Although the investment landscape may seem vast, there are options to suit everybody.

A great way to get started is to set investment goals. Once you have some clarity around your goals and budget, you can begin to research which assets or asset classes will suit your financial objectives and risk appetite.

Investment platforms that offer simple, automated investing strategies can be an easy place to begin. These strategies are built using expert analysis and data, reducing the need for prior expertise or in-depth research. An example here is Wealthyhood.

Investments in Exchange Traded Funds or ETFs (large investment portfolios investors can buy shares in) are also relatively straightforward. They’re managed by investment firms and require no work from an investor’s perspective. One example of a robo-adviser investment platform that uses ETFs is Nutmeg.

Or, if you’d like more control, you can research and make individual investment decisions yourself using brokers or self-investment platforms such as eToro.

Some investors only have one asset, such as a real estate (property) investment. Others own many different assets, forming what’s known as an investment portfolio.

When creating a portfolio, it’s important not to put all your eggs in one basket. It can be beneficial to invest smaller amounts across multiple assets, so your lower-risk investments balance the higher-risk ones – an investment strategy known as diversification. Doing this can increase the chances you’ll achieve the returns you expected while reducing the risk of significant losses.

Many investment platforms only require small amounts to get started. For example, on Mintos you can begin investing with just €50 (around £43). When you invest responsibly, even a little money can go a long way and bring you closer to achieving your financial goals.

As mentioned earlier, Mintos is a European crowdlending platform. Your money is invested in loans to businesses and private individuals arranged by MIntos’s partner lending companies from around the world.

As Mintos is a European operation, you will need to invest in euro and your returns will be paid in this currency. That obviously adds a layer of complication for UK residents, but there are various ways around this. If you have a UK bank account you will normally be able to make (and receive) payments in euro, but may be charged a transaction fee.

You could use your own bank to fund your account initially, but if you become a regular investor with Mintos you might want to use a service/account that charges lower fees. You could use a money transfer service such as Paysera or Wise (formally TransferWise). These will enable you to transfer funds between Mintos and your own bank account with (potentially) lower charges and a more favourable exchange rate.

Another option would be to open a euro account with a provider such as Starling. This will allow you to receive and make payments in both sterling and euro, again at a lower overall cost.

If you’d like to check out the options for inventors on Mintos – and learn more about how they operate and how risks are managed – please see this page of their website. Since 2015, investors with Mintos have earned a 9.54% net return per year on average. Of course, past performance is no guarantee of how any investment platform will do in future.

Special Bonus!

Until 30 August 2023, if you click through any link to Mintos in this article and invest €1000 or more, you will get a €50 instant bonus and a 1% bonus of your average investment in the first 90 days.

If you invest €5000, for example, in addition to the returns advertised, you will also receive a €50 instant bonus and a further 1% bonus of €50 after 90 days.

Thank you again to my friends at Mintos for their assistance with this article. If you have any comments or questions, as always, please do leave them below.

Disclosure: This is a collaborative post in association with Mintos. I am not a registered financial adviser and nothing in this article should be construed as personal financial advice. You should always do your own ‘due diligence’ before investing, and if in any doubt seek advice from a registered financial adviser before proceeding. All investing carries a risk of loss.

This post includes affiliate links. If you click through and make an investment (or perform some other designated action) I may receive a commission for introducing you. This will not affect the product or service you receive or any charges you may pay. Note also that the special bonus referred to in this article is only available if you click through one of my links and will not apply if you go to the Mintos website directly.

If you enjoyed this post, please link to it on your own blog or social media:

eToro is a Israeli fintech company based in Cyprus. The company also has registered offices in the UK, US and Australia. It is a hugely popular platform with 25 million customers from over 140 countries across the world.

eToro is regulated and authorised in the UK by the Financial Conduct Authority (FCA) and is covered by the Financial Services Compensation Scheme (FSCS). That means if eToro were to go bust any deposits with them up to £85,000 would be protected. Of course, the FSCS doesn’t protect you if you lose money simply due to your investments performing poorly.

eToro offers a wide range of investment products, from individual shares to cryptocurrencies, commodities to ETFs, currency pairs to copy trading, and thematic investing via smart portfolios. Today, though, I’m focusing on a feature that doesn’t require any outlay at all. This is the facility to operate a $100,000 virtual portfolio on the platform, to familiarise yourself with how it works and test out trading and investing strategies.

I have been an eToro investor for around a year now. I started with a virtual portfolio, but as regular readers will know I have also invested some real money. I do still use my virtual portfolio, however, and have learned a number of valuable lessons from it. So I thought today I’d set out some of these.

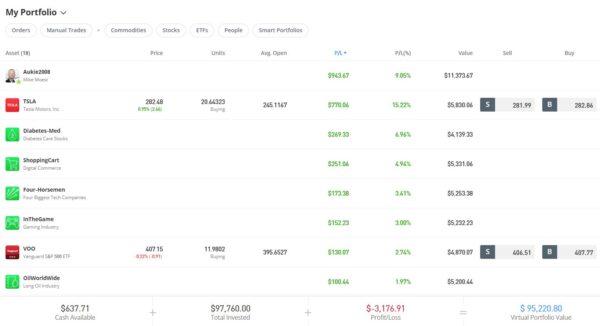

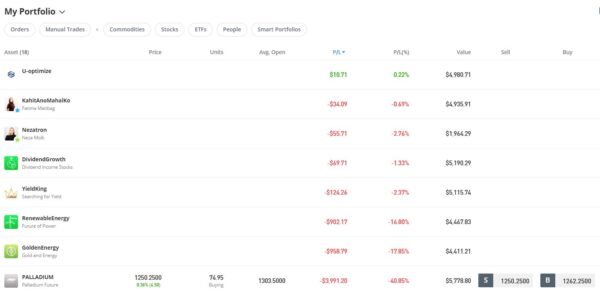

I’ll start by showing you some data on how my virtual portfolio has been performing. As I have quite a lot of different investments in this, I have taken two separate screen captures showing first the best performing and then the worst performing. As you will see, I am down a bit overall, but I’m not upset about that as obviously I have been experimenting to try to assess what works and what doesn’t.

Best Performing Investments

Worst Performing Investments

Some Lessons Learned

I hope you found the screen captures of my virtual portfolio interesting. They include most of my current investments apart from one or two in the middle. I can’t discuss every investment in detail here, but as promised here are some of the lessons that I have drawn from my experiences to date.

Copy trading can be profitable

As you can see, the best performing investment in my virtual portfolio is copy trading Aukie2008 (Mike Moest). This has generated a profit of almost $1000 for me. Regular readers will know that I also invested some real money following this trader and have done well from this too.

I am obviously a fan of the copy trading feature on eToro, though naturally some traders do better than others. When I was starting out I also considered investing some real money following a trader called Nezatron (of course, I wasn’t the least bit influenced by the fact that she is an attractive blonde…). But as you can see above, the results she has achieved over the last year aren’t nearly as impressive.

Another option for investors on eToro is commodities. These range from precious metals through to food products, including the famous (or infamous) pork bellies.

It’s important to understand that when trading in these markets, you are essentially betting on whether the price will go up or down in future. The mechanism for doing this is something called Contracts for Difference, or CFDs for.short.

CFDs are leveraged investment products. That means you can make a lot of money if they go the way you predict but also lose a lot if they go the opposite way.

In my virtual portfolio I have tried commodity trading three times. The first time was with Nickel and I made a big profit. The next was Gold, and I lost all the money I had made with Nickel and a bit besides. Finally, as you can see, I opened a ‘buy’ trade with the rare metal Palladium. This trade also went the wrong way, so I am currently sitting on a loss of almost $4000. Obviously I am glad that isn’t real money!

If you’re wondering why my Nickel and Gold trades aren’t showing in my screen captures, it’s because the stop-profit and stop-loss limits respectively were reached and the trades closed out. You are obliged to set stop profits and stop losses on the eToro platform, though you can of course adjust them subsequently if you wish..

To be fair to eToro, they have warnings across the site that trading with CFDs is extremely risky. But trying it myself (in virtual form) really has brought home to me the risk you are running, especially if you don’t fully understand what you’re doing. Indeed, if it wasn’t for my commodity-trading experiments, my virtual portfolio would be well in profit by now.

If, despite this, you still want to find out more about commodity trading using CFDs, the eToro website has a useful introductory guide here. As for me, I am not planning to try it again any time soon!

You can’t always trust ‘the wisdom of the crowd’

You might wonder how I chose which commodities to invest in. Well, eToro shows you what proportion of investors at any time are buying a particular commodity (i.e. forecasting its price will rise) and what proportion are selling (i.e. forecasting it will fall). Here is a screen capture illustrating this.

No doubt naïvely, I assumed that if a very high proportion of investors are ‘buying’ a particular commodity, doing likewise should be profitable. As mentioned, though, while that worked on the first occasion I tried it, it didn’t on the second or third. So while this information might be useful in some circumstances, my experiences indicate that it is definitely not to be relied upon.

Investing in renewables isn’t a one-way bet

You might also assume (as I did) that in the current (alleged) climate crisis and manic quest to achieve Net Zero, investing in renewables ought to be a profitable strategy.

To test this, I invested in two eToro smart portfolios in this sector. One is called Renewable Energy and the other Golden Energy. As you can see from my earlier screen capture, both have performed poorly and are at the bottom of my list (just above Palladium). I am currently down about $1000 on each.

In a somewhat ironic twist, my investment in a smart portfolio called Oil Worldwide is actually showing a small profit. Regular readers will be aware that I also have some real money in Oil Worldwide.

I don’t really know why companies in the renewable energy sector should be under-performing (on eToro at any rate). But again it does make the point that what may appear to be ‘nailed-on’ profitable investments can still end up losing money. There is never any guarantee!

As you can see, one of the best performing investments in my virtual portfolio was Diabetes-Med. This is a smart portfolio covering companies in the field of diabetes care, treatment and prevention. As someone who has previously been diagnosed prediabetic, I had a particular interest in this. And with diabetes on the rise across the world, it did seem to me it was a sector with good profit potential.

Another of my more profitable investments was Cancer-Med. Again I had personal reasons for wanting to invest in this, as my partner Jayne died from cancer and I have been treated for prostate cancer myself. Obviously a lot of research money goes into cancer, and successful treatments can prove extremely lucrative for the companies concerned.

AI, or artificial intelligence, is a major talking point at the moment. While some concerns have been expressed about its potential downsides, businesses are investing heavily in this field and the potential profits to be made appear huge. eToro doesn’t currently have an AI smart portfolio as such. You can, however, invest in four big tech companies (Microsoft, Amazon, Apple and Google) via the Four Horsemen smart portfolio. All four of these companies are currently pouring vast amounts of money into AI research.

My investment in Four Horsemen has generated a decent (virtual) profit for me so far and I don’t see that changing any time soon. I may well be investing some real money in this smart portfolio before long.

Obviously if you wish you can also invest in any of these companies individually via eToro. But the Four Horsemen smart portfolio provides a convenient method for investing in all four, with the portfolio regularly rebalanced to ensure that investors’ funds are divided proportionately among them.

Final Thoughts

So those are five lessons I have learned from my eToro virtual portfolio. I don’t claim any of them are particularly earth-shattering or that they represent deep universal truths. But I have found all of them valuable in different ways and they will certainly inform my investing in future.

If you are interested in investing and/or trading, I do therefore recommend setting up an eToro virtual portfolio and trying different strategies with it. I shall continue to do so myself, alongside my real investments in eToro and elsewhere.

As always, if you have any comments or questions about this article – or eToro more generally – please do post them below.

Disclaimer: I am not a professional financial adviser and nothing in this post should be construed as personal financial advice. You should always do your own ‘due diligence’ before investing, and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Please note also that posts on Pounds and Sense may include affiliate links. If you click through these and make a purchase or investment, I may receive a commission for introducing you. This will not affect in any way the price you pay or the product/service you receive. In some instances bonuses and other promotional incentives may only be available if you click through my link.

If you enjoyed this post, please link to it on your own blog or social media:

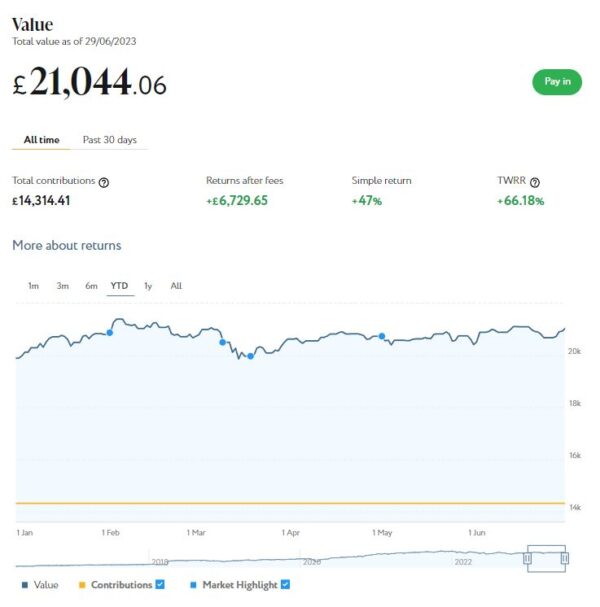

I’ll start as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

As the screenshot below for the year to date shows, my main Nutmeg portfolio is currently valued at £21,044. Last month it stood at £20,419 so that is a rise of £625.

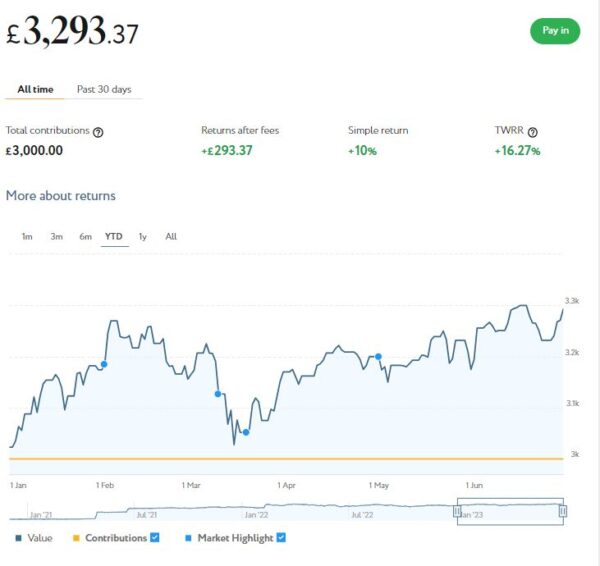

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £3,293 compared with £3,175 a month ago, an increase of £118. Here is a screen capture showing performance since the start of this year.

This has clearly been a better month for both my Nutmeg pots. Their total value has risen by £743 or 3.15% month on month. Since the start of 2023 the net value of my Nutmeg investments has grown by £1,417 or 6.18%.

Of course, all investing is (or should be) a long-term endeavour. Over a period of years stock market investments such as those used by Nutmeg typically produce better returns than cash accounts, often by substantial margins. But there are never any guarantees, and in in the short to medium term at least, losses are always possible.

Also, as you may know, both my Nutmeg pots have quite high risk levels (9/10 main, 5/5 Smart Alpha). If you haven’t yet seen it, you might like to check out my blog post in which I looked at the performance over time of Nutmeg fully managed portfolios at every risk level from 1 to 10 . I was pretty amazed by the difference risk level makes, with higher-risk ports over almost any period of three or more years in the last ten generating significantly better overall returns. If you are investing for the long term (and you almost certainly should be) choosing a hyper-cautious low-risk level might not therefore be the smartest strategy. The one exception is if you plan to withdraw your money soon and don’t want to risk losing too much if there is a sudden downturn.

You can read my full Nutmeg review here (including a special offer at the end for PAS readers). If you are looking for a home for your annual ISA allowance, based on my overall experience over the last seven years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs) and Junior ISAs as well.

Moving on, my Assetz Exchange investments continue to generate steady returns. Regular readers will know that this is a P2P property investment platform focusing on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my AE portfolio has generated a respectable £124.53 in revenue from rental income. As I said in last month’s update, capital growth has slowed, though, in line with UK property values generally.

At the time of writing, 12 of ‘my’ properties are showing gains, 2 are breaking even, and the remaining 12 are showing losses. My portfolio is currently showing a net decrease in value of £15.53, meaning that overall (rental income minus capital value decrease) I am up by £109. That’s still a decent return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Assetz Exchange most projects are socially beneficial as well.

Obviously the fall in capital value of my AE investments is slightly disappointing. But it’s important to bear in mind that unless and until I choose to sell the investments in question, it is largely theoretical. The rental income, on the other hand, is real money (which in my case I have chosen to reinvest in other AE projects to further diversify my portfolio).

I also spoke to the CEO of Assetz Exchange, Peter Read, recently. He made the point that capital values on the platform simply reflect the latest price at which shares in the property concerned have changed hands on their exchange. They do not represent objective or independent valuations of the properties. If you are investing long term with AE, the annual yield from rentals is really a much more important consideration.

Peter also made the point that the current high inflation rate has actually been beneficial for Assetz Exchange investors. That is because properties on the platform generally have an annual review when rentals are increased in line with inflation. That means from the end of the financial year in April, rentals have increased in most cases by around 10%. Assetz Exchange recently published a blog post about this which is worth a read.

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of AE as far as i am concerned. You can actually invest from as little as 80p per property if you really want to proceed cautiously.

Another property platform I have investments with is Kuflink. They continue to do well, with new projects launching every week. I currently have around £2,500 invested with them in 17 different projects. To date I have never lost any money with Kuflink, though some loan terms have been extended once or twice. On the plus side, when this happens additional interest is paid for the period in question.

My loans with Kuflink pay annual interest rates of 6 to 7.5 percent. These days I invest no more than £200 per loan (and often less). That is not because of any issues with Kuflink but more to do with losses of larger amounts on other P2P property platforms in the past. My days of putting four-figure sums into any single property investment are behind me now! Nowadays I mainly opt to reinvest the monthly repayments I receive from Kuflink, which has the effect of boosting the percentage rate of return on the projects in question

Obviously a possible drawback with Kuflink and similar platforms is that your money is tied up in bricks and mortar, so not as easily accessible as cash savings or even (to some extent) shares. They do, however, have a secondary market on which you can offer any loan part for sale (as long as the loan in question is performing and not in arrears). Clearly that does depend on someone else wanting to buy it, but my experience has been that any loan parts offered are typically snapped up very quickly. So if an urgent need arises, withdrawing your money (or part of it) is unlikely to be an issue.

You can read my full Kuflink review here. They offer a variety of investment options, including a tax-free IFISA paying up to 7% interest per year with built-in automatic diversification. Alternatively you can build your own IFISA, with most loans on the platform being IFISA-eligible.

Until 31 July 2023 Kuflink are offering enhanced promotional rates of up to 9.73% (gross annual interest equivalent rate) for their Auto-Invest products (IFISA-eligible). There is limited availability for this offer and it may be withdrawn any time before 31 July 2023 if the limit is reached. For more information, click here [affiliate link].

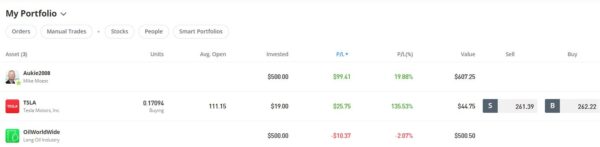

Last year I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios, Oil Worldwide. I also invested a small amount I had left over in Tesla shares.

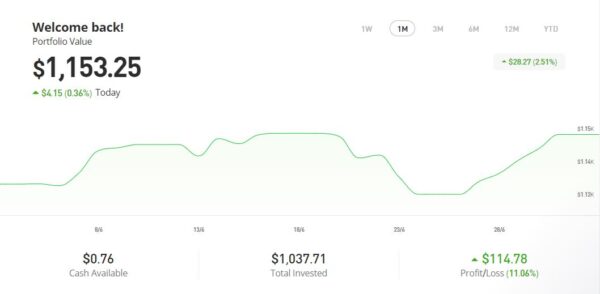

As you can see from the screen capture below, my original investment of $1,022.26 is today worth $1,153.25, an overall increase of $130.99 or 12.81%. in these turbulent times I am very happy with that.

Since last month the price of my Tesla shares has risen substantially and my copy trading portfolio with Aukie2008 has also done well (though less spectacularly). My most recent investment in Oil Worldwide has risen a bit this month but it’s still slightly down on when I invested. The Oil Worldwide portfolio has just been rebalanced by eToro, so I am hoping for better things in the months ahead

eToro also recently introduced the eToro Money app. This allows you to deposit money to your eToro account without paying any currency conversion fees, saving you up to £5 for every £1,000 you deposit. You can also use the app to withdraw funds from your eToro account instantly to your bank account. I tried this myself recently and was impressed with how quickly and seamlessly it worked. You can read my blog post about eToro Money here.

I had two more articles published in June on the excellent Mouthy Money website. The first was 10 Great Ways to Save Money on Amazon. Amazon is Britain’s – and the world’s – favourite online store. Prices on Amazon are generally competitive, but over the years I’ve discovered a variety of ways to ensure you get the best value for money from them. So in this article I set out my top ten tips for saving money on Amazon

My other article was Do You Need a Personal Financial Adviser? In this article I discuss the different types of financial adviser and what they do. I also revealed why – despite being a money blogger and considering myself reasonably financially savvy – I have a personal financial adviser myself.

As I’ve said before, Mouthy Money is a great resource for anyone interested in money-making and money-saving I always look forward to reading the articles by my fellow contributors. Shoestring Jane is a particular favourite and I enjoyed reading her recent article concerning how you can Save Money by Reducing Food Waste.

I also published several new posts on Pounds and Sense in June. One of these was My Short Break in Bath. Bath is, of course, a historic city on the River Avon, about 12 miles from Bristol. I went there for three days in June, the first time I had been for over 30 years. In my post I discuss the self-catering apartment where I stayed and reveal some of the things I did and saw. I also share a few top tips for visitors to Bath. The cover image shows the famous Pulteney Bridge, one of Bath’s best-known landmarks.

I also published a post based on a survey of Britons’ investing habits. This addressed questions such as what are the main barriers stopping people investing and where do people get their investment advice from. I thought the results were quite eye-opening. Take a look if you haven’t already.

Finally, I wanted to highlight that the free share offers described in last month’s update are both still open if you haven’t done them yet. The opportunity to Get a Free Share Worth up to £100 with Trading 212 was reopened after closing briefly. It is now on offer till 27 July 2023.

The opportunity to Get a Free ETF Share Worth up to £200 with Wealthyhood is also still open but the terms have changed slightly. To remind you, Wealthyhood is a DIY wealth-building app aimed especially at people who are new to stock market investing. As from 1 June 2023 they changed their fee structure to make it (even) more attractive to small investors. They have now increased the minimum investment to qualify for the free share offer from £20 to £50 – but on the plus side, they guarantee that your free ETF share will be worth at least £10.

That’s all for today. I hope you’re enjoying the summer months and taking the opportunity to get out and about in our beautiful country (or further afield).

As always, if you have any comments or queries, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media: