As you probably know, equity release is a method of unlocking funds tied up in your property. It is open to homeowners aged 55 and over (60 and over in the case of home reversion plans).

In recent years equity release has become increasingly popular, and even rising interest rates have done little to dampen this trend. So today I thought I would look at the main reasons people are opting for equity release. I am indebted to my colleagues from Equity Release Supermarket for providing information (based on their internal data) on the top reasons people are releasing equity, as well as which reasons are seeing the biggest increases.

The table below shows the top reasons people have been using equity release over the last six months.

Rank

Reason for equity release

1

Repay mortgage

2

Home improvements

3

Debt consolidation

4

Supplement income

5

New/second home purchase

As the table shows, repaying a mortgage is the number one reason over 55’s have released equity. The data shows that, on average, 21.1% of completed cases planned to pay off an existing mortgage with the money released.

Home improvements are the second most common reason, with an average of 17.9% of borrowers raising money for a renovation project.

Debt consolidation is the third most common reason for equity release, at a slightly lower average of 13.7%. Interestingly, when looking at the data by month, using equity release for debt consolidation peaked at 18% in December 2022.

The data also reveals which reasons for equity release have increased in popularity over the last six months, with home improvements seeing the biggest increase, growing by 7.7%.

Gifting money is becoming an increasingly popular reason to release equity too. In the last four months alone, gifting money that has been released through an equity release scheme has risen by 2%.

“Equity release is available for homeowners over the age of 55 who wish to free up some of the money, tax-free, that has been built up in the equity of their home. The interest rate is fixed for life and the plan is repaid when the homeowner dies or moves into long term care.

“It is perhaps unsurprising that repaying a mortgage is the top reason for equity release. As interest rates and living costs continue to rise, borrowers will be looking for ways to reduce their monthly payments. By using an equity release scheme, such as a lifetime mortgage, to pay off your existing interest only mortgage you will no longer need to make monthly payments unless desired. This can help make monthly savings and alleviate financial pressures, especially for those who have seen their mortgage payments rise in recent months due to interest rates.

“It is interesting to see that gifting money through equity release has risen over the last six months. Money gifted through equity release becomes exempt from inheritance tax, provided that the gift giver lives for seven years afterwards. Inheritance tax can significantly reduce the amount of wealth that you may be able to pass on, so we often find that many people turn to equity release as a strategy for reducing the impact it will have on an estate.

“In this uncertain economic climate, it is more important than ever that borrowers are getting advice on what product options are available across the whole equity release market. For anyone considering equity release, we would suggest discussing your plans with one of our equity release advisers.”

My Thoughts

If you’re looking for a way to release money from your property – whether to pay off debts/mortgages, fund specific purchases, assist children or other family members, or just make later life more comfortable – equity release is certainly something you may want to consider.

The main downside is – of course – that ultimately there will be less money to pass on to your beneficiaries. All reputable providers, however, offer a no-negative-equity guarantee. They may also be able to arrange plans where a certain amount of cash is guaranteed to remain in your estate, if you so wish.

Equity release interest rates in most cases are fixed for life, so you will know from the start the liability you are taking on. Of course, the longer you remain living in your home, the larger the debt eventually payable from your estate will be.

If you think equity release may be right for you, you will need to discuss this fully with an independent adviser before proceeding. As well as Equity Release Supermarket other well-known firms in this field include Key Equity Release and Age Partnership. The Equity Release Council has a full list of members on its website.

The adviser will discuss your needs and circumstances, and – assuming they think equity release is right for you – make a recommendation from the range of products on the market. You can, of course, speak to two or more different advisers if you wish before making any final decision.

Thank you again to my colleagues at Equity Release Supermarket for their assistance with this post. As always, if you have any comments or questions, please do leave them below as usual.

Today I’m featuring a way you can get a free ETF share worth up to £200 by signing up for a DIY wealth-building app for investors called Wealthyhood.

Wealthyhood offers a quick and easy method for even complete beginners to start investing in stocks and shares. And currently if you’re new to the platform you can get a free ETF share worth up to £200 just by signing up via any of the referral links in this post and investing at least £50. The ETF share you will get is chosen at random, but could be worth up to £200 (with a minimum value of £10). You can either keep this share or sell it (after 60 days).

For those who don’t know, ETF stands for Exchange Traded Fund. ETFs are a package of shares from a particular section of the stock market. For example, an ‘Asia Pacific ETF’ is a collection of shares from the Asia-Pacific region. ETFs are different to most investment funds in that they don’t usually have a manager running them. Instead, most ETFs are run by computers that regularly balance their portfolios automatically. This helps keep costs low, while still producing respectable returns in most cases. You can learn more about ETFs here if you wish.

How to Sign Up

Signing up with Wealthyhood is pretty straightforward. Just visit the Wealthyhood website via any of the (referral) links in this post and follow the on-screen instructions to register.

You will need to indicate the type (or types) of investment you are interested in. Four broad options are available: stocks, bonds, commodities and real estate. You can choose one or more of these (personally I chose stocks). You will also be invited to indicate whether you want your investments to be global or US only (I opted for global).

You can then choose the actual stocks you want or have this done automatically for you, and indicate the level of risk you are comfortable with. I chose ‘Optimized for Portfolio Weighting’ and then clicked on ‘Create my Portfolio’.

You will then be required to provide various items of personal information, including your address, date of birth, UK National Insurance number, and so on. Once you have entered all the required details, click on ‘Complete Verification’. After a few moments your account should be verified.

In some circumstances the process may take longer. If that happens, Wealthyhood will email you once you’ve been verified.

The next (and final) step will be to deposit a minimum of £100 into your Wealthyhood account and make a minimum £100 investment within seven days. You must do this within seven days of opening your account to qualify for the free ETF share. (If for some reason you’re not bothered about the free share, you can start investing with a minimum of £20.)

Within five days you should receive your free ETF share worth up to £200 (Wealthyhood say that 95% of users get their free ETF share within 1-2 days). You should receive notification about this in the My Account section of the Wealthyhood website when you log in.

You may wish to set a calendar reminder for 60 days, since (as mentioned above) you have to leave your free ETF share in your account for this long before you can sell it and withdraw the proceeds. You can, of course, leave it invested for longer if you wish, but bear in mind that fees may be applied (see below).

What Are The Fees?

Wealthyhood compares favourably with many other share-trading and investment platforms. Deposits and withdrawals are free, and other costs are kept to a minimum.

Until recently Wealthyhood charged all investors a platform fee of £1 a month. That wasn’t excessive (in my view) but for small investors (including those just wanting to take advantage of the free share offer) it was a bit of a deterrent.

As from 1st June 2023, however, the monthly platform charge was scrapped. Instead investors in Beginner accounts (everyone starts off with one of these) pay a small ‘custody fee’ of 0.18% per annum (or 0.015% per month). That works out as an annual custody fee of £1.80 for a £1,000 investment, or just 15p a month. In addition, they have introduced an acquisition charge of 0.45% per order (e.g. £4.50 for £1,000).

These new charges work out much cheaper for investors starting with small amounts and those just signing up for the free share. If you decide to stick with the platform, however, you might in due course want to consider upgrading to the new Wealthyhood Plus plan. This offers fully commission-free investing with no charges per order and no custody fees for £2.99 a month or £35.88 a year. This is obviously not worthwhile for very-small-scale investors, but once your portfolio gets up to around £6,000 (by my calculation) you should save money this way.

How Safe is Wealthyhood?

Wealthyhood is registered in England and Wales and authorized and regulated by the Financial Conduct Authority. In addition, all clients’ funds are kept separately in segregated bank accounts which are covered by the Financial Services Compensation Scheme. So even if the company itself were to go broke, any cash in your account would be protected up to a value of £85,000.

Of course, the FSCS guarantee doesn’t apply to the value of your stocks, which can go down as well as up. All investments carry a risk of loss, although in the case of your free ETF share you can never lose any more than the original cost, which was of course zero!

Referral Scheme

Any Wealthyhood member can also refer new members. All you have to do is send them your unique referral link which can be copied from your dashboard. If they join via your link and invest a minimum of £100 (as above), both you and they will then receive one free ETF share worth up to £200 (minimum £5). There is no limit to the number of friends you can refer by this means or the number of free ETF shares you can receive.

Don’t Miss Out!

I do just want to emphasize that in order to qualify for the free ETF share, you MUST click through a special referral link such as those in this article. If you simply go straight to the Wealthyhood website and join there, you won’t receive one.

What’s more, when I was researching this article I found that several other websites who were advertising this offer didn’t have the correct, up-to-date referral links. So even if you had clicked through them and signed up, you wouldn’t have qualified for a free share. To be safe, I strongly recommend clicking through my Wealthyhood referral link. You should then see a banner like this near the top of the page.

If you don’t see this banner, you haven’t clicked through a genuine, working referral link, and sadly will not receive a free ETF share.

Bear in mind also that this offer may be withdrawn any time. If and when I hear of that I will of course amend this post. But I do therefore strongly recommend taking advantage of this offer while you can.

Final Thoughts

Although in this post I have focused mainly on the free ETF share offer, Wealthyhood is also worth considering as an investment platform for the longer term.

Its low charges (especially from 1st June 2023) mean it is well suited for people who are dipping a toe into stock market investing for the first time. By contrast, the dealing fees and commissions charged by some other platforms can make small investments prohibitively expensive.

While you can’t invest in individual company shares through Wealthyhood, a wide range of ETFs is available via the platform. If you have a particular interest in an area such as video games, healthcare or clean energy (for example) you can invest in specific ETFs that track those sectors. This facility for thematic investing is not currently available through most other robo-adviser platforms, including Nutmeg.

I also like the simple, user-friendly Wealthyhood website. This allows you to easily build a balanced portfolio covering the investment types that interest you and reflecting the level of risk you are comfortable with. You can log in to your account at any time to see how your investments are performing and make any changes you wish to your portfolio, including investing more money or withdrawing.

In conclusion, I hope this post has inspired you to consider registering with Wealthyhood to claim your free ETF share. If you do, I hope you get a valuable one! Please let me know what share you receive in a comment below. And if you like Wealthyhood you may of course wish to consider investing long term via the platform as well.

As always, any comments or questions are very welcome.

Disclosure: Posts on Pounds and Sense may include my referral links. If you click on one of these and make a purchase or perform some other defined action on the website in question, I may receive a commission for introducing you. This will not affect the price you pay or the product or service you receive. Please note also that I am not a registered financial adviser and nothing in this post should be construed as individual financial advice. Everyone should do their own ‘due diligence’ before investing and seek advice from a professional financial adviser if in any doubt how best to proceed. All investment carries a risk of loss. Past performance is not a guarantee of future returns. Capital is at risk.

If you enjoyed this post, please link to it on your own blog or social media:

Regular readers of PAS will know I have a particular interest in P2P/crowdlending investment. Such platforms offer the opportunity to invest in loans to businesses or individuals and profit from the interest charged to borrowers.

With savings account interest rates still quite low, many investors are looking for better returns on their savings and investments. If that applies to you, European crowdlending platform Nibble is worth a look.

What is Nibble?

Nibble is a crowdlending platform launched in 2020 by IT Smart Finance, a company with over five years’ experience developing innovative products in financial technology. They offer a range of investment products which you can read about on the Nibble website. Today I am focusing on their latest offering, called the Legal Strategy.

What is the Legal Strategy?

The Legal Strategy offers the highest potential return of all the investment options on Nibble. The loans in question are in default and facing legal action (hence the name, of course).

For investment portfolios offered through the Nibble Legal Strategy, collection and litigation management are performed by Boostr. This is a company that buys overdue loans from banks and MFOs (Multiple Facility Organizations) at auctions at a typical discount of 85%, and automates the process of extra-judicial and legal recovery.

Nibble say that thanks to the deep experience and technologies developed by Boostr, it is possible to achieve a high percentage of capital return. The company draws on more than five years of successful experience in the area of debt recovery.

The Legal Strategy terms for investors, copied from the Nibble website, are shown below.

As you can see, the Legal Strategy comes with a deposit back guarantee. This is a guarantee to return the full investment amount at the end of the investment period and a minimum yield of 8% per year. The actual yield paid will depend on how successful recovery efforts prove, so you may end up with an annual return of anywhere between 8% and 14.5%. As you will probably know, this is above the average in the collective financing industry.

The minimum investment in Nibble’s Legal Strategy is €10 (about £8.70 at current exchange rates) and the maximum is €10,000. The platform has an auto-investment tool, allowing trading to be fast and straightforward. You aren’t required to choose individual loan portions, as this is all handled by the company. You simply choose your investment strategy based on the timescale over which you wish to invest and the level of risk you are comfortable with.

What Are the Risks?

No investment is without risk, but Nibble have gone to some lengths to keep this as low as possible. You can read a detailed article on this page of the Nibble website (warning: it is quite long!).

For investors in the new Legal Strategy, your money is invested in a portfolio comprising a large number of loans. The risk is therefore controlled and managed, as if any loans prove irrecoverable they will normally be offset by others that are successfully recovered (with interest and penalties).

As stated above, the risk is shared between the investor and the platform in the form of a variable interest rate. The rate paid is calculated automatically by Nibble every 90 days based on how the loan portfolio in question is performing. So every 90 days investors receive interest of between 8% (the guaranteed minimum) and 14.5% (the maximum). The actual rates paid can therefore vary from one quarter to another. Nibble say that average payouts currently are around 12.5% (this corresponds with my own experiences to date as a Legal Strategy investor).

If, for example, you invested €1000 in the Legal Strategy over 12 months, you could expect to receive anywhere between €80 and €145 in interest over the 12 month period, along with the return of your initial capital.

This is a fixed term investment, so it may be best to avoid if you think you might need the money back urgently before the end date. However, Nibble do say that if you change your mind, you can withdraw money from your portfolio ahead of schedule. They say they will find a new investor for your portfolio for a small commission fee.

The other risk, obviously, is that the platform itself will go bust. For various reasons set out on the Nibble website this appears unlikely, but of course it’s not impossible. If that were to happen, you would not be covered by the Financial Services Compensation Scheme (FSCS) which covers deposits in registered UK savings institutions up to £85,000. Nibble say that in the worst case scenario ‘a management company will be assigned to help the investor to recover funds in accordance with the rights of claim against the borrower. In addition, there is always a reserve fund which serves as an additional “safety airbag” for the investor.’

Finally, as loans are currently all in euro, UK investors will of course have to contend with exchange rate fluctuations. These could work for you or against you.

How Do You Get Started?

If you wish to invest via Nibble, the first thing you will need to do is set up an account via the Nibble website.

As Nibble is a European operation, you will need to invest in euro and your returns will be paid in this currency. That obviously adds a layer of complication for UK residents, but there are various ways around this. If you have a UK bank account you will normally be able to make (and receive) payments in euro, but may be charged a NSTF (Non-Sterling Transaction Fee).

You could use your own bank to fund your account initially, but if you become a regular investor with Nibble you might want to use a service/account that charges lower fees. You could use a money transfer service such as Paysera or Wise (formally TransferWise). These will enable you to transfer funds between Nibble and your own bank account with (potentially) lower charges and a more favourable exchange rate.

Another option would be to open a euro account with a provider such as Starling. This will allow you to receive and make payments in both sterling and euro, again at a lower overall cost.

My Experience

I wanted to try out Nibble myself,so I set up an account with them a while ago. The process was quick and straightforward. You just click on Create Account at the top of the Nibble homepage and follow the online instructions.

You are required to complete a short verification process before opening your account. This involves taking a photo of your passport, driving licence or some other form of ID, along with a selfie. You may use your mobile phone camera for this. It all worked smoothly and seamlessly in my case, and within a couple of minutes my application had been verified and approved.

After that, it is just a matter of making your initial deposit and deciding which of the strategies you want to use. Initially I chose their Classic Strategy as a low-risk test and everything went as promised. More recently I invested €100 in the Legal Strategy. This has also been running smoothly, with interest payments credited quarterly as promised.

Closing Thoughts

If you are looking for a more exciting home for some of your cash that allows you to take advantage of the higher interest rates on offer in continental Europe, Nibble is worth checking out.

The new Legal Strategy offers the highest rate of return of all their strategies. Of course, with higher returns typically come higher risks, and you do need to be comfortable with this. It is also important to note that with the Legal Strategy rates paid may vary over the period of your investment (though with an 8% guaranteed minimum).

The website’s ease of use is another attraction, as is the fact that Nibble doesn’t impose any fees or charges on investors. You do just need to bear in mind the need to switch between pounds and euro and the importance of minimizing the costs associated with this.

As a company based in Spain, NIbble doesn’t have too many UK reviews, but those that I have seen are generally positive. On the popular independent Trustpilot website, they have 11 reviews in total, six with 5 stars (‘Great’) and three with 4 stars (‘Very Good’). There are two 1-star reviews which reduce their average somewhat. These relate to difficulties withdrawing money. Nibble have replied to both and it appears that the problems arose due to the way the banks operate rather than being any fault of Nibble themselves. It also appears that the issues were satisfactorily resolved.

Obviously, nobody should put all their money into Nibble’s Legal Strategy, but it is worth considering within a diversified savings and investments portfolio. You should also bear in mind that your money won’t be protected by the Financial Services Compensation Scheme (FSCS), which protects deposits of up to £85,000 in most UK bank accounts. Of course, P2P/crowdlending platforms in the UK are not generally covered by the FSCS either.

I will continue to report on Pounds and Sense about how my Nibble investments fare.

New! Cashback Bonus. Until 31 July 2023 Nibble are offering a 2% cashback bonus for all new investments in their Legal Strategy. Visit their website for more info.

As always, if you have any comments or questions about this post, please do leave them below.

Disclaimer: I am not a qualified independent financial adviser and nothing in this post should be construed as personal financial advice. You should always do your own ‘due diligence’ before investing and seek professional advice if unsure how best to proceed. All investing carries a risk of loss. Note also that this review includes my affiliate (referral) links, so if you click through and end up investing with Nibble, I may receive a commission for introducing you. This will not affect the price you pay or the product/service you receive.

This is a sponsored post.

If you enjoyed this post, please link to it on your own blog or social media:

I recently returned from a three-day break in Aberdovey (Aberdyfi in Welsh). This is a small town on the mid-Wales coast. It was the first time I’d been to Aberdovey, though I’d heard good reports about it from friends.

I stayed in a two-bedroom apartment with a wonderful view across the estuary. I booked through Airbnb. I’ll say a bit more about the apartment below.

I should mention that although I travelled (and stayed) on my own, I met up with an old friend from Birmingham there. David recently lost his wife, for whom he had been caring for several years, so I thought he might appreciate a bit of company on his first solo trip away (I enjoyed his company as well, of course). David stayed at a pub/hotel called the Penhelig Arms. He liked it there, though car parking could be a bit of an issue. It appears their car park has been turned into a beer garden!

Aberdovey is about five miles south of Tywyn and 10 miles north of the university town of Aberystwyth. Here is a map of the area from Google Maps…

Accommodation

As mentioned, I stayed at an Airbnb property in Aberdovey. Under Airbnb’s rules I’m not supposed to reveal exactly where it was, but the location was certainly convenient. It was opposite the main car park, beyond which was the sea. The beach was around two minutes’ walk away, and all the restaurants, cafes and shops were within easy walking distance (not that there are very many – Aberdovey is only a small place).

You can read more about where I stayed on this page of the Airbnb website (you can also read my post about booking a holiday with Airbnb here). The apartment had a good-sized master bedroom with a comfortable double bed, and a smaller second bedroom with twin bunk beds. The latter would have been okay for children but adults might find it a bit of a squeeze.

The apartment had a decent-sized bathroom with (unusually these days in my experience) a bath with a shower over it. The shower worked well and there was plenty of hot water. I did try having a bath on my last night and found the taps very stiff, though. Possibly they don’t get used very much! I reported this to the host as I thought she would want to know, but it was no big deal, obviously.

The living room had a stunning view across the estuary (see photo below). It was quite spacious and had a good quality flat-screen TV (though no DVD player). The kitchen area just off the living room had all the facilities you would need/expect, including a toaster, fridge, sink, cooker, dishwasher, and so forth.

The apartment had gas central heating. As it was April I definitely appreciated this in the evenings and early mornings. There was a main thermostat in the living room and all the radiators also had thermostatic valves.

The apartment had free wifi which worked perfectly during my stay (not always the case in my experience). Although central, the location was quiet and peaceful, and I slept very well.

Finally I should say that communication from my Airbnb host (Irene) was excellent. She sent me very detailed instructions about how to get there, where to park, local amenities, and so on. One big plus was that residents in the apartment can use a council parking permit which allows them to park in the car park opposite (and various other places in Abverdovey) free of charge at any time. I left my car in the car park opposite, which was perfect for me.

Financials

As Pounds and Sense is primarily a money blog, I should say a few words about this.

I paid a total of £480 for my three-night stay. This was made up as follows:

£150 x 3 nights = £450

Cleaning fee £30

I was charged an initial deposit of £225, with the balance of £255 taken from my card a fortnight before my visit. The total price worked out to £160 a day. Obviously that’s not cheap but I thought it was reasonable bearing in mind the high standard of the accommodation and the convenience of the location.

Things to Do

As mentioned earlier, on this break I met up with an old friend, David. We spent some of the time together and some separately, which worked out well.

On our first full day we went on the Talyllyn Railway together (see photo below). This is a heritage steam railway that runs inland from the town of Tywyn, a short drive up the coast road from Aberdovey. I last went on the Talyllyn Railway five years ago (as described in this blog post) and was very happy to do so again.

We bought all-day tickets for £25 each and went all the way up the line and back in the morning. We then had lunch (tomato soup and a bread roll, both very good) at the station cafe in Tywyn. After that we travelled part of the way down the line to Dolgoch. Here we disembarked and spent an hour exploring the picturesque woodland with its many streams and waterfalls (see photo below). We then caught the last train back to Tywyn.

On our second full day we did our own thing. I stayed in Aberdovey, had a good wander round and got to know the place a bit better. I particular recommend the Medina Coffee House (picture below), where I went for both morning coffee and afternoon tea. You can sit inside or out here and enjoy a range of drinks, meals and snacks.

David went to Machynlleth, about 15 minutes drive away. Among other things, he visited the Centre for Alternative Technology (CAT). As a retired builder he was very interested to see some of the innovative building techniques being demonstrated here and said he would like to have stayed longer.

I met up with David each evening for a main meal. On two nights we went to the Penhelig Arms where he was staying. They serve traditional pub food, but none the worse for that. Their prices were very reasonable, and David got a 20 percent discount as a hotel resident, which was a nice touch (they also extended the discount to my meals, which was kind of them).

On the other evening we bought fish, chips and mushy peas from Aberdovey’s only chip ship (photo below). This was a stone’s throw from my apartment. We took it back to the apartment and sat watching the sun set over the sea while enjoying our meals. The food, the view and the company were all excellent!

Final Thoughts

As you may gather, I enjoyed my short break in Aberdovey, and am happy to recommend both the town and the accommodation where I stayed for a short break.

Aberdovey is a lovely place to relax and chill out. With its beautiful beach it could also be a good destination for families with young children. Older children and teenagers might find the lack of other entertainments a bit limiting, however. Although it’s not my thing, there are various water sports you can do there, including sailing, canoeing, sailboarding and paddle-boarding. There are also some lovely walks (and cycle rides) from the town.

In addition, the proximity of the Talyllyn Railway, Machynlleth and Aberystwyth offers good opportunities for days out. Aberdovey definitely isn’t a place you would go for the nightlife, though – even the fish-and-chip shop closes at 8 pm!

As always, if you have any comments or questions about this post, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

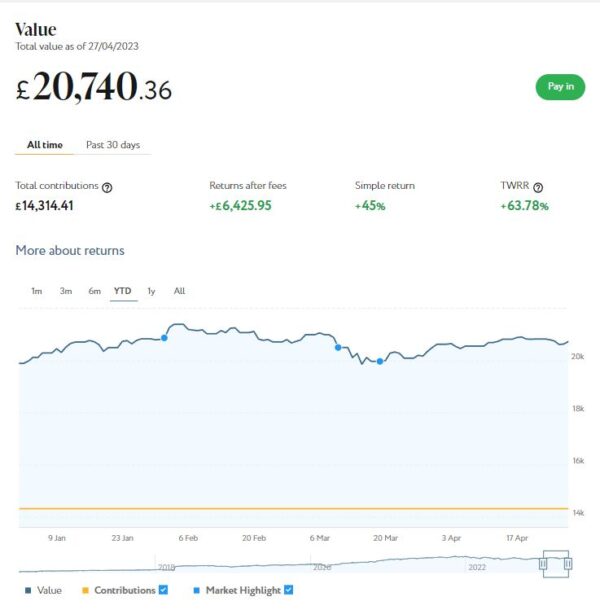

I’ll start as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

As the screenshot below for the year to date shows, my main Nutmeg portfolio is currently valued at £20,740. Last month it stood at £20,632 so that is a modest (but welcome) rise of £108.

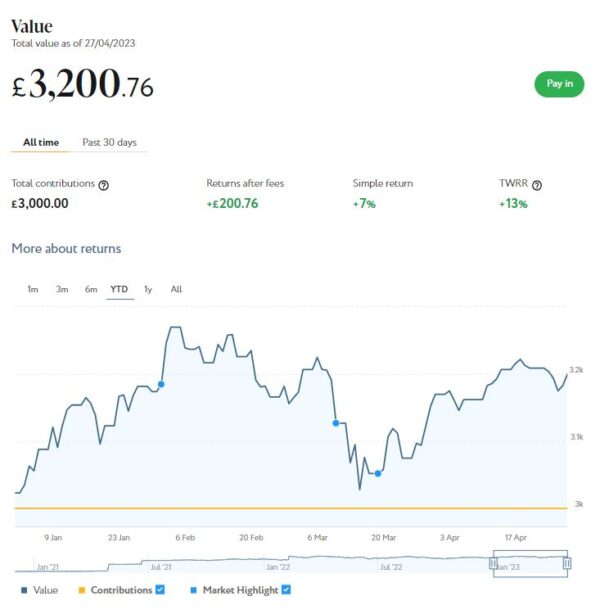

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £3,201 (rounded up to the nearest pound) compared with £3,170 a month ago, a small increase of £31. Here is a screen capture showing performance since the start of this year.

As you can see, this has been another up-and-down month for both my Nutmeg pots. Overall, though, the value of my investments rose by £139 or 0.58% month on month.

Of course, all investing is (or should be) a long-term endeavour. Over a period of years stock market investments such as those used by Nutmeg typically produce better returns than cash accounts, often by substantial margins. But there are never any guarantees, and in in the short to medium term at least, losses are always possible.

Also, as you may know, both my Nutmeg pots have quite high risk levels (9/10 main, 5/5 Smart Alpha). If you haven’t yet seen it, you might like to check out my blog post in which I looked at the performance over time of Nutmeg fully managed portfolios at every risk level from 1 to 10 . I was pretty amazed by the difference risk level makes, with higher-risk ports over almost any period of three or more years in the last ten generating significantly better overall returns. If you are investing for the long term (and you almost certainly should be) choosing a hyper-cautious low-risk level might not therefore be the smartest strategy. The one exception is if you plan to withdraw your money soon and don’t want to risk losing too much if there is a sudden downturn.

You can read my full Nutmeg review here (including a special offer at the end for PAS readers). If you are looking for a home for your annual ISA allowance, based on my overall experience over the last seven years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs) and Junior ISAs as well.

Moving on, my Assetz Exchange investments continue to generate steady returns. Regular readers will know that this is a P2P property investment platform focusing on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my AE portfolio has generated a respectable £110.99 in revenue from rental income. As I said in last month’s update, capital growth has slowed, though, in line with UK property values generally.

At the time of writing, 8 of ‘my’ properties are showing gains, 3 are breaking even, and the remaining 15 are showing (small) losses. My portfolio is currently showing a net decrease in value of £23.65, meaning that overall (rental income minus capital value decrease) I am up by £87.34. That’s still a reasonable rate of return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Assetz Exchange most projects are socially beneficial as well.

Obviously the fall in capital value of my AE investments is a bit disappointing. But it’s important to bear in mind that unless and until I choose to sell the investments in question, it is largely theoretical. The rental income, on the other hand, is real money (which in my case I have chosen to reinvest in other AE projects to further diversify my portfolio).

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of AE as far as i am concerned. You can actually invest from as little as 80p per property if you really want to proceed cautiously.

Another property platform I have investments with is Kuflink. They continue to do well, with new projects launching almost every day. I currently have around £2,500 invested with them in 18 different projects. To date I have never lost any money with Kuflink, though some loan terms have been extended once or twice. On the plus side, when this happens additional interest is paid for the period in question.

My loans with Kuflink pay annual interest rates of 6 to 7.5 percent. These days I invest no more than £200 per loan (and often less). That is not because of any issues with Kuflink but more to do with losses of larger amounts on other P2P property platforms in the past. My days of putting four-figure sums into any single property investment are behind me now! Nowadays I mainly opt to reinvest the monthly repayments I receive from Kuflink, which has the effect of boosting the percentage rate of return on the projects in question

Obviously a possible drawback with Kuflink and similar platforms is that your money is tied up in bricks and mortar, so not as easily accessible as cash savings or even (to some extent) shares. They do, however, have a secondary market on which you can offer any loan part for sale (as long as the loan in question is performing and not in arrears). Clearly that does depend on someone else wanting to buy it, but my experience has been that any loan parts offered are typically snapped up very quickly. So if an urgent need arises, withdrawing your money (or part of it) is unlikely to be an issue.

You can read my full Kuflink review here. They offer a variety of investment options, including a tax-free IFISA paying up to 7% interest per year with built-in automatic diversification. Alternatively you can build your own IFISA, with most loans on the platform being IFISA-eligible.

Until 31 May 2023 Kuflink are offering enhanced promotional rates of up to 9.73% (gross annual interest equivalent rate) for their Auto-Invest products (IFISA-eligible). There is limited availability for this offer and it may be withdrawn any time before 31 May 2023 if the limit is reached. For more information, click here [affiliate link].

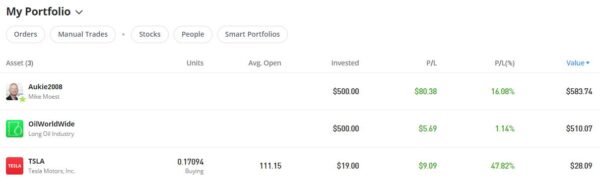

Last year I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios. I also invested a small amount I had left over in Tesla shares. My original investment of $1,022.26 is today worth $1,121.90, an increase of $99.64 or 9.75%. in these turbulent times I am quite happy with that.

Since last month the price of my Tesla shares has fallen somewhat (though still well in profit). My copy trading portfolio with Aukie2008 continues to perform steadily. And my most recent investment in Oil Worldwide is back into profit again, though – as you can see – not spectacularly so.

eToro also recently introduced the eToro Money app. This allows you to deposit money to your eToro account without paying any currency conversion fees, saving you up to £5 for every £1,000 you deposit. You can also use the app to withdraw funds from your eToro account instantly to your bank account. I tried this myself recently and was impressed with how quickly and seamlessly it worked. You can read my blog post about eToro Money here.

I had another article published in April on the excellent Mouthy Money website. This was Could You Save Money by Switching to an Electric Vehicle? I found this a very interesting article to research and write, even though there turned out to be no clear answer to the question posed in the title!

As I’ve said before, Mouthy Money is an excellent resource for anyone interested in money-making and money-saving. I always look forward to reading the articles by my fellow contributors. Shoestring Jane is a particular favourite of mine and I enjoyed reading her latest article How to Save Money in the Garden.

I was pleased to be able to publish a couple of interesting guest posts on Pounds and Sense in April. One of these was Investing in Classic Cars from my friends at the popular Car & Classic marketplace.

This is a subject I previously knew very little about and I found it quite an eye-opener. It was interesting (and slightly depressing!) to learn that some of the cars I drove as a young person are now regarded as ‘modern classics’ and fetching premium prices.

There can also be tax advantages to investing in classic cars, as they are generally not liable for capital gains tax (as discussed in this recent blog post).

The other guest post I published in April was Inflation – What Does It Mean for Your Savings or Loans? This one came from my colleagues at Money Marvel. Again it’s thought-provoking stuff, especially the fact that in some cases higher rates of inflation can actually be beneficial for consumers. Have a read and see what you think.

Pension credit is a seriously under-claimed benefit. Apart from the (admittedly modest) financial boost, it can act as a passport to a range of other benefits and discounts, including the government’s latest tranche of cost-of-living payments. So if you’re of pensionable age yourself, or have friends/relatives who are, I highly recommend looking into this. You can now apply for it online, which does make the whole process a bit quicker and simpler.

Finally in April I enjoyed a short break in Aberdovey, a charming coastal town in mid-Wales (see photo in cover image). I will be publishing a post on Pounds and Sense about my visit soon. What I will say here is that it’s a great place for a chilled-out seaside break, but you definitely wouldn’t go there for the nightlife 😀

That’s all for today. I hope you enjoy the holiday weekends in May, and in particular the festivities around the coronation. I am by no means an avid royalist, but we all need a bit of fun in these challenging times. So I’m looking forward to watching it on TV and going to a street party with my neighbours afterwards. The bunting will be going up soon!

As always, if you have any comments or queries, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!