As a bit of fun today, I am running a giveaway for some delicious Bahlsen biscuits. This is (of course) a sponsored post.

Everybody knows the festive season is the season of indulgence when every home and office is well-stocked with tasty treats and guilt-free pleasures. It’s a chance to treat those you love to something they’ll really enjoy and can nibble on all season long.

The brand new Bahlsen Choco Moments are the ultimate treats for Christmas, the perfect way to spread joy to friends and family during the festive season.

Choco Moments from Bahlsen – the experts in chocolate biscuits – are the perfect accompaniment to festive gatherings and cosy nights in. With a thick, luxurious coating of rich chocolate with crisp, satisfying crunch, drenched over buttery biscuit, they are the perfect melt-in-your-mouth treat, and come in two delicious flavours that will fight for space in your biscuit tin.

Choco Moments Crunchy Hazelnut combines smooth, creamy milk chocolate with warm hazelnut tones that are mouth-wateringly moreish, while Choco Moments Crunchy Mint perfectly balances the deep notes of dark chocolate with lively and refreshing mint.

So prepare to spread the Christmas joy and treat your loved ones to a seriously Choco Moment – the perfect moment to unwrap this festive season.

*** To be in with a chance of winning a pack of Choco Moments Crunchy Hazelnut or Crunchy Mint – your choice! – just leave a comment below by midnight on Tuesday 4 December 2018 saying why you love Bahlsen biscuits. I will pick a winner at random on Wednesday 5 December and arrange to send them the biscuits. Even if you don’t win, you can of course pick up Bahlsen Choco Moments biscuits from all good supermarkets and grocery shops and online stores including Amazon. The winner will be revealed here and via the Pounds & Sense Twitter and Facebook pages by Thursday 6 December 2018. UK residents only, I’m afraid. ***

Good luck, and let the season of indulgence begin!

Disclosure: as stated above, this is a sponsored post. I am receiving some delicious Bahlsen Choco Moments biscuits as a thank-you for posting it 😀

Blogging Secrets is an online course for anyone who would like to earn money as a blogger.

It has been created by UK blogger Jenny Lord, who runs a blog called Midwife and Life. The course is hosted on the Teachable platform.

Jenny was kind enough to allow me reviewer access to Blogging Secrets, so here’s what I found…

Blogging Secrets is a multimedia course organized in 12 main sections, as follows:

Welcome and Introduction

My Blogging Story

Before You Start

Setting Up Your Website with WordPress (.org)

The Business and Legal Side of Blogging

Blog Writing Secrets

Social Media Secrets

Where to Find Paid Blogging and Writing Work

Affiliate Marketing Secrets

Hosting and Running Giveaways

Scaling Up Your Blog Business

Bonus Section

Each section is further divided into anywhere from one to seven parts. Each part contains instructional text and/or a video lecture from Jenny.

As an example, the section titled Affiliate Marketing Secrets is in three parts: Affiliate Marketing and Affiliate Networks to Join, which are in written form, and a 16-minute video lecture titled The Secret of Making Affiliate Links Work for You in Your Sleep. I thought all the course content was very well written and presented. There is also a downloadable workbook to print out and fill in.

As you will gather, Blogging Secrets takes you through every aspect of setting up and running a money-making blog. Jenny recommends creating a self-hosted blog using the popular WordPress platform, which I would agree with (my blogs Pounds and Sense and Entrepreneur Writer are both hosted this way).

Be aware that the course doesn’t go into great detail about WordPress itself, though. The section about this includes a recommended list of WordPress plug-ins, but if you are brand new to WordPress you may need to do some additional studying on the technical aspects yourself (see below).

Where the course is particularly strong is about marketing and monetizing your blog. Although I am an experienced blogger myself, I still picked up some valuable tips and discovered a range of free and low-cost resources I hadn’t come across before. I found the sections about affiliate marketing and hosting and running giveaways especially eye-opening. Expect to see more of these on Pounds and Sense soon!

There is also a bonus section containing a variety of useful resources. I have listed these below, although as the course is constantly being revised and updated new ones may well have been added by the time you read this.

Pinterest Magic Ebook

Editorial Calendar

Email Template Swipe File

Blog Checklist

Weekly Blogging Sample Schedule

Pinterest Group Board List

Facebook Mastermind Group

There are some great resources here. I especially liked the Pinterest Magic ebook, which you can download and print out if you like. This explains how you can use this popular social bookmarking service to boost traffic to your blog. I have never entirely got my head around Pinterest , so I found this particularly helpful. Blogging Secrets costs £118.80 at the time of writing. Obviously that’s not cheap, but if it helps you set up a profitable blog that generates a growing monthly income, then it will clearly be money well spent. There is lots of great content on the business and creative aspects of running your blog. Personally I would like to have seen a little more on the technical side, but of course there is plenty of advice about this on the internet. I also recommend this regularly updated ebook by Dr Andy Williams about setting up a WordPress site, which I found very helpful personally when starting out.

As always, if you have any comments or questions about Blogging Secrets, please do post them below.

Disclosure: This post includes affiliate links. If you click through and make a purchase, I may receive a commission for introducing you. This will not affect the terms you are offered or the price you are charged.

If you enjoyed this post, please link to it on your own blog or social media:

Recently I’ve received a number of promotional emails about the Windfall Bonds on offer from the Family Building Society. The emails state, “Our Windfall Bond is a Better Bet Than Premium Bonds”. So I thought I’d take a closer look to see if this claim stacks up.

The unusual feature of the FBS Windfall Bonds is that every month you can win a cash prize, just like Premium Bonds. Unlike Premium Bonds, though, interest is also paid whether you win a prize or not. Interest rates are variable and tied to the Bank of England base rate. Currently they are paying an annual rate of 0.75%.

Each month, every qualifying Bond is entered into a draw for the following set of monthly prizes:

• Ten prizes of £1,000

• Two prizes of £10,000

• One prize of £50,000

As regards your chances of winning, on the FBS website they say:

The breakdown of prizes ensures that each bond has 13 opportunities to win a prize each month – 156 over the course of a year. The more bonds you hold, the greater the chance of winning. Even with one bond, your odds of landing a windfall are 64/1 in the course of the first 12 draws.

How Do Windfall Bonds Compare with Premium Bonds?

The first thing to note is that each Windfall Bond costs £10,000, so that is the minimum investment.

By contrast, the minimum purchase for Premium Bonds is just £100, which is reducing to £25 by March 2019. Windfall Bonds aren’t therefore an option unless you have a fairly sizeable lump sum to invest.

Assuming you do, however, how do the two compare? On the FBS website they say:

Odds of 64 to one are over five times better than the odds of winning £1,000 or more in the course of a year if you invested the same amount in Premium Bonds. And unlike Premium Bonds, the Windfall Bond pays interest, plus there’s no limit to how many Windfall Bonds you can hold.

I am sure that’s true as far as it goes. However, there is a bit more to consider than that.

First of all, Premium Bonds offer lots of smaller prizes than £1,000, including £25, £50, £100 and £500. According to the probabilities calculator on Martin Lewis’s Money Saving Expert website, with £10,000 worth of premium bonds you could expect on average to win £100 in prizes per year.

By contrast, with Windfall Bonds the guaranteed return at 0.75% is just £75 a year. So if you have one of the 63 out of 64 Windfall Bonds that don’t win a prize in a year, on average you will be £25 a year worse off.

Of course, it’s hard to compare the two directly, as the £100 annual return on Premium Bonds is just an average figure. In practice you might earn more or less than this in a year. You might also earn nothing at all.

A further consideration is that Premium Bonds also pay out larger prizes, including two one million pound prizes every month. The chances of winning a life-changing sum like this are extremely low – a mind-boggling 1 in 35,926,766,878 per month for a single £1 bond – but nonetheless every month two people have to win. The top prize with a Windfall Bond is £50,000. That’s still a handy sum, of course, but at just five times the purchase price of the bond it probably won’t be life-changing.

Another thing to bear in mind is that the interest paid on Windfall Bonds is taxable – so if you have exceeded your PSA (Personal Savings Allowance) you will have to pay tax on it at your highest marginal rate. The PSA for basic rate taxpayers is £1,000 and for higher rate taxpayers £500. Additional rate taxpayers (people earning over £150,000 a year) do not receive a PSA.

Under UK law, both Premium Bond and Windfall Bond prizes are tax-free.

Finally, with Windfall Bonds once you have paid your £10,000 to purchase a Bond you cannot withdraw all or part of it unless you close your account, which takes 35 days. With Premium Bonds you can withdraw all or part of your holding at any time, and the proceeds normally go through in just a few days.

Conclusions

In my view, once you cut through the hype, there isn’t a great deal to choose between Premium Bonds and the FBS Windfall Bonds. In the end it probably boils down to your personal circumstances and your attitude to risk.

If you have at least £10,000 to invest and like the security of a guaranteed 0.75% annual interest rate (variable) plus a small – but not minuscule – chance of winning a monthly prize of £1,000 to £50,000, Windfall Bonds are certainly worth considering.

With a holding of £10,000, with Premium Bonds you will win on average £100 in prizes in a year, compared with a guaranteed £75 interest (taxable) with Windfall Bonds. With Windfall Bonds though you will have a five times better chance of winning an additional prize from £1,000 to £50,000 per year than with Premium Bonds (though you won’t have the tiny chance of winning a life-changing sum).

As mentioned earlier, there are also other considerations, such as the ease of cashing in some or all of your Premium Bonds, compared with the slower cashing in process with Windfall Bonds and inability to make partial withdrawals.

So those are my thoughts, but what do you think? Are Windfall Bonds the way to go, or would you stick with Premium Bonds? Please leave any comments or questions below!

Please see also my 2017 post about Premium Bonds, where I reveal my own experiences with them and set out my thoughts on how they compare with other methods of saving/investment.

If you enjoyed this post, please link to it on your own blog or social media:

Today I am spotlighting Property Partner, a property crowdfunding platform I have been investing with since 2015.

As I have noted before on Pounds and Sense, I am something of an enthusiast for property investment (and specifically property crowdfunding). Among other things, I like the fact that you can make money from both rental income and capital growth. And investing in property can be a good way of spreading risk when you have equity-based investments.

Property Partner

Launched in January 2015, Property Partner has swiftly become the UK’s largest property crowdfunding website. They have over 11,500 investors, who between them have invested over £122.7 million in properties across the UK. Non-UK investors are welcome to join Property Partner too, so long as the legal system in their country permits it. Unfortunately US residents cannot invest via Property Partner at this time.

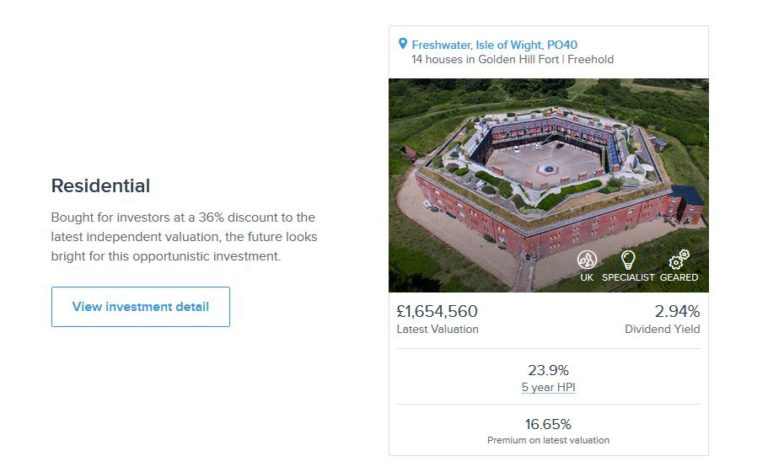

Property Partner offer shares in a wide range of properties. They include commercial buildings and residential ones, including PBSA (purpose built student accommodation). The properties tend to be on the larger side, so you won’t generally find single flats or terraced houses here. Neither do they sell shares in development or bridging loans, as offered by several other property crowdfunding platforms. This is what you might call ‘traditional’ property crowdfunding, where a property is bought on behalf of investors, who then receive a share of the rental income and any capital gains when the property (or their share in it) is sold. Here is a sample listing from their website…

One big attraction of Property Partner is that they have an active secondary market. That means investors can offer part or all of their portfolio for sale at any time. Obviously, to sell your shares in a property you will need a buyer, but Property Partner say that so long as they are priced reasonably (i.e. at or below the current official price) shares normally sell within 72 hours. By contrast, other property crowdfunding platforms such as The House Crowd and CrowdLords do not run formal secondary markets, though they say they will always help would-be sellers find a buyer if required.

Another attraction of Property Partner is that dividends are paid monthly, unlike other platforms which typically pay quarterly, biannually or annually. Money from dividends builds up in your account, and you can either withdraw it or reinvest it in other properties. When you add that you can get started on Property Partner for as little as £250, it is not all that surprising to me that they have enjoyed such success.

For legal reasons explained on the website, you can’t currently invest on Property Partner through a tax-efficient ISA or a SIPP. That means rental income will be liable for tax at your highest marginal rate, and any profits on selling will be subject to Capital Gains Tax (though there is quite a generous annual CGT allowance).

On the positive side, for anyone investing £5000 or more, you can opt for one of three managed plans: income focused, growth focused, or balanced. Your investments in them will be managed on your behalf to ensure good diversification of assets. Property Partner say that the net annual return (capital growth plus rental income) of the dividend plan should be at least 6.5%, the balanced plan at least 7.5% and the growth plan at least 8.5%.

My Experience

I have been investing with Property Partner for three years now, and have shares in a total of 17 properties. My largest single holding is around £2,550 (St David’s Lodge in Hastings, pictured above) and the smallest is £27.90.

I have aimed to build a diversified portfolio within Property Partner. I hold shares in both residential and commercial properties, in London and across the English regions (Property Partner doesn’t have properties in Scotland or Northern Ireland, and they have just one in Wales). To diversify further, I also recently bought a share in some purpose-built student accommodation in Leicester. Although as Leicester is my old university city, sentimental reasons may also have played a part in this decision!

During all the time I have been with Property Partner there have been no defaults or delays, and dividends have arrived in my account every month like clockwork. I understand that is true of all the properties on their books.

All properties on Property Partner are purchased for an initial five years. After the five years are up, all investors will get the opportunity to sell their share (or part of it) at a market valuation made by an independent chartered surveyor. As the platform hasn’t yet been going for 5 years, that hasn’t happened yet. Alternatively, as mentioned above, you can put your share up for sale at any time on the secondary market.

Pros and Cons

Based on my experiences, here is my list of pros and cons for Property Partner.

Pros

1. Fast, easy sign-up.

2. Well-designed, intuitive website.

3. Low minimum investment of just £250.

4. Property Partner take care of all the work involved in buying and managing properties. You just choose which ones to invest in.

5. Possibility to access your money at any time by selling on secondary market (though this does depend on another investor being willing to buy your shares at a price you find acceptable).

6. Guaranteed opportunity to sell at a fair market price after five years.

7. Customer service (in my experience anyway) is fast, friendly and helpful.

8. Charges are reasonable, with an initial 2% fee. There is no charge for selling shares.

9. Potential to profit through both capital appreciation and rental income.

10. Rental income is paid into your account every month. You can either withdraw it or reinvest it.

11. Up to £750 cashback is available for new investors of £2,000 or more via my referral link (see below).

12. Managed investment plans are available for investors of £5,000 or more.

Cons

1. No tax-free ISA or SIPP option available.

2. Rates of return are competitive but not the highest.

3. No development or bridging loans.

4. Some properties are purchased with gearing (loan finance). This makes them riskier if the value of the property should fall.

Conclusion

Overall, I have been impressed by my experiences with Property Partner. There have never been any delays or defaults, which can’t be said of every crowdfunding platform I have invested with. Property Partner state that the returns generated across all their properties since 2015 average 7.3% a year, taking into account both rental income and capital appreciation. That obviously beats bank and building society accounts by a considerable margin.

As ever, it is important to note that investments with Property Partner do not enjoy the same level of protection as bank and building society savings, which are covered (up to £85,000) by the Financial Services Compensation Scheme. All investments are secured against bricks and mortar, however, so even in a worst case scenario it is highly unlikely you would lose all your money.

The lack of liquidity with property investments generally means they should be regarded as medium- to long-term investments, and you should only invest money you are unlikely to need at short notice. The active secondary market on Property Partner does though mean that you should be able to recover your capital quickly if you need it, though there is no guarantee what price you will get.

Clearly, no-one should put all their spare cash into Property Partner (or any other investment platform). Nonetheless, it is certainly worth considering as part of a diversified portfolio. Not only are the rates of return significantly higher than those offered by banks and building societies, they are relatively unaffected by ups and downs in the stock market. Property investments aren’t a way of hedging your equity-based investments directly, but they do help spread the risk.

Welcome Offer

As an existing Property Partner investor, I can offer a special bonus for anyone joining via my link. If you click through this special invitation link, sign up and invest a minimum of £2,000 within 60 days, you will receive an extra bonus as follows (and so will I):

Not only that, once you are an investor with Property Partner, even if you only start with £250, you will be able to offer the same bonus to your friends and relatives and earn commission yourself. There is no limit to the number of people you can introduce through this scheme.

Obviously, this is a generous promotional offer by Property Partner and I assume it won’t be available forever. If you want to take advantage, therefore, don’t wait too long. I will remove this information if/when I hear the offer is no longer valid.

If you have any comments or questions about this review, as always, please do leave them below.

Disclosure: this post includes affiliate links. If you click through and make an investment at the website in question, I may receive a commission for introducing you. This has no effect on the terms or benefits you will receive. Please note also that I am not a professional financial adviser. You should do your own ‘due diligence’ before making any investment, and seek professional advice from a qualified financial adviser if in any doubt how best to proceed.

If you enjoyed this post, please link to it on your own blog or social media:

RESET is book aimed at mid-life professionals who feel as if they are in a rut and and want to get their lives back under control. I was kindly offered a review copy by the author, David Sawyer, so here are my thoughts about it…

The full title of the book is RESET: How to Restart Your Life and Get F.U. Money. By the latter, David means enough money so that you can say – er – “So long” to your employer if your job is causing you undue stress. The book does, though, emphasize that RESET doesn’t necessarily involve quitting your job, if you enjoy it and it is aligned with your personal goals and values.

RESET is available from Amazon in both hard copy and Kindle e-book versions. The printed version – which I received – amounts to quite a substantial 337 pages (plus a further 34 pages of preliminaries with Roman numbering!). The bulk of the book is arranged in six main sections, as follows:

1. What Matters to You?

2. Going Digital: How to Future-Proof Your Career

3. De-Clutter Your Life

4. Getting F.U. Money – a Plan

5. 11 Core Principles to Guide You in Work and in Life

6. 12 Do’s and Don’ts

Each section is divided into chapters. Part 4, Getting F.U. Money – a Plan, is the longest by some way and divided into 17 chapters. David is a PR professional, and as you might expect his book (which is published under the imprint of his PR company) is well written and presented.

RESET promotes, broadly speaking, the philosophy advocated by the FIRE movement. FIRE stands for Financial Independence, Retire Early. FIRE has been largely driven by some influential (mainly US-based) online bloggers.

The general idea of FIRE is that you seek to achieve financial independence at as early an age as possible, by simplifying your life, living more frugally, saving money and investing. The aim is to build up a substantial ‘pot’ of money that you can then use to buy yourself time and freedom. The ultimate aim – in many cases anyway – is to give up your job and retire early.

That doesn’t mean just joining the pipe and slippers brigade, though. It will typically involve spending more time enjoying life with loved ones, and working on projects that you enjoy and are important to you. These might involve anything from starting your own business to pursuing a hobby or interest, learning a new skill to doing voluntary work for a cause close to your heart.

As a money blogger myself I was familiar with quite a few of the concepts set out in the book, but David has done an impressive job of researching them and bringing them together in a highly accessible (and entertaining) way. As a semi-retired 62-year-old freelance writer I am not really in David’s main target readership, but I did still pick up some valuable tips and resources that I shall be using in my own life.

If you are a mid-career professional (roughly speaking between 35 and 60) and feeling stuck in a rut, this book will open your eyes to a range of strategies for regaining control of your life. You may not agree with every piece of advice David offers (I don’t share all his views about investment, for example) but you will almost certainly gain a lot of valuable, actionable tips and ideas. At the very least, it will open your eyes to a method that is increasingly being adopted by people on both sides of the Atlantic to take back control of their lives and achieve their long-term goals.

As always, if you have any questions or comments about RESET, please do post them below.

Disclosure: This post includes affiliate links. If you click through and make a purchase, I may receive a commission for introducing you. This will not affect the price you are charged or the terms you are offered.

If you enjoyed this post, please link to it on your own blog or social media: