Today I am looking at The Good Retirement Guide, an annual guide published by Kogan Page. I bought the current 2021 edition, which was published last month.

The Good Retirement Guide 2021 is 318 pages long. The text is fairly dense but broken up by plenty of headings and bullet-point lists. There are 14 chapters and an alphabetical index at the back. The chapter titles are as follows:

Are You Looking Forward to Retirement?

Money and Budgeting

Pensions

Tax

Investment

Your Home

Leisure Activities

Starting Your Own Business

Looking for Paid Work

Voluntary Work

Health

Holidays

Caring for Elderly Parents

No-one is Immortal

The chapter titles are pretty self-explanatory. The book attempts to cover every aspect of making the most of your senior years. The style is clear and readable, and additional resources are signposted as appropriate.

In contrast with Sod 60! which I also reviewed recently, The Good Retirement Guide covers the financial aspects of later life in some detail. I thought the information about pensions and benefits in particular was very good and tells you most of what you need to know.

Some of the other chapters are a bit less comprehensive. The one on leisure activities, for example, lists various things you might like to do – or take up – in retirement, but the information is frequently sketchy and can verge on stating the obvious. Here is what it has to say about poetry, for example:

There is an increasing enthusiasm for poetry and poetry readings in clubs, pubs and other places of entertainment. Special local events may be advertised in your neighbourhood.

And apart from a mention for the Poetry Society and a link to their website, that is all you get on this subject 🙂

I don’t want to appear too harsh. Obviously in a wide-ranging book like this, it can be hard to judge the degree of detail appropriate to any particular topic. At least by mentioning a wide range of possibilities, the book may give you some ideas about activities you might like to pursue further in retirement.

The health-related content is a bit of a mixed bag. Some subjects are covered in reasonable depth, others less so. There is just half a page devoted to keeping fit, for example, with a further couple of paragraphs about yoga and Pilates. On the other hand, there is some good information (and advice) on health insurance, long-term care plans, and so forth. Again, this illustrates that the book’s primary focus is on the financial aspects of retirement.

One thing that did surprise me is that although this 2021 edition of The Good Retirement Guide was only published last month, there is no mention of the pandemic in it. You will search in vain for Coronavirus or Covid-19 in the index. I know there can be long lead times in publishing, but in an annual guide you might think they could have inserted a section about it somewhere. Maybe we will have to wait for the 2022 version?

Even so, a lot of the subjects discussed in the guide – holidays, for example – have been seriously impacted by the pandemic. The advice and procedures for travel abroad in particular may be very different even after the pandemic is officially over.

Final Thoughts

Overall, I thought The Good Retirement Guide 2021 was a helpful book for people approaching retirement. As I’ve said above, it has a strong emphasis on financial matters, and is well worth reading for that alone. Some of the other content is a bit hit-and-miss, and the surprising lack of any mention of the pandemic means that at times it reads like a guide to an alternate world where Covid never happened. Of course, none of us really knows what the ‘new normal’ will be in future. We can but hope it will be not too far removed from the old normal we remember and which this book – despite the 2021 in its title – basically depicts.

As always, if you have any thoughts or questions about this post, please do leave them below.

Disclosure: As with many posts on Pounds and Sense, this post includes affiliate links. If you click through and make a purchase, I may receive a modest commission for introducing you. This will not affect in any way the price you pay or the product or service you receive.

If you enjoyed this post, please link to it on your own blog or social media:

As I write this we are still stuck in what feels like everlasting lockdown. But with the successful vaccine roll-out and rapidly falling case numbers – not to mention spring on the way – there are at least a few rays of hope on the horizon.

Anyway, to cheer you up, I’ve joined forces with some of my fellow UK bloggers to put together a giveaway with a top-of-the-range Dyson Airwrap worth £450 for the lucky winner.

As a mere male I must admit I had never heard of this before. But as I have read up about it now, I can tell you that the Dyson Airwrap is a high-tech hair-styling device. It harnesses an aerodynamic phenomenon called the Coanda effect, which curves air to attract and wrap hair to the barrel. So it styles using a flow of air, not extreme heat. This reduces the risk of heat-damage to your hair.

As I am currently sporting a mop of ‘lockdown hair’, I reckon I could probably do with one of these myself!

One lucky winner will win themselves the highly coveted Dyson Airwrap worth a whopping £450! The Dyson Airwrap is currently the hottest tool on the market and with it’s hefty price tag it’s not accessible for many.

The Dyson Airwrap comes with six hair styling attachments to dry, curl, wave and smooth hair. The Airwrap with intelligent heat control measures airflow temperature over 40 times a second and regulates heat, to ensure it always stays below 150°C.

The Dyson Airwrap also comes with a tan storage case to store your Airwrap and its attachments safely.

How to Enter

To enter simply complete all or any of the Rafflecopter entry options below. The more you complete, the more chances you have of winning.

The competition ends at midnight on Sunday 14th March and a winner will be drawn on Monday 15th March. If for any reason the chosen prize is out of stock at the time of the draw, the winner will be able to select an alternative prize up to the same value.

For full entry terms and conditions please see the Rafflecopter widget below.

One final small point is that if a winning entry comes from following someone on social media, the organizer (my colleague Neesha Rees) will check before awarding the prize that the winner is still following the account in question. If they aren’t, they will be disqualified and a new winner drawn. So, please, don’t follow and immediately unfollow, as your entry won’t then count.

Good luck, and here’s hoping we can all look forward to brighter times (and better hair) soon 🙂

If you enjoyed this post, please link to it on your own blog or social media:

In brief, Property Partner is a property crowdfunding platform. For the most part they specialize in ‘traditional’ property crowdfunding rather than loan or development finance.

Properties are bought and managed by Property Partner on investors’ behalf. Investors then receive a share of the rental income as dividends, and a share of any profits (plus return of their capital) when the property is sold.

Property Partner launched in January 2015. That date is significant, because after a property has been on the platform for five years, all investors get the chance to exit at a fair market price (determined by an independent surveyor). Due to the pandemic the five-year anniversary process was temporarily put on hold, but it is now proceeding again, albeit with delays as they work through the backlog.

How it operates is that in the run-up to the fifth anniversary of a property, all investors have the opportunity to say if they want to exit their investment at the valuation price or stay on for another five-year term (less than this if they subsequently exit via the resale market, of course).

All investors who have opted to leave will then have their shares pooled and put up for sale on Property Partner at the price stated. New investors are then able to buy these shares.

So long as all shares are sold, the original investors get their money (including any net profits) and the property continues under Property Partner’s management. If all shares don’t sell, however, Property Partner offer the property for sale on the open market. Investors then have to wait until the property is sold before getting their money back. As anyone who has been involved with buying or selling property will know, this is likely to take several months (quite possibly longer in the current circumstances).

The Opportunity

As Property Partner themselves have been pointing out, a number of properties that are coming up to their fifth anniversary are currently trading on the resale market at well below their latest valuation. Here is just one example:

This property in Tower Hill, London (not one I own shares in myself) is due to go through the fifth-anniversary process in April 2021 (or possibly a bit later due to the backlog). At the time of writing shares are available on the secondary market at a price of 91p, which is 28.28% below the latest valuation of £126.88. In theory, then, you could buy shares now and in the next few months sell up for a substantial short-term gain.

Of course, in practice it’s not as simple as that. Here are some reasons:

Nobody knows yet what the final five-year valuation will be. If it is lower than the current valuation (which is perfectly possible in the current economic climate) the net profit will be reduced, perhaps substantially.

There is no guarantee that the shares of all investors who wish to exit will actually sell on the platform. If they don’t, as mentioned, you could have a long wait before the property is sold on the open market. In addition, if this happens there is no guarantee that the property will sell at the valuation price. If it goes for less than this, your returns will be reduced accordingly.

There are platform fees to take into account. In particular, there is a 1% fee for buying on the secondary market and a further 0.5% stamp duty reserve tax charge. Thankfully there are no exit fees, though.

And finally, the number of shares available for any property on the secondary market is limited. Obviously the number you can buy depends on how many shares other investors want to sell at the price in question.

On the plus side, for the length of time you hold the shares you may receive monthly dividends at a rate between 1.5% and 6% per year (though dividend payments on some properties are currently suspended due to Covid). This will offset the fees mentioned above; but if you only intend to hold the shares for a few months it probably won’t cover them completely. Bear in mind that an Assets Under Management (AUM) fee is now deducted from dividends as well.

As an investor with Property Partner since almost the beginning (the cover image shows a property in Torquay I own shares in – I plan to retire there one day 😀 ), I am awaiting the five-year exit for my investments with considerable interest.

My personal circumstances have changed since I started investing with the platform, so I intend to take the opportunity to offload at least some of ‘my’ properties. Indeed, I have already voted to sell my shares in the first property I ever invested in with Property Partner (20 Phillimore Close) and am waiting to see how this pans out. I will update this post in due course once I know.

Nonetheless, I am still considering investing short term on the resale market to take advantage of the opportunity the five-year anniversary presents. In particular, I have already topped up my investments in some of the properties I already hold but am planning to dispose of.

I will, though, be cautious until I have a better idea how the first few five-year anniversaries have passed, so I can see if all shares put up by investors sell on Property Partner, or if they have to sell the properties concerned on the open market. As mentioned earlier, the latter route will clearly take longer and there is no guarantee what price would be achieved.

Would I recommend someone who is currently an investor in Property Partner to look into this? Yes, certainly. Whatever your current circumstances, you need to be aware of what is going on with any properties you hold with Property Partner. And if you wish to sell, you should definitely consider taking advantage of the five-year exit mechanic. Equally, if you have money available to invest, you could check out the opportunities buying now on the resale market – though do bear in my mind my cautionary comments above.

If you haven’t joined Property Partner, and you like the idea of investing some of your portfolio in property, the platform is certainly worth a look. As older properties come back on the market for new investors, there will be no shortage of opportunities in the months ahead. And my understanding is that, as the original costs of acquisition have been amortised, there will be less costs to cover from investors, thus boosting the potential returns from the properties in question.

In addition, as these properties have a five-year history already, you will be able to check how they have been performing in terms of dividends generated and capital appreciation. This is no guarantee of how well or badly they will do in the future, of course.

Take a look at my Property Partner review for much more information about the platform and how it works. Also, if you do decide to invest in Property Partner, there is a welcome bonus offer. For convenience I have copied details below from my review.

Welcome Offer

As an existing Property Partner investor, I can offer a special bonus for anyone joining via my link. If you click through this special invitation link, sign up and invest a minimum of £2,000 within 60 days, you will receive an extra bonus as follows (and so will I):

Not only that, once you are an investor with Property Partner, you will be able to offer the same bonus to your friends and relatives and earn commission yourself. There is no limit to the number of people you can introduce through this scheme.

If you have any comments or questions about this post, as always, please do leave them below.

Note: This is a fully updated version of a post published in 2019.

Disclosure: this post includes referral links. If you click through and make an investment, I may receive a commission for introducing you. This has no effect on the terms or benefits you will receive. Please note also that I am not a professional financial adviser. You should do your own ‘due diligence’ before making any investment, and seek professional advice from a qualified financial adviser if in any doubt how best to proceed. Be aware that all investments carry a risk of loss.

If you enjoyed this post, please link to it on your own blog or social media:

Here is my latest Coronavirus Crisis Update. Regular readers will know I have been posting these since the first lockdown started in the spring of 2020 (you can read my January 2021 update here if you like).

I plan to continue these updates until we are clearly over the pandemic and something resembling normal life has resumed. Obviously, I very much hope that will be sooner rather than later.

As ever, I will begin by discussing financial matters and then life more generally over the last few weeks.

Financial

I’ll begin as usual with my Nutmeg stocks and shares ISA, as I know many of you like to hear what is happening with this.

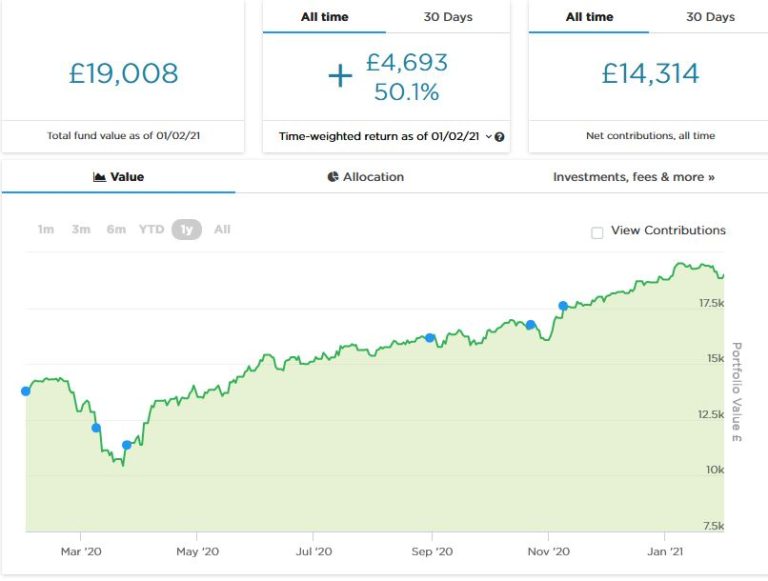

As the screenshot below shows, since last month’s update my main portfolio has been through some ups and downs. It is currently valued at £19,008. Last month it stood at £18,886, so it is at least up a little (£122) overall.

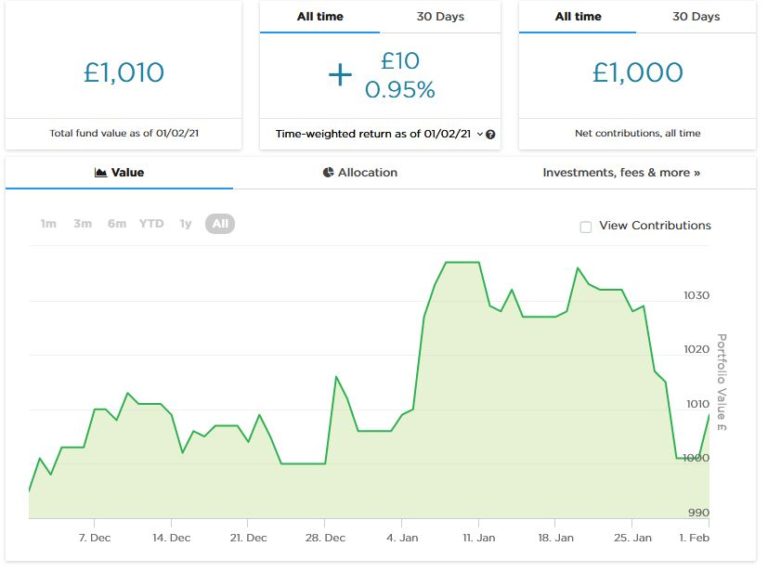

As you may recall, two months ago I put £1,000 into a second Nutmeg pot to try out Nutmeg’s new Smart Alpha option. The value of this pot rose as high as £1,037 in mid-January, though it currently stands at a more modest £1,010. Here is a screen capture showing performance to date, though obviously it is far too early to draw any conclusions from this.

Incidentally, I was recently asked by Nutmeg to contribute an article about my ‘Investing Journey’ for their blog. This was published in early January and you can read it here if you like. In the original version I was more explicit about why I left the charity I used to work for (basically a personality clash with the new Director who saw me as a rival). Nutmeg presumably decided this might ruffle a few feathers – even 25 years on! – so they changed it to something blandly neutral. Anyway, I thought I should let you know, as the opening section reads a little oddly now 🙂

The Nutmeg article brought quite a few new subscribers to this blog – so if that includes you, welcome to Pounds and Sense! I do hope you find my posts interesting.

Moving on, I had an email this week from the peer-to-peer lending platform RateSetter saying that all their lending activity is being transferred to Metro Bank (which now owns RateSetter). All investor accounts are therefore closing at the start of April, with investors’ money being returned to them in full along with all interest due.

I know some RateSetter investors are unhappy about this, but personally in these turbulent times I’m just glad to be getting my money back with interest. I originally invested £1,000 in September 2018 with an eye to claiming the £100 new investor bonus. The latter was duly credited to my account a year later, so by April I expect there to be a total of around £1,180 in my account. That equates to an annual interest rate of around 7%, which I am perfectly happy with.

This last year has undoubtedly been tough for P2P lending companies, with rising default rates and withdrawal requests along with reduced demand for loans. This has caused some platforms to experience cashflow problems and bad publicity. The only other one I have any money left with is ZOPA, which has also had a challenging year. I have only a few hundred pounds left in ZOPA as I switched some time ago from reinvesting repayments to withdrawing them. I’m not sure I can see much of a future for P2P lending in the UK, but of course in these unique times anything is possible. I don’t foresee myself putting any more money into P2P lending for a while, though.

I also heard recently from Property Partner. As you may know, this is a property crowdfunding platform. A few years ago, when I was investing regularly in property crowdfunding, I put around £5,000 into twenty or so properties on this platform.

Anyway, the email revealed that the first property I bought shares in has now reached its fifth anniversary. All investors therefore have the opportunity to sell up at the current independent valuation or else continue for a further five years. I voted to sell my shares, since (as mentioned in this recent post) I am currently trying to reduce the total amount I have invested in property crowdfunding.

The way the five-year anniversary process works is that all shares owned by investors who want to sell are bundled together and put up for sale on the Property Partner site. Assuming they are all bought by other investors, everyone who voted to sell then gets their money back at the current valuation. If that doesn’t happen, Property Partner put the property concerned up for sale. But obviously that is likely to take months and there is no guarantee the valuation price will be achieved. So you might end up getting back less than anticipated (or perhaps more in a best-case scenario).

Obviously I’m hoping this process goes smoothly and I get my money back soon. I would comment, though, that many of the properties that are coming up to their five-year anniversary are on offer on the resale market at well under the current valuation price. So if you are of a speculative persuasion, there is an opportunity to buy shares now at a discount and maybe make a quick-ish profit through selling up via the five-year anniversary process. I must admit I am tempted to try this, but haven’t made a decision yet!

Moving on, my two Buy2LetCars investments are still delivering the promised monthly returns without any fuss. As I am semi-retired but don’t yet qualify for the state pension, the £450 or so I receive from them every month represents a major part of my monthly income currently. I am also looking forward to receiving a substantial lump-sum payment in April when my first investment with them matures.

As I’ve said before, investors with Buy2LetCars put up the money to finance a car for a key worker such as a nurse or police officer. They then receive 36 monthly capital repayments followed by a final balancing payment of interest and capital. If you are looking for an income-producing investment with a substantial lump sum payment after three years – and you like the idea of doing a bit of good with your money too – they are well worth checking out (and likewise if you’re a key worker looking for a lease car yourself). If you’d like to learn more, you can read my review of Buy2LetCars here and my more recent article about the company here. And here is a link to Wheels4Sure, their car-leasing website. Note that you can’t invest with Buy2LetCars through an ISA, so the interest part of the final payment will have some tax deducted. Depending on your circumstances, you may be able to reclaim this.

Finally, several more readers have now signed up with the low-key matched betting opportunity mentioned in some previous updates. New members are still being accepted, but the company has had to reduce their payouts slightly. New members now receive £50 a month for the first six months, reducing to £25 a month thereafter. Considering that this opportunity is cost-free, risk-free and hands-free, that’s still a pretty good deal, though 🙂

As I said above, this opportunity is based on matched betting, a sideline-earning opportunity I have been pursuing for several years myself. I was asked not to divulge too many details about it publicly, for good reasons I will explain privately to anyone who may be interested (and no, it’s not illegal!). As I said above, it doesn’t require any financial outlay, is entirely hands-off, and will provide a passive income of £50 a month for the first six months and £25 a month thereafter.

No knowledge of betting is required, and you don’t have to place any bets yourself (this is all done by the company’s clever software). You just have to set up a separate bank account for bets to go through, but running the account is entirely financed by the company. Please note that this opportunity is only open to honest, trustworthy people who haven’t done matched betting before and have no more than two accounts already with online bookmakers. For more info (and to receive a no-obligation invitation) drop me a line including your email address via my Contact Me page.

Personal

I don’t know about you, but January to me has felt a very long month. It’s been cold, damp and depressing, with the whole country stuck in what seems like a never-ending lockdown.

As you may know, I live on my own since my partner, Jayne, passed away a few years ago. I am lucky to live in a fairly large house with a good-sized garden, so being mostly confined to home hasn’t been as big a challenge for me as I’m sure it has for some. Also, I am well used to working from home, having done this for the last 30 years or so. Even so, being unable to see friends and family has been hard for me, as has the closure of my local swimming pool (which I used to visit twice a week). And I appreciate that in many ways I am one of the lucky ones. I don’t have any major financial worries, and I’m not trying to home-school any children!

I did have a ‘day out’ at the end of January when I had to go to the eye clinic at Burton Hospital for a follow-up appointment. As regular readers will know, in the autumn I was diagnosed with a perforated retina in the left eye. I had laser treatment for this, and my January appointment was to assess how successful it had been.

As it turned out, there was some good news and some bad. The consultant told me that the treatment had been three-quarters successful. In one area it hadn’t ‘taken’, meaning I needed top-up treatment. He administered this then and there. I guess he cranked up the laser a bit, as unlike my first treatment it was somewhat painful and I had a headache for a couple of days afterwards. I have to go back at the start of March for what I very much hope will be a final check-up. Keep your fingers crossed for me!

Because they put drops in my eyes at these appointments, I can’t drive. I therefore took a taxi to the hospital and caught the train back. On previous occasions the trains have been very quiet, but there were noticeably more passengers this time. The roads too seemed pretty busy. I get the impression that people are (understandably) becoming fed up with lockdown now and the government’s Stay At Home message isn’t being as well complied with. Not a criticism, just an observation.

I am still aiming to go out for a walk once a day, though with some of the bad weather in January, I have missed a few. Here is a photo of my front garden about a fortnight ago 😮

On the plus side, I do enjoy watching the snow as long as I don’t have any essential trips to make. And I like to go for a walk in it once it has fallen. It was lovely to see (and hear) the local children getting out their sledges and enjoying some much-needed fun during these difficult times.

As far as evening entertainment is concerned, I finished my box-set of the tongue-in-cheek detective series Agatha Raisin and am happy to recommend that. On a similar note, I am enjoying the new (second) series of The Mallorca Files, which is currently on BBC iPlayer. It is just a shame that because of the pandemic they were only able to record six episodes.

Also, inspired by this post by my fellow blogger Caz, I have been investigating what is on offer on Amazon Prime Video. I have Amazon Prime mainly for the fast, free deliveries. But of course members do get access to a range of free films and TV series as well.

Anyway, I found a couple of series I really enjoyed. Being a Star Trek fan, I had to check out Lower Decks, a cartoon series focusing on the junior ranks on board one of the Federation’s least illustrious starships, the USS Cerritos. This has some great laugh-out-loud moments but some good stories as well. There are plenty of allusions to familiar Star Trek tropes that will keep any fan of the franchise amused. Watch out also for an appearance by an evil incarnation of Microsoft’s infamous ‘Office Assistant’ Clippy!

Of course, if you’re a Star Trek fan and haven’t yet seen Star Trek: Picard featuring the great Patrick Stewart as the eponymous hero, you should definitely watch this on Amazon Prime Video as well 🙂

The other series I enjoyed is Undone. Indeed, this is one of the best things I’ve seen on TV for quite a while. It’s almost impossible to describe, but it’s an animation that combines elements of mystery, comedy, romance, science fiction/fantasy, and more. And all with stunning, almost psychedelic, imagery, and strong acting and characterization. Here’s a screen capture that will give you some idea of the style. If you watch nothing else on Amazon Prime Video, give this a try..

Going back to the pandemic, there has at least been some good news this month. The vaccine roll-out has been going well – I’ve just heard that 10 million people have now had their first injection – and the number of new cases has been falling rapidly. As a 65-year-old I have not yet been called for vaccination but assume this is likely to happen fairly soon.

I do hope these developments will allow lockdown and other restrictions to be eased in the coming weeks, as in my view they are causing grave harm to people’s physical and mental well-being. In particular, I would like to see schools reopen, along with swimming pools and gyms. I would also like to see pubs, restaurants and hotels allowed to reopen before many have to close their doors for good. In the (slightly) longer term I would like to see all restrictions lifted so that normal life can resume. I am not a fan of mandatory masks and would like to see them made optional for those who believe they offer some useful protection from the virus (personally I have never been convinced of this).

As always, I hope you are staying safe and sane during these challenging times. If you have any comments or questions, please do post them below.

If you enjoyed this post, please link to it on your own blog or social media: