SBS are keen to demystify self-build and show it’s not just for wealthy people on Grand Designs!

As part of this, they recently commissioned research which highlights the misconceptions that still exist about self-build. The research was undertaken among 2,000 UK adults by Opinium on behalf of Suffolk Building Society.

Read on to discover how self-build may be more accessible than you think…

According to research from Suffolk Building Society, over two-thirds (69%) of potential self-builders do not know that some mortgage lenders will allow them to borrow to purchase land where planning permission has been granted.

Correspondingly, concern over financing a project was the number one barrier for those interested in self-build: other concerns were around seeking planning permission and difficulties in finding suitable land.

The Society believes the lack of awareness about being able to borrow for land may discourage people from considering self-build. Many incorrectly believe they either need to be sufficiently cash-rich to fund the land themselves before applying for a self-build mortgage, or be gifted a plot from land-owning family members.

Suffolk Building Society is aiming to normalize self-build and, in doing so, wants more people to know that self-build is a viable option for those with modest budgets. Its recent research found that over half (54%) of those who are considering a self-build at some point in the future believe that self-build is still reserved only for the very wealthy.

Richard Norrington, Chief Executive at Suffolk Building Society said: “Self-build television series undoubtedly make for great viewing, but they do set the bar remarkably high. One could easily assume that self-build is only for those with unlimited time and deep pockets.

“Self-build is considered a fairly standard route to home ownership in countries such as Hungary, France, and Sweden, and with better education and awareness, self-build could become more mainstream here in the UK too.”

Who Is Considering Self Build and Why?

The cost of living crisis has not significantly dampened people’s appetite for self-build: a third of people are still considering self-build, which is only a small decrease from 35% last time this survey was undertaken in July 2020.

The propensity to consider a self-build decreases with age: younger people in their 20s (60%) and 30s (56%) are significantly more interested than those in their 50s (16%) and 60s (7%), dispelling the myth that self-build is a project for retirement.

Of those considering self-build, 31% would prefer to go for a completely new build, 27% said they would opt for a knockdown/rebuild project, and 21% said they would undertake a major renovation to an existing property.

The main motivation cited by over a quarter (28%) was the ability to design the layout of their own home, but this is a significant drop from 51% in 2020. There was a broader range of reasons evident in this year’s research, including self-build being a more affordable way of creating an ideal home (15%) and having a home in the right location (12%). One in ten (9%) of those considering a self-build are doing so to create a home suitable for multiple generations under one roof.

Over four in five (83%) want to make eco-friendly decisions about their future property. However, of these, seven in ten would only prioritize this if it was within their budget. This is, of course, reflective of the current economic environment.

Self Build Register Awareness

The Self-build and Custom Housebuilding Act 2015 requires each relevant local authority to keep a register of individuals who are seeking to acquire serviced plots of land in the authority’s area for their self-build project.

Data published on 31 March 2023 showed a decline in individuals joining the Self Build Registers, which tallies with the research from Suffolk Building Society:

Only one in five potential self-builders (21%) are signed up to the Self Build Register and 41% of those considering self-build had not even heard of the Self Build Register.

Richard Norrington said: “The National Custom and Self Build Association campaigned diligently for the Self Build Registers in a bid to facilitate a greater number of self-build homes. But so far, this has not been realized. The Registers need promoting alongside resources that help people understand all that a self-build entails as, despite the current economic uncertainty, there is clearly still an appetite for self-build.

“As a country, we need to normalize self-build, encouraging regular people to build good homes, thus helping to reduce the housing shortage in the process and improving the collective carbon footprint of our housing stock.

“There are undoubtedly more hurdles in this process than in a standard house purchase – particularly at the moment with high labour and material costs. However, being able to design a property that meets your needs both in terms of function and aesthetics is hugely rewarding. We would like more people to know that some lenders are ready and willing to lend on land as well as for the build itself; and secondly, that self-build is more accessible than they might have previously thought.”

Many thanks to Suffolk Building Society for allowing me to reproduce their research – and comments about it – here.

If you would like more info about self-build mortgages from SBS, you can visit the relevant page of their website via this link. SBS say that although 80% of their members are in the east of England, the rest live across the UK.

As always, if you have any comments or questions about this article, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

A recent study conducted by Smart Money People reveals that one in ten people in a serious relationship, including marriage, civil partnerships, or cohabitation, maintain a secret savings account.

The research for the study was undertaken by Opinium on behalf of Smart Money People from 12 to 16 January 2024 among 2,000 UK adults aged 18 and over.

The SMP study highlights the prevalence of this practice among those in their 30s, with 30% acknowledging having such an account. Additionally, women are reported to be more likely than men to save secretly, indicating potential gender-related financial dynamics within relationships.

The reasons for maintaining a secret savings account vary, with the most common explanations being that individuals already had the account before entering the relationship (38%) or the desire to maintain financial independence (37%). However, a surprising 22% of respondents with a secret savings account admit to using it as an emergency break-up fund, anticipating potential costs associated with leaving a relationship, such as moving expenses or repurchasing shared assets like a car.

Interestingly, over half (51%) of those with a break-up fund also have a joint savings account with someone other than their partner, introducing an additional layer of complexity to the financial dynamics within relationships.

The study sheds light on the impact of financial matters on relationship stability, revealing that 18% of adults believe a lack of financial compatibility has contributed to a break-up in the past. The biggest savings-related causes of friction for those currently in a relationship are having different opinions on savings habits or when it’s okay to use savings (28%). This underscores the importance of aligning financial goals and strategies within a relationship.

Financial compatibility is considered crucial by 95% of couples living together, emphasizing the significance of shared financial values. Despite this, 10% of individuals still maintain secret savings accounts, illustrating a potential disparity between stated beliefs and actual financial behaviour.

The study indicates that half of people in relationships do not save the same amount of money as their partner, primarily due to unequal earnings (65%). An additional one-third attribute the difference in savings to disparate spending habits, with 40% of these individuals maintaining secret savings accounts.

In terms of relationship longevity, the research suggests that couples with joint savings accounts feel more financially compatible (90%) compared to those without. The data encourages open and honest discussions about money within relationships, emphasizing the importance of navigating financial decisions together.

Commenting on the findings, Jacqueline Dewey, CEO of Smart Money People, said, “Many people may already have methods of saving that work well for them prior to a new relationship, so although long-term partnerships bring about new joint financial goals, this shouldn’t negate any personal goals for each individual.

“Having different outlooks and opinions on savings isn’t necessarily a deal-breaker, but finding the most suitable ways to manage this is important.”

In summary, the SMP study highlights the complexities of financial dynamics within relationships, emphasizing the need for open communication, shared financial goals and mutual understanding, in order to maintain a healthy and long-lasting partnership.

I recently posted about the importance of compounding to investors. In the article I pointed out that compounding, when combined with the magic of compound interest, is a powerful tool for building wealth and long-term financial success.

Compounding involves earning interest on both your initial investment and the accumulated interest from previous periods. In other words, it’s the process of generating earnings from an asset’s reinvested earnings. The more frequently your money is compounded, the faster it grows. And the longer your money remains invested, the more significant the compounding effect becomes.

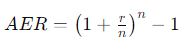

A reader asked me if the effect of compounding is equivalent to getting a higher annual interest rate. The answer to that is yes, if interest is compounded more than once a year. The more times per year interest is compounded, the higher the effective annual rate becomes. The official term for this is AER, or annual equivalent rate.

In this article I thought I would explain AER in a bit more detail, as it is a very important concept for savers and investors to grasp.

What is AER?

Annual Equivalent Rate (AER) is a standardized way of expressing the interest rate on savings or investment products over a one-year period. It allows investors to compare the potential returns on different financial products on a like-for-like basis. AER takes into account the effect of compounding, providing a more accurate representation of the overall return on an investment.

Why is AER Important?

AER is crucial for investors as it helps them make more informed decisions when comparing different savings and investment options. While nominal interest rates may seem attractive at first glance, they can be misleading. AER provides a more accurate reflection of the actual return on an investment by factoring in the compounding of interest over time.

Example

Let’s consider two savings accounts:

Savings Account A offers a nominal interest rate of 7% per annum, compounded annually.

Savings Account B offers a nominal interest rate of 7% per annum, compounded quarterly.

To compare these accounts accurately, we can use the AER formula:

Where:

r is the nominal interest rate (as a decimal)

n is the number of compounding periods per year

For Account A:

For Account B:

In this example, even though both accounts have the same nominal interest rate, Account B has a higher AER due to the more frequent compounding.

Let’s now add a third savings account, Account C, again with a nominal annual interest rate of 7% but this time compounded monthly. We can calculate the AER for Account C using the formula as before:

As you can see, the AER is higher again due to the increased frequency of compounding. If compounding was even more frequent (e.g. daily) the difference would be even more pronounced. In addition, the longer the period over which you invest, the greater the difference frequency of compounding will make.

While AER is often considered with regard to savings accounts, it also applies to investments. As I said in my earlier post, with a property crowdlending platform like Assetz Exchange [referral link] which pays monthly dividends (and has low minimum investments), you can keep reinvesting the income you receive to boost the returns you make.

Understanding AER is crucial for UK savers and investors as it provides a standardized measure to compare the true potential returns of different financial products.

By taking into account the compounding effect, AER offers a more accurate picture of overall returns on investments. When evaluating savings or investment opportunities, always look beyond nominal interest rates and consider the AER to make informed decisions that align with your financial goals. And take any opportunity that arises to reinvest your returns to harness the power of compounding to grow your wealth faster.

As ever, if you have any comments or questions about this post, please do leave them below.

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

If you enjoyed this post, please link to it on your own blog or social media:

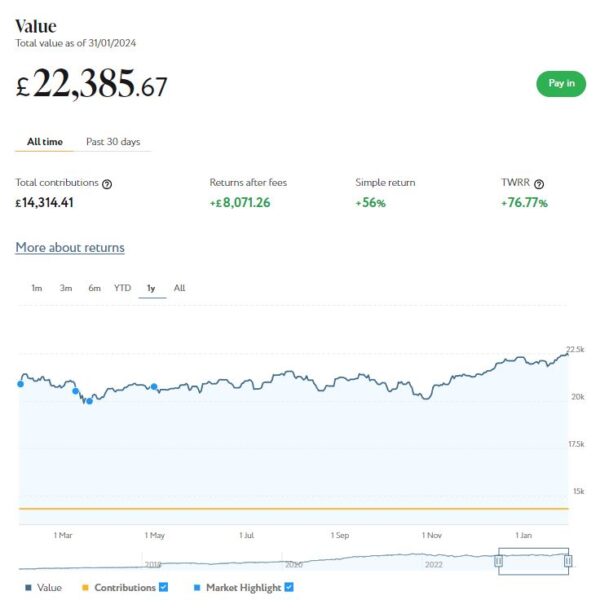

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

As the screenshot below for the last 12 months shows, my main Nutmeg portfolio is currently valued at £22,386. Last month it stood at £22,292 so that is a modest increase of £94.

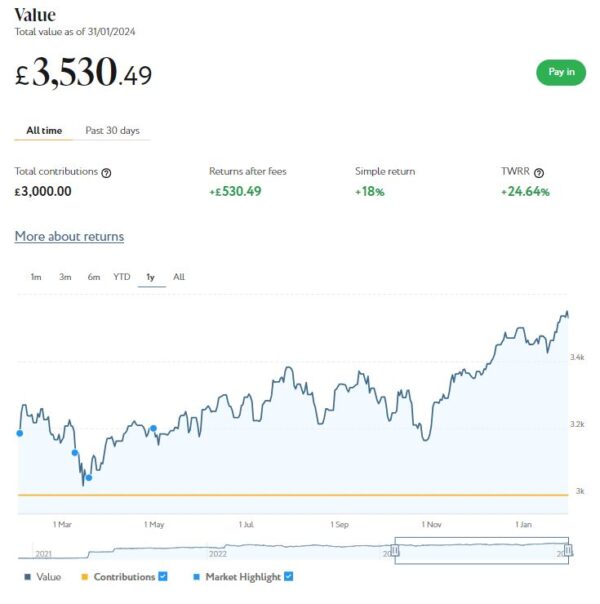

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £3,530 compared with £3,501 a month ago, a rise of £29. Here is a screen capture showing performance over the last 12 months.

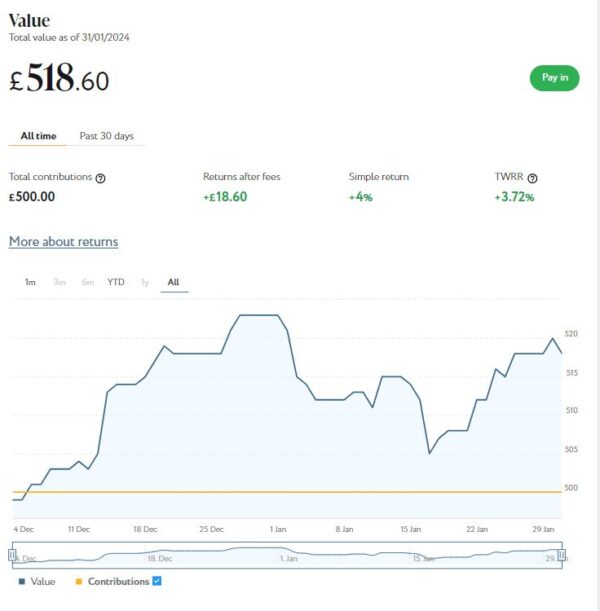

Finally, at the start of December 2023 I invested £500 in one of Nutmeg’s new thematic portfolios (Resource Transformation). As you can see from the screen capture below, after a storming start in December this fell back in January before recovering again to £519, a small drop of £4 or 0.76% month on month. It is still around 4% ahead since I invested at the start of December, though.

January was obviously a mixed month for my Nutmeg investments. Overall I was still £119 up, though. If you add this to the increase of £1,160 last month, that gives a total value increase over the last two months of £1,279 or 5.17%. In these turbulent times I am more than happy with that.

You can read my full Nutmeg review here (including a special offer at the end for PAS readers). If you are looking for a home for your annual ISA allowance, based on my overall experience over the last seven years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs), Lifetime ISAs and Junior ISAs as well.

I also have investments with the property crowdlending platform Kuflink. They continue to do well, with new projects launching every week. Last month I withdrew £350 from completed projects to help pay for a much-needed holiday in the spring. I currently have around £1,570 invested with them in 10 different projects paying interest rates averaging around 7%. I also have £14 in my Kuflink cash account.

To date I have never lost any money with Kuflink, though some loan terms have been extended once or twice. On the plus side, when this happens additional interest is paid for the period in question.

There is now an initial minimum investment of £1,000 and a minimum investment per project of £500. Kuflink say they are doing this to streamline their operation and minimize costs. I can understand that, though it does mean that the option to test the water with a small first investment has been removed. It also makes it harder for small investors (like myself) to build a well-diversified portfolio on a limited budget.

One possible way around this is to invest using Kuflink’s Auto/IFISA facility. Your money here is automatically invested across a basket of loans over a period from one to three years. Interest rates normally range from around 7% for one year to 9.83% gross for a three-year term.

As a special Valentine’s Day promotion, however, until 14 February 2024 they are offering enhanced rates of 9% for one year, 10.5% for two years and 12.25% gross for a three-year term. These figures are AER (annual equivalent rates) that incorporate reinvestment of interest paid at the end of each year. These are actually the highest rates I have ever seen Kuflink offering ❤

You can invest tax-free in a Kuflink Auto IFISA. Or if you have already used your annual iFISA allowance elsewhere, you can invest via a taxable Auto account. You can read my full Kuflink review here if you wish.

Moving on, my Assetz Exchange investments continue to generate steady returns. Regular readers will know that this is a P2P property investment platform focusing on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my AE portfolio has generated a respectable £161.85 in revenue from rental income. As I said in last month’s update, capital growth has slowed, though, in line with UK property values generally.

At the time of writing, 6 of ‘my’ properties are showing gains, 3 are breaking even, and the remaining 19 are showing losses. My portfolio is currently showing a net decrease in value of £40.87, meaning that overall (rental income minus capital value decrease) I am up by £120.98. That’s still a decent return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Assetz Exchange most projects are socially beneficial as well.

The overall fall in capital value of my AE investments is obviously a little disappointing. But it’s important to remember that until/unless I choose to sell the investments in question, it is largely theoretical, based on the most recent price at which shares in the property concerned have changed hands. The rental income, on the other hand, is real money (which in my case I’ve reinvested in other AE projects to further diversify my portfolio).

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of AE as far as i am concerned (especially now that Kuflink have raised their minimum investment per project to £500). You can actually invest from as little as 80p per property if you really want to proceed cautiously.

As I noted in this recent post, Assetz Exchange is particularly good if you want to compound your returns by reinvesting rental income. This effectively boosts the interest rate you are receiving. Personally, once I have accrued a minimum of £10 in rental payments, I reinvest this money in either a new AE project or one I have already invested in (thus increasing my holding). Over time, even if I don’t invest any more capital, this will ensure my investment with AE grows at an accelerating rate.

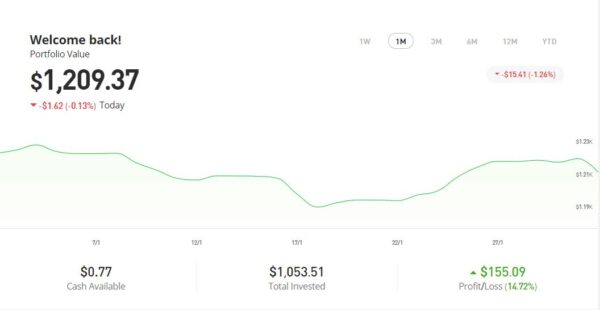

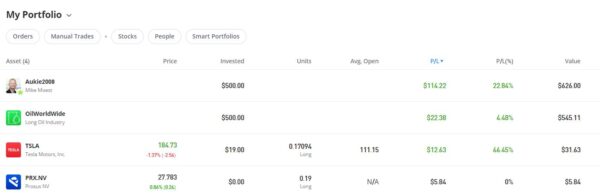

Last year I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios, Oil Worldwide. I also invested a small amount I had left over in Tesla shares.

As you can see from the screen captures below, my original investment totalling $1,022.26 is today worth $1,209.37, an overall increase of $187.11 or 18.30%.

eToro also recently introduced the eToro Money app. This allows you to deposit money to your eToro account without paying any currency conversion fees, saving you up to £5 for every £1,000 you deposit. You can also use the app to withdraw funds from your eToro account instantly to your bank account. I tried this myself and was impressed with how quickly and seamlessly it worked. You can read my blog post about eToro Money here.

I had three more articles published in January on the excellent Mouthy Money website. The first is How to Save Money on Your Water Bills. In Britain we’re lucky to have high-quality running water on tap whenever we need it. Like everything else in life it costs money, however. And in these times of rising prices and squeezed incomes, those costs can be a growing burden. So in this article I set out some ways you may be able to reduce your water bills.

Also in January Mouthy Money published How to Make Money With Classic Cars. In this article – written in association with my friends at the Car & Classic website – I described the surprising number of attractions to investing in classic cars, and provided a range of tips for those new to the field.

My final article published on Mouthy Money last month was Top Tips to Avoid Online Scams. This article set out my top ten tips for staying safe online and avoiding becoming a victim of the scammers. Do check it out!

As I’ve said before, Mouthy Money is a great resource for anyone interested in money-making and money-saving. I particularly like the ‘Deals of the Week’ feature compiled by Jordon Cox (‘Britain’s Coupon Kid’) which lists all the best current money-saving offers for savvy shoppers. Check out the latest edition here.

I am also a fan of my fellow MM contributor and money blogger Shoestring Jane. She writes mainly about money saving and frugal living. Her latest article How to Get Almost Everything More Cheaply has some great tips and ideas. You can see all of her articles for Mouthy Money via this web page.

I also published several posts on Pounds and Sense in January. I won’t bother mentioning those that are no longer relevant now, but the others are listed below.

In How to Start Copy Trading With eToro I discussed how to get started using the popular copy trading facility on eToro. This allows you to automatically copy successful traders on the platform – so when they make money, you make money too. As mentioned above, I have done this myself following Dutch professional investor Mike Moest and am currently around 23% in profit. You can read more in my post about copy trading on eToro and my experiences with it.

I also published HMRC Crackdown on Side Hustles – Truth and Fiction. As you may know, from January this year digital platforms like eBay, Etsy and Airbnb are required to collect additional information from sellers, including numbers of sales and amount of income generated. This data will be automatically shared with HMRC, who will compare it against their records to see if any tax may be due. This news has caused some consternation on social media, with many who have side hustles to help pay the bills worried they may be hit by an unexpected tax demand. In this post I explain what exactly is happening and set out to separate the truth from the fiction.

In Planning a UK Holiday This Year? Here Are Some Ideas For You! I set out a list of destinations in the UK I have visited myself, with links to my full reviews of the places concerned. They range from Bath to Barmouth, Lavenham to Llanbedrog. If you’re looking for ideas for a short break (or longer) in the UK this year, this could be a good source of inspiration for you 🙂

One Key Lesson About Investing I Learned From My Dad’s Big Mistake reveals an important lesson I learned from my late father about investing. It is a lesson I have tried to apply in all my investing myself. While it hasn’t stopped me making some mistakes along the way, it has certainly helped me avoid any disastrous losses. This article was first published in a slightly different form on Mouthy Money.

Finally in January I published How to Harness the Power of Compounding. In this article I discussed the power of compounding and compound interest. This is a wealth-building secret every saver and investor should embrace. I also revealed two particular types of investment where you can apply compounding to help boost your returns.

Also, from January I have become a regular contributor to the new Over 60s Discounts website. You can read my first article here: How to Cope With Loneliness in Later Life. As you may gather, as well as personal finance I will also be writing about ‘lifestyle’ matters for O60D.

On other things, the opportunity to get a free share worth up to £100 with Trading 212 has now closed. However, you can can also still Get a Free ETF Share Worth up to £200 with Wealthyhood. This DIY wealth-building app is aimed especially at people new to stock market investing. The minimum investment to qualify for the free share offer is £50 – but on the plus side, they now guarantee your free ETF share will be worth at least £10.

I am still using and getting good results from the cashback app JamDoughnut. You can see my review of JamDoughnut here, along with a referral code that will get you a £2 bonus when you sign up. To be honest I’m surprised more PAS readers haven’t taken advantage of this opportunity. Not only can you get discounts of up to 20% using the app, they also hold regular contests and promotions offering additional bonuses and discounts.

Finally, a quick reminder that you can also follow Pounds and Sense on Facebook or Twitter/X. Twitter/X is my number one social media platform these days and I post regularly there. I share the latest news and information on financial (and other) matters, and other things that interest, amuse or concern me. So if you aren’t following my PAS account, you are definitely missing out!

That’s all for today. As always, if you have any comments or queries, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media: