Retirement can be a wonderful stage of life, bringing more freedom and time to enjoy yourself. But for many people, it can also mean adjusting to a lower income and watching the pennies more carefully than before.

The good news is that there are plenty of money-saving perks and discounts available specifically for retired and older people in the UK. Some are well known, while others fly under the radar. Either way, taking advantage of them can make a real difference to your finances over the course of a year.

Here are some of the best perks and discounts worth knowing about.

Free Bus Passes

One of the best-known benefits for older people is the free bus pass.

In England, you can currently apply for an older person’s bus pass when you reach State Pension age. In Scotland, Wales and Northern Ireland the rules differ slightly, and eligibility may begin earlier.

A bus pass allows free off-peak travel on local buses and can save regular users hundreds of pounds a year. Even if you only use it occasionally, it can still be very handy for shopping trips, appointments or days out.

You can apply via your local council or transport authority website. You can find out more on this government website.

If you’re 60 or over and live in London, you can get free travel on buses, trains and other modes of transport in and around London with a 60+ London Oyster photocard.

Senior Railcards

If you travel by train even a few times a year, a Senior Railcard can easily pay for itself.

Available to people aged 60 and over, the card gives one-third off most rail fares across Britain. The annual fee is modest (£35 a year or £80 for three years), and discounts apply to both standard and first-class tickets. You can opt for either a physical card or a digital one to keep on your phone. Unfortunately you can’t have both.

You can buy a Senior Railcard at any staffed station, by phone, or via this website.

Discounts at Restaurants and Cafés

Some restaurant chains, cafés and garden centres offer senior discounts, although they are not always widely advertised.

Examples can include:

Reduced-price meals on certain days

Smaller “senior portions”

Discounted tea-and-cake deals

Special offers linked to pensioner clubs or loyalty cards

Independent cafés and local businesses may also offer discounts for older customers, so it never hurts to ask politely.

Cinema Discounts

Cinema trips can become much cheaper once you reach retirement age.

Major cinema chains including Odeon, Vue and Cineworld often offer reduced-price tickets for seniors, especially for daytime screenings. Some cinemas also run dedicated “silver screen” events that include tea, coffee or biscuits in the ticket price.

These can provide both affordable entertainment and a good social outing.

Savings on Prescriptions and Healthcare

In England, prescriptions become free once you reach the age of 60. Prescriptions are already free for everyone in Scotland, Wales and Northern Ireland.

You may also qualify for:

Free NHS eye tests

Help with dental costs

Discounts on glasses and hearing aids

Many opticians additionally offer special deals for pensioners. The Age UK website has more information about this

Council Tax Discounts

This is an area many people overlook.

While there is no general “pensioner discount” for council tax, some retired people may qualify for reductions depending on their circumstances.

Examples include:

Single person discount (25%)

Council Tax Reduction schemes for people on low incomes

Discounts linked to disability adaptations in the home

Rules vary between councils, so it is worth checking your local authority’s website.

Discounts on Leisure Activities

Retired people can often save money on:

Gym memberships

Swimming sessions

Golf clubs

Museums and heritage attractions

Theatre tickets

For example, Better Leisure Centres offer reduced-price Better Health Senior membership for people aged 66 and over. Members enjoy access to swimming pools and fitness classes, and can also take part in dedicated activities for senior members, from walking football to aqua aerobics. More info can be found here.

Many local councils run discounted leisure schemes for older residents, particularly during off-peak hours.

If you enjoy keeping active in retirement, these savings can add up quickly.

National Trust and English Heritage Memberships

If you enjoy visiting historic houses, gardens and beauty spots, memberships in these organizations can represent excellent value.

Both offer senior membership options, and members receive free entry to hundreds of attractions around the country. Note that in the case of the National Trust you will need to have been a member for at least three years before applying and will have to phone them on 0344 800 1895 and ask (there is no online application form). You will then get 25% off standard membership. With English Heritage the discount is available immediately and worth around 15% for individuals and 22% for joint members.

For keen visitors to historic attractions and gardens, the savings can easily outweigh the annual membership fee.

Retail Discounts for Older Shoppers

Some retailers offer occasional “senior discount days” or loyalty perks for older customers.

These are less common than they once were, but discounts can still sometimes be found at:

Department stores

Hairdressers

Garden centres

Charity shops

Independent retailers

For example, frozen food specialists Iceland offer senior citizens 10% off on Tuesdays. To be eligible you must be 60 or over. There is no minimum purchase. You just have to show proof of age – e.g. a bus pass – at the till.

Another example is the Boots Over 60s Rewards Scheme. If you’re over 60 and have a Boots Advantage Card, you can get a range of extra benefits, including 8 points for every pound you spend on Boots’ own brands and selected others (normally card-holders only get 4 points per pound spent). You can also get 300 Advantage Card points when you take a free Boots Hearing Health Check. Each Advantage Card point is worth 1p, so 1000 points would be worth £10. You can spend your points online or in store. For more info and to apply, visit Boots’ Over 60s web page.

At other stores, again, it is often worth asking discreetly whether any discounts are available.

Travel Insurance Savings

Travel insurance can become more expensive as we get older, but prices vary enormously between providers.

Shopping around is essential. Specialist insurers aimed at older travellers (e.g. SAGA Travel Insurance and AllClear Travel) can sometimes offer much better value than mainstream companies.

Annual multi-trip policies may also work out cheaper if you take several holidays a year.

Don’t Be Afraid to Ask

One important point is that many discounts for older people are not heavily promoted. Businesses may offer them quietly or only at certain times.

There is absolutely no harm in politely asking:

“Do you offer a senior discount?”

The worst they can say is no — and you may be pleasantly surprised.

Final Thoughts

Retirement does not have to mean giving up the things you enjoy. By making the most of the discounts and perks available to older people, you can stretch your income further while still maintaining a good quality of life.

Even small savings can add up over time. A discounted rail ticket here, a cheaper cinema trip there, and reduced council tax or free prescriptions can collectively save hundreds of pounds a year.

And of course, every pound saved is a pound that can be spent on something you truly value!

If you enjoyed this post, please link to it on your own blog or social media:

If you’re retired or semi-retired and looking for a flexible way to earn a little extra money from home, Prolific Academic could be the answer you are seeking.

No, you’re not going to make a fortune from it. But you can earn a useful extra income in your spare time, while helping genuine academic researchers and keeping your brain active into the bargain.

What Is Prolific Academic?

Prolific Academic is an online platform that connects researchers – mainly from universities and other academic institutions – with members of the public willing to take part in research studies.

Most studies involve answering questionnaires or surveys, though some include simple games, memory tests, opinion polls, or short interactive tasks. Researchers are generally looking for honest responses from people of all ages and backgrounds, and seniors are often especially valued because they are under-represented in many studies.

Unlike some survey sites, Prolific has built a strong reputation for treating participants fairly. Studies are normally well designed, interesting and clearly explained. You can also see in advance how long each study should take and how much you’ll be paid (see below).

Flexible and Easy to Fit Around Your Life

One of the biggest advantages of Prolific for seniors is the flexibility.

There are no fixed hours, targets or commitments. You simply log in when you want to and choose from whatever studies are available. If you’re busy with holidays, family commitments, gardening, golf, volunteering, or anything else, you can ignore it for days or weeks without any problem.

Equally, if you have a quiet afternoon and fancy earning a few pounds, you can complete several studies in one sitting.

That makes Prolific ideal for retirees who want a side hustle that fits around their lifestyle rather than the other way round.

The Studies Are Often Genuinely Interesting

This is another reason I particularly like Prolific.

Many studies are linked to real academic research in subjects such as psychology, health, behaviour, finance, education, politics, memory, and technology. Some are thought-provoking and even fun.

You may be asked your opinion on current issues, to test a new app or website, or to take part in experiments exploring how people make decisions. I’ve personally found many studies surprisingly engaging.

Of course, there are occasional dull ones too – but because you can pick and choose, you’re free to skip anything that doesn’t appeal.

A Useful Extra Income Stream

Let’s keep expectations realistic: Prolific isn’t a replacement for a salary or pension.

But it can provide a worthwhile supplementary income. Rates typically work out between £8 and £12 per hour, with bonuses sometimes awarded as well. Many users earn enough to cover treats, hobbies, meals out, subscription services, or part of a holiday budget.

Payments are made without any deductions via the online payment platform PayPal. You can request a payout any time your earnings reach £6 or more. Payments are reliable and prompt, which is another reason the platform has developed such a loyal following. And because you decide how much time to devote to it, you remain completely in control.

Good for Keeping Your Brain Active

One thing many retirees discover is that mental stimulation matters just as much as physical activity.

The variety of tasks on Prolific can help keep your brain engaged and alert. Memory exercises, problem-solving tasks, reading comprehension studies, and opinion-based questionnaires all encourage active thinking.

I’m certainly not claiming Prolific is some sort of miracle anti-ageing treatment! But regularly engaging with new ideas and challenges can only be a positive thing.

The Tax Advantage for Small Earners

Another point worth mentioning is the UK government’s £1,000 Trading Allowance.

Under current HMRC rules, if your total income from casual self-employed or side-hustle activities is under £1,000 a year, you generally do not need to declare it or pay tax on it.

That means many casual Prolific users may fall comfortably within this limit.

Obviously everyone’s tax situation is different, and tax rules can change – so if you expect to earn more than this or are unsure about your position, it’s sensible to check the latest HMRC guidance or seek professional advice.

How to Sign Up

If you like the idea of earning a sideline income as a Prolific Academic member, all you need do is visit the Prolific website and click on the Get Paid to Participate box (don’t click the box to sign up as a researcher, obviously!).

An application form will then open requesting various items of information from you, most importantly the PayPal email address via which you want to be paid 💰

Final Thoughts

There are countless so-called “side hustles” being promoted online these days. Many are unrealistic, risky or simply exhausting.

Prolific is refreshingly different.

It’s flexible, straightforward, low-pressure and genuinely interesting. You can do as much or as little as you like, earn a bit of extra money, help academic research and keep mentally active at the same time.

For many seniors, that combination makes it close to the ideal side hustle.

Have you tried Prolific Academic yourself and would you recommend it? Or do you have another favourite side hassle you would like to share? I’d love to hear your thoughts. Please comment below as usual 🙂

If you enjoyed this post, please link to it on your own blog or social media:

I’ll begin as usual with my JP Morgan Personal Investing (previously Nutmeg) Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

As regular readers will know, in June last year I transferred most of the money in my former Nutmeg Fully Managed portfolio (just under £25,000) to a new Nutmeg Income Portfolio. I discussed this in detail in this post, but basically money in this port is invested to generate an income from share dividends and other sources. This is then paid monthly. Capital appreciation is targeted as well, but these portfolios are aimed primarily at older people (and others) who want/need their investment to generate a regular cash income.

In April my JPM Investing income portfolio generated £66.11 of income, which was duly paid into my bank account on 24 April 2026. That means I have now received tax-free income of £339.79 in 2026 and a total of £811.25 since I opened the account in June last year. That’s a return on capital of just over 3% to date. That is – to be honest – a bit less than I would have hoped based on JPM’s original projected annual return of just under 5% for income ports at my chosen risk level (five).

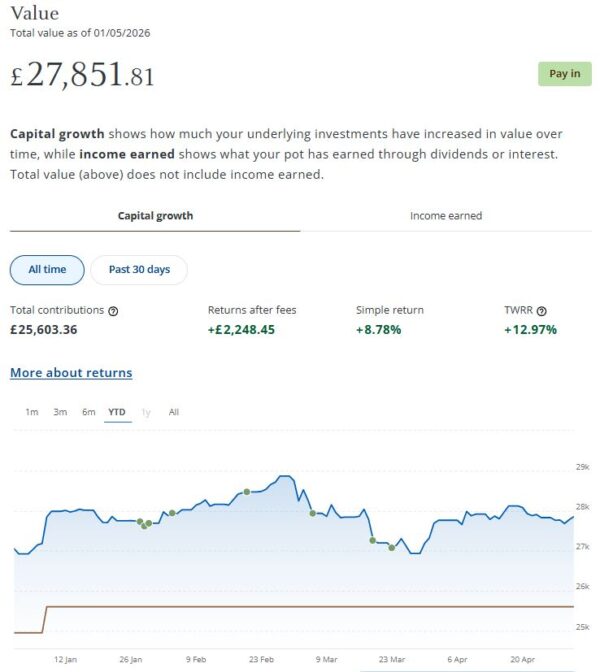

The better news is that my income portfolio increased in value in April (after its bigger fall in March). It’s now worth £27,852 compared with £27,320 at the start of last month, a rise of £532. You don’t need to be an investment expert to know that the volatility recently is due mainly to events in the Middle East. As I always say, you do have to expect ups and downs when investing. As the screen capture below shows, my income port is still up by a respectable £2,248 (8.78%) after fees since I opened it last June.

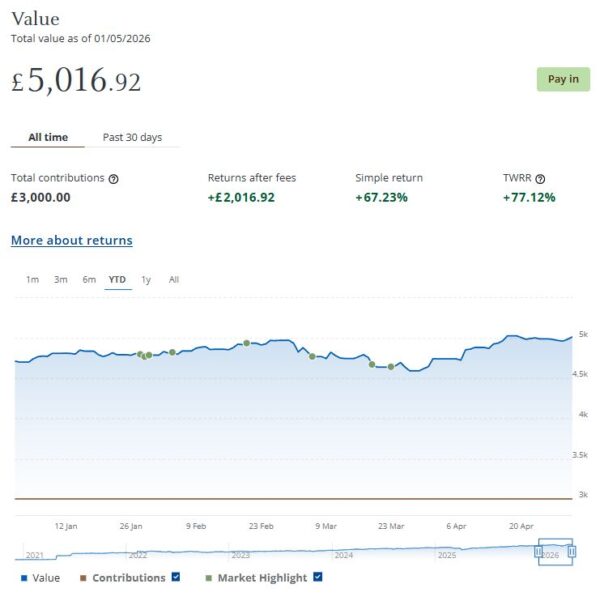

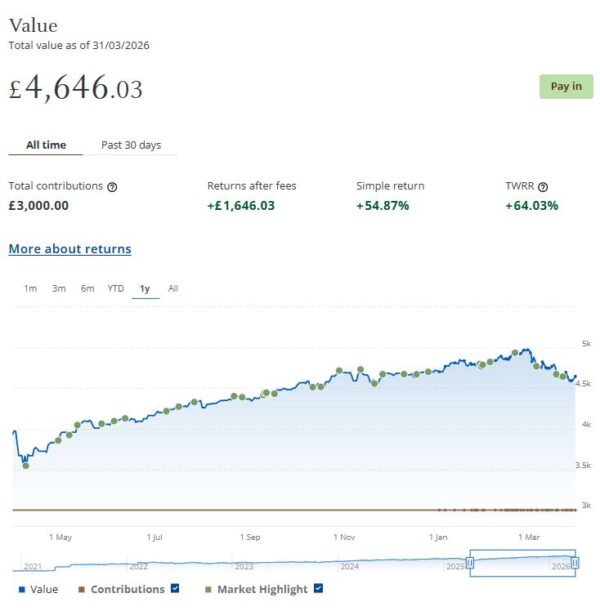

I still have a smaller, growth-oriented pot using JPM Investing’s Smart Alpha option. This is now worth £5,017 (rounded up) compared with £4,646 a month ago, a rise of £371. Here is a screen capture showing performance over the year to date.

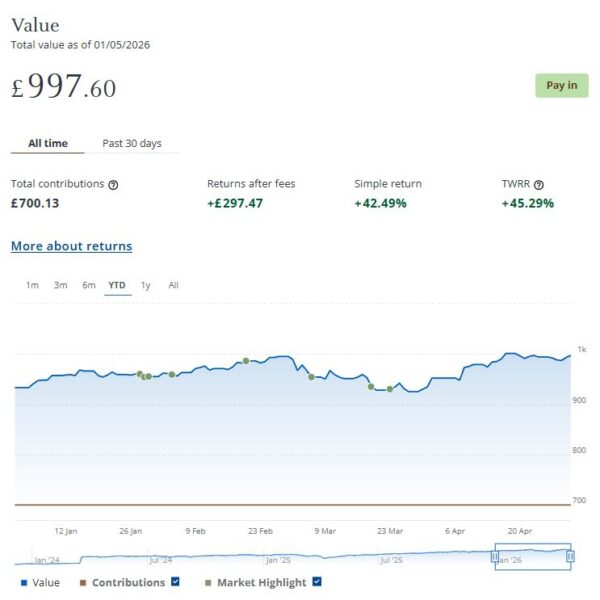

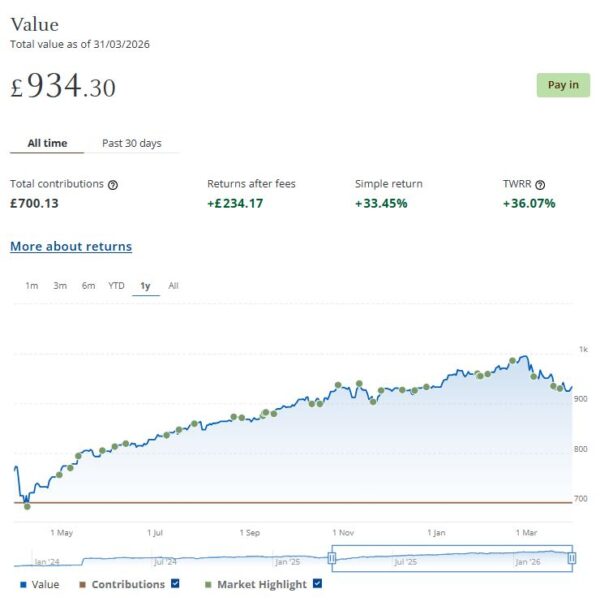

Finally, at the start of December 2023 I invested £500 in one of Nutmeg/JPM’s thematic portfolios (Resource Transformation). In March 2024 I also invested a further £200 from referral bonuses (something I no longer receive). As you can see from the YTD screen capture below, this portfolio is now worth £998 compared with £934 last month, a rise of £64.

Overall in April the value of my JPM investments rose by £967 or 3.02%. In addition I did, of course, receive £66.11 in income from my income portfolio. In total, then, I am £1,033.11 up for the month.

Excluding income generated, the overall value of my JPM investments is up by £4,630 or 15.72% since the start of May 2025. If you add to this the £811.25 of income generated by my Income portfolio to date, that gives a total profit for the last 12 months of £5,441.25 – a pretty good return in these uncertain times.

As I said above, some volatility is always to be expected with stock market investments, but in the longer term they tend to even themselves out (and typically outperform bank savings accounts, although that is never guaranteed). In general the worst thing you can do is panic and sell up when downturns occur (as happened in March). You are then crystallizing your losses rather than giving the markets time to recover. This is something I discussed last year in this blog post. Obviously nobody knows what will happen in the Middle East, but hopefully some sort of resolution will occur soon, if only because US President Trump desperately needs an exit strategy to pacify his critics back home. Once this happens, we will hopefully see world stock markets stabilize again. Though there is of course no guarantee about this.

You can read my full original Nutmeg/JPM review here. If you are looking for a home for your annual ISA allowance, based on my overall experience over the last nine years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs), Lifetime ISAs and Junior ISAs as well.

Moving on, I also have investments with P2P property investment platform Housemartin. As discussed in this post, the company rebranded last year from Assetz Exchange.

My investments with Housemartin continue to generate steady returns. Housemartin focuses on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my HM portfolio has generated a respectable £315.21 in revenue from rental income. I have made a small net loss of £17.60 on property disposals. Capital growth generally has slowed, in line with UK property values generally.

At the time of writing, 17 of ‘my’ properties are showing gains, 7 are breaking even, and the remaining 20 are showing losses. My portfolio of 44 properties is currently showing a net decrease in value of £71.59. That means that overall (rental income minus capital value decrease and loss on disposal) I am up by £243.62. That’s still a respectable return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Housemartin most projects are socially beneficial as well.

A further consideration is that property investments on Housemartin are less likely to be affected by stock market downturns, as happened in March due to the war in the Middle East. This again demonstrates the potential value of such investments for diversifying your portfolio during challenging times.

The net fall in capital value of my Housemartin investments is obviously a little disappointing. But it’s important to remember that until/unless I choose to sell the investments in question, it is largely theoretical, based on the latest price at which shares in the property concerned have changed hands. The rental income, on the other hand, is real money (which in my case I’ve reinvested in other HM projects to further diversify my portfolio).

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of Housemartin as far as i am concerned. You can actually invest from as little as £1 per property if you really want to proceed cautiously.

As I noted in this blog post, Housemartin is particularly good if you want to compound your returns by reinvesting rental income. This effectively boosts the interest rate you are receiving. Personally, once I have accrued a minimum of £10 in rental payments, I usually reinvest this money in either a new HM project or one I have already invested in (thus increasing my holding). Over time, even if I don’t invest any more capital, this will ensure my investment with Housemartin grows at an accelerating rate and becomes more diversified as well.

In 2022 I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios, Oil Worldwide. I also invested a small amount I had left over in Tesla shares.

In January this year, as Oil Worldwide hadn’t exactly been setting the world alight, I decided to switch my entire investment in this to another smart portfolio, InTheGame. This port, focusing on the computer gaming industry, has been the top performer for some time in my eToro virtual portfolio.

Unfortunately just as I switched away from Oil Worldwide, President Trump decided to invade Venezuela. This gave the oil industry a significant boost, which I would otherwise have benefited from. Meanwhile InTheGame went south, partly due to the war in the Middle East. At one point I was down by over 10% on this investment. Fortunately in the last few weeks InTheGame has made an impressive recovery and is now in profit by 7.91%.

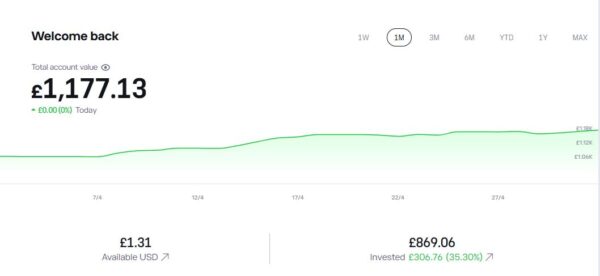

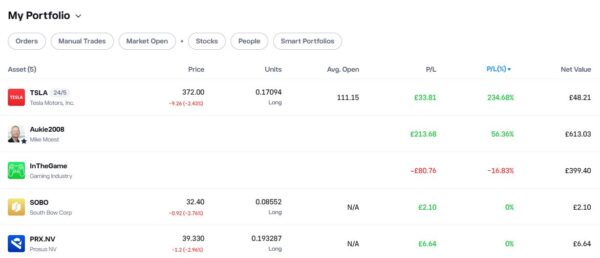

As you can see from the screen captures below, my original eToro investment (total value £888.36 in pounds sterling) is today worth £1,177.13, an overall increase of £288.77 or 25.77%.

Note: eToro now displays the value of investments in your native currency, although you can change this if you wish.

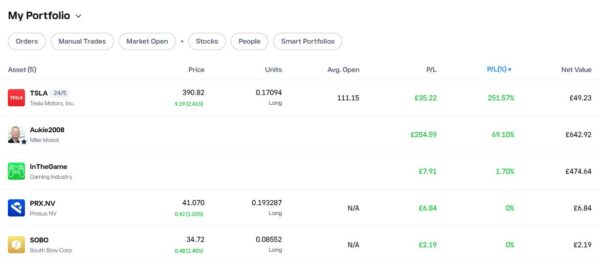

As mentioned above, my new investment in InTheGame is currently up by 7.91%. My copy trading investment with Aukie2008 also rose in value in April and is showing an impressive overall profit of 69.10%. Of course, I have held this investment for quite a bit longer.

My Tesla shares, which I purchased as an afterthought with some spare cash I had in my account, are also up this month and showing an overall profit of over 251% since I bought them. If only I had put a bit more money into this!

You might also notice that I have small holdings in Prosus NV, a Dutch internet group, and South Bow, a Canadian energy infrastructure company. To be honest I don’t understand how I acquired these, but I assume they are some sort of bonus I was awarded. In any event, I am happy to have them in my portfolio.

If you would like more information about setting up an eToro account, please click on this no-obligation website link [affiliate]. Don’t forget that you also get a free $100,000 virtual portfolio, which you can use to experiment with trading and investing strategies. I have certainly earned a lot from mine.

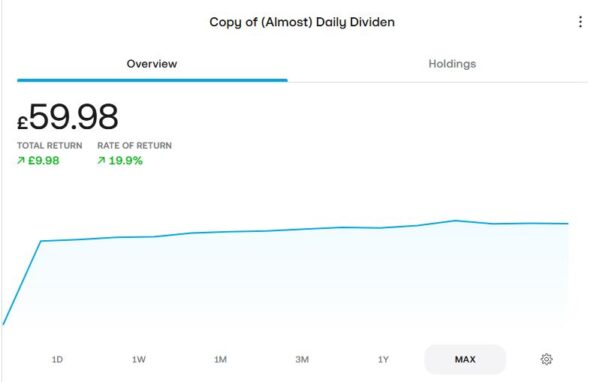

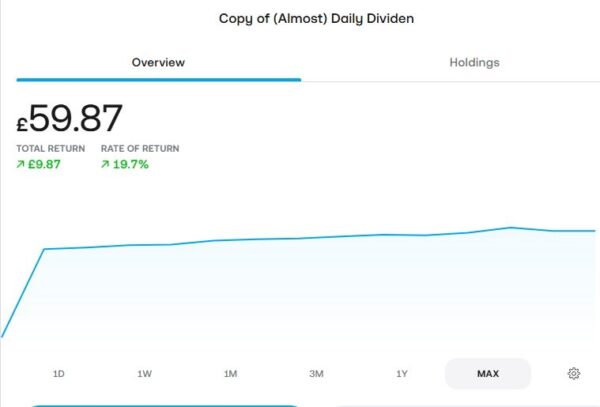

As an experiment, at the start of April 2025 I put £50 into an investment ISA with Trading 212. As mentioned in my blog post about dividend investing, I put it into the (Almost) Daily Dividends Portfolio, a ready-made portfolio or ‘pie’ on Trading 212. As you can see from the screen capture below, my portfolio is now worth £59.98. That’s a small rise of £0.12 since last month and an increase of £9.98 or 19.9% since I opened it just over a year ago. It has even accrued a grand total of £1.16 in dividends, most of which has now been (automatically) reinvested.

I am quite impressed with how this investment has been faring, despite the small amount I put in (which means I may be missing out on some smaller dividends). If I increased my investment I would almost certainly become eligible for more dividends, and even more the longer I remain invested. If I had any spare money at the moment, I would consider doing this. Of course, I do now have an income-focused portfolio with JPM Investing as well (see above).

Moving on, I published various posts on Pounds and Sense in April. I have listed below those that are still relevant.

In What is the Blue Light Card – And How Can It Help You Save Money? I discussed this discount scheme for people working in the emergency services and various other public services. For a modest fee (under £2.50 a year) you can access discounts on everything from restaurants to holidays, concerts and sporting events to insurance. You may also be eligible if you are retired from a qualifying occupation. Find out more in this article.

Finally in April I published Why Now Could Be the Ideal time to Take Advantage of Your New Tax-Free ISA Allowance. From the start of the new tax year on 6 April 2026, everyone has a new £20,000 tax-free ISA allowance. In this article I revealed why you might want to take advantage of at least some of this allowance sooner rather than later.

I’ll close with my customary reminder that you can also follow Pounds and Sense on Facebook or Twitter (or X as it is now). Twitter/X is my number one social media platform and I post regularly there. I share the latest news and information on financial matters, and other things that interest, amuse or concern me. So if you aren’t following my PAS account on Twitter/X, you are definitely missing out!

I am also on the BlueSky social media network under the username poundsandsense.bsky.social. Twitter/X remains my primary social media platform, but I also post details of my latest blog posts, third-party articles and other financial news and resources on BlueSky for those who prefer to follow me there.

As always, if you have any comments or questions, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts on PAS may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media:

If you work in the NHS, emergency services, or other frontline roles, you may be eligible for one of the UK’s most generous discount schemes: the Blue Light Card.

This little-known but highly valuable scheme offers access to thousands of discounts on everyday spending – and for many people, it can easily pay for itself many times over.

In this article, I’ll explain how the Blue Light Card works, who can apply, and how you can make the most of it.

What Is the Blue Light Card?

The Blue Light Card is a UK-wide discount scheme designed to recognize the contribution of people working in public service and frontline roles.

Members get access to over 15,000 discounts with retailers, restaurants, travel providers and more, both online and on the high street.

The scheme covers a wide range of spending categories, including:

Supermarkets and everyday shopping

Fashion and retail

Holidays and travel

Eating out and takeaways

Utilities, mobile, and insurance

In short, it’s a broad-based money-saving tool rather than a niche perk.

Who Is Eligible?

Despite the name, the Blue Light Card isn’t just for police or ambulance staff. Eligibility has expanded significantly in recent years.

You can typically apply if you are working, volunteering, or even retired from sectors such as:

NHS and healthcare

Emergency services (police, fire, ambulance)

Social care

Armed forces and veterans

Teaching and education staff

Certain volunteer organisations

This wide eligibility means millions of people across the UK now qualify.

Blue Light Card for Retired People – What You Need to Know

One aspect of the scheme that is especially relevant to many Pounds and Sense readers is that eligibility doesn’t necessarily end when you retire.

In fact, the scheme has been extended in recent years to include many retired workers from eligible sectors, allowing them to continue enjoying discounts even after leaving the workforce.

Who Qualifies in Retirement?

Retired eligibility covers a broad range of professions, including:

NHS staff

Police, fire and ambulance personnel

Armed forces veterans

Teachers and social care workers

So if you spent your career in public service, there’s a good chance you can still apply.

How Retired Eligibility Works

The main difference for retirees is how eligibility is verified.

Instead of a current work email or payslip, you’ll usually need to provide evidence of your former employment and/or pension. Examples include:

Pension documents (e.g. NHS or service pension statements)

P60s showing pension income

Certificates of service or employment history

Official letters confirming your role and dates of employment

The process can be slightly more involved than for current employees, but it is still very manageable.

Important Points to Be Aware Of

Documentation is key – applications may be rejected if proof isn’t clear

Requirements can vary depending on your former profession

Some roles may require minimum service periods

It’s worth taking a little care when applying to avoid delays.

What Discounts Can Retirees Expect?

Retired members receive exactly the same discounts as working members.

These can help reduce the cost of:

Travel and holidays

Dining out and entertainment

Home and garden purchases

Everyday shopping

For retirees on fixed incomes, this can be particularly valuable.

Is It Worth It for Retirees?

For many retired readers, the answer is a clear yes.

With a very modest upfront cost (see below) and potentially wide-ranging savings, the scheme offers a simple way to:

Offset rising living costs

Make pension income stretch further

Enjoy more affordable leisure activities

As always, the key is to use it regularly rather than letting it sit unused.

How Much Does It Cost?

One of the most appealing aspects of the scheme is its low cost.

£4.99 for two years’ membership

That’s less than £2.50 a year – meaning you only need to save a few pounds to break even. In practice, many members save far more than this over the course of a year.

The price for retired people is exactly the same as for those who are still working. There is no discounted or premium pricing tier for retirees, and they get exactly the same discounts and benefits as well. Note that there is a separate sign-up page for retired people in eligible occupations.

Verify your employment (or past employment, if retired)

Pay the small membership fee

Start accessing discounts via the website or app

Once approved, you can use either a physical card or a digital version on your phone.

What Kind of Discounts Are Available?

The range of offers is one of the scheme’s biggest strengths.

Typical deals include:

Percentage discounts (e.g. 10–20% off)

Cashback or gift card savings

Special promotions and limited-time offers

Discounted tickets and experiences

These can apply to both everyday essentials and occasional treats – helping stretch your budget further.

Pros and Cons

Advantages

Very low cost for two years

Huge range of discounts across everyday spending

Available to a wide range of professions, including retirees

Easy to use via app or card

Potential Drawbacks

Discounts vary and aren’t guaranteed at all retailers

Some offers may overlap with general promotions

You need to use it regularly to get full value

Is It Worth It?

For most eligible people – including retirees – the answer is yes.

Because the membership fee is so low, even modest use can justify the cost. If you regularly shop online, eat out, or book travel, the savings can quickly add up.

That said, it’s important to use the card sensibly. It should help you save money on things you would buy anyway, not encourage extra spending.

Final Thoughts

The Blue Light Card is a simple but effective way for frontline workers, public servants, and retirees from these sectors to reduce everyday costs.

At a time when many households are feeling the squeeze, it’s a useful reminder that small savings opportunities can make a real difference over time.

If you think you might be eligible – whether still working or now retired – it’s well worth checking. This could be one of the easiest wins in your personal finance toolkit.

As always, if you have any comments or questions about this article, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

As of 6 April 2026, UK investors have a fresh chance to supercharge their savings and investments with a new £20,000 Individual Savings Account (ISA) allowance.

To maximize the benefits of the new 2026/27 allowance, there’s a strong case for acting swiftly and using at least part of your £20,000 ISA allowance sooner rather than later. This is due to the power of compounding. By investing early, you give your money more time to grow, benefiting from the potential snowball effect of returns generating further returns. So the sooner you invest that £20,000 (assuming you are fortunate enough to have it) the more opportunity it has to multiply over time.

In addition to the tax-free ISA allowance remaining at a relatively generous £20,000 (for now – see below), the rules surrounding ISAs have undergone a welcome relaxation in recent years. One of the most significant changes is the ability to open more than one ISA of the same type (e.g. a stocks and shares ISA) with different providers in the same tax year. This means investors are no longer limited to a single provider for each type of ISA, giving them greater flexibility and choice in managing their investments.

Previously, investors were restricted to opening one cash ISA, one stocks and shares ISA and one innovative finance ISA (IFISA) per tax year. This restriction could prove frustrating for those seeking to diversify their investments or take advantage of new opportunities as the tax year progressed. Now, with the freedom to open multiple ISAs of the same type, investors can shop around for the best rates, terms and investment options without being limited to a single provider for each ISA type. They can also move some or all of their money from one provider to another without jeopardizing its tax-free status.

It’s important to remember, however, that while the rules have been relaxed, the overall annual ISA allowance remains fixed at £20,000. This means that any contributions made across multiple ISAs of any type will count towards your total allowance for the tax year. You should still therefore take care not to exceed the annual limit, to avoid any potential tax charges.

Note that from April 2027 the Cash ISA allowance has been reduced from £20,000 to £12,000 per year for savers under the age of 65. Until then it remains at £20,000 a year for all savers, though.

Cash ISAs offer a secure and accessible way to save, providing a tax-free environment for your savings with the added benefit of easy access to your funds when needed. Meanwhile, stocks and shares ISAs open the door to potential higher returns by investing in a wide range of assets such as equities, bonds, and funds, albeit with a higher level of risk. With a stocks and shares ISA you will never incur any liability for dividend tax, capital gains tax or income tax, even if your investments perform exceptionally well. Of course, there is no guarantee this will happen, but over a longer period stock market investments have typically outperformed cash savings, often by a substantial margin. IFISAs (e.g. from Housemartin, with whom I invest myself) allow you to invest is property crowdfunding and other forms of peer-to-peer finance. They are more specialized, but may appeal to some investors looking to further diversify their portfolios.

In recent years I have invested much of my own annual ISA allowance in a stocks and shares ISA with JP Morgan Personal Investing (previously Nutmeg), a robo-manager platform that has produced good returns for me. You can read how my Housemartin and JPM investments (and others) are faring in my monthly investment updates such as this one.

Closing Thoughts

The start of a new financial year is a good time for UK investors to review their savings and investment strategies. Whether you’re looking to start a new ISA or maximize your contributions to existing accounts, taking action early can set you on the path to optimizing your returns from this important tax-saving opportunity.

By investing sooner rather than later and taking advantage of the increased flexibility in ISA provider options, savers and investors can make the most of their money while minimizing their tax liabilities. So grasp this opportunity to build your wealth and protect it from the taxman today!

As always, if you have any comments or questions about this post, please do leave them below.

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

If you enjoyed this post, please link to it on your own blog or social media:

Volatile investment markets can be unsettling, particularly for older investors who may be more focused on preserving wealth than chasing high returns.

With ongoing geopolitical tensions, including the current conflict in the Middle East, market swings have become more pronounced. In this environment, a disciplined approach such as pound-cost averaging can help reduce risk and remove some of the stress from investing.

What Is Pound-Cost Averaging?

Pound-cost averaging (often abbreviated to PCA) is a simple investment strategy that involves investing a fixed amount of money at regular intervals, regardless of what the markets are doing.

Rather than trying to “time the market” – buying at the lowest point and selling at the highest – you invest regularly over time. This means you automatically buy more units when prices are low and fewer when prices are high.

How It Works in Practice

Suppose you invest £500 a month into a stock market fund:

In month one, prices are high, so your £500 buys fewer units.

In month two, prices fall, so the same £500 buys more units.

Over time, your average purchase cost tends to smooth out.

This reduces the risk of investing a large lump sum just before a market downturn – something that can be particularly damaging in retirement or near-retirement years.

The Key Benefits

1. Reduces Market Timing Risk

Even professional investors struggle to predict short-term market movements. Pound-cost averaging removes the need to guess when to invest, helping you avoid costly mistakes.

2. Smooths Out Volatility

By spreading your investments over time, you avoid the impact of sudden market swings. This is especially valuable during periods of uncertainty.

3. Encourages Discipline

Regular investing promotes good financial habits and helps ensure you stay committed to your long-term plan.

4. Emotion-Free Investing

Market falls can tempt investors to delay investing, while market highs can encourage overconfidence. PCA removes these emotional triggers.

Why It Matters Now

Recent instability linked to the Middle East conflict has contributed to increased volatility in global markets. Energy prices, inflation expectations and investor sentiment have all been affected.

In such conditions:

Markets can rise and fall sharply in short periods.

News headlines can trigger knee-jerk reactions.

Attempting to time entry points becomes even more difficult.

Pound-cost averaging provides a structured way to keep investing without being derailed by short-term events.

Lump Sum vs Regular Investing

It’s worth noting that, historically, investing a lump sum can sometimes produce higher returns – simply because more money is invested earlier.

However, this comes with higher risk. If markets fall soon after investing, losses can be significant.

For many people – particularly cautious investors or those approaching retirement – the lower risk and smoother ride offered by pound-cost averaging may be preferable.

Who Should Consider Pound-Cost Averaging?

This approach can be particularly suitable for:

New investors building confidence

Those investing monthly from income (e.g. pensions or earnings)

Investors concerned about current market volatility

Anyone looking to reduce emotional decision-making

It is also a natural fit for tax-efficient wrappers such as ISAs and pensions, where regular contributions are common.

Practical Tips for UK Investors

Use a Stocks and Shares ISA to shelter returns from tax

Set up an automatic monthly investment to maintain discipline

Choose diversified funds (e.g. global equity funds) to spread risk

Review periodically, but avoid reacting to short-term market noise

Final Thoughts

In uncertain times, trying to outguess the market can do more harm than good. Pound-cost averaging offers a steady, disciplined approach that helps reduce risk and maintain perspective.

While no strategy can eliminate volatility entirely, investing regularly over time can make market fluctuations work in your favour rather than against you – a valuable advantage in today’s unpredictable world.

As always, please feel free to leave any comments below. I am always delighted to hear from Pounds and Sense readers.

Disclaimer: I am not a qualified financial services professional and nothing in this post should be construed as personal financial advice. You should always do your own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

If you enjoyed this post, please link to it on your own blog or social media:

I’ll begin as usual with my JP Morgan Personal Investing (previously Nutmeg) Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

As regular readers will know, in June last year I transferred most of the money in my former Nutmeg Fully Managed portfolio (just under £25,000) to a new Nutmeg Income Portfolio. I discussed this in detail in this post, but basically money in this port is invested to generate an income from share dividends and other sources. This is then paid monthly. Capital appreciation is targeted as well, but these portfolios are aimed primarily at older people (and others) who want/need their investment to generate a regular cash income.

In January my JPM Investing income portfolio generated £75.54 of income, which was duly paid in to my bank account on 24 March 2026. That means I have now received tax-free income of £273.68 in 2026 and a total of £745.14 since I opened the account in June last year. That’s about what I would have expected based on JPM’s projected annual return of just under 5% for income ports at my chosen risk level (five).

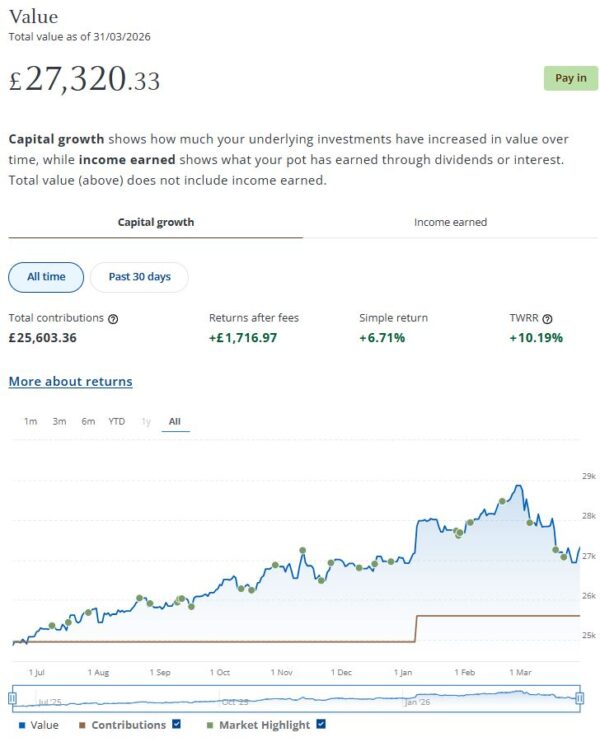

The less good news is that my income portfolio declined in value in March. It’s now worth £27,320 compared with £28,866 at the start of last month, a fall of £1,546. You don’t need to be an investment expert to know that this is mainly due to events in the Middle East. Nearly all of my share-based investments have been affected by this. Clearly it is disappointing, but as I always say, you do have to expect ups and downs when investing. As the screen capture below shows, my income port is still up by a respectable £1,716.97 (6.71%) after fees since I opened it last June.

I still have a smaller, growth-oriented pot using JPM Investing’s Smart Alpha option. This is now worth £4,606 compared with £4,974 (rounded up) a month ago, a fall of £368. Here is a screen capture showing performance over the last year.

Finally, at the start of December 2023 I invested £500 in one of Nutmeg/JPM’s thematic portfolios (Resource Transformation). In March 2024 I also invested a further £200 from referral bonuses (something I no longer receive). As you can see from the one-year screen capture below, this portfolio is now worth £934 compared with £996 (rounded up) last month, a decrease of £62.

Overall in March the value of my JPM investments fell by £1,976 or 5.55%. Against that I did, of course, receive £75.54 in income from my income portfolio. In total, then, I am £1900.46 down for the month.

On a more positive note, excluding income generated, the overall value of my JPM investments is still up by £3,385 or 11.47% since the start of April 2025. If you add to this figure the £745.14 of income generated by my Income portfolio to date, that gives a total profit for the last 12 months of £4,130.14 – still not a bad return in these uncertain times.

As I said above, some volatility is always to be expected with stock market investments, but in the longer term they tend to even themselves out (and typically outperform bank savings accounts, although that is never guaranteed). In general the worst thing you can do is panic and sell up when downturns occur (as happened last month). You are then crystallizing your losses rather than giving the markets time to recover. This is something I discussed last year in this blog post. Obviously nobody knows what will happen in the Middle East, but hopefully some sort of resolution will occur soon, if only because President Trump desperately needs an exit strategy to pacify his critics back home. Once a bit more stability returns to the region, we will hopefully see world stock markets rise again. Though of course there is no guarantee about this.

You can read my full original Nutmeg/JPM review here. If you are looking for a home for your annual ISA allowance, based on my overall experience over the last nine years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs), Lifetime ISAs and Junior ISAs as well.

Moving on, I also have investments with P2P property investment platform Housemartin. As discussed in this post, the company rebranded last year from Assetz Exchange.

My investments with Housemartin continue to generate steady returns. Housemartin focuses on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my HM portfolio has generated a respectable £309.64 in revenue from rental income. I have made a small net loss of £20.25 on property disposals. Capital growth generally has slowed, in line with UK property values generally.

At the time of writing, 17 of ‘my’ properties are showing gains, 3 are breaking even, and the remaining 24 are showing losses. My portfolio of 44 properties is currently showing a net decrease in value of £76.05. That means that overall (rental income minus capital value decrease and loss on disposal) I am up by £213.34. That’s still a respectable return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Housemartin most projects are socially beneficial as well.

A further consideration is that property investments on Housemartin are less likely to be affected by stock market downturns, as happened in March due to the war in the Middle East. This again demonstrates the potential value of such investments for diversifying your portfolio during challenging times.

The net fall in capital value of my Housemartin investments is obviously a little disappointing. But it’s important to remember that until/unless I choose to sell the investments in question, it is largely theoretical, based on the latest price at which shares in the property concerned have changed hands. The rental income, on the other hand, is real money (which in my case I’ve reinvested in other HM projects to further diversify my portfolio).

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of Housemartin as far as i am concerned. You can actually invest from as little as £1 per property if you really want to proceed cautiously.

As I noted in this blog post, Housemartin is particularly good if you want to compound your returns by reinvesting rental income. This effectively boosts the interest rate you are receiving. Personally, once I have accrued a minimum of £10 in rental payments, I usually reinvest this money in either a new HM project or one I have already invested in (thus increasing my holding). Over time, even if I don’t invest any more capital, this will ensure my investment with Housemartin grows at an accelerating rate and becomes more diversified as well.

In 2022 I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios, Oil Worldwide. I also invested a small amount I had left over in Tesla shares.

In January this year, as Oil Worldwide hadn’t exactly been setting the world alight, I decided to switch my entire investment in this to another smart portfolio, InTheGame. This port, focusing on the computer gaming industry, has been the top performer for some time in my eToro virtual portfolio.

Unfortunately just as I switched away from Oil Worldwide, President Trump decided to invade Venezuela. This gave the oil industry a significant boost, which I would otherwise have benefited from. Meanwhile InTheGame has gone south, partly due to the recent fall in AI stocks along with the war in the Middle East. At the time of writing the value of my investment in this has fallen by nearly 17%. Hey ho! This does of course demonstrate that there are never any guarantees when investing and unexpected events can thwart the best-laid plans…

As you can see from the screen captures below, my original eToro investment (total value £888.36 in pounds sterling) is today worth £1,070.78, an overall increase of £182.42 or 20.53%.

Note: eToro now displays the value of investments in your native currency, although you can change this if you wish.

As mentioned above, my new investment in InTheGame is currently down by nearly 17%. My copy trading investment with Aukie2008 also fell in value in March, but it’s still showing an impressive overall profit of 56.36%. Of course, I have held this investment for quite a bit longer.

My Tesla shares, which I purchased as an afterthought with some spare cash I had in my account, are also down this month, but still showing an overall profit of over 234% since I bought them. If only I had put a bit more money into this!

You might also notice that I have small holdings in Prosus NV, a Dutch internet group, and South Bow, a Canadian energy infrastructure company. To be honest I don’t understand how I acquired these, but I assume they are some sort of bonus I was awarded. In any event, I am happy to have them in my portfolio.

If you would like more information about setting up an eToro account, please click on this no-obligation website link [affiliate]. Don’t forget that you also get a free $100,000 virtual portfolio, which you can use to experiment with trading and investing strategies. I have certainly earned a lot from mine.

As an experiment, at the start of April last year I put £50 into an investment ISA with Trading 212. As mentioned in my blog post about dividend investing, I put it into the (Almost) Daily Dividends Portfolio, a ready-made portfolio or ‘pie’ on Trading 212. As you can see from the screen capture below, my portfolio is now worth £59.87. That’s a decrease of £1.97 since last month but an increase of £9.87 or 19.7% over the eleven-month period since I opened it. It has even accrued a grand total of £1.08 in dividends, most of which has now been (automatically) reinvested.

I am quite impressed with how this investment has been faring, despite the small amount I put in (which means I may be missing out on some smaller dividends). If I increased my investment I would almost certainly become eligible for more dividends, and even more the longer I remain invested. If I had any spare money at the moment, I would consider doing this. Of course, I do now have an income-focused portfolio with JPM Investing as well (see above).

Moving on, I published various posts on Pounds and Sense in March. I have listed below those that are still relevant.

In Beat the Postage Stamp Price Rise, I pointed out that the cost of stamps is rising (again) on Tuesday 7 April 2026. That will be the SEVENTH rise in the price of first class stamps in just four years! Standard and large-letter stamps don’t have values printed on them and will still be valid after the April price rise comes in, so my top tip is to stock up now while stamps are still at the old price.

I also posted an updated version of Get a Free Share Worth up to £100 with Trading 212. Anyone who hasn’t done this before can get a free share worth up to £100 just by signing up for a new Trading 212 investment account via my link. The current offer closes on Tuesday 28th April 2026.

Also in March I published Are River Cruises Suitable for Solo Travellers. This was a follow-up to my earlier posts about how to save money on cruise holidays and the pros and cons of river cruises (for older travellers in particular). In this post I addressed a question asked by several readers as to whether river cruises are a good choice for solo travellers. The article sets out the pros and cons as I see them. My view, as expressed in the article, is that they can be, but it does depend on your travel style and budget.

What Is An Annuity – And Who Should Consider Buying One? discusses a subject that confuses many people. In simple terms, an annuity is a financial product that converts a lump sum of money – typically from your pension pot – into a guaranteed regular income for life (or for a fixed period). You buy an annuity from an insurance company. In return for handing over some or all of your pension savings, they promise to pay you a regular income, usually monthly, for the rest of your life. In the article I look at the pros and cons of annuities, and whom they are (and aren’t) likely to be suitable for.

How to Save Money on Travel Insurance covers a subject on many people’s minds at this time of year. Travel insurance is one of those expenses that can feel like a grudge purchase – until you need it. For UK travellers, especially older holidaymakers, having adequate cover is essential. In this article I set out some ways you may be able to save on travel insurance without compromising your safety or security. I also discuss saving money on travel insurance as an older person, and the issues that can be caused by war and civil unrest (especially relevant for destinations in or near the Middle East at the moment).

Finally, in March I published Don’t Miss Out – Use Your £20,000 ISA Allowance Before It’s Too Late! As I say in the article, the end of the tax year on 5 April 2026 is fast approaching and so is the deadline to utilize the annual tax-free Individual Savings Account (ISA) allowance. Unless you take action in the next few days, this opportunity to maximize your tax-free savings for the 2025/26 financial year will be gone for ever.

And speaking of deadlines, time is also running out to take advantage of EDF Energy‘s enhanced switching offer. Until 6 April 2026 you can get a FREE £75 (increased from £50) credited to your energy account when you switch to EDF via my link at https://edfenergy.com/quote/refer-a-friend/sunny-koala-9462. Terms and conditions apply.

I’ll close with my customary reminder that you can also follow Pounds and Sense on Facebook or Twitter (or X as it is now). Twitter/X is my number one social media platform and I post regularly there. I share the latest news and information on financial matters, and other things that interest, amuse or concern me. So if you aren’t following my PAS account on Twitter/X, you are definitely missing out!

I am also on the BlueSky social media network under the username poundsandsense.bsky.social. Twitter/X remains my primary social media platform, but I also post details of my latest blog posts, third-party articles and other financial news and resources on BlueSky for those who prefer to follow me there.

As always, if you have any comments or questions, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts on PAS may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media:

Today I’m featuring a way you can get a free fractional share worth up to £100 by signing up (for the first time) with an online share trading platform called Trading 212.

Trading 212 is unusual in that it offers commission-free and fee-free share trading. As a special offer, until Tuesday 28th April 2026 they are offering people new to the platform a free fractional share just for signing up via a referral link (such as the links in this post). The share you will get is chosen at random, but could be worth up to £100. You can either keep this share or sell it.

How to Sign Up

Signing up with Trading 212 is pretty straightforward. Just visit the Trading 212 website via any of the (referral) links in this post and follow the on-screen instructions to register. Note that you will be required to provide various items of information, including your date of birth, National Insurance number, annual income, employment status, and contact details. I understand that this is to meet their legal ‘Know Your Customer’ duty.

You will also need to indicate the type of account you want from the options available (see screen capture below).

As you will see, the four account types on Trading 212 are Invest, CFD, Stocks ISA and Cash ISA. You can apply for any or all of these if you like.

CFD stands for Contract for Difference. CFDs are quite complex financial instruments and unless you know what you’re doing I recommend giving them a miss.

If you just want the free share my suggestion would be to tick the Stocks ISA box. An ISA is, of course, a tax-exempt Individual Savings Account. As from April 2024 you can open any number of ISA accounts in a year as long as you don’t exceed your annual £20,000 allowance.

If you have already used up your entire £20,000 this year, you should choose Invest instead to open a general investment account without any tax benefits. Obviously if you don’t want a Stocks ISA with Trading 212 for any reason, you can choose this option as well.

For more information about the Trading 212 Cash ISA, see my review here. Be aware that you must open either an Invest account or a Stocks ISA account to qualify for a free share. Of course, there is nothing to stop you opening a Cash ISA account as well, but my recommendation would be to open an Invest or Stocks ISA account first.

Getting Your Free Share

There is one more step you will need to take in order to get your free share. You will need to deposit a minimum of £1 into your account. There are various ways you can do this, but i just used my debit card. There is no obligation to invest the £1 (or whatever you choose to deposit) and if you wish you can withdraw it once your free share has been credited.

The next business day you should receive an email confirming that a free fractional share has been added to your account. As mentioned above, this is allotted at random. If you’re lucky you might get one worth up to £100. Even if you get a less valuable one, though, it’s still a share for free. If you choose to keep it, it may rise in value. There may also be dividends payable in future (and credited to your account).

Selling Your Share

You can’t sell your share immediately. You have to wait three business days before doing so, but it is then just a matter of clicking the Sell button on your member’s dashboard.

The money will be credited to your Trading 212 account but you will have to wait 30 days before withdrawing it. So there may be a case for waiting to see if your share’s value goes up in that time. Of course, it could also go down!

In my case, I received a free share in the Ford Motor Company worth just under £8 at the time. Obviously this wasn’t as exciting as I might have hoped, but it was still – in effect – free money for almost no time or effort 😀

How Safe Is Trading 212?

Trading 212 is registered in England and Wales and authorized and regulated by the Financial Conduct Authority. In addition, all clients’ funds are kept separately in segregated bank accounts which are covered by the Financial Services Compensation Scheme. So even if the company itself were to go broke, any cash in your account would be protected up to a value of £120,000.

Of course, the FSCS guarantee doesn’t apply to the value of your stocks and shares, which can go down as well as up. All investments carry a risk of loss, although in the case of your free share you can never lose any more than the original cost, which was of course zero!

Referral Scheme

Any Trading 212 member can also refer new members while this offer is on. In that case, both you and the person concerned will receive one free fractional share worth up to £100. Obviously, the links in this blog post include my referral code – so if you register and get a free share, I will receive one also. Under the terms of the current offer you can get up to five free shares in this way. Five is the limit per person. Although you can still refer new members who will get a free share after this, as a referrer you won’t receive one as well. If and when the offer reopens in future, you will be able to refer more new members and get free shares again.

Final Thoughts

I first heard about Trading 212 a while ago, but wasn’t initially sure whether it was legit and here for the long term. And I thought the free share offer was, frankly, too good to be true. However, my own experiences have been entirely positive. My original free share in the Ford Motor Company was credited the next business day as promised and I received an email notifying me about it.

I can log in to my Trading 212 account any time to see how my Ford share is doing. I have also collected a few other shares from referrals. These include a share in AMD (the semiconductor company), which is currently worth an impressive £152.69, and one in Nike, which is worth £72.48. I still have my original Ford Motor Company share and it has risen in value to £8.75. I have also received several dividend payments from them. I haven’t sold any of my free shares yet but could of course do so any time I choose. I am not in any rush, as Trading 212 do not impose any platform or inactivity fees.

Although in this post I have focused on the free share offer, Trading 212 is worth considering as a share-dealing platform too. In particular, the fact that it’s fee-free and commission-free means it is well suited for people who are dipping a toe in stocks and shares investment for the first time. By contrast, the dealing fees and commissions charged by some other share-trading platforms can make small share purchases prohibitively expensive. This review by Money Savvy Daddy looks at the pros and cons of Trading 212 as a share-dealing platform in a bit more detail.

It’s also worth bearing in mind that Trading 212 pays interest on any uninvested funds in your ISA or Invest account, currently at a rate of 3.80% AER. You can also make money allowing your shares to be lent out. Rates on offer for this vary according to investor demand, with the process handled automatically by Trading 212 once authorized. You can read more about share lending on Trading 212, including the risks and safeguards provided, here.

In conclusion, I hope this post has inspired you to consider registering with Trading 212 to claim your free share. If you do, I hope you get a valuable one! Please let me know what share you receive in a comment below. And, as always, any other comments or questions are very welcome too.

Don’t forget, the current free share offer ends on Tuesday 28th April 2026.

Disclosure: The links in this post include my referral code. If you click through and register as described above, I will receive a free share (as will you). Please note also that I am not a qualified financial adviser and nothing in this post should be construed as individual financial advice. Everyone should do their own ‘due diligence’ before investing and seek advice from a qualified financial adviser if in any doubt how best to proceed. All investment carries a risk of loss (although not in the case of free shares, obviously).

This is an update of my original post about this special offer.

If you enjoyed this post, please link to it on your own blog or social media:

As we reach the end of a long, cold winter, many people’s thoughts are turning to holidays. And that makes the topic of travel insurance a lot more relevant – in these uncertain times especially.

Travel insurance is one of those expenses that can feel like a grudge purchase – until you need it. For UK travellers, especially older holidaymakers, having adequate cover is essential. The good news is that there are plenty of ways to keep costs down without cutting corners on protection.

Here are some practical strategies to help you save money on travel insurance while still getting the cover you need.

Money Saving Strategies

1. Shop Around and Compare Policies

Prices can vary significantly between insurers for broadly similar cover. Using comparison sites such as Compare the Market, MoneySuperMarket, and GoCompare can quickly highlight the best-value options.

However, don’t rely solely on comparison sites. It’s also worth checking insurers directly, including Aviva and Staysure, as they sometimes offer exclusive deals.

2. Consider an Annual Multi-Trip Policy

If you take more than one trip a year, an annual (multi-trip) policy can be far cheaper than buying single-trip cover each time.

As a rough guide:

Two or three holidays a year can make an annual policy worthwhile

Frequent travellers can save substantially over time

Just ensure the policy covers the length of your longest trip, as many impose limits (e.g. 31 or 45 days per trip).

3. Only Pay for the Cover You Need

Policies often include extras that you may not require. Common add-ons include:

Gadget cover

Winter sports cover

Cruise cover

If these aren’t relevant, opt out. For example, if you’re taking a simple European city break, you likely don’t need winter sports or high-value gadget protection.

4. Check Existing Cover First

You may already have some level of travel insurance included with:

Packaged bank accounts

Credit cards

Membership organisations

For instance, some premium current accounts from Nationwide Building Society or HSBC include travel insurance as a perk.

That said, always read the small print carefully – cover levels, age limits, and exclusions may apply.

5. Increase the Excess (Carefully)

Choosing a higher excess (the amount you pay towards a claim) can reduce your premium.

For example:

£50 excess → higher premium

£150 excess → lower premium

This can be a sensible way to save money if you’re unlikely to make small claims. However, ensure the excess remains affordable if you do need to claim.

6. Be Honest About Medical Conditions

Failing to declare pre-existing medical conditions can invalidate your policy entirely.

Specialist insurers like AllClear Travel Insurance and Saga cater specifically to older travellers and those with medical histories.

While premiums may be higher, proper disclosure ensures you are fully covered – potentially saving thousands if something goes wrong.

7. Use the GHIC Card

UK residents can apply for a Global Health Insurance Card (GHIC), which provides access to state healthcare in EU countries and some others at reduced cost or sometimes free.

This won’t replace travel insurance, but it can reduce the level of medical cover you need – and may lower your premium slightly.

8. Travel Less Often? Consider Single-Trip Cover

If you only travel once a year, a single-trip policy is usually cheaper than an annual one.

You can also tailor it closely to your itinerary, ensuring you don’t pay for unnecessary cover.

9. Book Early – but Not Too Early

Buying insurance as soon as you book your trip is usually best. This ensures you’re covered for cancellation from day one.

However, prices can fluctuate, so it’s worth checking a few providers before committing rather than simply accepting the first quote offered.

Even modest savings of £10–£20 can add up over time.

Saving as an Older Traveller

Travel insurance tends to become more expensive as you get older, but there are still ways to keep costs under control without sacrificing essential cover.

One of the main issues older travellers face is higher premiums due to increased medical risk. Insurers often apply age bands, and prices can rise quite sharply once you reach your late 60s or 70s. In addition, pre-existing medical conditions – more common in later life – can further increase the cost or limit the number of insurers willing to provide cover.

Some mainstream providers also impose upper age limits, particularly on annual policies, which can restrict your options. This is where specialist insurers such as Saga and Staysure can be especially valuable, as they are geared towards older customers and often have no upper age limit.

To manage costs, it’s worth considering the following approaches:

Compare specialist providers: Companies focusing on older travellers may offer better value than standard insurers.

Tailor your cover carefully: Avoid unnecessary add-ons, but don’t skimp on medical cover, which is the most important element.

Consider single-trip policies: These can sometimes work out cheaper than annual cover for older travellers, particularly if you only take one holiday a year.

Get medical screening right: Providing accurate and detailed information can help avoid inflated premiums and ensures valid cover.

Travel within Europe where possible: Premiums are typically lower than for worldwide cover, especially when combined with a Global Health Insurance Card (GHIC).

While costs may be higher, careful shopping around and using specialist providers can make travel insurance much more affordable in retirement – allowing you to travel with confidence and peace of mind.

Travel Insurance and Wars

The ongoing conflict in parts of the Middle East is a reminder that global events can have a direct impact on your travel insurance – sometimes in ways that aren’t immediately obvious.

One key point is that most standard travel insurance policies exclude claims arising from war, military action or civil unrest. This means that disruption caused directly by the conflict – such as flight cancellations, airspace closures, or evacuations – may not be covered.

In addition, insurers often treat major conflicts as a “known event” once they are widely reported. If you buy a policy after this point, it’s unlikely to cover any claims related to that situation.

Another crucial issue is official government advice. The UK Foreign, Commonwealth & Development Office (FCDO) regularly updates its guidance for travellers. If it advises against travel to a destination (or all but essential travel), your insurance may be invalidated if you still choose to go.

Where plans are already in place, cover may depend on timing and policy wording. Some insurers will allow cancellation claims if FCDO advice changes after you have booked, but this is not guaranteed and varies between providers. Read your policy wording carefully, especially exclusions relating to war and unrest, and contact your insurer directly if travelling anywhere near affected regions.

The overall message is clear: if you are considering travel to, or even near, areas affected by conflict, proceed with caution. Insurance protection may be limited, and official advice should be taken seriously – not just for financial reasons, but for your personal safety as well.

Final Thoughts

Saving money on travel insurance isn’t about choosing the cheapest policy – it’s about finding the best value for your circumstances. For older travellers in particular, ensuring adequate medical cover should always be the priority.

By comparing providers, tailoring your cover, and making use of existing benefits, you can often reduce costs significantly without compromising on safety or protection.

As always, if you have any comments or questions about this post, please do leave them below. I am always delighted to hear from PAS readers.

If you enjoyed this post, please link to it on your own blog or social media:

As the end of the tax year on 5 April 2026 approaches, so too does the deadline to utilize the annual tax-free Individual Savings Account (ISA) allowance.

The clock is ticking, and unless you take action in the next few weeks, this opportunity to maximize your tax-free savings for the 2025/26 financial year will be gone.

ISAs are a popular choice for savers and investors alike, offering a tax-efficient way to grow your wealth. With a diverse range of options available, from cash ISAs to stocks and shares ISAs and innovative finance ISAs, individuals have the flexibility to tailor their savings strategy to suit their financial goals and risk appetite.

The current ISA allowance stands at £20,000, providing a significant opportunity to shield your savings and investments from tax. This allowance represents a generous sum that, if left unused, cannot be carried forward to future years. In essence, any portion of the £20,000 allowance that remains untapped by the upcoming deadline will be lost, representing a missed opportunity for tax-free growth.

For those who have yet to fully utilize their annual ISA allowance, now is the time to take action. Whether you’re looking to bolster your rainy-day fund with a cash ISA, seeking to invest in the stock market through a stocks and shares ISA, or diversify your investment portfolio with an IFISA, there’s no shortage of options available.

Cash ISAs offer a secure and accessible way to save, providing a tax-free environment for your savings with the added benefit of easy access to your funds when needed. Meanwhile, stocks and shares ISAs open the door to potentially higher returns by investing in a wide range of assets such as equities, bonds and funds, albeit with a higher level of risk. And an Innovative Finance ISA, or IFISA for short, allows you to invest via P2P/crowdfunding platforms, further diversifying your portfolio (though again with a higher level of risk).

With an ISA you will never incur any liability for dividend tax, capital gains tax or income tax, even if your investments perform exceptionally well. Of course, there is no guarantee this will happen, but over a longer period stock market investments have typically outperformed cash savings, often by a substantial margin.

In recent years I have invested much of my own annual ISA allowance in a stocks and shares ISA with JP Morgan Personal Investing (formerly Nutmeg). I have also invested some money in a property IFISA from Housemartin (previously Assetz Exchange). Check out the Housemartin website here [affiliate link].

Finally, for shorter-term savings, I am using the Trading 212 Cash ISA. This currently pays me an interest rate of 3.60% AER. Higher rates are typically on offer to new Trading 212 clients for their first 12 months.

Note that from April 2027 the Cash ISA allowance has been reduced from £20,000 to £12,000 per year for savers under the age of 65. Until then it remains at £20,000 a year for all savers, though.

With just a few weeks left to take advantage of this valuable tax benefit, delaying now could prove costly. By acting swiftly you can ensure that your savings and investments are positioned to grow tax-free, setting yourself up for a better financial future.

In summary, the £20,000 annual ISA allowance for the 2025/26 tax year presents a golden opportunity to maximize your tax-free savings and investments. Time is of the essence, though. Unless you act before the looming deadline of 5th April 2026, this valuable allowance will be lost forever. If you have the money available, therefore, seize the opportunity now to help secure your financial future.

As always, if you have any comments or questions about this article, please feel free to leave them below.

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.