What Are Investment Trusts and How Can You Invest in Them?

When most people think about investing, they picture stocks and shares, funds, ISAs and perhaps ETFs. But there’s another long-established option that often flies under the radar: Investment Trusts.

Despite the name, investment trusts aren’t trusts in the everyday sense. They are a distinctive type of investment company with some unique features – and for the right investor, they can offer real advantages.

In this article, I’ll explain what investment trusts are, how they work, and their pros and cons compared with alternatives such as ETFs and open-ended funds.

Table of Contents

What Is an Investment Trust?

An investment trust is a publicly listed company whose business is investing in other assets. These might include:

-

shares in UK or overseas companies

-

bonds and other fixed-interest investments

-

property or infrastructure projects

-

specialist assets such as private equity or renewable energy

When you invest in an investment trust, you’re buying shares in the company, not units in a fund. Investment trusts are listed on the London Stock Exchange, and their shares are bought and sold in the same way as any other quoted company.

Importantly, most investment trusts are actively managed, with a professional fund manager making decisions about what to buy and sell.

How Investment Trusts Differ from Funds and ETFs

The key difference lies in structure.

Closed-Ended Structure

Investment trusts have a fixed number of shares in issue. This means:

-

The manager does not need to sell assets to meet investor withdrawals.

-

The trust can take a long-term view and invest in less liquid assets.

By contrast, open-ended funds and ETFs create or cancel units as investors buy and sell.

Share Price vs Net Asset Value (NAV)

Because investment trusts trade on the stock market, their share price is driven by supply and demand. This means shares can trade:

-

At a discount to the value of the underlying assets (NAV)

-

At a premium to NAV

This feature can create opportunities – but also risks – for investors.

The Advantages of Investment Trusts

Potential to Buy Assets at a Discount

One of the biggest attractions is the ability to buy shares below NAV. In simple terms, you may be able to buy £1 of assets for 90p (or less).

Discounts can widen in difficult markets, potentially offering long-term investors attractive entry points.

Gearing (Borrowing to Invest)

Investment trusts are allowed to borrow money to invest, known as gearing.

-

Used well, gearing can enhance long-term returns

-

Used poorly, it can magnify losses

This makes investment trusts potentially more volatile than ETFs or open-ended funds.

Strong Income Records

Many UK investment trusts aim to provide a reliable and growing income.

Crucially, they can retain income in good years and use reserves to maintain or increase dividends in tougher times – something open-ended funds are not permitted to do.

Some UK equity income investment trusts have raised their dividends for decades.

Access to Specialist Assets

Because managers don’t have to meet daily redemptions, investment trusts can invest in:

-

infrastructure and renewable energy

-

private equity

-

property and specialist debt

These areas are often harder to access via ETFs.

Can Be Held in Tax-Free Wrappers

Most investment trusts can be held within tax-free SIPPs and stocks and shares ISAs. That means no tax is payable on income generated or capital growth.

The Disadvantages of Investment Trusts

Discounts Can Persist

While buying at a discount sounds attractive, there’s no guarantee it will narrow. Some trusts trade at persistent discounts for years.

Higher Volatility

The combination of share price movements, discounts and gearing can make investment trusts more volatile than ETFs tracking an index.

Active Management Risk

Most investment trusts rely on the skill of a fund manager. If the manager under-performs, returns may lag cheaper passive options.

Complexity

Compared with a simple FTSE 100 ETF, investment trusts require more understanding – particularly around discounts, premiums and gearing.

Investment Trusts vs ETFs: A Quick Comparison

| Feature | Investment Trusts | ETFs |

|---|---|---|

| Structure | Closed-ended company | Open-ended fund |

| Management | Usually active | Usually passive |

| Can use gearing | Yes | Rarely |

| Price vs NAV | Can trade at discount/premium | Very close to NAV |

| Income smoothing | Yes | No |

| Costs | Often higher | Usually low |

How Can You Invest in Investment Trusts?

You can buy investment trusts through most UK investment platforms, including:

-

Stocks and Shares ISAs

-

SIPPs (Self-Invested Personal Pensions)

-

dealing accounts

They trade just like shares, so you’ll usually pay a dealing fee when buying or selling.

Before investing, it’s wise to check:

-

the trust’s long-term performance

-

ongoing charges

-

gearing policy

-

dividend history

-

whether shares trade at a discount or premium

Are Investment Trusts Right for You?

Investment trusts aren’t for everyone. If you prefer:

-

low costs

-

simple, passive investing

-

minimal volatility

…then ETFs or index funds may be more suitable.

However, for investors willing to do a bit more research, investment trusts can offer:

-

attractive income

-

exposure to specialist assets

-

the chance to buy quality investments at a discount

As always, diversification matters – and investment trusts are best viewed as part of a broader, well-balanced portfolio.

UK Investment Trust Examples

Investment trusts cover a wide range of strategies and sectors, from global growth to income to specialist themes like biotech or renewable energy. Here are some well-known UK trusts across different categories to help bring the concept to life.

📊 Global Growth & Broad Equity

-

Scottish Mortgage Investment Trust (LSE: SMT) – One of the largest and most popular UK investment trusts. It invests globally with a growth-oriented portfolio that includes technology and disruptive companies. It frequently tops the most-bought lists among UK investors.

-

Alliance Witan – A large diversified global trust formed from the merger of Alliance Trust and Witan, offering broad exposure across markets.

-

Baillie Gifford US Growth Trust – Focuses on growing companies based in the United States, blending listed and (up to a limit of) unlisted holdings.

💰 Income-Focused Trusts

-

City of London Investment Trust (LSE: CTY) – A classic UK equity income trust with a long record of increasing dividends year-on-year.

-

JPMorgan Global Growth & Income – Offers a diversified global equity income strategy that regularly features among popular income trusts.

-

Murray International Trust – Another long-running global equity income trust often favoured for income within ISAs.

🌍 Regional & Sector-Specific Trusts

-

Schroder AsiaPacific Fund – Provides exposure to companies across Asia and Asia-Pacific regions (excluding Japan and Australasia).

-

BlackRock Smaller Companies Trust – Focuses on smaller company equities, often with a value or growth tilt.

-

RTW Biotech Opportunities – A sector-specific trust investing in biotechnology companies at various stages of development.

🔋 Other Interesting Themes

-

Greencoat UK Wind (LSE: UKW) – A renewable energy trust investing in UK wind assets. It’s popular among investors seeking income from alternative infrastructure, though returns can be more cyclical.

-

3i Group – A private equity–focused investment trust with a long track record and often high longer-term returns, though returns may be more volatile.

These examples are not recommendations – just familiar names that illustrate how diverse the investment trust world can be, from broad global strategies to niche sectors like biotech or renewables. Always do your own research (including yield, fees, discount/premium and underlying strategy) before investing.

My Own Trust Investments

Finally, I thought it might be of interest to mention the trusts I invest in myself. Again, I must emphasize that this in no way intended as a recommendation; it is for information purposes only.

I don’t have a lot of money in investment trusts these days, as they are a bit too volatile for my current circumstances and overall investing strategy. But in my Bestinvest SIPP (personal pension) I do hold the following…

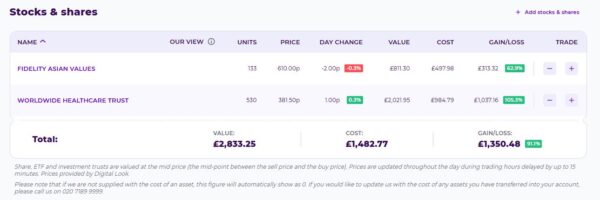

As you can see, I have shares in Fidelity Asian Values and Worldwide Healthcare Trust.

Both these trusts have done well for me, the latter in particular. I chose WHT because I wanted to put some of my pension money into the health sector. That is partly because I expect this sector to perform well as populations – in advanced industrial nations anyway – grow older. But it’s also because I like to think that some of my money may actually help drive advances in medicine/healthcare generally.

I invested in Fidelity Asian Values as my overall portfolio was a bit light on stocks from that region (and also, if I’m honest, because I saw this trust recommended on one of the investment news websites I follow!).

As always, if you have any comments or questions about this article, please do post them below. But bear in mind that I am not a qualified financial adviser and cannot give personal financial advice. All investment carries a risk of loss and past performance is no guarantee of future profits. You should always do your own “due diligence” before investing, and seek advice from a professional financial adviser/planner if in any doubt how best to proceed.