As you will doubtless know, yesterday the Chancellor delivered his 2023 Autumn Statement. This included various economic measures, which you can read about on the Moneysaving Expert website (among other places).

I thought today I would highlight one particular change to the rules about tax-free ISAs (Individual Savings Accounts) which caught my eye. From April 2024, you will be allowed to open more than one of any particular type of ISA in a single tax year. This is a change I was particularly pleased to see, and have in fact been advocating on Pounds and Sense for some time.

As you may know, there are various types of ISA, including the stocks and shares ISA, cash ISA and IFISA. The latter stands for Innovative Finance ISA and allows people to save tax-free with peer-to-peer lending and similar platforms. Everyone has an annual tax-free ISA allowance, which currently stands at £20,000. Despite rumours to the contrary, this limit was not changed in the Autumn Statement.

So why do I think the change in the rules announced yesterday is so important? Well, for one thing, it brings about much greater flexibility in ISA transfers. Investors will now be able to transfer funds freely between different types of ISA without jeopardizing their tax-free status. They will also be able to transfer just part of a holding to a different provider, regardless of when they paid in the money.

This will empower investors to optimize their investment strategy by making it easy to move money between cash, stocks and shares, and Innovative Finance ISAs. This enhanced transfer flexibility should enable investors to adapt to changing market conditions, seize new opportunities, and align their portfolios with their evolving financial goals.

A further benefit of the rule change is that it will make it easier for investors to build a well-diversified portfolio. Rather than having to put all their money into just one stocks and shares ISA per year (for example) they can divide it among a range of providers. Regular readers will know that I am a big fan of diversifying your portfolio as much as possible to help manage risk, and this rule change certainly facilitates that.

The change will also make it easier for investors to try out new platforms with relatively small investments initially. Previously they may have been deterred from doing this by the realization that once they had committed to one particular provider, they would have to stick with that provider for the rest of the financial year. FOMO (fear of missing out) may even have inhibited some people from investing at all.

This is certainly something I’ve experienced myself. At the start of a new financial year, I was wary of investing in any type of ISA, because I knew that once I did so, I would then have to stick with that provider for that type of ISA for the rest of the financial year.

So those are just some reasons I particularly welcome this rule change. From a broader perspective, I think it will also encourage more people to start investing, which has to be good for UK PLC in general. Apart from a few admin costs, it seems to me this measure will cost the government nothing, while bringing major benefits to the economy and individual investors. Really, the only thing I don’t understand is why it wasn’t done sooner!

So those are my thoughts anyway. But what do you think? Will the new rule encourage you to make more use of ISAs in future? I’d be interested to hear any views.

If you enjoyed this post, please link to it on your own blog or social media:

According to the government’s own figures, around a third of retirees who would be entitled to this state benefit aren’t currently claiming it. That means they are potentially missing out on an important boost to their pension.

Even more significantly, it means they may be missing out on a raft of other benefits and discounts too, for which pension credit acts as a gateway. More about this shortly.

Applying for pension credit is especially crucial for people who reached retirement age before April 2016 and therefore receive the old basic state pension rather than the new (higher) one. While it may seem (and indeed be) unfair that older pensioners receive a lower rate, they do have the opportunity to claim the savings credit element of pension credit, which newer retirees don’t.

Savings credit payments can provide an extra boost to your income and entitle you to other payments and benefits as well. And, very importantly, the eligibility rules are different from guarantee credit and (in my view anyway) a bit less stringent. But if you don’t apply for pension credit, you won’t get either.

But before we get into that, let’s recap on what pension credit is.

What is Pension Credit?

Pension credit is a state benefit that comes in two parts: guarantee credit and savings credit.

Guarantee credit boosts your weekly income to £182.60 if you’re single or £278.70 if you’re a couple (figures correct from 6 April 2023). You should be eligible for guarantee credit if you have reached state pension age and your total income is less than these amounts (even if you own your own home).

If you have under £10,000 in savings and investments this will not be taken into consideration. If you have over £10,000, it will be assumed that you earn £1 a week per £500 of savings and investments. This will be added to your total income when working out your eligibility for guarantee credit.

Savings credit is only available to people who reached the state pension age before 6 April 2016. It is meant as a reward for those who have made some additional provision for their retirement. It’s worth up to £15.94 a week for a single person or £17.84 for couples (2023/24 figures). Somewhat counter-intuitively, to qualify you must have a minimum income of £174.49 a week if you’re single and £277.12 a week for a couple (again 2023/24 figures). You must also have some savings or other extra income provision (e.g. a private pension).

It’s worth adding that if you pay mortgage interest or have other housing costs, have caring responsibilities, are responsible for a child, or are severely disabled, you may be entitled to more pension credit. If you receive attendance allowance or carers credit, for example, this may boost the amount that you’re entitled to.

The rules surrounding all this are complicated, but the government has provided a free online calculator you can use to work out whether you qualify and how much you might get. This is for guidance only, however. You can’t apply via the calculator and there is no guarantee you will receive the amount it shows you.

Until recently to actually apply for pension credit you had to phone the DWP’s pension credit helpline on 0800 991234 with your Nl number, details of your income, savings and investments, and your bank account details. The person you spoke to would then then take you through the application process. This option is still available, but recently an option to apply online has been added. This is quite separate from the free online calculator mentioned above.

As I recently helped an elderly friend do this, I can confirm that the online method works well, though the questions asked don’t entirely correspond with the questions on the free online calculator. But using the latter first should give you an idea whether you are likely to qualify for pension credit and how much you might get. You can also try the effect of changing the amount of capital/income in the calculator to see if you might qualify in future even if you don’t at present (perhaps due to having too much in savings).

Additional Benefits

As well as the money – which can amount to thousands of pounds a year – if you receive pension credit you will be entitled to a range of additional discounts and benefits. These may include:

Even if you only receive a small amount of pension credit, you may be eligible for any of the above. So it really is important to apply if there is any chance you may qualify.

More About Savings Credit

As I said above, only older pensioners who retired before April 2016 can get savings credit. But potentially a lot more people in this category may be eligible for it than is the case with guarantee credit.

Whereas guarantee credit is only paid to pensioners on a low income and with limited savings, that isn’t necessarily the case with savings credit. As I noted above, to qualify for savings credit there is actually a minimum earnings limit. And you do actually need to have some savings (or other income source/s apart from the state pension) to be eligible.

The rules are complicated, so – as I said above – the best thing is to use the free online calculator. If it appears you are eligible for savings credit (or guarantee credit) it will tell you, and how much.

It should be said that if you are only awarded savings credit and not guarantee credit, you may not qualify for all of the extra benefits mentioned above (free NHS dental treatment, for example). But even if, with savings credit only, you don’t qualify for the whole of the discounts mentioned, you may at least be eligible for a partial reduction.

For the latest news and information about pension credit, please click here.

Closing Thoughts

To sum up, if you’re of state pension age and have a limited income or savings, you should certainly look into pension credit. Similarly, if you have elderly friends or relatives, you should check eligibility on their behalf (with their permission, of course).

As I’ve said above, this applies especially to anyone who started receiving the state pension before April 2016 and is therefore getting the old basic state pension. This is lower than the new state pension, but you may potentially be eligible for the savings credit element of pension credit (as well as guarantee credit, which anyone of state pension age can qualify for).

While savings credit is generally only a small amount, receiving it will make you eligible for a range of other discounts and benefits, including (as from winter 2024) Winter Fuel Payments. So it really is well worth checking on the free online calculator and then applying (by phone or online) if it appears you might be eligible.

Finally, you might like to know that (thankfully) my friend’s online application was successful. He got a letter a week later saying that he would be receiving pension credit (savings credit only) at a rate of about £5 a week, rising to just over £6 a week the following April. Naturally he was pleased to hear this. And he was even more pleased when he realised he would be getting the other benefits and discounts mentioned earlier as well. As an 84-year-old man who has recently lost his wife, this will certainly help make life a little more bearable for him.

As always, if you have any comments or questions about this article, please do post them below. Just bear in mind that I am not a qualified financial adviser or benefits adviser and cannot provide personal financial advice. If you require specific advice or assistance, your local Citizens Advice office would be one good place to start.

If you enjoyed this post, please link to it on your own blog or social media:

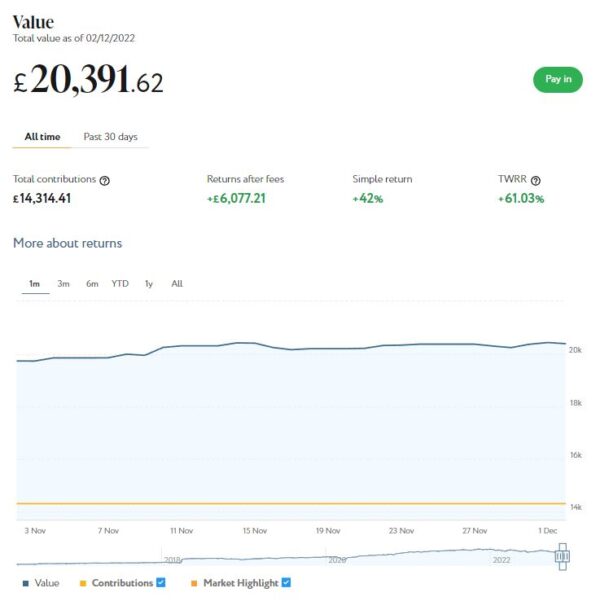

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension). I will discuss the latter a bit further down.

As the screenshot below of performance last month shows, my main Nutmeg portfolio is currently valued at £20,391. Last month it stood at £19,733 so that is a rise of £658.

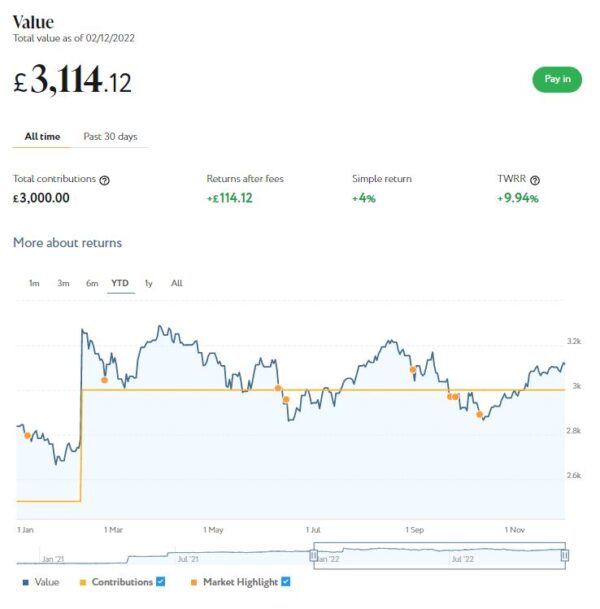

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £3,114 compared with £2,987 a month ago, an increase of £127.

Here is a screen capture showing performance since January 2022. As you can see, I topped up this account in February this year.

That is an overall month-on-month increase of £785. Furthermore since mid-October the total value of my Nutmeg investments has risen by £2,007 or around 8%. Anyone who was brave enough to invest in Nutmeg around the middle of October will therefore be looking at a substantial profit now. Of course, it’s always easy to spot an investment opportunity with 20/20 hindsight!

In my case, while the recent rises are very welcome, my Nutmeg investments are still down £1,607 or about 6.5% since the start of the year. To put this in context, though, in 2021 they rose by £3,552 (over 21%). And overall, I am still over £6,000 ahead since I started investing with Nutmeg in 2016. For my main portfolio that represents a return on capital of 42% or 51.03% time-weighted.

Of course, the real point of this is that investing is (or should be) a long-term endeavour. Over a period of years stock market investments such as those used by Nutmeg typically produce better returns than cash accounts, often by substantial margins. But there are never any guarantees, and in in the short to medium term at least, losses are always possible.

You can read my full Nutmeg review here (including a special offer at the end for PAS readers). If you are looking for a home for your annual ISA allowance, based on my experience over the last six years, they are certainly worth considering.

Moving on, my Assetz Exchange investments continue to perform well. Regular readers will know that this is a P2P property investment platform focusing on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my AE portfolio has generated £88.30 in revenue from rental and £17.59 in capital growth, a total of £105.89. That’s a decent rate of return on my £1,000 investment and does illustrate the value of P2P property investment for diversifying your portfolio when equity markets are volatile.

I now have investments in 23 different projects and all are performing as expected, generating rental income and in most cases showing a profit on capital as well. So I am very happy with how this investment has been doing. And it doesn’t hurt that most projects are socially beneficial as well.

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of AE as far as i am concerned. You can actually invest from as little as 80p per property if you really want to proceed cautiously.

Another property platform I have investments with is Kuflink. They continue to do well, with new projects launching almost every day. I currently have around £2,600 invested with them in 14 different projects. To date I have never lost any money with Kuflink, though some loan terms have been extended once or twice. On the plus side, when this happens additional interest is paid for the period in question. At present most of my Kuflink loans are performing to schedule, though two recently had their repayment dates put back by three months.

My loans with Kuflink pay annual interest rates of 6 to 7.5 percent. These days I invest no more than £200 per loan (and often less). That is not because of any issues with Kuflink but more to do with losses of larger amounts on other P2P property platforms in the past. My days of putting four-figure sums into any single property investment are behind me now!

Nowadays I mainly opt to reinvest the monthly repayments I receive from Kuflink, which has the effect of boosting the percentage rate of return on the projects in question

Obviously a possible drawback with Kuflink and similar platforms is that your money is tied up in bricks and mortar, so not as easily accessible as cash savings or even (to some extent) shares. They do, however, have a secondary market on which you can offer any loan part for sale (as long as the loan in question is performing and not in arrears). Clearly that does depend on someone else wanting to buy it, but my experience has been that any loan parts offered are typically snapped up very quickly. So if an urgent need arises, withdrawing your money (or part of it) is unlikely to be an issue.

You can read my full Kuflink review here. They offer a variety of investment options, including a tax-free IFISA paying up to 7% interest per year with built-in automatic diversification. Alternatively you can now build your own IFISA, with most loans on the platform (including the one shown above) being IFISA-eligible.

My investment in European crowdlending platform Nibble continues to perform as advertised. My latest investment was in their Legal Strategy. These are loans that are in default and facing legal action. Nibble buy these loans at a heavily discounted rate and then seek to recover as much as possible of the money owed. The minimum investment is 10 euros and the minimum period is six months. I invested 100 euros for 12 months initially at a target annual interest rate of 12.5%.

The Legal Strategy comes with a deposit-back guarantee. This is a guarantee to return the full investment amount at the end of the investment period and a minimum yield of 9% per year. The actual yield depends on how successful recovery efforts prove, so in practice you may end up with a return of anywhere between 9% and 14.5%. All has gone to plan so far, but I will obviously continue to report on this in the months ahead.

Earlier this year I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest). My investment has been up and down in the last few months, but it is currently $38 (about £31) in profit. In these turbulent times I am quite happy with that.

In any event, I’m looking on this as a long-term investment so won’t be judging it yet. I am also considering a further investment with eToro, possibly in one of their themed portfolios. You can read my full review of eToro here. You may also like to check out my recent more in-depth look at eToro copy trading.

Moving on, earlier I mentioned my Bestinvest SIPP (personal pension). This is now in drawdown, but regular readers will know that I suspended withdrawals from it in May this year to reduce the risk of pound-cost ravaging. I was able to do this because since December 2021 I have been receiving the state pension. And in association with my other income streams this has given me enough to live on (though by no means in luxury).

Anyway, with the cost of living crisis starting to bite, and energy bills shooting up at an alarming rate, I decided the time had come to resume taking payments from my SIPP. Plus, with the markets seemingly on an upward trajectory, the risk of pound-cost ravaging appeared to have receded.

I therefore asked Bestinvest to reinstate my payments from this month, though at a lower rate of £100 a month. One of the attractions of flexible drawdown pensions such as those from Bestinvest is that you can increase or decrease withdrawals at any time or even (as I did) suspend them completely. Obviously if you draw an excessive amount there is a risk of depleting your fund too quickly, so it runs out before you do. But Bestinvest sent me some reassuring projections that in any feasible scenario this was unlikely to happen in my case even if I live to the age of 99 (as I fully intend to 😀 ).

One other consideration I had with my SIPP is that withdrawals from it are taxable, whereas withdrawals from some of my other investments (e.g. Nutmeg ISA) are not. With the state pension also being taxable, this means withdrawing larger amounts from my SIPP would result in a portion of the money being grabbed by the taxman, which seems a waste. While I do of course accept that taxes have to be paid, I prefer to minimize my liability as much as possible (which we are all perfectly entitled to do).

I had two more articles published in November on the always-excellent Mouthy Money website. One of them was Win Fame and (Maybe) Fortune as a Quiz Show Contestant. This is something I have done myself in the past and enjoyed writing about again for MM. It can be a lot of fun, and any prizes you win are tax-free under UK law.

My other article was How to Cash in on Your Old Tech. Most of us have old technology we no longer use gathering dust in cupboards and drawers. This articles sets out ways you can make some much-needed cash out of this.

Obviously energy bills are a particular concern for many people at the moment, so I hope you are getting all the help you are entitled to. Everyone should be receiving a monthly rebate of £66 on their energy bill (going up to £67 in the new year). If you’re not, chase it up with your energy supplier.

I also recently updated my post about the Warm Home Discount, which this year is being increased from £140 to £150. The eligibility rules are changing somewhat, and I shall probably be one of the people who misses out, which is clearly disappointing. But on the plus side, most people won’t now have to apply for this benefit – if you are eligible, it should be applied automatically to your bill by your energy company.

The government’s Help for Households website has a helpful summary of all the financial assistance currently available and is regularly updated.

Please do check out as well some of the other posts on Pounds and Sense for advice and resources, especially in the Making Money and Saving Money categories.

Don’t forget, also, that there are currently two opportunities to claim a free share available. One is with Wealthyhood and the other with Trading 212 (the links will take you to the relevant blog posts). The current Trading 212 offer closes on 29 December 2022, so don’t delay if you want to take advantage of this one. As far as I know the Wealthyhood offer is open indefinitely, but that could always change, of course

That’s all for today. I hope you and your family are coping in these challenging times and wish you the happiest Christmas possible. I shall of course continue to update this blog over the coming weeks, and will return with a further update about my investments at the start of January.

As always, if you have any comments or queries, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media:

I’ve mentioned several times on PAS why I believe having an independent financial adviser makes sense, even if – like me – you consider yourself reasonably money-savvy.

So today I thought I would set out some reasons over-50s (in particular) may benefit from having an independent financial adviser (IFA) or at least speaking to one.

This post has been created in association with my colleagues at Unbiased.co.uk, a well-established financial services website that can put you in touch with suitable IFAs in your area.

Reasons for Having an IFA

1. Helping Your Children Through College or University

If you have children, you will naturally want to help them complete their education safely and with a reasonable degree of comfort. Sadly the days of student grants (which I was lucky enough to benefit from in the 1970s) are well behind us now. There are various options for helping finance your children’s college or university education and a financial adviser will be able to explore these with you. They will also explain the pros and cons of the student loans system.

2 – Pension Planning

If you are over 50 you will inevitably be thinking about pension options, including when you can retire and how much income you can expect. An IFA will go through your finances with you and look at ways you may be able to boost your pension pot. From 55 onwards you can normally start to draw your pension, but you shouldn’t do this unless a financial adviser has assured you it will last you through retirement.

3. Investing

Hopefully by your fifties you will be earning a decent salary and may also have paid off your mortgage. You may also receive an inheritance or other windfall. Either way, if you find yourself with some spare cash you will want to invest it to get the best possible returns from it. An IFA will have access to all the latest information about a vast range of investment opportunities. They will guide you towards investments that are suitable for you based on your financial goals, your investment timeframe and your appetite for risk.

4. Starting Your Own Business

Especially at this time of upheaval due to Covid, many people are looking to start their own businesses in mid-life. That may be in response to redundancy or unemployment, or simply in search of a better work/life balance. An IFA can help you with the financial aspects of doing this, including raising money for tools, premises, transport and so on, or perhaps buying a franchise.

5. Emigrating or Retiring Abroad

Another way to revitalize your life may be to start afresh somewhere else, with new challenges and opportunities (and perhaps a better climate as well!). Or you may be looking to move to a favourite vacation destination to enjoy your retirement. Either way, an IFA will be happy to discuss the pros and cons with you, point out all the things you will need to take into account, and assist you with the financial arrangements.

6. Divorce

Sadly middle age sees the largest number of divorces. Your first priority here will be appointing a good solicitor to act on your behalf and protect your interests. Beyond that, though, divorce can have major ramifications for your finances. An IFA can help you assess your situation objectively and plan for a financially secure and stable future.

7. Downsizing

As the children grow up and leave home you may want to move to a smaller property – to make life simpler, save time on housework and free up money for more exciting things. An IFA can help you explore the implications of doing this and make the necessary financial arrangements.

8. Equity Release

If you don’t want to move – and are over 55 – equity release is another option for releasing funds. In recent years it has grown a lot in popularity. There are various possibilities, including home reversion plans and flexible lifetime mortgages. Most now come with a no-negative-equity guarantee, ensuring you won’t end up passing on debts to your next of kin. An IFA can go over the options with you and point out the pros and cons before you contact any providers.

9. Estate Planning

This obviously includes writing your will, but depending on your circumstances it can cover a lot of other things as well. Nobody wants to see all their money and assets falling into the hands of the taxman rather than going to their nearest and dearest. Speaking to an IFA who specializes in estate planning can give peace of mind and ensure that your loved ones are well provided for when you are no longer here yourself.

10. Helping Elderly Relatives

If you have elderly parents (or other relatives) you may find they are increasingly reliant on you for help and support. It may be up to you to arrange care for them and/or set up power of attorney so you can manage their affairs if this becomes necessary. They may also need help with estate planning (see above). An IFA can assist with all these things as well.

Getting a Free Financial Check-Up

Independent financial advisers do of course charge for their services. They are by definition unaffiliated and do not receive commission, so any recommendations they make are based solely on their client’s best interests. As I have said before on PAS, I certainly don’t begrudge paying my own financial adviser, Mike, as he has undoubtedly saved (and made) me a lot more money than he has cost me over the years.

Nonetheless, most IFAs will be happy to see you for an initial financial healthcheck free of charge. This can focus on a particular area of concern, so you could request an investments review, a pension review or a mortgage review. Alternatively, if you’re not sure which aspect of your finances needs more attention – or indeed whether you need advice at all – you could simply request a broad financial healthcheck.

Here’s what. Adrian Kidd, a financial planner at Radcliffe & Newlands, says about his approach on the Unbiased website:

‘I’d generally offer one or possibly two free consultations, taking about an hour, and these can be as specific or as broad as required. When someone books a financial healthcheck with me, I ask them to bring along all their documents relating to their finances – savings, investments, mortgages, loans, insurance, pensions, the works – so I can build up a complete picture of their affairs. I then go through these in more detail after the consultation, and follow up with an email that gives a summary of their overall financial situation.’

In these free check-ups: advisers won’t generally talk to you about products at all. The process of choosing the right products comes later, after the adviser has built up an understanding of you as a person and your financial planning needs. Only then will they recommend products, if asked to do so.

If you follow my link to the Unbiased website, you can complete a short, step-by-step questionnaire designed to identify the best type of financial adviser for your needs. You will then be shown a selection of suitable advisers in your area with contact information. They will be happy to answer any queries you may have and arrange an initial meeting without obligation.

As ever, if you have any comments or questions about this post, please do leave them below.

Disclosure: This is a sponsored post on behalf of Unbiased.co.uk. If you click through my link and end up becoming a client of a financial adviser listed on the Unbiased site, I may receive a commission for introducing you. This will not affect the service you receive or any fees you are charged if you decide to proceed further.

This is a fully updated version of a post originally published in 2020.

If you enjoyed this post, please link to it on your own blog or social media:

I recently helped an elderly friend apply for the higher rate of Attendance Allowance. She was already receiving the lower rate, but sadly suffered a stroke which badly affected her balance and mobility.

As Pounds and Sense is aimed especially at older people (and those caring for them) I thought it might be of interest to describe what the process involves and my personal experiences with it. But first, let’s recap on the basics.

Attendance Allowance is paid at two different rates according to how much help and care you need.

The lower rate (currently £60 a week) is paid to people who need care through the day OR night

The higher rate (currently £89.60 a week) is paid if you need care through the day AND night, or if you are terminally ill.

Payments are normally made every four weeks direct to your bank account. The money is yours to spend as you wish to make your life a bit easier.

It is worth noting that you do not need to have someone currently caring for you in order to claim. Eligibility is based on your need for care rather than whether you are actually receiving it.

Another important point is that Attendance Allowance is not means-tested – eligibility is based purely on your care needs. Also, it is not taxable and will not normally affect your entitlement to other welfare benefits. Indeed, you may also be eligible for extra Pension Credit, Housing Benefit or Council Tax Reduction if you receive Attendance Allowance.

Attendance Allowance is administered by the Department for Work and Pensions (DWP) rather than local councils. In Northern Ireland the Department for Communities (DfC) has responsibility for it.

There is a long (31 pages) and detailed application form. You can either download this from the government website or you can phone them on 0800 731 0122 and ask for a form to be sent to you. In Northern Ireland you can download the form from this site or phone the Disability and Carers Service on 0800 587 0912. You can apply yourself or someone else can apply on your behalf (with your permission, of course).

Applying for the Higher Rate

Most people first applying for Attendance Allowance are awarded the lower rate. This is because they need help and support during the day but not (normally) at night. But of course – as in the case of my friend – that can change if your condition worsens.

If you – or the person you’re caring for – regularly need help during the night as well as the day, you may become eligible for the higher rate of Attendance Allowance. This also applies if you are diagnosed terminally ill (someone is classified as terminally ill if they are not expected to live longer than six months).

Anyway, after my friend had her stroke and received her diagnosis (this was delayed by a few weeks for reasons discussed below), I realised that she should now be eligible for the higher rate. Because of her reduced mobility and balance problems she now needs help getting to the bathroom at night, which previously she could manage herself. She also needs help taking medication at night, and so forth. All this means she does now regularly require assistance during the night as well as the day. So I phoned up the DWP Attendance Allowance helpline on the number above.

I spoke to a helpful young woman who asked me a few questions about my friend and how I was connected to her. I explained that I was an old family friend and had originally helped her apply for Attendance Allowance two years earlier. She accepted this without a quibble. She then asked me a few questions about my friend and why she (and I) believed she might now be eligible for the higher rate. I explained that – as stated above – due to her stroke she now required support at night as well as during the day.

The official told me she would be sending my friend a couple of forms to fill in. She reassured me that these were not as long as the original AA claim form, which I was pleased to hear. She said once they had received these they would re-evaluate her application. She cautioned me that this could result in her allowance being reduced as well as increased, which I duly noted.

Completing the Forms

I was told the forms could take up to 10 working days to arrive, but in fact they turned up at my friend’s house the next day. The form reference numbers were DBD420 and DBD138.

Form DBD420 comprises 5 pages. The first three pages are actually a letter explaining what you need to do with this and the other form. On pages 4 and 5 you are asked to explain why you are asking them to look at your application again. You are also asked why you didn’t get in touch sooner if your circumstances changed before the date you contacted them (shown on the form). This is an important point, so I’ll say a few more words about it now.

Unless you have a terminal diagnosis, you won’t become eligible for the higher rate of AA until six months after the change in your condition occurred. This is obviously somewhat arbitrary and you could argue that it is unfair, but that’s the rule. So it is important to contact DWP as soon as possible after your condition worsens, even though this may not be your top priority if you have just suffered a stroke 😮

In my friend’s case, she didn’t get an immediate diagnosis as the initial hospital tests were inconclusive. She therefore had to go back as an outpatient for an MRI scan. There was then a wait of several weeks until she got a letter confirming she had indeed suffered a stroke. I felt it would be best to wait until she had a definite diagnosis before applying for the higher rate of AA. In retrospect that might have been a mistake, although it’s hard to say for sure. But anyway, form DBD420 let’s you explain the reason there may have been a delay in applying, so we provided details as above. We also enclosed the diagnosis letter my friend (eventually) received.

The other form is DBD138. This is 11 pages long. I won’t go into detail about it here, but essentially it asks for information about your medical condition/s and – crucially – what help you need during the night and how many times. Inevitably this caused us a bit of head-scratching, but we filled it in to the best of our ability. It is important to note that you DON’T need to require constant watching over at night to qualify for the higher rate of Attendance Allowance. There must be a regular requirement for help at night, though – it can’t just be a one-off. Night is defined on the form as ‘when the household has closed down at the end of the day’ which made us think a bit of Downton Abbey 🙂

The Outcome

We sent off the forms in the reply-paid envelope provided. After three weeks my friend received a letter from DWP which was basically just an acknowledgment of the original query. Then the next day, rather to our surprise, a longer letter arrived confirming that her application had been reviewed and she was now eligible for the higher rate of Attendance Allowance.

The start date for the higher rate was six months after the date she suffered her stroke, which is what we requested on the form. Obviously, I was pleased about this and so was my friend. Although the extra money won’t compensate her for the loss of mobility she has suffered, she will be able to use it to pay for things that will make life a little more comfortable for her going forward.

If you (or someone you know) find yourself in a similar position to my friend, I hope you will find these notes helpful. As always, if you have any comments or questions, do post them below. But please bear in mind that I am not a trained welfare worker or financial adviser. If you need in-depth help, I would try Citizens Advice or an organization like Carers UK.

If you enjoyed this post, please link to it on your own blog or social media:

The number of people applying for Universal Credit has surged to record levels as a result of the Coronavirus pandemic and the numbers are set to rise further with the ongoing economic uncertainty.

In addition to a loss of income, households could also be facing a rise in energy-bills due to more time spent at home and cold weather approaching. Many will be coming to grips with the benefits system for the first time and starting to understand the rules, regulations and complexities around making a claim.

However, there is a little known silver lining for these claimants. Anyone who has claimed Universal Credit successfully will also be eligible for home improvements under the Government’s Energy Company Obligation (ECO) scheme.

This current scheme, called ECO3, targets people that have high energy costs comparative to household income. The scheme has a list of ‘qualifying benefits’ for eligibility. Universal Credit is on that list.

Plus, there are no savings or income-tests for the qualifying benefit part of the application, so if you receive any benefit on the list below (excluding Child Benefit, as that has an income cap), it’s likely you’ll be eligible.

According to Ofgem (who administer the ECO scheme), claimants will still be eligible for a period of 18 months following the date of the letter for the Universal Credit award (page 44 of the Ofgem ECO3 guidance has full details).

So if, say, you were awarded your Universal Credit in April but you got a job last week and came off Universal Credit today (for example), you still have a significant period of time (a year and a half) to apply for and install the measure, as you would still be classed as eligible even when you return to work. While you can wait to apply, it’s advisable to apply sooner rather than later, as funding rules can change at any time.

Even if you have returned to work or are planning to return to work, you will still be eligible, providing you have had at least one award for Universal Credit.

And it isn’t just Universal Credit recipients who are eligible for grants. Also on the ‘qualifying benefits’ list are the following:

You will still be eligible if you return to work as you can claim for a period of 18 months after claiming benefits.

What Grants Are Available?

There are a range of energy-efficiency measures that can be installed under the Energy Company Obligation (ECO) scheme, including boiler upgrades, home insulation and heating upgrades. The Scheme is funded by the major energy companies and if you claim benefits, you are entitled to this funding.

Table: Measures Available Under the Energy Company Obligation Scheme

Measure

Homeowners

Private Tenants

Housing Association Tenants

Landlords

Council Tenants

Air Source Heat Pump (ASHP)

✅

✅

✅

❌ Landlords ✅ Private tenants can apply

❌

Boiler Upgrade or Repair

✅

❌

❌

❌

❌

Cavity Wall Insulation

✅

✅

✅

❌ Landlords ✅ Private tenants can apply

❌

Electric Heating Upgrade

✅

✅

✅

❌ Landlords ✅ Private tenants can apply

❌

First Time Central Heating (FTCH)

✅

✅

✅

❌ Landlords ✅ Private tenants can apply

❌

Internal Wall Insulation

✅

✅

✅

❌ Landlords ✅ Private tenants can apply

❌

Underfloor Insulation

✅

✅

✅

❌ Landlords ✅ Private tenants can apply

❌

How Much Could You Get?

The amount of funding available depends on a range of factors, including property type, your existing heating, wall type and potential energy savings from proposed work.

The first step in working out what you could get is to check your eligibility online. There’s a quick form on the Energy Saving Genie website where you can enter your details to see if you are eligible.

If you meet the criteria, you can choose to apply and once your application has been submitted, it will be passed to a Registered Installer.

The Registered Installer will arrange a free survey of your property. You can choose to proceed ASAP with a survey taking place following strict health and safety guidelines or you can choose to wait until after Covid-19.

Once the survey has taken place, the surveyor will report back to the Registered Installer, who will talk you through the grants that are available towards energy-efficiency measures at your property.

The grant is paid directly to the installer and they are awarded on lifetime savings (LTS) scores. Currently electric heated properties and larger properties tend to receive the most funding. But even if your home isn’t large or heated by electricity, it is worth applying as you could still receive a significant grant towards home improvements.

So if you are one of the many million new Universal Credit claimants due to Covid-19, you can start the process of applying for a home improvement grant that will knock £££s of your energy bills for years to come, well after the pandemic has passed.

Disclosure; This is an adapted reblog of an original post by Energy Saving Genie. It is also a sponsored post. If you click through and end up taking advantage of this government scheme, I will receive a fee for introducing you. This will not affect any products or services you may receive or the value of any grants you may be awarded.

If you enjoyed this post, please link to it on your own blog or social media:

As you may have heard, the BBC has now confirmed that from 1st August 2020 people over 75 in the UK will lose their automatic right to a free TV licence and have to pay the same £157.50 a year as everyone else. This was originally due to happen in June 2020, but it was postponed due to the coronavirus pandemic.

For many old people, TV is their main (or only) source of company. Suddenly having to find this quite large sum out of (in many cases) a very limited income may cause them financial difficulties or downright hardship. Some may even have to choose between watching television and paying their heating bills.

This parlous situation has arisen because the BBC say they have to make economies, and continuing to subsidise free licences for the elderly would force them to cut back drastically in other areas. Meanwhile the government, despite their pre-election promises, has shown no sign of stepping in to preserve free TV licences for over 75s (which they could perfectly well do). Although charities such as Age UK have been raising petitions and applying as much pressure as they can, it now seems certain that this change is going to happen.

So what can people in this situation – or their relatives/friends/carers – do? The BBC have allowed just one concession – the poorest over-75s can continue to receive a free TV licence if they claim and receive pension credit. So let’s look at this in a bit more detail…

Pension Credit

Pension credit is a state benefit for people above retirement age who are on a low income. It can be paid to single people or to couples. It is usually paid weekly, though you can also choose to have it paid fortnightly or monthly.

Along with attendance allowance – which I discussed in this recent post – pension credit is one of the most under-claimed benefits. According to the Department for Work and Pensions, around 40 percent of eligible people, or two in five, fail to claim it. That’s an estimated 1.5 million eligible households in the UK who are missing out.

Pension credit actually comes in two parts – guarantee credit and savings credit. Guarantee credit boosts your weekly income to £167.25 if you’re single or £255.25 if you’re a couple (all figures correct as of March 2020). You may be eligible for guarantee credit if you have reached state pension age and your total income is less than these amounts (even if you own your own home). If you have under £10,000 in savings and investments this will not be taken into consideration. If you have over £10,000, it will be assumed that you earn £1 a week per £500 of savings and investments (equivalent to an interest rate of 10.4% – if only!). This will be added to your total income when working out your eligibility.

Savings credit is meant to be a reward for those who have saved for their retirement. It’s worth up to £13.73 a week for a single person or £15.35 for couples. To qualify, you must have a minimum income of £144.38 a week if you’re single, and £229.67 a week if you’re in a couple. For every £1 by which your income exceeds this amount, you get 60p of savings credit – up to the £13.73/£15.35 maximum. If your income is less than the £144.38/£229.67 savings credit threshold, you won’t qualify. Savings Credit is only available to people who reached state pension age before 6 April 2016. Couples where only one partner reached state pension age before 6 April 2016 can also retain savings credit if the older partner had reached 65 and qualified for savings credit before that date AND they have remained continuously entitled to it ever since.

It’s worth adding that if you pay mortgage interest or have other housing costs, have caring responsibilities, are responsible for a child, or are severely disabled, you may be entitled to more pension credit. If you receive attendance allowance or carers credit, for example, this may boost the amount you’re entitled to. The rules surrounding all this are complicated, but the government has provided a free online calculator you can use to work out whether you qualify and how much you might get. This is for guidance only, however. You can’t apply via the calculator and there is no guarantee that you will receive the amount it shows you.

To actually apply you will need to phone the DWP’s Pension Credit helpline on 0800 991234. You will need your National Insurance number, information about your income, savings and investments and your bank account details. The person you speak to will then take you through the application process. This is a subject I discussed in more detail in this blog post, as I recently helped an older friend to do this successfully.

What Does Pension Credit Entitle You To?

As well as the money – which can amount to thousands of pounds a year – if you receive pension credit you will be entitled to a range of additional benefits. A free TV licence if you are over 75 is just one of them. You may also get:

reduced council tax (or free if you are awarded guarantee credit)

Even if you only receive a small amount of pension credit, you will be eligible for all of the above. So it really is well worth applying if there is any chance you may qualify. As mentioned above, you can check first using the free online calculator here and then apply by phoning the DWP’s Pension Credit helpline on 0800 991234.

Don’t delay, as there are now just seven weeks left before the free TV licence for all over-75s becomes a cherished memory.

Equity Release to Boost Your Income

If you’re still struggling to pay the bills even with pension credit, there are other methods to help boost your income. In particular, UK homeowners are fortunate to have opportunities to unlock their property value. An equity release loan could provide the security you desire if you require the means to pay for life’s simple pleasures or cover essential costs.

What’s more, homeowners can unlock up to 65% of their property value, with no compulsory payments required during their lifetime. There’s no limit on how you can use the tax-free cash you receive, so an income lifetime mortgage could be the ideal way to pay your bills and have a bit extra for luxuries as well.

In this recent blog post I discussed how over-75s may be able to avoid losing their free TV licence by claiming pension credit.

As I said then, I have recently done this myself on behalf of an elderly couple who are friends of mine. As promised, today I’ll be sharing my experience of the telephone application process. I hope anyone thinking of doing this themselves or on behalf of elderly friends or relatives may find this helpful.

But first, let’s recap on what pension credit is…

Pension Credit

Pension credit is a state benefit for people above retirement age who are on a low income. It can be paid to single people or to couples. It is usually paid weekly, though you can also choose to have it paid fortnightly or monthly.

Along with attendance allowance – which I discussed in this recent post – pension credit is one of the most under-claimed benefits. According to the Department for Work and Pensions (DWP), around 40 percent of eligible people, or two in five, fail to claim it. That’s an estimated 1.5 million eligible households in the UK who are missing out.

Pension credit actually comes in two parts – guarantee credit and savings credit. Guarantee credit boosts your weekly income to £167.25 if you’re single or £255.25 if you’re a couple (all figures correct as of March 2020). You may be eligible for guarantee credit if you have reached state pension age and your total income is less than these amounts (even if you own your own home). If you have under £10,000 in savings and investments this will not be taken into consideration. If you have over £10,000, it will be assumed that you earn £1 a week per £500 of savings and investments (equivalent to an interest rate of 10.4%). This will be added to your total income when working out your eligibility.

Savings credit is meant to be a reward for those who have saved for their retirement. It’s worth up to £13.73 a week for a single person or £15.35 for couples. To qualify, you must have a minimum income of £144.38 a week if you’re single, and £229.67 a week if you’re in a couple. For every £1 by which your income exceeds this amount, you get 60p of savings credit – up to the £13.73/£15.35 maximum. If your income is less than the £144.38/£229.67 savings credit threshold, you won’t qualify.

While for most people pension credit won’t be a huge amount, it has the big advantage that it acts as a gateway to a range of other discounts and benefits. The free TV licence for over-75s is just one of them. Pension credit recipients may also get reduced council tax (or free if awarded guarantee credit), free NHS dental treatment, help towards the cost of glasses, help with the cost of travel to hospital, cold weather payments, automatic entitlement to the Warm Home Discount, help with rent, free home insulation and boiler grants, and more. All of this means it is well worth applying for, even if you’re not certain whether you qualify.

Checking Your Entitlement

The government is keen that anyone eligible for pension credit should claim it. To that end they recently launched a free online calculator you can use to work out whether you qualify and how much you might get.

You can use the calculator anonymously to check your entitlement (or someone else’s), either as an individual or a couple. You can’t actually apply via the calculator, though. It is just for guidance, to help you decide whether it’s worth putting in a claim.

The calculator asks a variety of questions about your circumstances and current income, including any pensions or other benefits you may receive. The latter may actually improve your chances of getting pension credit. For example, if you receive attendance allowance and/or carer’s credit (as my friends do) this can improve your chances of qualifying. When I did this on behalf of my friends, the calculator showed that they should be eligible for a payment of just over £10 a week.

As mentioned above, the results on the calculator are for guidance only, and there is no guarantee that you will receive the amount shown. However, in my friends’ case it definitely confirmed that applying would be worth doing.

Applying for Pension Credit

By far the easiest way to apply for pension credit is to phone the DWP’s Pension Credit Helpline on 0800 991234. You will need to have your National Insurance number, information about your income, savings and investments and your bank account details to hand.

If you’re applying on someone else’s behalf, the DWP like you to have the person concerned with you at the time. The call handler spoke briefly to my friend to confirm her personal details and that she was happy for me to take over the application process.

It turned out to be a two-stage procedure. Initially I spoke to a male call handler who asked a list of questions about my friends’ circumstances and their finances. This was basically the same set of questions I had answered on the online calculator. It was reasonably straightforward, and at the end he informed me that my friends did indeed appear to have a valid claim, so he was going to put me through to his colleague who would take me through the actual application.

This meant that I had to answer the same set of questions again from another DWP employee – a woman this time, as it happens. This did strike me and my friend as rather a waste of everyone’s time. We wondered why the answers I had given initially couldn’t just be passed on to the second person, but I suppose the DWP must have their reasons.

Anyway, we duly went through all the questions (and a few more) again. I would, incidentally, comment that the young woman I spoke to – who told me her name was Jenny – was extremely pleasant and helpful. At one point we went off at a tangent and started talking about our favourite cakes (well, it was tea-time by then). I felt she went out of her way to help us, and she certainly made the whole application process a lot less stressful.

After going through all the questions, Jenny said she would need information about how much exactly was in my friends’ bank accounts and when their (small) private pensions were paid in. This could have been problematic, as it involved logging in to my friends’ online bank accounts and finding this information there. But Jenny was patient and flexible about this, and in the end we found all the information she needed.

The whole process took a little over an hour. if you have to break off half-way through that is possible and you can ask for a reference number so you can complete the application another time. But I really wanted to get the whole thing done and dusted in one call, and thankfully – with Jenny’s help – we achieved that.

The Outcome

After about six weeks my friends received a letter from DWP saying their application had been successful and they had been awarded pension credit.

The amount was the same as had been shown on the online calculator. It was about £10.50 a week, going up to almost £12 in April (I’m sorry I can’t remember the exact figures). This money was savings credit rather than guarantee credit, but that makes no difference as far as the free TV licence is concerned. If you are over 75 and qualify for either type of pension credit (or both) you are entitled to a free TV licence.

We then submitted the short application form to the TV licence people, with a copy of the first page of the DWP letter confirming the award of pension credit. We haven’t heard any more since, but presumably my friends will receive their free TV licence in the coming weeks.

So that was my experience of applying for pension credit on my friends’ behalf. I hope it has encouraged you to proceed with your own application if you are considering making one. If you get to speak to the lovely Jenny in Scotland, do pass on my regards to her!

And if you have any comments or questions about this post, of course, pleased free free to leave them below as usual.

This is a fully updated repost of my March 2020 article.

If you enjoyed this post, please link to it on your own blog or social media:

…that’s the question I was asked recently by a Pounds and Sense reader after I mentioned in this blog post that I had a financial adviser.

Of course I replied to her directly at the time, but on reflection I thought it would be good to provide a more in-depth answer to this question on the blog.

To recap, my financial adviser is called Mike and he works for a company called Integrity Wealth Solutions. I was recommended to Mike by my accountant, and he has been advising me for over three years now.

Mike actually looks after about half of my portfolio. He advised me about this initially and set up the recommended investments on my behalf, making maximum use of my tax-free allowances. He continues to monitor my investments and makes any recommendations for adjustments as required. I see Mike once a year in person to review how things are going (both with the investments and me personally). But of course, I can also speak to him by phone (or email) any time if required.

The other half of my portfolio I look after myself, and it is fair to say it is well diversified! As regular readers of PAS will know, I have investments in property crowdfunding, P2P lending, the robo advisory platform Nutmeg, and various others.

Why then do I need Mike? Here are just some of the reasons…

1. Mike is a trained and experienced independent financial adviser/planner who works full-time in this field. I am a money blogger and obviously have a special interest in financial matters, but I have no professional training or direct work experience in this field. I can ask Mike for his professional opinion on any investment-related matters, and while I am not obliged to follow his advice I do of course take it very seriously.

2. Mike has a backup team in his office and access to specialist investment research services and software. He uses these resources to inform his advice, and also to provide in-depth reports (with snazzy-looking charts and spreadsheets!) regarding how my investments are performing.

3. As a regulated financial adviser, Mike has to follow all the correct protocols and ensure that all advice he gives follows best professional practice and is appropriate for my needs and circumstances. He cannot cut corners, invest on a whim or hunch, or let himself be distracted by the latest ‘bright shiny object’ in the investment world. I have to admit that I have been guilty of all of these things myself in the past!

4. As a professional financial adviser Mike also has access to certain investment opportunities or platforms that are not easily accessible to the general public. I won’t go into detail about this here, but it is certainly something I have had occasion to be grateful for in the current coronavirus outbreak.

5. Mike is able to provide personalized but objective advice about my finances, based on information I give him. Money and investment can be emotive subjects, and it’s great to have a sympathetic – but at the same time sensible and detached – professional advising you. I am sure Mike sometimes sighs inwardly at some of my more exotic investments, but he is always interested in what I have been doing with ‘my’ half of my portfolio and happy to offer his thoughts as appropriate.

Are there any drawbacks to having an adviser? Well, of course, you have to pay them! In the case of Mike I paid an up-front fee initially and now pay a small monthly commission. Hand on heart I can say that Mike is well worth his fee, and even in the current exceptional circumstances his charges have been more than covered by the amount by which my investments have grown.

So that is why I have a personal financial adviser. If you are fortunate enough to have money to invest, I strongly recommend you consider engaging one too.

If you would like to find out more about the service offered by Mike and his colleagues at Integrity Wealth Solutions, you can check out their website and contact them on 02476 388 911, or email them at advice@integritywealth.co.uk. They are friendly and not at all pushy, and will be delighted to talk you through the service they offer without obligation. If you do get in touch, please mention that you were recommended by Nick Daws of Pounds and Sense blog. If you end up becoming a client they have said that they will pay me a small fee to say thanks. This will help to cover my costs and ensure I am able to go on sharing tips and advice to Pounds and Sense readers.

As always, if you have any comments or questions about this post, just let me know.

If you enjoyed this post, please link to it on your own blog or social media:

For many older people the free bus pass (officially known as the older person’s bus pass) is a valuable concession. It helps them get about and maintain their independence without eating into their often limited income.

Holders typically get free bus travel within their local authority area between 9.30 am and 11 pm on weekdays and all day at weekends.

The rules for when you qualify for a free bus pass vary according to where in the UK you live. In Scotland, Wales and Northern Ireland, it’s straightforward. You qualify once you reach your 60th birthday.

Those living in England are not as fortunate. In this case, you won’t qualify until you reach the current state pension age. This is currently 66 for both men and women. The state pension age will start to increase again from 6 May 2026, and will reach 67 by 6 March 2028.

Once you have reached the qualifying age in whichever country of the UK you live, you can apply via the government’s Apply for an Older Person’s Bus Pass page. You will see a box on this page in which to enter your postcode. Clicking through this should take you to the website for your local authority (though you may have to navigate to the page for travel concessions from there). You can then apply online for your bus pass. Requirements can vary from one local authority to another, but in general you will be required to upload a passport-style photo, proof of identity, and proof of residency in the area concerned (e.g. a council tax bill). For info about how to renew your bus pass online, please click here.

If you don’t want to apply online, most authorities also offer an option to apply in person, e.g. at a public library. Your local authority website should have more information about this.

Some local authorities have their own schemes and concessions for older (and/or disabled) people. Again, your local authority website should tell you if there are any special concessions for older people in your area, or you can ask at your local library.

In London, once you reach the female state pension age you can apply for an Older Person’s Freedom Pass. This entitles you to 24-hour free travel across Transport for London’s networks (except for some river boats where travel is half price). You can check your eligibility for a Freedom Pass and apply here.

Cards and Discounts

Even if you don’t yet qualify for a free bus pass, there may be other ways you can get free or discounted travel.

If you live in London and are 60 or over, you can apply for a 60+ Oyster card. This provides free travel on the London Underground, Overground, trams and buses, as well as some TfL Rail and National Rail services, but you can’t use it outside London. The card has a one-off £20 administration fee. You can apply online from two weeks before your 60th birthday. For more information about the application process see the TfL website.

Also once you are 60 or over, you can apply for a Senior Railcard. This currently costs £30 a year and gets you a third off most rail journeys, local and national. You can get more information and apply here.

Or if you’re 60 or over and make regular use of National Express coaches, you can buy a Senior Coachcard which costs £12.50 (plus 2.50 p&p) and offers a third off travel throughout the year. With this card you can also buy a £15 day-return on Tuesdays, Wednesdays and Thursdays to anywhere in the UK (excluding airports) as long as you book three days in advance. You can apply for a Senior Coachcard via the National Express website.

As always, if you have any comments or questions about this post, please leave them below. Happy travels!

If you enjoyed this post, please link to it on your own blog or social media: