With the cost of living continuing to put pressure on household finances, many people in the UK are unaware they could be paying less for essential services like broadband, water and energy. If you’re on a low income or receiving certain benefits, you may be eligible for social tariffs – discounted rates offered by providers to help those most in need. Here’s what you need to know.

What Are Social Tariffs?

Social tariffs are specially discounted rates offered to people on low incomes and/or receiving certain means-tested benefits. These tariffs are often significantly cheaper than standard ones and aim to ensure everyone can afford access to essential utilities and services.

Unlike short-term promotions, social tariffs are designed to offer long-term affordability and typically come with flexible terms, e.g. no exit fees and the ability to switch back to regular plans when your circumstances change.

Social Tariffs for Broadband

Broadband internet is essential for accessing services, finding work, staying in touch, and more. Yet many people are paying standard prices when they could be saving money each month.

Who Offers Social Broadband Tariffs?

Most major UK broadband providers offer social tariffs. Some examples are shown in the table below.

Provider

Plan Name

Monthly Cost

Speed

Eligibility

BT

Home Essentials

£15

36 Mbps

Universal Credit, Pension Credit, ESA, JSA, Income Support

Virgin Media

Essential Broadband

£12.50

15 Mbps

Universal Credit

Sky

Broadband Basics

£20

36 Mbps

Universal Credit, Pension Credit

NOW

Broadband Basics

£20

36 Mbps

Universal Credit, Pension Credit

Hyperoptic

Fair Fibre Plan

£15

50 Mbps

Several means-tested benefits

Check each provider’s website for full details and availability in your area.

How to Apply

You’ll usually need to:

Be receiving a qualifying benefit (e.g. Universal Credit, Pension Credit, ESA, JSA)

Apply directly with the provider, often via a dedicated web page

Provide proof of eligibility (some providers check automatically)

Most social broadband tariffs have no setup fees, no mid-contract price rises, and shorter contract terms – typically 12 months or rolling monthly

Social Tariffs for Water Bills

As discussed in this recent blog post, water companies in England and Wales also offer discounted tariffs for customers who are struggling to afford their bills. These social water tariffs are designed to reduce charges for households on low incomes or receiving certain benefits.

What Support Is Available?

Each water company sets its own scheme, but most offer:

Reduced bills based on income and household circumstances

Debt support and payment plans

Water meters to help control usage

For example:

Water Company

Scheme Name

Support Offered

Thames Water

WaterHelp

Up to 50% off bills for low-income households

Severn Trent

Big Difference Scheme

Bills reduced by up to 90% depending on income

United Utilities

Help to Pay

Lower bills for those on Pension Credit

Yorkshire Water

WaterSupport

Tiered discount based on income and household size

Who Is Eligible?

Eligibility varies slightly by region, but in general you may qualify if:

Your household income is below a certain threshold (e.g. £21,000 per year)

You receive means-tested benefits

You have high water usage due to medical needs or a large family

How to Apply

Visit your water company’s website or contact them directly. You’ll likely need:

Proof of income or benefits

Recent water bills or meter readings

Details about your household size and needs

You can also get help from Citizens Advice or StepChange, who can assist with applications and managing arrears.

Social Tariffs for Energy

Energy prices remain high, and although the Energy Price Guarantee and price cap offer some protection, many households are still struggling.

While there is currently no mandatory social tariff for energy in the UK, some suppliers do offer extra support, and the government has been consulting on introducing a formal scheme.

Help Currently Available

Warm Home Discount: Offers £150 off your electricity bill automatically if you’re eligible. It’s not a social tariff, but it helps reduce costs.

Priority Services Register: Offers free support services (e.g. advance notice of outages, help reading meters) for vulnerable customers.

Energy Support Funds: Some suppliers (e.g. British Gas, EDF, E.ON Next, Octopus) offer hardship funds or discretionary credit for customers in financial difficulty.

Government Consultation: A formal energy social tariff could be introduced in the future, aiming to replace stop-gap measures like the Warm Home Discount.

Who Is Eligible?

Eligibility criteria vary by provider, but typically you must be receiving at least one of the following:

Universal Credit

Pension Credit (Guarantee Credit)

Income Support

Employment and Support Allowance (ESA)

Jobseeker’s Allowance (JSA)

Personal Independence Payment (PIP)

Attendance Allowance

Disability Living Allowance (DLA)

Carer’s Allowance

Even if you’re not sure, it’s worth checking — some providers may consider broader circumstances.

Tips to Save Even More

Use a benefits calculator (e.g. Turn2us or Entitledto) to check what you’re entitled to.

Switch providers: Even without a social tariff, switching could save you money.

Check for grants or local schemes via your council or Citizens Advice.

Final Thoughts

If you’re struggling with your broadband or energy bills, don’t suffer in silence. Social tariffs can offer substantial monthly savings and provide peace of mind during difficult times. They’re designed to be easy to apply for and are often available even if you’re already a customer.

Check with your provider or visit Ofcom’s website to find out more – and make sure you’re not paying more than you need to.

Have you benefited from a social tariff? Share your experience in the comments to help others who might be eligible too.

If you enjoyed this post, please link to it on your own blog or social media:

It can be normal to find our priorities shifting as we get older. Where once we may have focused on saving for a house, getting married or raising children, later life often brings concerns about financial security, and thoughts of what our loved ones would do financially if/when we are no longer around.

When it comes to loved ones, peace of mind is so important. That’s why in this article I’ve teamed up with Cover Today to take a look at how Over 50 Life Insurance can give your family some financial support if the worst were to happen.

So what is Over 50 Life Insurance and, more importantly, is it worth getting?

What is Over 50 Life Insurance?

In the UK, Over 50 Life Insurance is a type of policy specifically designed for people aged over 50. It offers a guaranteed, fixed cash payout when the policyholder dies, provided they’ve kept up with their monthly premiums.

Over 50 life insurance policies are generally “whole of life”, meaning they last until you pass away, as long as you keep up with premium payments. They’re often used to help cover funeral expenses, outstanding debts, or to leave a small inheritance.

With Cover Today, you can apply for cover in just minutes, with no need for medicals or blood tests – peace of mind is just a phone call away.

Is it worth getting?

Whether Over 50 Life Insurance is worth it depends on your personal circumstances. For many, Over 50 Life Insurance is about leaving a lasting legacy and providing financial assistance for your loved ones. If you have little to no savings or want to ensure that your funeral costs and other final expenses are covered without burdening your loved ones, this type of cover could be a practical choice.

What can it be used for?

The payout from an Over 50 Life Insurance policy could be used in a variety of ways, depending on your finances when you pass away, and your family’s needs. Some common uses for this type of payout include::

Funeral costs

Paying off small debts

Leaving a cash gift to children or grandchildren

Contributing to charitable causes

Even if you don’t have a particular plan for your benefit amount, many policyholders take comfort simply in knowing they’ve left something behind or reduced the financial stress for their families.

How much does it cost? What affects the premiums?

What you might pay for Over 50 Life Insurance will depend on your unique circumstances. For instance, if you smoke, it’s likely that your premiums will be higher to due to the related health risks. Your premiums will also depend on your age, and the amount of cover you choose for your benefit amount.

It’s important to note that, with a whole of life policy, you could end up paying more in premiums over the years than the policy will eventually pay out. However, as long as you keep up with your premiums, your loved ones are guaranteed a payout.

When should I take out cover?

Generally, the younger you are when you apply, the lower your premiums will be. This means that taking out a policy in your early 50s can be more cost-effective than waiting until your late 70s. So, it could be a good idea to apply earlier rather than later

Another reason to apply sooner is that many providers require a “waiting period” in their cover. This is an initial period after you purchase your policy where your cover would not provide a payout to your loved ones if you were to pass away. After that period – which usually lasts around 12 months – you’ll be fully covered.

However, with Cover Today, there is no waiting period. You’re fully covered from day 1.

When is it not worth it?

Over 50 life insurance might not be suitable for you if:

You already have sufficient savings or other cover in place.

You’re in poor health and may not live long enough to justify the premiums.

You want a policy that builds cash value or provides a higher payout.

In some cases, putting the money you’d spend on premiums into a savings account could be more beneficial, especially if you’re a consistent saver. Life insurance can be a very personal choice, and whether Over 50 cover is right for you will depend on your own financial situation and the needs of both you and your loved ones.

Closing thoughts

Over 50 Life Insurance can be useful for those seeking peace of mind and a simple way to provide for their loved ones after they’re gone. However, like any financial product, it’s not a one-size-fits-all solution. It is important to consider your financial situation, health and long-term goals before deciding. Speaking to an independent financial advisor can also help determine whether it’s the right choice for you.

This is a collaborative post.

If you enjoyed this post, please link to it on your own blog or social media:

In Britain we’re lucky to have high-quality running water on tap whenever we need it. LIke everything else in life it costs money, however. And in these times of rising prices and squeezed incomes, those costs can be a growing burden. So in this article I’ll be setting out some ways you may be able to reduce your water bills.

The first thing to say is that water pricing varies across the nations of the UK. In England and Wales, unless you have a water meter, the price you pay will depend on the rateable value of your home.

In Scotland, again unless you have a meter, you will pay a standard water charge with your council tax.

Domestic customers in Northern Ireland are fortunate in that they aren’t required to pay a water bill at all, though it is possible this may change in future.

Should You Get a Water Meter?

The average water bill for unmetered customers is currently around £470 a year.

If you’re on a low income, that can represent a significant chunk of your money. And unlike gas and electricity, you can’t just shop around for a better deal with a different supplier. You may, though, be able to make significant savings by having a water meter installed.

With a meter, you are of course charged according to how much water you use. A good rule of thumb here is that if your house has more bedrooms than occupants or the same number, it is definitely worth looking into getting a meter installed.

Of course, people vary considerably in how much water they use. So you can use this free online calculator from the Consumer Council for Water to check whether you are likely to save money with a meter. It asks a series of questions about your home and your water usage and reveals the estimated cost you would pay if you had a meter. You can then compare this with what you are paying currently.

The good news is that in England and Wales (though not Scotland) water companies will normally install a water meter free of charge if requested. Even better, they will usually let you switch back to unmetered within 12 or even 24 months if you find you are paying more with a meter than you were before. You should check with your water company to find out their policy about this.

If your water company can’t fit a meter for some reason, you can ask for an ‘assessed charge bill’. This is calculated based on the size of your home and how many people live there. If it comes to more than you’re currently paying you can stick with your present billing method, so there is nothing to lose by requesting this.

Saving Money With a Water Meter

Once you have a meter installed, there are lots of ways you can reduce your water usage and save yourself money (and benefit the environment as well!). Here are just a few suggestions…

Only ever use the washing machine with a full load.

Have showers rather than baths and keep them reasonably short.

Do all the washing-up in one go.

Use a dishwasher, or at least a washing-up bowl.

Turn off the tap while brushing your teeth.

Don’t use the toilet as a waste bin for paper tissues, etc.

Fix dripping taps and any other leaks as soon as possible.

Finally, most water companies have a range of gadgets to help save water they will send you for free. Give them a call or check on their website to find out what’s available.

Other Ways to Cut Your Water Bills

If you are on a low income, all the water companies have schemes and discounted tariffs to help you. These vary a lot and you will need to check with your water company what they offer.

Severn Trent, for example, has the Big Difference Scheme, which offers significant discounts (up to £390 a year) on water bills for eligible households, based on income.

My Experience

As a customer of South Staffs Water, I recently applied successfully for a discount on grounds of low household income (under £22,011) under their Assure scheme.

Under this rather odd (in my opinion!) scheme I will be getting 60% off my bills in the first year, 40% in the second year, and 20% in the third. I have no idea if I will then be able to reapply and start the process again. Even so, it will certainly help my finances in these challenging times. Under Assure (and similar schemes) it is only your household income taken into account, not any savings or investments.

Closing Thoughts

Water bills have risen rapidly in recent years, partly due to the major investment required in Britain’s creaking water-supply and sewerage infrastructure, along with a rising population.

From being at one time a relatively minor expense, water bills are now (if you’ll pardon the pun) a significant drain on many people’s household income.

With other bills rising fast as well, it’s therefore vital to grasp any opportunity to keep your water costs as low as possible.

As always, if you have any comments or questions about this post, please do leave them below.

This is a revised and fully updated version of my original post.

If you enjoyed this post, please link to it on your own blog or social media:

When people think about investing, their minds often jump to stocks and shares. But bonds – a less glamorous but more stable option – can play a key role in a well-rounded investment portfolio, especially for those seeking predictable, regular income and/or lower risk.

In this article, I’ll reveal what bonds are, how to invest in them, and the main pros and cons to consider.

What Are Bonds?

A bond is essentially a loan from you to a government or company. In return, they pay you interest (known as the “coupon”) over a set period (typically annually or semi-annually). When the bond reaches the end of its term (maturity), you get your original investment back.

There are several types of bonds, including:

Government bonds (gilts) – issued by the UK government

Corporate bonds – issued by companies

Inflation-linked bonds – designed to rise with inflation

Foreign bonds – issued by overseas governments or companies

How to Invest in Bonds

There are a few ways you can invest in bonds:

1. Buy Individual Bonds

You can buy gilts or corporate bonds directly through:

The London Stock Exchange

Brokers such as Hargreaves Lansdown or AJ Bell

The UK Debt Management Office for new gilt issues

Buying individual bonds gives you control, but requires a higher initial investment and comes with more risk if the issuer defaults.

2. Bond Funds

Instead of picking individual bonds, you can invest in a fund that holds a basket of bonds:

Bond Unit Trusts and OEICs (Open-Ended Investment Companies)

Bond ETFs (Exchange Traded Funds) – such as iShares UK Gilts or Vanguard Global Bond ETF

These offer instant diversification and lower entry costs, and can be held in tax-efficient wrappers like Stocks & Shares ISAs or Self-Invested Personal Pensions (SIPPs).

WiseAlpha is a UK fractional bond platform that allows retail investors to buy fractional corporate bonds – essentially, small slices of high-yield bonds that are normally only accessible to institutional investors. This opens up access to a wide range of corporate bonds from major companies (e.g. Travelodge, HSBC and Asda) without the need for thousands of pounds to get started. This can be a good middle ground if you want more control over your bond investments than is offered by a fund but don’t have the capital required to buy full bonds.

See also the comparison table of UK bond platforms at the end of this article. This also reveals which platforms allow you to buy bonds within a tax-efficient ISA

Pros of Investing in Bonds

1. Reliable Income

Most bonds pay regular interest, making them a good source of steady income, especially for retirees.

2. Lower Risk Than Shares

Bonds are generally less volatile than stocks, so they can act as a buffer during market downturns.

3. Capital Preservation

If held to maturity and the issuer doesn’t default, you’ll get your money back.

4. Tax Efficiency

UK government gilts are free from Capital Gains Tax, and interest from bonds can be tax-free if held within an ISA or pension.

Cons of Investing in Bonds

1. Inflation Risk

Fixed bond payments may lose value in real terms if inflation rises sharply.

2. Interest Rate Risk

When interest rates go up, bond prices usually go down. If you need to sell before maturity, you could get back less than you paid.

3. Credit Risk

With corporate bonds, there’s always a risk the company could default on payments.

4. Lower Returns Compared to Stocks

Over the long term, bonds typically offer lower returns than equities.

Who Are Bonds Suitable For?

Bonds can be a great choice if:

You’re approaching or in retirement and want regular income

You want to reduce your overall portfolio risk

You’re saving for the medium term and prefer more stability

Younger investors, or those with a higher risk appetite, may prefer a smaller bond allocation in favour of higher-growth assets like equities.

Bonds vs Dividend Investing: Which is Better?

Both bonds and dividend-paying shares (as discussed in this recent blog post) can provide regular income. But they do so in different ways, and each has its own risks and benefits.

Here’s how they compare:

Feature

Bonds

Dividend Stocks

Income Type

Fixed interest (coupon)

Variable dividend payments

Predictability

High – payments are usually fixed

Medium – dividends can fluctuate or be cut

Capital Risk

Lower if held to maturity

Higher – share prices can be volatile

Inflation Protection

Limited (unless using inflation-linked bonds)

Better – companies may increase dividends over time

Tax Treatment

Interest taxable outside ISA/SIPP

Subject to dividend tax outside ISA/SIPP*

Growth Potential

Very limited

Potential for capital gains and increasing income

Ease of Access

Widely accessible via funds or platforms

Also widely accessible via funds or direct shares

Note: *There is a tax-free personal allowance for dividend income of £500 a year (2025/26)

Which One Should You Choose?

Choose bonds if your priority is stability, capital preservation, and predictable income, especially in the short to medium term.

Choose dividend stocks if you’re comfortable with a bit more risk and want potential for both income and long-term growth.

Many investors choose to hold both as part of a diversified portfolio, using bonds for stability and equities for growth and rising income.

Final Thoughts

Investing in bonds can bring balance to your portfolio, reduce volatility and provide income. Whether you go for government gilts, corporate bonds, or a diversified bond fund, it’s important to understand the risks and benefits and how bonds fit with your investment goals.

And as always – consider holding your bonds in an ISA or pension for maximum tax efficiency.

Comparison Table: UK Bond Investment Platforms

Platform

Bond Types Available

Minimum Investment

Suitable For

ISA Available

Notes

Hargreaves Lansdown

Gilts, Corporate Bonds, Bond Funds, ETFs

£100+

Beginners to experienced investors

✅ Yes

Well-established platform with wide fund and bond choice

Unique access to high-yield bonds from major companies

Note: *As of now, WiseAlpha does not offer an ISA wrapper, so income and gains may be taxable depending on your personal circumstances.

Please bear in mind as always that I am not a registered financial adviser and cannot offer personal financial advice. You should always do your own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

If you enjoyed this post, please link to it on your own blog or social media:

I’m slightly off topic today, but it’s a subject I hope will resonate with many readers of this blog (which is, of course, aimed primarily at over-50s).

Have you ever dreamed of strumming a guitar, tickling the ivories or even giving the ukulele a go, but assumed it was too late to start? Think again. Learning to play a musical instrument offers a wide range of benefits at any age, but for older adults it can be especially rewarding.

Whether you’re newly retired with time on your hands or simply looking for a fulfilling hobby, picking up an instrument could be one of the best decisions you make. Here are just some reasons…

1. Boosts Brain Power

One of the most compelling reasons to learn an instrument later in life is the impact it can have on your brain. Playing music engages both hemispheres of the brain, stimulating areas linked to memory, attention, co-ordination and problem-solving.

Research suggests that music can help delay cognitive decline and even reduce the risk of conditions such as dementia. In other words, it’s not just fun – it’s a workout for your brain as well.

2. Improves Mental Well-being

Making music is a proven stress-buster. It encourages mindfulness, takes your mind off worries, and creates a sense of achievement. For many older adults, especially those navigating major life changes like retirement or bereavement, playing an instrument can offer comfort, purpose and emotional expression.

Even just twenty minutes of playing a day can lower levels of cortisol (the stress hormone) and lift your mood.

3. Enhances Social Connections

Music has a magical way of bringing people together. Joining a local choir, ensemble or jam session can help reduce feelings of isolation and forge new friendships. Many communities across the UK offer beginner music groups for adults – often with a focus on having fun rather than achieving perfection.

And in this digital age, it’s easier than ever to connect with fellow learners online or via apps such as YouTube, Yousician or Simply Piano.

4. It’s Never Been Easier (or Cheaper) to Get Started

You don’t need a Steinway or a Fender to begin. Many beginner-friendly instruments – like the ukulele, recorder, harmonica or keyboard – are available from under £30. Online tutorials abound, and you’ll find countless free or low-cost courses through adult education providers, community centres or your local U3A (University of the Third Age).

Libraries and music shops may also offer affordable rental options if you’re not ready to commit to buying. And community groups often have spare instruments they may be willing to lend to newbies who aren’t yet sure if this will suit them or not.

5. Physical Benefits Too

Certain instruments improve hand-eye coordination, finger strength and dexterity. Wind instruments like the clarinet or flute can also help with breath control, posture and lung function – especially beneficial for older adults.

Even setting aside time to practise regularly adds structure and movement to your daily routine, and can provide a subtle yet valuable boost to your physical activity level.

6. A Hobby That Grows With You

Unlike some pastimes, music evolves with you. Whether you’re playing nursery rhymes for your grandchildren or tackling a Chopin prelude, there’s always something new to learn. And because you can practise solo, with a partner or in a group, it’s an incredibly flexible and life-long hobby.

Five Easy Instruments to Start With

If you’re unsure where to begin, here are some popular beginner-friendly options that are perfect for older adults:

🎸 Ukulele – Lightweight, inexpensive, and easy on the fingers. Great for singalongs.

🎹 Keyboard – Perfect for learning piano basics with built-in rhythms and tutorials.

🎼 Recorder – A simple wind instrument ideal for learning to read music and control breath.

🪗 Harmonica – Pocket-sized and portable with bluesy charm.

🪕 Digital drum pad – A fun way to explore rhythm without needing a full drum kit.

Click through any of the links above [sponsored] for searches on Amazon UK for the instrument in question.

My Experience

As regular PAS readers will know, I have been a member of my local U3A for a couple of years now. When I saw they were starting a ukulele group for beginners, I decided to give it a try.

I approached the first session with considerable trepidation. I’ve always enjoyed listening to music but don’t come from a musical family. The last time I had attempted to play any instrument was the recorder at school, and it’s safe to say I didn’t display any natural aptitude for it. Initially, then, I felt well out of my comfort zone.

Very soon, however, I started to enjoy some of the benefits mentioned above. My U3A group is friendly and supportive, and we are fortunate to have an excellent (volunteer) tutor to guide us. One advantage of the ukulele is that it is actually quite easy to learn a few basic chords, and once you can do that there are literally hundreds of songs you can play. Of course, getting good on the ukulele (or any instrument) takes time and practice. But you can still have a lot of fun even if you’re not quite ready for Britain’s Got Talent!

As someone living on their own, I have also very much appreciated the social element of my ukulele group. We meet one morning a week, and I have to say it’s a highlight of my weekly schedule. As well as playing and tuition (last week we had a workshop on how to change the strings of a ukulele), there’s always time for a chat over coffee and biscuits at our mid-session break. I count several members of the group as good personal friends now.

As mentioned above, there are lots of online videos and other resources you can use to help learn an instrument. But I do highly recommend joining a group as well (or at least working with a teacher or partner). This makes learning more enjoyable and can help maintain your enthusiasm and motivation. Tutors or more experienced members may also be able to answer any questions you have and provide feedback on your playing, including any mistakes you are making. It is certainly possible to learn an instrument on your own, but in my opinion it is significantly harder and requires a lot of self-discipline.

Final Thoughts

Age should never be a barrier to creativity. In fact, many older adults find that with less time pressure and a more relaxed mindset, learning an instrument becomes a very enjoyable aspect of their lives.

So if you’ve ever fancied yourself as a secret rock star, jazz pianist or classical flautist – it’s time to stop dreaming and start playing.

The only question is: what instrument will you choose?

Have you taken up an instrument later in life? Let me know in the comments below and/or share any of your own tips for beginners!

If you enjoyed this post, please link to it on your own blog or social media:

Today I have a guest post for you from my friend Carla on behalf of the FreeStuffSpot website.

If you like getting freebies delivered regularly, as Carla explains below, this is a site you definitely need to check out!

Imagine this: You’re sitting comfortably at home, watching a movie in your pyjamas, getting cosy with a nice cuppa, when the postman suddenly brings free beauty products to your home. Sounds wonderful, doesn’t it? It might even seem unreal. But I’m here to tell you that I’ve lived the dream. Let me help you learn about freebies.

I’m a huge fan when it comes to makeup. That’s been true as far back as I can remember, and it’s not likely to ever change. I could empty an endless bank account on makeup shopping, but sadly I don’t seem to have one of those. To keep my infinite appetite for makeup satiated, I always keep my eyes and ears open for ways to save money on the best beauty products. When I discovered that I could start getting free makeup sent straight to my home, I was more than a little interested. I was exhilarated.

You might not know this now, but there are many different makeup and beauty products sent to UK homes all the time, including free hair products, toiletries, perfume samples, and cosmetics. Think about it. You can try a current or new brand, all without spending any cash, or even leaving your home! Can it get better than that? Here are my insights about using FreeStuffSpot to get free makeup and beauty products on top of other freebies I already enjoy.

Why Are Beauty Brands Giving Free Stuff Away?

Businesses are always trying to get prospective customers to try out their products or brands in exchange for some feedback. These arrangements bypass the middlemen that normally do market research. Given how many businesses are moving towards the social media giants, namely Facebook and Twitter/X at least, they now can speak directly to consumers while listening to their concerns.

They can also reach out to many new customers at the same time.

So How Do You Get Free Beauty Products Of Your Own?

It’s not hard. I just registered for a newsletter from FreeStuffSpot, guaranteed to have nine brand-new freebies every single day. This newsletter covers things from free samples, competitions, and just generally free stuff. The day after I signed up for the newsletter, I got an email with giveaways, offers, and even restaurant vouchers.

What Other Kinds Of Freebies Are Available?

The website has more categories than just the beauty products I love and adore. You can find food and beverage, kids and baby stuff, free pet things, and freebies for just about anyone in your home. You don’t want to keep such a great thing to yourself, right?

FreeStuffSpot doesn’t just do freebies. They also have tricks to save money, advice on how to make money, and tips about getting more savvy in terms of money overall. The next time I plan to eat out, I’ll be using the page for restaurant vouchers for sure. The free days out category is great for us as a family, since we have young ones that love being out where it’s open. We can have a fun family day outside our home without emptying our bank account.

I’ve also joined the fan group for FreeStuffSpot enthusiasts. This perky community is a place where members post pics of the freebies they get. Sure, some of it is bragging, but it’s also about letting everyone else know about freebies and offers they don’t yet know about.

Just How Easy Is It To Use FreeStuffSpot?

If you want to start enjoying freebies, it’s very simple:

Visit the website at FreeStuffSpot and register to receive their daily newsletter full of freebies.

Browse the website and then apply for freebies you like the sound of.

Then just wait for the freebies to show up at your home!

My Verdict Is In…

I’ve really enjoyed looking through FreeStuffSpot since I started writing online. I’ve already got a perfume sample that I fell in love with, to the point of buying the actual full-size product. I’ve also got a tea towel, face wipes, and even teabags!

Many thanks to Carla for her enthusiastic endorsement of FreeStuffSpot. If you’re a freebies fan I hope you will take a moment to check out the site for yourself.

As always, if you have any comments or questions about this article, please do post them below.

This is a sponsored guest post.

If you enjoyed this post, please link to it on your own blog or social media:

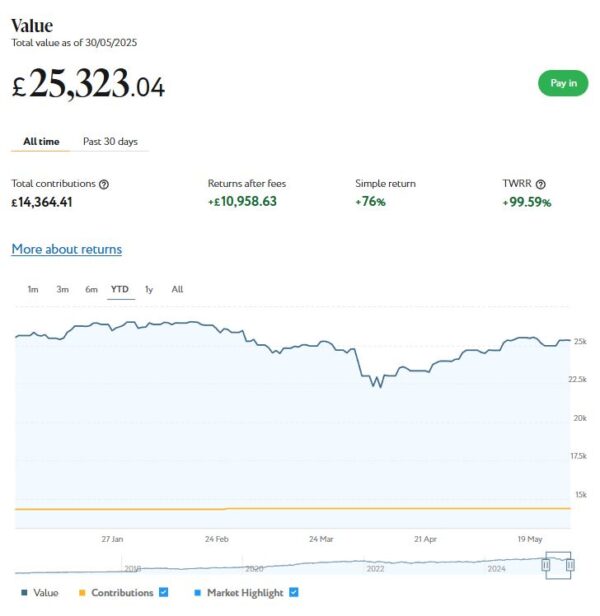

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

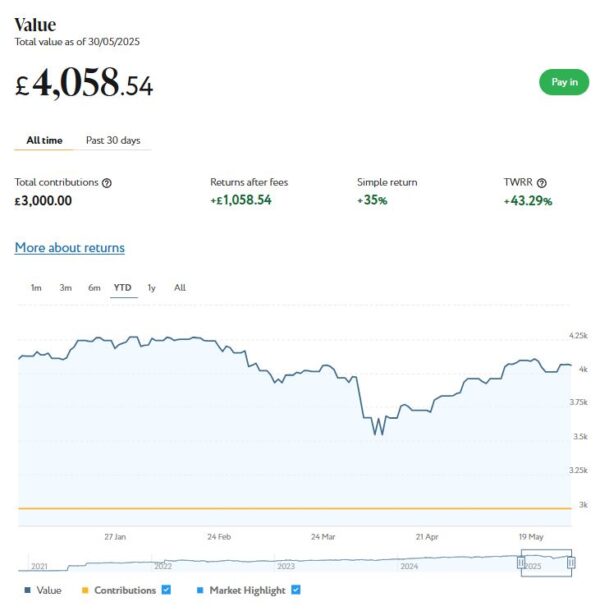

As the screenshot below for the year to date shows, my main Nutmeg portfolio is currently valued at £25,323. Last month it stood at £24,532, so that is a rise of £791.

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £4,059 (rounded up) compared with £3,934 a month ago, a rise of £125. Here is a screen capture showing performance for the year to date.

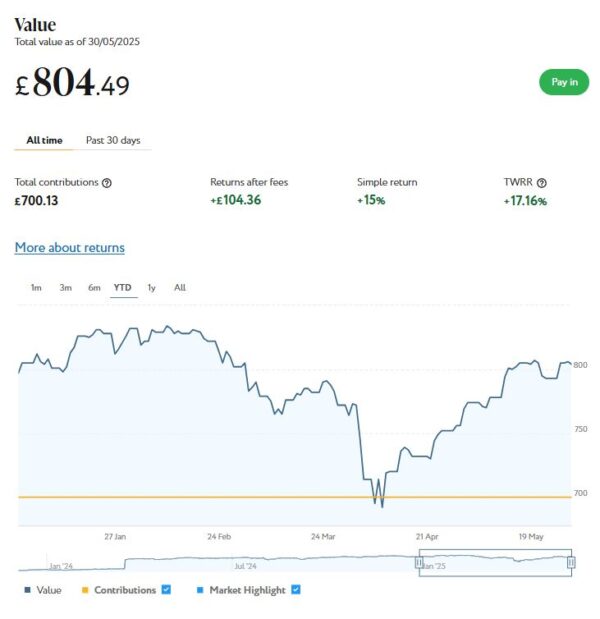

Finally, at the start of December 2023 I invested £500 in one of Nutmeg’s new thematic portfolios (Resource Transformation). In March 2024 I also invested a further £200 from referral bonuses. As you can see from the YTD screen capture below, this portfolio is now worth £804 compared with £770 last month, a rise of £34.

As you can see, May was a good month for my Nutmeg investments. Overall I was up by £950 or 3.25%.

I am still down slightly since the start of 2025, with the value of my investments decreasing by £242 or 0.08% since 1st January. On the other hand, their value has grown by £1,813 or 6.39% since the end of May last year. So, as I always say, the recent ups and downs do need to be taken in context. Some volatility is always to be expected with stock market investments, and over time they tend to even out. In general the worst thing you can do is panic and sell up when downturns occur (as happened in early April). You are then crystallizing your losses rather than giving the markets time to recover. This is something I had cause to discuss recently in this blog post.

You can read my full Nutmeg review here. If you are looking for a home for your annual ISA allowance, based on my overall experience over the last eight years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs), Lifetime ISAs and Junior ISAs as well.

Moving on, I also have investments with P2P property investment platform Assetz Exchange. As discussed in this recent post, the company recently rebranded as Housemartin.

My investments with Housemartin continue to generate steady returns. Housemartin focuses on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my HM portfolio has generated a respectable £251.16 in revenue from rental income. I have also made a net profit of £0.57 on property disposals. Capital growth has slowed, though, in line with UK property values generally.

At the time of writing, 16 of ‘my’ properties are showing gains, 3 are breaking even, and the remaining 18 are showing losses. My portfolio of 37 properties is currently showing a net decrease in value of £47.34. That means that overall (rental income and profit on disposal minus capital value decrease) I am up by £204.39. That’s still a decent return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Housemartin most projects are socially beneficial as well.

The net fall in capital value of my Housemartin investments is obviously a little disappointing. But it’s important to remember that until/unless I choose to sell the investments in question, it is largely theoretical, based on the latest price at which shares in the property concerned have changed hands. The rental income, on the other hand, is real money (which in my case I’ve reinvested in other HM projects to further diversify my portfolio).

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of Housemartin as far as i am concerned. You can actually invest from as little as £1 per property if you really want to proceed cautiously.

As I noted in this blog post, Housemartin is particularly good if you want to compound your returns by reinvesting rental income. This effectively boosts the interest rate you are receiving. Personally, once I have accrued a minimum of £10 in rental payments, I reinvest this money in either a new HM project or one I have already invested in (thus increasing my holding). Over time, even if I don’t invest any more capital, this will ensure my investment with Housemartin grows at an accelerating rate and becomes more diversified as well.

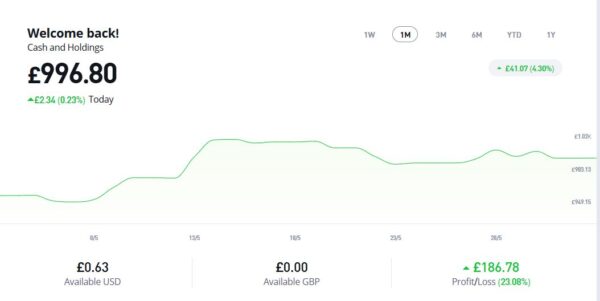

In 2022 I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios, Oil Worldwide. I also invested a small amount I had left over in Tesla shares.

As you can see from the screen captures below, my original investment (total value £888.36 in pounds sterling) is today worth £996.80, an overall increase of £108.44 or 12.21%.

Note: eToro now displays the value of investments in your native currency, although you can change this if you wish.

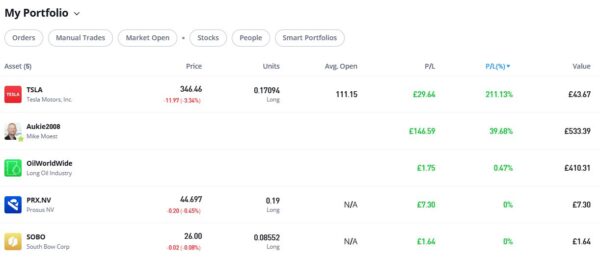

As you can see, my Oil WorldWide investment has recovered a bit since last time and is at least back in profit now, although it’s not exactly setting the world on fire (excuse the bad joke).

Thankfully my copy trading investment with Aukie2008 has been doing better, with an overall 39.64% profit. To be fair, I have held this investment a little longer.

My Tesla shares, which I bought as an afterthought with a bit of spare cash I had in my account, have done particularly well since I bought them, with an overall profit of 211.13%. If only I had put a bit more money into this! As a matter of interest, I do find it quite strange that my Tesla shares keep going up in value, despite all the stories in the press and social media about consumers boycotting Tesla. Go figure.

You might also notice that I have small holdings in Prosus NV, a Dutch internet group, and South Bow, a Canadian energy infrastructure company. To be honest I don’t understand how I acquired these, but I assume they are some sort of bonus I was awarded. In any event, I am happy to have them in my portfolio!

eToro also offer the free eToro Money app. This allows you to deposit money to your eToro account without paying any currency conversion fees, saving you up to £5 for every £1,000 you deposit. You can also use the app to withdraw funds from your eToro account instantly to your bank account. I tried this myself and was impressed with how quickly and seamlessly it worked. You can read my blog post about eToro Money here. Note that it can also serve as a cryptocurrency wallet, allowing you to send and receive crypto from any other wallet address in the world.

If you would like more information about setting up an eToro account, please click on this no-obligation website link [affiliate]. Don’t forget that you also get a free $100,000 virtual portfolio, which you can use to experiment with trading and investing strategies. I have certainly earned a lot from mine.

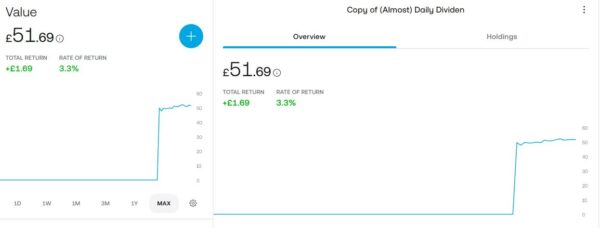

As a bit of an experiment, I recently put £50 into an investment ISA with Trading 212. As mentioned in my recent blog post about dividend investing, I put it into the (Almost) Daily Dividends Portfolio, a ready-made portfolio or ‘pie’ on Trading 212. As you can see from the screen capture below, my portfolio is now worth £51.69, an increase of 3.3% over the two-month period. It has even accrued a grand total of 9p in dividends!

I am quite impressed with how this investment has been faring, despite the small amount I put in (which means I may be missing out on some smaller dividends) and also because you need to have held shares for a certain period to qualify for dividend payments. If I increased my investment I would almost certainly become eligible for more dividends, and would qualify for more the longer I remain invested. If I had any spare money at the moment, I would certainly consider doing this!

Moving on, I published various posts on Pounds and Sense in May. I have listed below those that are still relevant

Why a Financial Remedy Order is Essential on Your Divorce is another guest post from my friends at HCR Law. If you are unfortunate enough to be in this position, this article contains important advice and information on how to ensure your personal financial security going forward.

Where to Get Pension Advice contains important information for anyone who may be coming up to retirement age, which of course includes many Pounds and Sense readers. This collaborative article includes details of six potential sources of pension advice, including the pros and cons of each.

Could You Benefit From Help to Save spotlights a lesser-known government scheme which, if you’re eligible, can give your finances a valuable boost. It’s an initiative aimed at helping people on low incomes (typically those receiving Universal Credit) build up their savings. Offering generous tax-free bonuses, this scheme can provide significant benefits for qualifying individuals.

How to Save Money on Rail Fares With Split Ticketing discusses a money-saving hack that savvy travellers can use to reduce their rail-fare costs – often by a substantial margin. Split ticketing involves breaking a journey into two or more smaller segments, purchasing separate tickets for each segment rather than one through-ticket. With the help of apps such as those discussed in the article, the process becomes simple and automated.

Finally, in What Are ETFs And How Can You Invest in Them? I shine a spotlight on these increasingly popular investment vehicles, explaining what they are, how you can invest in them, and how you can maximize the benefit by investing via tax-free ISAs.

I’ll close with a reminder that you can also follow Pounds and Sense on Facebook or Twitter (or X as we have to call it now). Twitter/X is my number one social media platform and I post regularly there. I share the latest news and information on financial matters, and other things that interest, amuse or concern me. So if you aren’t following my PAS account on Twitter/X, you are definitely missing out.

I am also on the BlueSky social media network under the username poundsandsense.bsky.social. Twitter/X remains my primary social media platform, but I will also post details of my latest blog posts, third-party articles and other financial news and resources on BlueSky for those who prefer to follow me there.

As always, if you have any comments or questions, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts on PAS may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media: