In case you’ve not heard, Amazon Prime Big Deals Day is almost with us. It extends over two days, Tuesday 7th and Wednesday 8th October 2025.

This is a special event for Amazon Prime members only. Amazon say they will be offering members their lowest prices of the year on selected products across a wide range of categories, from consumer electronics to groceries.

Some of the best deals will be reserved for Amazon’s own products, such as their Kindle e-book readers, Amazon Echo smart speakers and Ring video doorbells and security cameras. Discounts of up to 60% will be on offer for these products. If you’re thinking of buying any of them, Amazon Prime Big Deals Day is definitely the day – or two days – to do it.

There are also some great ‘early deals’ available now. For example, at the time of writing you can buy an Oral-B iO2 electric toothbrush for just £41.99, a 58% discount on the normal price of £100.

I have been a member of Amazon Prime for over ten years now. As a regular Amazon shopper, I find it well worth while for the free one-day delivery on millions of items alone. But as a Prime member you get access to a host of other benefits and services as well, including Amazon Prime Music and Amazon Prime Video.

If you’re thinking of joining Amazon Prime, therefore, I highly recommend doing it in the next few days, so you can benefit from the Prime Big Deals Day offers. Personally I think it’s worth it for the free delivery alone, let alone everything else that’s on offer. But if you wish, you can get a 30-day free trial now, take advantage of the Prime Big Deals Day offers, and then cancel without owing any money. It’s your choice!

You can also see all the latest Prime Big Deals Day offers by clicking here.

As always, if you have any comments about Amazon Prime or Prime Big Deals Day, please do post them below.

Disclosure: This post includes affiliate links. If you click through and make a purchase, I may receive a commission for introducing you. This will not affect the price you pay or the products or services you receive.

If you enjoyed this post, please link to it on your own blog or social media:

Free Wills Month brings together a group of well-respected charities to offer members of the public aged 55 and over the opportunity to have their wills written or updated free using participating solicitors across the UK.

The charities involved include the NSPCC, Dogs Trust, Samaritans, Mind, Age UK, The Stroke Association, PDSA, and many others. Free Wills Month happens twice a year, in March and October.

The scheme covers simple wills only, including ‘mirror wills’ for couples. In the latter case, only one member of the couple has to be 55 or over. If you need a complicated will (most people don’t) you can still have this done but may have to pay a top-up fee.

I have talked about the importance of creating a will and why you should get it done by a properly qualified solicitor previously on PAS. An up-to-date will written by a solicitor will ensure that your wishes are respected and will avoid causing legal complications for your loved ones after you are gone.

Free Wills Month means what it says. There are no catches, although the organizers hope that you will choose to leave a donation to charity in your will. There is no obligation to do this, however.

To take part in Free Wills Month click through to the website during October and fill in your details. You can then pick a solicitor from the list of companies taking part and contact them to book an appointment. Appointments are limited and on a first come, first served basis, so it’s best to apply as soon as possible to avoid disappointment.

Free Wills Month October 2025 starts officially on Wednesday 1st October 2025 but you can sign up on the FWM website to be notified when when the campaign starts in your area.

If you have any comments or questions about this subject, as ever, please do post them below.

Note: This is a revised and updated version of my original post on this subject.

If you enjoyed this post, please link to it on your own blog or social media:

Today I have a guest post for you on a subject many of us wonder about. It’s by Primrose Freestone, Senior Lecturer in Clinical Microbiology at theUniversity of Leicester.

Most of us spend around a third of our lives in bed. Sleep isn’t just downtime; it’s essential for normal brain function and overall health. And while we often focus on how many hours we’re getting, the quality of our sleep environment matters too. A clean, welcoming bed with crisp sheets, soft pillowcases and fresh blankets not only feels good, it also supports better rest.

But how often should we really be washing our bed linens?

According to a 2022 YouGov poll, just 28% of Brits wash their sheets once a week. A surprising number admitted to leaving it much longer, with some stretching to eight weeks or more between washes. So what’s the science-backed guidance?

Let’s break down what’s actually happening in your bed every night – and why regular washing is more than just a question of cleanliness.

Get your news from actual experts, straight to your inbox.Sign up to our daily newsletter to receive all The Conversation UK’s latest coverage of news and research, from politics and business to the arts and sciences.

That fresh sweat may be odourless, but bacteria on our skin, particularly staphylococci, break it down into smelly byproducts. This is often why you wake up with body odour, even if you went to bed clean.

But it’s not just about microbes. During the day, our hair and bodies collect pollutants, dust, pollen and allergens, which can also transfer to our bedding. These can trigger allergies, affect breathing, and contribute to poor air quality in the bedroom.

Dust mites, fungi and other unseen bedfellows

The flakes of skin we shed every night become food for dust mites – microscopic creatures that thrive in warm, damp bedding and mattresses. The mites themselves aren’t dangerous, but their faecal droppings are potent allergens that can aggravate eczema, asthma and allergic rhinitis.

If you sleep with pets, the microbial party gets even livelier. Animals introduce extra hair, dander, dirt and sometimes faecal traces into your sheets and blankets, increasing the frequency at which you should be washing them.

So, how often should you wash your bedding?

Sheets and pillowcases

When: Weekly, or every three to four days if you’ve been ill, sweat heavily, or share your bed with pets.

Why: To remove sweat, oils, microbes, allergens and dead skin cells.

How: Wash at 60°C or higher with detergent to kill bacteria and dust mites. For deeper sanitisation, tumble dry or iron. To target dust mites inside pillows, freeze for at least 8 hours.

Mattresses

When: Vacuum at least weekly and air the mattress every few days.

Why: Sweat increases moisture levels, creating a breeding ground for mites.

When: Every two weeks, or more often if pets sleep on them.

Why: They trap skin cells, sweat and allergens.

How: Wash at 60°C or as high as the care label allows. Some guidance recommends treating these like towels: regular and hot washes keep them hygienic.

Duvets

When: Every three to four months, depending on usage and whether pets or children share your bed.

Why: Even with a cover, body oils and mites eventually seep into the filling.

How: Check the label: many duvets are machine-washable, others may require professional cleaning.

Your bed may look clean – but it’s teeming with microbes, allergens, mites and irritants that build up fast. Washing your bedding isn’t just about keeping things fresh; it’s a matter of health.

Regular laundering removes the biological soup of sweat, skin, dust and microbes, which helps to reduce allergic reactions, prevent infections and keep odours at bay. And as research continues to show the profound effect of sleep on everything from heart health to mental clarity, a hygienic sleep environment is a small but powerful investment in your wellbeing.

So go ahead – strip the bed. Wash those sheets. Freeze your pillows. Your microbes (and your sinuses) will thank you.

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

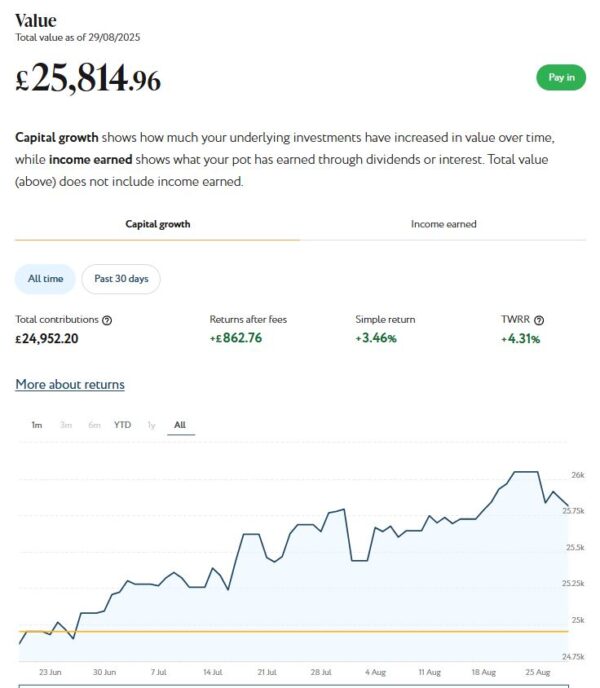

As regular readers will know, in June I transferred most of the money in my Nutmeg Fully Managed portfolio (just under £25,000) to a new Nutmeg Income Portfolio. I discussed this in detail in this recent post, but basically money in this port is invested to generate an income from share dividends and other sources. This is then paid monthly. Capital appreciation is targeted as well, but these portfolios are aimed primarily at older people (and others) who want/need their investment to generate a regular cash income.

In August my Nutmeg income portfolio generated £134.03 of income, which was duly paid in to my bank account on 22 August 2025. Based on Nutmeg’s estimated annual return of just under 5% for income ports at my chosen risk level (five), I had been expecting around £100, so this was somewhat better than that. Obviously it is far too early to draw any conclusions, though.

My income portfolio has also grown a little in value in August. It’s now worth £25,815 compared with £25,793 at the start of last month, an increase of £22. As the screen capture shows, the port has actually grown in value by £862.76 (3.46%) since I opened it.

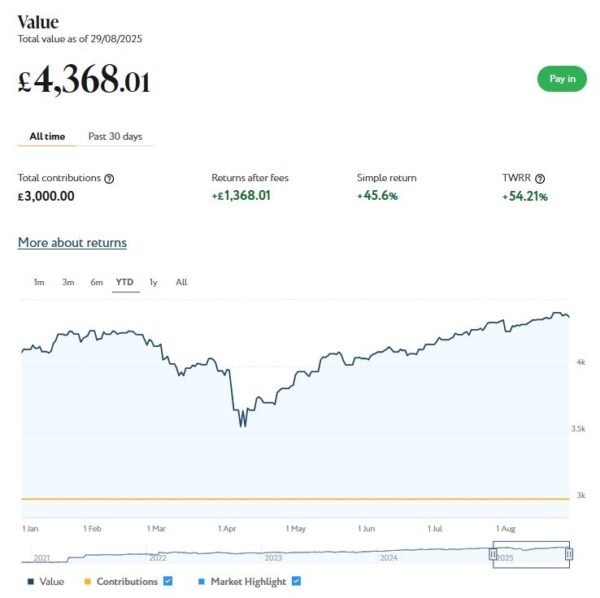

I still have a smaller, growth-oriented pot using Nutmeg’s Smart Alpha option. This is now worth £4,368 compared with £4,346 a month ago, a rise of £22. Here is a screen capture showing performance for the year to date.

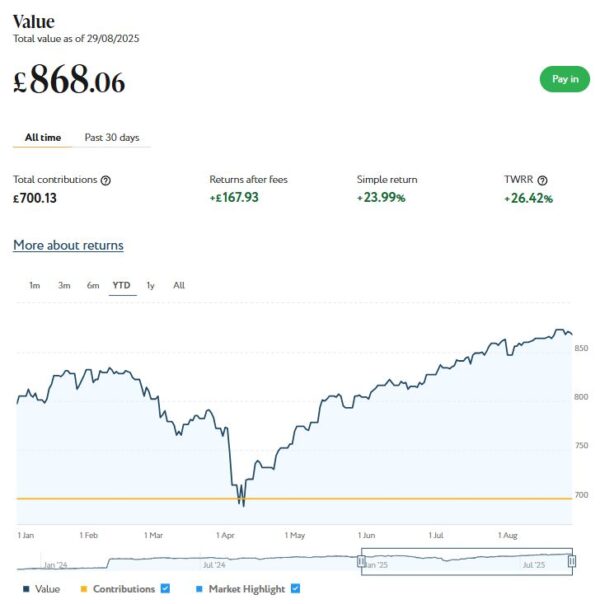

And at the start of December 2023 I invested £500 in one of Nutmeg’s thematic portfolios (Resource Transformation). In March 2024 I also invested a further £200 from referral bonuses (something I no longer receive for reasons I won’t bore you with). As you can see from the YTD screen capture below, this portfolio is now worth £868 compared with £863 last month, a rise of £5.

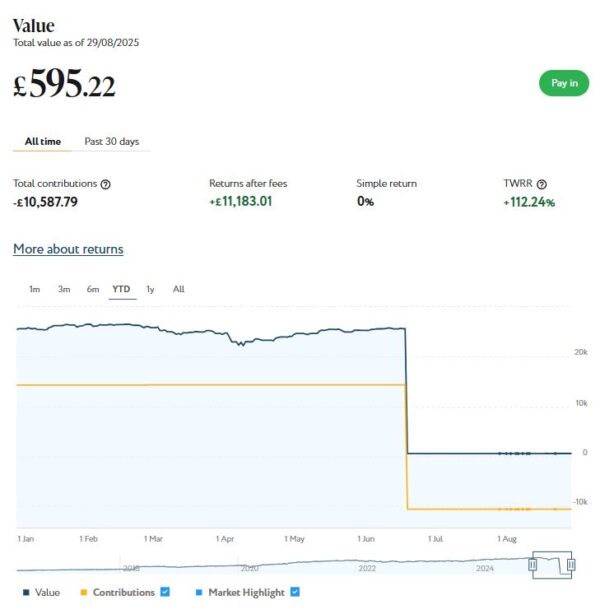

Finally, I still have a small amount left in my original Nutmeg Fully Managed portfolio. I have kept this largely for comparison purposes. This has increased in value from £594 at the start of August to £595 now, a rise of £1.

As you can see, August was a steady, if unexciting, month for my Nutmeg investments. Overall I was up by £50 or 0.16%. In addition I did, of course, receive £134.03 in income from my income portfolio.

Excluding income generated, the overall value of my Nutmeg investments is up by £1,218 since the start of 2025, so the April 2025 fall (caused largely by Trump’s tariffs) has now fully reversed. I am also up by £2,413 or 7.48% since the start of September last year, again excluding cash income received. All things considered, that’s not a bad result.

As I always have to say, some volatility is to be expected with stock market investments, but over the longer term they tend to even themselves out (and generally perform better than bank savings accounts, although that is never guaranteed). In general the worst thing you can do is panic and sell up when downturns occur (as happened in April this year). You are then crystallizing your losses rather than giving the markets time to recover. This is something I had cause to discuss in this blog post from earlier this year.

You can read my full Nutmeg review here. If you are looking for a home for your annual ISA allowance, based on my overall experience over the last nine years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs), Lifetime ISAs and Junior ISAs as well.

Moving on, I also have investments with P2P property investment platform Assetz Exchange. As discussed in this post, the company has rebranded as Housemartin.

My investments with Housemartin continue to generate steady returns. Housemartin focuses on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my HM portfolio has generated a respectable £266.87 in revenue from rental income. I have made a small net loss of £19.02 on property disposals. Capital growth generally has slowed, in line with UK property values generally.

At the time of writing, 16 of ‘my’ properties are showing gains, 3 are breaking even, and the remaining 19 are showing losses. My portfolio of 38 properties is currently showing a net decrease in value of £59.59. That means that overall (rental income minus capital value decrease and loss on disposal) I am up by £188.26. That’s still a respectable return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Housemartin most projects are socially beneficial as well.

The net fall in capital value of my Housemartin investments is obviously a little disappointing. But it’s important to remember that until/unless I choose to sell the investments in question, it is largely theoretical, based on the latest price at which shares in the property concerned have changed hands. The rental income, on the other hand, is real money (which in my case I’ve reinvested in other HM projects to further diversify my portfolio).

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of Housemartin as far as i am concerned. You can actually invest from as little as £1 per property if you really want to proceed cautiously.

As I noted in this blog post, Housemartin is particularly good if you want to compound your returns by reinvesting rental income. This effectively boosts the interest rate you are receiving. Personally, once I have accrued a minimum of £10 in rental payments, I usually reinvest this money in either a new HM project or one I have already invested in (thus increasing my holding). Over time, even if I don’t invest any more capital, this will ensure my investment with Housemartin grows at an accelerating rate and becomes more diversified as well.

In 2022 I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios, Oil Worldwide. I also invested a small amount I had left over in Tesla shares.

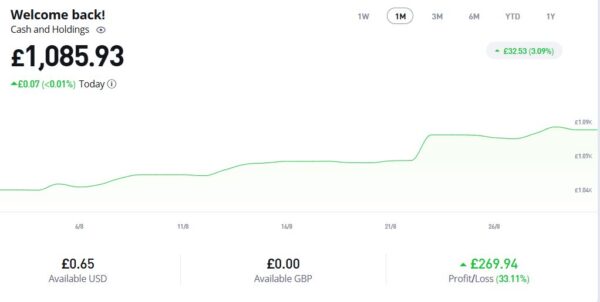

As you can see from the screen captures below, my original investment (total value £888.36 in pounds sterling) is today worth £1,085.93, an overall increase of £197.57 or 22.24%.

Note: eToro now displays the value of investments in your native currency, although you can change this if you wish.

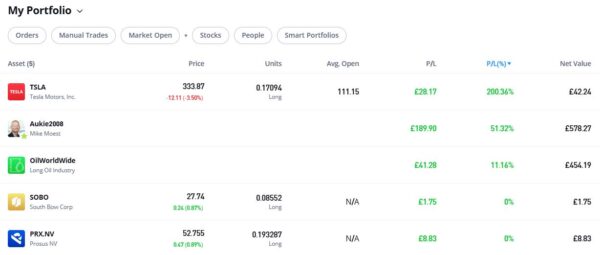

As you can see, my Oil WorldWide investment is in profit, though at 11.14% it is nothing too exciting. My copy trading investment with Aukie2008 has been doing better, with an overall 51.32% profit. To be fair, I have held this investment a bit longer.

My Tesla shares, which I bought as an afterthought with some spare cash I had in my account, are up again this month. They are showing an impressive overall profit of 200.36% since I bought them. If only I had put a bit more money into this!

You might also notice that I have small holdings in Prosus NV, a Dutch internet group, and South Bow, a Canadian energy infrastructure company. To be honest I don’t understand how I acquired these, but I assume they are some sort of bonus I was awarded. In any event, I am happy to have them in my portfolio.

eToro also offer the free eToro Money app. This allows you to deposit money to your eToro account without paying any currency conversion fees, saving you up to £5 for every £1,000 you deposit. You can also use the app to withdraw funds from your eToro account instantly to your bank account. I tried this myself and was impressed with how quickly and seamlessly it worked. You can read my blog post about eToro Money here. Note that it can also serve as a cryptocurrency wallet, allowing you to send and receive crypto from any other wallet address in the world.

If you would like more information about setting up an eToro account, please click on this no-obligation website link [affiliate]. Don’t forget that you also get a free $100,000 virtual portfolio, which you can use to experiment with trading and investing strategies. I have certainly earned a lot from mine.

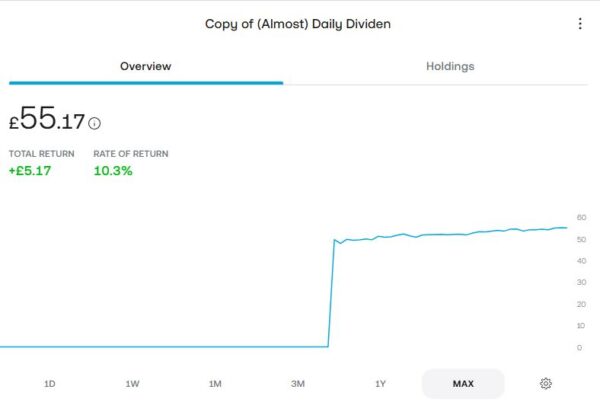

As an experiment, I recently put £50 into an investment ISA with Trading 212. As mentioned in my recent blog post about dividend investing, I put it into the (Almost) Daily Dividends Portfolio, a ready-made portfolio or ‘pie’ on Trading 212. As you can see from the screen capture below, my portfolio is now worth £55.17, an increase of £5.17 or 10.3% over the four-month period. It has even accrued a grand total of 38p in dividends!

I am quite impressed with how this investment has been faring, despite the small amount I put in (which means I may be missing out on some smaller dividends). If I increased my investment I would almost certainly become eligible for more dividends, and even more the longer I remain invested. If I had any spare money at the moment, I would consider doing this. Of course, I do now have an income-focused portfolio with Nutmeg as well (see above).

Moving on, I published various posts on Pounds and Sense in August. I have listed below those that are still relevant.

In Here’s Why I’m Not a Fan of FIRE I talked about the Financial Independence, Retire Early (FIRE) movement and explained why I am not an aficionado. I set out various reasons, including the impossibility of planning and predicting your life twenty or thirty years into the future.

In Could a Smart Thermostat Save You Money? I explained what these devices are and set out some hints and tips for making the most of them. I also discussed my own experience with a Hive smart thermostat.

In How to Check Your Tax Code and Correct it if Necessary I explained how to check this important piece of financial data. I revealed what the code means and what you should do if you believe yours is wrong. In my view everyone should check their tax code, as if it’s incorrect you may be paying too much tax or, conversely, too little. In the latter case you will still have to pay the tax when the error is discovered, potentially with added interest as well.

How Over-50s Can Save and Make Money Using Vinted discusses this very popular buying-and-selling platform among younger people. In the article I point out that Vinted can be an invaluable resource for older folk as well. I explain how it works and set out some hints and tips for making the most of it.

Finally, in Dividend Investing vs Total Return: Which Works Best for Income Investors? I look at these two popular approaches to drawing an income from your investments. Of course, this is something many retired and semi-retired people want (or need) to do. I compare the pros and cons of each method and discuss my personal experience.

I’ll close with a reminder that you can also follow Pounds and Sense on Facebook or Twitter (or X as we have to call it now). Twitter/X is my number one social media platform and I post regularly there. I share the latest news and information on financial matters, and other things that interest, amuse or concern me. So if you aren’t following my PAS account on Twitter/X, you are definitely missing out!

I am also on the BlueSky social media network under the username poundsandsense.bsky.social. Twitter/X remains my primary social media platform, but I also post details of my latest blog posts, third-party articles and other financial news and resources on BlueSky for those who prefer to follow me there.

As always, if you have any comments or questions, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts on PAS may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media: