Free Wills Month brings together a group of well-respected charities to offer members of the public aged 55 and over the opportunity to have their wills written or updated free using participating solicitors across the UK. The next one begins on Monday 2nd March 2026.

The charities involved include the NSPCC, Dogs Trust, Help for Heroes, Mind, Stroke Association, PDSA, Royal British Legion, Alzheimers Research UK, Mencap, British Heart Foundation, Age UK, and so on. You can see all the charities involved on this web page.

The scheme covers simple wills only, including ‘mirror wills’ for couples. In the latter case, only one member of the couple has to be 55 or over. If you need a complicated will (most people don’t) you can still have this done but may have to pay a top-up fee.

I strongly believe in using a properly qualified solicitor to draw up your will. In the last few years there have been a couple of occasions when failing to do this has caused problems and delays for members of my family. An up-to-date will written by a solicitor will ensure that your wishes are respected and will avoid causing legal complications for your loved ones after you are gone.

Free Wills Month means what it says. There are no catches, although the organizers obviously hope that you will choose to leave a donation to charity in your will. There is no obligation to do this, however.

To take part in Free Wills Month click through to the website on or after March 2nd 2026. You can then pick a solicitor from the list of companies taking part and contact them to book an appointment. Appointments are limited and on a first come, first served basis, so it’s important to call as soon as possible. Once all available appointments are taken, the campaign will close. This may happen before the end of March.

Until March 2nd you can enter brief details on the Free Wills Month website and will then receive an email reminder when the scheme opens.

If you have any comments or questions about this subject, as ever, please do post them below.

This is an annual update of this post.

If you enjoyed this post, please link to it on your own blog or social media:

In a recent post I talked about How to Save Money on Cruise Holidays. One or two people asked if I had any specific advice on river cruises, so today I thought I would address this subject.

River cruising has become one of the fastest-growing travel trends in recent years, and it’s not hard to see why. With scenic routes that wind through historic towns, a gentle pace, boutique ships and inclusive experiences, river cruises can feel like a dream holiday. But are they right for you?

In this post, I will explore the pros and cons of river cruising – particularly for older travellers – and share some tips to help you get the best value for money.

🌊 What Is a River Cruise?

Unlike ocean cruises that traverse vast stretches of sea, river cruises sail inland waterways – think the Danube, Rhine, Seine, Douro, Nile or Volga. Ships are typically smaller, with fewer passengers and a focus on cultural immersion and sightseeing.

👍 Pros of River Cruises

1. Gentle Pace & Easy Exploration

River cruises are designed for relaxation, with stops in multiple towns and cities. You often disembark right in the heart of destinations – no long transfers from ports. This is ideal for older travellers who want culture without stress.

2. All-Inclusive Comfort

Most river cruise packages include meals, onboard entertainment and guided excursions. Fewer hidden costs mean easier budgeting – a big plus if you’re watching the pounds and pence.

3. Accessible & Stress-Free

Ships have fewer stairs and lots of public open space. Many cabins and facilities are designed for accessibility, which suits older passengers or anyone with mobility issues.

4. Scenic Days & Scenic Nights

You rarely miss a view, cruising through vineyards, past castles and alongside charming villages. It’s like a constantly changing hotel window.

5. Sociable but Calm Atmosphere

With smaller ships and more mature crowds, river cruising tends toward a relaxed, sociable vibe without the “big ship” bustle.

👎 Cons of River Cruises

1. Higher Cost per Day

River cruises are often more expensive per person, per day than equivalent ocean cruises or land tours – especially during peak seasons.

2. Smaller Cabins

Space is at a premium. Cabins can feel compact – which might be uncomfortable if you like extra room.

3. Limited Onboard Activities

If you crave night-time entertainment, water-slides or casinos, river cruising might feel too sedate. It’s more about sightseeing than onboard spectacle.

4. Mobility Needed for Excursions

Most shore excursions involve walking tours. While many are gentle, some may not be suitable for travellers with limited mobility unless you choose accessible options.

5. Seasonal & Weather Dependent

River levels vary with the weather. Drought or heavy rain can affect itineraries – something to keep in mind when planning.

💡 River Cruise Tips – Get the Best Value for Money

If a river cruise sounds appealing, here’s how to make sure it’s a smart financial decision:

1. Book Early – Or Last-Minute

Booking early often secures the best cabins and lower prices. But some lines also discount last-minute sailings to fill unsold berths. Stay flexible and watch for deals.

2. Choose Shoulder Seasons

Travelling in spring or autumn often means lower prices, fewer crowds and milder weather — great for cost-conscious explorers.

3. Compare Inclusions

Don’t just look at headline prices. Check what’s included. Flights, transfers, excursions and drinks packages can add up.

A slightly higher headline price with lots included may represent better value overall.

4. Compare direct vs agent pricing

Sometimes booking directly with the cruise line is cheaper; other times a specialist agent will have better exclusive rates.

5. Fly from Regional Airports

River cruise packages often include flights. Compare prices from regional UK airports — you may find cheaper deals than London departures.

6. Consider Solo or Shared Cabins

Some lines offer solo cabins or shared spaces that can be more affordable if you’re travelling alone.

7. Use Loyalty Programmes & Travel Agents

Cruise line loyalty programmes can bring discounts, upgrades or onboard credits. Specialist cruise agents often know about promotions that aren’t publicised online.

8. Plan Your Excursions Wisely

Shore excursions arranged through the cruise can be expensive. Look into local guides or self-guided tours where safe and feasible.

🛳️ How to Book Your River Cruise (and Where to Find Deals)

Booking a river cruise might seem daunting at first – there are many companies, rivers, dates and price points to choose from. But with a bit of know-how and the right resources, you can find great value and a cruise that suits your travel style and budget.

🌐 Specialist River Cruise Websites (UK Focused)

For many UK travellers, booking through a river cruise specialist can be one of the easiest ways to find the best deals and get expert advice:

RiverCruising.co.uk – A UK-based specialist agent offering cruises from a range of operators, with ABTA and ATOL protection and support in choosing the best itinerary for you.

GlobalRiverCruising.co.uk – Independent UK specialists focused on delivering tailored itineraries and exclusive savings across multiple top cruise brands.

Blue Water Holidays / CruisingHolidays.co.uk – UK travel agencies that cover river and small-ship cruises with plenty of detailed itineraries, customer reviews and exclusive deals.

LoveitBookit.com – Another trusted UK cruise agency where you can explore river cruise options and get personalised support from cruise experts.

These specialist sites often bundle flights, transfers and insurance into your holiday package and can help you navigate which cruise line and dates are best for your budget.

💻 Discount and Deal Sites

If you’re hunting for current deals and discounts, here are a few places worth checking regularly:

Wowcher – Offers curated travel deals, including discounted river cruise holidays in Europe.

Cruise comparison sites like Cruise1st also list special seasonal offers and upgrades on river cruise itineraries.

💡 Pro tip: Sign up for newsletters from these sites and the cruise lines themselves — many discount offers (especially early-bird or seasonal sales) go out first to email subscribers.

🚢 Leading River Cruise Companies for UK Travellers

Here are some of the most popular and reputable river cruise operators you might consider when booking:

🌍 Major International River Cruise Lines

Viking River Cruises – One of the best-known names in river cruising, with a wide range of European itineraries and good UK-specific resources.

AmaWaterways – Highly regarded for quality service, food, and wine, with promotional offers on many routes.

Emerald Cruises – Offers strong value deals with flights and extras sometimes included, plus seasonal discounts.

Amadeus River Cruises – A traditional European operator focused on elegant boutique-style river experiences.

CroisiEurope – A family-run French line with a vast range of European river routes and good mid-range pricing.

Saga River Cruises – A UK-focused operator tailored for travellers over 50, offering all-inclusive European river cruises with added UK perks such as included chauffeur services and local departures.

📍 How They Work for UK Travellers

Many of these companies have UK-specific websites and/or call centres and offer flight-inclusive packages departing from UK airports.

Booking early – often 12–18 months ahead – can secure the best cabins and prices, as river cruises tend to sell out popular routes well in advance. (Cruise community insights also suggest booking early rather than waiting for last-minute deals due to limited capacity.)

💭 Closing Thoughts: Is a River Cruise Worth It?

If you love scenic travel, cultural immersion and a relaxed pace – and you’re willing to pay a bit more for convenience and comfort – river cruising can be an unforgettable experience. For older travellers, the accessibility, ease and inclusive nature are major advantages.

But if you’re after huge ships with lots of entertainment or travel on a tight budget, alternative holiday types (like escorted tours or independent travel) might suit you better.

Ultimately, it comes down to your travel priorities, mobility and budget. With smart planning and savvy spending, a river cruise can be both affordable and deeply rewarding.

Have you tried a river cruise yourself and would you recommend it? Have any other tips for saving money or making the most of your holiday? Please do leave a comment below!

If you enjoyed this post, please link to it on your own blog or social media:

Today I have a guest post on a subject close to many people’s hearts (including mine!) – what are the benefits (and risks) of coffee drinking and how much a day is best?

This subject may be of particular interest to older people, as the latest research indicates that the caffeine in coffee (and tea) may offer some protection from dementia.

Scientists have found that drinking two to three cups of coffee a day may significantly reduce your risk of developing dementia, but drinking more won’t help protect your brain any further.

A major study tracked 131,821 American nurses and health professionals for up to 43 years, starting when they were in their early 40s. During this time, 11,033 people – around 8% – developed dementia. But those who drank moderate amounts of caffeinated coffee or tea were notably less likely to be among them.

The protective effect was strongest in people aged 75 or younger, who saw their dementia risk drop by 35% if they consumed around 250mg-300mg of caffeine daily – roughly two to three cups of coffee. Crucially, drinking more than this didn’t provide any extra benefit.

Women in the study reported drinking around four and a half cups of coffee or tea per day when they joined, while men drank around two and a half cups. Those who drank more caffeinated coffee tended to be younger, but they also drank more alcohol, smoked and consumed more calories – factors that all have been found to increase dementia risk.

Interestingly, people who drank more decaffeinated coffee showed faster memory decline. Researchers believe this is probably because people switched to decaf after developing sleep problems, raised blood pressure, or heart rhythm disturbances – all of which are themselves linked to cognitive decline and dementia.

Why caffeine might protect the brain

There are sound biological reasons why caffeine could help keep our brains healthy. It works by blocking adenosine, a chemical that dampens the activity of brain messengers like dopamine and acetylcholine. These brain messengers (or neurotransmitters) can become less active as we age and in conditions such as Alzheimer’s disease, so caffeine’s stimulating effect may help counteract this decline.

Caffeine also appears to work through other mechanisms, including reducing inflammation and helping regulate blood sugar metabolism. People who did not have dementia (yet?) but drank more than two cups of coffee daily throughout their lives had lower levels of the toxic amyloid plaques, abundantly found in people’s brains who have Alzheimer’s disease.

Coffee and tea also contain many other beneficial compounds with antioxidant and blood vessel benefits which can all protect the ageing brain.

The American study found that only one to two cups of tea were linked to the best protection against dementia, which may reflect the fact that people in the US drink less tea than coffee overall. Green tea wasn’t examined separately, although most studies suggest it also protects against dementia.

Why does more caffeine stop being helpful? The researchers suggest it may be down to how our bodies break down coffee. Very high doses can also disrupt sleep and increase anxiety, which undermines any brain benefits.

A principle established back in 1908, known as the Yerkes-Dodson law, shows that when we become too stimulated – whether from anxiety or too much coffee – our mental performance starts to decline.

The findings from professional healthcare workers may not apply to everyone. But when researchers combined results from 38 other studies, they found similar results: caffeine drinkers had a 6%-16% lower dementia risk than non-drinkers, with one to three cups of coffee being optimal. Good news for tea lovers – in this broader analysis, drinking more tea was linked to greater protection.

Moderate caffeine intake doesn’t increase long-term blood pressure risk and may even reduce cardiovascular disease risk, which shares many risk factors with dementia. However, people with very high blood pressure are advised to limit themselves to perhaps one cup a day.

It’s worth noting that using “cups” as a measure doesn’t account for how much caffeine these actually contain. Fresh beans brewed at home contain different amounts of caffeine and can affect cholesterol levels differently than instant coffee, for instance.

But you don’t need much to feel a benefit. Even low doses of 40mg-60mg can improve alertness and mood in middle-aged people who normally did not drink (much) caffeine. More is not always better.

Today I’m sharing a guest article on a subject that – while it might seem unromantic – could be crucial to ensuring your financial security in later life.

Sadly, growing numbers of older people are seeing their marriages break down, leading in many cases to separation and divorce. Even if relatively amicable, this is likely to be stressful and emotionally exhausting. And – potentially even worse – it can have serious financial consequences for you and your family, both now and into the future.

My guest today, Richard Scott, a partner in the family team at HCR Law, knows this very well. In his article below he explains the benefit of having a post-nuptial agreement in place if, sadly, your marriage (or civil partnership) should come to an end.

Over to Richard then…

For many couples, the idea of a nuptial agreement is an unfamiliar and often unromantic concept. Yet, for those who have already married and whose financial circumstances have evolved, perhaps over many years, a post-nuptial agreement can offer clarity, protection and a far smoother path should the relationship ever break down.

In a climate where personal wealth, business interests and international assets are increasingly common, a carefully prepared post-nuptial agreement is a practical piece of financial planning that complements, rather than competes with, the marriage itself.

Legal status and why it matters

In England and Wales, post-nuptial agreements are not automatically legally binding. However, the courts are prepared to give decisive weight to a nuptial agreement where it is entered into freely by both spouses, with a full understanding of its implications, and where it is fair it is fair at the time of any future divorce.

In practice, that means a properly drafted post-nuptial agreement, supported by independent legal advice for both parties, full financial disclosure and the absence of coercion or pressure can be highly influential. It does not oust the court’s jurisdiction, but it does set a clear roadmap that the court will often follow unless needs or fairness dictate otherwise, particularly if the couple have independent children.

Financial clarity and reduced conflict

One of the principal benefits to any nuptial agreement is certainty. A post-nuptial agreement defines how assets would be treated if the marriage ends, reducing the scope for any dispute over property, savings, investments and pensions. That clarity can save significant legal costs and emotional upheaval by preventing arguments before they arise.

For couples who value transparency and orderly planning, the agreement functions as a financial charter that both parties can rely on, supporting trust rather than undermining it. In my experience, it is not uncommon for a post-nuptial agreement to be used as an option to re-establish trust in a faltering marriage. For instance, where perhaps one spouse has behaved poorly, or had an affair, the other spouse may require the reassurance of a post-nuptial agreement to help put the marriage back on track, instead of filing for divorce.

Protecting pre-acquired, family and business assets

Post-nuptial agreements are especially useful where one spouse brings pre-marital assets into the marriage or expects future inheritances or gifts. Ring-fencing such wealth helps ensure that family assets, heirlooms and intended legacies remain protected.

They are also invaluable for business owners, safeguarding a company’s continuity, shareholder relationships and value. By agreeing how shares and business interests would be treated, spouses reduce the risk of disruption to the enterprise, and this gives confidence to co-owners and investors.

Frequently I advise the children of business owners who are likely to inherit shares in a family business and who – often with their families –want to minimise any disruption to future succession planning by excluding those interests from the matrimonial pot with a post-nuptial agreement.

Sometimes couples who intend to enter into a pre-nuptial agreement simply run out of time to get the agreement finalised before the wedding. Rather than postpone the wedding, a post-nuptial agreement is a valuable alternative which is available to newlyweds and ensures that the opportunity to protect and ring-fence wealth acquired pre-marriage or any future inheritances, is not lost.

Adapting to life’s changes

Circumstances evolve after marriage: a career break to raise children, a relocation, the sale of a property, a windfall or the growth of a business. A post-nuptial agreement allows couples to recalibrate financial expectations to reflect these developments. This is particularly pertinent in second marriages, where there may be competing responsibilities to children from previous relationships, and in international families, where differing legal regimes can complicate outcomes. A tailored post-nuptial agreement brings order to complexity, aligning intentions with the realities of modern family life.

Fairness, safeguards and credibility

A robust agreement is not a blunt instrument. It can include review clauses, housing provisions and arrangements that meet needs fairly, especially where children are involved.

The process itself is not complicated. It involves both spouses’ obtaining independent legal advice, providing full disclosure of their assets and engaging in sensible negotiation. Most of of the clients I advise on this issue are pragmatic and are not out to engineer an unfair outcome, nor are their spouses – it’s about documenting a fair agreement with a view to avoiding contentious litigation in the future should the relationship break down at a later date.

A practical step in prudent planning

In summary, a post-nuptial agreement is a prudent step in managing financial risk. It offers peace of mind, helps safeguard hard-won family assets and businesses and significantly reduces the uncertainty and cost of a future dispute.

Lawyers advising on post-nuptial agreements often liken their importance to life insurance policies. The question for married couples should not be, “Can I afford one?” It should be, “Can I afford not to have one?” As such, for couples who value clarity and wish to protect their financial futures responsibly, it is an option well worth serious consideration.

Richard Scott (pictured below) is a partner in the family team at HCR Law.

Many thanks to Richard and his colleagues at HCR Law for an eye-opening article on this important topic. As Richard says, devoting some attention to this issue now can potentially save you and your family a lot of grief (and legal costs) in the future.

As always, if you have any comments or queries about this article, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

Today I’m featuring a way you can get a free fractional share worth up to £100 by signing up (for the first time) with an online share trading platform called Trading 212.

Trading 212 is unusual in that it offers commission-free and fee-free share trading. As a special offer, until Wednesday 4th March 2026 they are offering people new to the platform a free fractional share just for signing up via a referral link (such as the links in this post). The share you will get is chosen at random, but could be worth up to £100. You can either keep this share or sell it.

How to Sign Up

Signing up with Trading 212 is pretty straightforward. Just visit the Trading 212 website via any of the (referral) links in this post and follow the on-screen instructions to register. Note that you will be required to provide various items of information, including your date of birth, National Insurance number, annual income, employment status, and contact details. I understand that this is to meet their legal ‘Know Your Customer’ duty.

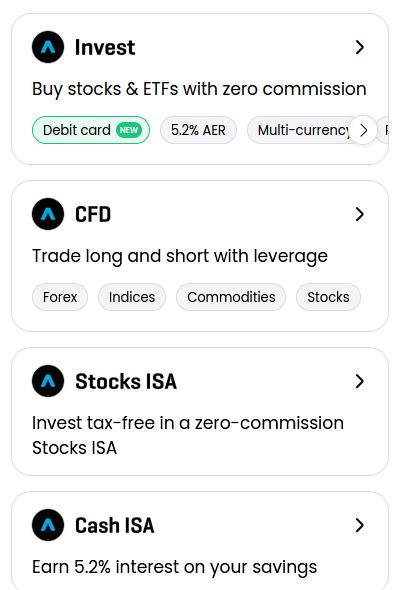

You will also need to indicate the type of account you want from the options available (see screen capture below).

As you will see, the four account types on Trading 212 are Invest, CFD, Stocks ISA and Cash ISA. You can apply for any or all of these if you like.

CFD stands for Contract for Difference. CFDs are quite complex financial instruments and unless you know what you’re doing I recommend giving them a miss.

If you just want the free share my suggestion would be to tick the Stocks ISA box. An ISA is, of course, a tax-exempt Individual Savings Account. As from April 2024 you can open any number of ISA accounts in a year as long as you don’t exceed your annual £20,000 allowance.

If you have already used up your entire £20,000 this year, you should choose Invest instead to open a general investment account without any tax benefits. Obviously if you don’t want a Stocks ISA with Trading 212 for any reason, you can choose this option as well.

For more information about the Trading 212 Cash ISA, see my review here. Be aware that you must open either an Invest account or a Stocks ISA account to qualify for a free share. Of course, there is nothing to stop you opening a Cash ISA account as well, but my recommendation would be to open an Invest or Stocks ISA account first.

Getting Your Free Share

There is one more step you will need to take in order to get your free share. You will need to deposit a minimum of £1 into your account. There are various ways you can do this, but i just used my debit card. There is no obligation to invest the £1 (or whatever you choose to deposit) and if you wish you can withdraw it once your free share has been credited.

The next business day you should receive an email confirming that a free fractional share has been added to your account. As mentioned above, this is allotted at random. If you’re lucky you might get one worth up to £100. Even if you get a less valuable one, though, it’s still a share for free. If you choose to keep it, it may rise in value. There may also be dividends payable in future (and credited to your account).

Selling Your Share

You can’t sell your share immediately. You have to wait three business days before doing so, but it is then just a matter of clicking the Sell button on your member’s dashboard.

The money will be credited to your Trading 212 account but you will have to wait 30 days before withdrawing it. So there may be a case for waiting to see if your share’s value goes up in that time. Of course, it could also go down!

In my case, I received a free share in the Ford Motor Company worth just under £8 at the time. Obviously this wasn’t as exciting as I might have hoped, but it was still – in effect – free money for almost no time or effort 😀

How Safe Is Trading 212?

Trading 212 is registered in England and Wales and authorized and regulated by the Financial Conduct Authority. In addition, all clients’ funds are kept separately in segregated bank accounts which are covered by the Financial Services Compensation Scheme. So even if the company itself were to go broke, any cash in your account would be protected up to a value of £120,000.

Of course, the FSCS guarantee doesn’t apply to the value of your stocks and shares, which can go down as well as up. All investments carry a risk of loss, although in the case of your free share you can never lose any more than the original cost, which was of course zero!

Referral Scheme

Any Trading 212 member can also refer new members while this offer is on. In that case, both you and the person concerned will receive one free fractional share worth up to £100. Obviously, the links in this blog post include my referral code – so if you register and get a free share, I will receive one also. Under the terms of the current offer you can get up to five free shares in this way. Five is the limit per person. Although you can still refer new members who will get a free share after this, as a referrer you won’t receive one as well. If and when the offer reopens in future, you will be able to refer more new members and get free shares again.

Final Thoughts

I first heard about Trading 212 a while ago, but wasn’t initially sure whether it was legit and here for the long term. And I thought the free share offer was, frankly, too good to be true. However, my own experiences have been entirely positive. My original free share in the Ford Motor Company was credited the next business day as promised and I received an email notifying me about it.

I can log in to my Trading 212 account any time to see how my Ford share is doing. I have also collected a few other shares from referrals. These include a share in AMD (the semiconductor company), which is currently worth an impressive £153.14, and one in Nike, which is worth £84.95. I still have my original Ford Motor Company share and it has risen in value to £10.11. I have also received several dividend payments from them. I haven’t sold any of my free shares yet but could of course do so any time I choose. I am not in any rush, as Trading 212 do not impose any platform or inactivity fees.

Although in this post I have focused on the free share offer, Trading 212 is worth considering as a share-dealing platform too. In particular, the fact that it’s fee-free and commission-free means it is well suited for people who are dipping a toe in stocks and shares investment for the first time. By contrast, the dealing fees and commissions charged by some other share-trading platforms can make small share purchases prohibitively expensive. This review by Money Savvy Daddy looks at the pros and cons of Trading 212 as a share-dealing platform in a bit more detail.

It’s also worth bearing in mind that Trading 212 pays interest on any uninvested funds in your ISA or Invest account, currently at a rate of 3.8% AER. You can also make money allowing your shares to be lent out. Rates on offer for this vary according to investor demand, with the process handled automatically by Trading 212 once authorized. You can read more about share lending on Trading 212, including the risks and safeguards provided, here.

In conclusion, I hope this post has inspired you to consider registering with Trading 212 to claim your free share. If you do, I hope you get a valuable one! Please let me know what share you receive in a comment below. And, as always, any other comments or questions are very welcome too.

Don’t forget, the current free share offer ends on Wednesday 4th March 2026.

Disclosure: The links in this post include my referral code. If you click through and register as described above, I will receive a free share (as will you). Please note also that I am not a qualified financial adviser and nothing in this post should be construed as individual financial advice. Everyone should do their own ‘due diligence’ before investing and seek advice from a qualified financial adviser if in any doubt how best to proceed. All investment carries a risk of loss (although not in the case of free shares, obviously).

This is an update of my original post about this special offer.

If you enjoyed this post, please link to it on your own blog or social media:

Cruise holidays have become increasingly popular with older adults, and it’s easy to see why. They offer a relaxed way to travel, with accommodation, meals, entertainment and transport between destinations all included in one package.

However, cruise prices can vary significantly, and it’s not always obvious where good value ends and unnecessary expense begins. With a bit of forward planning and careful comparison, it’s perfectly possible to enjoy a relaxing and comfortable cruise holiday without spending more than you need to.

Below are some sensible ways to keep cruise costs under control, while still getting the most from your time away.

1. Flexibility Can Make a Big Difference

One of the most effective ways to save money on a cruise is to be flexible about when and where you travel.

Cruises outside school holiday periods are usually much cheaper, which suits retirees and semi-retired travellers particularly well.

Spring and autumn “shoulder seasons” often combine reasonable weather with lower prices and fewer crowds.

Less well-known itineraries can offer excellent value, even though the onboard experience is often very similar.

If you can avoid setting your plans too tightly, you’re far more likely to find a good deal.

2. Compare Prices Using Cruise Deal Sites

Cruise prices are not always the same across different websites, so it’s well worth shopping around. In addition to checking cruise line websites directly, comparison and deal sites can be very useful.

Prices and inclusions can vary, so it’s important to look beyond the headline figure and check what’s actually included.

3. Think Carefully About Extras and Add-Ons

Many cruises offer optional extras such as drinks packages, speciality dining, wi-fi and organised shore excursions. While these can be convenient, they are not always good value for everyone.

For example:

Drinks packages tend to suit heavier drinkers, but can work out expensive if you only have the occasional drink.

Independent shore excursions, or simply exploring ports on your own, are often much cheaper than ship-organised trips.

Onboard wi-fi can be surprisingly expensive. You may be able to get free or low-cost wi-fi locally when the ship is in port.

Choosing only the extras you’ll genuinely use can keep overall costs much lower.

4. Cabin Choice Can Have a Big Impact on Price

Cabin type is another major factor in cruise pricing.

Inside cabins are usually the cheapest option and can be perfectly comfortable, especially if you spend most of your time enjoying the ship or going ashore.

Obstructed-view cabins often cost less than standard ocean-view cabins, but still offer natural light.

If having a balcony is not essential to you, opting for a more modest cabin can result in significant savings.

5. Consider Cruises Departing From the UK

Cruises that depart from UK ports such as Southampton, Tilbury or Liverpool can be excellent value for money.

They remove the need for flights, overnight hotels and airport parking, which can add substantially to the cost of a holiday. They also tend to be less stressful, which many older travellers appreciate.

6. Timing Your Booking Can Help

There are certain times of year when cruise deals are more common.

The early months of the year often bring a wave of promotions, including reduced deposits or onboard credit.

Late deals can offer good value if you are able to travel at short notice, although cabin choice may be limited.

Booking early can also pay off if you have a particular itinerary or ship in mind.

Signing up for email alerts from cruise lines and deal websites can help you spot price reductions.

7. Make Use of Loyalty Schemes

If you cruise more than once, loyalty schemes are worth considering. Over time, they can provide benefits such as onboard credit, discounted fares or priority services, all of which add to the overall value of your holiday.

Final Thoughts

Cruise holidays don’t have to be expensive, particularly for older adults who have the flexibility to travel outside peak periods. By comparing prices carefully, choosing cabins and extras sensibly, and taking advantage of UK-based cruise deals, it’s possible to enjoy a relaxing and well-organised holiday without overspending. The key is to focus on value for money, rather than paying for features or extras that don’t genuinely enhance your experience.

As always, any comments or questions on this post are welcome. In addition, if you have any tips of your own for saving money on cruise holidays, I would love to hear them! 🚢

If you enjoyed this post, please link to it on your own blog or social media:

I’ll begin as usual with my JP Morgan Personal Investing (previously Nutmeg) Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

As regular readers will know, in June last year I transferred most of the money in my former Nutmeg Fully Managed portfolio (just under £25,000) to a new Nutmeg Income Portfolio. I discussed this in detail in this post, but basically money in this port is invested to generate an income from share dividends and other sources. This is then paid monthly. Capital appreciation is targeted as well, but these portfolios are aimed primarily at older people (and others) who want/need their investment to generate a regular cash income.

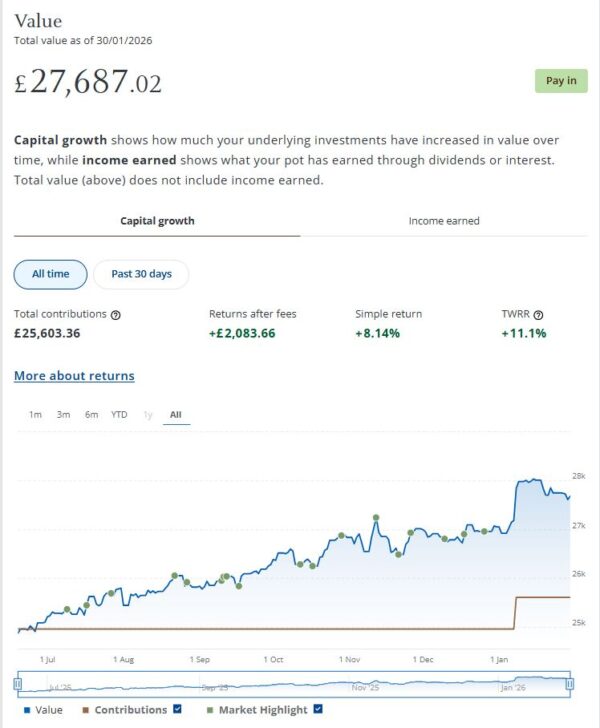

In January my JPM Investing income portfolio generated £72.70 of income, which was duly paid in to my bank account on 24 January 2026. That means I have now received a total (tax-free) income of £544.16 to date. That’s about what I would have expected based on JPM’s projected annual return of just under 5% for income ports at my chosen risk level (five).

My income portfolio grew in value again in January. It’s now worth £27,687 compared with £27,052 at the start of last month, a rise of £635. That, does, however, include £651 transferred from what remained in my Fully Managed account (mentioned above), which I have now closed. I had kept a small amount in this for comparison purposes. But as my new Income Portfolio appeared to be generating better returns overall, I couldn’t see much point keeping it. If you subtract this, the Income Portfolio actually fell slightly in value last month by £16.

As the screen capture below shows, this port has increased by £2,083.66 (8.14%) since I opened it in June last year. That’s clearly good going, though I don’t suppose it will carry on like this indefinitely. I should maybe also mention that performance may have been helped a bit by the no-fees introductory offer on Nutmeg/JPM income portfolios until the end of 2025 (which has of course ended now).

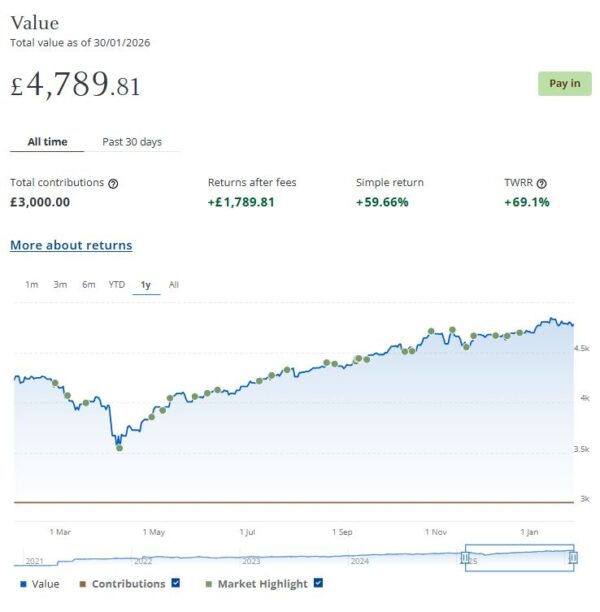

I still have a smaller, growth-oriented pot using JPM Investing’s Smart Alpha option. This is now worth £4,790 (rounded up) compared with £4,714 a month ago, an increase of £76. Here is a screen capture showing performance over the last year.

Finally, at the start of December 2023 I invested £500 in one of Nutmeg/JPM’s thematic portfolios (Resource Transformation). In March 2024 I also invested a further £200 from referral bonuses (something I no longer receive). As you can see from the screen capture below, this portfolio is now worth £956 (rounded up) compared with £934 last month, an increase of £22.

Overall in January I was up by £82 or 0.33%. In addition I did, of course, receive £72.70 in income from my income portfolio. Overall, then, I am in profit for the month by £154.70.

Excluding income generated, the overall value of my JPM investments is up by £1,805 or 5.71% since the start of February 2025, so the April 2025 fall (caused largely by Trump’s tariffs) has now fully reversed. If you add to this figure the £544.16 of income generated so far, that gives a total profit for the last 12 months of £2,349.16 – not a bad return in these uncertain times.

As I always have to say, some volatility is to be expected with stock market investments, but over the longer term they tend to even themselves out (and generally perform better than bank savings accounts, although that is never guaranteed). In general the worst thing you can do is panic and sell up when downturns occur (as happened in April last year). You are then crystallizing your losses rather than giving the markets time to recover. This is something I had cause to discuss in this blog post.

You can read my full original Nutmeg/JPM review here. If you are looking for a home for your annual ISA allowance, based on my overall experience over the last nine years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs), Lifetime ISAs and Junior ISAs as well.

Moving on, I also have investments with P2P property investment platform Housemartin. As discussed in this post, the company rebranded last year from Assetz Exchange.

My investments with Housemartin continue to generate steady returns. Housemartin focuses on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my HM portfolio has generated a respectable £297.72 in revenue from rental income. I have made a small net loss of £20.25 on property disposals. Capital growth generally has slowed, in line with UK property values generally.

At the time of writing, 14 of ‘my’ properties are showing gains, 7 are breaking even, and the remaining 23 are showing losses. My portfolio of 44 properties is currently showing a net decrease in value of £79.97. That means that overall (rental income minus capital value decrease and loss on disposal) I am up by £197.50. That’s still a respectable return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Housemartin most projects are socially beneficial as well.

The net fall in capital value of my Housemartin investments is obviously a little disappointing. But it’s important to remember that until/unless I choose to sell the investments in question, it is largely theoretical, based on the latest price at which shares in the property concerned have changed hands. The rental income, on the other hand, is real money (which in my case I’ve reinvested in other HM projects to further diversify my portfolio).

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of Housemartin as far as i am concerned. You can actually invest from as little as £1 per property if you really want to proceed cautiously.

As I noted in this blog post, Housemartin is particularly good if you want to compound your returns by reinvesting rental income. This effectively boosts the interest rate you are receiving. Personally, once I have accrued a minimum of £10 in rental payments, I usually reinvest this money in either a new HM project or one I have already invested in (thus increasing my holding). Over time, even if I don’t invest any more capital, this will ensure my investment with Housemartin grows at an accelerating rate and becomes more diversified as well.

In 2022 I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios, Oil Worldwide. I also invested a small amount I had left over in Tesla shares.

Last month, as Oil Worldwide hadn’t exactly been setting the world alight, I decided to switch my entire investment in this to another smart portfolio, InTheGame. This port, focusing on the computer gaming industry, has been the top performer for some time in my eToro virtual portfolio.

Unfortunately just as I switched away from Oil Worldwide, US President Trump decided to invade Venezuela. This gave the oil industry a significant boost, which I would otherwise have benefited from. Meanwhile InTheGame hasn’t been doing particularly well. At the time of writing the value of my investment in this has fallen by over 6%. Hey ho! This does of course demonstrate that there are never any guarantees when investing and unexpected events can thwart the best-laid plans. Hopefully in the coming months things will improve again!

As you can see from the screen captures below, my original eToro investment (total value £888.36 in pounds sterling) is today worth £1,119.21, an overall increase of £230.85 or 25.99%.

Note: eToro now displays the value of investments in your native currency, although you can change this if you wish.

You can read my full review of eToro here. You may also like to check out my more in-depth look at eToro copy trading. I also discussed thematic investing with eToro using Smart Portfolios in this post. The latter also reveals why I took the somewhat contrarian step of choosing the oil industry for my first thematic investment with them.

As mentioned above, my new investment in InTheGame is currently down by over 6%. My copy trading investment with Aukie2008 continues to do well, however, with an impressive overall profit of 65.20%. Of course, I have held this investment for quite a bit longer.

My Tesla shares, which I purchased as an afterthought with some spare cash I had in my account, are down this month but still showing an overall profit of over 280% since I bought them. If only I had put a bit more money into this!

You might also notice that I have small holdings in Prosus NV, a Dutch internet group, and South Bow, a Canadian energy infrastructure company. To be honest I don’t understand how I acquired these, but I assume they are some sort of bonus I was awarded. In any event, I am happy to have them in my portfolio.

If you would like more information about setting up an eToro account, please click on this no-obligation website link [affiliate]. Don’t forget that you also get a free $100,000 virtual portfolio, which you can use to experiment with trading and investing strategies. I have certainly earned a lot from mine.

As an experiment, at the start of April last year I put £50 into an investment ISA with Trading 212. As mentioned in my blog post about dividend investing, I put it into the (Almost) Daily Dividends Portfolio, a ready-made portfolio or ‘pie’ on Trading 212. As you can see from the screen capture below, my portfolio is now worth £58.80, an increase of £8.80 or 17.60% over the ten-month period. It has even accrued a grand total of 87p in dividends!

I am quite impressed with how this investment has been faring, despite the small amount I put in (which means I may be missing out on some smaller dividends). If I increased my investment I would almost certainly become eligible for more dividends, and even more the longer I remain invested. If I had any spare money at the moment, I would consider doing this. Of course, I do now have an income-focused portfolio with JPM Investing as well (see above).

Moving on, I published various posts on Pounds and Sense in January. I have listed below those that are still relevant.

In What Are Index Funds and How Can You Invest in Them? I looked at one of the most straightforward and cost-effective ways to invest in the stock market, especially for long-term savers and beginners. Index funds track a market index such as the FTSE 100, giving you broad exposure to many companies at once. This helps spread risk and keeps costs low.

I also posted What Are Investment Trusts and How Can You Invest in Them? Investment trusts are a distinctive type of investment company with some unique features; and for the right investor, they can offer real advantages. In this article, I explained what investment trusts are, how they work, and their pros and cons compared with alternatives such as ETFs and open-ended funds.

Also in January I published Planning a UK Holiday This Year? Here Are Some Ideas for you! In this article – an update of an annual post – I shared links to my blog posts about a variety of UK holiday destinations I’ve visited in the last few years, in case you might wish to consider them for short (or longer) breaks in the year ahead.

Finally, I published Make the Government Pay! How to Use Gift Aid to Redirect Your Tax Money. In this article I discussed a perfectly legal way to ensure that at least some of your tax money goes to causes you genuinely support than simply vanishing into the government’s coffers. Gift Aid is a scheme that allows charities to reclaim tax on donations made by UK taxpayers. You can of course use it to boost the value of your donations to the organizations in question – but, as my post reveals, you can even use it to reallocate some of your tax money without spending any money directly.

I’ll close with a reminder that you can also follow Pounds and Sense on Facebook or Twitter (or X as it is called now). Twitter/X is my number one social media platform and I post regularly there. I share the latest news and information on financial matters, and other things that interest, amuse or concern me. So if you aren’t following my PAS account on Twitter/X, you are definitely missing out!

I am also on the BlueSky social media network under the username poundsandsense.bsky.social. Twitter/X remains my primary social media platform, but I also post details of my latest blog posts, third-party articles and other financial news and resources on BlueSky for those who prefer to follow me there.

As always, if you have any comments or questions, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts on PAS may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media: