As more people in the UK find themselves paying income tax again – particularly retirees whose pensions, savings interest and state pension now push them over the personal allowance – it’s natural to feel frustrated about how that money is used.

While we don’t get much say over how most of our taxes are spent, there is one perfectly legal way to ensure that at least some of your tax money goes to causes you genuinely support than disappearing into the government’s coffers: Gift Aid.

Table of Contents

What Is Gift Aid?

Gift Aid is a simple scheme run by HMRC that allows UK charities to reclaim tax on donations made by UK taxpayers.

When you donate to a registered charity and tick the Gift Aid box (or complete a Gift Aid declaration), the charity can claim back the basic rate of income tax you have paid on that donation.

Because the basic rate of income tax is currently 20%, this effectively means:

For every £1 you donate, the charity receives £1.25.

You don’t pay anything extra.

The extra 25p comes from tax you’ve already paid.

Instead of that slice of tax being “wasted” by the government, it is redirected to a charity of your choosing 👍

You Don’t Even Have to Spend Any Money

One of the least appreciated aspects of Gift Aid is that you don’t necessarily have to spend any money at all to benefit from the scheme.

Many charity shops now operate Gift Aid on donated goods. When you drop off clothes, books or household items, you’ll often be asked if you’d like to Gift Aid them.

Here’s how it works:

The charity sells your donated items in its shop.

Whatever price they achieve is treated as a donation from you.

The charity then claims an extra 25% from HMRC on top.

So if your donated items sell for £40, the charity can claim an additional £10 in Gift Aid – all without you spending a penny. Once again, that extra money comes from tax you’ve already paid.

Gift Aid Isn’t Just for Obvious Donations

Gift Aid can also apply to payments you might not normally think of as charitable donations.

A good example is the National Trust, along with many other heritage and conservation organisations. When you visit one of their properties, you’ll often see two admission prices:

standard admission

Gift Aid admission (typically £1 more)

By choosing the Gift Aid price:

You pay £1 extra.

The charity can claim 25% of the full admission price from HMRC.

In most cases, this means the charity receives far more than the extra £1 you pay. It’s a very tax-efficient way of supporting organisations you already enjoy visiting, and another example of how Gift Aid lets you divert tax money away from HM Treasury and towards something you personally value.

Who Can Use Gift Aid?

You can use Gift Aid if:

You are a UK taxpayer, and

You have paid at least as much income tax or capital gains tax in the tax year as the charity will claim back.

This is increasingly relevant for older people who may not have paid tax for years but now do so again because of:

frozen personal tax allowances

rising state pensions

workplace or private pension income

interest on savings exceeding the personal savings allowance

If you are paying tax, Gift Aid is something you should at least consider using.

Example 1: A Simple Donation

Let’s say you donate £100 to a charity that supports a cause you care about.

You give £100.

The charity claims £25 from HMRC.

Total amount the charity receives: £125.

That £25 would otherwise have gone to the government. With Gift Aid, you decide where it goes.

Example 2: Higher-Rate Taxpayers Can Benefit Too

If you’re a higher-rate taxpayer (40%), Gift Aid can be even more powerful.

Using the same £100 donation:

The charity still receives £125.

You can reclaim the difference between basic-rate and higher-rate tax via Self Assessment.

This allows you to reclaim £25 personally, reducing the effective cost of your donation to £75.

What Information Do You Have to Provide?

To claim Gift Aid, charities are required by HMRC to collect some basic information from you. This usually includes:

your full name

your home address

a signature or confirmation (such as ticking a box online)

This is simply to confirm that you are a UK taxpayer and that the charity is entitled to reclaim the tax. It’s a one-off process for most organisations.

Gift Aid: A Small Act of Financial Control

People often feel they have little say over how their taxes are spent. Gift Aid doesn’t change the system, but it does offer a rare opportunity to exercise a degree of choice.

By using Gift Aid:

You increase the value of your support for charities you believe in.

You don’t pay any more tax overall.

You ensure some of your tax money is spent on causes you actually believe in.

A Final Word of Caution

Only use Gift Aid if you really are paying enough tax to cover it. If you don’t, HMRC can ask you to make up the difference.

If your tax position changes from year to year, keep this rule in mind. And if you’re only paying small amounts of tax, keep a record of your Gift Aid donations to ensure you don’t accidentally exceed the total tax you have paid.

That said, for millions of UK taxpayers, Gift Aid is a straightforward, perfectly legitimate way to make their money – and their tax – work harder and smarter.

And for those who find themselves now paying tax again in later life, claiming Gift Aid can feel like a small but satisfying win 🙂

If you give to charity – whether in cash, goods, or entrance fees to attractions – it makes sense to make the government contribute too.

As always, if you have any comments or questions about this article, please do post them below.

If you enjoyed this post, please link to it on your own blog or social media:

For many of us 2025 was another difficult year, with a cost-of-living crisis driven especially by rising gas and electricity costs.

With the festive season behind us now – and a cold and miserable start to the new year – many of us are understandably desperate for something to look forward to in the year ahead.

Some will be planning to head abroad in search of sunnier climes. But others may be deterred by the cost of going overseas and the additional hassles it may entail.

So today I thought I’d share links to my blog posts about some UK holiday destinations I’ve visited in the last few years, in case you wish to consider them for short (or longer) breaks in the year ahead. Clicking on any of the links below will open my post about the place concerned in a new tab, so you won’t have to keep clicking the Back button to return here.

Llandudno in North Wales is somewhere I’ve been visiting regularly for over ten years now (most recently in 2025, when I went twice). It’s a traditional British seaside resort with a long pier, Punch and Judy show, sweeping promenade, and plenty more (you can see the stunning Victorian seafront in the cover image). It’s very popular with both older people and young families. As well as my main review, my October 2020 Coronavirus Crisis Experience Update includes details of a short break I enjoyed there just before the Welsh government imposed another lockdown 😮

Minehead is a North Somerset coastal town. I enjoyed a short break there in 2020 as well, at a time when lockdown rules were relaxed. It was my first visit to Minehead and I particularly enjoyed visiting the National Trust property Dunster Castle, which is just a couple of miles down the road. Sadly the West Somerset Railway which starts (or ends) in Minehead was closed due to the pandemic when I went, but I’d love to go back for a trip on this heritage steam railway sometime in the future.

Aberystwyth is in mid-Wales on the Cardigan Bay coast. I have visited it three times now, the first two staying at the Marine Hotel and the most recent at a self-catering apartment called Sea Brin. Aberystwyth is quieter and less commercialized than Llandudno (mentioned above), and the fact it’s a university town means it has quite a cosmopolitan feeling. It’s a good place to chill out, but there are plenty of interesting things to see and do as well.

I visited Aberdovey for the first time in April 2023. It’s a small town on the mid-Wales coast. It’s about ten miles north of Aberystwyth and five miles south of Tywyn, the home of the Talyllyn Railway (see below). It’s a charming, laid-back place, perfect for a relaxing short break. It has a beautiful beach (with watersports for those who want them) and some great cafes and restaurants. I wouldn’t go there for the night-life, though – even the chip shop closes at 8 pm!

I had a particular reason to visit Hewenden MIll Cottages, as my sister Liz and her family live just a couple of miles down the road in Wilsden. Even if I didn’t have family connections, though, I would definitely recommend them for a short break. The accommodation consists of a number of former mill-workers’ cottages, in a beautiful woodland setting. The cottages (such as the one below, where I have stayed myself) are spacious and well equipped. From here you can visit Haworth – home of the Bronte sisters – and the Victorian model village of Saltaire. The area is also great for walking and cycling.

The Aberdunant Hall Holiday Park and Hotel (to give it its full name) is about four miles from the North Wales coastal town of Porthmadog You can stay in the hotel itself (which is quite compact) or in accommodation around the park. I stayed in what they call a Forest Pod, which is roughly the equivalent of half a caravan. It was okay for a short break but if you went as a couple the cramped conditions could put a strain on your relationship! If I went again I would book a room in the hotel or maybe one of the Woodland Escape Suites in the park. I still enjoyed my stay there, and found the location convenient for visiting a range of places including Portmeirion (where the sixties TV series The Prisoner was filmed) and the Ffestiniog Railway, which runs from Porthmadog to Baenau Ffestiniog. It’s also on the edge of Snowdonia, with lots of opportunities for walking and mountain climbing.

Lake Vyrnwy is a few miles over the border from Shropshire into Wales. I went there in 2019 after watching a TV show about the history of this artificial lake, which was originally created to provide a water supply for the people of Liverpool in the 19th century (it’s now naturalised and if you weren’t aware of its history you wouldn’t know it was man-made). I stayed at the Lake Vyrnwy Hotel and Spa, which is near the dam at the western end of the lake. This was originally built to accommodate senior managers and engineers on the construction project, though it has of course been extended and modernised many times since. If you want to visit Lake Vyrnwy, it’s the best (possibly the only) option. I happened to choose a bitterly cold weekend just before Easter for my visit, which spoiled it a bit. Still, I enjoyed the beautiful scenery and some great walks. It’s probably not a place to take children, however, as there might not be enough for them to do.

The Talyllyn Railway (also mentioned under Aberdovey) is a heritage steam railway in Wales. It starts in the town of Tywyn in mid-Wales, so in October 2018 I booked a short break there. To be honest there isn’t a great deal else to do in Tywyn, but it makes a good base for a day on the railway. And the railway itself takes you through some stunningly beautiful countryside. If you buy one of their very reasonably priced Day Rover tickets, you can get on and off at any station along the route. I highly recommend an hour or two at Dolgoch, which has some great walks and lovely waterfalls.

Warner Leisure Hotels have 16 country and coastal resort hotels across England and Wales. They have a strict adults-only policy, and appeal mainly to an older clientele (based on my experience, the average age is around seventy). As well as accommodation they offer a variety of leisure activities, including day trips, quizzes, guided walks, archery and bowls, social dancing, swimming, and so on. Most of these activities are included in the price, as is the evening entertainment. I have stayed at Bodelwyddan Castle in North Wales and Alvaston Hall in Cheshire. Some aspects I liked, others I wasn’t so keen on, as you can read in my review. You can also see their latest offers by clicking on the banner ad below [affiliate].

About five years ago I took a short break in the English Lake District. I stayed at the Waterhead Hotel, just south of Ambleside, at the north end of Lake Windermere (England’s largest lake). The hotel is located literally a few yards from the lake (hence the name, of course). If you haven’t visited the Lake District before, the area should definitely be on your ‘To Do’ list. There are many miles of beautiful countryside to explore, along with attractions such as Beatrix Potter’s house and Wray Castle. And, of course, you must buy a day ticket for the Windermere lake steamers. You can travel the length of the lake in style on these vessels, while sipping a hot chocolate (or something stronger) and listening to commentary on the scenery passing alongside. Highly recommended 🙂

I visited the Isle of Man for the first time in April 2024, staying in the island capital Douglas. I went on a heritage-railway-themed break offered by Newmarket Holidays. So naturally I had trips on the Isle of Man Steam Railway and also the Manx Electric Railway. The latter takes you from Douglas to Laxey and onward to Ramsey. Laxey is the home of the iconic Lady Isabella waterwheel, the largest working waterwheel in the world. The IOM is about the same latitude as Liverpool so obviously the weather can be variable, but I was lucky enough to get wall-to-wall sunshine during my stay. I flew to the island from Birmingham Airport which took about 45 minutes, but you can also get a ferry from Heysham or Liverpool. The Isle of Man is charming and verdant, and largely unspoiled. Definitely worth considering if you’re looking for something a little bit different for a short (or longer) holiday.

I visited Lanbedrog for the first time in July 2021. It’s a village on the Llyn (or Lleyn) Peninsula in NW Wales. I stayed at an Airbnb property, the first time I had done this (Llanbedrog doesn’t have any hotels as far as I know). It’s by the coast, roughly half way between Pwllheli (famed for its Butlins camp, now run by Haven Holidays) and trendy Abersoch. It has a beautiful sandy beach which would be perfect for families with young children (or grandchildren). I very much enjoyed my three-night stay and found it a perfect place to relax and chill out after months of lockdown. The National Trust mansion (and garden) Plas yn Rhiw is about seven miles away.

I stayed in Criccieth in North Wales for the first time in June 2022, although I had visited the town in the past. It’s a lovely place to relax and chill out. It has excellent road and rail connections, and there are also some high-quality tourist attractions nearby, including Portmeirion and the Ffestiniog Railway. Criccieth itself is best known for its castle which dominates the town. Although it’s a ruin, many of the walls are still standing and you can enjoy some amazing views across the bay, as far as Harlech Castle and beyond.

I visited Lavenham in Suffolk for the first time in August 2022. It is said to be England’s best-preserved medieval town, with over 300 listed, timber-framed houses. There are various historic buildings such as the Guildhall and Little Hall you can look around. Lavenham also boasts a variety of highly rated pubs and restaurants, and some lovely tea rooms and coffee houses as well! 🍮

Barmouth is a traditional Welsh seaside resort about ten miles south of Harlech. I visited in September 2022, staying at an elegant Victorian Gothic hotel called Tyr Graig Castle. Barmouth has a clean, attractive promenade and beautiful sandy beach which goes out a long way. There is plenty to do for families, including a funfair and amusement arcades. There are various restaurants and fast food outlets along the seafront. There is also a railway station with regular trains to Pwllheli in one direction and Aberystwyth and beyond in the other. Nearby attractions include Harlech Castle, Portmeirion and the Fairbourne miniature steam railway 🚂

I visited the historic city of Bath in June 2023. There is lots to see and do, although top of many people’s lists will be the stunning Roman Baths. Bath Abbey is well worth a look too, and you can admire the beautiful Georgian architecture around the city for free! Read my top tips for anyone visiting Bath in this post, including the excellent self-catering accommodation I stayed at.

Other Resources

Here are links to a few other blog posts that may be of interest if you are planning a UK holiday this year…

In recent years Airbnb has become increasingly popular for self-catering holidays. You can book anything from a spare room in someone’s home to a whole house or apartment. My recent short breaks in Lavenham and Llanbedrog (see list above) were in Airbnb properties. You can read all about the booking process in my post.

Finding a cashpoint in an unfamiliar town (or village) can be challenging, so you might find this free app a useful resource to download. It has helped me avoid embarrassment on several occasions.

If your thoughts are turning further afield, you may be considering a cruise holiday as an option. Even if you can’t go abroad, I can testify from personal experience that a cruise of the British Isles (like these, perhaps) can be very enjoyable and enlightening. My blog post sets out a range of tips and advice that will be particularly relevant for first-time and solo cruisers.

Finally, coach holidays are another very popular option among older people especially. I don’t have much experience of this myself, but my friends at Over 60s Discounts have a great article about coach holidays for over-60s in the UK. This includes a list of popular UK destinations and details of several companies offering low-cost coach holidays.

Closing Thoughts

I hope you have enjoyed reading this post and it has given you a some ideas for UK holidays.

Obviously I am a 60-something male and nowadays usually travel on my own. So if your circumstances are different from mine, I understand that some of the destinations mentioned above might not hold as much appeal. In addition, I live in Staffordshire, so the places I go are all reasonably accessible from there.

Finally – as I noticed when reading back my list – I do have a bit of a penchant for places with heritage steam railways nearby, so please bear that in mind as well 😀

Of course, I’d love to hear your views about any of the destinations mentioned, or any other places in the UK you would recommend for a short break or longer holiday. Please leave any comments or questions below as usual.

Note: This is a fully revised update of an annual post.

When most people think about investing, they picture stocks and shares, funds, ISAs and perhaps ETFs. But there’s another long-established option that often flies under the radar: Investment Trusts.

Despite the name, investment trusts aren’t trusts in the everyday sense. They are a distinctive type of investment company with some unique features – and for the right investor, they can offer real advantages.

In this article, I’ll explain what investment trusts are, how they work, and their pros and cons compared with alternatives such as ETFs and open-ended funds.

Table of Contents

What Is an Investment Trust?

An investment trust is a publicly listed company whose business is investing in other assets. These might include:

specialist assets such as private equity or renewable energy

When you invest in an investment trust, you’re buying shares in the company, not units in a fund. Investment trusts are listed on the London Stock Exchange, and their shares are bought and sold in the same way as any other quoted company.

Importantly, most investment trusts are actively managed, with a professional fund manager making decisions about what to buy and sell.

How Investment Trusts Differ from Funds and ETFs

The key difference lies in structure.

Closed-Ended Structure

Investment trusts have a fixed number of shares in issue. This means:

The manager does not need to sell assets to meet investor withdrawals.

The trust can take a long-term view and invest in less liquid assets.

By contrast, open-ended funds and ETFs create or cancel units as investors buy and sell.

Share Price vs Net Asset Value (NAV)

Because investment trusts trade on the stock market, their share price is driven by supply and demand. This means shares can trade:

At a discount to the value of the underlying assets (NAV)

At a premium to NAV

This feature can create opportunities – but also risks – for investors.

The Advantages of Investment Trusts

Potential to Buy Assets at a Discount

One of the biggest attractions is the ability to buy shares below NAV. In simple terms, you may be able to buy £1 of assets for 90p (or less).

Discounts can widen in difficult markets, potentially offering long-term investors attractive entry points.

Gearing (Borrowing to Invest)

Investment trusts are allowed to borrow money to invest, known as gearing.

Used well, gearing can enhance long-term returns

Used poorly, it can magnify losses

This makes investment trusts potentially more volatile than ETFs or open-ended funds.

Strong Income Records

Many UK investment trusts aim to provide a reliable and growing income.

Crucially, they can retain income in good years and use reserves to maintain or increase dividends in tougher times – something open-ended funds are not permitted to do.

Some UK equity income investment trusts have raised their dividends for decades.

Access to Specialist Assets

Because managers don’t have to meet daily redemptions, investment trusts can invest in:

infrastructure and renewable energy

private equity

property and specialist debt

These areas are often harder to access via ETFs.

Can Be Held in Tax-Free Wrappers

Most investment trusts can be held within tax-free SIPPs and stocks and shares ISAs. That means no tax is payable on income generated or capital growth.

The Disadvantages of Investment Trusts

Discounts Can Persist

While buying at a discount sounds attractive, there’s no guarantee it will narrow. Some trusts trade at persistent discounts for years.

Higher Volatility

The combination of share price movements, discounts and gearing can make investment trusts more volatile than ETFs tracking an index.

Active Management Risk

Most investment trusts rely on the skill of a fund manager. If the manager under-performs, returns may lag cheaper passive options.

Complexity

Compared with a simple FTSE 100 ETF, investment trusts require more understanding – particularly around discounts, premiums and gearing.

Investment Trusts vs ETFs: A Quick Comparison

Feature

Investment Trusts

ETFs

Structure

Closed-ended company

Open-ended fund

Management

Usually active

Usually passive

Can use gearing

Yes

Rarely

Price vs NAV

Can trade at discount/premium

Very close to NAV

Income smoothing

Yes

No

Costs

Often higher

Usually low

How Can You Invest in Investment Trusts?

You can buy investment trusts through most UK investment platforms, including:

Stocks and Shares ISAs

SIPPs (Self-Invested Personal Pensions)

dealing accounts

They trade just like shares, so you’ll usually pay a dealing fee when buying or selling.

Before investing, it’s wise to check:

the trust’s long-term performance

ongoing charges

gearing policy

dividend history

whether shares trade at a discount or premium

Are Investment Trusts Right for You?

Investment trusts aren’t for everyone. If you prefer:

However, for investors willing to do a bit more research, investment trusts can offer:

attractive income

exposure to specialist assets

the chance to buy quality investments at a discount

As always, diversification matters – and investment trusts are best viewed as part of a broader, well-balanced portfolio.

UK Investment Trust Examples

Investment trusts cover a wide range of strategies and sectors, from global growth to income to specialist themes like biotech or renewable energy. Here are some well-known UK trusts across different categories to help bring the concept to life.

📊 Global Growth & Broad Equity

Scottish Mortgage Investment Trust (LSE: SMT) – One of the largest and most popular UK investment trusts. It invests globally with a growth-oriented portfolio that includes technology and disruptive companies. It frequently tops the most-bought lists among UK investors.

Alliance Witan – A large diversified global trust formed from the merger of Alliance Trust and Witan, offering broad exposure across markets.

Baillie Gifford US Growth Trust – Focuses on growing companies based in the United States, blending listed and (up to a limit of) unlisted holdings.

💰 Income-Focused Trusts

City of London Investment Trust (LSE: CTY) – A classic UK equity income trust with a long record of increasing dividends year-on-year.

JPMorgan Global Growth & Income – Offers a diversified global equity income strategy that regularly features among popular income trusts.

Murray International Trust – Another long-running global equity income trust often favoured for income within ISAs.

🌍 Regional & Sector-Specific Trusts

Schroder AsiaPacific Fund – Provides exposure to companies across Asia and Asia-Pacific regions (excluding Japan and Australasia).

BlackRock Smaller Companies Trust – Focuses on smaller company equities, often with a value or growth tilt.

RTW Biotech Opportunities – A sector-specific trust investing in biotechnology companies at various stages of development.

🔋 Other Interesting Themes

Greencoat UK Wind (LSE: UKW) – A renewable energy trust investing in UK wind assets. It’s popular among investors seeking income from alternative infrastructure, though returns can be more cyclical.

3i Group – A private equity–focused investment trust with a long track record and often high longer-term returns, though returns may be more volatile.

These examples are not recommendations – just familiar names that illustrate how diverse the investment trust world can be, from broad global strategies to niche sectors like biotech or renewables. Always do your own research (including yield, fees, discount/premium and underlying strategy) before investing.

My Own Trust Investments

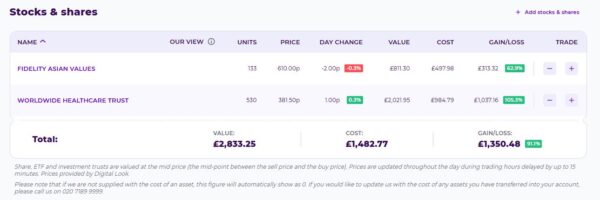

Finally, I thought it might be of interest to mention the trusts I invest in myself. Again, I must emphasize that this in no way intended as a recommendation; it is for information purposes only.

I don’t have a lot of money in investment trusts these days, as they are a bit too volatile for my current circumstances and overall investing strategy. But in my Bestinvest SIPP (personal pension) I do hold the following…

As you can see, I have shares in Fidelity Asian Values and Worldwide Healthcare Trust.

Both these trusts have done well for me, the latter in particular. I chose WHT because I wanted to put some of my pension money into the health sector. That is partly because I expect this sector to perform well as populations – in advanced industrial nations anyway – grow older. But it’s also because I like to think that some of my money may actually help drive advances in medicine/healthcare generally.

I invested in Fidelity Asian Values as my overall portfolio was a bit light on stocks from that region (and also, if I’m honest, because I saw this trust recommended on one of the investment news websites I follow!).

As always, if you have any comments or questions about this article, please do post them below. But bear in mind that I am not a qualified financial adviser and cannot give personal financial advice. All investment carries a risk of loss and past performance is no guarantee of future profits. You should always do your own “due diligence” before investing, and seek advice from a professional financial adviser/planner if in any doubt how best to proceed.

If you enjoyed this post, please link to it on your own blog or social media:

Today I thought I would take a closer look at Index Funds. These are among the most straightforward and cost-effective ways to invest in the stock market – especially for long-term savers and beginners.

Instead of trying to pick individual shares, index funds track a market index such as the FTSE 100, giving you broad exposure to many companies at once. This helps spread risk and keeps costs low.

In this article, I’ll explain what index funds are, which market indices they track (with a focus on popular UK and global examples), the pros and cons of index investing, and how you can invest in these funds from the UK.

Table of Contents

What Is an Index Fund?

An index fund is a type of pooled investment that aims to mirror the performance of a specific stock market index such as the FTSE 100 or the S&P 500, rather than trying to beat it via active stock picking.

Because these funds simply follow a set rule (i.e. “invest in all the companies in this index”), they tend to have much lower fees than actively managed funds.

Common Market Indices Tracked by Index Funds

UK Market Indices

FTSE 100 – Tracks the 100 largest companies on the London Stock Exchange, such as Shell and HSBC.

FTSE 250 – Covers mid-sized UK companies (not including those in the FTSE100), giving broader UK-specific economic exposure.

FTSE All-Share – Includes hundreds of UK companies across large, mid and small caps.

International Indices

S&P 500 (USA) – 500 of the largest US companies by market value.

FTSE All-World – Broad global coverage of thousands of companies across developed and emerging markets.

MSCI World – Tracks large and mid-cap companies in developed economies.

Popular UK Index Funds You Can Invest In

Here are some specific examples of index funds and ETFs available to UK investors:

UK-Focused Trackers

iShares Core FTSE 100 UCITS ETF (LSE: ISF) – Tracks the FTSE 100 index with a low ongoing charge (~0.07%).

Vanguard FTSE 100 UCITS ETF (VUKE) – Another FTSE 100 tracker, from Vanguard.

Vanguard FTSE 250 UCITS ETF – Provides exposure to mid-sized UK companies via the FTSE 250 index.

HSBC FTSE 250 Index Tracker – A low-cost option that tracks the FTSE 250.

Vanguard FTSE UK All-Share Index Fund – A broader UK fund tracking a wide range of UK shares.

Global and International Trackers

SPDR S&P 500 UCITS ETF – Tracks the S&P 500 for US market exposure.

FTSE All-World ETFs / Funds – Provide broad world-wide market exposure including developed and some emerging markets (often available via major brokers under names like FTSE All-World).

iShares MSCI World ETFs – Track global developed markets outside the UK.

💡 Most of these are available as ETFs you can buy and sell on the London Stock Exchange, and many can be held inside tax-efficient accounts like ISAs and SIPPs.

Pros of Investing in Index Funds

✅ Low Costs

Index funds usually have much lower fees than actively managed funds because there’s no expensive stock-picking involved.

✅ Diversification

A single index fund can give you exposure to hundreds or thousands of companies, spreading risk across many businesses.

✅ Simple and Transparent

The strategy and holdings are easy to understand – you know exactly which index you’re following.

✅ Competitive Long-Term Returns

Over long periods, passive index funds have often matched or beaten actively managed funds, especially after fees.

Cons of Investing in Index Funds

⚠️ You Can’t Beat the Market

Index funds aim to match the performance of their benchmark, not outperform it.

⚠️ No Protection in Downturns

When the market falls, your fund generally will too – there’s no active manager moving your investment into “safer” assets.

⚠️ Concentration Risk

Some indices (e.g. the S&P 500) are heavily weighted toward certain sectors (like tech), so your exposure might be concentrated.

Ways to Invest in Index Funds in the UK

🪙 Through a Stocks & Shares ISA

This is one of the most tax-efficient ways to hold index funds: you won’t pay UK taxes on gains or dividends each year.

🧓 Via a SIPP

Index funds can form the core of a low-cost SIPP (Self Invested Personal Pension) portfolio. Contributions may also receive tax relief.

📈 Through Investment Platforms

Platforms like Hargreaves Lansdown, AJ Bell, Interactive Investor and Trading 212 let you buy and manage index funds directly.

🤖 Robo-Advisers

Services like Nutmeg (recently renamed JP Morgan Personal Investing) or Moneybox automatically build diversified portfolios using index funds based on your risk profile.

Final Thoughts

Index funds are an excellent foundation for long-term investing – especially if you want a low-cost, diversified, hands-off approach. With options covering UK, US and global markets, you can build a portfolio that matches your goals and risk tolerance.

Disclaimer: I am not a qualified financial adviser and nothing in this article should be construed as personal financial advice. It’s important to do your own ‘due diligence’ before investing and speak to a professional financial adviser/planner if in any doubt how best to proceed. All investments carry a risk of loss.

If you enjoyed this post, please link to it on your own blog or social media:

I’ll begin as usual with my JP Morgan Personal Investing (previously Nutmeg) Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

As regular readers will know, in June this year I transferred most of the money in my former Nutmeg Fully Managed portfolio (just under £25,000) to a new Nutmeg Income Portfolio. I discussed this in detail in this post, but basically money in this port is invested to generate an income from share dividends and other sources. This is then paid monthly. Capital appreciation is targeted as well, but these portfolios are aimed primarily at older people (and others) who want/need their investment to generate a regular cash income.

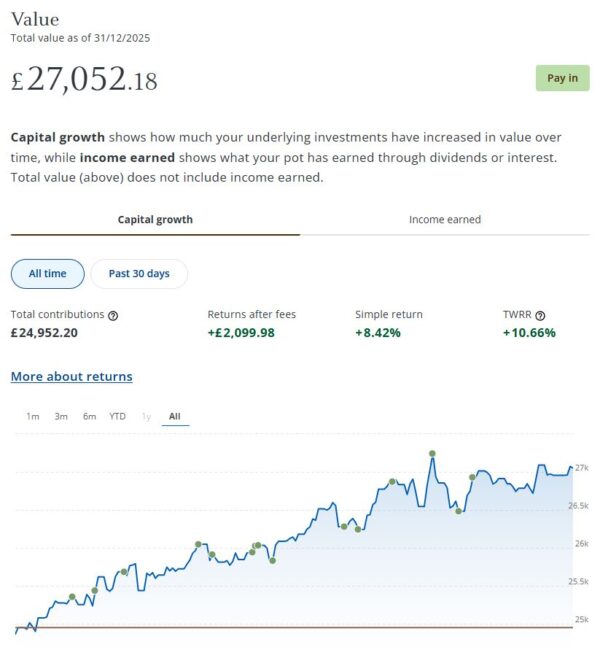

In December my JPM Investing income portfolio generated £75.04 of income, which was duly paid in to my bank account on 24 December 2025. That means I have now received a total (tax-free) income of £471.46 to date. That’s about what I would have hoped for based on JPM’s projected annual return of just under 5% for income ports at my chosen risk level (five).

My income portfolio grew in value again in December. It’s now worth £27,052 compared with £27,015 at the start of last month, a rise of £37. As the screen capture shows, the port has actually increased by £2,099.98 (8.42%) since I opened it in June this year. That’s clearly good going, though I don’t suppose it will carry on like this indefinitely. I should maybe also mention that performance may have been helped a bit by the no-fees introductory offer on Nutmeg/JPM income portfolios until the end of 2025. That has ended now, of course.

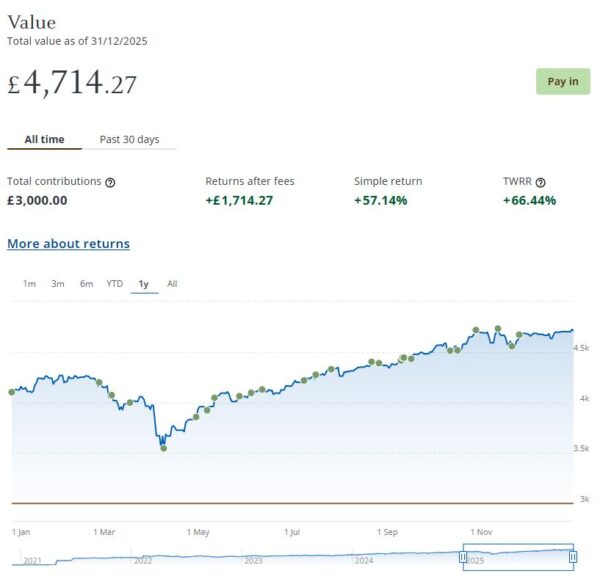

I still have a smaller, growth-oriented pot using JPM Investing’s Smart Alpha option. This is now worth £4,714 compared with £4,685 a month ago, an increase of £29. Here is a screen capture showing performance over the last year.

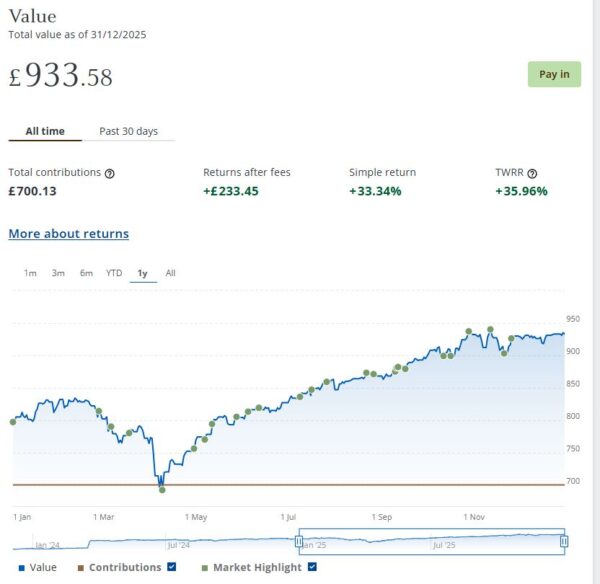

And at the start of December 2023 I invested £500 in one of Nutmeg/JPM’s thematic portfolios (Resource Transformation). In March 2024 I also invested a further £200 from referral bonuses (something I no longer receive for reasons I won’t bore you with). As you can see from the screen capture below, this portfolio is now worth £934 (rounded up) compared with £931 last month, a small increase of £3.

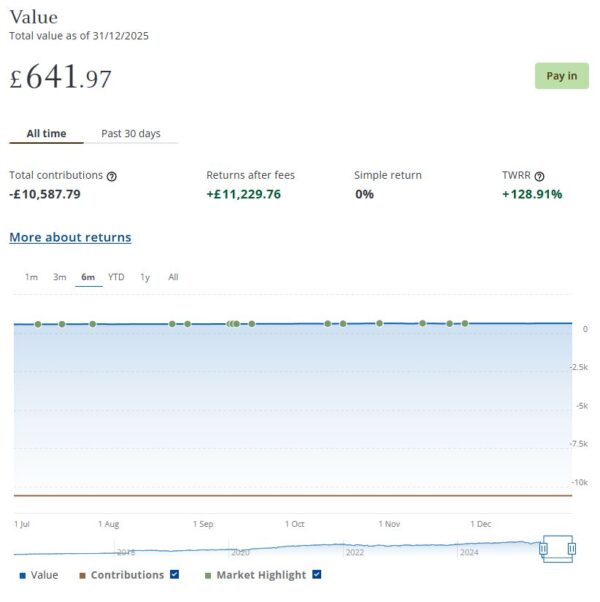

Finally, I still have a small amount left in my original Nutmeg/JPM Fully Managed portfolio. I have kept this largely for comparison purposes. This has also increased slightly in value from £637 at the start of December to £642 (rounded up) now, a rise of £5.

Overall in December I was up by £74 or 0.31%. In addition I did, of course, receive £75.04 in income from my income portfolio. Overall, then, I am in profit for the month by £149.04.

Excluding income generated, the overall value of my JPM investments is up by £2,914 or 9.58% since the start of 2025, so the April 2025 fall (caused largely by Trump’s tariffs) has now fully reversed. If you add to this figure the £471.46 of income generated so far, that gives a total profit for the last 12 months of £3,385.46 – not a bad return in these uncertain times.

As I always have to say, some volatility is to be expected with stock market investments, but over the longer term they tend to even themselves out (and generally perform better than bank savings accounts, although that is never guaranteed). In general the worst thing you can do is panic and sell up when downturns occur (as happened in April last year). You are then crystallizing your losses rather than giving the markets time to recover. This is something I had cause to discuss in this blog post.

You can read my full original Nutmeg/JPM review here. If you are looking for a home for your annual ISA allowance, based on my overall experience over the last nine years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs), Lifetime ISAs and Junior ISAs as well.

As mentioned above, Nutmeg have rebranded as J.P. Morgan Personal Investing and their website is now at www.personalinvesting.jpmorgan.com.

Moving on, I also have investments with P2P property investment platform Assetz Exchange. As discussed in this post, the company has rebranded as Housemartin.

My investments with Housemartin continue to generate steady returns. Housemartin focuses on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my HM portfolio has generated a respectable £291.50 in revenue from rental income. I have made a small net loss of £21.68 on property disposals. Capital growth generally has slowed, in line with UK property values generally.

At the time of writing, 13 of ‘my’ properties are showing gains, 5 are breaking even, and the remaining 24 are showing losses. My portfolio of 42 properties is currently showing a net decrease in value of £72.54. That means that overall (rental income minus capital value decrease and loss on disposal) I am up by £197.28. That’s still a respectable return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Housemartin most projects are socially beneficial as well.

The net fall in capital value of my Housemartin investments is obviously a little disappointing. But it’s important to remember that until/unless I choose to sell the investments in question, it is largely theoretical, based on the latest price at which shares in the property concerned have changed hands. The rental income, on the other hand, is real money (which in my case I’ve reinvested in other HM projects to further diversify my portfolio).

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of Housemartin as far as i am concerned. You can actually invest from as little as £1 per property if you really want to proceed cautiously.

As I noted in this blog post, Housemartin is particularly good if you want to compound your returns by reinvesting rental income. This effectively boosts the interest rate you are receiving. Personally, once I have accrued a minimum of £10 in rental payments, I usually reinvest this money in either a new HM project or one I have already invested in (thus increasing my holding). Over time, even if I don’t invest any more capital, this will ensure my investment with Housemartin grows at an accelerating rate and becomes more diversified as well.

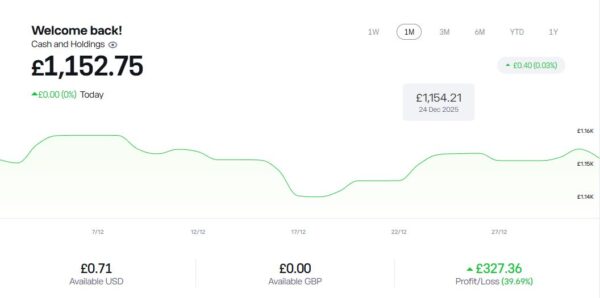

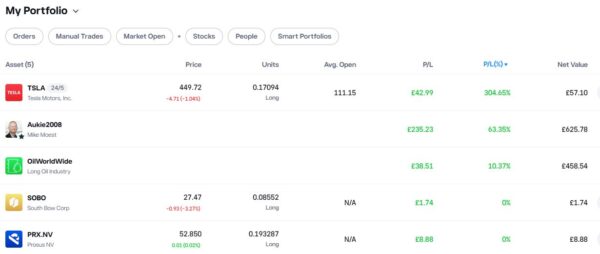

In 2022 I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios, Oil Worldwide. I also invested a small amount I had left over in Tesla shares.

As you can see from the screen captures below, my original investment (total value £888.36 in pounds sterling) is today worth £1,152.75 an overall increase of £264.39 or 29.76%.

Note: eToro now displays the value of investments in your native currency, although you can change this if you wish.

As you can see, my Oil WorldWide investment is in profit, though at 10.37% it is nothing to get excited about. My copy trading investment with Aukie2008 has been doing better, with an impressive overall profit of 63.35%. To be fair, I have held this investment a bit longer.

My Tesla shares, which I bought as an afterthought with some spare cash I had in my account, are up again this month. They are showing an overall profit of 304.65% since I bought them. If only I had put a bit more money into this!

You might also notice that I have small holdings in Prosus NV, a Dutch internet group, and South Bow, a Canadian energy infrastructure company. To be honest I don’t understand how I acquired these, but I assume they are some sort of bonus I was awarded. In any event, I am happy to have them in my portfolio.

If you would like more information about setting up an eToro account, please click on this no-obligation website link [affiliate]. Don’t forget that you also get a free $100,000 virtual portfolio, which you can use to experiment with trading and investing strategies. I have certainly earned a lot from mine.

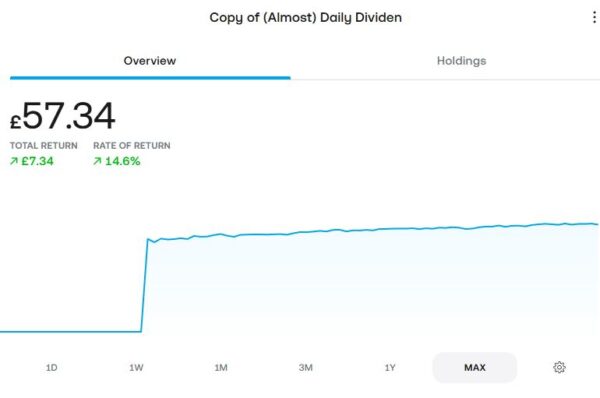

As an experiment, at the start of April this year I put £50 into an investment ISA with Trading 212. As mentioned in my recent blog post about dividend investing, I put it into the (Almost) Daily Dividends Portfolio, a ready-made portfolio or ‘pie’ on Trading 212. As you can see from the screen capture below, my portfolio is now worth £57.34, an increase of £7.34 or 14.60% over the nine-month period. It has even accrued a grand total of 77p in dividends!

I am quite impressed with how this investment has been faring, despite the small amount I put in (which means I may be missing out on some smaller dividends). If I increased my investment I would almost certainly become eligible for more dividends, and even more the longer I remain invested. If I had any spare money at the moment, I would consider doing this. Of course, I do now have an income-focused portfolio with JPM Investing as well (see above).

Moving on, I published various posts on Pounds and Sense in December. I have listed below those that are still relevant.

My Top 20 Posts of 2025 is pretty self-explanatory. In this post I listed the top twenty posts on Pounds and Sense in 2025, based on comments, page-views and social media shares, excluding any that were no longer relevant. I hope you might enjoy revisiting these posts, or seeing them for the first time if you are new to PAS.

In Why You Should Beware of Going ‘All-In’ on Electricity I focused on a topic that has become of increasing concern to me in recent months. Over the past decade, UK households have been encouraged to electrify almost everything. Cars are going electric. Gas boilers are being phased out in favour of electric heat pumps. Even cooking is increasingly moving from gas to electricity. Of course, on paper this all fits with the Government’s drive towards Net Zero. But in this post I addressed a growing issue that doesn’t get discussed nearly enough: What happens if the electricity supply isn’t always there when you need it?

Also in December I published New Trading 212 Offer – Get a Guaranteed £25 Cash. This is a rare opportunity to get a guaranteed £25 cash by opening a new Trading 212 Invest account (it’s different from their usual free share promotion, which is currently closed). My post explains what you have to do to claim this money. The offer ends on 20 January 2026.

I also published another syndicated guest post by Primrose Freestone, Senior Lecturer in Clinical Microbiology at Leicester University. This one is on the subject Can You Wear the Same Socks More Than Once? I published another article by Dr Freestone recently on how often you should wash your bedding, which generated a lot of interest. If you enjoyed that article, hopefully you will like this one as well. Again it contains a lot of eye-opening information, including some tips on when and how you should launder socks.

Finally, in What Are the Best Video Calling Tools for Older People? I discussed the benefits for older folk of using video-calling tools and apps to keep in touch with friends and family. I described a range of options, explaining how they work and whom they might be most suitable for. This article was published with Christmas in mind, but obviously it is relevant at other times of the year as well.

I’ll close with a reminder that you can also follow Pounds and Sense on Facebook or Twitter (or X as we have to call it now). Twitter/X is my number one social media platform and I post regularly there. I share the latest news and information on financial matters, and other things that interest, amuse or concern me. So if you aren’t following my PAS account on Twitter/X, you are definitely missing out!

I am also on the BlueSky social media network under the username poundsandsense.bsky.social. Twitter/X remains my primary social media platform, but I also post details of my latest blog posts, third-party articles and other financial news and resources on BlueSky for those who prefer to follow me there.

As always, if you have any comments or questions, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts on PAS may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media:

In my update today, I’m focusing on a topic that has become of growing concern to me in recent months.

Over the past decade, UK households have been encouraged to electrify almost everything. Cars are going electric. Gas boilers are being phased out in favour of heat pumps. Even cooking is increasingly moving from gas to electricity.

On paper, this all fits with the Government’s drive towards Net Zero. But there’s a growing issue that doesn’t get discussed nearly enough: What happens if the electricity supply isn’t always there when you need it?

As we look ahead to the coming years, relying solely on electricity to power and heat your home could leave you exposed – financially and practically.

Table of Contents

Growing Pressure on the UK’s Electricity System

Electricity demand in the UK is set to rise sharply. Two of the biggest drivers are:

Electric vehicles (EVs) – millions of households charging cars at home, often at similar times of day

Electric heat pumps – particularly air-source heat pumps, which draw large amounts of power in cold weather

At the same time, electricity generation is becoming increasingly weather-dependent. Wind and solar are growing fast, but they don’t always produce power when demand is highest – especially during cold, still winter evenings when heating demand peaks.

The National Grid has so far managed to keep the lights on, but it has done so by relying on emergency measures, reserve power contracts and public appeals to reduce usage at peak times. That’s a sign of a system under strain.

The Risk of Power Cuts Is Increasing, Not Decreasing

While widespread blackouts are still relatively rare, the risk of localised or short-term power cuts is rising.

Reasons include:

an ageing electricity distribution network

rapid increases in peak demand

greater reliance on intermittent renewable generation

delays and cost overruns in upgrading grid infrastructure

For households that depend entirely on electricity for heating, hot water and cooking, even a short power cut in winter can quickly become a serious problem.

When Electricity Goes Off, Everything Stops

If your home uses electric heating only:

heat pumps stop working

electric radiators go cold

immersion heaters stop producing hot water

induction hobs and electric ovens are unusable

By contrast, homes with non-electric power and heating options retain a degree of resilience. That resilience has real value, particularly for older people, families with young children, or anyone living in rural areas where power cuts tend to last longer.

Diversification Isn’t Just for Investments

Regular readers of Pounds and Sense will be familiar with the idea of diversification. You wouldn’t normally put all your savings into a single investment – and the same principle applies to household energy.

Having more than one way to heat your home reduces risk and gives you flexibility when prices spike or supplies are disrupted.

Alternative and Backup Heating Options to Consider

Here are some heating methods that can be used instead of, or alongside, electricity:

Gas Heating (Where Available)

Despite its declining popularity in policy circles, mains gas remains:

reliable

relatively inexpensive

highly controllable

independent of the electricity grid (for heat, though central heating boilers still need some power to operate)

A gas boiler can continue to provide warmth during electricity shortages if paired with a simple backup power source, such as a home storage battery or generator. In addition, most free-standing gas fires can operate without any need for electricity.

Wood-Burning or Multi-Fuel Stoves

A solid fuel stove can be an excellent backup heat source:

operates independently of electricity

provides direct radiant heat

can often heat a large living space effectively

Modern stoves are far cleaner and more efficient than older open fires, though fuel storage and local air-quality rules must be considered.

Open Fires and Solid Fuel Fires

While less efficient than stoves, open fires still provide:

a non-electric source of heat

emergency warmth during prolonged outages

They can also burn a range of fuels, depending on the fireplace and chimney setup. Again, fuel storage and local air-quality rules will need to be considered.

Oil or LPG Heating (Rural Homes)

For off-grid properties, oil or LPG systems offer:

independence from the electricity network for fuel supply

predictable heating performance in cold weather

They are often criticized on environmental grounds, but from a resilience perspective they remain useful options.

Portable Backup Options

Even smaller measures can help:

portable gas heaters (used safely and with ventilation)

camping stoves for boiling water

thermal storage heaters or insulated hot water tanks

These won’t heat a whole house but can make a big difference during short outages.

Balancing Net Zero with Common Sense

The Government’s rush towards Net Zero is placing enormous pressure on the UK’s energy system. Whether the huge cost and disruption caused can be justified is (in my opinion anyway) arguable. What’s in no doubt, however, is that thetransition period will be messy, expensive and uncertain.

Households that move too quickly to an all-electric setup may find themselves exposed to:

higher running costs

reduced resilience

greater vulnerability during supply disruptions

That doesn’t mean rejecting electrification entirely – but it does mean thinking very carefully before putting all your power and heating eggs in one basket.

My Personal Situation

I live in a detached house built about 40 years ago in suburban Staffordshire. I have gas central heating and an electric cooker. I also have a free-standing gas-fire in the lounge. I have solar panels on the roof and a Givenergy home-storage battery, which I bought a couple of years ago.

When I first heard about heat pumps I did look into the possibility of getting one. I soon realised, however, that I didn’t want to go down this route. As discussed above, I didn’t like the thought of becoming too reliant on electricity, especially with the growing likelihood of power outages. Also, the heating pipes in my house are quite narrow and I have been advised that if I were to get a heat pump, the existing pipes would all have to be taken out and replaced as well. Needless to say, that would add considerably to the cost, not to mention the disruption.

In addition, heat pumps generally operate at lower temperatures than gas central heating, meaning they have to be kept on all the time to ensure the house remains at a comfortable temperature. I have also heard it said that in very cold weather they may not be able to provide adequate warmth on their own. So you really do still need a back-up heating option anyway.

With all these considerations (and others), I therefore plan to stick with my present set-up for the foreseeable future. If at some point gas boilers are banned and/or gas is cut off completely, I will obviously have to rethink this. But as I am now 70, realistically that’s unlikely to happen in my lifetime. In the improbable event that it does, I would think about switching to an electric boiler, which could be installed instead of my old gas boiler without all the pipes in the house having to be torn out and replaced. This would be a lot cheaper to buy and less disruptive than switching to a heat pump, though possibly more expensive to run. Looking to the future, other non-heat-pump alternatives are very likely to appear as well.

Obviously, all of this is just my personal opinion. You may disagree, but I thought it might be helpful to explain my thinking on these matters as they stand now.

The Bottom Line

Electric heating will undoubtedly play a major role in the UK’s future. But in my view relying on electricity alone for heating is increasingly risky.

Where possible, having an alternative or supplementary heating source provides:

peace of mind

practical resilience

protection against both power cuts and price shocks

As with personal finance, a bit of diversification can go a very long way.

As always, I welcome any comments or questions on this article.

If you enjoyed this post, please link to it on your own blog or social media:

If you’ve been thinking about dipping your toes into investing – or you’re just after a quick cash boost at this expensive time of year – there’s a new Trading 212 offer on the table that’s worth checking out.

There is a £25 welcome reward for new UK customers who sign up and complete a few simple steps with Trading 212. Note that this is a limited-time offer that closes on 20 January 2026.

Table of Contents

💰 What’s the Offer?

Trading 212 is currently running a limited-time promotion in the UK where new customers can earn a £25 cash reward by:

Signing up for a Trading 212 Invest account using a referral link (like mine below)

Verifying your identity

Depositing funds and ordering a free Trading 212 card

Using the card to make 3 transactions of £5 or more each within 10 days of opening your account

Once those conditions are met, you get £25 in cash credited to your account – and you can use that money however you like!

Here’s a breakdown of what you need to do if you want to take part in this offer:

📌 Step 1: Sign Up Click through my referral link and register for a new Trading 212 Invest account (UK residents only, new users only).

📌 Step 2: Verify Your Account Trading 212 requires standard ID checks (passport, driving licence, address details, etc.). This helps satisfy regulatory “Know Your Customer” requirements.

📌 Step 3: Deposit Funds Add at least £1 to your Trading 212 account – although you may want to deposit a bit more so you can do Step 4 straight away as well.

📌 Step 4: Order & Use Your Card Order the free Trading 212 card and make three transactions of £5 or more – these can be everyday purchases you’d make anyway.

📌 Step 5: Get Your £25 After you meet the criteria, your £25 reward should be credited within a few business days. (You will have to wait 30 days before you can withdraw it.)

💷 What Is the Trading 212 Card?

As part of this offer, you need to order and use the Trading 212 card. So what exactly is it?

The Trading 212 card is a free debit card (physical and virtual) linked directly to your Trading 212 Invest account. It allows you to spend money held in your account just like you would with a normal bank debit card. Here is a quick summary of how it works…

Linked to your Trading 212 balance Any uninvested cash in your Trading 212 account can be used for card payments.

Everyday spending You can use the card in shops, online, and via contactless payments, just like a standard debit card.

No need to invest You don’t have to buy shares or funds to use the card. You can simply deposit money and spend it.

Free to order There’s no charge to order the card, and it’s managed through the Trading 212 app.

UK and overseas use The card can be used abroad, making it handy for travel or online purchases from overseas retailers (although exchange rates and fees can vary, so always check the latest terms).

Even after the bonus is paid, some people choose to keep the card as a secondary spending card, while others simply withdraw their money and stop using it. There’s no obligation to keep spending with it long term.

As always, it’s worth keeping an eye on Trading 212’s terms and conditions, as card features and fees can change over time.

💡 Why This Is a Good Deal

This is a no-brainer for most people because:

You don’t need to invest in stocks and shares to earn the £25 – just make normal card purchases you were planning to do anyway.

The minimum effort required is low: three card payments within 10 days.

You can withdraw the bonus cash after a short delay and spend it or reinvest it however you choose.

🧠 Things to Know

Offers like this can end or change at any time – so if you are interested, it’s worth acting sooner rather than later.

This is different from Trading 212’s free share promotion, which exists separately and offers up to £100 in free shares for new users. I discussed this offer in a separate blog post. Note that the Trading 212 free share offer is not available at the time of writing and I don’t know when (or if) it will return.

You must use a referral link to qualify for the £25 bonus.

You must also open an Invest account to qualify. A Stocks ISA, Cash ISA or CFD account won’t work (though you can open any of these subsequently).

📌 Final Thoughts

If you’ve been on the fence about trying out a stock trading or investment app, this £25 welcome reward from Trading 212 is a genuinely easy way to benefit from signing up. It doesn’t require any complicated investing – you can simply earn the bonus and decide what comes next. Just be sure to follow the steps above carefully and meet all the qualifying requirements.

And don’t forget that this limited-time offer closes on 20 January 2026.

As always, if you have any comments or questions about this post, please do leave them below.

Disclosure: If you take up this offer via my referral link, I will also receive a cash bonus for introducing you. The £25 cash bonus is guaranteed if you follow the steps set out above. If you choose to reinvest this money, however, be aware that – as with all investing – there is a risk of loss if you put the money into equities (stocks and shares). You should always do your own “due diligence” before investing and seek advice from a qualified financial planner/adviser if in any doubt how best to proceed.

If you enjoyed this post, please link to it on your own blog or social media:

As is customary for bloggers at this time of year, here are the top twenty posts on Pounds and Sense in 2025, based on comments, page-views and social media shares. They are in no particular order. I have excluded any posts that are no longer relevant.

I hope you will enjoy revisiting these posts, or seeing them for the first time if you are new to PAS.

All posts in the list below should open in a new tab/window when you click on the link concerned.

I’ll be taking a break from blogging over the festive period (though I’ll still be around on X/Twitter and Facebook). I’ll therefore close by wishing you a Very Merry Christmas (strikes and cost-of-living crisis permitting) and for all of us a brighter, more prosperous new year

If you have any comments or questions, of course, feel free to leave them below as usual.

If you enjoyed this post, please link to it on your own blog or social media:

Christmas will soon be here. But with flu and other respiratory infections at high levels – and the Covid pandemic still a fairly recent memory – many older people will be understandably cautious about how much face-to-face socialising they do at this time of year.

In addition, we’re still feeling the effects of the cost-of-living crisis. Many pensioners are cash-strapped, and rising energy costs make winter harder than ever. Add in bad weather, NHS and rail strikes, busy roads and crowded trains, and reduced face-to-face socialising becomes a real possibility, especially for older adults. Loneliness at Christmas can lead to anxiety, depression and other health issues.

While video calling isn’t a complete solution, it can be a lifeline for keeping in touch with distant friends, family, children and grandchildren – especially if travel or health concerns make meeting in person difficult.

So here’s an updated guide to the best video calling tools for older people in 2025, including what you need and the pros and cons of each option.

How to Get Started

To make video calls, you’ll need:

A device with a camera and microphone – like a smartphone, tablet, laptop, Chromebook or desktop with webcam.

A reliable internet connection – ideally wi-fi at home (video calls can use a lot of mobile data).

A video calling app – more on this below.

All modern smartphones (iPhones and Androids) have good-quality cameras. Tablets and laptops usually have larger screens which make conversations easier to see and more comfortable for group calls.

If you’re using a desktop, you might need a separate webcam and microphone unless your machine already has them built in.

Video Calling Tools Worth Considering

Table of Contents

1. FaceTime (for Apple Users)

Best for: iPhone and iPad users whose family also uses Apple devices

Smartphones: Yes

Tablets: Yes

Windows: No

Mac: Yes

FaceTime remains one of the easiest options if everyone is in the Apple ecosystem. It comes pre-installed on iPhones and iPads, and calls are seamless and high quality. You can add up to 32 people in a group call.

Pros:

Built into Apple devices – no extra download

High video quality and simple interface

Works with newer features like scheduling links and spatial audio

Cons:

Only works with Apple devices

Not cross-platform (except via browser links in newer versions)

2. WhatsApp

Best for: Informal chats with family and small group calls

Smartphones: Yes

Tablets: Limited (WhatsApp on some tablets may not support video yet)

Windows/Mac: Yes (via desktop app)

WhatsApp is one of the most widely used apps in the world and is familiar to many older people already. Recent updates now allow up to 32 people on one video call, plus screen-sharing and a “speaker spotlight” to highlight whoever’s talking.

Pros:

Very familiar and widely adopted

End-to-end encryption

Works across devices

Cons:

Requires contacts to use WhatsApp too

Owned by Meta — some users dislike data-sharing practices

3. Messenger (Meta/Facebook)

Best for: Users who already use Facebook and want extra features

Smartphones: Yes

Tablets: Yes

Windows/Mac: Yes

Messenger lets you video call directly from your Facebook contacts. It’s quite straightforward and supports up to 50 people with no time limit on group calls.

Pros:

Connects with existing Facebook friends

Fun features (filters, translation tools, games)

Works across all major platforms

Cons:

Requires a Facebook account

Some features may feel cluttered for very simple calls

4. Zoom

Best for: Larger family gatherings or planned group events

Smartphones/Tablets/PC/Mac: Yes

Zoom is still widely used for large group calls and celebrations. On the free plan you can host up to 100 people, though sessions may be time-limited (often around 40–60 minutes) unless you have a paid subscription.

Pros:

Great for big groups (birthdays, Christmas catch-ups)

Works on nearly all devices

Easy to join via links

Cons:

Time limits on free accounts

More features than some older people need

5. Google Meet

Best for: Longer chats and group calls without app installs

Smartphones/Tablets: Yes

Windows/Mac: Yes

Google Meet is a solid everyday option with no required paid plan for basic use, up to 100 people on free accounts, and features like live captions.

Pros:

Good for group calls of all sizes

Works in a browser (no app install needed)

Integration with Google Calendar

Cons:

May feel business-oriented for casual use

6. Microsoft Teams (Replacing Skype)

Best for: People who used Skype and want a modern replacement

Note: Skype was retired in 2025 and replaced by Microsoft Teams, so new Skype recommendations are no longer relevant. Users are being encouraged to move to Windows Teams where chat history and contacts can carry over.

Pros:

Continued support and development

Group calls and chatting similar to Skype

Cons:

More features than some users need

Setup can be more complex than simpler apps like WhatsApp

Devices That Make Calling Easier for Seniors

Beyond apps, there are dedicated devices that make video calling much simpler for older people:

Smart displays like the Amazon Echo Show – big screens, voice commands (“Alexa, video call Mum”), and simplified controls.

Senior-friendly tablets (such as this one) with simplified interfaces and large buttons.

These devices are ideal for those less comfortable with standard phones or computers.

✔ Keep software updated: The latest versions of apps are generally more reliable and secure. ✔ Use wi-fi: Video calls eat data – wi-fi helps avoid extra charges. ✔ Practice together: A short practice call before a big family chat can ease nerves. ✔ Label apps clearly: Rename icons on tablets or phones so they’re easy to find.

Closing Thoughts

Video calling isn’t just a tech trend for businesses and younger people – it’s a lifeline for older adults to stay connected, especially around busy times like Christmas.

The right setup – a good device, a reliable connection, and the right app – can make chatting over distance almost as good as being there in person.

I hope you have found this article helpful. As always, if you have any comments or questions about this post, please do leave them below.

Note: this is a fully revised update of an annual article.

If you enjoyed this post, please link to it on your own blog or social media:

It’s pretty normal to wear the same pair of jeans, a jumper or even a t-shirt more than once. But what about your socks?

If you knew what really lived in your socks after even one day of wearing, you might just think twice about doing it.

Our feet are home to a microscopic rainforest of bacteria and fungi – typically containing up to 1,000 different bacterial and fungal species. The foot also has a more diverse range of fungi living on it than any other region of the human body.

Most foot bacteria and fungi prefer to live in the warm, moist areas between your toes where they dine on the nutrients within your sweat and dead skin cells. The waste products produced by these microbes are the reason why feet, socks and shoes can become smelly.

For instance, the bacteria Staphylococcal hominis produces an alcohol from the sweat it consumes that makes a rotten onion smell. Staphylococcus epidermis, on the other hand, produces a compound that has a cheese smell. Corynebacterium, another member of the foot microbiome, creates an acid which is described as having a goat-like smell.

The more our feet sweat, the more nutrients available for the foot’s bacteria to eat and the stronger the odour will be. As socks can trap sweat in, this creates an even more optimal environment for odour-producing bacteria. And, these bacteria can survive on fabric for months. For instance, bacteria can survive on cotton for up to 90 days. So if you re-wear unwashed socks, you’re only allowing more bacteria to grow and thrive.

The types of microbes resident in your socks don’t just include those that normally call the foot microbiome home. They also include microbes that come from the surrounding environment – such as your floors at home or in the gym or even the ground outside.

In a study which looked at the microbial content of clothing which had only been worn once, socks had the highest microbial count compared to other types of clothing. Socks had between 8-9 million bacteria per sample, while t-shirts only had around 83,000 bacteria per sample.

Species profiling of socks shows they harbour both harmless skin bacteria, as well as potential pathogens such as Aspergillus, Candida and Cryptococcus which can cause respiratory and gut infections.

The microbes living in your socks can also transfer to any surface they come in contact with – including your shoes, bed, couch or floor. This means dirty socks could spread the fungus which causes Athlete’s foot, a contagious infection that affects the skin on and around the toes.

This is why it’s especially key that those with Athlete’s foot don’t share socks or shoes with other people, and avoid walking in just their socks or barefoot in gym locker rooms or bathrooms.

What’s living in your socks also colonises your shoes. This is why you might not want to wear the same pair of shoes for too many days in a row, so any sweat has time to fully dry between wears and to prevent further bacterial growth and odours.

Foot hygiene

To cut down on smelly feet and reduce the number of bacteria growing on your feet and in your socks, it’s a good idea to avoid wearing socks or shoes that make the feet sweat.

Washing your feet twice daily may help reduce foot odour by inhibiting bacterial growth. Foot antiperspirants can also help, as these stop the sweat – thereby inhibiting bacterial growth.

It’s also possible to buy socks which are directly antimicrobial to the foot bacteria. Antimicrobial socks, which contain heavy metals such as silver or zinc, can kill the bacteria which cause foot odour. Bamboo socks allow more air flow, which means sweat more readily evaporates – making the environment less hospitable for odour-producing bacteria.

Antimicrobial socks might therefore be exempt from the single-use rule depending on their capacity to kill bacteria and fungi and prevent sweat accumulation.

But for those who wear socks that are made out of cotton, wool or synthetic fibres, it’s best to only wear them once to prevent smelly feet and avoid foot infections.

It’s also important to make sure you’re washing your socks properly between uses. If your feet aren’t unusually smelly, it’s fine to wash them in warm water that’s between 30-40°C with a mild detergent.

However, not all bacteria and fungi will be killed using this method. So to thoroughly sanitise socks, use an enzyme-containing detergent and wash at a temperature of 60°C. The enzymes help to detach microbes from the socks while the high temperature kills them.

If a low temperature wash is unavoidable then ironing the socks with a hot steam iron (which can reach temperatures of up to 180–220°C) is more than enough kill any residual bacteria and inactivate the spores of any fungi – including the one that causes Athlete’s foot.

Drying the socks outdoors is also a good idea as the UV radiation in sunlight is antimicrobial to most sock bacteria and fungi.

While socks might be a commonly re-worn clothing item, as a microbiologist I’d say it’s best you change your socks daily to keep feet fresh and clean.