Nutmeg Launches New Income Investing Portfolios

Today I am looking at the new income investing option recently introduced by UK robo-adviser platform Nutmeg. This is designed for people who want to receive a regular monthly income while keeping their money invested (and hopefully still growing).

As a long-term Nutmeg investor myself (you can read my in-depth review here), I have already taken advantage of this opportunity. I will discuss my personal experience (so far) in more detail below. But first, here’s how it works in a nut(meg)shell, how it compares with Nutmeg’s traditional growth portfolios, and who might benefit the most.

How Nutmeg’s Income Portfolios Work

- Powered by J.P. Morgan Asset Management (JPMAM)

Nutmeg has collaborated with JPMAM to construct five risk‑rated portfolios, built around actively managed income-focused ETFs – including the JP Morgan Equity Premium Income strategy – so you’re investing in income-optimized assets while staying diversified.

2. Five Risk Levels to Suit You

You can choose from five different risk levels, ranging from 1 (cautious) to 5 (adventurous), based on your circumstances, goals and appetite for risk. Each level offers a different blend of equity and bond exposure to balance income generation with capital stability.

Here’s a table describing Nutmeg’s five income portfolio risk levels in simple terms…

| Risk Level | Description | Equity Exposure | Income Potential | Capital Risk |

| 1 – Cautious | Prioritizes stability over returns | Low | Low | Very Low |

| 2 – Conservative | Aims for modest, steady income with minimal volatility | Low to Moderate | Low to Medium | Low |

| 3 – Balanced | Balanced mix of bonds and equities for moderate income and risk | Moderate | Medium | Moderate |

| 4 – Growth-Oriented | Greater focus on equity income for higher payouts | Moderate to High | Medium to High | Moderate to High |

| 5 – Adventurous | Maximizes income potential with higher risk tolerance | High | High | High |

📌 Note: All portfolios are actively managed and diversified, but the mix of assets changes based on your selected risk level. Income smoothing and monthly payouts are available across all five.

3. Monthly Payouts with Optional Smoothing

One standout feature is income smoothing. This spreads out income across the year, so you receive consistent monthly payments – even if dividends or yields vary from month to month. This feature is optional, however – you can turn smoothing off if you’d rather receive income as it’s earned every month.

4. No Nutmeg Management Fee for 2025

These portfolios are available via ISA or General Investment Accounts (non-ISA) and have no Nutmeg management fee for the rest of 2025, though underlying ETF costs apply. A minimum investment of £10,000 is required.

5. Capital Remains Invested

Your core investment stays fully invested in the market – providing the potential for capital preservation or growth alongside the monthly income stream.

| Income Portfolio | Growth Portfolio | |

|---|---|---|

| Objective | Provide regular monthly income | Maximize long‑term capital growth |

| Payouts | Paid out monthly, with optional smoothing | Reinvested automatically for compounding |

| Yield Focus | Uses dividend and income-focused ETFs | Focus on market growth; income secondary |

| Suitability | Later-stage savers, retirees, cash flow needs | Long-term goals like retirement, wealth accumulation |

While Nutmeg’s growth-oriented portfolios reinvest dividends to compound, the income portfolios are specifically structured to generate ongoing monthly payments. This is ideal for those needing a regular income rather than capital appreciation (though some capital appreciation will hopefully occur as well).

Who Are These Portfolios Best For?

-

Retirees or near‑retirees needing a dependable income stream without selling assets.

-

Those reducing work hours or with varied income, using the monthly payouts to smooth out earnings.

-

Investors frustrated with traditional bond/dividend returns – Nutmeg’s own research shows 69% of UK investors prioritize income, yet many are unhappy with current options.

-

Investors seeking simplicity – You set your risk level once and Nutmeg then handles asset selection, portfolio rebalancing and (optional) income smoothing. As with all Nutmeg investments, you can change your risk level later if you wish (though some extra costs may be incurred when doing so).

Pros and Considerations

👍 Pros:

-

Monthly income stream without selling investments

-

Income smoothing for consistent payouts

-

Actively managed by experts at JPMAM

-

No Nutmeg fees until 2026

⚠️ Considerations:

-

Requires £10,000 minimum to start

-

Still carries investment risk – capital isn’t guaranteed

-

Fund fees apply for underlying ETFs

-

If you’re focused purely on capital growth, growth portfolios with reinvestment may outperform long-term

My Experience

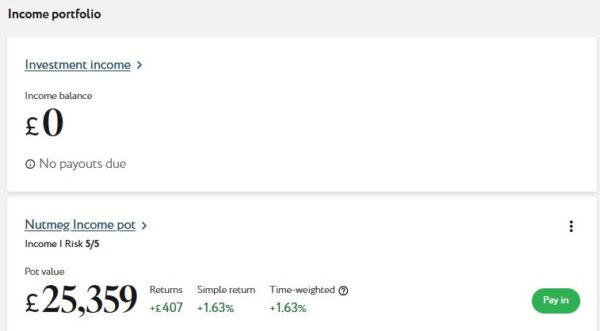

As you will know if you read my July 2025 Investments Update, in June I transferred most of the money in my Nutmeg Fully Managed portfolio (just under £25,000) to a new Nutmeg Income Portfolio. As my money was already invested via a Stocks and Shares ISA, my new income portfolio will enjoy that status as well, meaning income payments will be made without any deductions for tax. Likewise, any capital appreciation will not be taxable.

I selected a risk level of 5 (the maximum). That aligns with the risk level of my other Nutmeg investments, which should make it easier to compare them. More importantly, though, I have other investments that are lower risk, including my Bestinvest SIPP (personal pension) and – of course – my state pension. With my Nutmeg investments I hope to maximize their income and growth potential and am comfortable taking a few more risks to this end. As I have other, less risky investments, any reversals with Nutmeg shouldn’t be disastrous. Obviously as I get older – or if my circumstances change – I may revisit this.

For similar reasons, I chose not to select the ‘smoothing’ option. The income from my Nutmeg income portfolio will be in addition to other regular income streams I already have, so I can’t see any particular reason to have these payments smoothed out. Obviously I will monitor this and might change my mind in future, but for now I quite like the idea of having a variable extra payment each month. If it’s large, I may allow myself a few extra treats that month. If it’s small, I will adjust my expenditure accordingly.

- Of course, the above is solely my personal perspective and should not be construed as financial advice. Everyone’s circumstances are different. You should always do your own ‘due diligence’ before investing and seek professional advice if uncertain how best to proceed. All investing carries a risk of loss.

As the screenshot below shows, my Income portfolio is already showing a profit of over £400, which is obviously welcome. It hasn’t yet generated any income, but that is unsurprising. It can take a while for investments to qualify for dividend payments, so I am keeping my expectations modest, initially at least 🙂

I will update PAS readers on how my Nutmeg income portfolio performs in my future monthly investments updates.

Closing Thoughts

In my view, Nutmeg’s new Income Investing portfolios are a valuable addition for UK investors seeking a regular income, backed by diversified, actively managed ETFs. They offer monthly, optionally smoothed payouts, managed via Nutmeg’s simple, user-friendly interface. The fact that there is no initial Nutmeg management fee through 2025 is a further attraction.

If your priorities include current cash flow, retirement‑style income, or smoothing irregular income, this could be a good fit. If you’re younger or focused on maximizing long-term growth via compounding, however, Nutmeg’s established growth portfolios (e.g. Smart Alpha) remain compelling options.

If you have any comments or questions about this post – or Nutmeg more generally – please do leave them below. As always, bear in mind that I am not a qualified financial adviser and cannot offer personalized financial advice. As with all investments, your capital is at risk and there are no guarantees of profit. If in any doubt, consider speaking with a financial services professional.

July 11, 2025 @ 6:34 pm

Interesting to see Nutmeg going down the income investing route, but it feels like it could be marketing rather than sensible investing. There’s some really insightful research from Vanguard about how a ‘total return’ approach, usually leads to higher returns with less risk. For those looking to optimise how much they need to retire, this is key, where an income focused approach can require a much higher level of starting wealth. Have you looked into this?

July 11, 2025 @ 7:06 pm

Thanks, Edward. I’m inclined to agree that for younger people, a total return approach might work better. And yes, I do this myself with some other investments I hold. As I am now retired my circumstances have changed and income is a bigger priority for me. I am looking forward to seeing how my Nutmeg income portfolio performs going forward. It is obviously a bit of an experiment for me.