Free Wills Month brings together a group of well-respected charities to offer members of the public aged 55 and over the opportunity to have their wills written or updated free using participating solicitors across the UK.

The charities involved include the NSPCC, Dogs Trust, Samaritans, Mind, Age UK, The Stroke Association, PDSA, and many others. Free Wills Month happens twice a year, in March and October.

The scheme covers simple wills only, including ‘mirror wills’ for couples. In the latter case, only one member of the couple has to be 55 or over. If you need a complicated will (most people don’t) you can still have this done but may have to pay a top-up fee.

I have talked about the importance of creating a will and why you should get it done by a properly qualified solicitor previously on PAS. An up-to-date will written by a solicitor will ensure that your wishes are respected and will avoid causing legal complications for your loved ones after you are gone.

Free Wills Month means what it says. There are no catches, although the organizers hope that you will choose to leave a donation to charity in your will. There is no obligation to do this, however.

To take part in Free Wills Month click through to the website during October and fill in your details. You can then pick a solicitor from the list of companies taking part and contact them to book an appointment. Appointments are limited and on a first come, first served basis, so it’s best to apply as soon as possible to avoid disappointment.

Free Wills Month October 2025 starts officially on Wednesday 1st October 2025 but you can sign up on the FWM website to be notified when when the campaign starts in your area.

If you have any comments or questions about this subject, as ever, please do post them below.

Note: This is a revised and updated version of my original post on this subject.

If you enjoyed this post, please link to it on your own blog or social media:

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

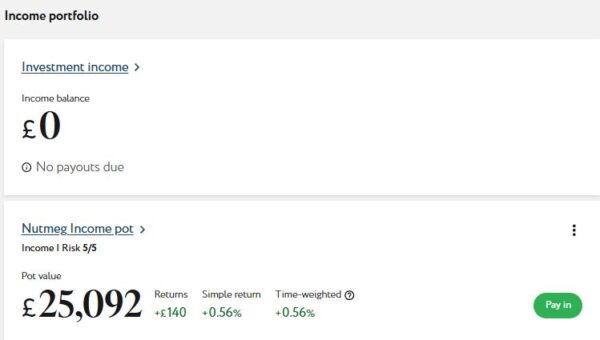

As regular readers will know, in June I transferred most of the money in my Nutmeg Fully Managed portfolio (just under £25,000) to a new Nutmeg Income Portfolio. I discussed this in detail in this recent post, but basically money in this port is invested to generate an income from share dividends and other sources. This is then paid monthly. Capital appreciation is targeted as well, but these portfolios are aimed primarily at older people (and others) who want/need their investment to generate a regular cash income.

In August my Nutmeg income portfolio generated £134.03 of income, which was duly paid in to my bank account on 22 August 2025. Based on Nutmeg’s estimated annual return of just under 5% for income ports at my chosen risk level (five), I had been expecting around £100, so this was somewhat better than that. Obviously it is far too early to draw any conclusions, though.

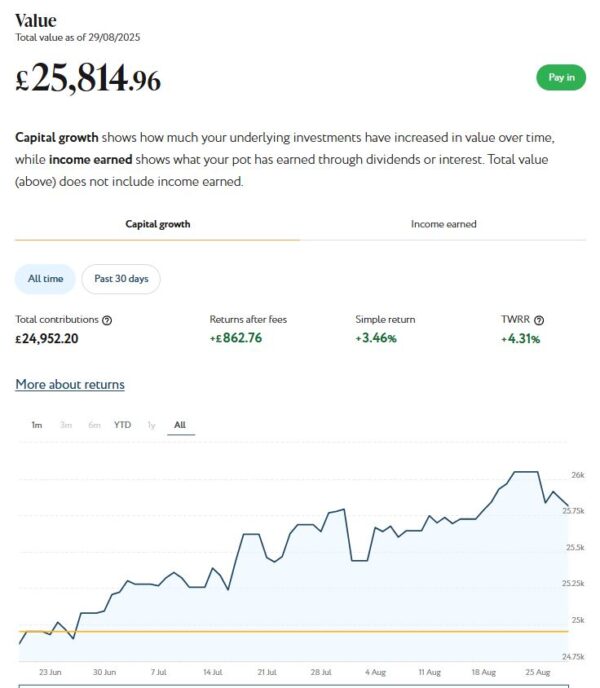

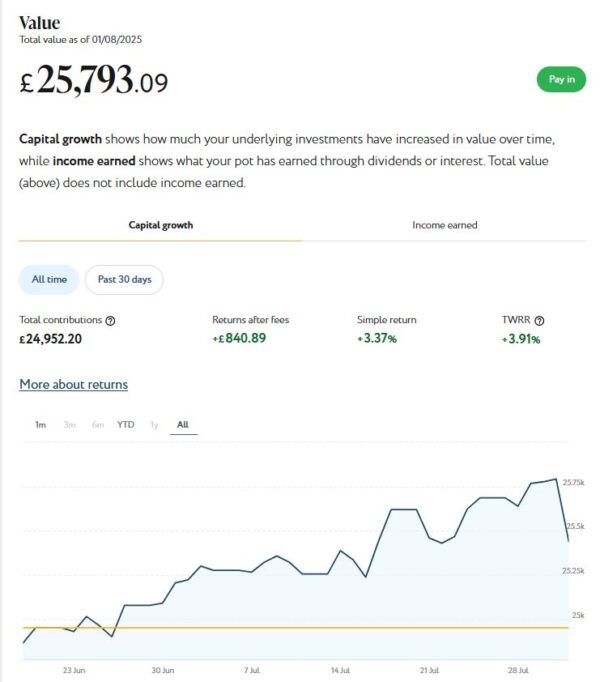

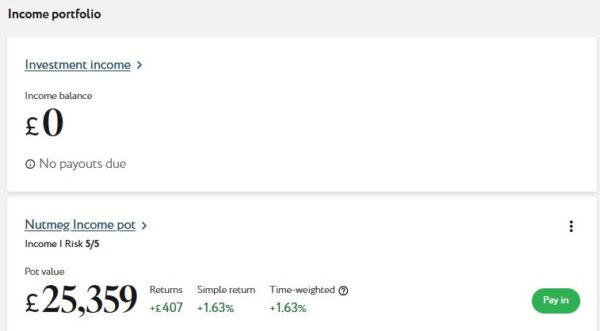

My income portfolio has also grown a little in value in August. It’s now worth £25,815 compared with £25,793 at the start of last month, an increase of £22. As the screen capture shows, the port has actually grown in value by £862.76 (3.46%) since I opened it.

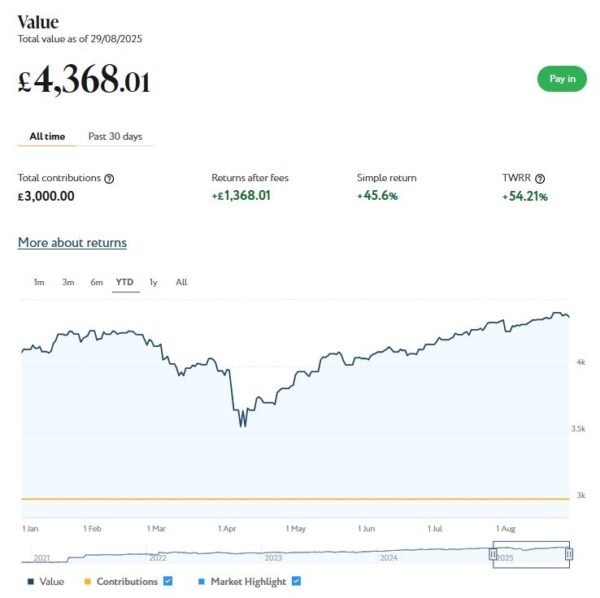

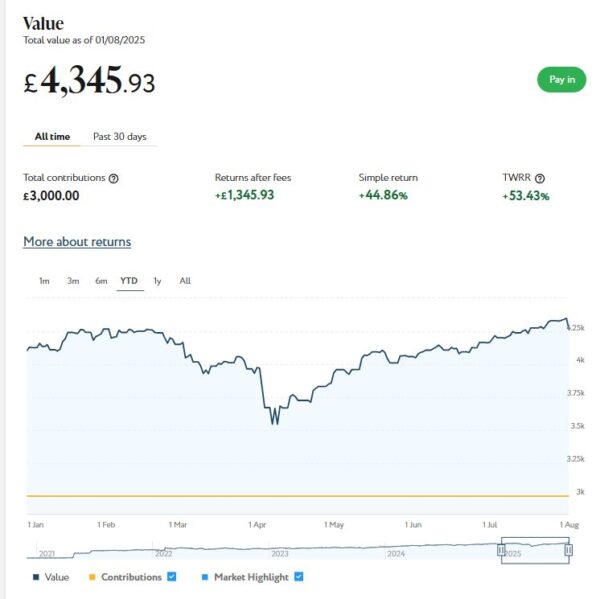

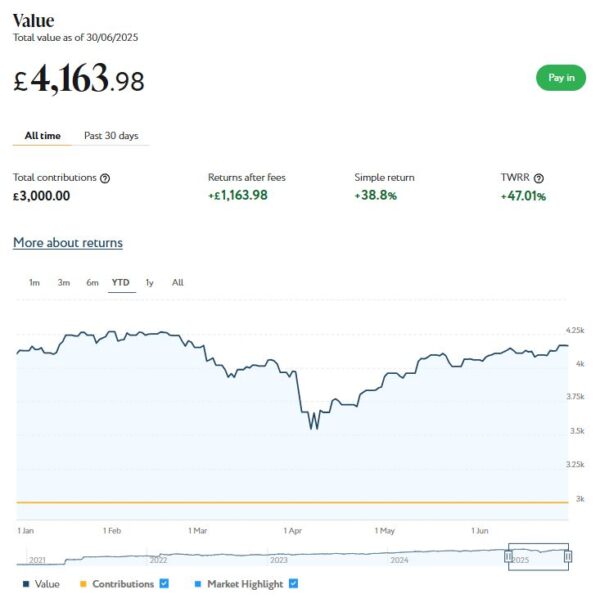

I still have a smaller, growth-oriented pot using Nutmeg’s Smart Alpha option. This is now worth £4,368 compared with £4,346 a month ago, a rise of £22. Here is a screen capture showing performance for the year to date.

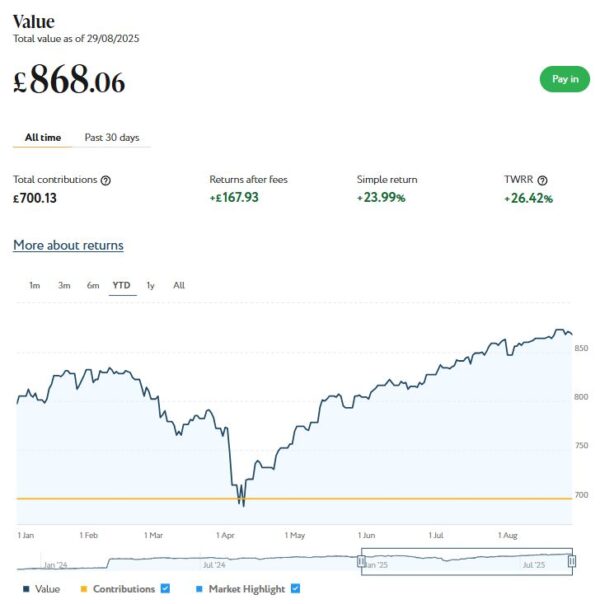

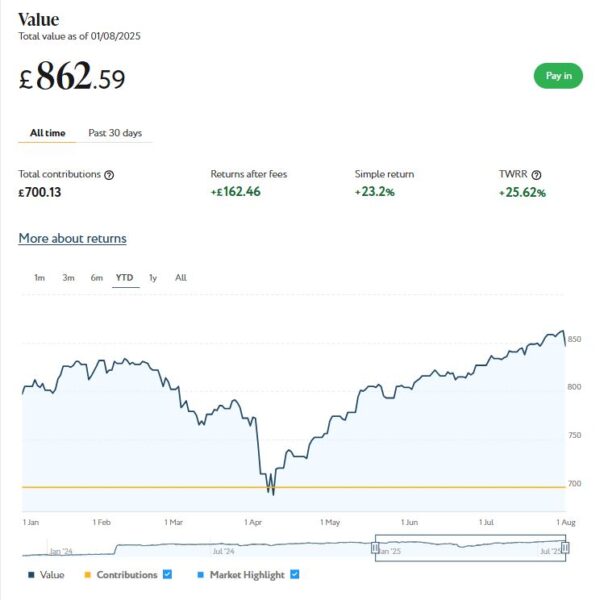

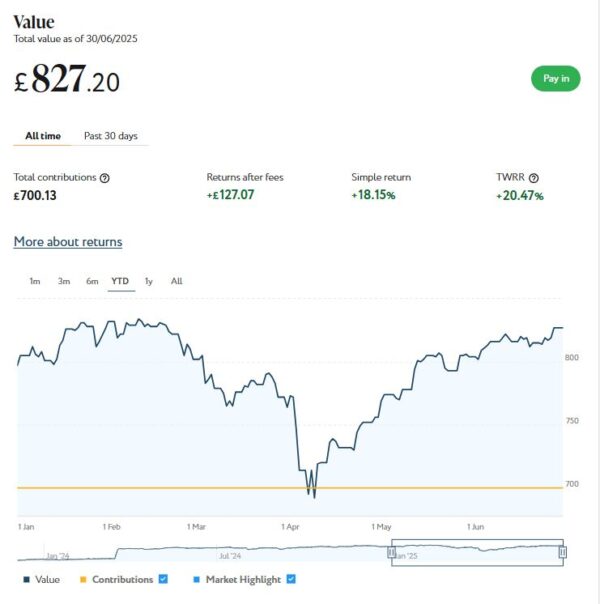

And at the start of December 2023 I invested £500 in one of Nutmeg’s thematic portfolios (Resource Transformation). In March 2024 I also invested a further £200 from referral bonuses (something I no longer receive for reasons I won’t bore you with). As you can see from the YTD screen capture below, this portfolio is now worth £868 compared with £863 last month, a rise of £5.

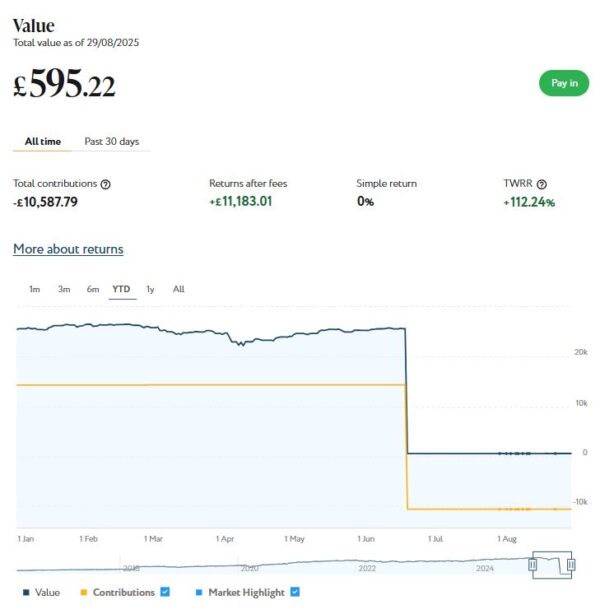

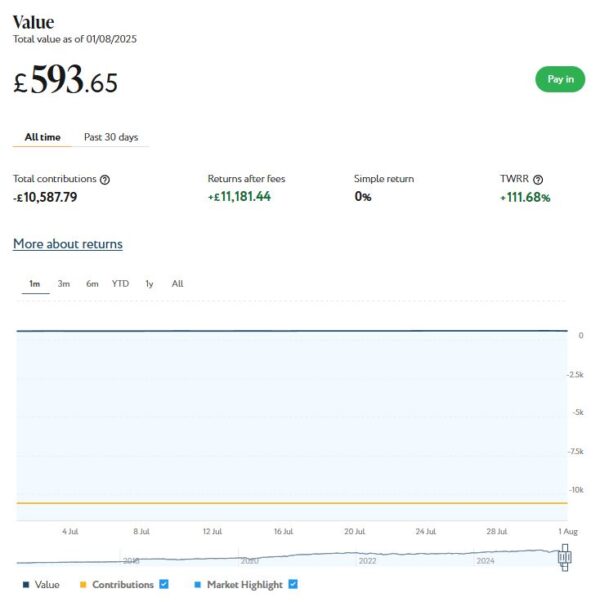

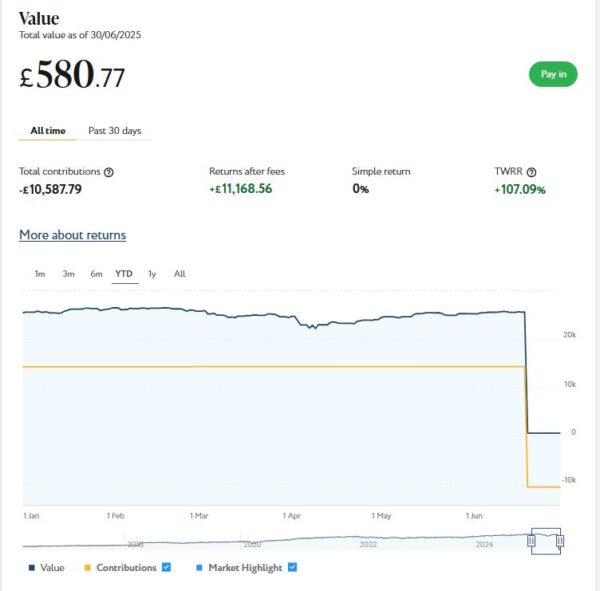

Finally, I still have a small amount left in my original Nutmeg Fully Managed portfolio. I have kept this largely for comparison purposes. This has increased in value from £594 at the start of August to £595 now, a rise of £1.

As you can see, August was a steady, if unexciting, month for my Nutmeg investments. Overall I was up by £50 or 0.16%. In addition I did, of course, receive £134.03 in income from my income portfolio.

Excluding income generated, the overall value of my Nutmeg investments is up by £1,218 since the start of 2025, so the April 2025 fall (caused largely by Trump’s tariffs) has now fully reversed. I am also up by £2,413 or 7.48% since the start of September last year, again excluding cash income received. All things considered, that’s not a bad result.

As I always have to say, some volatility is to be expected with stock market investments, but over the longer term they tend to even themselves out (and generally perform better than bank savings accounts, although that is never guaranteed). In general the worst thing you can do is panic and sell up when downturns occur (as happened in April this year). You are then crystallizing your losses rather than giving the markets time to recover. This is something I had cause to discuss in this blog post from earlier this year.

You can read my full Nutmeg review here. If you are looking for a home for your annual ISA allowance, based on my overall experience over the last nine years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs), Lifetime ISAs and Junior ISAs as well.

Moving on, I also have investments with P2P property investment platform Assetz Exchange. As discussed in this post, the company has rebranded as Housemartin.

My investments with Housemartin continue to generate steady returns. Housemartin focuses on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my HM portfolio has generated a respectable £266.87 in revenue from rental income. I have made a small net loss of £19.02 on property disposals. Capital growth generally has slowed, in line with UK property values generally.

At the time of writing, 16 of ‘my’ properties are showing gains, 3 are breaking even, and the remaining 19 are showing losses. My portfolio of 38 properties is currently showing a net decrease in value of £59.59. That means that overall (rental income minus capital value decrease and loss on disposal) I am up by £188.26. That’s still a respectable return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Housemartin most projects are socially beneficial as well.

The net fall in capital value of my Housemartin investments is obviously a little disappointing. But it’s important to remember that until/unless I choose to sell the investments in question, it is largely theoretical, based on the latest price at which shares in the property concerned have changed hands. The rental income, on the other hand, is real money (which in my case I’ve reinvested in other HM projects to further diversify my portfolio).

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of Housemartin as far as i am concerned. You can actually invest from as little as £1 per property if you really want to proceed cautiously.

As I noted in this blog post, Housemartin is particularly good if you want to compound your returns by reinvesting rental income. This effectively boosts the interest rate you are receiving. Personally, once I have accrued a minimum of £10 in rental payments, I usually reinvest this money in either a new HM project or one I have already invested in (thus increasing my holding). Over time, even if I don’t invest any more capital, this will ensure my investment with Housemartin grows at an accelerating rate and becomes more diversified as well.

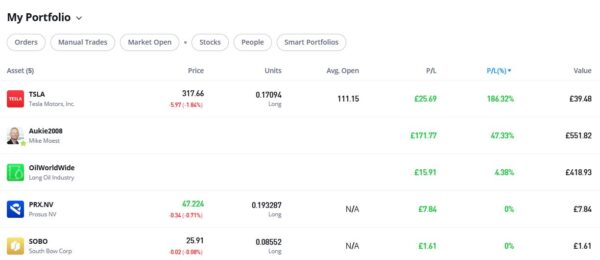

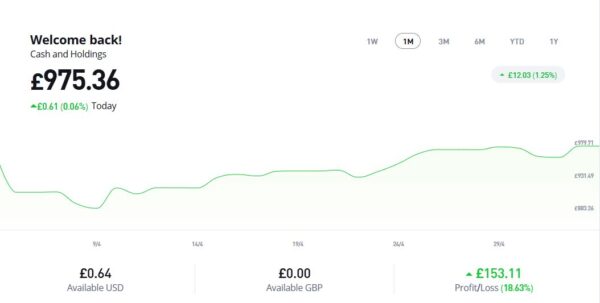

In 2022 I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios, Oil Worldwide. I also invested a small amount I had left over in Tesla shares.

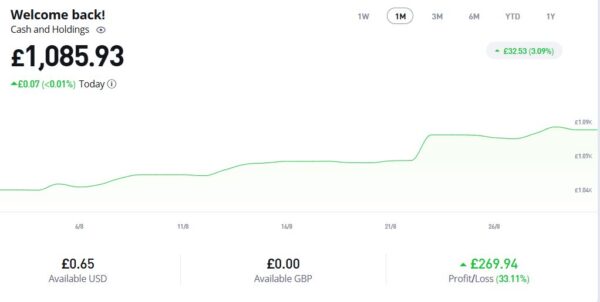

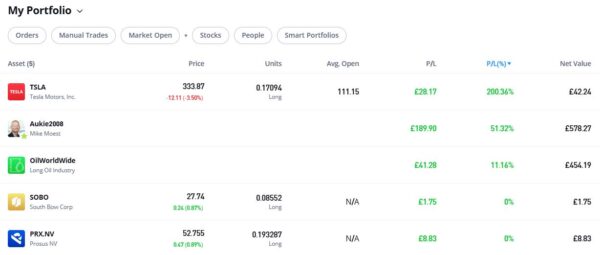

As you can see from the screen captures below, my original investment (total value £888.36 in pounds sterling) is today worth £1,085.93, an overall increase of £197.57 or 22.24%.

Note: eToro now displays the value of investments in your native currency, although you can change this if you wish.

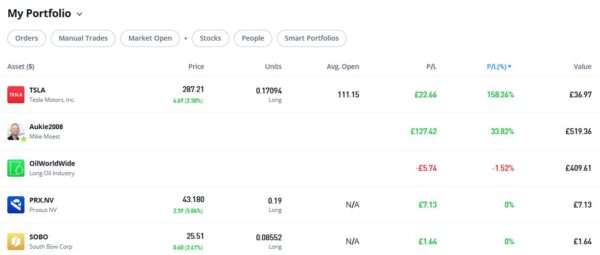

As you can see, my Oil WorldWide investment is in profit, though at 11.14% it is nothing too exciting. My copy trading investment with Aukie2008 has been doing better, with an overall 51.32% profit. To be fair, I have held this investment a bit longer.

My Tesla shares, which I bought as an afterthought with some spare cash I had in my account, are up again this month. They are showing an impressive overall profit of 200.36% since I bought them. If only I had put a bit more money into this!

You might also notice that I have small holdings in Prosus NV, a Dutch internet group, and South Bow, a Canadian energy infrastructure company. To be honest I don’t understand how I acquired these, but I assume they are some sort of bonus I was awarded. In any event, I am happy to have them in my portfolio.

eToro also offer the free eToro Money app. This allows you to deposit money to your eToro account without paying any currency conversion fees, saving you up to £5 for every £1,000 you deposit. You can also use the app to withdraw funds from your eToro account instantly to your bank account. I tried this myself and was impressed with how quickly and seamlessly it worked. You can read my blog post about eToro Money here. Note that it can also serve as a cryptocurrency wallet, allowing you to send and receive crypto from any other wallet address in the world.

If you would like more information about setting up an eToro account, please click on this no-obligation website link [affiliate]. Don’t forget that you also get a free $100,000 virtual portfolio, which you can use to experiment with trading and investing strategies. I have certainly earned a lot from mine.

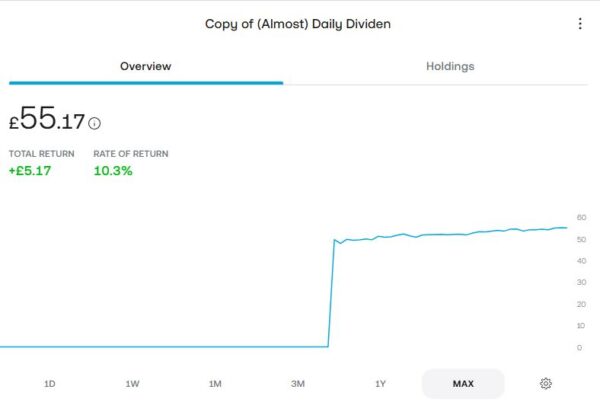

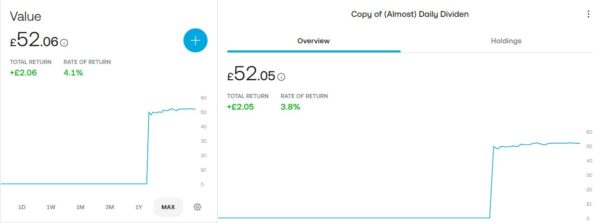

As an experiment, I recently put £50 into an investment ISA with Trading 212. As mentioned in my recent blog post about dividend investing, I put it into the (Almost) Daily Dividends Portfolio, a ready-made portfolio or ‘pie’ on Trading 212. As you can see from the screen capture below, my portfolio is now worth £55.17, an increase of £5.17 or 10.3% over the four-month period. It has even accrued a grand total of 38p in dividends!

I am quite impressed with how this investment has been faring, despite the small amount I put in (which means I may be missing out on some smaller dividends). If I increased my investment I would almost certainly become eligible for more dividends, and even more the longer I remain invested. If I had any spare money at the moment, I would consider doing this. Of course, I do now have an income-focused portfolio with Nutmeg as well (see above).

Moving on, I published various posts on Pounds and Sense in August. I have listed below those that are still relevant.

In Here’s Why I’m Not a Fan of FIRE I talked about the Financial Independence, Retire Early (FIRE) movement and explained why I am not an aficionado. I set out various reasons, including the impossibility of planning and predicting your life twenty or thirty years into the future.

In Could a Smart Thermostat Save You Money? I explained what these devices are and set out some hints and tips for making the most of them. I also discussed my own experience with a Hive smart thermostat.

In How to Check Your Tax Code and Correct it if Necessary I explained how to check this important piece of financial data. I revealed what the code means and what you should do if you believe yours is wrong. In my view everyone should check their tax code, as if it’s incorrect you may be paying too much tax or, conversely, too little. In the latter case you will still have to pay the tax when the error is discovered, potentially with added interest as well.

How Over-50s Can Save and Make Money Using Vinted discusses this very popular buying-and-selling platform among younger people. In the article I point out that Vinted can be an invaluable resource for older folk as well. I explain how it works and set out some hints and tips for making the most of it.

Finally, in Dividend Investing vs Total Return: Which Works Best for Income Investors? I look at these two popular approaches to drawing an income from your investments. Of course, this is something many retired and semi-retired people want (or need) to do. I compare the pros and cons of each method and discuss my personal experience.

I’ll close with a reminder that you can also follow Pounds and Sense on Facebook or Twitter (or X as we have to call it now). Twitter/X is my number one social media platform and I post regularly there. I share the latest news and information on financial matters, and other things that interest, amuse or concern me. So if you aren’t following my PAS account on Twitter/X, you are definitely missing out!

I am also on the BlueSky social media network under the username poundsandsense.bsky.social. Twitter/X remains my primary social media platform, but I also post details of my latest blog posts, third-party articles and other financial news and resources on BlueSky for those who prefer to follow me there.

As always, if you have any comments or questions, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts on PAS may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media:

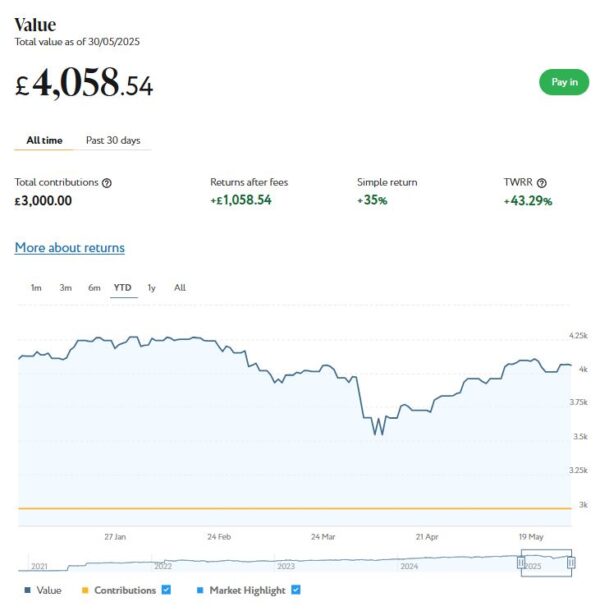

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

As regular readers will know, in June I transferred most of the money in my Nutmeg Fully Managed portfolio (just under £25,000) to a new Nutmeg Income Portfolio. I discussed this in detail in this recent post, but basically money in this port is invested to generate an income from dividends and other sources. This is then paid monthly. Capital appreciation is targeted as well, but basically these portfolios are aimed at older people (and others) who want/need their investment to generate a regular cash income.

My Income portfolio hasn’t yet generated any income for me. I assume that is because there is a qualifying period before you become eligible to receive dividends (I have asked Nutmeg for clarification about this and am awaiting an answer). Income is due to be paid in cash to my bank account on the 24th of each month, so hopefully I will have some income accrued by August 24th (check out next month’s Update to find out!).

Nutmeg have now confirmed I was basically correct above. They point out that – like all Nutmeg investments – the money in income portfolios is held in the form of ETFs (exchange traded funds). They say: ‘Usually for an ETF to pay a dividend, it is one month after it is recorded. Taking the example of the JP Morgan Global Equity Premium ETF, [a dividend] was declared and recorded in early July and will be paid in August.” It would therefore appear that you have to be invested for between one and two months to start receiving monthly payouts. Nutmeg say I can expect to receive my first income payout on August 24th, so I will await this with interest 🙂

The better news is that this portfolio has grown in value in July. It’s now worth £25,793 compared with £25,092 at the start of last month, an increase of £701 or 2.79%. As the screen capture shows, this portfolio has actually grown in value by £840.89 since I opened it.

I still have a smaller, growth-oriented pot using Nutmeg’s Smart Alpha option. This is now worth £4,346 (rounded up) compared with £4,164 a month ago, a rise of £182. Here is a screen capture showing performance for the year to date.

And at the start of December 2023 I invested £500 in one of Nutmeg’s thematic portfolios (Resource Transformation). In March 2024 I also invested a further £200 from referral bonuses. As you can see from the YTD screen capture below, this portfolio is now worth £863 (rounded up) compared with £827 last month, a rise of £36.

Finally, I still have a small amount left in my original Nutmeg Fully Managed portfolio. I have kept this largely for comparison purposes. This has increased from £581 at the start of July to £594 (rounded up) now, an increase of £13.

As you can see, July was a good month for my Nutmeg investments. Overall I was up by £932 or 2.69%.

I am up by £1,168 since the start of 2025, so the April 2025 fall (caused largely by Trump’s tariffs) has now fully reversed. I am also up by £2,583 or 8.90% since the start of August last year. All things considered, that’s not a bad result.

As I always have to say, some volatility is to be expected with stock market investments, but over the longer term they tend to even themselves out (and generally perform better than bank savings accounts, although that is never guaranteed). In general the worst thing you can do is panic and sell up when downturns occur (as happened in April). You are then crystallizing your losses rather than giving the markets time to recover. This is something I had cause to discuss recently in this blog post.

You can read my full Nutmeg review here. If you are looking for a home for your annual ISA allowance, based on my overall experience over the last eight years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs), Lifetime ISAs and Junior ISAs as well.

My investments with Housemartin continue to generate steady returns. Housemartin focuses on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my HM portfolio has generated a respectable £262.48 in revenue from rental income. I have made a small net loss of £0.71 on property disposals. Capital growth generally has slowed, in line with UK property values generally.

At the time of writing, 16 of ‘my’ properties are showing gains, 2 are breaking even, and the remaining 19 are showing losses. My portfolio of 37 properties is currently showing a net decrease in value of £60.06. That means that overall (rental income minus capital value decrease and loss on disposal) I am up by £201.71. That’s still a decent return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Housemartin most projects are socially beneficial as well.

The net fall in capital value of my Housemartin investments is obviously a little disappointing. But it’s important to remember that until/unless I choose to sell the investments in question, it is largely theoretical, based on the latest price at which shares in the property concerned have changed hands. The rental income, on the other hand, is real money (which in my case I’ve reinvested in other HM projects to further diversify my portfolio).

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of Housemartin as far as i am concerned. You can actually invest from as little as £1 per property if you really want to proceed cautiously.

As I noted in this blog post, Housemartin is particularly good if you want to compound your returns by reinvesting rental income. This effectively boosts the interest rate you are receiving. Personally, once I have accrued a minimum of £10 in rental payments, I usually reinvest this money in either a new HM project or one I have already invested in (thus increasing my holding). Over time, even if I don’t invest any more capital, this will ensure my investment with Housemartin grows at an accelerating rate and becomes more diversified as well. I did, however, withdraw £50 from my earnings in June to assist my cashflow in what was an expensive month for me

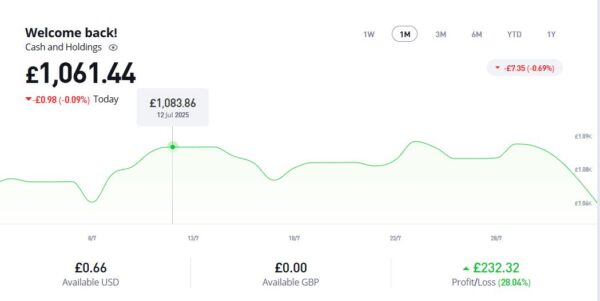

In 2022 I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios, Oil Worldwide. I also invested a small amount I had left over in Tesla shares.

As you can see from the screen captures below, my original investment (total value £888.36 in pounds sterling) is today worth £1,061.44, an overall increase of £173.08 or 19.48%.

Note: eToro now displays the value of investments in your native currency, although you can change this if you wish.

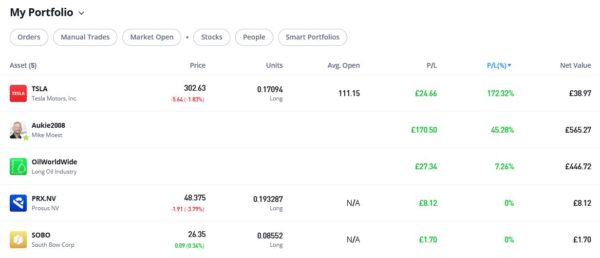

As you can see, my Oil WorldWide investment is in profit, though at 7.26% it is nothing to write home about. My copy trading investment with Aukie2008 has been doing a lot better, with an overall 45.28% profit. To be fair, I have held this investment a bit longer.

My Tesla shares, which I bought as an afterthought with some spare cash I had in my account, are down a little this month. But they are still showing an overall profit of 172.32% since I bought them. If only I had put a bit more money into this!

You might also notice that I have small holdings in Prosus NV, a Dutch internet group, and South Bow, a Canadian energy infrastructure company. To be honest I don’t understand how I acquired these, but I assume they are some sort of bonus I was awarded. In any event, I am happy to have them in my portfolio!

eToro also offer the free eToro Money app. This allows you to deposit money to your eToro account without paying any currency conversion fees, saving you up to £5 for every £1,000 you deposit. You can also use the app to withdraw funds from your eToro account instantly to your bank account. I tried this myself and was impressed with how quickly and seamlessly it worked. You can read my blog post about eToro Money here. Note that it can also serve as a cryptocurrency wallet, allowing you to send and receive crypto from any other wallet address in the world.

If you would like more information about setting up an eToro account, please click on this no-obligation website link [affiliate]. Don’t forget that you also get a free $100,000 virtual portfolio, which you can use to experiment with trading and investing strategies. I have certainly earned a lot from mine.

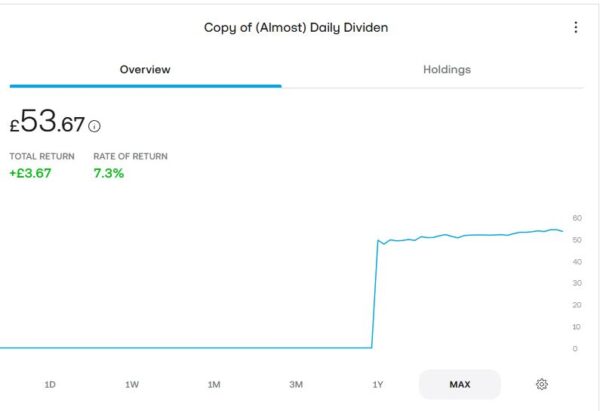

As an experiment, I recently put £50 into an investment ISA with Trading 212. As mentioned in my recent blog post about dividend investing, I put it into the (Almost) Daily Dividends Portfolio, a ready-made portfolio or ‘pie’ on Trading 212. As you can see from the screen capture below, my portfolio is now worth £53.67, an increase of £3.67 or 7.3% over the four-month period. It has even accrued a grand total of 31p in dividends (which is still more than I’ve had from my Nutmeg income port so far!).

I am quite impressed with how this investment has been faring, despite the small amount I put in (which means I may be missing out on some smaller dividends). If I increased my investment I would almost certainly become eligible for more dividends, and even more the longer I remain invested. If I had any spare money at the moment, I would consider doing this. Of course, I do now have an income-focused portfolio with Nutmeg as well (see above).

Moving on, I published various posts on Pounds and Sense in July. I have listed below those that are still relevant.

As mentioned above, in Nutmeg Launches New Income Investing Portfolios I discussed this new option from robo-adviser platform Nutmeg (with whom I am a long-term investor myself). I revealed how the new income investing portfolios work, and revealed why I decided to switch a substantial portion of my Nutmeg investments into one.

How to Tow a Caravan With an Electric Car in the UK covers a subject relevant to growing numbers of motorists. With over 1.5 million EVs now on UK roads – and staycations more popular than ever – more people are pairing their electric cars with touring caravans. But while the idea is appealing, towing with an EV requires careful planning, especially when it comes to battery range and charging stops. I am grateful to my my friends at specialist caravan insurers Compass Insurance and European EV charging infrastructure company Fastned for their expert tips and information.

In How to Invest in Gold in the UK I looked at another subject attracting growing attention. Gold is shiny, timeless, and often seen as a financial “safe haven” – especially when inflation is rising or the stock market is shaky. The growing popularity of gold among investors in recent months is testimony to this. In this post, I covered the pros and cons of investing in gold, the main ways to invest (even if you’re a beginner), and how to get started easily in the UK

Finally, in Is Private Health Insurance Worthwhile for Over-50s? I looked at the pros and cons of private medical insurance (PMI) for older people, and set out some key questions to help decide whether it makes financial sense for you. The article also discusses health cash plans, a less costly alternative that may be more suitable for some.

I’ll close with a reminder that you can also follow Pounds and Sense on Facebook or Twitter (or X as we have to call it now). Twitter/X is my number one social media platform and I post regularly there. I share the latest news and information on financial matters, and other things that interest, amuse or concern me. So if you aren’t following my PAS account on Twitter/X, you are definitely missing out!

I am also on the BlueSky social media network under the username poundsandsense.bsky.social. Twitter/X remains my primary social media platform, but I also post details of my latest blog posts, third-party articles and other financial news and resources on BlueSky for those who prefer to follow me there.

As always, if you have any comments or questions, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts on PAS may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media:

Today I am looking at the new income investing option recently introduced by UK robo-adviser platform Nutmeg. This is designed for people who want to receive a regular monthly income while keeping their money invested (and hopefully still growing).

As a long-term Nutmeg investor myself (you can read my in-depth review here), I have already taken advantage of this opportunity. I will discuss my personal experience (so far) in more detail below. But first, here’s how it works in a nut(meg)shell, how it compares with Nutmeg’s traditional growth portfolios, and who might benefit the most.

How Nutmeg’s Income Portfolios Work

Powered by J.P. Morgan Asset Management (JPMAM)

Nutmeg has collaborated with JPMAM to construct five risk‑rated portfolios, built around actively managed income-focused ETFs – including the JP Morgan Equity Premium Income strategy – so you’re investing in income-optimized assets while staying diversified.

2. Five Risk Levels to Suit You

You can choose from five different risk levels, ranging from 1 (cautious) to 5 (adventurous), based on your circumstances, goals and appetite for risk. Each level offers a different blend of equity and bond exposure to balance income generation with capital stability.

Here’s a table describing Nutmeg’s five income portfolio risk levels in simple terms…

Risk Level

Description

Equity Exposure

Income Potential

Capital Risk

1 – Cautious

Prioritizes stability over returns

Low

Low

Very Low

2 – Conservative

Aims for modest, steady income with minimal volatility

Low to Moderate

Low to Medium

Low

3 – Balanced

Balanced mix of bonds and equities for moderate income and risk

Moderate

Medium

Moderate

4 – Growth-Oriented

Greater focus on equity income for higher payouts

Moderate to High

Medium to High

Moderate to High

5 – Adventurous

Maximizes income potential with higher risk tolerance

High

High

High

📌 Note: All portfolios are actively managed and diversified, but the mix of assets changes based on your selected risk level. Income smoothing and monthly payouts are available across all five.

3. Monthly Payouts with Optional Smoothing

One standout feature is income smoothing. This spreads out income across the year, so you receive consistent monthly payments – even if dividends or yields vary from month to month. This feature is optional, however – you can turn smoothing off if you’d rather receive income as it’s earned every month.

4. No Nutmeg Management Fee for 2025

These portfolios are available via ISA or General Investment Accounts (non-ISA) and have no Nutmeg management fee for the rest of 2025, though underlying ETF costs apply. A minimum investment of £10,000 is required.

5. Capital Remains Invested

Your core investment stays fully invested in the market – providing the potential for capital preservation or growth alongside the monthly income stream.

Income vs Growth – What’s the Difference?

The difference between the two approaches is summed up in the table below.

Income Portfolio

Growth Portfolio

Objective

Provide regular monthly income

Maximize long‑term capital growth

Payouts

Paid out monthly, with optional smoothing

Reinvested automatically for compounding

Yield Focus

Uses dividend and income-focused ETFs

Focus on market growth; income secondary

Suitability

Later-stage savers, retirees, cash flow needs

Long-term goals like retirement, wealth accumulation

While Nutmeg’s growth-oriented portfolios reinvest dividends to compound, the income portfolios are specifically structured to generate ongoing monthly payments. This is ideal for those needing a regular income rather than capital appreciation (though some capital appreciation will hopefully occur as well).

Who Are These Portfolios Best For?

Retirees or near‑retirees needing a dependable income stream without selling assets.

Those reducing work hours or with varied income, using the monthly payouts to smooth out earnings.

Investors frustrated with traditional bond/dividend returns – Nutmeg’s own research shows 69% of UK investors prioritize income, yet many are unhappy with current options.

Investors seeking simplicity – You set your risk level once and Nutmeg then handles asset selection, portfolio rebalancing and (optional) income smoothing. As with all Nutmeg investments, you can change your risk level later if you wish (though some extra costs may be incurred when doing so).

Pros and Considerations

👍 Pros:

Monthly income stream without selling investments

Income smoothing for consistent payouts

Actively managed by experts at JPMAM

No Nutmeg fees until 2026

⚠️ Considerations:

Requires £10,000 minimum to start

Still carries investment risk – capital isn’t guaranteed

Fund fees apply for underlying ETFs

If you’re focused purely on capital growth, growth portfolios with reinvestment may outperform long-term

My Experience

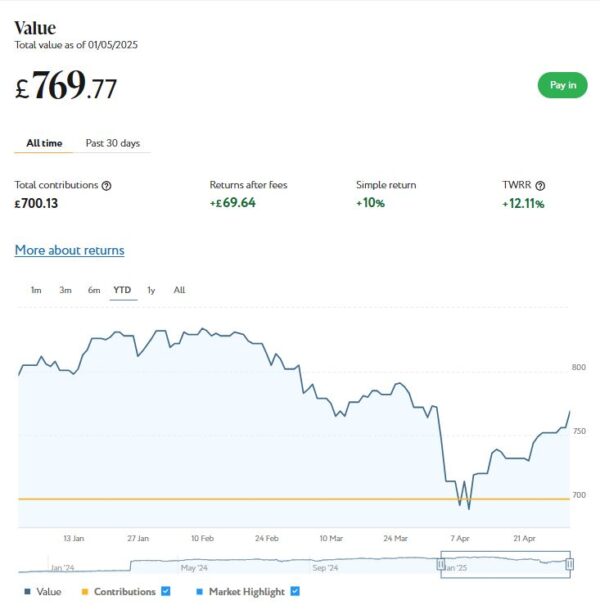

As you will know if you read my July 2025 Investments Update, in June I transferred most of the money in my Nutmeg Fully Managed portfolio (just under £25,000) to a new Nutmeg Income Portfolio. As my money was already invested via a Stocks and Shares ISA, my new income portfolio will enjoy that status as well, meaning income payments will be made without any deductions for tax. Likewise, any capital appreciation will not be taxable.

I selected a risk level of 5 (the maximum). That aligns with the risk level of my other Nutmeg investments, which should make it easier to compare them. More importantly, though, I have other investments that are lower risk, including my Bestinvest SIPP (personal pension) and – of course – my state pension. With my Nutmeg investments I hope to maximize their income and growth potential and am comfortable taking a few more risks to this end. As I have other, less risky investments, any reversals with Nutmeg shouldn’t be disastrous. Obviously as I get older – or if my circumstances change – I may revisit this.

For similar reasons, I chose not to select the ‘smoothing’ option. The income from my Nutmeg income portfolio will be in addition to other regular income streams I already have, so I can’t see any particular reason to have these payments smoothed out. Obviously I will monitor this and might change my mind in future, but for now I quite like the idea of having a variable extra payment each month. If it’s large, I may allow myself a few extra treats that month. If it’s small, I will adjust my expenditure accordingly.

Of course, the above is solely my personal perspective and should not be construed as financial advice. Everyone’s circumstances are different. You should always do your own ‘due diligence’ before investing and seek professional advice if uncertain how best to proceed. All investing carries a risk of loss.

As the screenshot below shows, my Income portfolio is already showing a profit of over £400, which is obviously welcome. It hasn’t yet generated any income, but that is unsurprising. It can take a while for investments to qualify for dividend payments, so I am keeping my expectations modest, initially at least 🙂

I will update PAS readers on how my Nutmeg income portfolio performs in my future monthly investments updates.

Closing Thoughts

In my view, Nutmeg’s new Income Investing portfolios are a valuable addition for UK investors seeking a regular income, backed by diversified, actively managed ETFs. They offer monthly, optionally smoothed payouts, managed via Nutmeg’s simple, user-friendly interface. The fact that there is no initial Nutmeg management fee through 2025 is a further attraction.

If your priorities include current cash flow, retirement‑style income, or smoothing irregular income, this could be a good fit. If you’re younger or focused on maximizing long-term growth via compounding, however, Nutmeg’s established growth portfolios (e.g. Smart Alpha) remain compelling options.

If you have any comments or questions about this post – or Nutmeg more generally – please do leave them below. As always, bear in mind that I am not a qualified financial adviser and cannot offer personalized financial advice. As with all investments, your capital is at risk and there are no guarantees of profit. If in any doubt, consider speaking with a financial services professional.

If you enjoyed this post, please link to it on your own blog or social media:

A quickie today to let you know that the annual Amazon Prime Day is almost with us. This year it extends over four days, Tuesday 8th to Friday 11th July 2025.

Prime Day is a special event for Amazon Prime members only. During it Amazon offers Prime members extra savings and special offers across a wide range of TVs, smart home products, kitchen equipment, grocery, toys, fashion, furniture, everyday essentials, and more.

Some of the best deals are typically reserved for Amazon’s own products, such as their Kindle e-book readers, Amazon Echo smart speakers and Ring video doorbells and security cameras. Discounts are often in the region of 40-50 percent for these products. If you’re thinking of buying any of them, Prime Day is definitely the day – or four days! – to do it.

I have been a member of Amazon Prime for over ten years now. As a regular Amazon shopper, I find it well worth while for the free one-day delivery on millions of items alone. But as a Prime member you get access to a lot of other benefits and services as well, including Amazon Prime Music and Amazon Prime Video.

If you’re thinking of joining Amazon Prime, therefore, I highly recommend doing it in the next day or two, so you can benefit from the Prime Day offers. Personally I think it’s worth it for the free delivery alone, let alone everything else that’s on offer. But if you wish, you can get a 30-day free trial now, take advantage of the Prime Day offers, and then cancel without owing any money. It’s your choice!

You can also see all the latest Prime Day deals by clicking here. This page also lists early deals before Prime Day itself.

As always, if you have any comments or questions about Amazon Prime or Prime Day, please do post them below.

Disclosure: This post includes affiliate links. If you click through and make a purchase, I may receive a commission for introducing you. This will not affect the price you pay or the products or services you receive.

If you enjoyed this post, please link to it on your own blog or social media:

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

A major change in June was that I transferred most of the money in my Nutmeg Fully Managed portfolio (£25,000) to the new Nutmeg Income Portfolio. I will talk more about this is in a separate post, but basically money in this portfolio is invested to generate an income from dividends and other sources. This is then paid monthly. Capital appreciation is targeted as well, but basically these portfolios are aimed at older people (and others) who want/need their investment to generate a regular cash income.

As the screenshot below shows, my Income portfolio has only just been set up, though it’s already showing a small profit. It hasn’t yet generated any income for me, but that is unsurprising. Income is due to be paid in cash to my bank account on the 24th of each month, so hopefully I may have some income accrued by then (check out next month’s Update to find out). Of course, it can take a while for an investor to qualify for dividend payments, so I am keeping my expectations modest, initially at least!

You do have the option to select a ‘smoothing’ option, where Nutmeg works out your likely monthly income from the size (and performance) of your investment and pays the same amount every month from then onward. For various reasons I have opted not to do this for now, however.

Finally, you can select a risk level from 1 to 5 for your Income Portfolio. After some thought I selected the maximum 5. Depending on how things go, I may reduce this in future.

I still have a smaller growth-oriented pot using Nutmeg’s Smart Alpha option. This is now worth £4,164 (rounded up) compared with ££4,059 a month ago, a rise of £105. Here is a screen capture showing performance for the year to date.

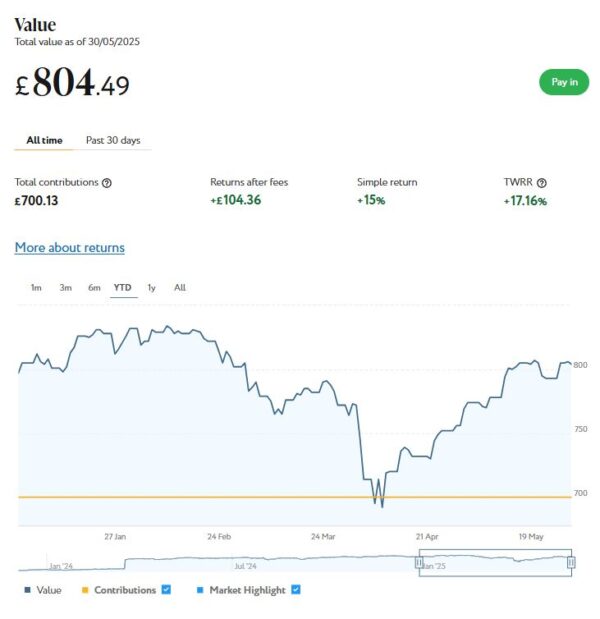

And at the start of December 2023 I invested £500 in one of Nutmeg’s thematic portfolios (Resource Transformation). In March 2024 I also invested a further £200 from referral bonuses. As you can see from the YTD screen capture below, this portfolio is now worth £827 compared with £804 last month, a rise of £23.

Finally, I still have a small amount left in my original Nutmeg Fully Managed portfolio. I have kept this largely for comparison purposes. Here’s a screen capture of how it stands now.

As you can see, June was another decent month for my Nutmeg investments. Overall I was up by £478 or 1.58%.

I am up by £236 since the start of 2025, so the April 2025 fall (caused largely by Trump’s tariffs) has now completely reversed. I am also up by £1,750 or 6.05% since the start of July last year. Considering the recent volatility of the markets (and world affairs generally) that’s not a bad result.

As I always have to say, some volatility is to be expected with stock market investments, but over the longer term they tend to even themselves out (and generally perform better than bank savings accounts, although that is never guaranteed). In general the worst thing you can do is panic and sell up when downturns occur (as happened in April). You are then crystallizing your losses rather than giving the markets time to recover. This is something I had cause to discuss recently in this blog post.

You can read my full Nutmeg review here. If you are looking for a home for your annual ISA allowance, based on my overall experience over the last eight years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs), Lifetime ISAs and Junior ISAs as well.

My investments with Housemartin continue to generate steady returns. Housemartin focuses on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my HM portfolio has generated a respectable £256.94 in revenue from rental income. I have also made a net profit of £0.57 on property disposals. Capital growth has slowed, though, in line with UK property values generally.

At the time of writing, 16 of ‘my’ properties are showing gains, 2 are breaking even, and the remaining 18 are showing losses. My portfolio of 36 properties is currently showing a net decrease in value of £53.93. That means that overall (rental income and profit on disposal minus capital value decrease) I am up by £203.58. That’s still a decent return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Housemartin most projects are socially beneficial as well.

The net fall in capital value of my Housemartin investments is obviously a little disappointing. But it’s important to remember that until/unless I choose to sell the investments in question, it is largely theoretical, based on the latest price at which shares in the property concerned have changed hands. The rental income, on the other hand, is real money (which in my case I’ve reinvested in other HM projects to further diversify my portfolio).

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of Housemartin as far as i am concerned. You can actually invest from as little as £1 per property if you really want to proceed cautiously.

As I noted in this blog post, Housemartin is particularly good if you want to compound your returns by reinvesting rental income. This effectively boosts the interest rate you are receiving. Personally, once I have accrued a minimum of £10 in rental payments, I usually reinvest this money in either a new HM project or one I have already invested in (thus increasing my holding). Over time, even if I don’t invest any more capital, this will ensure my investment with Housemartin grows at an accelerating rate and becomes more diversified as well. I did, however, withdraw £50 from my earnings in June to assist my cashflow in what was an expensive month for me 😮

In 2022 I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios, Oil Worldwide. I also invested a small amount I had left over in Tesla shares.

As you can see from the screen captures below, my original investment (total value £888.36 in pounds sterling) is today worth £1,020.09, an overall increase of £131.73 or 14.83%.

Note: eToro now displays the value of investments in your native currency, although you can change this if you wish.

As you can see, my Oil WorldWide investment is back in profit now. But my copy trading investment with Aukie2008 has been doing a lot better, with an overall 47.31% profit. To be fair, I have held this investment a little longer.

My Tesla shares, which I bought as an afterthought with some spare cash I had in my account, are down a bit this month. But they are still showing an overall profit of 186.32% since I bought them. If only I had put a bit more money into this!

You might also notice that I have small holdings in Prosus NV, a Dutch internet group, and South Bow, a Canadian energy infrastructure company. To be honest I don’t understand how I acquired these, but I assume they are some sort of bonus I was awarded. In any event, I am happy to have them in my portfolio!

eToro also offer the free eToro Money app. This allows you to deposit money to your eToro account without paying any currency conversion fees, saving you up to £5 for every £1,000 you deposit. You can also use the app to withdraw funds from your eToro account instantly to your bank account. I tried this myself and was impressed with how quickly and seamlessly it worked. You can read my blog post about eToro Money here. Note that it can also serve as a cryptocurrency wallet, allowing you to send and receive crypto from any other wallet address in the world.

If you would like more information about setting up an eToro account, please click on this no-obligation website link [affiliate]. Don’t forget that you also get a free $100,000 virtual portfolio, which you can use to experiment with trading and investing strategies. I have certainly earned a lot from mine.

As an experiment, I recently put £50 into an investment ISA with Trading 212. As mentioned in my recent blog post about dividend investing, I put it into the (Almost) Daily Dividends Portfolio, a ready-made portfolio or ‘pie’ on Trading 212. As you can see from the screen capture below, my portfolio is now worth £52.06, an increase of £2.06 or 4.12% (by my calculation) over the three-month period. It has even accrued a grand total of 18p in dividends!

I am quite impressed with how this investment has been faring, despite the small amount I put in (which means I may be missing out on some smaller dividends) and also because you need to have held shares for a certain period to qualify for dividend payments. If I increased my investment I would almost certainly become eligible for more dividends, and even more the longer I remain invested. If I had any spare money at the moment, I would consider doing this. Of course, I do now have a dividend-focused portfolio with Nutmeg as well (see above).

Moving on, I published various posts on Pounds and Sense in June. I have listed below those that are still relevant.

The Many Benefits of Learning a Musical Instrument in Later Life isn’t about personal finance. But as someone who has actually done this (ukulele) it’s a subject I feel quite passionate about. In this article I set out the many (sometimes surprising) benefits of learning to play an instrument as a senior, and offered a few tips based on my personal experience.

In What Are Bonds and How Can You Invest in Them, I explain what bonds are and their pros and cons compared with other investment vehicles. As I say in the article, bonds can play a key role in a well-rounded portfolio, especially for those – including many older people – who are seeking predictable, regular income and/or lower risk.

In How to Reduce Your Water Bills I discussed various ways you may be able to cut your water bill, including getting a water meter and (if you’re on a low income) applying for a reduced-rate social tariff. With water bills rising substantially in many parts of the country, it’s well worth checking what options you may have to cut them.

Is It Worth Getting Over 50 Life Insurance? is another sponsored post. It focuses on a type of life insurance specifically designed for people aged over 50. Such policies offer a guaranteed, fixed cash payout when the policyholder dies. Over 50 life insurance policies are generally “whole of life”, meaning they last until you pass away, as long as you keep up with premium payments. They’re often used to help cover funeral expenses, outstanding debts, or to leave a small inheritance.

Finally, How Social Tariffs Can Help You Reduce Your Household Bills looks at discounted tariffs that may be available for people on low incomes and/or certain means-tested benefits. Specifically, it covers broadband, water bills and energy bills. Do check this out if you are struggling with these bills at the moment.

I’ll close with a reminder that you can also follow Pounds and Sense on Facebook or Twitter (or X as we have to call it now). Twitter/X is my number one social media platform and I post regularly there. I share the latest news and information on financial matters, and other things that interest, amuse or concern me. So if you aren’t following my PAS account on Twitter/X, you are definitely missing out.

I am also on the BlueSky social media network under the username poundsandsense.bsky.social. Twitter/X remains my primary social media platform, but I will also post details of my latest blog posts, third-party articles and other financial news and resources on BlueSky for those who prefer to follow me there.

As always, if you have any comments or questions, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts on PAS may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media:

With the cost of living continuing to put pressure on household finances, many people in the UK are unaware they could be paying less for essential services like broadband, water and energy. If you’re on a low income or receiving certain benefits, you may be eligible for social tariffs – discounted rates offered by providers to help those most in need. Here’s what you need to know.

What Are Social Tariffs?

Social tariffs are specially discounted rates offered to people on low incomes and/or receiving certain means-tested benefits. These tariffs are often significantly cheaper than standard ones and aim to ensure everyone can afford access to essential utilities and services.

Unlike short-term promotions, social tariffs are designed to offer long-term affordability and typically come with flexible terms, e.g. no exit fees and the ability to switch back to regular plans when your circumstances change.

Social Tariffs for Broadband

Broadband internet is essential for accessing services, finding work, staying in touch, and more. Yet many people are paying standard prices when they could be saving money each month.

Who Offers Social Broadband Tariffs?

Most major UK broadband providers offer social tariffs. Some examples are shown in the table below.

Provider

Plan Name

Monthly Cost

Speed

Eligibility

BT

Home Essentials

£15

36 Mbps

Universal Credit, Pension Credit, ESA, JSA, Income Support

Virgin Media

Essential Broadband

£12.50

15 Mbps

Universal Credit

Sky

Broadband Basics

£20

36 Mbps

Universal Credit, Pension Credit

NOW

Broadband Basics

£20

36 Mbps

Universal Credit, Pension Credit

Hyperoptic

Fair Fibre Plan

£15

50 Mbps

Several means-tested benefits

Check each provider’s website for full details and availability in your area.

How to Apply

You’ll usually need to:

Be receiving a qualifying benefit (e.g. Universal Credit, Pension Credit, ESA, JSA)

Apply directly with the provider, often via a dedicated web page

Provide proof of eligibility (some providers check automatically)

Most social broadband tariffs have no setup fees, no mid-contract price rises, and shorter contract terms – typically 12 months or rolling monthly

Social Tariffs for Water Bills

As discussed in this recent blog post, water companies in England and Wales also offer discounted tariffs for customers who are struggling to afford their bills. These social water tariffs are designed to reduce charges for households on low incomes or receiving certain benefits.

What Support Is Available?

Each water company sets its own scheme, but most offer:

Reduced bills based on income and household circumstances

Debt support and payment plans

Water meters to help control usage

For example:

Water Company

Scheme Name

Support Offered

Thames Water

WaterHelp

Up to 50% off bills for low-income households

Severn Trent

Big Difference Scheme

Bills reduced by up to 90% depending on income

United Utilities

Help to Pay

Lower bills for those on Pension Credit

Yorkshire Water

WaterSupport

Tiered discount based on income and household size

Who Is Eligible?

Eligibility varies slightly by region, but in general you may qualify if:

Your household income is below a certain threshold (e.g. £21,000 per year)

You receive means-tested benefits

You have high water usage due to medical needs or a large family

How to Apply

Visit your water company’s website or contact them directly. You’ll likely need:

Proof of income or benefits

Recent water bills or meter readings

Details about your household size and needs

You can also get help from Citizens Advice or StepChange, who can assist with applications and managing arrears.

Social Tariffs for Energy

Energy prices remain high, and although the Energy Price Guarantee and price cap offer some protection, many households are still struggling.

While there is currently no mandatory social tariff for energy in the UK, some suppliers do offer extra support, and the government has been consulting on introducing a formal scheme.

Help Currently Available

Warm Home Discount: Offers £150 off your electricity bill automatically if you’re eligible. It’s not a social tariff, but it helps reduce costs.

Priority Services Register: Offers free support services (e.g. advance notice of outages, help reading meters) for vulnerable customers.

Energy Support Funds: Some suppliers (e.g. British Gas, EDF, E.ON Next, Octopus) offer hardship funds or discretionary credit for customers in financial difficulty.

Government Consultation: A formal energy social tariff could be introduced in the future, aiming to replace stop-gap measures like the Warm Home Discount.

Who Is Eligible?

Eligibility criteria vary by provider, but typically you must be receiving at least one of the following:

Universal Credit

Pension Credit (Guarantee Credit)

Income Support

Employment and Support Allowance (ESA)

Jobseeker’s Allowance (JSA)

Personal Independence Payment (PIP)

Attendance Allowance

Disability Living Allowance (DLA)

Carer’s Allowance

Even if you’re not sure, it’s worth checking — some providers may consider broader circumstances.

Tips to Save Even More

Use a benefits calculator (e.g. Turn2us or Entitledto) to check what you’re entitled to.

Switch providers: Even without a social tariff, switching could save you money.

Check for grants or local schemes via your council or Citizens Advice.

Final Thoughts

If you’re struggling with your broadband or energy bills, don’t suffer in silence. Social tariffs can offer substantial monthly savings and provide peace of mind during difficult times. They’re designed to be easy to apply for and are often available even if you’re already a customer.

Check with your provider or visit Ofcom’s website to find out more – and make sure you’re not paying more than you need to.

Have you benefited from a social tariff? Share your experience in the comments to help others who might be eligible too.

If you enjoyed this post, please link to it on your own blog or social media:

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

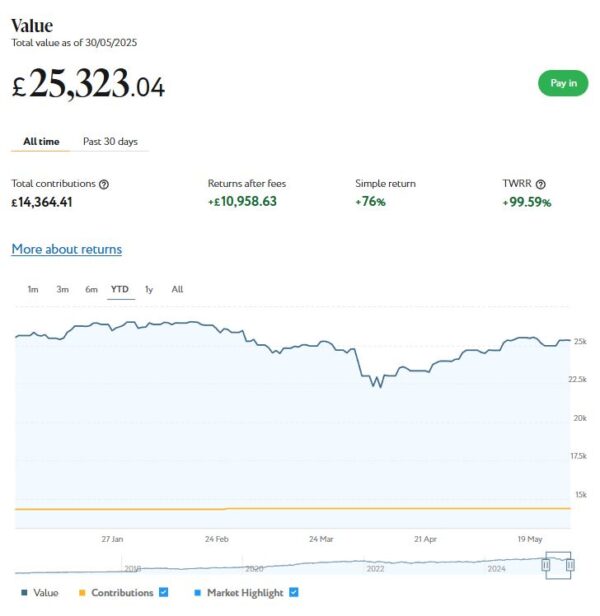

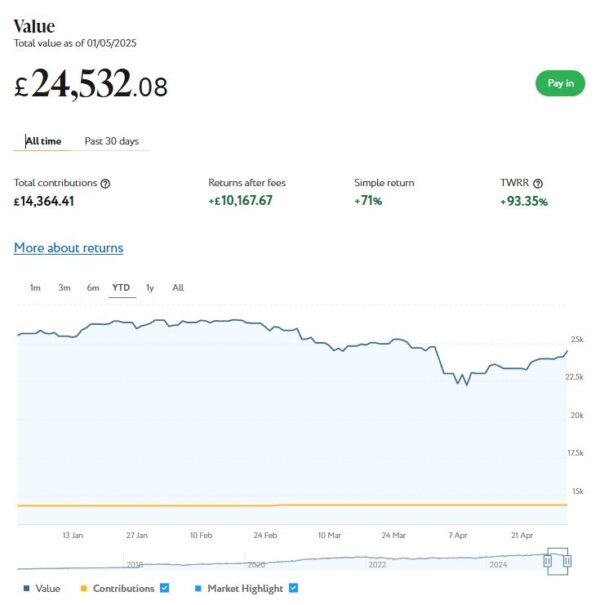

As the screenshot below for the year to date shows, my main Nutmeg portfolio is currently valued at £25,323. Last month it stood at £24,532, so that is a rise of £791.

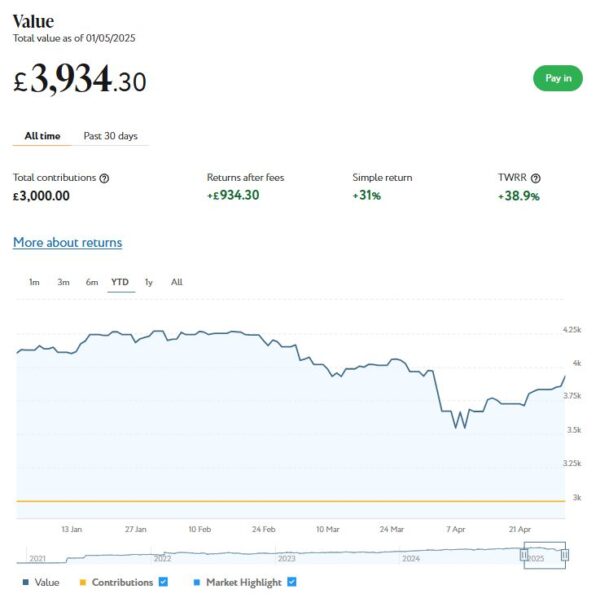

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £4,059 (rounded up) compared with £3,934 a month ago, a rise of £125. Here is a screen capture showing performance for the year to date.

Finally, at the start of December 2023 I invested £500 in one of Nutmeg’s new thematic portfolios (Resource Transformation). In March 2024 I also invested a further £200 from referral bonuses. As you can see from the YTD screen capture below, this portfolio is now worth £804 compared with £770 last month, a rise of £34.

As you can see, May was a good month for my Nutmeg investments. Overall I was up by £950 or 3.25%.

I am still down slightly since the start of 2025, with the value of my investments decreasing by £242 or 0.08% since 1st January. On the other hand, their value has grown by £1,813 or 6.39% since the end of May last year. So, as I always say, the recent ups and downs do need to be taken in context. Some volatility is always to be expected with stock market investments, and over time they tend to even out. In general the worst thing you can do is panic and sell up when downturns occur (as happened in early April). You are then crystallizing your losses rather than giving the markets time to recover. This is something I had cause to discuss recently in this blog post.

You can read my full Nutmeg review here. If you are looking for a home for your annual ISA allowance, based on my overall experience over the last eight years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs), Lifetime ISAs and Junior ISAs as well.

Moving on, I also have investments with P2P property investment platform Assetz Exchange. As discussed in this recent post, the company recently rebranded as Housemartin.

My investments with Housemartin continue to generate steady returns. Housemartin focuses on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my HM portfolio has generated a respectable £251.16 in revenue from rental income. I have also made a net profit of £0.57 on property disposals. Capital growth has slowed, though, in line with UK property values generally.

At the time of writing, 16 of ‘my’ properties are showing gains, 3 are breaking even, and the remaining 18 are showing losses. My portfolio of 37 properties is currently showing a net decrease in value of £47.34. That means that overall (rental income and profit on disposal minus capital value decrease) I am up by £204.39. That’s still a decent return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Housemartin most projects are socially beneficial as well.

The net fall in capital value of my Housemartin investments is obviously a little disappointing. But it’s important to remember that until/unless I choose to sell the investments in question, it is largely theoretical, based on the latest price at which shares in the property concerned have changed hands. The rental income, on the other hand, is real money (which in my case I’ve reinvested in other HM projects to further diversify my portfolio).

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of Housemartin as far as i am concerned. You can actually invest from as little as £1 per property if you really want to proceed cautiously.

As I noted in this blog post, Housemartin is particularly good if you want to compound your returns by reinvesting rental income. This effectively boosts the interest rate you are receiving. Personally, once I have accrued a minimum of £10 in rental payments, I reinvest this money in either a new HM project or one I have already invested in (thus increasing my holding). Over time, even if I don’t invest any more capital, this will ensure my investment with Housemartin grows at an accelerating rate and becomes more diversified as well.

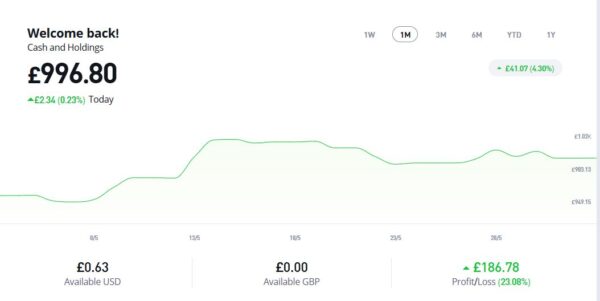

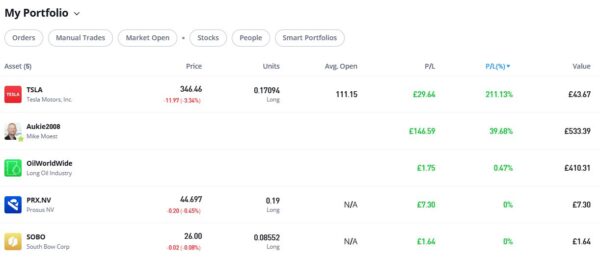

In 2022 I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios, Oil Worldwide. I also invested a small amount I had left over in Tesla shares.

As you can see from the screen captures below, my original investment (total value £888.36 in pounds sterling) is today worth £996.80, an overall increase of £108.44 or 12.21%.

Note: eToro now displays the value of investments in your native currency, although you can change this if you wish.

As you can see, my Oil WorldWide investment has recovered a bit since last time and is at least back in profit now, although it’s not exactly setting the world on fire (excuse the bad joke).

Thankfully my copy trading investment with Aukie2008 has been doing better, with an overall 39.64% profit. To be fair, I have held this investment a little longer.

My Tesla shares, which I bought as an afterthought with a bit of spare cash I had in my account, have done particularly well since I bought them, with an overall profit of 211.13%. If only I had put a bit more money into this! As a matter of interest, I do find it quite strange that my Tesla shares keep going up in value, despite all the stories in the press and social media about consumers boycotting Tesla. Go figure.

You might also notice that I have small holdings in Prosus NV, a Dutch internet group, and South Bow, a Canadian energy infrastructure company. To be honest I don’t understand how I acquired these, but I assume they are some sort of bonus I was awarded. In any event, I am happy to have them in my portfolio!

eToro also offer the free eToro Money app. This allows you to deposit money to your eToro account without paying any currency conversion fees, saving you up to £5 for every £1,000 you deposit. You can also use the app to withdraw funds from your eToro account instantly to your bank account. I tried this myself and was impressed with how quickly and seamlessly it worked. You can read my blog post about eToro Money here. Note that it can also serve as a cryptocurrency wallet, allowing you to send and receive crypto from any other wallet address in the world.

If you would like more information about setting up an eToro account, please click on this no-obligation website link [affiliate]. Don’t forget that you also get a free $100,000 virtual portfolio, which you can use to experiment with trading and investing strategies. I have certainly earned a lot from mine.

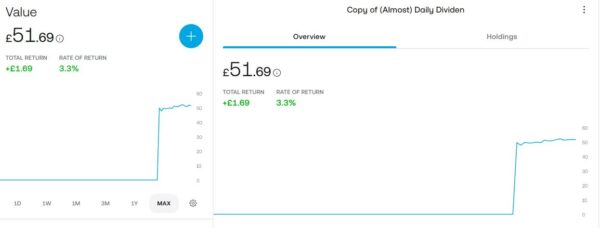

As a bit of an experiment, I recently put £50 into an investment ISA with Trading 212. As mentioned in my recent blog post about dividend investing, I put it into the (Almost) Daily Dividends Portfolio, a ready-made portfolio or ‘pie’ on Trading 212. As you can see from the screen capture below, my portfolio is now worth £51.69, an increase of 3.3% over the two-month period. It has even accrued a grand total of 9p in dividends!

I am quite impressed with how this investment has been faring, despite the small amount I put in (which means I may be missing out on some smaller dividends) and also because you need to have held shares for a certain period to qualify for dividend payments. If I increased my investment I would almost certainly become eligible for more dividends, and would qualify for more the longer I remain invested. If I had any spare money at the moment, I would certainly consider doing this!

Moving on, I published various posts on Pounds and Sense in May. I have listed below those that are still relevant

Why a Financial Remedy Order is Essential on Your Divorce is another guest post from my friends at HCR Law. If you are unfortunate enough to be in this position, this article contains important advice and information on how to ensure your personal financial security going forward.

Where to Get Pension Advice contains important information for anyone who may be coming up to retirement age, which of course includes many Pounds and Sense readers. This collaborative article includes details of six potential sources of pension advice, including the pros and cons of each.

Could You Benefit From Help to Save spotlights a lesser-known government scheme which, if you’re eligible, can give your finances a valuable boost. It’s an initiative aimed at helping people on low incomes (typically those receiving Universal Credit) build up their savings. Offering generous tax-free bonuses, this scheme can provide significant benefits for qualifying individuals.

How to Save Money on Rail Fares With Split Ticketing discusses a money-saving hack that savvy travellers can use to reduce their rail-fare costs – often by a substantial margin. Split ticketing involves breaking a journey into two or more smaller segments, purchasing separate tickets for each segment rather than one through-ticket. With the help of apps such as those discussed in the article, the process becomes simple and automated.

Finally, in What Are ETFs And How Can You Invest in Them? I shine a spotlight on these increasingly popular investment vehicles, explaining what they are, how you can invest in them, and how you can maximize the benefit by investing via tax-free ISAs.

I’ll close with a reminder that you can also follow Pounds and Sense on Facebook or Twitter (or X as we have to call it now). Twitter/X is my number one social media platform and I post regularly there. I share the latest news and information on financial matters, and other things that interest, amuse or concern me. So if you aren’t following my PAS account on Twitter/X, you are definitely missing out.

I am also on the BlueSky social media network under the username poundsandsense.bsky.social. Twitter/X remains my primary social media platform, but I will also post details of my latest blog posts, third-party articles and other financial news and resources on BlueSky for those who prefer to follow me there.

As always, if you have any comments or questions, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts on PAS may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media:

Today I’m sharing a guest article on a subject nobody likes to think about, but one that could be crucial to ensuring your financial security in later life..

Sadly, growing numbers of older people are seeing their marriages break down and having to undergo the painful process of divorce. Even if relatively amicable, this is likely to be stressful and emotionally exhausting. And – even worse – any mistakes you make now can have serious consequences for your finances, both now and into the future.

My guest today, Victoria Fellows, a partner and head of family at the Birmingham office of HCR Law, knows this very well. And she has some important advice for anyone who may find themselves in this situation.

Over to Victoria then…

Divorce rates among individuals aged 50 and over – often referred to as ‘silver splitters’ – have been on the rise in the UK over recent decades, with the number of over-60s legally separating doubling since the 1990’s. This trend contrasts with the decline in divorce rates across younger age groups. It can be put down to various factors, such as longer life expectancy, empty nest syndrome and the increasing numbers of financially independent women who are able to support themselves outside marriage.

At the end of 2024, the Law Commission published a scoping report on financial remedies on divorce. This indicated that 60% of the couples who divorced in 2023 had not properly dealt with their finances upon divorce, sometimes thinking it was not worth obtaining an order from the court as they believed they had no assets justifying the expense of formally separating their finances.

So while these couples are now divorced, both parties remain vulnerable to a financial claim application from their former spouse at any point until they remarry or die. The case of Vince v Wyatt illustrated why this was a mistake. The parties had nothing when they divorced and did not bother to get a clean break order. Post separation, Mr Vince became a multi-millionaire through his own business activities. Mrs Wyatt was allowed to bring financial claims against him 20 years after the divorce, resulting in a significant financial award being made in her favour.

Resolving financial issues during a divorce is therefore crucial for both immediate stability and long-term security. This is especially true for silver splitters undergoing ‘grey divorce’ – another term referring to divorces in later life. Unlike their younger counterparts, they will not have years of working life ahead of them to build up savings or pensions. It is therefore crucial that the marital assets are divided fairly to help ensure that both spouses have financial security during their retirement. There is also the possibility that in their fifties or sixties, one spouse will come into a substantial inheritance post-divorce which, without a financial remedy order, the former spouse could make a claim on in the future.

So What Do Financial Agreements Look Like?

As a result of being married, both parties have a number of financial claims that they can make against each other. The orders that a court can make are as follows:

Orders for maintenance pending suit (‘interim’ spousal maintenance)

Periodical payments orders (spousal maintenance for joint lives, specific term and/or a nominal amount)

Lump sum orders

Property adjustment orders

Pension sharing orders

In deciding whether to make any of the above orders, the court must consider all the circumstances. These will include:

a) The income, earning capacity, property and other financial resources of each party or what they are likely to have in the foreseeable future, including any increase in that earning capacity.

b) The financial needs, obligations and responsibilities which each of the parties to the marriage has or is likely to have in the foreseeable future.

c) The standard of living enjoyed by the parties before the breakdown of the marriage.

d) The age of each party to the marriage and duration of the marriage.

e) Any physical or mental disability of either party to the marriage.

f) The contributions which either of the parties have made or are likely to make in the foreseeable future to the welfare of the family, including any contribution by looking after the home or caring for the family.

In every case the court also has to consider whether a ‘clean break’ is appropriate. A clean break is where the parties’ finances are arranged to allow them to separate without any further financial responsibility for each other. While the court must give consideration to this, it does not mean that there can or should be a clean break in every case. This will necessarily depend upon the other factors involved.

How Are Agreements Reached?

There are a number of ways in which financial matters can be resolved:

Discussions directly between the parties if they are able to discuss and agree a financial settlement that both of them are comfortable with.

Mediation where both parties try to reach agreement between themselves with the assistance of a trained mediator.

Negotiation through solicitors. Each party can appoint a solicitor to negotiate on their behalf. This approach is suitable for complex financial situations or when mediation isn’t appropriate.

Other forms of dispute resolution. Arbitration and collaborative law are further alternatives. Arbitration is effectively a ‘private’ process that largely mirrors court proceedings but where the parties have more control in particular in respect of timescales. Collaborative law is a separate process which may only be suitable in certain circumstances. Each person appoints their own collaboratively trained lawyer and both parties and their lawyers meet together to work things out face to face.

Financial remedy proceedings. If all other options fail, it may be necessary for formal court proceedings to be issued to resolve financial matters. An application for financial remedy can only be commenced after a Divorce Petition has been filed with the court. The proceedings usually involve attending court on three occasions. If financial settlement is not agreed at either of the initial two hearings, or in between them, then a final hearing will be listed at which the Judge after hearing evidence makes a decision that is binding on the parties. This would be the most cost-prohibitive option and can end with resolution of financial matters being taken entirely out of the parties’ hands.

Top Tips to Make the Process Easier

Seek professional advice as soon as possible. Consult with financial advisors and solicitors who are experienced in later-life divorce and can help navigate complex financial issues and ensure a fair settlement is not only reached but also incorporated into an order to be approved by the court.

Enter into full financial disclosure to ensure that all assets are disclosed and taken into consideration when looking at overall settlements that plan for short- and long-term financial security. This will take time, so start sorting out your paperwork early. This is likely to include bank statements, pension records and documents relating to any other investments you might have, e.g. premium bonds, stocks and shares, rental income, and so on.

Remember to consider wills and estate planning as divorce does not automatically revoke a will. It’s crucial to update wills to reflect new circumstances and ensure assets are distributed according to current wishes.

Divorcing later in life presents unique challenges, but with careful planning and professional guidance, it is possible to navigate the process and achieve a fair and secure financial settlement.

Victoria Fellows (pictured, below) is a partner and the head of the family team of the Birmingham office of HCR Law.

Many thanks to Victoria and her colleagues at HCR Law for an eye-opening article on this important topic. If you are unfortunate enough to find yourself in this situation, devoting some attention to financial planning now can potentially save you and your family a lot of grief in the future.

As always, if you have any comments or queries about this article, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

As the screenshot below for the year to date shows, my main Nutmeg portfolio is currently valued at £24,532. Last month it stood at £25,065, so that is a fall of £533.

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £3,934 compared with £4,027 a month ago, a fall of £93. Here is a screen capture showing performance for the year to date.

Finally, at the start of December 2023 I invested £500 in one of Nutmeg’s new thematic portfolios (Resource Transformation). In March I also invested a further £200 from referral bonuses. As you can see from the YTD screen capture below, this portfolio is now worth £770 compared with £783 last month, a fall of £13.