Being a pet parent can be an enriching experience or an abject disaster, depending on how prepared you are. Whether you are looking to bring a fluffy, four-legged friend into your home or you’re looking for something more exotic, there are several things you should keep in mind when bringing any animal into your family.

Consider All the Costs Involved in Pet Keeping

When we consider adopting a pet, the cost may not be your first consideration, but it should be. Aside from the adoption fees and the cost to feed your new friend each month, there are several other costs you will need to consider when you’re budgeting for a new pet. According to some sources, the estimated cost to keep a pet dog in the UK is around 1,875 GBP a year, which excludes any adoption fees or travel costs associated with bringing your new companion home.

Unexpected veterinary bills can also involve hefty costs if you’re not prepared. To keep these unexpected costs to a minimum, consider taking out pet insurance from Petgevity for your new family member.

Prepare for a Long-Term Companion

While our furry, scaly, or feathered companions may not have the same lifespan as us, with some exceptions, it is essential that you research how long your pet’s average lifespan is in captivity before you adopt. Many people don’t consider that some fish can reach the ripe old age of 15 years old or that some reptiles have been known to exceed the 60-year mark. This is a huge time commitment and not one that should be taken lightly.

Pet-Friendly Properties and Pet Proofing

Thanks to the popularity of pet ownership, with an average of 62% of UK households owning at least one pet, many residential properties allow pet ownership in some form. However, while the average landlord may not have an issue with a small dog or cat, you should always check to see if they have any restrictions before starting any adoption process. This is particularly important if you plan to adopt a large dog breed or an exotic pet like a lizard or snake.

Even smaller animals that require some outdoor exercise time, like rabbits and guinea pigs, may not be welcome in all complexes. Once you’ve checked that your pet is welcome, ensure that your property is ready for them too. If you live in an area with open gardens, you may need to make a plan to install a fence or barrier to keep your pet within your property.

Get Your Whole Household On Board

While you may be super excited to adopt a new family member, pets tend to take over households. Whether it’s a cute kitten looking to make mischief under the sofa or a ball python that enjoys the occasional frolic around the living room, animals should be allowed some freedom to play outside of your bedroom. So, make sure your whole household approves of the new addition before you bring them home. Also, keep in mind that you may need to rely on the people in your house to take care of your animal when you are away, so making sure they are comfortable with your critters should be a top consideration.

Whether you are looking to add a cute fluffy hamster or a large scaly tortoise to your family circle, doing your research is key to a long and happy future together. And remember to always keep the animal’s needs and care requirements in mind before making any adoption decisions.

This is a collaborative post.

If you enjoyed this post, please link to it on your own blog or social media:

Investing can be confusing, and it’s easy to lose track of where your money is going. Thankfully, Microsoft Excel has many tools that can help you effortlessly track your investments.

Excel offers many ways for users to easily track their investments, such as by tracking the value of their portfolio over time, analyzing past performance, and comparing how different asset classes performed in similar market conditions.

Excel can also help investors stay on top of balances and transaction activity across multiple accounts. It allows them to visualize how these transactions affect their total wealth over time. This information can help investors decide when to invest more or pull out some cash for other uses.

Excel can be beneficial for investment tracking, especially if you’re saving for retirement and want to see how much progress you’ve made over time.

You can either enrol in Excel training to learn a few tips or tricks to analyze your investment data (which will serve you well for life), or you can follow the guide below for a quick solution.

Create a Portfolio

A portfolio is a collection of individual investments held by an investor. A typical portfolio will include stocks, bonds, mutual funds, exchange-traded funds (ETFs), options, and other securities.

If you’re looking to create a portfolio in Excel, here’s how to do it:

1. Open up the spreadsheet application on your computer,

2. Click on ‘File’ and select ‘New’.

3. Select ‘Blank Workbook’ from the new screen’s drop-down menu. This will open up a new file for you to start creating your portfolio in Excel.

4. Type the heading ‘Accounts’ in one of the columns. The accounts should be listed from largest to smallest by value or assets under management (AUM). We recommend listing these accounts as rows instead of columns to make it easy to track.

5. Create columns for the type of investment you have in your portfolio against each account. These include cash accounts, bonds, fixed-income funds, stocks and equity funds, commodities, and other assets like real estate or intellectual property rights.

6. Now create another column with the heading ‘Shares/Investment’ and enter the data for each investment appropriately.

7. You can add columns related to Date, Security Name, Number of Shares or Units Owned, Purchase Price Per Share/Unit (or Cost Basis), and Current Market Value Per Share/Unit (or Current Value). In addition, add columns for Cost Basis (the original purchase price), Gain/Loss Per Unit, and Total Gain/Loss For All Units (for each security).

8. You may also want to include columns for Percent Gain/Loss.

9. Save the spreadsheet as an Excel file and then close it.

Use the ‘Difference Formulas’ in Excel

Excel’s most useful feature is its ability to calculate differences between two numbers. For example, if you have a list of investment values and you want to know how much money you have made since your purchase, you can try the following method:

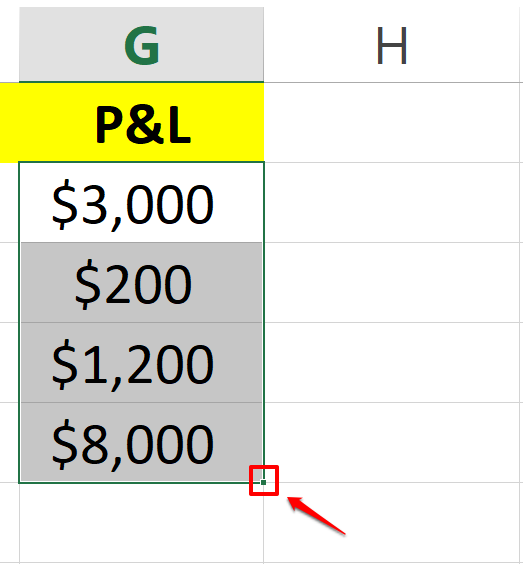

1. Click the cell where you want to calculate the difference between your asset’s current price minus its original purchase value.

2. Type the equal sign ‘=’ and then select the cell containing the current value of your investment.

3. Type the minus sign ‘-‘ and then select the cell containing the original purchase price of the investment.

4. Press enter, and the difference will be calculated.

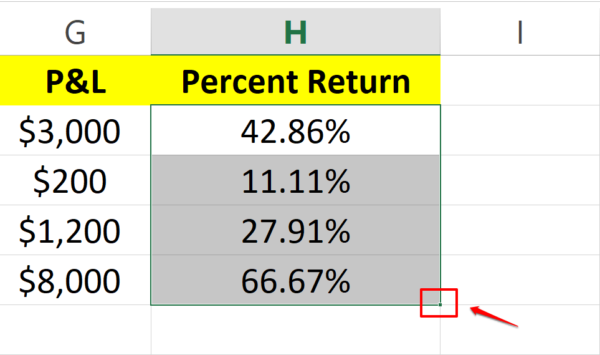

5. Now click and press the small square at the end of that cell (containing the difference), and drag it downwards to calculate the difference of each dataset automatically.

Use the ‘Percent Return Formulas’ in Excel

To track the return on investment over time, you can use Microsoft Excel’s percent return formulas. These formulas calculate the percentage increase or decrease in an investment’s value over time.

The formula for percent return is: (Current price – Purchase price) ÷ Purchase price

Here’s how you can apply the percent return formula in Excel:

1. Select the cell where you want the percent return formula to be calculated.

2. Type the equal sign ‘=’ and add an open parenthesis ‘(‘.

3. Select the cell containing the current value of your investment.

4. Type the minus sign ‘-‘ and select the cell containing the original purchase price of your investment and then close the parenthesis ‘)’.

5. Now, type the forward slash ‘/’ and select the cell containing the original purchase price.

6. Press enter, and the percent return will be calculated.

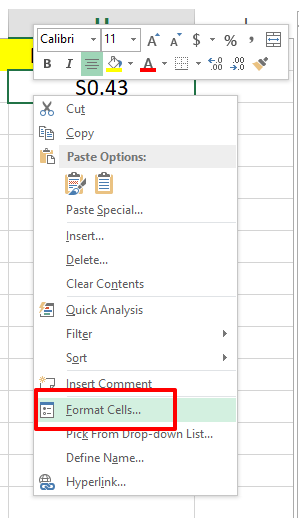

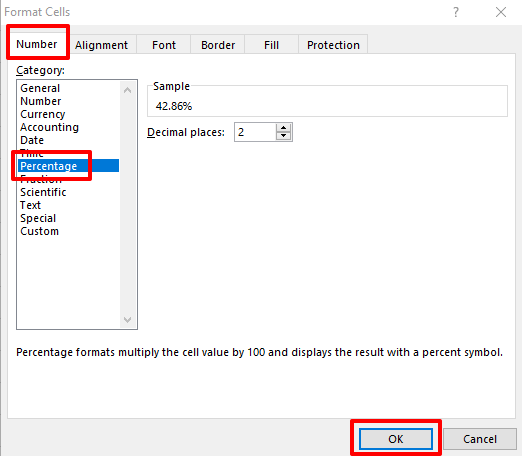

7. To make values appear as percentages, right-click on the cell, select the option of Format Cells, and select Percentage under the number tab.

8. Once done, click and drag the small square at the bottom right corner of your percent return cell and copy the formula for the rest of the dataset.

Use Advanced Excel Features to Customize your Sheet

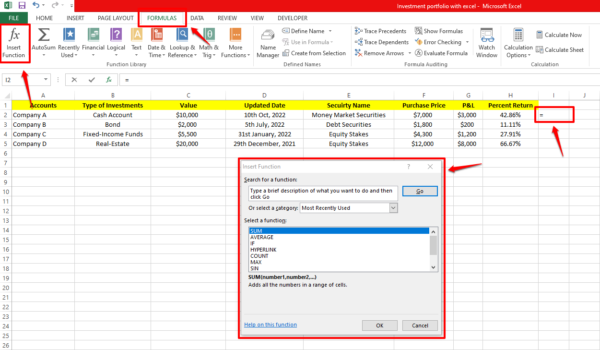

Functions in Excel are a way for you to manipulate data in Excel programmatically. They can be used to perform calculations, transform data, and create new values.

You can find a list of all built-in functions in the Formula tab menu in Excel. To access it, click on any cell, navigate to the Formula tab and choose the ‘Insert Function’ option. The Insert Function dialogue box will appear, from where you can choose the function you are looking for by going through the list.

Here are the 10 most popular functions in Excel:

SUM function

IF function

LOOKUP function

VLOOKUP function

MATCH function

CHOOSE function

DATE function

DAYS function

INDEX function

FIND, FINDB functions

The best way to learn about each function is by using it. Try out different arguments and see what happens.

To Conclude

Excel is an excellent way to track investments because it saves and calculates dependable data. Also, you can use the program to graph your data and see how they change over time.

Thank you to my friends at Acuity Training for an informative guest article.

I use Excel spreadsheets for keeping track of my self-employed earnings and send them to my accountant once a year so that he can produce my annual accounts from them.

I do also use Excel for keeping track of my investments, but only in a very basic way. This article has inspired me to be a bit more ambitious with Excel and use formulas to automatically calculate the total and percentage returns from my investments, and so forth.

As always, if you have any comments or questions about this post, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

Today I have a guest post for you from my fellow money blogger Bilquis, whose blog you can read at http://getmoneysaving.com.

In the article below, Bilquis sets out ten work-from-home jobs that can be done without large amounts of training or experience. Whether you’re looking for part-time or full-time work, there may be something suitable for you here.

Over to Bilquis then…

The pandemic has changed how we do many things. A big one is how we work. A lot of companies now prefer the work-from-home (WFH) method. This saves money for the business as they don’t have to pay as much for office space. For employees it means they don’t have to spend time and money commuting and can stay in the comfort of their own home and work there.

While working from home can have drawbacks as well as benefits, it can’t be denied there are lots of opportunities. In this post I will set out ten jobs you may be able to do on a WFH basis.

Sales

If you’re good at selling, this is perfect for you. With improved technology and cloud-based software, having a home-based sales job is a realistic possibility for many. You can sell anything from carpets to pet food. And the great thing about sales jobs is that most pay commission for every sale you make.

There are plenty of businesses looking for salespeople. Check out job boards like Indeed and search for “work from home sales” – plenty of jobs will come up! If you want to brush up your sales skills then I suggest going on YouTube and watching videos from experts like Zig Ziglar.

Customer Service

As with sales, customer service is now in many cases fully remote. Many companies are looking for home-based customer service reps to help with enquiries from customers. These jobs are generally very flexible, so if you can only manage a certain number of hours a week, employers will often be happy work around that.

Again, the best place to find customer service roles is job boards like Indeed.

Admin

If you are well organized and good at creating reports and spreadsheets then you might like working as an administrator. This might include other duties as and when required. Look on job sites like Indeed or WeWorkRemotely.

Social Media Management

Do you like using social media platforms like Instagram and Facebook? Businesses are willing to pay good money for people who can help them grow their business through social media. After all, millions of people use social media and the numbers are increasing every day. Many businesses are clueless when it comes to social media and don’t know how to make the most of it.

That’s where you come in. As a social media manager you will manage and grow their social media by adding interesting content and responding to queries from clients and potential clients. If you don’t know anything about growing social media accounts, you can always learn. Go to Udemy and take one of the many courses available there.

As a social media manager you can either take the freelance route applying for opportunities on Upwork and Fiverr, or you can start your own business. You could also get a job with a company, working in their marketing department.

To start your own business as a social media manager it might help to offer to work free for the first few clients, to gain reviews and social proof.

Audio Transcription

Audio transcription involves preparing a written version of spoken content such as a video or podcast. Podcasts are a very popular way to consume information but some people prefer to read a transcript or at least have it available for reference.

So if you have good typing speed and enjoy listening to podcasts this job could be for you. There are plenty of companies in this field like Happy Scribe, Rev.com and Accuro. Some of these companies do require you to be a native English speaker. According to Happy Scribe, their top earners are making $3,000 (£2,400) a month.

Voiceover Artist

If you have a good voice and enjoy speaking, doing voiceovers can be a great stay-at-home job. The work may involve creating voiceovers for videos and courses. You may also work on audiobooks and other projects.

A good website to get started is Mandy. Others include Voices.com, Voquent and Backstage. Companies or individuals post jobs on these sites and you can apply for them by submitting a short audition.

Top earners can earn over $50,000 (£40,000) per year

Teacher

High speed internet and software like Zoom and Skype has made it easy and convenient to teach online from home. If you are knowledgeable about a particular subject, you can set your own hours and work as many or few as you want. There is also a big demand for native English speakers who can teach the language and/or help learners practise their conversational skills.

All you need is a laptop, internet connection and a working webcam/microphone. Some websites you can try are Preply, Cambly and SkimaTalk. Some of these do require you to have qualifications and/or experience.

If you are looking to boost your income you can create online courses. Using platforms like Skillshare or Udemy you’re able to create online courses that people can sign up to and you can profit from each sign up.

Paralegal

As a paralegal you will be helping solicitors and barristers by preparing legal documents, researching, providing quotes to clients, going to court and performing admin work, all based from home.

Most paralegal jobs will not require you to have a law degree, but some do require you to have some legal training or experience.

You can find WFH paralegal jobs on Indeed, TotalJobs or even social networking site Linkedin.

Virtual Assistant

This WFH job involves helping businesses with any task they may have such as data entry, admin, email, research, simple bookkeeping, and so on. The job can be varied and interesting. You can find jobs for virtual assistants on Upwork, Freelancer, and so on.

Web Developer

Businesses need an online presence and can’t afford not to be online. If a business isn’t online and doesn’t have a website, their competition most likely will. As a home-based web developer, you can use your programming skills to build websites for business clients. You can also enjoy a continuing income maintaining and updating the site for them.

Conclusion

With high-speed internet connections and ever-improving technology, working from home is now commonplace. For many of these jobs you do not need any special experience or qualifications. And because you will be working from home, you – and your clients – can be based anywhere in the world.

If you want to work from home, opportunities have never been better, whether you want to work for an employer or become self-employed and seek out clients yourself.

Good luck, and enjoy your new WFH career!

Thank you again to Bilquis for an eye-opening article. Please do check out his blog at http://getmoneysaving.com.

As Bilquis says, there has never been a better time to seek work from home. And as someone who has done this himself for over 30 years, I do highly recommend it! But it must be said that it can have certain drawbacks as well. You might enjoy reading my blog post The Pros and Cons of Working From Home in which I discuss this in much more detail.

As always, if you have any comments or questions about this post, for me or for Bilquis, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

Today I have a guest post for you from my colleague Richard Winstone (not pictured above). Richard has just launched a new, diary-style blog called Financially Fat about his quest to achieve ‘financial fitness’.

I thought Financially Fat could be of interest to many Pounds and Sense readers, so I invited Richard to create a guest post about it. He was happy to oblige, so here is his article.

Hi everyone. I’m Richard Winstone and I write a blog called Financially Fat.

I want to start this post by thanking Nick for allowing me to guest blog on Pounds and Sense. I appreciate the feedback he has given on my blog and am really proud to have this opportunity to showcase Financially Fat to the Pounds and Sense community.

What is Financially Fat?

“If financial fitness is the aim, then I am Financially Fat.” This is the tag-line of the Financially Fat blog.

Being financially fat isn’t supposed to paint the image of a fat, wealthy man. It’s meant to imply that my finances are out of shape, which they are.

I’ve decided to take a no-holds-barred approach to financial honesty in my blog: the good, the bad and the ugly. So, in the second post I wrote down my complete financial position. I left nothing to the imagination and fully revealed my “financial nakedness”. I did this because I wanted my readers to know that I’m not another rich guy giving quick tips to save a few quid (not that there’s anything wrong with that), but that I’m actually financially struggling and that I’m taking action to improve my financial fitness.

Financially Fit is written as a diary, in which every Friday I comment on how I did with the previous week’s targets and set new targets for the following week. There are also a couple of sections of me rambling about my thoughts from the previous week, which I hope are insightful but may just be the ramblings of a mad man 😉

The purpose of the blog is two-fold. First, I want to chronicle my journey from being financially fat to being financially fit. I think this is easier to do weekly while I’m on the journey rather than try to remember what I did after (I hope) I’ve become financially fit. And second, I’m hoping to provide a step-by-step guide for others to follow to help improve their financial fitness. I write and post my blog to the over50smoney.com website and email it out to our over50smoney community each week.

So, below is a quick summary of how my blogging journey has gone so far, now that I’m five weeks in…

This is another introductory post, but it goes into much more detail. I start by detailing what I hope to gain from Financially Fat and then move on to set out my starting financial position, including my salary, savings, debts, shares, assets and anything else I could think of. It’s a complete works of my financial position, which I’ve committed to reviewing monthly in a similar format so I can see how my financial position improves month-to-month (the next review is this Friday and I’m nervous!).

Right, Week 2 is when it starts getting more interesting and where the format of the blog really starts to become clear. I started this post by highlighting three things I did that were bad for my finances over the previous week, which were:

Moving home (kind of unavoidable)

Working from Costa far too often

Dining out

I then came up with the idea of setting targets for the following week to address things that I’ve done wrong in the previous week, with the hope that I’ll eventually move away from bad habits that cost me way too much money. This seems to be working to be honest, at the moment I’m down to working from Costa only once or twice a week and usually only for a couple of hours each time rather than full days.

Continuing the development of the blog format, Week 3 is where I started titling the blog posts a little more nicely, and where I started summing up my financial savings from following the targets on my previous week.

In this post, I point out how working from Costa only once a week instead of five times a week can save me around £50 per week, over £200 per month! I also discuss setting yourself targets as you follow the blog. Reading it is (I hope) interesting, but for the blog to be useful you need to follow the thought processes I go through and make sure you’re applying them to your own life. So, if you have a small, seemingly inexpensive habit that you do frequently, then I recommend reviewing how much that habit has actually cost you over a month and see how much you could save by cutting down.

In Week 4 I discussed the target of reviewing my standing orders and direct debits. After just one review, which took about 45 minutes, I was able to save just under £600 per year! Which is insane. I continued to review into the following week but was only able to save an additional £1 per month by changing my gym membership.

This is also the week I formalised my “Ramblings” as an introduction to the blog, I hope you enjoy reading them and please feel free to email me any time to comment, ask questions or provide suggestions (I’ve been getting some great tips from readers!).

By this point, I’ve started getting really into the money-saving game. I’m also discussing things like increasing income to ensure I’m not reliant only on my salary.

But, as the title indicates, I talk about tackling my biggest challenge yet, which is currently destroying my finances – smoking! I know, it’s a horrible habit and I’m obviously very aware of the negative health affects as well as the impact it’s having on my bank balance. So, I’ve set out a five-week plan to quit (which I can say I’m currently doing okay on, but it has only been four days).

Cutting out smoking could save me around £2,400 per year, which means from the Financially Fat blog I would have saved around £3,200 a year in disposable income just in the first five weeks, and there’s still so much more work to do!

Follow the Financially Fat Blog

That’s it for the summary of my first six blog posts. I hope you will click through and give them a read as there’s a lot more information in there and some interesting views, I like to think.

If you’re interested in following my blog, please head over to over50smoney.com and sign-up for our newsletters. Or, if you’d rather not receive emails, you could just follow us on Facebook. I write and post every Friday and put links on our Facebook page, so please consider liking and following this. Thank you 🙂

I want to thank Nick again for letting me write this short summary of Financially Fat. I really hope you find it as useful as I am. If you have any questions or comments, or just fancy a chat about finances, please feel free to reach out to me directly at richard@over50smoney.com. I sometimes take a few days to reply, but I promise I get back to every email I receive.

I’m Richard Winstone and I am Financially Fat.

Many thanks to Richard Winstone (pictured, right) for this article. I hope you will take a moment to check out Financially Fat.

I particularly admire the honesty with which Richard sets out his financial position. I try to be honest about my finances on PAS as well, but not in nearly as systematic a way as he is doing!

If you are also ‘financially fat’ (as Richard defines it) I hope you may find the info and advice on the new blog inspires you in your own quest to achieve financial fitness.

As always, if you have any comments or questions about this post (for me or for Richard), please do share them below.

If you enjoyed this post, please link to it on your own blog or social media:

Today I have a (sponsored) guest post for you from my friends at Just Free Stuff.

They reveal some great ways you can get your hands on free and discounted baby products. Even though I know many PAS readers are beyond the age of having babies, many will have children (or grandchildren) who are now parents themselves. We all know having children is costly, so any help with saving money is always appreciated!

Over to Just Free Stuff then…

Looking for freebies is a growing trend in the UK and it’s easy to understand why.

Young mothers especially need help finding where and how to get the best baby free samples or other baby free stuff such as coupons, information, and so on. So, having been there ourselves, we decided to create this mini-guide, hoping you will enjoy it.

What Do We Mean by Free Baby Stuff?

Free baby stuff may include promo offers (e.g. get one and receive the second for free), money-off coupons, free samples or even information on where to go and buy baby products cheaply. The Internet is full of websites and blogs on this subject and it can become quite confusing. So we wrote this to give you a place to start.

Our Top Three Baby Freebie Sites

There are all sorts of freebie offers out there, some better than others, so we thought we should provide a short list of sites that include only the best. We will keep this updated when new offers arise, but right now you can check out our top three below.

Offer Oasis – This well-established website offers free samples and discount coupons. It also provides lots of valuable information on subjects related to the early months or years of a baby’s life, most-used products, etc. It also gives a helping hand through its online community of parents who discuss and advise or simply share their experiences, from which you can gain much free knowledge. Cherry on top: membership of this site is totally FREE.

Amazon Family – Amazon Prime members get access to this programme that offers a range of benefits to parents of babies and young children. They offer up to 20% discounts on most common baby products such as nappies and baby food, as well as up to 15% discounts on repeat deliveries. You do have to join Amazon Prime to get access to Amazon Family, but this brings many benefits in itself, including free, next-day delivery of many items.

Just Free Stuff – What could be the third option but our very own website? We post offers we find available in our BabyFree Samples category. You might want to come back and check out the newest additions to the list as they always appear on the top.

Why Do Companies Give Away Free Baby Stuff?

Free samples or promo offers for current or new products are a popular marketing strategy. Companies keep using them as they are known to be very effective. Why? Businesses need to create a loyal customer base. For this, they need customers to keep buying their products and not switch to competitors. So offering some products in special promos is a reward to customers for their loyalty and (hopefully) keeps them engaged with and enthusiastic about the company.

Also, new products are being developed every day and companies need customers to try them. So why not give away small quantities for free? A customer might think twice before spending money to try out a new product, as they may feel safer with products they have always used. But trying for free is something almost anyone would do. That is why there are always so many free samples and promo offers out there, and why there always will be. So do keep going back to check out the latest ones.

Many thanks to Free Stuff UK for sharing their tips and advice today. If you have any comments or questions – or other tips for saving money on baby products – please do share them below as usual.

Disclosure: this is a sponsored post for which I am receiving a fee.

If you enjoyed this post, please link to it on your own blog or social media:

Today I am pleased to bring you a guest post by Paul Green from Over50smoney. Paul is the founder and CEO of this popular website, which acts as a consumer champion for the over-50s.

Paul also has his own blog on Over50smoney, in which he mixes financial tips and guides with some personal pieces on subjects including sourdough bread making and growing his own fruit and vegetables!

In the article below (shared from his blog) Paul sets out some great tips for saving money that may particularly appeal to older people (though relevant to younger ones as well).

Over to Paul then…

My career has been spent helping people and businesses save money. With a business it makes sense to run operations efficiently as this enables investment to grow the business in the future. For individuals, saving money on everyday purchases is just the same. It enables you to save for the future. You can then spend the money you save however you like. This could be on holidays and enjoying life or maybe longer-term savings for your retirement. The choice is yours.

In this blog post I wanted to share five easy ways of saving money on everyday things that have worked for me. If you have other great tips that people over 50 could benefit from, please do share then below.

Don’t Take Out an Expensive Mobile Phone Contract

The smart phone has become a big part of most peoples lives. And this isn’t only the case for younger people. At Over50smoney about 80 percent of our website users visit the site with their mobile phones. However, those of us who wait in eager anticipation of upgrade time on our phone contracts are probably wasting hundreds of pounds. This used to include me until I realised how much money I was throwing away needlessly.

Let’s start by looking at why the standard type of pay monthly phone deal doesn’t make sense. The table below compares the latest Apple top of the range phone on a 24 month contact on the Vodaphone network against buying the phone upfront and getting the same data and minutes deal from Vodaphone on a SIM only deal. Taking out a phone contract is essentially the same as buying your mobile phone on Hire Purchase (HP). You have to pay for this. In the example below you are out of pocket to the tune of £250 over the course of a two-year deal.

You could also make buying your own phone and SIM even cheaper. If you shop around, you could get a significantly cheaper SIM deal depending on your needs. Keeping the same amount of data but giving up 5G capability can save money, but do you really use all your data anyway?

Comparison of a 24-month phone contract to buying your own phone

Phone contract

Get separately

Savings

Apple IPhone 12 Pro Max

£75 per month for 24 months = £1,800

Phone £1,099

Data £20 per month for 24 months = £480

Upfront payment

£29

£0

Total cost over 24 months

£1,829

£1,579

£250

*Data from Carphone Warehouse, Vodaphone and Apple, correct as at 31 May 2021

There are also cheaper SIM providers than the main networks so it’s worth considering providers like ID Mobile that uses the 3 network. The point is, if you buy your phone, you have more flexibility on the SIM deal you use.

Not everyone has a thousand pounds to buy a new top of the range phone outright. And in my opinion, this wouldn’t be the best option if you wanted to maximise savings on your smart phone anyway. Have a think about these ways of getting a good phone for less.

If you have a phone coming to the end of a contract why not keep it for another year? The build quality in modern phones is high, so unless you already have a problem with the phone, it’s likely to last for an additional year or two. It’s been a while since there were any real breakthroughs in phone design, so the extra benefits of upgrading are likely to be limited to things like a slightly more sophisticated camera. A friend of mine recently decided to keep his Samsung when he came to the end of his 24-month contract. He had been paying £65 per month during the contract term with O2. He wanted to stay with O2 so based on his usage he decided to move to an O2 SIM only deal and now pays £20 per month. As he stayed with the same provider, he didn’t even need to get a new SIM card. He now enjoys the same phone he really likes for £45 per month less than he was paying during the contract term.

If you want a new phone, it’s definitely worth looking at buying second hand. You can do this online or in many of the high street phone retailers. A quick Google search will show you several companies that specialise in selling high quality second-hand phones including WeSellTek [sponsored]. These will be wiped clean of previous owners’ data, refurbished and sanitized. You can get models that are currently being sold new for hundreds of pounds less. However, the biggest savings are usually on models that are just out of date. Given the pace at which the main manufacturers release new phones this probably means the phones are only a couple of years old and will have all the features and capabilities you want.

I’m not going to cover the pros and cons of moving to pay-as-you-go deals here. If you use your phone infrequently or usually have access to Wi-Fi this is something you could consider as additional cost savings are possible.

Double Savings With Amazon

Being someone who likes to shop local where I can, buying grocery items from Amazon initially went against the grain. However, financially it can make really good sense.

I first noticed this with a couple of items. We love coffee and a few years ago invested in a great, beans to cup, machine. This means we use a lot of coffee beans at home. Likewise, my wife makes amazing risotto. This is a staple on our menu once a week. Which means we also use a lot of arborio rice. Of course, we can pick up coffee beans and arborio rice from the supermarket, but they come in fairly small packets and we go through these pretty quickly. I discovered both coffee beans and arborio rice were available in big 1 kg sized packs from Amazon and that the price per KG is less buying these bigger packets than the smaller ones we used to get in store.

However, on top of the saving for buying bigger packets, if you use something regularly Amazon can give you additional savings. If you buy using Subscribe & Save you can control how often Amazon sends you a product. And, if you used less than normal it’s easy to delay an order so your cupboards don’t get too full. For most grocery items Subscribe and Save seems to offer a 10% price reduction initially that can increase to 15% with repeat orders over time. For some products the saving is lower, with a 5% initial reduction increasing to 10% over time.

So, I am now converted to getting some of my groceries from Amazon. The value is really good with both cheaper prices for bigger quantities and a Subscribe and Save discount on top of that. I also like the additional benefit of the products being delivered which means you don’t have to remember to put them on your shopping list and then carry them home!

Big Savings With Groupon

As the over-50s community is now well and truly online, I wanted to look at another couple of routes to savings when buying online. First up, Groupon.

Groupon has been around since 2008 and is based on the American love of coupons. The site works in the same way as cutting coupons out of a newspaper. You select an offer from the site, and read the small print so you understand things like the time period the offer is available for and how to claim it. Traditionally you had to print a voucher from Groupon, though nowadays that isn’t generally the case.

Groupon is easy to sign up for. You need an email address. It’s the most useful if you download the app to your phone or tablet as you can use the settings to get offer alerts close by when you are out. Groupon guarantees sellers a minimum number of customers. This means that they can create offers for the platform to drive sales when they need them. Groupon claim the typical discount on an offer on their site is the range of a 30-40% discount, although I have seen discounts stated as high as 90% and as low as 5%. Groupon earn a commission every time a customer takes an offer.

Groupon organises offers into different categories, making it easier to find what you want. The offers are updated all the time so if you can’t find what you want its worth coming back again. Different people I know use Groupon in different ways. For example, I have a friend who before the pandemic only bought toilet roll in bulk from Groupon (today, I have seen an offer of 120 rolls of Cusheen quilted luxury aloe vera toilet tissues for £17.50!). I’ve not typically used the site for “basics” but have found offers for services near where I live to be really useful. Again, before the pandemic when my wife and I went out with friends regularly, Groupon was a good source of mid-week deals on food in local pubs and restaurants.

So you understand why I like local deals on Groupon, these three are a selection from the recommendations near me as I write this post:

40% off a two-course meal for four people in a local fish restaurant. The price includes a glass of wine each and is reduced from £84 to £50. The offer is for Tuesdays, Wednesdays and Thursdays only, unless you book at least four weeks in advance when it also applies to Fridays;

60% off a spa day at a local hotel Mondays to Fridays or 56% off for Saturdays and Sundays. The offer for two people includes use of the spa facilities and hotel pool, Rasul mud treatment and lunch served with a glass of Prosecco. Mondays to Fridays the price is reduced from £201.90 to £79 or Saturdays and Sundays from £205.90 to £89. As it’s my wife’s birthday in couple of weeks this is an offer I may consider as it’s the type of experience she enjoys at a resort I know she likes;

The most interesting offer for me today is from a local chiropractor. Having hurt my back about a month ago lifting heavy pots in the garden I have put up with ongoing back ache. However, I will now book a visit for a chiropractic consultation and exam, which includes a report of findings and a treatment session. I haven’t been to this practice before, but it is offering a whopping 84% discount with the price reduced from £81 to £12.95. I wouldn’t have booked this at the full price but am happy to pay just under £13 to see if I can sort my ongoing backache out!

I think the two most important tips for using Groupon are to read the small print of the offers, especially availability in terms of dates or locations. Also, you do need to include the cost of postage when assessing an offer for goods. While the postage amount is specified on the site, for low value goods this can outweigh the savings from the offer.

Cashback Sites Offer Great Deals

I’ve written about cashback sites before and there is a range of content on the Over50smoney website about them. For example, they are mentioned on the short video here Revolutionise your finances – Part 2 (over50smoney.com).

You need to join a cashback site and because of the way they work this takes a little longer than signing up to Groupon. The two best cashback sites in the UK are TopCashback and Quidco. Both are well established, reputable businesses and free to join. Once you have signed up you can search the cashback offers available. If you select an offer, you will receive your goods or services and the appropriate cashback amount will be credited to your account. This can take a few weeks. Once the money is in your cashback account you will be able to transfer it into your bank account so long as you stay within the conditions of the site you are using. Transfers are usually straightforward. According to TopCashback members earn an average of £345 cashback a year. Retailers pay cashback sites a bonus based on volumes of sales. Cashback sites also earn revenue from sponsored adverts and promotions on their sites.

Cashback offers typically range from a few pounds for everyday products to hundreds of pounds for expensive items or ongoing services like energy or broadband deals. The important thing to remember with cashback sites is that while the offers can represent really good value for money you need to make sure you don’t get swayed just by the cashback amount. High cashback amounts can seem compelling but may be associated with high-cost products. You should be aware that many businesses use cashback sites to drive volumes when their prices may not be competitive. Always take a look online and see if the product or service you are thinking about is cheaper elsewhere when you include the cashback discount. If you have done your research and are confident that the cashback offer you have seen is a good overall deal, representing best value for money, it makes sense to purchase this way.

Both TopCashback and Quidco have a wide range of offers split into different categories including clothing, electricals, insurance, travel and so on. There are many offers in each category, so normally there will be a fair amount of choice if you want to make a purchase.

At the time of writing the following deals were available on TopCashback:

£210 off iPhone contracts with Tesco Mobile

£200 off energy with Scottish Power

Up to 8% discount on purchases from Marks & Spencer (different reductions depending on products purchased)

Up to 7% discount on purchases from ao.com (different reductions depending on products purchased)

3% discount on Lego

If you would buy online directly from a retailer it always makes sense to see if there is a discount available from a cashback site. For example, why send flowers from Marks & Spencer directly when you can save 8% buy buying through TopCashback?

Always Use the 30-Day Rule

As someone who used to be a spontaneous shopper, buying things I liked when I was out, the 30-Day Rule has been a godsend for me.

The 30-Day Rule goes like this:

If there is something you would like to buy, think about it for 30 days. If after that time you still want it, go and get it.

Putting this discipline in place stops you buying things you don’t really need or want. The ultimate waste of money is buying things you never use!

I think all of us have bought things on the spur of the moment because they seemed like a good idea, but ultimately, we didn’t really use them. Recently, I was talking to friends who were moving house. Their weakness was kitchen gadgets! They had cupboards full of things they were planning to give away before they moved. They had bought soup-makers, salad spinners, air fryers, rice cookers, etc, etc, that had seemed like a good idea but were ultimately only impulse buys. Bought, used once, and then forgotten about!

For me the 30-Day Rule has stopped this. Waiting 30 days gives me time to reflect on whether I really want something. I no longer waste money on things that I don’t use or enjoy.

Paul Green, 1 June 2021

Many thanks to Paul for an eye-opening guest post. I shall definitely be checking out Groupon more often in future! Do check out his blog on Over50smoney and the Over50smoney website itself.

I do strongly agree with Paul about the savings to be made through buying your mobile and SIM card separately. And there are some amazing deals out there right now. Personally I pay EE just £6 a month for a SIM-only deal with unlimited texts, unlimited voice calls and 5 GB a month of data. Okay, 5 GB might not be enough if you are out and about all day, but personally I’m nearly always within wifi range and don’t need that amount of data or anything like it.

Older people might also want to look into getting a big button mobile phone. These can be great for those whose eyesight isn’t what it once was and/or those with arthritis or similar who struggle to use the small buttons on modern mobiles. Click here for more information on big button mobile phones.

I am old enough to remember the days when mobile phone calls were so expensive you only made them when you really had to and kept calls as short as possible. How times have changed!

Release the Equity from Your Property

While 50 won’t cut it, the great news for homeowners over 55 is that you can use your property value while still retaining full ownership. So, if you’re not planning to move out any time soon and dream of retirement at home, then opting for a lifetime mortgage will provide you with up to 65% of your property value in tax-free cash.

You can receive your home equity as a lump sum, put it in a drawdown facility to release as you wish, or opt for a monthly salary lasting up to 25 years. What’s best is that the money can be used in any way you desire, and no repayments are necessary during your life.

Be warned that equity release can impact one’s access to means-tested benefits. Luckily, homeowners are required by Equity Release Council regulations to use a financial adviser to help with sound decision making throughout the process.

Today I am pleased to bring you a guest post from Haydn Martin, a UK blogger whose website is called Perpetual Prudence.

Haydn explores ideas relating to retail investing and other personal finance topics on his way to finding the solution to Lifetime Investing…

In his guest post today he discusses the risks of investing in ‘safe’ assets.

Over to Haydn, then…

Risk might be the most important consideration when making investment decisions (like what to invest your ISA allowance in). Get it wrong and you could be retiring on a pittance, running out of money during retirement, or even worse – asking friends/family for handouts. Risk must be taken seriously and properly dealt with, especially when you’re living off your investment portfolio.

It seems strange, then, that risk is so poorly understood by so many.

One aspect of risk that is particularly neglected is the chance of a truly disastrous event crushing the value of the asset in question. The chance of these catastrophic events is ‘unthinkable’ and so not really taken into account by people when making investment decisions.

This is the wrong approach. In this piece, I will be talking about some of the hidden risks of the ‘safest’ asset classes and their implications for the investor.

Cash

What could go wrong with pilling up cold, hard cash under your mattress? This, surely, I hear you claim, entails no risks at all?

As you might have guessed, not quite. First, there are the practical considerations. If you actually store large amounts of cash somewhere in your house, that cash will promptly disappear if you get burgled, if your house burns down, or if your partner changes their mind about this whole marriage thing and does a runner (with the money). If at some other secure location, it can always be pinched. Cash held at a bank is dependent on the fortunes of said bank. As 2008 showed, this might not be the safest place in the world. The government will cover you up to £85,000, sure, but for those of you lucky enough to have more than this, you’re relying on the prudence of bankers.

Aside from the physical, one must also consider the monetary. Inflation, that cruel mistress, is the biggest threat to holders of pound sterling. It may be practically non-existent these days, but casting your mind back to the 70s will remind you of the real damage inflation can inflict on your purchasing power. If inflation is higher than the rate of interest you earn on your cash (that pile under the mattress is earning 0%) then you’re losing money in real terms. You’re actually getting poorer without realising it.

Government Bonds

Taking this cash and dumping it into government bonds may seem like a sensible thing to do, then. The government is probably less likely to fail than banks. These bonds earn some kind of interest to help combat inflation, too. Happy days.

Unfortunately, most of these rates of interest are dependent on the whims of the Governor of the Bank of England, not directly linked to interest rates. If the govna’ wants to maintain low interest rates to stimulate the economy after, say, a global pandemic has put a halt to business activity, they may maintain low interest rates, even with substantial inflation. This means that your bonds will be earning a negative real return. What’s also nasty about these bonds is the fact that their value fluctuates with inflation and interest rates. This means that you don’t actually receive the yield to maturity unless you hold the bond…to maturity. Otherwise, your yield may be substantially lower.

The government acknowledges this problem with bonds and issues index-linked versions to counteract this inflation risk. These bonds return some percentage above inflation, supposedly ensuring that you maintain your purchasing power (and then some). This, however, relies on the fact that the government calculates the rate of inflation correctly. How confident are you in the competence of the government? There is also the chance that the government defaults on their outstanding debt. This is unlikely under a fiat system (because they can always just print more money), but it remains a risk nonetheless. Reckless monetary policy can lead to veeeery high inflation, which is difficult to stop (just look at Argentina for a contemporary example). In this instance, your bonds would be worth precisely 0.

Shares

It would seem then, that relying entirely on the government may not be the best idea. What about companies?

The apparently safest form of investing in shares is investing in whole markets (or parts of markets) using index funds or ETFs. The highest level of diversification one can get is by investing in every market, using a global ETF/index fund. One of the main risks here is fake diversification. A lot of these global trackers should actually be called ‘US & Friends’. For example, if we look at the Vanguard FTSE Global All Cap Index Fund, we see that the US makes up nearly 60% of the fund. If the US performs badly, these trackers will too. There is also the chance that the company doing the tracking goes bust, meaning you will lose some of your investment. This is a pretty unlikely scenario, but it’s a possibility nonetheless.

An alternative approach is to keep your hard-earned money inside the UK, by investing in a basket of British companies. This leaves you rather exposed to the fortunes of the UK. If we prosper in the next 20-50 years, it will probably be a good move. If not, UK companies might not do so well. You are already likely to be heavily exposed to the UK via your job or some other way (like owning a house here), so it may be a good idea to diversify internationally a bit.

Many assets have this problem, come to think of it. If you plan on moving to the French Riviera in ten years’ time, you are going to want some exposure to French assets before you move. Let’s say France does really well in this time period but the UK does not. France is now more expensive, which is fine for French people because they have been getting richer, too. It’s not so fine for you, for whom France is getting more and more expensive. There is also the exchange rate risk to consider. You don’t want to convert your fortune into Euro only to find that it’s not worth all that much.

Just a closing remark on shares. It’s not clear that they will rise over and above inflation, even over long periods of time. The market is a complex system. The 7% return that everyone seems to be claiming the market naturally drifts towards is not guaranteed in practice.

Asset Management

What about just letting someone do your investing for you? Professionals with years of experience and good track records? That’s safe, right?

When you use these managers, you are putting your fortune into their hands. It’s really hard to judge if these are competent hands or not. These funds can dazzle you with past performance and a good sales pitch, but that is not a good indicator of strong future performance. Take the recent Archegos Capital Management blow-up as a warning (it was the largest trading loss in history). You just never really know what these managers are doing and what risks they’re taking.

Other Assets

Seeing these risks, some prefer to shun the financial world in its entirety and invest in real stuff. Stuff they can see and touch that has a good track record of maintaining value. Things that have historically been valued highly – watches, cars, wine, oil, gold, silver, etc. – could be a good bet. The problem here is that the value of these items is very much dependent on tastes at the time you come to sell. The green initiative could accelerate, crushing the value of cars and oil, for example. Or the demand for watches may just simply die off for no particular reason. I see this as unlikely – things that have historically been highly valued don’t tend to lose their allure overnight without some kind of devaluing mechanism – but it’s possible all the same. The point is, these things are valued pretty much out of thin air.

Some assets are not valued out of thin air. Those that generate cash-flow can have their values reasonably estimated. A small business, for example. Or a property that you rent out. The risks here are specific to each individual case.

Summing Up

Everyone is an investor. You can’t escape it. Everything that can be valued fluctuates in real value. Every day you are making investment decisions, so you might as well know what you’re getting yourself into (or make sure your financial adviser does!).

A big part of this awareness is knowing about the risks of investments, especially the disastrous, not-often-mentioned risks discussed in this post. Nothing is risk-free. Everything can go to 0 and you can lose all your money as a result, making for a pretty grim retirement. It’s just something you have to live with. You have to be a bit paranoid when composing your portfolio or you could get burnt, and burnt badly.

Of course, risk should not be the only factor when making investment decisions. Your specific circumstances (your goals, your age, your income, etc.) must also be taken into account. But risk should be, in my view, the primary consideration. To thrive, first you must survive.

Thank you to Haydn for an interesting and thought-provoking article. Please do check out his excellent blog at Perpetual Prudence as well.

I do very much agree with Haydn that every investment (or savings option) carries some risk. It is therefore essential to be aware of the downside/worst-case-scenario with any investment, while setting this against the potential rewards. Taking excessive risks is clearly to be avoided, but being too risk-averse – and therefore missing out on profitable investment opportunities – can be counter-productive as well. That applies especially to younger people, who may have 30 or 40 years before they retire.

It is also, in my view, crucial to avoid the mistake of putting all your eggs in one investment basket. As regular readers will know, I am a big fan of diversifying your portfolio as widely as possible – across different investment types, asset classes, platforms and risk levels. That way, if one or two investments do go south, hopefully they will be more than compensated by others that succeed.

It is also important to remember that investing is a long-term game. You should generally have at least a five-year time-horizon, to allow for the inevitable ups and downs in markets to even out.

As ever, if you have any comments or questions on this post – for me or for Haydn – please do post them below.

Disclaimer: Everybody’s needs and circumstances are different, and nothing in this post should therefore be construed as personal financial advice. Everyone should perform their own ‘due diligence’ before investing and seek advice from a qualified financial adviser if in any doubt how best to proceed. All investment carries a risk of loss.

If you enjoyed this post, please link to it on your own blog or social media:

Today I am pleased to bring you a guest post from Cora Harrison, a UK blogger and vlogger (video blogger) whose website is called The Mini Millionaire.

Cora says she loves to explore new ways of making money, both online and offline. She has a particular interest in online selling (and reselling) and there are many posts on this subject on her blog.

In her guest post today she reveals how anyone with an interest in creating arts and crafts can boost their profits – potentially many times over – by selling their work online.

Over to Cora, then…

If you love creating arts and crafts products, you can of course sell them at local markets or craft fairs. If you are looking to sell more and make (much) more money, however, you should definitely consider selling online as well.

There are various ways you can display and sell your work online. Here are some of the most popular.

Your Own Website

Selling arts and crafts on your own website is probably the single best way to sell your hand-made items online.

Having your own website will allow you to contact customers directly, grow your brand, and avoid the fees charged by third-party platforms like Etsy and eBay. In addition, you will not be competing directly with other craftspeople selling similar items to the same pool of customers on the platform.

For this to work, however, you will need to create an attractive, professional-looking website. You will then need to drive traffic to it, using techniques such as search engine optimization (SEO) and perhaps paid advertising. You can use online website building tools such as Wix or Shopify to create your site or hire a professional website designer.

Selling on Etsy

Etsy is an online marketplace dedicated to hand-crafted items. It is known for vintage, unique and custom-made items. It is easy to use, so you can set up your store and sell your crafts online in no time. Many would-be buyers of hand-made products look on Etsy before going anywhere else. Customers can pay by various methods, including PayPal and Google Pay.

On the minus side, many other artists and craftspeople also use the platform. This means it can be hard to sell common items. In addition Etsy charge about 5% of the sales value as a transaction fee every time you make a sale. You also pay about $0.20 for each item you sell. PayPal (the most popular payment method on the platform) also charge a fee for processing payments. All of these fees and charges will eat into your profits.

Facebook Marketplace

Facebook Marketplace is a prime location for selling hand-made crafts products locally. Given that Facebook has a massive user base, you can reach many potential buyers in your area by posting your items there. Posting items is free and you can add up to 42 images of your product in every sales post. The post will also include a description of the product, your location, and the price of the item.

While there is no limit to the number of posts you can make in a day, Facebook may limit posting to avoid spamming the page with similar ads. You have the option of sharing posts on your wall so that your friends may see the posts you have shared in local buying and selling groups. Potential customers will message you for more information and selling terms. The Marketplace is available on the web-based version of Facebook and as an app.

Selling on eBay

eBay is of course primarily an auction marketplace where sellers post items and sell them to the highest bidder. However, you can also create fixed-price listings. It is therefore a good platform to sell hand-made crafts online. The platform uses PayPal as the payment provider for all transactions. Both eBay and PayPal have various fees that you will encounter.

You will also be required to pay a final value fee. The fee is applied at the end of the transaction after making a sale. The fee is a percentage of the purchase price. There are also shipping and handling fees. Shipping fees are based on the method chosen by the buyer unless for domestic shipping, where the fee is calculated from the cheapest shipping method.

You will pay the final value fee whether or not the client pays for the item. If the sale is unpaid, you can cancel the sale or report it as unpaid. Note that eBay will give you credit for this rather than a cash refund.

Why Selling Online is Beneficial

There are several reasons you should consider selling your hand-made crafts online compared with selling in person at craft fairs and so on (though you can of course do both).

First, as stated above, online selling exposes you to a much larger audience than in the case of a market stall. You can sell your items to potential buyers across the country – and further afield – with ease.

In an online store, there are no opening time restrictions. The store runs around the clock and customers can place orders at any time of the day or night, as opposed to a local venue with set opening hours. In addition, you can operate the business from anywhere and target potential buyers who are far away from your location.

An online store also requires less time and effort. Once you have set up your online store and posted your hand-made items, they will be seen whether you are online or not. This allows you to sell your crafts even if you are otherwise engaged.

An online store also has lower running costs than an off-line one. There are no utility bills, rent or other premises costs to pay. You can run your online store from your kitchen, living room or bedroom. All you need is a laptop or desktop computer with an internet connection.

Effectively Selling Your Items Online

The Quality of Photos Matters

Just like in an off-line store, in an online store your hand-made crafts need to look good to appeal to customers. It is therefore vital that you take clear, sharp photos of your items. You can take them from different angles to give the customer an all-round view.

A modern smartphone should produce good-quality images in ambient light, but place your items on a white surface to give them a professional look. You can also use image-editing software to make the image ‘pop’.

Give Your Items a Perfect Description

Since you will not be there to explain the features of your product in person, it is important to provide a good description alongside your image. Ensure that the customer gets a mental image of the item without getting too sales-y. Most platforms have a character limit within which you can write a description. Use this opportunity to explain all the features that might be of interest to a potential buyer.

Keep Checking Your Site Regularly

Keep checking the platform where you have posted the item regularly for customer queries or orders. If the account is linked to your email address, you can have ‘push notifications’ set on your phone so that you know when there is activity relating to your item. The ability to respond quickly to queries will boost your reputation and prevent you from losing customers.

You may wish to post on more than one platform to increase your exposure. Try to estimate the return versus the cost of placing ads on multiple platforms. Having many items listed rather than just a handful will increase your overall selling rates as well, so aim to build up your inventory as quickly as possible.

Good luck, and I wish you every success selling your hand-made arts and crafts online!

Many thanks to Cora Harrison (pictured, right) for some great tips and ideas.

Selling arts and craffs (online or off-) isn’t something I have ever tried myself, but I know it will interest many of my readers, so I was delighted to receive Cora’s article.

Obviously, you need some artistic talent to do this, but you definitely don’t need to be Leonardo (da Vinci, I mean, not DiCaprio). For example, using inexpensive software you can create attractive printables, which could sell well on Etsy and similar websites. You can read my blog post on this subject here.

But if you really don’t feel that selling arts and crafts online is your thing, you can still make good money selling and reselling products of all sorts online, from DVDs and collectables to Lego bricks! Check out Cora’s Mini Millionaire site for much more information about this..

As always, if you have any questions about this article, for Cora or myself, please do post them below.

If you enjoyed this post, please link to it on your own blog or social media:

Today I am pleased to bring you a guest post from my colleague Will Pointing from GreatDealsMadeEasy.com.

In his article below, Will sets out his top tips for saving money on many of your home utilities.

Over to Will then…

Many people stay with their utility providers for years and years without changing, on the principle that ‘loyalty pays’.

Sadly, this only really applies with lifelong friends and the Cafe Nero loyalty app (where you get a free coffee after buying eight!). With yearly price rises on most home utilities, it’s a good idea to review them annually (at least) and save yourself £100s in the process.

As a general rule, new customers get the best deals. Below are some tips on how to uncover the golden deals that are right for you…

Broadband – prices increase to £152/year when you remain with them

A survey by Which? magazine found that 71% of respondents stayed with their ISP (Internet Service Provider) for over three years. Most providers offer the best deals on broadband for 12-18-month contracts, meaning after that period prices shoot up significantly.

Tips: Look for what is included in your deal and whether you really need it. Do you need all those TV channels when you have Netflix? Do you need calls included when you have a mobile phone?

Mobile phone – prices increases to £264/year when you stay with them

It so easy to forget when you have paid off your mobile handset (the companies rarely remind you if you have) and then stay on an inflated monthly rate for years. Phone companies create these fashionable adverts to try and convince you to get the latest phone, when actually buying a SIM-only deal until you really need a handset upgrade is the cheapest way. If you want a new SIM-only deal or a new handset, check out comparison sites like my one here.

Tips: Out of contract? Switch to a SIM-only deal. If not, ensure you are on the right tariff for you and you are not paying for unnecessary data (use free wifi when you can to save on using your data).

Water – average bill is £415 a year

Water UK estimate that the average water and sewerage bill is £415 a year or £34.58 a month. It is recommended to get a water meter installed, so the cost is as accurate as possible.

Tips: Water saving tips include having a shower not a bath, washing up manually, and putting a full load of clothes into the washing machine. Many modern machines also have an ‘Eco’ mode, which uses less water and electricity.

Heating and power – cost around £1,254 a year

Using comparison sites to evaluate different energy suppliers and tariffs is perhaps the simplest, most valuable money-saving action you can take. You can often save hundreds of pounds a year by doing this, especially if you haven’t switched for a while (or ever). Again, many customers continue on a high rate for years without asking the question, ‘Is this the best deal for me?’ I suggest using websites like Compare The Market, Money Saving Expert and Go Compare.

Tips: After getting the best possible deal, I recommend submitting regular meter readings to your supplier, so you are not overpaying. And turn off your lights as much as possible!

GreatDealsMadeEasy.com is the website to help you save money online the easy way. Whether you’re looking to cut back on your broadband bill, save on a holiday abroad or come up with a side hustle, Great Deals Made Easy will help you find useful tips and top deals. Expect great articles, interviews, reviews and advice. It’s written by digital marketing expert Will Pointing. Expect to find out how you can save money every month, the easy way!

Many thanks to Will for some great money-saving tips. Do check out his website at GreatDealsMadeEasy.com as well.

My own top tip would be to check out deals from cashback websites when changing utility suppliers. Sites such as Quidco and Top Cashback are especially worth a look when swapping energy companies. I talked about this recently in my blog post about How to Save Money with Cashback Sites.

On various occasions I have pocketed £70 or more in cashback when switching my gas and electricity providers. You can do this directly by signing up with an energy company via the cashback site (check first on a price comparison site that they are offering a competitive deal, obviously). Alternatively, many comparison services are also listed on cashback sites – so by clicking through to the comparison site and then switching via them, you can get cashback – and a good deal – this way.

And speaking of energy suppliers, you can also save money by getting a smart meter installed. These are currently being fitted free of charge by the energy companies. They help you monitor your energy usage and discover ways you can save money. In addition, a growing number of energy suppliers now reserve their best tariffs for people with smart meters. Check out my blog post Should You Get a Smart Meter Installed?

As always, if you have any comments or questions about this article, for me or for Will, please do post them below.

If you enjoyed this post, please link to it on your own blog or social media:

Today I have a guest post for you from James Mackay, a certified financial planner and regular reader of Pounds and Sense 🙂

In his article below, James addresses an issue that will be real and pressing for many readers of this blog – how to prepare for retirement and enter it successfully.

Over to James then…

If you’re starting to think about your retirement, these are three important questions that you need to ask.

1. Have You Had Enough?

It’s Sunday evening and you’re winding down after a busy weekend with friends and family. As you sit back in your favourite chair and think about the week ahead, you can’t quite get comfortable.

The thought of going back to work on Monday morning makes you feel a bit uneasy. In fact, the thought of doing it for another 5–10 years makes you feel sick!

If you’ve ever experienced this, you might be approaching the point where you’ve had enough (that’s a technical term).

The question you need to ask yourself is whether the pain of going to work outweighs the benefit. If you find yourself in this situation; where you’re emotionally, physically and mentally drained and no longer excited to perform at the highest level, it’s time to do something about it.

Having had enough doesn’t mean that it’s necessarily time to retire. It simply means that you need to change the status quo.

Maybe you’ve had enough of your current role, but you’ve got more to give in another capacity. Your years of wisdom could be very valuable in a different guise. Perhaps you’ve had enough of having a boss and are ready to go it alone. With the years of experience, it’s no surprise that over 50s are the best entrepreneurs. Or maybe you’re happy to carry on but just want a little bit more flexibility around what you do and when you do it.

These are all useful options to explore, particularly if you haven’t got enough to hang your boots up yet. Sometimes, the benefit of working for “just one more year” can make a real difference to your financial situation.

2. Do You Have Enough?

If you’ve had enough, and are ready to move onto pastures new, the next question is do you have enough?

Whenever I ask this question, people start telling me how much they’ve got saved up. But they’ve got it all wrong. It’s like trying to build a house without the seeing the floor plans. You need to start with the end goal and work back from there.

Working out if you have enough requires knowing:

Your monthly number – this is how much a comfortable lifestyle is going to cost.

The gap – this is the difference between the two, and where your savings come in. Broadly speaking, if you’ve got 20x the gap in savings, you should be fine. Any less and you might not be quite there yet.

But, there’s more to retirement planning than just simply figuring out your ‘number’. Finding your purpose in retirement sounds wishy-washy, but without a clear purpose you’re likely to be one of the 25% of retirees who return to work.

3. Will You Have Enough to Do?

You need to ask yourself what you are going to do when you wake up on that Monday morning, free from the ties of work, and how are you going to fill your time.

If for the last 40 years you’ve been busy being busy – chances are you’re going to get pretty bored sitting around the house for 40 hours a week. I’ve seen many successful individuals retire, only to get bored and return to work within five years. The newly-found free time that retirement provides can be overwhelming for some.

Retirement is about having enough money to sleep at night and enough purpose to get up in the morning. It’s not just about the numbers, it’s about how you’re going to spend your time. Purpose will drive you in retirement, money will fund you. Try not to get those two mixed up.

The bottom line is this… retirement is the biggest transition you’re ever going to make. It’s not the sort of thing you do regularly and not the sort of thing you want to get wrong. By asking yourself these three questions, you’ll improve your chances of achieving a successful retirement.

Byline: James Mackay is a Certified Financial Planner at Frazer James. He has helped hundreds of clients to achieve financial independence and retire with confidence, clarity and purpose.

Many thanks to James (pictured above) for a valuable and thought-provoking post. As a semi-retired 63-year-old myself, I can identify with all of the points he raises.

Actually I think there is a strong case for phasing your retirement if possible, maybe reducing the number of days per week you work initially and/or moving to a less pressured role. This can make retirement feel more like going on an interesting journey rather than driving over a cliff!

I also think there’s a good case for continuing to do some work you enjoy during the early years of retirement at least, to boost your income, provide social interaction, and keep your mental and physical faculties sharp. Of course, voluntary work can do this as well (apart from boosting your income, which may or may not matter to you).

If you have any comments or questions about this article – for me or for James – as always, do feel free to post them below.

If you enjoyed this post, please link to it on your own blog or social media:

tic a way as he is doing!

tic a way as he is doing!