Today I have a guest post for you on a subject I’m sure will resonate with many Pounds and Sense readers.

We all love a freebie, but how do you ensure that by providing your details you aren’t opening the floodgates to a torrent of spam? Read and follow the tips below from my friends at All Free Stuff. And don’t forget to sign up for their free email newsletter to get details of all the latest free offers daily!

It’s completely possible for you to get free stuff. There are plenty of opportunities out there.

That said, for every legitimately free thing you can get, there are two complete scams set up to get your personal information at the cost of a few free samples. If you want to get free stuff without dealing with scams, try the following steps.

1. Set up a ‘spam catcher’ e-mail. This e-mail account is one you have no plans on using for normal correspondence, but rather the address you give out for giveaways and promotions. You can also use it when you register with a company that wants your e-mail address in exchange for free gifts. If you give the company your primary e-mail address, you’ll be swamped with a mass of promotional e-mails. It won’t take long for you to abandon your e-mail account in despair if this starts to happen.

2. Avoid giving personal information. You should never give out more than your name, e-mail address, physical address, and birthday. And you should be careful about giving away all of those, as well. If you can, try using a fake name or a PO Box. The more personal information you give out, the easier it will be for other companies to get that information. In addition, some websites ask for your credit card number ‘just to ensure you’re a real person’. Once they have your credit card information, you can’t make them forget it.

3. Be realistic about what you expect. If the deal seems too good to be true, it almost certainly is. It’s certainly possible the giveaway is legitimate, and if that’s the case then they should have company contact information readily available. You should also check the internet to see if you can find information. If the offer is that great, then plenty of people will be talking about it. Of course, if it’s a scam you’re liable to find discussion about that, too.

4. Visit only legitimate websites for samples. Manufacturers’ sites are generally trustworthy, whereas some retail-specific sites are not.

5. Write to the manufacturers of products you enjoy using. Companies are always happy to give a few freebies to customers willing to go out of their way to make their voice heard. It builds goodwill and often garners more customers. And all for the cost of a few free samples.

6. Learn to use coupons properly. It can take a huge amount of patience to learn to coupon well. That said, good couponing can save you so much you may even get free groceries. Couponing is a fairly big deal, so you can find plenty of websites that can help you learn. There are also many grocery stores or manufacturer sites that will keep you informed of what great deals and amazing coupons are available.

These are some of the best ways to get free stuff without dealing with scams. Do you have any other tips yourself? Please do leave them below!

Disclosure: This is a sponsored post.

If you enjoyed this post, please link to it on your own blog or social media:

Today I have a guest post on what can become a major issue for parents when making gifts or loans to their married children. Specifically it looks at what you can do to ensure that your wishes are respected should the worst happen and the marriage fails.

The article is by Joanna Toloczko, a partner, family law solicitor and mediator at UK law firm RWK Goodman.

Over to Joanna then…

According to the UK House Price Index in August 2023, the average house price in the UK was £291,000 and in London a whopping £536,000. To put this into context, the average house price back in January 2013 was £167,716, representing an increase of around 73%.

A bank or building society will normally require a minimum deposit of between 10% and 25% of the property value as a term of a mortgage offer, and the more you are able to put down as a deposit, the lower rate of interest you are able to secure. It is not surprising, then, that an increasing number of married couples rely on a contribution from one or both sets of parents for their deposit.

In my work as a family lawyer and mediator I often come across cases where a divorcing couple are at loggerheads about whether such a contribution was a loan or a gift. The party whose parents provided the funds will often argue that the funds were a loan which should be returned to their parents before the remaining funds are distributed between the husband and wife. The other party will usually argue that the funds were a gift and are available for distribution between the parties.

If the couple are not able to reach agreement and the case proceeds to court significant sums of money can be spent on arguing this point as a preliminary issue. Very often the parents will be drawn into the litigation.

Even if the Court accepts that the funds were a loan, it is possible that the Court will take the view that it was a “soft loan”, i.e. a loan where repayment is unlikely to be enforced. In these circumstances, the Court may choose to disregard the liability.

Usually, at the time the funds are made available to the couple no-one has formally addressed the issue of the nature of the advance. Everyone is excited about the new house purchase; no-one anticipates that the marriage may fail.

So, what can be done to ensure that gifts made to married children stay in the family of the parents making the gift, in the event of a divorce?

If the funds are being advanced to assist with the purchase of a property, a Declaration of Trust can be a useful tool. In this situation the married couple are the legal owners of the property and hold the property as “tenants in common”, which means that they have their own distinct share in the property. The Declaration of Trust can be used to set out the beneficial interests in the property, including the interests of third parties. For example, a Declaration of Trust could make it clear that as parents had contributed to the purchase price of the property, they are entitled to a specified share of the equity. Alternatively, the Declaration of Trust could set out that once the property is sold, the parents have to be reimbursed prior to the distribution of the remaining equity between the couple.

If parents are to receive a share of the equity, they need to be aware of a potential Capital Gains Tax liability, should their interest in the property increase in value.

Another alternative would be to use a formal loan agreement or for the parents to take a Legal Charge over the property. A Legal Charge works like a second mortgage. It is secured over the property and registered at the Land Registry. The Charge sets out details of the sum loaned to the couple, whether interest is payable and when/in what circumstances the parents are entitled to call for repayment of the loan.

Nuptial Agreements are also becoming more popular. These can be entered into either before the marriage (Prenuptial Agreement) or during the course of the marriage (Postnuptial Agreement).

These agreements make clear what is to happen to the couple’s assets in the event of divorce or separation.

If parents are gifting money, transferring properties, leaving an inheritance, providing an interest in a business, etc, and they wish to protect those assets in their child’s favour in the event of separation or divorce, a Pre- or Postnuptial agreement can be an extremely useful document.

Although Nuptial Agreements are not legally-binding and can be over-ruled by a judge in the divorce proceedings, if they are prepared in the correct manner, they have good prospects of being upheld or will certainly be heavily influential on the judge.

In summary, when advancing funds to a married child, always be clear about whether the funds are a gift or loan and seek legal advice about how best to ensure that the funds remain in the family in the event of a divorce. It is usually also a good idea to discuss any tax implications of your plans with an accountant or tax adviser.

Joanna Toloczko is a partner, family law solicitor and mediator at RWK Goodman and can be contacted on 07553 058485 or at Joanna.Toloczko@RWKGoodman.com.

Many thanks to Joanna Toloczko (pictured, below) for an informative and eye-opening article. Please do check out her company’s website (linked above).

While nobody likes to think about the marriage of their offspring failing, the reality is that an estimated 42% of marriages in the UK today will end in divorce. So it is vital to be realistic and ensure that, should the worst happen, any money you give or lend is returned or divided in accordance with your wishes.

As always, if you have any comments or questions about this article, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

Public speaking can be a good paying sideline for retired and semi-retired people. As well as the financial benefits, it can offer an enjoyable opportunity to talk about your hobbies and interests, or your current or former career. I’ve also known people who have done public speaking as a method of raising money for charities or other causes close to their heart. Although the pandemic and lockdowns temporarily put paid to most public speaking work, as life has returned to normal the opportunities are definitely out there again.

Over to Sally then…

Wouldn’t it be great to make extra money by following your passion? A hobby that pays makes ‘working’ a pleasure. Unfortunately, things like stamp-collecting, rambling and local history rarely turn a profit, but there is a way to make them pay: share your specialist knowledge with others.

Community organisations such as the WI, Probus and independent Leisure and Learning clubs struggle to find speakers for their meetings. I speak about novel-writing at many such groups and am always asked if I know of any other speakers open for bookings. These are paid gigs. How much you charge, how far you travel and what type of bookings you take are all up to you. Depending on the policy of the organisation, these events may also give you the opportunity to sell produce from your hobby. For example, I sell copies of my books, but a creator of conserves might sell jam and marmalade or an artist, his paintings.

Below are some tips for starting a speaking career:

Collate enough material for a 45-minute talk and sort it into a logical sequence. Include stories that will capture the listener rather than a lot of heavy facts.

Refine the material into minimal bullet-pointed notes. It’s important to talk freely around each bullet point rather than read from a manuscript. Reading makes eye contact with the audience difficult and hand gestures to illustrate your words are almost impossible.

Think about any visual aids; these add variety and colour to a talk. When I talk about thriller-writing I produce some ‘murder weapons’ – a rolling-pin, a (blunt) knife and a packet of tablets. The conserve creator might show her jam pan and specialist thermometer. The artist might have a range of brushes to discuss.

Practise! Producing a successful talk is like an iceberg. At least 90% of the work is in the preparation beforehand. However, once you’ve perfected your performance, you can give that same talk many times to different groups.

Don’t be surprised if you are handed a microphone to use. This often happens in large halls or where several audience members are hard of hearing. Hold it at a consistent distance from your mouth and don’t turn your face away from it. Practise at home by holding a wooden spoon – this will give you an idea of what it’s like to talk with only one free hand.

Enquire at your local church hall about community groups who meet there and use speakers.

Do a couple of small bookings for free and ask for feedback from the audience. Once you’re confident, don’t make a habit of speaking for free (unless it’s a charitable cause) because that makes it harder for other speakers to ask for a fee.

Receiving a cheque at the end of a talk is good but public speaking brings other benefits, such as the opportunity to meet new people and share your knowledge. It will improve your everyday confidence as well. When you can speak in front of an audience, complaining in a shop or restaurant is less daunting, putting your point of a view in a meeting is easier and making small talk with strangers at a party is no problem.

Many thanks to Sally Jenkins (pictured) for an interesting and inspiring article. Although as I said to her, I hope she never gets stopped by the police on the way to one of her public-speaking gigs and asked why she has all those ‘murder weapons’ in her bag!

I have done a bit of speaking myself, both for work reasons (in the long-ago days when I had a proper job) and to talk about writing or blogging. I always get nervous beforehand, but once I start I normally enjoy it and get a buzz from doing it.

I would maybe add one more tip to Sally’s list and that is to compile a list of topics you can speak about (with appropriate visual aids, of course). You can then offer potential bookers a ‘menu’ they can choose from. This has the benefit that if they don’t like one idea, they may well go for another. It also means you can potentially get repeat bookings, maybe on a regular basis, speaking on a different subject each time. This certainly happens with some of the speakers who are booked by my local U3A.

As always, if you have any questions about this article, for Sally or for me, please do post them below.

This is a fully updated version of an original post from 2019.

If you enjoyed this post, please link to it on your own blog or social media:

Today I have a guest post that may be of interest to many readers of this blog.

It has recently been reported that nearly 100,000 retirees have returned to work due to the cost of living crisis and the realization that they need more money to live in reasonable comfort.

To help those in or nearing retirement, my friends at Equity Release Supermarket have set out some of their top tips for older people on how best to manage their finances, time, and boundaries with loved ones, to support their overall mental and physical well-being.

Many consider retirement to be the first time in their adult lives that they can relax and prioritize doing what they enjoy most.

This new-found freedom can be overwhelming, however, and establishing a new routine can take time. What’s more, as the cost of living crisis continues, those in and approaching retirement likely need to pay closer attention to their personal finances and outgoings.

Mark Gregory, Founder and CEO at Equity Release Supermarket, explains: “We speak to hundreds of over 55s each week and, for many people, the prospect of spending more time with loved ones and being able to offer support to their family is what they look forward to most. We also see how people want to use retirement as an opportunity to pursue budding interests or fulfil personal goals.

“As a result, it is important that those in and approaching this stage of their life manage both their time and money, helping to get the most from their retirement plan and budget.”

To help, the experts at Equity Release Supermarket have shared steps for retirees to keep on top of their time and finances to ultimately support their well-being and achieve their retirement goals.

Set goals by creating a retirement plan

Whether retirement is a few years away or you’ve already stopped working, we recommend making a retirement plan.

Start by thinking about your long term goals, such as places you want to travel to or whether you’d be interested in learning a new skill in the future. Then, consider what day-to-day activities you enjoy doing, such as spending time with grandchildren or visiting friends, as well as tasks you want to tick off your to-do list. This could include anything from giving your garden a makeover to clearing out old items from the loft.

Mapping out your days, weeks, and even years with goals and activities that will bring you fulfilment will help you organize your priorities for retirement. You could write these goals down in a notepad or even create a vision board.

Regardless of your process, make sure your retirement plan is something you can physically refer to in the future, rather than just having all the ideas up in your head.

Check in with your budget

When it comes to planning your yearly budget, you will need to establish how much money you require for your outgoings and living costs, as well as any big expenses you have planned for retirement. This could be anything from a bucket-list travel destination to supporting a son or daughter in buying their first home.

If possible, you should also aim to create an emergency savings pot, to use for any unexpected expenses.

However, it is important to remember that just because you have set your budget, those figures are not set in stone.

There are many factors that can affect your outgoings, from the ongoing cost of living crisis to personal changes such as marriage, divorce, moving house/downsizing or serious illness. Be flexible with your budget and priorities to accommodate these changes and the impact they may have on your personal finances. You might find that you need to seek out other financial options or guidance to support both your retirement and your loved ones.

It’s also important to continually check whether the money you’ve set aside for big expenses is working for you and your well-being. You might realize that you want to spend more money on things you hadn’t planned for, such as renovating the house or going on a once-in-a-lifetime holiday – in which case, you will need to update your financial plan accordingly.

Communicate with loved ones

Although creating a clear plan for retirement is essential, you also need to be mindful that life does not follow a set path.

From your physical health and mobility to ticking off your travel plans, your goals and potential limitations in retirement will adjust over time – and that’s fine and to be expected.

As difficult as it may be to admit, it can become a burden to spend your free time exactly as planned or support loved ones as much as you hoped. In these instances, it is important to keep communicating with your loved ones and be honest with them, so they can offer you support too. This will help to alleviate any pressure you may be feeling and allow your family and friends to be more accommodating of your situation.

Take care of your physical and mental well-being

It is important to make time in retirement for activities that will aid your well-being, especially as loneliness and depression are increasingly prevalent in later life.

Without the daily company of colleagues, you need to ensure you still get chances to socialize and see friends. Whether it’s arranging a coffee catch-up or joining a new local club, there are plenty of ways to incorporate social activities into the week without spending too much money, seeing both old friends and making new ones.

You can also take up activities that will benefit your physical and mental health at the same time, such as walking or low-impact exercises such as Pilates or yoga.

Think about the future

Although retirement may have been the end goal for your working life, it doesn’t mean you should stop planning for the future.

For example, you can make financial decisions that will save time and money in the long run. This could include minimizing your monthly outgoings to pay off existing mortgages quicker, as well as potentially providing you and your loved ones with more freedom later down the line.

If you’re planning to leave an inheritance to your children or family members, it is also worth considering gifting this money instead. Money gifted through equity release [or otherwise] becomes exempt from inheritance tax, provided that the giver lives for seven years afterwards. This can be a useful strategy for those who want to offer more financial support to loved ones throughout retirement and see the positive impact of this themselves.

So there you have it, five tips for getting the most from retirement. For more information about finances in retirement, visit the Equity Release Supermarket website.

I do agree it’s important to cultivate a strong social network in retirement, both with existing friends and family and with new friends and connections.

Time and again, studies have found that older people are both mentally and physically healthier when they foster relationships with others and maintain strong social connections. By contrast, social isolation and loneliness in old age have been linked to higher risks of heart disease, obesity, depression, cognitive decline, and so on.

Staying connected is especially important if (like me) you live alone. Social groups such as U3A are inexpensive to join and offer a wide range of activities, from rambling to guitar-playing, bird-watching to music appreciation. It’s well worth checking if there is a U3A group in your area. I recently joined not one but two local U3A groups and plan to write a post about this soon.

it’s also important to pay careful attention to your finances in retirement. On the one hand, you need to watch your income and expenditure to ensure you don’t run out of money in old age. On the other hand, though, you don’t want to deprive yourself without good reason and end up leading an unnecessarily frugal existence in what should be your ‘golden years’.

If you’re unsure about your finances, it can be a good idea to have a chat with a professional financial adviser. You definitely don’t need to be super-wealthy for this. Take a look at my blog post 10 Reasons Over-50s May Need an Independent Financial Adviser for more information. Most advisers (including mine) will be happy to arrange an initial meeting free of charge and without obligation.

As always, if you have any comments or questions about this post, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

Today I am pleased to bring you a guest post on investing in classic cars, a subject which I freely admit I previously knew little about. The article comes from my friends at the popular Car & Classic website.

As they say at Car & Classic, not all collectable metal is gold…

More than ever, nowadays, investors may be on the lookout for sensible use of their cash; there are relatively higher interest rate savings accounts, granted, alongside the usual route to gold and fine art. Even wines appreciate in time, if the right bottles are purchased, and kept untouched.

However, unlike paintings, gold and building society accounts, there is an area of investment which can be actively enjoyed whilst the asset keeps increasing in value: classic cars. The drawback? You need to know which ones!

Introduction

Car & Classic’s CEO Tom Wood and Head of Editorial Chris Pollitt explain the company’s perspective on the classic car market at the end of another unusual year. Launched in 2005, Car & Classic is Europe’s largest classic cars marketplace and welcomes around four million visitors every month. With over 30,000 cars listed at any one time and a thriving online auction platform, it’s an excellent barometer of classic car trends.

The Drive Behind the Desire

Purchasing a classic car is never a straightforward, totally rational process. Most people have memories connected to specific cars of the past; and in the recollection process, those memories resurface, drenched in emotive, romanticised aspects.

It could be the old ‘Sweeney’ Granada, as seen on TV and driven by your dad on the school run, or your favourite uncle’s shiny red Capri: moments associated with events and fantasies of our earlier years. It is a fact that prices associated with ‘Young Timers’ (i.e. cars of the ‘80s, ‘90s and ‘00s, also known as ‘modern classics’) are increasing fast. This is fuelled by a generation coming into the market with money to invest and looking to buy the cars of their childhood, if not the one in the poster on their bedroom wall.

What Are the ‘Modern Classics’?

“The market, both in the UK and abroad, is moving quickly,” says Wood. “Certain vehicles and periods, such as modern classics, are doing well. Recent sales include a Ford Escort RS1600i achieving over £40,000. “We operate in a non-essential sector driven by passion and heritage. Our business is at the intersection of luxury and hobby sectors. We believe that the higher end of our core customer base, vehicles over £100,000, will be lightly affected, if at all, by the downturn. Just last month, we sold an Aston Martin DB2/4 in The Netherlands for 185,000 Euros. ‘Starter classics’ – cars around £5-£10,000 such as MG Midgets, certain Minis or base cars from the ‘70s and ‘80s – may not fetch ridiculous amounts of money, but the interest in them is no less strong.”

Benefits and Advantages

In the current financial climate, the advantages of owning a pre-1983 vehicle are unquestionable: zero cost road fund licence, MOT exemption (though it is advisable to continue testing your vehicle, to avoid safety concerns). In places like London, where Mayor Khan’s proposal to widen the ULEZ out to the M25 is not the most popular of decisions, pre-82 cars are exempt from the charge. Many large cities have a similar scheme and others are following suit. Over-40-year-old classic cars are indeed popular and their values may be increasing, but are they easy to live with?

Cars approaching the 40-year cut-off point, the ‘modern classics’, are in many ways much easier to live with than their older counterparts and accommodating enough to be used as everyday transport if necessary.

1980s and 1990s

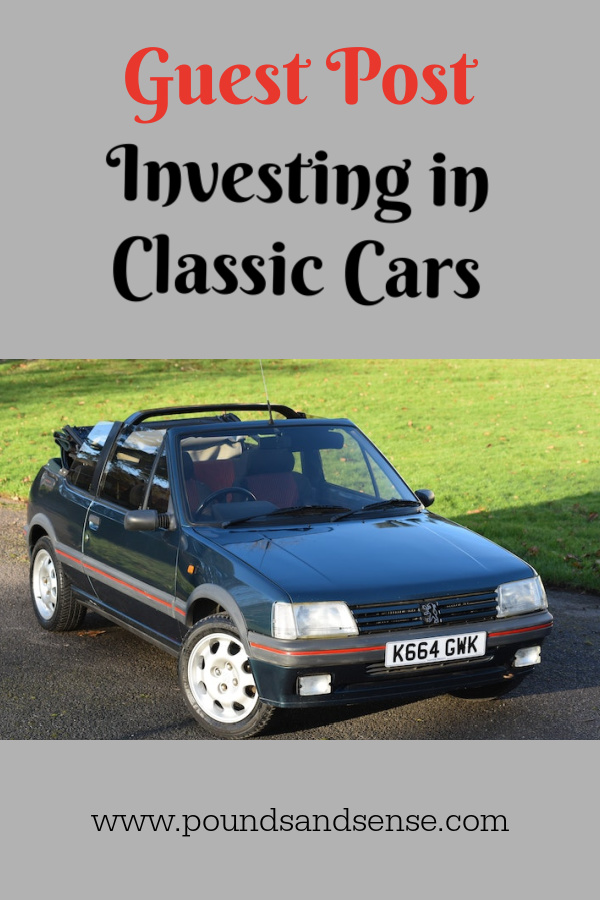

The Eighties gave us some great cars that are now as much fun to drive as they were back then; they have a raw energy and connection to the road that modern cars may lack. Some, like this Peugeot 205 CTI [photo in cover image], can be sporty, even with an open top. The Peugeot 205 GTI, Porsche 924/944, VW Golf GTI and Rover SD1 are a few other examples.

Accordingly, auction prices recently fetched reflect their desirability. “A 1990 Porsche 944 sold at auction for over £10,000 on Car & Classic is a classic (excuse the pun) example,” says Car & Classic Head of Editorial Chris Pollitt. “Want to try your hand at a light restoration, and don’t need the 3-litre engine? Then £5,000 will buy you a shiny red 2.5 2+2 GT 1988 944 Coupé.

“The 944 was considered by many to be a ‘poor man’s Porsche’; however, with fine handling, galvanised body and a reputation for reliability (chrome cylinder bores apart) it is, justifiably, a great entry model for the prestigious marque and a forgiving way into the world of classic cars.”

Brand names that many would assume to be out of their reach, like Rolls-Royce or Bentley, may often be overlooked, as super luxury models fall into disrepair if not properly maintained, and fuel cost may discourage ownership, but good and useable examples can be found for sale.

“This 1997 Bentley Turbo R [photo below] let its new owner become part of the rarefied community of powerful saloon fans for less than a 2015 BMW 330d M Sport,” says Pollitt.

Maintenance may be a greater issue for newer cars, counterbalancing some of the potential advantages: 90s’ electronics helped cars become more fuel-efficient and comfortable but upkeep is more onerous if they start to fail and could present owners with hefty garage repair bills, or the home mechanic with the prospect of long, cold days scouring breakers’ yards and internet sites for replacement electronic modules.

The Advice

For Wood, the nature of the hobby is a factor in how it will evolve during what many still expect to be a recession in 2023.

“The good with clear provenance will always attract the best money, but in the year ahead there could be some great bargains to be had too.

“The best advice is always to buy the best you can afford, no matter what decade the car belongs to. Originality is highly desirable and sells for the highest price, and the same can be said for rarity and a well-documented sales and dealer service history.”

Where Values May Be Going Down

“When talking to owners of older cars; pre-war and up to the early sixties, we are seeing values soften,” says Wood. “From our data, we predict that this will continue through the year ahead as the cost-of-living increases hit home and the impact of increased fuel prices is felt.”

Going Under the Radar

A few cars flying under the buyer’s radar at present come to mind.

As time marches on, specialist cars are becoming affordable and again offer potential investment opportunities. They include later Reliant Scimitars, Lotus Elans and TVR Tasmins [photo below] going for £4,000-8,000.

Humble ‘first’ cars are becoming sought-after too, from the Ford Fiesta, Renault Clio and smaller Peugeots. All are starting to become Cult Classics.

“If you have a big barn, fill it with today’s cars, because as electric vehicles become the norm and Government legislation ostracises combustion engines, today’s bangers could be tomorrow’s classics,” concludes Pollitt.

A Final Thought

Not unlike fine wines, classic cars (the right ones at any rate) are appreciating over time. Unlike vintage wines, though, they don’t need to be kept locked up in dark cellars and enjoyed just the once!

Thanks again to my friends at Car & Classic for an eye-opening and informative article. Do check out their site and the links to the cars in the article for further ideas and information.

One thing not mentioned above is that, as well as their potential as money-makers, investing in classic cars can offer tax advantages as well. As discussed in this guest article on PAS a few weeks ago, private cars can be sold for any price without attracting a charge to Capital Gains Tax (CGT) and that includes vintage and classic cars. This is particularly significant with CGT tax-free allowances due to be slashed in the coming years. Obviously tax laws may change in future – but according to the author of the article mentioned (an associate in the private client team at law firm RWK Goodman) that is how the law stands currently.

As always, if you have any questions or comments about this article, please do post them below.

Disclaimer: I am not a qualified financial adviser and nothing in this post should be construed as personal financial advice. You should always do your own ‘due diligence’ before investing and take professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

If you enjoyed this post, please link to it on your own blog or social media:

Today I have a guest post for you from my friends at Money Marvel about the effects of inflation on savings and loans.

With inflation currently over 10 percent and prices seemingly rising by the day, this is clearly a big concern for many people right now. It’s not always such a bad thing if you’re paying off debts, though. And if you’re saving for the longer term, higher rates of inflation can actually provide an extra incentive to invest. Learn more in the article below…

If you’ve been following the news at all in the UK over the past year you’ll have no doubt heard about inflation – it has been almost impossible to avoid it in the press. But what actually is inflation? And, more importantly, what does it mean for your savings and loans? Read on for my thoughts.

What is Inflation?

Simply put, inflation is the economic force that drives prices to change over time. Everyone has an item from their childhood that always surprises them with how much more it costs now (for me it’s the Freddo! I remember them being 10p each, now they’re almost 40p). That’s a great example of inflation in action: the gradual increase of prices over time.

Over the last year, the impact has been even more dramatic. Inflation rates in the UK are now at the highest they’ve been for over 40 years, with the CPI measure of inflation now running above 10%.

It has never been more important to consider inflation when planning your savings or loans.

What Impact Does Inflation Have on Savings?

Unfortunately, inflation is not good news for savers. It means that the cash you’ve built up and set aside will be worth less when you eventually spend it than it was when you first saved it.

In part, that’s why you’ll receive interest as a return on your savings. Savings are a mechanism for you to lend your money to banks and financial institutions, and the interest you get is your compensation for doing so.

You can straightforwardly compare the interest rate on your savings and the current UK inflation rate to see if your money is overall worth less or more over time. For example, if the headline inflation rate is 10% and you’re being offered 5% interest then you know you’re effectively losing 5% in value each year.

Sadly in the current economic reality, it’s almost impossible to find a savings interest rate higher than inflation, so most savers will have to accept the reality that they’ll be losing value year-on-year.

What Can Savers Do About It?

For those that need the security or guaranteed access that comes with a savings account, the unfortunate answer is that there isn’t much you can do about inflation. It’s important to be aware of it so that you can plan your future considering its impact, but sadly there’s nothing you can do to avoid it.

If your time horizons are a bit longer and you’re comfortable with a level of risk, then there are a variety of other investments that promise returns higher than the rate of inflation (for example, by investing in stocks and shares, or physical assets like gold). By their nature, they do come with a significantly higher level of risk and volatility than a savings account does. They may be suitable if you’re planning to save for a long time period (5 years+) and are willing to ride some ups and downs in the meantime.

Inflation alone shouldn’t lead you to take on risks with your savings that you otherwise wouldn’t, but it should help you understand the real returns that different savings products might offer. And if you’re determined to outpace inflation in the long run then savings accounts are likely not to be the best place for your money.

What About Debt?

High levels of inflation are much better news if you’re already holding significant debt. The force of inflation will gradually erode the value of the debt you have outstanding so that you end up effectively owing less money to the bank (or other lending institution). The £ value amount will stay the same, but the value of the money you use to pay off the debt will decline.

You’ll be paying interest to the bank to compensate them for their loss of value, but if you manage to get an interest rate lower than the inflation rate then you’ll be doing well overall. This is the case for many UK residents who took out long-term loans before the recent surge of inflation.

Inflation alone is not a reason to get yourself in debt (the banks will almost certainly have a better projection of future inflation rates than you do!), but it’s one to keep an eye on when thinking about the debt you already have.

Planning for the Future

Inflation is critically important when you’re planning for your financial future. This is most obviously the case when thinking about retirement. If you have more than a few years of working life remaining then money will almost certainly be worth less when you do come to retire.

When looking at retirement planners or pension benefits make sure you keep track of whether the numbers have been adjusted for inflation or not. If they haven’t, then keep that in mind and adjust your plans accordingly.

Many thanks to my friends at Money Marvel for an interesting and eye-opening article. Do check out the Money Marvel website for a wide range of personal finance information, advice and resources.

As always, if you have any comments or questions about this article, or the effects of inflation more generally, please leave them below.

This is a sponsored guest post.

Disclaimer: I am not a qualified financial adviser and nothing in this post should be construed as personal financial advice. You should always do your own ‘due diligence’ before investing and seek advice from a qualified professional if in any doubt how best to proceed. All investing carries a risk of loss.

If you enjoyed this post, please link to it on your own blog or social media:

Today I am pleased to bring you an expert guest post on a subject that unfortunately affects growing numbers of middle-aged and older people.

Separation and divorce can have a massive impact on your finances, so it’s important to be prepared and take advice as appropriate. Senior divorce lawyer Natalie Lester explains…

It’s always sad to see a marriage come to an end but it is particularly so when a couple have been together for 30 or 40 years. Unfortunately, divorce rates for those of retirement age are on the rise and our family law and divorce team have found a significant increase in the instructions received from those aged 55 and over.

There are several likely reasons for the increase, some of which include:

Life expectancy. People are living longer and many couples find they have grown apart by the time they get to their sixties and their children have left home. People often have many years ahead of them after they retire, and this can cause them to re-evaluate their life.

Reduced stigma. Throughout the 60s, 70s and 80s, there was a negative attitude and stigma towards divorce and divorcees. Today, we see a far more accepting attitude towards divorce in a more liberal society.

Female equality. In contrast to a few decades ago when women were far more likely to become housewives rather than pursue their own career ambitions, married women today often earn as much or even more than their husbands. Greater financial equality provides a greater sense of freedom so women of all ages are now more confident to end a marriage that has broken down.

Meeting new partners. This has become easier thanks to online dating websites and because retirees are more active in retirement., there is less fear that getting divorced will result in spending the rest of one’s life single and alone.

Menopause. This can be a particularly challenging time for couples and both partners can feel confused and concerned as they navigate the respective changes. Inevitably, it can highlight existing struggles, further damaging the connection between couples.

Divorcing and remarrying later in life typically involves added legal complexities. To address some of these, we have set out some top tips below:

Dividing assets on divorce after a long marriage

While it is always important that divorce settlements are divided fairly and in a mutually satisfactory manner, this issue is more crucial for older couples because after a long marriage, there is often a large matrimonial pot at stake. In addition, and in contrast to their younger counterparts, silver-splitters may be reliant on their pensions with no chance of acquiring new wealth through work. After a long marriage, assets are usually split 50/50.

The family home is often one of the most valuable assets in the matrimonial pot. There are various ways in which the court may decide to deal with this asset and it is important that you obtain legal advice to consider the options available. This will usually include selling the home and dividing the proceeds, transferring the property and buying the other spouse out or if there are multiple properties, one spouse retaining the home and the other spouse retaining another property. Court proceedings are a last resort and divorcing couples should take a constructive approach and consider all alternative dispute resolutions options to reach an agreement.

Like the family home, a couple’s pension is another key asset which needs to be divided up and the courts have extensive powers to deal with pensions upon divorce. One option (and the most common) is a pension sharing order. The order will state what percentage of your spouse’s pension pot you will receive. This share will be removed from the pension and placed into a pension in your sole name (some providers allow for internal pension transfers so that you can keep your pot within the same scheme). Pensions are a difficult area and you may need a pension expert to determine the real value of a pension pot and to advise on the various options. A good divorce lawyer will be able to advise on whether this is necessary.

Preparing for unforeseen circumstances

Loss of capacity. If one of you lacks capacity, then a litigation friend may be required. A litigation friend is someone who helps a “protected person” with their legal issues. This can be a parent, guardian, a family member or friend. If that is not possible, they will need to be represented by the Official Solicitor. The Official Solicitor acts for people who, because they lack mental capacity and cannot properly manage their own affairs, are unable to represent themselves and no other suitable person or agency is able or willing to act. It is important to consider who should step in as your litigation friend should you lose capacity to provide instructions to your lawyers. Your divorce cannot proceed until you have someone (other than your lawyer) acting on your behalf.

Wills. It is important to get a holding Will whilst you are going through the divorce process. If you were to die without a Will, the intestacy rules will kick-in. This would mean that your spouse would automatically inherit some or all of your estate. This is irrespective of the fact that you may be separated. A new Will should be drawn up once the divorce is finalised.

Protecting your wealth in new relationships including re-marriage

If a new relationship is on the horizon, it is important to think about getting a living together agreement drafted which will help protect your property should the new relationship fail.

Likewise, If remarriage is on the cards, a prenuptial agreement should be considered because a future marriage breakdown could significantly impact your financial position and any commitments you may have to children from a previous marriage. A lawyer specialising in succession planning will also be able to advise you on how to ringfence assets you may wish to pass to your children.

It is always wise to pay extra attention to tax planning after a long marriage. We encourage our clients to speak to an accountant, who can help with tax planning early on in the process.

While there is a lot to think about when getting divorced at a later stage in life, readers should remember that with the right advice, the process can be straightforward. Where possible, we always advise our clients to keep lines of communication open with their estranged spouse and to aim for a “good” divorce. By being open about your plans and finances, you are more likely to stay on amicable terms with your spouse which will benefit your wider family including any children, no matter how grown up they are! This will also help you to move the process along, not only saving time and money on legal fees, but also enabling you both to start what can be an exciting new chapter in your lives.

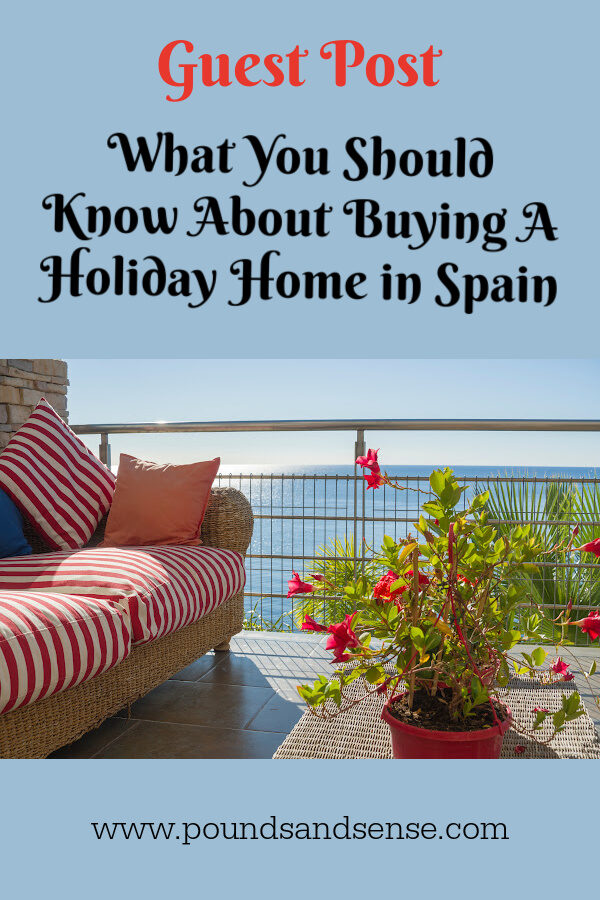

Today I have a guest post for you about something many of us in icebox Britain would no doubt love to do at the moment.

Buying a Spanish holiday home, both for your own enjoyment and as a potential investment, has many attractions. But there are various important matters to consider before signing on that dotted line.

Learn more below 🏖

If you and your partner have spent many happy years holidaying in Spain, perhaps you’d like to consider investing in a Spanish holiday home?

Not only would a stunning sun-kissed property provide a wonderful place to enjoy your retirement years, but you could also let it out while you are not there and make some additional income. After all, Spain is a highly popular vacation spot with much to recommend it, so you would certainly never be short of guests.

Whatever you would like to use your Spanish holiday property for, there are a few important things you need to be aware of before you start house-hunting on the Costa Blanca…

Many Stunning Locations To Choose From

As you surely already know if you relish a vacation in Spain, the country has a plethora of gorgeous locations to choose from. While on the one hand this is clearly a good thing, on the other, it could make deciding on a particular location rather tricky.

If you’re struggling to settle on one spot, take some time to think about your requirements for the property. For example, if you’re planning to purchase a home solely for your own use, it makes sense to choose a property in a location you particularly love. Alternatively, if you’re buying a home as an investment, you may prefer to think about the locale that draws the biggest number of visitors and has the highest rental prices.

Insurance Is Important

Insuring your Spanish holiday home is of the utmost importance, even if you won’t initially be spending a great deal of time there. After all, you never know what might go wrong – from fire and theft to flood damage or structural damage caused by extreme weather. If you don’t have cover then you could be liable for some truly hefty repair bills.

Fortunately, finding the right holiday home insurance for Spain should be a breeze, thanks to Quotezone.co.uk’s helpful comparison service. You can compare and contrast quotes from a range of UK providers and potentially save yourself a lot of time and money along the way.

You Will Need An NIE

When you buy a property in Spain as a foreigner, you will be required by law to have an NIE number. The authorities will be able to use this number to work out how much tax (if any) you owe each year.

Your NIE number can be applied for at the Spanish Consulate in your country of residence or in Spain itself. You will need to fill out forms and provide various supporting documents. The process can take anywhere between two weeks and two months.

Factor In All The Costs

Before you take the plunge and commit to buying your Spanish holiday home, it’s a good idea to dedicate some time to running through all the potential costs you are likely to incur.

After all, you won’t just be paying the asking price of the home itself. You will also have to pay various associated fees, not to mention mortgage payments, lawyers’ fees and surveyor charges.

There will also be additional annual costs, as you will have to keep the property maintained to a good standard, particularly if you’re letting it out.

To ensure a Spanish holiday home is the right choice for you and won’t prove to be too big a drain on your retirement savings, take some time to pause and reflect on the various costs involved. This will help ensure you choose the option that works best for you.

Thank you to my friends at Quotezone.co.uk for an informative article. If you have ever dreamed of owning a holiday property in Spain, I hope it will give you food for thought.

As always, please feel free to leave any comments or questions below as usual. I would be particularly interested to hear from any readers who have gone ahead and bought a property in Spain or are actively considering it.

This is a collaborative post.

If you enjoyed this post, please link to it on your own blog or social media:

Today I am pleased to bring you a guest post on a subject I freely admit I didn’t previously know much about.

Of course I was aware of Capital Gains Tax and the annual tax-free allowance. However, it transpires there is much more to know about CGT, especially surrounding the disposal of physical assets known in law as ‘chattels’. But I’ll let my guest Lilly Whale, an expert on this subject, explain in detail…

As well as freezing several tax thresholds, the Chancellor’s Autumn Statement also reduced the annual exemption amount for capital gains tax (CGT) from £12,300 this current tax year to £6,000 in 2023/2024 and to just £3,000 in 2024/2025. Any assets sold above the available threshold may be subject to CGT on the increase in the asset’s value between acquisition and disposal (disposal here means selling and gifting – of particular relevance for parents and grandparents who may wish to make gifts of long-held assets). Typically such assets could include second homes, buy-to-let properties, shares, business assets and valuable personal items such as jewellery and art.

During times of economic uncertainty, people with assets, such as a retirees, may be tempted to invest in alternative assets such as fine wine, art, classic cars and even luxury handbags – after all, the value of the much coveted Hermes Birkin bag has increased annually by approximately 14% over the last 35 years, easily outstripping returns on more traditional assets such as stocks and shares, property and even gold. As well as providing the lucky owners with considerable pleasure, these types of assets (or ‘chattels’) may have tax advantages over traditionally favoured assets, such as stocks and shares. This article focuses on the potential CGT triggers on a chattel’s sale and the potential advantages of investing in an asset of this kind.

What is a chattel?

A chattel is a legal term used to describe an asset which you can both touch and move. Many personal items are categorised as chattels, including books, fine wine, antiques, clothes, shoes, handbags, silverware, records, jewellery, art and cars. The definition also encompasses items of plant and machinery not permanently fixed to a building.

Chattels: exempt from CGT?

Disposals of chattels for £6,000 or less are exempt from CGT. Say, for instance, that you buy a piece of fine art from a little-known artist for £250. Over the next few years, that artist becomes exceptionally popular and you eventually sell the artwork for £5,000 – a realised gain of £4,750. Since the sale proceeds are less than £6,000, the chattels exemption is applicable and no CGT is due.

Sets of items

Care must be taken when a chattel forms part of a set: if the individual parts were owned at the same time and are sold either to the same person, a number of people acting together, or a number of people who are connected (e.g. family members), then the £6,000 limit will apply to the set collectively and not to the individual member of the set.

For example, many years ago you purchased four first-edition books by the same author on the same topic for £5,000 (£1,250 each). Today, the books altogether are worth £20,000 and you sell them all to a book collector.

If the limit was applied to each book’s sale price then all four disposals would be exempt from CGT because individually they are, at £5,000 apiece, under £6,000. However, in HMRC’s eyes the books would be a set and the £6,000 limit cannot apply. There would consequently be a maximum chargeable gain of £15,000 for CGT purposes.

Note that any costs relating to the sale can be deducted from this, and the annual exemption of – at least during the 2022/2023 tax year – up to £12,300, provided it has not been used against other asset sales in the same tax year. Accordingly CGT would be levied on £2,700 at either 18% or 28%.

Other exemptions

Some types of chattels qualify for CGT exemption no matter how large the sale proceeds or gain.

For instance, a private car can be sold for any price without attracting a charge to CGT – including vintage and classic cars. Further specific assets which attract no CGT on disposal are medals or decorations which, HMRC notes, were ‘awarded for valour or gallant conduct’; the seller, however, cannot have ‘acquire[d] it for money or money’s worth’. In practice this means that the seller benefits from this exemption if they were the person who was originally awarded the medal/decoration, or if they are the person to whom the medal/decoration was gifted or left as an inheritance by the individual so-awarded.

Wasting assets

Other chattels which qualify by right for CGT relief are ‘wasting assets’, i.e. assets with a predictable life of 50 years or less. Specific assets within this class range greatly and certain chattels, such as plant or machinery, will always be treated as wasting assets. Highlighted below are a few examples.

While the purchase of fine wine may provide long-term capital growth, whether it is classed as a wasting asset (and the consequent CGT ramifications) is a grey area. An everyday bottle bought from a supermarket (or as HMRC put it, ‘cheap table wine which may turn to vinegar’) would fall squarely within the wasting asset bracket, meaning that CGT on sale is not a consideration; not so, however, for port and other fortified wines with a storage life far beyond 50 years, which would not be considered a wasting asset and CGT on sale may well be relevant. But what about wines which are between these two extremities?

In short, there are several key factors which HMRC would consider when deciding if fine wine is a wasting asset or not and therefore subject to CGT on disposal. It should be noted that the 50-year time limit runs from the wine’s acquisition, not when it was first bottled: thus the drinkability in 50 years’ time of a recently purchased yet very old vintage compared with a relatively young vintage could be starkly different – one may have turned to vinegar; the other simply matured. Investors in this sphere are well-advised to keep detailed records pertaining to the wine’s condition, vintage, provenance, and so on.

Where wine is not considered a wasting asset, the seller can benefit from the £6,000 CGT exemption and therefore disposals of less than this are free from CGT. (Care should be taken if multiple wine bottles are sold at once as the above ‘set’ rules may be triggered.)

Other types of wasting assets include racehorses, shotguns, and clocks and watches (even very expensive ones, as their mechanics are deemed to have a predictable lifespan of not more than 50 years). However, this list is by no means exhaustive and a professional advisor can help to ascertain whether an investment would be considered a wasting asset or not.

There was no indication in the Autumn statement that the various chattels exemptions would be removed; yet clearly CGT thresholds and dispensations are of demonstrable importance to the Government. Now, therefore, seems an opportune moment for individuals to consider what allowances and reliefs – both for CGT and other tax purposes – may be useful and viable, and whether they can realise assets free of tax.

Lilly Whale is an associate in the private client team at RWK Goodman, the law firm.

Many thanks to Lilly Whale (pictured, right) for an informative and eye-opening article. Please do check out her company website (linked above).

As the article indicates, the special tax status of chattels can make them an attractive option for investors, especially if they have maxed out their other tax-free allowances. Passion investments, from rare books to classic cars, antique jewellery to fine art, typically fall into this category.

It is, however, essential to be aware of the rules that apply regarding CGT when the time comes to dispose of the assets in question. The same applies if you currently possess valuable assets you are planning to sell to raise funds (or indeed to give away). In either case, to minimize your tax liability and avoid any potential disputes with HMRC, it may well be advisable to speak to an experienced professional in this field.

As always, if you have any comments or questions about this article, please do leave them below.

Disclaimer: I am not a qualified financial adviser and nothing in this post should be construed as personal financial advice. You should always do your own ‘due diligence’ before investing and take professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

If you enjoyed this post, please link to it on your own blog or social media:

Today I have a guest post for you on a subject I don’t generally cover on Pounds and Sense.

Cryptocurrency investing/trading is risky and I appreciate that it may not appeal to many readers of this blog. On the other hand, I can’t deny there is a lot of interest in crypto, from younger people in particular. So today I am publishing a guest post for anyone who might be interested in finding out a bit more…

While some people prefer to invest in crypto as a side hustle, others want to take it a step further and become a full-time home-based crypto investor.

Investing time and money into crypto can be risky, so it’s important that you know what you are doing and you pay attention to how the markets change. In this article we will go over a few tips and tricks to help you get started.

Create a Working Space

One of the first things you will need to do is set up a working space for yourself. It is important that you have a designated area to work in, as this will help you stay concentrated and focused throughout the day. If you can, it would be a good idea to have your workspace away from anything else, as this will stop you from getting distracted. A spare room or even just a corner in one room of your house will work well.

Keep Updated with Crypto News

Keeping up to date with crypto news is a great way to start off as a crypto investor. The financial markets can be volatile, so you must stay current with all the latest changes so that you can make any necessary adjustments to your investments. There are plenty of ways to stay up to date, but it could be helpful to download a crypto app that will help you manage your investments and also learn about any changes to the market.

Research Ways to Earn Bitcoin

It would be beneficial for you as a home-based crypto investor to start researching ways that you can earn Bitcoin, one of the most popular types of cryptocurrency. Learning the different ways you can earn Bitcoin will help you become a successful investor. One way you can earn Bitcoin is by trading a gift card you don’t need for it. Paxful allows you to safely buy Bitcoin with a gift card, which makes earning Bitcoin super easy.

Join Crypto Communities

If you are new to the world of cryptocurrency, then a good way to get started is joining different crypto communities. There are plenty of discord servers or Reddit subs that are specifically for crypto investors, so these can be helpful to be a part of. Users share their different experiences with the crypto market and offer advice and suggestions about when and how you should invest. For someone starting out as a crypto investor this can be invaluable, as you will learn about crypto from people who have more knowledge and experience than you (though don’t take everything you read as gospel!). Having a supportive community behind you will allow you to learn and grow as a crypto investor.

Thank you to my friends at Paxful for an interesting article.

Just to emphasize what I said at the start, cryptocurrency trading is high risk and definitely not for everyone. Yes, you can make a lot of money, but you can also lose your shirt!

My personal advice if nonetheless you want to explore cryptocurrency trading/investment is to start small with money you can afford to lose in a worst-case scenario. I also like the idea mentioned in the article of earning cryptocurrency rather than buying it. Obviously if your crypto is something you have earned or otherwise acquired yourself (perhaps by exchanging a gift card), losing it isn’t likely to be as painful 😮

I would love to hear your reactions to this article, and whether you think I should cover cryptocurrency more often on Pounds and Sense. I’d also be interested to hear about your personal experiences with crypto (no spam, please). Please leave any comments or questions below as usual.

This is a collaborative post.

Disclaimer: Nothing in this article should be construed as personal financial advice. As stated in the article, cryptocurrency trading/investment can be very high risk and is not suitable for everyone. Proceed with care and take professional advice if in any doubt whether it is right for you. All investing carries a risk of loss and this is especially so with cryptocurrencies.

If you enjoyed this post, please link to it on your own blog or social media:

her public-speaking gigs and asked why she has all those ‘murder weapons’ in her bag!

her public-speaking gigs and asked why she has all those ‘murder weapons’ in her bag!