For many of us, our mortgage is our biggest monthly outgoing. So it’s important to keep a close eye on it and check regularly whether you could save money by switching to another provider.

That’s exactly what a new online service called Dashly aims to do. They evaluate your current mortgage deal against the whole market, taking into account your specific personal circumstances as well. If they find a better deal for you they let you know and – if you choose to proceed – assist you with the switching process.

How Does Dashly Work?

Dashly is available as a desktop site, with mobile apps for iOS and Android coming soon.

You start by registering and entering some details about your current mortgage and your personal circumstances. The latter is important, as things such as your income, employment type, credit score and age can all affect the deals you could be eligible for. This process takes 10-15 minutes. Dashly then compares your mortgage against an average of 10,000 products to find the best deal for you.

If they find a better deal than your present one, they send you a notification. You can then evaluate this and decide whether you want to switch. If you do, the team at Dashly will assist you with the switching process.

In addition, Dashly will continue monitoring your mortgage every month. If they find you could save money by switching again, they’ll let you know. It’s worth noting that the equity you have in your property changes on a monthly basis due to ever-changing house values and your decreasing mortgage balance. As your LTV (loan-to-value ratio) decreases, your mortgage may qualify for better, cheaper deals. Again, Dashly checks this on your behalf.

You receive a detailed personal report from Dashly about your mortgage every month. In addition, your dashboard will show you all the key facts at any time, from the changing value of your property to the amount of equity in it, any current deals that would save you money to your next payment date. It’s all there on one easy-to-read web page.

How Much Could You Save?

The savings can be substantial. Dashly say that on average their users save £2,620 (see footnote).

Of course, in practice savings will depend on a number of things, including the balance outstanding on your mortgage, the competitiveness of your current deal, the term left to run, and the effect of any early repayment penalties. Dashly takes all of these things into account in determining whether you could save money by switching to a new lender (and by how much).

Are There Any Costs?

Using Dashly is free. There are no hidden charges and Dashly say they will never hit you with advertisements or email campaigns to try to make money from you. They get paid out of mortgage provider fees, and are authorized and regulated by the Financial Conduct Authority.

Dashly are also founding members of Finance For Good, a charity run by social impact fintechs who put consumers first. They say that their security rivals that of the world’s leading banks.

In Conclusion

If you have a mortgage, in these uncertain times it’s more important than ever to ensure that you aren’t paying over the odds for it.

Dashly offers a free service that not only checks whether you are getting the best deal currently but also continues monitoring your situation month by month and recommends switching again if a new and better deal arises.

By using Dashly you could painlessly save hundreds or even thousands of pounds on the cost of your mortgage. There is never any obligation to switch or any fee to pay for the service. So you really have nothing to lose and everything to gain by registering for an account today.

Footnote: Your individual savings may vary and will depend on personal circumstances. £2,620 per year is the average amount based on research Dashly has conducted on the mortgage market. Find out more at www.dashly.com/reference-index.

Disclosure: This is a sponsored post on behalf of Dashly. If you sign up and make use of the service, I may receive a referral fee for introducing you. This will not affect in any way the service you receive or the deals you are offered.

If you enjoyed this post, please link to it on your own blog or social media:

Life insurance isn’t the most exciting of subjects, but in these uncertain times it’s something we all need to think about.

Not everyone requires life insurance. If you are single with no dependants and/or on a very low income, it may not be necessary or appropriate for you. But if you have a partner, children or other relatives who depend on your income, you probably should have life insurance to help provide for them in the event of your death.

What Is Life Insurance?

Life insurance is a type of insurance policy that protects your loved ones financially if you die. It can help minimize the financial impact that your death could have on your family and provide peace of mind for you and them.

Most life insurance policies are designed to pay a cash sum to your loved ones if you die while covered by the policy. This can help them cope with everyday money worries such as mortgage payments, household bills and childcare costs. It may also cover funeral costs. You can take out life insurance under joint or single names, and you can pay your premiums monthly or annually.

There are two main types of life insurance: term life insurance and whole of life insurance.

Term life insurance policies run for a fixed period such as 10, 20 or 25 years. These types of policy only pay out if you die during the term of the policy. A whole-of-life policy, on the other hand, pays out no matter when you die (as long as you keep up with your premium payments, of course).

There are three different types of term life insurance. With decreasing term insurance, the amount payable on death reduces over time. This type of policy is often taken out in conjunction with a mortgage as the payout reduces over time in line with the amount needed to clear the outstanding debt.

You can also get increasing term insurance, where the payout rises each year (typically to take account of inflation) and level term insurance, where it remains the same throughout. Not surprisingly, level term and (especially) increasing term policies are more expensive than decreasing term.

What Doesn’t It Cover?

Life insurance normally pays out only on death. If you become unable to work due to an accident or illness, you won’t generally be covered.

Some life insurance policies will pay out if you receive a terminal diagnosis. This is by no means always the case, though, so it’s important to check the wording of your policy carefully.

Most life insurance policies also have some exclusions, e.g. they might not pay out if you die from alcohol or drug abuse. In addition, if you take part in risky sports, you may have to pay a higher premium. If you have a serious health problem when you take out a policy, any cause of death related to that illness may be excluded.

For the above reasons, you may also want to consider taking out critical illness cover. This covers you if you get one of the medical conditions or injuries specified in the policy. Some examples of critical illnesses that might be covered include heart attack, stroke, cancer, and chronic, life-limiting conditions such as multiple sclerosis and MND. Most policies will also consider permanent disabilities as a result of injury or illness. These policies only pay out once and then the policy ends. Some policies will make a smaller payment for less severe conditions, or if one of your children contracts one of the specified conditions. Health conditions you knew you had before you took out the insurance won’t generally be covered.

What Does It Cost?

Life insurance can be surprisingly good value. Premiums start at just a few pounds a month. Prices vary a lot, however, so it’s important to shop around and take advice as appropriate.

A variety of factors may affect the price you are quoted. They include the following:

your age

your health

your weight

your occupation

your lifestyle

whether you smoke

your medical history

your family’s medical history

the length of the policy

the amount of money you want to cover

whether you want decreasing, level or increasing term cover

Other things being equal, the younger and healthier you are, the cheaper your policy is likely to be. But as the list above indicates, many other factors can affect the price you are quoted. In addition, women are typically charged a little less than men, as on average they live a few years longer.

The Bespoke Option

As you can see, while life insurance is a simple concept, in practice there are many variations. It is therefore important to establish what is the most appropriate option for you and your family, and shop around to get the best price for this.

A company that can help with both these things is Bespoke Financial. They are independent insurance and mortgage brokers, and will take the time to establish your exact requirements and design a ‘bespoke’ package to suit you and your family’s needs. Their trained advisers will visit you in your home (with all necessary Covid precautions) or you can speak on the phone to them. They can arrange all types of life insurance, critical illness cover, cover for long-term illness or disability, and so on.

To get an initial personalized quote, click through to the Life Insurance page of their website and answer six quick questions. You can then discuss this with an adviser to ensure you will be getting exactly the right type and level of cover for your needs.

And as an added bonus for readers of my blog, you can get a free will just by asking for a quotation. You can’t say fairer than that, now can you?

As always, if you have any comments or questions on this post, please do leave them below.

Disclosure: This is a sponsored post on behalf of Bespoke Financial. If you click through one of the links and end up making a purchase, i will receive a commission for introducing you. This will not affect in any way the product or service you receive.

If you enjoyed this post, please link to it on your own blog or social media:

A great number of people today need to transfer currencies, or receive transfers from abroad, for many different reasons. As globalization extends, this need has become more frequent as geographical borders become less relevant.

For example, our parents couldn’t even dream about services like eBay or Alibaba, where you can buy anything and have it delivered from a dozen countries away. And the whole thing might be cheaper than buying it in your local store!

But here is where the matter of foreign currency transfers becomes important. Paying for something abroad or getting money sent to you might not be cheap. That’s because not only do you have to pay bank fees for the transaction, you also lose money on currency exchange, which is often a mandatory step in cross-border transfers.

Luckily, today there are alternative money transfer services that allow you to cut these costs. You’ll need to look into them if you require regular foreign currency exchange (FX or forex) services.

Why You Might Need to Make Foreign Currency Transfers

One reason you might need to make a large money transfer abroad is real estate. Buying property is an important part of the retirement planning process and many Britons choose to retire abroad. For example, the latest data indicates that there are about 466,000 British pensioners living in the EU. There are even more among the 5.5 million Brits living worldwide.

Even if you don’t plan on moving or buying a vacation home on some tropical beach, you might consider investing. Investing in real estate is one of the less risky methods for growing your fortune. Of course, the coronavirus crisis has heavily affected this industry. But there are still some very promising prospects for the residential housing market.

Also, today you’ll need to make international payments when booking your holiday accommodation. So, if you plan to travel at all, you’ll need to look for cheap money transfer solutions.

Anyone involved in international business also needs to make and/or accept international payments. This also includes the simple process of buying goods through one of the many e-commerce platforms.

In addition to those reasons, if you are an expat or a traveller, you’ll need to exchange money regularly. The same goes for dealing with transfers like inheritance or even accepting dividend payments from your investments.

All in all, living in the modern world makes you exposed to foreign currency exchange and transfers in many ways. Therefore, the knowledge of how to save money on these transactions is sure to be useful.

How Much Do Foreign Currency Transfers Cost in a Bank?

The cost of an international bank wire transfer is a very complicated issue. First of all, you need to understand that banks will advertise, and sometimes even show you, only the transfer fee. In the UK those range from £8 to about £40. That doesn’t seem too bad, especially for large transfers, right?

However, the truth is that banks are deceiving customers most of the time. If they were fully transparent, you would understand that what truly matters is the FX rate margin. That’s the amount that the bank charges per currency conversion on top of the mid-market exchange rate.

Simply put, high FX margins are why you lose so much money on currency conversions. Different banks use different margins and that’s why they offer different exchange rates. But if you compare the options offered by top UK banks, you’ll see that they are all very close.

Therefore, you don’t have much of a choice.

Also, there might be additional fees involved in a cross-border money transfer. The recipient bank might charge its own fees. If there are any intermediary ‘stops’ along the way, more fees will come.

All things considered, the real cost of an international money transfer can go up to 3-10% of the transfer amount. This cost will be higher for exotic currencies and transfers to remote locations. It will go down a bit for large transfers because banks might offer better terms to VIP clients.

However, the total will always be quite high.

Leading Money Transfer Service Alternatives From the UK

With bank transfer costs so high, a necessity for an alternative emerged. The solution came in the form of FX brokers and money-transfer companies. These businesses offer services similar to banks, but they have much lower overhead costs. Therefore, they are able to keep both the margins and fees very low.

In fact, many companies charge no transfer fees at all for the majority of transactions. However, they use different margins that often depend on the transfer size. Thus, you should always compare foreign currency transfers before choosing a service. This won’t be difficult as all top companies in the industry offer free quotes. They also have transparent pricing schemes.

On average, a transfer with one of these companies will cost you 1-3% of the total. Industry leaders even offer options that allow you to cut costs below 1% for large transfers.

The most notable UK-based FX companies today are TransferWise and WorldFirst. There are other notable businesses as well. However, they cannot compete with these two giants that have multi-million funding.

TransferWise

TransferWise launched not even a decade ago and it has already become a major disruptor in the banking industry. It took over the FX money transfer industry rather fast as well. The main selling point of this company was offering not merely cheap transfers but also a fixed margin scheme.

This means that TransferWise managed to offer its customers consistency and a chance to save a great deal of money. Because of the fixed margins, its services were the most affordable in the industry. The company is now valued at over $3.5 billion and it’s expanded to many countries, including the US.

WorldFirst

WorldFirst is another veteran in the FX transfer industry. This company built a solid reputation for its reliability and trustworthiness. Launched back in 2004 literally from a basement, WorldFirst became one of the industry leaders within a few years.

In 2019 this fintech business was purchased by Ant Financial of the Alibaba Group. This allowed WorldFirst to launch a major change in pricing. It had already been one of the top companies, but it could not compete with TransferWise in affordability. However, the new pricing scheme with fixed margins that go below 0.55% makes WorldFirst a cheaper alternative even to TransferWise. At the moment, there is no cheaper option for foreign currency transfers in the UK. Also, WorldFirst has a very wide reach due to its association with Alibaba, though it’s not yet available in the US.

In Conclusion: Do Your Research for Saving Money on Foreign Currency Transfers

FX money transfer companies today offer great opportunities for money saving. However, do not forget that the lowest cost doesn’t necessarily mean the best offer. These companies have a number of requirements and additional services that you should research. For example, some have a minimum transfer limit. Others offer FX hedging tools that will be essential for reducing risks for businesses and investors.

Thus, be sure to compare all options you have available and research them thoroughly. Watch out for scammers, and choose only those businesses that have a good standing in the industry.

This is a sponsored post.

If you enjoyed this post, please link to it on your own blog or social media:

Today I’m talking about the important subject of home security.

Obviously it’s not something anyone likes to think about, but the risk of being burgled is very real. It is estimated that a burglary is committed every 40 seconds in the UK (it’s impossible to give exact figures as many such crimes aren’t reported). That means in the time it takes you to read this article, four homes are likely to have been burgled.

Of course, there are certain precautions you can take to reduce the chances of becoming a victim yourself. These include:

Keep all windows and doors locked even when you’re at home.

Keep garages and sheds locked as well, especially if they contain tools or other items that might be useful to a burglar.

Try to vary your daily routine so that burglars (who often live nearby) don’t notice and take advantage.

Avoid mentioning holiday plans too widely (especially not on Facebook or other social media).

Install timers on lights so they go on and off in a seemingly random way while you are out.

Install security lighting that will detect visitors (invited or uninvited) and illuminate them.

These and similar measures can reduce the likelihood of a burglar targeting your property. But of course, they are unlikely to be sufficient alone. You need a burglar alarm, and ideally a complete home security system. Like this one, perhaps…

Boundary Smart Security

If you’re reading this blog, chances are you have a burglar alarm already. But especially if it was fitted a few years ago, it may not be as effective as you hope.

Older alarm systems are easily defeated by determined, professional burglars. And especially if you live in a nice house and have an expensive car or other signs of wealth, you could well be targeted by such individuals. You need a modern smart security system to provide both maximum protection from burglars and the peace of mind that comes from this.

Boundary aims to provide UK residents with state-of-the-art home security at an affordable price. Their new high-tech Boundary Alarm system is based around a central hub (see cover image, above) that wirelessly connects to each Boundary device in your home and allows you to control them from anywhere using a single smartphone app. It’s a sophisticated system that can still be installed by anyone and set up easily (though optionally you can pay for professional installation if you prefer).

You can customize your alarm system as you wish with door and window sensors that detect exactly when any door or window opens in your home and set off an alarm. You can also incorporate infra-red motion detectors (wireless and pet-safe) that will detect any human movement when you’re not at home. Other features include a key tag to easily arm and disarm the system when you’re coming and going, and a 95-decibel siren (pictured below) to alert your neighbours if your home is broken into.

Plans

Boundary offer four different plans, with no long term contracts, cancellation fees or hidden costs. Full details can be viewed on the Boundary website, but briefly they are as follows…

Lite – This is the lowest cost option, with no ongoing fees. It covers two users, two sensors, the Boundary app, smart home integration and Boundary Neighbourhoods (once this service is launched). The latter is a ‘neighbourhood watch’ dashboard to allow people in local areas to connect online to share details of crime and suspicious activity. You will have the option to link your Boundary alarm so that if it goes off, your neighbours will automatically be notified.

Starter – This includes all the features above and others, including push notifications when the alarm goes off, alarm-set reminders when you leave the property, occupied home simulation (requiring smart light bulbs), and so on. This plan costs £4 a month.

Plus – This includes all the features above plus an extended three-year warranty, automated keyholder calling, partial setting (e.g. downstairs only), and more. This costs £8 a month.

Complete – This also includes police response. When the alarm goes off, a security guard at an alarm receiving centre (ARC) will be automatically notified and will immediately verify whether your home is being burgled. If confirmed, the security guard will request a police response and notify the property owner and/or nominated key holders. The complete plan also includes an annual maintenance visit by an engineer. The cost of this plan is £25 a month. Note that with this plan professional installation is mandatory.

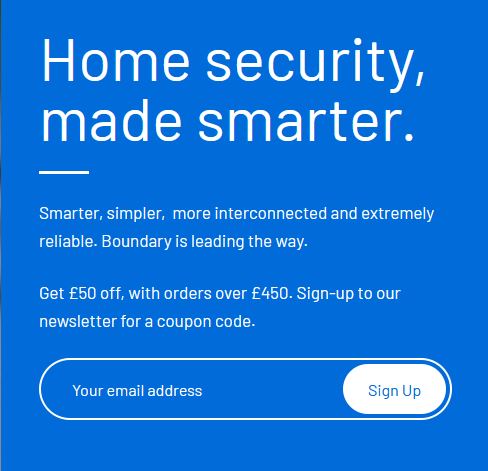

Boundary is still in pre-launch phase and right now you can get a voucher for £50 off the price of any system costing £450 or more just by signing up to their newsletter using the form on their website (screen capture below). There is of course no obligation to use this – but if you’re at all interested, I recommend signing up now to get your hands on the £50 discount code.

Self-install alarm systems are due to be sent out by the end of August, while for those who choose professional installation, the company say that currently they expect delivery and installation to take place in October.

You can ask for a no-obligation quotation via the website to get a price for a system tailored to your exact needs, with no nasty surprises further down the line. At the very least, if you think Boundary Alarm could be the answer to your home security needs, do sign up now for their email newsletter and £50 off voucher.

Note: This is a fully updated repost of my original article from April 2020.

Disclosure: This post includes my referral link, so if you click through and make a purchase, I may receive a commission for introducing you. This will not affect the price you pay or the service you receive.

If you enjoyed this post, please link to it on your own blog or social media:

Many older people find themselves asset rich but income poor. In other words, they own valuable assets such as their home but live on a modest income.

If that applies to you, equity release is an option you may want to consider, to release some of the cash locked up in your property.

There are two key requirements for doing this. The first is that you must be 55 or over (home reversion plans are only available to over 60s).

The second is that there must be equity available in your home. That means the mortgage must be paid off or the balance outstanding must be significantly lower than the house’s current value. Of course, many older people do find themselves in this situation.

There are two main types of equity release scheme, home reversion plans and lifetime mortgages. I’ll cover each of these in turn.

Home Reversion Plans

With a home reversion plan, a company buys your home but guarantees to let you and your partner (if you have one) go on living there rent-free until you die or go into long-term care.

After this the company normally sells the house and take its profit. Your beneficiaries will not receive any proceeds from the sale or benefit from any rise in the property’s value.

Note that as the company is allowing you to stay in the house until you no longer need it, you won’t receive the full market value of your property. Home reversion plan providers will usually pay you only 30 to 60% of the value of your home. How much you are offered depends on how old you are and how long the company expects you to go on living at the property.

Lifetime Mortgages

Lifetime mortgages are similar to ordinary mortgages except no repayments have to be made until the house is sold.

You receive tax-free cash to do whatever you like with. Eventually of course this will have to be repaid with interest, and the interest rates charged are typically a little higher than standard mortgage rates. However, as you retain ownership of the property until it is sold, this cost may be partly or wholly offset by the property’s rise in value.

There are two types of lifetime mortgage, lump sum and drawdown. A lump sum lifetime mortgage is a loan secured against your home, giving you access to a one-off pot of cash. A drawdown lifetime mortgage lets you draw down cash in stages after an initial lump sum, with interest only payable on the money released. A drawdown lifetime mortgage is therefore likely to work out significantly cheaper overall than a lump sum mortgage.

In either case, how much you can borrow depends on a number of factors, including your age, the value of the property and in some circumstances your health. At 67 you can typically borrow around a quarter of the value of your home, rising to around a third in your mid-70s,

If you have certain medical conditions, you may be able to borrow a higher proportion of your property’s value or obtain a better interest rate via an ‘enhanced’ plan.

Both types of equity release scheme have their attractions, but lifetime mortgages are nowadays by far the more popular option. This is because of their greater flexibility and the fact that you retain ownership of the house and can therefore benefit from any rise in its value.

Negative Equity

With both home reversion plans and lifetime mortgages, you are protected from negative equity (i.e. the risk you or your beneficiaries will end up owing more to the scheme provider than the property is worth). Provided the company is approved by the Equity Release Council (see below), any shortfall at the end will be written off.

Opting for equity release is a major decision, however, and will clearly affect how much money will be left for your children and any other beneficiaries to inherit. It’s important therefore to discuss it with them and get their views; although in the end it is of course your money and your right to do whatever you want with it.

More Points to Consider

Here are a few more things to bear in mind before opting for equity release.

Consider also downsizing to a smaller property and/or moving to a less expensive part of the country. This can be a cheaper way to release funds from your home if you don’t mind the disruption. But do this sooner rather than later, since people typically become more reluctant to move as they get older.

As mentioned above, ensure that the company you deal with is a member of the Equity Release Council. Their members must abide by a strict code of practice, and all offer a no-negative-equity guarantee.

Taking cash using equity release may affect your eligibility for means-tested benefits such as pension credit. This applies especially if you take a large lump sum, as you may then exceed the qualifying limit for benefits such as pension credit and council tax reduction. With a drawdown lifetime mortgage – where you take money in chunks as required – you may be able to remain under the capital limits and therefore qualify (or continue to qualify) for these benefits.

Leave it for as long as you can. The later you take equity release, the less costly it is likely to prove overall.

If you don’t have family or others you want to leave your wealth to, cost isn’t such an issue, though. In that case there is much to be said for taking equity release to improve your quality of life and leaving the money be repaid out of your estate when you die.

If you have bought your house on an interest-only mortgage and don’t have the money to pay it off, equity release can be a good way to repay the loan and reduce your monthly outgoings.

You don’t have to do it all in one go. Lifetime mortgages in particular are very flexible, and as mentioned with a drawdown plan you can take money in chunks when you need it and interest will only accrue on what you have withdrawn so far.

Key Equity Release

While equity release can be a great way to free up cash to help you enjoy later life, taking it is a major decision with many potential ramifications. It’s therefore very important (and indeed a regulatory requirement) to get independent professional advice before proceeding.

Key Equity Release [affiliate link] are leading equity release specialists who work with a wide range of financial service providers and provide no-obligation advice on the best options in your case.

Key Equity Release only arrange lifetime mortgages, but (as mentioned above) these are now by far the most popular option for equity release, with many advantages due to their flexibility and the fact you retain ownership of your home.

All advice from Key is free of charge, and due to the pandemic is now available in full over the phone. Key’s independent adviser will discuss your options with you, including checking that you are receiving all the state benefits you may be entitled to. They will recommend based on your needs and circumstances. For example, if you want to ensure some money remains for your descendants, however long you remain in your home, they have plans to cater for that. Equally, if your priority is getting the lowest interest rate or withdrawing the largest possible amount, they can arrange this too.

Key say that they have been able to access interest rates from as low as 2.45%, and most of their customers have received a fixed annual interest rate of 3.97% or lower.

The company also has mainly five-star reviews on Trust Pilot (average 4.9), which you can check out via this link. This is one of the highest average feedback scores I have seen on Trust Pilot.

Closing Thoughts

If you are looking for a way to release money from your property, whether to fund specific purchases or just to make later life more comfortable, equity release is definitely worth considering. The main downside is – of course – that ultimately there will be less money to pass on to your descendants. All reputable providers, however, offer a No Negative Equity Guarantee, and some such as Key Equity Release can arrange plans where a certain amount of cash is guaranteed to remain in your estate.

Equity release interest rates are at historically low levels, and in most cases are fixed for life. If equity release is right for you – and you will need to discuss this fully with an independent adviser before proceeding – now could be the ideal time to set the ball rolling. So why not get in touch with Key Equity Release today for a no-obligation discussion?

If you have any comments or queries about this article, as always, please do post them below.

Disclosure: This is a sponsored post. If you click through a link in it and arrange an equity release plan with the company in question, I may receive a commission for introducing you. This will not affect the service you receive or the terms you are offered. Please note also that I am not a registered financial adviser and nothing in this post should be construed as individual financial advice.

If you enjoyed this post, please link to it on your own blog or social media:

As you probably know, during the initial coronavirus lockdown, buying and selling property was almost impossible.

As restrictions are slowly easing, however, house buying and selling has become feasible again. Estate agents have been reporting a big upsurge in enquiries, as the long period of confinement to home has made many people more aware of the shortcomings of their current properties!

Of course, buying and selling houses while the virus remains a threat requires risks to be mitigated as much as possible. That means wearing gloves and masks when meeting agents, buyers or sellers. Following the standard hygiene rules about hand-washing and using hand sanitizers before and after any personal meetings is also vital.

The New Normal

With the need for social distancing and other precautions to reduce the risk of transmitting the virus, valuing and viewing properties has become more challenging. Most agents now offer virtual viewings – generally using a mobile phone camera – as an alternative to personal visits.

Vulnerable customers: customers that fall under the ‘vulnerable’ group as advised by the government, should let their local Yopa agent know and will then be offered a virtual valuation or viewing until there is government advice that the safety of this group is no longer a concern.

Preference: we appreciate that not everyone will want a face-to-face meeting with a Yopa agent yet – in which case, we will happily offer a virtual alternative as we have successfully throughout lockdown to date. We will keep in touch with you to understand if your preferences change as more information is issued by the government on infection rates and virus control.

Travel: we would advise our customers, where possible, to restrict travel on public transport to attend a valuation or a viewing.

Minimise contact: we ask that, at a minimum, only the buyer or seller of a property is present at a viewing or valuation – no other parties. All non-Yopa attendees should be from the same household. We would advise that we conduct viewings and valuations without the vendor present.

Distance: When meeting with a Yopa agent on a valuation or a viewing, where possible stand at a 2m distance and refrain from shaking hands.

On the property:

Gaining access: For vendors, your Yopa agent will call you when you are outside the property to gain access. For buyers, please call your Yopa agent when outside the property to gain access.

Duration: Valuation and viewing time should be kept as short as possible to minimize risk.

Air flow: we politely request that all windows and doors are opened in advance of the valuation or viewing where possible, so the Yopa agent and vendor/prospective buyer can move through the property without touching door handles or surfaces.

Refreshments: whilst very kind of our vendors to offer, we politely ask that refreshments are not offered to our agents whilst on the premises.

Documentation: as we are a digital business, no paper documentation needs to be transferred between Yopa and our customers – it can all be managed electronically.

Post valuation or viewing: if people have been shown around your current home, you should clean down surfaces, such as door handles, after each viewing with standard cleaning that products.

Yopa say that vendors conducting their own property viewings should complete these in accordance with the recommendations above.

If you are thinking of selling your home, an online agency such as Yopa is well worth considering.

They offer a full service, and say they can do anything a traditional estate agent does. They are also open at evenings and weekends.

Yopa charge a fixed fee which is agreed in advance, and never add commission. You can choose to pay when your home is sold, or up-front if you prefer.

Although Yopa are website-based, they have local agents whom they say will be with you at every step until your home is sold. You can also monitor viewings, offers and feedback any time you wish using the YopaHub online dashboard.

Finally, other services offered by Yopa include help with mortgages and conveyancing (via their commercial partners). In addition, every homeowner gets a free utilities switching service.

Final Thoughts

If you’re considering moving, it’s definitely not too soon to get started and benefit from the pent-up demand from other would-be buyers and sellers.

So why not check out the Yopa website today and see if their service could be the one to help you make your next move and find the home of your dreams 🙂

As always , if you have any comments or questions about this post, please do leave them below.

Disclosure: This is a sponsored post on behalf of Yopa. It includes affiliate links, so if you click through and end up making a purchase, I may receive a commission for introducing you. This will not affect in any way the service you receive or the price you pay.

If you enjoyed this post, please link to it on your own blog or social media:

Today I’m looking at a method for making money online I have used for many years, including (of course) on this blog.

Affiliate marketing entails promoting other people’s products and getting a proportion of the sales generated as commission.

In a way affiliate marketers are like freelance salespeople, but rather than visiting potential buyers in person, they simply have to get them to click through to their merchant partners’ websites via their affiliate links.

Why Affiliate Marketing?

For home-based entrepreneurs, affiliate marketing offers a great opportunity to make money online with a minimum of hassle. One beauty of the method is that you don’t actually have to supply the product or service you are promoting. Once you have delivered your prospect to the merchant’s sales page, the rest is up to them. You can simply sit back and await your commission!

A further benefit is that when someone clicks on your affiliate link, in many cases a tracking cookie is applied to them. These vary in duration from 24 hours to six months or more. If the prospect returns to the merchant’s website at any time during this period, as the referring affiliate you will still be credited with any commission generated.

Affiliate marketing can be great for earning a sideline income, but if you’re prepared to put a bit more work in, the returns can be substantial. Some so-called ‘superaffiliates’ allegedly make six-figure incomes this way. Of course, when first starting out your earnings are likely to be more modest than that, but there is no reason why in time you could not emulate their success.

There are lots of ways you can apply the affiliate marketing method. They include blogging, email newsletters, social media, and more. In fact, if you have any sort of online presence, the chances are you could boost your income through affiliate marketing. In this article I will look at some of the most popular (and effective) approaches. But before we get to that, let’s look at how it works in a bit more detail…

Getting Started

To become an affiliate marketer you will first need to be an online publisher. If that sounds daunting, don’t worry. It could simply mean setting up a free blog using Blogger.com, which you can do in 10 minutes or less. Or you could use social media and/or build a mailing list (all discussed in more detail below)

You can then apply to become an affiliate with one or more merchants. Affiliates are supplied by the merchants with special links and other advertising tools, and can place them on their websites. No particular technical expertise is required, just the ability to copy and paste a bit of code.

If someone visits your site and follows your affiliate link to the merchant’s site and buys something there, you will get a proportion of the money they pay as commission. Special tracking systems are used so that merchants know where customers have been referred from and pay affiliates their due.

Commissions vary widely. The biggest are typically paid in respect of downloadable products, such as e-books and software. Commissions of 50% or more are routinely paid for such products. By contrast, with physical products, where the merchant’s profit margins are typically much lower, your commission may be just a few percent. Of course, with an expensive item, even a commission of a few percent can be a significant amount.

Large companies such as Amazon run their own affiliate programmes. Many smaller companies, however, use the services of affiliate marketing platforms to run affiliate operations on their behalf. Some well-known affiliate marketing platforms include ClickBank, Commission Junction and Awin. As a publisher you can apply to join any of these platforms and will then be able to promote any of the merchants listed on them (though sometimes the merchant will need to give their approval as well).

I will now look at the platforms mentioned in a little more detail…

Affiliate Marketing Platforms

Amazon

Amazon is of course the world’s favourite online store. They sell a huge range of products, from books to clothing, cameras to garden equipment, computers to groceries.

Their affiliate programme is called Amazon Associates and any online publisher can apply to join. As long as your site looks reputable and has some relevant content, you are likely to be accepted.

Amazon does not offer especially generous commission to affiliates, currently starting at around 1% and going as high as 12% in limited cases. There are various good reasons for choosing to promote them, though. As well as the huge range of products on offer, Amazon have an excellent reputation for value and customer service. If you can get customers to the store, there is every chance they will buy something there.

A further consideration is that if a customer makes other purchases at the same time, you will also receive commission for these. In the run-up to Christmas in particular, when people often make multiple purchases, this can give your affiliate income a real boost.

ClickBank

ClickBank is an affiliate marketing platform. They list downloadable manuals and software in a wide range of categories, with commission of up to 80 percent paid by vendors. If you sign up as an affiliate with them you can immediately start promoting any of the thousands of products in their marketplace.

My top tip for new ClickBank affiliates is to focus on products with a “gravity” between 20 and 100. Gravity is a score given by ClickBank that shows how many affiliates have earned a commission by promoting that product during the last three months. Lower than 20, and it’s probably not selling very well. Over 100, and the competition from other affiliates will be intense.

Commission Junction

While ClickBank focuses solely on downloadable products, Commission Junction is an affiliate marketing platform covering a huge range of products and services. They list thousands of merchants, in categories from travel to legal services, beauty to sports and fitness.

As a publisher you start by applying to join Commission Junction. Once you have been accepted, you can then browse the merchant offers and apply to promote any that catch your eye. Some merchants automatically accept all applications, but others like to approve affiliates themselves. This normally only takes a day or two.

Commission rates on CJ vary considerably, but they are clearly set out on the site. Once you have been approved, you will be able to download affiliate links and advertising banners for the merchant in question. You will be able to monitor sales by logging in to your CJ account. Payments are then made monthly by direct transfer to your bank account.

Awin

Awin has lots of well-known consumer brands on board, and is a very popular platform among UK bloggers. It operates in a similar way to Commission Junction (see above). You have to pay a small fee (£5) to register as an affiliate with them, but this is refunded once you have earned enough commission to qualify for your first payout.

Blogging

In my view one of the best ways to make money from affiliate marketing is through blogging. If you don’t have a blog already, you can easily set one up at Blogger.com, the free blogging platform run by Google. Ideally, though, I recommend setting up your blog using a self-hosted WordPress platform (like Pounds and Sense). There is more of a learning curve with WordPress, but you have the freedom to configure your blog exactly as you want it.

The best type of blog for this purpose is a niche blog – that is to say, a blog devoted to a particular interest or activity. That could be anything from gardening to fishing, photography to computers. You can then write about this subject on your blog and include affiliate links to relevant products and services.

One of the best ways of doing this is by publishing reviews, with affiliate links to the product (or service) concerned. If a reader is inspired to buy after reading your blog review, as long as he/she visits the merchant’s site via your link, you will receive a commission.

Of course, if you’re going to do this, you will need to give a balanced review of whatever you are promoting. Emphasize its good qualities, certainly, but don’t be afraid to mention any shortcomings as well. Readers will be more inclined to believe you – and trust you in future – than if you simply hype any product you are selling to the skies.

Another tactic that can work well is to offer a free, downloadable bonus to anyone buying via your link. This can be especially effective with business opportunities and software products. You could offer a complementary product such as a user guide or case study. Ask people to email you a copy of their receipt and send them your bonus in the same way.

Naturally, for this type of marketing to work, you will need to attract a steady stream of interested visitors to your blog. A full discussion of how to do this is outside the scope of this post, but there is of course plenty of free information on this subject online (see also Taking It Further, below).

List Marketing

Affiliate marketing also works extremely well in conjunction with running a mailing list or online newsletter. If you have a list of people interested in a specific topic, you can email them with a series of affiliate offers relevant to their interest, and potentially make multiple sales to the same buyers.

Running a niche blog, as mentioned above, gives you a great opportunity to start building a list. All you need do is add a sign-up box on the front of your blog.

One thing I strongly recommend, though, is opening an account with a mailing list management service such as GetResponse or Aweber. These services handle subscribe and unsubscribe requests automatically, together with changes of email address. They also ensure that any would-be subscriber must click on a link in a confirmation email before being added. This ‘double opt-in’ method ensures you have proof they did actually subscribe to your list if any accusations to the contrary are made later.

There are many other benefits to using a mailing list service. For example, most such services will monitor how many people are opening your messages, and even let you selectively remail those who didn’t read them first time round.

As with affiliate reviews, another good tactic is to offer potential subscribers a ‘bribe’ for signing up. A short report or e-book could be a suitable choice. Choose a downloadable bonus if at all possible, as the process of getting it to your subscriber can then be automated.

Social Media

You can also promote affiliate offers through social media such as Facebook, Twitter and Instagram.

A word of warning is in order, however. The social media platforms all have their own rules about affiliate marketing and what they will and won’t allow. That means affiliate links may be frowned upon and in some cases banned. There are ways around this, e.g. you can convert your affiliate link using a link-shortening service such as the free tinyurl.com. This may work, but it’s not guaranteed! There are also rules to follow about disclosing promotional posts and/or affiliate links (see below).

A better method, in my opinion, is to use social media to help drive traffic to your blog posts, where your money-making affiliate links are located. Another option is to create a dedicated landing page which is designed to get visitors to click on your link (you could also use your landing page to sign people up for your newsletter). You will need your own blog or website to host a landing page, but you can also get basic landing pages for free if you join an autoresponder service such as Aweber.

Once you have a landing page, you can link to it from Facebook or other social media with no fear of being blocked or banned.

Affiliate Disclosure

In the UK (and most other countries) there is a legal requirement to make clear that you are using affiliate links for marketing purposes. This is to avoid consumers being misled.

In the UK this area is overseen by the Advertising Standards Authority (ASA). They publish guidelines which do not in themselves have the force of law but are based on the relevant laws.The guidelines are not always as clear or specific as one might like, but a guidance document relating to ‘influencers’ (which includes bloggers and social media personalities) can be downloaded here.

The main point made in the ASA guidelines is that it should always be clear to a visitor to your website (or whatever) when they are reading an advertisement or clicking on an affiliate link. There are no hard and fast rules about how exactly this must be done, so different people take different views. Personally with Pounds and Sense I have a general Affiliate Disclosure page, and also include a separate disclosure paragraph in any post with affiliate links or other commercial associations. At the start of each post it will also say if it is (for example) a sponsored post. I have never encountered any problems using this approach, but obviously it is something everyone needs to decide for themselves based on the guidelines.

If you also use email marketing, you can (and almost certainly should) include a note near the end of every email such as, ‘The sender of this email has an affiliate relationship with the authors of the products mentioned and may receive compensation from them in the event of a purchase.’

More Top Tips

Here are a few more tips for maximizing your income from affiliate marketing…

Promote products you can genuinely recommend, preferably because you’ve used them yourself, or at least based on solid evidence.

Talk about what you like and don’t like. Be honest with your readers and build trust. People are far more likely to buy things you recommend if they have learned to trust you in the past.

Take any opportunity to promote products in passing, as well as in dedicated posts. For example, in a gardening blog, if you’re talking about a particular plant species, you might mention in passing a supplier from whom you have received good specimens in the past. Low-key recommendations such as this can be surprisingly effective for generating sales.

Don’t put all your eggs in one basket. Promote multiple affiliate products. Better yet, diversify across all income streams. In other words, use affiliate marketing, but also use other forms of income generation such as selling your own product, offering a service, or selling advertising space on your blog.

Although most affiliate offers involve a payment per sale, in some cases merchants will pay for other outcomes, e.g. a quotation request (for insurance perhaps). As you gain experience it is worth looking out for such offers to promote, as they can be very lucrative. The same goes for recurring subscriptions.

Create a ‘Tools I Use’ or ‘Things I Love’ page on your blog. Many readers will enjoy seeing a handy list of your favourites, plus it’s an easy way to promote some affiliate links.

Taking It Further

Once you have made your first few commissions from affiliate marketing, the chances are you will want to take it further to increase your earnings from it.

Key to this is driving more potential buyers to your website. I have provided some tips above, but if you want to boost your income to the next level, you might want to consider engaging an SEO (search engine optimization) company – like my friends at the UK-based Lojix, perhaps.

Lojix are a digital marketing agency offering affordable SEO, pay-per-click advertising management, PR, marketing and website design services. They say they will work with you to increase the number of leads that you get from your website, whether that is an increase in orders from an e-commerce site or an increase in sales leads for businesses that are service providers. They say they work with businesses that require just a local presence right up to companies that trade all over the world. I asked my colleagues at Lojix what were their top tips for boosting your income from affiliate marketing, and they came up with the following:

1. Don’t be lazy by copying and pasting descriptions of products you want to promote. If your marketing strategy involves getting organic visits – which should be top of your list – Google is likely to ignore your content if you do this and won’t rank your site high in their search results at all.

2. If you are just starting out with your site or blog you should probably go down the niche route, as trying to get organic visits from Google for popular products will be difficult.

I definitely agree with both these points. There is much to be said for researching search terms and targeting those that have reasonable traffic but not so much competition that it’s hard (or impossible) to compete. A reputable, professional SEO agency such as Lojix can assist with this. If you think they might be able to help you – without any obligation – please do drop them a line.

Closing Thoughts

Affiliate marketing is a great way to make money online, with a minimum of hassle and expense. It is therefore ideally suited to home-based entrepreneurs. The method can be applied in many different ways, though blogging and email marketing are especially effective.

It has a further advantage in that once you have published, say, a product review on your blog, it will remain there indefinitely, potentially generating further affiliate fees for you over a long period. One review I wrote some years ago on my former freelance writing blog (for a self-development product) made me well over £3,000 in total.

Obviously, not all of your affiliate promotions are likely to prove as profitable as this, but the beauty of affiliate marketing is that you can promote almost anything you like. If one offer doesn’t perform as well as you hoped, there is always something else you can try.

Good luck, and I hope you make lots of money from affiliate marketing!

As always, if you have any comments or questions about this article, please do post them below.

Disclosure: This is a sponsored post on behalf of Lojix.

If you enjoyed this post, please link to it on your own blog or social media:

With Britain in near-lockdown at the moment, and many jobs and businesses under threat, big energy bills are the last thing any of us want to worry about right now.

So Dorset-based energy supplier Utility Point has come up with an innovative solution. Their new UP Support tariff credits customers with half (yes, half!) of the cost of their gas and electricity bills for their first three months on the tariff.

It’s a fixed tariff, so customers have the added reassurance of knowing that prices won’t increase through till next winter and beyond.

The UP Support tariff is open to everyone, though it may appeal especially to those who are seeing their income reduce but energy usage increase while self-isolating or working from home. It’s available now to both new and existing Utility Point customers. You can sign up on the Utility Point website, where further information is also available.

About Utility Point

Based in Poole, Dorset, Utility Point is one of the UK’s fastest growing domestic energy suppliers. Founded in 2018, the company has already grown to over 100 employees, and more than 245,000 customers.

They say their mission is to increase energy efficiency, provide a dedicated, personalized service and work together with customers to save money. These values have brought the company not only commercial success but also widespread public recognition. In March 2020, Utility Point was named in the prestigious Sunday Times Top 100 Small Companies to Work For list, the Top 75 Companies to Work For in the South West list, and awarded the highest available three-star Best Companies rating. The company is co-owned by Ben Bolt and Simon Yarwood.

My Thoughts

Right now money is a major worry for many people. And the next two or three months will be critical, with the lockdown (presumably) continuing and many people waiting for furlough payments and government aid to come through. So halving your energy bills for three months should help considerably, along with the added reassurance of knowing that your tariff won’t rise for at least a year.

In addition, though, it’s clearly important that the tariff itself is competitive once the three-month initial period is over. Utility Point say that their average price for a non-Economy-Seven dual-fuel customer is £76.60 per month, based on a typical medium user (3100 kWhs electricity and 12000 kWhs gas). That looks pretty competitive to me. But of course you can request a free quote on the Utility Point website and compare this with your current supplier, and I would strongly recommend doing this.

I also like the fact that Utility Point has a strong customer-service ethos, and that despite only launching in 2018 it has already earned a reputation as an excellent company to work for.

Finally, it’s worth mentioning that all Utility Point customers automatically get access to a free benefits programme called Utility Point Rewards. The programme includes a range of special offers, including significant discounts (up to 20%) at a host of high street stores, restaurants and websites. These include such big names as Sainsbury’s, Boots, Asda, Wilko, Halfords, Samsung, and more. The savings you can make from this over a year could be substantial, in addition to the money you will be saving on your energy bills.

As always, if you have any comments or questions about this post, please do leave them below.

Disclosure: This is a sponsored post on behalf of Utility Point.

If you enjoyed this post, please link to it on your own blog or social media:

Today I’m spotlighting a pension advisory service called AdviceBridge that may be of interest to any Pounds and Sense readers who are planning for their retirement.

There is no doubt that in recent years retirement planning has become more challenging. The pension reforms introduced by George Osborne in 2015 gave people much more freedom over how and when they can access their retirement savings. There are many benefits to those reforms – and I’m a fan of them myself – but it does mean most people now have big decisions to make over how to finance their retirement.

A further factor is the decline of ‘defined benefit’ pensions. These guaranteed a certain pension usually based on how long you had worked for an employer and how much you earned during your career. The great majority of working age people nowadays have ‘defined contribution’ pensions, where you build up a pension pot over the course of your working life. This then provides you with an income (alongside the state pension and any other investments) when you retire. Anyone with a pension of this type will have important choices to make over how, when and where to save for their pension, and what to do with it once they reach retirement age. Many people who are not financial services professionals understandably struggle with this and need some expert help (I did myself).

Getting professional financial advice can be expensive – typically pension advisers in the UK charge £2,000-£3,000 up front and then 0.5% a year. But a new service called AdviceBridge promises a personalized, affordable retirement planning service. Indeed, they say they can do this for as little as a tenth of the average adviser fee, partly by running the service online and over the phone (no face-to-face meetings required).

Although it is a low-cost service, AdviceBridge is staffed by fully trained and regulated financial advisers, and the company is authorized and regulated by the Financial Conduct Authority (FCA). AdviceBridge never holds investors’ money, even when they assist in the implementation of a retirement plan. The advice they give is though covered by the Financial Services Compensation Scheme (FSCS), which means clients can claim compensation of up to £85,000 if they receive bad advice.

Who Is AdviceBridge For?

In order to keep their charges low, AdviceBridge say that at the moment they are only able to help clients who meet the following criteria:

You are resident and domiciled in the UK.

You are generally in good health.

You do not have any unsecured loans.

You are not currently contributing to pensions with safeguarded benefits such as a final salary pension.

You do not own any buy-to-let property or any non-standard investments.

You do not receive any means-tested benefits.

You would like to plan individually, not as a couple.

How Does It Work?

Assuming you meet the criteria above, you start by filling in an online questionnaire and completing some electronically-signed compliance documents.

As well as the usual contact information, the questionnaire covers such matters as:

your age

your employment status

your annual income

any existing private or company pensions

whether you will qualify for a full state pension

other savings and investments

your target retirement age

how much income you hope to have in retirement

any major outgoings in future you need to plan for

and so on

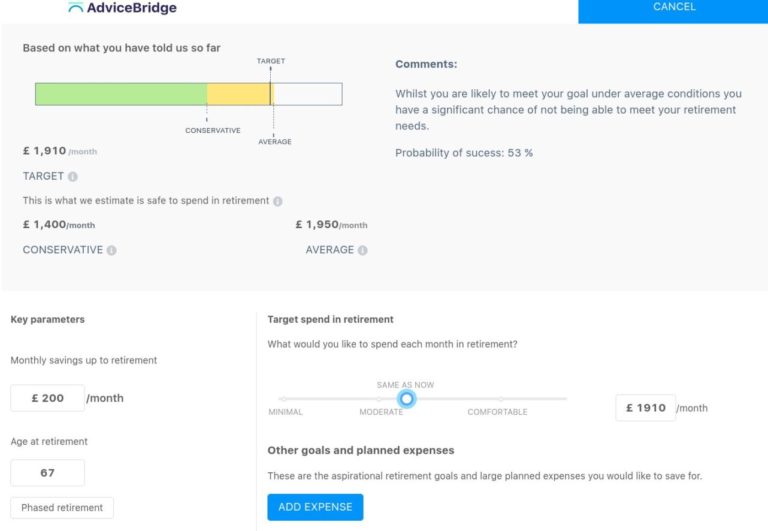

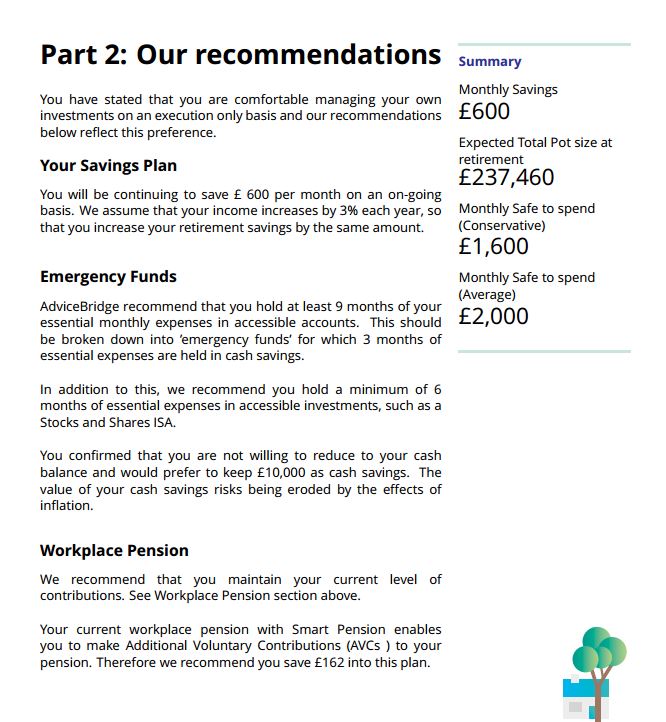

Once you have entered this information, you can create and log in to your account to see an overview of your financial situation. You can adjust the parameters in order to achieve a realistic and sustainable level of retirement income. Here is a screen capture showing part of this (an example account, not mine personally!).

Personalized Plan

Naturally, the above is just the first stage of the process. Once you have provided this information and set up your account, the AdviceBridge advisers will crunch the numbers and (with the aid of their specialist software) produce a personalized plan for you.

This is obviously a key document. The sample plan I saw came to 39 pages in PDF form. It was divided into three sections: About You, Our Recommendations and Advice, and Appendices.

About You sums up the information you have provided to AdviceBridge via the questionnaire. It covers your personal circumstances, your retirement savings and investments, and your progress so far towards achieving your retirement goals.

Our Recommendations and Advice is the longest section of the plan. It presents recommendations on every aspect of managing your finances for retirement, including restructuring your investment portfolio if required (with specific recommendations for low-cost personal pensions and ISAs). It also examines the likely outcome of following the recommendations, including both average and conservative projections. A sample page from this section of the plan is shown below.

Finally, the Appendices section includes a range of supplementary information, including more detail about the UK state pension, rules about annual pension allowances and taxation, your options for accessing your pension (drawdown, annuities, etc), and more.

It doesn’t end there, though. Once you have had a chance to read and digest your plan, you can arrange a call with a personal financial adviser from AdviceBridge to talk through the advice and recommendations and help you decide how to proceed. The advisers are not paid commission on product sales, so they are able to give unbiased advice about what investments may be best for you based on your specific circumstances.

So What Does It Cost?

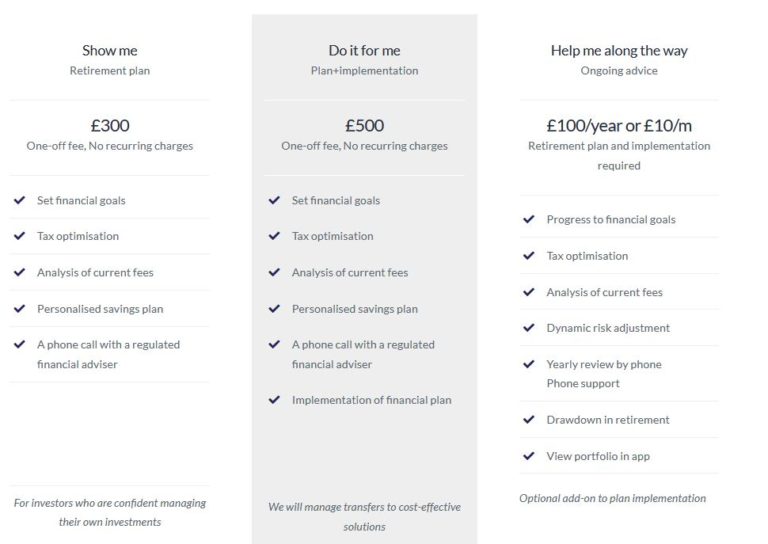

For the basic AdviceBridge service as described above, there is a one-off fee of £300 with no recurring charges. This service will suit people who are happy to arrange their own investments based on the advice given and the telephone call with an adviser.

If you want AdviceBridge to set up the recommended investments for you – to implement your financial plan, in other words – they will do this as well for an inclusive fee of £500, again with no recurring charges.

Finally, if you opt for the Plan+Implementation service and want ongoing support and assistance too, including dynamic risk adjustment, an annual telephone review, ongoing telephone support, assistance putting your pension into drawdown, and the opportunity to monitor your portfolio online using a dedicated app, AdviceBridge offer all this for an additional £100 a year or £10 a month.

All of the above is summed up in the table below which I have copied from the AdviceBridge website.

My Thoughts

Overall, I have been very impressed by AdviceBridge, both in terms of what they are offering and the prompt and friendly support they provided while I was writing this article. Here are some of the main things I like about their service:

much lower fees than traditional financial advisers

all fees quoted include any taxes due – what you see is what you pay

range of options according to how much (or little) work you want to take on yourself

non-commission-based advisers, so unbiased advice on what investments will suit you best

advisers are free to recommend across the entire range of investment opportunities

all digital process – no need for personal visits or face-to-face meetings

fully FCA authorized company and advisers

advice is covered up to £85,000 under the Financial Services Compensation Scheme (FSCS)

all personal information is securely encrypted

in-depth written advice and recommendations on your retirement finances backed up by telephone support

Any negatives? Well, the only real one I could find is that various groups are currently excluded from the service, e.g. buy-to-let landlords and holders of ‘non-standard investments’. I guess the latter might include me, as I have a proportion of my portfolio in P2P lending and property crowdfunding.

I do of course appreciate that to keep their service so inexpensive AdviceBridge have to streamline their service, but it is a pity if this excludes a significant proportion of people who could benefit from it. I understand that this is something that AdviceBridge keep under review and in future they may remove some of these restrictions. In the mean time, if you aren’t sure whether you are eligible, it is well worth giving them a ring or contacting them via the website to ask (without obligation).

In my opinion, if your circumstances match their criteria, AdviceBridge are well worth checking out. I particularly like their £500 Plan+Implementation service, which covers not only researching and producing a retirement plan for you but implementing it as well. I would also seriously consider paying the extra £100 a year (or £10 a month) for the ongoing service. Obviously that brings the price up a bit further, but it is still far less than you would pay a traditional financial adviser for a similar service.

As always, if you have any comments or questions about this post, please do leave them below.

Disclaimer: This is a sponsored post for which I am receiving a fixed fee (but no commission). Please note also that I am not a professional financial adviser and nothing in this post should be construed as individual financial advice. Everyone should do their own ‘due diligence’ before investing and take professional advice as appropriate. All investment carries a risk of loss.

If you enjoyed this post, please link to it on your own blog or social media:

With Christmas almost upon us, I thought I’d take a look today at how the cost of Christmas has changed over the years. I’ll also be suggesting some things you can do to keep the cost of the festive season under control.

Of course, Christmas has always been relatively expensive, as it’s one time of year nearly all of us push the boat out, buying gifts for friends and family, and generally spending more on food and drink and entertainment.

But all the usual bills still have to be paid at this time, including gas and electricity. For those of us in the UK, our energy use rises during the cold winter months anyway. And that effect is magnified over Christmas, when we may have extra guests visiting (and perhaps staying) as well. This all adds to our bills, and hence the total cost of Christmas.

The Cost of Christmas Past

So how much is your energy actually costing you, and are you paying more than you did ten or twenty years ago?

Take a look at the interacfive house graphic below – kindly provided by my friends at Energyhelpline.com – to see how average energy bills (along with our tastes in home decor and TV viewing!) have changed between 1970 and today.

As you can see from the graphic, average energy bills have fluctuated over the years, with the 1980s in particular being surprisingly expensive. In recent years the trend has been broadly upwards again, though this has been countered to some extent by the arrival of more energy-efficient appliances, from LED bulbs to condensing boilers.

Nonetheless, Christmas today is a very expensive time for many people. One reason is – of course – inflation. The cost of everything has risen over the years, so it makes sense that Christmas is all the more pricey too. But inflation aside, for many people today Christmas is a much bigger (and costlier) affair than it used to be.

Christmas in the 1960s wasn’t the long drawn out holiday we know now. As many readers of this blog will remember, most people only celebrated on the day itself, with Christmas Eve used for buying any gifts or food needed (unheard of today) and Boxing Day spent visiting family. With only two TV channels to choose from – BBC and ITV – everyone watched the same things, so there was no squabbling between Doctor Who and Die Hard!

The 1970s wasn’t much better on the TV channel front (the Christmas movie was a big highlight in the days before streaming and rentals) – though it did see a big surge in how much we spend on presents, with toys like Action Man and Evel Knievel making their debut during this period.

The 1980s saw an even bigger increase in the amount the UK would spend over the season, though you were more likely to sip a Babycham or eggnog in the days before you could get decent wine inexpensively. Wham’s ‘Last Christmas’ was the biggest festive hit. And the whole family would probably sit down together to watch Noel Edmonds on Christmas morning (hard to imagine in today’s multichannel, multimedia world).

The commercialization of Christmas took a new leap in the ‘90s, with toys like the Tamagotchi, Furby and Game Boy being huge sellers across the decade. Christmas TV might include Mr Bean, The Muppets Christmas Carol or even The Simpsons. It was also probably the last decade where the Christmas Number One was truly important – the Spice Girls dominating with three in a row.

Since then, the cost of Christmas has gone on increasing, as we spend ever more on gifts, decorations and events. And Christmas itself has spread ever wider as well, with festivities beginning weeks before the big day and continuing on into early January.

How to Keep Costs Down at Christmas

With the cost of Christmas (for many at least) having climbed alarmingly, here are some tips and suggestions for keeping your costs – and especially energy bills – down at this time.

Have your boiler serviced regularly, to ensure it is operating at peak efficiency.

If you have an old boiler that keeps breaking down, the time may have come to replace it. The Energy Saving Trust say that you could save up to up to 40 percent on your gas bill by installing a new ‘A’ rated condensing boiler with a programmer, room thermostat and thermostatic radiator controls.

If your radiators aren’t heating up properly at the top, you may need to bleed them to release air in the pipes. Depending on the radiator, you may need a special key to do this or a flat-bladed screwdriver.

Turn down your thermostat by one degree - this can reduce your heating bill by 10%.

Replace old light-bulbs with new energy-saving bulbs. The latest LED bulbs are just as bright as old incandescent bulbs and use a tenth of the energy. They last longer too.

Exclude draughts with heavy curtains and draught excluders by doors.

Turn off heaters in rooms you aren’t using and close the doors.

Don’t leave electrical appliances on standby.

Wash clothes at 30 degrees (or lower) and avoid using tumble driers whenever possible.

Get a smart meter installed if you haven’t already. The energy companies are fitting these free. They can help you see when and where you are spending money on energy and identify ways you could save money as a result.

If you’re an older person and/or on a low income, you may be able to get a discount of £140 on your winter energy bills through the Warm Home Discount scheme. The scheme for 2019/20 is currently open for applications, and most larger energy suppliers are offering it. But be aware that they only have a limited quota of discounts to give out, so you need to apply asap before applications close. My blog post about the Warm Home Discount scheme has more information about this.

Most older people who receive the state pension should get a Winter Fuel Payment from £100 to £300 in cash, based on their age and circumstances. Those in receipt of Pension Credit and some others on low incomes may also be eligible for a Cold Weather Payment of £25 if the average temperature in their area is at or below zero for seven days consecutively during the winter months.

Last but not least, the energy market is more competitive than ever these days, meaning you should be able to find a better deal pretty easily by shopping around. Energy Helpline can help you save up to £461 on your annual bills. Simply enter details of your current supplier on their website and they will handle the entire switching process for you. It’s that easy!

Christmas Prize Quiz

Here’s one more way you may be able to save some money this Christmas. Energy Helpline are currently running a Christmas-themed prize quiz on their website. Just click through here and scroll down to the quiz, where you can put your Christmas knowledge to the test! One lucky person will win a £100 M&S voucher. But don’t delay, as the winner will be drawn on Monday 23rd December 2019.

As always, if you have any comments or questions about this article, please do post them below.

Disclosure: this post is sponsored by Energy Helpline, an independent price comparison website.

If you enjoyed this post, please link to it on your own blog or social media: