If you work in the NHS, emergency services, or other frontline roles, you may be eligible for one of the UK’s most generous discount schemes: the Blue Light Card.

This little-known but highly valuable scheme offers access to thousands of discounts on everyday spending – and for many people, it can easily pay for itself many times over.

In this article, I’ll explain how the Blue Light Card works, who can apply, and how you can make the most of it.

What Is the Blue Light Card?

The Blue Light Card is a UK-wide discount scheme designed to recognize the contribution of people working in public service and frontline roles.

Members get access to over 15,000 discounts with retailers, restaurants, travel providers and more, both online and on the high street.

The scheme covers a wide range of spending categories, including:

Supermarkets and everyday shopping

Fashion and retail

Holidays and travel

Eating out and takeaways

Utilities, mobile, and insurance

In short, it’s a broad-based money-saving tool rather than a niche perk.

Who Is Eligible?

Despite the name, the Blue Light Card isn’t just for police or ambulance staff. Eligibility has expanded significantly in recent years.

You can typically apply if you are working, volunteering, or even retired from sectors such as:

NHS and healthcare

Emergency services (police, fire, ambulance)

Social care

Armed forces and veterans

Teaching and education staff

Certain volunteer organisations

This wide eligibility means millions of people across the UK now qualify.

Blue Light Card for Retired People – What You Need to Know

One aspect of the scheme that is especially relevant to many Pounds and Sense readers is that eligibility doesn’t necessarily end when you retire.

In fact, the scheme has been extended in recent years to include many retired workers from eligible sectors, allowing them to continue enjoying discounts even after leaving the workforce.

Who Qualifies in Retirement?

Retired eligibility covers a broad range of professions, including:

NHS staff

Police, fire and ambulance personnel

Armed forces veterans

Teachers and social care workers

So if you spent your career in public service, there’s a good chance you can still apply.

How Retired Eligibility Works

The main difference for retirees is how eligibility is verified.

Instead of a current work email or payslip, you’ll usually need to provide evidence of your former employment and/or pension. Examples include:

Pension documents (e.g. NHS or service pension statements)

P60s showing pension income

Certificates of service or employment history

Official letters confirming your role and dates of employment

The process can be slightly more involved than for current employees, but it is still very manageable.

Important Points to Be Aware Of

Documentation is key – applications may be rejected if proof isn’t clear

Requirements can vary depending on your former profession

Some roles may require minimum service periods

It’s worth taking a little care when applying to avoid delays.

What Discounts Can Retirees Expect?

Retired members receive exactly the same discounts as working members.

These can help reduce the cost of:

Travel and holidays

Dining out and entertainment

Home and garden purchases

Everyday shopping

For retirees on fixed incomes, this can be particularly valuable.

Is It Worth It for Retirees?

For many retired readers, the answer is a clear yes.

With a very modest upfront cost (see below) and potentially wide-ranging savings, the scheme offers a simple way to:

Offset rising living costs

Make pension income stretch further

Enjoy more affordable leisure activities

As always, the key is to use it regularly rather than letting it sit unused.

How Much Does It Cost?

One of the most appealing aspects of the scheme is its low cost.

£4.99 for two years’ membership

That’s less than £2.50 a year – meaning you only need to save a few pounds to break even. In practice, many members save far more than this over the course of a year.

The price for retired people is exactly the same as for those who are still working. There is no discounted or premium pricing tier for retirees, and they get exactly the same discounts and benefits as well. Note that there is a separate sign-up page for retired people in eligible occupations.

Verify your employment (or past employment, if retired)

Pay the small membership fee

Start accessing discounts via the website or app

Once approved, you can use either a physical card or a digital version on your phone.

What Kind of Discounts Are Available?

The range of offers is one of the scheme’s biggest strengths.

Typical deals include:

Percentage discounts (e.g. 10–20% off)

Cashback or gift card savings

Special promotions and limited-time offers

Discounted tickets and experiences

These can apply to both everyday essentials and occasional treats – helping stretch your budget further.

Pros and Cons

Advantages

Very low cost for two years

Huge range of discounts across everyday spending

Available to a wide range of professions, including retirees

Easy to use via app or card

Potential Drawbacks

Discounts vary and aren’t guaranteed at all retailers

Some offers may overlap with general promotions

You need to use it regularly to get full value

Is It Worth It?

For most eligible people – including retirees – the answer is yes.

Because the membership fee is so low, even modest use can justify the cost. If you regularly shop online, eat out, or book travel, the savings can quickly add up.

That said, it’s important to use the card sensibly. It should help you save money on things you would buy anyway, not encourage extra spending.

Final Thoughts

The Blue Light Card is a simple but effective way for frontline workers, public servants, and retirees from these sectors to reduce everyday costs.

At a time when many households are feeling the squeeze, it’s a useful reminder that small savings opportunities can make a real difference over time.

If you think you might be eligible – whether still working or now retired – it’s well worth checking. This could be one of the easiest wins in your personal finance toolkit.

As always, if you have any comments or questions about this article, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

As of 6 April 2026, UK investors have a fresh chance to supercharge their savings and investments with a new £20,000 Individual Savings Account (ISA) allowance.

To maximize the benefits of the new 2026/27 allowance, there’s a strong case for acting swiftly and using at least part of your £20,000 ISA allowance sooner rather than later. This is due to the power of compounding. By investing early, you give your money more time to grow, benefiting from the potential snowball effect of returns generating further returns. So the sooner you invest that £20,000 (assuming you are fortunate enough to have it) the more opportunity it has to multiply over time.

In addition to the tax-free ISA allowance remaining at a relatively generous £20,000 (for now – see below), the rules surrounding ISAs have undergone a welcome relaxation in recent years. One of the most significant changes is the ability to open more than one ISA of the same type (e.g. a stocks and shares ISA) with different providers in the same tax year. This means investors are no longer limited to a single provider for each type of ISA, giving them greater flexibility and choice in managing their investments.

Previously, investors were restricted to opening one cash ISA, one stocks and shares ISA and one innovative finance ISA (IFISA) per tax year. This restriction could prove frustrating for those seeking to diversify their investments or take advantage of new opportunities as the tax year progressed. Now, with the freedom to open multiple ISAs of the same type, investors can shop around for the best rates, terms and investment options without being limited to a single provider for each ISA type. They can also move some or all of their money from one provider to another without jeopardizing its tax-free status.

It’s important to remember, however, that while the rules have been relaxed, the overall annual ISA allowance remains fixed at £20,000. This means that any contributions made across multiple ISAs of any type will count towards your total allowance for the tax year. You should still therefore take care not to exceed the annual limit, to avoid any potential tax charges.

Note that from April 2027 the Cash ISA allowance has been reduced from £20,000 to £12,000 per year for savers under the age of 65. Until then it remains at £20,000 a year for all savers, though.

Cash ISAs offer a secure and accessible way to save, providing a tax-free environment for your savings with the added benefit of easy access to your funds when needed. Meanwhile, stocks and shares ISAs open the door to potential higher returns by investing in a wide range of assets such as equities, bonds, and funds, albeit with a higher level of risk. With a stocks and shares ISA you will never incur any liability for dividend tax, capital gains tax or income tax, even if your investments perform exceptionally well. Of course, there is no guarantee this will happen, but over a longer period stock market investments have typically outperformed cash savings, often by a substantial margin. IFISAs (e.g. from Housemartin, with whom I invest myself) allow you to invest is property crowdfunding and other forms of peer-to-peer finance. They are more specialized, but may appeal to some investors looking to further diversify their portfolios.

In recent years I have invested much of my own annual ISA allowance in a stocks and shares ISA with JP Morgan Personal Investing (previously Nutmeg), a robo-manager platform that has produced good returns for me. You can read how my Housemartin and JPM investments (and others) are faring in my monthly investment updates such as this one.

Closing Thoughts

The start of a new financial year is a good time for UK investors to review their savings and investment strategies. Whether you’re looking to start a new ISA or maximize your contributions to existing accounts, taking action early can set you on the path to optimizing your returns from this important tax-saving opportunity.

By investing sooner rather than later and taking advantage of the increased flexibility in ISA provider options, savers and investors can make the most of their money while minimizing their tax liabilities. So grasp this opportunity to build your wealth and protect it from the taxman today!

As always, if you have any comments or questions about this post, please do leave them below.

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

If you enjoyed this post, please link to it on your own blog or social media:

Volatile investment markets can be unsettling, particularly for older investors who may be more focused on preserving wealth than chasing high returns.

With ongoing geopolitical tensions, including the current conflict in the Middle East, market swings have become more pronounced. In this environment, a disciplined approach such as pound-cost averaging can help reduce risk and remove some of the stress from investing.

What Is Pound-Cost Averaging?

Pound-cost averaging (often abbreviated to PCA) is a simple investment strategy that involves investing a fixed amount of money at regular intervals, regardless of what the markets are doing.

Rather than trying to “time the market” – buying at the lowest point and selling at the highest – you invest regularly over time. This means you automatically buy more units when prices are low and fewer when prices are high.

How It Works in Practice

Suppose you invest £500 a month into a stock market fund:

In month one, prices are high, so your £500 buys fewer units.

In month two, prices fall, so the same £500 buys more units.

Over time, your average purchase cost tends to smooth out.

This reduces the risk of investing a large lump sum just before a market downturn – something that can be particularly damaging in retirement or near-retirement years.

The Key Benefits

1. Reduces Market Timing Risk

Even professional investors struggle to predict short-term market movements. Pound-cost averaging removes the need to guess when to invest, helping you avoid costly mistakes.

2. Smooths Out Volatility

By spreading your investments over time, you avoid the impact of sudden market swings. This is especially valuable during periods of uncertainty.

3. Encourages Discipline

Regular investing promotes good financial habits and helps ensure you stay committed to your long-term plan.

4. Emotion-Free Investing

Market falls can tempt investors to delay investing, while market highs can encourage overconfidence. PCA removes these emotional triggers.

Why It Matters Now

Recent instability linked to the Middle East conflict has contributed to increased volatility in global markets. Energy prices, inflation expectations and investor sentiment have all been affected.

In such conditions:

Markets can rise and fall sharply in short periods.

News headlines can trigger knee-jerk reactions.

Attempting to time entry points becomes even more difficult.

Pound-cost averaging provides a structured way to keep investing without being derailed by short-term events.

Lump Sum vs Regular Investing

It’s worth noting that, historically, investing a lump sum can sometimes produce higher returns – simply because more money is invested earlier.

However, this comes with higher risk. If markets fall soon after investing, losses can be significant.

For many people – particularly cautious investors or those approaching retirement – the lower risk and smoother ride offered by pound-cost averaging may be preferable.

Who Should Consider Pound-Cost Averaging?

This approach can be particularly suitable for:

New investors building confidence

Those investing monthly from income (e.g. pensions or earnings)

Investors concerned about current market volatility

Anyone looking to reduce emotional decision-making

It is also a natural fit for tax-efficient wrappers such as ISAs and pensions, where regular contributions are common.

Practical Tips for UK Investors

Use a Stocks and Shares ISA to shelter returns from tax

Set up an automatic monthly investment to maintain discipline

Choose diversified funds (e.g. global equity funds) to spread risk

Review periodically, but avoid reacting to short-term market noise

Final Thoughts

In uncertain times, trying to outguess the market can do more harm than good. Pound-cost averaging offers a steady, disciplined approach that helps reduce risk and maintain perspective.

While no strategy can eliminate volatility entirely, investing regularly over time can make market fluctuations work in your favour rather than against you – a valuable advantage in today’s unpredictable world.

As always, please feel free to leave any comments below. I am always delighted to hear from Pounds and Sense readers.

Disclaimer: I am not a qualified financial services professional and nothing in this post should be construed as personal financial advice. You should always do your own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

If you enjoyed this post, please link to it on your own blog or social media:

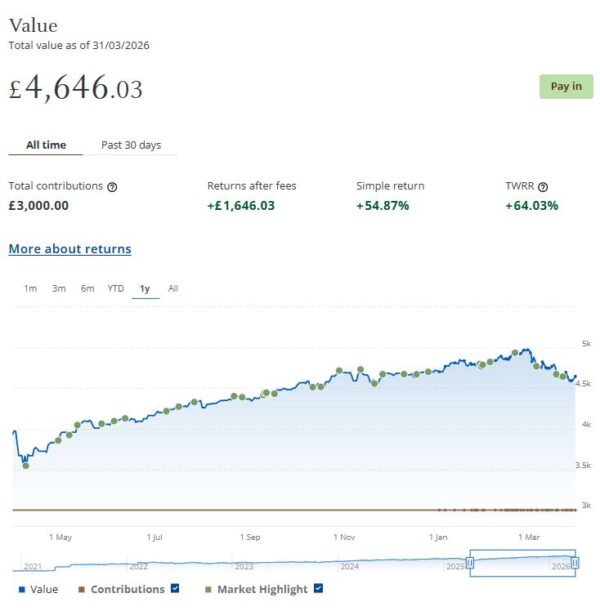

I’ll begin as usual with my JP Morgan Personal Investing (previously Nutmeg) Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

As regular readers will know, in June last year I transferred most of the money in my former Nutmeg Fully Managed portfolio (just under £25,000) to a new Nutmeg Income Portfolio. I discussed this in detail in this post, but basically money in this port is invested to generate an income from share dividends and other sources. This is then paid monthly. Capital appreciation is targeted as well, but these portfolios are aimed primarily at older people (and others) who want/need their investment to generate a regular cash income.

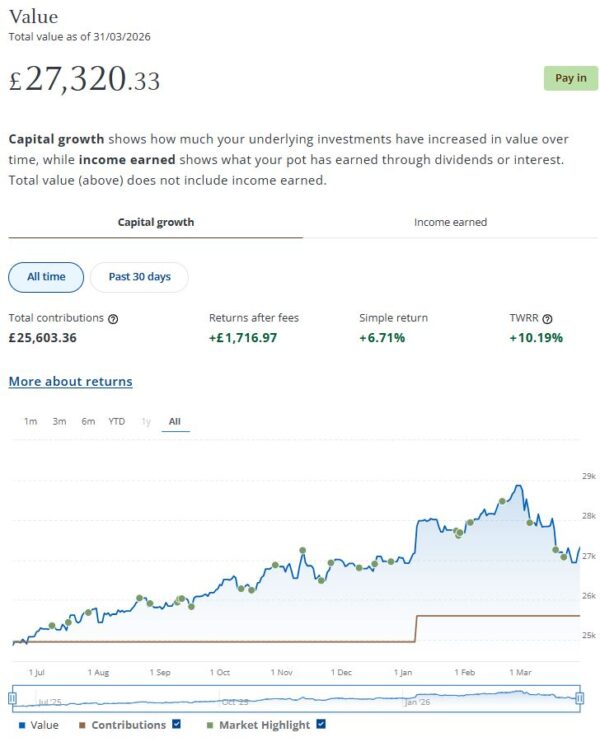

In January my JPM Investing income portfolio generated £75.54 of income, which was duly paid in to my bank account on 24 March 2026. That means I have now received tax-free income of £273.68 in 2026 and a total of £745.14 since I opened the account in June last year. That’s about what I would have expected based on JPM’s projected annual return of just under 5% for income ports at my chosen risk level (five).

The less good news is that my income portfolio declined in value in March. It’s now worth £27,320 compared with £28,866 at the start of last month, a fall of £1,546. You don’t need to be an investment expert to know that this is mainly due to events in the Middle East. Nearly all of my share-based investments have been affected by this. Clearly it is disappointing, but as I always say, you do have to expect ups and downs when investing. As the screen capture below shows, my income port is still up by a respectable £1,716.97 (6.71%) after fees since I opened it last June.

I still have a smaller, growth-oriented pot using JPM Investing’s Smart Alpha option. This is now worth £4,606 compared with £4,974 (rounded up) a month ago, a fall of £368. Here is a screen capture showing performance over the last year.

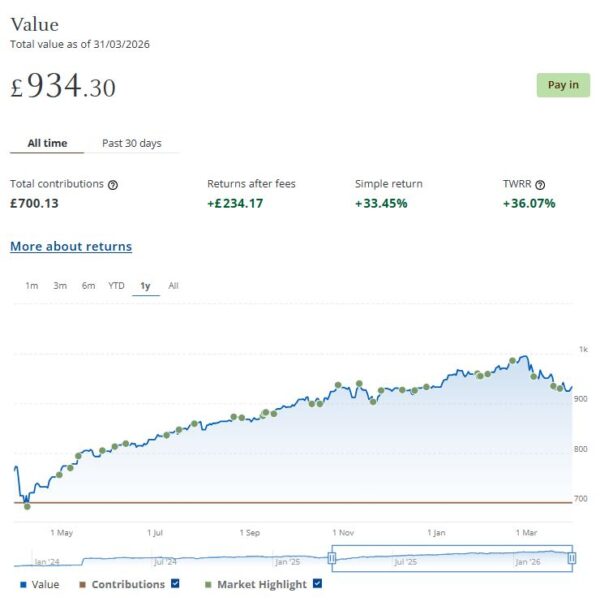

Finally, at the start of December 2023 I invested £500 in one of Nutmeg/JPM’s thematic portfolios (Resource Transformation). In March 2024 I also invested a further £200 from referral bonuses (something I no longer receive). As you can see from the one-year screen capture below, this portfolio is now worth £934 compared with £996 (rounded up) last month, a decrease of £62.

Overall in March the value of my JPM investments fell by £1,976 or 5.55%. Against that I did, of course, receive £75.54 in income from my income portfolio. In total, then, I am £1900.46 down for the month.

On a more positive note, excluding income generated, the overall value of my JPM investments is still up by £3,385 or 11.47% since the start of April 2025. If you add to this figure the £745.14 of income generated by my Income portfolio to date, that gives a total profit for the last 12 months of £4,130.14 – still not a bad return in these uncertain times.

As I said above, some volatility is always to be expected with stock market investments, but in the longer term they tend to even themselves out (and typically outperform bank savings accounts, although that is never guaranteed). In general the worst thing you can do is panic and sell up when downturns occur (as happened last month). You are then crystallizing your losses rather than giving the markets time to recover. This is something I discussed last year in this blog post. Obviously nobody knows what will happen in the Middle East, but hopefully some sort of resolution will occur soon, if only because President Trump desperately needs an exit strategy to pacify his critics back home. Once a bit more stability returns to the region, we will hopefully see world stock markets rise again. Though of course there is no guarantee about this.

You can read my full original Nutmeg/JPM review here. If you are looking for a home for your annual ISA allowance, based on my overall experience over the last nine years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs), Lifetime ISAs and Junior ISAs as well.

Moving on, I also have investments with P2P property investment platform Housemartin. As discussed in this post, the company rebranded last year from Assetz Exchange.

My investments with Housemartin continue to generate steady returns. Housemartin focuses on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my HM portfolio has generated a respectable £309.64 in revenue from rental income. I have made a small net loss of £20.25 on property disposals. Capital growth generally has slowed, in line with UK property values generally.

At the time of writing, 17 of ‘my’ properties are showing gains, 3 are breaking even, and the remaining 24 are showing losses. My portfolio of 44 properties is currently showing a net decrease in value of £76.05. That means that overall (rental income minus capital value decrease and loss on disposal) I am up by £213.34. That’s still a respectable return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Housemartin most projects are socially beneficial as well.

A further consideration is that property investments on Housemartin are less likely to be affected by stock market downturns, as happened in March due to the war in the Middle East. This again demonstrates the potential value of such investments for diversifying your portfolio during challenging times.

The net fall in capital value of my Housemartin investments is obviously a little disappointing. But it’s important to remember that until/unless I choose to sell the investments in question, it is largely theoretical, based on the latest price at which shares in the property concerned have changed hands. The rental income, on the other hand, is real money (which in my case I’ve reinvested in other HM projects to further diversify my portfolio).

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of Housemartin as far as i am concerned. You can actually invest from as little as £1 per property if you really want to proceed cautiously.

As I noted in this blog post, Housemartin is particularly good if you want to compound your returns by reinvesting rental income. This effectively boosts the interest rate you are receiving. Personally, once I have accrued a minimum of £10 in rental payments, I usually reinvest this money in either a new HM project or one I have already invested in (thus increasing my holding). Over time, even if I don’t invest any more capital, this will ensure my investment with Housemartin grows at an accelerating rate and becomes more diversified as well.

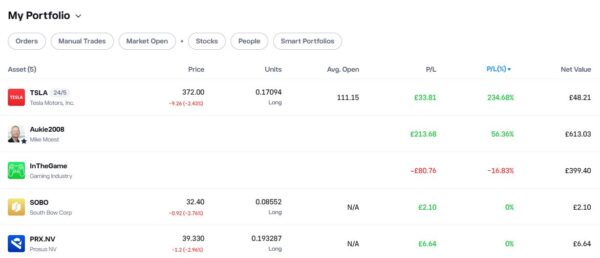

In 2022 I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios, Oil Worldwide. I also invested a small amount I had left over in Tesla shares.

In January this year, as Oil Worldwide hadn’t exactly been setting the world alight, I decided to switch my entire investment in this to another smart portfolio, InTheGame. This port, focusing on the computer gaming industry, has been the top performer for some time in my eToro virtual portfolio.

Unfortunately just as I switched away from Oil Worldwide, President Trump decided to invade Venezuela. This gave the oil industry a significant boost, which I would otherwise have benefited from. Meanwhile InTheGame has gone south, partly due to the recent fall in AI stocks along with the war in the Middle East. At the time of writing the value of my investment in this has fallen by nearly 17%. Hey ho! This does of course demonstrate that there are never any guarantees when investing and unexpected events can thwart the best-laid plans…

As you can see from the screen captures below, my original eToro investment (total value £888.36 in pounds sterling) is today worth £1,070.78, an overall increase of £182.42 or 20.53%.

Note: eToro now displays the value of investments in your native currency, although you can change this if you wish.

As mentioned above, my new investment in InTheGame is currently down by nearly 17%. My copy trading investment with Aukie2008 also fell in value in March, but it’s still showing an impressive overall profit of 56.36%. Of course, I have held this investment for quite a bit longer.

My Tesla shares, which I purchased as an afterthought with some spare cash I had in my account, are also down this month, but still showing an overall profit of over 234% since I bought them. If only I had put a bit more money into this!

You might also notice that I have small holdings in Prosus NV, a Dutch internet group, and South Bow, a Canadian energy infrastructure company. To be honest I don’t understand how I acquired these, but I assume they are some sort of bonus I was awarded. In any event, I am happy to have them in my portfolio.

If you would like more information about setting up an eToro account, please click on this no-obligation website link [affiliate]. Don’t forget that you also get a free $100,000 virtual portfolio, which you can use to experiment with trading and investing strategies. I have certainly earned a lot from mine.

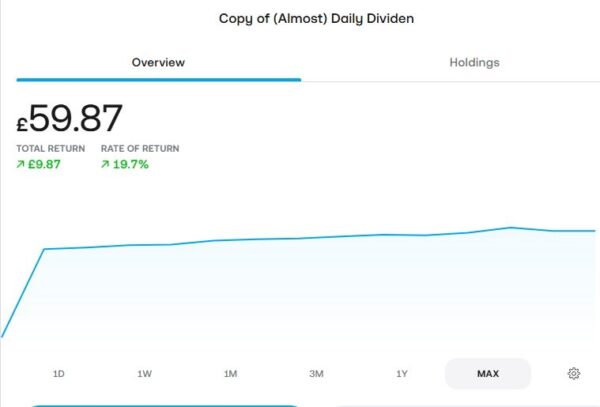

As an experiment, at the start of April last year I put £50 into an investment ISA with Trading 212. As mentioned in my blog post about dividend investing, I put it into the (Almost) Daily Dividends Portfolio, a ready-made portfolio or ‘pie’ on Trading 212. As you can see from the screen capture below, my portfolio is now worth £59.87. That’s a decrease of £1.97 since last month but an increase of £9.87 or 19.7% over the eleven-month period since I opened it. It has even accrued a grand total of £1.08 in dividends, most of which has now been (automatically) reinvested.

I am quite impressed with how this investment has been faring, despite the small amount I put in (which means I may be missing out on some smaller dividends). If I increased my investment I would almost certainly become eligible for more dividends, and even more the longer I remain invested. If I had any spare money at the moment, I would consider doing this. Of course, I do now have an income-focused portfolio with JPM Investing as well (see above).

Moving on, I published various posts on Pounds and Sense in March. I have listed below those that are still relevant.

In Beat the Postage Stamp Price Rise, I pointed out that the cost of stamps is rising (again) on Tuesday 7 April 2026. That will be the SEVENTH rise in the price of first class stamps in just four years! Standard and large-letter stamps don’t have values printed on them and will still be valid after the April price rise comes in, so my top tip is to stock up now while stamps are still at the old price.

I also posted an updated version of Get a Free Share Worth up to £100 with Trading 212. Anyone who hasn’t done this before can get a free share worth up to £100 just by signing up for a new Trading 212 investment account via my link. The current offer closes on Tuesday 28th April 2026.

Also in March I published Are River Cruises Suitable for Solo Travellers. This was a follow-up to my earlier posts about how to save money on cruise holidays and the pros and cons of river cruises (for older travellers in particular). In this post I addressed a question asked by several readers as to whether river cruises are a good choice for solo travellers. The article sets out the pros and cons as I see them. My view, as expressed in the article, is that they can be, but it does depend on your travel style and budget.

What Is An Annuity – And Who Should Consider Buying One? discusses a subject that confuses many people. In simple terms, an annuity is a financial product that converts a lump sum of money – typically from your pension pot – into a guaranteed regular income for life (or for a fixed period). You buy an annuity from an insurance company. In return for handing over some or all of your pension savings, they promise to pay you a regular income, usually monthly, for the rest of your life. In the article I look at the pros and cons of annuities, and whom they are (and aren’t) likely to be suitable for.

How to Save Money on Travel Insurance covers a subject on many people’s minds at this time of year. Travel insurance is one of those expenses that can feel like a grudge purchase – until you need it. For UK travellers, especially older holidaymakers, having adequate cover is essential. In this article I set out some ways you may be able to save on travel insurance without compromising your safety or security. I also discuss saving money on travel insurance as an older person, and the issues that can be caused by war and civil unrest (especially relevant for destinations in or near the Middle East at the moment).

Finally, in March I published Don’t Miss Out – Use Your £20,000 ISA Allowance Before It’s Too Late! As I say in the article, the end of the tax year on 5 April 2026 is fast approaching and so is the deadline to utilize the annual tax-free Individual Savings Account (ISA) allowance. Unless you take action in the next few days, this opportunity to maximize your tax-free savings for the 2025/26 financial year will be gone for ever.

And speaking of deadlines, time is also running out to take advantage of EDF Energy‘s enhanced switching offer. Until 6 April 2026 you can get a FREE £75 (increased from £50) credited to your energy account when you switch to EDF via my link at https://edfenergy.com/quote/refer-a-friend/sunny-koala-9462. Terms and conditions apply.

I’ll close with my customary reminder that you can also follow Pounds and Sense on Facebook or Twitter (or X as it is now). Twitter/X is my number one social media platform and I post regularly there. I share the latest news and information on financial matters, and other things that interest, amuse or concern me. So if you aren’t following my PAS account on Twitter/X, you are definitely missing out!

I am also on the BlueSky social media network under the username poundsandsense.bsky.social. Twitter/X remains my primary social media platform, but I also post details of my latest blog posts, third-party articles and other financial news and resources on BlueSky for those who prefer to follow me there.

As always, if you have any comments or questions, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts on PAS may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media: