As you may have heard, the BBC has now confirmed that from 1st August 2020 people over 75 in the UK will lose their automatic right to a free TV licence and have to pay the same £157.50 a year as everyone else. This was originally due to happen in June 2020, but it was postponed due to the coronavirus pandemic.

For many old people, TV is their main (or only) source of company. Suddenly having to find this quite large sum out of (in many cases) a very limited income may cause them financial difficulties or downright hardship. Some may even have to choose between watching television and paying their heating bills.

This parlous situation has arisen because the BBC say they have to make economies, and continuing to subsidise free licences for the elderly would force them to cut back drastically in other areas. Meanwhile the government, despite their pre-election promises, has shown no sign of stepping in to preserve free TV licences for over 75s (which they could perfectly well do). Although charities such as Age UK have been raising petitions and applying as much pressure as they can, it now seems certain that this change is going to happen.

So what can people in this situation – or their relatives/friends/carers – do? The BBC have allowed just one concession – the poorest over-75s can continue to receive a free TV licence if they claim and receive pension credit. So let’s look at this in a bit more detail…

Pension Credit

Pension credit is a state benefit for people above retirement age who are on a low income. It can be paid to single people or to couples. It is usually paid weekly, though you can also choose to have it paid fortnightly or monthly.

Along with attendance allowance – which I discussed in this recent post – pension credit is one of the most under-claimed benefits. According to the Department for Work and Pensions, around 40 percent of eligible people, or two in five, fail to claim it. That’s an estimated 1.5 million eligible households in the UK who are missing out.

Pension credit actually comes in two parts – guarantee credit and savings credit. Guarantee credit boosts your weekly income to £167.25 if you’re single or £255.25 if you’re a couple (all figures correct as of March 2020). You may be eligible for guarantee credit if you have reached state pension age and your total income is less than these amounts (even if you own your own home). If you have under £10,000 in savings and investments this will not be taken into consideration. If you have over £10,000, it will be assumed that you earn £1 a week per £500 of savings and investments (equivalent to an interest rate of 10.4% – if only!). This will be added to your total income when working out your eligibility.

Savings credit is meant to be a reward for those who have saved for their retirement. It’s worth up to £13.73 a week for a single person or £15.35 for couples. To qualify, you must have a minimum income of £144.38 a week if you’re single, and £229.67 a week if you’re in a couple. For every £1 by which your income exceeds this amount, you get 60p of savings credit – up to the £13.73/£15.35 maximum. If your income is less than the £144.38/£229.67 savings credit threshold, you won’t qualify. Savings Credit is only available to people who reached state pension age before 6 April 2016. Couples where only one partner reached state pension age before 6 April 2016 can also retain savings credit if the older partner had reached 65 and qualified for savings credit before that date AND they have remained continuously entitled to it ever since.

It’s worth adding that if you pay mortgage interest or have other housing costs, have caring responsibilities, are responsible for a child, or are severely disabled, you may be entitled to more pension credit. If you receive attendance allowance or carers credit, for example, this may boost the amount you’re entitled to. The rules surrounding all this are complicated, but the government has provided a free online calculator you can use to work out whether you qualify and how much you might get. This is for guidance only, however. You can’t apply via the calculator and there is no guarantee that you will receive the amount it shows you.

To actually apply you will need to phone the DWP’s Pension Credit helpline on 0800 991234. You will need your National Insurance number, information about your income, savings and investments and your bank account details. The person you speak to will then take you through the application process. This is a subject I discussed in more detail in this blog post, as I recently helped an older friend to do this successfully.

What Does Pension Credit Entitle You To?

As well as the money – which can amount to thousands of pounds a year – if you receive pension credit you will be entitled to a range of additional benefits. A free TV licence if you are over 75 is just one of them. You may also get:

reduced council tax (or free if you are awarded guarantee credit)

Even if you only receive a small amount of pension credit, you will be eligible for all of the above. So it really is well worth applying if there is any chance you may qualify. As mentioned above, you can check first using the free online calculator here and then apply by phoning the DWP’s Pension Credit helpline on 0800 991234.

Don’t delay, as there are now just seven weeks left before the free TV licence for all over-75s becomes a cherished memory.

Equity Release to Boost Your Income

If you’re still struggling to pay the bills even with pension credit, there are other methods to help boost your income. In particular, UK homeowners are fortunate to have opportunities to unlock their property value. An equity release loan could provide the security you desire if you require the means to pay for life’s simple pleasures or cover essential costs.

What’s more, homeowners can unlock up to 65% of their property value, with no compulsory payments required during their lifetime. There’s no limit on how you can use the tax-free cash you receive, so an income lifetime mortgage could be the ideal way to pay your bills and have a bit extra for luxuries as well.

Regular readers will know that I have been posting about my personal experience of the coronavirus crisis since lockdown started (you can read my June update here if you like).

In what I hope will be my final update, I thought I would discuss what has been happening with my finances and my life generally over the last few weeks. As previously, I will start with the money-related stuff…

Financial

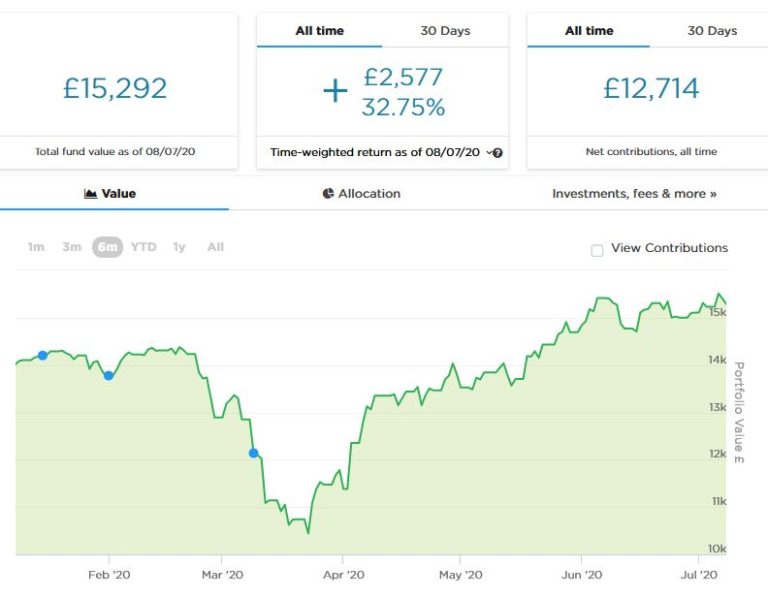

Overall things haven’t changed dramatically since my update last month. Here’s the latest chart showing how my Nutmeg stocks and shares ISA is faring…

As you can see, my ISA made a good recovery after losing over a third of its value in March (admittedly I helped things along by investing another £1,000 when the markets were near their lowest point). In the last few weeks things have plateaued somewhat, though the overall trend is still upward. Allowing for the extra £1,000 invested in March, my portfolio is now back at the level where it was before the crisis started.

Assuming there is no major second wave of the virus – and there has been little sign of that so far – I am hopeful the recovery will continue over the longer term. Of course, there are likely to be bumps along the way, and in the short term at least we face the likelihood of a recession. Even so, I am keeping my fingers crossed for a recovery over the next year or so, and am continuing to invest cautiously where I see value. I haven’t put any more money into my Nutmeg ISA yet but definitely plan to. I may, though, take the opportunity to reduce my risk level (which is easy to do from the Nutmeg dashboard). Do take a look at my in-depth Nutmeg review if you haven’t already.

My monthly payments from my two Buy2LetCars investments (totalling around £420) continue to appear in my bank account every month like clockwork. I was initially wary about this, as it is obviously a bit outside the usual range of investments. However, I have had no issues at all, and am glad also to be supporting key workers by providing reasonably priced transport for them.

Again, if you’d like to learn more, you can read my review of Buy2LetCars here and my more recent article about the company here. Obviously the minimum investment is £7,000 so this opportunity isn’t going to be for everyone – but if I had that sort of money burning a hole in my pocket right now, I wouldn’t hesitate to invest through them again. Each car generates a monthly income, with a large lump sum at the end of the three-year term. Interest rates range from 7 to 12 percent per year.

My other equity-based investments generally are doing about as well as could be expected in the circumstances and in some cases better. In particular, my Bestinvest SIPP hasn’t lost any significant value when you allow for the fact that it’s in drawdown and I am currently withdrawing £200 a month from it. I’m not claiming any special skills as a stock picker, but having a broad range of funds in my portfolio has undoubtedly served me well. Years ago, also, I decided to invest some of my pension money in specialist healthcare funds, and these have done better than average over the last few months 🙂

On the property crowdfunding side, the picture isn’t so rosy. A number of my property investments still seem to be stuck in limbo, though I did hear from The House Crowd that they had received an offer for a house in Liverpool in which I invested £1,000 six years ago (pictured below).

The offer was for slightly less than the original purchase amount, but nonetheless the investors (including me) voted by a clear majority to accept it. So I will get a bit less than my original £1,000 back, though when you add in the dividend payments (from rent) since I first invested, I should be slightly up overall. But that’s before you allow for inflation, of course!

I am hoping that the Stamp Duty holiday announced by chancellor Rishi Sunak this week will help get the housing market moving and maybe ‘unstick’ some of my other property crowdfunding investments that have been on hold for a while. In retrospect I probably let my enthusiasm for the property crowdfunding concept run away with me a bit in the past. Overall I have still made some money from these investments, but not as much as I hoped or expected. And I still have a fair-sized sum tied up in properties I really expected to be sold by now. I do still think property crowdfunding can merit a place in people’s portfolios, but would advise diversifying as much as possible across platforms and properties. And definitely don’t invest money you might need any time soon!

Finally on this subject, I would just say that I exclude property loan investment platform Kuflink from the criticisms above. All of my investments with them have been doing well. Although there was a short delay with one loan, it has now been repaid (with added interest). Kuflink are adding new investment opportunities to the platform most days and I have been investing modestly in them, along with loan portions that have just a few months left to run via the Kuflink Marketplace. See my Kuflink review here for more information. Their up-to-£4,000 cashback offer for new investors is still open, incidentally.

One other thing I have mentioned before is that I have a few invitations available for an unusual sideline-earning opportunity based on matched betting. I have been asked not to divulge too many details about it on the blog for very good reasons I will explain privately to anyone who may be interested (and no, it’s not illegal!). What I can say is that it doesn’t require any financial outlay, is entirely hands-off, and will provide an income of £50 a month. No knowledge of betting is required, and you won’t have to place any bets yourself. Just note that the opportunity is only open to people who haven’t done matched betting before and have no more than two accounts already with online bookmakers. For more info (and receive a no-obligation invitation) drop me a line including your email address via my Contact Me page 🙂

Personal

As I’ve said before, I live on my own since my partner, Jayne, passed away a few years ago. I am lucky to live in a fairly large house with a good-sized garden, so being mostly confined to home hasn’t been as big a challenge for me as I’m sure it has for some. Also, I am well used to working from home, having done this for the last 30 years or so.

Nonetheless, the ongoing nature of the crisis is undoubtedly taking its toll on me. Every day seems so similar it is starting to feel like Groundhog Day. And while that is one of my all-time favourite movies, I definitely don’t want to live in it myself. Mind you, I saw someone on Twitter compare their experience of lockdown at home with the Overlook Hotel in The Shining. At least I wouldn’t claim it’s as bad as that!

So far as work is concerned, as you may know I’m a semi-retired freelance writer and editor (age 64). I’ve had very little work since the lockdown started, and was duly grateful to receive some financial support from the government’s SEISS scheme. I have, though, been keeping myself busy (and sane) with this blog and – as you may have noticed – have enjoyed quite a productive period. I ran out of inspiration a bit this week, but hopefully that is just a temporary blip.

I am still available for freelance writing, editing or proofreading work, although I am not taking on book-length projects any more. Feel free to drop me a line if you think my services might be of interest to you 🙂

Life generally is changing now as – touch wood – the worst of the pandemic appears to be behind us. The experience of shopping is still evolving and I guess it will be many months before it is entirely back to normal. I haven’t yet been to any ‘non-essential’ shops, but at my local Morrisons supermarket it feels a bit more relaxed. I would say only about a quarter of people are wearing masks or other face coverings now. I was wearing a bandana over my nose and mouth but have mostly stopped that unless I find myself surrounded by other shoppers. Of course, in England face coverings are now compulsory on public transport, so I will be keeping my bandanas washed and ready for that.

UPDATE: Just heard that the government is considering making the wearing of face-masks in shops in England compulsory. I find that bizarre at a time when – apart from a few local outbreaks – the virus is waning rapidly. It also sends out a mixed message at a time when the government is encouraging people to eat out, obviously not wearing masks. And the evidence in favour of wearing masks in public is weak anyway. Personally I really hope.the government refrains from doing this.

Many pubs are open again now. I walked past my nearest, The Drill, on Sunday afternoon. It all looked quite continental, with people sitting at tables outside and waitresses going in and out with trays of beer and other drinks. There was a happy buzz of conversation and laughter. The only less cheerful note was struck by the manager standing by the door with a clipboard, presumably taking the contact details of people as they arrived for contact-tracing purposes. I wasn’t tempted to go in myself, though I don’t rule out going for a drink and a meal soon, maybe taking advantage of the government’s £10 off vouchers 🙂

I am still looking forward to my short break in Minehead in September, which I booked before this crisis happened. I am also mulling over whether to try to book a couple of days away in August. I worked out the other day that I have been to Wales every year for over 30 years, and it would be a shame to break that long run in 2020. Llandudno or Aberystwyth could both be contenders.

I am still working my way through my box sets of Deep Space Nine and Bergerac. With the latter, it’s quite interesting to see how mobile phones evolved as the series was made. In the earliest episodes I guess they didn’t exist at all, and Bergerac’s office generally seemed to know telepathically where he was and phoned him at his father-in-law’s or wherever. Later on car phones make an appearance, and then house-brick-sized mobiles with aerials sticking out of them. Ah, the nostalgia!

I am trying not to spend too much time on social media as I know it’s bad for my mental health. There are a few people I follow regularly on Twitter and and enjoy hearing from, though. Last time I mentioned Professor Karol Sikora, a well-respected cancer specialist with a doctorate in immunology. Many people, including me, have found him a beacon of hope amid all the negativity, with his generally positive and optimistic view (though still informed by science and statistics). He doesn’t have a political axe to grind and is willing to give the government credit for things they have done well and criticize things they have done badly. If you want one person to follow for unbiased news about the pandemic with a measure of hope for the future, I highly recommend checking out his Twitter page.

Lately I’ve also been enjoying reading the posts of Scottish blogger Effie Deans (who blogs as Lily of St Leonards). She is a Scottish academic who has a lot of interesting things to say about nationalism, education, culture, and more. You may or may not agree with all her views; but if you want an interesting and genuinely thought-provoking perspective on events from someone who isn’t afraid to challenge current orthodoxies, I highly recommend checking out her Twitter page and blog.

To end on a positive note, I am looking forward to having my hair cut for the first time in four months next week. I’ve actually quite enjoyed revisiting my long-haired student days, but enough is definitely enough! I am also looking forward to going swimming again after it was announced that outdoor pools can reopen from tomorrow and indoor pools a fortnight later. The David Lloyd Leisure club I belong to has both indoor and outdoor pools, so I am waiting to hear whether they will be opening the outdoor pool immediately or whether I will have to wait a bit longer till both pools can reopen. (UPDATE – Now heard I have to wait another fortnight 🙁 )

So that has been my experience of the coronavirus crisis to date. I do of course appreciate that I am in a fortunate position compared with many others, and hope you and your family are coping in these strange and worrying times. Here’s hoping that things continue to improve and we can all return in due course to something approximating normal life.

As ever, I’d love to hear your thoughts and experiences. If you have any comments or questions, as always, please do post them below.

Disclaimer: I am not a registered financial adviser and nothing in this post should be construed as personal financial advice. You should always do your own ‘due diligence’ before investing and seek advice from a qualified financial adviser/planner if in any doubt how best to proceed. All investments carry a risk of loss.

If you enjoyed this post, please link to it on your own blog or social media:

Many older people find themselves asset rich but income poor. In other words, they own valuable assets such as their home but live on a modest income.

If that applies to you, equity release is an option you may want to consider, to release some of the cash locked up in your property.

There are two key requirements for doing this. The first is that you must be 55 or over (home reversion plans are only available to over 60s).

The second is that there must be equity available in your home. That means the mortgage must be paid off or the balance outstanding must be significantly lower than the house’s current value. Of course, many older people do find themselves in this situation.

There are two main types of equity release scheme, home reversion plans and lifetime mortgages. I’ll cover each of these in turn.

Home Reversion Plans

With a home reversion plan, a company buys your home but guarantees to let you and your partner (if you have one) go on living there rent-free until you die or go into long-term care.

After this the company normally sells the house and take its profit. Your beneficiaries will not receive any proceeds from the sale or benefit from any rise in the property’s value.

Note that as the company is allowing you to stay in the house until you no longer need it, you won’t receive the full market value of your property. Home reversion plan providers will usually pay you only 30 to 60% of the value of your home. How much you are offered depends on how old you are and how long the company expects you to go on living at the property.

Lifetime Mortgages

Lifetime mortgages are similar to ordinary mortgages except no repayments have to be made until the house is sold.

You receive tax-free cash to do whatever you like with. Eventually of course this will have to be repaid with interest, and the interest rates charged are typically a little higher than standard mortgage rates. However, as you retain ownership of the property until it is sold, this cost may be partly or wholly offset by the property’s rise in value.

There are two types of lifetime mortgage, lump sum and drawdown. A lump sum lifetime mortgage is a loan secured against your home, giving you access to a one-off pot of cash. A drawdown lifetime mortgage lets you draw down cash in stages after an initial lump sum, with interest only payable on the money released. A drawdown lifetime mortgage is therefore likely to work out significantly cheaper overall than a lump sum mortgage.

In either case, how much you can borrow depends on a number of factors, including your age, the value of the property and in some circumstances your health. At 67 you can typically borrow around a quarter of the value of your home, rising to around a third in your mid-70s,

If you have certain medical conditions, you may be able to borrow a higher proportion of your property’s value or obtain a better interest rate via an ‘enhanced’ plan.

Both types of equity release scheme have their attractions, but lifetime mortgages are nowadays by far the more popular option. This is because of their greater flexibility and the fact that you retain ownership of the house and can therefore benefit from any rise in its value.

Negative Equity

With both home reversion plans and lifetime mortgages, you are protected from negative equity (i.e. the risk you or your beneficiaries will end up owing more to the scheme provider than the property is worth). Provided the company is approved by the Equity Release Council (see below), any shortfall at the end will be written off.

Opting for equity release is a major decision, however, and will clearly affect how much money will be left for your children and any other beneficiaries to inherit. It’s important therefore to discuss it with them and get their views; although in the end it is of course your money and your right to do whatever you want with it.

More Points to Consider

Here are a few more things to bear in mind before opting for equity release.

Consider also downsizing to a smaller property and/or moving to a less expensive part of the country. This can be a cheaper way to release funds from your home if you don’t mind the disruption. But do this sooner rather than later, since people typically become more reluctant to move as they get older.

As mentioned above, ensure that the company you deal with is a member of the Equity Release Council. Their members must abide by a strict code of practice, and all offer a no-negative-equity guarantee.

Taking cash using equity release may affect your eligibility for means-tested benefits such as pension credit. This applies especially if you take a large lump sum, as you may then exceed the qualifying limit for benefits such as pension credit and council tax reduction. With a drawdown lifetime mortgage – where you take money in chunks as required – you may be able to remain under the capital limits and therefore qualify (or continue to qualify) for these benefits.

Leave it for as long as you can. The later you take equity release, the less costly it is likely to prove overall.

If you don’t have family or others you want to leave your wealth to, cost isn’t such an issue, though. In that case there is much to be said for taking equity release to improve your quality of life and leaving the money be repaid out of your estate when you die.

If you have bought your house on an interest-only mortgage and don’t have the money to pay it off, equity release can be a good way to repay the loan and reduce your monthly outgoings.

You don’t have to do it all in one go. Lifetime mortgages in particular are very flexible, and as mentioned with a drawdown plan you can take money in chunks when you need it and interest will only accrue on what you have withdrawn so far.

Key Equity Release

While equity release can be a great way to free up cash to help you enjoy later life, taking it is a major decision with many potential ramifications. It’s therefore very important (and indeed a regulatory requirement) to get independent professional advice before proceeding.

Key Equity Release [affiliate link] are leading equity release specialists who work with a wide range of financial service providers and provide no-obligation advice on the best options in your case.

Key Equity Release only arrange lifetime mortgages, but (as mentioned above) these are now by far the most popular option for equity release, with many advantages due to their flexibility and the fact you retain ownership of your home.

All advice from Key is free of charge, and due to the pandemic is now available in full over the phone. Key’s independent adviser will discuss your options with you, including checking that you are receiving all the state benefits you may be entitled to. They will recommend based on your needs and circumstances. For example, if you want to ensure some money remains for your descendants, however long you remain in your home, they have plans to cater for that. Equally, if your priority is getting the lowest interest rate or withdrawing the largest possible amount, they can arrange this too.

Key say that they have been able to access interest rates from as low as 2.45%, and most of their customers have received a fixed annual interest rate of 3.97% or lower.

The company also has mainly five-star reviews on Trust Pilot (average 4.9), which you can check out via this link. This is one of the highest average feedback scores I have seen on Trust Pilot.

Closing Thoughts

If you are looking for a way to release money from your property, whether to fund specific purchases or just to make later life more comfortable, equity release is definitely worth considering. The main downside is – of course – that ultimately there will be less money to pass on to your descendants. All reputable providers, however, offer a No Negative Equity Guarantee, and some such as Key Equity Release can arrange plans where a certain amount of cash is guaranteed to remain in your estate.

Equity release interest rates are at historically low levels, and in most cases are fixed for life. If equity release is right for you – and you will need to discuss this fully with an independent adviser before proceeding – now could be the ideal time to set the ball rolling. So why not get in touch with Key Equity Release today for a no-obligation discussion?

If you have any comments or queries about this article, as always, please do post them below.

Disclosure: This is a sponsored post. If you click through a link in it and arrange an equity release plan with the company in question, I may receive a commission for introducing you. This will not affect the service you receive or the terms you are offered. Please note also that I am not a registered financial adviser and nothing in this post should be construed as individual financial advice.

If you enjoyed this post, please link to it on your own blog or social media:

If you’re looking for a way to make steady money from home, setting up as a virtual assistant (VA for short) has a lot to recommend it.

Most VAs work from home providing services to businesses and solo entrepreneurs. Services may include anything from secretarial support to book-keeping, answering calls and emails to updating the company blog. In all cases, though, the work involves using modern communication tools to perform tasks that in the past would typically have been performed in-house.

Opportunities for VAs have grown at an accelerating rate as businesses have come to understand the benefits they can offer. In particular, businesses save by not having to provide office space or equipment for VAs, and only paying them when there is a specific task they need doing. In these cash-strapped times, such savings can present a compelling argument for hiring a VA.

For VAs too, there are many attractions to the role. The main one, of course, is that you can work from home, with all the advantages this confers. These range from fitting in work around childcare responsibilities to big savings on commuting time and costs. In addition, the work can be varied and interesting, and you can specialize in those areas that appeal to you most.

Skills Required

Most virtual assistants have several years’ experience working in offices, whether in a managerial, administrative or secretarial capacity. It goes without saying that you need good keyboard skills. An excellent telephone manner is essential as well, as is a good command of written English.

You will need skills in popular software packages, especially Microsoft Office (ideally including Word, Excel, PowerPoint and Outlook). The ability to work on a Mac is an added bonus. Knowledge of social media is a big plus, as is website design and maintenance.

Many businesses nowadays use WordPress for running blogs and websites, so some knowledge of this platform will be very helpful too.

Beyond this, you will need the ability to communicate with a wide range of clients and quickly grasp what they require and deliver it. A good VA anticipates clients’ needs and suggests ways they may be able to help them boost their productivity and achieve their goals.

You will need to be well-organised and self-disciplined. As a VA you will be self-employed and won’t have a boss looking over your shoulder all the time. You must be able to resist distractions and focus on the task in hand, and be willing put in an extra shift when required to meet your clients’ deadlines.

Finally, you will require all of the personal qualities required by any self-employed person, including tenacity, stamina, perseverance, enthusiasm, and the ability to cope with (and even thrive on!) stress.

Tools and Equipment

You don’t need to spend thousands when you’re starting out, but some tools and equipment are pretty much essential. Here are the main things you are likely to need…

Computer – A desktop is fine for working from home, but really you need a laptop. You can take this with you to clients’ premises for meetings and presentations. It will also allow you to work on the go, anywhere from coffee shops and motorway service stations to your back garden 🙂

Printer – You won’t need this all the time, but for some tasks it’s essential. Get a good quality laser model that will print in black and white or in colour. You could also get a multi-function device that serves as a scanner and photocopier as well.

Internet Connection – You will need a reliable broadband internet connection for email, website work, research, etc. It will also let you use Skype for phoning clients across the world and apps like Zoom for meetings and tele-conferencing.

Smartphone – This will allow you to keep in touch with clients when you are away from home, and also keep you up to date with emails and social media. For some jobs a smartphone camera can come in useful.

Business Cards – These are an essential marketing tool. You don’t need anything too jazzy, but they should look smart and professional. Moo.com is a website offering high-quality business cards printed to your specifications, and you can order as few as 50 if you wish.

There may also be other tools and equipment you need, depending on the services you intend to provide.

One thing you DON’T need when starting out is a dedicated office. If you have one in your home (or elsewhere) that’s great, but otherwise anywhere you can set up your laptop will be fine. Even a corner of the kitchen table is okay, as long as you aren’t being constantly interrupted. Many VAs work for at least some of the time in co-working spaces and even coffee shops and bars.

Services You Can Offer

I’ve already talked about some of the services offered by VAs, but there are plenty more as well. Here is a list to set you thinking. Clearly you don’t have to offer all the following, but the more you have in your repertoire, the more demand there is likely to be for your services.

Website and Graphic Design

Website Maintenance and Updates

Online and Offline Marketing and Promotion

Accounting/Bookkeeping

Data Entry

Creating PowerPoint and SlideShare Presentations

Desktop Publishing

Handling Travel Arrangements

Proofreading and Editing

Report and Article Writing

Minute Taking

Blogging and Podcasting

Market Research

Secretarial Services

Transcription (General, Legal, Medical, and so on)

Database Management

Personal Assistant Services

Event Planning

Technical Support

Coaching/Consulting

Staff and Manager Training

Customer Service

One thing to bear in mind is that the more specialized your services are, the less saturated the market will be. It is therefore important if you have specialist skills or expertise to look for ways you can use them to your advantage to create a niche for yourself (and boost your fees). If you speak a second language, for example, you may want to target potential clients who speak this language and/or have clients that do.

It’s also important to take the time to update your skills and add new ones. The 21st century workplace is constantly changing, with corresponding changes in the services clients are looking for. Be prepared to invest a proportion of your earnings in training and personal development, so your skills remain in high demand.

Your VA Website

However good your skills, nobody is going to beat a path to your door to hire you. You will need to market yourself, and one essential tool for doing this is a website.

Nowadays a basic one-page site with a photo and a bit of text won’t cut it. As an aspiring virtual assistant you need to come across as someone at ease in the world of business who knows how to present themselves professionally (online as well as off-). Your website is your shop window, and you will be judged on it!

Unless you have website design/building skills yourself, you may want to consider hiring a professional in this field and get them to create your site for you. The end result will look much more professional. Hiring a designer will cost you money, but it should more than repay itself in the higher fees you are able to negotiate. Search online for website designers and take time to check out examples of their work.

Your website should outline the range of services you offer, and be easy to read and navigate. There is no need for fancy graphics or animations – a clean, readable layout is far more likely to impress potential clients.

One other thing is to try to ensure that your website is search engine optimized by incorporating relevant keywords and phrases throughout the content. The aim here is to ensure that your site ranks high in the search results of people looking for someone providing the services you offer.

If money is tight initially, you could start by using a free website builder such as Blogger.com. Sooner or later, however, there is much to be said for building your website on a self-hosted WordPress platform (as I use for Pounds and Sense). There are many excellent free and low-cost themes you can use that would work well for a VA (I use Themify personally).

A well-designed WordPress site should send a strong message about your skills and professionalism to potential clients. In addition, running such a site will help hone your own WordPress skills, which (as mentioned earlier in this article) are much in demand among businesses.

Marketing Your Services

A website is, of course, an essential marketing tool, but there are many other things you can do as well.

One of the most powerful is networking. The chances are if you are setting up as a virtual assistant, you have previously worked for businesses and other organizations. So let them know that you are now offering your services on a freelance basis, and make full use of any contacts you may have.

In addition, there are agencies for VAs that you can join to find work. One of the best known is Time Etc. They match up virtual assistants with businesses (and solo entrepreneurs) who need their services, and pay them an agreed hourly rate. You can apply via this page of their website.

Some other marketing methods you can try include the following:

Go to business conventions and exhibitions (once these are running again) and introduce yourself to any exhibitors you think might be in the market for your services. Don’t forget to take along a good supply of business cards.

Set up a profile on the career networking website LinkedIn. As with your website, use this to set out the skills and services you offer. Send invitations to anyone you know in business to build your network, and join any relevant special interest groups.

Set up a Facebook business page and Twitter account and use these to help promote yourself as well. Do this in a low-key way, to avoid putting people off following you. Share interesting links and even the occasional humorous item, along with reminders of the services you offer.

You may also want to list yourself on job auction sites such as People Per Hour. On these sites would-be clients list tasks they want done and freelances can then bid on them. Fees are likely to be on the low side for VAs who are just starting out, but nonetheless they can provide a way to gain experience (and references) – and in some cases a one-off job can lead on to a long-term contract.

More Top Tips

Here are a few more tips for anyone starting out in this field…

Always back up work you are doing for clients and (especially) any original documents you receive from them. Never assume clients have kept copies themselves! It’s best to back up everything at least twice, once to a separate device such as a USB stick and once to a cloud-based storage solution such as Google Drive.

For many jobs you’ll be paid by the hour, so to keep a record it’s worth investing in some time-tracking software. Toggl is a good basic time-tracker that is free for use by individuals and can keep track of time spent on any number of projects.

Ask for feedback from clients when you have completed a job for them. Good comments can be incorporated as testimonials on your website (with the clients’ permission), but criticisms are valuable as well, as they reveal ways you can improve the service you offer.

Keep in touch with former clients and, without being pushy, try to ensure you remain at the forefront of their minds if another job comes up you might be suitable for. If you start offering a new service, for example, that could be a good pretext for an email or even a phone call.

Consider joining one of the professional associations for VAs. There are several you can choose from, but my recommendation would be the IVAA (International Virtual Assistants Association). Members enjoy a range of benefits, including training and mentoring, a private Facebook group, a listing in a public directory of VAs, and more. For further information, see their website at www.ivaa.org.

It’s also well worth checking out The VA Handbook website and blog. This is run by UK virtual assistant Joanne Munro and is a treasure trove of advice and resources for aspiring VAs.

Closing Thoughts

I hope in this article to have opened your eyes to a way of making money from home you may not have considered before. If you have administrative and/or secretarial skills, setting up as a virtual assistant can provide you with a good living that fits in with your lifestyle and family circumstances.

You can work full-time or part-time, whatever suits you best. You can specialize in the sort of work that interests you most, and can pretty much guarantee that every day will offer new challenges and surprises.

While a majority of VAs are female, there is nothing to stop men becoming VAs as well, as long as they have the skills and experience required. Being a VA can be a great option for older people too, allowing them to work flexibly from home while making use of skills they may have honed over many years in the workplace.

What’s more, now is a great time to be entering this field. With the coronavirus pandemic, more and more companies (and individuals) are realizing the benefits of engaging home-based VAs. If you can provide the services they want, an ever-expanding range of opportunities is out there.

Another attraction of VA work is that potential clients may be located anywhere. Most of the tasks a VA does can be performed remotely using the Internet and phone – so there is nothing to stop you working for anyone, anywhere in the world.

And equally, as a VA you can – if you choose – work in ‘real world’ locations as well. As the rules about lockdown and social distancing are eased, you might be asked to do anything from organizing events and conferences to training clients’ staff in their offices, or even looking after clients’ homes while they’re away. It’s entirely up to you what services you choose to offer, and when and where you want to do so.

Good luck, and I hope you make lots of real money as a virtual assistant!

As ever, if you have any comments or queries about this article, please do post them below.

If you enjoyed this post, please link to it on your own blog or social media:

As you probably know, during the initial coronavirus lockdown, buying and selling property was almost impossible.

As restrictions are slowly easing, however, house buying and selling has become feasible again. Estate agents have been reporting a big upsurge in enquiries, as the long period of confinement to home has made many people more aware of the shortcomings of their current properties!

Of course, buying and selling houses while the virus remains a threat requires risks to be mitigated as much as possible. That means wearing gloves and masks when meeting agents, buyers or sellers. Following the standard hygiene rules about hand-washing and using hand sanitizers before and after any personal meetings is also vital.

The New Normal

With the need for social distancing and other precautions to reduce the risk of transmitting the virus, valuing and viewing properties has become more challenging. Most agents now offer virtual viewings – generally using a mobile phone camera – as an alternative to personal visits.

Vulnerable customers: customers that fall under the ‘vulnerable’ group as advised by the government, should let their local Yopa agent know and will then be offered a virtual valuation or viewing until there is government advice that the safety of this group is no longer a concern.

Preference: we appreciate that not everyone will want a face-to-face meeting with a Yopa agent yet – in which case, we will happily offer a virtual alternative as we have successfully throughout lockdown to date. We will keep in touch with you to understand if your preferences change as more information is issued by the government on infection rates and virus control.

Travel: we would advise our customers, where possible, to restrict travel on public transport to attend a valuation or a viewing.

Minimise contact: we ask that, at a minimum, only the buyer or seller of a property is present at a viewing or valuation – no other parties. All non-Yopa attendees should be from the same household. We would advise that we conduct viewings and valuations without the vendor present.

Distance: When meeting with a Yopa agent on a valuation or a viewing, where possible stand at a 2m distance and refrain from shaking hands.

On the property:

Gaining access: For vendors, your Yopa agent will call you when you are outside the property to gain access. For buyers, please call your Yopa agent when outside the property to gain access.

Duration: Valuation and viewing time should be kept as short as possible to minimize risk.

Air flow: we politely request that all windows and doors are opened in advance of the valuation or viewing where possible, so the Yopa agent and vendor/prospective buyer can move through the property without touching door handles or surfaces.

Refreshments: whilst very kind of our vendors to offer, we politely ask that refreshments are not offered to our agents whilst on the premises.

Documentation: as we are a digital business, no paper documentation needs to be transferred between Yopa and our customers – it can all be managed electronically.

Post valuation or viewing: if people have been shown around your current home, you should clean down surfaces, such as door handles, after each viewing with standard cleaning that products.

Yopa say that vendors conducting their own property viewings should complete these in accordance with the recommendations above.

If you are thinking of selling your home, an online agency such as Yopa is well worth considering.

They offer a full service, and say they can do anything a traditional estate agent does. They are also open at evenings and weekends.

Yopa charge a fixed fee which is agreed in advance, and never add commission. You can choose to pay when your home is sold, or up-front if you prefer.

Although Yopa are website-based, they have local agents whom they say will be with you at every step until your home is sold. You can also monitor viewings, offers and feedback any time you wish using the YopaHub online dashboard.

Finally, other services offered by Yopa include help with mortgages and conveyancing (via their commercial partners). In addition, every homeowner gets a free utilities switching service.

Final Thoughts

If you’re considering moving, it’s definitely not too soon to get started and benefit from the pent-up demand from other would-be buyers and sellers.

So why not check out the Yopa website today and see if their service could be the one to help you make your next move and find the home of your dreams 🙂

As always , if you have any comments or questions about this post, please do leave them below.

Disclosure: This is a sponsored post on behalf of Yopa. It includes affiliate links, so if you click through and end up making a purchase, I may receive a commission for introducing you. This will not affect in any way the service you receive or the price you pay.

If you enjoyed this post, please link to it on your own blog or social media:

At the risk of stating the obvious, the last few months have been stressful for all of us.

As mentioned in this post last month, a YouGov survey in May found that over a third of respondents (39%) reported a decline in their mental health since March 2020, when the lockdown and other anti-virus measures started. A month on, it’s quite likely that figure would be even higher.

I’ve certainly noticed that I am feeling more stressed and anxious than usual, and I’m luckier than many. Although I live alone, I do have a large house and garden, and also have the advantage of years of experience of working from home. How people in tower block flats have been coping is hard to imagine, particularly if they have young children they are home-schooling as well.

I was keen to find out what methods other people are using to preserve their mental health in these challenging times, so I asked some fellow UK money bloggers what worked for them. I was intrigued by their varied replies, so I’ve set out their comments below. I’ll share some of my own thoughts and experiences afterwards

What Are Other Bloggers Doing?

Emma from Bee Money Savvy says, ‘Writing lists has been my saviour these last few months. I get down if I don’t feel like I’ve achieved much in a day, so having a list of things I’ve managed to do (even small things like eating a healthy breakfast or putting a wash on) has helped me feel somewhat productive and more positive about the day I’ve had.’

Bex from How to B Welthy says her strategies include reading self help books e.g. Good Vibes, Good Life, along with breathing exercises, meditation, getting a good night’s sleep and going out for a walk. She adds that she suffers with mental health issues constantly, though, not just in lockdown.

Collette from Cashback Collette writes, ‘Ive been trying really hard to get outdoors at least once a day either for a walk or a jog – sometimes with my fiance or on my own to clear my head and get some fresh air and vitamin D. I’ve also found I’m in a much better mood and feel more positive on days I speak to friends and family, so I have been chatting to them as much as possible.’

Claire from Money Saving Central says, ‘I have been having an hour to myself in the garden or upstairs every day, once my partner gets in from work. I am not used to all this background noise of iPads, TVs, and children whilst I am trying to work. I really need to sit quietly for just an hour to let my head breathe.’

Blogging duo Joleisa from Joleisa.com say, ‘We have been doing two things really to help us keep sane: crafting, and checking in virtually on elderly friends. We’ve always thought that showing concern for others gives you a boost too.‘

Jennifer from Monethalia says, ‘What’s really helping me is exercising every morning. I’ve never been a gym person but since lockdown happened, I’ve started doing home workouts.’

Nicola from The Frugal Cottage says, ‘I’ve been trying to stay in a routine and focus on finding something positive each day. This is easier on some days than others!’

Pete from Household Money Saving says, ‘I have been watching old box sets on Netflix. I’ve found it comforting to watch something familiar that reminds me of calmer times.’

Charlotte of Charlotte Musha says, ‘Gardening and in particular weeding have been the best thing for my mental health during lockdown. It’s one of those small jobs that make a big difference, so you always feel like you’ve achieved something.’

Laura from Harley Counselling writes, ‘I’m a talking therapist and counsellor, and one of the top tips I’m giving to my clients is to actively build a positive structure into their routine. Designating certain days for activities which we know are good for us gives us a sense of rhythm and familiarity. Things like going for a walk or run, meditation, reading, journalling or gardening can be really restorative and give us space to order our thoughts.’

Katie from Student Skint says, ‘The first 6-8 weeks it was running errands to help give me a reason to get out of the house. But now since rules have eased a bit, it’s making plans to see other people. I find that if I have plans with a friend (or friends) a couple of times a week then it feels more ‘normal’ because I’m seeing and speaking to the people I usually would in person.’

Dan from The Financial Wilderness writes, ‘I meditate. Personally I use the Headspace app which is fantastic, but there are other great resources both free and paid out there.

I always though meditation was a bit, er, ‘woo-woo’ and was deeply skeptical, but I can honestly say after trying it for some time I really notice the benefits, feel calmer and am able to control my thoughts a lot better.’ Dan adds, ‘I am also really enjoying picking up my PlayStation again. I loved gaming throughout my teens but find life is often too busy to be able to – it’s been lovely to rediscover that pleasure.’

Zoe of Eco-Thrifty Living comments, ‘I wrote a blog post about how to deal with anxiety on a budget. I have suffered from anxiety and panic attacks in the past and have found things that have helped me. They include doing CBT – I link to some free online self help workbooks in the post, running, drawing and doing a risk register. Not mentioned in the post, but I also find hypnotherapy downloads can be really helpful.’

Joseph who blogs at Thrifty Chap says, ‘Photography. I have a photography YouTube channel and have previous discussed how my mental health benefits from it.’

Bear from Save Like a Bear writes, ‘For me it’s a combination of things: 1. Spending 99% of my social media time on 1-1 conversations rather than anxious scroll holes.

2. Taking a time out to cook dinner from scratch every night no matter how busy I think I am. This has been a good way to get creative and use up what’s in the cupboards because of shopping very rarely too.

3. I’ll echo all the great comments above about what a difference a bit of daily exercise/fresh air/vitamin D makes. I use those walks to listen to podcasts so learning something each day feels like a productive distraction.

4. Having a shutdown routine at night because sleep is so important.

5. This is a very money blogger thing to do, but I had a financial audit and made sure my money was exactly where I wanted it/changed a few systems. It’s one way to feel in control when the world is out of control.‘

Si of Financial Expert says, ‘I’ve been using the Headspace app for 10 minutes each morning to gain a 10 minute window of calm before I begin work. It must be working, as it’s three months in and I now look forward to it.’

Nicola from My Savings Journal says, ‘I’ve tried to let go of my own self-imposed ideas on how productive I should be and the desire to maximise every moment of my time. Instead, I’ve let myself explore hobbies, enjoyed time working on my blog, and tried new ways of keeping my home organised. It’s definitely helped to keep my anxiety and stress levels at bay, as well as creating a new “normal” in terms of balancing relaxation with productivity.’

Michelle from Time and Pence says, ‘I have made sure that we, as a family, have gone out on regular long walks so we have plenty of time out of the house. I believe that has been the real key to coping. While at home, lots of gardening, video chats and games with family and friends. And also we bought my son a keyboard for his lockdown birthday so we’ve all enjoyed learning how to play using tutorials on YouTube.’ And she adds, ‘My mom is shielding due to COPD and she ordered herself lots of painting by numbers, with all the equipment. She set herself a little art studio up at home and she has loved it. It’s made a massive difference to her.’

Rhian of Rhian Westbury says, ‘To keep my mental health high during this period I try and maintain a routine. I need to maintain a good sleeping pattern to maintain good mental health so I wake up every morning at near enough the same time as I would if I was going into the office. And I don’t stay up really late and maintain my normal bedtime. The routine helps me to continue as much as normal during this time.’

Emma of TuppenysFIREplace says, ‘We moved to the Lake District last year so we could spend more time on the fells, only to find they’ve been closed since lockdown. We are not used to being together quite so much so decided we needed to plan our days to counter this. We have regular ‘date nights’ at home where we dress up as if we were going out, and we have at least one TV/internet-free night so we can focus on quality time together. Makes up for the little spats that happen during the day!’

Thank you very much to all my money blogging colleagues for sharing their thoughts. I do hope you found them as interesting as I did, and they may have given you one or two ideas for coping strategies you could try as well.

One thing that did surprise me a bit is that nobody mentioned baking, which I know has been very popular during lockdown. I was also surprised that there was little mention of video gaming, as I hear lots of people during this time have been escaping into the virtual worlds of Animal Crossing (see picture below), Stardew Valley, Minecraft and so on 🙂

My Own Coping Strategies

So what have I been doing to try to preserve my sanity through this challenging period?

As mentioned in my earlier update, I am finding daily walks therapeutic. I especially enjoy a walk after breakfast, and intend to keep this going even after the crisis is over.

Like many of my fellow bloggers (see above) I find it helpful to have a daily routine. After I return from my walk, I generally do a few hours’ work, usually on the blog or any other paid work (writing, editing or proofreading) I may have. I try to stop at lunch time and do other things from then on, though – I am meant to be semi-retired, after all!

I aim to speak to somebody every day, if not in person then over the phone or (occasionally) via Skype. Living alone I think that’s super-important. In the afternoons I go for another walk, or shopping, or spend some time working/relaxing in the garden.

I have a love-hate relationship with social media nowadays. On the one hand, it can be great for keeping in touch with friends and family, and I also use it as a source of news and information. On the other hand, with Twitter especially, there can be a lot of negativity, rudeness and even outright hatred (especially when politics raises its head). If I spend too long there I can feel my stress levels start to rise. I try to limit my time on social media – and recommend everyone else does likewise – but that isn’t always easy, as it pulls you in insidiously.

In the evenings I usually make an effort to cook something nice rather than relying on convenience foods (though they have their place). As mentioned before I typically seek out some escapist entertainment in the evening. This often involves watching one or two episodes of a box-set, even if it’s something I’ve already seen. Recently I have been re-watching the detective series Bergerac with John Nettles which – as you probably know – is set on Jersey. I enjoy the stories but also the lovely island scenery, which reminds me of holidays there and in Guernsey with Jayne in happier times.

Finally, when I am feeling particularly anxious, I find CBD Oil for Anxiety helpful for calming me down and helping to get a restful night’s sleep. Based on my experience it’s definitely worth a try!

Further Advice

I think my top tip to anyone who is struggling with their mental health at the moment is don’t be afraid to reach out for support if you need it. Speak to friends and family, and to health professionals if appropriate. There is also some great advice about looking after your mental health during the pandemic at www.mind.org.uk/coronavirus.

Money – or the lack of it – can obviously cause stress as well. The YouGov survey mentioned earlier found that nearly a quarter of people (24%) are avoiding talking about finances with friends and family, for fear of burdening them or making them anxious. The same survey also found that 36% of people said that the pandemic had already had a negative impact on their personal finances, with 35% trying to cut costs during lockdown.

Above all else, though, be kind to yourself, and don’t suffer in silence. And equally, if you know someone who may be struggling – or you just haven’t seen or heard from them for a while – reach out by phone or at least message them to check they are okay. It may be a cliche, but we really are all in this together. And pretty much everyone is struggling in their own way.

So that’s how I and my fellow UK money bloggers are getting through our days at the moment. But I’d love to hear what works for you. Are you baking for Britain or painting pebbles, writing your memoirs or tending your virtual island? Please post any comments or questions below as usual!

If you enjoyed this post, please link to it on your own blog or social media:

I’ve joined forces today with some of my fellow UK bloggers to put together a giveaway of a Maevea Rattan-Effect 4-Seater Coffee Set from B&Q. You can see a photo of it above.

This set is currently on sale for £541 on the B&Q website. Details – copied from the site – are as follows:

Create your own space in your garden with this modular rattan design Maevea coffee set.

Easily change the configuration when you have guests over, or want to try something a little different.

The space saving design is easy to store and keep tucked away in a corner when not being used.

The armchairs store behind the sofa for easy storage.

Easy to clean glass top table.

Features

removable cushion covers

exclusive to B&Q with a 2 year guarantee

this coffee set is modular – it has 4 different orientations

Armchair: 565 x 62 x 770mm

Table: 520 x 360 x 925mm

Sofa: 1550 x 700 x 795mm

You can see more information about the set (and more photos) on the B&Q website. If the chosen prize is no longer available when the draw is complete, another suitable garden set will be substituted.

Here then are all the details you need to enter, provided by my colleague Emma Drew (who is co-ordinating this event). Good luck! It would be great if a Pounds and Sense reader wins this great prize 🙂

Some UK bloggers have teamed up to offer you a fantastic giveaway for this summer, organised by Emma Drew. Keep reading to see who is involved and how to enter.

One final small point is that if a winning entry comes from following someone on social media, Emma will check before awarding the prize that the winner is still following the account in question. If they aren’t, they will be disqualified and a new winner drawn. So, please, don’t follow and immediately unfollow, as your entry won’t then count.

Good luck, and I really do hope you win this fabulous prize. But even if you don’t, I hope you enjoy entering and discovering some other amazing money bloggers!

As always, if you have any comments or questions about this post, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

As you may know, for many years I made my living primarily as a freelance writer. But I also had a sideline as a freelance proofreader and editor.

Obviously the skills required are closely related, and I enjoyed the variety of proofreading and editing work. I still do a bit today, though I am semi-retired now.

So in this post I thought I would discuss how to make money as a freelance proofreader and/or editor.

Let’s start with the basics, though…

What Do Proofreaders and Copy Editors Do?

Proofreaders perform a final check on the text of books and other written documents before they are sent to be printed. They mark up any errors they find using a standard set of proofreading marks (usually BS 5261 part 2). These corrections are then incorporated by the typesetter before the book goes to print.

Proofreaders are typically asked to work in one of two ways. They may be sent the author’s original typescript with the copy editor’s corrections marked on it, along with a copy of the proofs. In this case they are required to check that the typesetter has carried out all the editor’s instructions and not inserted any errors of his/her own. This task is known as reading against copy.

Alternatively, the proofreader may simply be sent a set of proofs and be asked to read through them checking for any errors (e.g. spelling, punctuation or factual mistakes). This is known as a straight (or blind) reading.

Either way, proofreaders generally make two marks per correction: one in the margin and another in the text itself. The idea is that the typesetter can glance down the margins to see where a correction might be required, and then look across the line in question to find it. This reduces the chances of a correction being overlooked.

Copy editors are involved at an earlier stage of the publishing process. They generally work with the author’s original typescript. As well as correcting spelling and punctuation mistakes, their task also includes correcting grammatical errors, checking for bias or possible libel, and generally polishing the text so that it reads well and conforms to the publisher’s house style. They also apply ‘weights’ to section headings (H1, H2, H3, etc.), so that headings and sub-headings are properly printed and arranged in a logical hierarchy.

Copy editing is a more creative task than proofreading, and also more demanding. Many freelances start off as proofreaders and perhaps graduate to copy editing later.

Both proofreading and copy editing are increasingly done electronically. That means working on screen, on a word-processed document rather than on paper. The underlying skills required are the same, of course, but you won’t be required to make the traditional proofreading (or editing) marks. You will, though, be expected to use ‘tracking’ to ensure that any amendments you make are easy to see (and can be reversed if the author or publisher dislikes them!).

What Do I Need to Get Started?

To start with, you must have an interest in language and a love of good writing. A good grasp of grammar, spelling and punctuation is essential, though you can take courses if you are not as strong in this area as you ought to be.

You will also need to learn the standard proofreading marks. These are reproduced on various websites (e.g. this one) and in a number of published books, e.g. The Writers’ and Artists’ Yearbook (see below).

You should also have a good modern dictionary to check spellings and usage, and – for copy editing at least – a style guide such as the Oxford Guide to Plain English (see below).

Clearly you will also need a computer and an internet connection. Even if you are working on paper in the traditional way, this will still be required for corresponding with clients, marketing your services, invoicing and record-keeping, and so on.

Who Will My Customers Be?

Your main clients will be book, magazine and newspaper publishers. You may also obtain work from businesses looking for someone to edit and proofread their brochures, newsletters, annual reports and so on. Writers and aspiring writers may also require your services – in the case of the latter, they may be hoping you can bring their work up to a publishable standard.

Other potential customers include design houses, advertising and public relations agencies, printers and typesetters.

How Much Can I Make?

For freelance proofreading, the NUJ (National Union of Journalists) Freelance Fees Guide recommends a minimum rate of £24.00 an hour and for copy editing a minimum of £28.00 an hour. In practice you may not always be able to get NUJ minimum rates when you are starting out. Equally, however, you may be able to negotiate rates above the NUJ minimum as you gain experience.

How Can I Sell My Services?

You could start by sending a mailshot to publishing houses offering your services. A good selection can be found in The Writers’ and Artists’ Yearbook, mentioned above. This is a highly competitive sphere, however, so it may be best to focus on those publishers who are active in areas where you have some specialist knowledge. If you are a keen birdwatcher, for example, you might decide to target specifically those publishers who produce ornithological titles. When you write, don’t forget to mention any relevant qualifications and experience.

Local businesses and advertising/PR agencies are also well worth trying. In addition, you could try advertising your services in publications likely to be read by potential clients. Several proofreaders advertise regularly in journals such as The Author and Writers News, and this can be a good way to attract business from writers. You could also try advertising in local business magazines and directories (online and off-).

Having your own website/blog and perhaps a Facebook page to promote your service is also highly desirable.

Where Can I Get More Help?

There are various distance-learning courses you can take in proofreading and copy editing. One long-established commercial provider is Chapterhouse. They offer a range of introductory courses in proofreading and copy editing. These cover the basics and will help you discover whether proofreading and editing is something you enjoy and have an aptitude for.

More advanced (and expensive) courses are offered by the Publishing Training Centre. These include short, classroom-based courses, online tutor-guided courses (leading to the award of a certificate of achievement from the Publishing Qualifications Board), and e-learning modules. If you want to gain an industry-recognized qualification, studying with the PTC is probably the way to go.

The professional organization for freelance proofreaders and editors in the UK (and overseas) is the Chartered Institute of Editing and Proofreading (CIEP). Members receive a regular newsletter and discounts on various publications. They are also entitled to a listing in the Institute’s Directory of Editorial Services. CIEP also run workshops and online training courses in proofreading and editing.

Final Thoughts

Freelance proofreading and/or editing can be a great part-time sideline, or even a full-time business. No special tools or equipment are required, so it’s quick, cheap and easy to get started. It’s reasonably paid, and you can work from home at hours to suit yourself.

It’s also suitable for older people and people with disabilities, with the one proviso that it becomes a little harder if – as in my case – your eyesight isn’t as good as it once was.

I am, however, still available for small- to medium-sized proofreading and editing projects – so if you need any help in this department, please do drop me a line!

I hope you have enjoyed reading this post. If you have any comments or questions, as always, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

A couple of months ago I wrote this blog post about my experience of the coronavirus pandemic and lockdown. Two months on, I thought it was time I provided another update.

As I said before, I live on my own since my partner, Jayne, passed away a few years ago. I am lucky to live in a fairly large house with a good-sized garden, so being mostly confined to home hasn’t been as big a challenge for me as I’m sure it has for some. Also, I am well used to working from home, having done this for the last 30 years or so.

Of course, that doesn’t mean the crisis hasn’t affected me in a variety of ways. As Pounds and Sense is primarily a money blog, I will (again) start off with that…

Financial

At the time I wrote my last update, world stock markets were in free fall. I was naturally concerned to see my equity-based investments – and in particular my pension fund – tumbling in value. Being 64 and semi-retired with my SIPP in drawdown, this was particularly worrying for me. But I tried to follow my own advice and avoid panicking and selling up.

Thankfully, in recent weeks stock markets have made an astonishing recovery. I am pleased to say that my pension fund and other equity-based investments are mostly back to near pre-Covid levels (and even in some cases above them).

Below is a copy of the six-month chart for my Nutmeg stocks and shares ISA. At one point this was down to just over £10,000 in value, but in just a few weeks it has climbed back to over £15,000. Admittedly I did put in an extra £1,000 when the markets were (as things stand now) close to their lowest point. Even so, it’s been an impressive rally.

Assuming there is no major second wave of the virus – and world-wide there has been no sign of that so far – I am hopeful that the recovery will continue over the longer term. Of course, there are likely to be bumps along the way, and in the short term at least we face the likelihood of an economic recession. Even so, I am keeping my fingers crossed for a recovery over the next year or so, and am continuing to invest cautiously where I see value.

As mentioned in this recent post, I did also decide to invest £7,000 – the proceeds of another maturing investment – in another vehicle for Buy2LetCars. As regular readers will know, I’ve had one (new) car with this car loan investment platform for about two years now, and the monthly repayments have been coming through like clockwork. So I decided to invest my £7,000 (the minimum investment with Buy2LetCars) in another car – a pre-owned one this time, of course.

I particularly liked the idea of investing again with Buy2LetCars, as they lease vehicles to key workers such as nurses and other NHS staff (along with teachers, prison officers, police, and so on). These people all need cars for their (essential) work. They are responsible individuals, and have every incentive to look after the vehicles (though as they are fully insured, investors don’t bear any risk from accidents themselves).

Unfortunately Buy2LetCars don’t tell you who has leased ‘your’ car, but I like to think the ones I have bought are providing transport and security for two hard-working NHS nurses at this moment 🙂

In May I received a modest but nonetheless welcome payment from the government’s Self Employment Income Support Scheme (SEISS). I was pleased to hear recently that the government is extending this for a further three months, albeit at a slightly lower rate. It does help a lot at this uncertain time, and I know for many self-employed people it has provided a lifeline.

Personal

Thankfully I have managed to avoid contracting the virus so far. I know a local family who probably all had it, but they are thankfully well recovered now.

I also know people who have been badly affected by the lockdown. One young man of my acquaintance was furloughed from his job and became depressed alone in his bedsit. He started drinking excessively and wound up in hospital, where he spent several days being detoxed and having his liver checked out. Thankfully he doesn’t appear to have suffered any long-term damage, but it does demonstrate the stress many people are under right now. As I’ve said before on PAS, it’s more important than ever to keep in regular touch with friends, relatives and neighbours, especially if they live on their own.

As for myself, I am doing my best to keep on an even psychological keel. Like everyone else, there are things I am missing. Top of the list is seeing friends and relatives, going for days out, pub lunches, and so forth. I am also missing swimming (which is probably affecting my fitness as well). And I am really missing seeing my hairdresser. For the first time in my life, I have been wishing that, like many men of my age, I had gone bald 😉

At least two concerts I booked tickets for were cancelled. I have also had to cancel two holidays this year (so far). I have just one other holiday arranged, a short break in Minehead in September. I am optimistic that this will still go ahead, though how exactly it will be affected by social distancing and other anti-virus measures remains to be seen.

I am very glad that the panic buying has stopped now, though certain things can still be difficult to buy locally. Supplies of flour, eggs and rice are still variable, and I found it more difficult than expected to get a bag of compost for the garden. Supermarket shopping – as I’m sure you know – is a very different experience these days. You have to allow time for queuing outside beforehand, and expect to be marshalled inside the store as well. But things generally are far better than they were, so I’m certainly not complaining.

I still take daily walks – sometimes even two now as the rules about that have eased. I particularly enjoy going out in the (fairly) early morning. The air seems fresher and there are fewer people about, so less need for zig-zagging to preserve social distancing. I also find it sounds more natural to say ‘Good morning’ or just ‘Morning’ to people I pass. ‘Good afternoon’ is a mouthful and makes me sound like the village policeman, while ‘Hello’ just sounds lame. It’s a shame English doesn’t have an equivalent all-purpose expression to the French ‘Bonjour’!

As the crisis has continued, I have been watching less and less TV. Partly there hasn’t been much that has captured my interest, and my attention span for things like films has reduced. In addition, I have found the endless debate about the virus – and especially the negative tone of much of it – depressing and demoralizing. Instead I have been watching a lot of catch-up comedy and drama, and DVD box-sets.

Among the latter, I am enjoying Deep Space Nine, a Star Trek spin-off series (actually seven series) that I mostly missed first time round. And for light relief, I am watching The Brittas Empire, a 1990s sitcom with Chris Barrie set in a leisure centre. I highly recommend this for a bit of undemanding, escapist fun!

I have also just finished re-watching The Singing Detective by Dennis Potter, again on DVD. If you haven’t seen this, it’s a brilliant, multi-layered, musical drama serial, superbly written and acted. Since I first watched it I have acquired a lot more experience of hospitals (where much of the action takes place) so that has given me a new perspective on the show. I was also struck that in the days when it was made, there was clearly nothing unusual about patients being allowed to smoke in their hospital beds. How times have changed!