Today I’m spotlighting a piece of official data about you that might seem dry and boring, but is actually crucial to ensuring you don’t pay more tax than you need to.

Your tax code is set by HM Revenue and Customs (HMRC). It determines how much income tax is deducted from your salary, wages or pension before you receive it.

Understanding your tax code and ensuring its accuracy can prevent you from overpaying (or underpaying) tax.

What is a Tax Code?

A tax code is a combination of numbers and letters that helps your employer or pension provider calculate how much tax to deduct from your income.

For example, a common tax code for the 2025/26 tax year is 1257L. This indicates that you are entitled to a tax-free personal allowance of £12,570, with tax due on any income you receive over this.

The letter in your tax code provides additional information about your circumstances, such as whether you have more than one source of income or are being taxed on an emergency basis.

How to Find Your Tax Code

Your tax code can be found on any of the following:

your payslip

your P60 or P45 (for those who have changed jobs or retired recently)

Here’s a breakdown of what the numbers and letters mean:

Numbers: Multiply the number in your tax code by 10 to calculate your tax-free allowance. For example, 1257 means you can earn up to £12,570 a year tax-free.

Letters: These Indicate specific circumstances.

L: standard personal allowance

M: you’ve received a marriage allowance transfer

BR: all income is taxed at the basic rate (20%)

NT: no tax is deducted from your income

S: taxpayers living in Scotland

C: taxpayers living in Wales (Cymru)

Common Reasons for Incorrect Tax Codes

Your tax code might be wrong if any of the following apply:

you’ve started a new job

you’ve received a pay rise or bonus

you’re receiving income from multiple sources

you’ve claimed or stopped claiming benefits like marriage allowance

HMRC hasn’t been updated about changes in your circumstances, such as retirement or moving abroad

What to do if Your Tax Code is Incorrect

Check your tax code: Review your payslip and/or other relevant documents to confirm your tax code.

Use the HMRC tax code calculator: This tool is available on the HMRC website. It can help you determine if your tax code is correct, based on your circumstances. It will also reveal your annual tax-free allowance.

Contact HMRC: If you suspect an error, contact HMRC directly. You can do this by any of the following means:

When contacting HMRC, have the following information ready:

National Insurance number

details of all income sources

recent payslips or P60s

Of course, if you have an accountant, you may prefer to ask him or her to handle this for you. Accountants are well accustomed to dealing with these matters and will normally be happy to contact HMRC on your behalf.

Adjustments and Refunds

Once HMRC updates your tax code, your employer or pension provider will use the new code in your next payslip. If you’ve overpaid tax, HMRC will issue a refund automatically or else adjust your tax deductions in future months.

Preventing Future Errors

To avoid future tax code errors:

inform HMRC promptly about changes in your income or circumstances

regularly check your payslip and tax code notifications

By staying proactive and understanding your tax code, you can ensure your finances remain in order and avoid any unpleasant surprises when it comes to your taxes.

As always, if you have any comments or questions about this post, please do leave them below.

An earlier version of this article was first published on the Mouthy Money website.

If you enjoyed this post, please link to it on your own blog or social media:

As I write this, the UK is enjoying a period of fine summer weather; but of course autumn and winter will be along soon enough.

With energy prices continuing to rise, it’s more important than ever to explore ways to cut your home heating costs while staying comfortable.

An increasingly popular solution is a smart thermostat. But what exactly are these devices and can they really save you money? In this post I’ll try to answer these questions and discuss my own experiences with one.

What is a Smart Thermostat?

A smart thermostat is an internet-connected device that allows you to control your home’s heating (and sometimes cooling) remotely via a smartphone app, tablet or computer.

They may use advanced technology such as machine learning, motion sensors and geolocation to optimize your heating schedule, based on your habits and preferences.

Unlike traditional thermostats, which require manual adjustment or rely on fixed schedules, smart thermostats can automatically learn your routines and adjust your heating to ensure comfort and energy efficiency.

Smart thermostats will work with most (but not all) boilers, including gas, heating oil and electric boilers. It is also possible to use them with heat pumps, but you will need a special type of smart thermostat that works a bit differently. In this post I will concentrate on smart thermostats for ‘traditional’ heating systems. This article has some useful information about smart thermostats for heat pumps.

Benefits of a Smart Thermostat

Energy savings – Smart thermostats can significantly reduce energy wastage by heating your home only when needed. For example, they can lower the temperature when you’re out and preheat the house before you return.

Remote control – Forgot to turn off the heating before leaving the house? No problem. With a smart thermostat, you can adjust settings from anywhere using your smartphone.

Insights and reports – Most smart thermostats provide detailed energy usage reports, helping you understand your consumption patterns and identify opportunities to save money.

Smart integrations – Most models integrate with voice assistants like Amazon Alexa, Google Assistant, or Apple HomeKit, allowing for hands-free adjustments.

Top Smart Thermostat Brands

Here are the three most popular smart thermostat brands available in the UK, along with their pros and cons.

Table of Contents

1. Nest Thermostat (Google)

Pros

sleek design and intuitive interface

learns your habits and automatically creates a heating schedule

works seamlessly with Google Home and integrates with other smart devices

energy-saving features like ‘Eco Mode’ when you’re away

Cons

higher up-front cost compared to some competitors

limited compatibility with certain heating systems

2. Hive Active Heating (British Gas)

Pros

easy to use and install

works with a wide range of heating systems

excellent app interface with multiple scheduling options

offers add-ons like smart radiator valves and light bulbs for a complete smart home experience

Cons

lacks advanced learning features compared to Nest

some additional features require a monthly subscription

3. Tado Smart Thermostat

Pros

strong focus on energy efficiency with geofencing and open-window detection

offers granular control with smart radiator valves

provides detailed energy-saving reports

compatible with almost all UK heating systems

Cons

subscription required for premium features like geofencing

simpler design might not appeal to those looking for a high-tech aesthetic

My Experience

I got a Hive smart thermostat for my gas central heating in October 2024. I chose this based on the advice of my regular heating engineer, Dave. He has a Hive himself and recommended it for its simplicity and ease of operation.

I paid Dave to supply and fit the device, for which he charged around £300. If you’re a keen DIY’er it’s perfectly possible to install a smart thermostat yourself, maybe with the aid of an online guide and/or YouTube video. Personally I was happy to leave the manual parts of the job to Dave, though I assisted with the electronic and online aspects.

With a Hive (and I assume other smart thermostats) you basically get three components. There is a hub you have to connect to your router using a cable; the thermostat itself, which I have on the wall of my living room (though you can detach it and move it from room to room if you like); and the main control unit, which is where my old controller used to be in the kitchen. You’ll also want to download the relevant app, so you can control the heating using your phone.

Set up was pretty straightforward. The only delay was when connecting the app. For some reason this took a few tries (Dave told me this was common in his experience), but we got there eventually.

I set up a weekly schedule for my heating and hot water, and after that basically let the thermostat do its thing. I’ve found the insights page on the app really helpful for seeing temperature changes in the house throughout the day and when the heating has cut in and out. This works far more efficiently than my old manual thermostat ever did, and is undoubtedly saving me money by only heating the house to the temperature I require.

One small issue I experienced was that initially I kept getting a message on the app that the internet connection was weak. After a bit of research I discovered this was being caused by the fact I’d left the Hive hub too close to my router. Once I moved it a couple of feet, the problem vanished and never returned.

Hints and Tips for Making the Most of Your Smart Thermostat

Here are some tips on maximizing the energy-saving potential of your smart thermostat.

1. Let it learn your routine

If your smart thermostat has a learning feature (like the Nest), give it a week or two to adapt to your schedule. Avoid making constant manual adjustments, as this can interfere with its ability to learn.

2. Use geofencing features

Many smart thermostats, such as Tado, use geofencing to adjust the heating when no-one is home. Ensure this feature is activated and that your phone’s location services are enabled for the app.

3. Set realistic temperatures

Aim for a comfortable yet energy-efficient temperature, typically around 18-21°C. Lower the temperature slightly at night or when you’re away to save more.

4. Take advantage of zones

If your system supports zoning (e.g. Hive with smart radiator valves), heat only the rooms you use regularly. For instance, keep bedrooms cooler during the day and focus heat in living areas.

5. Schedule around your lifestyle

Use scheduling tools to preheat your home only when necessary. For example, program the heating to turn on 30 minutes before you wake up or arrive home.

6. Use insights to adjust habits

Review the energy usage reports provided by your thermostat’s app to identify patterns of wastage. Adjust your settings accordingly to reduce unnecessary heating.

7. Integrate with smart home devices

Pair your thermostat with voice assistants like Alexa or Google Assistant for convenient control. You can also integrate it with other smart home devices, such as lights or sensors, for automated routines.

8. Utilize holiday modes

Going away? Use the vacation or holiday mode to keep your home at a low but frost-protecting temperature while minimizing energy use.

9. Check compatibility with your boiler

Ensure your boiler and heating system are compatible with your chosen thermostat. This will avoid efficiency issues and ensure full functionality. Personally I have a traditional heating system with a separate hot water tank, but others will have a more modern combi boiler. It’s essential to purchase the right smart thermostat for your system (Hive have two different versions for traditional and combi systems, for example).

10. Stay updated

Keep your thermostat’s firmware up to date. Manufacturers often release updates to improve efficiency, fix bugs or add new features.

Bonus Tip: Combine with other energy-saving measures

Combine your smart thermostat with energy-efficient practices, such as proper insulation, draught-proofing and using energy-saving curtains, for even greater savings.

In addition, try turning down your thermostat by one degree. According to the Energy Saving Trust, this can save you up to £145 annually on your heating bills.

Closing Thoughts

So can a smart thermostat save you money? My short answer is yes – though how much will depend on your usage habits and the size of your household.

By reducing energy wastage, offering precise temperature control, and providing actionable insights, it is estimated that a smart thermostat can lower your energy bills by 10-20% annually. This can translate to savings of £100-£200 a year.

While the initial investment for a smart thermostat may seem steep (ranging from £100 to £300, plus installation), for most people the long-term savings should outweigh this. Additionally, some energy providers offer discounts or schemes to help with purchase.

A smart thermostat isn’t just about saving money, though. It’s also about convenience, comfort and doing your bit for the environment by reducing your energy consumption.

Whether you opt for Nest, Hive or Tado, investing in a smart thermostat should set you on the path to a more energy-efficient and comfortable home.

As always, if you have any comments or questions about this post, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

As a Pounds and Sense reader there’s a good chance you’ll be familiar with the FIRE concept already. But just in case you’re not, it stands for Financial Independence, Retire Early.

The term was first coined in the US but soon crossed the pond to Britain and Europe. FIRE involves working hard to make (and save) as much money as you can, until you have enough capital to give up your day job and retire early.

At first glance it sounds appealing, but as you’ll gather from the title I’m not a fan. In this article I will explain some of the reasons I recommend caution when contemplating a FIRE strategy, starting with the one I regard as most compelling…

Table of Contents

1. Life Doesn’t Always Go To Plan

When you’re in your twenties or even thirties, it’s tempting to believe you can plan your whole life year by year, decade by decade.

As a FIRE aficionado, you might intend to put your nose to the grindstone for 20 to 30 years and retire in middle age, leaving you free to do whatever you want for the rest of your life.

That’s great in theory, but one thing my 69 years have taught me is that life may have other plans. Sadly, none of us knows when the Reaper will come calling. I’ve had friends and relatives who have passed away at all ages, from their twenties to their sixties. Around one in five men don’t live long enough to collect their state pension, which is a sobering statistic.

Even if that doesn’t happen, other life events can throw a big spoke in your FIRE wheel. These include accidents, serious illness, disability, separation and divorce, losing your job, and so forth. These are things you can’t plan for but they happen all too often. The danger then is that you may have ‘wasted’ the good years that came before.

Let me tell you about my partner, Jayne. She became seriously ill soon after her 50th birthday and passed away four years later. That was clearly tragic, but one small scrap of comfort is that in her early forties she decided to go part-time in her teaching career, to have more time for other interests. We also decided that, as we both enjoyed travel, we would fit in as many trips as we could, even though money was often tight. We had some wonderful holidays that would never have happened if we’d both been working all hours and saving frantically for a future that in her case would never happen.

2. Are You Willing to Write Off the Best Years of Your Life?

If you’re assiduously pursuing FIRE, you will be working your socks off during the day and scrimping and saving in your leisure time. Is this really how you want to spend what are arguably the best years of your life?

An example here is my old schoolfriend Phil (name changed). Phil was the brightest guy in my class (and probably the whole school). He aced all his exams and went to Oxford, where he got a first class honours degree in Agriculture and Forestry. Everyone predicted a stellar career for him.

Except that was never Phil’s plan. He was into FIRE before the term was even invented. He told me he was going to retire at forty. So he took a job he didn’t enjoy but paid well. He saved every penny he could, even running an ancient Austin A40, for which he didn’t have to pay road tax. He even taught himself mechanics and welding, so he didn’t have to waste money on garage fees.

Phil used to visit me and Jayne when we were younger. We admired his intellect and his single-minded determination, but did wonder about the price he was paying. He never (to my knowledge) had a relationship, and never went to concerts, the theatre or anything like that. We took him to a Chinese restaurant once, and he told us he had never been in one before (by this point he must have been in his late thirties). It certainly wasn’t a lifestyle either of us envied or would have chosen for ourselves.

3. What Will You Do When You Achieve Your Goal?

My friend Phil duly achieved his ambition. He was good at investing (naturally) and accumulated enough money to retire at his target age of forty. He then began devoting himself to volunteer conservation work.

So far so good, but he became more and more of a recluse. He became physically ill and (I’m pretty sure) mentally as well. He broke off all connection with us and other friends. Last time I heard, he was living alone in the New Forest. I hope he is happy but am not convinced this is really a blueprint for how anyone should live their life.

If you have a clear vision of what you want to do when you’ve achieved FIRE, that will undoubtedly help. If you don’t, though, that should set off an alarm that you need to think very carefully before proceeding.

Even if you do have a plan – as Phil did – your post-FIRE life may not turn out to be as fulfilling or enjoyable as you hoped. How will you feel then about all the privations in the years leading up to it?

4. What About Work-Life Balance?

You may disagree, but it does seem to me that FIRE and work-life balance are two concepts that are almost by definition at odds with each other.

For most people, their aim is to achieve a good work-life balance from day to day, with time for work, family, leisure, holidays, hobbies, and so on. For FIRE enthusiasts, however, the balance is more over the course of a lifetime, with work dominating the earlier years and ‘life’ the remainder. Aside from the risks mentioned above in assuming you can plan your whole life this way, that doesn’t seem like a recipe for good physical or mental health to me.

Final Thoughts

So those are some reasons I’m dubious about pursuing a FIRE strategy.

Of course, I’m not saying you shouldn’t save for the future or indeed make sensible economies. But from my perspective as a 69-year-old, I strongly believe in striking a balance between making the most of your life today and planning prudently for tomorrow.

We only get one life, and sacrificing (say) twenty-five years of it for a very uncertain future is a huge gamble. In my view it’s a journey you should think very carefully about before embarking on.

Better, in my opinion, to seek work that brings you satisfaction and fulfilment rather than merely being a means to an end. Make the most of everything life has to offer while you still can, since – as I well know – none of us can ever be sure what the future will hold.

Or as the old Guy Lombardo song (see below) has it: ‘Enjoy yourself, it’s later than you think!’

As always, if you have any comments or questions about this article, please do leave them below.

An earlier version of this article was first published on the Mouthy Money website.

If you enjoyed this post, please link to it on your own blog or social media:

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

As regular readers will know, in June I transferred most of the money in my Nutmeg Fully Managed portfolio (just under £25,000) to a new Nutmeg Income Portfolio. I discussed this in detail in this recent post, but basically money in this port is invested to generate an income from dividends and other sources. This is then paid monthly. Capital appreciation is targeted as well, but basically these portfolios are aimed at older people (and others) who want/need their investment to generate a regular cash income.

My Income portfolio hasn’t yet generated any income for me. I assume that is because there is a qualifying period before you become eligible to receive dividends (I have asked Nutmeg for clarification about this and am awaiting an answer). Income is due to be paid in cash to my bank account on the 24th of each month, so hopefully I will have some income accrued by August 24th (check out next month’s Update to find out!).

Nutmeg have now confirmed I was basically correct above. They point out that – like all Nutmeg investments – the money in income portfolios is held in the form of ETFs (exchange traded funds). They say: ‘Usually for an ETF to pay a dividend, it is one month after it is recorded. Taking the example of the JP Morgan Global Equity Premium ETF, [a dividend] was declared and recorded in early July and will be paid in August.” It would therefore appear that you have to be invested for between one and two months to start receiving monthly payouts. Nutmeg say I can expect to receive my first income payout on August 24th, so I will await this with interest 🙂

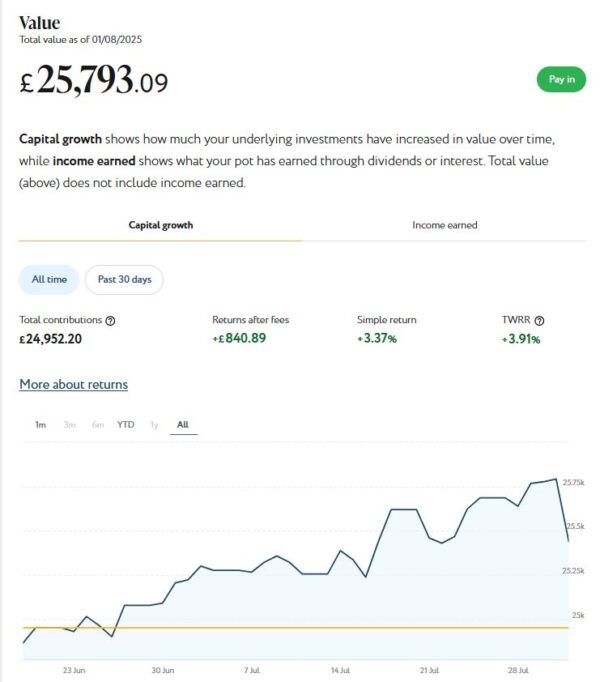

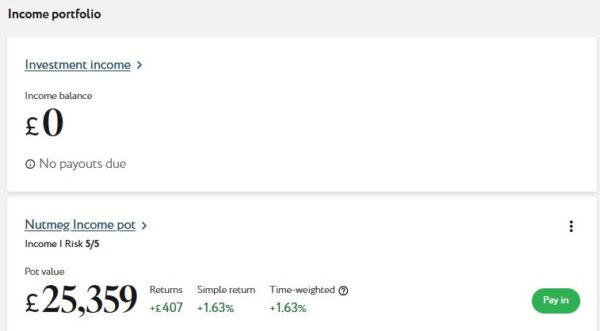

The better news is that this portfolio has grown in value in July. It’s now worth £25,793 compared with £25,092 at the start of last month, an increase of £701 or 2.79%. As the screen capture shows, this portfolio has actually grown in value by £840.89 since I opened it.

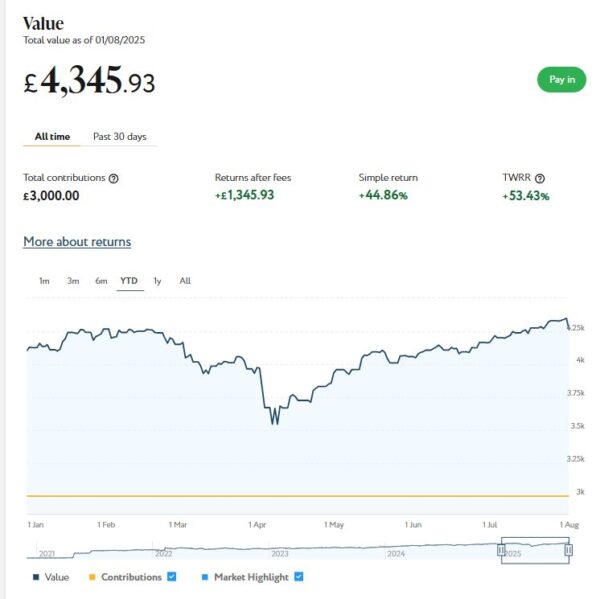

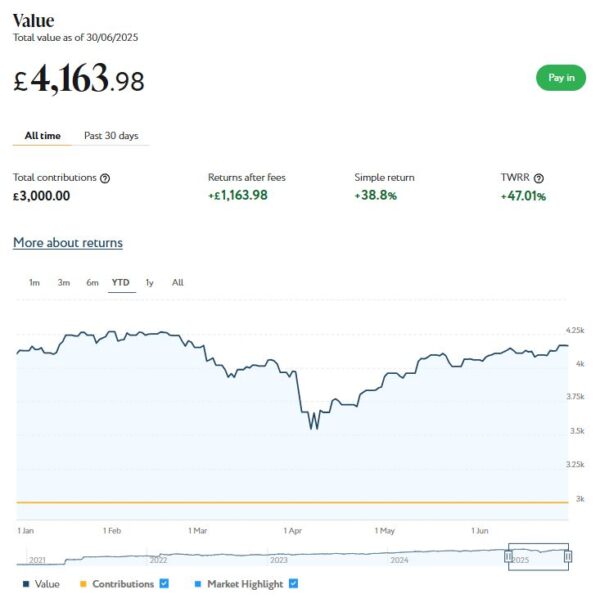

I still have a smaller, growth-oriented pot using Nutmeg’s Smart Alpha option. This is now worth £4,346 (rounded up) compared with £4,164 a month ago, a rise of £182. Here is a screen capture showing performance for the year to date.

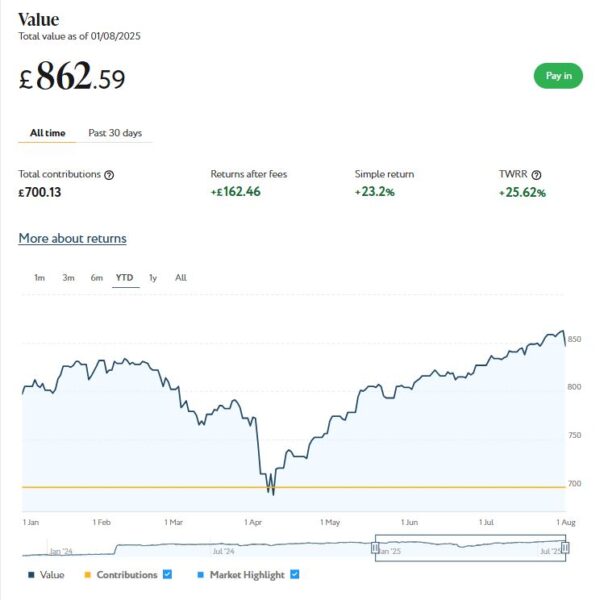

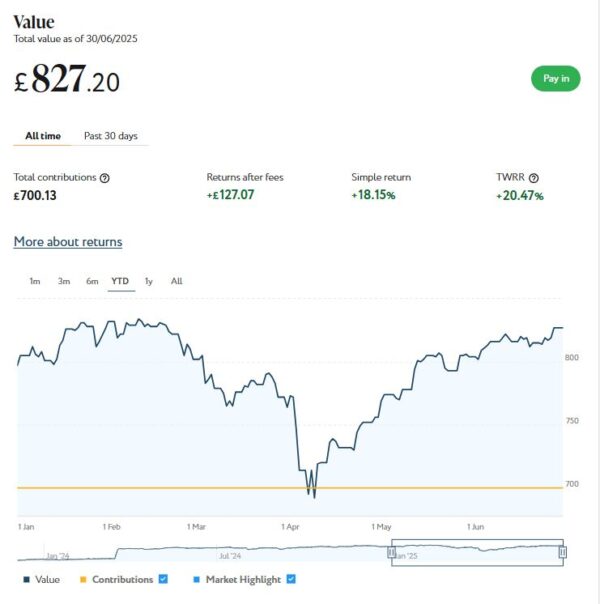

And at the start of December 2023 I invested £500 in one of Nutmeg’s thematic portfolios (Resource Transformation). In March 2024 I also invested a further £200 from referral bonuses. As you can see from the YTD screen capture below, this portfolio is now worth £863 (rounded up) compared with £827 last month, a rise of £36.

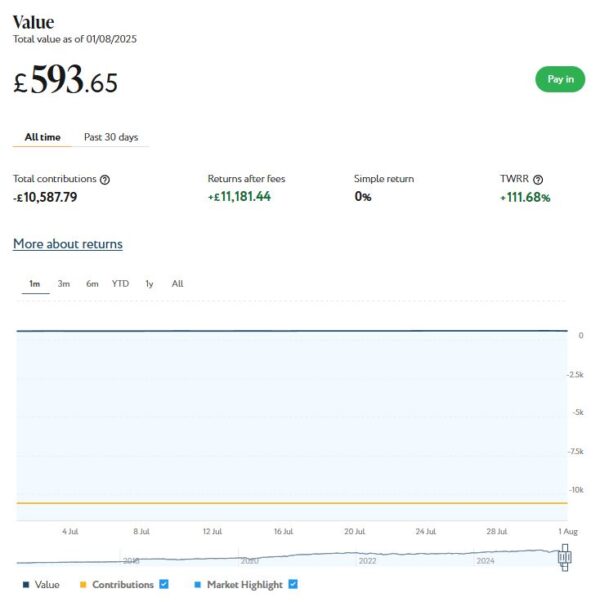

Finally, I still have a small amount left in my original Nutmeg Fully Managed portfolio. I have kept this largely for comparison purposes. This has increased from £581 at the start of July to £594 (rounded up) now, an increase of £13.

As you can see, July was a good month for my Nutmeg investments. Overall I was up by £932 or 2.69%.

I am up by £1,168 since the start of 2025, so the April 2025 fall (caused largely by Trump’s tariffs) has now fully reversed. I am also up by £2,583 or 8.90% since the start of August last year. All things considered, that’s not a bad result.

As I always have to say, some volatility is to be expected with stock market investments, but over the longer term they tend to even themselves out (and generally perform better than bank savings accounts, although that is never guaranteed). In general the worst thing you can do is panic and sell up when downturns occur (as happened in April). You are then crystallizing your losses rather than giving the markets time to recover. This is something I had cause to discuss recently in this blog post.

You can read my full Nutmeg review here. If you are looking for a home for your annual ISA allowance, based on my overall experience over the last eight years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs), Lifetime ISAs and Junior ISAs as well.

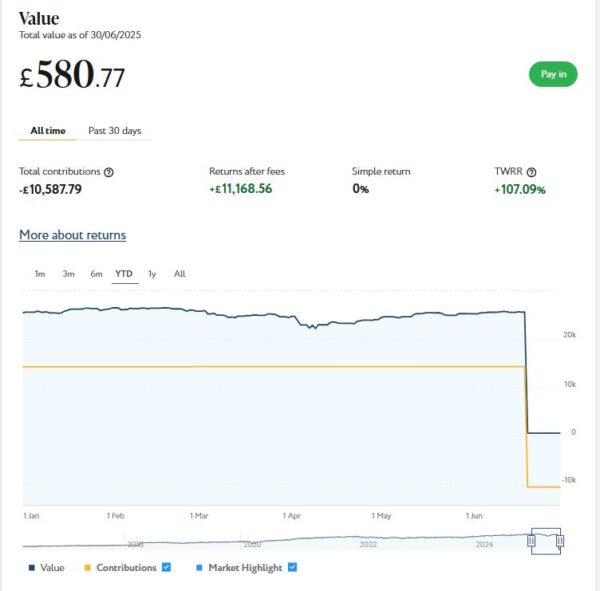

My investments with Housemartin continue to generate steady returns. Housemartin focuses on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my HM portfolio has generated a respectable £262.48 in revenue from rental income. I have made a small net loss of £0.71 on property disposals. Capital growth generally has slowed, in line with UK property values generally.

At the time of writing, 16 of ‘my’ properties are showing gains, 2 are breaking even, and the remaining 19 are showing losses. My portfolio of 37 properties is currently showing a net decrease in value of £60.06. That means that overall (rental income minus capital value decrease and loss on disposal) I am up by £201.71. That’s still a decent return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Housemartin most projects are socially beneficial as well.

The net fall in capital value of my Housemartin investments is obviously a little disappointing. But it’s important to remember that until/unless I choose to sell the investments in question, it is largely theoretical, based on the latest price at which shares in the property concerned have changed hands. The rental income, on the other hand, is real money (which in my case I’ve reinvested in other HM projects to further diversify my portfolio).

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of Housemartin as far as i am concerned. You can actually invest from as little as £1 per property if you really want to proceed cautiously.

As I noted in this blog post, Housemartin is particularly good if you want to compound your returns by reinvesting rental income. This effectively boosts the interest rate you are receiving. Personally, once I have accrued a minimum of £10 in rental payments, I usually reinvest this money in either a new HM project or one I have already invested in (thus increasing my holding). Over time, even if I don’t invest any more capital, this will ensure my investment with Housemartin grows at an accelerating rate and becomes more diversified as well. I did, however, withdraw £50 from my earnings in June to assist my cashflow in what was an expensive month for me

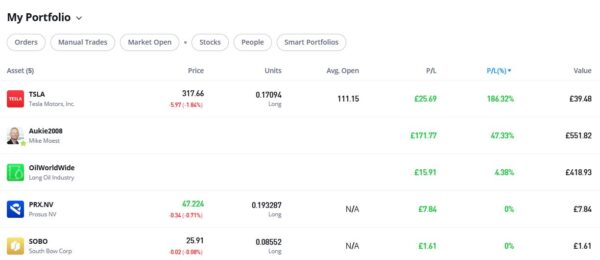

In 2022 I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios, Oil Worldwide. I also invested a small amount I had left over in Tesla shares.

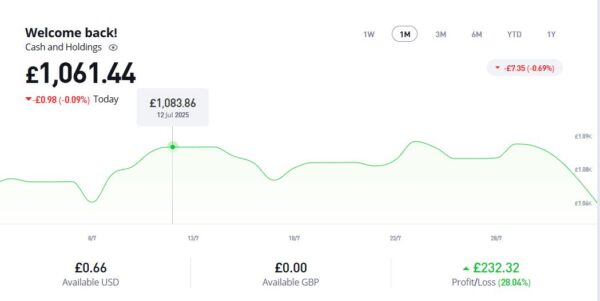

As you can see from the screen captures below, my original investment (total value £888.36 in pounds sterling) is today worth £1,061.44, an overall increase of £173.08 or 19.48%.

Note: eToro now displays the value of investments in your native currency, although you can change this if you wish.

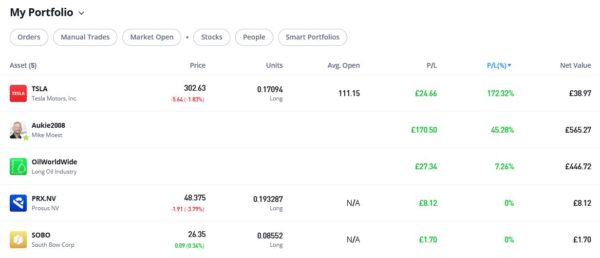

As you can see, my Oil WorldWide investment is in profit, though at 7.26% it is nothing to write home about. My copy trading investment with Aukie2008 has been doing a lot better, with an overall 45.28% profit. To be fair, I have held this investment a bit longer.

My Tesla shares, which I bought as an afterthought with some spare cash I had in my account, are down a little this month. But they are still showing an overall profit of 172.32% since I bought them. If only I had put a bit more money into this!

You might also notice that I have small holdings in Prosus NV, a Dutch internet group, and South Bow, a Canadian energy infrastructure company. To be honest I don’t understand how I acquired these, but I assume they are some sort of bonus I was awarded. In any event, I am happy to have them in my portfolio!

eToro also offer the free eToro Money app. This allows you to deposit money to your eToro account without paying any currency conversion fees, saving you up to £5 for every £1,000 you deposit. You can also use the app to withdraw funds from your eToro account instantly to your bank account. I tried this myself and was impressed with how quickly and seamlessly it worked. You can read my blog post about eToro Money here. Note that it can also serve as a cryptocurrency wallet, allowing you to send and receive crypto from any other wallet address in the world.

If you would like more information about setting up an eToro account, please click on this no-obligation website link [affiliate]. Don’t forget that you also get a free $100,000 virtual portfolio, which you can use to experiment with trading and investing strategies. I have certainly earned a lot from mine.

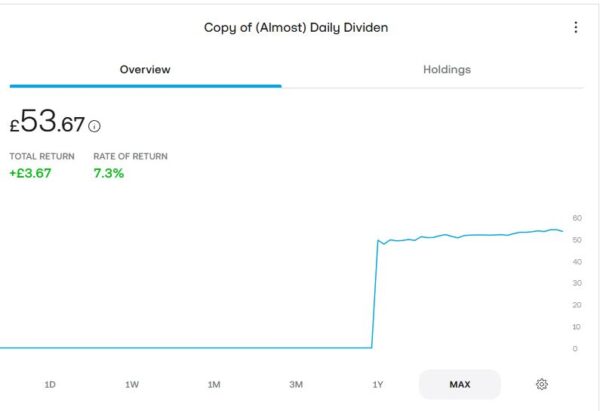

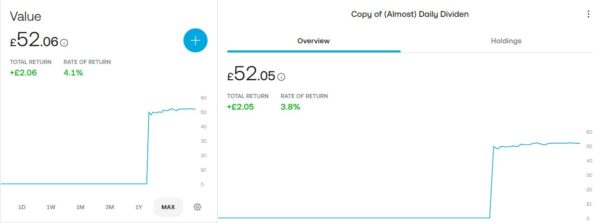

As an experiment, I recently put £50 into an investment ISA with Trading 212. As mentioned in my recent blog post about dividend investing, I put it into the (Almost) Daily Dividends Portfolio, a ready-made portfolio or ‘pie’ on Trading 212. As you can see from the screen capture below, my portfolio is now worth £53.67, an increase of £3.67 or 7.3% over the four-month period. It has even accrued a grand total of 31p in dividends (which is still more than I’ve had from my Nutmeg income port so far!).

I am quite impressed with how this investment has been faring, despite the small amount I put in (which means I may be missing out on some smaller dividends). If I increased my investment I would almost certainly become eligible for more dividends, and even more the longer I remain invested. If I had any spare money at the moment, I would consider doing this. Of course, I do now have an income-focused portfolio with Nutmeg as well (see above).

Moving on, I published various posts on Pounds and Sense in July. I have listed below those that are still relevant.

As mentioned above, in Nutmeg Launches New Income Investing Portfolios I discussed this new option from robo-adviser platform Nutmeg (with whom I am a long-term investor myself). I revealed how the new income investing portfolios work, and revealed why I decided to switch a substantial portion of my Nutmeg investments into one.

How to Tow a Caravan With an Electric Car in the UK covers a subject relevant to growing numbers of motorists. With over 1.5 million EVs now on UK roads – and staycations more popular than ever – more people are pairing their electric cars with touring caravans. But while the idea is appealing, towing with an EV requires careful planning, especially when it comes to battery range and charging stops. I am grateful to my my friends at specialist caravan insurers Compass Insurance and European EV charging infrastructure company Fastned for their expert tips and information.

In How to Invest in Gold in the UK I looked at another subject attracting growing attention. Gold is shiny, timeless, and often seen as a financial “safe haven” – especially when inflation is rising or the stock market is shaky. The growing popularity of gold among investors in recent months is testimony to this. In this post, I covered the pros and cons of investing in gold, the main ways to invest (even if you’re a beginner), and how to get started easily in the UK

Finally, in Is Private Health Insurance Worthwhile for Over-50s? I looked at the pros and cons of private medical insurance (PMI) for older people, and set out some key questions to help decide whether it makes financial sense for you. The article also discusses health cash plans, a less costly alternative that may be more suitable for some.

I’ll close with a reminder that you can also follow Pounds and Sense on Facebook or Twitter (or X as we have to call it now). Twitter/X is my number one social media platform and I post regularly there. I share the latest news and information on financial matters, and other things that interest, amuse or concern me. So if you aren’t following my PAS account on Twitter/X, you are definitely missing out!

I am also on the BlueSky social media network under the username poundsandsense.bsky.social. Twitter/X remains my primary social media platform, but I also post details of my latest blog posts, third-party articles and other financial news and resources on BlueSky for those who prefer to follow me there.

As always, if you have any comments or questions, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts on PAS may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media:

As we get older, our health needs inevitably become more complex – and that’s when many of us (me included) start to wonder: Is private health insurance worthwhile?

In the UK, we’re fortunate to have the NHS, which offers free healthcare at the point of delivery to everyone. But with increasing waiting times and growing pressure on NHS services – not to mention strikes and other disruptions – growing numbers of older people are wondering whether it’s time to consider going private.

Let’s take a look at the pros and cons, and key questions to help you decide whether private medical insurance (PMI) makes financial sense for you.

Table of Contents

✅ Why Consider Private Health Insurance?

1. Shorter Waiting Times

Waiting for an operation or diagnostic scan can be stressful—especially when you’re in pain or worried. One of the biggest attractions of private health insurance is the ability to skip long NHS queues for consultations, scans and treatments.

2. Access to Private Hospitals and Specialists

Private cover often gives you access to a broader network of consultants and hospitals. This can be particularly useful if you want to see a specific specialist or prefer the amenities of a private facility.

3. More Comfortable Experience

Private rooms, flexible appointment times, and continuity of care are common benefits of going private. If you value comfort and control in how you’re treated, insurance can help deliver that.

4. Extra Services

Many policies include extras like physiotherapy, mental health support, or complementary therapies—services that can be hard to access promptly (or at all) on the NHS.

⚠️ Things to Think About Before You Buy

💷 It Can Be Expensive

There’s no getting around it—health insurance becomes more expensive as you get older. If you’re in your 60s or 70s, you could be looking at £100 to £250+ per month, depending on your cover level and health history.

If you’re living on a pension or fixed income, it’s important to weigh up whether the cost is sustainable long term.

⚕️ Pre-existing Conditions May Not Be Covered

If you’ve had health issues in the past—as many of us over 50 have—be aware that these may be excluded from cover, at least initially. Some insurers offer “moratorium” or “full medical underwriting” policies, so be sure to understand the terms.

📜 Not All Treatments Are Included

Private insurance usually doesn’t cover emergency care, chronic disease management (like diabetes or heart failure), or maternity services. These are still handled by the NHS—so PMI should be seen as a complement, not a replacement.

🏥 You’ll Still Use the NHS

Even with private insurance, many people continue to rely on the NHS for things like A&E, cancer care, and follow-up treatment. The NHS remains an essential part of your healthcare safety net.

💡 Who Might Benefit Most?

Private medical insurance may be worth considering if:

You value fast access to treatment or want more choice in who treats you.

You have the financial means to comfortably afford the monthly premiums.

You have health concerns that may require ongoing monitoring or elective procedures.

You want the peace of mind that comes with having private options available if needed.

🏥 Comparing Health Insurance Providers

If you’re over 50 and considering private health insurance, choosing the right provider can feel overwhelming. Below is a comparison of five well-known UK insurers, focusing on how they stack up for older adults.

Provider

Pros

Cons

Bupa

– Trusted name with a wide hospital network

– 24/7 GP appointments via phone or video

– Tailored cover options, including cover for mental health and physiotherapy

– One of the more expensive providers

– Some policies have strict limits on outpatient care

AXA Health

– Offers a 24/7 health helpline with nurses

– Includes mental health cover and diagnostics

– Often good for families and couples too

– Can be costly if you add multiple optional extras

– Some treatments may require pre-authorisation

Vitality Health

– Rewards scheme offers discounts on fitness, gym, travel and health-related spending

– Offers some cover for pre-existing conditions after a waiting period

– Complex rewards system can be hard to understand

– Requires engagement (like activity tracking) to get maximum benefit

Aviva

– Competitive pricing, especially for older adults

– Strong focus on modular plans—pay for what you need

– Digital tools and fast claims process

– Fewer perks and extras compared to some rivals

– Limited cover for some complementary therapies

Saga (underwritten by Bupa)

– Specifically designed for over-50s

– No upper age limit on new policies

– Includes access to private GPs and specialists

– Can be pricey, especially for comprehensive cover

– May still require medical screening depending on age and conditions

Health Insurance Cost Estimator

As a rough guide, here is an online tool that will give you a ballpark estimate for how much health insurance might cost you, based on your age and type of cover required. It assumes you are a non-smoker with no chronic health conditions.

🧮 Private Health Insurance Cost Estimator

Note that this tool gives an approximate cost only. Prices vary by insurer, health status, where you live in the UK, and exact policy terms (including the excess you’re willing to pay). Always get a personalized quote before purchasing cover.

When comparing policies, keep these key factors in mind:

Outpatient limits – Do you get full cover for scans and consultations?

Excess options – Choosing a higher excess can lower your premium.

Cover for pre-existing conditions – Look closely at what’s included and excluded.

Hospital list – Make sure your preferred hospitals or clinics are included.

Added-value benefits – Think virtual GP access, helplines and therapy sessions.

💡 Extra Tip

Most insurers offer a cooling-off period (usually 14 days) after purchase, so you can change your mind. It’s also worth calling insurers directly to ask about over-50s discounts, flexible policies, or joint plans with your partner.

Private medical insurance is a personal investment—and choosing the right provider can make a big difference in both your care and your costs.

💷 What About Health Cash Plans?

If the cost of full private health insurance feels out of reach, health cash plans could be a more affordable alternative—especially for those in their 50s, 60s and beyond who want help covering everyday healthcare costs.

🩺 What Is a Health Cash Plan?

A health cash plan is not the same as private medical insurance. Instead of paying for private operations or hospital stays, cash plans reimburse you for routine healthcare expenses such as:

Dental check-ups and treatment

Eye tests and glasses

Physiotherapy and chiropractic care

Prescription costs

GP consultations and health screenings

You usually pay a fixed monthly fee—typically between £10 and £30 depending on your level of cover—and can claim back part or all of the cost of certain treatments or services.

🏥 Popular Health Cash Plan Providers

Provider

Typical Monthly Cost

Key Features

Benenden Health

£11.90 (flat rate)

– No age limit or exclusions for pre-existing conditions

– Offers access to private GP, mental health support, and diagnostics

– Not-for-profit mutual organisation

Medicash

From £7.50

– Cash back on dental, optical, and therapy treatments

– Family cover available

– App with virtual GP and health tools

Health Shield

From £10

– Offers wellbeing support, counselling, and claim-back options for everyday healthcare

– No medical underwriting

Simplyhealth

From £10

– Long-standing provider with a range of plan levels

– Can cover optical, dental, chiropody, physiotherapy, etc.

– Optional extras for higher-level plans

👍 Pros of Health Cash Plans

✅ Much more affordable than private medical insurance

✅ Ideal for managing common or routine health costs

✅ Often no medical screening required

✅ Useful for retirees managing a fixed income

✅ Can offer peace of mind for dental, optical and therapies

⚠️ Things to Keep in Mind

❌ Cash plans won’t cover private operations or major surgery

❌ Most plans have maximum claim limits per benefit each year

❌ You usually have to pay upfront and claim back later

✅ Is a Health Cash Plan Right for You?

For many over-50s, particularly those without serious ongoing health issues, a health cash plan offers a practical and low-cost way to stay on top of everyday health needs.

If you’re happy using the NHS for major treatments but want support with dentist bills, eye care, and physiotherapy, this could be a smart middle-ground—especially when budgets are tight.

🧮 Closing Thoughts: Is PMI Worth the Money?

There’s no one-size-fits-all answer. Private medical insurance can offer convenience, faster access and a better experience—but it comes at a cost.

Ask yourself:

Can I afford this now and in 10 years’ time?

What do I want most from my healthcare—speed, choice, comfort?

Would I get peace of mind knowing I can go private if I need to?

For some, especially those with complex health needs or busy lifestyles, private insurance can be a good investment in their well-being. For others, the NHS may still offer all the care they need—at no additional cost.

You also have the option to self-fund one-off private treatments instead of paying monthly insurance premiums. You might also use the NHS for most care, but go private for specific issues—like orthopaedics or diagnostics—where waiting lists are longest.

If you’re considering private health insurance, it’s well worth using a comparison service like ActiveQuote, GoCompare, or Compare the Market to explore your options. You may also want to speak to an independent financial adviser to help decide if it’s the right move for your health and your wallet.

If you have any comments or questions about this article, as always, feel free to post them below. I’d also be interested to hear about your own experiences with health insurance and health cash plans, and whether you recommend them or not.

If you enjoyed this post, please link to it on your own blog or social media:

Gold has a reputation few other investments can match. It’s shiny, timeless, and often seen as a financial “safe haven” – especially when inflation is rising or the stock market is shaky. The growing popularity of gold among investors in recent months is testimony to this.

But is investing in gold the right move for you?

In this post, I’ll cover:

The pros and cons of investing in gold

The main ways to invest (even if you’re a beginner)

And how to get started easily in the UK

Table of Contents

Why Invest in Gold?

For centuries, gold has been viewed as a store of value. Unlike cash, which can lose its buying power over time, gold tends to hold its worth – especially during times of economic uncertainty.

In 2025, with inflation still a concern and markets volatile and unpredictable, more UK savers and investors than ever are thinking about adding gold to their portfolios. But like any asset, it has both upsides and downsides.

✅ Pros of Investing in Gold

🔒 1. A Hedge Against Inflation

As prices rise and the pound’s purchasing power shrinks, gold often increases in value. That’s why many investors use it as a hedge against inflation.

🌍 2. A Safe Haven in Uncertain Times

Gold tends to perform well during economic turbulence, financial crises or geopolitical shocks. When confidence in markets wobbles, gold often shines.

📊 3. Portfolio Diversification

Gold doesn’t typically move in the same direction as stocks or bonds, so adding it to your portfolio can reduce overall risk.

💷 4. High Liquidity

Whether it’s gold coins, bars or gold ETFs, gold can usually be bought and sold easily in the UK through dealers or online investment platforms.

🧱 5. It’s a Physical, Tangible Asset

Physical gold appeals to those who like to see and touch what they own. It can feel more secure than digital investments.

❌ Cons of Investing in Gold

🚫 1. No Income

Gold doesn’t pay interest, dividends or rent. You only make money if the price rises and you sell at a profit.

🔐 2. Storage and Security Costs

If you buy physical gold, you’ll need to store it safely – at home, in a bank, or with a specialist provider. This can add ongoing costs.

📉 3. Short-Term Price Fluctuations

Gold prices can be volatile in the short term, reacting to interest rates, currency shifts and global events.

💰 4. Capital Gains Tax (CGT)

If you make a profit on gold, you might pay CGT – unless you buy UK legal tender coins like Britannias or Sovereigns, which are CGT-free.

💸 5. Premiums and Dealer Fees

When buying physical gold, you’ll usually pay a premium above the market (spot) price, plus delivery and possibly VAT (on some bars or non-investment gold).

🛠️ How to Start Investing in Gold

1. 🪙 Buy Physical Gold (Coins or Bars)

If you want to hold gold directly, coins and bars are your best bet.

Coins like Britannias and Sovereigns are CGT-exempt and easy to sell.

Bars are available in various weights (from 1g to 1kg) and may offer better value per gram.

✅ You can even hold gold ETFs in a Stocks and Shares ISA to shield your gains from tax. See also my recent blog post about ETFs and how to invest in them.

3. ⛏️ Buy Shares in Gold Mining Companies

Prefer businesses over bullion? Invest in gold miners like:

Fresnillo (listed on the London Stock Exchange)

Barrick Gold

Newmont Corporation

⚠️ These company shares are higher risk – they’re influenced by more than just the gold price, e.g. management performance, debt, and political factors.

4. 🖥️ Use a Digital Gold Account

Want exposure to gold without the hassle of storage? Try digital gold platforms.

Gold futures and options allow speculation on gold price movements — but they’re complex, leveraged, and risky.

🛑 Definitely not suitable for beginners!

🧠 Closing Thoughts: Is Gold Right for You?

Gold can be a smart addition to your investment mix – especially if you’re worried about inflation, market crashes and/or want to diversify your portfolio.

But it’s not perfect. It doesn’t generate income, and short-term prices can be unpredictable.

A sensible approach? Treat gold as a long-term insurance policy, not a get-rich-quick plan. Many financial advisers recommend allocating around 5–10% (at most) of your portfolio to gold.

If you’re just getting started, two good options are:

Gold coins like Britannias or Sovereigns

A low-cost gold ETF inside a tax-exempt Stocks & Shares ISA

And remember: if you’re not sure, speak to a financial adviser before making any big investment decisions.

💬 Over to You

Have you invested in gold – or are you thinking about it?

Share your thoughts or questions in the comments below 👇

Disclaimer: I am not a qualified financial adviser and nothing in this article should be construed as personal financial advice. You should always do your own “due diligence” before investing and seek advice from a financial services professional if in any doubt before proceeding. All investing carries a risk of loss.

If you enjoyed this post, please link to it on your own blog or social media:

Today I’m looking at a subject relevant to growing numbers of UK motorists: what are the practicalities of towing a caravan with an EV?

In this post I have teamed up with my friends at specialist caravan insurers Compass Insurance and European EV charging infrastructure company Fastned. I am very grateful to them for their expert tips and information.

With over 1.5 million EVs now on UK roads – and staycations more popular than ever – more people are pairing their electric cars with touring caravans. But while the idea is appealing, towing with an EV requires careful planning, especially when it comes to battery range and charging stops.

Why Towing With an EV Is Different

Although many modern electric cars are perfectly capable of towing – with some legally able to handle loads up to 2,500 kg – pulling a caravan takes a toll on battery life. You could see your EV’s range drop by up to 50% when towing a typical 4-berth caravan.

This means you’ll likely need to stop more often to charge. But here’s the catch: most public EV chargers aren’t designed for hitched-up vehicles. Accessing a charger with a caravan in tow can be tricky at best and downright impossible at worst.

Kevin Minnear, Head of Underwriting at Compass Insurance, explains:

“Electric cars have come a long way, but towing a caravan with one is still a logistical challenge. With range reduced and many public charging stations not designed to accommodate a hitched caravan, it’s essential to plan ahead.”

The Charging Challenge

As of summer 2025, there are now over 80,000 public EV charging points across the UK, and around 20% of them are classed as rapid or ultra-rapid. But the problem isn’t quantity; it’s access. Many charging bays aren’t suitable for caravans, especially in tourist hotspots during peak season.

Tom Hurst, UK Country Director at EV charging company Fastned, says this is starting to change:

“We’ve prioritised ultra-rapid hubs with drive-thru layouts that make it easier for caravanners to pull in, charge, and continue their journey without the hassle of unhitching.”

Still, the infrastructure needs to catch up with demand — particularly in rural areas where many caravan sites are located.

Tips for Towing a Caravan with an EV

Whether you’re a seasoned tourer or trying it for the first time, these practical tips from Compass Insurance can help make your EV-powered getaway go more smoothly:

Table of Contents

✅ Check Your EV’s Towing Capacity

Not all electric vehicles are built to tow. Check the VIN plate, manual, or manufacturer website to confirm. As a rule of thumb, newbies should follow the 85% rule – your caravan should weigh no more than 85% of the EV’s kerbweight.

✅ Plan Your Route with Charging in Mind

Use EV-specific apps like Zap-Map or A Better Routeplanner to find caravan-accessible chargers. Avoid peak hours (usually 11 am to 1 pm), and check for reviews and layout photos before setting off.

✅ Prepare for Extra Stops

Towing significantly reduces range. On a 250-mile journey, you may need to stop twice. Charging from 10% to 80% can take 30–60 minutes, so build this into your journey.

✅ Unhitching Might Be Unavoidable

Most chargers won’t let you pull in with a caravan attached. Travel with a second adult when possible so someone can stay with the caravan while you charge.

✅ Know What’s Available at Your Campsite

Call ahead to check if EV charging is available, and at what cost. If possible, top up overnight with a dedicated charger. Never plug into your caravan’s standard hookup unless you’re absolutely certain it’s allowed and safe.

✅ Drive Efficiently

Stick to 50 to 60 mph, use cruise control, and take advantage of regenerative braking to extend your range.

✅ Don’t Overpack

Watch your payload! Most caravans allow 150 to 170kg for luggage. Overloading can affect safety, handling, and battery efficiency – especially if you’re carrying heavy extras like e-bikes or awnings.

Caravan Parks: Time to Think Ahead

With more EV drivers hitting the road, holiday parks and campsites also need to adapt. Standard domestic sockets aren’t a safe substitute for dedicated EV chargers. They can overheat, pose tripping hazards, and even create security risks if left through windows or doors.

Compass Insurance urges park operators to consider investing in proper EV charging infrastructure, both to improve safety and to meet growing guest expectations.

As Kevin Minnear points out:

“By exploring safe, compliant charging solutions, park operators can help ensure both convenience and peace of mind for their visitors.”

Closing Thoughts

Towing a caravan with an electric vehicle is absolutely do-able – and increasingly common – but it does take more thought than simply packing your bags and hitting the road. With a bit of forward planning and the right tools and equipment, your EV-powered holiday can be just as relaxing as any other… without the emissions.

Whether you’re heading to Cornwall or the Cairngorms, planning your journey, charging stops and destination ahead of time will make all the difference.

Today I am looking at the new income investing option recently introduced by UK robo-adviser platform Nutmeg. This is designed for people who want to receive a regular monthly income while keeping their money invested (and hopefully still growing).

As a long-term Nutmeg investor myself (you can read my in-depth review here), I have already taken advantage of this opportunity. I will discuss my personal experience (so far) in more detail below. But first, here’s how it works in a nut(meg)shell, how it compares with Nutmeg’s traditional growth portfolios, and who might benefit the most.

How Nutmeg’s Income Portfolios Work

Powered by J.P. Morgan Asset Management (JPMAM)

Nutmeg has collaborated with JPMAM to construct five risk‑rated portfolios, built around actively managed income-focused ETFs – including the JP Morgan Equity Premium Income strategy – so you’re investing in income-optimized assets while staying diversified.

2. Five Risk Levels to Suit You

You can choose from five different risk levels, ranging from 1 (cautious) to 5 (adventurous), based on your circumstances, goals and appetite for risk. Each level offers a different blend of equity and bond exposure to balance income generation with capital stability.

Here’s a table describing Nutmeg’s five income portfolio risk levels in simple terms…

Risk Level

Description

Equity Exposure

Income Potential

Capital Risk

1 – Cautious

Prioritizes stability over returns

Low

Low

Very Low

2 – Conservative

Aims for modest, steady income with minimal volatility

Low to Moderate

Low to Medium

Low

3 – Balanced

Balanced mix of bonds and equities for moderate income and risk

Moderate

Medium

Moderate

4 – Growth-Oriented

Greater focus on equity income for higher payouts

Moderate to High

Medium to High

Moderate to High

5 – Adventurous

Maximizes income potential with higher risk tolerance

High

High

High

📌 Note: All portfolios are actively managed and diversified, but the mix of assets changes based on your selected risk level. Income smoothing and monthly payouts are available across all five.

3. Monthly Payouts with Optional Smoothing

One standout feature is income smoothing. This spreads out income across the year, so you receive consistent monthly payments – even if dividends or yields vary from month to month. This feature is optional, however – you can turn smoothing off if you’d rather receive income as it’s earned every month.

4. No Nutmeg Management Fee for 2025

These portfolios are available via ISA or General Investment Accounts (non-ISA) and have no Nutmeg management fee for the rest of 2025, though underlying ETF costs apply. A minimum investment of £10,000 is required.

5. Capital Remains Invested

Your core investment stays fully invested in the market – providing the potential for capital preservation or growth alongside the monthly income stream.

Income vs Growth – What’s the Difference?

The difference between the two approaches is summed up in the table below.

Income Portfolio

Growth Portfolio

Objective

Provide regular monthly income

Maximize long‑term capital growth

Payouts

Paid out monthly, with optional smoothing

Reinvested automatically for compounding

Yield Focus

Uses dividend and income-focused ETFs

Focus on market growth; income secondary

Suitability

Later-stage savers, retirees, cash flow needs

Long-term goals like retirement, wealth accumulation

While Nutmeg’s growth-oriented portfolios reinvest dividends to compound, the income portfolios are specifically structured to generate ongoing monthly payments. This is ideal for those needing a regular income rather than capital appreciation (though some capital appreciation will hopefully occur as well).

Who Are These Portfolios Best For?

Retirees or near‑retirees needing a dependable income stream without selling assets.

Those reducing work hours or with varied income, using the monthly payouts to smooth out earnings.

Investors frustrated with traditional bond/dividend returns – Nutmeg’s own research shows 69% of UK investors prioritize income, yet many are unhappy with current options.

Investors seeking simplicity – You set your risk level once and Nutmeg then handles asset selection, portfolio rebalancing and (optional) income smoothing. As with all Nutmeg investments, you can change your risk level later if you wish (though some extra costs may be incurred when doing so).

Pros and Considerations

👍 Pros:

Monthly income stream without selling investments

Income smoothing for consistent payouts

Actively managed by experts at JPMAM

No Nutmeg fees until 2026

⚠️ Considerations:

Requires £10,000 minimum to start

Still carries investment risk – capital isn’t guaranteed

Fund fees apply for underlying ETFs

If you’re focused purely on capital growth, growth portfolios with reinvestment may outperform long-term

My Experience

As you will know if you read my July 2025 Investments Update, in June I transferred most of the money in my Nutmeg Fully Managed portfolio (just under £25,000) to a new Nutmeg Income Portfolio. As my money was already invested via a Stocks and Shares ISA, my new income portfolio will enjoy that status as well, meaning income payments will be made without any deductions for tax. Likewise, any capital appreciation will not be taxable.

I selected a risk level of 5 (the maximum). That aligns with the risk level of my other Nutmeg investments, which should make it easier to compare them. More importantly, though, I have other investments that are lower risk, including my Bestinvest SIPP (personal pension) and – of course – my state pension. With my Nutmeg investments I hope to maximize their income and growth potential and am comfortable taking a few more risks to this end. As I have other, less risky investments, any reversals with Nutmeg shouldn’t be disastrous. Obviously as I get older – or if my circumstances change – I may revisit this.

For similar reasons, I chose not to select the ‘smoothing’ option. The income from my Nutmeg income portfolio will be in addition to other regular income streams I already have, so I can’t see any particular reason to have these payments smoothed out. Obviously I will monitor this and might change my mind in future, but for now I quite like the idea of having a variable extra payment each month. If it’s large, I may allow myself a few extra treats that month. If it’s small, I will adjust my expenditure accordingly.

Of course, the above is solely my personal perspective and should not be construed as financial advice. Everyone’s circumstances are different. You should always do your own ‘due diligence’ before investing and seek professional advice if uncertain how best to proceed. All investing carries a risk of loss.

As the screenshot below shows, my Income portfolio is already showing a profit of over £400, which is obviously welcome. It hasn’t yet generated any income, but that is unsurprising. It can take a while for investments to qualify for dividend payments, so I am keeping my expectations modest, initially at least 🙂

I will update PAS readers on how my Nutmeg income portfolio performs in my future monthly investments updates.

Closing Thoughts

In my view, Nutmeg’s new Income Investing portfolios are a valuable addition for UK investors seeking a regular income, backed by diversified, actively managed ETFs. They offer monthly, optionally smoothed payouts, managed via Nutmeg’s simple, user-friendly interface. The fact that there is no initial Nutmeg management fee through 2025 is a further attraction.

If your priorities include current cash flow, retirement‑style income, or smoothing irregular income, this could be a good fit. If you’re younger or focused on maximizing long-term growth via compounding, however, Nutmeg’s established growth portfolios (e.g. Smart Alpha) remain compelling options.

If you have any comments or questions about this post – or Nutmeg more generally – please do leave them below. As always, bear in mind that I am not a qualified financial adviser and cannot offer personalized financial advice. As with all investments, your capital is at risk and there are no guarantees of profit. If in any doubt, consider speaking with a financial services professional.

If you enjoyed this post, please link to it on your own blog or social media:

A quickie today to let you know that the annual Amazon Prime Day is almost with us. This year it extends over four days, Tuesday 8th to Friday 11th July 2025.

Prime Day is a special event for Amazon Prime members only. During it Amazon offers Prime members extra savings and special offers across a wide range of TVs, smart home products, kitchen equipment, grocery, toys, fashion, furniture, everyday essentials, and more.

Some of the best deals are typically reserved for Amazon’s own products, such as their Kindle e-book readers, Amazon Echo smart speakers and Ring video doorbells and security cameras. Discounts are often in the region of 40-50 percent for these products. If you’re thinking of buying any of them, Prime Day is definitely the day – or four days! – to do it.

I have been a member of Amazon Prime for over ten years now. As a regular Amazon shopper, I find it well worth while for the free one-day delivery on millions of items alone. But as a Prime member you get access to a lot of other benefits and services as well, including Amazon Prime Music and Amazon Prime Video.

If you’re thinking of joining Amazon Prime, therefore, I highly recommend doing it in the next day or two, so you can benefit from the Prime Day offers. Personally I think it’s worth it for the free delivery alone, let alone everything else that’s on offer. But if you wish, you can get a 30-day free trial now, take advantage of the Prime Day offers, and then cancel without owing any money. It’s your choice!

You can also see all the latest Prime Day deals by clicking here. This page also lists early deals before Prime Day itself.

As always, if you have any comments or questions about Amazon Prime or Prime Day, please do post them below.

Disclosure: This post includes affiliate links. If you click through and make a purchase, I may receive a commission for introducing you. This will not affect the price you pay or the products or services you receive.

If you enjoyed this post, please link to it on your own blog or social media:

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

A major change in June was that I transferred most of the money in my Nutmeg Fully Managed portfolio (£25,000) to the new Nutmeg Income Portfolio. I will talk more about this is in a separate post, but basically money in this portfolio is invested to generate an income from dividends and other sources. This is then paid monthly. Capital appreciation is targeted as well, but basically these portfolios are aimed at older people (and others) who want/need their investment to generate a regular cash income.

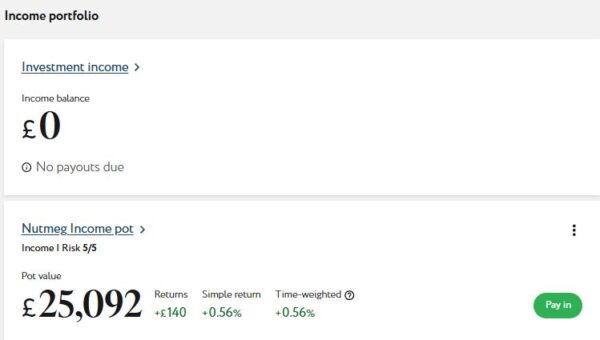

As the screenshot below shows, my Income portfolio has only just been set up, though it’s already showing a small profit. It hasn’t yet generated any income for me, but that is unsurprising. Income is due to be paid in cash to my bank account on the 24th of each month, so hopefully I may have some income accrued by then (check out next month’s Update to find out). Of course, it can take a while for an investor to qualify for dividend payments, so I am keeping my expectations modest, initially at least!

You do have the option to select a ‘smoothing’ option, where Nutmeg works out your likely monthly income from the size (and performance) of your investment and pays the same amount every month from then onward. For various reasons I have opted not to do this for now, however.

Finally, you can select a risk level from 1 to 5 for your Income Portfolio. After some thought I selected the maximum 5. Depending on how things go, I may reduce this in future.

I still have a smaller growth-oriented pot using Nutmeg’s Smart Alpha option. This is now worth £4,164 (rounded up) compared with ££4,059 a month ago, a rise of £105. Here is a screen capture showing performance for the year to date.

And at the start of December 2023 I invested £500 in one of Nutmeg’s thematic portfolios (Resource Transformation). In March 2024 I also invested a further £200 from referral bonuses. As you can see from the YTD screen capture below, this portfolio is now worth £827 compared with £804 last month, a rise of £23.

Finally, I still have a small amount left in my original Nutmeg Fully Managed portfolio. I have kept this largely for comparison purposes. Here’s a screen capture of how it stands now.

As you can see, June was another decent month for my Nutmeg investments. Overall I was up by £478 or 1.58%.

I am up by £236 since the start of 2025, so the April 2025 fall (caused largely by Trump’s tariffs) has now completely reversed. I am also up by £1,750 or 6.05% since the start of July last year. Considering the recent volatility of the markets (and world affairs generally) that’s not a bad result.

As I always have to say, some volatility is to be expected with stock market investments, but over the longer term they tend to even themselves out (and generally perform better than bank savings accounts, although that is never guaranteed). In general the worst thing you can do is panic and sell up when downturns occur (as happened in April). You are then crystallizing your losses rather than giving the markets time to recover. This is something I had cause to discuss recently in this blog post.

You can read my full Nutmeg review here. If you are looking for a home for your annual ISA allowance, based on my overall experience over the last eight years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs), Lifetime ISAs and Junior ISAs as well.

My investments with Housemartin continue to generate steady returns. Housemartin focuses on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my HM portfolio has generated a respectable £256.94 in revenue from rental income. I have also made a net profit of £0.57 on property disposals. Capital growth has slowed, though, in line with UK property values generally.

At the time of writing, 16 of ‘my’ properties are showing gains, 2 are breaking even, and the remaining 18 are showing losses. My portfolio of 36 properties is currently showing a net decrease in value of £53.93. That means that overall (rental income and profit on disposal minus capital value decrease) I am up by £203.58. That’s still a decent return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Housemartin most projects are socially beneficial as well.

The net fall in capital value of my Housemartin investments is obviously a little disappointing. But it’s important to remember that until/unless I choose to sell the investments in question, it is largely theoretical, based on the latest price at which shares in the property concerned have changed hands. The rental income, on the other hand, is real money (which in my case I’ve reinvested in other HM projects to further diversify my portfolio).

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of Housemartin as far as i am concerned. You can actually invest from as little as £1 per property if you really want to proceed cautiously.

As I noted in this blog post, Housemartin is particularly good if you want to compound your returns by reinvesting rental income. This effectively boosts the interest rate you are receiving. Personally, once I have accrued a minimum of £10 in rental payments, I usually reinvest this money in either a new HM project or one I have already invested in (thus increasing my holding). Over time, even if I don’t invest any more capital, this will ensure my investment with Housemartin grows at an accelerating rate and becomes more diversified as well. I did, however, withdraw £50 from my earnings in June to assist my cashflow in what was an expensive month for me 😮

In 2022 I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios, Oil Worldwide. I also invested a small amount I had left over in Tesla shares.

As you can see from the screen captures below, my original investment (total value £888.36 in pounds sterling) is today worth £1,020.09, an overall increase of £131.73 or 14.83%.

Note: eToro now displays the value of investments in your native currency, although you can change this if you wish.

As you can see, my Oil WorldWide investment is back in profit now. But my copy trading investment with Aukie2008 has been doing a lot better, with an overall 47.31% profit. To be fair, I have held this investment a little longer.

My Tesla shares, which I bought as an afterthought with some spare cash I had in my account, are down a bit this month. But they are still showing an overall profit of 186.32% since I bought them. If only I had put a bit more money into this!

You might also notice that I have small holdings in Prosus NV, a Dutch internet group, and South Bow, a Canadian energy infrastructure company. To be honest I don’t understand how I acquired these, but I assume they are some sort of bonus I was awarded. In any event, I am happy to have them in my portfolio!

eToro also offer the free eToro Money app. This allows you to deposit money to your eToro account without paying any currency conversion fees, saving you up to £5 for every £1,000 you deposit. You can also use the app to withdraw funds from your eToro account instantly to your bank account. I tried this myself and was impressed with how quickly and seamlessly it worked. You can read my blog post about eToro Money here. Note that it can also serve as a cryptocurrency wallet, allowing you to send and receive crypto from any other wallet address in the world.

If you would like more information about setting up an eToro account, please click on this no-obligation website link [affiliate]. Don’t forget that you also get a free $100,000 virtual portfolio, which you can use to experiment with trading and investing strategies. I have certainly earned a lot from mine.

As an experiment, I recently put £50 into an investment ISA with Trading 212. As mentioned in my recent blog post about dividend investing, I put it into the (Almost) Daily Dividends Portfolio, a ready-made portfolio or ‘pie’ on Trading 212. As you can see from the screen capture below, my portfolio is now worth £52.06, an increase of £2.06 or 4.12% (by my calculation) over the three-month period. It has even accrued a grand total of 18p in dividends!

I am quite impressed with how this investment has been faring, despite the small amount I put in (which means I may be missing out on some smaller dividends) and also because you need to have held shares for a certain period to qualify for dividend payments. If I increased my investment I would almost certainly become eligible for more dividends, and even more the longer I remain invested. If I had any spare money at the moment, I would consider doing this. Of course, I do now have a dividend-focused portfolio with Nutmeg as well (see above).

Moving on, I published various posts on Pounds and Sense in June. I have listed below those that are still relevant.

The Many Benefits of Learning a Musical Instrument in Later Life isn’t about personal finance. But as someone who has actually done this (ukulele) it’s a subject I feel quite passionate about. In this article I set out the many (sometimes surprising) benefits of learning to play an instrument as a senior, and offered a few tips based on my personal experience.

In What Are Bonds and How Can You Invest in Them, I explain what bonds are and their pros and cons compared with other investment vehicles. As I say in the article, bonds can play a key role in a well-rounded portfolio, especially for those – including many older people – who are seeking predictable, regular income and/or lower risk.

In How to Reduce Your Water Bills I discussed various ways you may be able to cut your water bill, including getting a water meter and (if you’re on a low income) applying for a reduced-rate social tariff. With water bills rising substantially in many parts of the country, it’s well worth checking what options you may have to cut them.

Is It Worth Getting Over 50 Life Insurance? is another sponsored post. It focuses on a type of life insurance specifically designed for people aged over 50. Such policies offer a guaranteed, fixed cash payout when the policyholder dies. Over 50 life insurance policies are generally “whole of life”, meaning they last until you pass away, as long as you keep up with premium payments. They’re often used to help cover funeral expenses, outstanding debts, or to leave a small inheritance.

Finally, How Social Tariffs Can Help You Reduce Your Household Bills looks at discounted tariffs that may be available for people on low incomes and/or certain means-tested benefits. Specifically, it covers broadband, water bills and energy bills. Do check this out if you are struggling with these bills at the moment.

I’ll close with a reminder that you can also follow Pounds and Sense on Facebook or Twitter (or X as we have to call it now). Twitter/X is my number one social media platform and I post regularly there. I share the latest news and information on financial matters, and other things that interest, amuse or concern me. So if you aren’t following my PAS account on Twitter/X, you are definitely missing out.

I am also on the BlueSky social media network under the username poundsandsense.bsky.social. Twitter/X remains my primary social media platform, but I will also post details of my latest blog posts, third-party articles and other financial news and resources on BlueSky for those who prefer to follow me there.

As always, if you have any comments or questions, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts on PAS may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media: