Review: How to Make Money Using Your Mobile by Kathy Cakebread

Today I am reviewing a Kindle e-book by my fellow UK money blogger Kathy Cakebread titled How to Make Money Using Your Mobile. Kathy was kind enough to offer me a free review copy.

As you may gather from the name, this e-book is aimed at anyone who would like to boost their income using their mobile phone, generally by installing and using certain apps.

According to Amazon How to Make Money Using Your Mobile has 96 pages, though in practice of course that will depend on the device you are reading on and the font size selected.

My first impression was that it was well written and attractively presented. That being said, I was a little disappointed that there is no table of contents at the front. That makes it harder to navigate than it ought to be.

The book lists money-making apps in six categories as follows:

- Survey Apps

- Make Money Through Receipts

- Get Paid to Shop

- Make Money Doing What You’re Good At

- Earn Money Through Cashback

- Ways That Influencers Can Make Money

46 apps are described in total: 24 in survey apps, 4 in receipts apps, 9 in get paid to shop, 4 in make money doing what you’re good at, 3 in cashback apps, and 2 in influencers.

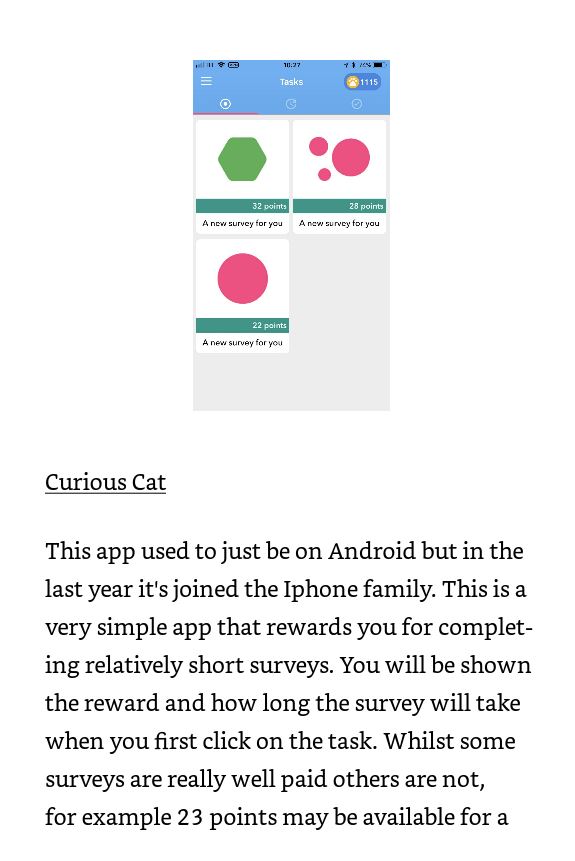

Within each category a number of apps/opportunities are presented. Kathy uses a standard format throughout for this, which is sensible. She starts with a phone screen capture of the app in question followed by a one- to three-paragraph description. Here’s a typical example…

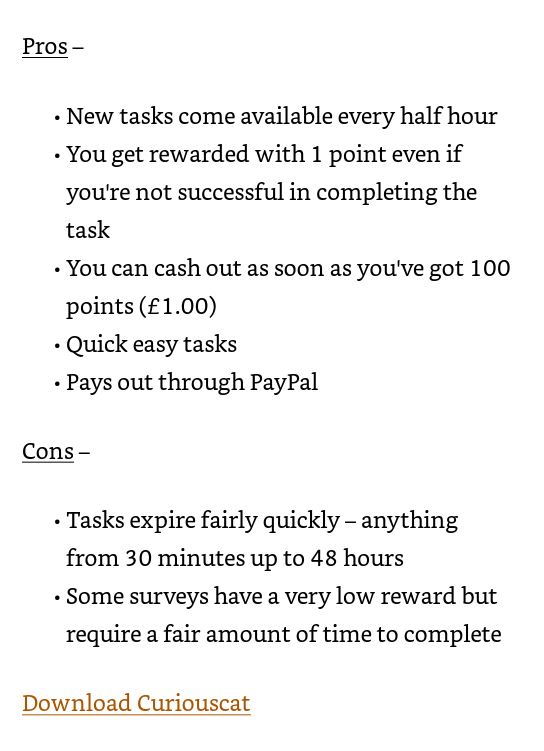

The description is followed by a list of pros and cons for the app in question, and (in most cases) a download link. Again, here is an example:

In some cases the download link takes you to the website for the app, but in others it takes you to to the Apple (iOS) App Store. It is a pity there aren’t also links to the Google Play Store for Android users (like myself). This means the book is probably best suited for iPhone users. Android users can benefit from it as well, but they may have to search for the relevant app themselves in the Google Play Store.

In some cases the download link takes you to the website for the app, but in others it takes you to to the Apple (iOS) App Store. It is a pity there aren’t also links to the Google Play Store for Android users (like myself). This means the book is probably best suited for iPhone users. Android users can benefit from it as well, but they may have to search for the relevant app themselves in the Google Play Store.

On the plus side, I was amazed by the number of sideline-earning apps Kathy has identified. Some, of course, I knew about already, but many I didn’t. I can see I will be busy for some time checking out all these money-making resources!

I like the concise, well-written descriptions, which tell you everything you need to decide whether an app may be of interest. The list of pros and cons is also invaluable. Kathy appears to have tried all these apps herself (which would be a full-time job, I’d have thought) and she shares her advice and experiences using every app, good and not so good!

As the book’s subtitle, Get a side income for extra treats for you and your family, indicates, you won’t make a fortune from these apps or even (probably) enough for a full-time living. But you can definitely earn a valuable sideline income. Some pay in cash – usually via PayPal – while others pay you in Amazon (or other store) gift vouchers. (Personally, I’m a big fan of MobileXpression, which I wrote about in this blog post. It keeps on churning out £20 Amazon vouchers for me every few weeks, for doing no more than keeping the app installed on my phone.)

As indicated earlier, I did think the book could be better organised. In particular, I would like to have seen a table of contents at the front, with the content organised under proper chapter headings and hyperlinked. That would make it much easier to use as a reference resource. It would also be good if the apps described in each chapter were arranged in alphabetical order rather than (I assume) randomly.

Overall, though, How to Make Money Using Your Mobile is a great little e-book, and anyone hoping to boost their income is bound to find something of interest – and value – in it. At the current modest asking price of £2.99 (or free on Kindle Unlimited) it would make a good value addition to your sideline-earning library.

- Even if you don’t have a Kindle e-reader, you can read Kindle e-books using Amazon’s free Kindle app or a range of other free apps and programs. This article on the Huffpost website provides a useful guide.

As well as How to Make Money Using Your Mobile, you might like to check out Kathy Cakebread’s Glitz and Glamour Makeup blog, which also has a section devoted to money-making tips.

As always, if you have any comments or questions about this post, please do leave them below.