As is customary for bloggers at this time of year, here are the top twenty posts on Pounds and Sense in 2024, based on comments, page-views and social media shares. They are in no particular order. I have excluded any posts that are no longer relevant.

I hope you will enjoy revisiting these posts, or seeing them for the first time if you are new to PAS.

All posts in the list below should open in a new tab/window when you click on the link concerned.

Thank you for being a valued Pounds and Sense reader. Just a reminder that you can get notifications every time the blog is updated via the Subscribe box on the right (or scroll down on mobile devices). You can also follow PAS on X/Twitter and Facebook and now on BlueSky as well 🙂

If you have any comments or questions about this post, of course, feel free to leave them below as usual.

If you enjoyed this post, please link to it on your own blog or social media:

In this post a few weeks ago I discussed EDF Energy’s ‘Sunday Saver’ challenge. I explained why I had some reservations about the scheme and wasn’t therefore taking it up.

The post attracted a lot of interest. It actually generated more comments than any other post I have made on Pounds and Sense. Various people (especially Harry and KenM – thanks, guys!) posted in some detail about their experiences with the scheme. As a result I changed my opinion somewhat and decided to sign up when the opportunity arose the following month.

In this update I thought I would talk about why I changed my mind and the results I have achieved myself over the last few weeks. But first, a word of explanation…

What is EDF’s Sunday Saver Challenge?

This scheme is intended to reward EDF customers for switching some of their energy usage away from peak times.

The way it works is that you’re given targets to shift your electricity consumption on weekdays away from peak hours (4pm-7pm). When you hit your weekly target (which is set individually for each user by EDF), you earn free electricity the following Sunday.

EDF say, ‘The more you shift, the more you earn – reduce your weekly peak usage by 40% and you could earn up to 16 hours of free electricity per week.’ The challenge takes place monthly, starting on the first Monday of each month.

Why Did I Have Reservations?

As I said above, I had various reservations about the scheme prior to signing up. I have copied below the relevant paragraphs from my original post.

To benefit from this scheme you have to cut your daily energy usage every weekday between 4pm and 7pm. That’s quite a long period (three hours), and coincides with when I would normally be cooking my evening meal. To have any realistic chance of cutting my energy use during this time, I would have to eat either ridiculously early or significantly later than normal. For various reasons, including my health, I prefer to eat between 6 and 7 pm and no later. So that in itself is a big ask and would impact drastically on my normal routine.

Free electricity on Sunday sounds great, but the devil is in the detail. EDF say that you will get ‘up to 16 hours’ of free electricity if you meet their targets, but are very vague about what this means in practice. Specifically, they don’t explain how your energy-saving targets are calculated, how any reduction in usage translates to free hours, or when on Sunday you will be able to use the free electricity awarded.

In addition, they say there are ‘fair usage’ limits to how much free electricity you can have. Again, they are vague about what this means in practice. The obvious way to use your free electricity would be to charge your EV, and I strongly suspect limits would be placed on this. As for me, I don’t have an EV and don’t want one, so my options for benefiting from the free electricity would be limited. I could shift use of appliances like my washing machine to Sunday but doubt if I could save more than a few kw/h this way (obviously the exact number would depend on how many free hours I was allocated, which is anyone’s guess). That means my free electricity would likely benefit me by no more than a pound or two.

Lastly, as a solar panel owner I already get some free electricity anyway. My panels obviously generate less in the winter, but during daylight hours they still produce something. That means any benefit from free electricity on Sundays will be reduced, especially if (as is likely) the free hours are in the day rather than at night.

So What Changed?

The comments and info posted by readers who had signed up for the challenge and (in general) had benefited from it changed my views somewhat. They also addressed some of the doubts I had expressed in my original post.

As regards the free hours on Sunday, depending on how much you reduce your usage you can get anything from 4 hours to a maximum of 16. The free hours always start at 8 am and go on until as late as 12 midnight if you achieve the full target saving.

There are indeed ‘fair usage’ limits for the free hours you are awarded. They are as follows: 11.25 kWh with 4 free hours; 22.5 kWh with 8 free hours; 33.75 kWh with 12 free hours; and 45 kWh with 16 hours. EDF say these amounts are subject to change.

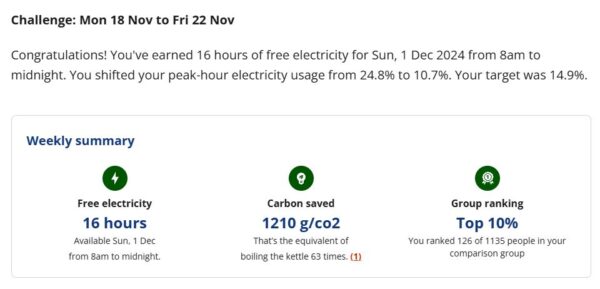

I still don’t know how exactly the saving targets are set, but here is a screen capture showing the ones I was set last week and the results I obtained.

As you can see, that was a successful week! I’ll talk more about my personal experiences with the Sunday Saver challenge below.

I also realised that, while I don’t have an EV, I could use a fair-sized portion of my free electricity charging my home storage battery from the grid. This wasn’t something I had done before (I got my battery mainly to store power generated by my solar panels) but obviously I knew it was possible. As things turned out (see below) it wasn’t without its challenges. But without doing this I’m not convinced I could have used enough free electricity to make the scheme worthwhile.

I do, incidentally, still think that EDF should make the terms and conditions of the challenge clearer prior to signing up. But anyway, based on info received from my readers, I felt it was worth giving it a try. So here’s a bit about my experiences with the November challenge.

So What Happened?

When I decided to do the EDF Sunday Saver challenge, I was clear I wasn’t going to cause myseff a ton of hassle cutting my electricity usage to the bone (I live on my own these days, incidentally). I decided I could probably defer starting my (electric) cooking till 7 pm. That was a minor inconvenience, but so far anyway I’ve been getting around it by eating meals that are quick to cook (yesterday I had gnocchi with pesto and spinach, for example). I’ll admit I’ve had a few microwave meals as well. I did also do some healthier batch cooking on one of the Sundays to produce meals I could quickly heat up during the week.

Shifting my main cooking time has undoubtedly done more than anything to reduce my peak-time energy use. Apart from that I have done little. I wouldn’t normally be hoovering or using the washing machine at peak times anyway. I have made a point of turning off my desktop computer by 4 pm (something I should probably have been doing anyway). I’ve also been a bit more careful about switching off lights when I don’t need them. And obviously I don’t use any electric heating during peak hours (thankfully I have gas central heating and a separate gas fire in the lounge). And that’s it really. For the first three weeks of the November challenge I achieved my targets fairly easily, earning the maximum 16 hours for two of them and 12 hours for the other.

I saved all my hoovering and clothes washing for Sundays to make use of the free electricity. In addition, as mentioned above, I set my home battery to charge from the grid that day. Unfortunately because I hadn’t done this before – and the software isn’t as intuitive as it should be – the first time it didn’t work at all. The following Sunday I got it working but somehow must have set it to charge every day in the evening. So on the Monday the battery started charging at the maximum rate (6 kw/h) at 5 pm. Unfortunately I didn’t notice this until around 6 pm, so that drove a coach and horses through my weekly energy-saving target. At the time of writing, my weekly dashboard shows that I am currently using 97.5% of my electricity during peak hours and – unsurprisingly – am ‘not on target’ to achieve the 14.9% set for me. Obviously, then, I will have to write off this week. I just hope that my poor performance will encourage EDF to set me generous targets in December!

Closing Thoughts

Overall, my experiences have been positive enough to want to continue the Sunday Saver challenge. I will have saved some money by doing it, which will be credited to my account in December.

It will be interesting to see what usage targets EDF set me next month, especially after I messed up the final week of the challenge. But in any event, EDF have also let me know that anyone signing up for the December challenge will get an automatic eight hours of free electricity on Christmas Day regardless of any energy savings they make. So that is another incentive to sign up for December (which I have already done),.

So those were my experiences with the EDF Sunday Saver challenge in November. I’d be interested to hear how you got on if you did it too, and whether you will be continuing the challenge. Also, if you are on a similar scheme with another energy company, I’d love to hear how that’s going for you. Please post any comments below as usual, not forgetting to allow me a few hours to approve them.

As I have said before on PAS, I can offer anyone switching to EDF £50 off their bills if they use my refer-a-friend link at https://edfenergy.com/quote/refer-a-friend/sunny-koala-9462 when applying. I will also get £50 off my bill if you do this (£75 till 12 December 2024), which is duly appreciated

If you enjoyed this post, please link to it on your own blog or social media:

Recently my energy supplier, EDF Energy, has been sending me invitations to sign up for what it calls its ‘Sunday Saver’ challenge.

The way this works is that you sign up to shift some of your electricity usage on weekdays away from peak hours (4pm-7pm). When you hit your target (which is set individually for each user by EDF), you earn free electricity the following Sunday.

EDF say, ‘The more you shift, the more you earn – reduce your weekly peak usage by 40% and you could earn up to 16 hours of free electricity per week.’

The challenge is due to take place monthly, starting on the first Monday of each month.

At first glance you might think this is a good offer. But as I have looked into it more, my doubts have grown. Here are my main reservations…

To benefit from this scheme you have to cut your daily energy usage every weekday between 4pm and 7pm. That’s quite a long period (three hours), and coincides with when I would normally be cooking my evening meal. To have any realistic chance of cutting my energy use during this time, I would have to eat either ridiculously early or significantly later than normal. For various reasons, including my health, I prefer to eat between 6 and 7 pm and no later. So that in itself is a big ask and would impact drastically on my normal routine.

Free electricity on Sunday sounds great, but the devil is in the detail. EDF say that you will get ‘up to 16 hours’ of free electricity if you meet their targets, but are very vague about what this means in practice. Specifically, they don’t explain how your energy-saving targets are calculated, how any reduction in usage translates to free hours, or when on Sunday you will be able to use the free electricity awarded.

In addition, they say there are ‘fair usage’ limits to how much free electricity you can have. Again, they are vague about what this means in practice. The obvious way to use your free electricity would be to charge your EV, and I strongly suspect limits would be placed on this. As for me, I don’t have an EV and don’t want one, so my options for benefiting from the free electricity would be limited. I could shift use of appliances like my washing machine to Sunday but doubt if I could save more than a few kw/h this way (obviously the exact number would depend on how many free hours I was allocated, which is anyone’s guess). That means my free electricity would likely benefit me by no more than a pound or two.

Lastly, as a solar panel owner I already get some free electricity anyway. My panels obviously generate less in the winter, but during daylight hours they still produce something. That means any benefit from free electricity on Sundays will be reduced, especially if (as is likely) the free hours are in the day rather than at night.

Overall, then, I am not much enamoured of EDF’s Sunday Saver challenges and won’t be signing up. Ultimately, I am not prepared to make major changes to my day-to-day schedule in pursuit of what will likely be (in my case anyway) minuscule rewards.

Obviously some will see this differently and I wish them well. And it’s good that EDF (and other companies) are exploring ways to help customers reduce their bills. I do just think this particular one – for me anyway – is a non-starter.

I would be interested to hear any comments from people doing this challenge (or similar ones from other energy companies) as to whether they find it worthwhile, and whether the benefits really do justify the changes you are required to make.

I do still recommend EDF Energy based on my personal experiences with them. And as I’ve said before on PAS, I can offer anyone switching to EDF £50 off their bills if they use my refer-a-friend link at https://edfenergy.com/quote/refer-a-friend/sunny-koala-9462 when applying. I will also get £50 off my bill if you do this, which is duly appreciated 🙂

UPDATE 22 OCTOBER 2024 – I am indebted to the readers (especially Harry!) who have taken the time to comment on this article and address some of the points raised in my original post. Based on this I have changed my views somewhat and am considering registering for the scheme when it reopens in November. If you’re still wondering whether to take the plunge, please do take the time to read the comments as (like me) they may influence your decision. I will publish an update in due course if I proceed with it next month.

UPDATE 28 NOVEMBER 2024 – Thanks again to everyone who commented on this post. Sorry I couldn’t reply to everyone individually. You may like to know that I just added a new post about why I changed my mind and registered for the EDF ‘Sunday Saver’ Challenge and how I got on in my first month. Please see https://www.poundsandsense.com/heres-why-i-changed-my-mind-about-edf-energys-sunday-saver-challenge/

If you enjoyed this post, please link to it on your own blog or social media:

The first budget under new Labour Chancellor Rachel Reeves is scheduled for Wednesday 30 October 2024.

Speculation is rife about potential tax rises aimed at addressing the country’s economic challenges. But while tax increases appear inevitable, there is still time to take proactive steps to minimize their impact on your finances.

Here are some tips for how to prepare for and reduce the burden of potential tax hikes.

1. Maximize Tax-Efficient Savings and Investments

One of the most effective ways to protect yourself from higher taxes is by taking full advantage of tax-efficient savings and investment vehicles. These include:

ISA Allowances: The annual ISA (Individual Savings Account) allowance is currently £20,000. Money saved in an ISA grows tax-free, meaning you won’t pay any income tax, dividend tax or capital gains tax (CGT) on any profits made. As well as Cash ISAs, you can invest in Stocks and Shares ISAs and Innovative Finance ISAs (IFISAs).

Personal Savings Allowance (PSA): Basic rate taxpayers can earn up to £1,000 in savings interest tax-free. Higher rate taxpayers get a reduced allowance of £500.

Starting Rate for Savings: For those with a low overall income, the starting rate for savings can be especially beneficial. If your total income (excluding savings interest) is less than £17,570, you may qualify for the starting rate for savings, which can provide up to an additional £5,000 in tax-free interest. This is discussed in more detail in my recent post How to Maximize Your Tax-Free Savings Interest.

Venture Capital Schemes: For those willing to take more risk, schemes like the Enterprise Investment Scheme (EIS) and Seed Enterprise Investment Scheme (SEIS) offer significant tax reliefs, including income tax relief and capital gains tax exemption on profits.

2. Diversify Your Investments

Diversification remains a cornerstone of sound investment strategy, especially in times of political and economic uncertainty. By spreading your investments across different asset classes – such as equities, bonds and property – you can reduce the risk of any single investment adversely affecting your portfolio. Consider international diversification as well to hedge against possible downturns in the UK economy.

3. Consider Using a ‘Bed and ISA’ Strategy

If you hold a lot of investments outside an ISA or other tax shelter, this can be a good strategy to reduce your tax liability.

Bed-and-ISA involves selling taxable stocks and shares and then repurchasing them within an ISA wrapper. This allows you to transfer investments into a tax-protected environment, where future gains and income will be sheltered from tax. Note that you cannot transfer taxable stocks and shares directly into an ISA, but Bed-and-ISA performs the same function.

On the minus side, Bed-and-ISA may incur some costs in terms of transaction fees and any difference (spread) between selling and buying prices. You may also become liable for CGT if any profits realized exceed your annual tax-free allowance. The long-term benefits can be substantial, however. This applies especially if – as seems likely – tax-free CGT allowances are reduced and the rates payable are increased. Of course, the Conservatives started doing this when they were in power.

4. Rebalance Your Portfolio Towards Tax-Efficient Assets

Different types of investments are subject to different levels of tax. It’s important to rebalance your portfolio to favour assets that could be less impacted by tax hikes.

Dividends: The tax-free dividend allowance for 2024/25 is £500, and anything above this is taxed at rates of 8.75% (basic rate taxpayers), 33.75% (higher rate), and 39.35% (additional rate). If dividend tax rises further, you may want to limit investments in dividend-paying stocks outside of tax-free wrappers like ISAs and pensions (see above).

Capital Gains: The capital gains tax (CGT) allowance has dropped to £3,000 for the 2024/25 tax year, and there are fears it could be cut further. Consider selling assets to crystallize gains while you can still use your allowance, or shift investments into tax-free vehicles like ISAs using the ‘Bed and ISA’ (or ‘Bed and Pension’) strategy discussed above..You can also offset capital gains with capital losses. If you have investments that have performed poorly, selling them to realize a loss can help offset gains elsewhere in your portfolio. Remember that CGT only applies when a profit (or loss) is actually realised.

Bonds: Government and corporate bonds are often seen as lower-risk investments and may be less vulnerable to tax increases than equity income streams. You might want to consider including more bonds in your portfolio.

Commodities: Gold and other commodities have traditionally been seen as a safe haven in times of economic upheaval. There are risks, however, and it’s important to do your own ‘due diligence’ and seek professional advice before going down this route.

5. Use Your Pension Allowance

Pensions are one of the most tax-efficient ways to save for the future. Contributions receive tax relief at your marginal income tax rate, which means for every £100 you contribute, the government effectively adds £20 for basic-rate taxpayers, £40 for higher-rate taxpayers, and £45 for additional-rate taxpayers.

Consider increasing your pension contributions to mitigate the impact of other tax rises. Just be sure to keep within the current £60,000 annual pension contribution limit. Note that for those earning over £260,000 (adjusted income), the tax-free allowance tapers. More info about this can be found on the government website.

If you’re self-employed, consider setting up or increasing contributions to a private pension or Self-Invested Personal Pension (SIPP) to take full advantage of these benefits.

6. Plan for Inheritance Tax (IHT) Rises

Inheritance tax has long been a controversial topic, and it may well increase under the new government. Currently, the IHT threshold is £325,000, with an additional £175,000 allowance if you’re passing your main home to direct descendants. Anything above this is currently taxed at 40%.

To mitigate IHT risks:

Consider making gifts: You can give away up to £3,000 per year tax-free, with additional allowances for wedding gifts and gifts from surplus income. Gifts between spouses are normally exempt from CGT or IHT, allowing you to transfer assets and take advantage of both partners’ allowances.

Set up a trust: Placing assets in a trust may help reduce IHT liabilities.

Life insurance policies: Some people take out policies specifically designed to cover future IHT bills. Always seek professional advice, however, as trusts and insurance policies can be complex.

7. Review Your Income Structure

Reeves may target income tax thresholds and reliefs, particularly for higher earners. Reviewing how your income is structured could help mitigate the impact.

Salary Sacrifice Schemes: Consider participating in salary sacrifice schemes, where you give up part of your salary in exchange for benefits like pension contributions, childcare vouchers, or cycle-to-work schemes. This will reduce your taxable income.

Dividend Income: If you run a business or own shares, taking income as dividends can be more tax-efficient than a salary, particularly if the dividend tax rates remain lower than income tax rates. Any good accountant will be able to advise you.

Spousal Income Splitting: If your spouse is in a lower tax bracket, transferring income-generating assets to them can reduce your overall tax burden. This is particularly useful for rental income or dividends from jointly held investments.

8. Prepare for Property Tax Changes

Property taxes, including stamp duty and council tax, could see reforms or increases. Here’s how to plan.

Bring Forward Property Transactions: If you’re considering buying (or selling) property, it may be wise to do so before any potential stamp duty increases are announced. Locking in current rates could save you significant costs.

Consider Downsizing: If you anticipate increased council tax rates or other property-related taxes, downsizing to a smaller home could reduce your future tax liabilities and lower your overall living costs. And, of course, doing this should release some of the equity in your property, which you can then use to help maintain your standard of living.

9. Enhance Charitable Giving

If Reeves increases income tax or reduces the thresholds for higher tax rates, charitable giving can become a more attractive option.

Gift Aid: Donations made under Gift Aid are tax-efficient, as charities can claim an additional 25% from the government. Higher-rate taxpayers can claim back the difference between the basic rate and higher rate of tax on their donations.

Donor-Advised Funds: These funds allow you to make a charitable contribution, receive an immediate tax deduction, and then recommend grants from the fund over time. It’s a strategic way to manage charitable giving while benefiting from tax relief.

10. Stay Informed and Seek Professional Advice

Tax planning can be complex, especially in an uncertain economic environment. Staying informed about potential changes in the budget and seeking professional financial advice can help you adapt your strategy to minimize your tax liabilities effectively.

Monitor Budget Announcements: Keep an eye on the budget and any subsequent economic statements to understand how proposed changes might affect you. Quick responses can sometimes yield significant tax savings.

Consult a Financial Adviser: A qualified financial adviser can help tailor a tax-efficient strategy to your individual circumstances, taking into account your income, assets, and long-term financial goals.

Closing Thoughts

While tax rises in Rachel Reeves’ first budget may be inevitable, UK residents have various strategies at their disposal to mitigate the impact.

By taking advantage of tax-efficient investments, restructuring income and staying informed, you can protect your wealth and ensure that any tax increases have a minimal effect on your financial well-being. As always, professional advice tailored to your specific situation is invaluable in navigating these changes effectively.

If you have any comments or questions about this post, please do leave them below. But bear in mind that I am not a qualified tax adviser and cannot provide personal financial advice. All investing carries a risk of loss.

If you enjoyed this post, please link to it on your own blog or social media:

In these challenging times, we all need to ensure our savings stretch as far as possible. So today I thought I’d set out the range of tax-free allowances you can use to help do this.

Personal Savings Allowance (PSA)

The Personal Savings Allowance (PSA) was introduced in April 2016 and allows you to earn a certain amount of interest tax-free each year. The amount of your PSA depends on your income tax band:

Basic Rate Taxpayers (20%): You can earn up to £1,000 in savings interest tax-free.

Higher Rate Taxpayers (40%): You can earn up to £500 in savings interest tax-free.

Additional Rate Taxpayers (45%): You do not receive a PSA, meaning all interest earned is taxable.

For example, if you are a basic rate taxpayer and earn £900 in interest from your savings in a tax year, this amount is within your PSA and therefore tax-free. However, if you earn £1,200 in interest, £200 of that will be subject to tax at your marginal rate.

Individual Savings Accounts (ISAs)

ISAs are another powerful tool for earning tax-free interest. There are several types of ISA, with varying annual contribution limits and benefits:

Cash ISAs: You can save up to £20,000 per year, and the interest earned is entirely tax-free.

Stocks and Shares ISAs: Also with a £20,000 annual limit, any capital gains or dividends received are tax-free.

Lifetime ISAs (LISAs): Designed for first-time homebuyers or retirement savings, you can contribute up to £4,000 annually to a LISA, with a 25% government bonus on contributions. The interest earned is tax-free.

Innovative Finance ISAs (IFISAs): These allow you to earn tax-free interest from peer-to-peer lending within the £20,000 annual limit.

You can mix and match these ISAs and you can now open as many as you like within a single tax year. But the total amount you contribute in a tax year cannot exceed the overall limit of £20,000.

Starting Rate for Savings

For those with a lower overall income, the starting rate for savings can be particularly beneficial. If your total income (excluding savings interest) is less than £17,570, you may qualify for the starting rate for savings, which can provide up to an additional £5,000 in tax-free interest.

Here’s how it works:

If your non-savings income is below £12,570 (the personal allowance for most people), you can use the full £5,000 starting rate for savings.

For every £1 your non-savings income exceeds £12,570, your starting rate for savings decreases by £1.

For example, if your non-savings income is £15,000, your PSA is reduced by £15,000 minus £12,570 = £2,430. Subtracting £2,430 from £5,000 leaves £2,570. You can therefore earn up to £2,570 in interest tax-free under the starting rate.

If you qualify for both the starting rate for savings and the PSA, you can earn up to £5,000 in interest tax-free under the starting rate, plus an additional £1,000 (or £500 for higher rate taxpayers) under the PSA. For example, if you’re a basic rate taxpayer with £12,000 in non-savings income, you could potentially earn up to £6,000 in interest tax-free (£5,000 from the starting rate and £1,000 from the PSA). Both allowances can be combined to maximize the amount of interest you can earn tax-free.

Premium Bonds provide a chance to win tax-free prizes each month. While the odds of a big win may be slim, any winnings are tax-free. Similarly, some NS&I savings products, like certain Savings Certificates, offer tax-free interest.

Summing Up

By understanding and utilizing these tax-free allowances, you can maximize the interest you earn on your savings without paying tax. Here’s a quick recap:

Personal Savings Allowance: Up to £1,000 for basic rate taxpayers, £500 for higher rate taxpayers.

ISAs: Up to £20,000 per year across various types.

Starting Rate for Savings: Up to £5,000 if your non-savings income is below £17,570.

Premium Bonds and Some Other NS&I Products: Tax-free interest and prizes.

Be sure to review your financial situation regularly and consider using these allowances to optimize your savings strategy. By leveraging these benefits, you can grow your savings more effectively and keep more of your hard-won interest.

Finally, this post sums up the situation currently. The new government is looking to raise extra tax revenue any way it can, however, and tax-free savings allowances certainly aren’t immune. Obviously I will update this article (and/or publish a new one) if the rules are changed in future.

As always, if you have any comments or questions about this post, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

As you may have heard, UK citizens are currently bearing the highest tax burden since WW2.

And with the new government looking to raise more money to pay for its ambitious spending plans, there is no sign of that changing any time soon. So today I thought I’d set out some ways you may be able to boost your finances without increasing your tax liability.

As you’ll see, doing this needn’t involve complicated investment strategies or seeking ‘loopholes’ in tax legislation. There are numerous perfectly legal ways to boost your finances without worrying about the taxman. Here are ten methods to consider…

1. Maximize Your ISA Contributions

Individual Savings Accounts (ISAs) offer a fantastic way to save money tax-free. The annual ISA allowance for 2024/25 is (still) £20,000. Whether you choose a Cash ISA, a Stocks and Shares ISA, an Innovative Finance ISA (IFISA), or a combination of all three, any returns you make are entirely tax-free. This makes ISAs a straightforward and effective way to boost your savings.

2. Utilize Your Personal Savings Allowance

For basic-rate taxpayers, the first £1,000 of interest on savings is tax-free each year. Higher-rate taxpayers can earn up to £500 in interest before paying tax. This means you can keep more of the interest you earn from your savings accounts, helping your money grow more quickly.

3. Invest in Premium Bonds

Premium Bonds, offered by National Savings & Investments (NS&I), provide a unique way to save money tax-free. Instead of earning interest, your bonds enter a monthly prize draw for cash prizes. Any winnings are tax-free.

Premium bonds are guaranteed by the UK government and you can get your money back at any time. Obviously there are never any guarantees how much you will win (or if you will win at all) so it’s strongly advised that you have other savings and investments as well.

4. Try Matched Betting

Matched betting is a method used to exploit free bet promotions offered by bookmakers. When done correctly it’s risk-free and the earnings are tax-free in the UK. Matched betting involves placing bets on all possible outcomes of an event using free bets to ensure a profit regardless of the result. While it requires careful attention to detail, it can be an effective way to boost your finances. Just be aware that the longer you do it, the more difficult it may become to find suitable opportunities. But if you need a short-term, tax-free income boost, matched betting can certainly fit the bill.

If you’re married or in a civil partnership and one of you earns less than the personal allowance (£12,570 in 2024/25), you could transfer £1,260 of your allowance to your partner, reducing their tax bill by up to £252 a year. This one simple step can provide a meaningful boost to your household finances.

6. Earn Up To £1,000 Tax-free

If you have a hobby or skill, consider monetizing it. The UK government allows you to earn up to £1,000 (gross) tax-free each year from trading or property income under the Trading and Property Allowance. This could include doing odd jobs, selling handmade crafts, offering tutoring services, or renting out a spare room occasionally. As long as you keep under the £1,000 annual limit, you don’t have to pay tax on this money or even tell the taxman about it.

7. Utilize Cashback and Rewards Cards

Cashback and rewards credit cards can provide a significant boost to your finances if used wisely. By earning points or cashback on everyday purchases, you can effectively reduce your outgoings. Just remember to pay off any balance in full each month to avoid interest charges. Cashback cards and apps (e.g. Jam Doughnut) are tax-free, as HMRC regard them as simply returning your own money to you.

8. Rent a Room Scheme

Under the Rent a Room Scheme, you can earn up to £7,500 per year (gross) tax-free by renting out a furnished room in your home. This is a great way to utilise extra space and generate additional income without incurring any tax liability.

9. Switch and Save

Regularly switching your utility providers, insurance, bank account and other services can save you hundreds of pounds each year. Comparison websites such as Compare the Market make it easy to find the best deals, and many offer incentives for switching. These savings are effectively tax-free boosts to your disposable income. And switching bonuses (as offered by some banks) are tax-free, as HMRC regard them as a form of cashback.

10. Sell Stuff You No Longer Need on eBay

Selling items you no longer need or use on platforms like eBay can provide a significant financial boost. The taxman allows individuals to sell personal items without paying tax on the proceeds provided it’s not done as a business. This decluttering process can turn unused possessions into tax-free cash.

Just be aware that if you buy things with the intention of reselling them, that would be seen as trading and there could be tax to pay. Also, if you sell a product for more than you originally paid for it, you could be liable for capital gains tax (CGT) if the profit made exceeds your annual CGT tax-free allowance.

Closing Thoughts

So there you are – ten ways you can boost your finances without incurring any extra tax liability. Of course, there is no guarantee that the government won’t change the law on some of these, so I will update this article if that happens. For the time being, though, I urge you to take advantage of as many of these opportunities as you can. In the current cost of living crisis, we all need to hang on to as much of our hard-earned money as possible!

As always, if you have any comments or questions about this article – or other tax-free opportunities that you think should have been covered as well – please do leave them below.

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss. Note also that posts on PAS may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media:

For better or worse, the UK has elected a Labour government. There will undoubtedly be many changes in economic policy, taxation and regulation, which of course will affect personal finances. So today I am setting out some ways in which you may be able to safeguard your savings and investments as Labour take control.

As Pounds and Sense is aimed especially at older readers, I am obviously writing from that perspective, but many of these points will apply equally to younger people as well.

1. Diversify Your Investments

Diversification remains a cornerstone of sound investment strategy, especially in times of political uncertainty. By spreading your investments across different asset classes – such as equities, bonds and property – you can reduce the risk of any single investment adversely affecting your portfolio. Consider international diversification to hedge against domestic political risks. This means investing in global markets to mitigate potential local economic disruptions. Historically, gold and commodities can also act as a hedge against economic upheavals.

2. Understand Tax Implications

Labour governments typically lean towards higher taxes on wealth and income to fund public services. Stay informed about potential changes in tax policies, such as higher rates of capital gains tax, dividend tax or inheritance tax. To mitigate the impact:

Utilize ISAs and Pensions – make full use of tax-efficient accounts like Individual Savings Accounts (ISAs) and pensions, which can shield your investments from tax.

Consider Timing of Asset Sales – if changes in capital gains tax (CGT) are anticipated, you might want to accelerate the sale of certain assets before new rates take effect.

Inheritance Planning – review your estate plans and consider trusts or gifts to mitigate higher inheritance taxes.

3. Consider a Bed-and-ISA Strategy

If you hold a lot of investments outside an ISA or other tax shelter, this can be a good strategy to reduce your tax liability.

Bed-and-ISA involves selling taxable stocks and shares and then repurchasing them within an ISA wrapper. This allows you to transfer investments into a tax-protected environment, where future gains and income will be sheltered from tax. Note that you cannot transfer taxable stocks and shares directly into an ISA, but Bed-and-ISA performs the same function.

On the minus side, Bed-and-ISA may incur some costs in terms of transaction fees and any difference (spread) between selling and buying prices. You may also become liable for CGT if any profits realized exceed your annual tax-free allowance. The long-term benefits can be substantial, however. This applies especially if – as seems likely under Labour – tax-free CGT allowances are reduced and the rates payable are increased. Of course, the Conservatives have started doing this already.

Some Online Platforms Will Undertake Bed-and-ISA on Your Behalf – that means you don’t have to do the share selling and buying yourself. One such platform is AJ Bell. This can obviously save you a bit of time and may work out cheaper as well. Be aware that you will still have to pay some fees and charges, however, along with CGT on any capital gains above your personal allowance.

A Similar Option is Bed-and-SIPP – with this you sell taxable stocks and shares and then buy the same ones back within your private pension (SIPP).

This Strategy is Named After an Older One Called Bed-and-Breakfasting – at one time this was deployed to minimize CGT liability. The law was changed to make bed-and-breakfasting less effective, but Bed-and-ISA can still work well.

Bed-and-ISA Can Also Be Used to Crystallize a Loss – this can then be set against other taxable profits in the year concerned to reduce your CGT liability.

Property has long been a favoured investment in the UK. However, the Labour government may introduce policies adversely affecting buy-to-let investors, such as rent controls or higher taxes on second properties. To protect your property investments:

Assess Rental Yields and Potential Regulations – ensure your rental income can withstand potential regulatory changes.

Consider Property Ownership Structures – holding property through a limited company can sometimes be more tax-efficient.

Stay Liquid – keep some liquidity to manage any unforeseen expenses or changes in regulation.

5. Focus on Stable Income Investments

Investments that provide steady income can be particularly valuable during uncertain times. Consider:

Dividend-Paying Stocks – companies with a history of stable dividends can provide a reliable income stream.

Bonds and Fixed Income – government and high-quality corporate bonds can offer stability and predictability.

Infrastructure Funds – these often provide regular income and are less sensitive to economic cycles.

6. Monitor Inflation and Interest Rates

Economic policies under Labour may lead to changes in inflation and interest rates. Historically, increased government spending can drive inflation, which in turn erodes the value of savings. And if inflation rises, the Bank of England is very likely to respond by raising interest rates. To combat this:

Consider Inflation-Linked Investments – investments that adjust with inflation, such as inflation-linked bonds.

Review Savings Accounts – ensure your savings accounts offer competitive interest rates. A cash ISA will also shelter your savings from tax.

Consider Fixed-Rate Mortgage Deals – if interest rates rise under Labour, a fixed-rate deal on your mortgage will offer some protection.

Take Action on Equity Release – if you’ve been considering this, there is a case for proceeding sooner rather than later, in case long-term interest rates rise

7. Stay Informed and Flexible

The political landscape can change rapidly. Regularly review your investment portfolio and financial plans to ensure they align with current and anticipated economic policies. Consider consulting with a financial advisor who can provide tailored advice based on the latest developments. Depending on your circumstances, you may want to consult with an accountant as well.

8. Invest in Knowledge and Skills

An often-overlooked investment is in your own knowledge and skills. By staying informed about personal finance and economic policies, you can make better decisions. Attend financial planning seminars, read reputable financial news, and consider taking financial education courses. There are also some excellent personal finance websites, including Money Saving Expert, Which? Money and This Is Money. I recommend reading and following all of them.

And naturally you should keep reading Pounds and Sense as well. Why not take a moment to subscribe in the right-hand column so as never to miss any of my posts in future? ➡➡➡

Closing Thoughts

While the Labour government may introduce changes that impact savings and investments, proactive planning and informed decision-making can help protect your financial future.

By diversifying your portfolio, making good use of tax-efficient investments such as ISAs and pensions, focusing on stable income investments, and staying adaptable, you can navigate the uncertainties and safeguard your assets. Remember, the best defence is a well-thought-out strategy and staying informed about the changing economic landscape. Good luck, and I wish you every success in achieving your financial goals.

As always, if you have any comments or questions about this post, please do leave them below.

Disclaimer: I am not a qualified financial adviser and nothing in this post should be construed as personal financial advice. You should always do your own ‘due diligence’ before investing, and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

This is an updated version of my original article.

If you enjoyed this post, please link to it on your own blog or social media:

Navigating personal finances can be challenging, especially for those on a limited income. Recognising this, the UK government introduced the Help to Save scheme, which is designed to encourage and support individuals receiving certain benefits to build their savings.

Here’s an overview of how the scheme works, who is eligible, and the benefits it offers.

What is the Help to Save Scheme?

Help to Save is a government-backed savings account that offers a generous bonus to low-income earners. Launched in September 2018, the scheme aims to encourage regular savings by offering a 50% bonus on the amount saved over four years. This means that for every £1 saved, the government adds 50p, potentially providing a significant financial boost for those who participate.

Who is Eligible?

The scheme is targeted at individuals who are receiving certain benefits. Specifically, you can open a Help to Save account if you are:

receiving Working Tax Credit

entitled to Working Tax Credit and receiving Child Tax Credit

or claiming Universal Credit and have earned income of £722.45 or more in your last monthly assessment period

It’s important to note that you need to be living in the UK to be eligible, though if you are a Crown servant or a member of the armed forces posted overseas, you can still apply.

How Does It Work?

Once you open a Help to Save account, you can save between £1 and £50 each calendar month. The maximum you can save over four years is £2,400. You don’t have to pay in every month, and you can make multiple deposits each month, provided the total does not exceed £50.

The key feature of the scheme is the bonus structure. Here’s how it works:

Year 1 and 2 Bonus: After the first two years, you’ll receive a bonus of 50% of the highest balance you’ve achieved during those two years.

Year 3 and 4 Bonus: At the end of the fourth year, you’ll receive another 50% bonus on the difference between the highest balance you’ve achieved in the second two years and the highest balance in the first two years.

This means you could earn up to £1,200 in bonuses over the four years if you save the maximum amount. No other savings scheme can come close to beating this.

Are There Any Age Limits for Help to Save?

One of the appealing aspects of the Help to Save scheme is its inclusivity in terms of age. There are no specific age restrictions for opening a Help to Save account, provided you meet the eligibility criteria related to benefits and the general requirement of living in the UK (unless you are a Crown servant or a member of the armed forces posted overseas).

Theoretically there is no upper age limit for Help to Save, but all the qualifying benefits do require you to be earning some work-related income. So if you are retired and living entirely off your pensions and benefits you are unlikely to qualify. If in any doubt, however, you can always apply anyway and see what response you receive.

Why Should You Consider It?

The Help to Save scheme provides a risk-free way to build a financial cushion. The bonuses are guaranteed and tax-free, which makes it an attractive option for those looking to save a small amount regularly without any risk of losing their money.

Additionally, the flexibility of the scheme allows you to save what you can, when you can. There is no penalty for missing a month or for withdrawing your money. However, frequent withdrawals might impact the bonuses, as they are calculated based on the highest balance achieved.

How to Apply

Opening a Help to Save account is straightforward. You can apply online via the official government website or through the HMRC app. To apply, you will need a Government Gateway User ID and password. If you don’t have one, you can create one during the application process.

Closing Thoughts

For those receiving eligible benefits, the Help to Save scheme offers a valuable opportunity to build a savings pot with the added advantage of tax-free government bonuses. It’s designed to be simple and flexible, making it easier for individuals to develop a habit of saving and improve their financial security. If you qualify, it’s certainly worth considering as a step towards a more stable financial future.

Trading 212, a well-known platform in the UK for trading stocks and shares, recently introduced a new product to its lineup: the Trading 212 Cash ISA.

This addition comes as part of the company’s efforts to diversify its offerings and cater to a broader range of financial needs. Today I’ll be delving into the details of this new product, highlighting its pros and cons. I’ll also reveal why I decided to open a Trading 212 Cash ISA myself.

Let’s start with the basics though…

What is a Cash ISA?

A Cash ISA (Individual Savings Account) is a tax-free savings account where the interest earned is not subject to income tax. Each tax year, individuals can deposit up to a certain limit, which for the 2025/26 tax year is £20,000. Cash ISAs are a popular choice for those looking to save money without the risk associated with investments in the stock market.

Pros and Cons of the Trading 212 Cash ISA

Pros

Tax-Free Interest: Like all ISAs, the interest earned in a Trading 212 Cash ISA is completely tax-free. This makes it an attractive option for savers looking to maximize their returns without the burden of paying income tax on their earnings.

Competitive Interest Rate: The current rate is 5.07% per annum, which puts it at or near the top of the Best Buy tables. This includes a special introductory bonus of 0.72% for the first 12 months, after which it reduces to 4.35%. Rates are variable and can fluctuate based on market conditions, so it’s possible they will fall in future. The platform will want to remain competitive with other financial institutions, however.

No Fees: The Trading 212 Cash ISA is an entirely fee-free account.

User-Friendly Platform: Trading 212 is known for its intuitive and user-friendly interface. The same ease of use applies to their Cash ISA, making it simple for users to manage their savings, check balances and track interest earned. You can manage your account via the Trading 212 website or an app on your phone.

Low Minimum Investment: You can start with as little as £1 if you like. There is no upper limit other than the annual £20,000 ISA allowance (for all ISAs you hold).

Security: Funds held in a Trading 212 Cash ISA are protected under the Financial Services Compensation Scheme (FSCS) up to £85,000 per individual. This provides peace of mind to savers, knowing their money is secure.

Accessibility: You can withdraw whenever you want and as often as you want.

Daily Interest Payments: Interest is credited to your account daily and added to your account at the end of each month (before that it is shown as ‘pending’). There is no need to wait up to a year to receive interest as with some other savings accounts.

Integration with Other Products: For existing Trading 212 users, the Cash ISA seamlessly integrates with other accounts and products on the platform such as the Trading 212 Stocks and Shares ISA and general investment account.

Easy Transfers: You can transfer in your ISA from another provider and you’ll be able to freely transfer between your Trading 212 Stocks and Shares ISA as well.

Flexible ISA: You can withdraw from it and return your funds in the same tax year without it counting twice against your annual ISA allowance. For example, if you invest £10,000 and then withdraw £5,000, you can still invest £15,000 in that tax year (the remaining £10,000 of your £20,000 allowance plus return of the £5,000 you withdrew). Not all cash ISAs currently offer this.

Cons

Interest Rate Variability: As mentioned above, while Trading 212 currently offers a competitive rate, this may change and it may not always be the highest on the market. It’s always a good idea to compare rates with other providers to ensure you are getting the best deal. That obviously applies especially if you are reading this article some time after it was first published (though I will endeavour to update it from time to time).

Not Instant Access: You can withdraw money any time via the website or app but it may take up to three days to arrive in your bank account. So it is quick access but not instant.

No High Street Presence: Trading 212 operates entirely online. They do have a customer service department which you can contact by phone or email. They are not set up to provide telephone banking, though.

Limited Track Record: As a fairly new product, the Trading 212 Cash ISA does not have a long track record. Some more cautious savers might prefer established Cash ISA providers with a proven history.

No Investment Growth: Unlike a Stocks and Shares ISA, a Cash ISA does not offer the potential for investment growth. While it is safer, it may yield lower returns in the long term compared with investment-based ISAs. Of course, there is no reason why you can’t have both.

Inflation Risk: The interest earned on a Cash ISA may not always keep pace with inflation, potentially diminishing the real value of savings over time.

Contribution Limits: The annual contribution limit of £20,000 applies across all ISAs. If you are already investing in a Stocks and Shares ISA or other type of ISA, the amount you can contribute to a Cash ISA will be reduced.

APR vs APY

One other thing to note is that the interest rate quoted by Trading 212 is described as APY. This is short for annual percentage yield. This is another term for AER (annual equivalent rate) which I discussed a while ago in this blog post.

What this means is that the rate quoted by Trading 212 – currently 5.07% for the first 12 months – incorporates the compounding of interest payments. As mentioned above, in the Trading 212 Cash ISA interest is credited daily, and once it is in your account you get interest on the interest as well. That is obviously a good thing, but it does mean the advertised APY already accounts for this. If the interest rate was quoted instead as an APR, it would actually be slightly lower.

Does this matter? Well, yes and no. If you keep your money in the account for a full year, you will get the full rate of interest quoted (as APY). But if you withdraw it earlier – after six months, say – you won’t receive exactly half of this, as the compounding effect won’t have had as long to work. So instead of half the quoted 5.07% (currently) for six months, you would receive marginally less. It would only make a very small difference, but is worth bearing in mind if you are saving for a short-term goal in particular.

My Own Example

As mentioned above, I opened a Trading 212 Cash ISA myself. I already had a Trading 212 General Investment account, so that made the decision easier. But I was also attracted by the competitive interest rate and the fact that interest was calculated daily.

A further consideration is that there is now no limit to the number of different ISAs you can open (as long as you don’t exceed the overall £20,000 annual limit). So opening a Trading 212 Cash ISA doesn’t preclude opening another Cash ISA with a different provider later in the year if circumstances change. It is also easier now to transfer money from one ISA to another.

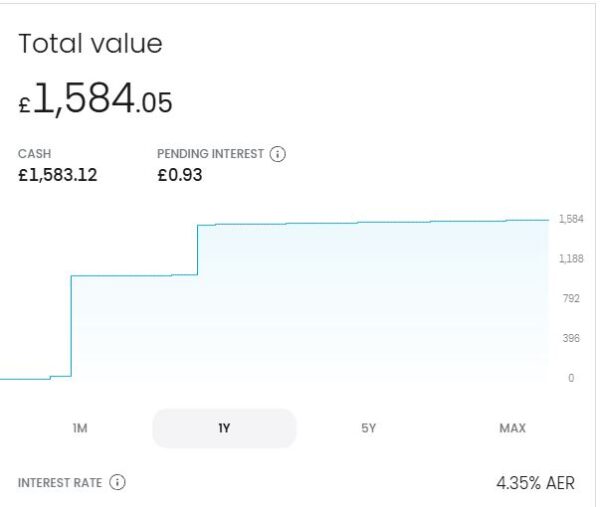

I have a Santander Edge bank account which comes with a linked Edge Savings account (non-ISA). At the time this was paying a market-leading 7% (AER) on balances of up to £4,000 (it’s now reduced to 4.41%). I had maxed this out, however, so was looking for an alternative, tax-efficient home for the balance of my short- to medium-term savings (the other savings offers from Santander were a lot less appealing). The Trading 212 Cash ISA seemed ideal for me, therefore. I started by depositing £25 and as that went fine I added another £1,500. Interest has been credited every day as promised, and as of 5 May 2025 my original £1,525 has grown to £1,584.05 (see screen capture below). Note that the total quoted includes £0.93 in pending interest accrued so far during May, which (as mentioned above) will be credited to my account at the end of the month.

Conclusion

In my view, the Trading 212 Cash ISA is an enticing addition to the range of financial products available to UK savers.

It combines the tax-free benefits of a traditional ISA with the user-friendly experience Trading 212 is known for. And the interest rate (at present anyway) is very competitive. But obviously you should weigh up the pros and cons set out above carefully before deciding if it’s right for you. As always, it’s wise to compare options and consider your financial goals – both short and longer term – before proceeding.

As always, if you have any comments or questions about this post, please do leave them below.

Disclaimer: I am not a professional financial adviser and nothing in this post should be construed as personal financial advice. You should always do your own ‘due diligence’ before investing and take professional advice if in any doubt how best to proceed.

If you enjoyed this post, please link to it on your own blog or social media:

Today I have another guest post for you on the subject of saving money and getting freebies 🙂

My friends at Hot Free Stuff have put together this list of seven top money-saving websites where you can get freebies, discount codes, downloadable coupons, and more. Check them out, and don’t forget to sign up for free emails from Hot Free Stuff to get all the latest free offers daily!

Are you a stressed-out mum (or dad) trying to make the family budget work?

It takes juggling to make the household budget balance without the need for taking a calculator on every shopping trip. That is because just a click of your mouse or a swipe of your tablet can reel in huge savings on credit card bills, home goods, fashion, electricity, and fun-filled family activities!

We have done the work of trawling the Internet to find you seven of the best money-saving websites around. We’ll help you get freebies, codes, downloadable coupons and more, so that you can do more with your budget every week. Here is our point-and-click guide to savings…

HotFreeStuff.co.uk

This site gets you access to lots of free samples you can really use, from lotions to perfumes. Save money using this site on lots of household goods and get a chance to try new products for free as soon as they are available.

Gumtree

At this so-called ‘classified community’ you can snap up lots of great deals on pets to property. There are many listings for rentals and jobs throughout the UK and Ireland. You will enjoy the deals, but you can also get free items via the freebies section. Just scroll beyond the ads and sponsor links to find many free listings for household items and furniture. At the time of writing there were listings on the London site for free sofas and mattresses, a working Hotpoint fridge-freezer, and free haircuts. Just a word of caution – we suggest for any classified site that you take someone along with you to collect any items, and be careful about giving away too much personal info when responding to ads.

HotUKDeals

This site has been around for well over a decade and is the most reputable place for people to share information on the freebies and discounts they have picked up on their website travels. It is free to register and features include ‘Top 10 Hottest Offers’, requests for offers, and fun, free competitions to enter.

My Voucher Codes

Get over 2000 discount codes at Britain’s biggest voucher website. Tabs include top listings as well as categories, together with the ability to print out vouchers.

Groupon

Never underestimate the power of Groupon! Many times it can seem like a venue for free or cut-price beauty treatments. There are, however, great deals on family attractions, meals and holiday getaways as well.

Moneysaving Expert (MSE)

This massive site set up by financial journalist Martin Lewis has saved the UK millions. It is clearly written, easy to understand, and has lots of information on getting deals on everything from home and car insurance to broadband and mortgages.

Travel Supermarket

This is the best site to find travel deals and compare flights and hotel offers in one easy-to-navigate resource.

Many thanks to Hot Free Stuff for sharing their advice and information. If you have any comments or questions – or other tips and resources for saving money – please do share them below as usual.

Disclosure: this is a sponsored post.

If you enjoyed this post, please link to it on your own blog or social media: