A quickie today to let you know that until the end of August 2023, you can get a massive 25 percent off the cost of a new English Heritage membership if you pay by annual direct debit. This applies to all types of membership, including Over-65s (which is already discounted).

English Heritage looks after nearly 400 historic sites and buildings across England, including Stonehenge, Hadrian’s Wall, Dover Castle, the Iron Bridge in Telford (see cover photo), and more. Members get free admission to all properties. Other benefits include free parking in car parks owned by English Heritage, free or reduced-price admission to hundreds of special events, and free entry to properties for up to six children per member. You also receive a free members’ handbook and a magazine (published three times a year).

A further attraction of joining English Heritage is that they have reciprocal arrangements with Scottish Heritage and CADW in Wales. Members therefore get reduced or free admission to most properties owned by these organizations as well.

You can get current membership prices from the English Heritage website. Family, Joint, Individual and Lifetime memberships are available. To claim the current special offer discount, you have to enter the code IMAGINE50 on the online form when applying.

In my case I qualified for Over-65 membership. This would normally cost £63 a year, but with my 25% discount it was reduced to £47.25. Of course, the discount price is for one year only, but you can always cancel the direct debit before it’s due to renew if you wish.

There are various English Heritage sites near where I live. Later this week I am planning to visit Boscobel House in Staffordshire, which is only around 30 minutes’ drive from where I live. Although I have only just joined, I received a temporary membership card by email prior to my full membership pack arriving in the post. So I will be saving at least £11 straight away!

I duly visited Boscobel House on Thursday 18 August. My temporary membership was accepted without quibble, so I saved £11 on admission and also £3 on parking. I also discovered another benefit of English Heritage membership which I couldn’t see mentioned on the website. Once you have been a member for a year or more, you qualify for a 10% discount on any purchases in their shops or tea rooms.

English Heritage obviously has some similarities with the National Trust, but it’s an entirely separate organization and only operates in England (though see my comments above about reciprocal arrangements with organizations in Wales and Scotland).

I know from messages on social media that some people have been deterred from joining or rejoining the National Trust due to their controversial stance on some current issues (see this article, for example). So far anyway, English Heritage seem to have stuck to their core remit of looking after heritage sites and properties and avoided divisive political messaging. For those who have resigned from the National Trust or no longer wish to join, English Heritage may therefore offer an attractive alternative. Of course, there is nothing to stop you joining both if you wish!

As always, if you have any questions or comments about this post, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

Today I’m sharing a sideline money-making opportunity that – if you’re in a position to do it – can bring in a steady income for very little effort.

The shortage of parking spaces in many towns and cities has created an opportunity for anyone who has a driveway (or garage) they aren’t using all the time.

One of the best-known operators in this field is JustPark. Through their website and mobile app, they put drivers in touch with home-owners and businesses who have parking spaces (and/or EV charging spaces) available near their destination. They say they help over 10 million drivers a year find parking spaces at over 45,000 UK locations.

Listing your space is free and you can set your own price based on how long the driver wishes to stay. JustPark will suggest an appropriate price based on your location and the facilities you are offering, but you aren’t obliged to accept this.

JustPark charges space-owners a 3% fee on one-off bookings (so if you charge £10 they will take 30p, meaning you receive £9.70). For longer term or rolling bookings over two months, they charge space-owners a higher fee of 20% for the first month, with the fee reverting to the standard 3% after that.

JustPark also make money from drivers, adding up to 25% of the space-owner’s asking price to the fee charged. They say, however, that charges to drivers are still typically 30% lower than ad hoc street parking (if you can find it), which makes the service attractive to motorists as well.

One big attraction of JustPark is that they handle all the admin on your behalf. All payments are made via the website, and space-owners can withdraw earnings via PayPal or direct to their bank account. JustPark also ensure you still get paid even if the booker doesn’t turn up.

JustPark say that the money you earn from renting out your parking space is included in the property trading income allowance introduced by the government in April 2017 – so you can make up to £1,000 per year completely tax-free (and no need to declare it to the taxman).

All drivers using the service have to register on the site, so you know exactly who will be using your space on any given day. There is also a rating system so you can see any comments other users of the service have made about them. Space-owners are also rated by drivers, incidentally.

You can offer spaces by the day, week or month, and set any restrictions you wish on when your space is available. Anyone is welcome to advertise spaces on JustPark, but the locations in most demand are those near airports, stations and stadiums, and in major cities. According to one recent article in the Daily Mail, people in such areas are making more than £4,000 a year doing this. Even if that doesn’t apply to you, though, you can still earn from a few hundred pounds a year to £1000 or more by this means.

Obviously the pandemic and working from home reduced demand for parking spaces. But with life returning to normal now, demand for parking spaces is steadily increasing again.

Of course, if you don’t have a suitable space to offer, you won’t be able to benefit from this opportunity. You could still use JustPark to save money on your own parking costs, though. Either way, the service is well worth checking out 🙂

Another option for cheaper parking is Your Parking Space. Over 60s can get an exclusive 10% discount on this service through my friends at Over 60s Discounts.

Disclosure: As well as being a registered user of JustParkI am an affiliate for them and will therefore receive a small commission if you click through any of my links and sign up. This will not affect the money you earn through the site and/or any savings you make if you use them to find parking spaces.

Cover image by courtesy of BingAI.

This is a fully revised and updated version of my original article on this subject.

If you enjoyed this post, please link to it on your own blog or social media:

I’ll start as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

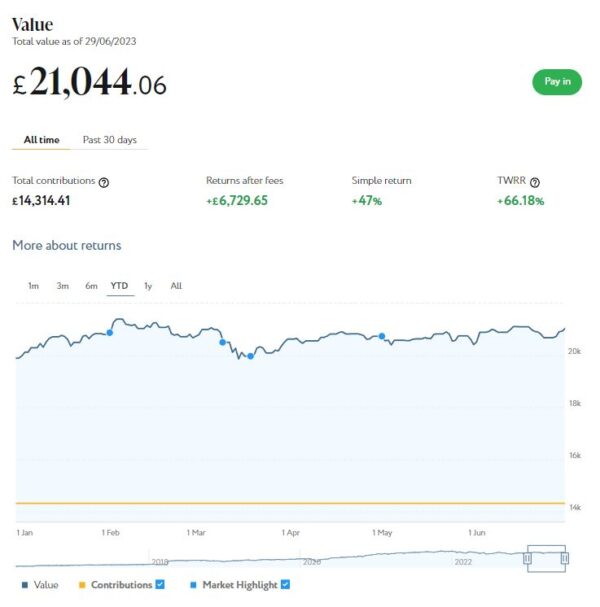

As the screenshot below for the year to date shows, my main Nutmeg portfolio is currently valued at £21,044. Last month it stood at £20,419 so that is a rise of £625.

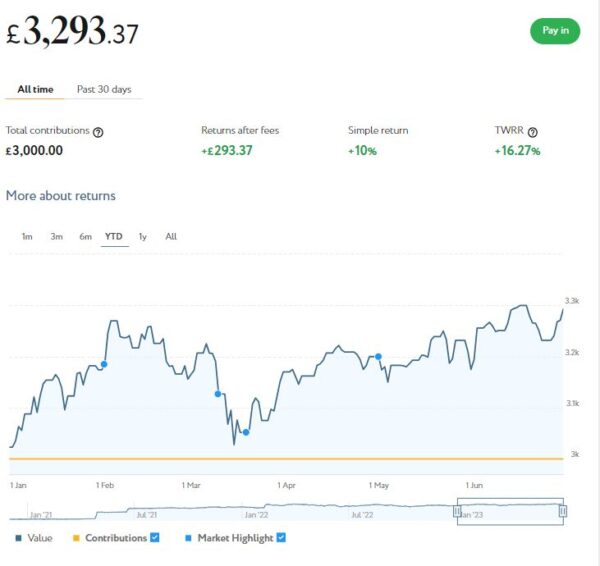

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £3,293 compared with £3,175 a month ago, an increase of £118. Here is a screen capture showing performance since the start of this year.

This has clearly been a better month for both my Nutmeg pots. Their total value has risen by £743 or 3.15% month on month. Since the start of 2023 the net value of my Nutmeg investments has grown by £1,417 or 6.18%.

Of course, all investing is (or should be) a long-term endeavour. Over a period of years stock market investments such as those used by Nutmeg typically produce better returns than cash accounts, often by substantial margins. But there are never any guarantees, and in in the short to medium term at least, losses are always possible.

Also, as you may know, both my Nutmeg pots have quite high risk levels (9/10 main, 5/5 Smart Alpha). If you haven’t yet seen it, you might like to check out my blog post in which I looked at the performance over time of Nutmeg fully managed portfolios at every risk level from 1 to 10 . I was pretty amazed by the difference risk level makes, with higher-risk ports over almost any period of three or more years in the last ten generating significantly better overall returns. If you are investing for the long term (and you almost certainly should be) choosing a hyper-cautious low-risk level might not therefore be the smartest strategy. The one exception is if you plan to withdraw your money soon and don’t want to risk losing too much if there is a sudden downturn.

You can read my full Nutmeg review here (including a special offer at the end for PAS readers). If you are looking for a home for your annual ISA allowance, based on my overall experience over the last seven years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs) and Junior ISAs as well.

Moving on, my Assetz Exchange investments continue to generate steady returns. Regular readers will know that this is a P2P property investment platform focusing on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my AE portfolio has generated a respectable £124.53 in revenue from rental income. As I said in last month’s update, capital growth has slowed, though, in line with UK property values generally.

At the time of writing, 12 of ‘my’ properties are showing gains, 2 are breaking even, and the remaining 12 are showing losses. My portfolio is currently showing a net decrease in value of £15.53, meaning that overall (rental income minus capital value decrease) I am up by £109. That’s still a decent return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Assetz Exchange most projects are socially beneficial as well.

Obviously the fall in capital value of my AE investments is slightly disappointing. But it’s important to bear in mind that unless and until I choose to sell the investments in question, it is largely theoretical. The rental income, on the other hand, is real money (which in my case I have chosen to reinvest in other AE projects to further diversify my portfolio).

I also spoke to the CEO of Assetz Exchange, Peter Read, recently. He made the point that capital values on the platform simply reflect the latest price at which shares in the property concerned have changed hands on their exchange. They do not represent objective or independent valuations of the properties. If you are investing long term with AE, the annual yield from rentals is really a much more important consideration.

Peter also made the point that the current high inflation rate has actually been beneficial for Assetz Exchange investors. That is because properties on the platform generally have an annual review when rentals are increased in line with inflation. That means from the end of the financial year in April, rentals have increased in most cases by around 10%. Assetz Exchange recently published a blog post about this which is worth a read.

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of AE as far as i am concerned. You can actually invest from as little as 80p per property if you really want to proceed cautiously.

Another property platform I have investments with is Kuflink. They continue to do well, with new projects launching every week. I currently have around £2,500 invested with them in 17 different projects. To date I have never lost any money with Kuflink, though some loan terms have been extended once or twice. On the plus side, when this happens additional interest is paid for the period in question.

My loans with Kuflink pay annual interest rates of 6 to 7.5 percent. These days I invest no more than £200 per loan (and often less). That is not because of any issues with Kuflink but more to do with losses of larger amounts on other P2P property platforms in the past. My days of putting four-figure sums into any single property investment are behind me now! Nowadays I mainly opt to reinvest the monthly repayments I receive from Kuflink, which has the effect of boosting the percentage rate of return on the projects in question

Obviously a possible drawback with Kuflink and similar platforms is that your money is tied up in bricks and mortar, so not as easily accessible as cash savings or even (to some extent) shares. They do, however, have a secondary market on which you can offer any loan part for sale (as long as the loan in question is performing and not in arrears). Clearly that does depend on someone else wanting to buy it, but my experience has been that any loan parts offered are typically snapped up very quickly. So if an urgent need arises, withdrawing your money (or part of it) is unlikely to be an issue.

You can read my full Kuflink review here. They offer a variety of investment options, including a tax-free IFISA paying up to 7% interest per year with built-in automatic diversification. Alternatively you can build your own IFISA, with most loans on the platform being IFISA-eligible.

Until 31 July 2023 Kuflink are offering enhanced promotional rates of up to 9.73% (gross annual interest equivalent rate) for their Auto-Invest products (IFISA-eligible). There is limited availability for this offer and it may be withdrawn any time before 31 July 2023 if the limit is reached. For more information, click here [affiliate link].

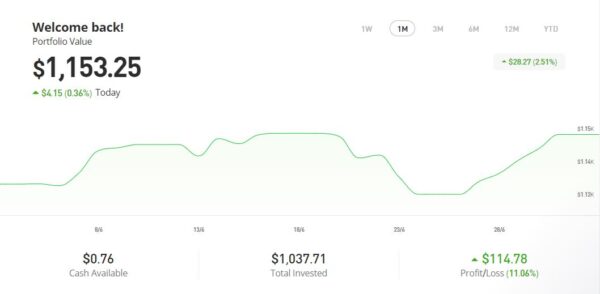

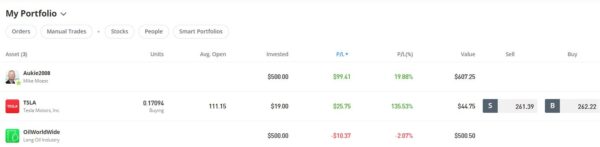

Last year I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios, Oil Worldwide. I also invested a small amount I had left over in Tesla shares.

As you can see from the screen capture below, my original investment of $1,022.26 is today worth $1,153.25, an overall increase of $130.99 or 12.81%. in these turbulent times I am very happy with that.

Since last month the price of my Tesla shares has risen substantially and my copy trading portfolio with Aukie2008 has also done well (though less spectacularly). My most recent investment in Oil Worldwide has risen a bit this month but it’s still slightly down on when I invested. The Oil Worldwide portfolio has just been rebalanced by eToro, so I am hoping for better things in the months ahead

eToro also recently introduced the eToro Money app. This allows you to deposit money to your eToro account without paying any currency conversion fees, saving you up to £5 for every £1,000 you deposit. You can also use the app to withdraw funds from your eToro account instantly to your bank account. I tried this myself recently and was impressed with how quickly and seamlessly it worked. You can read my blog post about eToro Money here.

I had two more articles published in June on the excellent Mouthy Money website. The first was 10 Great Ways to Save Money on Amazon. Amazon is Britain’s – and the world’s – favourite online store. Prices on Amazon are generally competitive, but over the years I’ve discovered a variety of ways to ensure you get the best value for money from them. So in this article I set out my top ten tips for saving money on Amazon

My other article was Do You Need a Personal Financial Adviser? In this article I discuss the different types of financial adviser and what they do. I also revealed why – despite being a money blogger and considering myself reasonably financially savvy – I have a personal financial adviser myself.

As I’ve said before, Mouthy Money is a great resource for anyone interested in money-making and money-saving I always look forward to reading the articles by my fellow contributors. Shoestring Jane is a particular favourite and I enjoyed reading her recent article concerning how you can Save Money by Reducing Food Waste.

I also published several new posts on Pounds and Sense in June. One of these was My Short Break in Bath. Bath is, of course, a historic city on the River Avon, about 12 miles from Bristol. I went there for three days in June, the first time I had been for over 30 years. In my post I discuss the self-catering apartment where I stayed and reveal some of the things I did and saw. I also share a few top tips for visitors to Bath. The cover image shows the famous Pulteney Bridge, one of Bath’s best-known landmarks.

I also published a post based on a survey of Britons’ investing habits. This addressed questions such as what are the main barriers stopping people investing and where do people get their investment advice from. I thought the results were quite eye-opening. Take a look if you haven’t already.

Finally, I wanted to highlight that the free share offers described in last month’s update are both still open if you haven’t done them yet. The opportunity to Get a Free Share Worth up to £100 with Trading 212 was reopened after closing briefly. It is now on offer till 27 July 2023.

The opportunity to Get a Free ETF Share Worth up to £200 with Wealthyhood is also still open but the terms have changed slightly. To remind you, Wealthyhood is a DIY wealth-building app aimed especially at people who are new to stock market investing. As from 1 June 2023 they changed their fee structure to make it (even) more attractive to small investors. They have now increased the minimum investment to qualify for the free share offer from £20 to £50 – but on the plus side, they guarantee that your free ETF share will be worth at least £10.

That’s all for today. I hope you’re enjoying the summer months and taking the opportunity to get out and about in our beautiful country (or further afield).

As always, if you have any comments or queries, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media:

Today I am sharing some interesting data from my friends at HSBC regarding British people’s investing habits.

This information comes from a survey conducted last year by Sticky and Censuswide on behalf of HSBC. The survey was conducted online, with a total sample size of 2018 adults. It reveals how and why people in the UK are investing, and (very importantly) why many are not.

The research revealed that nearly two-thirds of people had some form of savings (64%), with more than one in three (36%) saying they had investments. Nearly half (47%) believed investing was a better way of achieving future financial goals in the current financial climate.

More than half of people (53%) who said they would like to invest but haven’t yet said they didn’t know how to begin. Just over 1 in 3 Brits are currently investing, so almost two-thirds are not.

Saving vs Investing

Somewhat reassuringly, two-thirds of people in the survey said they currently have savings (64%) and just under three-quarters (72%) said they have enough money put away to cover three months’ living expenses despite increases in the cost of living.

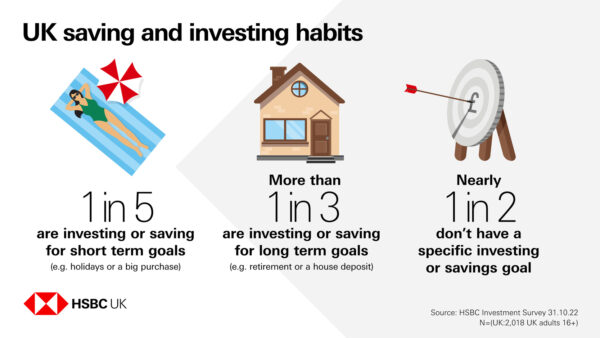

The main reasons people have for saving and investing are summed up in the infographic below…

As you can see, nearly half of people in the HSBC survey (46%) didn’t have a particular goal for their saving or investing – but those who did have a target were much more likely to be saving for something long-term (37%) like a house deposit or their retirement than short-term goals like holidays or other large purchases (20%).

In general, of course, saving for short-term goals is best done through cash savings accounts – but for long-term goals, typically five years or more ahead, investing is likely to produce better overall returns.

Investment Choices

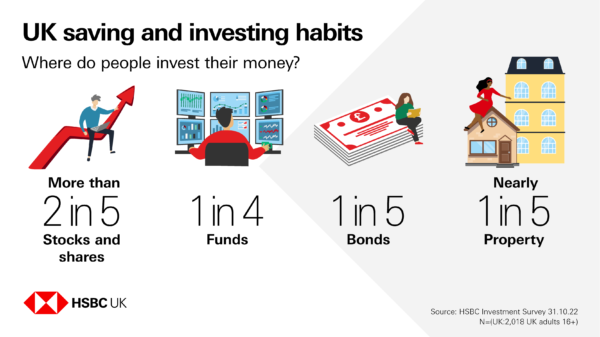

The infographic below shows the main ways people in the UK are currently investing.

As you can see, the most popular investment is stocks and shares (44%), followed by funds (25%), bonds (20%) and property (19%).

When people were asked how they’d decided to invest, the most common reason given for choosing stocks and shares was the expectation of good returns (34%). Bonds were most often seen as a “safe” investment (38%).

Meanwhile, the reason for choosing funds was more equally balanced between being seen as offering good returns (34%) and being “safe” (30%), with the same being true of property (39% good return, 35% “safe”).

Barriers to Investing

When people were asked why they hadn’t chosen to invest, the most common answer (45%) was thinking they didn’t have enough money to do so. But nearly a quarter (23%) said they didn’t know enough about how to invest, ahead of the one in five (21%) who said they would worry about losing all their money.

For those who said they were scared of losing money, the main driver of those worries was the fact that investments can go down as well as up (40%). But that was followed by concerns about the need for access to their cash – with 37% saying they might need their money at short notice, and another 30% stating that their financial situation meant they couldn’t lock away money for a long time.

Those who chose to invest in jewellery and alternatives (wine, art, whisky, etc) were the most likely to say they had done so because they had expertise in that area (25%).

Investment Knowledge

When it comes to detailed financial knowledge, more than one in three (34%) said they didn’t feel they had enough information about investing. And those who wanted more help with their financial planning were most likely to need information about where to invest (25%), followed by support on types of investments (22%), the cost of investing (20%), and which investments are more or less risky (20%).

People who said they already received some information on investing were most likely to get that from their family (17%), their bank (16%), friends (15%) and social media (15%) – all ahead of financial newspapers (13%) and financial blogs (11%).

Nearly a quarter (24%) said they’d like to receive more information about investing from their bank as the primary source of information, ahead of getting help from investors (16%), social media (13%), family (11%) and financial blogs (11%) or financial newspapers (11%).

My Thoughts

Many thanks to my friends from HSBC for allowing me to share and discuss their data and graphics.

I’m not surprised that many people are wary of investing, as the subject isn’t generally taught in schools and the huge number and variety of potential investments can be bewildering.

What I find a little more surprising (and concerning) is that many more people have investments in the form of stocks and shares (46%) rather than funds (25%). I suspect this may partly be to do with people having a few shares they acquired from the big privatizations of the past such as BT and British Gas. There may also be a number who have shares through employee share schemes. Nonetheless – as I said in this recent guest post for the popular Money Talk blog – as an investment individual shares are a lot more volatile and risky. If you are new to investing, I highly recommend starting off with a collective investment such as a tracker fund or robo-adviser platform (see below). This will give you much broader diversification, which helps mitigate the risks involved.

As I’ve said before, if you suddenly find yourself in possession of a large lump sum (perhaps through an inheritance) there is a strong case for seeking advice from a trained and experienced independent financial adviser. You might like to check out my blog post on why, despite being a money blogger and considering myself reasonably financially savvy, I still have an IFA myself.

If you just want to get started in investing, there are various low-cost and relatively low-risk options you could consider. Regular readers will know that I am a fan of the robo-adviser platform Nutmeg, with whom I have been investing since 2016. Even with the recent turmoil in the markets caused by the pandemic etc., I have made an overall return of 37 percent from my investments with them. You can read my in-depth review of Nutmeg here if you wish.

Another possibility might be the wealth-building platform Wealthyhood, which is aimed especially at novice investors. You can get started on this with as little as £20 – and right now they are offering a free ETF share worth up to £200 to new investors, which should get you off to a good start! You can see my blog post about Wealthyhood and their special offer here.

Of course, all investing carries a risk of loss, in the short- to medium-term especially. You should therefore always do your own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed.

As always, if you have any comments or questions about this post, please do leave them below.

Disclaimer: I am not a professional financial adviser and nothing in this post should be construed as personal financial advice.

If you enjoyed this post, please link to it on your own blog or social media:

Regular readers of PAS will know I have a particular interest in P2P/crowdlending investment. Such platforms offer the opportunity to invest in loans to businesses or individuals and profit from the interest charged to borrowers.

With savings account interest rates still quite low, many investors are looking for better returns on their savings and investments. If that applies to you, European crowdlending platform Nibble is worth a look.

What is Nibble?

Nibble is a crowdlending platform launched in 2020 by IT Smart Finance, a company with over five years’ experience developing innovative products in financial technology. They offer a range of investment products which you can read about on the Nibble website. Today I am focusing on their latest offering, called the Legal Strategy.

What is the Legal Strategy?

The Legal Strategy offers the highest potential return of all the investment options on Nibble. The loans in question are in default and facing legal action (hence the name, of course).

For investment portfolios offered through the Nibble Legal Strategy, collection and litigation management are performed by Boostr. This is a company that buys overdue loans from banks and MFOs (Multiple Facility Organizations) at auctions at a typical discount of 85%, and automates the process of extra-judicial and legal recovery.

Nibble say that thanks to the deep experience and technologies developed by Boostr, it is possible to achieve a high percentage of capital return. The company draws on more than five years of successful experience in the area of debt recovery.

The Legal Strategy terms for investors, copied from the Nibble website, are shown below.

As you can see, the Legal Strategy comes with a deposit back guarantee. This is a guarantee to return the full investment amount at the end of the investment period and a minimum yield of 8% per year. The actual yield paid will depend on how successful recovery efforts prove, so you may end up with an annual return of anywhere between 8% and 14.5%. As you will probably know, this is above the average in the collective financing industry.

The minimum investment in Nibble’s Legal Strategy is €10 (about £8.70 at current exchange rates) and the maximum is €10,000. The platform has an auto-investment tool, allowing trading to be fast and straightforward. You aren’t required to choose individual loan portions, as this is all handled by the company. You simply choose your investment strategy based on the timescale over which you wish to invest and the level of risk you are comfortable with.

What Are the Risks?

No investment is without risk, but Nibble have gone to some lengths to keep this as low as possible. You can read a detailed article on this page of the Nibble website (warning: it is quite long!).

For investors in the new Legal Strategy, your money is invested in a portfolio comprising a large number of loans. The risk is therefore controlled and managed, as if any loans prove irrecoverable they will normally be offset by others that are successfully recovered (with interest and penalties).

As stated above, the risk is shared between the investor and the platform in the form of a variable interest rate. The rate paid is calculated automatically by Nibble every 90 days based on how the loan portfolio in question is performing. So every 90 days investors receive interest of between 8% (the guaranteed minimum) and 14.5% (the maximum). The actual rates paid can therefore vary from one quarter to another. Nibble say that average payouts currently are around 12.5% (this corresponds with my own experiences to date as a Legal Strategy investor).

If, for example, you invested €1000 in the Legal Strategy over 12 months, you could expect to receive anywhere between €80 and €145 in interest over the 12 month period, along with the return of your initial capital.

This is a fixed term investment, so it may be best to avoid if you think you might need the money back urgently before the end date. However, Nibble do say that if you change your mind, you can withdraw money from your portfolio ahead of schedule. They say they will find a new investor for your portfolio for a small commission fee.

The other risk, obviously, is that the platform itself will go bust. For various reasons set out on the Nibble website this appears unlikely, but of course it’s not impossible. If that were to happen, you would not be covered by the Financial Services Compensation Scheme (FSCS) which covers deposits in registered UK savings institutions up to £85,000. Nibble say that in the worst case scenario ‘a management company will be assigned to help the investor to recover funds in accordance with the rights of claim against the borrower. In addition, there is always a reserve fund which serves as an additional “safety airbag” for the investor.’

Finally, as loans are currently all in euro, UK investors will of course have to contend with exchange rate fluctuations. These could work for you or against you.

How Do You Get Started?

If you wish to invest via Nibble, the first thing you will need to do is set up an account via the Nibble website.

As Nibble is a European operation, you will need to invest in euro and your returns will be paid in this currency. That obviously adds a layer of complication for UK residents, but there are various ways around this. If you have a UK bank account you will normally be able to make (and receive) payments in euro, but may be charged a NSTF (Non-Sterling Transaction Fee).

You could use your own bank to fund your account initially, but if you become a regular investor with Nibble you might want to use a service/account that charges lower fees. You could use a money transfer service such as Paysera or Wise (formally TransferWise). These will enable you to transfer funds between Nibble and your own bank account with (potentially) lower charges and a more favourable exchange rate.

Another option would be to open a euro account with a provider such as Starling. This will allow you to receive and make payments in both sterling and euro, again at a lower overall cost.

My Experience

I wanted to try out Nibble myself,so I set up an account with them a while ago. The process was quick and straightforward. You just click on Create Account at the top of the Nibble homepage and follow the online instructions.

You are required to complete a short verification process before opening your account. This involves taking a photo of your passport, driving licence or some other form of ID, along with a selfie. You may use your mobile phone camera for this. It all worked smoothly and seamlessly in my case, and within a couple of minutes my application had been verified and approved.

After that, it is just a matter of making your initial deposit and deciding which of the strategies you want to use. Initially I chose their Classic Strategy as a low-risk test and everything went as promised. More recently I invested €100 in the Legal Strategy. This has also been running smoothly, with interest payments credited quarterly as promised.

Closing Thoughts

If you are looking for a more exciting home for some of your cash that allows you to take advantage of the higher interest rates on offer in continental Europe, Nibble is worth checking out.

The new Legal Strategy offers the highest rate of return of all their strategies. Of course, with higher returns typically come higher risks, and you do need to be comfortable with this. It is also important to note that with the Legal Strategy rates paid may vary over the period of your investment (though with an 8% guaranteed minimum).

The website’s ease of use is another attraction, as is the fact that Nibble doesn’t impose any fees or charges on investors. You do just need to bear in mind the need to switch between pounds and euro and the importance of minimizing the costs associated with this.

As a company based in Spain, NIbble doesn’t have too many UK reviews, but those that I have seen are generally positive. On the popular independent Trustpilot website, they have 11 reviews in total, six with 5 stars (‘Great’) and three with 4 stars (‘Very Good’). There are two 1-star reviews which reduce their average somewhat. These relate to difficulties withdrawing money. Nibble have replied to both and it appears that the problems arose due to the way the banks operate rather than being any fault of Nibble themselves. It also appears that the issues were satisfactorily resolved.

Obviously, nobody should put all their money into Nibble’s Legal Strategy, but it is worth considering within a diversified savings and investments portfolio. You should also bear in mind that your money won’t be protected by the Financial Services Compensation Scheme (FSCS), which protects deposits of up to £85,000 in most UK bank accounts. Of course, P2P/crowdlending platforms in the UK are not generally covered by the FSCS either.

I will continue to report on Pounds and Sense about how my Nibble investments fare.

New! Cashback Bonus. Until 31 July 2023 Nibble are offering a 2% cashback bonus for all new investments in their Legal Strategy. Visit their website for more info.

As always, if you have any comments or questions about this post, please do leave them below.

Disclaimer: I am not a qualified independent financial adviser and nothing in this post should be construed as personal financial advice. You should always do your own ‘due diligence’ before investing and seek professional advice if unsure how best to proceed. All investing carries a risk of loss. Note also that this review includes my affiliate (referral) links, so if you click through and end up investing with Nibble, I may receive a commission for introducing you. This will not affect the price you pay or the product/service you receive.

This is a sponsored post.

If you enjoyed this post, please link to it on your own blog or social media:

Today I have a guest post for you from my friends at Money Marvel about the effects of inflation on savings and loans.

With inflation currently over 10 percent and prices seemingly rising by the day, this is clearly a big concern for many people right now. It’s not always such a bad thing if you’re paying off debts, though. And if you’re saving for the longer term, higher rates of inflation can actually provide an extra incentive to invest. Learn more in the article below…

If you’ve been following the news at all in the UK over the past year you’ll have no doubt heard about inflation – it has been almost impossible to avoid it in the press. But what actually is inflation? And, more importantly, what does it mean for your savings and loans? Read on for my thoughts.

What is Inflation?

Simply put, inflation is the economic force that drives prices to change over time. Everyone has an item from their childhood that always surprises them with how much more it costs now (for me it’s the Freddo! I remember them being 10p each, now they’re almost 40p). That’s a great example of inflation in action: the gradual increase of prices over time.

Over the last year, the impact has been even more dramatic. Inflation rates in the UK are now at the highest they’ve been for over 40 years, with the CPI measure of inflation now running above 10%.

It has never been more important to consider inflation when planning your savings or loans.

What Impact Does Inflation Have on Savings?

Unfortunately, inflation is not good news for savers. It means that the cash you’ve built up and set aside will be worth less when you eventually spend it than it was when you first saved it.

In part, that’s why you’ll receive interest as a return on your savings. Savings are a mechanism for you to lend your money to banks and financial institutions, and the interest you get is your compensation for doing so.

You can straightforwardly compare the interest rate on your savings and the current UK inflation rate to see if your money is overall worth less or more over time. For example, if the headline inflation rate is 10% and you’re being offered 5% interest then you know you’re effectively losing 5% in value each year.

Sadly in the current economic reality, it’s almost impossible to find a savings interest rate higher than inflation, so most savers will have to accept the reality that they’ll be losing value year-on-year.

What Can Savers Do About It?

For those that need the security or guaranteed access that comes with a savings account, the unfortunate answer is that there isn’t much you can do about inflation. It’s important to be aware of it so that you can plan your future considering its impact, but sadly there’s nothing you can do to avoid it.

If your time horizons are a bit longer and you’re comfortable with a level of risk, then there are a variety of other investments that promise returns higher than the rate of inflation (for example, by investing in stocks and shares, or physical assets like gold). By their nature, they do come with a significantly higher level of risk and volatility than a savings account does. They may be suitable if you’re planning to save for a long time period (5 years+) and are willing to ride some ups and downs in the meantime.

Inflation alone shouldn’t lead you to take on risks with your savings that you otherwise wouldn’t, but it should help you understand the real returns that different savings products might offer. And if you’re determined to outpace inflation in the long run then savings accounts are likely not to be the best place for your money.

What About Debt?

High levels of inflation are much better news if you’re already holding significant debt. The force of inflation will gradually erode the value of the debt you have outstanding so that you end up effectively owing less money to the bank (or other lending institution). The £ value amount will stay the same, but the value of the money you use to pay off the debt will decline.

You’ll be paying interest to the bank to compensate them for their loss of value, but if you manage to get an interest rate lower than the inflation rate then you’ll be doing well overall. This is the case for many UK residents who took out long-term loans before the recent surge of inflation.

Inflation alone is not a reason to get yourself in debt (the banks will almost certainly have a better projection of future inflation rates than you do!), but it’s one to keep an eye on when thinking about the debt you already have.

Planning for the Future

Inflation is critically important when you’re planning for your financial future. This is most obviously the case when thinking about retirement. If you have more than a few years of working life remaining then money will almost certainly be worth less when you do come to retire.

When looking at retirement planners or pension benefits make sure you keep track of whether the numbers have been adjusted for inflation or not. If they haven’t, then keep that in mind and adjust your plans accordingly.

Many thanks to my friends at Money Marvel for an interesting and eye-opening article. Do check out the Money Marvel website for a wide range of personal finance information, advice and resources.

As always, if you have any comments or questions about this article, or the effects of inflation more generally, please leave them below.

This is a sponsored guest post.

Disclaimer: I am not a qualified financial adviser and nothing in this post should be construed as personal financial advice. You should always do your own ‘due diligence’ before investing and seek advice from a qualified professional if in any doubt how best to proceed. All investing carries a risk of loss.

If you enjoyed this post, please link to it on your own blog or social media:

Today I thought I’d set out my views on where best to seek advice on tax-related matters. From feedback received I know that this is a topic that concerns a lot of people, especially the growing number who are turning to ‘side hustles’ to help make ends meet.

I’ve been self-employed for around 30 years now and have quite strong opinions on this subject, especially as I see a lot of dodgy advice about tax being bandied about. So let me start by setting out the two places that in my view you shouldn’t generally turn for tax advice (and you definitely shouldn’t rely on).

1. Social Media

I am thinking especially here about Facebook groups and online forums (or messageboards). These are popular places for people with a shared interest to ask (and answer) questions about subjects that concern them.

I belong to various groups and forums aimed at UK writers and bloggers, and get a lot of useful information and support from them. However, I regularly see people asking questions on them about tax matters, and I’m not at all convinced that this is useful or sensible.

What typically happens in these cases is that other members weigh in with their advice and opinions. Although these are offered with the best of intentions, they are often contradictory and sometimes downright wrong. I imagine that in many cases the original questioner ends up more confused than when they started. Or – perhaps worse – they proceed on the basis of dubious advice which could result in them facing fines and penalties or, conversely, paying more tax than they need to.

Most people in these groups are not trained accountants, but that doesn’t stop some of them airily dishing out tax advice anyway. Replies beginning with phrases such as ‘I’ve always understood’ or ‘I’m pretty sure that’ or ‘As far as I know’ or ‘I could be wrong, but’ should always be regarded with considerable scepticism.

Groups also often have ‘gurus’ who claim (and may or may not have) a deeper knowledge of these matters. Their pronouncements may be treated as akin to holy writ by other members. Again, be cautious about blindly following advice from these individuals, even if they apparently have qualifications and/or professional experience. I have seen advice from such people that is definitely wrong or at least highly questionable, but nobody in the group dares challenge them about it. This happens in other fields as well as tax, incidentally.

I would also extend my caution about getting advice from social media to blogs (yes, including mine). I have seen some good advice on blogs, but also plenty I would regard as debatable to say the least. Definitely don’t take anything you read about tax on a blog as gospel, even if the person in question does have thousands of followers!

2. HMRC

Yes, you read that correctly. In my view, HMRC should seldom be your first port of call for tax advice.

There are various reasons for this. One is that, when you phone HMRC, the person you will generally speak to is a call handler. They will (or should) obviously have a reasonable working knowledge of how the tax system works, but they are definitely not expert in every aspect. If you ask them complex questions about (say) what expenses you can and can’t claim against income or what counts as a capital gain as opposed to taxable income, you are likely to get different and contradictory advice according to whom you speak to. Or they may simply tell you that advising you about this is outside their remit.

In addition, it’s important to bear in mind that HMRC are not in business for your benefit. Their job is to maximize tax revenues for the government. They can’t and won’t advise you on how to legally organise your affairs in such a way as to minimize your tax liabilities (which every taxpayer is perfectly entitled to do).

That being said, there are certain occasions when you can and should contact HMRC. This is when you have specific questions about your taxes, e.g. whether a certain tax payment has been received, what is your tax code, when is your next tax payment due, and so on. The call handlers should have this information easily accessible on their computers and will be happy to pass it on to you.

So Where Should You Turn for Tax Advice?

You may have guessed already, but if not I won’t keep you in suspense. The answer is a professional accountant.

Accountants are trained and experienced in all aspects of the tax system. They have both theoretical and practical knowledge of how the system works and how the (complex) rules are typically interpreted by HMRC. And they have to keep themselves up to date with the endless legal and procedural changes.

Also, unlike HMRC, an accountant is four-square on your side. They will advise you on the best way to organize your affairs to minimize your tax liability. They will answer any questions you may have, e.g. what records you need to keep. When the time comes, they will (if you want them to) compile your accounts and submit the relevant figures to HMRC in your tax return. And if any queries or problems arise, they will act on your behalf to try to resolve them.

A further benefit of having your accounts prepared by an accountant is that HMRC will know that a finance professional – someone who speaks their language – has compiled them. Other things being equal, this is likely to mean they will be more inclined to accept the figures and not dispute them.

Even if you prefer to prepare your own accounts (perhaps using accounting software online), having an accountant check your work (and maybe submit it on your behalf) can be a shrewd policy and reduce the risk of HMRC querying your tax return.

Even if you aren’t running any sort of business, there may still be a case for getting an accountant to help with your taxes. Many older people, for example, have multiple streams of income, from stocks and shares to ISA accounts, property rentals to pensions. Some of this income may be taxable and some not, and varying tax rates and tax-free allowances may apply. Most accountants are more than happy to provide a service to people in this situation as well.

There is, of course, one drawback to engaging an accountant, and that is the cost. This will probably amount to a few hundred pounds a year (maybe more in some cases). Not to pay this, however, is in my view a false economy. A good accountant is likely to save you at least as much in unnecessary tax as they cost you. And the reassurance (and relief) of having a finance professional available at the end of a phone when any queries with taxation arise is impossible to put a price on (but extremely valuable).

After thirty years of self-employment (and being semi-retired now), I still wouldn’t dream of not having an accountant. And since I’m mentioning this, a shout-out here for my own accountant, Rob Ollerenshaw, who has looked after my tax affairs for over twenty years. I recommend him without reservation to anyone in the North Birmingham/South Staffordshire area, or indeed further afield (he tells me he has clients as far away as Cornwall!).

So those are my thoughts about where best to get tax advice, but what do YOU think? Please post any comments or questions below as usual.

This is a revised and updated version of my original post.

If you enjoyed this post, please link to it on your own blog or social media:

I have mentioned Mouthy Money a few times on Pounds and Sense. Some of you will be aware I’m a regular contributor to this UK personal finance website.

But while I’ve talked about it in passing a few times, I have never really discussed Mouthy Money properly on PAS. So I thought I should rectify that today!

What Is Mouthy Money?

Mouthy Money is a website dedicated to helping people understand financial matters and make the most of their money. It is run by a small, dedicated team from an office in London. Their efforts are supplemented by a team of freelance writers, researchers and bloggers, including myself.

Every week new articles are added to the website. They are in four main categories, as follows:

Earning covers boosting your income, e.g. by starting a side hustle. Saving is all about reducing your outgoings, while Spending is about getting the best value for your money, e.g. on your weekly groceries shop. Your Questions answers specific questions sent in by readers, e.g. What happens if I can’t pay my tax bill?

The main menu runs across the top of the page. You can scroll down to see the latest articles in the order in which they were added. Alternatively, you can click on any of the four category titles to see the latest articles in the category concerned.

If you scroll further down the Mouthy Money homepage, you will see brief biographies of all the regular contributors, including myself. They include my fellow bloggers and writers Shoestring Jane, Finance Dee, Tolu Frimpong, Jordon Cox, Dana Raer, and so on. There are also bios of the site’s co-editors Paul Thomas and Edmund Greaves. Clicking on any of these will take you to a page listing all articles on Mouthy Money by the person in question.

Example Articles

Here are just a few of my favourite articles from Mouthy Money. I hope this will give you a flavour of the breadth and quality of the content:

I hope you enjoy reading these and many other articles on Mouthy Money and will add the site to your list of finance websites to visit regularly (along with Pounds and Sense, of course!). You can also follow Mouthy Money on Facebook and on Twitter.

As with Pounds and Sense, you can also subscribe to receive emails from Mouthy Money notifying you about the latest posts. The blue sign-up box can be found near the top of most articles on the site (not in the sidebar as on PAS).

One final thing is that if you run a personal finance blog yourself, Mouthy Money are always on the lookout for additional (paid) contributors. You can find out more and apply via this page of the MM website.

As always, if you have any comments or questions about this post, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

In just a few weeks (5th April 2023) it will be the end of the financial year. And that means if you want to make the most of your 2022/23 ISA allowance, you will need to take action soon.

As you may know, ISA stands for Individual Savings Account. ISAs are saving and investment products where you aren’t taxed on the interest you earn or any dividends you receive or capital gains you make. An ISA is basically a tax-free ‘wrapper’ that can be applied to a huge range of financial products.

With ISAs you don’t get any extra contribution from the government in the form of tax relief as you do with pensions. But – except in the case of the Lifetime ISA – you can withdraw your money at any time (subject to any rules about the term and notice period required) and you won’t be taxed on it.

Everyone has an annual ISA allowance, which is the maximum amount you can invest in ISAs in the year concerned. In the current financial year (2022/23) this is a generous £20,000.

There are four main ISA categories: Cash ISA, Stocks and Shares ISA, Innovative Finance ISA (IFISA) and Lifetime ISA (LISA). You can divide your £20,000 ISA allowance among these in any way you choose, though the most you can invest in a Lifetime ISA in a year is £4,000. Note also that you are only allowed to invest in one ISA in each category per year.

Let’s look at each ISA type in a bit more detail…

Cash ISA

Cash ISAs are like standard savings accounts, except the interest you receive doesn’t incur tax.

While interest rates for cash ISAs have been rising over the last few months, they are still pretty unexciting. According to the Money Saving Expert website, the best rate for an instant-access cash ISA is 2.91% with Shawbrook Bank. With inflation currently running at 10.1% that means even in the best-paying cash ISA your money will still be losing spending power when invested this way.

What’s more, the Personal Savings Allowance (PSA) means that basic-rate taxpayers can earn up to £1000 in savings interest without paying tax anyway (higher-rate taxpayers get a £500 tax-free allowance and additional-rate taxpayers earning over £150,000 a year nothing at all).

And as if that wasn’t enough, you can actually get higher rates of return from instant-access accounts that are NOT cash ISAs. For example, at the time of writing Money Saving Expert say the best rate on offer for an instant-access savings account is 3.11% from Cynergy Bank.

As a result of these things, cash ISAs have lost much of their appeal, unless perhaps you’re in the relatively small group of people who have to pay interest on their savings. But if interest rates continue to rise, they may of course become more attractive again. In addition, money invested in a cash ISA remains tax-free year after year, so if in years to come interest rates on cash ISAs rise, the benefit of having money in one will increase as well.

Nonetheless, I decided not to invest any of my ISA allowance in a cash ISA this year, as I have (in my view) better uses for my money. You might see this differently, of course 🙂

Stocks and Shares ISA

Stocks and shares ISAs are a good choice for many people saving long term. Over a longer period the stock market has outperformed bank savings accounts, often by a considerable margin. You do, though, have to expect some ups and downs in the value of your investments in the short to medium term.

You can opt for a standard stocks and shares ISA offered by a wide range of financial institutions and let them choose your investments for you. Alternatively you can use self-investment platforms such as Hargreaves Lansdown to choose your own investments from the wide range of shares and funds available.

IFISAs are on offer from a growing range of peer-to-peer (P2P) lending platforms. P2P platforms allow people to lend money to businesses and private individuals and get their money back with interest as the loans are repaid. If you invest in the form of an IFISA all the interest you receive from P2P lending is paid tax-free, otherwise it is taxed as income (though interest from P2P lending does qualify for the Personal Savings Allowance of up to £1,000 a year, mentioned above).

Peer-to-peer platforms generally offer more attractive interest rates than bank and building saving accounts (or cash ISAs) – from around 3% to 12% or more. They aren’t covered by the same guarantees as the banks and are therefore riskier, though. And if you need your money back urgently there may be delays and/or extra charges to pay.

Nonetheless, in the current climate of low-interest savings accounts and volatile stock markets, growing numbers of people are looking to IFISAs as a home for at least some of their savings.

One such option I have used myself is Kuflink, a P2P property investment platform. They offer an IFISA with automatic diversification over a 1, 3 or 5 year term (you can also choose your own self-select loans within an IFISA wrapper). Note that until 30 May 2023 Kuflink are offering an enhanced promotional rate of up to 9.73% a year (gross annual interest equivalent rate) for their Auto-Invest offers. You can read my full review of Kuflink here..

Another potential IFISA option (which I am using myself this year) is Assetz Exchange. They prioritize lower-risk property investments, which you can invest in through a self-select IFISA. You can read my full review of Assetz Exchange here.

Lifetime ISAs or LISAs are a new-ish initiative from the government to encourage younger people to save. They do have one big drawback for many readers of this blog – you have to be under the age of 40 (though over 18) to open one.

LISAs are designed for two specific purposes: buying your first home and saving for retirement. How they work is that you can pay in up to £4,000 a year (lump sums or regular contributions) and the government will top this up with another 25%. As long as you open your LISA before the age of 40 you will continue to receive the bonuses on your contributions until you reach 50.

So if you pay in the maximum £4,000 in a year, the government will top this up to £5,000. If you pay in the full £4,000 every year from the age of 18 to the upper limit of 50, you will therefore get a maximum possible bonus from the government of £32,000.

LISAs are therefore somewhat different from the other types of ISA mentioned above, but nonetheless any money you invest in one comes out of your annual ISA allowance (currently £20,000). So if you pay the maximum £4,000 into a LISA this year, that comes out of your £20,000 ISA allowance, leaving you with ‘just’ £16,000 to invest in other sorts of ISA.

Your money will grow without any tax deductions in a LISA, and you can also withdraw without having to pay tax. However, there are certain restrictions. In particular, you can only use the money in your LISA for one of two purposes: paying a deposit on your first home or saving for retirement. While you can access your money for other reasons, you will then lose 25% of the total, including your own contribution and the government bonus along with any investment growth. That means in many cases you will get back less money than you put in.

The 2022/23 ISA allowance is a generous £20,000 and offers the potential to save a lot of money on tax, assuming you are lucky enough to have this amount to save or invest. But, very importantly, it cannot be rolled over. So if you don’t use your 2022/23 ISA allowance by 5th April 2023 at the latest, it will be gone forever. It is therefore important to attend to this now and ensure you get as much benefit as possible from this valuable tax-saving concession.

As always, if you have any comments or questions about this post, please do leave them below.

This is a fully updated post from last year.

Disclaimer: Please note that I am not a professional financial adviser and cannot give personal financial advice. You should do your own ‘due diligence’ before making any investment, and seek professional advice from a qualified financial adviser if in any doubt how best to proceed. All investments carry a risk of loss.

Note, also, that posts on Pounds and Sense may include affiliate links. If you click through one of these and go on to perform a qualifying transaction at the website in question, I may receive a fee for introducing you. This will not affect any fees you may be charged or the product or service you receive.

If you enjoyed this post, please link to it on your own blog or social media:

Today I have a collaborative post with my friends at HSBC Life for you. It’s about home insurance and how well people really understand it.

Let’s start with the most basic question, though…

What Is Home Insurance?

Home insurance provides financial protection in the event of something happening to your property (i.e. home) or your possessions. There are two main types of home insurance, contents and buildings.

Contents insurance covers your belongings for loss or damage caused by fire, theft, flood and other disasters. Buildings insurance covers the structure of the building itself, including the walls, floors, ceilings, roof, etc.

While contents insurance is generally optional (though highly recommended), buildings insurance is likely to be compulsory if buying your home with a mortgage. People who are renting will not normally require buildings insurance as this is the landlord’s responsibility, but they may still wish to take out contents insurance.

You can have separate buildings and contents insurance, but if you need both it will usually work out cheaper to get a combined policy. This may also make life simpler when the time comes to make a claim.

Home insurance clearly isn’t the most exciting of subjects, with most people regarding it as a necessary evil. But of course, if the worst happens, having the appropriate insurance cover may stop a misfortune turning into a catastrophe.

HSBC recently commissioned a study from market research company YouGov about people’s attitudes to home insurance. They polled 2,000 people in the survey, the fieldwork for which took place in May 2022.

Survey Results

The main questions asked in the HSBC survey are set out below, along with the results.

What are the main reasons people do or don’t have home insurance?

30% say it is expensive

18% say it is comforting

41% say it gives them peace of mind

49% say it is necessary

31% say it is reassuring

How much time does the average person spends researching their home insurance?

47% up to 1 hour

17% 1-2 hours

7% 1 day to 1 week

Where they do their research, if at all?

60% use price comparison websites

16% recommendations

12% customer reviews

What consideration is most important to them if they do select an insurer?

69% say price

71% say quality of cover

38% say reputation

Even for those who have purchased, do they understand what they’re buying?

72% say they understand what they have purchased

10% say they do not understand

Finally, what proportion have made a claim on their home insurance before?

39% of respondents have made a claim before

61% of respondents have not made a claim before

My Thoughts

One thing the HSBC survey results suggest is that many people don’t fully understand home insurance or give it the careful consideration it merits. In these times of rapidly rising living costs, that could be a serious mistake.

I would offer two main pieces of advice. First, think carefully about what home insurance you require. Do you need both buildings and contents insurance, or just one or the other? Think also how much cover you need, based on the value of your belongings (for contents insurance) and of your property (for buildings insurance). In the latter case, you should insure for total rebuilding costs rather than just market value, as this is what you would have to pay if your house was destroyed by fire, flood or some other disaster.

And second, shop around for your home insurance, as prices vary widely. Using a price comparison service such as GoCompare can be a smart strategy, though bear in mind that not all insurers appear on these platforms (Aviva, Zurich and Direct Line are three that don’t).

I also recommend using cashback sites like Top Cashback, as these frequently offer cashback to people taking out home insurance from companies listed with them. They may also offer cashback to anyone purchasing via a price comparison service listed on the cashback site, giving you the best of both worlds.

I’d also highly recommend reading my blog post How I Saved £511.08 on my Annual Home Insurance. And yes, I really did save that much. Though as you’ll see I had clearly been paying over the odds for my home insurance for some time. I had separate buildings and contents insurance which, as mentioned above, typically works out more expensive. What’s more, I had lazily allowed both policies to keep rolling over year after year without checking whether better deals were available. Don’t make the same mistakes I did!

Many thanks again to my friends at HSBC Life for sharing their survey results with me and allowing me to reproduce them.

As always, if you have any comments or questions about this post, please do leave them below.

This is a collaborative post.

If you enjoyed this post, please link to it on your own blog or social media: