Today I am looking at the Warm Home Discount scheme. The 2024/25 version of this has just launched.

The WHD scheme provides people on low incomes and/or certain means-tested benefits with a discount of £150 on their electricity bill. This is a one-off payment that will be credited to your electricity account by March 2025. It won’t be paid to you in cash.

If you have a pre-payment electricity meter you can still get WHD. You may be given a voucher you can use to top up your payments. Your electricity supplier will tell you exactly how and when you will receive this.

You may be able to get the discount on your gas bill instead if your supplier provides you with both gas and electricity. You will need to ask your supplier about this.

To get the £150 discount, you need to have your name on the bill and either receive a qualifying benefit or (in Scotland) qualify under your supplier’s low-income criteria (see below).

If you live in England or Wales, you will qualify if you either:

An important thing to note is that only pensioners who receive the Guarantee element of Pension Credit will qualify automatically for the Warm Home Discount. These people are known as ‘Core Group 1’ in England and Wales and the ‘Core Group’ in Scotland. If you’re in this group you should receive a letter between October 2024 and early January 2025 telling you when and how the discount will be paid. If you don’t get a letter and think you are eligible for the core group, you should contact the Warm Home Discount helpline on 0800 030 9322.

You should also still qualify for WHD if you live in England or Wales and:

your energy supplier is part of the scheme (see below)

you get certain means-tested benefits or tax credits

your property has a high energy cost score (see below)

your name (or your partner’s) is on the bill

This is known as being in ‘Core Group 2’. The qualifying means-tested benefits are:

Housing Benefit

income-related Employment and Support Allowance (ESA)

income-based Jobseeker’s Allowance (JSA)

Income Support

the ‘Savings Credit’ part of Pension Credit

Universal Credit

You could also qualify if your household income falls below a certain threshold and you get either:

Again, you should receive a letter between October 2024 and early January 2025 telling you about the discount if you’re eligible. In most cases you are no longer required to apply for it.

Most eligible households will receive an automatic discount. Your letter will say if you need to call a helpline by 28 February 2025 to confirm your details.

If you’re eligible, your electricity supplier will apply the discount to your bill by 31 March 2025.

If you live in Scotland and don’t get the Guarantee Element of Pension Credit, you may qualify to receive WHD if:

your energy supplier is part of the scheme

you (or your partner) get certain means-tested benefits or tax credits

your name (or your partner’s) is on the bill

Your supplier may have additional criteria so you will need to check with them if you’re eligible. This is known as being in the ‘broader group’. To get the discount you’ll need to stay with your supplier until it’s paid.

As mentioned above, if you are not in Core Group 1 in England and Wales, to qualify for WHD your property must also have a high energy cost score.

The Government models the energy cost score of your property based on official data about its characteristics. These include the property type, age, and floor area. The Government uses data from the Valuation Office Agency (VOA) to model your property’s energy cost score. They may also use your property’s Energy Performance Certificate (EPC), assuming it has one. Other sources and statistical methods may also be used for the small proportion of households where data is not otherwise available.

Each year the Government will decide what constitutes a high energy cost score. It’s not straightforward for an individual to determine whether they will be eligible under this criterion. If you fill in the online eligibility checker, however, it should indicate whether or not you are likely to qualify (when I tried this for some elderly friends, it said they would ‘probably’ qualify and should wait to receive a letter).

Which Suppliers Offer Warm Home Discount?

All the large energy suppliers offer WHD and some of the lesser-known ones as well. Below is a list of suppliers copied from the government webpage devoted to Warm Home Discount. You can check your eligibility on the supplier’s website or phone them up and ask.

100Green (formerly Green Energy UK or GEUK)

Affect Energy – see Octopus Energy

Boost

British Gas

Bulb Energy – see Octopus Energy

Co-op Energy – see Octopus Energy

E – also known as E (Gas and Electricity)

Ecotricity

E.ON Next

EDF

Fuse Energy

Good Energy

Home Energy

London Power

Octopus Energy

Outfox the Market

OVO

Rebel Energy

Sainsbury’s Energy

Scottish Gas – see British Gas

ScottishPower

Shell Energy Retail

So Energy

Tomato Energy

TruEnergy

Utilita

Utility Warehouse

The government say that if the electricity supplier you were with stops trading, you may still be eligible for the Warm Home Discount. Ofgem will appoint your new supplier for you, and you should check with the new supplier to find out if you’re eligible for the discount.

If you are in the market for a new energy supplier, you may like to know that if you switch to EDF Energy you can get £50 credited to your account by clicking on my EDF referral link. I am an EDF customer myself and will also get £50 credited to my account if you do this and switch to EDF. This will not affect in any way the service you receive or the rate you are charged.

Other Winter Fuel Benefits

Two other benefits are also available to qualifying individuals.

1. People born before 23rd September 1958 and in receipt of pension credit or certain other welfare benefits are eligible for a Winter Fuel Payment. This is worth £200 or £300 per person and will be paid in November or December 2024. More information including eligibility details can be found on the official government website. As you may know, previously all state pensioners were entitled to WFP, but the new Labour government has chosen to restrict it to the poorest pensioners only.

2. In the event of a prolonged cold spell, most people receiving Pension Credit will receive Cold Weather Payments. People on Income Support, Jobseeker’s Allowance, Employment and Support Allowance (ESA) and Universal Credit may also qualify depending on their circumstances, e.g. if they have a disability and/or a disabled child living with them. You will get this payment if the average temperature in your area is recorded as, or forecast to be, zero degrees Celsius or below for seven consecutive days. You get £25 for each seven-day period of very cold weather between 1 November and 31 March. Note that people in Scotland don’t get Cold Weather Payments but might get an annual £50 Winter Heating Payment instead. This is paid regardless of weather conditions in your area.

As always, if you have any comments or questions about this post, please do leave them below.

This is the 2024 update of an annual post.

If you enjoyed this post, please link to it on your own blog or social media:

Recently my energy supplier, EDF Energy, has been sending me invitations to sign up for what it calls its ‘Sunday Saver’ challenge.

The way this works is that you sign up to shift some of your electricity usage on weekdays away from peak hours (4pm-7pm). When you hit your target (which is set individually for each user by EDF), you earn free electricity the following Sunday.

EDF say, ‘The more you shift, the more you earn – reduce your weekly peak usage by 40% and you could earn up to 16 hours of free electricity per week.’

The challenge is due to take place monthly, starting on the first Monday of each month.

At first glance you might think this is a good offer. But as I have looked into it more, my doubts have grown. Here are my main reservations…

To benefit from this scheme you have to cut your daily energy usage every weekday between 4pm and 7pm. That’s quite a long period (three hours), and coincides with when I would normally be cooking my evening meal. To have any realistic chance of cutting my energy use during this time, I would have to eat either ridiculously early or significantly later than normal. For various reasons, including my health, I prefer to eat between 6 and 7 pm and no later. So that in itself is a big ask and would impact drastically on my normal routine.

Free electricity on Sunday sounds great, but the devil is in the detail. EDF say that you will get ‘up to 16 hours’ of free electricity if you meet their targets, but are very vague about what this means in practice. Specifically, they don’t explain how your energy-saving targets are calculated, how any reduction in usage translates to free hours, or when on Sunday you will be able to use the free electricity awarded.

In addition, they say there are ‘fair usage’ limits to how much free electricity you can have. Again, they are vague about what this means in practice. The obvious way to use your free electricity would be to charge your EV, and I strongly suspect limits would be placed on this. As for me, I don’t have an EV and don’t want one, so my options for benefiting from the free electricity would be limited. I could shift use of appliances like my washing machine to Sunday but doubt if I could save more than a few kw/h this way (obviously the exact number would depend on how many free hours I was allocated, which is anyone’s guess). That means my free electricity would likely benefit me by no more than a pound or two.

Lastly, as a solar panel owner I already get some free electricity anyway. My panels obviously generate less in the winter, but during daylight hours they still produce something. That means any benefit from free electricity on Sundays will be reduced, especially if (as is likely) the free hours are in the day rather than at night.

Overall, then, I am not much enamoured of EDF’s Sunday Saver challenges and won’t be signing up. Ultimately, I am not prepared to make major changes to my day-to-day schedule in pursuit of what will likely be (in my case anyway) minuscule rewards.

Obviously some will see this differently and I wish them well. And it’s good that EDF (and other companies) are exploring ways to help customers reduce their bills. I do just think this particular one – for me anyway – is a non-starter.

I would be interested to hear any comments from people doing this challenge (or similar ones from other energy companies) as to whether they find it worthwhile, and whether the benefits really do justify the changes you are required to make.

I do still recommend EDF Energy based on my personal experiences with them. And as I’ve said before on PAS, I can offer anyone switching to EDF £50 off their bills if they use my refer-a-friend link at https://edfenergy.com/quote/refer-a-friend/sunny-koala-9462 when applying. I will also get £50 off my bill if you do this, which is duly appreciated 🙂

UPDATE 22 OCTOBER 2024 – I am indebted to the readers (especially Harry!) who have taken the time to comment on this article and address some of the points raised in my original post. Based on this I have changed my views somewhat and am considering registering for the scheme when it reopens in November. If you’re still wondering whether to take the plunge, please do take the time to read the comments as (like me) they may influence your decision. I will publish an update in due course if I proceed with it next month.

UPDATE 28 NOVEMBER 2024 – Thanks again to everyone who commented on this post. Sorry I couldn’t reply to everyone individually. You may like to know that I just added a new post about why I changed my mind and registered for the EDF ‘Sunday Saver’ Challenge and how I got on in my first month. Please see https://www.poundsandsense.com/heres-why-i-changed-my-mind-about-edf-energys-sunday-saver-challenge/

If you enjoyed this post, please link to it on your own blog or social media:

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

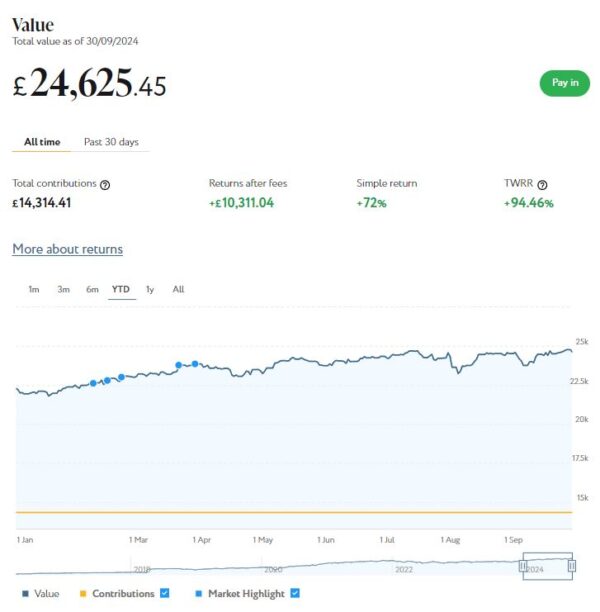

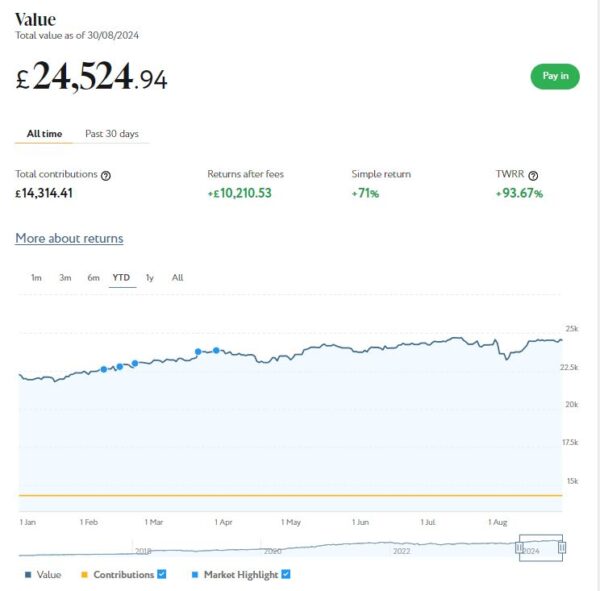

As the screenshot below for the year to date shows, my main Nutmeg portfolio is currently valued at £24,625. Last month it stood at £24,525, so that is an increase of £100.

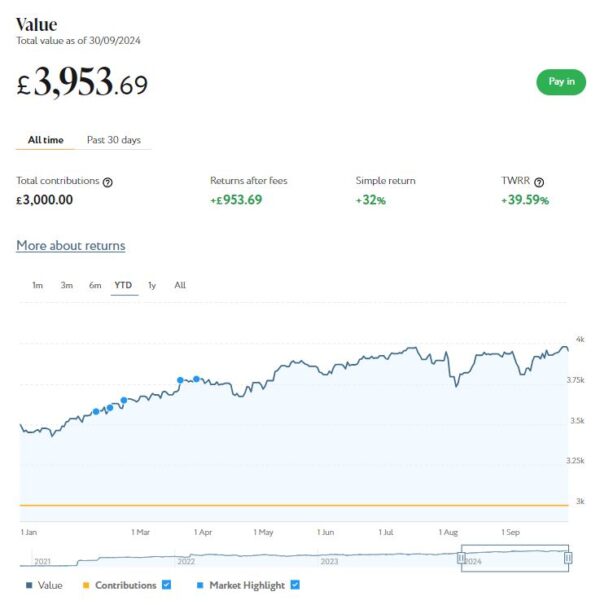

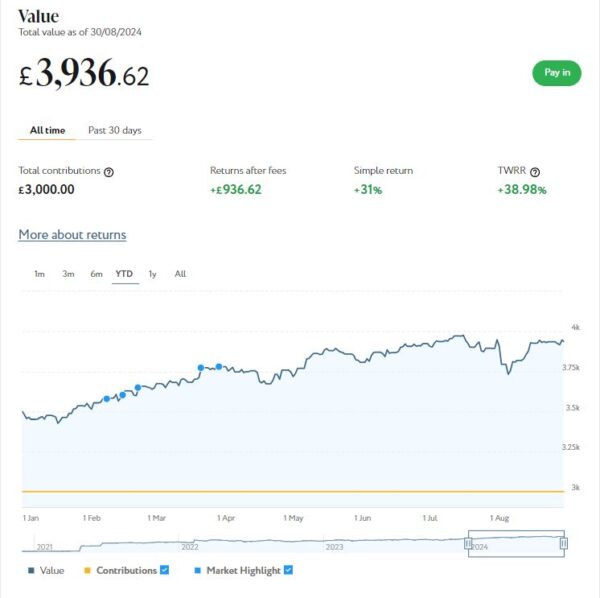

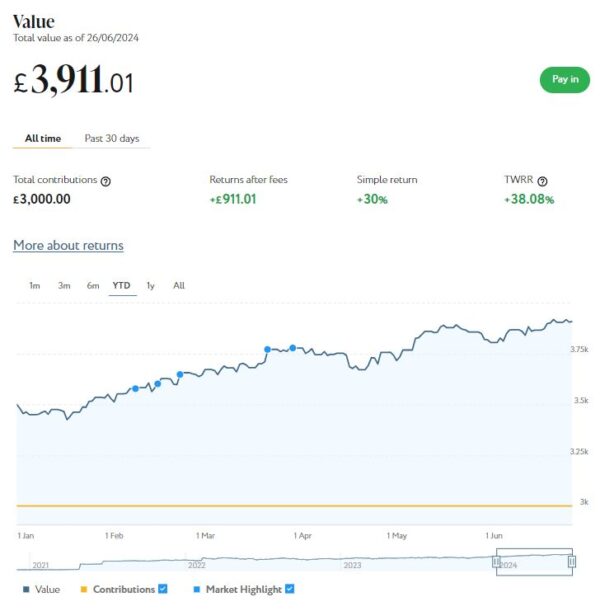

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £3,954 (rounded up) compared with £3,937 a month ago, a rise of £17. Here is a screen capture showing performance over the year to date.

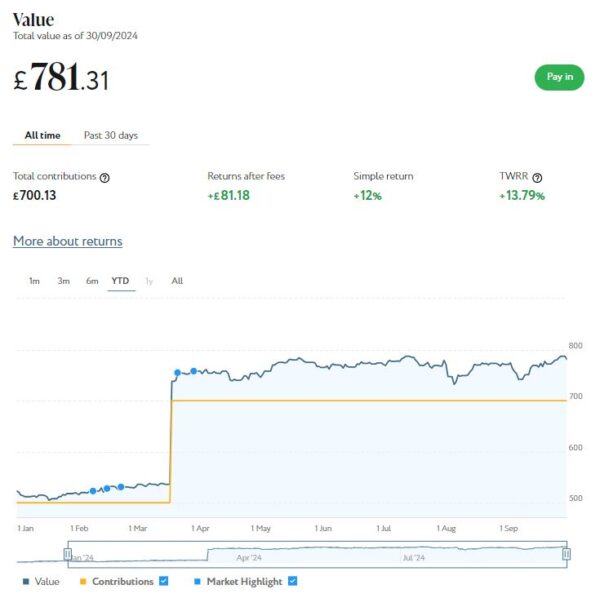

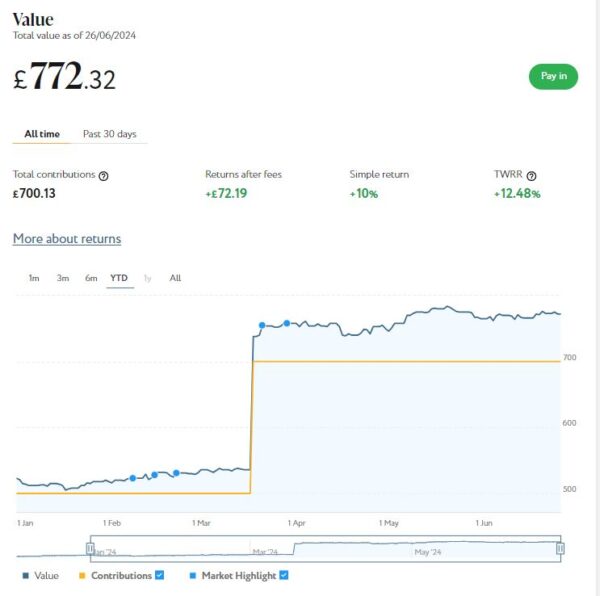

Finally, at the start of December 2023 I invested £500 in one of Nutmeg’s new thematic portfolios (Resource Transformation). In March I also invested a further £200 from ‘Refer a Friend’ bonuses. As you can see from the YTD screen capture below, this portfolio is now worth £781 compared with £772 last month, a small rise of £9.

As you can see, September was another decent though unspectacular month for my Nutmeg investments. Their overall value has risen by £126 or 0.43% since the start of September. They are also up by £3,045 or 11.57% since the start of the year.

You can read my full Nutmeg review here. If you are looking for a home for your annual ISA allowance, based on my overall experience over the last eight years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs), Lifetime ISAs and Junior ISAs as well.

Note that I am no longer an affiliate for Nutmeg. That means you won’t find any affiliate links in my review (or anywhere else on PAS). And you will no longer see the no-fees-for-six-months offer I used to promote as an affiliate. However, the better news is that you can still get six months free of any management fees by registering with Nutmeg via my Refer a Friend link. I will receive a gift voucher if you do this, which is duly appreciated

Don’t forget, also, that the current tax year began on 6 April 2024 and you have a full £20,000 tax-free ISA allowance for 2024/25. In a change to the rules, you can now open any number of ISAs with different providers in the same tax year, as long as you don’t exceed your overall £20,000 allowance. So opening a stocks and shares ISA with Nutmeg won’t prevent you from also opening one with another S&S ISA provider (should you wish to) later in the financial year.

Moving on, I also have investments with the property crowdlending platform Kuflink. They continue to do well, with new projects launching every week. I currently have around £833 invested with them in 7 different projects paying interest rates averaging around 7%. I also have £40 in my Kuflink cash account.

To date I have never lost any money with Kuflink, though some loan terms have been extended once or twice. On the plus side, when this happens additional interest is paid for the period in question.

There is now an initial minimum investment of £1,000 and a minimum investment per project of £500. Kuflink say they are doing this to streamline their operation and minimize costs. I can understand that, though it does mean that the option to test the water with a small first investment has been removed. It also makes it harder for small investors (like myself) to build a well-diversified portfolio on a limited budget.

One possible way around this is to invest using Kuflink’s Auto/IFISA facility. Your money here is automatically invested across a basket of loans over a period from one to five years. Interest rates range from 7% to around 10%, depending on the length of term you choose. Full up-to-date details can be found on the Kuflink website.

You can invest tax-free in a Kuflink Auto IFISA. Or if you have already used your annual ISA allowance elsewhere, you can invest via a taxable Auto account. You can read my full Kuflink review here if you wish.

Moving on, my Assetz Exchange investments continue to generate steady returns. Regular readers will know that this is a P2P property investment platform focusing on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my AE portfolio has generated a respectable £208.97 in revenue from rental income. Capital growth has slowed, though, in line with UK property values generally.

At the time of writing, 11 of ‘my’ properties are showing gains, 5 are breaking even, and the remaining 17 are showing losses. My portfolio of 33 properties is currently showing a net decrease in value of £42.75, meaning that overall (rental income minus capital value decrease) I am up by £166.22. That’s still a decent return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Assetz Exchange most projects are socially beneficial as well.

The overall fall in capital value of my AE investments is obviously a little disappointing. But it’s important to remember that until/unless I choose to sell the investments in question, it is largely theoretical, based on the latest price at which shares in the property concerned have changed hands. The rental income, on the other hand, is real money (which in my case I’ve reinvested in other AE projects to further diversify my portfolio).

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of AE as far as i am concerned (especially after Kuflink raised their minimum investment per project to £500). You can actually invest from as little as 80p per property if you really want to proceed cautiously.

As I noted in this recent post, Assetz Exchange is particularly good if you want to compound your returns by reinvesting rental income. This effectively boosts the interest rate you are receiving. Personally, once I have accrued a minimum of £10 in rental payments, I reinvest this money in either a new AE project or one I have already invested in (thus increasing my holding). Over time, even if I don’t invest any more capital, this will ensure my investment with AE grows at an accelerating rate and becomes more diversified as well.

My investment on Assetz Exchange is in the form of an IFISA so there won’t be any tax to pay on profits, dividends or capital gains. I’ve been impressed by my experiences with Assetz Exchange and the returns generated so far, and intend to continue investing with them. You can read my full review of Assetz Exchange here. You can also sign up for an account on Assetz Exchange directly via this link [affiliate]. Bear in mind that, as from this financial year (2024/25), you can open more than one IFISA per year.

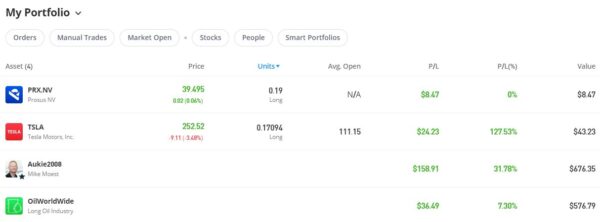

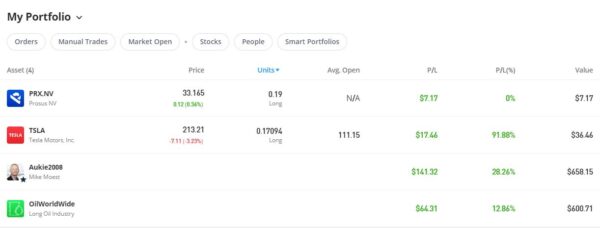

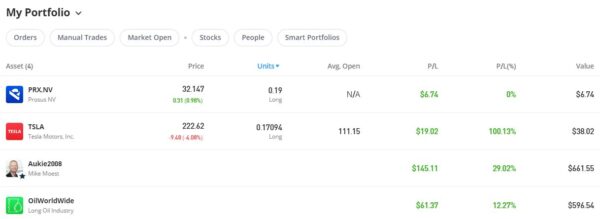

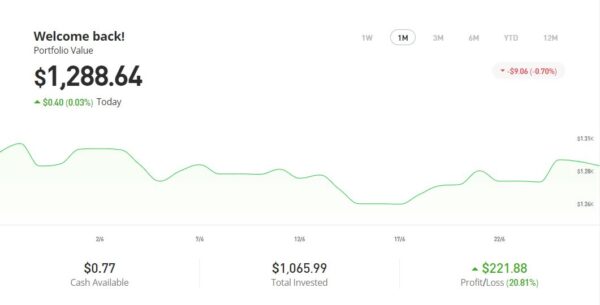

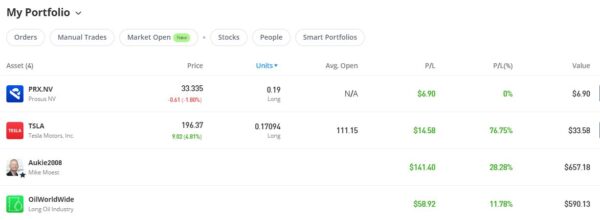

In 2022 I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios, Oil Worldwide. I also invested a small amount I had left over in Tesla shares.

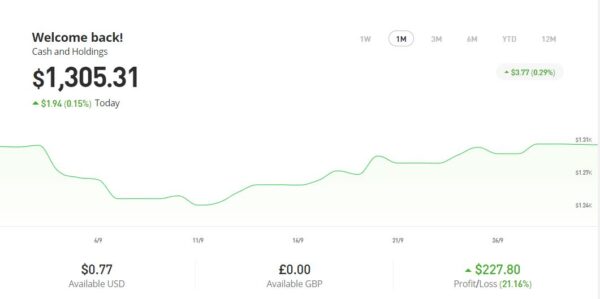

As you can see from the screen captures below, my original investment totalling $1,022.26 is today worth $1,305.31 an overall increase of $283.05 or 27.69%.

As you can see, my Oil WorldWide investment is showing 7.30% profit. That’s okay but not spectacular. Obviously my copy trading investment with Aukie2008 has been doing much better. The Oil WorldWide port was recently rebalanced by eToro, so I hope this may boost its performance. The investment team at eToro periodically rebalance all smart portfolios to ensure that the mix of investments remains aligned with the portfolio’s goals, and to take advantage of any new opportunities that may present themselves.

As a matter of interest, since I wrote the above war has effectively broken out in the Middle East. This has led to fears that oil supplies from the region will be compromised and the price of oil will rise. As a consequence of this (I assume) the value of my Oil Worldwide investment has gone up. I say this not to gloat over the tragedy that is unfolding in the area, but to highlight the fact that a diversified portfolio can often help to hedge against economic downturns resulting from world events.

You might also notice that I have a small holding in Prosus NV, a Dutch internet group. To be honest I don’t understand how I acquired this, but it may be connected to my copy trading investment with MIke Moest (who is Dutch). In any event, I am happy to have it in my portfolio as well!

eToro also offer the free eToro Money app. This allows you to deposit money to your eToro account without paying any currency conversion fees, saving you up to £5 for every £1,000 you deposit. You can also use the app to withdraw funds from your eToro account instantly to your bank account. I tried this myself and was impressed with how quickly and seamlessly it worked. You can read my blog post about eToro Money here. Note that it can also serve as a cryptocurrency wallet, allowing you to send and receive crypto from any other wallet address in the world.

I had three more articles published in September on the excellent Mouthy Money website. The first is Are Electric Boilers Better Than Heat Pumps?. As you doubtless know, the government are pushing heat pumps hard as a means of achieving their Net Zero goals. They are definitely not a one-size-fits-all solution, though. In this article I highlighted an alternative that may be more suitable for some, electric boilers. These are cheaper, smaller and quieter than heat pumps (though their running costs may be higher). You can read all about the pros and cons of heat pumps versus electric boilers in the article.

Also in September I revealed How to Get Free Stuff Online. In this article, I explained how you can get your hands on a wide range of freebies online, from samples and giveaways to promotional offers and rewards programmes – all without having to spend a single penny!

Finally, in September I discussed How to Save Money With Cashback Sites. If you ever buy anything online, you can almost certainly save by signing up with these sites. In this article I revealed how they work and set out some hints and tops for making the most of them.

As I’ve said before, Mouthy Money is a great resource for anyone interested in money-making and money-saving. From the variety of articles published in September, I particularly enjoyed Secondhand September: Good for Your Purse and the Planet by regular MM contributor Shoestring Jane. Jane writes mainly about money saving and frugal living. You can see all of her articles for Mouthy Money via this web page.

I also published (or republished) several posts on Pounds and Sense in September. Some are no longer relevant due to closing dates having passed, but I have listed the others below.

In Can You Still Make Money From Matched Betting? I discussed this tax-free money-making opportunity. As I said in the article, this is something I did for several years and earned about £3,000 from. I am not doing it nearly as much these days, for reasons explained in the article. But if you’ve never done it before, I do still highly recommend it as a way of making some quick tax-free cash. The article explains what matched betting is and how to get started.

The price of stamps is rising again on Monday 7 October 2024. That is the second price rise this year, after they also went up in April. So in How to Beat the Postage Stamp Price Rise, I revealed just how much (some) prices are rising and suggested ways to mitigate this.

In case you didn’t know, October is Free Wills Month. So in Get Your Will Written Free of Charge in October, I discussed how you can use this no-strings scheme to get your will written free at a range of participating solicitors across the UK. There are only limited slots available, so I recommend moving quickly if you want to take advantage of this opportunity.

Also in September I published How to Save Money on Your Heating Bills This Winter. As you doubtless know, gas and electricity bills have gone up considerably in the last year or two. And many older people will no longer get Winter Fuel Payments, as the new Labour government have opted to restrict this to just the very poorest pensioners (those in receipt of Pension Credit). So in this article I set out a range of ways you may be able to save money on your heating and energy bills. Following these tips could save you hundreds of pounds in the months and years ahead.

Finally, I published Amazon Big Deals Day is Almost Here. This annual event extends over two days, Tuesday 8th and Wednesday 9th October 2024. It is is a special event for Amazon Prime members only. Amazon say they will be offering members their lowest prices of the year on selected products from leading brands including Philips, Logitech, Oral-B, Braun, Tefal, Ghd, Swarovski, Bosch, Shark, and so on.

Next, some odds and ends. First up, Trading 212 recently reopened their free share offer, so I have updated my post Get a Free Share Worth Up to £100 With Trading 212. This explains how, if you haven’t done so already, you can get a free share when you open a new Invest or Stocks ISA with Trading 212. Note that opening a Cash ISA with T212 alone will not qualify you for a free share, but of course you can do both. My advice is to start by opening a Stocks ISA or (non-ISA) Invest account to qualify for your free share and apply (if you wish) for the Cash ISA after that. This new free share offer closes on 6 November 2024.

A few months ago I invested just over £1,000 in a Scottish wind farm project via a platform called Ripple Energy. The way this works is that you pay a fee towards building the wind farm, and in exchange receive lower-cost, ‘green’ electricity once the wind farm is up and running. This will continue for the life of the wind farm (an estimated 20 years). The original closing date for this was the end of May, but the date was extended and the share offer is still open at the time of writing. You can pay by 12 monthly instalments rather than a single lump sum if you like. If you’re interested in learning more, you can visit the Ripple website via my referral link. If you decide to invest, you will get a £25 bonus credited to your account when generation starts (and so will I). Note that you will need to invest a minimum of £1,000 to qualify for the £25 bonus, but you can invest from as little as £25 if you wish.

Speaking of energy, a quick reminder that if you switch to EDF Energy via my refer-a-friend link (below) you can get a FREE £50 credited to your energy account (and so will I). For more info and to sign up, click on https://edfenergy.com/quote/refer-a-friend/sunny-koala-9462

Finally, I wanted to highlight (again) the decision by the new government to abolish Winter Fuel Payments for all pensioners except those on pension credit. Like many others, I feel this is a terrible decision that will badly impact some of the poorest people in society and quite likely lead to increased deaths by hypothermia in the winter ahead (and others to follow).

it is therefore more important than ever that older people who may be eligible for pension credit apply for it. I recently updated my blog post about pension credit in light of the announcement. If you have older relatives, friends or neighbours, please encourage them to apply if they may be eligible. The application process is not as straightforward as it should be, so they may well appreciate some help with it

Even so, be aware that only the very poorest pensioners qualify for pension credit. If you get the full new state pension, even with no other source of income, you likely won’t qualify. I do therefore recommend writing to your MP and asking for this Draconian decision to be reversed. You may also like to sign one of the various petitions that have sprung up, including this one on Change.org and this one from Age UK. The former has over 100,000 signatures now and the latter over half a million.

That’s all for now. If you have any comments or queries about this update, as ever, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss. Note also that posts on PAS may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media:

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

As the screenshot below for the year to date shows, my main Nutmeg portfolio is currently valued at £24,525 (rounded up). Last month it stood at £24,237, so that is an increase of £288.

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £3,937 compared with £3,895 a month ago, a rise of £42. Here is a screen capture showing performance over the year to date.

Finally, at the start of December 2023 I invested £500 in one of Nutmeg’s new thematic portfolios (Resource Transformation). In March I also invested a further £200 from ‘Refer a Friend’ bonuses. As you can see from the YTD screen capture below, this portfolio is now worth £772 compared with £769 last month, a small rise of £3.

As you can see from the charts, August was generally a decent month for my Nutmeg investments, despite a hiccup early in the month. Their overall value has risen by £333 or 1.16% since the start of August. They are also up by £2,919 or 11.08% since the start of the year.

You can read my full Nutmeg review here. If you are looking for a home for your annual ISA allowance, based on my overall experience over the last eight years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs), Lifetime ISAs and Junior ISAs as well.

Note that I am no longer an affiliate for Nutmeg. That means you won’t find any affiliate links in my review (or anywhere else on PAS). And you will no longer see the no-fees-for-six-months offer I used to promote as an affiliate. However, the better news is that you can still get six months free of any management fees by registering with Nutmeg via my Refer a Friend link. I will receive a gift voucher if you do this, which is duly appreciated

Don’t forget, also, that the current tax year began on 6 April 2024 and you have a full £20,000 tax-free ISA allowance for 2024/25. In a change to the rules, you can now open any number of ISAs with different providers in the same tax year, as long as you don’t exceed your overall £20,000 allowance. So opening a stocks and shares ISA with Nutmeg won’t prevent you from also opening one with another S&S ISA provider (should you wish to) later in the financial year.

Moving on, I also have investments with the property crowdlending platform Kuflink. They continue to do well, with new projects launching every week. I currently have around £833 invested with them in 7 different projects paying interest rates averaging around 7%. I also have £40 in my Kuflink cash account.

To date I have never lost any money with Kuflink, though some loan terms have been extended once or twice. On the plus side, when this happens additional interest is paid for the period in question.

There is now an initial minimum investment of £1,000 and a minimum investment per project of £500. Kuflink say they are doing this to streamline their operation and minimize costs. I can understand that, though it does mean that the option to test the water with a small first investment has been removed. It also makes it harder for small investors (like myself) to build a well-diversified portfolio on a limited budget.

One possible way around this is to invest using Kuflink’s Auto/IFISA facility. Your money here is automatically invested across a basket of loans over a period from one to five years. Interest rates range from 7% to around 10%, depending on the length of term you choose. Full up-to-date details can be found on the Kuflink website.

You can invest tax-free in a Kuflink Auto IFISA. Or if you have already used your annual ISA allowance elsewhere, you can invest via a taxable Auto account. You can read my full Kuflink review here if you wish.

Moving on, my Assetz Exchange investments continue to generate steady returns. Regular readers will know that this is a P2P property investment platform focusing on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my AE portfolio has generated a respectable £200.41 in revenue from rental income. Capital growth has slowed, though, in line with UK property values generally.

At the time of writing, 10 of ‘my’ properties are showing gains, 6 are breaking even, and the remaining 17 are showing losses. My portfolio of 33 properties is currently showing a net decrease in value of £43.69, meaning that overall (rental income minus capital value decrease) I am up by £156.72. That’s still a decent return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Assetz Exchange most projects are socially beneficial as well.

The overall fall in capital value of my AE investments is obviously a little disappointing. But it’s important to remember that until/unless I choose to sell the investments in question, it is largely theoretical, based on the most recent price at which shares in the property concerned have changed hands. The rental income, on the other hand, is real money (which in my case I’ve reinvested in other AE projects to further diversify my portfolio).

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of AE as far as i am concerned (especially after Kuflink raised their minimum investment per project to £500). You can actually invest from as little as 80p per property if you really want to proceed cautiously.

As I noted in this recent post, Assetz Exchange is particularly good if you want to compound your returns by reinvesting rental income. This effectively boosts the interest rate you are receiving. Personally, once I have accrued a minimum of £10 in rental payments, I reinvest this money in either a new AE project or one I have already invested in (thus increasing my holding). Over time, even if I don’t invest any more capital, this will ensure my investment with AE grows at an accelerating rate and becomes more diversified as well.

My investment on Assetz Exchange is in the form of an IFISA so there won’t be any tax to pay on profits, dividends or capital gains. I’ve been impressed by my experiences with Assetz Exchange and the returns generated so far, and intend to continue investing with them. You can read my full review of Assetz Exchange here. You can also sign up for an account on Assetz Exchange directly via this link [affiliate]. Bear in mind that, as from this financial year (2024/25), you can open more than one IFISA per year.

In 2022 I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios, Oil Worldwide. I also invested a small amount I had left over in Tesla shares.

As you can see from the screen captures below, my original investment totalling $1,022.26 is today worth $1,303.27 an overall increase of $281.01 or 27.51%.

As you can see, my Oil WorldWide investment is showing 12.85% profit. That’s okay but not spectacular. Obviously my copy trading investment with Aukie2008 has been doing better. The Oil WorldWide port was recently rebalanced by eToro, so I hope this may boost its performance. The investment team at eToro periodically rebalance all smart portfolios to ensure that the mix of investments remains aligned with the portfolio’s goals, and to take advantage of any new opportunities that may present themselves.

You might also notice that I have a small holding in Prosus NV, a Dutch internet group. To be honest I don’t understand how I acquired this, but it may be connected to my copy trading investment with MIke Moest (who is Dutch). In any event, I am happy to have it in my portfolio as well!

eToro also offer the free eToro Money app. This allows you to deposit money to your eToro account without paying any currency conversion fees, saving you up to £5 for every £1,000 you deposit. You can also use the app to withdraw funds from your eToro account instantly to your bank account. I tried this myself and was impressed with how quickly and seamlessly it worked. You can read my blog post about eToro Money here. Note that it can also serve as a cryptocurrency wallet, allowing you to send and receive crypto from any other wallet address in the world.

I had three more articles published in August on the excellent Mouthy Money website. The first is Win Fame and (Maybe) Fortune as a TV Quiz Show Contestant. This can be an exciting and occasionally lucrative pastime. I revealed how to find opportunities and apply for them. I also explained how the auditioning process works, and offered some tips on how to boost your chances of success.

Also in August I revealed my Ten Top Tips for Working From Home. This is something I’ve done for over 30 years now, so in this article I set out my top ten tips based on my experience. If you have recently started working from home, or expect to do so in future, you may find this article helpful.

Finally, I wrote an article titled How Understanding Cognitive Dissonance Theory Can Help Us Manage Our Finances Better. This article drew on my experiences of studying psychology back in the 1970s. Developed by psychologist Leon Festinger in 1957, cognitive dissonance theory explores the discomfort we experience when we simultaneously hold conflicting beliefs or attitudes. By understanding this, we can gain insights into our financial behaviour, helping us make more informed decisions and achieve better financial results.

As I’ve said before, Mouthy Money is a great resource for anyone interested in money-making and money-saving. From the variety of articles published in August, I particularly enjoyed How to Save Money on Your Home Removal by regular MM contributor Shoestring Jane. Jane writes mainly about money saving and frugal living. You can see all of her articles for Mouthy Money via this web page.

I also published several posts on Pounds and Sense in August. Some are no longer relevant due to closing dates having passed, but I have listed the others below.

In these challenging times, we all need to ensure our savings stretch as far as possible. So in How to Maximize Your Savings Interest l set out a range of tax-free allowances you can use to help do this. They include the Personal Savings Allowance (PSA), Starting Rate for Savings, Individual Savings Accounts (ISAs), and various others.

I also published How to Win Cash and Prizes in Online Competitions. This can be another tax-free way to boost your finances! In this post I revealed how to find online competitions to enter, why you should set up dedicated ‘comping’ accounts, how to identify potential scams, and more. Good luck if you decide to try this 🤞

As we all know Labour achieved a landslide victory in the general election, and it appears that austerity measures are on the way now. So in How to Reduce the Impact of Tax Rises in Rachel Reeves’ First Budget, I set out some recommended steps to try to protect your finances in the months (and years) ahead. The Chancellor’s first budget is scheduled for 30th October 2024, with tax rises and cuts to public services widely anticipated.

Finally, in August I published What Alternatives Are There to Heat Pumps? The government are currently pushing heat pumps hard in their frantic quest to achieve Net Zero. For a range of reasons, however, they are not suitable for every property. And even if your home might theoretically be suitable, there are good reasons you might not want one (discussed a while ago in this Mouthy Money article). So in this post I set out some possible alternatives you might like to consider instead.

Next, a few odds and ends. I recently invested some money (just over £1,000) in a Scottish wind farm project via a platform called Ripple Energy. The way this works is that you pay a one-off fee towards building the wind farm, and in exchange receive lower-cost, ‘green’ electricity once the wind farm is up and running. This will continue for the life of the wind farm (an estimated 20 years). The original closing date for this was the end of May, but the date was extended and the share offer is still open at the time of writing.

If you’re interested in learning more, you can visit the Ripple website via my referral link. If you decide to invest, you will get a £25 bonus credited to your account when generation starts (and so will I). Note that you will need to invest a minimum of £1,000 to qualify for the £25 bonus, but you can invest from as little as £25 if you like.

Speaking of energy, a quick reminder that if you switch to EDF via my refer-a-friend link (below) you can get a FREE £50 credited to your energy account (and so will I). For more info and to sign up, click on https://edfenergy.com/quote/refer-a-friend/sunny-koala-9462

Finally, I wanted to highlight the decision by the new Labour government to abolish Winter Fuel Payments for all pensioners except those on pension credit. Like many others, I feel this is a terrible decision that will badly impact some of the poorest people in society and quite likely lead to increased deaths by hypothermia in the winter ahead (and others to follow).

it is therefore more important than ever that older people who may be eligible for pension credit apply for it. I recently updated my blog post about pension credit in light of the announcement. If you have older relatives, friends or neighbours, please encourage them to apply if they may be eligible. The application process is not as straightforward as it should be, so they may well appreciate some help with it

Even so, be aware that only the very poorest pensioners qualify for pension credit. If you have any source of income apart from the state pension, even a tiny one, the chances are you won’t be eligible. I do therefore recommend writing to your MP and asking for this Draconian decision to be reversed. You may also like to sign one of the various petitions that have sprung up, including this one on Change.org and this one from Age UK. The latter is up to almost half a million signatures now.

That’s all for now. If you have any comments or queries about this update, as ever, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss. Note also that posts on PAS may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media:

Yes, it’ s time for another exciting giveaway here on Pounds and Sense. This one has a ‘back to school’ theme. In most parts of the UK, of course, this occurs in early September. Scottish schools generally return a bit earlier, around mid-August.

Again I have clubbed together with some of my fellow UK bloggers to provide a plethora of great prizes. And the best news is, it’s entirely free to enter. The giveaway is open now and will close on September 1st 2024.

The prizes have been hand-picked for children and young people returning to school this autumn, so they should be ideal for your children or grandchildren. But if you want to keep any for yourself, we promise we won’t tell!

This event has (again) been organized by Rowena Becker, who blogs at My Balancing Act. No small amount of effort has been involved in arranging and co-ordinating it, so many thanks again to Rowena for her hard work and dedication.

Without further ado, then, I’ll hand you over to Rowena to introduce the giveaway…

Back to School Giveaway

Get ready for an exciting opportunity as some of the top UK bloggers unite to bring you a fantastic back-to-school giveaway! We’ve teamed up to offer one lucky winner a fabulous collection of school essentials that will make heading back to the classroom a breeze.

From stylish lunch bags and durable water bottles, to school shoes and jackets, this giveaway promises to equip you with some great goodies to kick off the school year in style. Join us in this collaborative celebration and enter for your chance to win these amazing prizes. Let’s make this school year the best one yet!

In order to be able to bring you this incredible giveaway, some of the UK’s top bloggers got together. A massive thank you to all involved! The bloggers taking part are:

Start-Rite Shoes is giving one lucky winner the chance to win a pair of school shoes for their child.

The foundation of any school uniform is a quality fitted pair of shoes, but there is nothing uniform about a Start-Rite school shoe! With 12 new styles added to their school shoe collection this season, Start-Rite is more prepared than ever to protect your children’s feet. No one size fits all, as every pair of feet has individual requirements to ensure healthy physical development.

Whether you’re looking to support wide or narrow feet, a high instep, or shoes that double for a special occasion, Start-Rite has a style to suit every child.

EcoSplash Fleece Lined Jacket Navy from Muddy Puddles

Gear up for the ultimate back-to-school season with Muddy Puddles’ in our back-to-school giveaway! Included in the prize bundle is a top-tierkids waterproof jacket that ensures your young adventurers are ready for any weather.

This navy raincoat features an impressive waterproof rating of 10,000mm to keep your child dry during heavy downpours, perfect for rainy days. Crafted from durable, breathable fabric made from recycled plastic bottles, it’s both eco-friendly and long-lasting. The soft fleece lining provides extra warmth, while the jacket’s design makes it easy to layer across various seasons. Fully taped seams offer robust protection against the elements, and reflective details enhance visibility in low-light conditions for added safety. Plus, it’s machine washable at 30 degrees for easy care.

Muddy Puddles has your kids covered for back to school with theirback to school jackets, waterproofs, and more—ensuring every rainy walk to school, puddle-jumping session, and chilly playground adventure is tackled in style and comfort!

Smash lunch bag and water bottle set

Gear up for the school year with an essential lunch bag and water bottle set! TheSmash Lunch Bag is your kids perfect lunchtime companion, designed with full insulation and an antibacterial lining to ensure their meals are as fresh as possible. Made from premium neoprene, this lunch bag is not only fully washable but also brings a splash of personality and fun to every meal.

Stay hydrated in style with theSmash Twin Wall Soda Bottle. Made from durable stainless steel, this sustainable bottle features a sleek design and a removable cap, making it an ideal everyday accessory. It’s BPA-free, food-safe, non-toxic, and offers a smart, twin-walled construction.

Create-a-Space™ Storage Centre from Learning Resources

Introducing a stylish addition to any back-to-school setup: the Create-a-Space™ Storage Centre from Learning Resources, which is part of our exclusive giveaway prize bundle! Perfectly blending modern design with practicality, this white 10-piece set will seamlessly fit into any décor theme, whether at home or in the classroom.

The carousel-style design features 8 removable containers, providing the perfect solution for organising essentials like glue sticks, crayons, pens and more. Keep your workstation clutter-free and enjoy a space that is as functional as it is chic with this versatile storage centre.

LittleLife Flip-Top Water Bottle!

Family active outdoors brand, LittleLife, is giving one person their choice of aflip-top water bottle, perfect for the school day.

Made from impact-resistant Tritan copolyester, a watertight lid and holding 550ml, these bottles are durable and fit fuss-free into your child’s school rucksack or backpack. LittleLife’s water bottles also come with a chew-resistant straw to avoid lingering tastes and odours due to being BPA-free.

Brainstorm Toys Children’s 14cm Desktop World Globe

Discover new horizons with the Brainstorm Toys Children’s 14cm Desktop World Globe, a shining star in our back-to-school giveaway prize bundle! This compact yet high-quality globe is a treasure trove of knowledge, showcasing detailed political boundaries, natural wonders like lakes, rivers, and deserts, as well as capitals and major cities.

Perfect for curious minds, this globe is ideal for home or school, making it a must-have for any aspiring explorer. The sturdy base ensures stability, while its easy rotation allows young adventurers to seamlessly explore different areas of the world. Enhance your child’s learning experience and ignite curiosity with this engaging educational tool.

Little Brian Scribble Paint Sticks

Unleash your creativity withScribble Paint Sticks by Little Brian, a standout addition to our giveaway prize bundle! These innovative paint sticks are perfect for adding intricate details and patterns to your artwork, thanks to their finer tip. Featuring 12 vibrant classic colours, they bring your child’s artistic visions to life with ease. Enjoy a mess-free painting experience where paint twists up and down just like a glue stick and dries in under 60 seconds. Whether you’re working on paper, card, wood, or glass, these versatile paint sticks make it simple to explore your creativity without the clean-up hassle.

How to Enter

You can enter this Back to School Giveaway by completing as many Rafflecopter widget entry options below as you like. All entries will be collated, and one winner will be randomly chosen via Rafflecopter.

The giveaway will run from 4 pm 23rd August 2024 to 8 pm 1st September 2024.

The winner will be notified by email from rowena@mybalancingact.co.uk

The winner will have 7 days to respond, after which time we reserve the right to select an alternative winner.

This prize draw is in no way sponsored, endorsed or administered by, or associated with, Facebook, Instagram, X, YouTube, BlogLovin or Pinterest or any other social media platform.

Prizes open to over 18s only. Age verification may be required to receive some prizes.

Some or all of the prizes may take a few weeks to arrive.

If any prizes are out of stock then we will do our best to find a suitable replacement but cannot guarantee it.

Anyone who unfollows before the giveaway ends or doesn’t complete the required entry action will be disqualified.

The prize is non-transferable, non-refundable and cannot be exchanged for monetary value.

We may be using a parcel service or Royal Mail for some of the prizes and their standard compensation will apply in the event of loss or damage.

Some items may be sent directly by the supplier and we do not have responsibility if these go missing and we cannot replace such items.

In the unlikely event that one of the companies withdraws a prize, we cannot offer an alternative.

The winner’s name will be stated on some or all of our bloggers’ websites and announced on Twitter/X and other social media channels. It will also be displayed on the Rafflecopter entry form. By entering this prize draw, you give your permission for this.

Please note the winner may have the same name as you so if you see your name displayed, be aware that you are not the winner unless you have been notified by us.

There may be some delays in receiving prizes.

Good luck, and I hope a Pounds and Sense reader wins this fabulous prize bundle!

Note: This post (and others on Pounds and Sense) includes affiliate links. If you click through and make a purchase or perform some other specified action, I may receive a commission for introducing you. This will have no effect on the product or service you receive or the price you pay for it, but it does help me pay my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media:

The first budget under new Labour Chancellor Rachel Reeves is scheduled for Wednesday 30 October 2024.

Speculation is rife about potential tax rises aimed at addressing the country’s economic challenges. But while tax increases appear inevitable, there is still time to take proactive steps to minimize their impact on your finances.

Here are some tips for how to prepare for and reduce the burden of potential tax hikes.

1. Maximize Tax-Efficient Savings and Investments

One of the most effective ways to protect yourself from higher taxes is by taking full advantage of tax-efficient savings and investment vehicles. These include:

ISA Allowances: The annual ISA (Individual Savings Account) allowance is currently £20,000. Money saved in an ISA grows tax-free, meaning you won’t pay any income tax, dividend tax or capital gains tax (CGT) on any profits made. As well as Cash ISAs, you can invest in Stocks and Shares ISAs and Innovative Finance ISAs (IFISAs).

Personal Savings Allowance (PSA): Basic rate taxpayers can earn up to £1,000 in savings interest tax-free. Higher rate taxpayers get a reduced allowance of £500.

Starting Rate for Savings: For those with a low overall income, the starting rate for savings can be especially beneficial. If your total income (excluding savings interest) is less than £17,570, you may qualify for the starting rate for savings, which can provide up to an additional £5,000 in tax-free interest. This is discussed in more detail in my recent post How to Maximize Your Tax-Free Savings Interest.

Venture Capital Schemes: For those willing to take more risk, schemes like the Enterprise Investment Scheme (EIS) and Seed Enterprise Investment Scheme (SEIS) offer significant tax reliefs, including income tax relief and capital gains tax exemption on profits.

2. Diversify Your Investments

Diversification remains a cornerstone of sound investment strategy, especially in times of political and economic uncertainty. By spreading your investments across different asset classes – such as equities, bonds and property – you can reduce the risk of any single investment adversely affecting your portfolio. Consider international diversification as well to hedge against possible downturns in the UK economy.

3. Consider Using a ‘Bed and ISA’ Strategy

If you hold a lot of investments outside an ISA or other tax shelter, this can be a good strategy to reduce your tax liability.

Bed-and-ISA involves selling taxable stocks and shares and then repurchasing them within an ISA wrapper. This allows you to transfer investments into a tax-protected environment, where future gains and income will be sheltered from tax. Note that you cannot transfer taxable stocks and shares directly into an ISA, but Bed-and-ISA performs the same function.

On the minus side, Bed-and-ISA may incur some costs in terms of transaction fees and any difference (spread) between selling and buying prices. You may also become liable for CGT if any profits realized exceed your annual tax-free allowance. The long-term benefits can be substantial, however. This applies especially if – as seems likely – tax-free CGT allowances are reduced and the rates payable are increased. Of course, the Conservatives started doing this when they were in power.

4. Rebalance Your Portfolio Towards Tax-Efficient Assets

Different types of investments are subject to different levels of tax. It’s important to rebalance your portfolio to favour assets that could be less impacted by tax hikes.

Dividends: The tax-free dividend allowance for 2024/25 is £500, and anything above this is taxed at rates of 8.75% (basic rate taxpayers), 33.75% (higher rate), and 39.35% (additional rate). If dividend tax rises further, you may want to limit investments in dividend-paying stocks outside of tax-free wrappers like ISAs and pensions (see above).

Capital Gains: The capital gains tax (CGT) allowance has dropped to £3,000 for the 2024/25 tax year, and there are fears it could be cut further. Consider selling assets to crystallize gains while you can still use your allowance, or shift investments into tax-free vehicles like ISAs using the ‘Bed and ISA’ (or ‘Bed and Pension’) strategy discussed above..You can also offset capital gains with capital losses. If you have investments that have performed poorly, selling them to realize a loss can help offset gains elsewhere in your portfolio. Remember that CGT only applies when a profit (or loss) is actually realised.

Bonds: Government and corporate bonds are often seen as lower-risk investments and may be less vulnerable to tax increases than equity income streams. You might want to consider including more bonds in your portfolio.

Commodities: Gold and other commodities have traditionally been seen as a safe haven in times of economic upheaval. There are risks, however, and it’s important to do your own ‘due diligence’ and seek professional advice before going down this route.

5. Use Your Pension Allowance

Pensions are one of the most tax-efficient ways to save for the future. Contributions receive tax relief at your marginal income tax rate, which means for every £100 you contribute, the government effectively adds £20 for basic-rate taxpayers, £40 for higher-rate taxpayers, and £45 for additional-rate taxpayers.

Consider increasing your pension contributions to mitigate the impact of other tax rises. Just be sure to keep within the current £60,000 annual pension contribution limit. Note that for those earning over £260,000 (adjusted income), the tax-free allowance tapers. More info about this can be found on the government website.

If you’re self-employed, consider setting up or increasing contributions to a private pension or Self-Invested Personal Pension (SIPP) to take full advantage of these benefits.

6. Plan for Inheritance Tax (IHT) Rises

Inheritance tax has long been a controversial topic, and it may well increase under the new government. Currently, the IHT threshold is £325,000, with an additional £175,000 allowance if you’re passing your main home to direct descendants. Anything above this is currently taxed at 40%.

To mitigate IHT risks:

Consider making gifts: You can give away up to £3,000 per year tax-free, with additional allowances for wedding gifts and gifts from surplus income. Gifts between spouses are normally exempt from CGT or IHT, allowing you to transfer assets and take advantage of both partners’ allowances.

Set up a trust: Placing assets in a trust may help reduce IHT liabilities.

Life insurance policies: Some people take out policies specifically designed to cover future IHT bills. Always seek professional advice, however, as trusts and insurance policies can be complex.

7. Review Your Income Structure

Reeves may target income tax thresholds and reliefs, particularly for higher earners. Reviewing how your income is structured could help mitigate the impact.

Salary Sacrifice Schemes: Consider participating in salary sacrifice schemes, where you give up part of your salary in exchange for benefits like pension contributions, childcare vouchers, or cycle-to-work schemes. This will reduce your taxable income.

Dividend Income: If you run a business or own shares, taking income as dividends can be more tax-efficient than a salary, particularly if the dividend tax rates remain lower than income tax rates. Any good accountant will be able to advise you.

Spousal Income Splitting: If your spouse is in a lower tax bracket, transferring income-generating assets to them can reduce your overall tax burden. This is particularly useful for rental income or dividends from jointly held investments.

8. Prepare for Property Tax Changes

Property taxes, including stamp duty and council tax, could see reforms or increases. Here’s how to plan.

Bring Forward Property Transactions: If you’re considering buying (or selling) property, it may be wise to do so before any potential stamp duty increases are announced. Locking in current rates could save you significant costs.

Consider Downsizing: If you anticipate increased council tax rates or other property-related taxes, downsizing to a smaller home could reduce your future tax liabilities and lower your overall living costs. And, of course, doing this should release some of the equity in your property, which you can then use to help maintain your standard of living.

9. Enhance Charitable Giving

If Reeves increases income tax or reduces the thresholds for higher tax rates, charitable giving can become a more attractive option.

Gift Aid: Donations made under Gift Aid are tax-efficient, as charities can claim an additional 25% from the government. Higher-rate taxpayers can claim back the difference between the basic rate and higher rate of tax on their donations.

Donor-Advised Funds: These funds allow you to make a charitable contribution, receive an immediate tax deduction, and then recommend grants from the fund over time. It’s a strategic way to manage charitable giving while benefiting from tax relief.

10. Stay Informed and Seek Professional Advice

Tax planning can be complex, especially in an uncertain economic environment. Staying informed about potential changes in the budget and seeking professional financial advice can help you adapt your strategy to minimize your tax liabilities effectively.

Monitor Budget Announcements: Keep an eye on the budget and any subsequent economic statements to understand how proposed changes might affect you. Quick responses can sometimes yield significant tax savings.

Consult a Financial Adviser: A qualified financial adviser can help tailor a tax-efficient strategy to your individual circumstances, taking into account your income, assets, and long-term financial goals.

Closing Thoughts

While tax rises in Rachel Reeves’ first budget may be inevitable, UK residents have various strategies at their disposal to mitigate the impact.

By taking advantage of tax-efficient investments, restructuring income and staying informed, you can protect your wealth and ensure that any tax increases have a minimal effect on your financial well-being. As always, professional advice tailored to your specific situation is invaluable in navigating these changes effectively.

If you have any comments or questions about this post, please do leave them below. But bear in mind that I am not a qualified tax adviser and cannot provide personal financial advice. All investing carries a risk of loss.

If you enjoyed this post, please link to it on your own blog or social media:

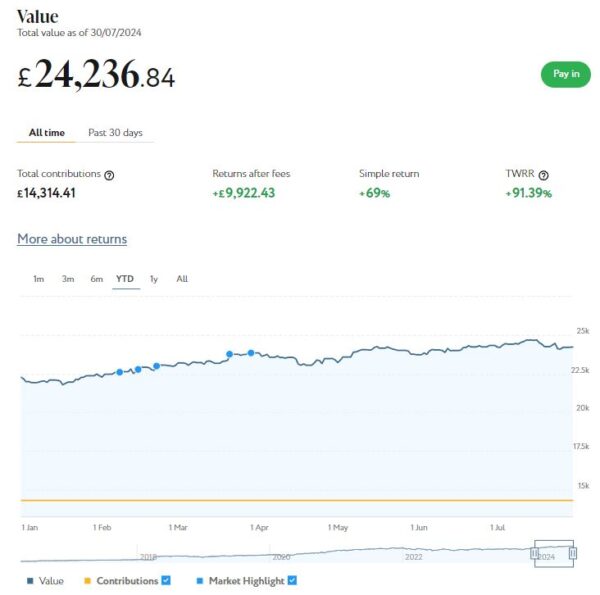

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

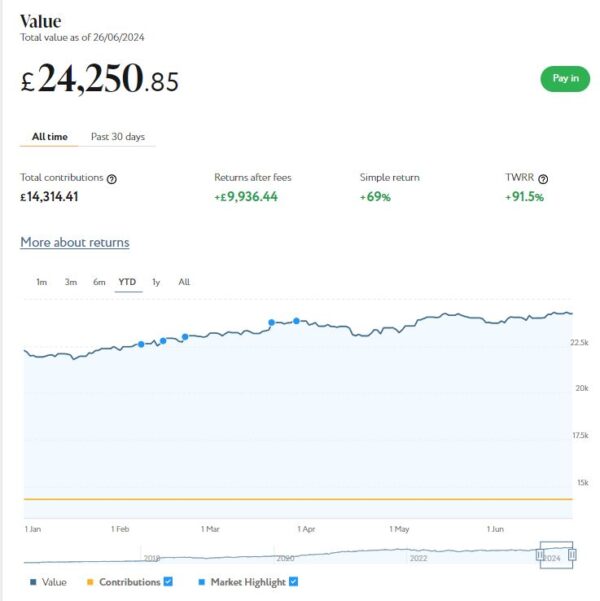

As the screenshot below for the year to date shows, my main Nutmeg portfolio is currently valued at £24,237 (rounded up). Last month it stood at £24,250, so that is a small decrease of £13.

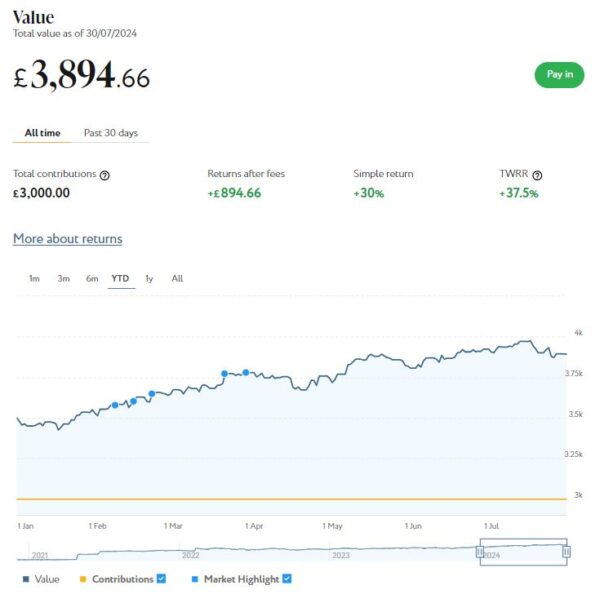

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £3,895 compared with £3,911 a month ago, a fall of £16. Here is a screen capture showing performance over the year to date.

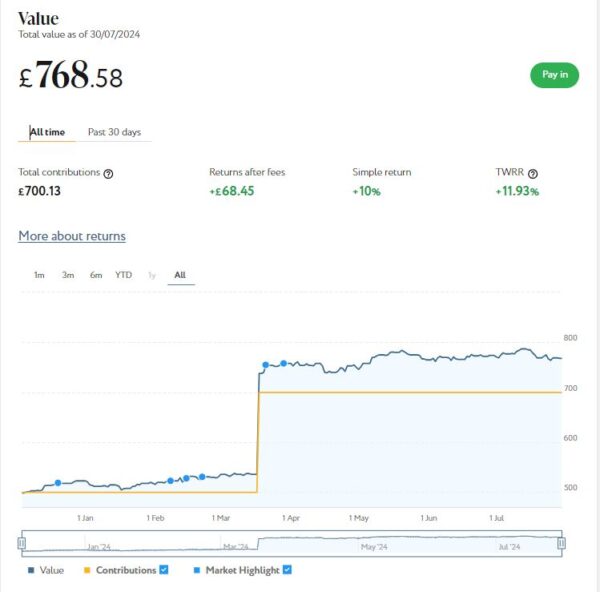

Finally, at the start of December 2023 I invested £500 in one of Nutmeg’s new thematic portfolios (Resource Transformation). In March I also invested a further £200 from ‘Refer a Friend’ bonuses. As you can see from the all-time screen capture below, this portfolio is now worth £769 compared with £772 last month, a small decrease of £3.

As you can see from the charts, July was an up-and-down month for my Nutmeg investments. Their overall value has fallen by a modest £32 or 0.11% since the start of July.

Although any fall is disappointing, short-term ups and downs are very much very much to be expected with stock market investments. And it is worth observing that the overall value of my Nutmeg investments is still up by £2,586 or 9.82% since the start of the year.

You can read my full Nutmeg review here. If you are looking for a home for your annual ISA allowance, based on my overall experience over the last eight years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs), Lifetime ISAs and Junior ISAs as well.

You may like to note that I am no longer an affiliate for Nutmeg. That means you won’t find any affiliate links in my review (or anywhere else on PAS). And you will no longer see the no-fees-for-six-months offer I used to promote as an affiliate. However, the better news is that you can still get six months free of any management fees by registering with Nutmeg via my Refer a Friend link. I will receive a gift voucher if you do this, which is duly appreciated

Don’t forget, also, that the new tax year began on 6 April 2024 and and you have a whole new £20,000 tax-free ISA allowance for 2024/25. In a change to the rules, you can now open any number of ISAs with different providers in the same tax year, as long as you don’t exceed your overall £20,000 allowance. So opening a stocks and shares ISA with Nutmeg won’t prevent you from also opening one with another S&S ISA provider (should you so wish) later in the financial year.

Moving on, I also have investments with the property crowdlending platform Kuflink. They continue to do well, with new projects launching every week. I currently have around £833 invested with them in 7 different projects paying interest rates averaging around 7%. Last month I withdrew £500 from completed loans and now have £40 remaining in my Kuflink cash account.

To date I have never lost any money with Kuflink, though some loan terms have been extended once or twice. On the plus side, when this happens additional interest is paid for the period in question.

There is now an initial minimum investment of £1,000 and a minimum investment per project of £500. Kuflink say they are doing this to streamline their operation and minimize costs. I can understand that, though it does mean that the option to test the water with a small first investment has been removed. It also makes it harder for small investors (like myself) to build a well-diversified portfolio on a limited budget.

One possible way around this is to invest using Kuflink’s Auto/IFISA facility. Your money here is automatically invested across a basket of loans over a period from one to five years. Interest rates range from 7% to around 10%, depending on the length of term you choose. Full up-to-date details can be found on the Kuflink website.

You can invest tax-free in a Kuflink Auto IFISA. Or if you have already used your annual ISA allowance elsewhere, you can invest via a taxable Auto account. You can read my full Kuflink review here if you wish.

Moving on, my Assetz Exchange investments continue to generate steady returns. Regular readers will know that this is a P2P property investment platform focusing on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my AE portfolio has generated a respectable £195.87 in revenue from rental income. As I said in last month’s update, capital growth has slowed, though, in line with UK property values generally.

At the time of writing, 13 of ‘my’ properties are showing gains, 5 are breaking even, and the remaining 15 are showing losses. My portfolio is currently showing a net decrease in value of £28.74, meaning that overall (rental income minus capital value decrease) I am up by £167.13. That’s still a decent return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Assetz Exchange most projects are socially beneficial as well.

The overall fall in capital value of my AE investments is obviously a little disappointing. But it’s important to remember that until/unless I choose to sell the investments in question, it is largely theoretical, based on the most recent price at which shares in the property concerned have changed hands. The rental income, on the other hand, is real money (which in my case I’ve reinvested in other AE projects to further diversify my portfolio).

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of AE as far as i am concerned (especially after Kuflink raised their minimum investment per project to £500). You can actually invest from as little as 80p per property if you really want to proceed cautiously.

As I noted in this recent post, Assetz Exchange is particularly good if you want to compound your returns by reinvesting rental income. This effectively boosts the interest rate you are receiving. Personally, once I have accrued a minimum of £10 in rental payments, I reinvest this money in either a new AE project or one I have already invested in (thus increasing my holding). Over time, even if I don’t invest any more capital, this will ensure my investment with AE grows at an accelerating rate and becomes more diversified as well.

My investment on Assetz Exchange is in the form of an IFISA so there won’t be any tax to pay on profits, dividends or capital gains. I’ve been impressed by my experiences with Assetz Exchange and the returns generated so far, and intend to continue investing with them. You can read my full review of Assetz Exchange here. You can also sign up for an account on Assetz Exchange directly via this link [affiliate]. Note that as from this financial year (2024/25), you can open more than one IFISA per year.

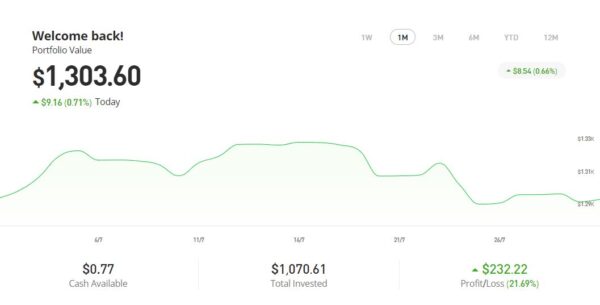

In 2022 I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios, Oil Worldwide. I also invested a small amount I had left over in Tesla shares.

As you can see from the screen captures below, my original investment totalling $1,022.26 is today worth $1,303.60 an overall increase of $281.34 or 27.52%.

As you can see, my Oil WorldWide investment is showing just over 12% profit. That’s okay but not spectacular. Obviously my copy trading investment with Aukie2008 has been doing better. The Oil WorldWide port was recently rebalanced by eToro, so I hope this may boost its performance. The investment team at eToro periodically rebalance all smart portfolios to ensure that the mix of investments remains aligned with the portfolio’s goals, and to take advantage of any new opportunities that may present themselves.

eToro also offer the free eToro Money app. This allows you to deposit money to your eToro account without paying any currency conversion fees, saving you up to £5 for every £1,000 you deposit. You can also use the app to withdraw funds from your eToro account instantly to your bank account. I tried this myself and was impressed with how quickly and seamlessly it worked. You can read my blog post about eToro Money here. Note that it can also serve as a cryptocurrency wallet, allowing you to send and receive crypto from any other wallet address in the world.

I had two more articles published in June on the excellent Mouthy Money website. The first is Seven Ways to Make Money From Your Garden. In this article I set out seven ways you can make money from your garden (if you’re lucky enough to have one). None of these is likely to make you a fortune, but they can all help your finances stretch further in these challenging times.

Also in July I revealed how you can Make a Sideline Income Renting Out Your Driveway. If you have a parking space or driveway that sits empty most of the day, turning it into a source of passive income is easier than you might think. In this article I explained how you can get started and make the most from this opportunity.

As I’ve said before, Mouthy Money is a great resource for anyone interested in money-making and money-saving. From the wide range of articles published in July, I particularly enjoyed Five Ways Tracking Your Spending Can Improve Your Finances by regular MM contributor Shoestring Jane. Jane writes mainly about money saving and frugal living, and this article is a good example of her work. You can see all of Jane’s articles for Mouthy Money via this web page.

I also published several posts on Pounds and Sense in June. Some are no longer relevant due to closing dates having passed, but I have listed the others below.

How to Protect Your Savings and Investments Under a Labour Government was originally written and published before the general election. I revised and updated it after Labour’s widely anticipated victory, but the advice remains largely the same. A significant part of this involves making the most of tax-free opportunities such as ISAs and (to an extent) pensions, but various other methods and strategies are suggested as well. Nothing that has happened since Labour came into power has suggested to me that the advice in the article needs changing.

Also in July I published Ten Tax-Free Ways to Boost Your Finances. As you may have heard, UK citizens currently bear the highest tax burden since WW2. And with the new government looking to raise more money to pay for its ambitious spending plans, there is no sign of that changing any time soon. So in this article I set out some ways you may be able to boost your finances without increasing your tax liability. As you’ll see, doing this needn’t involve complicated investment strategies or seeking ‘loopholes’ in tax law. The article sets out ten perfectly legal ways you can boost your finances without having to worry about the taxman.

Next, a few odds and ends. I recently invested some money (just over £1,000) in a Scottish wind farm project via a platform called Ripple Energy. The way this works is that you pay a one-off fee towards building the wind farm, and in exchange receive lower-cost, ‘green’ electricity once the wind farm is up and running. This will continue for the life of the wind farm (an estimated 20 years). The original closing date for this was the end of May, but the date was extended and the share offer is still open at the time of writing.

If you’re interested in learning more, you can visit the Ripple website via my referral link. If you then decide to invest yourself, you will get a £25 bonus credited to your account when generation starts (and so will I). Note that you will need to invest a minimum of £1,000 to qualify for the £25 bonus, but you can invest from as little as £25 if you like.

Speaking of energy, a quick reminder that if you switch to EDF via my refer-a-friend link (below) you can get a FREE £50 credited to your energy account (and so will I). For more info and to sign up, click on https://edfenergy.com/quote/refer-a-friend/sunny-koala-9462

Finally, I wanted to highlight the decision by the new government to abolish Winter Fuel Payments for all pensioners except those on pension credit. Like many others, I feel this is a terrible decision that will badly impact some of the poorest people in society and quite likely lead to increased deaths by hypothermia in the winter ahead (and others to follow).

it is therefore more important than ever that older people who may be eligible for pension credit apply for it. I recently updated my blog post about pension credit in light of the announcement. If you have older relatives, friends or neighbours, please encourage them to apply if they may be eligible. The application process is not as straightforward as it should be, so they may well appreciate some help with it 🙏

Even so, be aware that only the very poorest pensioners qualify for pension credit. If you get the full state pension and/or a private pension (even just a tiny one) the chances are you won’t be eligible. I do therefore recommend writing to your MP and asking for this Draconian decision to be rescinded. You may also like to sign one of the various petitions that have sprung up, including this one on Change.org and this one from Age UK.

Sorry to end on a downbeat note. At least in this cold, damp, depressing summer we are currently enjoying a few days of warm sunshine, so I hope you have been able to get out and make the most of it. I am sure normal service will be resumed soon!