Today I’m sharing a sideline money-making opportunity that – if you’re in a position to do it – can bring in a steady income for very little effort.

The shortage of parking spaces in many towns and cities has created an opportunity for anyone who has a driveway (or garage) they aren’t using all the time.

One of the best-known operators in this field is JustPark. Through their website and mobile app, they put drivers in touch with home-owners and businesses who have parking spaces (and/or EV charging spaces) available near their destination. They say they help over 10 million drivers a year find parking spaces at over 45,000 UK locations.

Listing your space is free and you can set your own price based on how long the driver wishes to stay. JustPark will suggest an appropriate price based on your location and the facilities you are offering, but you aren’t obliged to accept this.

JustPark charges space-owners a 3% fee on one-off bookings (so if you charge £10 they will take 30p, meaning you receive £9.70). For longer term or rolling bookings over two months, they charge space-owners a higher fee of 20% for the first month, with the fee reverting to the standard 3% after that.

JustPark also make money from drivers, adding up to 25% of the space-owner’s asking price to the fee charged. They say, however, that charges to drivers are still typically 30% lower than ad hoc street parking (if you can find it), which makes the service attractive to motorists as well.

One big attraction of JustPark is that they handle all the admin on your behalf. All payments are made via the website, and space-owners can withdraw earnings via PayPal or direct to their bank account. JustPark also ensure you still get paid even if the booker doesn’t turn up.

JustPark say that the money you earn from renting out your parking space is included in the property trading income allowance introduced by the government in April 2017 – so you can make up to £1,000 per year completely tax-free (and no need to declare it to the taxman).

All drivers using the service have to register on the site, so you know exactly who will be using your space on any given day. There is also a rating system so you can see any comments other users of the service have made about them. Space-owners are also rated by drivers, incidentally.

You can offer spaces by the day, week or month, and set any restrictions you wish on when your space is available. Anyone is welcome to advertise spaces on JustPark, but the locations in most demand are those near airports, stations and stadiums, and in major cities. According to one recent article in the Daily Mail, people in such areas are making more than £4,000 a year doing this. Even if that doesn’t apply to you, though, you can still earn from a few hundred pounds a year to £1000 or more by this means.

Obviously the pandemic and working from home reduced demand for parking spaces. But with life returning to normal now, demand for parking spaces is steadily increasing again.

Of course, if you don’t have a suitable space to offer, you won’t be able to benefit from this opportunity. You could still use JustPark to save money on your own parking costs, though. Either way, the service is well worth checking out 🙂

Another option for cheaper parking is Your Parking Space. Over 60s can get an exclusive 10% discount on this service through my friends at Over 60s Discounts.

Disclosure: As well as being a registered user of JustParkI am an affiliate for them and will therefore receive a small commission if you click through any of my links and sign up. This will not affect the money you earn through the site and/or any savings you make if you use them to find parking spaces.

Cover image by courtesy of BingAI.

This is a fully revised and updated version of my original article on this subject.

If you enjoyed this post, please link to it on your own blog or social media:

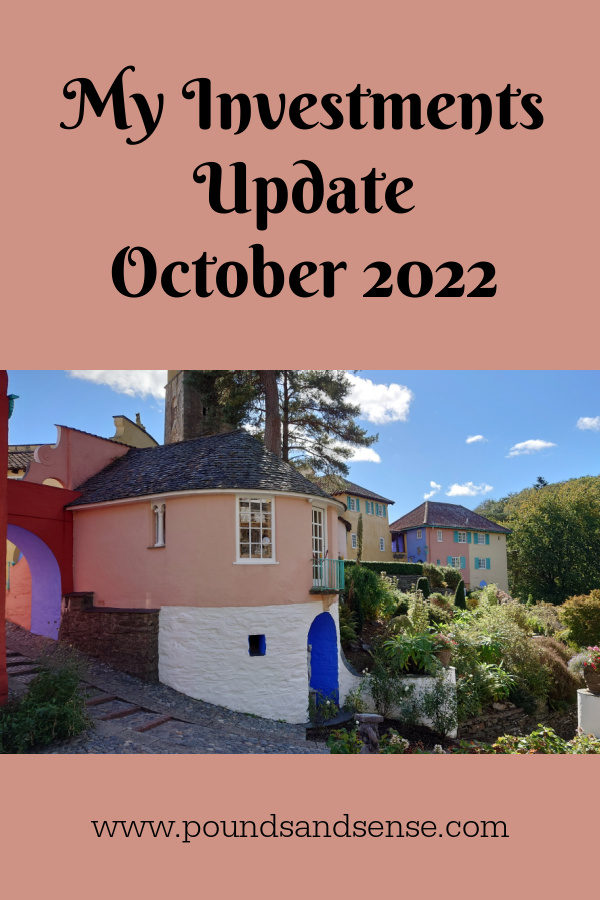

I’ll start as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

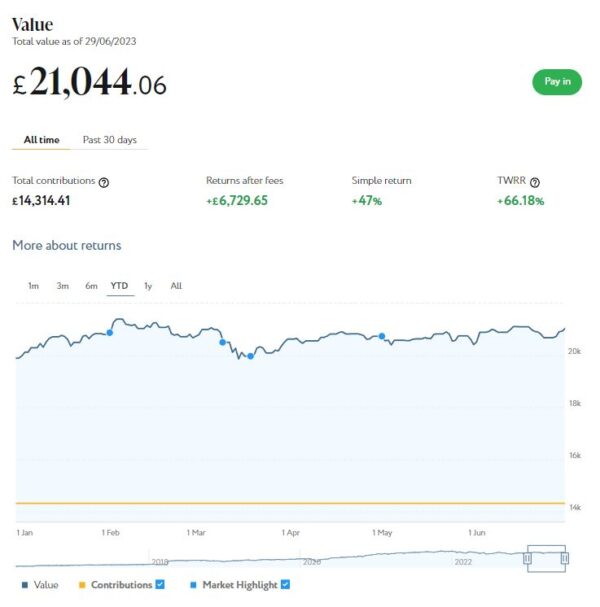

As the screenshot below for the year to date shows, my main Nutmeg portfolio is currently valued at £21,044. Last month it stood at £20,419 so that is a rise of £625.

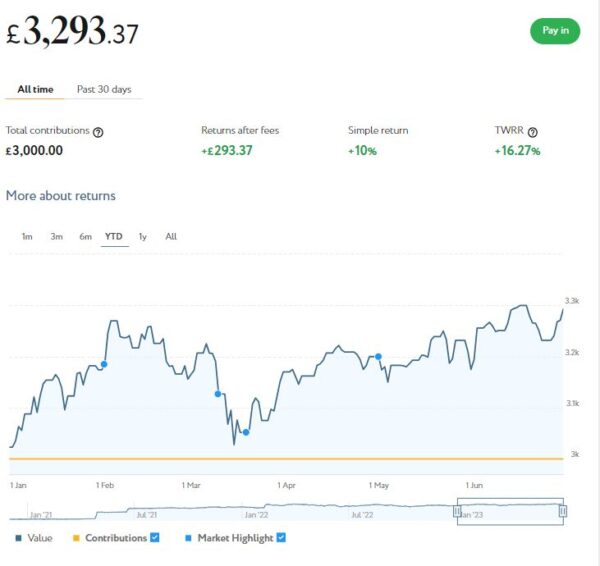

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £3,293 compared with £3,175 a month ago, an increase of £118. Here is a screen capture showing performance since the start of this year.

This has clearly been a better month for both my Nutmeg pots. Their total value has risen by £743 or 3.15% month on month. Since the start of 2023 the net value of my Nutmeg investments has grown by £1,417 or 6.18%.

Of course, all investing is (or should be) a long-term endeavour. Over a period of years stock market investments such as those used by Nutmeg typically produce better returns than cash accounts, often by substantial margins. But there are never any guarantees, and in in the short to medium term at least, losses are always possible.

Also, as you may know, both my Nutmeg pots have quite high risk levels (9/10 main, 5/5 Smart Alpha). If you haven’t yet seen it, you might like to check out my blog post in which I looked at the performance over time of Nutmeg fully managed portfolios at every risk level from 1 to 10 . I was pretty amazed by the difference risk level makes, with higher-risk ports over almost any period of three or more years in the last ten generating significantly better overall returns. If you are investing for the long term (and you almost certainly should be) choosing a hyper-cautious low-risk level might not therefore be the smartest strategy. The one exception is if you plan to withdraw your money soon and don’t want to risk losing too much if there is a sudden downturn.

You can read my full Nutmeg review here (including a special offer at the end for PAS readers). If you are looking for a home for your annual ISA allowance, based on my overall experience over the last seven years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs) and Junior ISAs as well.

Moving on, my Assetz Exchange investments continue to generate steady returns. Regular readers will know that this is a P2P property investment platform focusing on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my AE portfolio has generated a respectable £124.53 in revenue from rental income. As I said in last month’s update, capital growth has slowed, though, in line with UK property values generally.

At the time of writing, 12 of ‘my’ properties are showing gains, 2 are breaking even, and the remaining 12 are showing losses. My portfolio is currently showing a net decrease in value of £15.53, meaning that overall (rental income minus capital value decrease) I am up by £109. That’s still a decent return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Assetz Exchange most projects are socially beneficial as well.

Obviously the fall in capital value of my AE investments is slightly disappointing. But it’s important to bear in mind that unless and until I choose to sell the investments in question, it is largely theoretical. The rental income, on the other hand, is real money (which in my case I have chosen to reinvest in other AE projects to further diversify my portfolio).

I also spoke to the CEO of Assetz Exchange, Peter Read, recently. He made the point that capital values on the platform simply reflect the latest price at which shares in the property concerned have changed hands on their exchange. They do not represent objective or independent valuations of the properties. If you are investing long term with AE, the annual yield from rentals is really a much more important consideration.

Peter also made the point that the current high inflation rate has actually been beneficial for Assetz Exchange investors. That is because properties on the platform generally have an annual review when rentals are increased in line with inflation. That means from the end of the financial year in April, rentals have increased in most cases by around 10%. Assetz Exchange recently published a blog post about this which is worth a read.

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of AE as far as i am concerned. You can actually invest from as little as 80p per property if you really want to proceed cautiously.

Another property platform I have investments with is Kuflink. They continue to do well, with new projects launching every week. I currently have around £2,500 invested with them in 17 different projects. To date I have never lost any money with Kuflink, though some loan terms have been extended once or twice. On the plus side, when this happens additional interest is paid for the period in question.

My loans with Kuflink pay annual interest rates of 6 to 7.5 percent. These days I invest no more than £200 per loan (and often less). That is not because of any issues with Kuflink but more to do with losses of larger amounts on other P2P property platforms in the past. My days of putting four-figure sums into any single property investment are behind me now! Nowadays I mainly opt to reinvest the monthly repayments I receive from Kuflink, which has the effect of boosting the percentage rate of return on the projects in question

Obviously a possible drawback with Kuflink and similar platforms is that your money is tied up in bricks and mortar, so not as easily accessible as cash savings or even (to some extent) shares. They do, however, have a secondary market on which you can offer any loan part for sale (as long as the loan in question is performing and not in arrears). Clearly that does depend on someone else wanting to buy it, but my experience has been that any loan parts offered are typically snapped up very quickly. So if an urgent need arises, withdrawing your money (or part of it) is unlikely to be an issue.

You can read my full Kuflink review here. They offer a variety of investment options, including a tax-free IFISA paying up to 7% interest per year with built-in automatic diversification. Alternatively you can build your own IFISA, with most loans on the platform being IFISA-eligible.

Until 31 July 2023 Kuflink are offering enhanced promotional rates of up to 9.73% (gross annual interest equivalent rate) for their Auto-Invest products (IFISA-eligible). There is limited availability for this offer and it may be withdrawn any time before 31 July 2023 if the limit is reached. For more information, click here [affiliate link].

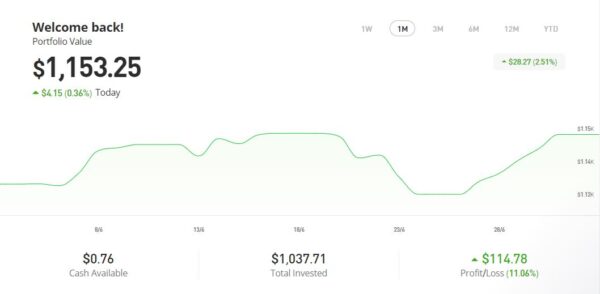

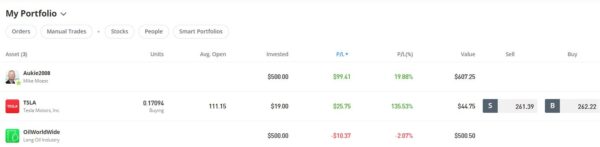

Last year I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios, Oil Worldwide. I also invested a small amount I had left over in Tesla shares.

As you can see from the screen capture below, my original investment of $1,022.26 is today worth $1,153.25, an overall increase of $130.99 or 12.81%. in these turbulent times I am very happy with that.

Since last month the price of my Tesla shares has risen substantially and my copy trading portfolio with Aukie2008 has also done well (though less spectacularly). My most recent investment in Oil Worldwide has risen a bit this month but it’s still slightly down on when I invested. The Oil Worldwide portfolio has just been rebalanced by eToro, so I am hoping for better things in the months ahead

eToro also recently introduced the eToro Money app. This allows you to deposit money to your eToro account without paying any currency conversion fees, saving you up to £5 for every £1,000 you deposit. You can also use the app to withdraw funds from your eToro account instantly to your bank account. I tried this myself recently and was impressed with how quickly and seamlessly it worked. You can read my blog post about eToro Money here.

I had two more articles published in June on the excellent Mouthy Money website. The first was 10 Great Ways to Save Money on Amazon. Amazon is Britain’s – and the world’s – favourite online store. Prices on Amazon are generally competitive, but over the years I’ve discovered a variety of ways to ensure you get the best value for money from them. So in this article I set out my top ten tips for saving money on Amazon

My other article was Do You Need a Personal Financial Adviser? In this article I discuss the different types of financial adviser and what they do. I also revealed why – despite being a money blogger and considering myself reasonably financially savvy – I have a personal financial adviser myself.

As I’ve said before, Mouthy Money is a great resource for anyone interested in money-making and money-saving I always look forward to reading the articles by my fellow contributors. Shoestring Jane is a particular favourite and I enjoyed reading her recent article concerning how you can Save Money by Reducing Food Waste.

I also published several new posts on Pounds and Sense in June. One of these was My Short Break in Bath. Bath is, of course, a historic city on the River Avon, about 12 miles from Bristol. I went there for three days in June, the first time I had been for over 30 years. In my post I discuss the self-catering apartment where I stayed and reveal some of the things I did and saw. I also share a few top tips for visitors to Bath. The cover image shows the famous Pulteney Bridge, one of Bath’s best-known landmarks.

I also published a post based on a survey of Britons’ investing habits. This addressed questions such as what are the main barriers stopping people investing and where do people get their investment advice from. I thought the results were quite eye-opening. Take a look if you haven’t already.

Finally, I wanted to highlight that the free share offers described in last month’s update are both still open if you haven’t done them yet. The opportunity to Get a Free Share Worth up to £100 with Trading 212 was reopened after closing briefly. It is now on offer till 27 July 2023.

The opportunity to Get a Free ETF Share Worth up to £200 with Wealthyhood is also still open but the terms have changed slightly. To remind you, Wealthyhood is a DIY wealth-building app aimed especially at people who are new to stock market investing. As from 1 June 2023 they changed their fee structure to make it (even) more attractive to small investors. They have now increased the minimum investment to qualify for the free share offer from £20 to £50 – but on the plus side, they guarantee that your free ETF share will be worth at least £10.

That’s all for today. I hope you’re enjoying the summer months and taking the opportunity to get out and about in our beautiful country (or further afield).

As always, if you have any comments or queries, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media:

I recently returned from a three-day break in the historic city of Bath. It was the first time in over 30 years I’d been to Bath, so it’s fair to say I was approaching it with fresh eyes!

I stayed in a one-bedroom self-catering apartment in a large multi-occupied property called Elmbrook. This was about twenty minutes’ walk from the centre of Bath. I arranged it through Booking.com. I’ll say a bit more about the apartment below.

For those who don’t know, Bath is on the River Avon, about 12 miles from Bristol. Here is a map of the area from Google Maps…

Accommodation

As mentioned, I stayed in a self-catering apartment in a property called Elmbrook. This was on the Weston Road, a short but pleasant walk from the centre of Bath via the Royal Victoria Park and botanical gardens.

You can read more about where I stayed on this page of the Booking.com website (and see photos). One big attraction for me was that a reserved (and free) off-road parking space was available. In Bath – as in many popular tourist areas – finding somewhere to park can be tricky.

The apartment had a good-sized master bedroom with a comfortable double bed. It had a small but perfectly adequate bathroom with a modern power shower (though, somewhat ironically, no bath). The shower worked well and there was plenty of hot water.

The lounge was quite spacious. It was at the front of the house and had a small patio leading from it. Although I didn’t use the patio during my stay, the patio door provided a quick and convenient method for getting my luggage from and to the car! The lounge had a good-quality flat-screen TV and a DVD player with a small selection of DVDs.

The kitchen was at the back of the apartment and had all the facilities you would need or expect, including a modern electric oven and hob, microwave, toaster, fridge, sink, dishwasher, washing machine, and so forth.

The apartment had central heating on a thermostat, though as it was June I didn’t need this. It had free wifi which worked perfectly during my stay (not always the case in my experience). The location was quiet and peaceful, and I slept very well.

Finally I should say that communication from my Booking.com hosts (Nigel and Alison) was excellent. Nigel sent me detailed instructions about how to get there and how to get in (I used the key safe, though he offered to meet me in person if I preferred). They also left me a welcome letter and a basket of goodies, including a bottle of wine, muesli, milk, ground coffee, and so on. That was a kind gesture and obviously much appreciated.

Financials

As Pounds and Sense is primarily a money blog, I should say a few words about this.

I paid a total of £351 (including VAT) for my three-night visit, which works out to £117 a day. I thought that was very reasonable bearing in mind the high standard of the accommodation and the convenience of the location.

Obviously as it was self-catering no meals were included and neither was there a daily housekeeping visit. But on the plus side, I got a lot more space and facilities than I would have had at a hotel, and complete privacy throughout my stay. I’d have to admit that these days I prefer to go self-catering when possible, even if I do miss hotel breakfasts a bit!

Things to Do

I won’t give you a blow-by-blow account of everything I did on my visit. I will share some highlights and personal recommendations, though.

The first thing I did was book a ticket on the Hop On, Hop Off open-top sightseeing buses. My ticket cost me just under £20 after my over-60s discount and a small reduction for booking online. The most you will pay is £22.50, though.

A ticket allows you unlimited travel on two routes, the City Tour and the Skyline Tour. As you would expect, the City Tour takes you round all the main attractions in or near the centre, including the Royal Crescent, The Circus, Bath Abbey, the Roman Baths, Theatre Royal, and so on. You can listen to a commentary that tells you some interesting facts about Bath and its history. Earphones are provided for no extra charge, and you can choose from ten different languages (including English, naturally!). I found this a great way of getting my bearings.

The Skyline Tour takes you further afield, through some of the beautiful countryside surrounding Bath. It affords some wonderful views over the city, and you get to see a range of other interesting locations, including the university, the American museum and two National Trust parks and gardens. Again, an informative commentary is available. On both tours you can get on or off at any of the stops along the route. It’s worth noting that tickets are nominally valid for 24 hours, but I was told you can use them any time over a two-day period, which potentially makes them even better value. I definitely recommend doing this.

One ‘must see’ attraction in Bath is, of course, the stunning Roman Baths that gave the city its name (see cover photo). They aren’t especially cheap to visit (I paid the discounted price of £25 plus £5 for a guidebook), but are definitely worth it. Collect a free handset as you go in. You can then key in the code numbers displayed around the buildings to hear a commentary about what is on view in any particular area. There is loads to see, so I recommend allowing a couple of hours here at least.

Another top tip for visiting the Baths is to pre-book your ticket. I made the mistake of assuming I could just pay the admission fee and walk in, but that’s not generally the case. To manage numbers, visitors have to book a timed slot. I arrived at about midday but the earliest slot available then was 3.15. So I had to book using my mobile phone and come back later. It wasn’t a problem as there were plenty of other things I wanted to see and do – but if I was going again I’d definitely book my preferred day and time well in advance. Similar advice applies to other popular attractions in Bath, including the Jane Austen Centre and the No. 1 Royal Crescent Museum, incidentally.

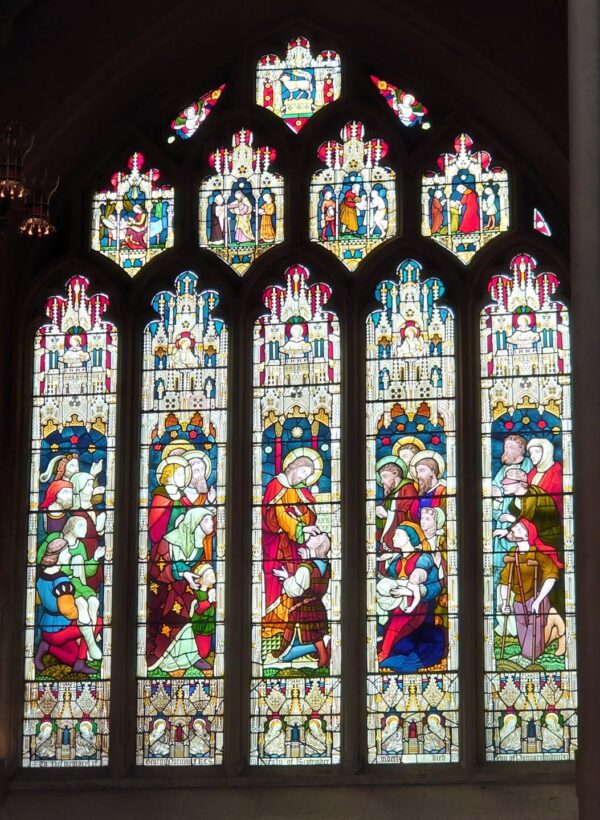

Another place I especially enjoyed visiting was Bath Abbey. This church and one-time Benedictine monastery in the centre of Bath goes back to the 7th century, though it has been rebuilt several times since then. It is a fine example of Gothic Perpendicular architecture and particularly noted for its beautiful fan vaulting (see my photo below). There is an admission fee but it is relatively modest at about £6.50 (no over-60s discount, I’m afraid!).

I visited the Abbey with my old friend Jeff, who lives quite near Bath. We were lucky in that when we arrived a free tour of the Abbey was just about to begin, led by a knowledgeable voiunteer guide. We found this interesting and informative, especially when he explained about the Abbey’s new underfloor heating system, which is powered by heat from the spa water!

There are some lovely – though not especially old – stained glass windows in the Abbey, as the photo below shows. There are also some informative displays and exhibitions, along with a gift shop and (free) toilets.

Here are a few more quick hints and tips for visitors to Bath, based on my experience…

You can download an excellent free map of Bath from this website. I printed this out and found it invaluable for finding my way around.

Be sure to take a few 20p coins with you. Quite a few public conveniences require these 😮

Keep a close eye on your speed if driving around (or towards) Bath. Many of the roads have a low 20 mph limit.

There is also a low emission zone in Bath, though currently charges don’t apply to most private cars and motorbikes.

You can’t actually swim in the Roman Baths, as this is set up as a tourist attraction. There are, though, a few places you can swim in spa water, most notably the Thermae Bath Spa. Be aware this costs a minimum of £40 for a two-hour session.

As mentioned above, I highly recommend pre-booking visits to popular attractions. Not only will this guarantee admission at your preferred time, it may work out a bit cheaper as well.

But don’t miss out, either, on admiring the stunning Georgian architecture of Bath, including the famous Royal Crescent and arguably even more impressive Circus. This is something you can do for free 🙂

As you may gather, I enjoyed my short break in Bath, and am happy to recommend both the city and the accommodation where I stayed for a short break.

Bath is quite compact but there is plenty to see and do. As well as the historical sites, there are lots of charming cafes and coffee shops, and some highly regarded pubs and restaurants. But it can also be a great place to chill out, with lovely green spaces such as the Royal Victoria Park and adjacent botanical gardens (both free to visit). I shall definitely be returning again before too long!

As always, if you have any comments or questions about this post, please do leave them below. Also, if you have visited Bath yourself and have any additional tips or recommendations, I would love to hear them!

If you enjoyed this post, please link to it on your own blog or social media:

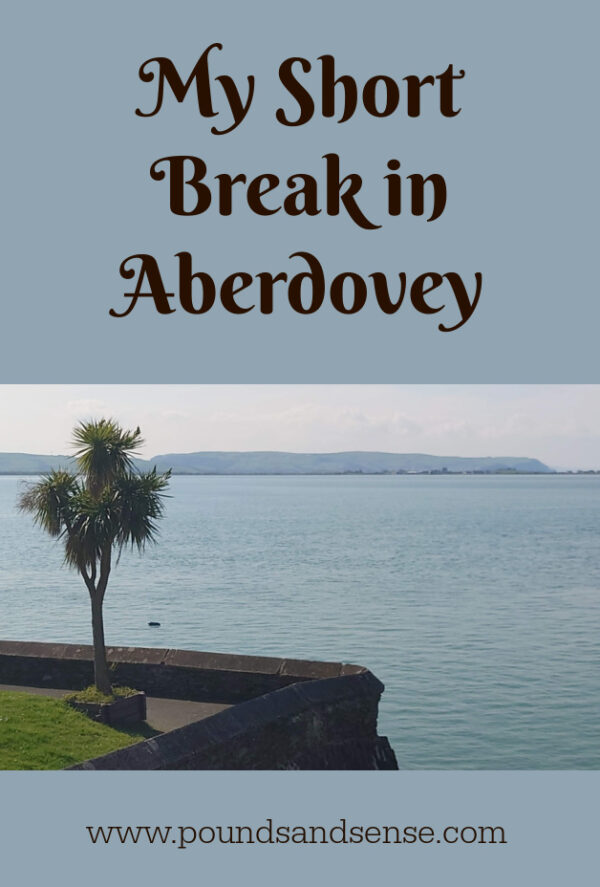

I recently returned from a three-day break in Aberdovey (Aberdyfi in Welsh). This is a small town on the mid-Wales coast. It was the first time I’d been to Aberdovey, though I’d heard good reports about it from friends.

I stayed in a two-bedroom apartment with a wonderful view across the estuary. I booked through Airbnb. I’ll say a bit more about the apartment below.

I should mention that although I travelled (and stayed) on my own, I met up with an old friend from Birmingham there. David recently lost his wife, for whom he had been caring for several years, so I thought he might appreciate a bit of company on his first solo trip away (I enjoyed his company as well, of course). David stayed at a pub/hotel called the Penhelig Arms. He liked it there, though car parking could be a bit of an issue. It appears their car park has been turned into a beer garden!

Aberdovey is about five miles south of Tywyn and 10 miles north of the university town of Aberystwyth. Here is a map of the area from Google Maps…

Accommodation

As mentioned, I stayed at an Airbnb property in Aberdovey. Under Airbnb’s rules I’m not supposed to reveal exactly where it was, but the location was certainly convenient. It was opposite the main car park, beyond which was the sea. The beach was around two minutes’ walk away, and all the restaurants, cafes and shops were within easy walking distance (not that there are very many – Aberdovey is only a small place).

You can read more about where I stayed on this page of the Airbnb website (you can also read my post about booking a holiday with Airbnb here). The apartment had a good-sized master bedroom with a comfortable double bed, and a smaller second bedroom with twin bunk beds. The latter would have been okay for children but adults might find it a bit of a squeeze.

The apartment had a decent-sized bathroom with (unusually these days in my experience) a bath with a shower over it. The shower worked well and there was plenty of hot water. I did try having a bath on my last night and found the taps very stiff, though. Possibly they don’t get used very much! I reported this to the host as I thought she would want to know, but it was no big deal, obviously.

The living room had a stunning view across the estuary (see photo below). It was quite spacious and had a good quality flat-screen TV (though no DVD player). The kitchen area just off the living room had all the facilities you would need/expect, including a toaster, fridge, sink, cooker, dishwasher, and so forth.

The apartment had gas central heating. As it was April I definitely appreciated this in the evenings and early mornings. There was a main thermostat in the living room and all the radiators also had thermostatic valves.

The apartment had free wifi which worked perfectly during my stay (not always the case in my experience). Although central, the location was quiet and peaceful, and I slept very well.

Finally I should say that communication from my Airbnb host (Irene) was excellent. She sent me very detailed instructions about how to get there, where to park, local amenities, and so on. One big plus was that residents in the apartment can use a council parking permit which allows them to park in the car park opposite (and various other places in Abverdovey) free of charge at any time. I left my car in the car park opposite, which was perfect for me.

Financials

As Pounds and Sense is primarily a money blog, I should say a few words about this.

I paid a total of £480 for my three-night stay. This was made up as follows:

£150 x 3 nights = £450

Cleaning fee £30

I was charged an initial deposit of £225, with the balance of £255 taken from my card a fortnight before my visit. The total price worked out to £160 a day. Obviously that’s not cheap but I thought it was reasonable bearing in mind the high standard of the accommodation and the convenience of the location.

Things to Do

As mentioned earlier, on this break I met up with an old friend, David. We spent some of the time together and some separately, which worked out well.

On our first full day we went on the Talyllyn Railway together (see photo below). This is a heritage steam railway that runs inland from the town of Tywyn, a short drive up the coast road from Aberdovey. I last went on the Talyllyn Railway five years ago (as described in this blog post) and was very happy to do so again.

We bought all-day tickets for £25 each and went all the way up the line and back in the morning. We then had lunch (tomato soup and a bread roll, both very good) at the station cafe in Tywyn. After that we travelled part of the way down the line to Dolgoch. Here we disembarked and spent an hour exploring the picturesque woodland with its many streams and waterfalls (see photo below). We then caught the last train back to Tywyn.

On our second full day we did our own thing. I stayed in Aberdovey, had a good wander round and got to know the place a bit better. I particular recommend the Medina Coffee House (picture below), where I went for both morning coffee and afternoon tea. You can sit inside or out here and enjoy a range of drinks, meals and snacks.

David went to Machynlleth, about 15 minutes drive away. Among other things, he visited the Centre for Alternative Technology (CAT). As a retired builder he was very interested to see some of the innovative building techniques being demonstrated here and said he would like to have stayed longer.

I met up with David each evening for a main meal. On two nights we went to the Penhelig Arms where he was staying. They serve traditional pub food, but none the worse for that. Their prices were very reasonable, and David got a 20 percent discount as a hotel resident, which was a nice touch (they also extended the discount to my meals, which was kind of them).

On the other evening we bought fish, chips and mushy peas from Aberdovey’s only chip ship (photo below). This was a stone’s throw from my apartment. We took it back to the apartment and sat watching the sun set over the sea while enjoying our meals. The food, the view and the company were all excellent!

Final Thoughts

As you may gather, I enjoyed my short break in Aberdovey, and am happy to recommend both the town and the accommodation where I stayed for a short break.

Aberdovey is a lovely place to relax and chill out. With its beautiful beach it could also be a good destination for families with young children. Older children and teenagers might find the lack of other entertainments a bit limiting, however. Although it’s not my thing, there are various water sports you can do there, including sailing, canoeing, sailboarding and paddle-boarding. There are also some lovely walks (and cycle rides) from the town.

In addition, the proximity of the Talyllyn Railway, Machynlleth and Aberystwyth offers good opportunities for days out. Aberdovey definitely isn’t a place you would go for the nightlife, though – even the fish-and-chip shop closes at 8 pm!

As always, if you have any comments or questions about this post, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

Today I have a guest post for you about something many of us in icebox Britain would no doubt love to do at the moment.

Buying a Spanish holiday home, both for your own enjoyment and as a potential investment, has many attractions. But there are various important matters to consider before signing on that dotted line.

Learn more below 🏖

If you and your partner have spent many happy years holidaying in Spain, perhaps you’d like to consider investing in a Spanish holiday home?

Not only would a stunning sun-kissed property provide a wonderful place to enjoy your retirement years, but you could also let it out while you are not there and make some additional income. After all, Spain is a highly popular vacation spot with much to recommend it, so you would certainly never be short of guests.

Whatever you would like to use your Spanish holiday property for, there are a few important things you need to be aware of before you start house-hunting on the Costa Blanca…

Many Stunning Locations To Choose From

As you surely already know if you relish a vacation in Spain, the country has a plethora of gorgeous locations to choose from. While on the one hand this is clearly a good thing, on the other, it could make deciding on a particular location rather tricky.

If you’re struggling to settle on one spot, take some time to think about your requirements for the property. For example, if you’re planning to purchase a home solely for your own use, it makes sense to choose a property in a location you particularly love. Alternatively, if you’re buying a home as an investment, you may prefer to think about the locale that draws the biggest number of visitors and has the highest rental prices.

Insurance Is Important

Insuring your Spanish holiday home is of the utmost importance, even if you won’t initially be spending a great deal of time there. After all, you never know what might go wrong – from fire and theft to flood damage or structural damage caused by extreme weather. If you don’t have cover then you could be liable for some truly hefty repair bills.

Fortunately, finding the right holiday home insurance for Spain should be a breeze, thanks to Quotezone.co.uk’s helpful comparison service. You can compare and contrast quotes from a range of UK providers and potentially save yourself a lot of time and money along the way.

You Will Need An NIE

When you buy a property in Spain as a foreigner, you will be required by law to have an NIE number. The authorities will be able to use this number to work out how much tax (if any) you owe each year.

Your NIE number can be applied for at the Spanish Consulate in your country of residence or in Spain itself. You will need to fill out forms and provide various supporting documents. The process can take anywhere between two weeks and two months.

Factor In All The Costs

Before you take the plunge and commit to buying your Spanish holiday home, it’s a good idea to dedicate some time to running through all the potential costs you are likely to incur.

After all, you won’t just be paying the asking price of the home itself. You will also have to pay various associated fees, not to mention mortgage payments, lawyers’ fees and surveyor charges.

There will also be additional annual costs, as you will have to keep the property maintained to a good standard, particularly if you’re letting it out.

To ensure a Spanish holiday home is the right choice for you and won’t prove to be too big a drain on your retirement savings, take some time to pause and reflect on the various costs involved. This will help ensure you choose the option that works best for you.

Thank you to my friends at Quotezone.co.uk for an informative article. If you have ever dreamed of owning a holiday property in Spain, I hope it will give you food for thought.

As always, please feel free to leave any comments or questions below as usual. I would be particularly interested to hear from any readers who have gone ahead and bought a property in Spain or are actively considering it.

This is a collaborative post.

If you enjoyed this post, please link to it on your own blog or social media:

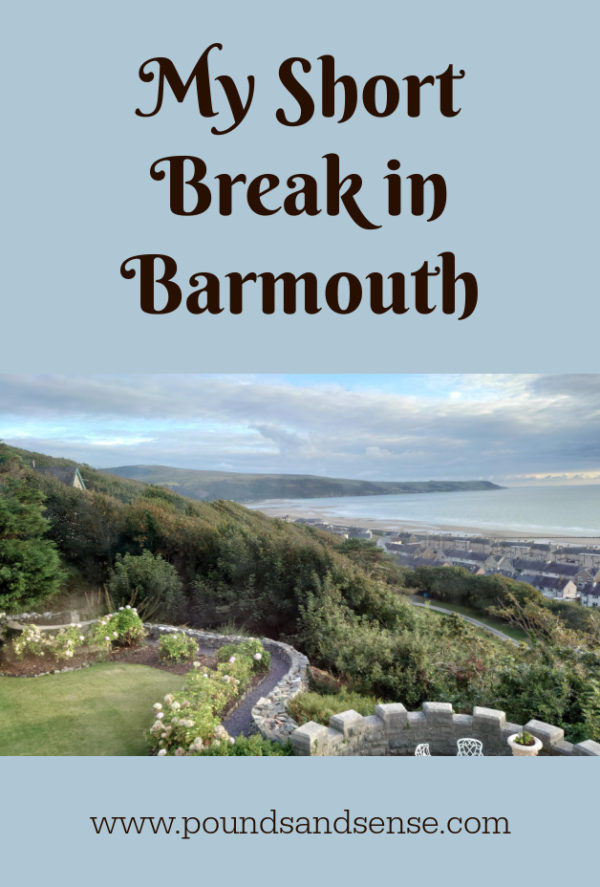

I recently returned from a three-night break in Barmouth in Wales. The town is also known by its Welsh name of Abermaw.

Barmouth is a traditional Welsh seaside resort. I’ve visited a few times over the last few years but haven’t actually stayed there for over 25. I thought it was high time I rectified that!

On this occasion I stayed at Tyr Graig Castle, a hotel I discovered online and booked via Booking.com. I’ll say more about the accommodation below.

Barmouth is about ten miles south of Harlech. The nearest large town is Aberystwyth. Here is a map of the area from Google Maps.

Accommodation

As mentioned above, I stayed at a hotel called Tyr Graig Castle. Unfortunately I neglected to take any photos of the exterior, but you can see the view from my bedroom window in the cover image (including a length of parapet!). There are, of course, more photos on the hotel website.

Tyr Graig Castle is a characterful Victorian building, originally constructed in the late 1890s. it retains the style of the Victorian era, with stained glass windows, wood panelling and highly decorated floors and ceilings.

Tyr Graig is a traditional Welsh name and translates as ‘House on the Rock’. It stands about 200 feet above Barmouth, overlooking Cardigan Bay, across which can be seen the Llyn peninsula and Bardsey Island. The building was completed in 1892 as a family home for W.W. Greener, a famous Birmingham gunsmith. It was designed in the Gothic style that was popular at the time. Its unique shape was chosen by Mr Greener himself. It resembles both a medieval castle and an open double-barrelled shotgun when viewed from above.

I stayed in a first-floor turret room. This had round walls, and windows providing stunning views across the bay. There was a small bathroom with a shower rather than a bath. While generally I found the room perfectly comfortable, I did find the lighting rather dim. There was no ceiling light, just some uplighters on the walls and bedside lamps with low-powered energy-saving bulbs. My eyes are admittedly not the best these days, but I had to use the torch app on my phone in the evening to see well enough to read!

The breakfasts (and optional evening meals) at Tyr Graig Castle are served in the dining room and adjacent conservatory. The latter has wonderful views out to sea and there was a bit of a rush to get one of the four window tables (see photo below). Early risers had a definite advantage here! I was pleased to discover that they recently reinstated the breakfast buffet, where you can help yourself to cereal, fruit, yogurt and so forth. You could then order a cooked breakfast which was brought to your table. These were excellent and set me up for the day 🙂

You could also opt to eat in the restaurant in the evening. Like most guests (as far as I could judge) I chose to do this, as Tyr Graig Castle is a little way out of the town centre and other dining options in the area are limited unless you want to drive. The food was good and the portions were generous. My only slight criticism is that the menu was the same every night. There was a reasonable choice, but a bit more variety day to day (even if just a daily special) would have been appreciated.

The service from both the staff and the charming owners (Mike and Trudy) was uniformly excellent. The hotel had free wifi which worked perfectly during my stay (not always the case in my experience).

One other observation is that this is the first time I had stayed in a hotel – as opposed to self-catering – since the days of the pandemic. I was pleased to discover that by and large things are back to normal now. One small difference is that I was asked at check-in if I wanted my room serviced every day. It was the first time I can remember being asked this, as pre-Covid it would have been assumed. But I guess some people are still nervous about having someone else in their room even if they aren’t there at the time. So I do understand why the hotel ask this now.

Financials

As Pounds and Sense is primarily a money blog, I should say a word about this.

I paid £336 for my three-night stay at Tyr Graig Castle, which works out to £112 per night (including VAT). Considering that included a substantial breakfast as well, I thought the price was very reasonable.

The optional evening meals were, of course, extra. The prices were, I would say, good value as well. I paid around £25 a night for my evening meals, which included a main course and dessert (or cheese and biscuits) and coffee. I generally had a small bottle of sparkling water with the meal, but if I had gone for wine or beer, that would obviously have pushed the price up a bit.

Things to Do

I won’t give you a full account of everything I did while I was there, but here are a few highlights.

Harlech

Harlech is about 20 minutes’ drive north from Barmouth (or a short train journey on the scenic Cambrian line). I spent my first morning here.

Harlech has some charming shops and cafes, and a long, sandy beach. But it is probably best known for its stunning castle (see photo above).

Harlech Castle was built by Edward I during his invasion of Wales between 1282 and 1289. Since then it has had a long and interesting history, including serving as the home and military HQ of Owen Glendower, the Welsh prince who led a long-running war of independence with England during the late Middle Ages. UNESCO considers Harlech Castle, with three others at Beaumaris, Conwy and Caernarfon, to be one of “the finest examples of late 13th century and early 14th century military architecture in Europe”, and it is classed as a World Heritage Site.

Admission to Harlech Castle costs £8.30 for adults or £7.70 for seniors (over 65). You can also buy a family ticket for two adults and up to three children for £27.40. Children under 5 receive free entry, as do people with disabilities and their companions. All prices are correct as at September 2022.

Harlech Castle is impressive and well worth a visit. You can climb the stone staircases in several of the towers and walk along the battlements (obviously you need to be reasonably fit to do this). From up here you can enjoy spectacular views across the sea and towards the mountains of Snowdonia. At ground level there is a room with some information about the castle and its history. I was glad to have this, as the ticket office had run out of guidebooks in English and only Welsh language ones were available.

I should maybe also mention that Harlech Castle has an excellent cafe with plenty of seating inside and out. I enjoyed a very nice cappuccino and cake here!

Portmeirion

Portmeirion is a beautiful Italianate village created by the architect Clough Williams Ellis. These days it is probably best known as the location for the 1960s cult TV series The Prisoner, starring Patrick McGoohan. I drove here in the afternoon after spending the morning in Harlech. It’s a wonderful place to while away a few hours.

There is an admission fee to get into Portmeirion, At the time of writing (September 2022) this is as follows:

Adult £17.00

Concessions £13.50 (this applies to anyone aged 60+ or a student with a valid student ID)

Children £10.00 (5-15 years)

Children (under 5 years) Free

There are also discounted family tickets for various permutations of adults and children.

You can also get free admission (in the afternoon) by booking a minimum two-course lunch at Castell Deudraeth; this is part of the Portmeirion estate, a short walk from the village itself. Free admission to the village is also available if you book a spa treatment or afternoon cream tea there.

More information is available on the Portmeirion website. One thing you may need to know is that they don’t allow dogs (other than guide dogs) into the grounds.

Fairbourne Railway

The Fairbourne Railway is a miniature steam railway. It’s a bit of a drive to get there from Barmouth, as you have to cross the estuary, which entails driving several miles inland and back again. However, you can get a ferry (actually a motorboat) from Barmouth seafront that takes you to the far end of the Fairbourne Railway in under ten minutes. This costs the princely sum of £2.50 (September 2022 price) and provides some wonderful views of Barmouth and the railway bridge. Highly recommended!

If you are energetic you can also walk from Barmouth to Fairbourne via the railway bridge (which isn’t open to cars). On this visit I ended up walking to the Fairbourne Railway and then getting a ferry back.

A one-way trip on the Fairbourne Railway costs £7.60. Alternatively you can buy a Day Rover ticket for £11.50 which entitles you to go up and down the line as many times as you like. This is obviously better value! You can choose whether to travel in an open or closed carriage (it all costs the same). There is a small museum at the Fairbourne end of the line with information about the railway’s history and some exhibits. There is also a separate room housing a large model railway. This is free to enter, but you have to insert a coin to watch the train go round 🙂

The ticket office at Fairbourne incorporates a cafe selling drinks, sandwiches and snacks (no cooked meals though). At the Barmouth Ferry end of the line there is also a cafe but this is only open during the peak summer months.

Final Thoughts

I enjoyed my short break in Barmouth and am happy to recommend both the town and the hotel where I stayed for a short break.

As mentioned above, Barmouth is a traditional Welsh seaside resort, and none the worse for that. It has a clean, attractive promenade and a beautiful sandy beach which goes out a long way to the sea. It is hard to imagine it getting overcrowded!

There is plenty to do for families with children, including a funfair and amusement arcades. There are various restaurants and fast food outlets along the seafront. There is also a railway station with regular trains to Pwllheli in one direction and Aberystwyth and beyond in the other. Road connections are good as well.

Also worth checking out while you are there are Ty Crwn, a 19th century lockup for drunks and petty offenders (picture below). There is also a small museum near the seafront dedicated to the town’s maritime history. Entry to this is free, though donations are appreciated.

Finally, as mentioned above, I recommend taking a stroll across the half-mile-long railway bridge over the Afon Mawddach river. This is the longest timber viaduct in Wales and one of the oldest in regular use in Britain (it opened in 1867). It offers some stunning views across the estuary. You can also walk on to Fairbourne and the Fairbourne Railway (see above).

As always, if you have any comments or questions about this post, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

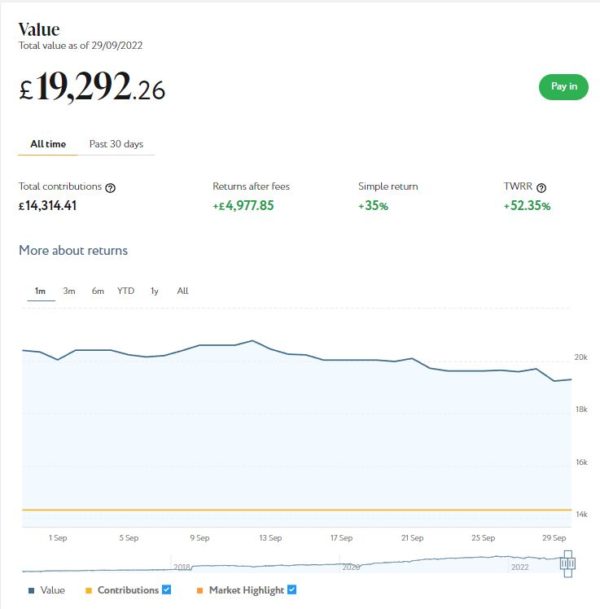

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension). Withdrawals from the latter are still on hold, incidentally, to avert the risk of pound-cost ravaging.

As the screenshot below of performance last month shows, my main portfolio is currently valued at £19,292. Last month it stood at £20,344 so that is a fall of £1,052.

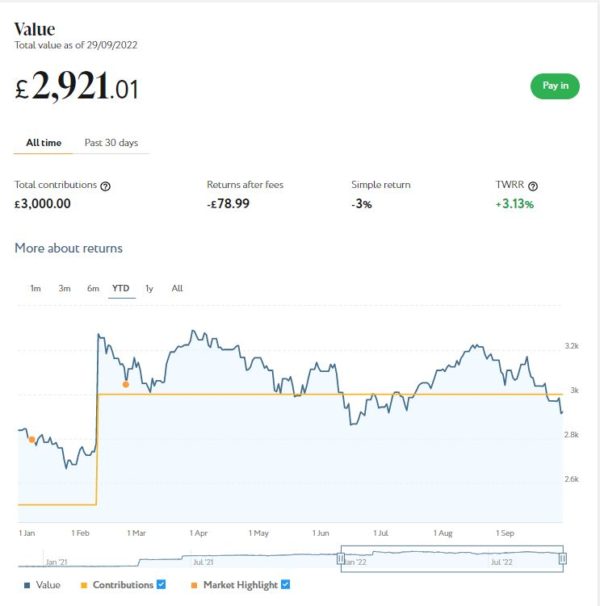

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £2,921 compared with £3,091 a month ago, another fall of £170.

Here is a screen capture showing performance since January 2022. As you can see, I topped up this account in February this year.

There is no denying that these falls are disappointing, especially with my Smart Alpha portfolio now worth less in total than I have contributed to it. As I’ve noted previously on PAS, however, you do have to expect ups and downs with equity-based investments. And this year there has been no lack of volatility, caused by rising inflation, the war in Ukraine and the aftermath of the pandemic (among other things).

About my only consolation is that things could have been even worse if – paradoxically – I’d opted for a lower-risk level with my investments. In their latest blog update, Nutmeg reveal that low and medium-risk portfolios actually performed worse overall last month than high-risk ones. I have copied below their explanation for this:

By design, Nutmeg’s low- and medium-risk portfolios have more exposure through ETFs to assets that are priced in sterling and with limited foreign currency exposure. As you will have seen in the headlines this week, the pound hit an all-time low against the dollar with markets initially placing little faith in the chancellor’s tax-cutting and pro-growth agenda.

This year it has been rewarding to hold foreign currency with sterling particularly weak versus the dollar. Some of our high-risk portfolios have benefited from currency moves, while low- and medium-risk portfolios have not. They haven’t lost money from having low foreign currency exposure, they just haven’t benefited from it.

Secondly, low- and medium-risk portfolios by design have more exposure – again through ETFs – to government bonds, which in ‘normal’ times are considered something of a safe haven and have much lower volatility than equities. After all, it is still highly unlikely that the UK government would default on its debts.

In a nutshell (no pun intended) low- and medium-risk Nutmeg portfolios hold a higher proportion of investments in pounds sterling and UK government bonds. These are normally regarded as lower risk, but last month both took a particular hammering. So in comparison nominally higher-risk portfolios like mine actually performed somewhat better.

This is one more reason I’m glad I opted for higher risk levels with my Nutmeg portfolios (9/10 for my main one and 5/5 for my Smart Alpha). If you haven’t yet seen it, you might also like to check out my blog post in which I looked at the performance over time of Nutmeg fully managed portfolios at every risk level from 1 to 10 . I was actually pretty amazed by the difference risk level makes, with higher-risk ports over almost any period of three or more years in the last ten generating significantly better overall returns. If you are investing for the long term (and you almost certainly should) opting for a hyper-cautious low-risk strategy may not be the smartest thing to do.

Since I started investing with Nutmeg in 2016 – and despite everything that has happened this year – I have still made a total net return on capital of £4,977 (35% or 52.35% time-weighted) on my main portfolio. So I can afford to be philosophical about the recent falls. Indeed, I am considering topping up my Nutmeg investments again now while asset values are depressed.

You can read my full Nutmeg review here (including a special offer at the end for PAS readers). If you are looking for a home for your annual ISA allowance, based on my experience over the last six years, they are certainly worth considering.

Moving on, my Assetz Exchange investments continue to perform well. Regular readers will know that this is a P2P property investment platform focusing on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my AE portfolio has generated £76.51 in revenue from rental and £63.58 in capital growth, a total of £140.09. That’s a decent rate of return on my £1,000 investment and does illustrate the value of P2P property investment for diversifying your portfolio when equity markets are volatile.

I now have investments in 23 different projects and all are performing as expected, generating rental income and in most cases showing a profit on capital as well. So I am very happy with how this investment has been doing. And it doesn’t hurt that most projects are socially beneficial as well.

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of AE as far as i am concerned. You can actually invest from as little as 80p per property if you really want to proceed cautiously.

Another property platform I have investments with is Kuflink. They continue to do well, with new projects launching almost every day. I currently have around £2,500 invested with them in 14 different projects. To date I have never lost any money with Kuflink, though some loan terms have been extended once or twice. On the plus side, when this happens additional interest is paid for the period in question. At present most of my Kuflink loans are performing to schedule, though two recently had their repayment dates put back by three months.

My loans with Kuflink pay annual interest rates of 6 to 7.5 percent. These days I invest no more than £200 per loan (and often less). That is not because of any issues with Kuflink but more to do with losses of larger amounts on other P2P property platforms in the past. My days of putting four-figure sums into any single property investment are behind me now!

Nowadays I mainly opt to reinvest the monthly repayments I receive from Kuflink, which has the effect of boosting the percentage rate of return on the projects in question

Obviously a possible drawback with Kuflink and similar platforms is that your money is tied up in bricks and mortar, so not as easily accessible as cash savings or even (to some extent) shares. They do, however, have a secondary market on which you can offer any loan part for sale (as long as the loan in question is performing and not in arrears). Clearly that does depend on someone else wanting to buy it, but my experience has been that any loan parts offered are typically snapped up very quickly. So if an urgent need arises, withdrawing your money (or part of it) is unlikely to be an issue.

You can read my full Kuflink review here. They offer a variety of investment options, including a tax-free IFISA paying up to 7% interest per year with built-in automatic diversification. Alternatively you can now build your own IFISA, with most loans on the platform (including the one shown above) being IFISA-eligible.

My investment in European crowdlending platform Nibble continues to perform as advertised. My latest investment was in their Legal Strategy. These are loans that are in default and facing legal action. Nibble buy these loans at a heavily discounted rate and then seek to recover as much as possible of the money owed. The minimum investment is 10 euros and the minimum period is six months. I invested 100 euros for 12 months initially at a target annual interest rate of 12.5%.

The Legal Strategy comes with a deposit-back guarantee. This is a guarantee to return the full investment amount at the end of the investment period and a minimum yield of 9% per year. The actual yield depends on how successful recovery efforts prove, so in practice you may end up with a return of anywhere between 9% and 14.5%. All has gone to plan so far, but I will obviously continue to report on this in the months ahead.

Moving on, I had another article published on the always-excellent Mouthy Money website. This one is entitled My Odd Smart Meter Story and Why Despite This I Still Recommend Them. In the article I discuss my rather strange experiences with a smart meter, which stopped working after I switched supplier and then rather mysteriously started again two years later! As per the article title, I do still recommend getting a smart meter, especially in these times of soaring energy bills.

Also in September I enjoyed a final (probably) short break of the year in Barmouth in Wales. I stayed at a Victorian Gothic hotel called Tyr Graig Castle. I was lucky with the weather, and enjoyed visiting nearby Harlech and Portmeirion (see cover image) as well as Barmouth itself.

I shall be publishing a full review of my short break in Barmouth soon. In the meantime, here is a photo of a rather splendid sunset taken from the hotel restaurant…

Finally, I know a lot of people are extremely anxious about the cost-of-living crisis. As I said last time, though, it’s important not to panic. I recommend a three pronged-approach of maximizing your income, minimizing your expenditure, and budgeting carefully (using your resources as effectively as possible, in other words).

Bear in mind, also, that a range of government support measures have been announced to mitigate the worst effects of the crisis. This government Help for Households website has a useful summary of all the help available and is regularly updated.

In the meantime, please do check out some of the other posts on Pounds and Sense for additional advice and resources, especially in the Making Money and Saving Money categories.

That’s all for today. As always, if you have any comments or queries, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media:

I recently returned from a four-night break in Lavenham in Suffolk.

Lavenham is said to be England’s best-preserved medieval town, with over 300 listed, timber-framed houses (see cover image). But I must admit I had never heard of it until I read that my favourite Pink Floyd tribute band, Darkside, were performing there in August. It seemed a great opportunity to see the band and visit somewhere new at the same time. As I live in Staffordshire I normally head west towards Wales for my UK short breaks, so it felt quite strange to be driving east on the A14 instead!

I stayed in a beautiful, self-contained cottage in the heart of Lavenham, which I booked through Airbnb. I’ll say more about the accommodation below.

Lavenham is around five miles north-east of Sudbury. The nearest large town is Bury St Edmunds. Here is a map of the area from Google Maps.

Accommodation

I stayed in a charming, self-catering cottage called The Hay Loft in the centre of Lavenham. It had two bedrooms and bathrooms, so was actually larger than I needed.

I originally booked it so my sister Annie could join me for some of the time. Sadly she broke her wrist in a fall the day before, however, which meant she couldn’t come after all. So I had plenty of room to spread myself out!

This being an Airbnb property, I am not supposed to say exactly where it is, but I guess I can reveal that it’s in a very convenient, central location. There was plenty of free parking on the road outside and in the village itself. The location was quiet and peaceful (in the evenings especially) and I slept well throughout my stay. You can see a photo of the front of the cottage below.

You can read more about the accommodation on this page of the Airbnb website. It had an open-plan lounge/kitchen/dining room on the first floor, and two bedrooms and bathrooms (one ensuite) downstairs. That’s a slightly unusual configuration, but I was actually very grateful for it as my visit coincided with a four-day heatwave. Being downstairs, the bedrooms stayed comfortably cool. Electric fans were thoughtfully provided, though.

The cottage had all the facilities you could want for a short (or longer) stay. The kitchen area was well equipped with a gas cooker, microwave, fridge/freezer, dishwasher, toaster, sink, and so forth.

The cottage had free wifi which worked perfectly during my stay (not always the case in my experience). There was also a small garden at the front, down some steps from the gate. This was well tended and pleasant to sit out in (when it wasn’t too hot!).

Financials

As Pounds and Sense is primarily a money blog, I should say a word about this.

I paid £550 for my four-night stay, which works out to £137.50 per day. I thought that was very reasonable bearing in mind the size and standard of the accommodation and the convenience of the location. Obviously as this was self-catering no meals were included, but there was more space and better facilities than you would get in any comparable hotel or B&B.

Things to Do

I won’t give you a blow-by-blow account of what I did while I was there, but here are a few highlights.

The Guildhall

Lavenham Guildhall is an impressive timber-framed building. It was originally built in the early 16th century for the Guild of Corpus Christi, an alliance of wealthy local merchant families. In later years, as Lavenham’s wool trade declined, it served as a bridewell (prison) and workhouse. More recently in WW2 it housed a social club for American troops and also served as a restaurant around that time.

The Guildhall became the property of the National Trust in 1951 and it was subsequently opened to the public as a local history museum. It has a range of interesting exhibits, though I did find some of the material about the building’s use as a prison and workhouse a little depressing. My favourite room housed an exhibition dedicated to Lavenham in WW2, including posters and other interesting documents from that period.

At one end of The Guildhall, with its own entry from the square, is the National Trust tea-room. This serves the usual range of snacks and light lunches. It also has a very pleasant garden outside. You don’t need to pay for admission to the Guildhall to use the tea room or sit in its garden.

Little Hall

Little Hall is a late 14th century hall house on Lavenham main square. First built in the 1390s as a family house and workplace, it was enlarged, improved and modernised in the mid-1550s, and greatly extended later. By the 1700s it was giving homes to six families. It was restored in the 1920s/30s.

Little Hall was restored by the Gayer-Anderson brothers, who were both soldiers. They filled the house with art and artefacts collected during their extensive travels, many of which can still be seen there. It is privately owned – by a trust, I believe – and open to the public most afternoons for an entry fee of about £5.

I enjoyed visiting Little Hall and hearing about its long and varied history from the volunteer guide. It also has an attractive walled garden. It doesn’t have any refreshment facilities, but then again the Guildhall tea-room is just a stone’s thrown away!

The Church of St Peter and St Paul

My Airbnb hostess Sheila told me that the Church of St Peter and St Paul was a ‘must see’ in Lavenham and she wasn’t wrong. To quote from the Wikipedia article about it, ‘It is a notable wool church and regarded as one of the finest examples of Late Perpendicular Gothic architecture in England.’

When I arrived a service was just ending and there were quite a few people milling around. While it’s obviously a beautiful building, it is also a busy parish church. I enjoyed browsing in the second-hand bookshop and spent some time admiring pictures by local artists in an exhibition by the main door. But what really impressed me most were the magnificent stained glass windows, such as the one below.

Final Thoughts

As you may gather, I enjoyed my short break in Lavenham and am happy to recommend both the village and the accommodation where I stayed for a short break.

Lavenham is a lovely place to relax and chill out. It is full of beautiful, historic buildings to admire (and photograph) and several you can visit to get a sense of the village’s long history.

Of course, my initial reason for going was to see Darkside (pictured at the foot of this post), and that was inevitably a highlight for me. The concert took place in a large marquee (‘Lavenham Air Theatre’) in a field between the church and the local tennis club. It was a magical setting as the sun went down and a full moon appeared in the clear summer sky. And yes, the band did perform the classic Pink Floyd album Dark Side of the Moon!

Although I didn’t eat out in the evenings, there are some highly regarded pubs and restaurants which if I hadn’t been on my own (and staying in a self-catering cottage) I would certainly have tried. I had lunch at the National Trust tea-room at The Guildhall on two days. Another day I had a delicious light lunch at The Nook, a cosy bookshop-cum-cafe just down the road from the church.

There are also some lovely circular walks from Lavenham (ask at the tourist information office near the Guildhall for more details). And a bit further afield there are other National Trust properties such as Melford Hall and Ickworth, and the historic village of Long Melford. Because it was so hot during my stay I didn’t really want to go out in my car (which doesn’t have working aircon). But if – or more likely when – I return, I will certainly explore this beautiful area a little more widely.

As always, if you have any comments or questions about this post, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

I recently returned from a three-night break in Criccieth. This is a village on the Llyn (or Lleyn) Peninsula in NW Wales. It was the first time I had stayed in Criccieth, although I have visited a few times before.

The place I stayed was a self-contained, self-catering apartment facing the sea-front. I booked it using the website Booking.com. I’ll say more about the accommodation below.

Criccieth is by the coast, roughly half way between Porthmadog (home of the Ffestiniog Railway) and Pwllheli (famed for its Butlins camp, now run by Haven Holidays). Here is a map of the area from Google Maps.

Accommodation

As mentioned, I stayed in a self-catering apartment in Criccieth. This was on the second floor, with a view of the sea from the kitchen/lounge. The owners’ name for the apartment is Foel Wen.

The main Criccieth beach was ten minutes’ walk away, but I was happy where I was. It was quiet, there was plenty of free parking on the road outside, and while it wasn’t the most stunning length of beach, there was a small promenade which was pleasant to walk along in the morning or evening. You can see a photo of the beach opposite my apartment below.

You can read more about the accommodation on this page of the Booking.com website. It had a lounge/kitchen at the front, a small bedroom with bunk beds in the middle (which I didn’t use) and the main bedroom at the rear. The bathroom was next to the small bedroom; it was quite compact but fine for a short stay. There was a good-quality modern electric shower but no bath.

The kitchen area was well equipped with an electric cooker, microwave, fridge/freezer, dishwasher, toaster, sink, and so on. On my first and last nights I cooked for myself (Criccieth isn’t exactly crammed with eating places) and on the middle night I got fish, chips and peas from a local takeaway, Castle Fish and Chips, which was excellent 🙂

The apartment had free wifi which worked perfectly during my stay (not always the case in my experience). The location was quiet and peaceful, and I slept very well.

Financials

As Pounds and Sense is primarily a money blog, I should say a word about this.

I paid £355 for my three-night stay, which works out to around £118 per day. I thought that was very reasonable bearing in mind the high standard of the accommodation and the convenience of the location. Obviously as this was self-catering no meals were included, but there was more space and better facilities than you would get in a comparable hotel or B&B.

Things to Do

I won’t give you a blow-by-blow account of what I did while I was there, but here are a few highlights.

Portmeirion

This is about 15 minutes’ drive from Criccieth (or a short train journey to Minffordd and a ten-minute walk). I spent my first morning here.

Portmeirion is a beautiful Italianate village created by the architect Clough Williams Ellis. These days it is probably best known as the location for the 1960s cult TV series The Prisoner, starring Patrick McGoohan. It is a wonderful place to while away a few hours.

There is an admission fee to get into Portmeirion, At the time of writing (July 2022) this is as follows:

Adult £17.00

Concessions £13.50 (this applies to anyone aged 60+ or a student with a valid student ID)

Children £10.00 (5-15 years)

Children (under 5 years) Free

There are also discounted family tickets for various permutations of adults and children.

You can also get free admission (in the afternoon) by booking a minimum two-course lunch at Castell Deudraeth; this is part of the Portmeirion estate, a short walk from the village itself. Free admission to the village is also available if you book a spa treatment or afternoon cream tea there.

More information is available on the Portmeirion website. One thing you may need to know is that they don’t allow dogs (other than guide dogs) into the grounds.

Ffestiniog Railway

This heritage steam railway has two separate lines, both of which run from Porthmadog.

The Welsh Highland Railway takes you on a scenic two-and-a-quarter hour trip through the heart of Snowdonia to Caernarfon, while the original Ffestiniog Railway takes you on a one-hour trip to Blaenau Ffestiniog. On this occasion I took the shorter journey, but I have done the Welsh Highland Railway trip before and highly recommend it as well. You can get more info on both (and book in advance) via the Ffestiniog Railway website.

The harbour station in Porthmadog has a small car park which quickly gets full, but there is a free car park for people travelling on the railway at the back of the public car park opposite (Llyn Bach). I used that myself on this occasion. There were plenty of spaces when I arrived at around 10 a.m. but I noticed it was full later. So my top tip if going by car is to book a ticket on a morning train rather than leaving it until the afternoon!

You can also travel to Porthmadog via the mainline railway if you wish. This is on the beautiful Cambrian Coast line which runs from Pwllheli at one end to Aberdyfi (and beyond) at the other.

Criccieth Castle

My accommodation was literally five minutes walk from Criccieth Castle, so of course I had to pay it a visit.

The castle itself is a ruin but (as the photo shows) plenty of the walls are still standing. There is also a visitor centre where, as well as buying your ticket and guidebook, you can learn more about the history of the castle and see some relics that have been found there.

Arguably the best reason for visiting the castle, though, is the spectacular views. The photo below shows the main Criccieth beach. You can even see as far as Harlech Castle from here, although you might need binoculars!

Final Thoughts

As you may gather, I enjoyed my short break in Criccieth, and am happy to recommend both the village and the accommodation where I stayed for a short break.

Criccieth is a lovely place to relax and chill out. It has excellent road and rail connections, and – as mentioned above – there are also some high-quality tourist attractions nearby.

One thing I really enjoyed about this holiday was the number of casual conversations I struck up with other visitors, staff, locals and so on. This applied especially on my Ffestiniog Railway trip, where I ended up chatting with half the people in my carriage! I’d have to say it did help that only a small minority of people are nowadays wearing face-masks. That human contact is something I missed during the pandemic, and as a solo traveller especially it is great to be able to get back to chatting with strangers again 😀

As always, if you have any comments or questions about this post, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

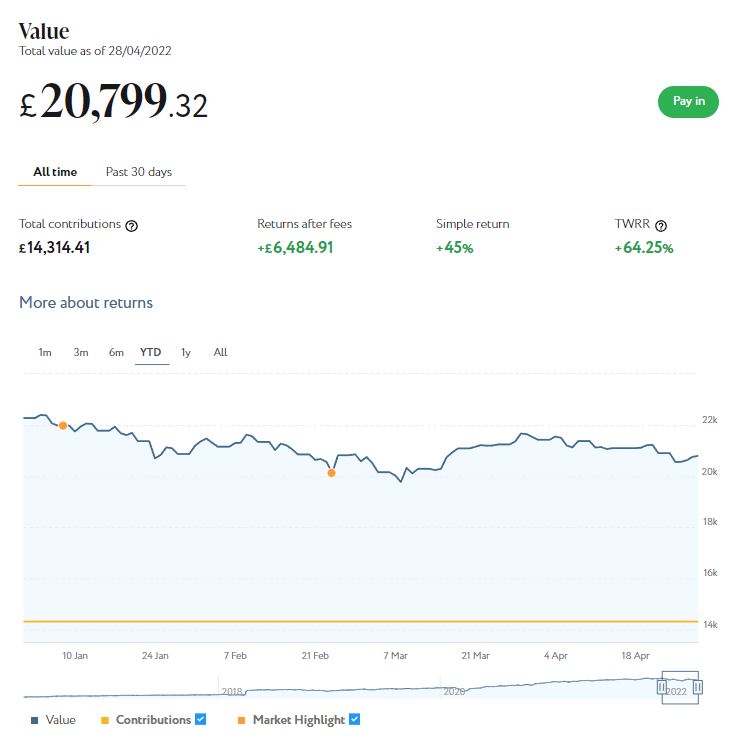

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

As the screenshot below shows, my main portfolio is currently valued at £20,799. Last month it stood at £21,646, so that is a fall of £847.

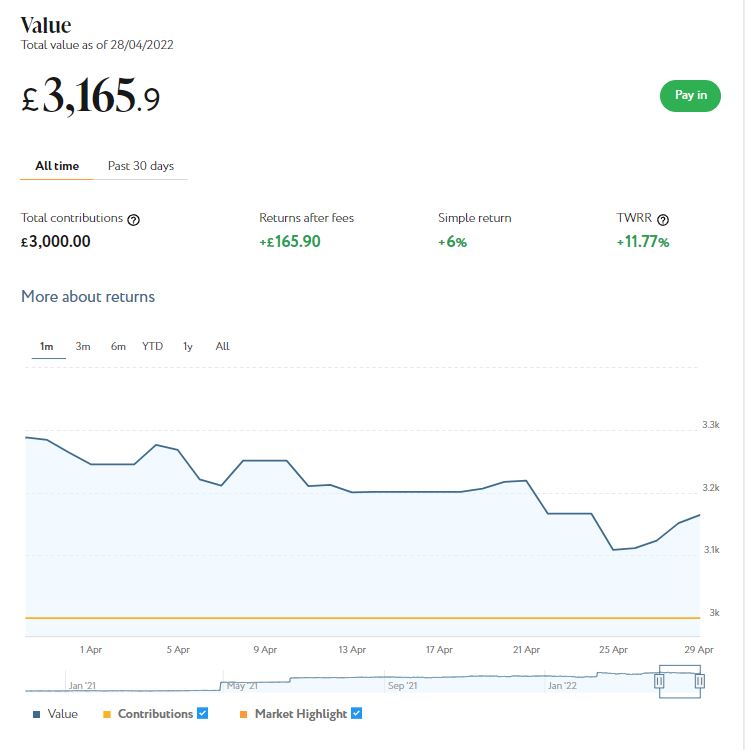

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £3,166 compared with £3,286 last month, a fall of £120

Here is a screen capture showing performance over the last month.

Obviously the falls are disappointing (although they come after broadly similar rises the month before). As I’ve noted previously on PAS, you do have to expect ups and downs with equity-based investments, and certainly over the last few months there has been no shortage of volatility in world markets. And it’s also worth noting that since I started investing with Nutmeg in 2016 I have still enjoyed a total return on my main portfolio of 45% (or 64.25% time-weighted).

I should also mention that I selected quite a high risk level for both my Nutmeg accounts (9/10 for the main one and 5/5 for Smart Alpha). This has served me well generally, but I’m sure investors who selected lower risk levels will have seen smaller falls last month.

If you also have a Nutmeg portfolio and plan to withdraw from it in the next few months, there is certainly a case for switching to a lower risk level right now.

You can read my full Nutmeg review here (including a special offer at the end for PAS readers). If you are looking for a home for your annual ISA allowance, based on my experience over the last six years, they are certainly worth considering.

I won’t go into detail about my Assetz Exchange investments this month. Briefly, though, regular readers will know that this is a P2P property investment platform focusing on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000. Since I opened my account, my AE portfolio has generated £51.50 in revenue from rental and £82.29 in capital growth, a total of £133.79. That’s a decent rate of return on my £1,000 investment and does illustrate the value of P2P property investment for diversifying your portfolio when equity markets are volatile. You can read my full review of Assetz Exchange here. You can also sign up for an account on Assetz Exchange directly via this link [affiliate].

Another property platform I have investments with is Kuflink. They have been doing well recently, with new projects launching almost every day. I currently have over £2,150 invested with them, a significant proportion of which comes from reinvested profits. To date I have never lost any money with Kuflink, although some loan terms have been extended once or twice. On the plus side, when this happens additional interest is paid for the period in question. At present all my Kuflink loans are performing to schedule, with several due to mature in the next few months.

Kuflink recently announced that they were ending their cashback incentive for new members. This used to pay up to £4,000. I know several PAS readers availed themselves of this offer. It’s obviously disappointing it’s now ended, but in a way it’s good news as well. It demonstrates that Kuflink is thriving and they don’t need to offer ‘bribes’ to bring in new investors. As they themselves said in a recent email, ‘We feel now is the right time for us to move away from these campaigns [cashback and refer-a-friend] and utilise the funds within the business to make further enhancements to our products and the platform.’

Even without the cashback incentive, I do still recommend Kuflink and will continue to invest with them. You can read my full Kuflink review here. They offer a variety of investment options, including a tax-free IFISA paying up to 7% interest per year with built-in automatic diversification. Alternatively you can now build your own IFISA, with most loans on the platform being IFISA-eligible.

Another platform in which I have a modest investment is the European crowdlending platform Nibble. This has continued to perform as promised. Several of the loans I invested in have matured and each time I have reinvested the proceeds.

Nibble recently added a new loan category to their offering. This is in the debt collection market; Nibble describe it as their Legal Strategy. This involves investing in loans that are overdue and facing legal action for recovery. Nibble buy these loans at a fraction of their value and then attempt to recover as much of the outstanding debt as possible.

Nibble investors can buy portions of these loans for prices starting at 100 euro (about £84). The company say that investors will receive annual interest rates of between 8 and 14.5% according to how successful their recovery efforts prove. But in any event they offer a ‘buyback guarantee’ that even in the worst case you will receive 8% interest and return of your original investment. I will be trying this out myself soon and also updating my original review, which you can read here if you wish. You can also sign up directly on the Nibble website if you like [affiliate link].