This is the second in a three-part series of collaborative posts about equity release. This article looks at the likely effect of rising interest rates on the equity release market.

The equity release industry is booming. Homeowners from across the UK may find the financial freedom they desire by unlocking one of these attractive products.

If you’re a homeowner over 55 and haven’t heard of equity release, you need to do your research. These products allow you to access cash tied up in your property for any purpose you wish. No tax is payable on this money, and you will never be obliged to move out of your home.

John Lawson from SovereignBoss has done extensive research on the future of the equity release interest rates. He has discovered that after reaching an all-time low in March 2021, equity release interest rates are rising. The big question is, how significant will the rate increase be, and will this have a short-term effect on the industry as a whole? Let’s take a look at what Mr Lawson has to say.

Interest Rate Increase

When interest rates rise, the equity release sector is inevitably impacted as well. In March 2021 interest rates hit a historic low, with some homeowners having the opportunity to unlock equity with fixed rates as low as 2.3%. This unprecedented rate drop was exciting because it wasn’t much more expensive for a homeowner to opt for an equity release than it was to have a traditional mortgage. Plus, with no repayments required in one’s lifetime, retired homeowners could save a fortune by eliminating monthly mortgage payments. (1)

Recently interest rates have increased slightly but are still quite low. Current rates range between 2.9% and 6.4%. The interest rates you achieve will be lender-dependent, but they will also be determined by your age, health condition and property value.

Experts predict that interest rates are set to rise until 2024. And with the latest announcement by the Equity Release Council (see below), now could be the cheapest opportunity to access the cash tied up in your property through an equity release mortgage.

New Compulsory Optional Repayments

In addition to interest rates rising but still being stable, on 31st March 2021, the Equity Release Council enforced guidance on lenders to offer all their lifetime mortgage clients the option for penalty-free voluntary repayments. This means that homeowners can now repay up to 40% of the amount borrowed each year.

The exact offer you receive will depend on the lender you select. But in principle, if you have the means to do so, you could pay off your equity release plan within three to 10 years, restoring your property’s value.

But that’s not all. Once you’ve released equity, there is no risk of foreclosure. You can stop and start making repayments whenever you wish. Voluntary repayments are a great idea if you can afford them, as they reduce the overall cost of your loan by preventing compound interest.

So How Badly Will the Industry Be Affected?

With interest rates still reasonable and the above announcement by the Equity Release Council, the industry is set for another record-breaking year. Eighty percent of experts agree that the industry’s value is rising, and we at Sovereign Boss are excited to see further innovation from lenders and the Equity Release Council.

In Conclusion

Whether now is the best time to opt for an equity release product is very personal. You will need to consult a financial advisor who will help you determine the best course of action for your needs. If it’s in your interest to unlock equity at this stage, however, you’re likely to find a fantastic deal, with product flexibility better than ever.

So, while interest rates are rising, they’re not too much of an issue at this stage. And there is certainly no indication that there will be any short-term impact on the equity release industry. On the contrary, we are set for another record-breaking year.

That being said, it’s too early to predict the long-term impact that interest rates increase will have on the industry. But SovereignBoss considers it their responsibility to keep you updated with the latest industry trends.

This is a collaborative post.

If you enjoyed this post, please link to it on your own blog or social media:

Today I am looking at P2P property investment platform Kuflink.

I have been investing with Kuflink for five years now, so this is a fully updated repost of my original review.

What is Kuflink?

Kuflink is an online platform offering opportunities to invest in loans secured against property. These loans are typically made to developers who require short- to medium-term bridging finance, e.g. to complete a major property renovation project, before refinancing with a commercial mortgage.

Kuflink offer three types of investment, as follows:

Auto Invest and IFISAs both automatically invest your money across a number of loans and pay a fixed interest rate, typically between 7 and 9%. You can choose a 1-year, 2-year or 3-year term, and interest is paid annually (it is automatically reinvested at the end of each year with the two-year and three-year products). The Auto-Invest product is basically the same as the IFISA, but without the tax-free wrapper.

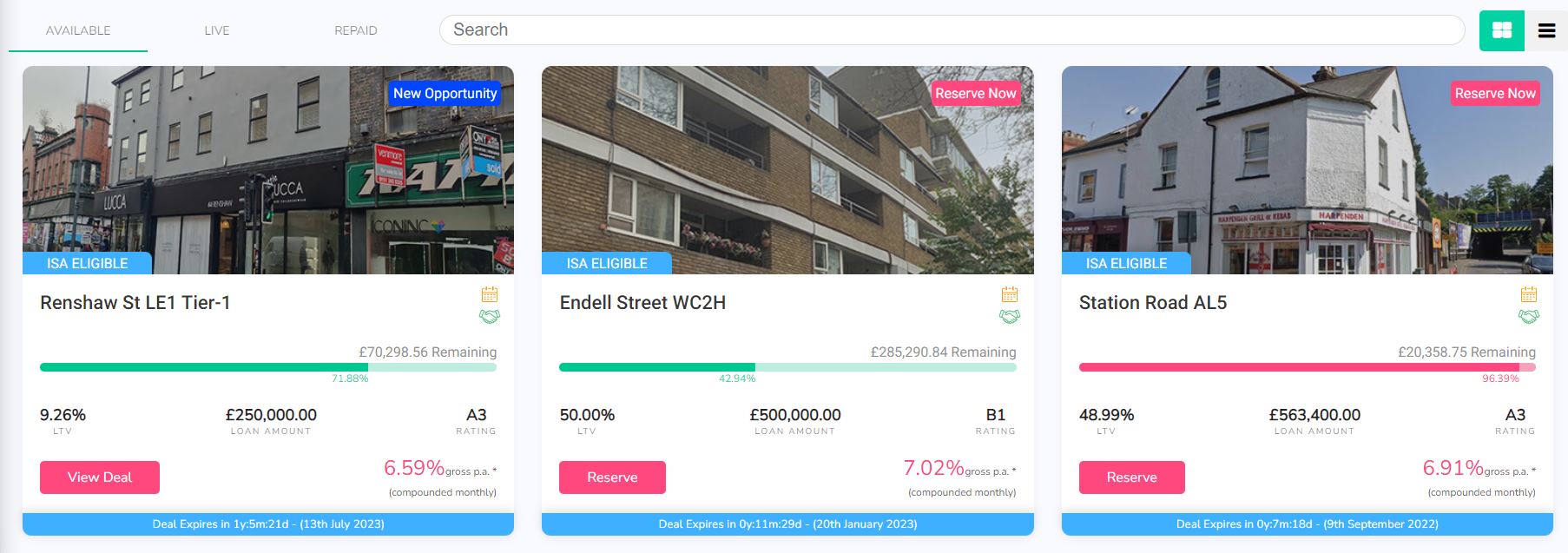

At one time only the Auto-Invest option was available for IFISAs, but nowadays you can choose your own investments if you prefer. The great majority of Self-Select loans on the Kuflink platform are IFISA-eligible. If you check out the Self-Select listings on the Kuflink website (see image below), this will tell you whether any particular loan is IFISA-eligible or not.

Individual Select-Invest loans pay interest rates varying between about 6 and 7.2%, depending largely on the LTV of the loan (loan to value, a measure of how secure the loan would be in the event of a default). The higher the LTV, the riskier the loan, and – other things being equal – the higher the interest rate paid in consequence. You can see a screen capture below of three Select-Invest loans available on the platform at the time of writing.

As a reasonably experienced P2P investor, I put my money into Select-Invest loans. These typically have a duration of six months to a year and (as mentioned above) pay interest from around 6 to 7.20 percent. That obviously isn’t as much as some P2P property platforms (e.g. BLEND), but I think it represents a fair balance between risk and reward. Kuflink also invest in every loan themselves up to 5% of the value of each loan – so, as the expression goes, they have skin in the game.

My Kuflink Review

I found signing up with Kuflink a quick and easy process. They do the obligatory money-laundering checks, but in my case anyway this was all done electronically behind the scenes. I uploaded a copy of my passport and was approved almost immediately. I started by depositing £500, but you can start with as little as £100 if you like.

Initially I put my money into a 12-month loan paying 7% annual interest. One good feature I didn’t grasp initially is that with Select-Invest loans interest is paid monthly. So once a month I receive interest payments on all the loans I am currently invested in. This is paid into a wallet, from which you can either withdraw to your bank account or reinvest.

Kuflink recently introduced an option to have monthly loan repayments automatically reinvested rather than paid into your account as cash. This effectively boosts your interest rate by the power of compounding, as you then receive interest on the reinvested payments as well. Currently this option is available for most, but not all, loans on the platform. You can see which of your loans compounding is available for via your Kuflink dashboard.

I have continued to invest in Kuflink, and have also reinvested in new loans when the original ones were paid off. Another good feature is that money invested in a loan but not yet released to the borrower attracts interest which is paid as cashback once the loan has gone live.

There have been no defaults so far on any of my loans, and Kuflink say on their website that to date nobody has lost a penny on their platform. I have experienced short delays with loans being repaid, but in such cases you continue to earn interest, of course.

Secondary Market

A new feature on Kuflink I like is the Marketplace (secondary market). Here you can buy loan parts from other investors who want to sell up early. You can also put up for sale any (or all) of your own loan parts.

The number of loan parts listed in the Marketplace went up in the early months of the pandemic, as many investors understandably wanted (or needed) to access their cash. This created short-term buying opportunities which I was happy to take advantage of. Loan parts offered via the Marketplace typically have only a few months to run, so you can expect to get your capital back quickly (and can then reinvest it if you wish). Only loans in good standing with monthly repayments up to date may be listed on the Marketplace, so that offers some reassurance against default – though of course it is by no means a guarantee.

In recent months the number of loan parts listed on the Marketplace has reduced considerably. And those that are tend to be snapped up quickly. As a would-be investor this is slightly disappointing, but it does indicate that people are keen to take advantage of the opportunities on offer. It also means that if you want (or need) to exit a loan early, accessing your money should be a quick and easy process.

Pros and Cons

Based on my experiences, here is my list of pros and cons for the Kuflink investment platform.

Pros

1. Easy sign-up process.

2. Low minimum investment.

3. All loans secured against property.

4. Choice of investments and approaches.

5. Manual and auto-invest options.

6. Kuflink invest in all loans themselves, so they have a strong incentive to ensure they are safe and secure.

7. They also cover the first 5% of losses on any loan before investors are affected (although this has never happened yet).

8. Money invested but not yet released to the borrower attracts interest which is paid as cashback once the loan has gone live.

9. In-depth information is provided on the website about all loans, so you can see exactly how your money will be used (and by whom).

10. There have been (according to Kuflink) no investor losses to date.

11. Customer service (in my experience anyway) is fast, friendly and helpful.

12. There is a 14-day cooling off period for new investors.

13. Marketplace (secondary market) for buying and selling loan parts.

14. No charges to investors lending on the primary market and only a 0.25% fee if you resell a loan part on the secondary market.

15. On most loans you can opt to reinvest monthly repayments to boost your net interest rate.

16. Tax-free IFISA option available.

Cons

1. Rates paid aren’t the highest in P2P lending.

2. Delays with some loans being repaid (although investors do earn extra interest if this happens).

3. No mobile app [UPDATE FEB 2023 – An app is now available.]

Conclusion

Overall, my experiences with Kuflink so far have been entirely positive and my investments have been generating the promised returns. I started cautiously with them, but have gradually built up the amount I have invested on the platform. Although – like all property P2P platforms – they were adversely affected by the pandemic, they appear to have come through it strongly, with new loans now being added almost daily.

As mentioned above, although Kuflink don’t pay the highest rates in P2P lending, I think the returns on offer are realistic and sustainable. The steady expansion of the platform seems to testify to this, as does the fact that they have received several industry awards. These include Best Alternative Business Funding Provider in the Business Moneyfacts Awards in both 2018 and 2019 and Best Service From an Alternative Funding Provider in 2020.

Kuflink are also highly rated on the independent TrustPilot website, with an average 4.6 out of 5 (‘Excellent’). At the time of writing 82% of reviewers award them the maximum five-star rating, which is among the highest figures I have seen for a financial services platform.

As with all P2P lending, your money does not enjoy the same level of protection as bank and building society accounts, which are covered (up to £85,000) by the Financial Services Compensation Scheme. Nonetheless, the rates of return on offer are significantly better than those from most financial institutions. And the fact that all loans are secured against bricks and mortar – and Kuflink themselves have cash invested in them – clearly offers some reassurance.

From my experience, Self-Select loans tend to fill up quickly. On the positive side, this shows investors have confidence in Kuflink and want to invest through the platform. On the minus side, it means there are typically no more than two or three new loans open for investment at any time.

Clearly, no-one should put all their spare cash into Kuflink (or any other P2P investment platform). Nonetheless, it is certainly worth considering as part of a diversified portfolio. Not only are the rates of return much higher than those offered by banks and building societies, they are relatively unaffected by ups and downs in the stock market. P2P loans aren’t a way of hedging your equity-based investments directly, but they do help spread the risk.

If you have any comments or questions about this review or Kuflink in general, as always, please do leave them below.

Disclosure: As stated above, I am an investor with Kuflink myself, and if you invest £500 or more via my link above I will receive a bonus for introducing you. Money is at risk. You should always do your own ‘due diligence’ before investing, and seek advice from a qualified financial adviser if in any doubt how best to proceed.

If you enjoyed this post, please link to it on your own blog or social media:

As is customary for bloggers at this time of year, here are the top twenty posts on Pounds and Sense in 2021, based on comments, page-views and social media shares. They are in no particular order. I have excluded any posts that are no longer relevant.

I hope you will enjoy revisiting these posts, or seeing them for the first time if you are new to PAS. Don’t forget, you can always subscribe using the box on the right to be notified of new posts as soon as they appear.

All posts in the list below should open in a new tab/window when you click on the link concerned.

I’ll be taking a break from blogging over the festive period (though I’ll still be around on Twitter and Facebook). I’ll therefore close by wishing you a very merry Christmas (Covid and the government permitting), and for all of us a far better new year 🙂

If you have any comments or questions, of course, feel free to leave them below as usual.

If you enjoyed this post, please link to it on your own blog or social media:

If you like saving money – at this expensive time of the year especially – have you considered shopping at an online auction house?

To be clear, I am not talking about eBay here (much as I love them). Rather I’m talking about more traditional auction houses, who nowadays conduct much or even all of their business online.

An example is Simon Charles. They have four auction centres in the Greater Manchester area and are one of the largest auction houses in Europe. Partly in response to Covid, they now conduct all of their auctions online. Anyone in the UK (or further afield) can therefore bid on them.

Disclosure: I have received assistance with this article from Simon Charles Auctioneers, but don’t have any other connection with them, commercial or otherwise.

Of course, auctions are typically associated with expensive art at one extreme and complete tat at the other. This is not invariably the case, though. While these types of auction houses do exist, there are many that specialize in other areas.

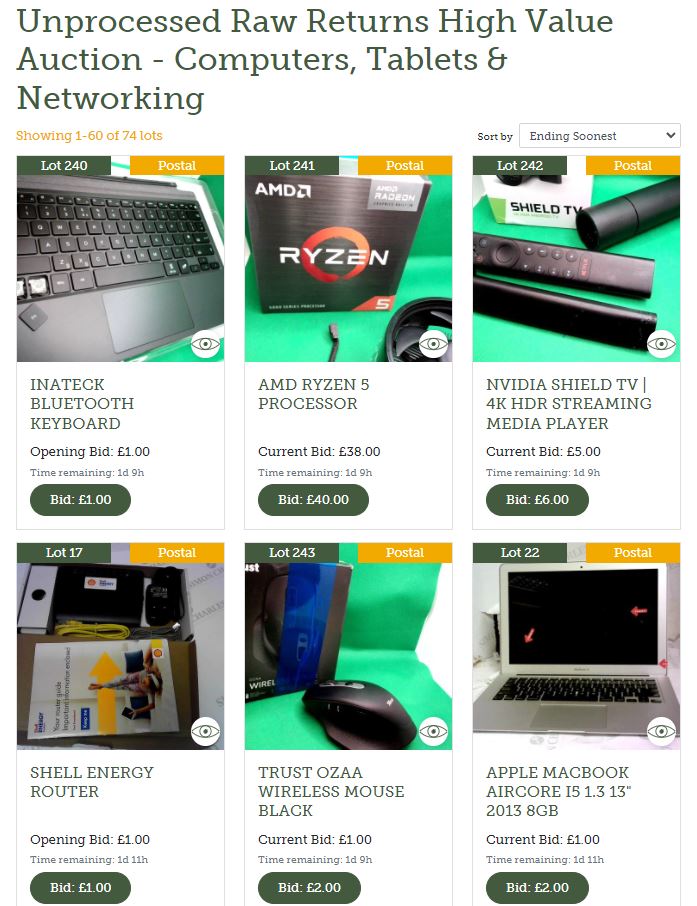

Simon Charles Auctioneers specializes in new, used and returned goods provided to them by high-end retailers. Many of these items are in excellent condition, often still in their original packaging. And with very low or no reserve prices, they can often be snapped up for ridiculously low prices. Here is a screen capture from the Simon Charles website showing some examples…

As you will see, all of the items above have a ‘Postal’ tag at the top right. This means they can be sent by post for a small additional fee. In practice most items sold at SC auctions can be sent by post within the UK. Those that can’t, typically because of their size or weight, are marked for collection only.

In common with other auction houses (and eBay) Simon Charles do impose some additional charges. All lots sold with them are subject to a 18.5% + VAT buyers premium, all lots sold online are subject to 5% + VAT internet fee, and all lots unless otherwise specified are subject to 20% VAT on the hammer price of the item. So it is important to bear these charges in mind when bidding on an item, along with postal costs if you aren’t able to collect your purchase/s in person.

It’s also important to remember that lots sold this way may not be brand new. The products sold at Simon Charles come from high street and online retailers, wholesalers and distributors across the UK. They are in a range of different conditions, from brand new to customer-returned or faulty. They say they don’t always have the chance to test and check items and all products are therefore ‘sold as seen’. But they do have viewing times available to come and check the condition (these times can be found by clicking the Book Viewing button on the auction catalogue or lot page). In these times of Covid, social distancing and masks are required for viewings, which must be booked in advance.

If it’s not possible for you to view in person, they also have an ‘Ask a Question’ feature on each item, so you can gain a better understanding of the product before bidding.

I asked my contact at Simon Charles why they believe buying this way can be better than eBay. Here’s the reply I received: ‘The main benefit of buying from auction over eBay is that our stock tends to be cheaper than eBay. The fact that we’re selling all the stock ourselves means that if you were to buy several lots you could combine shipping, decreasing overall costs. Also, at Simon Charles we work with several large retailers to bring their overstock and returns to auction. These goods aren’t influenced by a price point and can therefore be offered from a much lower amount than someone on eBay might be willing to sell.’

Final Thoughts

I must admit that I had never really thought about buying this way before, but can certainly see the attraction. There are undoubtedly bargains to be had if you are looking for Christmas/birthday gifts or just want to save some money. But I can also see that this method might particularly appeal to small traders looking for stock to resell on market stalls or even on eBay and similar websites. Obviously, if you are a trader registered for VAT, you would be able to reclaim this part of the cost.

In any event, I should like to thank my friends at Simon Charles Auctioneers for bringing this opportunity to my attention. If you have any comments or questions, as always, please do post them below.

If you enjoyed this post, please link to it on your own blog or social media:

Today I am reviewing a children’s book called Grandpa’s Fortune Fables. An ebook copy of this was kindly sent to me by the author, Will Rainey.

Grandpa’s Fortune Fables contains a series of short stories, each following from the last. The central character is a 13-year-old girl called Gail. Over the course of the book she shares a number of lessons she has learned from her Grandpa about money with a boy named Boris (no relation to our PM, I’m sure!).

Boris starts off by bullying Gail, whom he calls a ‘dork’, but she stands up to him and in time they become friends. Gail shares her Grandpa Jack’s money-saving and money-making advice with Boris. He is eager to learn, as his family have always been bad with money.

We learn that Gail’s Grandpa travelled to a (mythical) far-away island, where he learned how to look after his money and became a very wealthy man. Gail has been following his advice and even at her young age is now quite wealthy herself.

Each chapter is essentially a fable illustrating one particular lesson Gail learned from her Grandpa. So one concerns the dangers of Get Rich Quick schemes, another the importance of saving and reinvesting your money, and so on. There are also chapters on the subject of paying tax (‘The Money BIrds’) and the value of donating some of your money to charity.

At the core of Grandpa’s Fortune Fables are three key principles. I hope Will won’t mind if I reproduce them below:

1. Keep one out of every ten seeds you receive 2. Plant the seeds you keep 3. Let your trees GROW

As you may gather, the fables in the book all derive ultimately from the application of these three principles.

Grandpa’s Fortune Fables is designed to teach children about saving, investing and entrepreneurship in an entertaining but informative way (and parents/grandparents may learn some useful lessons too). The stories are all very much of the here and now – even the pandemic and lockdowns get a brief mention (to illustrate how unforeseen events can impact upon specific investments). It’s all very cleverly written, with some charming cartoon-style illustrations as well (see example below).

In my view Grandpa’s Fortune Fables would make a great Christmas/birthday gift for any child aged around 8 to 12 (it could also work for younger and older children). I like how each chapter ends with questions to provoke further thought and discussion. In addition, by correctly answering the multiple-choice questions in each chapter, a letter is revealed. If the child gets all the letters right, they spell out a message which can win them a prize. This is a great idea and a good incentive for reading every chapter (not that such an incentive would likely be needed).

Grandpa’s Fortune Fables is available in print or e-book versions from Amazon (just click on any of the links in this review), or you can order it from any good bookshop. At the time of writing the price is £9.99 for the print version or £3.99 for the e-book. I note that this title is currently number one on Amazon’s best-seller list for children’s books about money and saving, which doesn’t surprise me at all.

Thanks again to Will Rainey for sending me a review copy of his excellent book. If you have any comments or questions – for me or for Will – please do post them below.

Disclosure: As mentioned above, I received a free ebook version of Grandpa’s Fortune Fables for review purposes. In addition, this review includes Amazon affiliate links. If you click through to Amazon and make a purchase, I will receive a small commission for introducing you. This will not affect the price you pay or the product/service you receive.

If you enjoyed this post, please link to it on your own blog or social media:

Although the pandemic is now largely behind us, many of us are seeing bills rise as a consequence of lockdowns and other government measures, world-wide supply chain issues, gas/electricity and petrol price rises, the war in Ukraine, and so forth.

So today I thought I would set out some ways you may be able to make a few pounds extra to help defray the rising cost of living. None of these is likely to make you a fortune, but together they can certainly help keep your bank balance ticking over.

I have linked to relevant posts on Pounds and Sense for further information where appropriate. I have direct experience of all the methods set out below and therefore know that they work and are not scams.

1. Prolific Academic

Prolific Academic is a platform used by academic researchers world-wide to recruit participants for online studies/surveys. These are varied and often surprisingly interesting. They require anything from two minutes to an hour to complete, with payments based on how long (on average) they take. I’ve earned almost £400 to date from Prolific. For more information, see my blog post Make Money and Help Academic Researchers With Prolific Academic.

2. MobileXpression

If you have a smartphone, this is an easy way to make money from it. Just install this app (which tracks your browsing anonymously) and every few weeks you will receive a £20 Amazon voucher for your trouble (Amazon vouchers are pretty much as good as money, as you can of course buy almost anything there). You can read my full review of the MobileXpression app in this post.

3. Shop and Scan

Shop and Scan is a market research programme run by Kantar Worldpanel. Anyone can apply to become a panelist, and when you are accepted (which may be immediate or after a few weeks) you receive a barcode scanner and guidebook in the post. You are then required to scan all your shopping when you bring it home (or it’s delivered) and scan and submit your receipts..For doing this you get points. When you have enough, these can be converted into vouchers for a wide range of online stores (again, I normally pick Amazon). You can earn extra points by performing other tasks such as completing online questionnaires, so it doesn’t take long to earn enough points for a £10 voucher. For more information, see my blog post Make Money From Your Shopping With ShopandScan.

4. The Viewers

The Viewers is another market research company always looking for new members for its (paid) audience panel. As the name suggests, they research people’s TV viewing habits via surveys and focus groups. They pay participants in cash (via PayPal) or Amazon vouchers. They run ‘real world’ focus groups in large cities, and online studies of various types. For more information, see my blog post Make Money Watching TV With The Viewers.

5. People for Research

This is another opportunity to make money taking part in consumer research. People for Research are constantly recruiting people to take part in studies. Some of these take place in large cities (London and Bristol especially) but many are done remotely via the phone or the internet. The studies cover a huge range of topics and are for the most part interesting and enjoyable. But the best thing is that they are fairly (and sometimes generously) recompensed – usually in cash, though sometimes Amazon vouchers. For more information, see my blog post Earn a Sideline Income with People for Research.

6. Populus Live

Populus Live is a survey website that wants your opinions and pays cash for them. You can sign up free of charge and will then receive email notifications any time they have a survey you may be eligible for. Each survey is worth a set number of points. Once you have accrued 50 points you will be paid £50 (each point is worth £1, in other words). Admittedly it can take a little while to reach the payment threshold, but £50 is undoubtedly a useful sum to have when you receive it. For more information, see my blog post Make Extra Money From Populus Live.

7. Selling on eBay

One great way to generate some extra cash is to have a clear-out of things you no longer need and put them up for sale on eBay. All sorts of things sell here, and if you have never tried selling via the site you will be pleasantly surprised by how easy it is. What’s more, as long as you are selling your own possessions (and not buying stuff to resell) it’s tax-free too. For more tips about this, see Twelve Top Tips for Selling on eBay, a guest post on PAS by my money blogging colleague Luci Olivia.

8. Matched Betting

In the last year or two matched betting has undoubtedly become harder, partly due to the pandemic and partly to bookmakers becoming less generous with their offers. If you haven’t yet tried matched betting, though, there is still money to be made.

For those who don’t know, matched betting involves taking advantage of online bookmaker offers (especially welcome offers) to generate a guaranteed profit. It is emphatically not the same as gambling (which I don’t recommend at all). As per my blog post Can You Make Money from Matched Betting? if you are new to this field I recommend starting with the matched betting support and advisory service Outplayed [referral link] previously called Profit Accumulator. You can earn up to £45 (tax free) by taking advantage of the offers available to free members. You could then leave it at that or sign up as a full member with unlimited profit potential.

9. Trading 212

This online share trading platform is offering anyone who signs up and deposits a minimum of £1 a free share. This is chosen at random but could be worth up to £100. You can sell this after three days if you wish and withdraw the proceeds (including your initial deposit) after 30 days. I got a share in Ford Motor Company which was worth about £8. Obviously this wasn’t as exciting as I might have hoped, but it was still – in effect – free money for almost no time or effort. And, who knows, the value of my share could skyrocket in future if the ‘internal combustion engine’ really catches on 😉 For more information on Trading 212, including how to get your free share, see my blog post Get a Free Share Worth Up to £100 With Trading 212. Note that the current free share offer closes on 8 June 2023.

Most of us have old gadgets we no longer use that are just gathering dust. They include mobile phones, tablets, laptops, cameras, games consoles, and even desktop computers. They may still work, but we have replaced them with new and (hopefully) better products. If that sounds like you, there are lots of ways you can make money from your old tech, even if (in many cases) it doesn’t work any more. Check out my blog post How to Make Money From Your Old Tech for a range of methods for doing this.

11. Freelance Writing

This is a subject close to my heart, as for many years I was a full-time freelance writer (I’m semi-retired now). It’s a competitive field, but there is still lots of money to be made. You don’t need to be Shakespeare either, just have a reasonable grasp of written English and be willing and able to write what the market wants. Check out my blog post My Top Ten Tips for Making Money as a Freelance Writer here. You can also read my posts Should You Write a Book? and How to Publish Your Own E-book on Kindle.

12. Cashback Websites

I’ve mentioned cashback sites a few times on PAS. These are sites such as Top Cashback and Quidco, where any time you make a purchase with a certain online store, if you go via the cashback site, you get some money refunded to your account. Obviously you aren’t actually making money in this case – but if you were going to make the purchase anyway you get some money back, and over time this can add up to a tidy sum. In addition, there are some offers listed on the sites where you can get ‘cashback’ without actually making a purchase. For more information, see my blog posts Save Money With Cashback Sites and Six Ways to Make Money With Cashback Sites. You may also like to check out my recent posts about Cashback Angel, a cashback site comparison service, and My Money Pocket, a new and upcoming cashback site.

13. Comping

Okay, comping, or entering consumer competitions, isn’t a guaranteed way of making a sideline income. Nonetheless, there are stacks of cash and prizes on offer at any time, and somebody has to win them. There’s no reason it couldn’t be you! There are lots that you can enter online – just check out competition listing website Loquax, for example. For hints and tips on getting started, see How to Win Cash and Prizes in Consumer Competitions, a guest post on PAS by Cora Harrison. I also highly recommend the book Superlucky Secrets by my UK blogging colleague Di Coke (also known as Superlucky Di). You can read my review of this in-depth guide to comping here.

14. Free Online Lotteries

This is obviously another opportunity where returns are not guaranteed. Nonetheless, there are various online lotteries you can enter free with a chance of winning (in most cases) cash prizes. Typically you have to return to the lottery site every day to see if you are a winner. My favourite such site is Pick My Postcode [referral link]. This site offers multiple chances to win every day, with prizes ranging from £10 to over £1,000. I have a particular soft spot for PMP, as back in the days when it was called Free Postcode Lottery, I was lucky enough to win £614.53 on it. You can learn more in my blog post titled How to Cash in on Free Lottery Websites.

I make money this way, and there’s no reason you couldn’t as well. Blogging is by no means a get-rich-quick opportunity. But if you are prepared to put some time and effort in, the rewards will come. You can blog about any subject you like (though some subjects are easier to make money from than others). Once your blog is up and running you can earn from it in various ways, including advertising, affiliate marketing, sponsored posts, and so on. To get an idea how this works, check out this guest post by Ruth Hinds titled Five Things You Really Need to Know About How to Make Money from Blogging. In addition, my UK blogging colleague Emma Drew has an excellent course about making money from blogging called Turn Your Dreams Into Money, which i reviewed here.

17. Online Design and Print

This is a great home-based sideline earning opportunity. No special skills are needed beyond a little imagination; although if you do have art and design skills, so much the better. I’m talking here about designing and selling clothes and other products, from tee-shirts to tote bags, hoodies to coffee mugs. By designing I mean coming up with slogans and/or graphics to adorn these products that will appeal to a particular target market. This opportunity has been opened up by web-based companies such as TeeMill that allow you to design and sell your products online. They provide all the back-end services, including taking payments and fulfilling orders. They charge you a set fee for this, which is covered from the fee paid by your customer. You charge your customers a bit more, and your profit is (of course) the difference between the two. For more information, see my blog post How to Make Money with Online Design and Print.

18. Virtual Assistant Work

There is a steady demand for virtual assistants who can perform a wide variety of tasks from home via the internet. The sorts of things VAs do may include research, writing, proofreading and editing, graphic design, publicity, data entry, programming and other technical tasks, and much more. Social media management is another very popular area. You can read my in-depth blog post on how to make money as a virtual assistant here.

19. Fiverr.com

As you may know, Fiverr is US-based site that lets anyone advertise ‘gigs’ they are willing to perform for five dollars (hence the name, of course). Gigs range from the serious (e.g. write a press release) to the creative (e.g. write a customized solo piano track) to the downright quirky (e.g. write a message, name or URL in chocolate). Most gigs are services delivered electronically, though there is nothing to stop you selling physical products if you wish (you can charge extra for postage). Obviously $5 isn’t a lot, but if you can perform your gig in just a few minutes it can still work out as a decent hourly rate. It’s also possible to charge additional amounts for ‘extras’ such as rapid delivery or upgraded features. See my blog post How to Make Money on Fiverr for much more information about this.

20. Investing for Income

This is obviously a different take from the preceding ideas. If you have money in the bank earning a derisory rate of interest (or nothing at all), however, you might like to consider investing some to provide an additional income stream for you.

This is obviously a huge subject and I can’t go into detail about it here. There are lots of possibilities, though. One would be to invest some of your money in dividend-paying shares. This subject was covered in an excellent guest post for my blog by Lewys Lew titled How to invest For Income From High Yield Share Dividends.

Of course, you should research any possible investment carefully and be prepared to lose money in the short term at least (see below). Note also that some companies – e.g. the big banks and oil companies – cut their dividends during the Covid crisis, so it’s important to pick your sectors carefully.

Regular readers will know I am also a big fan of the robo-adviser investment platform Nutmeg. They are primarily aimed at helping people build a savings (or pensions) pot rather than providing an income, but you can of course withdraw money from your account as and when you wish. You can read my full review of Nutmeg here.

Of course, all investment carries a risk of loss, so you should always do your own ‘due diligence’ and take advice if in any doubt before deciding to invest. You should also ensure you have enough cash and/or easily accessible savings to get you through a period of three to six months in case of emergencies.

As always, if you have any comments or questions about this post, please do leave them below. And keep reading Pounds and Sense for more money-saving and money-making ideas in the weeks and months ahead.

Disclosure: Some of the links in this post (and elsewhere on PAS) include my referral links. That means if you click through and make a purchase (or perform some other defined action) I may receive a commission for introducing you. This will not affect the price you pay or the products/services you are offered.

If you enjoyed this post, please link to it on your own blog or social media:

Today I am sharing some information about personal finance podcasts. This is not a subject I previously knew very much about, so I am grateful to my friends at All Finance Tax for supplying the excellent infographic and some of the other info below.

What is a Podcast?

A podcast is like a series of radio programmes on a particular theme or topic, from politics to cycling. You can subscribe for free using a suitable app on your smartphone (or other internet-enabled device). You can then listen whenever and wherever you like, via headphones, earphones, through speakers, in the car, on the train, and so on.

Podcasts are a booming medium and one of the major trends of the last five years. There are now podcast shows on nearly every topic you can think of. And with the rise of both independent and conglomerate podcast production studios, it seems likely this new medium will be in our lives for many years to come.

In the same way people were once passionate about certain radio shows, podcasts have the same dedicated followings, thanks to hosts who become familiar audio friends. Some even run live events. As a medium, podcasts are incredibly accessible, with few barriers beyond an internet connection and a smartphone or other device that can stream audio. No matter where you are or what you’re doing, podcasts offer content that educates, inspires and entertains. If you have never listened to a podcast before, the BBC Sounds podcasts page is one good place to start.

How to Listen to a Podcast

The easiest way to find and listen to podcasts is by using an app on your smartphone.

If you have an iPhone, it will have a built-in app called Apple Podcasts. This works very well and allows you to search for and subscribe to any of a huge range of podcasts. All you have to do then is open the app any time you want to listen and choose the episode you require.

Android owners can use the free Google Podcasts app. You can download this from the Google Play Store if you don’t have it already. It is not as user-friendly as the Apple app and doesn’t have as many features, but will certainly get you started. There are also other free or inexpensive apps you can download from Google Play such as the highly-rated Pocket Casts or Castbox.FM.

Finance Podcasts

One genre with a surprisingly large, dedicated listenership is finance. While to some that might sound a dry, unpromising subject, the podcast medium has enabled content to be reinvented with an unexpected, creative approach.

With hosts ranging from seasoned finance professionals to novice FIRE (financial independence) enthusiasts, podcasts allow people who would never previously have been interested in finance – or perhaps even have been intimidated by the topic – to access valuable information presented in an engaging, inclusive way.

All Finance Tax rounds up the top finance podcasts in the infographic guide below. Find out about the must-listen shows, including podcasts about:

Entrepreneurship

Billionaire case studies

Female-led finance

Personal and couples’ finance

Start-ups

And more!

With snapshots of real reviews plus the best episodes to start with, this resource will help you find the right show for your personal interests and needs regardless of your outlook on finance. Read on for the full list of finance podcasts to start your listening journey!

Many thanks again to my friends at All Finance Tax for their help with this article. I have listed below all the podcasts recommended in the infographic, with links to their homepages (or another website) where you can find out more. You can also listen to the podcasts on the web via these pages, though using an app on your smartphone (as discussed earlier) may be more convenient generally.

One more I would add is the Ask Martin Lewis podcast from BBC Radio Five Live. Martin is, of course, a well-known personal finance guru (and founder of the hugely popular MoneySavingExpert website). Although I can take or leave his TV shows, his podcasts are less gimmicky and include valuable, accessible advice on all aspects of personal finance (not including investing).

As always, if you have any comments or questions about this post, please do leave them below. I’d also love to hear about any personal finance podcasts not mentioned above which you enjoy and recommend!

If you enjoyed this post, please link to it on your own blog or social media:

Due to the pandemic many people are now working from home some or all of the time. And many others, who may have lost their jobs due to the crisis, are now running home-based businesses or considering setting one up.

I have been working from home for over 30 years now, so in this post I thought I’d set out the main pros and cons as I see them. I hope if you have recently started working from home, or expect to in future, you might find this helpful.

I’ll start with some of the advantages…

The Pros

Save money – If you work from home you will avoid having to pay travel costs and potentially other work-related expenses like takeaway coffees and meals.

Be safer – Working from home means there is less chance of catching (or passing on) Covid-19 or other infections. You also avoid having to venture out during the winter months on dangerous wet or icy roads and pavements.

Save time – You will also avoid wasting many potentially productive hours in your car or on public transport. Many people (e.g. with jobs in London and other major cities) spend two or more hours a day just commuting; added up over a year, the total amount of time ‘lost’ in this way can be quite staggering.

Feel more comfortable – In general you can wear whatever you like. You don’t even have to dress or shave if you don’t wish (though you will, of course, need to make an effort with your appearance when meeting other people in real life or on online platforms like Zoom). You can take tea, coffee and meal breaks as you like, whenever it happens to suit you. You can arrange your office furniture, lighting, temperature and so on exactly as you prefer. And unlike many offices and other workplaces at the moment, you won’t have to wear a mask all day!

Benefit from flexibility – Many aspects of family life can be easier to arrange if you work from home. For example, if you want to pop out at 3.30 to collect your youngest child from school, this should be a lot more feasible. To a degree you will be able to choose your own hours, working early in the morning or late at night if these options suit you best. You can be around in the day when the plumber or meter reader calls; you can put out the washing and bring it back in if it starts to rain; and you will not miss important deliveries because you are toiling away at a separate workplace.

Enjoy tax advantages – If you run a home-based business you may be able to claim a proportion of your household expenses (heating, lighting, mortgage/rent, etc.) against tax. Even if you are working for an employer, you may be able to claim working from home tax relief.

Improve home security – The fact that you are around in the day can help deter burglars (most burglaries in residential areas take place during the daytime). You will also be on the premises – and therefore able to take prompt action – in the event of fires, burst pipes and other such emergencies. Some insurance companies are starting to recognise this fact and offer lower premiums for homeworkers – though this must be set against the fact that work-related computers and other equipment may have to be insured separately for an additional premium.

If you run your own home business there are various additional advantages.

You will no longer have to endure the horrors of office politics or attend long, dull, pointless meetings (been there, got the tee-shirt). With your own business you can work as many or as few hours as you wish. If you want to work a fifteen-hour day, you can (though hopefully not every day!). Equally, however, you can work part-time if you prefer, perhaps to fit in with family responsibilities. You can also set your own pace, with no-one standing over you telling you to work harder or faster. For older people, or those with disabilities that slow them down, this can be a particular attraction.

As long as your business is bringing in enough money to meet your needs and those of your dependants, you can work as hard or as easily as you wish – you have complete control over your ‘terms and conditions’. But, of course, while you won’t have a boss looking over your shoulder, you will still have clients/customers who will expect a good quality product or service from you within a certain deadline.

The Cons

Although working from home has many attractions, it does possess a few potential drawbacks as well. Some of the main points to consider are set out below.

May disrupt family life – Working from home means you and your family’s domestic lives will inevitably be affected. Obviously you will need a space in the house to work that might otherwise be used by other family members. If running a business you may have to work during the evenings, public holidays and weekends, when most ‘normal’ people are at leisure. Clients may contact you by phone at any time, even outside normal working hours, so family members will need to become accustomed to receiving calls and be briefed on how to handle them. If you have other heavy phone users in the house you may need to get a separate line for business calls.

May be distractions – Friends and relatives who would never dream of interrupting you at a ‘proper’ job may think nothing of phoning up or arriving unannounced, not realising (or perhaps caring) that you are at work. Regular interruptions of this nature can seriously reduce your productivity. Even if you avoid this problem, working from home offers a huge range of potential distractions, from pets and family matters, through shopping and household chores, to gardening and watching television. You will need to be self-disciplined, or you can fritter away many working hours on non-productive (in business terms anyway) activities such as these.

May be lonely – Working from home can be lonely at times. This applies especially if you live on your own, when you may not speak to another person face-to-face (apart from perhaps the post office clerk) for days on end. Even if you do have a family – or at least a spouse/partner – you may find the isolation during the day difficult to bear. This applies especially if you have previously worked in a busy office or factory, or you have a naturally sociable temperament.

Can be hard to get away from work – If you work from home, you may find that work and domestic life become indivisible and it is very hard to ‘switch off’ and relax when the day’s work is done. People who have previously worked in a separate establishment often find the journey between home and workplace provides a valuable psychological dividing line. When your home is also your workplace this line is gone, and the distinction between work and leisure can therefore become blurred.

May need better security – As mentioned previously, in some ways working from home is helpful for home security. But if you have high-value, easily portable equipment such as computers, cameras, tools, and so on, this may make your home a more attractive target for burglars. You may therefore need to increase your security, perhaps fitting a burglar alarm, security lighting/cameras, window locks, and so on.

Finally, if you are setting up a home-based business, planning restrictions may apply. This is most likely to be a problem if your business is likely to cause noise or other irritation to your neighbours. If you live in rented accommodation, the landlord may object to your running a business from his property; and if you are buying your house with the aid of a loan or mortgage, the lenders may be unhappy. There may also be terms in the lease or deeds of your property prohibiting its use for business purposes. And there is a possibility that running a business from home may mean that you become liable for business rates as well as your normal council tax.

The best types of business for running from home are those that are small and office-based – or based predominantly on clients’ premises – rather than those requiring workshops and machinery or selling directly to the public. A wide range of home-based franchise opportunities are also available.

In Conclusion

As I said at the start, I have worked from home for over thirty years now, initially as a freelance writer and editor, more recently as a blogger.

I enjoy working from home and in general do recommend it. I do just think that there are two key secrets to doing it successfully in the long term.

First, you should have a part of your home as your designated workspace. Ideally this could be a separate study or office, but at least a quiet corner where you can set up your equipment and files and not have to pack everything away at the end of the day. Growing numbers of people are now using garden sheds or extensions for home working, and this can also be a good solution. But if that’s not an option, work pods can provide a space-saving refuge in which you can avoid noise and other distractions and focus on getting your work done.

I also think that if you’re working from home, it’s vital not to let yourself become isolated. I know that has been easier said than done during the pandemic, but it’s very important to keep up connections with friends, family and colleagues. Home working can be especially challenging if you like and are accustomed to having colleagues to talk to. You really do need to build some social interactions into every day if possible – ideally face to face, but at least via the phone and/or social media. Your mental health may depend on it!

If you have any other comments or questions, as always, please do post them below.

Disclosure: This is a sponsored post.

If you enjoyed this post, please link to it on your own blog or social media:

In my previous article I explained the basics of franchising and revealed some of the attractions of the method to anyone hoping to set up a business of their own.

I also discussed the personal qualities and skills required to run a business, whether a franchise or otherwise. You don’t need to have all of these initially to make a success of running your own business, but you will almost certainly need to develop them.

Today I’ll be setting out some advice on choosing the right franchise for you, and how to run your franchise successfully. I’ll also be listing a selection of current franchise opportunities, along with resources for finding many more.

Before that, though, let’s recap on the main attractions of the franchise route, along with a couple of possible drawbacks.

Franchising Pros and Cons

The main attraction of franchising is that you are buying into a ready-made business format.

While this does not guarantee the success of your business, with a good franchise you will be getting a format that has worked well for others, and with a little luck (and a lot of hard graft) should work for you too.

Another benefit is that, as a franchisee, you are not alone. If you have any problems or queries, the franchisor will be available to advise and support you. They will also in most cases provide training, promotional materials, and so on. You may also be able to network with franchisees in other areas for mutual support.

On the downside, running a franchise will require you to follow the franchisor’s format very closely. If you are a free spirit who likes to carve your own path in life, you may find the restrictions imposed difficult to bear.

The other drawback is, of course, you have to pay the franchisor! Typically there will be an up-front fee and further regular payments for support, training, materials, and so on. Obviously, with a good franchise you get plenty back for your money, but ultimately all these costs have to be covered by you and your business.

As mentioned last time, some big franchises such as McDonalds will set you back a six-figure sum. Finance deals may be available through the franchisor and other lenders, but you are still likely to have to fund a substantial chunk of the initial cost yourself.

If money is tight, however, there are lower-cost franchise opportunities as well. Later in this article I will set out a range of options to suit all budgets.

Choosing a Franchise

It’s important not to rush into choosing your franchise. Nowadays a huge range is available, and it’s vital to take some time to assess the options and identify which might be the most suitable for you.

A good place to start is a franchise exhibition. Held in cities across the UK, these events give you the chance to check out many different franchises and – just as important – chat with the franchisors. Obviously the pandemic meant many exhibitions had to be cancelled, but as normal life gradually resumes they are returning to the calendar again.

The biggest exhibitions are those organised by the British Franchise Association in cities including Manchester, Glasgow, London and Birmingham. Entry is generally free as long as you register in advance. A good place to find out about upcoming exhibitions (and much more besides) is the website https://www.franchiseinfo.co.uk.

Here are a few more tips for choosing the right franchise…

Choose something that interests you personally. You are more likely to succeed in a business you enjoy, as you will put more effort and enthusiasm into it. If you like cars, for example, there are franchises covering everything from vehicle rentals to fixing dents and scratches. If working in the outdoors appeals, you could focus on areas such as landscape gardening or window cleaning.

Look for franchises that will fit in with your family and personal circumstances. Sectors such as retail and catering involve long hours, often in the evening and at weekends. If you have childcare concerns, or simply fancy seeing your other half and friends now and then, you might prefer to focus on franchises that allow you a bit more free time.

Aim to pick a franchise with a good track record and reputation. Be wary of new franchises, especially those based around an unproven product or service. Remember that the franchise is going to have to provide your livelihood potentially for many years to come. You don’t want to hitch your wagon to a business that may prove no more than a short-lived fad.

Once you’ve identified some franchises that interest you, ask the franchisors for contact details of existing franchisees you can speak to. Don’t let them fob you off with one or two names. Request a list and choose a few at random to contact. Ask in particular how they get on with the franchisor and what the quality of support has been.

If at all possible, arrange to visit one or two existing franchises and stay a few hours to see what the work involves and whether or not it would appeal to you. This can be very illuminating.

Ensure the financials stack up. Study the projections provided by the franchisor and see if they tally with your own research, bearing in mind local market conditions. Your accountant, bank and existing franchisees can help verify your findings and assumptions. If the projected revenues look too good to be true, they probably are!

Also bear in mind that your start-up costs will need to be deducted from your revenues, so don’t leave yourself short. It may be 6–12 months until your business is fully established, and during that time you will need to have enough money to cover all your costs and expenses, including feeding yourself and your family!

Before proceeding further, an essential step is to draw up a detailed business plan. This should cover such things as the size of your territory, local competition, the national and local economic climate, trends affecting the product/service you will be supplying, and so on. It should also include a cash-flow projection showing anticipated monthly income and expenditure for at least the first twelve months.

Your business plan will be an invaluable guide when planning and running your business, and it will also be a necessity if you have to apply to a bank for finance.

Running Your Franchise

Having bought your franchise, you will of course want to get it making money for you in the shortest possible time. Here are some tips for starting and running a successful franchise…

Keep in regular touch with your franchisor and act on any advice they give you. Whatever issues you may be facing, you can guarantee that someone, somewhere has already faced something similar, and the franchisor will be able to advise you how they dealt with it. Use the franchisor’s knowledge to your advantage rather than learning the hard way. That is why you paid for a franchise rather than setting out on your own.

Improve your business skills. While franchisors will teach you their system, most also expect you to bring some basic business skills to the table. If you don’t know accounting basics, how to read and work with financial documents or how to hire and manage employees, you’re likely to encounter problems. If your sales skills are rusty, your knowledge of business taxes is shaky or you’re not up to speed on internet marketing, consider taking a class to improve your skills. Classes are often available at local colleges, and there are also online courses and seminars that require less time and monetary investment.

Likewise, make it your business to learn everything there is to know about your industry (in addition to whatever you found out during your franchise research). Almost every sector has associations and meetings where business owners gather and share ideas – these can provide a great forum for learning and networking. And, as mentioned earlier, your fellow franchisees can also provide invaluable insights into your industry.

Monitor your cash flow carefully. Regularly compare the figures in your forecast with the reality, and use this to make informed decisions about your business. It’s important not to under-estimate the working capital required to run a business day to day while it is growing. Cash-flow problems can be mistaken for poor profitability, in the early months especially. Careful planning and monitoring will reveal how you are really doing and prevent unpleasant surprises.

Market your business. Even with the franchisor’s name and system behind you, your business won’t sell itself. The fact is there is no-one better to market your business than you. Use the passion you have for your product or service to talk to people face to face. Enthusiasm is infectious and you will be more successful. Monitor carefully the results of any marketing activity, however. You don’t want to waste your money in future if a campaign has not proved profitable for you.

Master time management. As a business owner you only have so many hours per day and it’s important to deploy them wisely. Planning and flexibility are the keys to success when it comes to time management. Time spent planning saves a lot more time in the long run. But be flexible as well, and constantly assess any task associated with running your business to see if it can be done more efficiently.

Stay up to date with paperwork. Don’t leave it for a month then attempt to do it all in one day. Not only does this become a depressing chore, but by the end of that day you are more likely to be tired and make mistakes.

Wherever possible invest in IT and developing your computer skills. Many aspects of running a business can be performed faster and better with the aid of computers, from invoicing to accounts, marketing to stock control. Don’t forget to back everything up on a regular basis!

Recognize your strengths and weaknesses and use them to your advantage. If you really are terrible at managing one aspect of your business, employ someone to manage it for you. Your time will be better spent on the aspects of your business you are good at and enjoy.

Reward Yourself. The responsibility of running your business is down to you, and that includes rewarding yourself when things go well. Set yourself a goal and when you achieve it give yourself a little reward. You would do it for an employee, so why not for yourself?

And finally, enjoy yourself. The chances are you decided to start a business because you wanted to enjoy your work more than you were previously. Yes, running a franchise does require effort, determination and tenacity, but don’t lose sight of the reason you started. Stay positive, enjoy the challenges, and never lose your sense of humour. Have fun!

Example Franchise Opportunities

As promised, I have set out below a selection of franchise opportunities you might like to consider. As well as some high-profile (and high-cost) franchises, I have also included some that may appeal to those on a more limited budget.

This is a pet-sitting and home-care franchise. The work involves visiting clients’ homes while they are away and looking after their pets, as well as keeping an eye on their homes and gardens.

This franchise involves setting up your own Kumon maths and English study centre. To become a Kumon instructor you should have an interest in education, an understanding of business, and enjoy working with children.

Harmony at Home is a recruitment and consultancy agency for the childcare industry, providing both permanent, temporary and supply nannies and childcare staff, as well as training courses and consultancy services. The franchise can be operated from home or from an office.

Everyone needs their windows cleaned, so there will always be a market for this business. My Window Cleaner offers training, marketing assistance and admin support via an app.

This business involves going round in a van installing and removing estate agents’ signs. You can start with a single van, and get more vans and take on staff to boost profits further.

This franchise involves running a local branch of Haus Maids, a company that provides one-off and regular cleaning services for domestic homes. This is a managerial franchise, so the work involves managing a workforce of cleaners rather than actually doing any cleaning yourself.

Travel Counsellors is a company that offers clients the opportunity to book a bespoke holiday or business trip, planned for them to the finest detail by a trained and experienced Travel Counsellor. Experience in the travel industry is a particular asset with this franchise. It’s not essential, however, as full training is provided to bring franchisees up to the required standard.

McDonald’s is one of the best-recognised brands in the world. A growing number of their restaurants are run by franchisees. This is not an opportunity for the faint-hearted, and applicants have to submit to a selection process as well as having at least £100,000 in unencumbered funds. For those accepted, though, the financial rewards can be considerable.

Note that all the costs stated above are approximate minimum amounts and do not include any ongoing payments that may also be required. VAT is also likely to be charged, though you may be able to claim this back once your business is up and running (and registered for VAT).

As I hope I have demonstrated in these articles, if you want to start your own business, buying into a franchise is definitely something you should consider.

Not only will you be getting a tried-and-tested business format to follow, you will also have access to advice and support from the franchisor any time you need it. You will still need to put in some hard work yourself, of course, but your chances of success should be significantly boosted compared with going it alone.

What’s more, there are thousands of different franchises available, in a wide range of industries, and at prices to suit all budgets. Don’t rush into buying a franchise, therefore, but take some time to explore a range of options. And hopefully in less time than you think there is every chance you will be running your own profitable franchise and enjoying the many benefits of being a successful business owner.

As always, if you have any comments or questions on these articles, or franchising in general, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

If you want to be your own boss, the franchise route is well worth considering.

Franchising isn’t a business in itself, but rather a method of ‘buying into’ a brand and format devised by someone else. With a franchise you typically pay the franchisor an up-front fee, and possibly additional fees once you’re up and running as well.

Franchising has become a very popular method for getting started in business. It has the great advantage that you aren’t starting from scratch. In exchange for your fee, you gain the right to trade under the franchisor’s brand name. You get a ready-made (and hopefully proven) business plan, along with training, materials, assistance with marketing, and access to advice and support any time you need it.

A huge range of franchises is available, and there’s something to suit most budgets. At the lower end of the scale, you can get started as an Avon distributor for as little as £10. At the other end of the scale, you could pay up to £800,000 to purchase a McDonald’s franchise (see cover image).

In between these is a wide variety of businesses, from carpet cleaning to recruitment, gardening to children’s entertainment. While some franchises require business premises, many others can be run from home and/or a car or van.

Of course, some franchises are better than others, and it’s important to research any that interest you carefully. So in this two-part series I’ll be sharing some tips on choosing the best franchise for you and getting the most out of it. I’ll also be setting out a range of current UK franchise opportunities to give you an idea of what’s available.

In this first article, though, I want to start by addressing the more fundamental questions of what running a business entails and the skills and aptitudes required.

Business Basics

At the risk of stating the obvious, running a business is a very different thing from doing an ordinary job.

As a business-owner, you will be responsible for every aspect of your business’s operation. As well as providing a product or service, all the ancillary matters from marketing to book-keeping, purchasing to recruitment will become your responsibility.

Of course, you will get help with many of these from the franchisor, and you may also choose to outsource some to professionals such as book-keepers and/or paid staff. Nonetheless, you will need to oversee all of these tasks and ensure they are done properly even if you don’t do them yourself. That is quite different from an ordinary job, where you simply do whatever task you are paid for and leave everything else for your employer to worry about.

Running your own business requires a particular set of aptitudes and skills, and there is no doubt it suits some people better than others. In the next section I’ll set out the main qualities you need for business success.

Requirements for Success

Everyone has different views on which qualities are the most important for success in business, but there are certain ones that come up time and time again…

(1) Determination

Many people talk about starting a business, but only a small proportion do anything about it. Starting a business is a major decision that will undoubtedly change your life and that of your family. It is important that you are committed to your new career before making such a move; and that once you have started the business you are determined to see it through to success.

(2) Willingness to Work

We all think we are willing to work hard, but if you start a business you will soon find out what this means in practice! In the early days at least you are likely to have to work longer hours than the average employee. Although as your business becomes established some of the pressure may ease, you must still expect to work longer and harder than most people in paid employment.

(3) Persistence and Perseverance

Successful business people let nothing get in the way of achieving their goals. If they encounter problems, they try to find ways to overcome them. If their first attempt doesn’t succeed, they try a different approach; and, if this doesn’t work, another. They are not put off by pitfalls, or discouraged – other than temporarily – by failure. They persevere in their efforts until, eventually, they do succeed.

(4) Stamina

In view of the hours you are likely to have to put in, stamina and at least reasonably good health are important. People running businesses have to avoid taking time off for sickness if at all possible. As a self-employed sole trader in particular, if you are not working you are not generating any income. And if you let down a customer, next time he is likely to go elsewhere.

(5) Self-discipline

If you are in a paid job the chances are you will have a manager or supervisor, part of whose duty is to ensure that you fulfil your obligations to your employer. Your reasons for wishing to start a business may include escaping from such individuals! However, while as a business owner you will have no-one standing watch over you, you will still have obligations to customers, suppliers, employees, officials, and so on. If your business is to go on running successfully, it is important that you have the self-discipline to fulfil all your responsibilities and see a job through to the end.

(6) Willingness to Take Risks

All business people have to take calculated risks. Whereas in a job you have the relative security of a regular wage or salary, as a business owner there is no guarantee what your income will be from one month to the next. You will constantly find yourself having to make decisions about where and how to advertise, which areas to specialize in, when to invest in new equipment, and so on. Although this constant decision-making can be stressful, it can also be satisfying and enjoyable. Solving problems and making decisions can give you a sense of power and confidence. And if you are running a franchise, you will be able to get advice and assistance from the franchisor, of course.

(7) Ability to Cope with Stress

Starting and running a business will inevitably impose a range of stresses, both on you and your family. In the beginning at least, long hours, hard work and disruption to family life can cause tension. To be successful in business you need to be able to cope with, and even thrive on, this kind of pressure.

(8) Enthusiasm

Enthusiasm is an essential ingredient of every business owner. If you are half-hearted about your venture you may have difficulty summoning sufficient determination to overcome problems when they arise. If you are enthusiastic, on the other hand, you will relish the challenges your business presents. What’s more, your enthusiasm will rub off onto customers, employees (if you have them) and other people you have to deal with. Most of us would far rather work with or buy from someone who is enthusiastic and enjoys his work, rather than someone who is permanently depressed about it.

(9) Ambition

Most business people have a driving ambition to achieve the best they can for themselves and their loved ones: as well as money, this may include financial security and a better way of life. With such ambitions they can cope with any setbacks along the way, because in their mind they have a goal or vision that drives them on. Ambition and determination together can overcome many obstacles. In business, as in most others aspects of life, if you know what you want and are determined to achieve it, the chances are excellent that you will succeed.

(10) Honesty and Willingness to Give Good Service

Finally, every business depends for its continuing survival on a circle of satisfied customers. If people are pleased with the service they have received from you, they are likely to recommend you to others as well as keep coming back themselves. By contrast, if you give poor service then, even if they do not complain at the time, they will not return; and rather than recommend you to others, they will warn them about you (quite possibly nowadays on review websites that anyone can find). If you have a good reputation this will ensure that more people keep coming to you. For this reason, successful business people go to great lengths to obtain and keep a good name for themselves.

Franchisors are, understandably, fiercely protective of the good name of their brand. In many cases they will want to conduct checks to satisfy themselves that you are a suitable person to run a business in their name. Don’t be surprised or offended if this happens, therefore. It’s actually a good thing, as it demonstrates the franchisor’s long-term commitment to preserving their reputation.

Friends and Family

Just as it is important to have the right personal qualities yourself, you will also need a supportive family and friends.

If you decide to start your business from home, this will inevitably cause changes and disruption in the family routine. Even if you use separate business premises, your friends and family will still have to come to terms with your working long hours and having less time and energy for leisure activities. If you are married or living together, it is especially important that your partner understands the implications of your setting up in business, and supports what you are trying to do.

There is also a positive side, of course. Your family may be a valuable source of help in all sorts of areas, from answering the phone and writing letters, to book-keeping and assisting customers. Having others closely involved with the business can assist when problems arise, as they will bring different ideas and perspectives to the situation.

Although it is not absolutely essential to have a supportive family, there is no doubt that you are more likely to succeed if you have discussed your plans with them and have their wholehearted support.

Your Skills

To run your business successfully, as well as the right personal qualities and a supportive family and friends, you will need a range of skills. These are described in general terms below. If you lack any of these it does not necessarily mean that you should not set up in business. However, if you feel any of these areas is going to present serious problems, you might want to consider taking on a partner or employee to handle that aspect of the business, or using a specialist adviser or consultant. You might also consider taking additional courses to acquire the skills you need.

(1) Technical Skills

These are the skills that you need to actually deliver the service you are offering. In the case of a franchise, training will normally be provided to help you achieve the necessary standard. Obviously some types of business will require more in the way of technical skills than others, and you may also choose to employ staff to deliver services on a day-to-day basis. Even if the latter applies, however, you should still have an in-depth knowledge of the service in question, so you can ensure that all your customers receive the high quality service they expect.

(2) Financial

To run a business successfully you will need a range of financial skills. These include such matters as book-keeping, negotiating credit terms with suppliers, invoicing, credit control, estimating, drawing up budgets and controlling cash flow (the flow of money into and out of the business). Again, the franchisor or should be able to help with this, but it will be down to you to master the skills required and/or hire staff who can perform them to a suitable standard.

(3) Marketing

Marketing is the process by which you identify potential customers and persuade them to buy your products or services. It includes selling skills, and also such matters as pricing, advertising, sales promotions, public relations, and market research.

(4) Management

If you are going to employ others, you will need a variety of management skills in such areas as recruitment, motivating staff and team building. You will need a knowledge of employment law and health and safety requirements. You will also need to be able to fulfil legal requirements in matters such as deducting tax from employees’ pay.