Today I’m addressing an issue that will be critical to many people approaching (or in) retirement. That is, how much to draw from your pension pot (and other investments) to supplement your state pension.

I’ll start by telling you about a conversation I had recently that made me think about this…

Talking to Mike

A few weeks ago I had my annual review with my financial adviser, Mike (if you want to know why a money blogger needs a financial adviser, you can read my post about this here). It was done by video call on this occasion, naturally.

One major topic of conversation was the fact that later this year (God willing) I will reach my 66th birthday and start receiving my state pension. I should qualify for the full state pension, which from April 2021 will be £179.60 a week or £9,339.20 a year.

As Mike pointed out, when you add this to my other income from this blog, my small private pension, other investments and my solar panels, this will put me in quite a strong financial position. So he recommended that at that time I reduce the amount I draw from the other investments or even stop taking anything at all and let them carry on growing year by year (financial downturns permitting).

I could see where Mike was coming from. If I don’t actually need the money it might be sensible to leave it all where it is. For both practical and psychological reasons, however, I told him I don’t want to do that. Here are the two main reasons I gave him:

1. If I take no income from my investments, I will still be somewhat dependent on my blog for income. While I have no plans to stop running Pounds and Sense at the moment, I don’t want to have to rely on it to cover my outgoings as I grow older. Also, the income from my solar panels will end in about ten years – possibly sooner if there are any major technical issues (or I move).

2. I don’t have any particular beneficiaries I wish to leave my money to (I live alone since my partner Jayne died a few years ago and we didn’t have children). I don’t therefore see any merit in accumulating a large ‘pot’ that simply goes to benefit my sisters (much as I love them). I would rather enjoy the money while I can, while aiming to ensure that it lasts me out.

I told him my plan was therefore to reduce my withdrawals to a sensible level where my capital should be preserved and hopefully continue to grow a little. Four percent is a common rule of thumb for this, so I am looking at that as a starting point (though willing to accept Mike’s expert advice on the exact level). I plan to review this every year, based on my needs and circumstances and how my portfolio has been performing.

If I have more money coming in than I require, I don’t see that as a problem. I will spend it (maybe on a few extra holidays), save it or reinvest it, and maybe give some to charity and/or friends/relatives who are in need. As they say, you can’t take it with you, so I have decided that will be one of my guiding principles going forward!

I shared these thoughts in a subsequent email to Mike but haven’t so far received a reply from him. If I do, I’ll update this post accordingly 🙂

That Crucial Question

I am obviously not alone in facing a decision of this nature. With most people nowadays relying on a pension pot to finance retirement rather than a guaranteed lifetime pension, many of us will have to grapple with the question of how much income we should be withdrawing to supplement the state pension.

And yes, I know the state pension will continue as long as we need it. But while it is obviously an important source of income for most people in retirement, it is nowhere near enough to finance a comfortable retirement on its own.

Of course, none of us comes with a sell-by date. Pension planning would be so much simpler if we did. If we knew the exact date we were going to expire, we could plan our retirement precisely.

So if I knew I was going to die in five years, I could live the (moderately) high life, burn my way through my savings and investments, and leave just enough for my relatives to pay for my funeral!

On the other hand, if I knew I could look forward to another thirty years, that would of course be wonderful, but I would need to plan carefully to ensure my pot didn’t run out before I did. But as none of us knows how long we have on this planet, a long-term strategy is the only sensible option really.

The question of how much to draw from your pension pot (and other investments if any) therefore needs very careful thought. In particular, the following considerations may apply:

It’s clearly sensible to try to ensure that enough money will remain in your pot to see you through to deep old age (e.g. 100).

If you’re keen to pass on a legacy to your children (or some cause dear to your heart) you will need to be more cautious about how much you withdraw.

On the other hand, if you aren’t so worried about passing your wealth on, then there is no point in depriving yourself now.

Tolerance for risk is another factor. If you worry that the 4% rule is too chancy, you could reduce your withdrawals to 3% or less.

There may be other considerations too. For example, if you have a life-limiting medical condition, that may alter the equation in favour of a more bullish approach.

There is also the matter of whether you own your home. If so, you will have the scope to raise extra money if needed by downsizing or using equity release.

Tax may be an issue as well. The state pension counts as taxable income and so do most private pensions. If the total amount you draw exceeds your personal allowance, you may have to pay tax on it. This is something you might want to discuss with a financial adviser.

And finally, if you have a particular ambition or goal you wish to achieve during retirement (going on a world cruise, for example), you will of course need to ensure enough money is set aside to cover that when the time comes.

As mentioned above, a common rule of thumb is that to provide the best chance of preserving the value of your investments, you should limit withdrawals to no more than 4% of your capital per year. So if, for example, you have a pension pot of £50,000 and draw 4% annually from that, that would be £2,000 a year or about £167 a month. Drawing that would hopefully ensure that the value of withdrawals is on average balanced out (at least) by growth in the value of your investments.

Of course, the 4% rule is only a rough guide and needs reviewing regularly according to how your portfolio performs.

When pension freedoms were introduced in 2015, there was some concern that people might ‘blow’ their pension pot on a luxury car or a yacht, but actually I think the vast majority of older people are more sensible than that. Indeed, I think the opposite mistake is more common – people drawing too little and leading a life in retirement that is unnecessarily frugal rather than enjoying the money they accrued during their working lives. But in any event, this is a question we all need to think very carefully about as we attempt to chart a balanced course into retirement and old age.

So those are my thoughts on this important subject (one I know many people don’t really like to think about). But what is YOUR view? Please post any comments or questions below as usual

If you enjoyed this post, please link to it on your own blog or social media:

Today I’m looking at P2P property investment platform Assetz Exchange (launched in January 2019)..

As I have noted before on Pounds and Sense, I am something of an enthusiast for property investment (and specifically property crowdfunding). Among other things, I like the fact that you can make money from both rental income and capital growth. And investing in property can be a good way of spreading the risk when you have equity-based investments.

Of course, investing in property directly is costly and carries all the risk inherent in putting all your eggs in one basket. A major attraction of P2P property crowdfunding investment is that you can get started with much less money and build a diversified portfolio to help mitigate the risks.

In addition, if you invest this way you don’t have to deal with the day-to-day hassles of being a landlord, from finding tenants to repairing broken boilers. This is taken care of by the platform itself and/or their management company. You just have to sit back and – all being well – wait for the rental income and (hopefully) capital gains to materialize.

That said, there have been a few reversals in the P2P property sector over the last few months (see this recent post, for example). So I am now more concerned than ever to ensure that any investments I make in this category control risk as effectively as possible.

Table of Contents

What Is Assetz Exchange?

As mentioned above, Assetz Exchange is a licensed P2P property investment platform. It is owned by well-known P2P lending platform Assetz Capital, but run quite separately from them. If you already have an account with Assetz Capital, you will have to register separately with Assetz Exchange.

Assetz Exchange aims to offer net yields to investors of between 5.2 and 7.2% per year. These are generally paid by institutional tenants through multi-year leases. All properties are unleveraged, providing additional security (and stability) for investors.

Assetz Exchange has some similarities with Property Partner, but they differ in some important ways. For one thing, many of the properties are rented out to charities (e.g. NACRO) or housing associations. These organizations generally sign longer contracts than private individuals. They don’t have voids (periods when the property is untenanted and producing no income). Neither are there any maintenance costs, as the organizations take responsibility for this themselves. And finally, these organizations are directly funded by the government, giving them a secure income stream.

Another area of specialism is show homes. Working with a national housebuilder, Avant Homes, Assetz Exchange purchases fully furnished show homes from multiple sites around the country. These are then leased back to the developer for fixed periods of up to five years to be used to help sell other plots. This eliminates potential void periods and avoids any maintenance costs. At the end of the leases, investors will be able to vote on whether to lease the houses to tenants or sell them to home-buyers on the open market.

Assetz Exchange also offers investors the chance to get involved with a new generation of modular eco-homes. This is already a popular approach to house-building in Europe and the United States. Assetz Exchange fund the acquisition and conversion of land into serviced plots, allowing buyers to then order a house to be built on that plot to their own specification. These modular-built eco-homes are sustainable and low energy. They are also typically quick to complete and have a lower impact on the environment.

Assetz Exchange do also buy and let some standard properties as well, offering investors the chance to further diversify their portfolios.

Signing Up

Before you can invest through Assetz Exchange, you will of course have to sign up on the platform. This is pretty straightforward. You just visit the Assetz Exchange website, read the information there, and click on Register in the top-right-hand corner.

You will then be required to enter your contact details and confirm which of four categories of investor you fall into. The options are as follows:

High Net Worth Investor – This includes individuals who have an annual income of £100,000 or more or net assets of £250,000 or more.

Self-certified Sophisticated Investor – This includes individuals who have made more than one peer-to-peer investment in the last two years or who meet certain other criteria relating to investment experience. This is the category I selected myself.

Investment Professional – Including corporate investors and SIPP or SSAS professional service providers.

Everyday Investor – This category is for investors who don’t fit into any of the categories above. They can still invest via Assetz Exchange but must pledge not to invest more than 10 per cent of their portfolio in P2P loans.

You will also be required to answer some multiple-choice questions to confirm that you understand the nature of investments that can be made on the platform. I found some of these questions quite challenging, and was pleased to get them all right first time. I would therefore recommend reading the information on the Assetz Exchange website (including the Help pages) carefully before proceeding to register. If you do make any mistakes, however, feedback is provided, and you can take the test again until you achieve a 100% correct score.

Once you have done all this, you will be able to fund your account. This must be done by bank transfer, as Assetz Exchange do not allow debit card payments. You will then be able to browse the range of currently available property investments:

Investing

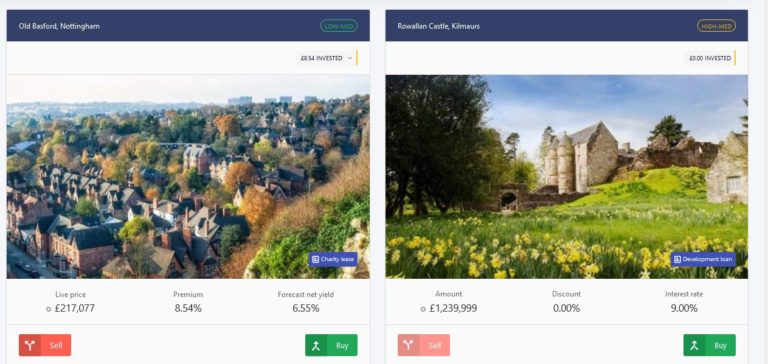

Once you are registered on the platform and signed in, click on Exchange in the menu at the top of the screen and all current projects will be displayed. Here are a couple that are showing at the time of writing…

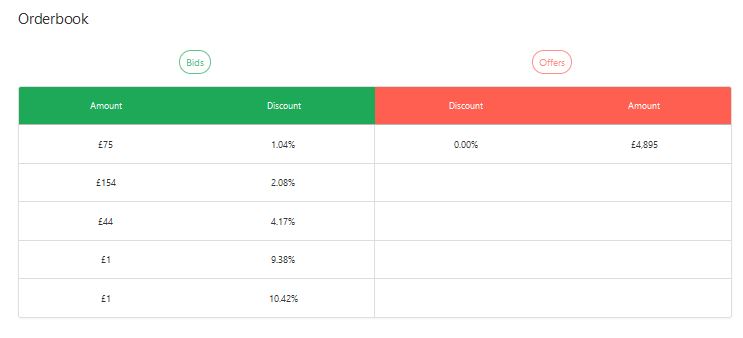

Clicking on any of these will open a page devoted to the investment concerned. Here you can read all about it, view reports and site plans, and so on. One very important area is the Order Book (see example below).

All buying and selling on the platform is conducted via an exchange (otherwise known as the Order Book) which works similarly to the secondary market on Property Partner.

So if you want to buy shares in a particular project, you can do so by accepting the best price currently available on the exchange. In the example above, there are £4,895 of shares available at zero discount (i.e. the original offer price).

If you want to get your shares at a lower price than this, you can make a bid. In the example, an investor has put in a bid for £75 at a 1.04% discount and another investor (or maybe the same one) has put in a bid for £154 at a 2.08% discount.

Conversely, if you wish to sell some or all of your shares at any time, you can accept the best bid (or bids) on the Order Book currently, or place an offer and wait to see if this is matched.

It does take a little bit of getting your head around at first, but it’s actually a simple and straightforward process. One thing to note is that if there is nothing showing on the right-hand-side of the Order Book (under Offers) you won’t be able to buy shares in that project there and then – though you can of course place a bid if you wish and see if a seller wants to match it.

In any event, if you want to buy, just click on the green Buy button (either on the Exchange page or the details page) and complete the short online form. You will need to indicate how much you want to invest, whether this should be from your General or IFISA account (see below), and whether the amount should include the FCC or not (see What Are The Charges? below).

You will also need to indicate whether you want to buy at the current best price (selected by default) or you want to try for a better price (in which case your bid will be added to the left-hand column in the Order Book).

The IFISA Option

As mentioned above, if you wish you can invest with Assetz Exchange via an IFISA (Innovative Finance ISA). As discussed in this recent post, this type of ISA for P2P investing gives you the same tax advantages as a cash or stocks and shares ISA. You don’t have to pay any tax on the money you make, whether this takes the form of dividends, income or capital gains.

Everyone has a generous annual ISA allowance of £20,000 in the current 2020/21 tax year (and next year as well). This can be divided any way you like among the three types of ISA. So if you open an Assetz Exchange IFISA, you can still have cash and stocks and shares ISAs with other providers as well, so long as you don’t invest more than £20,000 in total. You can also only invest money in one of each type of ISA in any one financial year.

Choosing the IFISA option on Assetz Exchange is very easy. You can do it when first registering on the site or later. The only extra thing you have to do is enter your National Insurance number.

If you have maxed out your ISA allowance – or have already invested in another IFISA in the current tax year – you can still invest via your default ‘Regular’ account. You can invest any amount this way, but of course any profits you make will potentially be taxable.

What Are The Fees?

Assetz Exchange do not charge any monthly fees to investors (this is in contrast to Property Partner, who made the unpopular decision to impose an Assets Under Management charge and monthly fee, greatly impacting small investors on the platform especially). The company does have to make money somehow, of course, and they do this from three sources:

Arrangement fee

When a property is first purchased, Assetz Exchange charge an arrangement fee which is included in the Fixed Costs & Contingency (FCC). When parts of the property are sold on the Exchange, this fee is added to the purchase price of the buyer (see above) and so is recovered by the seller. The size of this fee is included in the loan conditions.

Monitoring fee

Assetz Exchange charge a percentage of the gross rent received for the property. The percentage is stated in the loan conditions of the property.

Property disposal fee

A fee of 2% of the gross sales proceeds is charged if investors vote to sell and the property is physically sold.

What Are The Safeguards?

Like most other property crowdfunding platforms, all investments in any project on Assetz Exchange are held in a Special Purpose Vehicle (SPV) for the project concerned. This gives investors in the project some protection if the main company were to go into administration.

A contingency balance is held within each SPV which acts in a similar manner to a provision fund, covering unexpected short-term cash-flow disruptions. It is topped up from receipts and no distributions are made to investors if it falls below a certain level.

SPVs also benefit from indemnity insurance which covers non-payments from tenants. This in theory also covers disruption to cash-flow, but it does not cover voids (periods where the property does not have a paying tenant). For reasons mentioned above, voids should not be an issue with most of the properties listed on the platform.

In common with most other P2P investment platforms, Assetz Exchange does not fall within the remit of the Financial Services Compensation Scheme (FSCS), which covers customers with UK financial services firms up to £85,000 if the institution in question were to go bust.

3. Low minimum investment (as little as £1 per project!) – this makes building a diversified portfolio straightforward.

4. Assetz Exchange take care of all the work involved in buying and managing properties. You just choose which ones to invest in.

5. Option to access money any time by selling on the secondary market (though this does depend on another investor being willing to buy your shares at a price you find acceptable).

6. Relatively low-risk investment options (though of course there are no guarantees)

7. Customer support (in my experience anyway) is fast, friendly and helpful.

8. Charges are reasonable. There is no charge for selling investments.

9. Potential to make money through both capital appreciation and rental income.

10. Rental income is paid into your account every month. You can either withdraw or reinvest it.

11. No monthly fees and only transaction-based charges to pay.

12. Opportunity to invest in socially beneficial developments such as sheltered housing

13. Tax-free IFISA option to which any investment on the platform can be added

14. Investors can vote for their favoured exit option (e.g. selling up) when the time comes

Cons

1. Can’t invest using a debit card

2. No auto-invest option currently available

3. Not as many opportunities as some P2P platforms (although the number is increasing steadily)

Closing Thoughts

I was impressed enough with Assetz Exchange to invest a small amount (£100) of my own money initially and will report back on PAS about how my portfolio fares. Here is how it’s looking at the time of writing, roughly a month after I opened my account. As you can see, my initial investment has grown by £3.87 from a combination of income received and capital growth. For a month that’s not bad at all – if it carries on growing at that rate I’ll be delighted! – but of course it is much too soon to draw any firm conclusions from this.

I particularly like the fact that with the low minimum investment on Assetz Exchange, even if you’re starting very cautiously (as I am) it’s easy to build a diversified portfolio. I like the relative simplicity of investing on the website and the fact that you can exit an investment any time via the exchange (though that does depend on willing buyers being available at a price that is acceptable to you). It is also good that there are no charges associated with selling on the exchange.

You can, of course, withdraw uninvested funds from your Assetz Exchange account at any time.

Obviously there are risks in any form of investing and it is important to do your own ‘due diligence’ before proceeding. You should also bear in mind that this type of investment is not covered by the Financial Services Compensation Scheme, which covers savers with UK banks and other financial institutions up to £85,000. On the other hand, the potential returns are significantly better than the fractions of a percent typically on offer from savings institutions right now, while the risks appear to be at the lower end of the spectrum, with many of the properties on long-term leases with corporate/institutional tenants.

To be very clear, nobody should put all their spare cash into Assetz Exchange (or any other investment platform for that matter) but in my opinion there is definitely a case for including AE within a diversified portfolio.

As mentioned above, I shall be reporting back on how my Assetz Exchange investments perform on PAS in future. In the mean time, if you have any comments or questions about this post, or Assetz Exchange more generally, please do leave them below as usual.

UPDATE JANUARY 2025 – Assetz Exchange have now rebranded as Housemartin. They continue to operate as described above, but going forward will focus entirely on supported housing projects, as these have proven the most reliable and hassle-free (not to mention the social/community benefits). For more info, see my new blog post P2P Property Investment Platform Assetz Exchange Rebrands as Housemartin.

Disclaimer: I am not a registered financial adviser and nothing in this post should be construed as personal financial advice. You should always perform your own ‘due diligence’ before making any investment and speak to a qualified professional adviser if in any doubt how best to proceed. All investments carry a risk of loss.

Please note also that this review uses my affiliate links. If you click through and make an investment or perform some other qualifying transaction, I may receive a commission for introducing you. This will not affect any charges you pay or the product/service you receive.

If you enjoyed this post, please link to it on your own blog or social media:

At the time of writing there is just over a fortnight till the end of the 2020/21 ISA season. That is all the time you have left to make use of this year’s allowance of £20,000 before it is gone forever.

If you haven’t already used your allowance – and you have money available to invest – it is therefore essential to take action now. Investing via an ISA means that any profits you make will be free of Income Tax, Dividends Tax or Capital Gains Tax. And you won’t even have to declare it on your tax return, which if you’re anything like me will be a welcome simplification…

You can of course put your money into a Cash ISA, but the rates of return on such accounts are currently derisory, and basic rate taxpayers now have a £1000 tax-free savings allowance anyway (higher rate tapayers get £500 and top rate taxpayers nothing at all). The argument for investing in a cash ISA is therefore weak for most people, although if you think interest rates are likely to rise significantly in future there might still be a case for using one. Count me out, though 🙂

That leaves Stocks and Shares ISAs and the relatively new Innovative Finance ISAs (which are mainly for P2P lending). You can invest in either or both of these ISAs up to your annual £20,000 limit, though you can only put money into one of each type in any tax year. In today’s post I wanted to reveal some ways you may be able to get an extra cash boost if you plan to invest in an ISA in the next couple of weeks.

Table of Contents

Cashback Sites

I have mentioned cashback sites on various occasions on Pounds and Sense. Basically, these sites refund some of the commission they receive from ‘introducing’ you to a company if you click through to it via a link on the cashback site. The two best-known cashback sites in the UK are Top Cashback and Quidco, though newcomers My Money Pocket are also worth joining and checking out. You might also like to try Cashback Angel, a comparison service for UK cashback websites, which I reviewed here recently.

Clearly you will need to sign up for an account with a cashback site before you can get any cashback from them. I highly recommend registering with Quidco and Top Cashback and maybe My Money Pocket too, even if you aren’t planning to invest in an ISA immediately.

So what cashback offers are currently available with ISAs? On Top Cashback (my personal favourite) one of the best comes from Fidelity. They are offering a maximum of £160 cashback if you open a new Fidelity Stocks and Shares ISA with a minimum deposit of £15,000. But even if you begin with as little as £2,500, you will get £50 cashback. You have to be a new customer and remain invested for a minimum of three months to get the cashback.

If you invest in a Shepherds Friendly Stocks and Shares ISA, an even more generous top payment of £305 is on offer for a maximum £20,000 ISA investment. Or you can earn up to £300 cashback if you set up monthly deposits, though to get this amount you will need to put in £1,500 a month or more. Again, you must remain invested for a minimum of three months to receive the cashback.

Over on Quidco there are also some great offers. With Foresters Friendly Society, for example, at the time of writing you can get £244 cashback with a maximum £20,000 investment. Or you can get £40 cashback with a minimum initial investment of £5,000 (other options are available as well). Again, you must remain invested for a minimum of three months to receive the cashback.

Please be aware that cashback offers change frequently, so I can’t promise that the exact offers mentioned above will still be available by the time you read this post.

For more ideas, just browse the Investment category on either Top Cashback or Quidco. Alternatively – or in addition – you can try searching for any ISA provider you are interested in to see if they have a cashback deal on offer.

Obviously you shouldn’t invest in an ISA purely for the cashback. But if you are thinking of doing so anyway, it is well worth checking what deals are available on cashback sites to get the benefit of the extra money available.

Special Offers

Of course, all investment platforms know that now is a peak time for ISA investment, so they compete extra vigorously to attract new customers. It is therefore well worth shopping around right now to see what offers are available.

In addition, as an ISA investor and money blogger myself, I have access to some special deals and bonuses that I can offer my readers. I’ve put a couple below, both with ISA providers I have invested with personally.

Kuflink

Kuflink is a P2P property loans platform I have been investing with for around three years now. They offer a range of investment options, including an IFISA. They have a generous welcome offer, where you can earn up to £4,000 cashback on a £100,000 investment. Of course, that’s well over the ISA annual limit. But if you invest £20,000 in an IFISA with Kuflink you can get 3 percent cashback or £600, which still isn’t too shabby. For more information about Kuflink and their welcome offer, check out my Kuflink review.

Nutmeg

Nutmeg is a robo-adviser investment platform I have been investing with since 2016. As you will see from my Nutmeg review, I have enjoyed very good returns from them (55.5% to date). They offer a Stocks and Shares ISA using ETFs (Exchange Traded Funds). If you sign up with Nutmeg via my link, while I can’t offer you a cash bonus, you will get six months’ portfolio management free of charge.

I hope this post has encouraged you to use your 2020/21 ISA allowance before it’s gone and maybe take the chance to pocket a bonus or cashback as well. If you have any comments or questions, as always, please do leave them below.

Disclaimer: I am not a professional financial adviser and nothing in this post should be construed as individual financial advice. Everyone should do their own ‘due diligence’ before investing and seek advice from a qualified financial adviser if in any doubt how best to proceed. All investment carries a risk of loss. In addition, please be aware that some links in this post include my affiliate (referral) code, so if you click through and make a purchase, i will receive a commission for introducing you. This will not affect in any way the terms and benefits you receive,. Indeed, as stated above, some offers are only available to people investing via my link.

If you enjoyed this post, please link to it on your own blog or social media:

FI Money (as I’ll call it for short from now on) is a self-published paperback of 222 pages (it’s also available as a Kindle ebook). It is organized into 28 main chapters plus additional material. I won’t list all the chapters here, but here are the first ten to give you a flavour of the content (and style).

Force yourself to smile

YouTube obsession

Your relationship with money

Overthinker

Understanding our ‘Chimp’ emotions

Goals written down

Crystal clear goals

Stress less

Mental training

How NOT to invest

FI Money is a personal account of one man’s journey towards financial independence (the FI referred to in the title). It is a self-development book, but as Peter says in the Introduction it isn’t the usual success story typically associated with such books. He says, ‘I am a work in progress, similar to a building under construction.’

The chapters are generally quite short. They are well written and broken up with bullet-points, headings, To Do lists, and so on. Peter focuses on different aspects of his quest for financial independence, with a particular emphasis on buy-to-let. As this is not something I have ever got into myself (apart from some investments on property crowdfunding platforms) I was particularly intrigued by this. Peter talks about his experiences with refreshing honesty and is not afraid to disclose some of the mistakes he has made along the way. If you’re thinking of investing in buy-to-let yourself, there are some valuable lessons to be learned here.

The book covers many other subjects as well, including property renovation, tax, investing, keeping records, and more. I particularly enjoyed Chapter 10 ‘How NOT to Invest’ which focuses on some of Peter’s less successful investments. These include Premium Bonds (like me he’s not a fan), Bitcoin and other cryptocurrencies, and a particularly ill-advised buy-to-let project early in his career. There are some salutary lessons to be learned from all this (and a few laughs to be had as well!).

In addition to the practical advice, FI Money has a particular emphasis on the psychological aspects of achieving financial independence – the money mindset, as Peter calls it. He is a firm believer in building your financial knowledge, but also adopting the right emotional and practical disciplines and carefully planning and managing your journey towards FI. There is a lot of food for thought in the book from someone who really has been on this particular journey himself (or at least is well on the way there).

As mentioned earlier, Peter also runs a personal finance blog called Duffmoney. This is well worth a read as well, and will give you a flavour of Peter’s style and his attitude towards investing and money matters generally.

As always, if you have any comments or questions about this review, please do post them below.

Disclosure: In common with many posts on Pounds and Sense, this review includes affiliate links. If you click through and make a purchase, I may receive a fee for introducing you. This will not affect in any way the price you pay or the product or service you receive.

If you enjoyed this post, please link to it on your own blog or social media:

Here is my latest monthly Coronavirus Crisis Update. Regular readers will know I’ve been posting these updates since the first lockdown started a year ago now (you can read my February 2021 update here if you like).

I plan to continue these updates until we are clearly over the pandemic and something resembling normal life has resumed. Obviously, I very much hope that will be sooner rather than later.

As ever, I will begin by discussing financial matters and then life more generally over the last few weeks.

Financial

I’ll begin as usual with my Nutmeg stocks and shares ISA, as I know many of you like to hear what is happening with this.

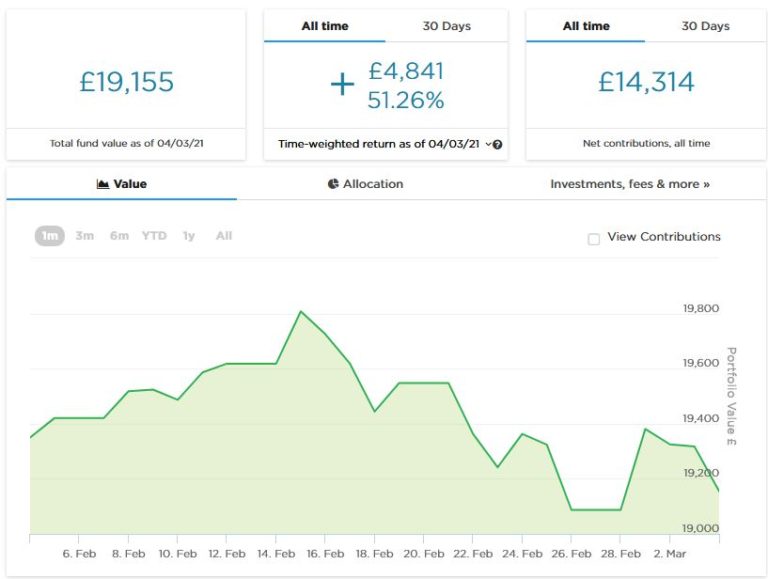

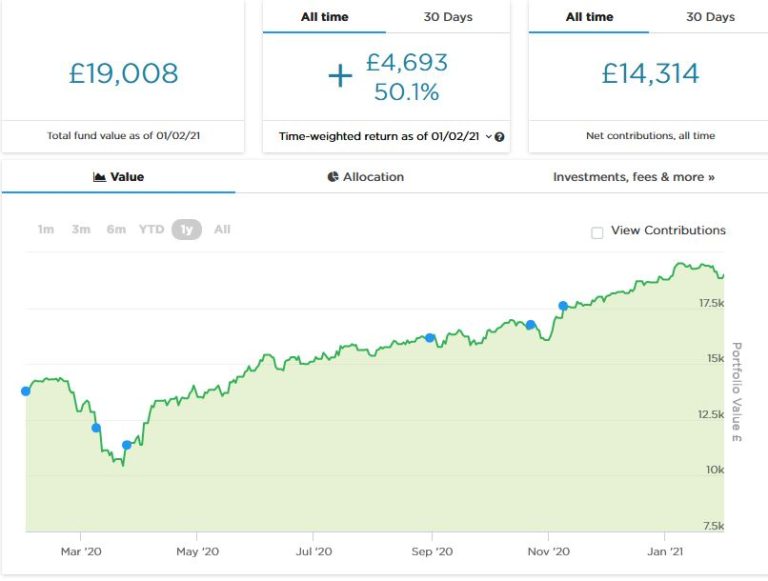

As the screenshot below shows, since last month’s update my main portfolio has been through some ups and downs. It is currently valued at £19,155. Last month it stood at £19,008, so it is at least up a little (£147) overall.

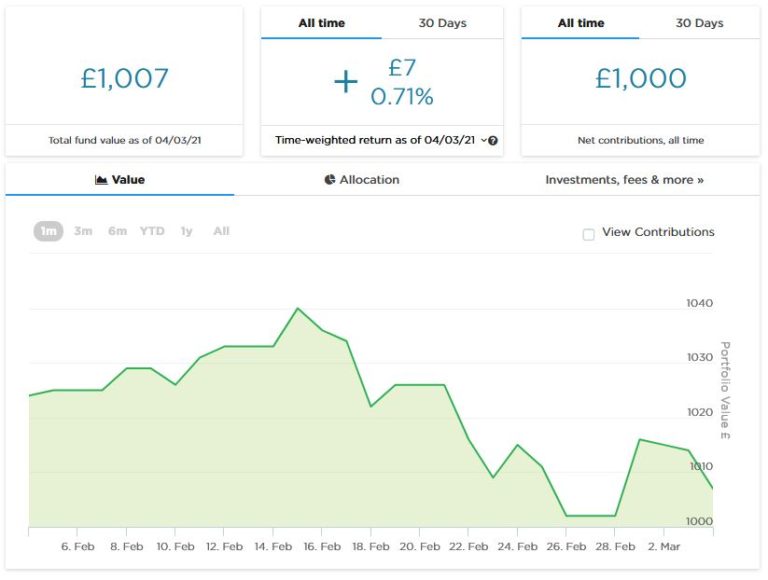

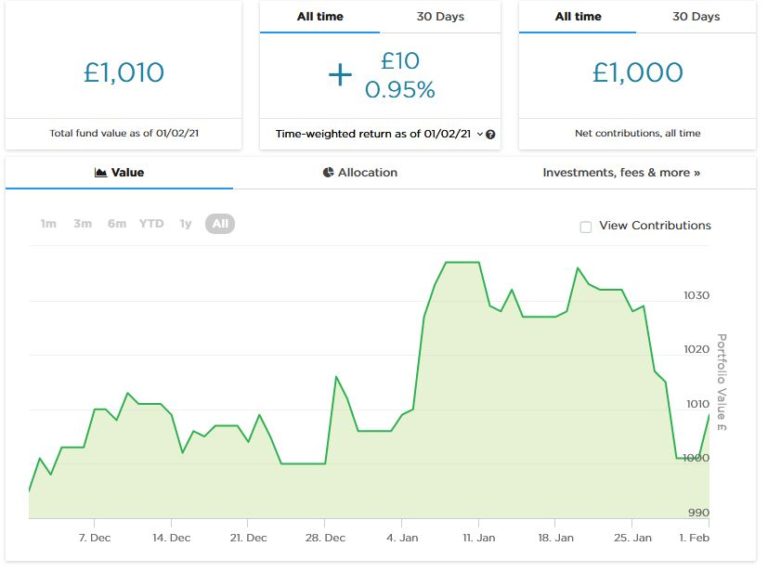

As you may recall, three months ago I put £1,000 into a second Nutmeg pot to try out Nutmeg’s new Smart Alpha option. The value of this pot rose as high as £1,040 in mid-February, though it currently stands at a more modest £1,007. Here is a screen capture showing performance to date, though obviously it is much too early to draw any conclusions from this.

I mentioned last time that my first investment with P2P property investment platform Property Partner reached its five-year anniversary, at which point investors can vote to sell their shares or continue for another five years. Along with just under half of the other investors, I voted to sell my shares.

The shares of everyone who wanted to sell were duly put up for sale on the platform. Unfortunately, though, there were few buyers, so with a substantial number of shares unsold, the property has been put up for sale on the open market. That means there will be a period of several months – possibly longer – before a buyer is found, and there is no guarantee that the independent valuation price will be achieved.

That is obviously disappointing, though as I only have a very small amount invested in this property (about £50) I’m not going to lose any sleep over it. In my view Property Partner didn’t make much effort to market these shares to investors. I suspect the same may be the case with at least some of the other properties coming up to their five-year anniversaries. It may be that Property Partner are happy to get some of the smaller houses and apartments off their books, especially the city-based ones for which demand has fallen as a result of the pandemic. Currently I have another small investment going through the five-year process. I voted to sell my shares in this too, but suspect the outcome will be the same.

As I have noted before on PAS, shares in many properties on Property Partner are currently available on the secondary market at a discount to the independent valuation price Based on my experiences to date, however, I would advise caution about regarding this as a buying opportunity. If properties that are relisted attract little interest from existing PP investors, they will have to be sold on the open market. In that case you are likely to have a long wait until you see any return on your investment, and there is no guarantee of an overall profit even then. I shan’t therefore be investing on the Property Partner secondary market for the foreseeable future.

That wasn’t the only disappointing financial news last month. Property crowdfunding investment platform The House Crowd unexpectedly announced that it was going into administration. I still have some investments with THC, though thankfully not as many as I did two or three years ago.

Apart from one small loan – which I accepted some time ago had gone south – my remaining investments are in traditionally crowdfunded properties, all of which are currently up for sale. The money is therefore secured by bricks and mortar, so I expect to get at least some of it back (and have of course been receiving dividend payments from rent received). As with other property crowdfunding platforms, each THC property is owned and managed by a separate Special Purpose Vehicle (SPV), which gives it legal protection from claims against THC by creditors. How this will pan out in practice remains to be seen, but I note that the administrators have said that their appointment is ‘not expected to have a material impact on investors.’

So I am being philosophical about this and awaiting further developments. These have undoubtedly been tough times for property investors, and regular readers will know that I also recently lost money with another property crowdfunding platform called Crowdlords. Overall, when you allow for my successful property investments and rental income, I am more or less breaking even, but even so (as I have said on the blog before) I am a lot more cautious about this type of investment nowadays.

Personal

February was another long, cold month, but at least there are signs of better times ahead now. The vaccine roll-out continues to go well and case numbers are dropping rapidly, giving us all hope for a return to something approximating normal life in the weeks and months ahead.

And, of course, we are heading into the spring now, with longer, brighter days and – eventually – the prospect of some warmer ones!

One thing that always lifts my spirit at this time of year – and especially in the current circumstances – is the arrival of spring flowers. In my garden I have crocuses and snowdrops out at the moment, and it won’t be long until the daffodils are in bloom. Here’s a photo of a flower bed in my front garden…

I had my first Covid jab in February, at the Whitemore Lakes mass vaccination centre near Lichfield. It was run by a team of NHS staff, military and volunteers. Everyone was friendly and efficient. The only slight blip came when I was checking in. I happened to notice that the clerk had put ‘female’ on my form, doubtless due to my lockdown hair. She was embarrassed when I pointed this out, but of course I couldn’t just say nothing. I shall be very pleased when we are allowed to visit hairdressers again!

I received the Oxford-Astra Zeneca vaccine. After I had a bad reaction to my last flu jab (fever and nausea) I was prepared for something similar with this, but thankfully that didn’t happen. Apart from very slight soreness in my arm the next day, I had no side-effects at all. I hope I am just as lucky with my second jab, which I have already booked for May.

Also on a medical theme. I had my latest trip to the eye clinic at Queens Hospital Burton last week. Regular readers will know that last autumn I was diagnosed with a perforated retina in my left eye. My first laser treatment was only partly successful, so Iast time I received a (more powerful) top-up treatment. This visit was to check if it had been successful, and I was pleased and relieved to hear that it had. So once again I need to express my thanks and gratitude to all the staff there, and especially to Mr Brent, the consultant who performed my final laser treatment and gave me the good news this time. I have been told that if something like this happens once it increases the chances of it happening again, so I have to be on the lookout for any potentially worrying changes to my eyesight in future. But that aside I am lucky that this problem was detected early before anything more drastic (e.g. a detached retina) occurred – so big thanks to my optician at Vision Express Lichfield as well!

As I write this update, the schools are just about to reopen to all students. I am delighted about that, as I know that it has been a tough time for many children. While some schools have been very good about running online classes, these can never be a complete substitute for face-to-face teaching. I also know from speaking to friends that some schools have been less supportive, simply sending pupils written lessons or assignments to complete on their own. That is obviously less than ideal for younger children especially.

I do think it is regrettable that the government has advised that secondary school children should wear masks in classrooms. The same applies to the mandatory twice-weekly testing. In my view these measures will achieve little apart from traumatizing young people and making it harder for them to learn. I understand these measures have been introduced partly to placate the teaching unions and some worried parents, but hope they will be swiftly withdrawn when (as I fully expect) there is no big ‘spike’ in virus cases following the return. Okay, I’ll get off my soapbox now!

As always, I hope you are staying safe and sane during these challenging times. If you have any comments or questions, please do post them below.

If you enjoyed this post, please link to it on your own blog or social media:

The world is an expensive place, so it’s no wonder many people are obsessed with getting freebies.

However, when entering the freebie-hunting world it is important that you adhere to certain rules in order to make the most of it. This article will set out some top tips for novice freebie-hunters – and you may learn a thing or two as a seasoned freebie-hunter as well.

Table of Contents

If It Sounds Too Good To Be True, It Probably Is

The excitement of (potentially) getting a freebie from a favourite brand can easily cloud your judgement.

According to Karen Newman at Mega Free Stuff, the majority of transactions have both an upside and a downside; however, when a transaction is free the downside is temporarily forgotten. ‘Free’ provides people with a strong emotional charge, where the individual perceives the item on offer to be more valuable than it actually is. This basically means that the person will set aside common sense if they are being offered a freebie.

Some companies are willing to give freebies, but fans of a brand are often willing to sell their soul (or at least provide all sorts of valuable personal information) in exchange for a minute sample. This is detrimental, and it is essential that you know how big the sample is and what exactly you will be getting. Be sure the freebie is genuine and always read the terms and conditions before applying for any offers.

If You Do Not Ask, You Will Not Receive

It is always worthwhile writing letters or sending emails to companies asking if they have any samples available for you to try. This may seem obnoxious and pointless to some, but those who complete this task have often received large boxes of free items or discount vouchers from the companies as a means of gaining feedback on their products. Furthermore, if you do not like a product, be honest about this. In many cases companies are happy to offer replacement freebies (plus an extra item) if their products do not meet with the user’s approval.

Do Not Expect Too Much

A full-sized freebie is a rare occurrence, with the majority of free products being delivered in small envelopes or tiny sachets. Of course, the primary goal is not to obtain a full-sized freebie but a free sample to see if you enjoy the product for a future purchase.

Furthermore, do not expect to receive all free items applied for. Even if you have claimed a free sample noted as available online, it is unlikely that you will get a 100% return. In fact, the most you can expect is approximately 70%. Do not give up hope and keep applying, and soon you will be enjoying masses of freebies. Once again, though, be sure to check that any freebie is worthwhile, and always read the terms and conditions regarding the size and number of samples.

Do Not Feel Guilty

While some individuals may feel a degree of guilt about asking for freebies, this is completely unnecessary. The company sending a freebie is not losing millions of pounds on the free products; in fact, they are benefiting from the free item. Think about it – for every sample sent out, there is the potential of a new customer. If you receive a free sample and like it, there is every chance you will make a future purchase of that product and might even become a regular customer.

Set Up a Second Email Address

One important – but often neglected – tip is to set up a second email address. To avoid receiving spam mail to your primary address, use this second address to claim freebies and enter competitions.

We have found an amazing competition here, where you can have the chance to win one of 20 Lindt chocolate Easter Eggs (see picture below). This competition ends on 1st April 2021.

Disclosure: This is a sponsored post for which I am receiving a fee.

If you enjoyed this post, please link to it on your own blog or social media:

Today I am looking at The Good Retirement Guide, an annual guide published by Kogan Page. I bought the current 2021 edition, which was published last month.

The Good Retirement Guide 2021 is 318 pages long. The text is fairly dense but broken up by plenty of headings and bullet-point lists. There are 14 chapters and an alphabetical index at the back. The chapter titles are as follows:

Are You Looking Forward to Retirement?

Money and Budgeting

Pensions

Tax

Investment

Your Home

Leisure Activities

Starting Your Own Business

Looking for Paid Work

Voluntary Work

Health

Holidays

Caring for Elderly Parents

No-one is Immortal

The chapter titles are pretty self-explanatory. The book attempts to cover every aspect of making the most of your senior years. The style is clear and readable, and additional resources are signposted as appropriate.

In contrast with Sod 60! which I also reviewed recently, The Good Retirement Guide covers the financial aspects of later life in some detail. I thought the information about pensions and benefits in particular was very good and tells you most of what you need to know.

Some of the other chapters are a bit less comprehensive. The one on leisure activities, for example, lists various things you might like to do – or take up – in retirement, but the information is frequently sketchy and can verge on stating the obvious. Here is what it has to say about poetry, for example:

There is an increasing enthusiasm for poetry and poetry readings in clubs, pubs and other places of entertainment. Special local events may be advertised in your neighbourhood.

And apart from a mention for the Poetry Society and a link to their website, that is all you get on this subject 🙂

I don’t want to appear too harsh. Obviously in a wide-ranging book like this, it can be hard to judge the degree of detail appropriate to any particular topic. At least by mentioning a wide range of possibilities, the book may give you some ideas about activities you might like to pursue further in retirement.

The health-related content is a bit of a mixed bag. Some subjects are covered in reasonable depth, others less so. There is just half a page devoted to keeping fit, for example, with a further couple of paragraphs about yoga and Pilates. On the other hand, there is some good information (and advice) on health insurance, long-term care plans, and so forth. Again, this illustrates that the book’s primary focus is on the financial aspects of retirement.

One thing that did surprise me is that although this 2021 edition of The Good Retirement Guide was only published last month, there is no mention of the pandemic in it. You will search in vain for Coronavirus or Covid-19 in the index. I know there can be long lead times in publishing, but in an annual guide you might think they could have inserted a section about it somewhere. Maybe we will have to wait for the 2022 version?

Even so, a lot of the subjects discussed in the guide – holidays, for example – have been seriously impacted by the pandemic. The advice and procedures for travel abroad in particular may be very different even after the pandemic is officially over.

Final Thoughts

Overall, I thought The Good Retirement Guide 2021 was a helpful book for people approaching retirement. As I’ve said above, it has a strong emphasis on financial matters, and is well worth reading for that alone. Some of the other content is a bit hit-and-miss, and the surprising lack of any mention of the pandemic means that at times it reads like a guide to an alternate world where Covid never happened. Of course, none of us really knows what the ‘new normal’ will be in future. We can but hope it will be not too far removed from the old normal we remember and which this book – despite the 2021 in its title – basically depicts.

As always, if you have any thoughts or questions about this post, please do leave them below.

Disclosure: As with many posts on Pounds and Sense, this post includes affiliate links. If you click through and make a purchase, I may receive a modest commission for introducing you. This will not affect in any way the price you pay or the product or service you receive.

If you enjoyed this post, please link to it on your own blog or social media:

As I write this we are still stuck in what feels like everlasting lockdown. But with the successful vaccine roll-out and rapidly falling case numbers – not to mention spring on the way – there are at least a few rays of hope on the horizon.

Anyway, to cheer you up, I’ve joined forces with some of my fellow UK bloggers to put together a giveaway with a top-of-the-range Dyson Airwrap worth £450 for the lucky winner.

As a mere male I must admit I had never heard of this before. But as I have read up about it now, I can tell you that the Dyson Airwrap is a high-tech hair-styling device. It harnesses an aerodynamic phenomenon called the Coanda effect, which curves air to attract and wrap hair to the barrel. So it styles using a flow of air, not extreme heat. This reduces the risk of heat-damage to your hair.

As I am currently sporting a mop of ‘lockdown hair’, I reckon I could probably do with one of these myself!

One lucky winner will win themselves the highly coveted Dyson Airwrap worth a whopping £450! The Dyson Airwrap is currently the hottest tool on the market and with it’s hefty price tag it’s not accessible for many.

The Dyson Airwrap comes with six hair styling attachments to dry, curl, wave and smooth hair. The Airwrap with intelligent heat control measures airflow temperature over 40 times a second and regulates heat, to ensure it always stays below 150°C.

The Dyson Airwrap also comes with a tan storage case to store your Airwrap and its attachments safely.

How to Enter

To enter simply complete all or any of the Rafflecopter entry options below. The more you complete, the more chances you have of winning.

The competition ends at midnight on Sunday 14th March and a winner will be drawn on Monday 15th March. If for any reason the chosen prize is out of stock at the time of the draw, the winner will be able to select an alternative prize up to the same value.

For full entry terms and conditions please see the Rafflecopter widget below.

One final small point is that if a winning entry comes from following someone on social media, the organizer (my colleague Neesha Rees) will check before awarding the prize that the winner is still following the account in question. If they aren’t, they will be disqualified and a new winner drawn. So, please, don’t follow and immediately unfollow, as your entry won’t then count.

Good luck, and here’s hoping we can all look forward to brighter times (and better hair) soon 🙂

If you enjoyed this post, please link to it on your own blog or social media:

In brief, Property Partner is a property crowdfunding platform. For the most part they specialize in ‘traditional’ property crowdfunding rather than loan or development finance.

Properties are bought and managed by Property Partner on investors’ behalf. Investors then receive a share of the rental income as dividends, and a share of any profits (plus return of their capital) when the property is sold.

Property Partner launched in January 2015. That date is significant, because after a property has been on the platform for five years, all investors get the chance to exit at a fair market price (determined by an independent surveyor). Due to the pandemic the five-year anniversary process was temporarily put on hold, but it is now proceeding again, albeit with delays as they work through the backlog.

How it operates is that in the run-up to the fifth anniversary of a property, all investors have the opportunity to say if they want to exit their investment at the valuation price or stay on for another five-year term (less than this if they subsequently exit via the resale market, of course).

All investors who have opted to leave will then have their shares pooled and put up for sale on Property Partner at the price stated. New investors are then able to buy these shares.

So long as all shares are sold, the original investors get their money (including any net profits) and the property continues under Property Partner’s management. If all shares don’t sell, however, Property Partner offer the property for sale on the open market. Investors then have to wait until the property is sold before getting their money back. As anyone who has been involved with buying or selling property will know, this is likely to take several months (quite possibly longer in the current circumstances).

The Opportunity

As Property Partner themselves have been pointing out, a number of properties that are coming up to their fifth anniversary are currently trading on the resale market at well below their latest valuation. Here is just one example:

This property in Tower Hill, London (not one I own shares in myself) is due to go through the fifth-anniversary process in April 2021 (or possibly a bit later due to the backlog). At the time of writing shares are available on the secondary market at a price of 91p, which is 28.28% below the latest valuation of £126.88. In theory, then, you could buy shares now and in the next few months sell up for a substantial short-term gain.

Of course, in practice it’s not as simple as that. Here are some reasons:

Nobody knows yet what the final five-year valuation will be. If it is lower than the current valuation (which is perfectly possible in the current economic climate) the net profit will be reduced, perhaps substantially.

There is no guarantee that the shares of all investors who wish to exit will actually sell on the platform. If they don’t, as mentioned, you could have a long wait before the property is sold on the open market. In addition, if this happens there is no guarantee that the property will sell at the valuation price. If it goes for less than this, your returns will be reduced accordingly.

There are platform fees to take into account. In particular, there is a 1% fee for buying on the secondary market and a further 0.5% stamp duty reserve tax charge. Thankfully there are no exit fees, though.

And finally, the number of shares available for any property on the secondary market is limited. Obviously the number you can buy depends on how many shares other investors want to sell at the price in question.

On the plus side, for the length of time you hold the shares you may receive monthly dividends at a rate between 1.5% and 6% per year (though dividend payments on some properties are currently suspended due to Covid). This will offset the fees mentioned above; but if you only intend to hold the shares for a few months it probably won’t cover them completely. Bear in mind that an Assets Under Management (AUM) fee is now deducted from dividends as well.

As an investor with Property Partner since almost the beginning (the cover image shows a property in Torquay I own shares in – I plan to retire there one day 😀 ), I am awaiting the five-year exit for my investments with considerable interest.

My personal circumstances have changed since I started investing with the platform, so I intend to take the opportunity to offload at least some of ‘my’ properties. Indeed, I have already voted to sell my shares in the first property I ever invested in with Property Partner (20 Phillimore Close) and am waiting to see how this pans out. I will update this post in due course once I know.

Nonetheless, I am still considering investing short term on the resale market to take advantage of the opportunity the five-year anniversary presents. In particular, I have already topped up my investments in some of the properties I already hold but am planning to dispose of.

I will, though, be cautious until I have a better idea how the first few five-year anniversaries have passed, so I can see if all shares put up by investors sell on Property Partner, or if they have to sell the properties concerned on the open market. As mentioned earlier, the latter route will clearly take longer and there is no guarantee what price would be achieved.

Would I recommend someone who is currently an investor in Property Partner to look into this? Yes, certainly. Whatever your current circumstances, you need to be aware of what is going on with any properties you hold with Property Partner. And if you wish to sell, you should definitely consider taking advantage of the five-year exit mechanic. Equally, if you have money available to invest, you could check out the opportunities buying now on the resale market – though do bear in my mind my cautionary comments above.

If you haven’t joined Property Partner, and you like the idea of investing some of your portfolio in property, the platform is certainly worth a look. As older properties come back on the market for new investors, there will be no shortage of opportunities in the months ahead. And my understanding is that, as the original costs of acquisition have been amortised, there will be less costs to cover from investors, thus boosting the potential returns from the properties in question.

In addition, as these properties have a five-year history already, you will be able to check how they have been performing in terms of dividends generated and capital appreciation. This is no guarantee of how well or badly they will do in the future, of course.

Take a look at my Property Partner review for much more information about the platform and how it works. Also, if you do decide to invest in Property Partner, there is a welcome bonus offer. For convenience I have copied details below from my review.

Welcome Offer

As an existing Property Partner investor, I can offer a special bonus for anyone joining via my link. If you click through this special invitation link, sign up and invest a minimum of £2,000 within 60 days, you will receive an extra bonus as follows (and so will I):

Not only that, once you are an investor with Property Partner, you will be able to offer the same bonus to your friends and relatives and earn commission yourself. There is no limit to the number of people you can introduce through this scheme.

If you have any comments or questions about this post, as always, please do leave them below.

Note: This is a fully updated version of a post published in 2019.

Disclosure: this post includes referral links. If you click through and make an investment, I may receive a commission for introducing you. This has no effect on the terms or benefits you will receive. Please note also that I am not a professional financial adviser. You should do your own ‘due diligence’ before making any investment, and seek professional advice from a qualified financial adviser if in any doubt how best to proceed. Be aware that all investments carry a risk of loss.

If you enjoyed this post, please link to it on your own blog or social media:

Here is my latest Coronavirus Crisis Update. Regular readers will know I have been posting these since the first lockdown started in the spring of 2020 (you can read my January 2021 update here if you like).

I plan to continue these updates until we are clearly over the pandemic and something resembling normal life has resumed. Obviously, I very much hope that will be sooner rather than later.

As ever, I will begin by discussing financial matters and then life more generally over the last few weeks.

Financial

I’ll begin as usual with my Nutmeg stocks and shares ISA, as I know many of you like to hear what is happening with this.

As the screenshot below shows, since last month’s update my main portfolio has been through some ups and downs. It is currently valued at £19,008. Last month it stood at £18,886, so it is at least up a little (£122) overall.

As you may recall, two months ago I put £1,000 into a second Nutmeg pot to try out Nutmeg’s new Smart Alpha option. The value of this pot rose as high as £1,037 in mid-January, though it currently stands at a more modest £1,010. Here is a screen capture showing performance to date, though obviously it is far too early to draw any conclusions from this.

Incidentally, I was recently asked by Nutmeg to contribute an article about my ‘Investing Journey’ for their blog. This was published in early January and you can read it here if you like. In the original version I was more explicit about why I left the charity I used to work for (basically a personality clash with the new Director who saw me as a rival). Nutmeg presumably decided this might ruffle a few feathers – even 25 years on! – so they changed it to something blandly neutral. Anyway, I thought I should let you know, as the opening section reads a little oddly now 🙂

The Nutmeg article brought quite a few new subscribers to this blog – so if that includes you, welcome to Pounds and Sense! I do hope you find my posts interesting.

Moving on, I had an email this week from the peer-to-peer lending platform RateSetter saying that all their lending activity is being transferred to Metro Bank (which now owns RateSetter). All investor accounts are therefore closing at the start of April, with investors’ money being returned to them in full along with all interest due.

I know some RateSetter investors are unhappy about this, but personally in these turbulent times I’m just glad to be getting my money back with interest. I originally invested £1,000 in September 2018 with an eye to claiming the £100 new investor bonus. The latter was duly credited to my account a year later, so by April I expect there to be a total of around £1,180 in my account. That equates to an annual interest rate of around 7%, which I am perfectly happy with.

This last year has undoubtedly been tough for P2P lending companies, with rising default rates and withdrawal requests along with reduced demand for loans. This has caused some platforms to experience cashflow problems and bad publicity. The only other one I have any money left with is ZOPA, which has also had a challenging year. I have only a few hundred pounds left in ZOPA as I switched some time ago from reinvesting repayments to withdrawing them. I’m not sure I can see much of a future for P2P lending in the UK, but of course in these unique times anything is possible. I don’t foresee myself putting any more money into P2P lending for a while, though.

I also heard recently from Property Partner. As you may know, this is a property crowdfunding platform. A few years ago, when I was investing regularly in property crowdfunding, I put around £5,000 into twenty or so properties on this platform.

Anyway, the email revealed that the first property I bought shares in has now reached its fifth anniversary. All investors therefore have the opportunity to sell up at the current independent valuation or else continue for a further five years. I voted to sell my shares, since (as mentioned in this recent post) I am currently trying to reduce the total amount I have invested in property crowdfunding.

The way the five-year anniversary process works is that all shares owned by investors who want to sell are bundled together and put up for sale on the Property Partner site. Assuming they are all bought by other investors, everyone who voted to sell then gets their money back at the current valuation. If that doesn’t happen, Property Partner put the property concerned up for sale. But obviously that is likely to take months and there is no guarantee the valuation price will be achieved. So you might end up getting back less than anticipated (or perhaps more in a best-case scenario).

Obviously I’m hoping this process goes smoothly and I get my money back soon. I would comment, though, that many of the properties that are coming up to their five-year anniversary are on offer on the resale market at well under the current valuation price. So if you are of a speculative persuasion, there is an opportunity to buy shares now at a discount and maybe make a quick-ish profit through selling up via the five-year anniversary process. I must admit I am tempted to try this, but haven’t made a decision yet!

Moving on, my two Buy2LetCars investments are still delivering the promised monthly returns without any fuss. As I am semi-retired but don’t yet qualify for the state pension, the £450 or so I receive from them every month represents a major part of my monthly income currently. I am also looking forward to receiving a substantial lump-sum payment in April when my first investment with them matures.

As I’ve said before, investors with Buy2LetCars put up the money to finance a car for a key worker such as a nurse or police officer. They then receive 36 monthly capital repayments followed by a final balancing payment of interest and capital. If you are looking for an income-producing investment with a substantial lump sum payment after three years – and you like the idea of doing a bit of good with your money too – they are well worth checking out (and likewise if you’re a key worker looking for a lease car yourself). If you’d like to learn more, you can read my review of Buy2LetCars here and my more recent article about the company here. And here is a link to Wheels4Sure, their car-leasing website. Note that you can’t invest with Buy2LetCars through an ISA, so the interest part of the final payment will have some tax deducted. Depending on your circumstances, you may be able to reclaim this.

Finally, several more readers have now signed up with the low-key matched betting opportunity mentioned in some previous updates. New members are still being accepted, but the company has had to reduce their payouts slightly. New members now receive £50 a month for the first six months, reducing to £25 a month thereafter. Considering that this opportunity is cost-free, risk-free and hands-free, that’s still a pretty good deal, though 🙂

As I said above, this opportunity is based on matched betting, a sideline-earning opportunity I have been pursuing for several years myself. I was asked not to divulge too many details about it publicly, for good reasons I will explain privately to anyone who may be interested (and no, it’s not illegal!). As I said above, it doesn’t require any financial outlay, is entirely hands-off, and will provide a passive income of £50 a month for the first six months and £25 a month thereafter.

No knowledge of betting is required, and you don’t have to place any bets yourself (this is all done by the company’s clever software). You just have to set up a separate bank account for bets to go through, but running the account is entirely financed by the company. Please note that this opportunity is only open to honest, trustworthy people who haven’t done matched betting before and have no more than two accounts already with online bookmakers. For more info (and to receive a no-obligation invitation) drop me a line including your email address via my Contact Me page.

Personal

I don’t know about you, but January to me has felt a very long month. It’s been cold, damp and depressing, with the whole country stuck in what seems like a never-ending lockdown.

As you may know, I live on my own since my partner, Jayne, passed away a few years ago. I am lucky to live in a fairly large house with a good-sized garden, so being mostly confined to home hasn’t been as big a challenge for me as I’m sure it has for some. Also, I am well used to working from home, having done this for the last 30 years or so. Even so, being unable to see friends and family has been hard for me, as has the closure of my local swimming pool (which I used to visit twice a week). And I appreciate that in many ways I am one of the lucky ones. I don’t have any major financial worries, and I’m not trying to home-school any children!

I did have a ‘day out’ at the end of January when I had to go to the eye clinic at Burton Hospital for a follow-up appointment. As regular readers will know, in the autumn I was diagnosed with a perforated retina in the left eye. I had laser treatment for this, and my January appointment was to assess how successful it had been.

As it turned out, there was some good news and some bad. The consultant told me that the treatment had been three-quarters successful. In one area it hadn’t ‘taken’, meaning I needed top-up treatment. He administered this then and there. I guess he cranked up the laser a bit, as unlike my first treatment it was somewhat painful and I had a headache for a couple of days afterwards. I have to go back at the start of March for what I very much hope will be a final check-up. Keep your fingers crossed for me!

Because they put drops in my eyes at these appointments, I can’t drive. I therefore took a taxi to the hospital and caught the train back. On previous occasions the trains have been very quiet, but there were noticeably more passengers this time. The roads too seemed pretty busy. I get the impression that people are (understandably) becoming fed up with lockdown now and the government’s Stay At Home message isn’t being as well complied with. Not a criticism, just an observation.

I am still aiming to go out for a walk once a day, though with some of the bad weather in January, I have missed a few. Here is a photo of my front garden about a fortnight ago 😮

On the plus side, I do enjoy watching the snow as long as I don’t have any essential trips to make. And I like to go for a walk in it once it has fallen. It was lovely to see (and hear) the local children getting out their sledges and enjoying some much-needed fun during these difficult times.

As far as evening entertainment is concerned, I finished my box-set of the tongue-in-cheek detective series Agatha Raisin and am happy to recommend that. On a similar note, I am enjoying the new (second) series of The Mallorca Files, which is currently on BBC iPlayer. It is just a shame that because of the pandemic they were only able to record six episodes.

Also, inspired by this post by my fellow blogger Caz, I have been investigating what is on offer on Amazon Prime Video. I have Amazon Prime mainly for the fast, free deliveries. But of course members do get access to a range of free films and TV series as well.

Anyway, I found a couple of series I really enjoyed. Being a Star Trek fan, I had to check out Lower Decks, a cartoon series focusing on the junior ranks on board one of the Federation’s least illustrious starships, the USS Cerritos. This has some great laugh-out-loud moments but some good stories as well. There are plenty of allusions to familiar Star Trek tropes that will keep any fan of the franchise amused. Watch out also for an appearance by an evil incarnation of Microsoft’s infamous ‘Office Assistant’ Clippy!

Of course, if you’re a Star Trek fan and haven’t yet seen Star Trek: Picard featuring the great Patrick Stewart as the eponymous hero, you should definitely watch this on Amazon Prime Video as well 🙂

The other series I enjoyed is Undone. Indeed, this is one of the best things I’ve seen on TV for quite a while. It’s almost impossible to describe, but it’s an animation that combines elements of mystery, comedy, romance, science fiction/fantasy, and more. And all with stunning, almost psychedelic, imagery, and strong acting and characterization. Here’s a screen capture that will give you some idea of the style. If you watch nothing else on Amazon Prime Video, give this a try..

Going back to the pandemic, there has at least been some good news this month. The vaccine roll-out has been going well – I’ve just heard that 10 million people have now had their first injection – and the number of new cases has been falling rapidly. As a 65-year-old I have not yet been called for vaccination but assume this is likely to happen fairly soon.

I do hope these developments will allow lockdown and other restrictions to be eased in the coming weeks, as in my view they are causing grave harm to people’s physical and mental well-being. In particular, I would like to see schools reopen, along with swimming pools and gyms. I would also like to see pubs, restaurants and hotels allowed to reopen before many have to close their doors for good. In the (slightly) longer term I would like to see all restrictions lifted so that normal life can resume. I am not a fan of mandatory masks and would like to see them made optional for those who believe they offer some useful protection from the virus (personally I have never been convinced of this).

As always, I hope you are staying safe and sane during these challenging times. If you have any comments or questions, please do post them below.

If you enjoyed this post, please link to it on your own blog or social media: