As you will doubtless know, yesterday the Chancellor delivered his 2023 Autumn Statement. This included various economic measures, which you can read about on the Moneysaving Expert website (among other places).

I thought today I would highlight one particular change to the rules about tax-free ISAs (Individual Savings Accounts) which caught my eye. From April 2024, you will be allowed to open more than one of any particular type of ISA in a single tax year. This is a change I was particularly pleased to see, and have in fact been advocating on Pounds and Sense for some time.

As you may know, there are various types of ISA, including the stocks and shares ISA, cash ISA and IFISA. The latter stands for Innovative Finance ISA and allows people to save tax-free with peer-to-peer lending and similar platforms. Everyone has an annual tax-free ISA allowance, which currently stands at £20,000. Despite rumours to the contrary, this limit was not changed in the Autumn Statement.

So why do I think the change in the rules announced yesterday is so important? Well, for one thing, it brings about much greater flexibility in ISA transfers. Investors will now be able to transfer funds freely between different types of ISA without jeopardizing their tax-free status. They will also be able to transfer just part of a holding to a different provider, regardless of when they paid in the money.

This will empower investors to optimize their investment strategy by making it easy to move money between cash, stocks and shares, and Innovative Finance ISAs. This enhanced transfer flexibility should enable investors to adapt to changing market conditions, seize new opportunities, and align their portfolios with their evolving financial goals.

A further benefit of the rule change is that it will make it easier for investors to build a well-diversified portfolio. Rather than having to put all their money into just one stocks and shares ISA per year (for example) they can divide it among a range of providers. Regular readers will know that I am a big fan of diversifying your portfolio as much as possible to help manage risk, and this rule change certainly facilitates that.

The change will also make it easier for investors to try out new platforms with relatively small investments initially. Previously they may have been deterred from doing this by the realization that once they had committed to one particular provider, they would have to stick with that provider for the rest of the financial year. FOMO (fear of missing out) may even have inhibited some people from investing at all.

This is certainly something I’ve experienced myself. At the start of a new financial year, I was wary of investing in any type of ISA, because I knew that once I did so, I would then have to stick with that provider for that type of ISA for the rest of the financial year.

So those are just some reasons I particularly welcome this rule change. From a broader perspective, I think it will also encourage more people to start investing, which has to be good for UK PLC in general. Apart from a few admin costs, it seems to me this measure will cost the government nothing, while bringing major benefits to the economy and individual investors. Really, the only thing I don’t understand is why it wasn’t done sooner!

So those are my thoughts anyway. But what do you think? Will the new rule encourage you to make more use of ISAs in future? I’d be interested to hear any views.

If you enjoyed this post, please link to it on your own blog or social media:

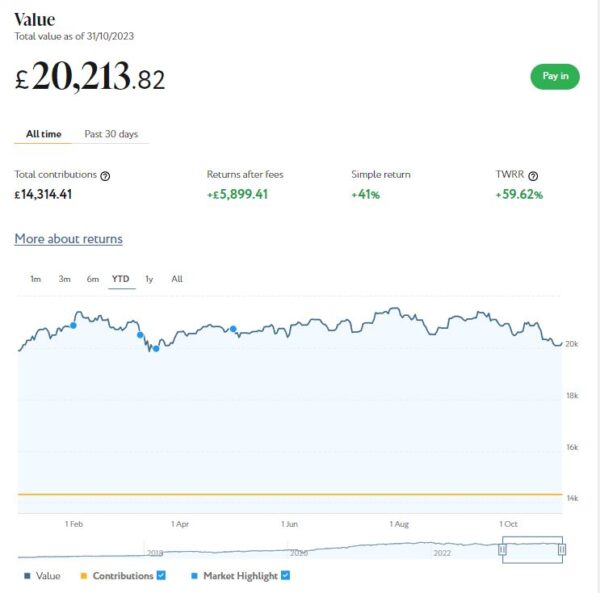

I’ll start as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

As the screenshot below for the year to date shows, my main Nutmeg portfolio is currently valued at £20,214. Last month it stood at £20,945 so that is a fall of £731.

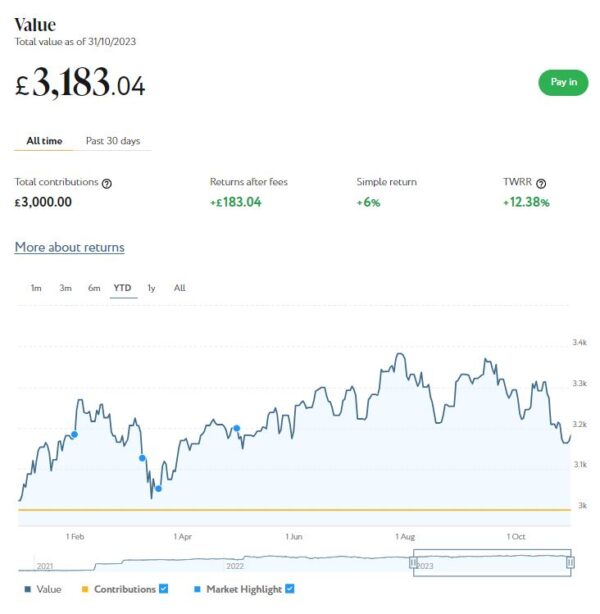

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £3,183 compared with £3,295 a month ago, a fall of £112. Here is a screen capture showing performance since the start of this year.

The net value of all my Nutmeg investments has fallen this month by £843 or 3.47% month on month. That’s obviously disappointing, but both pots are still up on where they were at the start of the year. Their total value has risen by £476 (2.08%) since 1st January 2023. I’m not saying that’s anything to cheer about, but due to world events nearly all stock market investments have taken a hit in the last few weeks, and Nutmeg is no exception.

As I always say, investing is (or should be) a long-term endeavour. Over a period of years stock market investments such as those used by Nutmeg typically produce better returns than cash accounts, often by substantial margins. But there are never any guarantees, and in in the short to medium term at least, losses are always possible.

As you may know, I recently revised and updated my full Nutmeg review. This was mainly to incorporate details of their new thematic investment option, but I took the opportunity to update some other information and performance stats as well.

As it says in the updated review, the new thematic style provides a globally diversified, risk adjusted portfolio with a tilt (up to 20% of equity exposure) towards your chosen theme. The majority of the portfolio will be actively managed by Nutmeg’s investment team, whilst the ’tilted’ part of the portfolio will be made up of ETFs that their investment team believes will deliver the best returns from the trend in question (to be reviewed annually).

Currently three themes are available, these being Technical Innovation, Resource Transformation and Evolving Consumer. For more details about what each of these comprises, check out the Nutmeg website.

Nutmeg thematic portfolios are only available on Risk Level 5 or above. There’s a minimum investment of £100 for Junior ISAs and Lifetime ISAs or £500 for stocks and shares ISAs and pensions. There is a 0.75% management fee.

I do quite like the new thematic styles on Nutmeg and may well be investing in one myself. They are similar in concept to the so-called smart portfolios on eToro, which I discussed in this recent blog post. Nutmeg’s thematic styles appear to be more broadly diversified, however, so may be a good choice for those who are new to thematic investing and want to dip a cautious toe in the water first.

You can read my full Nutmeg review here (including a special offer at the end for PAS readers). If you are looking for a home for your annual ISA allowance, based on my overall experience over the last seven years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs), Lifetime ISAs and Junior ISAs as well.

I also have investments with the property crowdlending platform Kuflink. They continue to do well, with new projects launching every week. I currently have around £1,400 invested with them in 12 different projects paying interest rates typically around 7%. I also have just over £600 in my cash account after several loans were recently repaid.

To date I have never lost any money with Kuflink, though some loan terms have been extended once or twice. On the plus side, when this happens additional interest is paid for the period in question.

As mentioned last time, Kuflink recently changed their terms and conditions. There is now an initial minimum investment of £1,000 and a minimum investment per project of £500.

Kuflink say they are doing this to streamline their operation and minimize costs. I can understand that, though it does mean the option to ‘test the water’ with a small first investment has been removed. It will also make it harder for small investors (like myself) to build a well-diversified portfolio on a limited budget.

One possible way around this is to invest using Kuflink’s Auto/IFISA facility. Your money here is automatically invested across a basket of loans over a period from one to three years. The rates currently on offer are shown in the graphic below.

As you may gather, you can invest tax-free in a Kuflink Auto IFISA. Or if you have already used your annual iFISA allowance elsewhere, you can invest via a taxable Auto account. You can read my full Kuflink review here if you wish.

Moving on, my Assetz Exchange investments continue to generate steady returns. Regular readers will know that this is a P2P property investment platform focusing on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my AE portfolio has generated a respectable £145.22 in revenue from rental income. As I said in last month’s update, capital growth has slowed, though, in line with UK property values generally.

At the time of writing, 6 of ‘my’ properties are showing gains, 2 are breaking even, and the remaining 16 are showing losses. My portfolio is currently showing a net decrease in value of £37.80, meaning that overall (rental income minus capital value decrease) I am up by £107.42. That’s still a decent return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Assetz Exchange most projects are socially beneficial as well.

Obviously the fall in capital value of my AE investments is disappointing. But it’s important to remember that until/unless I choose to sell the investments in question, it is largely theoretical, based on the most recent price at which shares in the property concerned have changed hands. The rental income, on the other hand, is real money (which in my case I have chosen to reinvest in other AE projects to further diversify my portfolio).

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of AE as far as i am concerned (especially now that Kuflink have raised their minimum investment per project to £500). You can actually invest from as little as 80p per property if you really want to proceed cautiously.

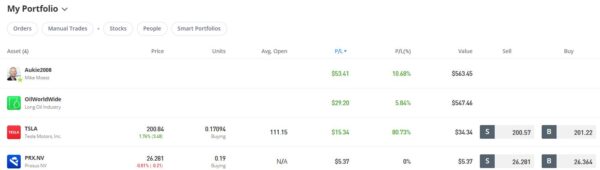

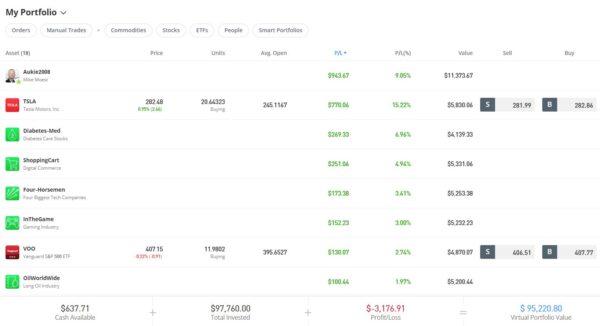

Last year I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios, Oil Worldwide. I also invested a small amount I had left over in Tesla shares.

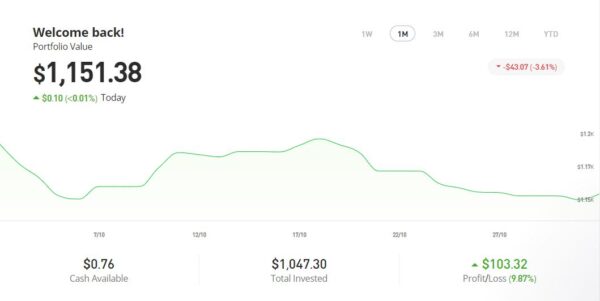

As you can see from the screen captures below, my original investment totalling $1,022.26 is today worth $1,151.38, an overall increase of $129.12 or 12.63%. in these turbulent times I am happy enough with that.

Incidentally, if you’re wondering what the bottom item in the list is (PRX.NV), it’s a partial share in Dutch internet company Prosus NV. I don’t honestly know where this has come from – it’s not something I deliberately bought. I assume it may be some sort of bonus from eToro, or maybe it’s connected with my copy trading account with Dutch investor Mike Moest. But I’m happy to have it in my portfolio, obviously!

eToro also recently introduced the eToro Money app. This allows you to deposit money to your eToro account without paying any currency conversion fees, saving you up to £5 for every £1,000 you deposit. You can also use the app to withdraw funds from your eToro account instantly to your bank account. I tried this myself and was impressed with how quickly and seamlessly it worked. You can read my blog post about eToro Money here.

I had two more articles published in October on the excellent Mouthy Money website. The first was How to Make Money From Retail Deal Arbitrage. This is a relatively under-used approach to online auction trading (though you don’t necessarily have to use online auctions at all). It normally proceeds one item at a time, so you don’t need large amounts of space (or capital) for stock. You can ramp it up to multiple items later if you like, though.

I also wrote Could You Make Money as a Freelance Proofreader and Editor. This can be a great sideline, or even a full-time business, for anyone who enjoys working with words. No special tools or equipment are required, so it’s quick, cheap and easy to get started. It’s reasonably paid, and you can work from home at hours to suit yourself. It’s also suitable for older people and people with disabilities (with the one proviso that it becomes harder if – as in my own case – your eyesight isn’t as good as it once was).

I also updated my article published last month titled Will a Heat Pump Save You Money? This is obviously a hot topic and one where policy is constantly changing. I thought I should update it with the latest information about government bribes – sorry, incentives – to get one. Do take a look if you haven’t already!

As I’ve said before, Mouthy Money is a great resource for anyone interested in money-making and money-saving. I particularly like the ‘Deals of the Week’ feature compiled by Jordon Cox (‘Britain’s Coupon Kid’) which lists all the best current money-saving offers for savvy shoppers. Check out the latest edition here

I am also a fan of my fellow MM contributor and money blogger Shoestring Jane. She writes mainly about money saving and frugal living. Her articles – such as this one on Frugal Swaps to Save You Money – are always worth a read. You can see all her articles for Mouthy Money via this web page.

I also published various posts on Pounds and Sense in October. I won’t bother to mention those that are out of date now, but the rest are listed below.

Exploring the Potential of Investing in Alternative Rental Properties was a guest post by my colleague Jackie Edwards. Jackie is a semi-retired property developer and restorer. In her article she presents the case for businesses and individuals to invest in rental properties for the growing over-50s market. At the end of the article I also suggest an alternative method for those whose pockets may not be as deep to invest in this field.

I also published Will You Get the Warm Home Discount? The 2023/24 WHD scheme opened in October. As last year, those eligible will receive a £150 discount off their energy bills. Most people no longer have to apply for WHD and should receive it automatically. Read the article to learn more, along with other support towards the cost of your energy bills that you may also qualify for.

Finally, I published a short post about Over 60s Discounts, a new website dedicated to helping older people save money. It’s free to sign up, and there are loads of savings, discounts and concessions on offer. Read my blog post for more info, and check out the website yourself!

On other matters, the opportunity to Get a Free ETF Share Worth up to £200 with Wealthyhood is still open. This DIY wealth-building app is aimed especially at people new to stock market investing. The minimum investment to qualify for the free share offer was raised recently from £20 to £50 – but on the plus side, they now guarantee that your free ETF share will be worth at least £10. What’s more, for the next two months Wealthyhood say they will plant a tree for every new account opened, so what’s not to like 🙂 🏝

Another thing that happened in October is that I finally got some of my money back from the Bricklane property REIT. I invested several thousand pounds in this a few years ago. At first all went well, but then came the Grenfell Tower tragedy followed by the cladding scandal.

Bricklane (or more precisely investors such as me) owned a number of properties which required (expensive) remedial work. Bricklane didn’t go into liquidation, but they felt they had no option but to sell their entire property portfolio and distribute whatever funds were generated (after all costs had been covered) to investors.

Anyway, to cut a long story short, investors in the Bricklane London fund (including me) should all now have been repaid. I got about £880 of my £1,000 investment back, which I suppose isn’t too bad considering. The Bricklane Regional Capitals fund, in which I also invested, is taking a bit longer to wind up, and I am not expecting to see any return from this until some time next year.

Finally, a quick reminder that you can also follow Pounds and Sense on Facebook or Twitter (or X as we have to learn to call it now). Twitter/X is my number one social media platform these days and I post regularly there. I share the latest news and information on financial (and other) matters, and other things that interest, amuse or concern me. So if you aren’t following my PAS account, you are definitely missing out!

That’s all for today. As always, if you have any comments or queries, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media:

Today I have a guest article for you by my colleague Jackie Edwards.

Jackie is a professional property investor and property restorer. In her article below she sets out the case for investing in alternative rental properties – in particular, for the growing over-50s market.

Over to Jackie then…

While discussion around the mortgage and rental market often focuses on younger people – particularly first-time buyers and millennials – just as important are the over 50s.

A 2022 report in The Guardian sheds light on an alarming trend: individuals over 50 are finding themselves compelled into room-sharing arrangements, a consequence of being priced out of independent living options. The data supports this unsettling shift, citing a steep 114% surge in room search enquiries from people aged 45-55, compounded by a staggering 239% uptick in enquiries from those in the 55-64 age bracket.

Despite being often well-experienced and highly skilled, these individuals find themselves at the mercy of a punishing housing market. This situation signals a promising investment opportunity for businesses and individuals prepared to invest in accommodation tailored for those aged over 50. Already, a handful of forward-thinking schemes across the nation are demonstrating this growing potential.

What’s Required

Of course, a range of factors need to be considered when providing bespoke housing to over-50s. Disability, for example. According to the Office of National Statistics, the incidence rate of disability increases significantly after the age of 50, and it becomes more likely that the applicant will need adaptations to their accommodation.

As anyone living with a disability will know, it can be difficult to find accessible housing. According to disability advocates Eachother.org.uk, only 9% of UK rentals are suitable for people with a disability. Landlords that can prepare and provide accessible accommodation, at reasonable asking prices, will be providing a valuable service which is very much in demand.

What a Rental Requires

With that in mind, it’s important to consider the specific needs of the 50s-and-over market. According to PropertyRoad.co.uk, 15% of all rentals are now occupied by people over 50, an increase of 61% from the previous recorded figures in 2012. This may not necessarily be a bad thing, however.

In the Guardian’s survey of the renting situation, an interesting factor was highlighted. While many older people are pushed into renting as a result of rising costs, many others actually prefer the flexibility of not being tied to a mortgage and, crucially, the feeling of community that comes with communal living.

One scheme the Evening Standard highlights is a house sharing scheme that specifically matches up younger and older people, with company the key factor, but with a degree of agreement from the younger party to assist with chores and housework.

Intermediate Rent

As highlighted by ShareToBuy.com, intermediate rent is a scheme where renters agree to charge lower rentals (generally at least 20% below the standard private market rates in the area) in exchange for longer-term contracts. For the younger generation who may be looking to move around a lot, these schemes are less attractive. For over 50s, who are happy in one area and looking for something affordable for the medium to long term, it may well be an excellent option.

What is crucial is that landlords and property businesses offer these properties more widely in bespoke packages for over 50s. Currently the market in such properties is very limited, though a few smaller companies and organizations have embraced this challenge. They include Cohabitas, certain schemes on Spareroom, Flatmates.co.uk and RoomPortal.

More needs to be done with alternative rental accommodation for this niche – yet rapidly growing – demographic. A lot of focus is placed on millennials, but much more needs to be done for older renters, to help them find high-quality and long-lasting accommodation. For landlords and businesses who want to generate a stable rental income while also offering a valuable service to older individuals, this could represent a very appealing proposition.

About the author: A career in property investing led Jackie Edwards to develop a passion for restoring old homes. And even in her free time, she’s renovating her own with her husband. They’re both semi-retired (though by no means retirement age) and to keep her interest alive Jackie writes articles on home and lifestyle. In any free time she has, she’s walked by her two dogs Barker and Corbett and she volunteers for a local foodbank.

Many thanks to Jackie for an interesting and thought-provoking article.

Obviously not everyone will have the money to invest in alternative rental accommodation directly. If, however, you are attracted to the idea of investing in this sector, a more affordable option is presented by Assetz Exchange.

Assetz Exchange is a P2P property crowdfunding platform. They focus on lower-risk, socially beneficial accommodation, such as supported housing for people with physical or mental disabilities.

Properties are bought jointly by investors under the usual crowdfunding/P2P model. Most are then leased to charities and housing associations. This means they are securely funded and there is a low risk of defaults.

Of course, defaults could still happen in certain circumstances – but as investors jointly own the property in question, ultimately you could still expect to get your capital (or most of it) back when the property is sold.

I have been investing with Assetz Exchange since February 2021 and have gradually built up the amount I have with them. I put an initial £100 into AE in February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000. Since I opened my account, my AE portfolio has generated £143.56 in revenue from rentals. That’s a decent rate of return on my £1,000 (staged) investment and does illustrate the value of P2P property investment for diversifying your portfolio when equity markets are volatile (as at the moment).

I now have investments in 23 different projects and all are generating rental income as expected. Capital values have declined slightly overall – in line with the UK property market generally – but of course this isn’t really relevant until or unless you want to sell up. Overall I am very happy with how my AE investment has been doing, and the fact that projects are generally beneficial to society as well.

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of AE as far as I am concerned. You can actually invest from as little as 80p per property if you really want to proceed cautiously.

As always, if you have any comments or questions about this article, you are very welcome to post them below.

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media:

In April 2016 I invested some money with the Nutmeg investment platform. It turned out to be one of my better investments, so in this update I thought I’d say a bit more about it.

What Is Nutmeg?

Nutmeg is a low-cost online investment platform. It is aimed at people who want to invest to take advantage of the potentially better returns, but don’t want the hassle of researching every investment themselves. Nutmeg has 200,000 investors as of May 2024 and over £5 billion in Assets Under Management (AUM).

With Nutmeg you simply choose the type of account you want and your investment style and how long you want to invest your money for (you don’t have to stick to this, of course, although they recommend to remain invested for at least 3 years). You can deposit a lump sum and/or set up monthly payments. Nutmeg then invests your money in a range of Exchange Traded Funds (ETFs).

For those who don’t know, ETFs are a package of shares from a particular section of the stock market. For example, an ‘Asia Pacific ETF’ is a collection of shares from the Asia-Pacific region. ETFs are different to most investment funds in that they don’t usually have a manager running them. Instead, most ETFs are run by computers that regularly balance their portfolios automatically. This helps keep costs low, though there is of course no guarantee of returns. You can learn more about ETFs here if you wish.

Nutmeg currently has five different types of investment product on offer. They are as follows:

ISA (individual Savings Account) – These accounts have to be funded from your after-tax income, but they grow tax efficiently and withdrawals are free of tax. Everyone has a maximum annual ISA allowance, which is currently a generous £20,000.

SIPP (Self Invested Personal Pension) – A SIPP has the big attraction that you get tax relief on your contributions, so the government effectively tops up every contribution you make. On the downside, you can’t withdraw money from a SIPP until you are at least 55, and only a quarter of the money you withdraw is tax-free, with the balance counting towards your total taxable income.

Lifetime ISA – A Lifetime ISA, sometimes called a LISA for short, is a tax-efficient vehicle launched in 2016. You can use a LISA for one of two specific purposes – buying your first home or saving for retirement. You have to be under 40 to open a Lifetime ISA. The government will then top up any contributions you make with an extra 25%. The maximum you can contribute to a LISA is £4,000 per year.

Junior ISA – A Junior ISA is an ISA opened by a parent or guardian on behalf of a child under 18. In the 2022 to 2023 tax year, the savings limit for Junior ISAs is £9,000.

General Investment Account (GIA) – This is for when you have used up all your other tax-free allowances. You can use this for whatever you like, but there are no tax benefits or top-ups.

As with all investing, your capital is at risk. The value of your portfolio with Nutmeg can go down as well as up and you may get back less than you invest. Tax treatment depends on your individual circumstances and may be subject to change in the future.

My Own Experience

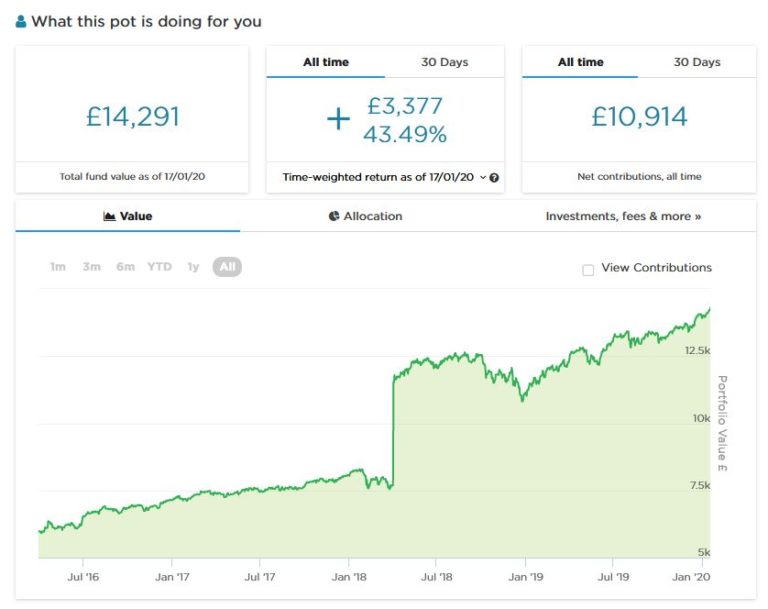

I invested £6,188 in a Fully Managed Nutmeg Stocks and Shares ISA in April 2016. If you’re wondering why it was such an odd sum, I put in £6,000 from my savings. The other £188 came from another small ISA account I thought I might as well transfer at the same time.

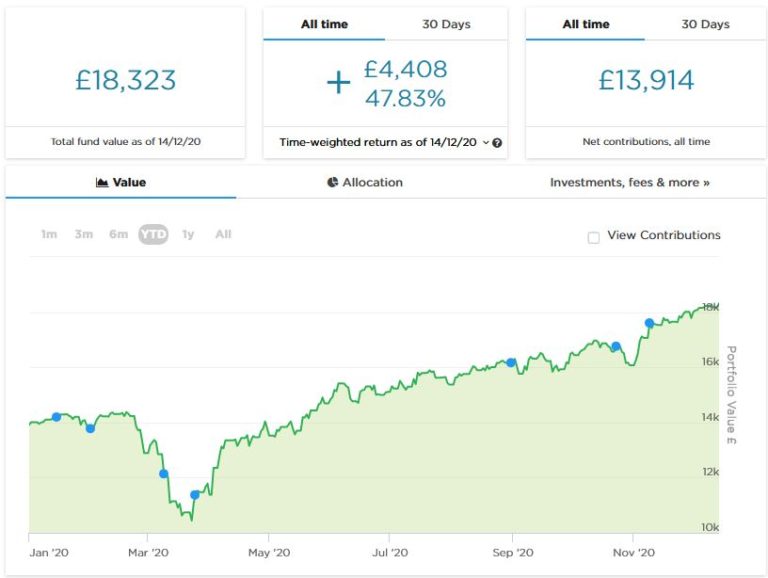

I was pleased by how my initial investment performed, so in April 2018 I transferred £4,000 from another stocks and shares ISA that had been under-performing. By January 2020 my investment had grown by £3,377 to £14,291. Here’s a chart showing how my investment performed up to 17th January 2020.

I accepted a high risk level (9/10) with this account, which may partly explain the performance achieved.

A few months ago I did a ‘deep dive’ into performance stats for Nutmeg fully managed portfolios from level 1 (lowest risk) to level 10 (highest risk). This confirmed that risk level does actually make a big difference to results obtained. You can read my article about this here and I strongly recommend that you do so if you are considering investing with Nutmeg. Obviously everyone needs to make their own decision about what level of risk they are comfortable with – but looking back over the last 10 years (since Nutmeg started) the higher the risk level you chose, the better the results you would have obtained over any three-year or longer period. Of course, past performance is no guarantee of what will happen in future, but it is certainly food for thought.

As with all investing, your capital is at risk. The value of your portfolio with Nutmeg can go down as well as up and you may get back less than you invest. Tax treatment depends on your individual circumstances and may be subject to change in the future.

2020 – Year of the Virus

In 2020 the markets were thrown into turmoil by the world-wide coronavirus pandemic. Inevitably, my Nutmeg portfolio was affected by this. Here is a chart showing performance from January to December 2020…

As you can see, through late February and March my Nutmeg ISA plummeted in value, going from around £14,000 to just over £10,000. That was obviously a worrying time, but nonetheless I decided to risk investing another £3,000 when the markets were (as things stand now) near their lowest ebb.

From late March – and even allowing for my £3,000 top-up – my ISA made a remarkable recovery. By mid-December 2020 it was worth £18,323. Even if you take off the extra £3,000, that means my portfolio as a whole was worth over £1,000 more than it was before the pandemic struck.

As with all investing, your capital is at risk. The value of your portfolio with Nutmeg can go down as well as up and you may get back less than you invest. Tax treatment depends on your individual circumstances and may be subject to change in the future.

2021 – Lockdown and Recovery

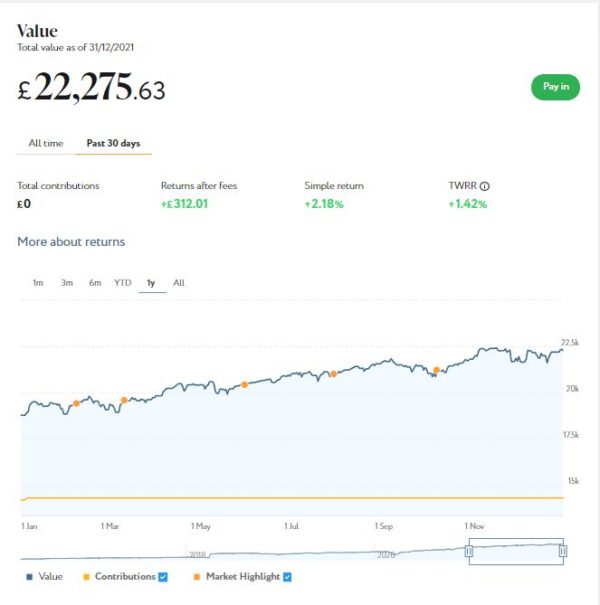

My Nutmeg ISA continued on a largely upward trajectory in 2021. Here is a screen capture showing how it stood at the end of December 2021. As you will see, Nutmeg have changed how performance is displayed on the website slightly.

I added a further £400 to my ISA eariy in the year. But even if you deduct this, the total fund value rose to £21,875.63, an increase of £3552 (over 21%) since December 2020.

As with all investing, your capital is at risk. The value of your portfolio with Nutmeg can go down as well as up and you may get back less than you invest. Tax treatment depends on your individual circumstances and may be subject to change in the future.

2022 – Ukraine and Cost of Living Crisis

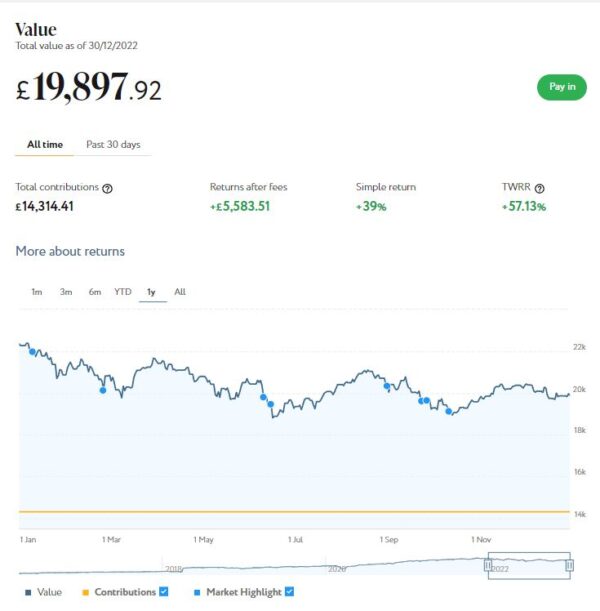

2022 was a challenging year for my Nutmeg investments. A variety of factors – including the war in Ukraine, rising inflation and the aftermath of the pandemic – have caused turmoil in world markets, and Nutmeg was obviously not immune. This is how my main portfolio performed in the year to 30 December 2022.

As you can see, my portfolio fell In value from £22,275.63 to £19,897.92. That’s a drop of £2377.71 or 10.68%.

That’s clearly disappointing, but it’s worth noting that it is still a lot less than the amount by which it went up in 2021. And at that point I was still over £5,500 in profit overall. I was therefore philosophical about this, recognizing that all investments have their ups and downs, and Nutmeg was hardly alone in seeing a drop in values in 2022. But I do understand why people who only started investing with them at the start of 2022 may have felt disappointed.

Quick update: As of 21 May 2024 the value of my main Nutmeg portfolio has risen to £24,249, an increase of £4,352 (21.44%) since 1 January 2023.

As with all investing, your capital is at risk. The value of your portfolio with Nutmeg can go down as well as up and you may get back less than you invest. Tax treatment depends on your individual circumstances and may be subject to change in the future.

Nutmeg Fees and Investments

Nutmeg charge a fee of 0.75% a year on Fully Managed portfolios (see Portfolio Options, below) of up to £100,000, and 0.35% on investments beyond that. That’s competitive compared with traditional mutual funds, although you can find cheaper investment opportunities and platforms if you look around. You may or may not get such good overall results, of course.

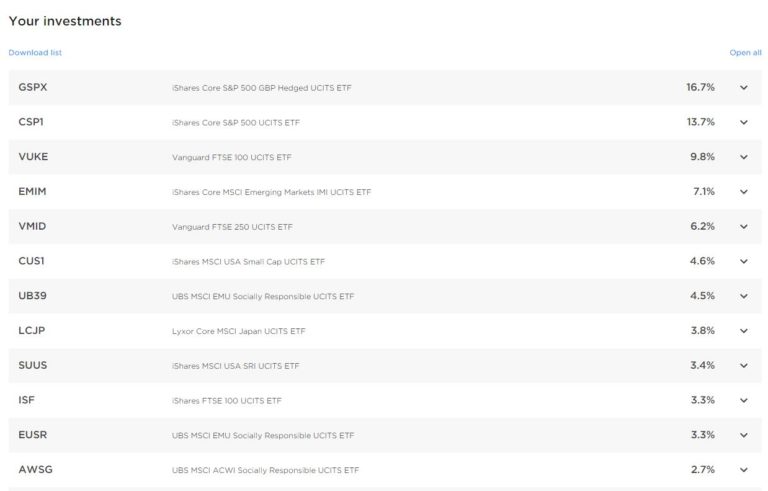

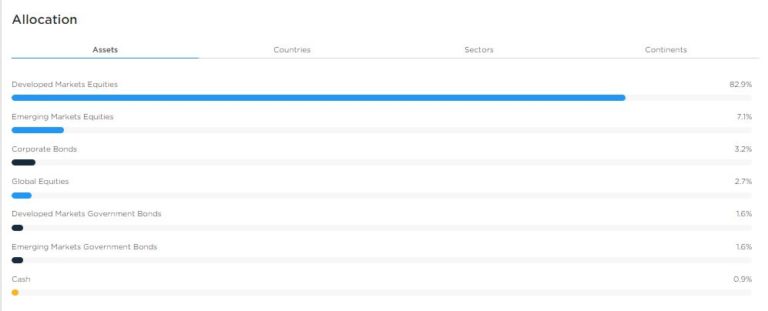

A reader asked if Nutmeg reveal what ETFs your money is invested in. The answer is that they do. In case you are interested, here is a list from the website showing how my money is invested. Note that these are the top 12 funds. There are others in my portfolio as well, but this was the most I could capture in one screengrab 🙂

As a matter of interest, here is a copy of the table showing how the investments in my portfolio are allocated by asset class.

As you will see, quite a large proportion of my portfolio is invested in equity markets. As I said earlier, I opted for a high-risk, high-returns strategy. If I had chosen a lower risk level, a larger proportion would undoubtedly be in bonds and cash. Note that high-risk can also mean higher loss.

You can make changes to the risk level and investment style of any Nutmeg pot at any time. Nutmeg do just caution that making frequent changes to your portfolio may impact your returns. So they suggest you review your risk level when your goals change and avoid trying to ‘time’ the market.

It’s also worth noting that Nutmeg invests mainly in accumulation rather than income-generating funds. Most do not produce dividends, and with those that do, the money is automatically reinvested back into your portfolio. Nutmeg is really intended for people who are aiming to build a ‘pot’ – a nest-egg, if you prefer – rather than looking for a source of income. But you can of course sell all or part of your investment at any time.

Capital at risk. Past performance is not a reliable indicator of future performance.

Portfolio Options

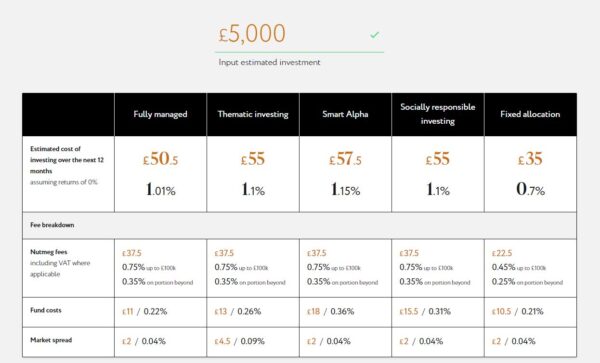

Since I first signed up, Nutmeg have added some other options to their offering. In particular, they now offer five different types of ISA portfolio: Fixed Allocation, Fully Managed, Thematic (launched 2023), Smart Alpha, Socially Responsible and Fixed Allocation. To save time, I have copied the information on the Nutmeg website about each of these portfolio types below. Note that by default the estimated total fees per year refer to a portfolio worth £5,000. You can change this if you wish by entering a new figure at the top.

Please note that the figures above are correct as of 19 March 2024 but may have changed subsequently. As you will note, the Fixed Allocation portfolio has lower charges than the other three.

The Socially Responsible portfolio aims to optimize your investments according to various environmental, social and governance (ESG) factors. So it focuses on companies with a good track record and proactive strategy in such areas as water use, pollution, greenhouse gas emissions, proportion of female board members, and so on.

Nutmeg’s Smart Alpha portfolios are powered by J.P. Morgan Asset Management. They include five risk-rated portfolios, each holding between 10 and 14 passive and active ETFs. They are managed by J.P. Morgan’s multi-asset solutions team, giving Nutmeg clients access to the investment giant’s experience and expertise. You can read more about the Smart Alpha range in this blog post. The new Nutmeg Thematic Investments are discussed in more detail further down.

As mentioned above, my own ISA is in the Fully Managed category (the only one available when I opened my account). I have considered switching to Socially Responsible, but as my investment has performed well overall I am reluctant to rock the boat. You might see this differently, of course.

I did, though, create a new pot within my ISA with Smart Alpha as the investment style. The risk level is 4/5, which roughly corresponds with the 9/10 risk level in my Fully Managed portfolio. I started in December 2020 with £1,000 and as all was going well added a further £1,000 in April and another £500 in June. By the end of 2021 my Smart Alpha portfolio was worth £2,837. That is an increase of £337 or around 13% expressed as an annual rate. In February 2022 I added another £500, bringing my total investment to £3,000. During 2022, like most stock market investments, the value of my SA portfolio fell back, but like my main portfolio it has recovered in 2023. At the time of writing (16 November 2023) it is worth £3,361, a net increase on capital of £361 (12.03%). Considering how turbulent the last two years have been for investors, I am happy enough with that.

I will of course continue to report on PAS about how my Nutmeg investments perform. Obviously, if my Smart Alpha pot seems to be doing significantly better than my Fully Managed one, or vice versa, I will switch my money between them. I am also considering investing in a new thematic investment pot. It is one of the attractions of Nutmeg that you can have multiple pots within a single ISA with different investment styles and risk levels attached to them.

Capital at risk. Past performance is not a reliable indicator of future performance.

New: Nutmeg Thematic Portfolios

As of 23 October 2023, Nutmeg introduced a new portfolio option. Nutmeg’s Thematic Investment style gives you a globally diversified, risk adjusted portfolio with a tilt (up to 20% of equity exposure) towards your chosen theme. They say the majority of the portfolio will be actively managed by Nutmeg’s investment team, whilst the ’tilted’ part of the portfolio will be made up of ETFs that the investment team believes will deliver the best returns from the growth of the trend in question (to be reviewed annually).

Currently three themes are available, these being Technical Innovation, Resource Transformation and Evolving Consumer. For more details about what each of these comprises, check out the Nutmeg website.

Nutmeg thematic portfolios are only available on Risk Level 5 or above. There is a minimum investment of £100 for Junior ISAs and Lifetime ISAs or £500 for stocks and shares ISAs and pensions. There is a 0.75% management fee.

Thematic investing carries specific risks and is not for everyone.

Withdrawing Money From Nutmeg

You can withdraw any or all of your money from your Nutmeg ISA at any time on request. Investments are sold on a twice-weekly cycle, so depending on when you submit your request Nutmeg say it will typically take 3-7 business days for the money to appear in your bank account. This means the value of your investments may change during this period, and you might not therefore receive the exact amount requested.

If you are withdrawing from an ISA, it’s important to remember that any allowance used in the current tax year will remain used; you won’t get it back if you later pay back into your ISA. As mentioned earlier, everyone has a generous annual £20,000 ISA allowance, so this rule may or may not be of concern to you.

Other types of account such as SIPPs and Lifetime ISAs have specific legal restrictions on withdrawals set down by the government, e.g. you can’t normally withdraw money from a SIPP until you reach the age of 55.

In Conclusion

I am obviously a fan of Nutmeg and – as I said above – plan to continue investing with them. Of course, I am not a qualified financial adviser and everyone should do their own research (and/or take professional advice) before deciding to invest with Nutmeg. Based on my own experiences, though, I am happy to recommend them. They provide a simple, easy to understand investment platform, the customer service is excellent, and certainly in my case the results achieved have been good (even allowing for the downturn last year).

Nutmeg also has an excellent mobile phone app with an App Store average rating of 4.8 (16K reviews) and a Google Play Store rating of 4.3 (2.6K reviews). On the independent Trust Pilot website Nutmeg averages 3.9 stars (‘Great’). This figure fell a bit as some members expressed dissatisfaction with the performance of their portfolios last year during the cost-of-living crisis. It is, though, worth noting that 69% of Trust Pilot reviewers still give Nutmeg the maximum 5 stars (‘Excellent’) rating. All figures and ratings are correct as of 21 February 2024.

If you have any comments or questions about this post or Nutmeg in general, please do leave them below.

PLEASE NOTE:As with all investing, your capital is at risk. Tax treatment depends on your individual circumstances and may be subject to change in the future. The value of your portfolio with Nutmeg can go down as well as up and you may get back less than you invest.

Note also that I am not a qualified independent financial adviser and nothing in this review should be construed as personal financial advice. You should always do your own ‘due diligence’ before investing and take professional advice if in any way uncertain how best to proceed. All investing carries a risk of loss.

Please note also that posts on Pounds and Sense may include affiliate links. If you click through and make an investment or perform some other qualifying transaction, I may receive a commission for introducing you. This will not affect in any way the terms you are offered or any fees you may be charged.

This is a fully updated repost of my original Nutmeg review.

If you enjoyed this post, please link to it on your own blog or social media:

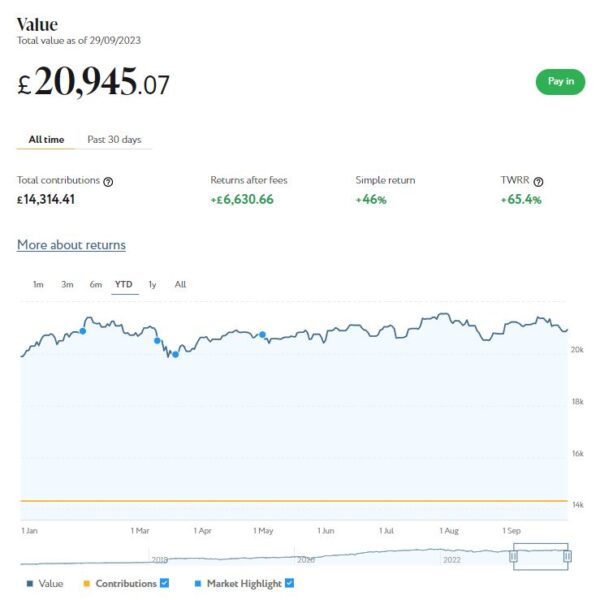

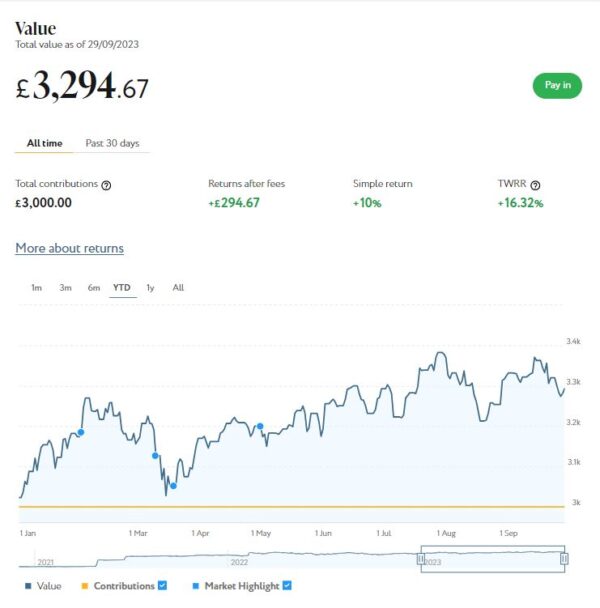

I’ll start as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

As the screenshot below for the year to date shows, my main Nutmeg portfolio is currently valued at £20,945. Last month it stood at £21,188 so that is a fall of £243.

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £3,295 compared with £3,325 a month ago, a fall of £30. Here is a screen capture showing performance since the start of this year.

The net value of all my Nutmeg investments has fallen this month by £273 or 1.11% month on month. That’s obviously a bit disappointing, but both pots are still comfortably up on where they were at the start of the year. Their total value has risen by £1,320 (5.76%) since 1st January 2023.

Of course, all investing is (or should be) a long-term endeavour. Over a period of years stock market investments such as those used by Nutmeg typically produce better returns than cash accounts, often by substantial margins. But there are never any guarantees, and in in the short to medium term at least, losses are always possible.

You can read my full Nutmeg review here (including a special offer at the end for PAS readers). If you are looking for a home for your annual ISA allowance, based on my overall experience over the last seven years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs) and Junior ISAs as well.

I also have investments with the property crowdlending platform Kuflink. They continue to do well, with new projects launching every week. I currently have around £2,000 invested with them in 15 different projects paying interest rates typically around 7%. I also have just over £100 in my cash account after another loan was recently repaid.

To date I have never lost any money with Kuflink, though some loan terms have been extended once or twice. On the plus side, when this happens additional interest is paid for the period in question.

As mentioned last time, Kuflink recently changed their terms and conditions. As from Monday 21st August there is an initial minimum investment of £1,000 and a minimum investment per project of £500.

Kuflink say they are doing this to streamline their operation and minimize costs. I can understand that, though it does mean the option to ‘test the water’ with a small first investment has been removed. It will also make it harder for small investors (like myself) to build a well-diversified portfolio on a limited budget. As mentioned, my current portfolio of £2,145 comprises 17 different investments ranging from £50 to £200. If I was starting out again now, that same amount of money would only stretch to four deals!

One possible way around this is to invest using Kuflink’s Auto/IFISA facility. Your money here is automatically invested across a basket of loans over a period from one to three years. The rates on offer from August 1 2023 are shown in the graphic below.

As you may gather, you can invest tax-free in a Kuflink Auto IFISA. Or if you have already used your annual iFISA allowance elsewhere, you can invest via a taxable Auto account. You can read my full Kuflink review here if you wish.

Moving on, my Assetz Exchange investments continue to generate steady returns. Regular readers will know that this is a P2P property investment platform focusing on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my AE portfolio has generated a respectable £141.06 in revenue from rental income. As I said in last month’s update, capital growth has slowed, though, in line with UK property values generally.

At the time of writing, 8 of ‘my’ properties are showing gains, 2 are breaking even, and the remaining 16 are showing losses. My portfolio is currently showing a net decrease in value of £31.41, meaning that overall (rental income minus capital value decrease) I am up by £109.65. That’s still a decent return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Assetz Exchange most projects are socially beneficial as well.

Obviously the fall in capital value of my AE investments is disappointing. But it’s important to remember that until/unless I choose to sell the investments in question, it is largely theoretical, based on the most recent price at which shares in the property concerned have changed hands. The rental income, on the other hand, is real money (which in my case I have chosen to reinvest in other AE projects to further diversify my portfolio).

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of AE as far as i am concerned (especially now that Kuflink have raised their minimum investment per project to £500). You can actually invest from as little as 80p per property if you really want to proceed cautiously.

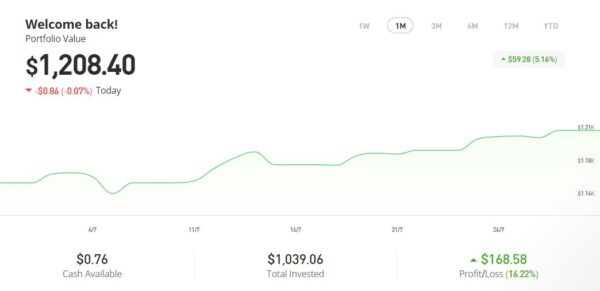

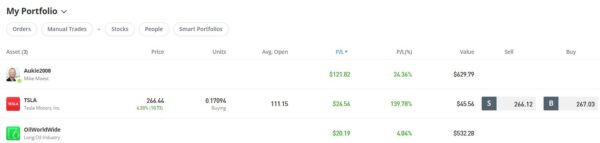

Last year I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios, Oil Worldwide. I also invested a small amount I had left over in Tesla shares.

My original investment totalling $1,022.26 is today worth $1,193.36, an overall increase of $171.10 or 16.73%. in these turbulent times I am quite happy with that.

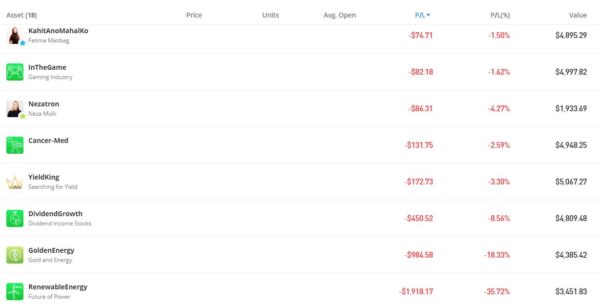

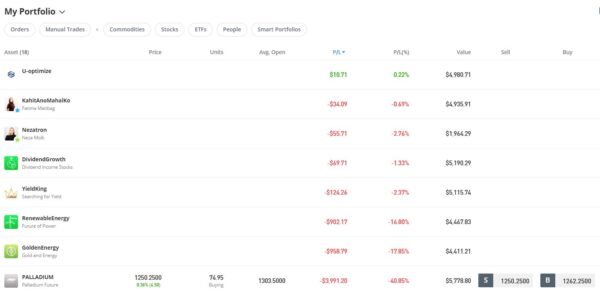

I thought it might also be interesting to update you on how my eToro virtual portfolio is faring (I wrote about my virtual portfolio a few weeks ago in this blog post). Overall, this is down by $2558 in value, largely due to some big losses experimenting with commodity trading (I decided this wasn’t for me). It is very interesting to see which investments in my virtual portfolio have been doing well and which poorly, though.

I can’t get all of the investments in this port into a single screen capture, but here are the top performers…

And here are the worst-performing ones…

As you can see, the best performing investment in my virtual portfolio is Oil Worldwide. This continues to forge ahead since it was rebalanced in July by eToro. The second best is my copy trading portfolio with Aukie2008. I am obviously glad I have both of these in my real money portfolio as well!

By contrast, the two renewables smart portfolios I hold, Golden Energy and Renewable Energy, are currently showing substantial (thankfully virtual) losses.

Renewable Energy has actually lost over 35% in value since I notionally invested in it. This certainly does seem to confirm that investing in renewables is risky and by no means a guaranteed route to profit, despite all the green energy hype at the moment. I am tempted to suggest that Just Buy Oil might be a better strategy 😉

eToro also recently introduced the eToro Money app. This allows you to deposit money to your eToro account without paying any currency conversion fees, saving you up to £5 for every £1,000 you deposit. You can also use the app to withdraw funds from your eToro account instantly to your bank account. I tried this myself and was impressed with how quickly and seamlessly it worked. You can read my blog post about eToro Money here.

I had two more articles published in September on the excellent Mouthy Money website. The first was Will a Heat Pump Save You Money? The government is pushing heat pumps hard as a method for achieving its Net Zero target, but do the sums add up for hard-pressed consumers? In this article I took a ‘deep dive’ into the pros and cons of heat pumps and set out my personal views on whether or not they represent good value for money.

I also wrote Get Your Will Written Free of Charge in October. For those who may not know, October is Free Wills Month, when some solicitors in England and Scotland offer members of the public aged 55 and over the chance to have their wills written or updated free of charge. In my article I explain how the scheme works, and also explain why I believe everyone should have their will drawn up by a qualified solicitor.

As I’ve said before, Mouthy Money is a great resource for anyone interested in money-making and money-saving. I particularly like the ‘Deals of the Week’ feature compiled by Jordon Cox (‘Britain’s Coupon Kid’) which lists all the best current money-saving offers for savvy shoppers. Check out the latest edition here

I also published two new posts on Pounds and Sense in September (I was away quite a lot last month, which didn’t leave much time for blogging!).

The first was a revised and updated guest post by my friend and near-neighbour Sally Jenkins titled Make Money From Public Speaking.

Sally is a successful author and makes a steady sideline income speaking about writing and related subjects (including a little while ago to my local U3A group!). I added a few thoughts of my own at the end of the article. There is definitely money to be made in this field; so if it’s something that might appeal to you, do check it out.

My other post last month was a review of a new money-saving shopping app called JamDoughnut. This app lets you earn cashback on gift vouchers from over 150 shops and restaurants, for which you get up to 20% cashback. You can then use the gift vouchers as money at the retailer concerned and pocket the cashback. Read Save Money on Your Shopping With JamDoughnut for more info (and a special bonus offer!).

The opportunity to get a free share worth up to £100 by signing up Trading 212 is now closed (for the time being anyway). I hope you took advantage if eligible and your free share is doing well. The opportunity to Get a Free ETF Share Worth up to £200 with Wealthyhood is still open. This DIY wealth-building app is aimed especially at people new to stock market investing. The minimum investment to qualify for the free share offer was raised recently from £20 to £50 – but on the plus side, they now guarantee that your free ETF share will be worth at least £10.

Finally, a quick reminder that you can also follow Pounds and Sense on Facebook or Twitter (or X as we have to learn to call it now). Twitter/X is my number one social media platform these days and I post regularly there. I share the latest news and information on financial (and other) matters, and other things that interest, amuse or concern me. So if you aren’t following my PAS account, you are definitely missing out!

That’s all for today. As always, if you have any comments or queries, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media:

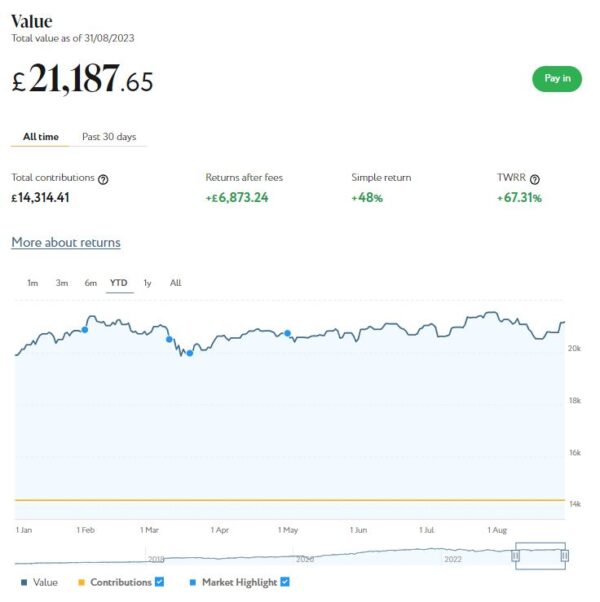

I’ll start as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

As the screenshot below for the year to date shows, my main Nutmeg portfolio is currently valued at £21,188. Last month it stood at £21,548 so that is a fall of £360.

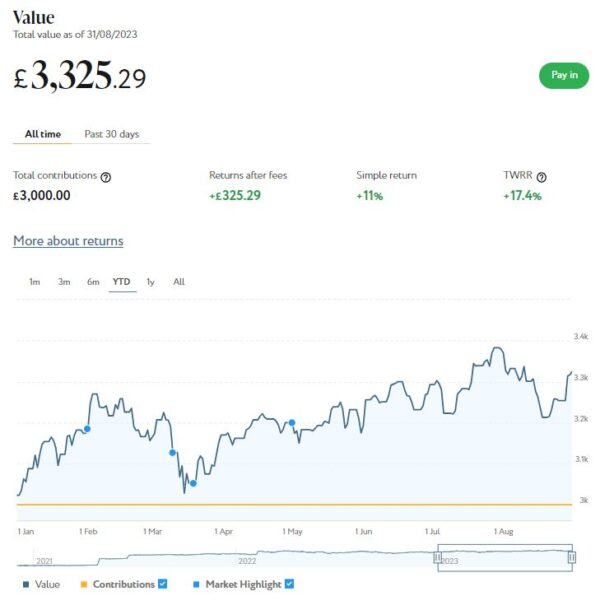

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £3,325 compared with £3,383 a month ago, a fall of £58. Here is a screen capture showing performance since the start of this year.

The net value of all my Nutmeg investments has fallen this month by £418 or 1.68% month on month. That’s obviously a bit disappointing, but both pots are still comfortably up on where they were at the start of the year. Their total value has risen by £1,592 (6.95%) since 1st January 2023.

Of course, all investing is (or should be) a long-term endeavour. Over a period of years stock market investments such as those used by Nutmeg typically produce better returns than cash accounts, often by substantial margins. But there are never any guarantees, and in in the short to medium term at least, losses are always possible.

You can read my full Nutmeg review here (including a special offer at the end for PAS readers). If you are looking for a home for your annual ISA allowance, based on my overall experience over the last seven years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs) and Junior ISAs as well.

I also have investments with the property crowdlending platform Kuflink. They continue to do well, with new projects launching every week. I currently have £2,145 invested with them in 17 different projects paying interest rates typically around 7%. I also have just over £100 in my cash account after another loan was repaid. I am currently considering whether to withdraw this money or (in due course) reinvest it.

To date I have never lost any money with Kuflink, though some loan terms have been extended once or twice. On the plus side, when this happens additional interest is paid for the period in question.

As mentioned last time, Kuflink recently changed their terms and conditions. As from Monday 21st August there is an initial minimum investment of £1,000 and a minimum investment per project of £500. I wondered if this would also apply to their secondary market and this does indeed seem to be the case. When I checked just now, there was only one loan on offer for under £500 (£413) and all the others were £500 or more.

Kuflink say they are doing this to streamline their operation and minimize costs. I can understand that, though it does mean the option to ‘test the water’ with a small first investment has been removed. It will also make it harder for small investors (like myself) to build a well-diversified portfolio on a limited budget. As mentioned, my current portfolio of £2,145 comprises 17 different investments ranging from £50 to £200. If I was starting out again now, that same amount of money would only stretch to four deals!

One possible way around this is to invest using Kuflink’s Auto/IFISA facility. Your money here is automatically invested across a basket of loans over a period from one to three years. The rates on offer from August 1 2023 are shown in the graphic below.

As you may gather, you can invest tax-free in a Kuflink Auto IFISA. Or if you have already used your annual iFISA allowance elsewhere, you can invest via a taxable Auto account. You can read my full Kuflink review here if you wish.

Moving on, my Assetz Exchange investments continue to generate steady returns. Regular readers will know that this is a P2P property investment platform focusing on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my AE portfolio has generated a respectable £134.95 in revenue from rental income. As I said in last month’s update, capital growth has slowed, though, in line with UK property values generally.

At the time of writing, 9 of ‘my’ properties are showing gains, 1 is breaking even, and the remaining 16 are showing losses. My portfolio is currently showing a net decrease in value of £28.83, meaning that overall (rental income minus capital value decrease) I am up by £106.12. That’s still a decent return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Assetz Exchange most projects are socially beneficial as well.

Obviously the fall in capital value of my AE investments is disappointing. But it’s important to remember that until/unless I choose to sell the investments in question, it is largely theoretical, based on the most recent price at which shares in the property concerned have changed hands. The rental income, on the other hand, is real money (which in my case I have chosen to reinvest in other AE projects to further diversify my portfolio).

Also, as I noted last time, the recent high inflation rate has actually been beneficial for Assetz Exchange investors. That is because properties on the platform generally have an annual review when rentals are increased in line with inflation. That means from the end of the financial year in April, rentals have increased in most cases by around 10%. Assetz Exchange recently published a blog post about this which is worth a read.

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of AE as far as i am concerned (especially now that Kuflink have raised their minimum investment per project to £500). You can actually invest from as little as 80p per property if you really want to proceed cautiously.

Last year I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios, Oil Worldwide. I also invested a small amount I had left over in Tesla shares.

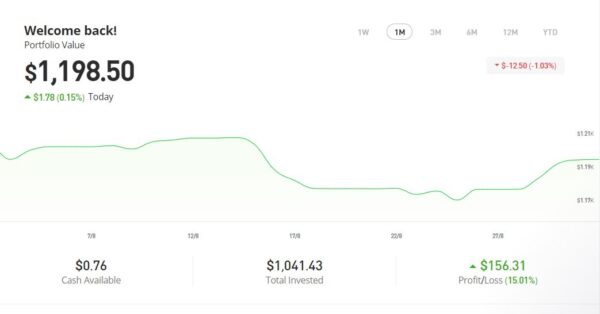

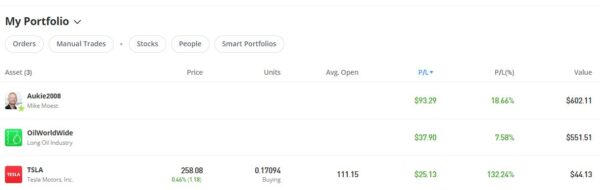

As you can see from the screen capture below, my original investment of $1,022.26 is today worth $1,198.50, an overall increase of $176.24 or 15.05%. in these turbulent times I am very happy with that.

In the last month my copy trading portfolio with Aukie2008 has fallen in value, though I am not too concerned about this as the investment is still well up overall. My Tesla shares have again done well (thank you, Elon Musk). I am also pleased that Oil Worldwide continues to forge ahead since it was rebalanced in July by eToro. Looking at my eToro virtual portfolio, I can see that Oil Worldwide is still doing much better than the two renewables smart portfolios I hold, which are currently showing substantial (thankfully virtual) losses. Make of this what you will!

eToro also recently introduced the eToro Money app. This allows you to deposit money to your eToro account without paying any currency conversion fees, saving you up to £5 for every £1,000 you deposit. You can also use the app to withdraw funds from your eToro account instantly to your bank account. I tried this myself and was impressed with how quickly and seamlessly it worked. You can read my blog post about eToro Money here.

I had three more articles published in August on the excellent Mouthy Money website. The first was Can You Make Money From Holiday Lets? This is a dream for many people, and there is no doubt you can make a valuable extra income this way (not to mention the opportunity to enjoy cheap holidays at the property yourself!). In my article I set out some key things you need to be aware of.

I also wrote How to Become an Amazon Vine Reviewer. This is a subject close to my heart. I’ve been an Amazon Vine reviewer for over ten years and in some ways it’s been the most profitable sideline I’ve ever had. You don’t get paid for Amazon Vine reviews, but you do get to keep the items concerned (my most valuable so far being a £1200 gaming laptop). In my article I spill the beans on how the scheme works and suggest how you might get an invitation to become a ‘Vine Voice’ yourself.

My third article was Play Your Supermarket Loyalty Cards Right. In this article I explained why stores use loyalty cards and their pros and cons for customers. I also described the leading loyalty cards in the UK (including Tesco Clubcard, Nectar, Morrisons, Boots, and so on), covering how they work in practice and how to get the most from them.

As I’ve said before, Mouthy Money is a great resource for anyone interested in money-making and money-saving. I particularly like the ‘Deals of the Week’ feature compiled by Jordon Cox (‘Britain’s Coupon Kid’) which lists all the best current money-saving offers for savvy shoppers. Check out the latest edition here

I also published several new posts on Pounds and Sense in August. The deadlines on some of these have now passed, so I hope you took advantage at the time! You might, however, still want to check out What is U3A and Is It For You?

U3A stands for University of the Third Age. It is a non-profit organization offering a range of leisure activities for retired and semi-retired people. I recently joined my local U3A myself, and in this post set out my experiences and impressions, for the benefit of anyone else who might be interested in joining now or in future.

In other news, the Trading 212 free share offer is back. If you haven’t done this before, you can get a free share worth up to £100. You just have to sign up on the website and deposit a minimum of £1 into your account. This offer is running till 27 September 2023. See Get a Free Share Worth up to £100 with Trading 212 for more info.

The opportunity to Get a Free ETF Share Worth up to £200 with Wealthyhood is also still open. Wealthyhood is a DIY wealth-building app aimed especially at people new to stock market investing. As from June 2023 they changed their fee structure to make it (even) more attractive to small investors. They have increased the minimum investment to qualify for the free share offer from £20 to £50 – but on the plus side, they guarantee that your free ETF share will be worth at least £10.

Finally, a quick reminder that you can also follow Pounds and Sense on Facebook or Twitter (or X as we have to learn to call it now). Twitter/X is my number one social media platform these days and I post regularly there. I share the latest news and information on financial (and other) matters, and other things that interest, amuse or concern me. So if you aren’t following my PAS account, you are definitely missing out!

As a matter of interest, I recently paid £100 for Twitter/X premium membership. Although I do like the snazzy blue tick, my main reason was to get continued access to the scheduling tool Tweetdeck (now called X-pro) which became subscriber-only last month. I was accused the other day of ‘selling out’ to Elon Musk for doing this. But personally I don’t begrudge the money, as the extra tools and features make working with Twitter much easier and more enjoyable. And if my money helps keep the platform afloat, that’s an additional benefit in my book.

That’s all for today. As always, if you have any comments or queries, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media:

Today I’m spotlighting Mintos, a European crowdlending platform based in Latvia but open to people in the UK. You may have seen my earlier post on Investing Basics for Beginners, which was sponsored by MIntos.

With Mintos, your money is invested in loans to businesses and private individuals arranged by Mintos’s partner lending companies around the world. Mintos act as intermediaries between lenders and borrowers. They aim to ensure that both groups act responsibly and loans are repaid in a timely way.

Currently Mintos offer the opportunity to invest in agricultural loans, business loans, car loans, car rentals, invoice financing, mortgage loans, personal loans, pawnbroking loans and short-term loans.

You can begin investing with just €50 (around £43). Since 2015, investors with Mintos have earned a 9.54% net return per year on average. Of course, past performance is no guarantee of how any investment platform will do in future. Currently, however, interest rates on the platform are averaging around 12.50%.

What Guarantees Are There?

To ensure security, Mintos provides a return-on-investment guarantee. If a loan instalment remains unpaid 60 days after becoming due, Mintos say they will repay the investment at face value with any accrued interest.

Mintos further insist that all lenders on their platform maintain 5-10% of any loan on the platform themselves. This means that in the event of a default, the lender will lose some of their own money also. So they have ‘skin in the game’, as the expression goes 🙂

The other main risk, of course, is the collapse of the platform itself. While this could happen, it’s worth noting that Mintos is licensed and supervised by Latvijas Banka, the central bank of Latvia, and a member of the Latvian national InvestorCompensation Scheme. If Mintos fails to provide investment services, retail investors are entitled to compensation of 90% of the irrevocable loss resulting from the non-provision, up to a limit of €20 000.

In addition, as is generally the case with crowdlending/P2P platforms, your assets are held quite separately from Mintos’s assets.

Investing in Euro

As Mintos is a European operation, you will need to invest in euro and your returns will be paid in this currency. That obviously adds a layer of complication for UK residents, but there are various ways round this. If you have a UK bank account you will normally be able to make (and receive) payments in euro, but may be charged a transaction fee.

You could use your own bank to fund your account initially, but if you become a regular investor with Mintos you might want to use a service/account that charges lower fees. You could use a money transfer service such as Paysera or Wise (formally TransferWise). These will enable you to transfer funds between Mintos and your own bank account with (potentially) lower charges and a more favourable exchange rate.

Another option would be to open a euro account with a provider such as Starling. This will allow you to receive and make payments in both sterling and euro, again at a lower overall cost.

Opening an Account

To open a Mintos account, your first step will be to click on Create Account at the top of the Mintos homepage. There are then certain preliminary steps you will need to take…

Verify your identity and answer some questions about yourself

This is necessary to comply with anti-money laundering laws and KYC (Know Your Customer) requirements.

Take the Suitability & Appropriateness assessment

As a licensed investment firm, Mintos are required to ensure that the products they offer are suitable and appropriate for investors. Based on your answers, they will make certain methods of investing available to you and set a responsible investment limit for your account. You can retake the assessment at any time if your situation changes.

Transfer funds to your Mintos account (see above)

Once this has been done, you can start investing. You have various options here. The simplest is to use one of Mintos’s automated strategies. These work as follows:

Choose a strategy that matches your preference: Diversified, Conservative, or High-yield.

Your strategy will buy small fractions of many different loans or Sets of Notes from different lending companies around the world.

You will be shown the weighted average interest rate of available investments before you invest.

Mintos can (if you wish) reinvest your returns so your money can work continuously and earn even more interest.

You can get your investment back any time by cashing out funds from your Mintos strategy.

You can start or stop your strategy at any time.

Your exposure is capped at 15% per lending company.

Alternatively, you can use a custom strategy, where you choose from a huge range of available investments yourself. You can filter by more than 20 different investing criteria and diversify your portfolio according to your preferences. You can do this entirely manually or create a custom automated investing strategy based on the rules you set.

When you want to withdraw money, your Mintos Core portfolio will automatically sell investments in your portfolio to other investors. Selling may take from a couple of minutes to a few days, depending on demand from other investors at the time. Note that loans which are in default cannot be cashed out this way, and you will have to wait until the loan in question is back in good stead or the 60-day guarantee (see above) kicks in. In some circumstances you may be able to sell loans which are unavailable for cashing out on Mintos’s secondary market, for which a 0.85% fee will be charged. This article on the MIntos website has more information about the cashing out rules and restrictions.

Special Bonus!

Until 30 November 2023, if you click through any link to Mintos in this article and invest €1000 or more, you will get a €50 instant bonus and a 1% bonus of your average investment in the first 90 days.

If you invest €5000, for example, in addition to the returns advertised (currently averaging 12.5%), you will also receive a €50 instant bonus and a further 1% bonus of €50 after 90 days. Effectively that’s an extra 2% bonus. Remember, this special offer closes on 30 November 2023.

If you have any comments or questions, as always, please do leave them below.

Disclosure: I am not a registered financial adviser and nothing in this article should be construed as personal financial advice. You should always do your own ‘due diligence’ before investing, and if in any doubt seek advice from a registered financial adviser before proceeding. All investing carries a risk of loss.

This post includes affiliate links. If you click through and make an investment (or perform some other designated action) I may receive a commission for introducing you. This will not affect the product or service you receive or any charges you may pay. Note also that the special bonus referred to in this article is only available if you click through one of my links. It will not apply if you go to the Mintos website directly.

If you enjoyed this post, please link to it on your own blog or social media:

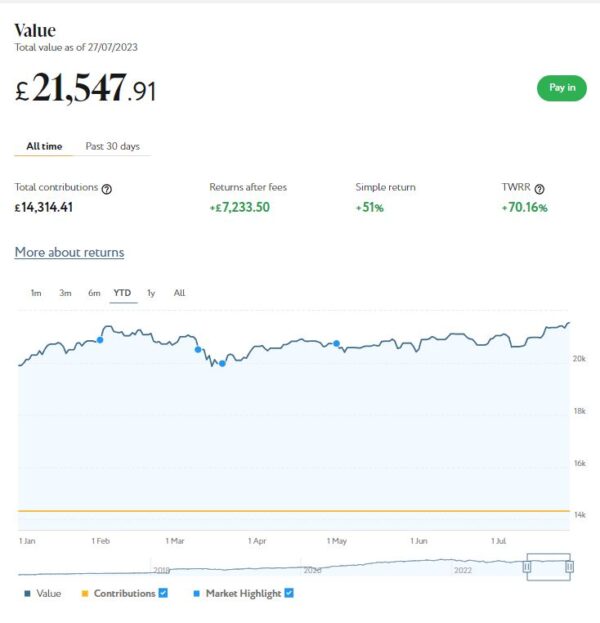

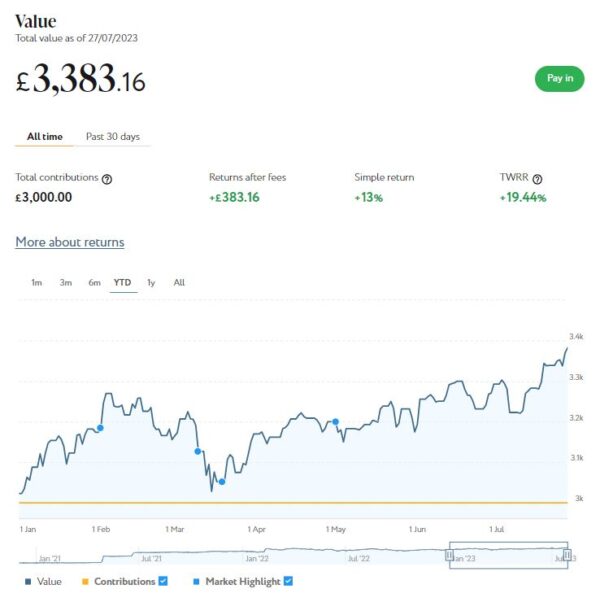

I’ll start as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

As the screenshot below for the year to date shows, my main Nutmeg portfolio is currently valued at £21,548. Last month it stood at £21,044 so that is a rise of £504.

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £3,383 compared with £3,293 a month ago, an increase of £90. Here is a screen capture showing performance since the start of this year.

This has clearly been another good month for both my Nutmeg pots. Their total value has risen by £594 or 2.44% month on month. Since the start of 2023 the net value of my Nutmeg investments has grown by £2,010 or 8.78%. Compared with mid-October last year that’s an impressive rise of £3,118 or 14.29%.

Of course, all investing is (or should be) a long-term endeavour. Over a period of years stock market investments such as those used by Nutmeg typically produce better returns than cash accounts, often by substantial margins. But there are never any guarantees, and in in the short to medium term at least, losses are always possible.

Also, as you may know, both my Nutmeg pots have quite high risk levels (9/10 main, 5/5 Smart Alpha). If you haven’t yet seen it, you might like to check out my blog post in which I looked at the performance over time of Nutmeg fully managed portfolios at every risk level from 1 to 10 . I was pretty amazed by the difference risk level makes, with higher-risk ports over almost any period of three or more years in the last ten generating significantly better overall returns. If you are investing for the long term (and you almost certainly should be) choosing a hyper-cautious low-risk level might not therefore be the smartest strategy. The one exception is if you plan to withdraw your money soon and don’t want to risk losing too much if there is a sudden downturn.

You can read my full Nutmeg review here (including a special offer at the end for PAS readers). If you are looking for a home for your annual ISA allowance, based on my overall experience over the last seven years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs) and Junior ISAs as well.

I also have investments with the property crowdlending platform Kuflink. They continue to do well, with new projects launching every week. I currently have £2,185 invested with them in 18 different projects paying interest rates typically around 7%. To date I have never lost any money with Kuflink, though some loan terms have been extended once or twice. On the plus side, when this happens additional interest is paid for the period in question.

Last month a couple of my Kuflink loans were repaid, so I got my capital back with interest. I decided to withdraw about half of the proceeds to help pay for a couple of big purchases. The other half I reinvested in short-term loans on Kuflink’s secondary marketplace.

I heard this month that Kuflink are changing their terms and conditions. Specifically, from Monday 21st August there will be an initial minimum investment of £1,000 and a minimum investment per project of £500.

Kuflink say they are doing this to streamline their operation and minimize costs. I can understand their reasoning, though it does mean the option to ‘test the water’ with a small first investment has been removed. It will also make it harder for small investors (like myself) to build a well-diversified portfolio on a limited budget. As mentioned, my current portfolio of £2,185 comprises 18 different investments ranging from £50 to £200. Once the minimum £500 per project limit applies, the same amount of money would only stretch to four!

One possible way around this is to invest using Kuflink’s Auto/IFISA facility. Your money here is automatically invested across a basket of loans over a period from one to three years. The rates on offer from August 1 2023 are shown in the graphic below.

As you may gather, you can invest tax-free in a Kuflink Auto IFISA. Or if you have already used your annual iFISA allowance elsewhere, you can invest via a taxable Auto account.

You can read my full Kuflink review here. Note that I haven’t updated the information there about minimum investments as yet, but will do so shortly. You can of course still invest smaller amounts than £500 until the August 21st deadline.