Today I’m looking at some ways you may be able to cut the amount you spend on motoring.

Right now, as I’m sure you know, the cost of motoring is rising fast. Fuel prices are obviously a major issue, with the war in Ukraine and economic sanctions on Russia driving up prices that were already increasing anyway.

But in addition, drivers are having to contend with ever-rising road taxes, congestion charges, insurance premiums, repair and servicing bills, and more. And while these costs keep going up, many of us are also having our incomes squeezed.

So today I thought I would share some tips and ideas for cutting your motoring costs…

Table of Contents

Travel Light

The more weight you carry around in your car, the worse the fuel economy is likely to be. So empty your boot as much as possible and remove the roof rack if you’re not using it. The latter will also aid fuel economy by reducing air resistance.

Check Your Tyres

According to the RAC, tyres under inflated by 15 psi – a difference you might not notice visually – can use 6% more fuel. Not only that, under-inflated tyres wear out faster, meaning you will need to replace them sooner.

You can check your tyre pressure at most filling stations or buy an electric pump (like this one maybe). The correct pressure for your tyres will be in the owner’s manual or handbook.

Drive for Fuel Economy

There are many ways you can improve the fuel economy of your car. One of the best and simplest is to avoid braking and accelerating sharply. That means reading the road, anticipating changes in gradients and traffic conditions, and making any necessary adjustments in good time. A good satnav (see example ad below) can help with this.

Another tip is to keep your speed moderate. According to government statistics, driving at a steady 50 mph rather than 70 can improve fuel economy by 25%. For most cars the sweet spot is between 50 and 60 mph. Once you get much over this, fuel economy starts to drop rapidly.

Finally, having lots of electrical devices running – from heating to aircon – can reduce fuel economy as well, especially at lower speeds. So try to keep this to a minimum, but without of course compromising your comfort or safety.

Shop Around for Petrol

Clearly driving miles out of your way to save a penny a litre isn’t likely to be cost-effective. But if you have a choice of local filling stations, it is well worth monitoring them regularly to see which is cheapest.

There are also various websites that can help you check prices locally, though you may have to register with them to view full details. Two to try are Petrolprices.com and GoCompare.

Don’t Fill Your Tank

Petrol is heavy, and the added weight will reduce your car’s fuel economy. Ideally don’t fill your tank more than half-way, though of course this may not always be practical.

Don’t Rev the Engine When Starting

This is something that until recently I was guilty of myself, having grown up in the days when you had to do this to prevent a cold engine from stalling.

But with modern cars, many of which have computer-controlled ignition systems, it is no longer necessary. If (like me) you still do this habitually, train yourself to turn the ignition and keep your foot well away from the accelerator pedal. This will save petrol and help with fuel economy.

Consider Car Sharing

Car sharing can work well if someone else you know is travelling the same route as you, ideally on a regular basis. You can split the fuel costs and (if you both agree) the driving duties. And as fans of Peter Kay’s Car Share will know, you can make new friends and enjoy some stimulating conversations too!

For one-off journeys, you could try ride-sharing. The website BlaBlaCar lets you search for other drivers who are making a similar journey and have space for you in their vehicle. Alternatively, if you are planning a long journey you can help defray the cost by offering to take one or more paying passengers. Fees are paid in advance via the website, so there is no awkward passing over of cash on the day.

There are also ‘car pool’ companies like ZipCar that offer members the opportunity to hire a car from their fleet when needed for a modest price. If you only require a car now and then, this could be a cost-effective alternative to owning a car yourself.

Shop Around for Motor Insurance

It’s easy to fall into the habit of renewing every year with the same insurer, but there are big savings to be made by shopping around.

Use a price comparison service such as Go Compare or Confused.com to get quotes from a range of insurers, therefore. But also check cashback sites such as Top Cashback and Quidco, which have some good offers too. For example, Top Cashback are currently offering up to £20 cashback on car insurance from the AA.

One other top tip is to get a quote for fully comprehensive insurance, even if you normally opt for third party, fire and theft (TPFT). Surprisingly, because of the way insurance companies’ algorithms work, comprehensive insurance often comes out cheaper, even though you are actually getting better cover.

Go Electric

Finally, if you haven’t done so already, you could consider going electric (or hybrid).

Electricity prices are going up at the moment too, but you should still save a lot compared with buying petrol or diesel. Electric cars are obviously expensive but prices are starting to come down and there is a growing second-hand market as well. This article from the Buyacar website includes a useful round-up of the pros and cons of electric cars.

If you have any comments or questions – or any other tips for saving money on motoring – please do leave a comment as usual.

If you enjoyed this post, please link to it on your own blog or social media:

This is the third in a series of collaborative articles on the subject of equity release. This one looks at the important question of whether you can still rent out your house (or part of it) if you take equity release.

As the equity release industry expands, UK-based older homeowners are being offered more flexible retirement mortgage solutions to combat the problem of insufficient funds in retirement.

While equity release is a fantastic product, there are some terms and conditions that may put limitations on what you do with your property.

74% of UK-based retirees own homes, and many of those live in large family properties where the kids have moved out. With the chance to make up to £7,500 tax-free a year through the government’s Rent-a-Room scheme (including qualifying Airbnb lets), renting out a room or your whole property can be a great way for retirees to generate extra income.

But if equity release is something you’re considering, the big question is, can you rent out your house after taking equity release?

Equity release expert John Lawson of SovereignBoss explores this topic in the following report to help you understand all the equity release criteria to ensure you make a sound decision.

Table of Contents

What is Equity Release?

Equity release is a financial product designed for older homeowners to unlock the cash in their property while still living there.

What’s great about these products is that repayments are completely voluntary and there is no risk of foreclosure. Instead, the loan and any compound interest are repaid when the last homeowner passes away or enters long-term care. Money taken through equity release is tax-free and can be used for any purpose.

Finally, equity release borrowers can opt to release their money in a lump sum, place it in a drawdown facility, or receive it as a monthly income.

Lodgers v. Tenants and Equity Release

One of the key components to an equity release loan is that you need to live in your home for at least six months a year and it must be considered your primary residence. Does this mean you can welcome lodgers or tenants?

There are some key differences between the two:

A Tenant – A tenant generally has more rights than a lodger due to a Tenancy Agreement. The landlord will need to get permission to enter the rented space and must conduct regular gas safety checks (if gas is connected). Once a contract is signed, a landlord can evict the tenant after six months, providing acceptable practices are followed. A landlord will also need to return the tenant’s deposit as per The Tenancy Deposit Scheme (TDS).

A Lodger – On the other hand, a lodger can be removed from the property at any time, given ‘sufficient’ notice. This is usually 28 days but can be less. A big difference between a tenant and a lodger is that a licence is signed instead of a lease agreement. The document will set out the terms and conditions of the agreement and the rules of the property.

Very importantly, the general rule with equity release is that homeowners may have lodgers but not tenants. (1)

Can I Rent Out My Home with Equity Release While I’m on Holiday?

In short, no. As per the logic above, you may not rent out your home while you’re on holiday, even if you live in the property for only six months a year. That being said, these rules could differ from one lender to the next. Therefore, should you receive income from renting out your home for half a year while moving to your holiday home, it’s worth consulting your financial adviser to see if they can find an equity release plan that permits this.

Airbnb and the Rent-a-Room Scheme with Equity Release

The great news is that Airbnb and the Rent-a-Room scheme are both considered to be lodger agreements, so you can rent out one or more rooms in your home using one (or both) of these options. With the UK being a popular tourist destination, this is a great form of retirement income, and you have the opportunity to mingle with guests and entertain people from across the world.

Of course, some areas are more popular than others for this. But even if you don’t live in a tourist hot-spot, there may still be a demand for short-term accommodation for people attending business meetings, conferences, sporting events, concerts, and so on.

In Conclusion

Equity release is a great way to gain access to property wealth, but can limit your opportunities to make money through rentals. It’s therefore important to weigh up the pros and cons carefully.

Your best bet is to discuss your future plans and intentions with your financial adviser. In general, as stated above, you can’t rent out your home once you’ve unlocked equity. But you can usually make extra income by taking lodgers, and that can be a great way to keep you busy (and supplement your pension) during your retirement years.

This is a collaborative post.

If you enjoyed this post, please link to it on your own blog or social media:

This is the second in a three-part series of collaborative posts about equity release. This article looks at the likely effect of rising interest rates on the equity release market.

The equity release industry is booming. Homeowners from across the UK may find the financial freedom they desire by unlocking one of these attractive products.

If you’re a homeowner over 55 and haven’t heard of equity release, you need to do your research. These products allow you to access cash tied up in your property for any purpose you wish. No tax is payable on this money, and you will never be obliged to move out of your home.

John Lawson from SovereignBoss has done extensive research on the future of the equity release interest rates. He has discovered that after reaching an all-time low in March 2021, equity release interest rates are rising. The big question is, how significant will the rate increase be, and will this have a short-term effect on the industry as a whole? Let’s take a look at what Mr Lawson has to say.

Table of Contents

Interest Rate Increase

When interest rates rise, the equity release sector is inevitably impacted as well. In March 2021 interest rates hit a historic low, with some homeowners having the opportunity to unlock equity with fixed rates as low as 2.3%. This unprecedented rate drop was exciting because it wasn’t much more expensive for a homeowner to opt for an equity release than it was to have a traditional mortgage. Plus, with no repayments required in one’s lifetime, retired homeowners could save a fortune by eliminating monthly mortgage payments. (1)

Recently interest rates have increased slightly but are still quite low. Current rates range between 2.9% and 6.4%. The interest rates you achieve will be lender-dependent, but they will also be determined by your age, health condition and property value.

Experts predict that interest rates are set to rise until 2024. And with the latest announcement by the Equity Release Council (see below), now could be the cheapest opportunity to access the cash tied up in your property through an equity release mortgage.

New Compulsory Optional Repayments

In addition to interest rates rising but still being stable, on 31st March 2021, the Equity Release Council enforced guidance on lenders to offer all their lifetime mortgage clients the option for penalty-free voluntary repayments. This means that homeowners can now repay up to 40% of the amount borrowed each year.

The exact offer you receive will depend on the lender you select. But in principle, if you have the means to do so, you could pay off your equity release plan within three to 10 years, restoring your property’s value.

But that’s not all. Once you’ve released equity, there is no risk of foreclosure. You can stop and start making repayments whenever you wish. Voluntary repayments are a great idea if you can afford them, as they reduce the overall cost of your loan by preventing compound interest.

So How Badly Will the Industry Be Affected?

With interest rates still reasonable and the above announcement by the Equity Release Council, the industry is set for another record-breaking year. Eighty percent of experts agree that the industry’s value is rising, and we at Sovereign Boss are excited to see further innovation from lenders and the Equity Release Council.

In Conclusion

Whether now is the best time to opt for an equity release product is very personal. You will need to consult a financial advisor who will help you determine the best course of action for your needs. If it’s in your interest to unlock equity at this stage, however, you’re likely to find a fantastic deal, with product flexibility better than ever.

So, while interest rates are rising, they’re not too much of an issue at this stage. And there is certainly no indication that there will be any short-term impact on the equity release industry. On the contrary, we are set for another record-breaking year.

That being said, it’s too early to predict the long-term impact that interest rates increase will have on the industry. But SovereignBoss considers it their responsibility to keep you updated with the latest industry trends.

This is a collaborative post.

If you enjoyed this post, please link to it on your own blog or social media:

Today I have the first in a series of three collaborative posts on the subject of equity release. This one examines the growing popularity of equity release and why it looks set to boom in the year ahead.

The equity release industry saw a massive expansion in 2021, with a record-breaking sum of over £4.8 billion being unlocked by retirees across the UK. This unprecedented growth has been welcomed amid a global pandemic, as the Equity Release Council helps regulate a retirement product that has given many retirees the means to a desperately needed income in these tough economic times.

Mark Patterson, the equity release expert from EveryInvestor, joins the ranks of fellow industry authorities in predicting that 2022 is set to be another record-breaking year. Let’s take a look at what’s expected and determine if unlocking equity is a good idea over the next few months.

Table of Contents

What Is Equity Release?

Equity release is a widely popular financial product for UK-based homeowners older than 55. In a nutshell, it gives you the opportunity to use your property’s equity but still live at home. With a third of UK retirees having less than £10,000 in retirement savings, equity release offers a lifeline to many. What’s more, the money can be used for any purpose.

According to figures from the Equity Release Council (ERC), equity release clients borrowed a total of £4.8 billion last year, a 24% rise on 2020’s figure.

Why is the Equity Release Industry Growing Amid a Tough Economy?

While many industries have crumbled in the wake of Covid 19, the equity release sector has grown tremendously. This is for several reasons, including:

Equity release provides financial security in a tough economic time.

The Equity Release Council has made the industry safe and is shifting a historically bad reputation.

Interest rates hit an all-time low in March 2021, and homeowners have received the best deals yet, with fixed-for-life interest rates.

Finally, growth inspires growth. As the industry expands, lenders offer more flexible products with bonus features, such as a free valuation or no completion fee.

What’s Predicted for 2022?

The future of equity release looks bright in 2022, and 80% of experts predict growth, with some believing this will be vastly beyond regular inflation. There are some key industry features that are likely to impact the industry (1).

First, the Equity Release Council announced on 31 January 2022 that all equity release lenders must offer the opportunity for voluntary loan and interest repayments. This announcement is welcome for potential borrowers, as voluntary repayments can vastly reduce the cost of your loan, yet there’s no obligation or risk of foreclosure.

On a slightly less positive note, equity release interest rates will rise in 2022 and should continue to do so until 2024. However, this could actually mean further industry growth. Rates are set to rise only slightly, and homeowners applying now will likely begin their equity release plans before we see any further increases.

Should I Unlock Equity from My Home at This Time?

With the market as it stands, it is a good idea to unlock equity if you’ve been planning to do so. However, it’s more complicated than just looking at the state of the industry.

Whether or not you should unlock equity from your home will depend on your personal circumstances and stage of life. What’s great is that equity release is safe; it’s overseen by the Equity Release Council and regulated by the Financial Conduct Authority (FCA).

However, to determine if it’s a good idea to unlock equity from your home, you should speak to a financial adviser. After all, seeking advice is compulsory when opting for an equity release product. The team at EveryInvestor will always encourage a whole-market financial adviser as they have an overview of the whole equity release market.

In Conclusion

Between flexible plans, the opportunity for voluntary repayments, and interest rates still low, now is a great time to release your property value through equity release. With another record-breaking year ahead of us, the industry is booming, and many more retirees are set to sign up to an equity release plan. Could you be next?

This is a collaborative post.

If you enjoyed this post, please link to it on your own blog or social media:

Today I have a sponsored guest post for you from my friends at Best Free Stuff. There are some great tips and ideas for getting things free, plus at the end is a link to a free competition where you can win a Lindt Chocolate Bunny just in time for Easter!

There are lots of great ways to get free stuff. For many, this is like a treasure hunt. Once people get their deal, they tend to share the good news with others. So a free deal can go viral quickly. Here are some suggestions for how you can get loads of quality, free products.

Free samples are really popular. Manufacturers like to give them out because it is a very effective way to promote a product. When a product is launched, people may not buy it right away because they don’t know if they will like it. However, if they have a chance to try it for free, then they can buy it if they like it. You may have seen vendors giving out samples at a carnival or community festival. Companies know that no-one can resist a free product. So it’s a win-win for both companies and consumers with free samples.

You can also get freestuff when you search online. There are many websites that have a special focus on gathering information on all kinds of free offers. You can get skincare samples, snacks, cleaning products, movie rentals, and just about anything consumers would want. You just have to click on a link that is connected with the product and fill out some information. Do realize that the provider of the free item will probably add your contact information to their mailing list. So, if you request a lot of free things, you should get ready to receive a lot of email advertisements. You will get the option to unsubscribe, however. So there is little risk in signing up.

Sometimes you can get free trials on full-sized products, such as a software download or a subscription. Do beware of any free trials that require you to enter your credit card information, though. Sometimes it may not be that easy to cancel after the trial.

Don’t forget about classified ads too. Ordinary people are giving away good-quality things every day for various reasons. Perhaps their children have outgrown their toys. Maybe they are moving to a new home and don’t want to take their old furniture with them. A business that is closing offices may be liquidating office furniture and equipment. Craigslist is a popular online classified platform that lists thousands of free items every day, in all major cities around the world. You never know what will be listed each day. If you are looking for something in particular, just type in a search term under the ‘free’ category and see what comes up.

These are just some common ways you can get great free stuff. Free things get snapped up quickly, so if you want the best stuff, you need to be diligent and monitor places that list these giveaways. Sign up for email alerts and keep checking back. If you are in the right place at the right time, you can score a great deal.

If you like to enter competitions, then we found this great competition where you can win 1 of 300 Lindt Bunnies (see cover picture). Click this link to enter today!

This is a sponsored post.

If you enjoyed this post, please link to it on your own blog or social media:

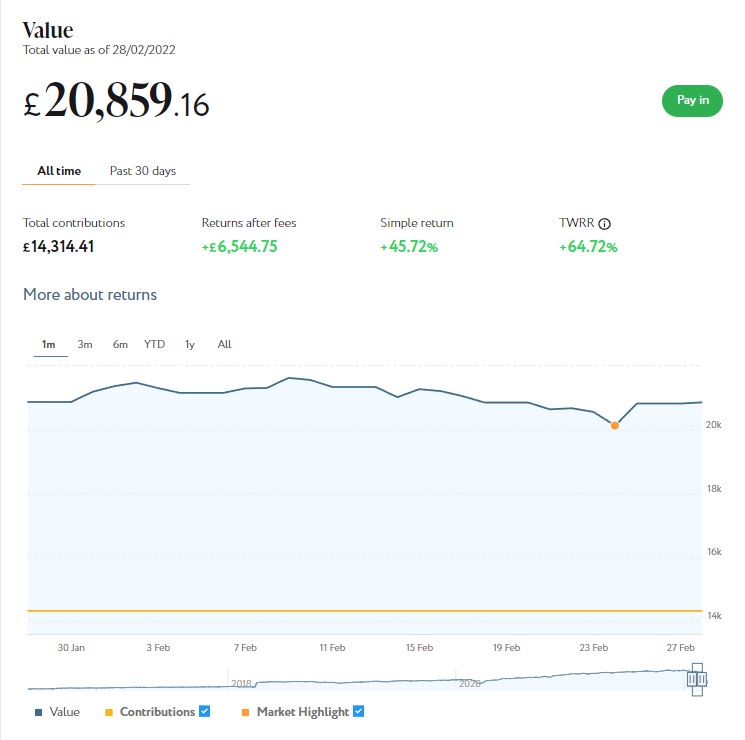

I’ll begin as usual with my Nutmeg Stocks and Shares ISA, as I know many of you like to hear what is happening with this.

As the screenshot below shows, my main portfolio is currently valued at £20,859. Last month it stood at £20,870, so that is a modest fall of £11.

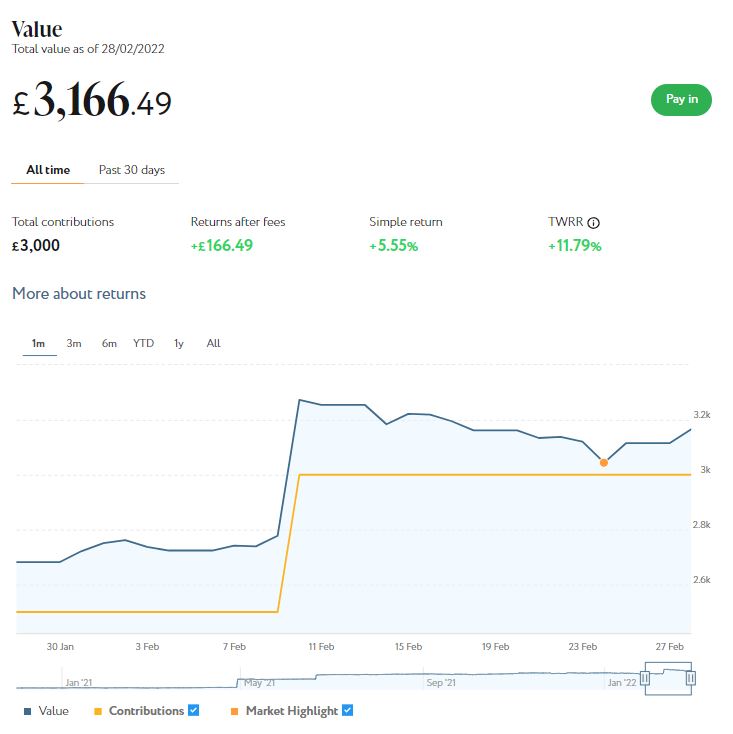

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £3,166 compared with £2,682 last month. However, that includes an extra £500 I deposited in February. If you deduct this from the current value that gives a figure of £2,666, a net fall of £16.

Here is a screen capture showing performance over the last month.

Obviously a big factor affecting equity prices this month has been the situation in Ukraine. The orange dot on both charts above shows the date when Russia invaded.

The war in Ukraine is above all a human tragedy, but inevitably it has serious implications for investors as well. So far, as you can see from the charts, the invasion hasn’t had a major impact on my Nutmeg investments (there was actually a bigger fall the previous month, due partly to tensions in Ukraine but also to economic factors like rising inflation). But obviously, if things go badly in the coming weeks, there could be bigger losses to come.

Even so, I intend to stay calm and avoid any panic reaction. I certainly don’t intend to crystallize my losses since the start of 2022 by selling up. I have already topped up my investment once while asset values are depressed and intend to do so again before this year’s ISA allowance ends in April.

As I have said before on PAS, all equity investments should be regarded as medium to long term. And it is worth noting that since I started investing with Nutmeg in 2016 I have still enjoyed a total return on my main portfolio of 45.72% (or 64.72% time-weighted). I should also mention that I selected quite a high risk level for both my Nutmeg accounts (9/10 for the main one and 5/5 for Smart Alpha). This has served me well generally, but I’m sure investors who selected lower risk levels will have seen smaller falls over the last couple of months.

If you also have a Nutmeg portfolio and plan to withdraw from it in the next few months, there is certainly a good case for switching to a lower risk level right now.

You can read my full Nutmeg review here (including a special offer at the end for PAS readers). If you are still looking for a home for your 2021/22 ISA allowance, based on my experience over the last six years, they are certainly worth considering.

As regular readers will know, this year I am using Assetz Exchange for my IFISA. This is a P2P property investment platform that focuses on lower-risk properties (e.g. sheltered housing on long leases). I put an initial £100 into this in mid-February 2021 and another £400 in April. Everything went well, so in June 2021 I added another £500, bringing my total investment on the platform up to £1,000.

Since I opened my account, my Assetz Exchange portfolio has generated £44.26 in revenue from rental and £74.68 in capital growth, a total of £118.94. That’s a decent rate of return on my £1,000 investment and does illustrate the value of P2P property investment for diversifying your portfolio when equity markets are volatile.

I won’t bother publishing a statement on this occasion as it’s not hugely different from last time. The bottom line is that I (still) have investments in 21 different projects with them and all are performing as expected, generating income and – in every case now – showing a profit on capital. So I am very happy with how this investment has been doing.

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of AE as far as i am concerned. You can actually invest from as little as 80p per property if you really want to proceed cautiously.

Another property platform I have investments with is Kuflink. They have been doing well recently, with new projects launching almost every day. I currently have over £2,100 invested with them, quite a large proportion of which comes from reinvested profits. To date I have never lost any money with Kuflink, though some loan terms have been extended once or twice. On the plus side, when this happens additional interest is paid for the period in question. At present all my Kuflink loans are performing to schedule.

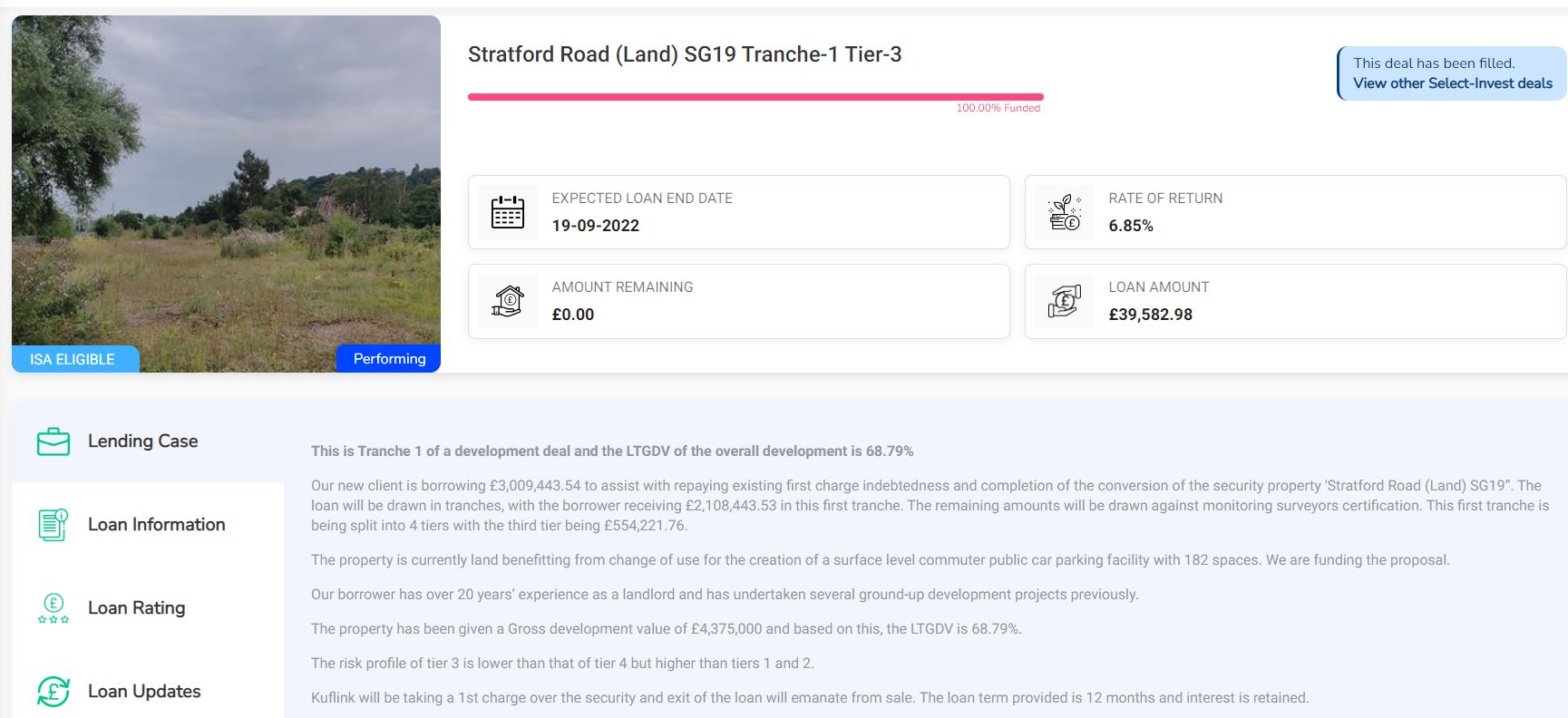

Another of my Kuflink investments reached maturity in the last few weeks and I reinvested the capital released. You can see a screen capture of the new project below, a loan to convert some waste ground in the Stevenage district into a car park. It was a different sort of project from those I have previously invested in, but the case set out on the website seemed convincing.

My loans with Kuflink pay annual interest rates of 6 to 7.5 percent. As mentioned above, these days I invest no more than around £150 per loan (and often less). That is not because of any issues with Kuflink but more to do with losses of larger amounts on other P2P property platforms in the past. My days of putting four-figure sums into any single property investment are behind me now!

Nowadays I mainly opt to reinvest the monthly repayments I receive from Kuflink, which has the effect of boosting the percentage rate of return on the projects in question

You can read my full Kuflink review here. They offer a variety of investment options, including a tax-free IFISA paying up to 7% interest per year with built-in automatic diversification. Alternatively you can now build your own IFISA, with most loans on the platform (including the one shown above) being IFISA-eligible.

I’d also particularly draw your attention to Kuflink’s revised and more generous cashback offer for new investors [affiliate link]. They are now paying cashback on new investments from as little as £500 (it used to be £1,000). And if you are looking to invest larger amounts, you can earn up to a maximum of £4,000 in cashback. That is one of the best cashback offers I have seen anywhere (though admittedly you will need to invest £100,000 or more to receive that!).

I also recently published a blog post about another P2P property investment platform called BLEND. Like Kuflink, they offer the opportunity to invest in secured loans to experienced property developers. They offer (on average) somewhat higher rates of return than Kuflink, though arguably with a little more risk. As well as my blog post about BLEND, you can also check out what they have to offer on their website [affiliate link].

Moving on, I have another article on the always-excellent Mouthy Money website. This is quite a personal one in which I set out my views about the FIRE (Financial Independence, Retire Early) movement. For various reasons set out in the article I am not a fan of this. You can read my article here 🙂

That’s more than enough for now, so I’ll sign off till next time. I hope you are keeping safe and well, and (if you live in England especially) are enjoying the more relaxed Covid restrictions that now apply. Here’s looking forward to a more normal spring and summer than the last two years. If you’re planning any UK short breaks, don’t forget I have a list of places I have visited and recommend here 🙂

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that this post includes affiliate links (disclosed). If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered.

If you enjoyed this post, please link to it on your own blog or social media:

As I’m sure you know, energy bills in the UK (and worldwide) are rising rapidly at the moment. Add this to tax hikes and surging inflation, and many of us will undoubtedly be feeling the pinch in the months (and years) ahead.

The government has announced various measures to try to mitigate the impact of energy price rises. These include £150 council tax rebates for those in Bands A to D and a (somewhat controversial) £200 rebate on energy bills, repayable at £40 a year over five years. These measures may help a bit, but they are unlikely to cover all the increased costs on their own.

So today I am looking at how you may be able to cut your bills by reducing the amount of gas and electricity you use. I am indebted to my friends at renewable energy specialists Ecoflow for their infographic (below) and research, which I shall be quoting from in this article.

Table of Contents

Infographic

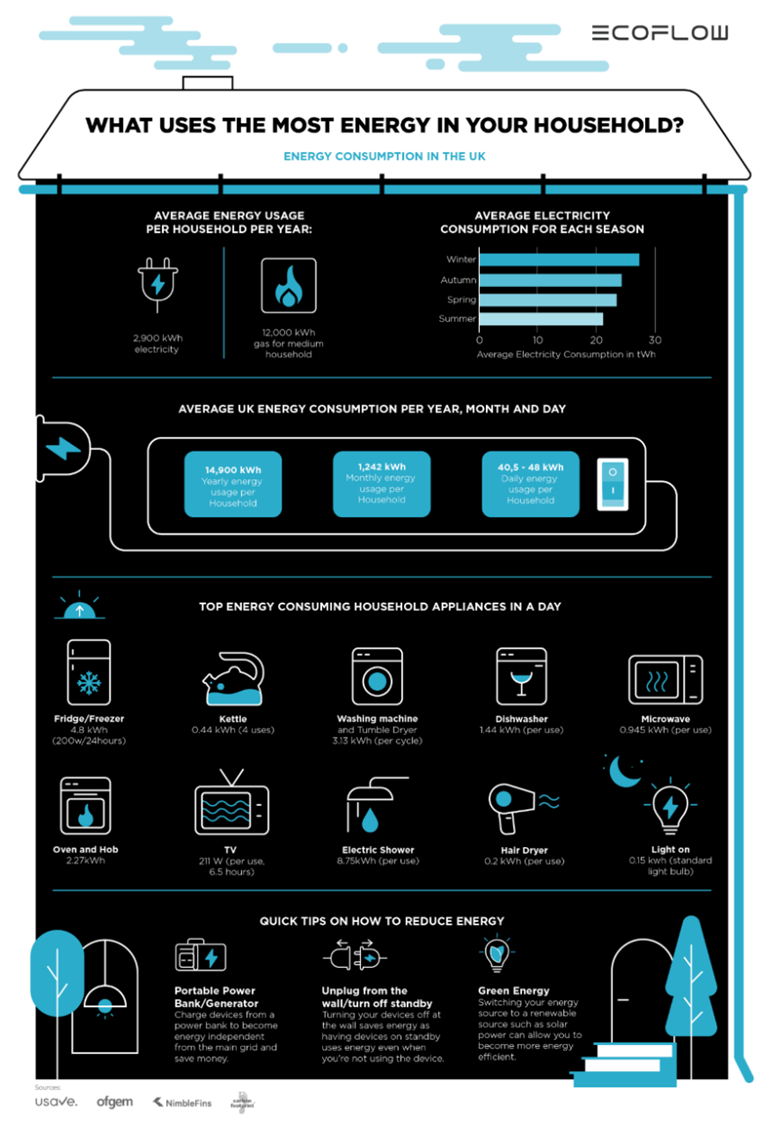

The Ecoflow infographic below shows a range of data about household energy consumption, including how much electricity we typically use in a year and which appliances use the most.

The graphic shows that an average UK household consumes 14,900 kWh of energy (gas and electricity) per year. That represents a daily energy consumption of 40.5 – 48 kWh per household.

The graphic also shows the amount of power used by different appliances in the home. Not surprisingly, the ones using most energy are cookers (19% of our total energy consumption) and so-called wet appliances (21%). Wet appliances include any that use water – washing machines, dishwashers, electric showers, and so on.

Covid has of course led to a huge increase in working from home – a trend which looks set to continue even as we move out of the pandemic. This has inevitably resulted in an increase in household energy consumption. Ecoflow say that the UK’s electricity consumption saw a 10% increase in 2021, reversing the trend in 2020 during which consumption fell by 14% year on year. The sharp increase in 2021 came largely from a return to relative normality following the restrictions and lockdowns of 2020.

When Is Most Energy Used?

EcoFlow have produced a breakdown of how our daily habits affect our energy consumption, which appliances are the most energy-hungry, and how we can change our habits to reduce our energy consumption. I have set out the main findings below, along with some ‘top tips’ for reducing energy consumption in the part of the day concerned.

Morning

A survey into Britain’s most popular breakfast choices found that 4/5 of Brits’ favourite breakfast foods are cooked. Despite changing lifestyles and eating habits, a cooked breakfast is clearly still a very popular choice. But how much electricity does it consume? Cooking appliances such as hobs (0.71 kWh per use), ovens (1.56 kWh per use) and microwaves (0.945 kWh per use) account for 19% of average electricity use.

Top Tip – As microwaves are more energy efficient than ovens, try batch cooking at the beginning of the week and reheating leftovers, rather than using the oven for every meal.

Afternoon

Working from home obviously increases electricity consumption, as devices such as laptops (0.4 kWh for 8-hour days), monitors and webcams become essential aspects of our home office. But WFH also allows us to carry out daily chores such as vacuuming and using the dishwasher (3.13 kWh per cycle) throughout the day. As mentioned above, wet appliances account for around 21% of our total electricity use.

Top Tip – Simple things to look out for to reduce electricity consumption include switching your washing machine to ‘eco’ mode and ensuring you only run it when it’s full. This will not only save energy, it will save water as well (and money if you are on a water meter).

Evening

Ecoflow’s research found that electricity consumption increased by 21% during the winter of 2020 compared to the summer. As the days become shorter during the winter months, our electricity consumption goes up and use of lighting increases significantly. Lighting accounts for 14% of the overall electricity usage in a home – per bulb this is 0.84 kWh.

Top Tip – Turning off lights and/or switching to energy-saving LED bulbs is an essential part of moving towards a more energy-efficient way of living.

More Tips for Saving Energy

Here are a few more tips for reducing your energy consumption and cutting bills, starting with one from the infographic.

Unplug devices from the wall and turn off standby. Leaving devices such as TVs on standby uses extra electricity. Though only a relatively small amount, if devices are left on 24/7 the cost adds up.

With rising energy prices, switching to renewables such as solar panels becomes ever more attractive. Although the government has reduced financial incentives such as feed-in tariffs, the savings alone from generating your own energy are increasingly compelling.

Insulating your home to keep warmth in during the winter months can reduce your heating bills. Even simple, inexpensive things like putting draft-excluders at the bottom of doors can make a significant difference over the course of a year.

If you have an old, inefficient gas boiler, consider replacing it with a more modern one. The Energy Saving Trust estimates that an average household could save £195 by switching from an old, G-rated boiler to a new, A-rated condensing boiler with a programmer, room thermostat and thermostatic radiator valves. If you live in a detached house, you could save up to £300 a year. Obviously installing a new boiler isn’t cheap, but if you can find the money it should be a very good investment.

If you have an old, inefficient boiler and receive pension credit or tax credits, you may be eligible for a FREE boiler replacement under the government’s ECO scheme. For more information about this, check out the in-depth article above from my colleagues at Over 60s Discounts.

Keep tumble dryer usage to a minimum as they use large amounts of electricity. According to the Energy Saving Trust, an average tumble dryer uses roughly 4.5 kWh of electricity per cycle. Dry clothes outside if possible or over an airer.

Wash clothes at 30 degrees (or cooler) wherever possible. Modern washing machines will still do a good job at these lower temperatures, and again the energy savings add up.

Closing Thoughts

Obviously I hope rising energy costs will not cause you serious hardship. No-one should ever be forced to choose between ‘heating and eating’. But I hope the information and tips in this article will at least help you reduce your energy consumption in the months ahead and hence lower your bills.

Remember also that if you’re on a low income, there are government schemes such as the Warm Home Discount to help you.

In addition, you may be able to save money by switching energy supplier. Right now there aren’t many good deals around, but if you switch to EDF via my (affiliate) link you can get £50 credited towards your energy account, which should certainly help a little 🙂

Thank you again to my friends at Ecoflow for their infographic and research data. As their R&D Director, Thomas Chan, says: ‘We have to remain mindful of our energy usage and the direct effects it has on the environment and climate change. By becoming energy independent and using renewable sources of energy such as solar, people can avoid high electricity bills during the winter months.’

As always, if you have any comments or questions about this post, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

Today I’m looking at Hargreaves Lansdown, an investment platform I have used on various occasions myself over the last few years.

HL describes itself as ‘the UK’s number 1 investment platform for private investors’ and it’s hard to argue with that. It is officially the largest stockbroker in the UK and listed on the FTSE 100.

At the start of 2022 the company had a staggering £135.5 billion of assets under administration (AUA) – considerably more than their two biggest rivals in the UK, AJ Bell YouInvest and Interactive Investor.

Table of Contents

What Does HL Offer?

As you might expect for such a large company, Hargreaves Lansdown offers a wide range of accounts. These include:

Within their investment accounts, clients can select from a huge range of funds and individual company shares. HL have over 500 funds listed, including OEICs and unit trusts. You can also invest in thousands of individual company shares on the UK, US, European and Canadian markets.

What Are The Charges?

HL charges an annual platform fee of 0.45% for shares, ETFs and investment trusts.

For funds, the fee begins at 0.45% for the first £250,000, 0.25% for the next £750,000, and 0.1% for the next £1,000,000. There are no additional charges for any fund holdings over £2,000,000.

There are caps on maximum charges for different account types, e.g. a maximum £45 annual management charge on shares in a Stocks and Shares ISA. For more information about fees and charges, see the HL website.

Share dealing charges start at £11.95 per deal but reduce to as little as £5.95 based on the number of deals you made in the month before. This is set out in the table below.

Note that there is an added foreign exchange charge for overseas share deals, depending on deal size

Information and Advice

As well as dealing and portfolio management, Hargreaves Lansdown also offer investment information and advice.

For starters they have The Wealth Shortlist, a list of recommended funds researched and chosen by HL for their long-term potential. This can help investors narrow down their choice of funds from the vast number available on the platform.

HL also offer a service called Portfolio+. This is aimed at people who want to invest but prefer to leave the choice and management of investments to HL’s experts. You simply choose one of six ready-made portfolios that invest in a broad mix of assets across a range of countries and regions, giving lots of diversification (something regular readers will know I’m a big fan of).

Portfolio+ offers simplicity, performance potential and a low minimum investment of £1,000. Portfolios can be sold at any time free of charge (though of course they should only be bought as long-term investments). Once invested, portfolios are automatically rebalanced twice a year. No additional charges are levied for managing your portfolio. Not surprisingly, Portfolio+ is a popular choice among HL investors.

Personalized advice from professional financial advisers is also available via the HL platform. There is (of course) a charge for this, but the initial consultation is free. Again, see the HL website for more information.

For those brand new to investing, a very useful resource is HL’s Investing – As Easy As 1, 2, 3 page. This takes you through the basics of why, when and how to invest.

What Are the Pros and Cons of Hargreaves Lansdown?

Pros

Large, well-established platform with huge (over 1.5 million) client base

Wide range of accounts to meet all needs

Well-designed, user-friendly website

Mobile app also available

No dealing fees when buying or selling funds

Highly rated UK-based customer service team

Information, advice and ready-made portfolios available

Cons

Share dealing fees of up to £11.95 per deal are above average

Management charges for larger (over £50,000) portfolios are less competitive

What Do Users Think?

On the popular independent TrustPilot website, HL has an average rating of 4.2 (‘Great’) at the time of writing, with 55% of users awarding them a maximum five stars rating. That is on a par with the other leading UK investment platforms.

Positive comments emphasize the high-quality customer service, the well-designed website, and the range of investment products available. There are fewer negative comments, but some of these concern HL’s above-average charges for some services. There are also a few complaints regarding technical issues with the website.

Hargreaves Lansdown has also received various industry awards, including ‘Best Share Dealing Platform 2021’ (UK Investor Magazine) and ‘Best Digital ISA’ (Boring Money 2021 Best Buys).

Closing Thoughts

If you are planning to start investing (or switch from your current platform) Hargreaves Lansdown undoubtedly has a lot going for it. It’s a popular, well-established platform with a wide range of accounts and services on offer. Their charges are generally competitive, and (as I can testify myself) the UK-based customer service is first rate.

Their Portfolio+ service is an attractive option for novice investors – but equally, if you are happy to pick your own shares and funds, HL has all the info and tools you need.

If you are planning to regularly buy and sell individual shares, Hargreaves Lansdown is on the pricey side. In that case a low-cost share-dealing service such as eToro might be better for you. They offer commission-free trading on shares and charge no monthly account fee. That makes them ideal for short-term traders and investors looking to build a portfolio of shares cheaply. Of course, this is a much riskier approach to investing, and not recommended for those new to the field.

As ever, if you have any comments or questions about this blog post, please do leave them below.

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that this post includes affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered.

If you enjoyed this post, please link to it on your own blog or social media:

I’ll begin as usual with my Nutmeg Stocks and Shares ISA, as I know many of you like to hear what is happening with this.

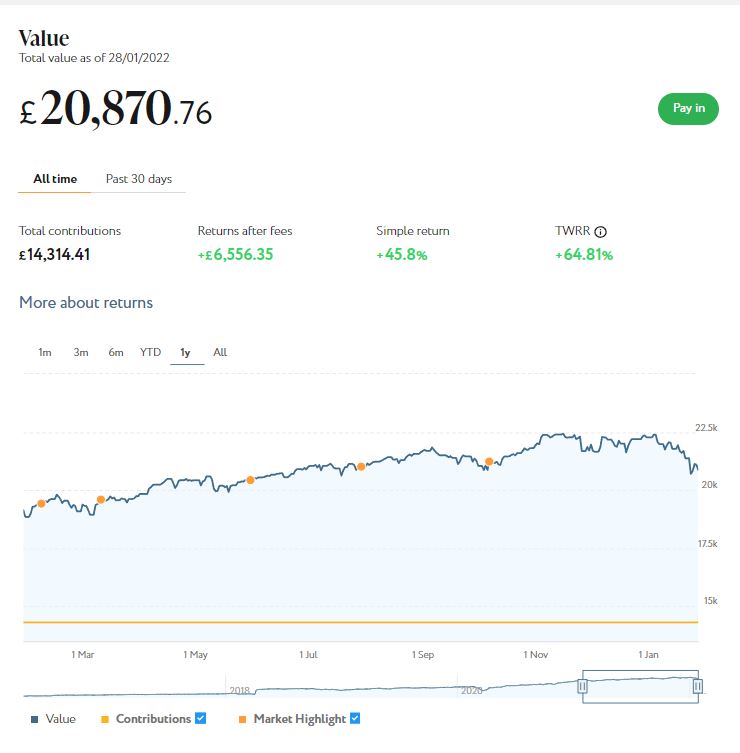

As the screenshot below shows, my main portfolio is currently valued at £20,870. Last month it stood at £22,275, so that is a fall of £1,405.

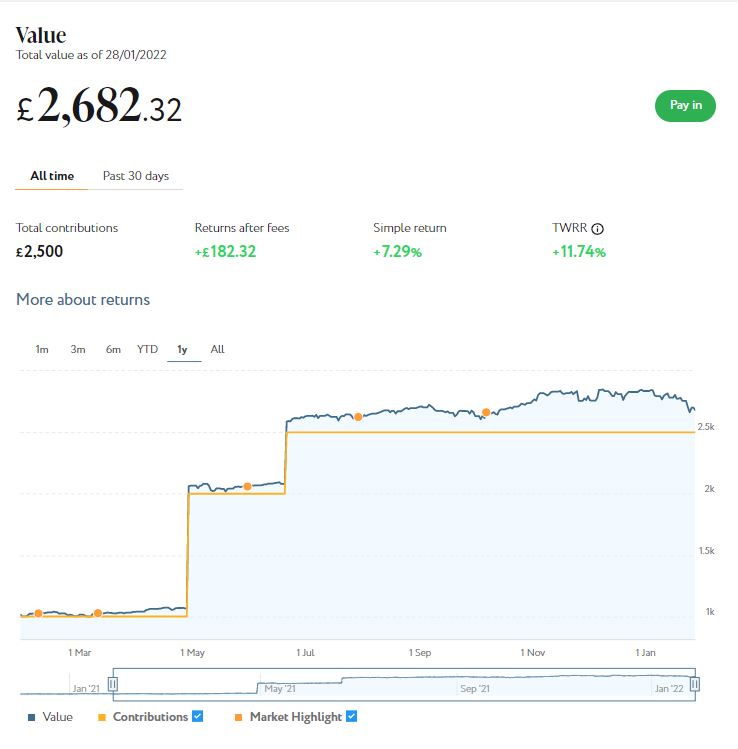

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £2,682 compared with £2,837 last month, a net fall of £155. Here is a screen capture showing performance over the last year.

There is no denying 2022 has got off to a disappointing start as far as these investments are concerned. Overall, they take the value of my portfolio back to where it was at the end of June 2021.

It is though worth noting that since I started investing with Nutmeg in 2016 I have still enjoyed a total return on my main portfolio of 45.8% (or 64.81% time-weighted). I should also mention that I have selected quite a high risk level for both my Nutmeg accounts (9/10 for the main one and 5/5 for Smart Alpha). This has served me well generally, but I’m sure investors who selected lower risk levels will have seen smaller falls this month.

Of course, it’s not just Nutmeg investors who have had a bad month. Equities generally have taken a tumble in the last few weeks. Commentators have varying opinions about this, but two reasons are typically mentioned: (1) the rising tensions (and threat of war) in Ukraine; and (2) rising inflation rates allied with the removal of monetary stimulus measures as we come out of the pandemic. Obviously nobody knows for sure which way things will go, but this recent post from the Nutmeg blog sets out some grounds for cautious optimism over the year ahead.

Personally I intend to take advantage of the current dip by topping up my Nutmeg investment while asset values are depressed. I plan to add to my Smart Alpha holding, as overall this has been doing slightly better than my main portfolio. I’m also conscious that the end of the 2021/22 tax year will soon be upon us. That means the end of the current year’s ISA allowance, so it really is a case of use it or lose it!

The above is just my view, of course, and should not be construed as personal financial advice for anyone else to follow.

You can read my full Nutmeg review here (including a special offer at the end for PAS readers). If you are still looking for a home for your 2021/22 ISA allowance, based on my experience over the last six years, they are certainly worth considering.

As regular readers will know, this year I am using Assetz Exchange for my IFISA. This is a P2P property investment platform that focuses on lower-risk properties (e.g. sheltered housing on long leases). I put an initial £100 into this in mid-February 2021 and another £400 in April. Everything went well, so in June 2021 I added another £500, bringing my total investment on the platform up to £1,000.

Since I opened my account, my Assetz Exchange portfolio has generated £37.18 in revenue from rental and £91.19 in capital growth, for a total return of £128.37. That’s an increase of £35.99 on last month alone, and does I guess illustrate the potential value of P2P property investment for diversifying your portfolio when equity markets are volatile.

I won’t bother publishing a statement on this occasion as it’s not massively different from last time. The bottom line is that I (still) have investments in 21 different projects with them and all are performing as expected, generating income and – in every case now – showing a profit on capital. So I am very happy with how this investment has been doing.

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of AE as far as i am concerned. You can actually invest from as little as 80p per property if you really want to proceed cautiously.

Another property platform I have investments with is Kuflink. They have been doing well recently, with new projects launching almost every day. I currently have just over £2,000 invested with them, quite a large proportion of which comes from reinvested profits. To date I have never lost any money with Kuflink, though some loan terms have been extended once or twice. On the plus side, when this happens additional interest is paid for the period in question.

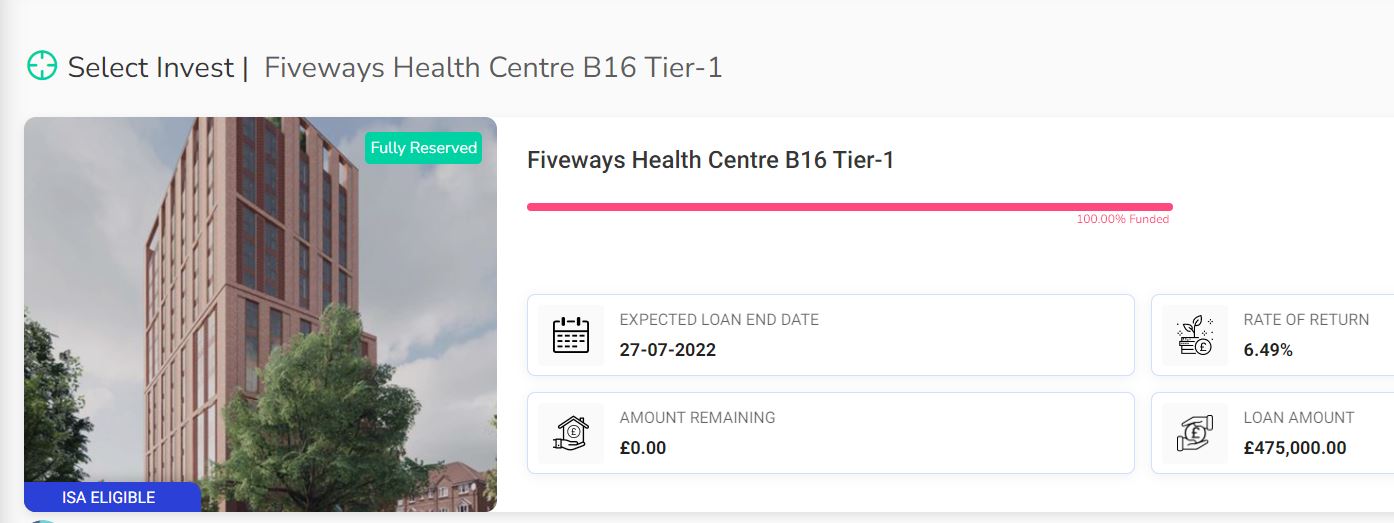

Several of my Kuflink investments reached maturity in the last few weeks and I reinvested the capital released. Here is one of the new projects I invested in, a loan to convert a disused medical centre in Five Ways, Birmingham into residential accommodation. It looked a solid investment, and I also liked the fact that it was redeveloping a derelict building in Birmingham, a city where I lived for around twenty years.

My loans with Kuflink pay annual interest rates of 6 to 7.5 percent. As mentioned above, these days I invest no more than around £150 per loan (and often less). That is not because of any issues with Kuflink but more to do with losses of larger amounts on other P2P property platforms in the past. My days of putting four-figure sums into any single property investment are behind me now!

Nowadays I mainly opt to reinvest the monthly repayments I receive from Kuflink, which has the effect of boosting the percentage rate of return on the projects in question

You can read my full Kuflink review here. They offer a variety of investment options, including a tax-free IFISA paying up to 7% interest per year with built-in automatic diversification. Alternatively you can now build your own IFISA, with most loans on the platform (including the one shown above) being IFISA-eligible.

I’d also particularly draw your attention to Kuflink’s revised and more generous cashback offer for new investors [affiliate link]. They are now paying cashback on new investments from as little as £500 (it used to be £1,000). And if you are looking to invest larger amounts, you can earn up to a maximum of £4,000 in cashback. That is one of the best cashback offers I have seen anywhere (though admittedly you will need to invest £100,000 or more to receive that!).

I also recently published a blog post about another P2P property investment platform called BLEND. Like Kuflink, they offer the opportunity to invest in secured loans to experienced property developers. They offer (on average) somewhat higher rates of return than Kuflink, though arguably with a little more risk. As well as my blog post about BLEND, you can also check out what they have to offer on their website [affiliate link].

Next up, I wanted to give another plug for an excellent low-key sideline-earning opportunity I have mentioned previously on Pounds and Sense. This opportunity is based on matched betting, a sideline I have pursued for several years myself. Several PAS readers (including my sister Annie!) have signed up for this and are now enjoying a tax-free, hassle-free sideline income from it 🙂

I have been asked not to divulge too many details about this publicly, for good reasons I will explain privately to anyone who may be interested (and no, it’s not illegal!). It doesn’t require any financial outlay and is risk-free and entirely hands-off (once you have set up your account). No knowledge of betting is required and you don’t have to place any bets yourself (this is all done by the company’s clever software). You just have to set up a separate bank account for bets to go through, but running the account is entirely financed by the company.

The company has changed its terms somewhat for new members. You now get a larger £100 initial reward payment once your account is up and running, and then £25 every month you remain a member. I think this is a good move personally, as setting up the account does involve a little work on your part (though it’s certainly not like going down the mines). So the £100 in effect compensates you for your time, and once it’s done you continue to get £25 a month for no effort at all.

The company is constantly developing its offering, partly in response to feedback from PAS readers. They recently launched a new mobile-friendly website to make it even easier for new members to sign up (once you’re up and running you shouldn’t need to use the website at all). They also recently incorporated an Open Banking app so that members don’t have to provide their online banking info to the company, as some people were concerned about this.

Please note that this opportunity is only open to honest, trustworthy people who haven’t done matched betting before and have no more than two accounts already with online bookmakers. For more information (and to receive a no-obligation invitation) drop me a line including your email address via my Contact Me page. And yes, I will receive a reward for introducing you, but this will not affect the service or the rewards you receive.

In the interests of full transparency, I should say that if you do matched betting yourself, you may be able to make more money than that being offered by the company. However, you will have to research the techniques in detail, place all bets yourself, and probably subscribe to a matched betting advisory service such as Profit Accumulator [affiliate link]. This opportunity is really for those who want an easy way to make some extra money without the hassle (or expense) of learning/applying matched-betting methods themselves.

Moving on, I have another article on the always-excellent Mouthy Money website. Coincidentally, this is about my experiences with P2P property investment over the last few years, both good and not-so-good. Do check it out! 🙂

I was also quoted by Jackie Annett of the Express newspaper in this article about working after retirement. It’s a short but interesting read, especially if you’re coming up to retirement (or already there) yourself.

That’s more than enough for now, so I’ll sign off till next time. I hope you are keeping safe and well, and (if you live in England especially) are enjoying the more relaxed Covid restrictions that now apply. Here’s hoping that normal life across the whole of the UK will be able to resume very soon!

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that this post includes affiliate links (disclosed). If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered.

If you enjoyed this post, please link to it on your own blog or social media:

Today I have a guest post for you from my friends at Broadway Autocentres. As specialists in this field, they know exactly what it takes to get the most out of your car tyres.

Over to the experts, then…

When it comes to driving your own car, all the costs seem to mount up. If you’re not saving for the next service, you’re putting money aside for the MOT. And just when that is out of the way, you realise that you don’t know how old your tyres are or when they will need to be replaced.

There is no way to have your car use less fuel or oil, and skipping services is a bad idea – but if you can reduce the wear and tear on the vehicle whenever possible, so much the better for your purse or wallet.

Tyres are one of the biggest expenses you will face, so let us look at five ways to get the most out of your tyres before you bow to fate and replace them!

Table of Contents

Buy Them in Twos

Buying a set of four tyres can seem impossible with a tight budget, so why not replace your tyres in twos instead? Depending on whether your car is front or back wheel drive, either the front set or back set will take the most punishment. It is the most worn tyres that should be replaced, with the more lightly worn set moving to take their place and the new tyres going where they will receive less wear. This system may seem inconsistent, but it will ensure that you stay safe while on the road without needing to spend a lot of money all at once.

Drive Sensibly

Drive according to the Highway Code at all times and resist the temptation to put your car through its paces. Maintain a safe speed, avoid rough or unsurfaced roads, and increase and decrease speed slowly whenever possible. All of these will help to keep your tyres in good condition for longer, so you can keep saving for their eventual replacements.

Buy the Best

While it may seem counter-intuitive, buying the best quality tyre you can afford is often more economical when taken over time. Budget tyres are sometimes made with flaws that can weaken the tyres more quickly, or with inferior rubber that begins to crumble and break apart. Better quality tyres will last better – sometimes twice as long as budget tyres, thereby comparatively halving their cost to you. You can book your tyres in Buckinghamshire at Broadway Autocentres (01494 680914).

Regular Checks

Get into the habit of checking your tyres often, looking for early signs of damage or weakness. In many cases, prompt corrective action or a swift repair can keep the tyre in place for some time, giving you the chance to continue getting out and about without suddenly needing to spend money on a new set or pair of tyres.

Proper Inflation

Modern tyres – no matter whether budget or premium – are designed to be used within a narrow recommended range of pressure, and will often perform poorly outside of this range. Keep your tyres inflated to within the range recommended by the manufacturer (this can be found online, sometimes on the tyre itself, or inside the car owner’s handbook) to ensure that not only do your tyres last as long as possible, but you are safer on the roads during this time. Correctly inflated tyres also aid fuel economy, saving you money that way as well.

Thanks again to my friends at Broadway Autocentres for their expert advice. As always, if you have any comments of questions about this post, please do leave them below.

This is a sponsored post.

If you enjoyed this post, please link to it on your own blog or social media: