Today I am spotlighting BLEND, a peer-to-peer property platform that lends to established businesses (mostly experienced property developers). BLEND’s loan-based crowdfunding platform was founded by a team of former investment bankers with substantial experience in real estate and finance.

What Does BLEND Offer?

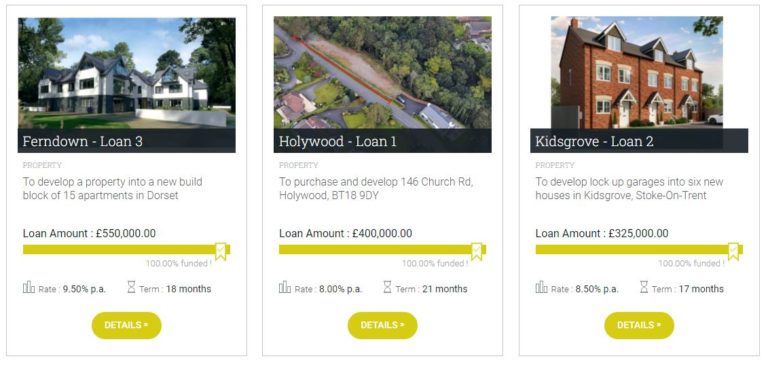

BLEND offers individuals the chance to invest in loans secured against property. They specialize in loans in geographical areas that banks and other lending platforms typically pay less attention to, e.g. Northern Ireland, though they fund projects across the whole of the UK. Loans are typically for small developments or building renovation/conversion projects. Some examples are shown in the screen capture below.

As mentioned above, all loans are secured against property. The LTV (loan-to-value ratio) is usually quite low, giving greater security for investors. Interest rates on offer range from 7 to 12 percent.

BLEND has some similarities with Kuflink, which I reviewed in this blog post a while ago (and invest in myself). Both offer the opportunity to invest in secured loans. Kuflink typically offers lower interest rates, however, between 5 and 7 percent. The risk level with Kuflink loans is (arguably) lower, but it should be said that BLEND so far has an unblemished record, with no loans in arrears or default.

The minimum investment on BLEND is £1,000, which means it is really aimed at high net worth and professional investors. It’s also worth noting that only a small number of new loans tends to be available at any given time and they typically sell out very quickly.

Using the AutoLend feature is recommended to ensure that you don’t miss out when a new loan comes on to the market.

Secondary Market

One drawback with any type of property investment is that it’s not as liquid as (say) equity-based investments. BLEND does offer a way around this with its secondary market, however.

Lenders who wish to liquidate early can sell their loan parts on the secondary market. Note that finding a buyer on the secondary market may take time and there is always a risk of no-one wanting to buy your loan part. You can start selling a loan in multiples of £1,000 on the secondary market as soon as funds have been released to the borrower.

Unlike the primary market, as a lender you will be charged a secondary market fee of 0.60% (or £6 for every £1,000 of capital) on capital outstanding. BLEND only charge this upon the successful resale of the loan portion you have listed in the secondary market. The secondary market is free for buyers.

Pros and Cons

A full list of Pros and Cons for BLEND is shown below.

Pros

1. Easy sign-up process

2. Well designed, user-friendly website

3. All loans secured against property

4. Low LTV ratios for added security

5. Manual and auto-invest options

6. In-depth info provided on the website about loans, so you can see exactly how your money will be used (and by whom)

7. No investor losses to date

8. Marketplace (secondary market) for buying and selling loan parts

9. No charges to investors lending on the primary market and only a 0.6% fee if you resell a loan part on the secondary market

10. Rates of return of up to 12% are at the upper end for P2P lending

11. Can invest via a SIPP or SSAS (private pension scheme)

Cons

1. Minimum investment of £1,000

2. Limited supply of new loans to invest in

3. No tax-free IFISA option

Final Thoughts

With a minimum investment of £1,000 (per project), BLEND obviously won’t be suitable for everyone. But if you have that sort of money available, the promised returns of up to 12 percent are undoubtedly enticing.

I like the fact that BLEND are very selective in the projects they back, even if that does mean the flow of new opportunities is limited. It’s also good that they perform in-depth ‘due diligence’ on every loan and publish full details about this on the website, including independent valuations. This means investors know exactly what the potential risks and rewards of a project are.

The absence of any charges to investors (apart from on the secondary market) is another big plus. And the presence of a secondary market offers the opportunity to exit loans early if your circumstances change (though, as noted above, you aren’t guaranteed to find a buyer).

BLEND is probably at the riskier end of the P2P property spectrum, but in my opinion the returns on offer fairly reflect this. Risks are also mitigated by generally low LTV ratios and the detailed research mentioned above. The fact that no loan has so far gone into default or even into arrears is impressive, though there is of course no guarantee this couldn’t happen in future. It does offer some reassurance though.

Finally, BLEND has an average Trustpilot rating of 4.6 (‘Excellent’), with 95% of people awarding them a maximum five stars rating. This is among the highest ratings I have seen for an investment platform on Trustpilot.

As always, if you have any questions or comments about this post or P2P property investment more generally, please do leave them below.

Disclaimer: I am not a qualified financial adviser and nothing in the article above should be construed as personal financial advice. You should always do your own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Please note also that this post includes affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect in any way the terms you are offered or the product/service you receive.

If you enjoyed this post, please link to it on your own blog or social media:

As regular readers will know, I recently started posting monthly updates about my investments. These partly replace the ‘Coronavirus Crisis Updates’ I was posting from March 2020. You can read my November 2021 Investments Update here if you like

I’ll begin as usual with my Nutmeg Stocks and Shares ISA, as I know many of you like to hear what is happening with this.

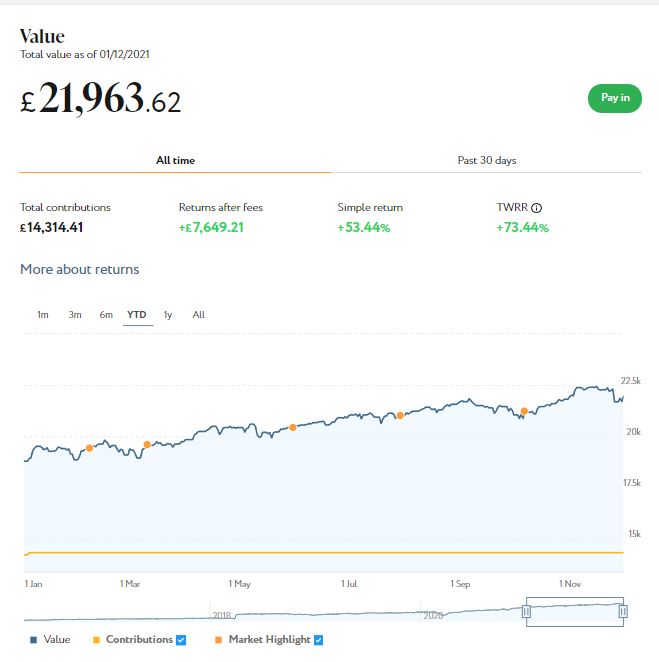

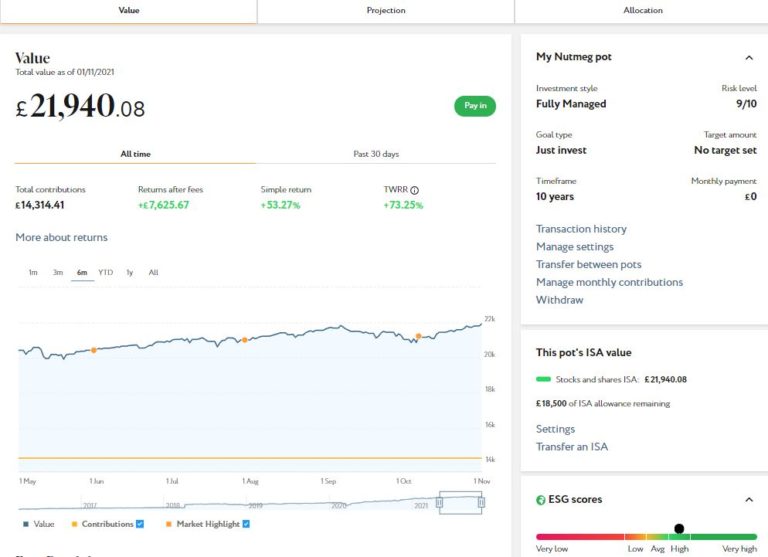

As the screenshot below shows, my main portfolio is currently valued at £21,963. Last month it stood at £21,940, so that is a modest rise of £23. Those figures don’t tell the whole story, though. In the early part of November, the value of this portfolio rose as high as £22,398. Unfortunately then news of the new Omicron variant spooked the markets and share prices fell dramatically. In the last few days there has been a modest recovery, resulting in the small month-on-month gain referred to above.

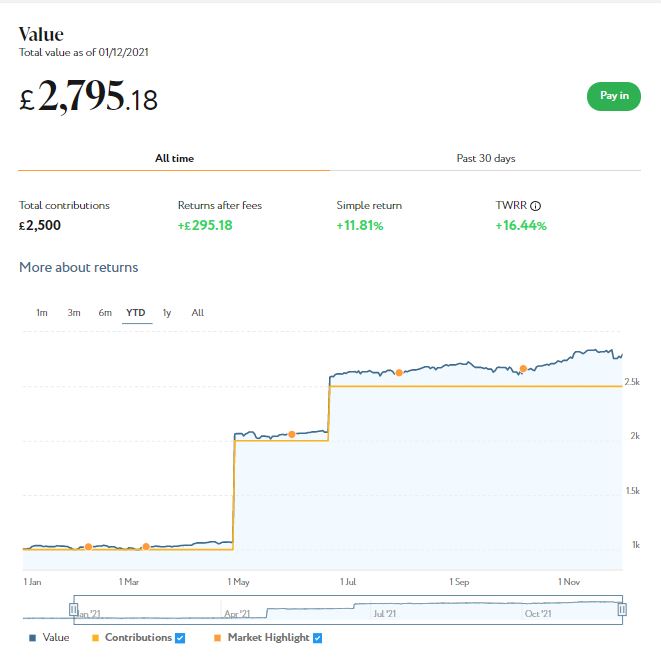

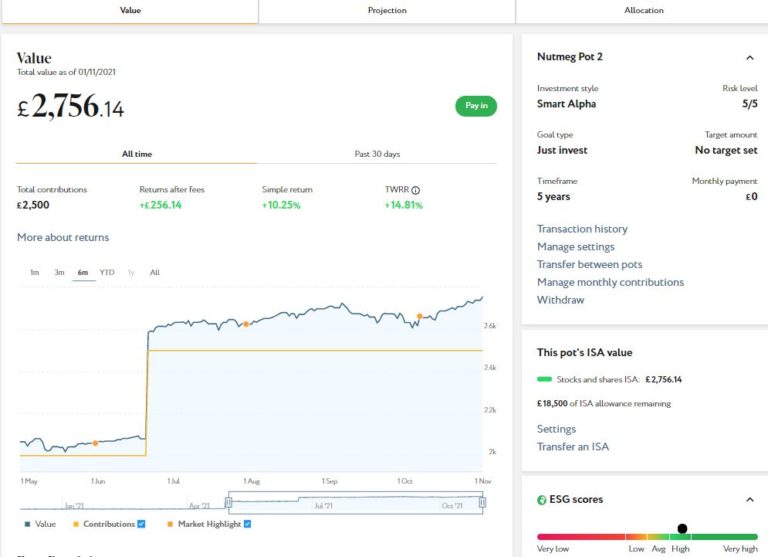

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This has followed a similar trajectory, though it has actually done a bit better than my main pot. It is now worth £2,795 compared with £2,756 last month, a net monthly increase of £39. Here is a year-to-date screen capture showing performance to the start of December 2021.

As I always say, you shouldn’t judge the performance of any equity-based investment on a month-by-month basis. But in these strange times I remain very happy with how my Nutmeg investments are doing. Hopefully the initial panic over Omicron may prove to have been excessive (it may help that there is growing evidence that this new variant typically causes only a mild illness). That being the case, I remain optimistic that the modest recovery in the markets over the last few days will continue.

You can read my full Nutmeg review here (including a special offer at the end for PAS readers). If you are still looking for a home for your 2021/22 ISA allowance, based on my experience they are certainly worth considering. If you haven’t yet seen it, check out also my blog post in which I looked at the performance of Nutmeg fully managed portfolios at every risk level from 1 to 10 (my main port is level 9). I was actually pretty amazed by the difference the risk level you choose makes. If you are investing for the long term (and you almost certainly should) in my view opting for a hyper-cautious low-risk strategy may not be the smartest thing to do.

As regular readers will know, this year I am using Assetz Exchange for my IFISA. This is a P2P property investment platform that focuses on lower-risk properties (e.g. sheltered housing on long leases). I have invested a total of around £1,000 in AE so far (I began with £100 in February 2021 and topped up twice).

Since I opened my account, my portfolio has generated £29.50 in revenue from rental and £45.86 in capital growth, for a total return of £75.36. I won’t bother publishing a statement on this occasion as it’s not massively different from last time. The bottom line is that I (still) have investments in 21 different projects with them and all are performing as expected, generating income and in most cases showing a profit on capital. So I am very happy with how this investment has been going.

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of AE as far as i am concerned. You can actually invest from as little as 80p per property if you really want to proceed cautiously.

Another property platform I have some investments with is Kuflink [referral link]. They appear to be doing well, with new projects launching almost every day. I currently have just over £2,000 invested with them, quite a large proportion of which comes from reinvested profits. To date I have never lost any money with Kuflink, though some loan terms have been extended once or twice. On the plus side, where this happens additional interest is paid for the period in question.

My loans with Kuflink pay annual interest rates of 6 to 7.5 percent. As mentioned above, these days I invest no more than around £100 per loan (and often less). That is not because of any issues with Kuflink but more to do with losses of larger amounts on other P2P property platforms (such as this one). My days of putting four-figure sums into any single property investment are behind me now!

Nowadays I mainly opt to reinvest the monthly repayments I receive from Kuflink, which has the effect of boosting the percentage rate of return on the projects in question

You can read my full Kuflink review here. They offer a variety of investment options, including a tax-free IFISA paying up to 7% interest per year with built-in automatic diversification. Alternatively you can now build your own IFISA, with most loans on the platform being IFISA-eligible.

I’d also particularly draw your attention to their revised and more generous cashback offer for new investors. They are now paying cashback on new investments from as little as £500 (it used to be £1,000). And if you are looking to invest larger amounts, you can earn up to a maximum of £4,000 in cashback. That is one of the best cashback offers I have seen anywhere (though admittedly you will need to invest £100,000 or more to receive that!).

Kuflink has some similarities with Assetz Exchange (see above). However, it’s important to note that with Kuflink you are investing in loans secured by property, whereas with Assetz Exchange your money is going into actual bricks and mortar. Kuflink loans typically pay around 7% annual interest. With Assetz Exchange projected yields from rental are generally a bit lower at around 5%, but you do of course have the potential for capital appreciation as well. There is also an argument that investments on AE are more secure as properties are typically rented out to organizations such as housing associations which are publicly funded. But I should emphasize that over the years I have been investing with Kuflink I have never lost any money with them and I understand nobody else has either. That is of course no guarantee it couldn’t happen in the future, but personally I find it quite reassuring.

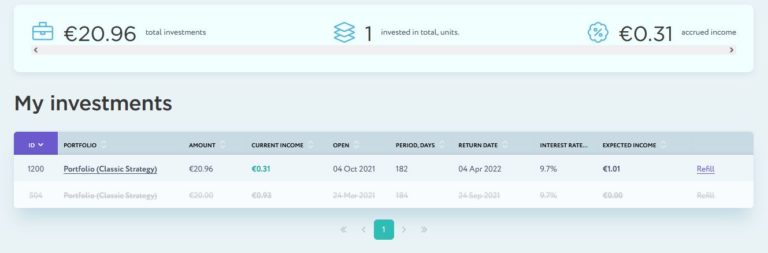

I haven’t mentioned my trial investment on European loan crowdfunding platform Nibble for a while, so thought I should remedy that this month. This has been proceeding without any issues. My initial test investment of 20 euros matured in September so I reinvested the entire sum at the same annual interest rate of 9.7 percent (see screen capture below).

I get weekly updates from Nibble confirming how much interest has been added to my account. Money has been a bit tight recently so I haven’t topped up my initial investment. Once I start getting my state pension (see below), however, I should have more available to invest, and Nibble is definitely on my list. My full review of Nibble can be found here.

Moving on, I have another article on the always-excellent Mouthy Money website. This is about how to save money on your motoring costs. I enjoyed researching this and learned some new and surprising things while doing so!

Finally, as I mentioned in this blog post, December 2021 marks a landmark for me, as I shall reach my 66th birthday and qualify for the new state pension. I am due to get my first payment on Christmas Eve. Tempting though it is, I probably won’t be blowing it all on a big party! 🎈🎈🎈

That’s all for now, so please stay safe (and warm) in these challenging times. And please don’t let scare stories in the mainstream media freak you out. At the time of writing hospitalizations and deaths from Covid in the UK have actually been falling steadily for weeks. So despite what the fear-mongers would have you believe, it really isn’t all bad news!

Have a lovely Christmas, enjoy socializing with friends and family, and I’ll be back again with another investments update at the start of 2022.

As always, if you have any comments or questions about this post, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

As regular readers will know, I recently started posting monthly updates about my investments. These (partly) replace the ‘Coronavirus Crisis Updates’ I was posting from March 2020. You can read my October 2021 Investments Update here if you like

I’ll begin as usual with my Nutmeg Stocks and Shares ISA, as I know many of you like to hear what is happening with this.

As the screenshot below shows, my main portfolio is currently valued at £21,940. Last month it stood at £21,046, so that is a rise of £894. That means it has recovered from the £675 drop last month and is now £250 higher in value than it was two months ago.

I know some PAS readers were worried about the falls in their Nutmeg portfolios (and equities generally) in September 2021, so I hope this will provide some reassurance. As I said last time, stock market investments in general should be regarded as medium- to long-term. In the short term some ups and downs are entirely to be expected.

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This pot also rose in value in October. It is now worth £2,756 compared with £2,633 last month. That’s a rise of £123, which again covers the fall last month with a bit to spare. Here is a six-month screen capture showing performance to the end of October 2021.

You can read my full Nutmeg review here (including a special offer at the end for PAS readers). If you are still looking for a home for your 2021/22 ISA allowance, based on my experience they are certainly worth considering. If you haven’t yet seen it, check out also my recent blog post in which I looked at the performance of Nutmeg fully managed portfolios at every risk level from 1 to 10 (my main port is level 9). I was actually pretty amazed by the difference the risk level you choose makes. If you are investing for the long term (and you almost certainly should be) opting for a hyper-cautious low-risk strategy may not be the smartest thing to do.

As regular readers will know, this year I am using Assetz Exchange for my IFISA. This is a P2P property investment platform that focuses on lower-risk properties (e.g. sheltered housing on long leases). I have invested a total of just under £1,000 in AE so far (I began with £100 in February 2021 and topped up twice).

Since I opened my account, my portfolio has generated £24.80 in revenue from rental and £59.97 in capital growth, for a total return of £84.77. I won’t bother publishing a statement on this occasion as it’s not massively different from last month. The bottom line is that I (still) have investments in 21 different projects with them and all are performing as expected, generating income and in most cases showing a profit on capital. So I am very happy with how this investment has been going.

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of AE as far as i am concerned. You can actually invest from as little as 80p per property if you really want to proceed cautiously.

Another property platform I have some investments with is Kuflink [referral link]. They appear to be doing well, with new projects launching almost every day. I currently have just over £2,000 invested with them, quite a large proportion of which comes from reinvested profits. To date I have never lost any money with Kuflink, though some loan terms have been extended once or twice. On the plus side, where this happens additional interest is paid for the period in question.

My loans with Kuflink pay annual interest rates of 6 to 7.5 percent. As mentioned above, these days I invest no more than around £100 per loan (and often less). That is not because of any issues with Kuflink but more to do with losses of larger amounts on other P2P property platforms (such as this one). My days of putting four-figure sums into any single property investment are behind me now!

Nowadays I mainly opt to reinvest the monthly repayments I receive from Kuflink, which has the effect of boosting the percentage rate of return on the projects in question

You can read my full Kuflink review here. They offer a variety of investment options, including a tax-free IFISA paying up to 7% interest per year with built-in automatic diversification. Alternatively you can now build your own IFISA, with most loans on the platform being IFISA-eligible.

I’d also particularly draw your attention to their revised and more generous cashback offer for new investors. They are now paying cashback on new investments from as little as £500 (it used to be £1,000). And if you are looking to invest larger amounts, you can earn up to a maximum of £4,000 in cashback. That is one of the best cashback offers I have seen anywhere (though admittedly you will need to invest £100,000 or more to receive that!).

Kuflink has some similarities with Assetz Exchange (see above). However, it’s important to note that with Kuflink you are investing in loans secured by property, whereas with Assetz Exchange your money is going into actual bricks and mortar. Kuflink loans typically pay around 7% annual interest. With Assetz Exchange projected yields from rental are generally a bit lower at around 5%, but you do of course have the potential for capital appreciation as well. There is also an argument that investments on AE are more secure as properties are typically rented out to organizations such as housing associations which are publicly funded. But I should emphasize that over the years I have been investing with Kuflink I have never lost any money with them and I understand nobody else has either. That is of course no guarantee it couldn’t happen in the future, but personally I find it quite reassuring.

On the subject of property investments, I also have a modest amount in the property crowdfunding platform Property Partner. At one time I was a big fan of this platform, but I lost a bit of enthusiasm when they introduced a raft of extra fees and charges.

Nonetheless, I do still have investments in around a dozen properties with PP, valued from about £30 to £2000 (in one case). The five-year-anniversary process restarted a while ago after being suspended due to Covid. For those who don’t know, after five years investors in a property are given the opportunity to exit at the current market value, as long as there are enough other investors on the platform willing to buy their shares at this price. If not, the property concerned is sold on the open market.

About half of ‘my’ properties have now gone through this process. I voted to sell on each occasion, as I am looking to reduce the total I have invested in property (as I feel too much of my portfolio is still in this form). In some cases all went to plan and I received payment for my shares, which I then withdrew. In other cases, however, not enough investors wanted to buy the shares that investors such as me wanted to sell. Consequently these properties are now being sold, which may of course take many months. Unfortunately the property in which I had £2,000 invested is one of those. To add to the joy, dividends are suspended on all properties that are being sold, so all I can do now is wait for the sales to go through.

On the plus side, Property Partner was taken over a while ago by the US digital home-ownership company Better. One of the first decisions taken by the new owners was to scrap the unpopular £1 monthly account fee and reduce the AUM (Assets Under Management) fee from 1.2% p.a. to 1.0% p.a. They are also offering fee rebates for their most active traders. All of this means that Property Partner may be worth another look now, especially as there’s a steady flow of opportunities to invest in properties going through the five-year process. That means you can buy shares in these properties at a fair market price without having to pay the usual fees associated with new listings.

Anyway, if you’d like to know more, here is a link to the Property Partner website [affiliate]. Note that if you sign up with Property Partner via my link and invest with them, I will split the commission I receive with you, meaning you could get up to £750 cash back.

In addition, last weekend the Express newspaper published an article about me and my blog, in which I shared some top tips for saving money on food shopping. Do check it out!

That’s all for now, so please stay safe and warm, and look out for your friends and neighbours as well as we head into the cold winter months. I’ll be back again with another investments update at the start of December.

As always, if you have any comments or questions about this post, please do leave them below.

Disclosure: I am not a qualified financial adviser and nothing in this post should be construed as personal financial advice. You should always do your own ‘due diligence’ before investing and take professional financial advice if in any doubt before proceeding. All investing carries a risk of loss.

If you enjoyed this post, please link to it on your own blog or social media:

If you’re reading this post you will almost certainly know what an ISA is.

The term stands for Individual Savings Account. ISAs effectively serve as tax-free wrappers for various types of savings account. The two best-known types are the Cash ISA and the Stocks and Shares ISA.

You get an annual allowance for your ISA investments which currently stands at a generous £20,000 a year. Money saved in an ISA is permanently exempt from taxes such as income tax, dividends tax, capital gains tax, and so on.

So What Is An IFISA?

IFISAs are a lesser-known type of ISA that can be used for peer-to-peer (P2P) lending. They were launched in April 2016. After a slow start, the range available has grown steadily.

You can put any amount into an IFISA up to your annual ISA allowance. In the current 2021/22 tax year, as mentioned, this is £20,000. This can be divided however you choose between a cash ISA, a stocks and shares ISA, a Lifetime ISA (if eligible – you have to be under 40) and an IFISA. So, for example, you could invest £6,000 in a cash ISA, £10,000 in a stocks and shares ISA and £4,000 in an IFISA.

Note that under current rules you are only allowed to invest new money in one of each type of ISA in a tax year. It is though generally possible to transfer money from one type of ISA to another without it affecting your annual entitlement (although there may be platform fees to pay).

IFISAs vary considerably in the returns they offer. Annual rates range from from around 4% to 15%. Obviously, the higher rates reflect the higher levels of risk involved.

Although all IFISAs involve P2P lending, a number of different types are available. They may include lending for all the following purposes:

property development

business loans

personal loans

green energy projects

bonds and debentures

entertainment industry loans

infrastructure projects

What Are The Risks?

All UK IFISA providers have to be authorized by the Financial Conduct Authority (FCA) and HMRC. This doesn’t in itself protect lenders (or investors if you prefer) against the failure of a platform, however. While savers with UK banks and building societies are covered by the government’s Financial Services Compensation Scheme (FSCS), which guarantees to reimburse up to £85,000 of losses, this does not generally apply to IFISA platforms.

All IFISA providers do offer various safeguards, though. These vary, but include provision funds to cover potential losses, insurance policies, and so forth. In many cases loans are made against the security of property or other assets, which in the worst case could be sold to pay off any debts.

Even so, IFISA investors don’t enjoy the same level of protection in the UK as bank savers. This is, of course, a major reason why the returns on offer are significantly higher. It’s therefore important to be aware of the risks and ensure you are comfortable with them before investing this way. It’s also important to lend across a range of platforms and loans, and not make the mistake of putting all your savings eggs into one P2P lending basket.

What Are The Attractions?

So why might you want an IFISA? There are several reasons.

One is that they offer the potential of much higher rates of return that ordinary (bank) savings accounts. Even the best of these are currently paying interest rates of under 1 percent. IFISAs typically pay several times more than that (though obviously at somewhat greater risk).

Another big attraction of an IFISA is that it provides a way of gaining extra diversification for your portfolio. As mentioned earlier, the law currently only allows you to invest in one type of stocks and shares ISA per year. This rather perverse rule actually makes it harder to diversify your investments. But you can have an IFISA as well as a stocks and shares ISA, so long as you don’t exceed your total £20,000 allowance. So having an IFISA gives you a way of diversifying your investments while keeping them all protected within a tax-free ISA wrapper.

And finally, IFISA investments are typically not tied to the performance of stock markets in the way a stocks and shares ISA would be. This is a different type of investment, with different risks and rewards. While an IFISA won’t provide a way of hedging your equity investments directly, it is likely to be less directly affected by short-term fluctuations in the markets.

Two IFISA Examples

Two IFISAs of which I have direct experience are offered by Kuflink and Assetz Exchange. Both of these platforms offer tax-free IFISA options. They are both based around property investing.

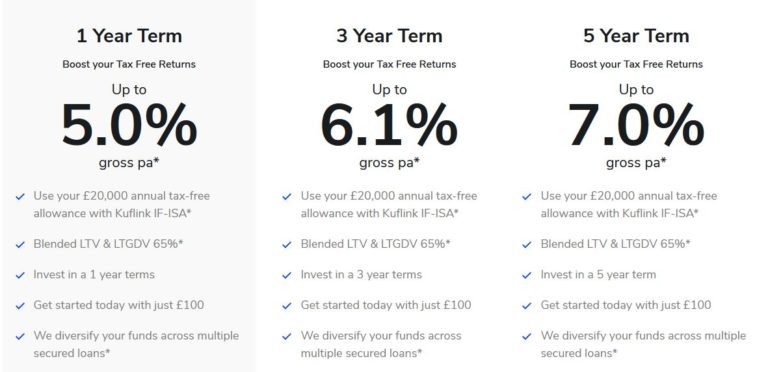

Kuflink – which I reviewed in this post – offers an automatically diversified IFISA comprising loans on property. They quote interest rates from 5% to 7%, depending how long you invest for. Your money is automatically diversified across a range of secured loans. The screen capture below from the Kuflink website sets out the main features of their IFISA.

One point to be aware of is that there is no ‘self-select’ option with the Kuflink IFISA. So you have no choice about which projects your money is invested in. But, of course, it does make investing in a Kuflink IFISA very quick and simple.

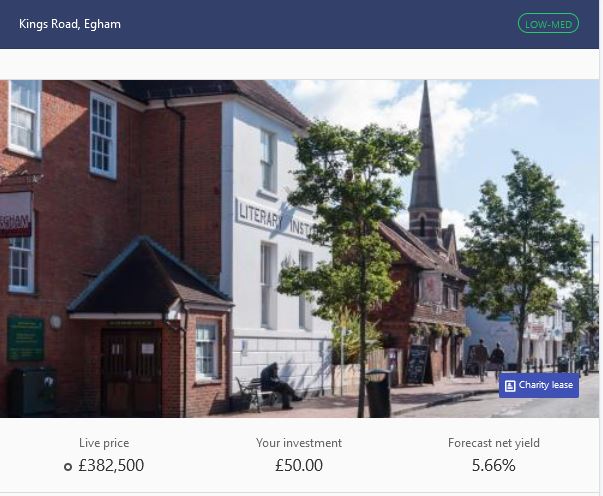

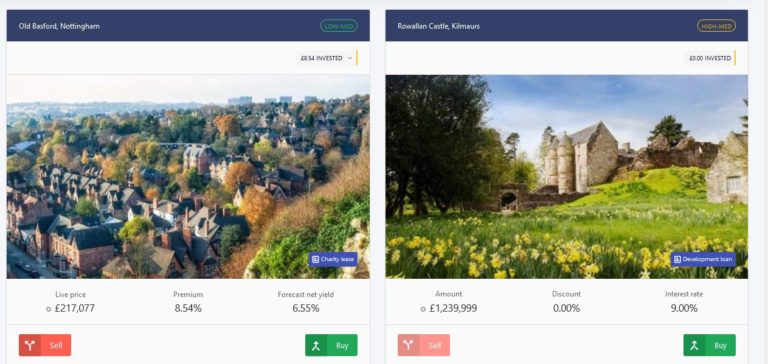

Assetz Exchange – which I reviewed in this post – has some similarities with Kuflink. But they concentrate on low-risk investments, typically with corporate clients (e.g. charities) on long leases. Here’s an example of the sort of investment I mean…

Assetz Exchange aims to offer net yields to investors of between 5.2 and 7.2% per year. One thing I especially like about them is that you can choose your own IFISA investments (indeed, they don’t currently offer an auto-select option). In addition, you can invest as little as 80 pence per project, making it easy to build a well-diversified portfolio even if you are only investing small amounts.

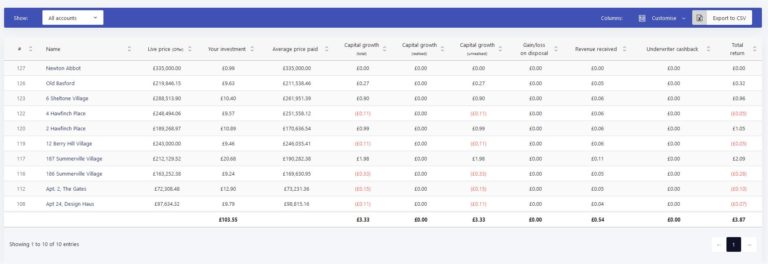

I am using Assetz Exchange for my 2021/22 IFISA, so here is a screen capture of my current portfolio for your interest. Note that while I have only invested £500 so far, I already have a well-diversified portfolio with 17 different investments!

Summing Up

If you are looking for a home for some of your savings that can offer better interest rates than banks and building societies and won’t incur any tax charges, an IFISA is certainly worth considering.

As well as the higher interest rates, they can add diversity to your investments, helping you ride out peaks and troughs in the financial markets.

Just be aware of the risks involved in P2P lending, diversify as widely as possible, and ensure you invest only as part of a well-balanced portfolio.

As always, if you have any comments or questions about this blog post, please do leave them below.

Disclaimer: I am not a registered financial adviser and nothing in this post should be construed as personal financial advice. You should always do your own ‘due diligence’ before investing, and speak to a professional financial adviser/planner if in any doubt before proceeding. All investments carry a risk of loss.

This post (and others on Pounds and Sense) includes my referral links. If you click through and make a qualifying transaction, I may receive a commission for introducing you. This will not affect the products or services you receive or any fees you may be charged.

If you enjoyed this post, please link to it on your own blog or social media:

Another month has passed, so it’s time for another of my Coronavirus Crisis Updates. Regular readers will know I’ve been posting these updates since the first lockdown started in March 2020 (you can read my April 2021 update here if you like).

As ever, I will begin by discussing financial matters and then life more generally over the last few weeks.

Financial

I’ll begin as usual with my Nutmeg stocks and shares ISA, as I know many of you like to hear what is happening with this.

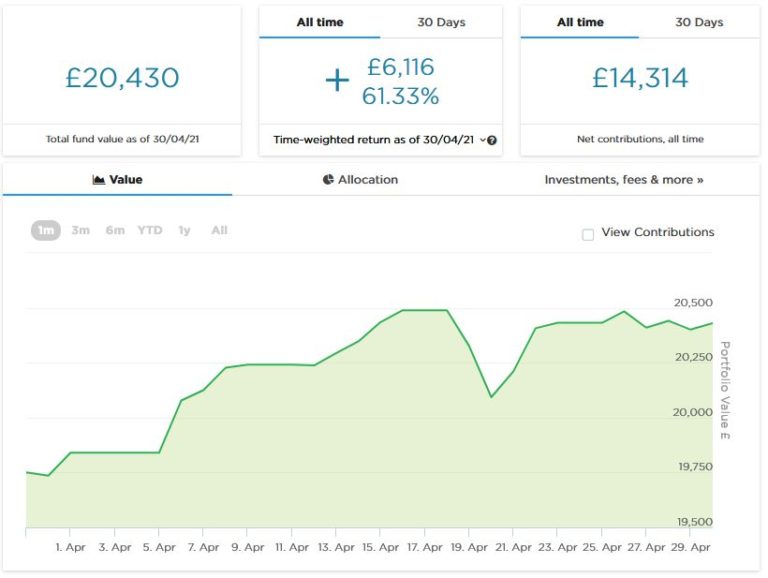

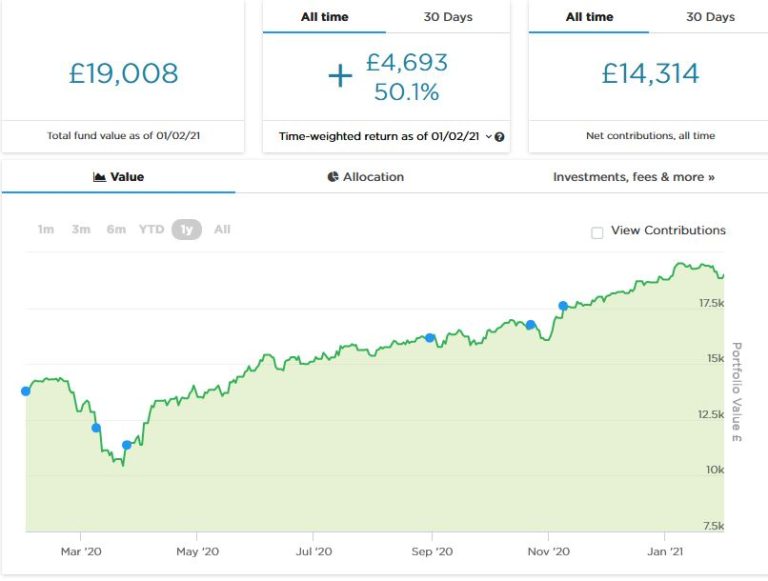

As the screenshot below shows, the value of my main portfolio rose fairly steadily in the first half of April, after which it remained around the same level (apart from a brief dip around the 20th). It is currently valued at £20,430. Last month it stood at £20,078, so overall it has gone up by £352. I am happy enough with that.

Apart from my main portfolio, five months ago I put £1,000 into a second pot to try out Nutmeg’s new Smart Alpha option. This has done pretty well, so in April I added another £1,000 from some money returned to me by RateSetter (as discussed in last month’s update). This pot is now worth £2,067. Here is a screen capture showing performance in April.

I updated my full Nutmeg review in April and you can read the new version here (including a special offer at the end for PAS readers). If you are looking for a home for your new 2021/22 ISA allowance, based on my experience they are certainly worth a look.

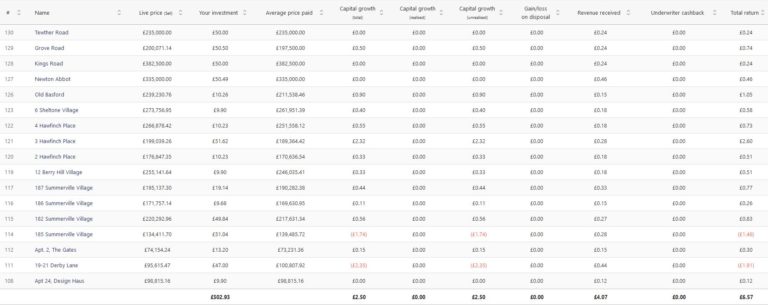

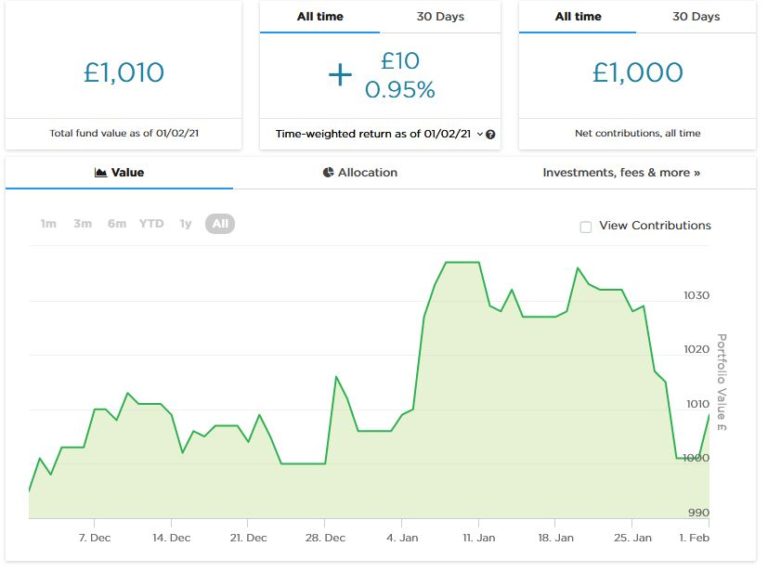

I also added £400 (from RateSetter again) to my initial test investment of £100 with Assetz Exchange. As you may recall, Assetz Exchange is a P2P property investment platform that focuses on lower-risk properties (e.g. sheltered housing on long leases). I put £100 into this in mid-February and (as mentioned) another £400 in April. Since then my portfolio has generated £3.05 in revenue received from rental (equivalent to an annual interest rate of about 10% on my original £100 investment). Here’s my current statement in case you’re interested:

As you can see, even though I have only invested £500, I already have a well-diversified portfolio. This is a particular attraction of Assetz Exchange in my view. You can actually invest from as little as 80p per property if you really want to proceed cautiously!

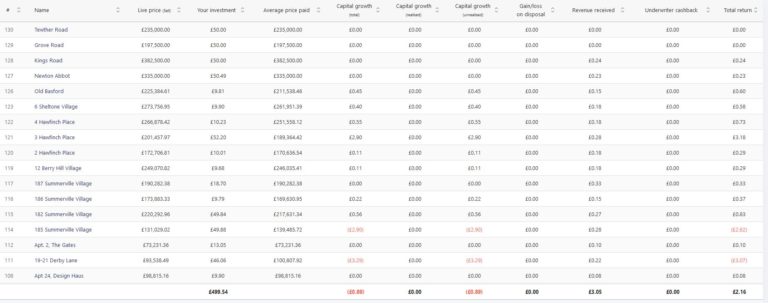

You may also notice that some of the properties in my portfolio have gone up in value and some have gone down. This makes it a bit harder to judge overall performance compared with an equity-based investment like Nutmeg. The property values quoted by Assetz Exchange represent the best price you can sell at currently on the exchange, which is where all investments on AE are bought and sold. But they are only really relevant if you want to buy or sell that day. By contrast, Property Partner (a somewhat similar P2P property investment platform) quote a value for each property based on an independent surveyor’s valuation every 6-12 months. That means the values displayed on Property Partner are more stable, but of course they are only theoretical as there is no guarantee that this valuation would be achieved if the property was put on the market.

In case you’re not aware, everyone has a generous £20,000 tax-free ISA allowance in the current tax year (2021/22). However, for some reason the government only allows you to invest in one of each type of ISA in any particular.tax year. So you can only put new money into one stocks and shares ISA per year, but you can invest in a cash ISA and/or IFISA as well if you wish – just as long as you don’t exceed the £20,000 total limit. In the 2021/22 tax year I am therefore investing in a Nutmeg stocks and shares ISA and an Assetz Exchange IFISA. This gives me additional diversification compared with investing in just one type of ISA.

Moving on, I heard last month that I will not be eligible for any more SEISS income support payments for the self-employed. Along with many other self-employed people, my income took a hit when the pandemic struck and this money from the government came in very useful (though I do thankfully have a personal pension and other investments as well). However, I have become a victim of the rule that says to receive SEISS your average self-employed income must represent at least half of your total income.

For the first three rounds of SEISS that was indeed the case. However, the latest round of payments incorporates another set of tax returns (2019/20) when calculating average income. Because my income was lower in these accounts (partly due to the pandemic) my four-year average is now less than what I draw from my personal pension. So at a stroke I am no longer eligible for any more support. It’s not the end of the world, but I do find it bizarre that a scheme intended to support self-employed people whose livelihoods have been affected by the pandemic can cut off completely when your average income drops. Commiserations to any PAS readers who may have found themselves in a similar situation 🙁

Personal

In April, as I’m sure you know, some of the government’s lockdown restrictions finally began to be lifted.

I was glad to be able to go for a swim for the first time since Christmas, and have been doing so twice a week since it became possible again. I am a member of the David Lloyd Club in Lichfield which has two pools, one inside and one out. Although I’ve heard that you have to book slots at some swimming pools, that has never been the case at DL Lichfield, and in fact in many ways it feels reassuringly normal. Of course, you have to wear a mask as you enter the building, but thankfully not in the changing rooms or the pool 😀

I have just been told that if the pools get very busy, DL staff ask people to wait in the changing rooms until others have left. I haven’t witnessed this myself and don’t think it happens very often, but am happy to place this info on record.

What I do find bizarre is the rules about buying and consuming refreshments. The club room (aka coffee shop) at DL Lichfield is open for the purchase of drinks and light meals, but you can’t consume them within the building. You are, however, allowed to sit at a table in the club room (no need for a mask) to read and relax or just stare at the four walls. But heaven help you if you try to eat or drink anything.

I was told by a staff member that it was okay to take a drink to the outdoor pool as long as I was going for a swim, but not if I simply wanted to lie on a sunbed. Even though I am fast becoming a connoisseur of strange lockdown rules, this one seems barmy to me and I’d love to know how DL Lichfield plan to enforce it (“Unless you get in that pool in the next five minutes, I’m taking your coffee away.”). I’d like to support the DL club room/coffee shop, but the incomprehensible rules have defeated me. So I’m now taking a flask of tea and a biscuit with me and having that on the poolside or in the changing room after my swim. So far no Covid police have come for me.

I have also been pleased (and relieved) to have my hair cut again, six months after this was last done. Thankfully I didn’t have to queue up, as my hairdresser comes to me and cuts my hair in my conservatory. We have both had Covid jabs and agreed to dispense with masks and just kept the door and window open (thankfully it was quite a warm day). Again, it all felt reassuringly normal.

I haven’t so far taken advantage of the reopening of pub gardens, largely because it has been so cold (and wet) most days. It’s good to see at least some of my local pubs open again, but a shame they still aren’t allowed to open inside as well as out. Last year we had Eat Out to Help Out at a time when there were more Covid cases and deaths then there are now (just one death yesterday, I read). I am looking forward to May 17th when pubs and restaurants can reopen inside as well, but believe this has been delayed too long personally.

I am probably one of the few people who didn’t watch the Line of Duty finale. Indeed, I haven’t watched any of the series, as it didn’t really appeal to me. For one thing it sounded downbeat and depressing, and life has been grim enough recently. But also, it appeared a bit too complicated for my liking. Especially as i grow older, I find following series with large casts and labyrinthine plots increasingly challenging. I can remember laughing (affectionately) at my dad when he expressed confusion at the plot of some TV detective show, but I am obviously going down the same route myself now 😮

I have watched a couple of shows I enjoyed this month, though, so thought I’d share details in case anyone fancies giving them a try.

The first is an Amazon Prime Video series called Upload. This is a dystopian science fiction tale, set in a not-too-distant future when a method has been found for transferring people’s minds at the point of death (or before) to a virtual afterlife. This service is provided by a number of large corporations. They employ minimum-wage ‘angels’ in large warehouse-like offices to monitor these worlds and support the clients who live in them (at least, until their money runs out). It is quite a dark concept, but full of laugh-out-loud moments and some great characters. There is also a mystery in it, and a romance between a female ‘angel’ and one of her (deceased) male clients. It’s well worth a watch if you like something a bit different (and have Amazon Prime Video, of course).

I am also enjoying a US fantasy series called The Librarians (see below). I originally caught a couple of episodes on an obscure Freeview channel and decided I’d like to watch the whole (four) series from the beginning. Doing that proved a bit more challenging than I anticipated, but eventually I managed to track down a DVD box set on eBay.

The Librarians is a tongue-in-cheek fantasy series with a certain retro feel to it. It reminds me a bit of the old Avengers TV show in its heyday (with Diana Rigg as Emma Peel).

The Librarians are a group of misfits who are recruited to work at the mysterious Library, a place where magical artefacts of all kinds are stored. Early in the first series magic is released into the world again, having been suppressed for many centuries. In each episode the Librarians investigate some mysterious incident and try to stop evil individuals deploying magic for nefarious ends, generally using their intelligence rather than violence.

Again, it’s hard to explain in a few words, but you soon get the hang of things. And the characters, while perhaps excessively goofy at times, are all endearing in different ways. The Librarians is really old-fashioned family entertainment (with little if any swearing) and none the worse for that. If you can get hold of it – I’m not sure whether it’s on any streaming services – it offers an enjoyable (and at times hilarious) drop of escapism, something I guess many of us need at the moment.

As always, I hope you are staying safe and sane during these challenging times. If you have any comments or questions, please do post them below.

If you enjoyed this post, please link to it on your own blog or social media:

I have written about property crowdfunding on various occasions on Pounds and Sense. It’s a way for ordinary individuals to invest in bricks and mortar without requiring huge amounts of capital.

Why Property Crowdfunding?

Property investors get a double benefit – rent from tenants for as long as they own the property, and – in most cases – a profit if and when they sell.

Of course, property doesn’t come cheap. And even if you can stretch to buying a modest house or flat for investment purposes, you are taking the risk of putting all your eggs in one basket. As a result, many people of more modest means have concluded that property investment is not for them.

Property crowdfunding has changed all that, however. A number of platforms now exist that allow ordinary individuals the chance to buy a share (or fraction) in an investment property. Investors then receive a proportion of the rental income generated and also get a share of any profit when the property is sold (or refinanced).

A further attraction of property crowdfunding is that the platform (and its agents) take care of managing the property and tenants on your behalf. Unlike direct property ownership, property crowdfunding (or crowdlending if you prefer) is a genuine hands-free investment.

Brickowner Review

Brickowner is one of a number of property crowdfunding platforms that also includes Property Partner, Assetz Exchange and CrowdProperty. They allow investors to buy a share of individual property investments.

Brickowner focuses on institutional investments. They buy shares in large, high-return property investment deals that were traditionally only offered to institutions or high-net-worth individuals. They then offer smaller shares in these (a minimum of £500) to members wanting to invest in them.

How It Works

Before you can access the Brickowner platform, you will need to register on the site and confirm that you are allowed by law to invest in this type of product. This is a requirement imposed by the Financial Conduct Authority (FCA), which regulates this type of investment. In practical terms it means you will have to confirm that you meet one of the following descriptions:

High Net Worth Individual – This includes individuals who have an annual income of £100,000 or more or net assets of £250,000 or more and have made a declaration acknowledging the consequences of making investments based on financial promotions that have not been approved by an FCA-authorised firm.

Self-certified Sophisticated Investor – This includes individuals who have prior relevant investment experience and have made a declaration acknowledging the consequences of making investments based on financial promotions that have not been approved by an FCA-authorised firm.

Representative of a High Net Worth Body – This includes companies and partnerships with at least £5 million net assets and trusts with assets of £10 million.

Investment Professional – Including corporate investors and SIPP or SSAS professional service providers.

You will also be required to answer some questions to confirm that you understand the nature of the investments that can be made on the platform.

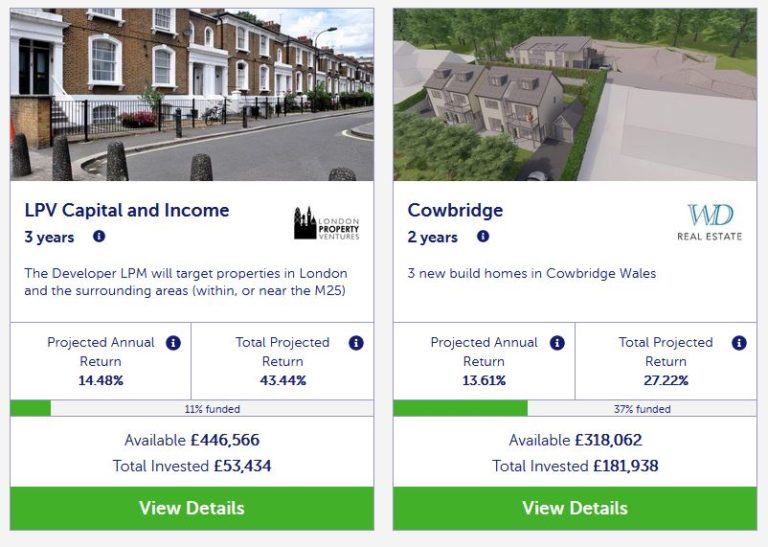

Once you are registered (and not before) you will be able to browse from the range of currently available property investments, such as the example below:

If you see a current project you like, you can invest in it, from £500 up to the maximum available. You can (and probably should) build a diversified portfolio by investing in a number of different properties. You can add funds and increase the size of your portfolio any time you want.

Investments have a fixed term: anything from one to five years. During that time you may receive dividends from any rental income received. These are added to your account and available to withdraw or reinvest. You also receive a share of any profits along with return of your capital at the end of the investment period.

In common with other property crowdfunding platforms, the pandemic has caused delays – in some cases a year or longer – to some projects on Brickowner, As far as I am aware no projects have failed completely, though.

Secondary Market

Brickowner recently introduced a secondary market where investors who need to release funds before the end of an investment term can put their share up for sale to other members. Here is a screen capture showing part of the secondary market currently.

As you may notice, some of the projects on the secondary market have less than £500 available. I asked if this meant you could therefore invest less than £500 in these cases, but was told no. Here is the exact reply I received:

£500 is the minimum investment in both the primary and secondary market. The reason there are smaller amounts on the secondary market is that there is a taxi-rank system, whereby available shares are listed and allocated in order of listing to a queue of buyers. So if I wanted to invest, say, £520 in Tamlaght, and there were no other prospective Tamlaght share buyers ahead of me BUT there were only £120 worth of shares available, I would have to wait until £520 worth of shares were available before my transaction went through. Prospective Tamlaght buyers in the queue would have to wait until my order had been filled before they moved forward in the queue.

In effect, then, you would have to place a bid for at least £500 of the project in question, and would have to wait till additional sellers materialized before getting anything. That is probably not ideal, but I can understand that Brickowner want to avoid the situation where some investors end up with tiny holdings in certain projects.

Charges

Brickowner fees are outlined within the property term sheet for each specific investment. There is no charge for depositing money with Brickowner, and no charge at the end of the investment period when your money and (hopefully) profits are returned to you.

My Thoughts

Brickowner offers an interesting option for people who want to add property to their investment portfolio. As mentioned above, there is a good case for doing this both in terms of dividends and capital growth, and to diversify your overall portfolio.

The Brickowner website is attractive and professional looking. One thing I have noticed is that most of their investment opportunities fill up very quickly. That is good insofar as it indicates that Brickowner is succeeding in attracting investors who believe in the proposition being offered. On the other hand, it does mean that at any particular time there may not be many (or any) projects to invest in. You will therefore need to build your portfolio gradually.

As mentioned above, Brickowner has a minimum investment of £500. This is not as low as some platforms (e.g. Assetz Exchange will let you invest as little as 80p) so it may be less suited to investors on a limited budget. But on the positive side, they are transparent about the fees they charge, and it is good that no fees are imposed for depositing or withdrawing money. It’s also good that a secondary market now exists for investors who wish (or need) to exit early.

As you can see from the screen capture above, the projected returns on investments with Brickowner are at the higher end for property crowdfunding platforms. Of course, this generally means the risks are higher as well. In any event it is important to read the financial information on each project carefully, to ensure that the investment aligns with your own needs and goals. Bear in mind also that some projects offer income as well as the potential for capital appreciation, while others aim for capital growth only.

During the coronavirus pandemic and lockdown, property transactions slowed considerably and many commercial property values in particular fell. However, there is clear evidence that a recovery is now under way. My own view is that there are good opportunities at present for property investors, but obviously in this uncertain time there are never any guarantees. Every investor needs to assess the situation carefully in light of their personal circumstances and tolerance for risk and proceed accordingly.

Investor Protection

The returns on offer from Brickowner are significantly better than you would get from a bank savings account at present, but clearly they don’t carry the same level of protection. For example, you are not protected by the Financial Services Compensation Scheme, which will refund up to £85,000 if a bank with which you have an account goes bust.

On the other hand, your money is invested in bricks and mortar, so it’s unlikely you would lose it all. A further level of protection is that – in common with other property crowdfunding platforms – your money is invested via an SPV (Special Purposes Vehicle). This is effectively an independent company with responsibility for the project in question. If Brickowner were to go bust, funds in the SPV would be protected and returned to investors once the property was sold.

Even if Brickowner were to go under before your money was invested, your funds are paid into a separate, ring-fenced client account. If the platform went belly-up the day after you sent the money, your funds would simply be returned to you.

Overall, then, whilst investing in Brickowner is clearly not as safe as leaving your money in the bank, the measures set out above do provide a reasonable level of protection (and reassurance). As with any investment, however, the higher potential returns on offer come with a greater risk of loss. In my view (and I’m not a qualified financial adviser, just an individual who has put thousands of pounds of his own money into property crowdfunding) Brickowner offers a reasonable balance between risk and reward. But clearly, you should invest only as part of a balanced portfolio combined with other, more liquid types of investment. .

If you would like more information about Brickowner and to set up an account, just click through any of the links in this post.

Disclosure: The links in this post are affiliate links. If you click through and set up an account at Brickowner and make an investment with them, I may receive a fee for introducing you. This will not affect the terms or returns you are offered. Please note also that I am not a registered financial adviser and nothing in this post should be construed as personal financial advice. Before making any investment it is important to do your own due diligence, and seek advice from a qualified financial adviser if you are in any doubt how best to proceed. All investment carries a risk of loss.

If you have any comments or questions about Brickowner or property crowdfunding in general, as always, please do post them below.

Note: This is a fully revised and updated repost of my original article about Brickowner.

If you enjoyed this post, please link to it on your own blog or social media:

Today I’m looking at P2P property investment platform Assetz Exchange (launched in January 2019)..

As I have noted before on Pounds and Sense, I am something of an enthusiast for property investment (and specifically property crowdfunding). Among other things, I like the fact that you can make money from both rental income and capital growth. And investing in property can be a good way of spreading the risk when you have equity-based investments.

Of course, investing in property directly is costly and carries all the risk inherent in putting all your eggs in one basket. A major attraction of P2P property crowdfunding investment is that you can get started with much less money and build a diversified portfolio to help mitigate the risks.

In addition, if you invest this way you don’t have to deal with the day-to-day hassles of being a landlord, from finding tenants to repairing broken boilers. This is taken care of by the platform itself and/or their management company. You just have to sit back and – all being well – wait for the rental income and (hopefully) capital gains to materialize.

That said, there have been a few reversals in the P2P property sector over the last few months (see this recent post, for example). So I am now more concerned than ever to ensure that any investments I make in this category control risk as effectively as possible.

What Is Assetz Exchange?

As mentioned above, Assetz Exchange is a licensed P2P property investment platform. It is owned by well-known P2P lending platform Assetz Capital, but run quite separately from them. If you already have an account with Assetz Capital, you will have to register separately with Assetz Exchange.

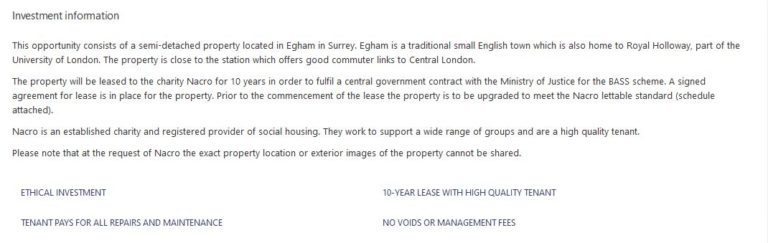

Assetz Exchange aims to offer net yields to investors of between 5.2 and 7.2% per year. These are generally paid by institutional tenants through multi-year leases. All properties are unleveraged, providing additional security (and stability) for investors.

Assetz Exchange has some similarities with Property Partner, but they differ in some important ways. For one thing, many of the properties are rented out to charities (e.g. NACRO) or housing associations. These organizations generally sign longer contracts than private individuals. They don’t have voids (periods when the property is untenanted and producing no income). Neither are there any maintenance costs, as the organizations take responsibility for this themselves. And finally, these organizations are directly funded by the government, giving them a secure income stream.

Another area of specialism is show homes. Working with a national housebuilder, Avant Homes, Assetz Exchange purchases fully furnished show homes from multiple sites around the country. These are then leased back to the developer for fixed periods of up to five years to be used to help sell other plots. This eliminates potential void periods and avoids any maintenance costs. At the end of the leases, investors will be able to vote on whether to lease the houses to tenants or sell them to home-buyers on the open market.

Assetz Exchange also offers investors the chance to get involved with a new generation of modular eco-homes. This is already a popular approach to house-building in Europe and the United States. Assetz Exchange fund the acquisition and conversion of land into serviced plots, allowing buyers to then order a house to be built on that plot to their own specification. These modular-built eco-homes are sustainable and low energy. They are also typically quick to complete and have a lower impact on the environment.

Assetz Exchange do also buy and let some standard properties as well, offering investors the chance to further diversify their portfolios.

Signing Up

Before you can invest through Assetz Exchange, you will of course have to sign up on the platform. This is pretty straightforward. You just visit the Assetz Exchange website, read the information there, and click on Register in the top-right-hand corner.

You will then be required to enter your contact details and confirm which of four categories of investor you fall into. The options are as follows:

High Net Worth Investor – This includes individuals who have an annual income of £100,000 or more or net assets of £250,000 or more.

Self-certified Sophisticated Investor – This includes individuals who have made more than one peer-to-peer investment in the last two years or who meet certain other criteria relating to investment experience. This is the category I selected myself.

Investment Professional – Including corporate investors and SIPP or SSAS professional service providers.

Everyday Investor – This category is for investors who don’t fit into any of the categories above. They can still invest via Assetz Exchange but must pledge not to invest more than 10 per cent of their portfolio in P2P loans.

You will also be required to answer some multiple-choice questions to confirm that you understand the nature of investments that can be made on the platform. I found some of these questions quite challenging, and was pleased to get them all right first time. I would therefore recommend reading the information on the Assetz Exchange website (including the Help pages) carefully before proceeding to register. If you do make any mistakes, however, feedback is provided, and you can take the test again until you achieve a 100% correct score.

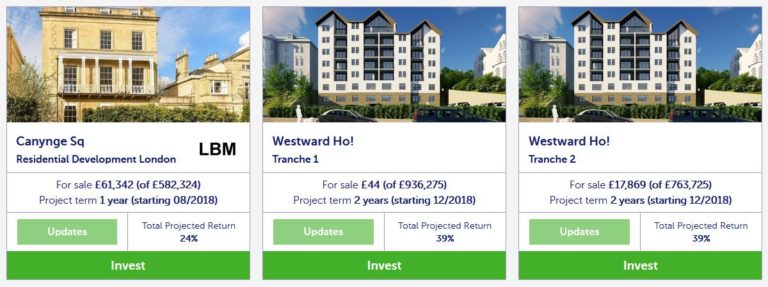

Once you have done all this, you will be able to fund your account. This must be done by bank transfer, as Assetz Exchange do not allow debit card payments. You will then be able to browse the range of currently available property investments:

Investing

Once you are registered on the platform and signed in, click on Exchange in the menu at the top of the screen and all current projects will be displayed. Here are a couple that are showing at the time of writing…

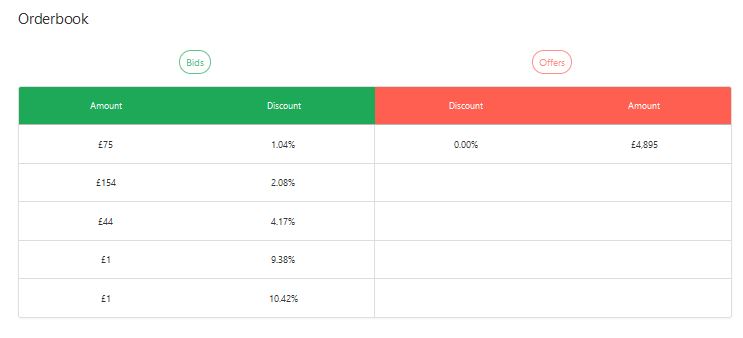

Clicking on any of these will open a page devoted to the investment concerned. Here you can read all about it, view reports and site plans, and so on. One very important area is the Order Book (see example below).

All buying and selling on the platform is conducted via an exchange (otherwise known as the Order Book) which works similarly to the secondary market on Property Partner.

So if you want to buy shares in a particular project, you can do so by accepting the best price currently available on the exchange. In the example above, there are £4,895 of shares available at zero discount (i.e. the original offer price).

If you want to get your shares at a lower price than this, you can make a bid. In the example, an investor has put in a bid for £75 at a 1.04% discount and another investor (or maybe the same one) has put in a bid for £154 at a 2.08% discount.

Conversely, if you wish to sell some or all of your shares at any time, you can accept the best bid (or bids) on the Order Book currently, or place an offer and wait to see if this is matched.

It does take a little bit of getting your head around at first, but it’s actually a simple and straightforward process. One thing to note is that if there is nothing showing on the right-hand-side of the Order Book (under Offers) you won’t be able to buy shares in that project there and then – though you can of course place a bid if you wish and see if a seller wants to match it.

In any event, if you want to buy, just click on the green Buy button (either on the Exchange page or the details page) and complete the short online form. You will need to indicate how much you want to invest, whether this should be from your General or IFISA account (see below), and whether the amount should include the FCC or not (see What Are The Charges? below).

You will also need to indicate whether you want to buy at the current best price (selected by default) or you want to try for a better price (in which case your bid will be added to the left-hand column in the Order Book).

The IFISA Option

As mentioned above, if you wish you can invest with Assetz Exchange via an IFISA (Innovative Finance ISA). As discussed in this recent post, this type of ISA for P2P investing gives you the same tax advantages as a cash or stocks and shares ISA. You don’t have to pay any tax on the money you make, whether this takes the form of dividends, income or capital gains.

Everyone has a generous annual ISA allowance of £20,000 in the current 2020/21 tax year (and next year as well). This can be divided any way you like among the three types of ISA. So if you open an Assetz Exchange IFISA, you can still have cash and stocks and shares ISAs with other providers as well, so long as you don’t invest more than £20,000 in total. You can also only invest money in one of each type of ISA in any one financial year.

Choosing the IFISA option on Assetz Exchange is very easy. You can do it when first registering on the site or later. The only extra thing you have to do is enter your National Insurance number.

If you have maxed out your ISA allowance – or have already invested in another IFISA in the current tax year – you can still invest via your default ‘Regular’ account. You can invest any amount this way, but of course any profits you make will potentially be taxable.

What Are The Fees?

Assetz Exchange do not charge any monthly fees to investors (this is in contrast to Property Partner, who made the unpopular decision to impose an Assets Under Management charge and monthly fee, greatly impacting small investors on the platform especially). The company does have to make money somehow, of course, and they do this from three sources:

Arrangement fee

When a property is first purchased, Assetz Exchange charge an arrangement fee which is included in the Fixed Costs & Contingency (FCC). When parts of the property are sold on the Exchange, this fee is added to the purchase price of the buyer (see above) and so is recovered by the seller. The size of this fee is included in the loan conditions.

Monitoring fee

Assetz Exchange charge a percentage of the gross rent received for the property. The percentage is stated in the loan conditions of the property.

Property disposal fee

A fee of 2% of the gross sales proceeds is charged if investors vote to sell and the property is physically sold.

What Are The Safeguards?

Like most other property crowdfunding platforms, all investments in any project on Assetz Exchange are held in a Special Purpose Vehicle (SPV) for the project concerned. This gives investors in the project some protection if the main company were to go into administration.

A contingency balance is held within each SPV which acts in a similar manner to a provision fund, covering unexpected short-term cash-flow disruptions. It is topped up from receipts and no distributions are made to investors if it falls below a certain level.

SPVs also benefit from indemnity insurance which covers non-payments from tenants. This in theory also covers disruption to cash-flow, but it does not cover voids (periods where the property does not have a paying tenant). For reasons mentioned above, voids should not be an issue with most of the properties listed on the platform.

In common with most other P2P investment platforms, Assetz Exchange does not fall within the remit of the Financial Services Compensation Scheme (FSCS), which covers customers with UK financial services firms up to £85,000 if the institution in question were to go bust.

3. Low minimum investment (as little as £1 per project!) – this makes building a diversified portfolio straightforward.

4. Assetz Exchange take care of all the work involved in buying and managing properties. You just choose which ones to invest in.

5. Option to access money any time by selling on the secondary market (though this does depend on another investor being willing to buy your shares at a price you find acceptable).

6. Relatively low-risk investment options (though of course there are no guarantees)

7. Customer support (in my experience anyway) is fast, friendly and helpful.

8. Charges are reasonable. There is no charge for selling investments.

9. Potential to make money through both capital appreciation and rental income.

10. Rental income is paid into your account every month. You can either withdraw or reinvest it.

11. No monthly fees and only transaction-based charges to pay.

12. Opportunity to invest in socially beneficial developments such as sheltered housing

13. Tax-free IFISA option to which any investment on the platform can be added

14. Investors can vote for their favoured exit option (e.g. selling up) when the time comes

Cons

1. Can’t invest using a debit card

2. No auto-invest option currently available

3. Not as many opportunities as some P2P platforms (although the number is increasing steadily)

Closing Thoughts

I was impressed enough with Assetz Exchange to invest a small amount (£100) of my own money initially and will report back on PAS about how my portfolio fares. Here is how it’s looking at the time of writing, roughly a month after I opened my account. As you can see, my initial investment has grown by £3.87 from a combination of income received and capital growth. For a month that’s not bad at all – if it carries on growing at that rate I’ll be delighted! – but of course it is much too soon to draw any firm conclusions from this.

I particularly like the fact that with the low minimum investment on Assetz Exchange, even if you’re starting very cautiously (as I am) it’s easy to build a diversified portfolio. I like the relative simplicity of investing on the website and the fact that you can exit an investment any time via the exchange (though that does depend on willing buyers being available at a price that is acceptable to you). It is also good that there are no charges associated with selling on the exchange.

You can, of course, withdraw uninvested funds from your Assetz Exchange account at any time.

Obviously there are risks in any form of investing and it is important to do your own ‘due diligence’ before proceeding. You should also bear in mind that this type of investment is not covered by the Financial Services Compensation Scheme, which covers savers with UK banks and other financial institutions up to £85,000. On the other hand, the potential returns are significantly better than the fractions of a percent typically on offer from savings institutions right now, while the risks appear to be at the lower end of the spectrum, with many of the properties on long-term leases with corporate/institutional tenants.

To be very clear, nobody should put all their spare cash into Assetz Exchange (or any other investment platform for that matter) but in my opinion there is definitely a case for including AE within a diversified portfolio.

As mentioned above, I shall be reporting back on how my Assetz Exchange investments perform on PAS in future. In the mean time, if you have any comments or questions about this post, or Assetz Exchange more generally, please do leave them below as usual.

UPDATE JANUARY 2025 – Assetz Exchange have now rebranded as Housemartin. They continue to operate as described above, but going forward will focus entirely on supported housing projects, as these have proven the most reliable and hassle-free (not to mention the social/community benefits). For more info, see my new blog post P2P Property Investment Platform Assetz Exchange Rebrands as Housemartin.

Disclaimer: I am not a registered financial adviser and nothing in this post should be construed as personal financial advice. You should always perform your own ‘due diligence’ before making any investment and speak to a qualified professional adviser if in any doubt how best to proceed. All investments carry a risk of loss.

Please note also that this review uses my affiliate links. If you click through and make an investment or perform some other qualifying transaction, I may receive a commission for introducing you. This will not affect any charges you pay or the product/service you receive.

If you enjoyed this post, please link to it on your own blog or social media:

FI Money (as I’ll call it for short from now on) is a self-published paperback of 222 pages (it’s also available as a Kindle ebook). It is organized into 28 main chapters plus additional material. I won’t list all the chapters here, but here are the first ten to give you a flavour of the content (and style).

Force yourself to smile

YouTube obsession

Your relationship with money

Overthinker

Understanding our ‘Chimp’ emotions

Goals written down

Crystal clear goals

Stress less

Mental training

How NOT to invest

FI Money is a personal account of one man’s journey towards financial independence (the FI referred to in the title). It is a self-development book, but as Peter says in the Introduction it isn’t the usual success story typically associated with such books. He says, ‘I am a work in progress, similar to a building under construction.’

The chapters are generally quite short. They are well written and broken up with bullet-points, headings, To Do lists, and so on. Peter focuses on different aspects of his quest for financial independence, with a particular emphasis on buy-to-let. As this is not something I have ever got into myself (apart from some investments on property crowdfunding platforms) I was particularly intrigued by this. Peter talks about his experiences with refreshing honesty and is not afraid to disclose some of the mistakes he has made along the way. If you’re thinking of investing in buy-to-let yourself, there are some valuable lessons to be learned here.

The book covers many other subjects as well, including property renovation, tax, investing, keeping records, and more. I particularly enjoyed Chapter 10 ‘How NOT to Invest’ which focuses on some of Peter’s less successful investments. These include Premium Bonds (like me he’s not a fan), Bitcoin and other cryptocurrencies, and a particularly ill-advised buy-to-let project early in his career. There are some salutary lessons to be learned from all this (and a few laughs to be had as well!).

In addition to the practical advice, FI Money has a particular emphasis on the psychological aspects of achieving financial independence – the money mindset, as Peter calls it. He is a firm believer in building your financial knowledge, but also adopting the right emotional and practical disciplines and carefully planning and managing your journey towards FI. There is a lot of food for thought in the book from someone who really has been on this particular journey himself (or at least is well on the way there).

As mentioned earlier, Peter also runs a personal finance blog called Duffmoney. This is well worth a read as well, and will give you a flavour of Peter’s style and his attitude towards investing and money matters generally.

As always, if you have any comments or questions about this review, please do post them below.

Disclosure: In common with many posts on Pounds and Sense, this review includes affiliate links. If you click through and make a purchase, I may receive a fee for introducing you. This will not affect in any way the price you pay or the product or service you receive.

If you enjoyed this post, please link to it on your own blog or social media:

In brief, Property Partner is a property crowdfunding platform. For the most part they specialize in ‘traditional’ property crowdfunding rather than loan or development finance.

Properties are bought and managed by Property Partner on investors’ behalf. Investors then receive a share of the rental income as dividends, and a share of any profits (plus return of their capital) when the property is sold.

Property Partner launched in January 2015. That date is significant, because after a property has been on the platform for five years, all investors get the chance to exit at a fair market price (determined by an independent surveyor). Due to the pandemic the five-year anniversary process was temporarily put on hold, but it is now proceeding again, albeit with delays as they work through the backlog.

How it operates is that in the run-up to the fifth anniversary of a property, all investors have the opportunity to say if they want to exit their investment at the valuation price or stay on for another five-year term (less than this if they subsequently exit via the resale market, of course).

All investors who have opted to leave will then have their shares pooled and put up for sale on Property Partner at the price stated. New investors are then able to buy these shares.

So long as all shares are sold, the original investors get their money (including any net profits) and the property continues under Property Partner’s management. If all shares don’t sell, however, Property Partner offer the property for sale on the open market. Investors then have to wait until the property is sold before getting their money back. As anyone who has been involved with buying or selling property will know, this is likely to take several months (quite possibly longer in the current circumstances).

The Opportunity

As Property Partner themselves have been pointing out, a number of properties that are coming up to their fifth anniversary are currently trading on the resale market at well below their latest valuation. Here is just one example:

This property in Tower Hill, London (not one I own shares in myself) is due to go through the fifth-anniversary process in April 2021 (or possibly a bit later due to the backlog). At the time of writing shares are available on the secondary market at a price of 91p, which is 28.28% below the latest valuation of £126.88. In theory, then, you could buy shares now and in the next few months sell up for a substantial short-term gain.

Of course, in practice it’s not as simple as that. Here are some reasons:

Nobody knows yet what the final five-year valuation will be. If it is lower than the current valuation (which is perfectly possible in the current economic climate) the net profit will be reduced, perhaps substantially.

There is no guarantee that the shares of all investors who wish to exit will actually sell on the platform. If they don’t, as mentioned, you could have a long wait before the property is sold on the open market. In addition, if this happens there is no guarantee that the property will sell at the valuation price. If it goes for less than this, your returns will be reduced accordingly.

There are platform fees to take into account. In particular, there is a 1% fee for buying on the secondary market and a further 0.5% stamp duty reserve tax charge. Thankfully there are no exit fees, though.

And finally, the number of shares available for any property on the secondary market is limited. Obviously the number you can buy depends on how many shares other investors want to sell at the price in question.

On the plus side, for the length of time you hold the shares you may receive monthly dividends at a rate between 1.5% and 6% per year (though dividend payments on some properties are currently suspended due to Covid). This will offset the fees mentioned above; but if you only intend to hold the shares for a few months it probably won’t cover them completely. Bear in mind that an Assets Under Management (AUM) fee is now deducted from dividends as well.

As an investor with Property Partner since almost the beginning (the cover image shows a property in Torquay I own shares in – I plan to retire there one day 😀 ), I am awaiting the five-year exit for my investments with considerable interest.

My personal circumstances have changed since I started investing with the platform, so I intend to take the opportunity to offload at least some of ‘my’ properties. Indeed, I have already voted to sell my shares in the first property I ever invested in with Property Partner (20 Phillimore Close) and am waiting to see how this pans out. I will update this post in due course once I know.

Nonetheless, I am still considering investing short term on the resale market to take advantage of the opportunity the five-year anniversary presents. In particular, I have already topped up my investments in some of the properties I already hold but am planning to dispose of.

I will, though, be cautious until I have a better idea how the first few five-year anniversaries have passed, so I can see if all shares put up by investors sell on Property Partner, or if they have to sell the properties concerned on the open market. As mentioned earlier, the latter route will clearly take longer and there is no guarantee what price would be achieved.

Would I recommend someone who is currently an investor in Property Partner to look into this? Yes, certainly. Whatever your current circumstances, you need to be aware of what is going on with any properties you hold with Property Partner. And if you wish to sell, you should definitely consider taking advantage of the five-year exit mechanic. Equally, if you have money available to invest, you could check out the opportunities buying now on the resale market – though do bear in my mind my cautionary comments above.

If you haven’t joined Property Partner, and you like the idea of investing some of your portfolio in property, the platform is certainly worth a look. As older properties come back on the market for new investors, there will be no shortage of opportunities in the months ahead. And my understanding is that, as the original costs of acquisition have been amortised, there will be less costs to cover from investors, thus boosting the potential returns from the properties in question.

In addition, as these properties have a five-year history already, you will be able to check how they have been performing in terms of dividends generated and capital appreciation. This is no guarantee of how well or badly they will do in the future, of course.

Take a look at my Property Partner review for much more information about the platform and how it works. Also, if you do decide to invest in Property Partner, there is a welcome bonus offer. For convenience I have copied details below from my review.