Why I Am (Still) Not a Fan of Premium Bonds

In February 2017 I wrote this post about premium bonds explaining why I was withdrawing a large amount of the money I had invested in them.

To recap, at that time the interest rate paid on premium bonds (from which the monthly prize fund is calculated) had been cut eight months earlier in June 2016. This led me to sell the majority of my holding, as the amount I was earning in prizes had fallen considerably. The rate was cut again a few months later in May 2017, which led me to sell nearly all my remaining bonds. I now have just £5 left, to avoid closing my account completely.

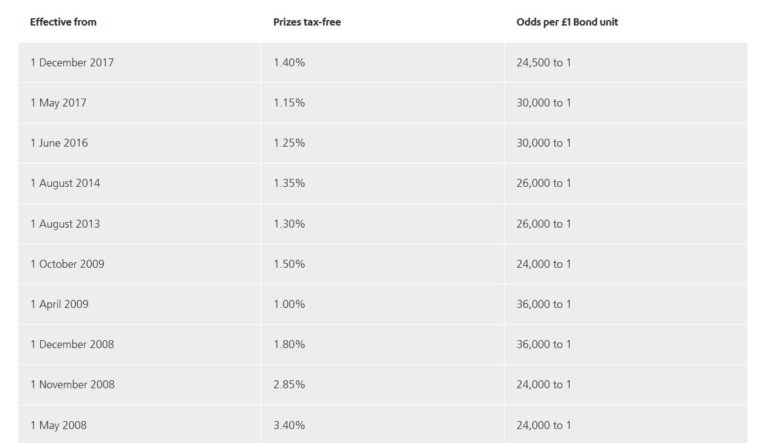

So what has happened since then? The good news for bond owners was that from December 2017 the prize fund was raised by 0.25% to 1.40%. This improved the odds of an individual bond winning a prize in any monthly draw from 30,000 to 1 to 24,500 to 1 (although it still didn’t tempt me to reinvest).

The not-so-good news is that from May 2020 the rate is being cut by 0.1% to 1.3%. As a matter of interest, here is a table copied from the NS&I website showing the changes in prize rates and the odds of winning a prize over the last twelve years. The new rate from May 2020 isn’t shown on the table.

From May 2020 the chances of winning a prize with a single bond will be reduced to 26,000 to 1. Over 170,000 fewer prizes are set to be given out in May 2020 than in February as a result of this change, with less than half the number of £100 and £50 prizes expected to be awarded (source: MoneySavingExpert).

My Thoughts

A first glance you might think that an interest rate of 1.30% percent still isn’t so bad in these days of (very) low interest savings accounts. It’s much the same as the current top paying easy-access savings accounts. Premium bond prizes are tax-free and you can withdraw your capital any time if you need it within a few days. Your money is protected by the UK government and you have an outside chance of winning a life-changing sum. So what’s not to like?

Well, quite a lot in my opinion. Most importantly, although the interest rate is currently 1.40% (reducing to 1.30% in May) in practice most people won’t make this amount. The interest rate is a mean (average) figure and this is skewed by the two one-million pound prizes (which statistically you are highly unlikely to win – see below) and the small number of other other high-value prizes. For these big prizes to be paid out, a lot of people have to win nothing. The more bonds you have, the closer to the average your prize earnings are likely to be. But the reality is that most premium bond owners won’t earn the interest rate quoted (and they may make nothing at all).

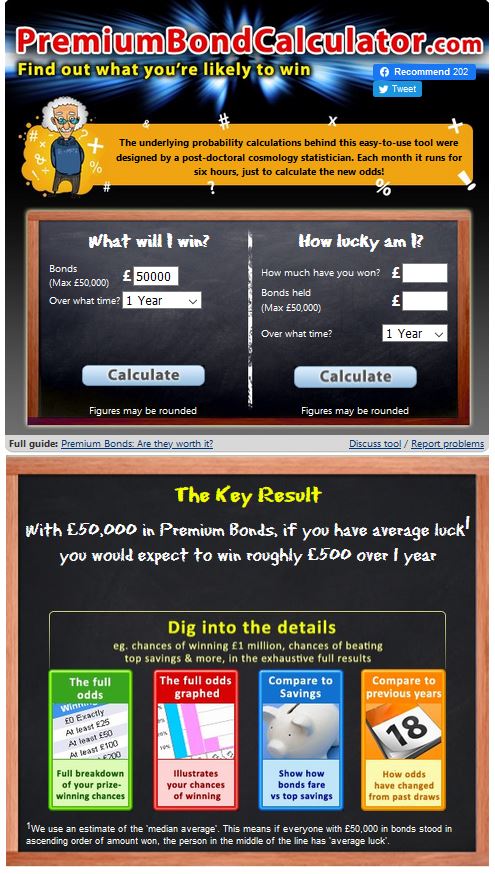

A better measure of what you are likely to make over a year is the median average. The way to think about this is that if you lined up all premium bond-holders with a certain number of bonds (e.g. £50,000) in order from those earning the least in a year (probably nothing) to the most (a million pounds plus), the median is the person right in the middle of the line. Half of all holders will earn more than this person (or the same) and an equal number will earn less. The median in this context is therefore a measure of what you can expect to earn from your premium bonds in a year with ‘average luck’. The clever folks at MoneySavingExpert have built a Premium Bond probability calculator which uses this metric to indicate how much you are likely to win per year, with average luck, with any given holding.

With the £50,000 maximum, the calculator reveals that with average luck you will win just £500 of prizes a year, equivalent to an interest rate of just 1.0 percent (see screen capture below). And that is at the current (February 2020) interest rate. From May 2020 that figure will inevitably go down. Obviously you might have better than average luck, but (as stated above) around half of all bond-holders will have worse. You can read a much more detailed explanation about this on this page of the MSE website.

The calculator also reveals that with £5,000 in premium bonds you could expect to win £50 a year with average luck, and with £1,000 nothing at all. Only about one in three people with £1,000 worth of bonds will win a prize in any one year, so the median (‘average luck’) winnings are zero. Over a two-year period, however, about five out of nine holders of £1,000 will win at least one prize, so the median earnings over two years with £1,000 in bonds are £25 (the lowest and by far the most common prize). This does I guess demonstrate that the ‘average luck’ method used in the MSE calculator has its limitations as a way of estimating likely earnings (although it is still likely to be more accurate than applying the headline interest rate to your investment).

Clearly the longer you hold your bonds, the better are your chances of winning a larger prize, so over a period of years average annual earnings may edge up slightly. Even so, the large majority of bond-holders won’t ever earn the headline rate.

At one time the tax-free status of premium bond prizes would have been a significant attraction, but nowadays that doesn’t apply to nearly the same extent. All basic rate taxpayers now benefit from a Personal Savings Allowance of £1,000 worth of tax-free savings interest every year (higher rate taxpayers get £500 and top rate taxpayers nothing at all). In practice 95% of people now pay no tax on their savings interest. If you are in the 5% who do, premium bonds become a more attractive option. Even so, a typical return of 1% or less, even if it is tax free, isn’t going to set many pulses racing.

Finally, you do of course have a chance of winning a big prize, but it’s important to be realistic about what that chance is. Even with the maximum £50,000 holding, MoneySavingExpert calculate that your chances of winning the million pound top prize in any one year are 1 in 69,876. To put this into perspective, if you had held £50,000 in premium bonds since the year 68000 BC (assuming of course they existed then) with average luck at the current interest rate you could have expected to win the jackpot just once. I looked this up, and 68000 BC is the middle of the Stone Age!

- I also highly recommend this premium bonds prize calculator from MoneyMarvel which works a bit differently from the MSE tool and some may find easier to use 🙂

My Recommendations

Overall, then, I cannot recommend premium bonds as a home for your savings, especially with the coming rate cut in May 2020.

I can understand why premium bonds are a popular investment, as they offer a bit of excitement every month checking whether you have won and how much. But the fact remains that overall, for most people, the total prize money received is likely to average little more than 1 percent a year at current rates. It may very well be less than this, especially after May 2020 when – as already mentioned – the number of lower value prizes (£25 to £100) will be cut substantially. I look forward to checking on the MSE calculator then to see how much a person with average luck might expect to make in a year.

If you are lucky enough to have £50,000 burning a hole in your pocket, my first advice would be to put enough into an easy-access savings account such as the Post Office Online Saver (currently paying 1.30% including a fixed 0.8% bonus for the first 12 months) to cover your outgoings for up to three months in the event of emergencies. After that, you could invest the balance in a low-cost tracker fund, or a portfolio of investment funds, or a robo-advisory platform like Nutmeg. You could perhaps put a proportion of the money into P2P lending or property crowdfunding as well. Over several years, for the great majority of people, this will outperform an equivalent premium bond portfolio many times over.

As always, if you have any comments or questions about this post, please do leave them below.

February 23, 2020 @ 2:31 pm

The table comparison is really good to get a snapshot of the changes over the years. Sadly I’d agree with how little value Premium Bonds really are any more, not just with prizes reduces in size but with how chances of actually winning something have been slashed. The April changes feel more like a death knell for Premium Bonds. I’ve only ever one 1x £25 in probably 12 years of having them. However, that’s probably more than I’ve accrued from a Barclays ISA (absolutely awful!) Fantastic write-up, Nick.

Caz x

February 23, 2020 @ 3:16 pm

Thanks, Caz. It was certainly an interesting post to research and write. I guess a proportion of people will always invest in premium bonds in the hope of winning a big prize but that chance really is depressingly small. I’d say a far better strategy is to invest your spare money along the lines mentioned in my post, and then have a couple of quid a week on the National Lottery if you want the excitement of a potentially life-changing win.