As from 6 April 2024, UK investors have a fresh chance to supercharge their savings and investments with a new £20,000 Individual Savings Account (ISA) allowance.

To maximize the benefits of the new 2024/25 allowance, there’s a strong case for acting swiftly and using at least part of your £20,000 ISA allowance sooner rather than later. This is due to the power of compounding. By investing early, you give your money more time to grow, benefiting from the potential snowball effect of returns generating further returns. So the sooner you invest that £20,000 (assuming you are fortunate enough to have it) the more opportunity it has to multiply over time.

But the good news doesn’t end there. In addition to the ISA allowance remaining at a relatively generous £20,000, the rules surrounding ISAs have undergone a welcome relaxation from this tax year onward. One of the most significant changes is the ability to open more than one ISA of the same type (e.g. a stocks and shares ISA) with different providers in the same tax year. This means investors are no longer limited to a single provider for each type of ISA, giving them greater flexibility and choice in managing their investments.

Previously, investors were restricted to opening one cash ISA, one stocks and shares ISA and one innovative finance ISA (IFISA) per tax year. This restriction could prove frustrating for those seeking to diversify their investments or take advantage of new opportunities as the tax year progressed. Now, with the freedom to open multiple ISAs of the same type, investors can shop around for the best rates, terms, and investment options without being limited to a single provider for each ISA type. They can also move some or all of their money from one provider to another without jeopardising its tax-free status.

It’s important to note, however, that while the rules have been relaxed, the overall annual ISA allowance remains fixed at £20,000. This means that any contributions made across multiple ISAs of any type will count towards your total allowance for the tax year. You should still therefore take care not to exceed the annual limit to avoid any potential tax charges.

Cash ISAs offer a secure and accessible way to save, providing a tax-free environment for your savings with the added benefit of easy access to your funds when needed. Meanwhile, stocks and shares ISAs open the door to potential higher returns by investing in a wide range of assets such as equities, bonds, and funds, albeit with a higher level of risk. With a stocks and shares ISA you will never incur any liability for dividend tax, capital gains tax or income tax, even if your investments perform exceptionally well. Of course, there is no guarantee this will happen, but over a longer period stock market investments have typically outperformed cash savings, often by a substantial margin. IFISAs (e.g. from Assetz Exchange) allow you to invest is property crowdfunding and other forms of peer-to-peer finance. They are more specialized, but may appeal to some investors looking to further diversify their portfolios.

In recent years I have invested much of my own annual ISA allowance in a stocks and shares ISA with Nutmeg, a robo-manager platform that has produced good returns for me. You can read my in-depth review of Nutmeg here if you wish.

Closing Thoughts

In light of the new 2024/25 ISA allowance and relaxation of the rules surrounding them, now is the perfect time for UK investors to review their savings and investment strategies. Whether you’re looking to kickstart a new ISA or maximize your contributions to existing accounts, taking action early can set you on the path to optimizing your returns from this important tax-saving opportunity. By investing sooner rather than later and taking advantage of the increased flexibility in ISA provider options, savers can make the most of their money while minimizing their tax liabilities. So seize this opportunity to build your wealth and protect it from the taxman today!

As always, if you have any comments or questions about this post, please do leave them below.

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Cartoon image by courtesy of Bing AI.

If you enjoyed this post, please link to it on your own blog or social media:

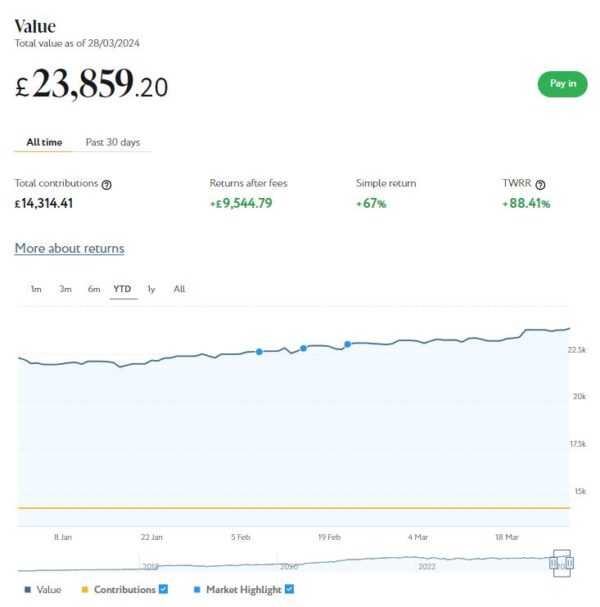

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

As the screenshot below for the year to date shows, my main Nutmeg portfolio is currently valued at £23,859. Last month it stood at £22,994 so that is a welcome increase of £865.

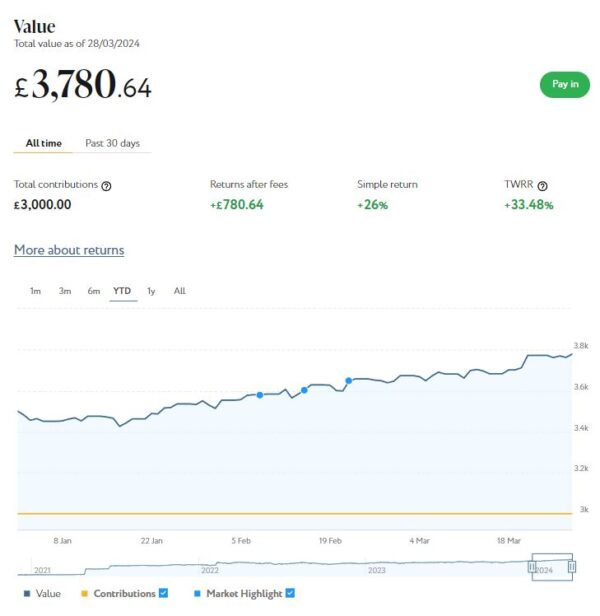

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £3,781 compared with £3,640 a month ago, a rise of £141. Here is a screen capture showing performance over the year to date.

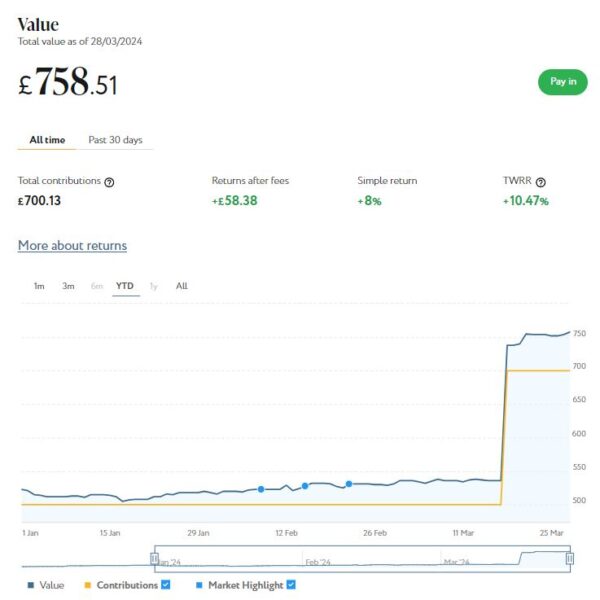

Finally, at the start of December 2023 I invested £500 in one of Nutmeg’s new thematic portfolios (Resource Transformation). As you can see from the screen capture below, this is now worth £759 compared with £530 last month, an increase of £229 since last month.

I should though say that £200 of this is ‘new money’. This came from a ‘Refer a Friend’ bonus, which I decided to pay into this pot rather than withdrawing. So if you disregard that, this portfolio has actually risen in value by £29 since last month.

March was obviously another good month for my Nutmeg investments. Overall – and disregarding the £200 RAF bonus – I was up £1,035 or 3.55%. And since the start of the year (again disregarding the £200 RAF bonus in March) I am up by £1,882 or 7.15%. In these turbulent times I am more than happy with that.

You can read my full Nutmeg review here (including a special offer at the end for PAS readers). If you are looking for a home for your annual ISA allowance, based on my overall experience over the last eight years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs), Lifetime ISAs and Junior ISAs as well.

Don’t forget, the current tax year ends on 5 April 2024 and after that the 2023/24 tax-free ISA allowance of £20,000 will be gone forever. But the good news is that you will then have a whole new £20,000 ISA allowance for 2024/25!

I also have investments with the property crowdlending platform Kuflink. They continue to do well, with new projects launching every week. I currently have around £1,570 invested with them in 10 different projects paying interest rates averaging around 7%. I also have £14 in my Kuflink cash account.

To date I have never lost any money with Kuflink, though some loan terms have been extended once or twice. On the plus side, when this happens additional interest is paid for the period in question.

There is now an initial minimum investment of £1,000 and a minimum investment per project of £500. Kuflink say they are doing this to streamline their operation and minimize costs. I can understand that, though it does mean that the option to test the water with a small first investment has been removed. It also makes it harder for small investors (like myself) to build a well-diversified portfolio on a limited budget.

One possible way around this is to invest using Kuflink’s Auto/IFISA facility. Your money here is automatically invested across a basket of loans over a period from one to five years. Interest rates range from 7% to around 10%, depending on the length of term you choose. Full up-to-date details can be found on the Kuflink website.

You can invest tax-free in a Kuflink Auto IFISA. Or if you have already used your annual iFISA allowance elsewhere, you can invest via a taxable Auto account. You can read my full Kuflink review here if you wish.

Moving on, my Assetz Exchange investments continue to generate steady returns. Regular readers will know that this is a P2P property investment platform focusing on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my AE portfolio has generated a respectable £173.90 in revenue from rental income. As I said in last month’s update, capital growth has slowed, though, in line with UK property values generally.

At the time of writing, 8 of ‘my’ properties are showing gains, 7 are breaking even, and the remaining 14 are showing losses. My portfolio is currently showing a net decrease in value of £35.05, meaning that overall (rental income minus capital value decrease) I am up by £138.85. That’s still a decent return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Assetz Exchange most projects are socially beneficial as well.

The overall fall in capital value of my AE investments is obviously a little disappointing. But it’s important to remember that until/unless I choose to sell the investments in question, it is largely theoretical, based on the most recent price at which shares in the property concerned have changed hands. The rental income, on the other hand, is real money (which in my case I’ve reinvested in other AE projects to further diversify my portfolio).

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of AE as far as i am concerned (especially now that Kuflink have raised their minimum investment per project to £500). You can actually invest from as little as 80p per property if you really want to proceed cautiously.

As I noted in this recent post, Assetz Exchange is particularly good if you want to compound your returns by reinvesting rental income. This effectively boosts the interest rate you are receiving. Personally, once I have accrued a minimum of £10 in rental payments, I reinvest this money in either a new AE project or one I have already invested in (thus increasing my holding). Over time, even if I don’t invest any more capital, this will ensure my investment with AE grows at an accelerating rate and becomes more diversified as well.

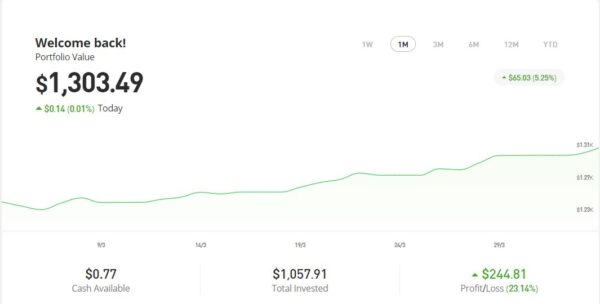

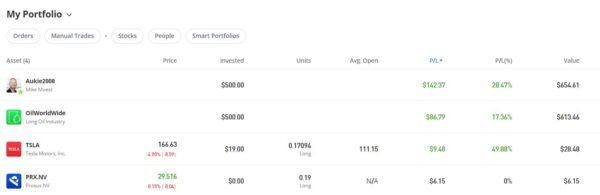

In 2022 I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios, Oil Worldwide. I also invested a small amount I had left over in Tesla shares.

As you can see from the screen captures below, my original investment totalling $1,022.26 is today worth $1,303.49, an overall increase of $281.23 or 27.51%.

eToro also offer the free eToro Money app. This allows you to deposit money to your eToro account without paying any currency conversion fees, saving you up to £5 for every £1,000 you deposit. You can also use the app to withdraw funds from your eToro account instantly to your bank account. I tried this myself and was impressed with how quickly and seamlessly it worked. You can read my blog post about eToro Money here. Note that it can also serve as a cryptocurrency wallet, allowing you to send and receive crypto from any other wallet address in the world.

I had two more articles published in March on the excellent Mouthy Money website. The first is Saving versus Investing – What’s the Difference and Why You Should Do Both. People often get confused between saving and investing, and it doesn’t help that the words are sometimes used loosely and interchangeably. In reality, though, there is a clear difference between them. In this article I explain why saving should always be your first priority, but ideally you should do both.

Also in March Mouthy Money published my article Are Solar Panels Still Worthwhile? As you probably know, solar PV panels generate electricity from sunlight. Growing numbers of homeowners (me included) have them on their roofs. At one time solar panels came with generous payment tariffs known as FiTs (feed-in tariffs), but those days are long gone. So in this article I examine what incentives exist today for installing panels and whether the sums still add up. I also look at the other pros and cons of solar panels.

As I’ve said before, Mouthy Money is a great resource for anyone interested in money-making and money-saving. I am a particular fan of my fellow MM contributor and money blogger Shoestring Jane. She writes mainly about money saving and frugal living. Her latest article Save Money on Gifts Throughout the Year sets out some top tips for saving money on gifts without (of course!) being a skinflint. You can see all of Jane’s articles for Mouthy Money via this web page.

I also published several posts on Pounds and Sense in March. I won’t bother mentioning those that are no longer relevant now, but the others are listed below.

One was a reminder that the Trading 212 welcome offer has reopened. If you haven’t done this before, you can get a free share worth up to £100. As I said in the article, my free share in AMD is now worth £151.88! This offer closes on 16 April 2024.

Also in March I published Don’t Miss Out! Use Your £20,000 ISA Allowance Before It’s Too Late. This was a reminder to use your 2023/24 allowance before it vanishes on 6th April 2024. Obviously you will need to move very smartly if you are going to do this now. But (as I said earlier) the good news is that everyone will have a fresh £20,000 allowance from that date.

One other bit of news this month is that I finally got around to buying a home storage battery to connect to my solar panels (see my recent MM article about panels). I used a local (Staffordshire) company called The Energy Box for this, and am very happy to recommend them.

I’ve had my battery for just over a fortnight now and it’s been quite eye-opening. Using the battery app I can see how much electricity my solar panels are generating at any time and how much I am using in my home. I can also check the battery charge level and whether it’s charging or discharging. Even at this time of year, if there’s a bit of sunshine I am generating enough electricity in the day to cover my needs and charge the battery to a level where I’m running the house from it till well into the evening.

In the summer I’d expect to be generating enough to live off solar-generated power entirely, meaning there will only be the dreaded standing charge to pay. So I will actually be saving more money than I originally anticipated, though admittedly it will still be a number of years before the cost is covered.

It wasn’t just a financial decision, though. My other aim was to be able to continue as normal in the event of power cuts (which I expect to become more frequent in coming years as the UK transitions away from fossil fuels), and that should be the case too. The only issue might be a power cut in the depths of winter when the battery hasn’t charged up from the panels. Even so, if I know (or suspect) a cut is coming I can charge the battery in advance from the mains.

I’ve written an article going into more detail about home storage batteries (including my own) for my regular clients at Mouthy Money. This will be published in April, so keep an eye out for it!

Finally, a quick reminder that you can also follow Pounds and Sense on Facebook or Twitter/X. Twitter/X is my number one social media platform these days and I post regularly there. I share the latest news and information on financial (and other) matters, and other things that interest, amuse or concern me. So if you aren’t following my PAS account, you are definitely missing out!

That’s all for today. As always, if you have any comments or queries, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media:

As the end of the tax year on 5 April 2024 approaches, so too does the deadline to utilize the annual tax-free Individual Savings Account (ISA) allowance.

The clock is ticking, and unless you take action in the next couple of weeks, this opportunity to maximize your tax-free savings for the 2023/24 financial year will be gone forever.

ISAs are a popular choice for savers and investors alike, offering a tax-efficient way to grow your wealth. With a diverse range of options available, from cash ISAs to stocks and shares ISAs and innovative finance ISAs, individuals have the flexibility to tailor their savings strategy to suit their financial goals and risk appetite.

The current ISA allowance stands at £20,000, providing a significant opportunity to shield your savings and investments from tax. This allowance represents a generous sum that, if left unused, cannot be carried forward to future years. In essence, any portion of the £20,000 allowance that remains untapped by the upcoming deadline will be lost, representing a missed opportunity for tax-free growth.

For those who have yet to fully utilize their annual ISA allowance, now is the time to take action. Whether you’re looking to bolster your rainy-day fund with a cash ISA or seeking to invest in the stock market through a stocks and shares ISA, there’s no shortage of options available. But bear in mind that under current rules you can only invest in one of each type of ISA in any one tax year (though this rule is changing from 2024/25). So if you already invested in, say, a stocks and shares ISA this year, you are not allowed to invest in a S&S ISA with a different provider in the current tax year. You will only be able to top up your current S&S ISA to whatever remains of your total £20,000 allowance.

Cash ISAs offer a secure and accessible way to save, providing a tax-free environment for your savings with the added benefit of easy access to your funds when needed. Meanwhile, stocks and shares ISAs open the door to potential higher returns by investing in a wide range of assets such as equities, bonds, and funds, albeit with a higher level of risk. With a stocks and shares ISA you will never incur any liability for dividend tax, capital gains tax or income tax, even if your investments perform exceptionally well. Of course, there is no guarantee this will happen, but over a longer period stock market investments have typically outperformed cash savings, often by a substantial margin.

In recent years I have invested much of my own annual ISA allowance in a stocks and shares ISA with Nutmeg, a robo-manager platform that has produced good returns for me. You can read my in-depth review of Nutmeg here if you wish.

With just a few weeks left to take advantage of this valuable tax benefit, procrastination could prove costly. By acting now, you can ensure that your savings and investments are positioned to grow tax-free, setting yourself up for a better financial future.

In summary, the £20,000 annual ISA allowance for the 2023/24 tax year presents a golden opportunity for UK residents to maximize tax-free savings and investments. Time is of the essence, though, and unless you act before the impending deadline on 5th April 2024, this valuable allowance will be lost forever. If you have the money available, therefore, seize the opportunity now to help secure your financial future.

As always, if you have any comments or questions about this article, please feel free to leave them below.

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

If you enjoyed this post, please link to it on your own blog or social media:

A quickie today to let you know that the price of stamps is rising (again!) on Tuesday 2nd April 2024.

Standard second-class stamps will be going up by 10p to 85p, while first-class stamps will also rise by 10p to £1.35.

A first-class stamp for a large letter will rise by 15p from £1.95 to £2.10. The price of a second-class stamp for a large letter will remain at £1.55.

Standard letters can weigh up to 100g and measure a maximum of 24cm x 16.5cm x 5mm. Large letters can measure 35.3cm x 25cm x 2.5cm but still have to weigh under 100g. If they weight over 100g, higher rates apply, and if they weigh over 750g they have to go at parcel rates.

Saving Money on Stamps

So is there anything you can do to mitigate the impact of the latest price rises?

Well, my number one recommendation is to stock up now while stamps are still at the old price. Standard and large-letter stamps don’t have values printed on them and will still be valid after the April price rise comes in.

If you can afford to buy (say) 100 standard first-class stamps and 100 second-class, that will save you an impressive £20 in total. If you’re anything like me, that will keep you going till Christmas 2024 and beyond!

The best bet for buying stamps is – of course – your local post office. If you don’t have one near at hand, however, you can also buy in bulk from various suppliers, including Viking Direct. They sell books of first and second class stamps at the current price, with postage free for orders of over £59. You can also buy stamps online from The Royal Mail Shop.

Amazon also sell postage stamps, though costs vary and when I checked some prices were significantly higher than at post offices. But they may be worth a look, especially if you are an Amazon Prime member.

Another option to consider is the online auction site eBay (search for “new UK stamps”). There can be good savings to be made here, but check reviews and ratings carefully and be wary of offers that are clearly too good to be true.

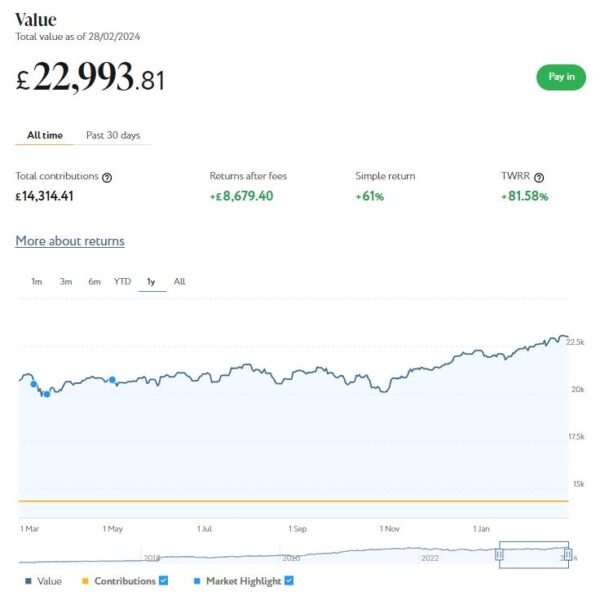

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

As the screenshot below for the last 12 months shows, my main Nutmeg portfolio is currently valued at £ £22,994. Last month it stood at £22,386 so that is a welcome increase of £608.

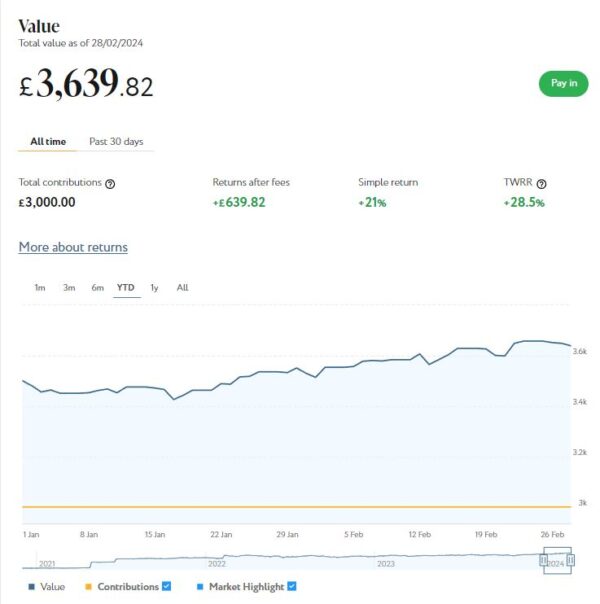

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £3,640 compared with £3,530 a month ago, a rise of £110. Here is a screen capture showing performance over the last 12 months.

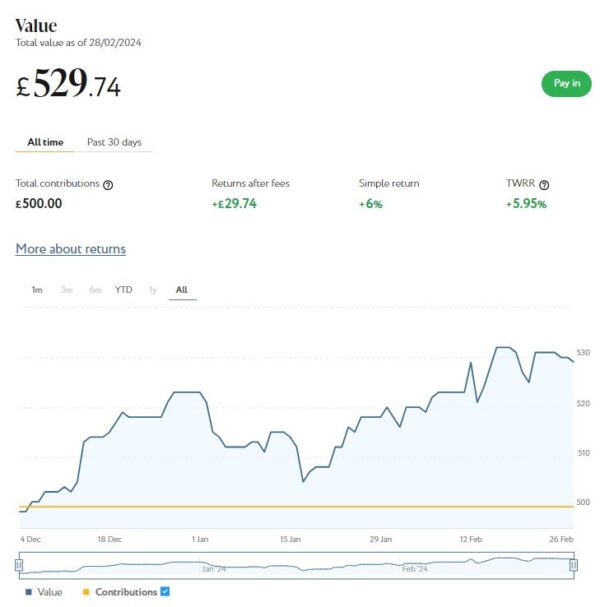

Finally, at the start of December 2023 I invested £500 in one of Nutmeg’s new thematic portfolios (Resource Transformation). As you can see from the screen capture below, this is now worth £530, an increase of £11 since last month and £30 or 6% over the three-month period since I first invested.

February was obviously a good month for my Nutmeg investments. Overall I was up £737 or 2.79%. In these turbulent times I am more than happy with that.

You can read my full Nutmeg review here (including a special offer at the end for PAS readers). If you are looking for a home for your annual ISA allowance, based on my overall experience over the last seven years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs), Lifetime ISAs and Junior ISAs as well.

Don’t forget, the current tax year ends on 5 April 2024 and after that the 2023/24 tax-free ISA allowance of £20,000 will be gone forever!

I also have investments with the property crowdlending platform Kuflink. They continue to do well, with new projects launching every week. I currently have around £1,570 invested with them in 10 different projects paying interest rates averaging around 7%. I also have £14 in my Kuflink cash account.

To date I have never lost any money with Kuflink, though some loan terms have been extended once or twice. On the plus side, when this happens additional interest is paid for the period in question.

There is now an initial minimum investment of £1,000 and a minimum investment per project of £500. Kuflink say they are doing this to streamline their operation and minimize costs. I can understand that, though it does mean that the option to test the water with a small first investment has been removed. It also makes it harder for small investors (like myself) to build a well-diversified portfolio on a limited budget.

One possible way around this is to invest using Kuflink’s Auto/IFISA facility. Your money here is automatically invested across a basket of loans over a period from one to five years. Interest rates range from 7% to around 10%, depending on the length of term you choose. Full up-to-date details can be found on the Kuflink website.

You can invest tax-free in a Kuflink Auto IFISA. Or if you have already used your annual iFISA allowance elsewhere, you can invest via a taxable Auto account. You can read my full Kuflink review here if you wish.

Moving on, my Assetz Exchange investments continue to generate steady returns. Regular readers will know that this is a P2P property investment platform focusing on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my AE portfolio has generated a respectable £168.53 in revenue from rental income. As I said in last month’s update, capital growth has slowed, though, in line with UK property values generally.

At the time of writing, 10 of ‘my’ properties are showing gains, 4 are breaking even, and the remaining 15 are showing losses. My portfolio is currently showing a net decrease in value of £40.01, meaning that overall (rental income minus capital value decrease) I am up by £128.52. That’s still a decent return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Assetz Exchange most projects are socially beneficial as well.

The overall fall in capital value of my AE investments is obviously a little disappointing. But it’s important to remember that until/unless I choose to sell the investments in question, it is largely theoretical, based on the most recent price at which shares in the property concerned have changed hands. The rental income, on the other hand, is real money (which in my case I’ve reinvested in other AE projects to further diversify my portfolio).

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of AE as far as i am concerned (especially now that Kuflink have raised their minimum investment per project to £500). You can actually invest from as little as 80p per property if you really want to proceed cautiously.

As I noted in this recent post, Assetz Exchange is particularly good if you want to compound your returns by reinvesting rental income. This effectively boosts the interest rate you are receiving. Personally, once I have accrued a minimum of £10 in rental payments, I reinvest this money in either a new AE project or one I have already invested in (thus increasing my holding). Over time, even if I don’t invest any more capital, this will ensure my investment with AE grows at an accelerating rate.

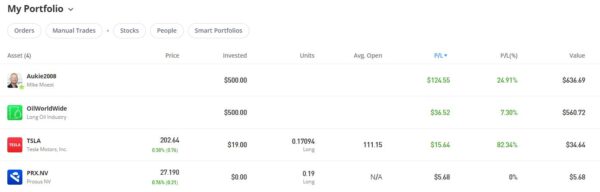

In 2022 I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios, Oil Worldwide. I also invested a small amount I had left over in Tesla shares.

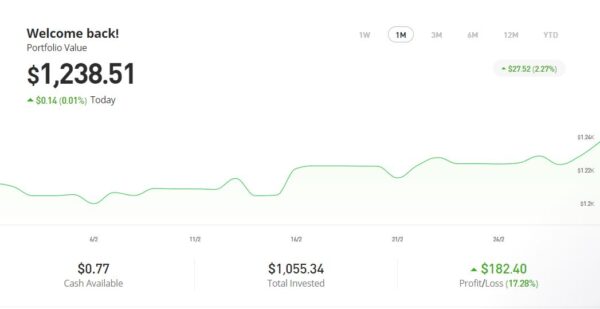

As you can see from the screen captures below, my original investment totalling $1,022.26 is today worth $1,238.51, an overall increase of $216.25 or 21.15%.

eToro also offer the free eToro Money app. This allows you to deposit money to your eToro account without paying any currency conversion fees, saving you up to £5 for every £1,000 you deposit. You can also use the app to withdraw funds from your eToro account instantly to your bank account. I tried this myself and was impressed with how quickly and seamlessly it worked. You can read my blog post about eToro Money here. Note that it can also serve as a cryptocurrency wallet, allowing you to send and receive crypto from any other wallet address in the world.

I had three more articles published in January on the excellent Mouthy Money website. The first is How to Save Money on Motoring. Like everything else in life the cost of motoring is going up and up, so in this article I set out a variety of ways – from ride-sharing to driving for fuel economy – you may be able to reduce it.

Also in February Mouthy Money published Are You Making the Most of Your Annual ISA Allowance?. As mentioned earlier, the 2023/24 tax year ends in just a few weeks’ time. And after that the £20,000 tax-free ISA allowance for that year will be gone forever. In this article I describe the different types of ISA – Cash ISA, Stocks and Shares ISA, Innovative Finance ISA (IFISA) and Lifetime ISA (LISA) – and explain how they work and the differences between them. I also provide some tips and advice for making the most of your annual ISA allowance.

My final article published on Mouthy Money last month was Can You Save Money on Your Shopping with JamDoughnut? Regular PAS readers will know that I am a fan of the JamDoughnut app, which enables you to save up to 20% on purchases with a growing range of retailers. The article also reveals how you can get a £2 head-start by using my referral code.

As I’ve said before, Mouthy Money is a great resource for anyone interested in money-making and money-saving. I am a particular fan of my fellow MM contributor and money blogger Shoestring Jane. She writes mainly about money saving and frugal living. Her latest article Frugal Skills to Save You Money sets out a selection of life skills that can save you money (and aren’t hard to learn). You can see all of Jane’s articles for Mouthy Money via this web page.

I also published several posts on Pounds and Sense in February. I won’t bother mentioning those that are no longer relevant now, but the others are listed below.

In Get Your Will Written Free of Charge in March I revealed how you can get your will written (or updated) free of charge during Free Wills Month. This regular event supports a range of leading charities. Obviously the hope is that you will include a bequest to charity in your will, but there is absolutely no obligation to do this. Free Wills Month is now up and running. If you want to take advantage and get your will written free, I recommend acting now as there are only limited spots available.

Also in March I published a guest post titled Building Your Own Home – It’s Not Just for the Super Rich! This post was written on behalf of Suffolk Building Society, who are trying to raise awareness of the self-build option in the UK. As they say in the article, they can provide mortgages to purchase land suitable for self-build projects. SBS emphasize that this option is suitable and available for ‘ordinary people’, not just the super-rich folk you see on TV shows like Grand Designs!

I also published Saving for a Rainy Day or a Stormy Breakup? The Surprising Facts About Secret Savings Accounts. This post is based on some eye-opening research from my friends at Smart Money People, which revealed (among other things) that one in ten people in a serious relationship, including marriage, civil partnerships, or cohabitation, maintain a secret savings account. Find out more in this post.

Also, from January this year I became a regular contributor to the new Over 60s Discounts website. You can read my latest article here: Who Cares for the Carers? This is about help available for unpaid carers in the UK, both financial and practical. I highly recommend registering at Over 60s Discounts, by the way – they list a growing range of discounts and bonuses for older people, including some that are unique to O60D.

One other thing is that this month I switched my Santander 123 Lite current account to a Santander Edge current account. I will try to find time to write a separate post about this soon. But briefly, my main reason was because having an Edge current account allows you to open an Edge savings account, which offers a market-leading 7% interest rate (AER) for amounts of up to £4,000 for one year (it then falls to 4.5% AER).

The Santander Edge account has slightly higher fees (£3 a month as opposed to £2) and the cashback on offer is slightly less. However, when I crunched the numbers, the value of having an Edge savings account easily outweighed this. Though I am fortunate in that I had £4,000 I could put into it immediately from another, lower-paying savings account. If I hadn’t had that, it wouldn’t have been worth switching to the Edge account.

Finally, a quick reminder that you can also follow Pounds and Sense on Facebook or Twitter/X. Twitter/X is my number one social media platform these days and I post regularly there. I share the latest news and information on financial (and other) matters, and other things that interest, amuse or concern me. So if you aren’t following my PAS account, you are definitely missing out!

That’s all for today. As always, if you have any comments or queries, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media:

Mother’s Day is coming, so here’s a chance to make it extra special for one lucky winner!

I’ve joined forces with some of my fellow UK bloggers in this giveaway with multiple prizes. Entering the giveaway is free of charge and full instructions can be found below.

There are multiple ways to enter, and the more you do, the better your chances of winning. But note that where an entry requires following a social media account, you will need to continue following this account until the winner has been drawn on Sunday 10th March 2024 (Mother’s Day). Before the winner is announced the organisers will check that they are still following the account in question. If not, they will be disqualified and another winner drawn.

This giveaway has been organised by my fellow blogger Rowena Becker, who blogs at My Balancing Act. Please check out her blog and those of the other talented bloggers taking part (listed below). And read on for full details from Rowena of all the prizes on offer and how you could win this great prize bundle!

Welcome to the ultimate Mother’s Day Giveaway and Gift Guide! This is brought to you by a collaboration of some of the UK’s leading bloggers.

We understand that finding the perfect gift to express gratitude and love for the special women in our lives can be a daunting task. That’s why we’ve come together to curate an exceptional selection of prizes that are sure to delight any mother.

This guide not only aims to make your gift shopping easier but also adds an exciting twist with a giveaway that could win you these wonderful items.

Join us in celebrating motherhood this year by taking part in this fantastic opportunity to spoil your mum – or yourself! Show her just how much she means to you ❤

Meet the Bloggers

In order to be able to bring you this incredible giveaway, some of the UK’s top bloggers got together. A massive thank you to our bloggers! The bloggers taking part are:

Art File Jungle Animals 1000 Piece Jigsaw Puzzle from Gibsons Games

Delight in the vibrant Art File Jungle Animals 1000 Piece Jigsaw Puzzle. A tribute to the diverse beauty of our planet’s wildlife. Crafted with precision and creativity by an award-winning designer from The Art File, this puzzle captures the essence of nature’s splendour. As a joint venture between Gibsons Games and The Art File, two renowned British family businesses, this jigsaw puzzle represents their shared commitment to quality and innovation.

Each of the 1000 pieces contributes to a stunning visual experience, making it not just a puzzle but a piece of art. This makes it an excellent gift for mums who appreciate both the challenge of a jigsaw and the aesthetics of fine art. Plus, it’s part of our exciting prize bundle – a perfect blend of challenge, relaxation, and artistic appreciation.

Liquid Silk Perfect Cleansing Oil (100ml) from DJUSIE

Introducing Liquid Silk Cleansing Oil, the ultimate cleansing oil that will leave your skin feeling smooth and rejuvenated. Designed for all skin types and ages, this luxurious oil delivers a refreshing clean to both oily and dry skin, leaving it perfectly balanced and radiant. Not only is it functional. It also provides a luscious sensory experience with its effortless formula to even remove waterproof makeup.

The refreshing and uplifting scent of lime, red grapefruit, jasmine, and geranium creates a fruity and nuanced aroma that will invigorate your senses. This luxurious blend not only nourishes your skin but also has a positive impact on your mood. The application process is simple. Massage a few drops onto dry skin in circular motions to dissolve impurities and makeup. Then rinse with water. Your mum will be left with soft, supple, and glowing skin that she’ll love. We have one to giveaway to our lucky prize winner!

Pure Shea Butter (180ml) from Aviela

Next up on our pamper list is the 100% pure, highest grade unrefined Shea butter. The perfect choice of gift to show our appreciation and love for the incredible mothers or women in our lives. Packed with essential fatty acids, vitamins A and E, with natural soothing properties, the Shea butter deeply hydrates and nourishes the skin. It quickly absorbs into the skin, leaving it supple and glowing while also creating a protective barrier to prevent moisture loss. This makes it an ideal addition to any skincare routine for all skin types.

The luxurious butter, suitable for use from hair to toe, offers exceptional hydration, outstanding nourishment, and remarkable skin-softening effects for all skin types. It’s particularly effective in combating dryness and soothing irritated skin. As part of our Mother’s Day giveaway, we’re excited to offer one lucky winner the chance to experience these benefits firsthand. Don’t miss out on your opportunity to win this sumptuous treat for your skin!

TIMELESS RENEWAL BIO-RETINOL BODY OIL (100ml) from Evolve Organic Beauty

Evolve Organic Beauty’s latest addition to the age-defying product line, this divinely scented firming body oil is a treat for all skin types, including dry ones. The blend of Retinol analogue Bidens Pilosa, Hyaluronic Acid, Organic Macadamia Oil, and Apricot oils work in harmony to nourish, firm, rejuvenate and smooth your skin while also improving its elasticity and locking in hydration for a youthful glow.

Infused with the organic essential oils of Rose Geranium, Ylang Ylang and Mandarin, the timeless renewal bio-retinol body oil not only pampers your skin but also delights your senses. This Mother’s Day, consider gifting this luxurious body oil to the most important woman in your life. It’s a thoughtful gift that shows you care about her well-being and is part of our Mother’s Day prize bundle. This product is more than just skincare. It’s a chance for her to indulge in a moment of self-care, making it the perfect gift for any occasion.

Paradise Luxury Gloss (Colour: Spell) from Doll Smash Cosmetics

Presenting the Paradise Luxury Gloss from Doll Smash Cosmetics. A luxe lip enhancer that promises brilliant shine, a smooth look, and a luscious feel. This high-quality gloss is designed to elevate your lips while diminishing any imperfections. Its unique formula is far from the sticky or tacky feel of traditional lip glosses. Instead offering a soft, creamy texture that leaves your lips feeling deliciously smooth. The immediate, radiant shine it delivers makes it an instant favourite.

As part of our prize bundle, this gloss makes an excellent gift for mums who appreciate a touch of luxury in their makeup routine. It’s more than just a gloss – it’s a ticket to a pampering experience that every mum deserves.

£50 Amazon Voucher from Make Money Without A Job

Make Money Without A Job is donating a £50 Amazon Voucher to our lucky winner! Check out Make Money Without A Job if you’re looking for ways to earn extra money. Because Make Money Without A Job does exactly what it says. There are over 3,000 articles about making money from side hustles and starting your own business. Whether you want to make £100 a month or £5,000 a month there are ideas for everyone!

What’s more, there’s a free daily draw to win £10, and if it isn’t claimed, the prize rolls over. They’ve given away multiple prizes over £100 to lucky winners. Check out the draw at www.makemoneywithoutajob.com/draw

How to Enter

You can enter the Giveaway by completing as many Rafflecopter widget entry options below as you like. All entries will be collected, and one winner will be randomly chosen via Rafflecopter. Good luck!

The giveaway will run from 8 pm 3rd March 2024 to 8 pm 10th March 2024.

The winners will be notified by email from rowena@mybalancingact.co.uk

The winner will have 7 days to respond after which time we reserve the right to select an alternative winner.

This prize draw is in no way sponsored, endorsed or administered by, or associated with, Facebook, Instagram, X, YouTube, BlogLovin or Pinterest or any other social media platform.

Prize open to over 18s only. Age verification may be required to receive some prizes.

Some or all of the prizes may take a few weeks to arrive.

If any prizes are out of stock then we will do our best to find a suitable replacement but cannot guarantee it.

Anyone who unfollows before the giveaway ends or doesn’t complete the required entry action will be disqualified.

The prize is non-transferable, non-refundable and cannot be exchanged for monetary value.

We may be using a parcel service or Royal Mail for some of the prizes and their standard compensation will apply in the event of loss or damage.

Some items may be sent directly by the supplier and we do not have responsibility if these go missing and we cannot replace these.

In the unlikely event one of the companies withdraws a prize, we cannot offer an alternative.

The winner’s name will be stated on some or all of our bloggers’ websites and announced on Twitter and other social media channels. It will also be displayed on the Rafflecopter entry form. By entering this prize draw, you give your permission for this.

Please note the winner may have the same name as you so if you see your name displayed, be aware that you are not the winner unless you have been notified by us.

There may be some delays in receiving prizes.

Good luck, and I hope a Pounds and Sense reader wins this wonderful prize bundle!

If you enjoyed this post, please link to it on your own blog or social media:

Free Wills Month brings together a group of well-respected charities to offer members of the public aged 55 and over the opportunity to have their wills written or updated free using participating solicitors across the UK. The next one begins on Friday March 1st 2024.

The charities involved include the NSPCC, Dogs Trust, Samaritans, Mind, The Stroke Association, PDSA, The National Trust, Mencap, Age UK, and many more.

The scheme covers simple wills only, including ‘mirror wills’ for couples. In the latter case, only one member of the couple has to be 55 or over. If you need a complicated will (most people don’t) you can still have this done but may have to pay a top-up fee.

I strongly believe in using a properly qualified solicitor to draw up your will. In the last few years there have been a couple of occasions when failing to do this has caused problems and delays for members of my family. An up-to-date will written by a solicitor will ensure that your wishes are respected and will avoid causing legal complications for your loved ones after you are gone.

Free Wills Month means what it says. There are no catches, although the organizers hope that you will choose to leave a donation to charity in your will. There is no obligation to do this, however.

To take part in Free Wills Month click through to the website on or after March 1st 2024. You can then pick a solicitor from the list of companies taking part and contact them to book an appointment. Appointments are limited and on a first come, first served basis, so it’s important to call as soon as possible. Once all available appointments are taken, the campaign will close. This may happen before the end of March.

Until March 1st you can enter brief details on the Free Wills Month website and will then receive an email reminder when the scheme opens.

If you have any comments or questions about this subject, as ever, please do post them below.

This is an annual update of this post.

If you enjoyed this post, please link to it on your own blog or social media:

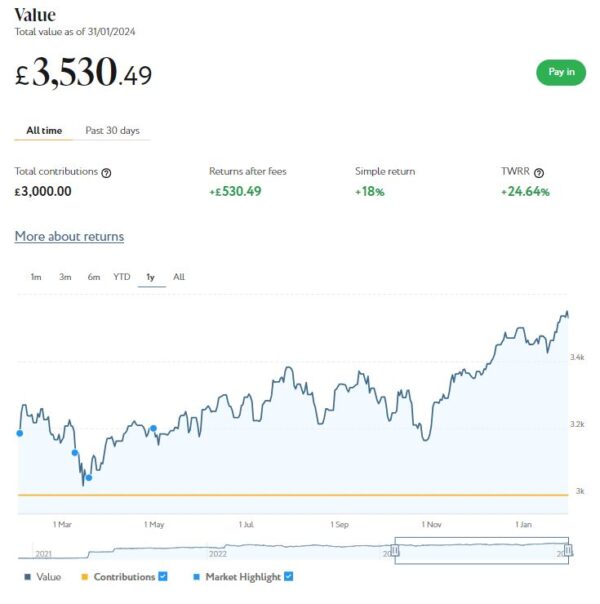

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

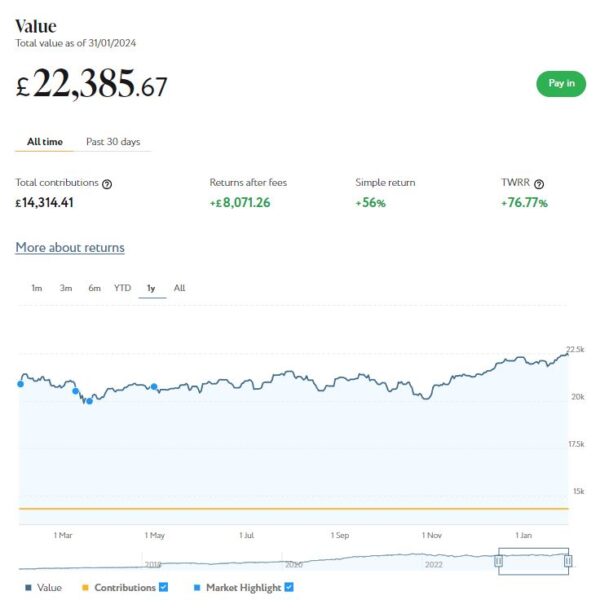

As the screenshot below for the last 12 months shows, my main Nutmeg portfolio is currently valued at £22,386. Last month it stood at £22,292 so that is a modest increase of £94.

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £3,530 compared with £3,501 a month ago, a rise of £29. Here is a screen capture showing performance over the last 12 months.

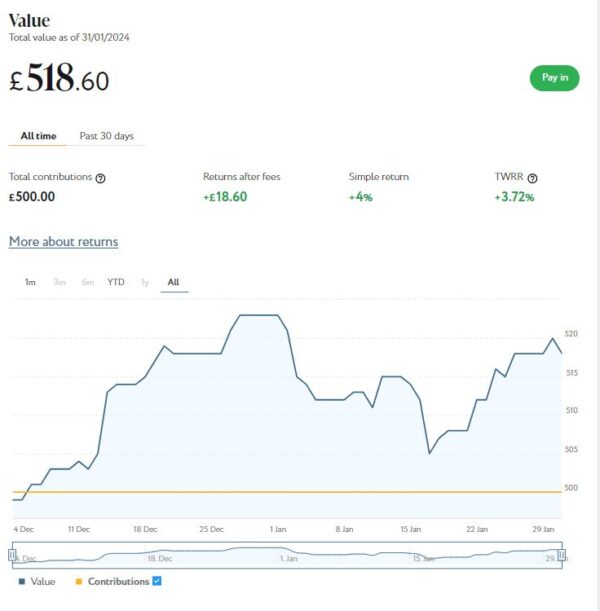

Finally, at the start of December 2023 I invested £500 in one of Nutmeg’s new thematic portfolios (Resource Transformation). As you can see from the screen capture below, after a storming start in December this fell back in January before recovering again to £519, a small drop of £4 or 0.76% month on month. It is still around 4% ahead since I invested at the start of December, though.

January was obviously a mixed month for my Nutmeg investments. Overall I was still £119 up, though. If you add this to the increase of £1,160 last month, that gives a total value increase over the last two months of £1,279 or 5.17%. In these turbulent times I am more than happy with that.

You can read my full Nutmeg review here (including a special offer at the end for PAS readers). If you are looking for a home for your annual ISA allowance, based on my overall experience over the last seven years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs), Lifetime ISAs and Junior ISAs as well.

I also have investments with the property crowdlending platform Kuflink. They continue to do well, with new projects launching every week. Last month I withdrew £350 from completed projects to help pay for a much-needed holiday in the spring. I currently have around £1,570 invested with them in 10 different projects paying interest rates averaging around 7%. I also have £14 in my Kuflink cash account.

To date I have never lost any money with Kuflink, though some loan terms have been extended once or twice. On the plus side, when this happens additional interest is paid for the period in question.

There is now an initial minimum investment of £1,000 and a minimum investment per project of £500. Kuflink say they are doing this to streamline their operation and minimize costs. I can understand that, though it does mean that the option to test the water with a small first investment has been removed. It also makes it harder for small investors (like myself) to build a well-diversified portfolio on a limited budget.

One possible way around this is to invest using Kuflink’s Auto/IFISA facility. Your money here is automatically invested across a basket of loans over a period from one to three years. Interest rates normally range from around 7% for one year to 9.83% gross for a three-year term.

As a special Valentine’s Day promotion, however, until 14 February 2024 they are offering enhanced rates of 9% for one year, 10.5% for two years and 12.25% gross for a three-year term. These figures are AER (annual equivalent rates) that incorporate reinvestment of interest paid at the end of each year. These are actually the highest rates I have ever seen Kuflink offering ❤

You can invest tax-free in a Kuflink Auto IFISA. Or if you have already used your annual iFISA allowance elsewhere, you can invest via a taxable Auto account. You can read my full Kuflink review here if you wish.

Moving on, my Assetz Exchange investments continue to generate steady returns. Regular readers will know that this is a P2P property investment platform focusing on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my AE portfolio has generated a respectable £161.85 in revenue from rental income. As I said in last month’s update, capital growth has slowed, though, in line with UK property values generally.

At the time of writing, 6 of ‘my’ properties are showing gains, 3 are breaking even, and the remaining 19 are showing losses. My portfolio is currently showing a net decrease in value of £40.87, meaning that overall (rental income minus capital value decrease) I am up by £120.98. That’s still a decent return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Assetz Exchange most projects are socially beneficial as well.

The overall fall in capital value of my AE investments is obviously a little disappointing. But it’s important to remember that until/unless I choose to sell the investments in question, it is largely theoretical, based on the most recent price at which shares in the property concerned have changed hands. The rental income, on the other hand, is real money (which in my case I’ve reinvested in other AE projects to further diversify my portfolio).

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of AE as far as i am concerned (especially now that Kuflink have raised their minimum investment per project to £500). You can actually invest from as little as 80p per property if you really want to proceed cautiously.

As I noted in this recent post, Assetz Exchange is particularly good if you want to compound your returns by reinvesting rental income. This effectively boosts the interest rate you are receiving. Personally, once I have accrued a minimum of £10 in rental payments, I reinvest this money in either a new AE project or one I have already invested in (thus increasing my holding). Over time, even if I don’t invest any more capital, this will ensure my investment with AE grows at an accelerating rate.

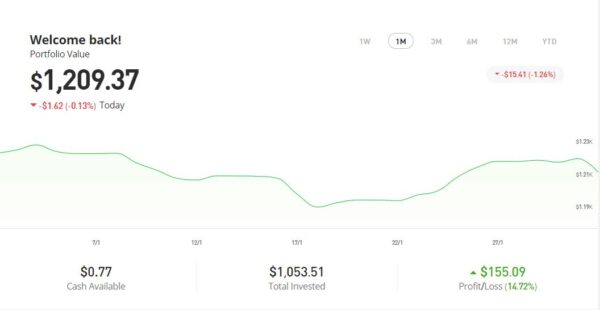

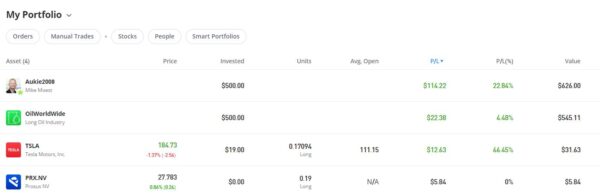

Last year I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios, Oil Worldwide. I also invested a small amount I had left over in Tesla shares.

As you can see from the screen captures below, my original investment totalling $1,022.26 is today worth $1,209.37, an overall increase of $187.11 or 18.30%.

eToro also recently introduced the eToro Money app. This allows you to deposit money to your eToro account without paying any currency conversion fees, saving you up to £5 for every £1,000 you deposit. You can also use the app to withdraw funds from your eToro account instantly to your bank account. I tried this myself and was impressed with how quickly and seamlessly it worked. You can read my blog post about eToro Money here.

I had three more articles published in January on the excellent Mouthy Money website. The first is How to Save Money on Your Water Bills. In Britain we’re lucky to have high-quality running water on tap whenever we need it. Like everything else in life it costs money, however. And in these times of rising prices and squeezed incomes, those costs can be a growing burden. So in this article I set out some ways you may be able to reduce your water bills.

Also in January Mouthy Money published How to Make Money With Classic Cars. In this article – written in association with my friends at the Car & Classic website – I described the surprising number of attractions to investing in classic cars, and provided a range of tips for those new to the field.

My final article published on Mouthy Money last month was Top Tips to Avoid Online Scams. This article set out my top ten tips for staying safe online and avoiding becoming a victim of the scammers. Do check it out!

As I’ve said before, Mouthy Money is a great resource for anyone interested in money-making and money-saving. I particularly like the ‘Deals of the Week’ feature compiled by Jordon Cox (‘Britain’s Coupon Kid’) which lists all the best current money-saving offers for savvy shoppers. Check out the latest edition here.

I am also a fan of my fellow MM contributor and money blogger Shoestring Jane. She writes mainly about money saving and frugal living. Her latest article How to Get Almost Everything More Cheaply has some great tips and ideas. You can see all of her articles for Mouthy Money via this web page.

I also published several posts on Pounds and Sense in January. I won’t bother mentioning those that are no longer relevant now, but the others are listed below.

In How to Start Copy Trading With eToro I discussed how to get started using the popular copy trading facility on eToro. This allows you to automatically copy successful traders on the platform – so when they make money, you make money too. As mentioned above, I have done this myself following Dutch professional investor Mike Moest and am currently around 23% in profit. You can read more in my post about copy trading on eToro and my experiences with it.

I also published HMRC Crackdown on Side Hustles – Truth and Fiction. As you may know, from January this year digital platforms like eBay, Etsy and Airbnb are required to collect additional information from sellers, including numbers of sales and amount of income generated. This data will be automatically shared with HMRC, who will compare it against their records to see if any tax may be due. This news has caused some consternation on social media, with many who have side hustles to help pay the bills worried they may be hit by an unexpected tax demand. In this post I explain what exactly is happening and set out to separate the truth from the fiction.

In Planning a UK Holiday This Year? Here Are Some Ideas For You! I set out a list of destinations in the UK I have visited myself, with links to my full reviews of the places concerned. They range from Bath to Barmouth, Lavenham to Llanbedrog. If you’re looking for ideas for a short break (or longer) in the UK this year, this could be a good source of inspiration for you 🙂

One Key Lesson About Investing I Learned From My Dad’s Big Mistake reveals an important lesson I learned from my late father about investing. It is a lesson I have tried to apply in all my investing myself. While it hasn’t stopped me making some mistakes along the way, it has certainly helped me avoid any disastrous losses. This article was first published in a slightly different form on Mouthy Money.

Finally in January I published How to Harness the Power of Compounding. In this article I discussed the power of compounding and compound interest. This is a wealth-building secret every saver and investor should embrace. I also revealed two particular types of investment where you can apply compounding to help boost your returns.

Also, from January I have become a regular contributor to the new Over 60s Discounts website. You can read my first article here: How to Cope With Loneliness in Later Life. As you may gather, as well as personal finance I will also be writing about ‘lifestyle’ matters for O60D.

On other things, the opportunity to get a free share worth up to £100 with Trading 212 has now closed. However, you can can also still Get a Free ETF Share Worth up to £200 with Wealthyhood. This DIY wealth-building app is aimed especially at people new to stock market investing. The minimum investment to qualify for the free share offer is £50 – but on the plus side, they now guarantee your free ETF share will be worth at least £10.

I am still using and getting good results from the cashback app JamDoughnut. You can see my review of JamDoughnut here, along with a referral code that will get you a £2 bonus when you sign up. To be honest I’m surprised more PAS readers haven’t taken advantage of this opportunity. Not only can you get discounts of up to 20% using the app, they also hold regular contests and promotions offering additional bonuses and discounts.

Finally, a quick reminder that you can also follow Pounds and Sense on Facebook or Twitter/X. Twitter/X is my number one social media platform these days and I post regularly there. I share the latest news and information on financial (and other) matters, and other things that interest, amuse or concern me. So if you aren’t following my PAS account, you are definitely missing out!

That’s all for today. As always, if you have any comments or queries, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media:

For many of us 2023 was another difficult year. While the pandemic receded, we now face a cost-of-living crisis driven especially by rising gas and electricity costs.

With the festive season behind us now and the worst months of the winter still (probably) to come, many of us are understandably desperate for something to look forward to in the year ahead.

Some will be planning to go abroad, perhaps for the first time since the pandemic. But others may be deterred by the cost of going overseas and the additional hassles it may (still) entail.

So today I thought I’d share links to my blog posts about some UK holiday destinations I’ve visited in the last few years, in case you wish to consider them for short breaks – or longer – in the year ahead. Clicking on any of the links below will open my post about the place concerned in a new tab, so you won’t have to keep clicking the Back button to return here.

Llandudno in North Wales is somewhere I have been visiting regularly for over ten years now. It’s a traditional British seaside resort with a long pier, Punch and Judy show, sweeping promenade, and plenty more (you can see the stunning Victorian seafront in the cover image). It’s very popular with both older people and young families. As well as my main review, my October 2020 Coronavirus Crisis Experience Update includes details of a short break I enjoyed there just before the Welsh government imposed another lockdown 😮

Minehead is a North Somerset coastal town. I enjoyed a short break there in 2020 as well, at a time when lockdown rules were relaxed. It was my first visit to Minehead and I particularly enjoyed visiting the National Trust property Dunster Castle, which is just a couple of miles down the road. Sadly the West Somerset Railway which starts (or ends) in Minehead was closed due to the pandemic when I went, but I’d love to go back for a trip on this heritage steam railway sometime in the future.

Aberystwyth is in mid-Wales on the Cardigan Bay coast. I have visited it three times now, the first two staying at the Marine Hotel and the most recent at a self-catering apartment called Sea Brin. Aberystwyth is quieter and less commercialized than Llandudno (mentioned above), and the fact it’s a university town means it has quite a cosmopolitan feeling. It’s a good place to chill out, but there are plenty of interesting things to see and do as well.

I visited Aberdovey for the first time in April 2023. It’s a small town on the mid-Wales coast. It’s about ten miles north of Aberystwyth and five miles south of Tywyn, the home of the Talyllyn Railway (see below). It’s a charming, laid-back place, perfect for a relaxing short break. It has a beautiful beach (with watersports for those who want them) and some great cafes and restaurants. I wouldn’t go there for the night-life, though – even the chip shop closes at 8 pm!

I had a particular reason to visit Hewenden MIll Cottages, as my sister Liz and her family live just a couple of miles down the road in Wilsden. Even if I didn’t have family connections, though, I would definitely recommend them for a short break. The accommodation consists of a converted mill and a number of former workers’ cottages, all in a beautiful woodland setting. The apartments and cottages are spacious and well equipped. From here you can visit Haworth – home of the Bronte sisters – and the Victorian model village of Saltaire. The area is also great for walking and cycling.

I went back to Hewenden Mill in October 2021 for a family reunion. I stayed in a cottage on the main site (picture below). I went for a long weekend but ended up staying almost a week. This was from necessity rather than choice, as the petrol crisis struck and I was unable to buy fuel to get home. The management at Hewenden were wonderful, though, and said I could stay on as long as I needed for no further charge. I therefore recommend them even more highly now!

The Aberdunant Hall Holiday Park and Hotel (to give it its full name) is about four miles from the North Wales coastal town of Porthmadog You can stay in the hotel itself (which is quite compact) or in accommodation around the park. I stayed in what they call a Forest Pod, which is roughly the equivalent of half a caravan. It was okay for a short break but if you went as a couple the cramped conditions could put a strain on your relationship! If I went again I would book a room in the hotel or maybe one of the Woodland Escape Suites in the park. I still enjoyed my stay there, and found the location convenient for visiting a range of places including Portmeirion (where the sixties TV series The Prisoner was filmed) and the Ffestiniog Railway, which runs from Porthmadog to Baenau Ffestiniog. It’s also on the edge of Snowdonia, with lots of opportunities for walking and mountain climbing.

Lake Vyrnwy is a few miles over the border from Shropshire into Wales. I went there in 2019 after watching a TV show about the history of this artificial lake, which was originally created to provide a water supply for the people of Liverpool in the 19th century (it’s now naturalised and if you weren’t aware of its history you wouldn’t know it was man-made). I stayed at the Lake Vyrnwy Hotel and Spa, which is near the dam at the western end of the lake. This was originally built to accommodate senior managers and engineers on the construction project, though it has of course been extended and modernised many times since. If you want to visit Lake Vyrnwy, it’s the best (possibly the only) option. I happened to choose a bitterly cold weekend just before Easter for my visit, which spoiled it a bit. Still, I enjoyed the beautiful scenery and some great walks. It’s probably not a place to take children, however, as there might not be enough for them to do.

The Talyllyn Railway (also mentioned under Aberdovey) is a heritage steam railway in Wales. It starts in the town of Tywyn in mid-Wales, so in October 2018 I booked a short break there. To be honest there isn’t a great deal else to do in Tywyn, but it makes a good base for a day on the railway. And the railway itself takes you through some stunningly beautiful countryside. If you buy one of their very reasonably priced Day Rover tickets, you can get on and off at any station along the route. I highly recommend an hour or two at Dolgoch, which has some great walks and lovely waterfalls.

Warner Leisure Hotels have 16 country and coastal resort hotels across England and Wales. They have a strict adults-only policy, and appeal mainly to an older clientele (based on my experience, the average age is around seventy). As well as accommodation they offer a variety of leisure activities, including day trips, quizzes, guided walks, archery and bowls, social dancing, swimming, and so on. Most of these activities are included in the price, as is the evening entertainment. I have stayed at Bodelwyddan Castle in North Wales and Alvaston Hall in Cheshire. Some aspects I liked, others I wasn’t so keen on, as you can read in my review. You can also see their latest offers by clicking on the banner ad below [affiliate].

About four years ago I took a short break in the English Lake District. I stayed at the Waterhead Hotel, just south of Ambleside, at the north end of Lake Windermere (England’s largest lake). The hotel is located literally a few yards from the lake (hence the name, of course). If you haven’t visited the Lake District before, the area should definitely be on your ‘To Do’ list. There are many miles of beautiful countryside to explore, along with attractions such as Beatrix Potter’s house and Wray Castle. And, of course, you must buy a day ticket for the Windermere lake steamers. You can travel the length of the lake in style on these vessels, while sipping a hot chocolate (or something stronger) and listening to commentary on the scenery passing alongside. Highly recommended 🙂

I visited Lanbedrog for the first time in July 2021. It’s a village on the Llyn (or Lleyn) Peninsula in NW Wales. I stayed at an Airbnb property, the first time I had done this (Llanbedrog doesn’t have any hotels as far as I know). It’s by the coast, roughly half way between Pwllheli (famed for its Butlins camp, now run by Haven Holidays) and trendy Abersoch. It has a beautiful sandy beach which would be perfect for families with young children (or grandchildren). I very much enjoyed my three-night stay and found it a perfect place to relax and chill out after months of lockdown. The National Trust mansion (and garden) Plas yn Rhiw is about seven miles away.

I stayed in Criccieth in North Wales for the first time in June 2022, although I have visited the town in the past. It is a lovely place to relax and chill out. It has excellent road and rail connections, and there are also some high-quality tourist attractions nearby, including Portmeirion and the Ffestiniog Railway. Criccieth itself is best known for its castle which dominates the town. Although it’s a ruin, many of the walls are still standing and you can enjoy some amazing views across the bay, as far as Harlech Castle and beyond.

I visited Lavenham in Suffolk for the first time in August 2022. It is said to be England’s best-preserved medieval town, with over 300 listed, timber-framed houses. There are various historic buildings such as the Guildhall and Little Hall you can look around. Lavenham also boasts a variety of highly rated pubs and restaurants, and some lovely tea rooms and coffee houses as well! 🍮

Barmouth is a traditional Welsh seaside resort about ten miles south of Harlech. I visited in September 2022, staying at an elegant Victorian Gothic hotel called Tyr Graig Castle. Barmouth has a clean, attractive promenade and beautiful sandy beach which goes out a long way. There is plenty to do for families, including a funfair and amusement arcades. There are various restaurants and fast food outlets along the seafront. There is also a railway station with regular trains to Pwllheli in one direction and Aberystwyth and beyond in the other. Nearby attractions include Harlech Castle, Portmeirion and the Fairbourne miniature steam railway 🚂

I visited the historic city of Bath in June 2023. There is lots to see and do, although top of many people’s lists will be the stunning Roman Baths. Bath Abbey is well worth a look too, and you can admire the beautiful Georgian architecture around the city for free! Read my top tips for anyone visiting Bath in this post, including the excellent self-catering accommodation I stayed at.

Other Resources

Here are links to a few other blog posts that may be of interest if you are planning a UK holiday this year…

In recent years Airbnb has become increasingly popular for self-catering holidays. You can book anything from a spare room in someone’s home to a whole house or apartment. My recent short breaks in Lavenham and Llanbedrog (see list above) were in Airbnb properties. You can read all about the booking process in my post.

Finding a cashpoint in an unfamiliar town (or village) can be challenging, so you might find this free app a useful resource to download. It has helped me avoid embarrassment on several occasions.

If your thoughts are turning further afield, you may be considering a cruise holiday as an option. Even if you can’t go abroad, I can testify from personal experience that a cruise of the British Isles (like these, perhaps) can be very enjoyable and enlightening. My blog post sets out a range of tips and advice that will be particularly relevant for first-time and solo cruisers.

Finally, coach holidays are another very popular option among older people especially. I don’t have much experience of this myself, but my friends at Over 60s Discounts have a great article about coach holidays for over-60s in the UK. This includes a list of popular UK destinations and details of several companies offering low-cost coach holidays.

Closing Thoughts

I hope you have enjoyed reading this post and it has given you a few ideas for UK vacations (I refuse to call them ‘staycations’, as in my view that means staying at home for a holiday, and we’ve all had enough of that!).

Obviously I am a 60-something male and nowadays usually travel on my own. So if your circumstances are different from mine, I understand that some of the destinations mentioned above might not hold as much appeal. In addition, I live in Staffordshire, so the places I go are all reasonably accessible from there.

Finally – as I noticed when reading back my list – I do have a bit of a penchant for places with heritage steam railways nearby, so please bear that in mind as well 😀

Of course, I’d love to hear your views about any of the destinations mentioned, or any other places in the UK you would recommend for a short break or longer holiday. Please leave any comments or questions below as usual.

Note: This is a fully revised update of a post originally published in February 2021.

As you may have heard, from January 1, 2025, digital platforms like eBay, Etsy and Airbnb will be required to collect additional information from sellers, including number of sales and amount of income generated.

This data will be automatically shared with HM Revenue & Customs (HMRC) by January 31, 2025, covering the 2024 calendar year. HMRC will then compare this against their records to see if any tax may be due.

This news has caused some consternation on messageboards and social media, with many who have ‘side hustles’ to help pay the bills worried they may be hit by an unexpected tax demand. Some of this concern may be justified, but (thankfully) much of it isn’t.

So today I thought I’d explain what’s actually happening and how you can minimize your tax liability from side hustles and reduce the risk of unwanted attention from the taxman (while staying within the law, of course).

So What’s Happening?

Digital platforms will automatically share seller information with HMRC if a seller has made 30 or more sales a year or earned over €2,000 (approximately £1,700).

The reporting threshold is set in Euro as this is a multi-national initiative by the Organisation for Economic Co-operation and Development (OECD) which aims to tackle tax evasion globally. The new rules apply to various digital platforms, defined as any app, website or software connecting sellers to consumers of goods and services.

It’s important to understand that this is a reporting change and not a change in tax law. If you didn’t have to declare certain earnings or pay tax on them before, that remains the case now. In particular, if you are selling personal possessions you no longer want/need – as opposed to items you bought with a view to selling them for profit – that wouldn’t normally count as trading and no tax would be due.

The other important exemption is that everyone in the UK has an annual trading allowance of £1,000. This means you are allowed to make up to £1,000 (gross) per year from self-employed work including side hustles. If your total annual income by this means is below £1,000, there is no need to declare it to HMRC or pay tax on it (even if you have a separate day job). Note, however, that in the case of online auction trading, that £1,000 is income before any platform fees and other selling costs are deducted.

If your taxable earnings from a side hustle are over £1,000 a year, you will need to notify HMRC via a self-assessment tax return. You will then be required to pay income tax on this, unless your total taxable earnings from all sources are below the personal tax-free allowance (currently £12,570).

Top Tips

As promised, here are some tips to help you negotiate the rules surrounding side hustles, minimize any potential tax liability, and reduce the chances of attracting unwanted attention from HMRC, all while staying within the law.

Keep careful records of all your business activities. That includes activities that you don’t believe count as trading, e.g. selling your unwanted possessions. You may need this info if you are challenged by HMRC.

In particular, keep a running record of total sales and number of transactions on platforms such as eBay. If you’re having a clear-out, it won’t be hard to exceed the 30-item or €2,000 limit that will trigger a report to HMRC. As mentioned above, if you’re just selling your old stuff, there shouldn’t be any tax liability. But you might understandably prefer to avoid having to field queries from HMRC about your selling activities.

It might therefore be a good idea to use a variety of platforms for selling your stuff rather than just one. So instead of just eBay, use other similar sites such as Facebook Marketplace, Gumtree, Vinted, Craigslist, Ziffit, eBid, and so on. Aim to keep your total sales on any one platform to under 30 and under €2,000 in total.

If you are selling items you have made yourself (e.g. clothing or jewellery) on websites like Etsy, be aware that this will also usually count as trading and any profits may be taxable. Again you can claim the £1,000 trading allowance, though.

If you think what you are doing counts as trading, monitor when your gross annual income (or turnover if you prefer) is approaching £1,000. At this point you might prefer to ‘shut up shop’ until the following year. Otherwise you will need to declare your earnings to the taxman and (if required) pay tax on them.

Be aware that cashback earned through websites such as Quidco and Top Cashback is not taxable. Neither is the cashback paid with certain bank accounts.

Note also that lottery and competition prizes are not generally taxable in the UK. Neither are gambling wins (not that I recommend this) or any profits made through matched betting.

I hope this article will have clarified the situation for you if you’re pursuing a side hustle or considering doing so. As I said earlier, the tax rules haven’t changed, but with the new reporting regime it’s more important than ever to understand what the tax and trading rules are and ensure you stay within them.

If you have any comments or queries, as always, feel free to leave them below. Please note that I am not a tax professional, however, and cannot answer detailed questions about your personal financial circumstances. As I said in this blog post a while ago, if you need advice with tax matters, in my view a qualified accountant should always be your first port of call.

If you enjoyed this post, please link to it on your own blog or social media: