As you doubtless know, one of the first acts of the new Labour government last year was to scrap the Winter Fuel Payment (WFP) for all but the very poorest pensioners (those eligible for pension credit).

Such was the outcry they had to backtrack and most pensioners will now receive WFP this winter – but with one major catch. Here’s everything you need to know…

1. What’s changed this year

The good news is that the Winter Fuel Payment has been reinstated for most pensioners. Here’s how it works…

If you were born on or before 21 September 1959 and meet the usual residence criteria, you are eligible for the payment.

For winter 2025/26 a household will normally receive £200 if the oldest person is under 80, or £300 if someone in the household is aged 80 or over.

Payment is automatic for most people — you don’t need to apply, unless perhaps you haven’t received it before.

2. The income threshold – what it means

Although the payment is available again for most, there is a taxable income threshold of £35,000 a year.

If your taxable income is £35,000 or less for the tax year 2025/26, you keep the full amount of the payment.

If your taxable income is over £35,000, you’ll still receive the payment initially, but it will be reclaimed via the tax system (either through your tax code if under PAYE, or via Self Assessment) or you may opt out of receiving the payment. Note that the deadline for opting out of the 2025/26 payment has now passed.

It’s important to note that the threshold applies to each individual, not to the household income. So in a couple living together, if one person’s taxable income is over £35,000 and the other’s is not, the higher earner’s share will be clawed back while the other may keep theirs.

3. What counts towards that £35,000 taxable income?

This is probably the trickiest part, so let’s break it down simply.

What does count (i.e. taxable income elements):

Your State Pension (because this is taxable income).

Interest on savings if it is taxable (e.g. outside an ISA) or dividends from investments (again depending on whether taxable).

Rental income or other taxable income streams.

What does not count:

Income from savings within an ISA (Individual Savings Account) is tax-free and does not count towards the £35,000 threshold.

Tax-free state benefits such as Pension Credit, Attendance Allowance or Personal Independence Payment.

The Winter Fuel Payment itself is tax-free and does not count as income for this threshold.

Capital gains (e.g. profits from sale of property or shares) are not included.

Premium Bond prizes

4. What to do next

Here are some practical pointers for you (or your friends/family):

Check your estimated taxable income for the year 2025/26. If you expect it to be under £35,000, you’re fine for this payment.

If your taxable income is likely to be over £35,000, you’ll still receive the payment (it’s too late now to opt out) but will be required to repay it via the tax system. In future years you might want to opt out of the payment, though many may still prefer to receive it and repay the money later.

If you have savings, consider whether holding them in tax-free vehicles (e.g. ISAs) can help reduce your taxable income, as interest received outside an ISA may count.

Make sure you are receiving any other benefits you may be entitled to (e.g. Pension Credit) — even though Winter Fuel Payment is partly means-tested now, those on very low income will often qualify for multiple sources of support.

Be alert to scams: you do not need to apply for this if you’re eligible, and the government will not ask you by text or email for bank details to “claim” this payment.

5. Quick recap

You are eligible if you reached State Pension age by the “qualifying week” (15–21 September 2025) and meet residence rules.

The payment is worth £200 (if all under 80 in the household) or £300 (if someone 80+) for winter 2025/26 in England & Wales.

Taxable income threshold: £35,000 per person. Under that → you keep it; over that → it will be clawed back.

Taxable income includes pensions, savings interest (outside ISAs), earnings, etc. Doesn’t include ISAs, Pension Credit, Attendance Allowance.

You don’t have to claim unless perhaps you haven’t received before; it’s automatic for most. Payments expected November/December 2025.

As always, if you have any comments or questions about this blog post, do leave them below. Please be aware that I am not a qualified financial adviser and under UK law cannot give personal financial advice.

If you enjoyed this post, please link to it on your own blog or social media:

For older people in particular, heating bills can be among their biggest expenses. And it’s especially important for older people to keep warm, as getting chilled can lower your body’s resistance to infection and – in the worst cases – lead to hypothermia.

In addition, as you doubtless know, gas and electricity bills have gone up considerably in the last year or two. Growing numbers of older people are literally finding themselves in a position where they have to choose between heating and eating 😮

So today I thought I’d set out some ways you may be able to save money on your heating and energy bills. Following these tips could save you hundreds of pounds in the months and years ahead.

Switch Energy Supplier

It’s important to check regularly whether you could save money by switching to a different supplier and/or tariff. The quick and easy way of doing this is via a price comparison website. There are a number of these available, including GoCompare and USwitch.

Just visit the comparison site and enter a few details, including your current supplier and tariff and how much you spend on gas and electricity in the course of a year (it doesn’t have to be exact). The site will then display the best deals currently open to you and how much you might be able to save by switching to them. In most cases you can also start the switching process by clicking on the relevant link. Before you do, though, it’s worth checking on cashback sites like Quidco and Top Cashback, as some energy companies pay cashback via these sites to people switching their supply to them.

If you are one of the 1.1 million households who use oil for heating, you can save money by shopping around for suppliers too. Check out the oil price comparison service BoilerJuice. Type in your postcode and how many litres of heating oil you’re looking to buy, and BoilerJuice will show you quotes from suppliers covering your area.

Switching energy suppliers is generally quick and easy, and can save you hundreds of pounds a year at a stroke. In these challenging times, it should be high on your list of potential money-saving strategies this winter.

Special Offer! If you switch to EDF Energy via my link, you can get a FREE £50 credited to your energy account. Terms and conditions apply. For more info, click on https://edfenergy.com/quote/refer-a-friend/sunny-koala-9462 [referral link].

Get Financial Help

If you’re in certain priority groups, you may be able to get cash payments to help offset your energy bills.

Winter Fuel Payment is a one-off annual payment of £100 to £300 which was previously made to everyone over state pension age. Last year the new Labour government took the decision to cancel WFP for all but the very poorest pensioners (those in receipt of pension credit). Such was the outcry that they had to back-track, so now everyone over state pension age will receive the payment this winter. The only catch is that if you earn more than £35,000 a year, you will be required to pay it back. See this article for more information.

In addition, those on certain welfare benefits (including Pension Credit, Income Support and Universal Credit) may be eligible for Cold Weather Payments. This is £25 for any period of seven consecutive days when temperatures fall below zero. More information can be found on this page of the government website.

You may also be eligible for £150 off your energy bill under the Warm Home Discount Scheme. This is run by some (not all) of the energy companies. If you get the Guaranteed Credit element of Pension Credit you will qualify automatically. But if you’re on a low income and meet the energy supplier’s other criteria, you may also qualify. Contact your supplier directly for more information. The large energy companies such as EDF and British Gas all operate this scheme, but some of the smaller ones don’t. The Warm Home DIscount scheme for 2025/26 opens at the end of October 2025. More information can be found on the official website.

Finally, if you’re on a very low income, you may qualify for help from the Household Support Fund: This is money provided to councils by the government to assist pensioners and others on very low incomes. You will need to contact your local council to find out if you’re eligible.

More Top Tips

Here are some more ways you may be able to save money on your heating and energy bills.

Have your boiler serviced regularly, to ensure it is operating at peak efficiency.

If you have an old boiler that keeps breaking down, the time may have come to replace it. The Energy Saving Trust say that you could save up to up to 40 percent on your gas bill by installing a new ‘A’ rated condensing boiler with a programmer, room thermostat and thermostatic radiator controls.

Upgrading your insulation can also cut bills by reducing the amount of heat going to waste. Depending on your circumstances, you may be able to get a free boiler and/or insulation under the government’s Energy Company Obligation (ECO) scheme. You can apply for this via your energy company. Even if you’re not on a low income, you may be able to get a discount on home insulation, so it’s worth checking to see what’s available.

If your radiators aren’t heating up properly at the top, you may need to bleed them to release air in the pipes. Depending on the radiator, you may need a special key to do this or a flat-bladed screwdriver.

Turn down your thermostat by one degree - this can reduce your heating bill by up to 10%.

Ensure you don’t put furniture right in front of radiators, as this can block heat from entering the room.

Replace old light-bulbs with new energy-saving bulbs. The latest LED bulbs are just as bright as old incandescent bulbs and use a tenth of the energy. They last longer too.

Exclude draughts with heavy curtains and draught excluders by doors.

Turn off heaters in rooms you aren’t using and close the doors to keep heat in.

Place reflective foil behind radiators on exterior walls to bounce heat back into the room.

It can also help to clean behind radiators (using a brush such as this one) to remove dust and dirt.

Don’t leave electrical appliances on standby.

Wash clothes at 30 degrees and try to avoid using tumble driers. Hang washing outside whenever possible or place it over an airer.

Consider investing in a smart thermostat system such as Nest or Hive. This will give you precise, automated control over your heating system, allowing you to use just as much energy as you need and no more. See my blog post about smart thermostats for more information.

If your funds are limited and you have or develop a disability you may be able to get a Disabled Facilities Grant (DFG) from your local authority to pay for adaptations such as stairlifts.

By taking these steps you should be able to cut your heating and energy bills significantly this winter.

If you have any comments or questions about this post, as always, please do leave them below.

This is a fully updated version of my original post on this subject.

If you enjoyed this post, please link to it on your own blog or social media:

We are currently heading into the peak season for flu and other respiratory viruses (including Covid). These infections can be a nuisance at least. And – in the case of older people especially – they can sometimes be life-threatening.

While a balanced diet, regular exercise and adequate sleep remain the cornerstones of good health, certain supplements can provide an extra layer of protection. Here’s a guide to the best supplements to support your immune system during the colder months.

1. Vitamin D

Why it’s essential: With limited sunlight during UK winters, many people experience a drop in their vitamin D levels. This nutrient plays a crucial role in immune function and helps reduce the risk of respiratory infections.

How to take it: Public Health England recommends everyone consider a daily supplement of 10 micrograms (400 IU) of vitamin D during the autumn and winter months. Higher doses may be necessary for those with deficiencies, but consult a healthcare professional first.

2. Vitamin C

Why it’s essential: Vitamin C is known for its immune-boosting properties and its ability to reduce the duration and severity of colds. It’s also a powerful antioxidant that helps protect cells from damage.

How to take it: A daily dose of 500–1,000 mg is generally safe for most people. You can also pair supplementation with dietary sources like oranges, kiwi fruit and bell peppers.

3. Zinc

Why it’s essential: Zinc is vital for immune cell function and has been shown to shorten the duration of cold symptoms when taken early. It also helps your body fight off viruses more effectively.

How to take it: Lozenges containing 10–15 mg of zinc can be taken at the onset of a cold. Long-term supplementation should not exceed 25 mg daily unless advised by a healthcare professional.

4. Probiotics

Why it’s essential: A healthy gut microbiome supports immune function, and probiotics help maintain this balance. Some strains, like Lactobacillus and Bifidobacterium, are particularly effective in reducing the risk of upper respiratory tract infections.

How to take it: Look for a high-quality probiotic supplement with at least 1 billion CFUs (colony-forming units). Yogurt and fermented foods like kimchi and sauerkraut can also be excellent natural sources.

5. Elderberry Extract

Why it’s essential: Elderberries have been traditionally used to fight colds and flu. They are rich in antioxidants and may reduce the severity and duration of symptoms.

How to take it: Elderberry syrup or capsules are common forms. Follow the recommended dosage on the product label, and avoid taking it if you have an autoimmune condition without consulting a doctor.

6. Echinacea

Why it’s essential: Echinacea is a popular herbal remedy that may help prevent and reduce the severity of colds by boosting immune activity.

How to take it: Look for standardised extracts and follow the manufacturer’s dosage guidelines. Echinacea is best taken at the first sign of illness.

7. Omega-3 Fatty Acids

Why it’s essential: Omega-3s, particularly EPA and DHA found in fish oil, have anti-inflammatory properties that support immune function and overall health.

How to take it: Aim for 250–500 mg of combined EPA and DHA daily. Vegetarian or vegan options include algae-based supplements.

8. Garlic Supplements

Why it’s essential: Garlic contains allicin, a compound with antimicrobial and immune-boosting properties. Regular garlic intake has been associated with fewer colds and flu.

How to take it: Opt for aged garlic extract supplements or incorporate fresh garlic into your diet for the best benefits.

Final Tips

Consult a GP or pharmacist: Always check with a healthcare professional before starting new supplements, especially if you’re pregnant, nursing or on medication.

Choose quality brands: Look for products that are third-party tested for purity and potency. A wide range of supplements and vitamins is available from Amazon.

Maintain healthy habits: Supplements work best when combined with a balanced diet, regular exercise, good hygiene and adequate sleep.

By supporting your immune system with the right supplements, you can give yourself a better chance of staying healthy this cold and flu season.

This is a revised update of an annual post.

If you enjoyed this post, please link to it on your own blog or social media:

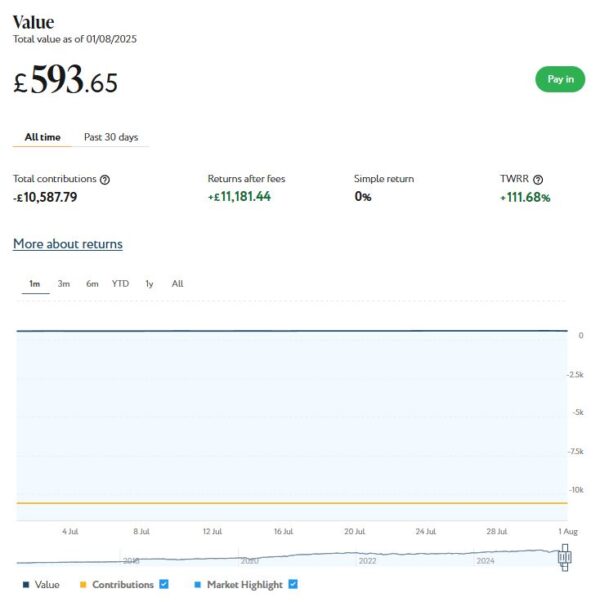

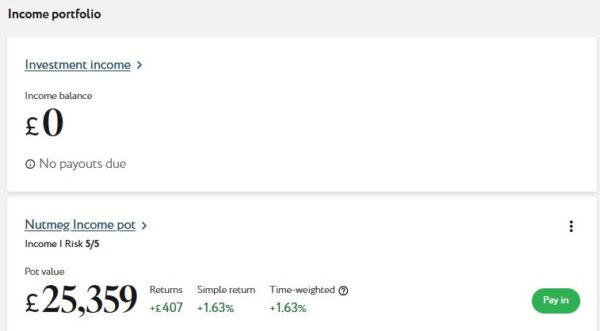

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

As regular readers will know, in June I transferred most of the money in my Nutmeg Fully Managed portfolio (just under £25,000) to a new Nutmeg Income Portfolio. I discussed this in detail in this recent post, but basically money in this port is invested to generate an income from share dividends and other sources. This is then paid monthly. Capital appreciation is targeted as well, but these portfolios are aimed primarily at older people (and others) who want/need their investment to generate a regular cash income.

In September my Nutmeg income portfolio generated £78.72 of income, which was duly paid in to my bank account on 24 September 2025. That is down a bit on the £134.03 I received in August, but it means I have now received a total (tax-free) income of £212.75 to date. That is in line with Nutmeg’s projected annual return of just under 5% for income ports at my chosen risk level (five). Obviously it is too early to draw any significant conclusions from this, though.

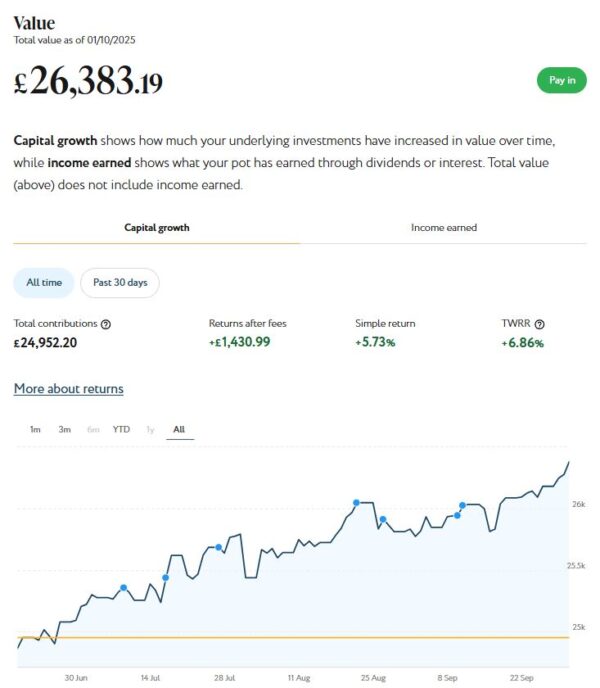

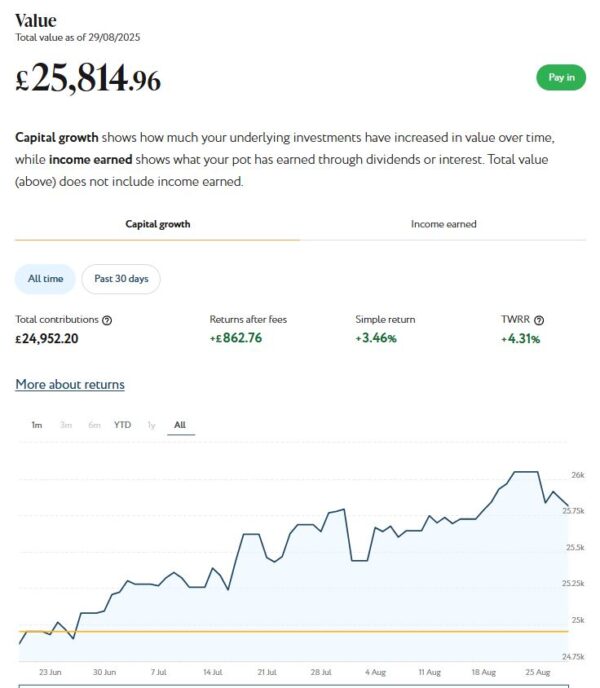

My income portfolio also grew in value in September. It’s now worth £26,383 compared with £25,815 at the start of last month, a rise of £568. As the screen capture shows, the port has actually increased by £1,430.99 (5.73%) since I opened it in June. That’s good going, though I don’t suppose it will carry on like this indefinitely!

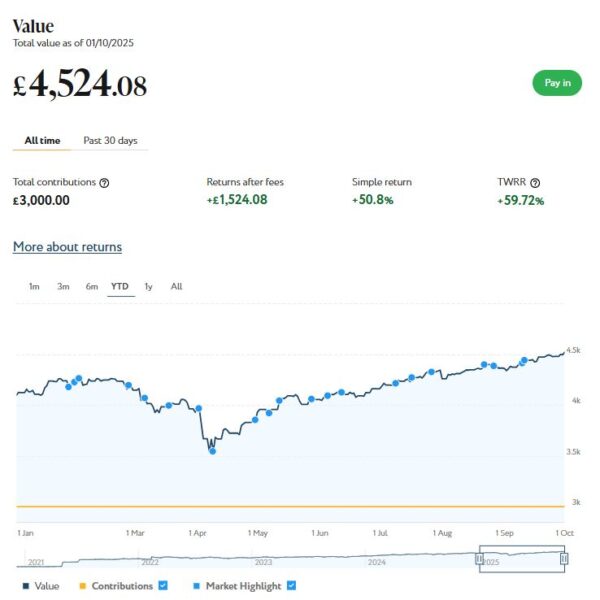

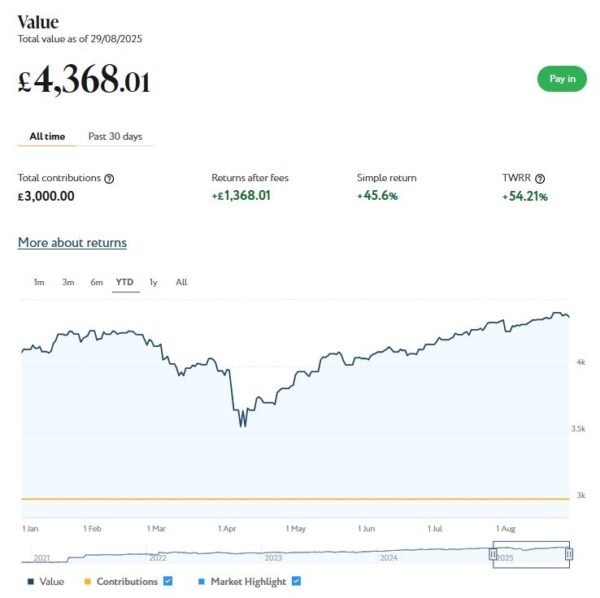

I still have a smaller, growth-oriented pot using Nutmeg’s Smart Alpha option. This is now worth £4,524 compared with £4,368 a month ago, a rise of £156. Here is a screen capture showing performance for the year to date.

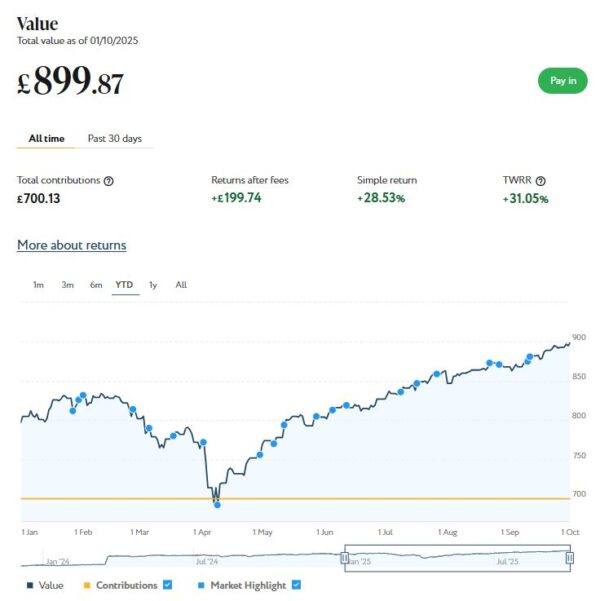

And at the start of December 2023 I invested £500 in one of Nutmeg’s thematic portfolios (Resource Transformation). In March 2024 I also invested a further £200 from referral bonuses (something I no longer receive for reasons I won’t bore you with). As you can see from the YTD screen capture below, this portfolio is now worth £900 (rounded up) compared with £868 last month, a rise of £32.

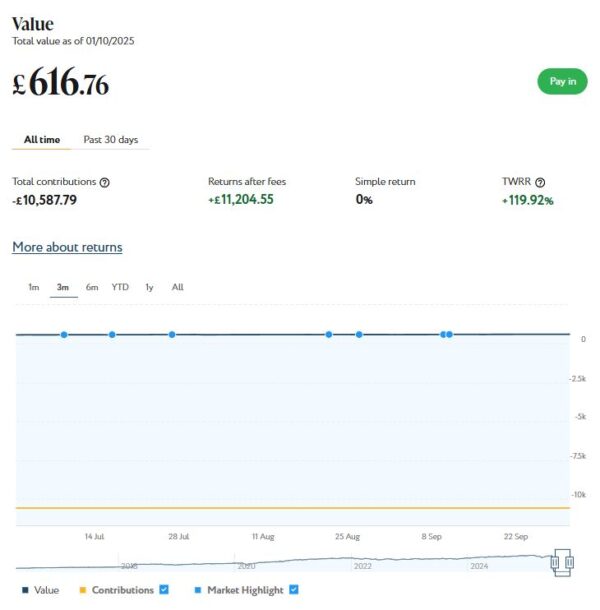

Finally, I still have a small amount left in my original Nutmeg Fully Managed portfolio. I have kept this largely for comparison purposes. This has increased in value from £595 at the start of September to £617 (rounded up) now, a rise of £22.

As you can see, September was a pretty good month for my Nutmeg investments. Overall I was up by £778 or 2.46%. In addition I did, of course, receive £78.72 in income from my income portfolio.

Excluding income generated, the overall value of my Nutmeg investments is up by £1,996 since the start of 2025, so the April 2025 fall (caused largely by Trump’s tariffs) has now fully reversed. I am also up by £3,069 or 10.45% since the start of October last year, again excluding cash income received. All things considered, that’s not a bad result.

As I always have to say, some volatility is to be expected with stock market investments, but over the longer term they tend to even themselves out (and generally perform better than bank savings accounts, although that is never guaranteed). In general the worst thing you can do is panic and sell up when downturns occur (as happened in April this year). You are then crystallizing your losses rather than giving the markets time to recover. This is something I had cause to discuss in this blog post from earlier this year.

You can read my full Nutmeg review here. If you are looking for a home for your annual ISA allowance, based on my overall experience over the last nine years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs), Lifetime ISAs and Junior ISAs as well.

Moving on, I also have investments with P2P property investment platform Assetz Exchange. As discussed in this post, the company has rebranded as Housemartin.

My investments with Housemartin continue to generate steady returns. Housemartin focuses on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my HM portfolio has generated a respectable £273.80 in revenue from rental income. I have made a small net loss of £19.02 on property disposals. Capital growth generally has slowed, in line with UK property values generally.

At the time of writing, 16 of ‘my’ properties are showing gains, 7 are breaking even, and the remaining 17 are showing losses. My portfolio of 40 properties is currently showing a net decrease in value of £43.52. That means that overall (rental income minus capital value decrease and loss on disposal) I am up by £211.26. That’s still a respectable return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Housemartin most projects are socially beneficial as well.

The net fall in capital value of my Housemartin investments is obviously a little disappointing. But it’s important to remember that until/unless I choose to sell the investments in question, it is largely theoretical, based on the latest price at which shares in the property concerned have changed hands. The rental income, on the other hand, is real money (which in my case I’ve reinvested in other HM projects to further diversify my portfolio).

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of Housemartin as far as i am concerned. You can actually invest from as little as £1 per property if you really want to proceed cautiously.

As I noted in this blog post, Housemartin is particularly good if you want to compound your returns by reinvesting rental income. This effectively boosts the interest rate you are receiving. Personally, once I have accrued a minimum of £10 in rental payments, I usually reinvest this money in either a new HM project or one I have already invested in (thus increasing my holding). Over time, even if I don’t invest any more capital, this will ensure my investment with Housemartin grows at an accelerating rate and becomes more diversified as well.

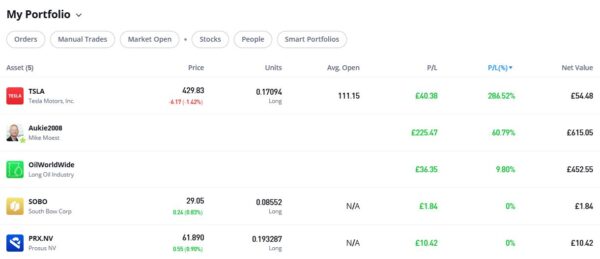

In 2022 I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios, Oil Worldwide. I also invested a small amount I had left over in Tesla shares.

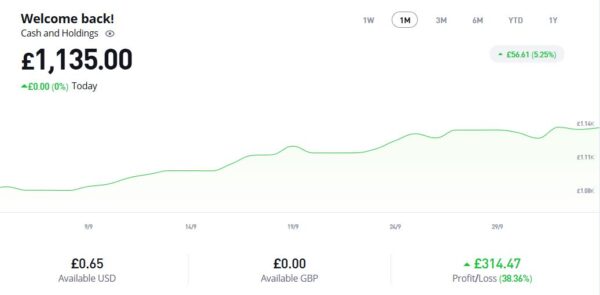

As you can see from the screen captures below, my original investment (total value £888.36 in pounds sterling) is today worth £1,135.00 an overall increase of £246.64 or 27.76%.

Note: eToro now displays the value of investments in your native currency, although you can change this if you wish.

As you can see, my Oil WorldWide investment is in profit, though at 9.80% it is nothing too exciting. My copy trading investment with Aukie2008 has been doing better, with an overall 60.79% profit. To be fair, I have held this investment a bit longer.

My Tesla shares, which I bought as an afterthought with some spare cash I had in my account, are up again this month. They are showing an impressive overall profit of 286.52% since I bought them. If only I had put a bit more money into this!

You might also notice that I have small holdings in Prosus NV, a Dutch internet group, and South Bow, a Canadian energy infrastructure company. To be honest I don’t understand how I acquired these, but I assume they are some sort of bonus I was awarded. In any event, I am happy to have them in my portfolio.

eToro also offer the free eToro Money app. This allows you to deposit money to your eToro account without paying any currency conversion fees, saving you up to £5 for every £1,000 you deposit. You can also use the app to withdraw funds from your eToro account instantly to your bank account. I tried this myself and was impressed with how quickly and seamlessly it worked. You can read my blog post about eToro Money here. Note that it can also serve as a cryptocurrency wallet, allowing you to send and receive crypto from any other wallet address in the world.

If you would like more information about setting up an eToro account, please click on this no-obligation website link [affiliate]. Don’t forget that you also get a free $100,000 virtual portfolio, which you can use to experiment with trading and investing strategies. I have certainly earned a lot from mine.

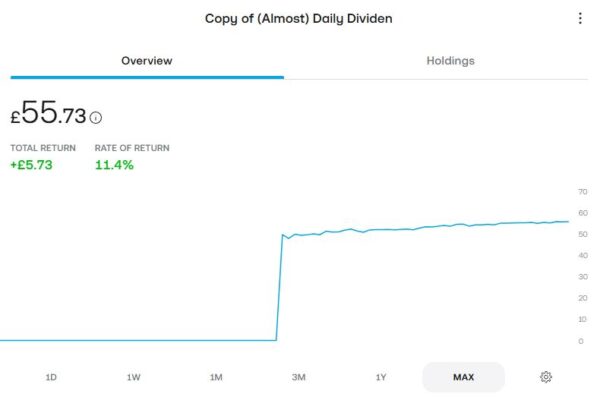

As an experiment, at the start of April this year I put £50 into an investment ISA with Trading 212. As mentioned in my recent blog post about dividend investing, I put it into the (Almost) Daily Dividends Portfolio, a ready-made portfolio or ‘pie’ on Trading 212. As you can see from the screen capture below, my portfolio is now worth £55.73, an increase of £5.73 or 11.4% over the six-month period. It has even accrued a grand total of 50p in dividends!

I am quite impressed with how this investment has been faring, despite the small amount I put in (which means I may be missing out on some smaller dividends). If I increased my investment I would almost certainly become eligible for more dividends, and even more the longer I remain invested. If I had any spare money at the moment, I would consider doing this. Of course, I do now have an income-focused portfolio with Nutmeg as well (see above).

Moving on, I published various posts on Pounds and Sense in September. I have listed below those that are still relevant.

In Get a Free Share Worth Up To £100 With Trading 212, I revealed that this popular offer had reopened. If you have never held an account with Trading 212, you can get a free share worth up to £100 just by signing up with them. You do have to open a Stocks ISA or (non-ISA) Invest account – a Cash ISA won’t qualify you for the free share. This offer is still open but it closes on Monday 6 October 2025 – so if you want to take advantage, you need to get your skates on now.

In Get Your Will Written Free of Charge in October, I pointed out that October is Free Wills Month. This event brings together a group of well-respected charities to offer members of the public aged 55 and over the opportunity to have their wills written or updated free of charge using participating solicitors across the UK. Free Wills Month is now up and running, so see my blog post to find out how you can benefit.

And in Amazon Prime Big Deals Day Is Almost Here I spotlighted the fact that this annual promotional event begins on Tuesday 7 October 2025. This is a special event for Amazon Prime members only. Amazon say they will be offering members their lowest prices of the year on selected products across a wide range of categories, from consumer electronics to groceries. Personally I shall be looking for a new electric shaver this time 🙂

Finally, How Often Should You Really Be Washing Your Bedding? is a syndicated guest post by professional microbiologist Primrose Freestone. Dr Freestone looks at everything from sheets and pillowcases to blankets and duvet covers and even mattresses. Personally I found her expert advice quite eye-opening. I definitely need to do better in future!

I’ll close with a reminder that you can also follow Pounds and Sense on Facebook or Twitter (or X as we have to call it now). Twitter/X is my number one social media platform and I post regularly there. I share the latest news and information on financial matters, and other things that interest, amuse or concern me. So if you aren’t following my PAS account on Twitter/X, you are definitely missing out!

I am also on the BlueSky social media network under the username poundsandsense.bsky.social. Twitter/X remains my primary social media platform, but I also post details of my latest blog posts, third-party articles and other financial news and resources on BlueSky for those who prefer to follow me there.

As always, if you have any comments or questions, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts on PAS may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media:

In case you’ve not heard, Amazon Prime Big Deals Day is almost with us. It extends over two days, Tuesday 7th and Wednesday 8th October 2025.

This is a special event for Amazon Prime members only. Amazon say they will be offering members their lowest prices of the year on selected products across a wide range of categories, from consumer electronics to groceries.

Some of the best deals will be reserved for Amazon’s own products, such as their Kindle e-book readers, Amazon Echo smart speakers and Ring video doorbells and security cameras. Discounts of up to 60% will be on offer for these products. If you’re thinking of buying any of them, Amazon Prime Big Deals Day is definitely the day – or two days – to do it.

There are also some great ‘early deals’ available now. For example, at the time of writing you can buy an Oral-B iO2 electric toothbrush for just £41.99, a 58% discount on the normal price of £100.

I have been a member of Amazon Prime for over ten years now. As a regular Amazon shopper, I find it well worth while for the free one-day delivery on millions of items alone. But as a Prime member you get access to a host of other benefits and services as well, including Amazon Prime Music and Amazon Prime Video.

If you’re thinking of joining Amazon Prime, therefore, I highly recommend doing it in the next few days, so you can benefit from the Prime Big Deals Day offers. Personally I think it’s worth it for the free delivery alone, let alone everything else that’s on offer. But if you wish, you can get a 30-day free trial now, take advantage of the Prime Big Deals Day offers, and then cancel without owing any money. It’s your choice!

You can also see all the latest Prime Big Deals Day offers by clicking here.

As always, if you have any comments about Amazon Prime or Prime Big Deals Day, please do post them below.

Disclosure: This post includes affiliate links. If you click through and make a purchase, I may receive a commission for introducing you. This will not affect the price you pay or the products or services you receive.

If you enjoyed this post, please link to it on your own blog or social media:

Free Wills Month brings together a group of well-respected charities to offer members of the public aged 55 and over the opportunity to have their wills written or updated free using participating solicitors across the UK.

The charities involved include the NSPCC, Dogs Trust, Samaritans, Mind, Age UK, The Stroke Association, PDSA, and many others. Free Wills Month happens twice a year, in March and October.

The scheme covers simple wills only, including ‘mirror wills’ for couples. In the latter case, only one member of the couple has to be 55 or over. If you need a complicated will (most people don’t) you can still have this done but may have to pay a top-up fee.

I have talked about the importance of creating a will and why you should get it done by a properly qualified solicitor previously on PAS. An up-to-date will written by a solicitor will ensure that your wishes are respected and will avoid causing legal complications for your loved ones after you are gone.

Free Wills Month means what it says. There are no catches, although the organizers hope that you will choose to leave a donation to charity in your will. There is no obligation to do this, however.

To take part in Free Wills Month click through to the website during October and fill in your details. You can then pick a solicitor from the list of companies taking part and contact them to book an appointment. Appointments are limited and on a first come, first served basis, so it’s best to apply as soon as possible to avoid disappointment.

Free Wills Month October 2025 starts officially on Wednesday 1st October 2025 but you can sign up on the FWM website to be notified when when the campaign starts in your area.

If you have any comments or questions about this subject, as ever, please do post them below.

Note: This is a revised and updated version of my original post on this subject.

If you enjoyed this post, please link to it on your own blog or social media:

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

As regular readers will know, in June I transferred most of the money in my Nutmeg Fully Managed portfolio (just under £25,000) to a new Nutmeg Income Portfolio. I discussed this in detail in this recent post, but basically money in this port is invested to generate an income from share dividends and other sources. This is then paid monthly. Capital appreciation is targeted as well, but these portfolios are aimed primarily at older people (and others) who want/need their investment to generate a regular cash income.

In August my Nutmeg income portfolio generated £134.03 of income, which was duly paid in to my bank account on 22 August 2025. Based on Nutmeg’s estimated annual return of just under 5% for income ports at my chosen risk level (five), I had been expecting around £100, so this was somewhat better than that. Obviously it is far too early to draw any conclusions, though.

My income portfolio has also grown a little in value in August. It’s now worth £25,815 compared with £25,793 at the start of last month, an increase of £22. As the screen capture shows, the port has actually grown in value by £862.76 (3.46%) since I opened it.

I still have a smaller, growth-oriented pot using Nutmeg’s Smart Alpha option. This is now worth £4,368 compared with £4,346 a month ago, a rise of £22. Here is a screen capture showing performance for the year to date.

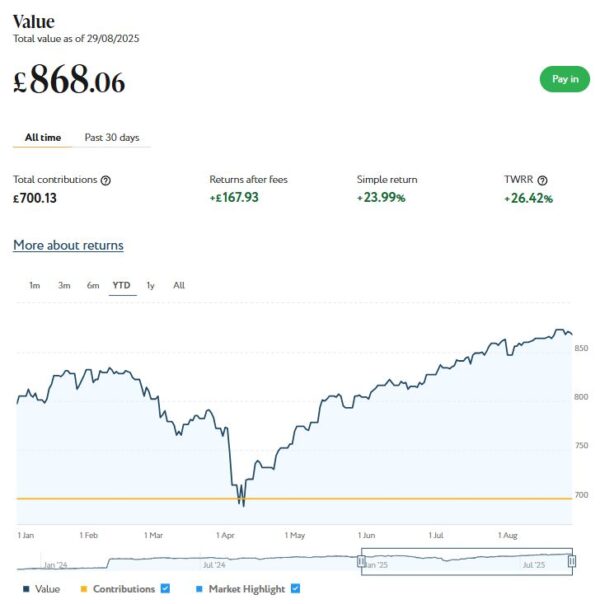

And at the start of December 2023 I invested £500 in one of Nutmeg’s thematic portfolios (Resource Transformation). In March 2024 I also invested a further £200 from referral bonuses (something I no longer receive for reasons I won’t bore you with). As you can see from the YTD screen capture below, this portfolio is now worth £868 compared with £863 last month, a rise of £5.

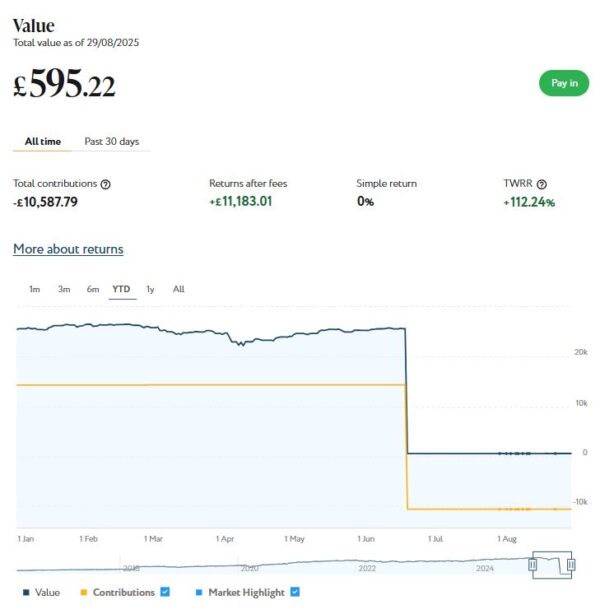

Finally, I still have a small amount left in my original Nutmeg Fully Managed portfolio. I have kept this largely for comparison purposes. This has increased in value from £594 at the start of August to £595 now, a rise of £1.

As you can see, August was a steady, if unexciting, month for my Nutmeg investments. Overall I was up by £50 or 0.16%. In addition I did, of course, receive £134.03 in income from my income portfolio.

Excluding income generated, the overall value of my Nutmeg investments is up by £1,218 since the start of 2025, so the April 2025 fall (caused largely by Trump’s tariffs) has now fully reversed. I am also up by £2,413 or 7.48% since the start of September last year, again excluding cash income received. All things considered, that’s not a bad result.

As I always have to say, some volatility is to be expected with stock market investments, but over the longer term they tend to even themselves out (and generally perform better than bank savings accounts, although that is never guaranteed). In general the worst thing you can do is panic and sell up when downturns occur (as happened in April this year). You are then crystallizing your losses rather than giving the markets time to recover. This is something I had cause to discuss in this blog post from earlier this year.

You can read my full Nutmeg review here. If you are looking for a home for your annual ISA allowance, based on my overall experience over the last nine years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs), Lifetime ISAs and Junior ISAs as well.

Moving on, I also have investments with P2P property investment platform Assetz Exchange. As discussed in this post, the company has rebranded as Housemartin.

My investments with Housemartin continue to generate steady returns. Housemartin focuses on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my HM portfolio has generated a respectable £266.87 in revenue from rental income. I have made a small net loss of £19.02 on property disposals. Capital growth generally has slowed, in line with UK property values generally.

At the time of writing, 16 of ‘my’ properties are showing gains, 3 are breaking even, and the remaining 19 are showing losses. My portfolio of 38 properties is currently showing a net decrease in value of £59.59. That means that overall (rental income minus capital value decrease and loss on disposal) I am up by £188.26. That’s still a respectable return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Housemartin most projects are socially beneficial as well.

The net fall in capital value of my Housemartin investments is obviously a little disappointing. But it’s important to remember that until/unless I choose to sell the investments in question, it is largely theoretical, based on the latest price at which shares in the property concerned have changed hands. The rental income, on the other hand, is real money (which in my case I’ve reinvested in other HM projects to further diversify my portfolio).

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of Housemartin as far as i am concerned. You can actually invest from as little as £1 per property if you really want to proceed cautiously.

As I noted in this blog post, Housemartin is particularly good if you want to compound your returns by reinvesting rental income. This effectively boosts the interest rate you are receiving. Personally, once I have accrued a minimum of £10 in rental payments, I usually reinvest this money in either a new HM project or one I have already invested in (thus increasing my holding). Over time, even if I don’t invest any more capital, this will ensure my investment with Housemartin grows at an accelerating rate and becomes more diversified as well.

In 2022 I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios, Oil Worldwide. I also invested a small amount I had left over in Tesla shares.

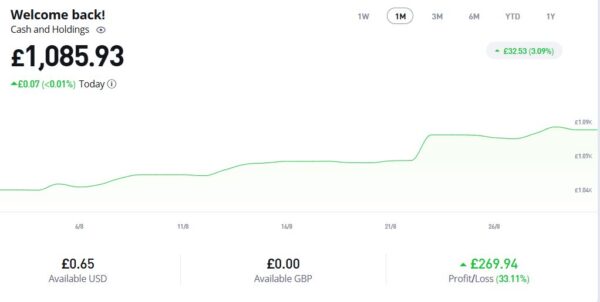

As you can see from the screen captures below, my original investment (total value £888.36 in pounds sterling) is today worth £1,085.93, an overall increase of £197.57 or 22.24%.

Note: eToro now displays the value of investments in your native currency, although you can change this if you wish.

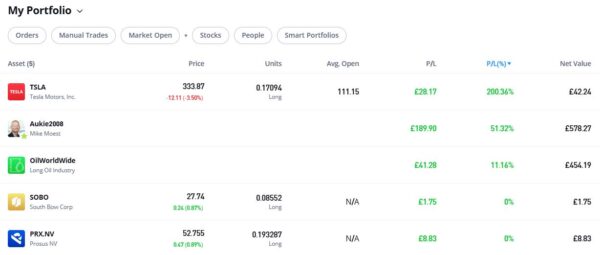

As you can see, my Oil WorldWide investment is in profit, though at 11.14% it is nothing too exciting. My copy trading investment with Aukie2008 has been doing better, with an overall 51.32% profit. To be fair, I have held this investment a bit longer.

My Tesla shares, which I bought as an afterthought with some spare cash I had in my account, are up again this month. They are showing an impressive overall profit of 200.36% since I bought them. If only I had put a bit more money into this!

You might also notice that I have small holdings in Prosus NV, a Dutch internet group, and South Bow, a Canadian energy infrastructure company. To be honest I don’t understand how I acquired these, but I assume they are some sort of bonus I was awarded. In any event, I am happy to have them in my portfolio.

eToro also offer the free eToro Money app. This allows you to deposit money to your eToro account without paying any currency conversion fees, saving you up to £5 for every £1,000 you deposit. You can also use the app to withdraw funds from your eToro account instantly to your bank account. I tried this myself and was impressed with how quickly and seamlessly it worked. You can read my blog post about eToro Money here. Note that it can also serve as a cryptocurrency wallet, allowing you to send and receive crypto from any other wallet address in the world.

If you would like more information about setting up an eToro account, please click on this no-obligation website link [affiliate]. Don’t forget that you also get a free $100,000 virtual portfolio, which you can use to experiment with trading and investing strategies. I have certainly earned a lot from mine.

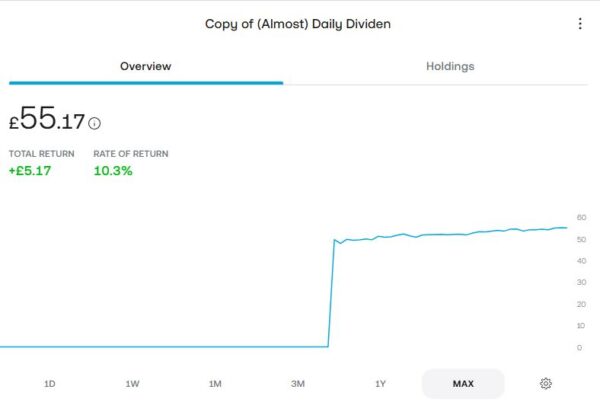

As an experiment, I recently put £50 into an investment ISA with Trading 212. As mentioned in my recent blog post about dividend investing, I put it into the (Almost) Daily Dividends Portfolio, a ready-made portfolio or ‘pie’ on Trading 212. As you can see from the screen capture below, my portfolio is now worth £55.17, an increase of £5.17 or 10.3% over the four-month period. It has even accrued a grand total of 38p in dividends!

I am quite impressed with how this investment has been faring, despite the small amount I put in (which means I may be missing out on some smaller dividends). If I increased my investment I would almost certainly become eligible for more dividends, and even more the longer I remain invested. If I had any spare money at the moment, I would consider doing this. Of course, I do now have an income-focused portfolio with Nutmeg as well (see above).

Moving on, I published various posts on Pounds and Sense in August. I have listed below those that are still relevant.

In Here’s Why I’m Not a Fan of FIRE I talked about the Financial Independence, Retire Early (FIRE) movement and explained why I am not an aficionado. I set out various reasons, including the impossibility of planning and predicting your life twenty or thirty years into the future.

In Could a Smart Thermostat Save You Money? I explained what these devices are and set out some hints and tips for making the most of them. I also discussed my own experience with a Hive smart thermostat.

In How to Check Your Tax Code and Correct it if Necessary I explained how to check this important piece of financial data. I revealed what the code means and what you should do if you believe yours is wrong. In my view everyone should check their tax code, as if it’s incorrect you may be paying too much tax or, conversely, too little. In the latter case you will still have to pay the tax when the error is discovered, potentially with added interest as well.

How Over-50s Can Save and Make Money Using Vinted discusses this very popular buying-and-selling platform among younger people. In the article I point out that Vinted can be an invaluable resource for older folk as well. I explain how it works and set out some hints and tips for making the most of it.

Finally, in Dividend Investing vs Total Return: Which Works Best for Income Investors? I look at these two popular approaches to drawing an income from your investments. Of course, this is something many retired and semi-retired people want (or need) to do. I compare the pros and cons of each method and discuss my personal experience.

I’ll close with a reminder that you can also follow Pounds and Sense on Facebook or Twitter (or X as we have to call it now). Twitter/X is my number one social media platform and I post regularly there. I share the latest news and information on financial matters, and other things that interest, amuse or concern me. So if you aren’t following my PAS account on Twitter/X, you are definitely missing out!

I am also on the BlueSky social media network under the username poundsandsense.bsky.social. Twitter/X remains my primary social media platform, but I also post details of my latest blog posts, third-party articles and other financial news and resources on BlueSky for those who prefer to follow me there.

As always, if you have any comments or questions, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts on PAS may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media:

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

As regular readers will know, in June I transferred most of the money in my Nutmeg Fully Managed portfolio (just under £25,000) to a new Nutmeg Income Portfolio. I discussed this in detail in this recent post, but basically money in this port is invested to generate an income from dividends and other sources. This is then paid monthly. Capital appreciation is targeted as well, but basically these portfolios are aimed at older people (and others) who want/need their investment to generate a regular cash income.

My Income portfolio hasn’t yet generated any income for me. I assume that is because there is a qualifying period before you become eligible to receive dividends (I have asked Nutmeg for clarification about this and am awaiting an answer). Income is due to be paid in cash to my bank account on the 24th of each month, so hopefully I will have some income accrued by August 24th (check out next month’s Update to find out!).

Nutmeg have now confirmed I was basically correct above. They point out that – like all Nutmeg investments – the money in income portfolios is held in the form of ETFs (exchange traded funds). They say: ‘Usually for an ETF to pay a dividend, it is one month after it is recorded. Taking the example of the JP Morgan Global Equity Premium ETF, [a dividend] was declared and recorded in early July and will be paid in August.” It would therefore appear that you have to be invested for between one and two months to start receiving monthly payouts. Nutmeg say I can expect to receive my first income payout on August 24th, so I will await this with interest 🙂

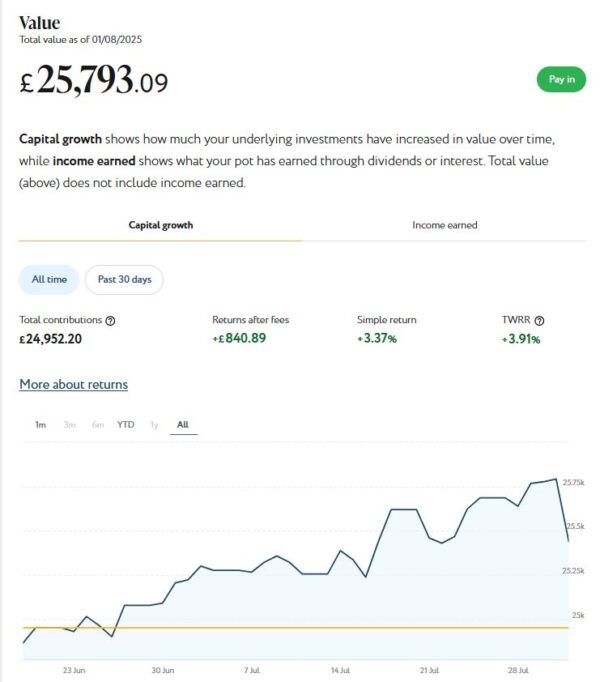

The better news is that this portfolio has grown in value in July. It’s now worth £25,793 compared with £25,092 at the start of last month, an increase of £701 or 2.79%. As the screen capture shows, this portfolio has actually grown in value by £840.89 since I opened it.

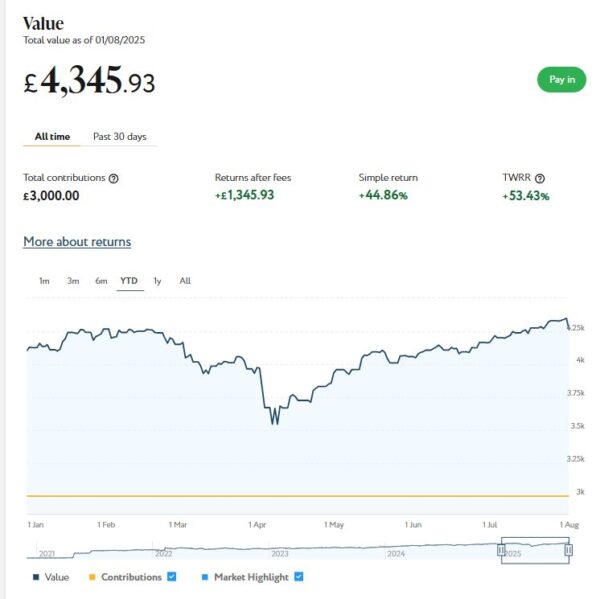

I still have a smaller, growth-oriented pot using Nutmeg’s Smart Alpha option. This is now worth £4,346 (rounded up) compared with £4,164 a month ago, a rise of £182. Here is a screen capture showing performance for the year to date.

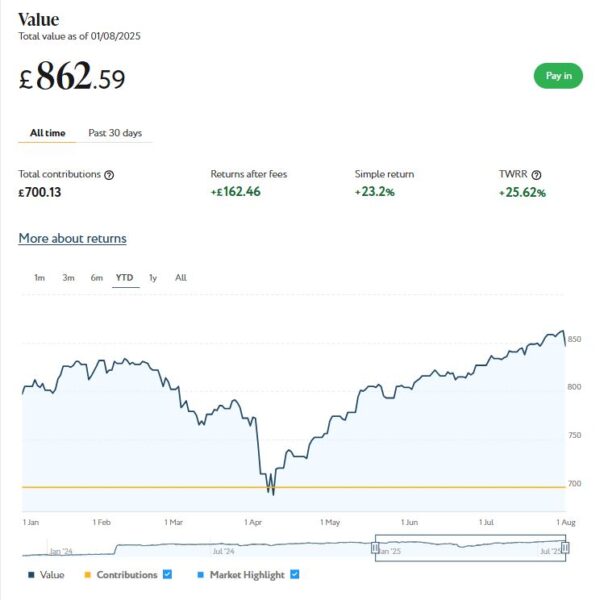

And at the start of December 2023 I invested £500 in one of Nutmeg’s thematic portfolios (Resource Transformation). In March 2024 I also invested a further £200 from referral bonuses. As you can see from the YTD screen capture below, this portfolio is now worth £863 (rounded up) compared with £827 last month, a rise of £36.

Finally, I still have a small amount left in my original Nutmeg Fully Managed portfolio. I have kept this largely for comparison purposes. This has increased from £581 at the start of July to £594 (rounded up) now, an increase of £13.

As you can see, July was a good month for my Nutmeg investments. Overall I was up by £932 or 2.69%.

I am up by £1,168 since the start of 2025, so the April 2025 fall (caused largely by Trump’s tariffs) has now fully reversed. I am also up by £2,583 or 8.90% since the start of August last year. All things considered, that’s not a bad result.

As I always have to say, some volatility is to be expected with stock market investments, but over the longer term they tend to even themselves out (and generally perform better than bank savings accounts, although that is never guaranteed). In general the worst thing you can do is panic and sell up when downturns occur (as happened in April). You are then crystallizing your losses rather than giving the markets time to recover. This is something I had cause to discuss recently in this blog post.

You can read my full Nutmeg review here. If you are looking for a home for your annual ISA allowance, based on my overall experience over the last eight years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs), Lifetime ISAs and Junior ISAs as well.

My investments with Housemartin continue to generate steady returns. Housemartin focuses on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my HM portfolio has generated a respectable £262.48 in revenue from rental income. I have made a small net loss of £0.71 on property disposals. Capital growth generally has slowed, in line with UK property values generally.

At the time of writing, 16 of ‘my’ properties are showing gains, 2 are breaking even, and the remaining 19 are showing losses. My portfolio of 37 properties is currently showing a net decrease in value of £60.06. That means that overall (rental income minus capital value decrease and loss on disposal) I am up by £201.71. That’s still a decent return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Housemartin most projects are socially beneficial as well.

The net fall in capital value of my Housemartin investments is obviously a little disappointing. But it’s important to remember that until/unless I choose to sell the investments in question, it is largely theoretical, based on the latest price at which shares in the property concerned have changed hands. The rental income, on the other hand, is real money (which in my case I’ve reinvested in other HM projects to further diversify my portfolio).

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of Housemartin as far as i am concerned. You can actually invest from as little as £1 per property if you really want to proceed cautiously.

As I noted in this blog post, Housemartin is particularly good if you want to compound your returns by reinvesting rental income. This effectively boosts the interest rate you are receiving. Personally, once I have accrued a minimum of £10 in rental payments, I usually reinvest this money in either a new HM project or one I have already invested in (thus increasing my holding). Over time, even if I don’t invest any more capital, this will ensure my investment with Housemartin grows at an accelerating rate and becomes more diversified as well. I did, however, withdraw £50 from my earnings in June to assist my cashflow in what was an expensive month for me

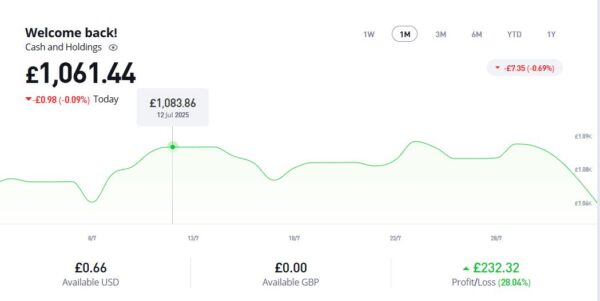

In 2022 I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios, Oil Worldwide. I also invested a small amount I had left over in Tesla shares.

As you can see from the screen captures below, my original investment (total value £888.36 in pounds sterling) is today worth £1,061.44, an overall increase of £173.08 or 19.48%.

Note: eToro now displays the value of investments in your native currency, although you can change this if you wish.

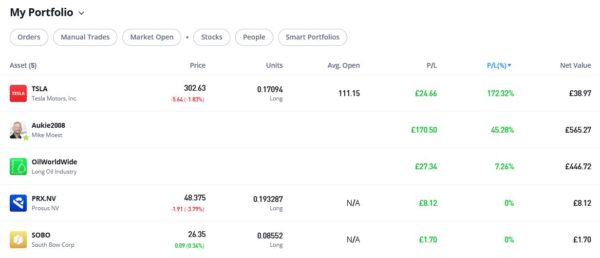

As you can see, my Oil WorldWide investment is in profit, though at 7.26% it is nothing to write home about. My copy trading investment with Aukie2008 has been doing a lot better, with an overall 45.28% profit. To be fair, I have held this investment a bit longer.

My Tesla shares, which I bought as an afterthought with some spare cash I had in my account, are down a little this month. But they are still showing an overall profit of 172.32% since I bought them. If only I had put a bit more money into this!

You might also notice that I have small holdings in Prosus NV, a Dutch internet group, and South Bow, a Canadian energy infrastructure company. To be honest I don’t understand how I acquired these, but I assume they are some sort of bonus I was awarded. In any event, I am happy to have them in my portfolio!

eToro also offer the free eToro Money app. This allows you to deposit money to your eToro account without paying any currency conversion fees, saving you up to £5 for every £1,000 you deposit. You can also use the app to withdraw funds from your eToro account instantly to your bank account. I tried this myself and was impressed with how quickly and seamlessly it worked. You can read my blog post about eToro Money here. Note that it can also serve as a cryptocurrency wallet, allowing you to send and receive crypto from any other wallet address in the world.

If you would like more information about setting up an eToro account, please click on this no-obligation website link [affiliate]. Don’t forget that you also get a free $100,000 virtual portfolio, which you can use to experiment with trading and investing strategies. I have certainly earned a lot from mine.

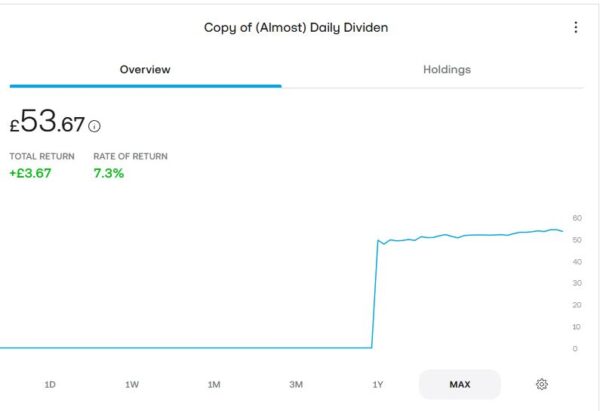

As an experiment, I recently put £50 into an investment ISA with Trading 212. As mentioned in my recent blog post about dividend investing, I put it into the (Almost) Daily Dividends Portfolio, a ready-made portfolio or ‘pie’ on Trading 212. As you can see from the screen capture below, my portfolio is now worth £53.67, an increase of £3.67 or 7.3% over the four-month period. It has even accrued a grand total of 31p in dividends (which is still more than I’ve had from my Nutmeg income port so far!).

I am quite impressed with how this investment has been faring, despite the small amount I put in (which means I may be missing out on some smaller dividends). If I increased my investment I would almost certainly become eligible for more dividends, and even more the longer I remain invested. If I had any spare money at the moment, I would consider doing this. Of course, I do now have an income-focused portfolio with Nutmeg as well (see above).

Moving on, I published various posts on Pounds and Sense in July. I have listed below those that are still relevant.

As mentioned above, in Nutmeg Launches New Income Investing Portfolios I discussed this new option from robo-adviser platform Nutmeg (with whom I am a long-term investor myself). I revealed how the new income investing portfolios work, and revealed why I decided to switch a substantial portion of my Nutmeg investments into one.

How to Tow a Caravan With an Electric Car in the UK covers a subject relevant to growing numbers of motorists. With over 1.5 million EVs now on UK roads – and staycations more popular than ever – more people are pairing their electric cars with touring caravans. But while the idea is appealing, towing with an EV requires careful planning, especially when it comes to battery range and charging stops. I am grateful to my my friends at specialist caravan insurers Compass Insurance and European EV charging infrastructure company Fastned for their expert tips and information.

In How to Invest in Gold in the UK I looked at another subject attracting growing attention. Gold is shiny, timeless, and often seen as a financial “safe haven” – especially when inflation is rising or the stock market is shaky. The growing popularity of gold among investors in recent months is testimony to this. In this post, I covered the pros and cons of investing in gold, the main ways to invest (even if you’re a beginner), and how to get started easily in the UK

Finally, in Is Private Health Insurance Worthwhile for Over-50s? I looked at the pros and cons of private medical insurance (PMI) for older people, and set out some key questions to help decide whether it makes financial sense for you. The article also discusses health cash plans, a less costly alternative that may be more suitable for some.

I’ll close with a reminder that you can also follow Pounds and Sense on Facebook or Twitter (or X as we have to call it now). Twitter/X is my number one social media platform and I post regularly there. I share the latest news and information on financial matters, and other things that interest, amuse or concern me. So if you aren’t following my PAS account on Twitter/X, you are definitely missing out!

I am also on the BlueSky social media network under the username poundsandsense.bsky.social. Twitter/X remains my primary social media platform, but I also post details of my latest blog posts, third-party articles and other financial news and resources on BlueSky for those who prefer to follow me there.

As always, if you have any comments or questions, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts on PAS may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media:

Today I am looking at the new income investing option recently introduced by UK robo-adviser platform Nutmeg. This is designed for people who want to receive a regular monthly income while keeping their money invested (and hopefully still growing).

As a long-term Nutmeg investor myself (you can read my in-depth review here), I have already taken advantage of this opportunity. I will discuss my personal experience (so far) in more detail below. But first, here’s how it works in a nut(meg)shell, how it compares with Nutmeg’s traditional growth portfolios, and who might benefit the most.

How Nutmeg’s Income Portfolios Work

Powered by J.P. Morgan Asset Management (JPMAM)

Nutmeg has collaborated with JPMAM to construct five risk‑rated portfolios, built around actively managed income-focused ETFs – including the JP Morgan Equity Premium Income strategy – so you’re investing in income-optimized assets while staying diversified.

2. Five Risk Levels to Suit You

You can choose from five different risk levels, ranging from 1 (cautious) to 5 (adventurous), based on your circumstances, goals and appetite for risk. Each level offers a different blend of equity and bond exposure to balance income generation with capital stability.

Here’s a table describing Nutmeg’s five income portfolio risk levels in simple terms…

Risk Level

Description

Equity Exposure

Income Potential

Capital Risk

1 – Cautious

Prioritizes stability over returns

Low

Low

Very Low

2 – Conservative

Aims for modest, steady income with minimal volatility

Low to Moderate

Low to Medium

Low

3 – Balanced

Balanced mix of bonds and equities for moderate income and risk

Moderate

Medium

Moderate

4 – Growth-Oriented

Greater focus on equity income for higher payouts

Moderate to High

Medium to High

Moderate to High

5 – Adventurous

Maximizes income potential with higher risk tolerance

High

High

High

📌 Note: All portfolios are actively managed and diversified, but the mix of assets changes based on your selected risk level. Income smoothing and monthly payouts are available across all five.

3. Monthly Payouts with Optional Smoothing

One standout feature is income smoothing. This spreads out income across the year, so you receive consistent monthly payments – even if dividends or yields vary from month to month. This feature is optional, however – you can turn smoothing off if you’d rather receive income as it’s earned every month.

4. No Nutmeg Management Fee for 2025

These portfolios are available via ISA or General Investment Accounts (non-ISA) and have no Nutmeg management fee for the rest of 2025, though underlying ETF costs apply. A minimum investment of £10,000 is required.

5. Capital Remains Invested

Your core investment stays fully invested in the market – providing the potential for capital preservation or growth alongside the monthly income stream.

Income vs Growth – What’s the Difference?

The difference between the two approaches is summed up in the table below.

Income Portfolio

Growth Portfolio

Objective

Provide regular monthly income

Maximize long‑term capital growth

Payouts

Paid out monthly, with optional smoothing

Reinvested automatically for compounding

Yield Focus

Uses dividend and income-focused ETFs

Focus on market growth; income secondary

Suitability

Later-stage savers, retirees, cash flow needs

Long-term goals like retirement, wealth accumulation

While Nutmeg’s growth-oriented portfolios reinvest dividends to compound, the income portfolios are specifically structured to generate ongoing monthly payments. This is ideal for those needing a regular income rather than capital appreciation (though some capital appreciation will hopefully occur as well).

Who Are These Portfolios Best For?

Retirees or near‑retirees needing a dependable income stream without selling assets.

Those reducing work hours or with varied income, using the monthly payouts to smooth out earnings.

Investors frustrated with traditional bond/dividend returns – Nutmeg’s own research shows 69% of UK investors prioritize income, yet many are unhappy with current options.

Investors seeking simplicity – You set your risk level once and Nutmeg then handles asset selection, portfolio rebalancing and (optional) income smoothing. As with all Nutmeg investments, you can change your risk level later if you wish (though some extra costs may be incurred when doing so).

Pros and Considerations

👍 Pros:

Monthly income stream without selling investments

Income smoothing for consistent payouts

Actively managed by experts at JPMAM

No Nutmeg fees until 2026

⚠️ Considerations:

Requires £10,000 minimum to start

Still carries investment risk – capital isn’t guaranteed

Fund fees apply for underlying ETFs

If you’re focused purely on capital growth, growth portfolios with reinvestment may outperform long-term

My Experience

As you will know if you read my July 2025 Investments Update, in June I transferred most of the money in my Nutmeg Fully Managed portfolio (just under £25,000) to a new Nutmeg Income Portfolio. As my money was already invested via a Stocks and Shares ISA, my new income portfolio will enjoy that status as well, meaning income payments will be made without any deductions for tax. Likewise, any capital appreciation will not be taxable.

I selected a risk level of 5 (the maximum). That aligns with the risk level of my other Nutmeg investments, which should make it easier to compare them. More importantly, though, I have other investments that are lower risk, including my Bestinvest SIPP (personal pension) and – of course – my state pension. With my Nutmeg investments I hope to maximize their income and growth potential and am comfortable taking a few more risks to this end. As I have other, less risky investments, any reversals with Nutmeg shouldn’t be disastrous. Obviously as I get older – or if my circumstances change – I may revisit this.

For similar reasons, I chose not to select the ‘smoothing’ option. The income from my Nutmeg income portfolio will be in addition to other regular income streams I already have, so I can’t see any particular reason to have these payments smoothed out. Obviously I will monitor this and might change my mind in future, but for now I quite like the idea of having a variable extra payment each month. If it’s large, I may allow myself a few extra treats that month. If it’s small, I will adjust my expenditure accordingly.

Of course, the above is solely my personal perspective and should not be construed as financial advice. Everyone’s circumstances are different. You should always do your own ‘due diligence’ before investing and seek professional advice if uncertain how best to proceed. All investing carries a risk of loss.

As the screenshot below shows, my Income portfolio is already showing a profit of over £400, which is obviously welcome. It hasn’t yet generated any income, but that is unsurprising. It can take a while for investments to qualify for dividend payments, so I am keeping my expectations modest, initially at least 🙂

I will update PAS readers on how my Nutmeg income portfolio performs in my future monthly investments updates.

Closing Thoughts

In my view, Nutmeg’s new Income Investing portfolios are a valuable addition for UK investors seeking a regular income, backed by diversified, actively managed ETFs. They offer monthly, optionally smoothed payouts, managed via Nutmeg’s simple, user-friendly interface. The fact that there is no initial Nutmeg management fee through 2025 is a further attraction.

If your priorities include current cash flow, retirement‑style income, or smoothing irregular income, this could be a good fit. If you’re younger or focused on maximizing long-term growth via compounding, however, Nutmeg’s established growth portfolios (e.g. Smart Alpha) remain compelling options.

If you have any comments or questions about this post – or Nutmeg more generally – please do leave them below. As always, bear in mind that I am not a qualified financial adviser and cannot offer personalized financial advice. As with all investments, your capital is at risk and there are no guarantees of profit. If in any doubt, consider speaking with a financial services professional.

If you enjoyed this post, please link to it on your own blog or social media:

A quickie today to let you know that the annual Amazon Prime Day is almost with us. This year it extends over four days, Tuesday 8th to Friday 11th July 2025.

Prime Day is a special event for Amazon Prime members only. During it Amazon offers Prime members extra savings and special offers across a wide range of TVs, smart home products, kitchen equipment, grocery, toys, fashion, furniture, everyday essentials, and more.

Some of the best deals are typically reserved for Amazon’s own products, such as their Kindle e-book readers, Amazon Echo smart speakers and Ring video doorbells and security cameras. Discounts are often in the region of 40-50 percent for these products. If you’re thinking of buying any of them, Prime Day is definitely the day – or four days! – to do it.

I have been a member of Amazon Prime for over ten years now. As a regular Amazon shopper, I find it well worth while for the free one-day delivery on millions of items alone. But as a Prime member you get access to a lot of other benefits and services as well, including Amazon Prime Music and Amazon Prime Video.

If you’re thinking of joining Amazon Prime, therefore, I highly recommend doing it in the next day or two, so you can benefit from the Prime Day offers. Personally I think it’s worth it for the free delivery alone, let alone everything else that’s on offer. But if you wish, you can get a 30-day free trial now, take advantage of the Prime Day offers, and then cancel without owing any money. It’s your choice!

You can also see all the latest Prime Day deals by clicking here. This page also lists early deals before Prime Day itself.

As always, if you have any comments or questions about Amazon Prime or Prime Day, please do post them below.

Disclosure: This post includes affiliate links. If you click through and make a purchase, I may receive a commission for introducing you. This will not affect the price you pay or the products or services you receive.

If you enjoyed this post, please link to it on your own blog or social media: