As you may know, this is a best-selling book by Claire Parker and Sir Muir Gray, published by Bloomsbury. I bought a hardback copy from Amazon. A slightly cheaper ebook version for Kindle is also available.

Sir Muir Gray is also the author of Sod 70!, a similar healthy living guide aimed at the over-70s.

Review

Sod 60! is 232 pages long. The text – which is very readable – is broken up by lots of sub-headings, diagrams and cartoon-style illustrations (by David Mostyn). There are nine main chapters, each covering an aspect of how to live well in your sixties. The chapter titles are as follows:

Getting Older Doesn’t Matter – Getting Active and Getting Attitude Does

Keeping Active is Fitness Friendly

Your Attitude and Its Soulmates: Mind and Mood

Keeping Your Metabolism Healthy

Take Care of Your…Bits

Rhythm and Blues

Stuff Happens

Decisions, Decisions

Health Care: Choosing and Using It Wisely

Some of those chapter titles are self-explanatory, others less so. For example, Chapter 5 ‘Take Care of Your…Bits’ isn’t about what you might think. It actually covers looking after different parts of your body, from your brain to your feet. Sexual health is then covered in Chapter 6, ‘Rhythm and Blues’. Those both seem pretty odd choices of chapter title to me, but I suppose the aim was to help give the book a ‘quirky’ personality.

That small criticism aside, the style of the book is friendly and relatable. It’s also down to earth and practical, and I like the way that the text is interspersed with exercises, resolutions, and so on. It is very much a hands-on, practical guide.

Sod 60! concerns the importance of looking after your body and mind as you grow older. The authors stress the need to stay as active as you can, both physically and mentally.

Chapter 2 includes a range of physical exercises to try, and also sets out some general principles for exercising healthily as you get older. I thought this was one of the most useful chapters in the book.

Chapter 3, which focuses on attitude, mind and mood, is also very good. It looks at the importance of keeping a positive attitude, and staying connected with friends and family, your neighbours, local community, and so on. It also discusses maintaining a good relationship with your partner (assuming you have one). Getting enough sleep and dealing with stress are covered as well, though not in great detail.

Chapter 4 ‘Keeping your Metabolism Healthy’ focuses on diet and weight. The authors advocate following a balanced and varied Mediterranean-style diet, with plenty of fresh fruit and vegetables. That seems eminently sensible to me. I wouldn’t say there was much in this chapter I hadn’t heard before, and some of the advice such as avoiding sugary drinks struck me as stating the obvious. But this is of course very important to long-term health, so I guess it had to be said.

Chapter 5, as I’ve already mentioned, focuses on different organs/parts of the body. It discusses how to keep each one healthy, and warning signs to look out for as you get older. It also covers age-related changes and what you may be able to do to help prevent problems. Having a good diet, staying active, giving up smoking and reducing alcohol intake all crop up quite frequently. Again, there were no huge surprises for me here.

Chapter 6 is about sexual health and related matters such as bladder and (for men) prostate problems. On the sexual side, the advice could be broadly summed up in five words: Use it or lose it! The advice on matters such as urinary incontinence is – to be honest – a bit depressing, but nonetheless important to be aware of.

Chapter 7 ‘Stuff Happens’ is also a bit depressing, though again it covers some important topics. These include how to deal with the problems later life can throw at you, including depression, isolation, bereavement, serious illness, and so on. There is some excellent advice here, especially on the importance of cultivating and maintaining a support network of friends, relatives, health professionals, and so on.

Finally, Chapters 8 and 9 are both about healthcare and could easily have been combined in my opinion. They look at such matters as how to navigate healthcare decisions, self-care to prevent (or at least mitigate) serious health problems, drugs and vaccinations, and so forth.

In Conclusion

Overall I thought Sod 60! was a useful guide for sixty-somethings though maybe not an earth-shattering one. The book covers a range of issues that anyone in their sixties will need to think about and prepare for. It was first published in 2016, so there is no reference to the Coronavirus pandemic. The advice in the book still applies and in some ways is even more cogent now. With the UK still in lockdown at the time of writing, for example, we all need our support networks more than ever at the moment…

Sod 60! is really a ‘mind and body’ book. It doesn’t cover financial issues such as pensions and benefits (and indeed doesn’t claim to). And it doesn’t have much to say about the challenges and opportunities retirement can bring, or the pros and cons of carrying on working. For advice on these and similar matters, something like the annual Good Retirement Guide (which I hope to review soon) would be good. And keep on reading Pounds and Sense, of course!

If you want a readable and entertaining guide to making the most of your sixties and preserving your physical and mental health, though, Sod 60! would certainly fit the bill. It would also make a great (and relatively inexpensive) birthday or Christmas gift for anyone in this age category.

As ever, if you have any comments or questions about this post, please do leave them below.

Disclosure: As with many posts on Pounds and Sense, this post includes affiliate links. If you click through and make a purchase, I may receive a modest commission for introducing you. This will not affect in any way the price you pay or the product or service you receive.

If you enjoyed this post, please link to it on your own blog or social media:

This isn’t an easy post to write, but I like to be honest with readers about my investing failures as well as successes. So here’s the sad story of one failed investment…

Table of Contents

How It Happened

About a week before Christmas 2020 I got a cryptic email from the property crowdfunding platform Crowdlords directing me to their website for information about one of my investments. The email didn’t give anything away, but I had a premonition it wasn’t going to be good news.

Anyway, I followed the link to the Crowdlords site and logged in. The update concerned a property development I had invested £3,000 in back in 2016. Originally this was referred to as Seven Eco-Apartments (CL Number Four), but latterly it has been described simply as Kennington Road.

There was a long, involved explanation of what had been going on with the development. But the bottom line was that it had failed completely and investors were going to lose not just some but all of their money.

At first I wasn’t entirely sure I had read this correctly, so I emailed Crowdlords for confirmation. I received a quick reply from Richard Bush, co-founder of Crowdlords. Among other things, he said:

‘Kennington Road is one of two investments (from 72 we’ve completed to date) which have suffered from a very unusual combination of factors – delays, cost overruns, lost sales due to Covid and then further delays getting back to the market only to find the values have dropped. The perfect storm, almost.’

So there it was. At a stroke I had lost £3,000. As you may imagine, I felt pretty sick about this. I have subsequently heard from other people who lost much larger (five-figure) sums on the projects concerned (I’m not sure what the other project was). But that was no consolation, of course. About the only positive thing I can say is that I have had other Crowdlords investments which did deliver the promised returns. But even so, I am well down on my investments via the platform overall.

While it’s tempting to blame Crowdlords for the losses, I accept they are not directly responsible. Clearly they – along with many other businesses – have been the victims of unique and challenging circumstances in 2020. I do, though, think their communications with investors could have been a lot better, especially when it was becoming clear that problems were mounting. While they were quick enough to notify investors about successes – and new projects requiring investment – I couldn’t help feeling that failing projects were being swept quietly under the carpet. To be fair, Crowdlords aren’t the only investment platform I have noticed this with.

I do think it would be a nice gesture if Crowdlords were to offer modest ex-gratia compensation payments from their own profits to investors who have lost all their money. Even a book token would be nice. But realistically, I will be surprised if this happens now.

Lessons Learned

So what lessons have I learned from this experience? I’ll try to sum them up below.

Be a Sceptical Investor

Perhaps I’m stating the obvious here. But when I started investing in property crowdfunding it was pretty new and I found the concept intriguing and exciting. At that point, of course, there hadn’t been any failures to take the shine off. Plus I had recently come into some money through an inheritance and was looking for interesting and profitable ways to invest it.

Looking back now, I can see that I was a bit too ready to buy into the property crowdfunding idea, and put too much faith (and money) in it. I am not saying property crowdfunding can’t work (many of my investments did pay off). Nowadays, however, I am a lot more sceptical when assessing such projects and the claims made about them by their promoters.

It’s important to remember that property crowdfunding platforms are all in business to make a profit. To put it bluntly, they make their money by persuading potential investors to part with theirs.

There is nothing automatically wrong about that – all businesses do it – but it’s essential to examine any potential investment carefully and objectively before opening your wallet. That includes ensuring you understand exactly what the project entails and what the risks for investors are. Which brings me neatly to my second lesson…

Know What You are Getting Into

Property crowdfunding investment opportunities take many different forms.

In ‘traditional’ property crowdfunding a group of investors jointly purchase a property. They then receive rental income pro rata to their investment and a share of any profits when the property concerned is sold. With this type of investment, your money is effectively secured by bricks and mortar, so you are unlikely to lose your shirt. On the other hand, problems (from bad tenants to fire or flood) can arise leading to lower rental income than anticipated and/or delays in selling up. And obviously, if the value of the property doesn’t rise, you may not get all your capital back, let alone any profit on sale.

Development projects, which may launch with no more than a set of architect’s plans, are even riskier. If you invest in a development project (such as Kennington Road), while you may ultimately make a bigger profit, there is a real risk of the project failing completely for any number of reasons. In this case (as I discovered) you risk losing your entire investment sum.

Finally, there are platforms such as Kuflink that allow people to invest in loans secured against property (including bridging loans). If such loans are not repaid, the property can be sold to pay off the debt, so again you shouldn’t lose your entire investment. But even so, the legal processes involved can be time-consuming and expensive; and again you may end up losing some of your capital after all costs are paid off. And even if it doesn’t go that far, there are quite often delays in repaying loans (especially at the moment) meaning you don’t get your money back when you expect it.

So my second lesson is to be very clear what type of property crowdfunding you are investing in and what the risks are. And be especially cautious about investing in development projects, which are by nature more speculative and carry a greater risk of losing all your money.

Spread the Risk

This is of course an important principle in all investing but one that applies especially to property crowdfunding.

If you invest £3,000 in one project (as I did with Kennington Road) unless you’re Bill Gates that’s putting a lot of eggs in one basket. When I started in property crowdfunding I put as much as £5,000 into a single project. That is definitely not something I would do any more.

I am not investing as much in property crowdfunding as I did originally, but where I am still doing it I generally put no more than £100 into a single project. If I lose that money in a worst-case scenario, obviously that is not going to hit my finances nearly as hard. My approach nowadays is to have larger numbers of small investments spread across multiple platforms. This spreads the risk while still giving me control over what I invest in.

It’s interesting to note that most of the remaining property crowdfunding platforms (some have gone to the wall or are no longer serving private investors) also now offer some form of shared investment with automatic diversification. An example mentioned earlier is Kuflink, who offer an ‘Auto-Invest’ account paying up to 7% interest per year. Investments are automatically spread across a wide range of projects on the platform. If you want an easy way to diversify your property crowdfunding investments, this approach has some merit. Personally I prefer to build a diversified portfolio myself (which you can also do with Kuflink), but the automated approach is worth considering if you don’t have the time or inclination for that.

If you want to make use of your ISA allowance with Kuflink, you will need to open an Auto-Invest IFISA with them. You can’t create an ISA and choose your own investments, for reasons I’m not clear about.

Remember the Big Picture

Finally, it’s important always to remember that property crowdfunding is just one way of investing your money. It is also – as I have indicated – a relatively high-risk one.

So if you are going to include property crowdfunding investments in your overall portfolio, it should only comprise a fairly small part of it – I suggest no more than 10 percent. The rest of your money can then be spread across a variety of other investment types to provide good diversification. And as I have noted before, you should also have at least three months’ of income in easily accessible form in case of sudden, unexpected emergencies.

When I first started in property crowdfunding I made the mistake of putting about a third of my money into this type of investment. I am down to around 20% now, which is still (in my view) too much, but some money is tied up in long-term projects where an exit currently looks some way off. But at least hopefully there won’t be any more complete write-offs now.

Closing Thoughts

So that is the story of my failed £3,000 property crowdfunding investment and the lessons I have learned from it.

I am trying to be philosophical and remember that many of my other property crowdfunding investments have made money for me. Nonetheless, in retrospect I wish I had taken a more cautious approach initially. If I had simply put all the money into my Nutmeg stocks and shares ISA, for example, I don’t doubt that financially I would be better off overall.

Nonetheless, I do still believe in the property crowdfunding concept and am happy to have some money still in it. As I’ve said before in Pounds and Sense, property is relatively less affected by ups and downs in the economy than stocks and shares. Property investments don’t provide a method for hedging your equity investments directly, but they do offer an extra element of diversification and spreading of your financial risks. And alright, I will admit that a part of me does rather enjoy (for example) having a small amount invested in student accommodation in Leicester, my old university city 🙂

As always, if you have any comments or questions about this post, please do leave them below.

Disclaimer: Please be aware that I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. You should always do your own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

If you enjoyed this post, please link to it on your own blog or social media:

Today I’m discussing a subject that will be relevant to any of you who have blogs yourself or are thinking of starting one.

I’ve been blogging for almost twenty years now. I started off blogging about freelance writing and moved on to personal finance with Pounds and Sense. I make money from my blog by various means, but the most important (and lucrative) is through collaborations with businesses and agencies on sponsored posts, sponsored links, and so on.

Companies are always on the lookout for ‘influencers’ who can help get their message across to their target audience. They have budgets for this purpose, but before sending any money your way they will almost certainly want to see your blog’s media kit (also known as a press kit). If you don’t have one – or it’s not up to scratch – you can expect to lose out on many paying opportunities.

Table of Contents

So What Goes Into a Media Kit?

As a blogger, your media kit is an advertisement for you and your blog and the services you can offer. It will typically consist of one or two pages you can send (or hand out) to anyone enquiring about potential advertising opportunities or collaborations

A good media kit will ensure you create a strong and professional first impression. Everybody’s media kit is different, but here are some things you should consider including in yours…

Biography

In this section you provide a brief account of yourself, including such things as your age, location, occupational background, hobbies and interests, family, and so on. Companies want to know whom they will be working with, to reassure themselves that you and your blog will be a good fit for their target audience. Let your personality shine through, therefore, quirks and all! You should also include a good-quality portrait-style photo of yourself (see the example in the header image).

Blog Description

In this section you talk about your blog itself – the subjects you cover, your target readership, and any other information that may interest potential advertisers. You may also wish to include your blog’s logo.

Stats

Advertisers want to know the size and nature of the audience you can deliver for them. So it’s important to share some key stats, including such things as total unique views, social media following, email newsletter subscribers, and so forth. Clearly you will want to pick the most impressive-looking stats – so if you don’t have many Instagram followers (for example) just leave that out. But don’t exaggerate either. Clients can and will check your stats, and if they don’t appear to correspond with the figures you have quoted, they are unlikely to want to proceed further

Collaboration Options

Here you list ways brands can collaborate or advertise with you. Some possibilities include:

Sponsored Posts

Sponsored Links

Product Reviews

Contests and Giveaways

Banner Ads

Social Media Campaigns

You can also include prices for these services in your media kit if you like. Personally I don’t do this, as I like to leave room to negotiate over price.

Testimonials

If you have worked for business clients before, I would strongly recommend including any testimonials you may have received. And don’t be afraid to ask for testimonials after a successful collaboration. This type of social proof provides invaluable reassurance for would-be clients that you can deliver on your promises and achieve good results for them.

Contact Information

The most important one of all! Don’t forget to include your contact details so that potential clients can get back to you. You will probably want to include your email address, phone numbers (home and mobile), postal address, and so on.

Media Kit Design

As a blogger you aren’t necessarily expected to have an all-singing, all dancing, media kit, but the smarter and more professional it looks, the better. Your kit should work both electronically (e.g. as an email attachment) and when printed out in colour.

Fortunately you don’t need to be a design guru to produce a great-looking media kit. There are lots of free and inexpensive templates available, which you can edit and personalize to your heart’s content. A great place to look for such templates is the Design Bundles website – just put “Media Kits” in the search box on that website.

Win a Design Bundle!

Here’s a great opportunity to win a media kit template and any other design resources you would like too 🙂

My friends at Design Bundles are running a giveaway to win a prize worth £100. This comprises a £50 credit for Design Bundles to use on Media Kit templates and any other products you’d like from them, along with a four-month premium subscription to Canva. As you probably know, Canva is a brilliant design website you can use to create a media kit and other amazing graphics for your blog as well. You can enter via the Rafflecopter widget below.

Anyone world-wide can enter. All fields are optional, so you can choose which ones you’d like to complete. But obviously, the more you do, the better your chances of winning.

The contest is open now and will close at midnight on Tuesday 26th January 2021. The winner will be contacted by the end of that week to arrange their prize.

Good luck in the giveaway, and with creating an attractive and compelling media kit!

As always, if you have any comments or questions about this post, please do leave them below.

Disclosure: This is a sponsored post for which I am receiving a fee.

If you enjoyed this post, please link to it on your own blog or social media:

In the past buy-to-let seemed a relatively easy way to make money.

So long as you had the capital – or were able to borrow it – you could buy a house, put tenants in it, and collect a steady income from rental payments, along with potentially a lump-sum profit if you sold up at a higher price later on.

In recent years, though, tax and regulatory changes have made buy to let less appealing – to a point where many wonder if there is still money to be made this way. So in my post today I want to address this question.

Let’s start, though, by looking at the upside…

Table of Contents

The Attractions of Buy to Let

As stated above, property investors get a double benefit. They enjoy rental income from tenants for as long as they own the property, and also have the potential to make a substantial lump sum profit when the time comes to sell.

A further attraction of buy to let is that your tenants effectively pay off your mortgage for you. So if, for example, you are buying a £400,000 property, you might ‘only’ need to find a deposit of £100,000. As long as your tenants’ rental payments cover your mortgage repayments (with a bit to spare), after 25 years or so the mortgage will be paid off. You will then fully own a second property, having originally paid only a quarter of the full property price. And that doesn’t even allow for the prospect of capital growth. If your property eventually sells for £600,000, you’ll have made an additional £200,000 capital gain.

Of course, you don’t have to borrow to fund your buy-to-let. If you already have the capital you need, investing in a buy-to-let property will provide you with a steady income while the capital value of your property (hopefully) appreciates over time.

Buy to let can also be a good way of diversifying your investment portfolio. Rental income is relatively stable, especially if you have a number of properties and tenants. And property values aren’t directly related to the state of the stock market. So while property doesn’t provide a method for hedging your stock market investments directly, it can certainly help spread the risk.

Of course, property prices took a knock in the 2008 credit crunch and subsequent recession, and more recently were affected by the pandemic (though prices generally are on an upward trajectory again now). In the longer term, though, prices have been on a strongly upward trend since the 1970s. On average, house prices have grown faster in the UK than they have in any other European country.

There’s every indication that prices will go on rising in the coming years as well. The UK currently has a serious shortage of housing, caused by various factors. To start with, the UK population is growing rapidly. This inevitably means demand for housing will go on rising, thereby driving up the price of property. According to the Office of National Statistics there will be an annual shortfall of housing in the UK of over 100,000 properties each year for the next decade. This could mean a shortfall of one million properties by 2025 if current trends continue.

Various factors have combined to boost rental demand, including immigration, more people living alone, people moving around the country for work reasons, and rising house prices stopping first-time buyers getting onto the housing ladder. The latter is obviously challenging for young people, but it’s great news for landlords whose buy-to-let properties are being let extremely quickly, while their rental income keeps increasing. All of the above means that residential property can represent a profitable and attractive investment option.

What Are The Drawbacks?

One obvious drawback for anyone wanting to invest directly in property is that it’s expensive! And if you can only afford a single property, you are taking the risk of putting all your eggs in one basket. To mention just a few things…

There may be periods when you don’t have tenants (voids, to use estate agent jargon). At these times your property will be costing you money rather than making it for you.

Bad tenants are all too real and can be a nightmare for landlords. If they don’t pay their rent, it will take time and money to evict them. And that’s not to mention the costly damage to your property a malicious – or just careless – tenant can cause.

There will be maintenance and repair bills to pay. If something expensive goes wrong – the roof or the central heating boiler, say – the cost of the necessary work may wipe out several months of profits for you.

In general, being a landlord – at least, a responsible one – is a hands-on role. While you can outsource some aspects of managing your property to an agency (for a fee) you will still have to keep a watchful eye on your property and tenants to ensure that your investment is protected.

A further drawback is that property isn’t a liquid asset. Yes, putting your money in bricks and mortar gives you a degree of security – but if you need to access your capital urgently this may be difficult or impossible. Even if you’re able to find a buyer quickly, if the timing is bad you could end up selling at the bottom of the market and making only a small net profit or even a loss.

And there’s more bad news for buy-to-let investors. As I said earlier, legal changes over the last couple of years have made the whole buy-to-let process more costly and burdensome. For one thing, from April 2016 anyone buying a residential buy-to-let property (or second home) has had to pay an extra 3% in Stamp Duty. In some quarters this has been dubbed the Landlord Tax.

Another major legal change has affected landlords who use mortgage loans to purchase buy-to-let properties. Before April 2017 landlords were allowed to deduct all of the interest they paid on buy-to-let mortgages from their taxable income. In effect, that meant they paid tax on their net profit from rentals rather than their turnover. The government decided to change the rules, however, arguing they gave buy-to-let landlords an unfair advantage over ordinary homeowners. So from April 2017 landlords were only allowed to claim relief on 75% of their mortgage interest. From April 2018 that dropped to 50%, and it kept falling by 25% a year until it reached 0% in 2020. It was then replaced by a less attractive tax credit equivalent to 20% of mortgage interest (which was particularly disadvantageous to higher rate taxpayers). All of this has meant that borrowing money to fund a buy-to-let has undoubtedly become less attractive (and profitable) than it used to be..

Other changes affecting landlords have come in too. For example, from April 2018 all new tenancies and renewals have had to be rated ‘E’ or better on their Energy Performance Certificates, with fines of up to £5,000 for landlords who don’t comply. Most recently built homes should qualify for this rating, but landlords of older, less energy-efficient properties may have to spend large sums bringing them up to scratch. And, of course, this all adds to the administrative burden for landlords, even if it is ultimately helping to save the planet!

One effect of all this has been that some smaller landlords have decided that buy-to-let is no longer worth the effort for them, and they are selling up and moving out of the sector.

So Is There Still Money to be Made?

My answer to this is a qualified yes.

There is definitely still money in buy to let, but it is no longer the ‘one-way bet’ it might once have appeared. You should therefore research opportunities carefully and adopt a highly professional and businesslike approach to the whole process.

A key consideration here is ‘yield’. This is the net amount (rental minus costs) you can expect to make from a buy-to-let property per year, as a percentage of the purchase price. Yield can be compared with the interest rate paid on a savings account. By this means you can assess how profitable a buy-to-let opportunity is and whether it makes sense as an investment vehicle. Clearly, if the yield is less than you could get by leaving your money in the bank, there is not much point in investing this way.

The website Totally Money recently analysed data from nearly half a million properties across England, Scotland and Wales, to calculate the buy-to-let yield for each postcode. The results were eye-opening to say the least. They found that buy-to-lets in the top 25 postcode areas were still delivering excellent returns. At the top was Liverpool, where landlords can enjoy 10% yields. Falkirk (9.51%) and Glasgow (8.71%), both in Scotland, came second and third respectively. Even postcodes at the lower end of the top 25, such as Lancaster and Aberdeen, were returning respectable yields of over 7%. All of these are clearly far better rates of return than you could get from a savings account, and you will have an asset that is hopefully increasing in value as well (see below).

Location is therefore a key consideration for any potential buy-to-let investment and must be researched thoroughly. In addition, the best area for your investment will depend on whether you intend to put your money into flats for professionals, student accommodation, family homes, etc. At the risk of stating the obvious, there needs to be solid demand in the area from would-be tenants for the type of rental property you intend to buy.

Of course, while it’s very important, yield/income potential isn’t the only consideration for property investors. In the longer term you will likely be hoping for capital growth as well – so ideally you should be looking to invest in properties in up-and-coming areas rather than those in long-term decline.

Getting Started

Having weighed up the pros and cons, if you do decide that buy-to-let is right for you, here are some top tips to get you started…

Speak to a professional independent financial adviser to discuss your plans. They will help you decide how much to invest and the level of return you should realistically be aiming for.

You should also speak to a mortgage broker to find out what deals are available and ideally get approval in principle for a mortgage. This means you will be well placed to make an offer as soon as you find a suitable property.

If there is a particular area you are considering, visit several times to get a feel for the place. That applies especially if it’s a location you’re not already familiar with. Check out the housing stock, public transport, car parking, shopping and schools, hospitals, and so on. Try to speak to other landlords in the area and local letting agents to get an idea of the size and nature of the rental market and the sorts of rentals that may be achievable. Always remember that the bottom line for any buy-to-let investor is return on capital or yield.

Once you find a potential property (with or without existing tenants) research it carefully as well. Obviously before buying you will need to do all the usual searches and a structural survey. As with all property sales, you can expect this process to take several months to complete.

Arrange insurance for your buy-to-let. Along with the usual buildings insurance, you should almost certainly have landlord insurance to protect you from financial losses associated with renting out a property. This will typically cover such things as fixtures and fittings, public and landlord’s liability, subsidence, replacement of windows, locks and keys, and so forth. It will also normally cover malicious damage caused by tenants, along with rent arrears and legal expenses (though the last two may not necessarily be included as standard). You can compare landlord insurance here.

To find tenants you can either go through an agency or do this yourself. Obviously going through an agency will add to your costs but can save you a lot of hassle, especially if you haven’t the time (or inclination) to be too hands-on.

Even if you pick your own tenants – and perhaps already know them personally – draw up a legally-binding contract. That means everyone knows where they stand from the start and can help to avoid potential unpleasantness later on.

Review your buy-to-let mortgage arrangements regularly and be prepared to switch to a better deal when your current one expires.

Ensure that your rental income is declared in a tax-efficient way and set against any allowable expenses. A good accountant will be able to help with this.

Your accountant will also be able to advise you about the pros and cons of running your buy-to-let through a limited company. This comes with additional costs (and paperwork) but for landlords of multiple properties in particular the tax benefits can be significant – not least because you can claim all the interest paid on your buy-to-let mortgage/s against income rather than just 20%.

And finally, once your first buy-to-let is up and running successfully, consider adding more. Multiple properties will give you a bigger income and will also reduce the risk inherent in putting all your eggs in one basket (as discussed earlier).

In Conclusion

If you’re considering buy to let, I hope this article will have helped you make up your mind. There is undoubtedly still money to be made this way, but you do need to choose your location and property carefully, and approach the whole process in a professional and businesslike way. That applies from the initial planning stage right through to the day-to-day – and year-by-year – management of your property.

As ever, if you have any comments or questions about this post, please do leave them below. I would also be very interested to hear from any readers who have invested in buy-to-let themselves, along with any tips (or warnings!) they would like to share.

Disclosure: this is a sponsored post.

If you enjoyed this post, please link to it on your own blog or social media:

For many of us (including me) the stress of the Covid-19 pandemic is playing havoc with our sleep patterns. That’s bad news for a variety of reasons.

Scientifically it’s been proven we all need at least 6 to 9 hours sleep a night. The amount required varies between individuals. It also reduces a little as we get older (though not as much as some people would have you believe).

Getting enough good-quality sleep is essential for a number of reasons. For one thing, sleep is when our body repairs itself so it is ready to face another day. In addition, scientists now believe that sleep – REM sleep when we are dreaming especially – plays an important role in consolidating learning and memories from the day before.

Not getting enough sleep leaves us tired and irritable, more prone to anxiety and depression, less able to concentrate and be productive. It may also make us more likely to put on weight, weaken our immune system, and increase our risk of heart disease.

So today I thought I’d share some top tips for sleeping better at this stressful time. Some of these are from my own experience (and research) while others have been contributed by my fellow UK bloggers. I hope you will find some helpful ideas among them…

Table of Contents

Top Tips for Sleeping Better

1. Try to Keep to a Regular Routine

Aim to go to sleep at the same time every day and at weekends. This well help set your body clock and ensure you are able to get to sleep quickly and wake up refreshed and ready to start the day.

2. Make Your Bedroom as Dark as Possible

Darkness signals to your body it is time to sleep and stimulates the production of our natural sleep hormone, melatonin. Avoid as much as possible light from electrical devices such as mobile phones and TVs on stand-by. Ideally such devices should be banished from the bedroom completely or at least covered up at night.

I also recommend having blackout curtains or blinds in the bedroom. These can cut out light from outside almost completely. Until I got blackout curtains I got woken up on various occasions by the security lights on the house opposite when (I assume) a fox or something passed by in the early hours.

3. Brighten Your Mornings, Dim Your Evenings

Try to get some natural light (ideally sunlight) as soon as possible after waking up. In the evening, though, dim the lights, especially in the hour or two before bedtime. This all helps strengthen your daily rhythm of sleep and wakefulness.

4. Exercise Daily, but not in the Evening

Getting enough exercise is crucial to sleeping well. But do it in the morning if possible. Exercising then will energise you for the rest of the day, and later ensure that you are physically tired enough to sleep well. By contrast, if you exercise in the evening, this will speed up your metabolism, raise your body temperature, and stimulate the production of hormones such as adrenaline and cortisol. This is not a problem if you’re taking exercise in the morning or afternoon, but too close to bed and it can interfere with your sleep.

5. Avoid Caffeine and Alcohol at Night

I guess for many of you this is stating the obvious. Nonetheless, it’s worth pointing out that caffeine is a natural stimulant and can interfere with sleep if taken at night.

Coffee is the best known source of caffeine, but tea contains it as well (even green tea). People vary in their sensitivity to caffeine. Even so, for most folk a milky bedtime drink is likely to be a better choice. Or you could drink decaffeinated coffee. Personally, though, I find this generally tastes like dishwater, and prefer simply to avoid coffee from afternoon onward.

Alcohol, on the other hand, is a nervous system depressant. This means it can help you to sleep, but the quality of your sleep is likely to be impaired. For one thing, it can be dehydrating, meaning you wake up in the middle of the night needing water. You may also have to get up for additional bathroom visits. And drinking alcohol can make you more prone to snoring, which can affect your sleep quality (and that of your partner!).

6. Change Your Mattress

Many of us keep our mattresses for too long before changing them. Ideally you should get a new mattress every eight years or so. Old mattresses tend to lose their spring and become lumpy and uncomfortable. Even worse, detritus can build up in them including dead skin cells and dust mites. This can cause allergic reactions, affecting your sleep quality.

7. Get Comfortable Pillows

Like mattresses, many of us wait too long before changing our pillows, but for similar reasons they need to be changed regularly (as a rule of thumb every one to two years). A pillow of the right size and firmness will hold your head in a comfortable, ‘neutral’ position while you sleep, ensuring you don’t wake up with a stiff, aching neck in the morning.

The type of pillow you get is a matter of individual preference. Personally I like feather and down, but others may prefer memoryfoam or microfibre. In any event, it’s important to choose your pillows carefully, and don’t begrudge paying a bit more for quality – it will be an investment in your health.

8. Don’t Eat Late at Night

Eating late will raise your blood sugar level at a time when it should be falling and make it harder to get to sleep. It may also, of course, cause indigestion. If you want a late night snack, something light like cheese and biscuits, a piece of fruit, or a bowl of cereal may fit the bill. In any event, you should try to avoid eating anything from an hour before you go bed.

9. Keep Your Bedroom Cool and Quiet

The optimum temperature for sleeping is between 16 and 18 degrees Celsius. Obviously it can be difficult to ensure that your room stays at this temperature all night, especially in the depths of winter and the heights of summer. Do what you can to stay cool (though not cold) all night, though, and your sleep quality will improve as a result.

Noise can be another obstacle to sleeping. This will obviously depend a lot on where you live, how much traffic there is outside, and how quiet (or otherwise) your neighbours are. Even if noise is a problem, however, there are things you can do to improve matters. Earplugs are one solution, though they don’t suit everyone. And a fan or similar device can help drown out noises from outside (personally I have a dust extractor which whirs away quietly all night and clears the air as well as covering up other noises). Finally, there are lots of free smartphone apps that will generate relaxing background sounds to help you sleep, with rain and sea sounds especially popular.

10. Wind Down at Night

Try to spend the hour before going to bed doing a calming activity such as reading, listening to music or even meditating. Try to avoid touchy discussions, work-related worries and so on. All this will help put your mind and body into sleep mode. If possible avoid using electronic devices such as laptops and mobile phones late at night, as the blue light they emanate can make it harder to fall asleep.

11. Bath Before Bedtime

This is something I swear by myself. A warm bath is a great of way of relaxing your body and easing the tensions of the day in preparation for sleep. Adding a few drops of lavender oil can assist in this. You can also add bath cream or bubble bath if that’s your thing.

12. Ask for Help

Finally, don’t be afraid to ask your GP if your sleep problems continue for more than a few weeks. She will be able to check to see if a health condition — such as acid reflux, arthritis, asthma, or depression — or a medicine you take may be part of the problem. She will also be able to talk you through any lifestyle changes or medications that might be helpful.

I haven’t mentioned sleeping pills until now. Personally I am dubious about taking these if I don’t have to, and concerned that I might become dependent on them. There are, though, various natural/herbal remedies you can try, including chamomile tea and St John’s Wort.

I have also had good results from a health supplement called 5-HTP, which is made from the African plant Griffonia. This boosts the production in the body of serotonin (the so-called happy hormone) and can therefore help with depression. But serotonin is also a precursor to melatonin, our body’s natural sleep hormone. I take one of these at night if I have had a stressful day and do find they seem to improve my quality of sleep. Below is a link to one such supplement on Amazon. Read the description and reviews and see what you think. But if you have any pre-existing medical conditions, I would strongly recommend speaking to your GP before you start supplementing with 5-HTP (or anything else).

Top Tips from UK Bloggers

As mentioned above, I also asked my UK blogging friends to let me know what worked well from them. Here are some of the answers they came up with…

Joanna from My Anxious Life says: ‘I like to play little games or make lists in my head. I often play “I Went To The Shop And I Bought…” or the Alphabet Game, for example listing all the foods beginning with C or all the girls names beginning with S. It helps to give me something simple and repetitive to concentrate on other than my constant stream of thoughts. It’s the adult’s version of counting sheep!’

Kier from Beyond the Blues says, ‘I always open my window about half an hour-ish before I’m going to go to bed so that it’s extra cold in my bedroom, and then I take my hot water bottle to bed when I’m ready to sleep. I don’t know what it is about sleeping in a cold bed with a hot water bottle but it just makes me feel so calm and cosy that I fall asleep pretty quick!’

Nikki from Best Brunch or Breakfast says, ‘When I want to go straight to sleep, I have a really hot bath. Not a relaxing soak – a REALLY hot bath (be sensible and don’t end up in A&E, obviously!). When I get out I get quickly dry and then I am that exhausted I fall straight asleep!’

Claire from Stapo’s Thrifty Life Hacks says, ‘I put my phone on charge away from the bed and get my Soothe Kit out, which has lots of comforting bits in it. Everyone’s Soothe Kit will be different, depending on what works for them, but mine contains herbal tea, a colouring book, some slime, a lavender body lotion and my favourite blanket. The items relax me and take my mind off the day’s worries.’

Emma from Bee Money Savvy says, ‘This may contradict a lot of advice about avoiding electronic devices before bed but right now I’m finding playing Animal Crossing on the Nintendo Switch really soothing before bed. My advice would be to find something that relaxes you; whether that’s a game, doing yoga, meditating or having a bath in the hours leading up to bedtime.’

Rebecca from Views From My Garden Bench says, ‘I was an insomniac for years until I worked out what helped me – calm spoken words or classical music. At the moment, I’m listening to Patrick Stewart reading a Shakespeare sonnet a day – his voice is so restful, and because it’s poetry there is a cadence to his words. Also I listen to modern classical music from Ludovico Einaudi [Italian pianist and composer].’

Anna from Goodness Me Nutrition says, ‘I’m a nutritional therapist and write about gut health and sleep. Allowing three hours between your last meal of the day and sleep makes a big dfference. Eating in time with your circadian rhythms is a big factor.’

Joanna who blogs at Joanna Journals says, ‘For me, I find that the best way to sleep soundly is simply to have a routine. When I was at uni, I slept so badly because I just had no sleeping pattern, but in my final year, and now I’m working, I have a set bedtime and wake-up time, and I fall asleep so quickly and soundly. It really is amazing how our bodies work; once we’ve got used to our body clock, it works wonders!’

Victoria from Semi Charmed Life says, ‘White noise really helps me. I usually have a fan on when I sleep which does the trick (and keeps the air circulating, making me feel better).’

Georgia of Big Fashion Talk says, ‘I add on my pillow some drops of lavender essential oil and it has helped me tremendously!‘

Anne from The Platinum Line says, ‘I find I need to keep to a routine. I still get up and dressed at about 8 o’clock and try to stick to regular meal times. I find I am sleeping better as there is less traffic noise and our student neighbours are at home.’

Ren from Queer Little Family says, ‘I’m an insomniac and my general advice is if you can’t get to sleep don’t force it. Get up and start again. Go have a cup of tea, spend twenty minutes, half an hour away from your bed and from trying to sleep. Then go back to bed and try again. It doesn’t always work but it breaks it up.’

Marina from Marina Writes Life says, ‘Back in the day, I used to search up techniques on how to sleep better and ways to make you fall asleep as, quite frankly, I was really struggling due to the stresses of college, etc. I found a list of foods based on old wives’ tales that supposedly make you sleepy, two of which were chocolate and banana (there were others like turkey and sunflower seeds, but as a midnight snack – ew). Five years later, still to this day, I eat a chocolate and banana toastie at night when I can’t sleep and, honestly, it works a treat!’

Rob from The Sober Odyssey says, ‘I’ve taken CBD oil for the more than six months and found that has helped with much better sleep. Then giving up alcohol in January improved my sleep even more. I track my sleep with my Fitbit.’

Finally, Marie from Broke Girl in the City says, ‘Write a list of the important things you need to do in the evening to prevent yourself from worrying. Also, nice clean sheets work a treat!’ Marie also has a great blog post with tips for sleeping better from UK money bloggers. It was published specially for Mental Health Awareness Week, 18-24 May 2020. Here’s a link to her post.

Persistent ear infections such as Otitis Externa (Swimmer’s Ear) can also disrupt sleep as well as reducing quality of life generally. The specialist ear doctors at Auris Ear Care can diagnose and treat your condition in the comfort and safety of your own home using their fully mobile and CQC-regulated service.

Many thanks again to my UK blogging friends for their tips and ideas. Please do take a moment to check out their blogs!

Final Thoughts

I hope you have enjoyed reading this post and it has given you some ideas to try if sleeping is a problem for you. I am definitely going to try out chocolate and banana toasties 😀

This is undoubtedly a difficult and stressful time, but hopefully there are at least a few signs of light at the end of the tunnel now. If you need advice and support, however, don’t be afraid to reach out to others, be they friends and family, counsellors and chaplains, financial advisers, healthcare professionals, and so on. And make time to contact people whom you know may be struggling right now or you simply haven’t heard from for a while. We really are all in this together, and by supporting one another we will make it through together to better times ahead.

Good luck, and sleep well!

As always, if you have any comments or questions about anything in this post, please do leave them below.

Disclosure: This post includes Amazon affiliate links. That means if you click through and make a purchase, I will receive a small fee from Amazon as a reward for introducing you. This will not affect the price you pay or the product or service you receive.

Note: This is an update of a post first published last year.

If you enjoyed this post, please link to it on your own blog or social media:

British people generally are not very good at saving.

A third of us have under £600, and 1 in 10 have no savings at all (source: https://www.finder.com/uk/saving-statistics). Having so little money put away makes people especially vulnerable in the event of a sudden change in their circumstances such as redundancy or divorce.

So today I thought I’d bring to your attention a money-management app called Plum that aims to help with this problem.. Plum is designed to help you set money aside painlessly for any purpose – from holidays to major purchases or simply for a ‘rainy day’ fund.

Plum is one of a growing range of apps that make use of so-called Open Banking. This allows third-party apps to access your financial information (read only) – so long as you provide the necessary authorization, of course – and perform certain transactions on your behalf, if you choose to set up a direct debit.

Open Banking is now becoming well established in the UK, and safeguards are in place to ensure that your security isn’t compromised. Even so, this is something you need to be aware of – and comfortable with – before signing up with Plum or similar apps.

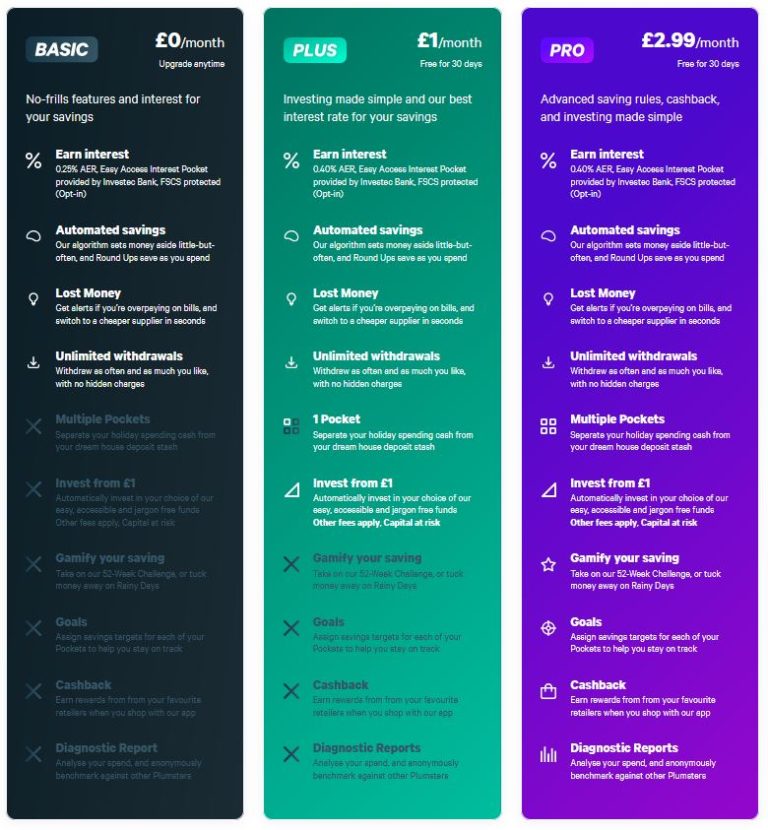

In this post I am looking at features available on the Plum Free (or Basic) account and the paid-for Plum Plus and Plum Pro Accounts. The Plum Free account is – of course – free of all charges. Plum Plus costs £1 a month (the first month is free) and Plum Pro costs £2.99 a month (again, the first month is free if upgrading from a Plum Free account). Plum Plus and Plum Pro offer a wider range of features and higher interest rates in interest-bearing ‘Pockets’ (further discussed below).

The screen capture below from the Plum website shows the features available with each type of account.

You can read more about the three account types if you wish on the Plum website.

Table of Contents

How It Works

Plum is available as an iOS and Android app. It uses Open Banking in combination with a direct debit authorized by you to manage and grow your money for you in an intelligent way.

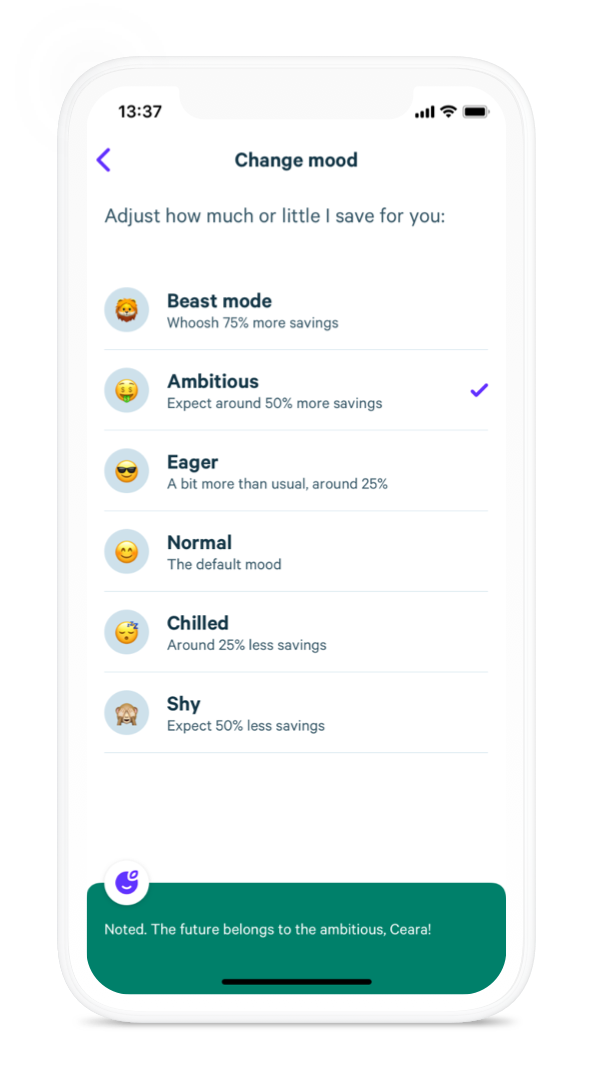

Every few days, Plum’s algorithm calculates what you can afford to stash away based on your spending habits. It then transfers that money automatically from your current account to your Plum account. In this way you put money aside regularly while barely being aware of it – so it builds up, and in due course you can spend it on things that really matter to you.

You can change the amounts the app takes at any time, and also pause the service if you wish. This means you don’t have to worry about Plum pushing you into the red. You always stay in control and can change the ‘mood’ at any time if you want to be more ambitious or cautious with your saving (see picture below).

Plum currently works with most major UK banks. The full list from the website is as follows:

Barclays

Danske Bank

First Direct

Halifax

HSBC

Lloyds

M&S

Monzo

Nationwide

Natwest

Revolut

RBS

Santander

Bank of Scotland

Starling

Tesco

TSB

Ulster Bank

Currently business accounts and joint accounts are not supported by Plum. They also do not support Channel Island bank branches.

How to Get Started

Start by downloading the app free of charge from Google Play or the Apple iStore (see links here).

Once you’ve downloaded the app and signed up, you can begin a dialogue with the Plum chatbot to help you set up your account. You will, of course, have to connect the app to your bank, so you will need to have your current account details to hand. Once it’s all set up, turn notifications on. This will allow the app to alert you when it wants to start setting money aside for you.

There is an option to speak to a real person if you need to. You can also increase or decrease the amount to stash away, set up ‘Pockets’ for specific purposes (see below), and even pause any transactions completely if you wish.

Do You Get Interest?

With the default ‘Primary Pocket’ on your Plum account the answer is no. The app is free and helps you set money aside painlessly, but Plum doesn’t pay interest on this.

Even Plum Free accounts can, however set up a secondary interest-paying Pocket. This facility is provided by Investec Bank and takes the form of an easy-access account paying 0.20% for all users

Plum Plus users can also set up one easy-access Pocket paying 0.40% interest. And Plum Pro users can have up to 10 such Pockets for different purposes, all paying 0.40% interest.

What Exactly Are Pockets?

Pockets let you set money aside with a specific goal and amount, e.g. to buy a car, save for a trip, or put down a deposit on a house. You can think of them as ‘pots’ or even jam-jars!

As money accumulates in each Pocket, the app will show your percentage progress towards achieving that goal.

All Pockets (except the default Primary Pocket) can be interest-bearing as well, as explained above. The interest paid will contribute towards achieving your goal/s.

Where Do Plum Keep Your Money (And Is It Safe?)

The app puts money away in your Plum account, which is the safeguarded account created when you sign up.

Your Plum funds in your Primary Pocket are held as e-Money by PayrNet (a subsidiary of Railsbank), Plum’s e-Money provider. Your funds are safeguarded with a UK Bank chosen by PayrNet. Your money is safeguarded because e-money cannot be lent out (this is also why it doesn’t earn interest). That same safeguarding also prevents any of Plum’s or PayrNet’s creditors from claiming your money in the event that either business should go bankrupt. Both Plum and PayrNet are regulated by the Financial Conduct Authority (the UK’s financial watchdog). Plum also boasts 256-bit TLS encryption to ensure your data is kept safe.

Money saved with Plum in interest Pockets is held on Trust with a UK Bank (Investec). A Trust is a legal mechanism that means Plum can look after your money but legally it never stops belonging to you. This means that if anything were to happen to Plum then the bank would return your money to you directly. Should something happen to the bank itself, you would be protected up to £85,000 under the Financial Services Compensation Scheme (FSCS).

How Easy Is It to Withdraw?

Transfers from non-interest Pockets back to your Primary Pocket are usually instantaneous. it is different with transfers from interest-bearing Pockets:

• When requesting an interest Pocket withdrawal before 15:00 UK time on business days, it will be completed the same day.

• When requesting after 15:00 UK time on business days or during weekends, it will be completed the next business day.

Note that withdrawals from interest and non-interest Pockets go back to your Primary Pocket initially. Withdrawals to your bank account will always be from your Primary Pocket. Such withdrawals are processed the same day (typically in around 30 mins) and will appear on your bank statement under your full name.

Other Benefits

As well as making it easier to put money aside, Plum can help you keep track of your income and expenditure. You can set it to provide daily or weekly balance updates, and it will also automatically track your transactions by category, week and month. Plum will let you know all of this without having to wade through bank statements.

In addition, Plum has AI (artificial intelligence) built in, so if it notices you are being overcharged on a bill or for a financial product, it lets you know. It will also suggest cheaper solutions for you and – if you wish – help you switch over in just a few clicks.

Plum also offers a variety of optional automated features. These include

Round Ups – Get Plum to round up your past week transactions to the nearest £1 and transfer the spare change.

52-Week Challenge – Starting with £1 in the first week, £2 in the second week and increasing up to £52 in the final week of the challenge, Plum can help you set aside £1,378 in a year. This feature is only available through Plum Pro.

Rainy Days – Once activated, Plum squirrels away extra cash automatically each day it rains where you live. This feature is also only available through Plum Pro.

Pay Days – The best time to set money aside is when you get paid, so tell Plum an amount and it’ll move this automatically for you on payday.

Plum Reviews

Plum has an average rating of 4.5 stars (‘Excellent’) from over 1200 reviewers on the independent Trust Pilot website. Just over three-quarters (76%) gave it the maximum five stars, with many mentioning the great customer service and how the app had helped them to save more. Of those who gave Plum three stars or less, the main issues mentioned were delays or problems in withdrawing. To be fair, the Plum team generally respond to such comments on the Trust Pilot website explaining how the app works and offering additional help where issues have arisen.

Final Thoughts

If you want to set more money aside but need a little help and encouragement to do so, Plum is well worth a look.

I like the way it stashes money away automatically, so in all probability you won’t even notice it. You can set it to take as much or as little as you like, and you can also make one-off additional payments if you are feeling particularly flush. You can also withdraw some or all of your money back to your bank account at any time.

Pockets are a great feature, allowing you to set aside money for specific purposes. And, as mentioned above, by using an interest-bearing Pocket, you can get interest as well (0.20% with a Plum Free account and up to 0.40% with a Plum Plus or Pro account). Obviously that’s not a fortune, but in the current low-interest rate environment it is still very competitive (and a lot better than nothing!).

In my view Plum is likely to work best for people with a regular monthly (or weekly) income. If you receive income more irregularly – e.g. you’re self-employed – it might not work quite as well. Even so, Plum say that their algorithm can detect patterns in your income and expenditure and adjust your transfer amounts accordingly.

In any event, there’s no reason not to try Plum yourself to see if it can help you set aside more. Just click through this link for more information and to sign up.

As always, if you have any comments or questions about this post, please do leave them below.

Note: This is a fully revised and extended version of my original Plum review from last year.

Disclosure: I am an affiliate for Plum so if you click through any link in this article and sign up, I will receive a modest referral fee for introducing you. This will not affect the service or benefits you receive in any way. Please note also that I am not a registered financial adviser and nothing in this post should be construed as personal financial advice.

If you enjoyed this post, please link to it on your own blog or social media:

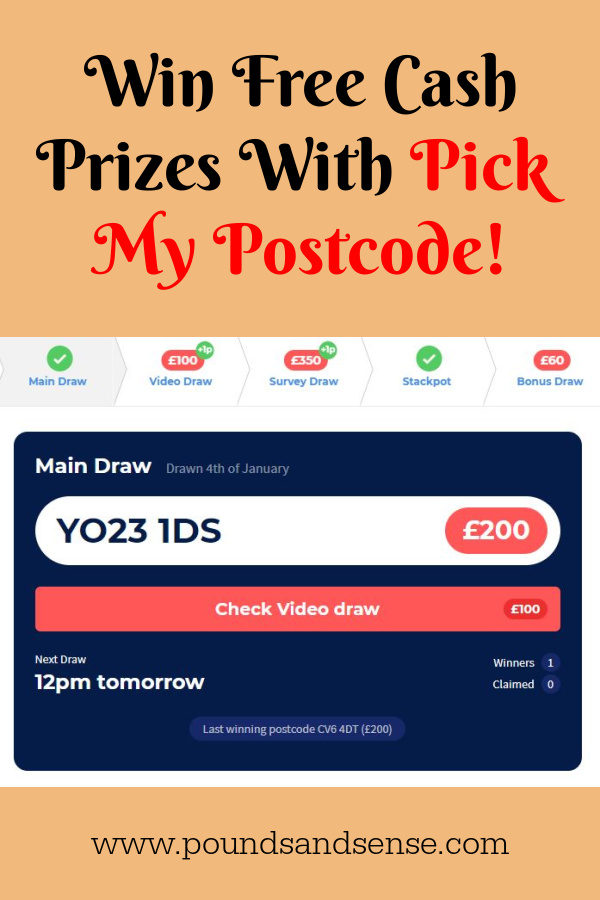

Today I’m highlighting a fun and free way you may be able to boost your income in 2021. And all you have to do is check the website in question once a day to see if your postcode is a winner!

Main Draw Each day one postcode is picked at random for this draw, which has the biggest prizes. The main daily prize – which I was lucky enough to win – can be over £1,000. When I had my own win, the prize was £1,200, though as one other person in my postcode area also claimed, the prize was split between us. So I got £600 plus a small bonus (explained below) – not a life-changing amount, but certainly a day-changing one 😀

Video Draw – To see the winning postcode in this draw, you first have to watch a short video. Though to be honest I find that you just have to watch the ad that plays first and the winning postcode is then displayed – you don’t have to watch the whole of the video unless you want to. This draw pays a minimum of £50, with the prize rolling over to the next day if not claimed. I have seen up to £400 on offer in this draw.

Survey Draw – To see if you have won this draw, you first have to complete a very short survey (generally just one question). As with the Video Draw there is a minimum prize of £50 and it rolls over to the next day if unclaimed. When I checked today there was a £300 prize, so it must have rolled over for a few days previously.

Stackpot – The Stackpot lists a variable number of postcodes with £10 prizes for those claiming them. When I checked this morning there were 14 prizes up for grabs and one that had already been claimed (it is first come, first served with the Stackpot).

Bonus Draw – With the Bonus Draw there is a daily £5 prize, £10 prize and £20 prize. To be eligible you need to have built up a Bonus (see below) equal in value to the prize in question by visiting the site regularly. So to qualify for the £20 Bonus Draw, you need to have accumulated a Bonus worth at least £20 yourself.

All lottery prizes are tax-free, of course, in accordance with UK gambling laws.

One is £5 Flash Draws. These appear at random on advertising spaces around the PMP website. They look like the sample image below. They appear to individual visitors at random. I have never seen one myself, but obviously it’s worth keeping an eye out for them. If you spot one, you just have to click to claim (it doesn’t matter about your postcode). The £5 prize is paid by PayPal as usual.

As for the Bonus, this is a sum of money that is added to your prize any time you win (with the exception of the £5 Flash prizes). It accrues over time as you visit the site. It increases by 1p for every new Main Draw, Survey Draw or Video Draw that you check. That may not sound much, but if you return to the site every day it soon adds up. My Bonus is up to £41.90 now!

If you wish, you can boost your Bonus even more by referring friends and neighbours and taking up some of the offers that appear on the site.

It’s important to note that you can’t withdraw your Bonus until you win a prize. But even £10 in the Stackpot or £5 in the Bonus Draw will qualify. So if I were to win a £10 Stackpot or Bonus Draw prize today, I would actually receive £10 plus £41.90 = £51.90. Another good feature is that your Bonus is added to your winnings every time you win a prize – it doesn’t reset to zero after a win.

I am not normally a great one for lotteries, but I make an exception for Pick My Postcode. As I said above, it’s free to enter, there are loads of prizes on offer, and the longer you go on playing, the bigger those prizes can become. And obviously, having previously won over £600 on the Main Draw myself, I know that it’s genuine and would love to win again!

Finally, if you still need further reassurances about the site, check out the reviews on the independent Trust Pilot website (average 4.8/5 stars, with 94% of people rating it ‘Excellent’).

As always, if you have any comments or questions about Pick My Postcode, please do leave them below.

Disclosure: This post includes my referral link. If you click through and sign up for free, I will receive a small commission for introducing you. This will not affect your potential earnings in any way.

If you enjoyed this post, please link to it on your own blog or social media:

Happy New Year! Here’s hoping it’s a better one for all of us than the year just past 🙁

I shall be continuing my monthly coronavirus crisis updates in 2021, at least till we are clearly over the pandemic and something resembling normal life has resumed. Obviously I very much hope that will be sooner rather than later.

Regular readers will know I have been posting these updates since the first lockdown started in the spring of 2020 (you can read my December 2020 update here if you like).

As ever, I will begin by discussing financial matters and then life more generally over the last few weeks.

Financial

I’ll begin as usual with my Nutmeg stocks and shares ISA, as I know many of you like to hear what is happening with this.

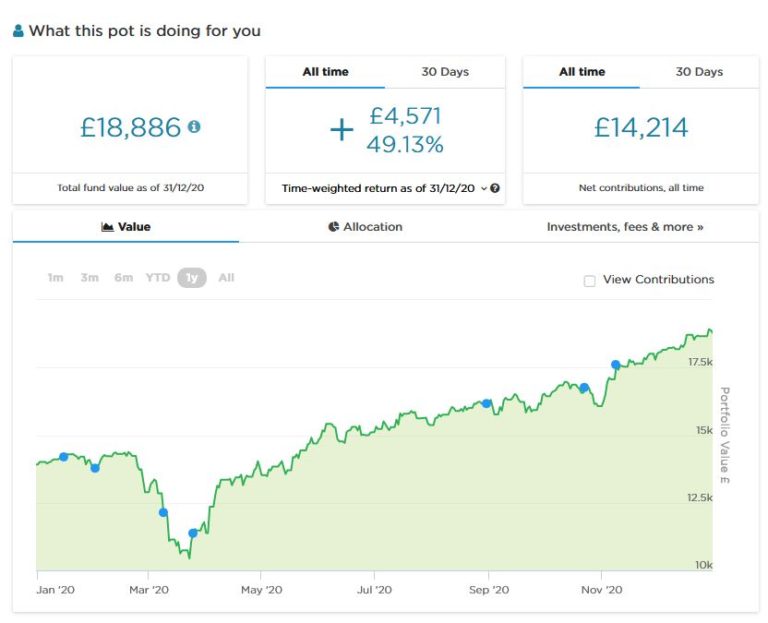

As the screenshot below shows, since last month’s update my main portfolio has continued on a generally upward trajectory and is currently valued at £18,886. Last month it stood at £18,008, so it has gone up by over £800 in value since then. Considering national and world events at the moment, I am more than happy with this.

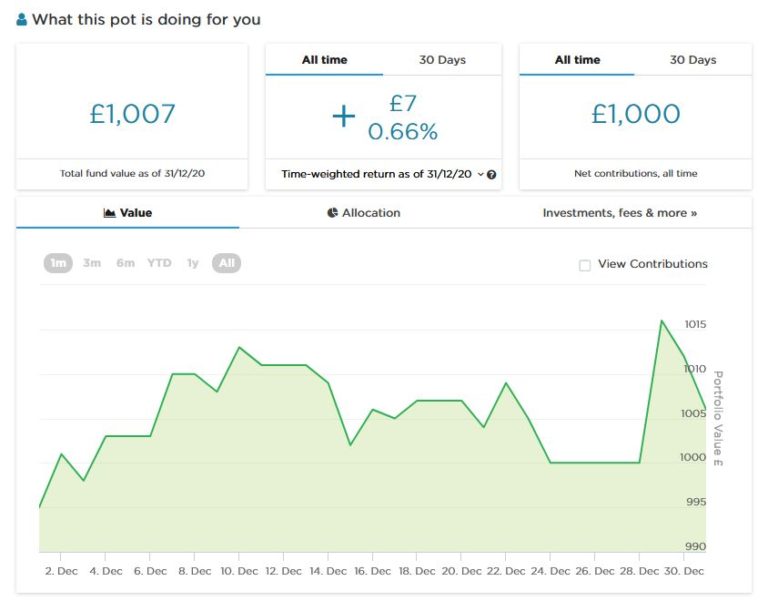

As you may recall, about a month ago I put £1,000 into a second Nutmeg pot to try out Nutmeg’s new Smart Alpha option. This pot has risen as high as £1,015 in value and currently stands at £1,007. Here is a screen capture showing performance to date, though obviously it is far too early to draw any conclusions from this.

You can see my in-depth Nutmeg review here (including a special offer for PAS readers). As a matter of interest I was recently asked by Nutmeg to contribute an article about my investing journey for their blog. I will add a link to the article here once it is published.

I had some bad financial news last month from Crowdlords, one of the property crowdfunding platforms I invested with. Three years ago I put £3,000 into a development project to build what was originally described as six eco-homes (it has lately been known more prosaically as Kennington Road). An update on the Crowdlords website revealed that due to a ‘perfect storm’ of problems caused directly or indirectly by the pandemic, the development had made a loss and investors would receive no returns. At a stroke I lost £3,000, which was (as you may imagine) a bitter pill to swallow.

I plan to write a more in-depth post about this soon, including lessons learned from the experience. But i will say two things now. One is that property development projects are inherently very risky and you shouldn’t invest in them unless it really is money you can afford to lose in a worst-case scenario. And second, while I don’t blame Crowdlords themselves for the failure of this project, I do think their communications about it could have been a lot better. I also think it would be a nice gesture if they were to offer modest ex-gratia compensation payments from their own profits to investors who have been hit hard (I know some people lost a lot more than I did). Events such as this clearly damage the reputation of property crowdfunding and mean investors are less likely to risk their money this way in future. I know I shall certainly be a lot more cautious now!

In fairness to Crowdlords I should add that I have had other investments on their platform which did deliver the promised returns, However, with the loss described above I am certainly down overall with them.

On a brighter note, a couple of the loans I invested in with Kuflink were repaid (with interest) last month, and I duly reinvested the money in other loans.

Kuflink is primarily a platform for investing in bridging loans, and generally these are safer than development projects such as the one mentioned above. There is still a risk of loss, of course, but as your investment is secured by bricks and mortar, it is unlikely you would lose all your money (though delays in repaying loans can and do happen). I have a diversified portfolio of loans with them paying annual interest rates of 6 to 7.5 percent. These days I generally invest a few hundred pounds per loan at most (and quite often under £100). My days of putting four-figure sums into any single property investment are definitely behind me now!

As you may be aware, I recently updated my full Kuflink review. You can read it here if you like. They recently passed the milestone of £100 million loaned, and say that since their launch no investor has lost money on the platform. I’d particularly draw your attention to their revised and more generous cashback offer for new investors. They are now paying cashback on new investments from as little as £500 (it used to be £1,000). And if you are looking to invest larger amounts, you can earn up to a maximum of £4,000 in cashback. That is one of the best cashback offers I have seen anywhere (though admittedly you will need to invest £100,000 or more to receive that!).

Moving on, my two Buy2LetCars investments are still delivering the promised monthly returns without any fuss. As I am semi-retired but don’t yet qualify for the state pension, the £450 or so I receive from them every month represents a major part of my monthly income currently.

As you may remember, investors with Buy2LetCars put up the money to finance a car for a key worker such as a nurse or police officer. They then receive 36 monthly capital repayments followed by a final balancing payment of interest and capital. If you are looking for an income-producing investment with a substantial lump sum payment after three years – and you like the idea of doing a bit of good with your money too – they are well worth checking out (and likewise if you’re a key worker looking for a lease car yourself). If you’d like to learn more, you can read my review of Buy2LetCars here and my more recent article about the company here. And here is a link to Wheels4Sure, their car-leasing website.

Finally, I am still getting a few queries about the low-key matched betting opportunity mentioned in some previous updates. I checked with my contact there and they are still accepting new members, but for reasons related to the pandemic have had to reduce their payouts slightly. New members now receive £50 a month for the first six months, reducing to £25 a month thereafter. Considering that this opportunity is cost-free, risk-free and hands-free, that’s still a pretty good deal, though 🙂

As I said above, this opportunity is based on matched betting, a sideline-earning opportunity I have been pursuing for several years myself. I was asked not to divulge too many details about it publicly, for good reasons I will explain privately to anyone who may be interested (and no, it’s not illegal!). As I said above, it doesn’t require any financial outlay, is entirely hands-off, and will provide a passive income of £50 a month for the first six months and £25 a month thereafter.

No knowledge of betting is required, and you won’t have to place any bets yourself (this is all done by the company’s clever software). You just have to set up a separate bank account for bets to go through, but running the account is entirely financed by the company. Please note though that this opportunity is only open to trustworthy people who haven’t done matched betting before and have no more than two accounts already with online bookmakers. For more info (and to receive a no-obligation invitation) drop me a line including your email address via my Contact Me page.

Personal

December was another strange month in a depressing year.

A week before Christmas I had my 65th birthday. Normally reaching that landmark would be cause for celebration, but inevitably in the circumstances it was low key. I did at least manage to meet up with a couple of old friends for a birthday tea (don’t tell Matt Hancock!). It was great to see them and they did their best to make the occasion feel special. We had some laughs and a very nice cake, but it still wasn’t anything like I might have imagined my 65th. I didn’t even have the small consolation of being able to start claiming my state pension, as I am in the cohort of people for whom the age has just been raised to 66.

Work-wise it has remained very quiet (as you probably know, I’m a semi-retired freelance writer/editor). I’ve had very little paid work since the pandemic started and was grateful to receive further financial support from the government’s SEISS scheme. This time round you had to state that your income had been directly affected by the pandemic. I did agonize a bit over this, as it begged the question of how much money I would have been earning if things were normal. I honestly don’t know the answer to that, but it seems to me that the pandemic and government counter-measures have stopped the economy in its tracks, meaning there is less work around generally. Anyway, I applied and was paid without quibble.

The main good news over the last few weeks has concerned the vaccines. Two are now approved, with the Pfizer vaccine being distributed since before Christmas and the Oxford-AZ version coming on stream this week. One benefit of turning 65 is that I have presumably moved up the pecking order to receive it.

The government appears to be pinning all its hopes on vaccines bringing this pandemic to an end by spring/summer. I hope they are right, as the next couple of months in particular look pretty grim. At the time of writing my area has just moved to Tier 4, which effectively means lockdown. So I will have little/no opportunity to see friends or relatives, no more swimming, no more trips away, and the prospect of sporting ‘lockdown hair’ again. But I am still lucky compared to many, I know.

In my blog post Surviving the Covid Winter I mentioned some plans I had for getting through the winter months. In December I started several of these. In particular, I began a couple of DIY jobs I had been putting off. One of these was redecorating the en suite. Initially I planned just to repaint one wall where the paintwork was fading. But the new paint colour didn’t match the old one, so I am now planning to repaint the rest of the room as well. As is so often the case with DIY, what appeared a small job at first has grown into a much bigger one!

I have also taken my first tentative steps in the world of video gaming (my experience prior to this had been limited to Space Invaders/Asteroids and the games bundled with MS Windows such as Solitaire). With some trepidation I signed up with the games platform Steam and downloaded Coffee Talk to my Windows laptop. This was a game I had read about some time ago and liked the sound of. Here’s a typical scene from it…

Coffee Talk is actually more like an interactive movie or novel. You take the role of owner/barista at a late-night coffee shop in an alternative Seattle frequented by a mixture of human beings and mythological characters such as elves.

Mostly your customers chat with you and other customers about their lives and problems, while you prepare coffee and other drinks for them. This isn’t especially taxing, though I was quite pleased when one of the regulars, Freya, returned and asked for ‘the usual’ and I remembered what it was. It’s a pleasant enough way of spending a few hours, though I am thinking I might try something a little more ambitious next time 🙂