The number of people applying for Universal Credit has surged to record levels as a result of the Coronavirus pandemic and the numbers are set to rise further with the ongoing economic uncertainty.

In addition to a loss of income, households could also be facing a rise in energy-bills due to more time spent at home and cold weather approaching. Many will be coming to grips with the benefits system for the first time and starting to understand the rules, regulations and complexities around making a claim.

However, there is a little known silver lining for these claimants. Anyone who has claimed Universal Credit successfully will also be eligible for home improvements under the Government’s Energy Company Obligation (ECO) scheme.

This current scheme, called ECO3, targets people that have high energy costs comparative to household income. The scheme has a list of ‘qualifying benefits’ for eligibility. Universal Credit is on that list.

Plus, there are no savings or income-tests for the qualifying benefit part of the application, so if you receive any benefit on the list below (excluding Child Benefit, as that has an income cap), it’s likely you’ll be eligible.

According to Ofgem (who administer the ECO scheme), claimants will still be eligible for a period of 18 months following the date of the letter for the Universal Credit award (page 44 of the Ofgem ECO3 guidance has full details).

So if, say, you were awarded your Universal Credit in April but you got a job last week and came off Universal Credit today (for example), you still have a significant period of time (a year and a half) to apply for and install the measure, as you would still be classed as eligible even when you return to work. While you can wait to apply, it’s advisable to apply sooner rather than later, as funding rules can change at any time.

Even if you have returned to work or are planning to return to work, you will still be eligible, providing you have had at least one award for Universal Credit.

And it isn’t just Universal Credit recipients who are eligible for grants. Also on the ‘qualifying benefits’ list are the following:

You will still be eligible if you return to work as you can claim for a period of 18 months after claiming benefits.

What Grants Are Available?

There are a range of energy-efficiency measures that can be installed under the Energy Company Obligation (ECO) scheme, including boiler upgrades, home insulation and heating upgrades. The Scheme is funded by the major energy companies and if you claim benefits, you are entitled to this funding.

Table: Measures Available Under the Energy Company Obligation Scheme

Measure

Homeowners

Private Tenants

Housing Association Tenants

Landlords

Council Tenants

Air Source Heat Pump (ASHP)

✅

✅

✅

❌ Landlords ✅ Private tenants can apply

❌

Boiler Upgrade or Repair

✅

❌

❌

❌

❌

Cavity Wall Insulation

✅

✅

✅

❌ Landlords ✅ Private tenants can apply

❌

Electric Heating Upgrade

✅

✅

✅

❌ Landlords ✅ Private tenants can apply

❌

First Time Central Heating (FTCH)

✅

✅

✅

❌ Landlords ✅ Private tenants can apply

❌

Internal Wall Insulation

✅

✅

✅

❌ Landlords ✅ Private tenants can apply

❌

Underfloor Insulation

✅

✅

✅

❌ Landlords ✅ Private tenants can apply

❌

How Much Could You Get?

The amount of funding available depends on a range of factors, including property type, your existing heating, wall type and potential energy savings from proposed work.

The first step in working out what you could get is to check your eligibility online. There’s a quick form on the Energy Saving Genie website where you can enter your details to see if you are eligible.

If you meet the criteria, you can choose to apply and once your application has been submitted, it will be passed to a Registered Installer.

The Registered Installer will arrange a free survey of your property. You can choose to proceed ASAP with a survey taking place following strict health and safety guidelines or you can choose to wait until after Covid-19.

Once the survey has taken place, the surveyor will report back to the Registered Installer, who will talk you through the grants that are available towards energy-efficiency measures at your property.

The grant is paid directly to the installer and they are awarded on lifetime savings (LTS) scores. Currently electric heated properties and larger properties tend to receive the most funding. But even if your home isn’t large or heated by electricity, it is worth applying as you could still receive a significant grant towards home improvements.

So if you are one of the many million new Universal Credit claimants due to Covid-19, you can start the process of applying for a home improvement grant that will knock £££s of your energy bills for years to come, well after the pandemic has passed.

Disclosure; This is an adapted reblog of an original post by Energy Saving Genie. It is also a sponsored post. If you click through and end up taking advantage of this government scheme, I will receive a fee for introducing you. This will not affect any products or services you may receive or the value of any grants you may be awarded.

If you enjoyed this post, please link to it on your own blog or social media:

Another month, another coronavirus crisis update. Regular readers will know I have been posting these updates since the first lockdown started (you can read my October update here if you like).

As always, I will discuss what has been happening with my finances and my life generally over the last few weeks.

Financial

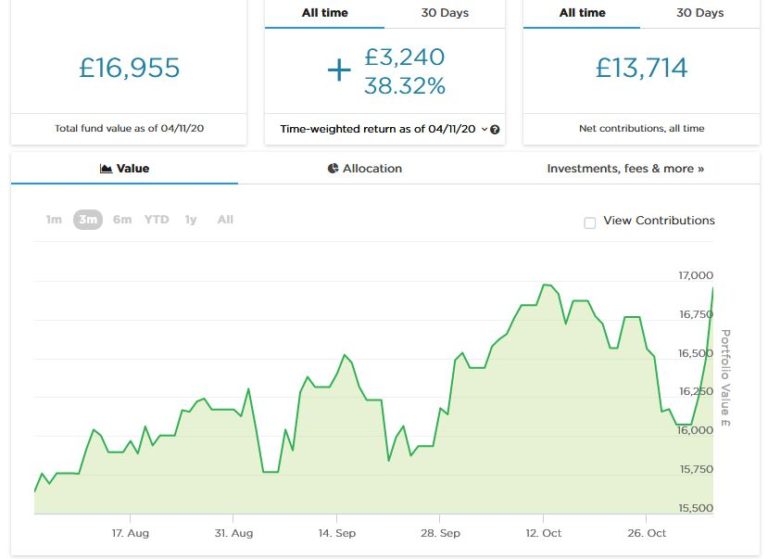

I’ll begin as usual with my Nutmeg stocks and shares ISA, as from feedback received I know many of you like to follow this.

As the screenshot below shows, my portfolio has been on a roller-coaster ride over the last few weeks but is currently valued at £16,955, about £500 up on last month. Considering national and world events at the moment I am very happy with this. You can read my in-depth Nutmeg review here (including a special offer for PAS readers).

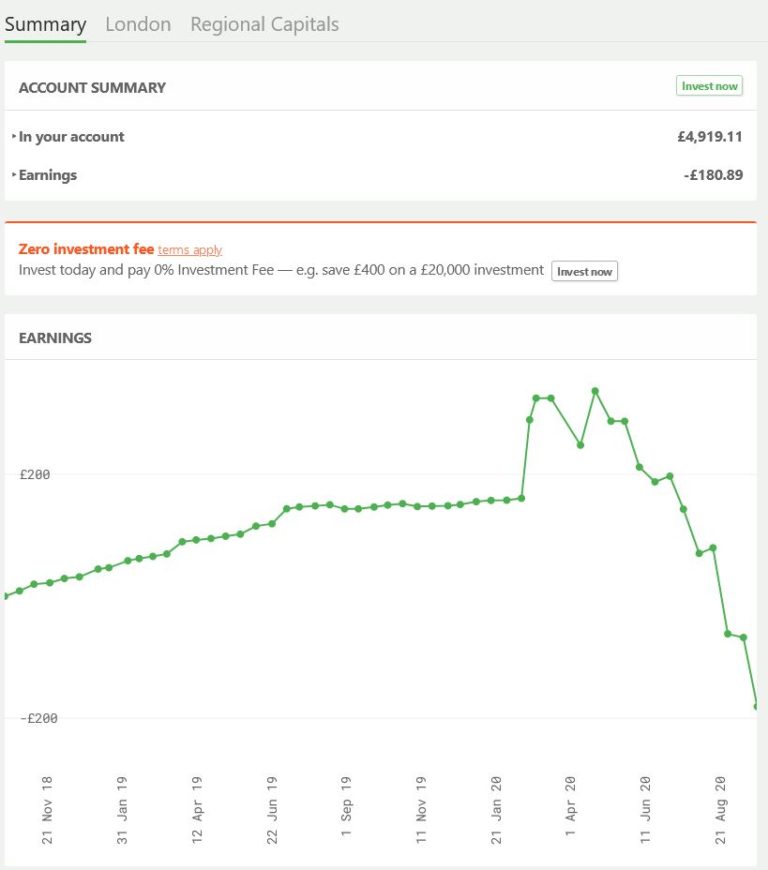

I haven’t mentioned my Bricklane Property ISA for a while, so I thought I should rectify that this month. As discussed in my blog review, Bricklane – not be confused with Brickowner – is a REIT (Real Estate Investment Trust). Investors’ money is pooled to purchase properties. Rental income is then distributed to investors, who also stand to benefit if the value of the REIT goes up. As you can see from the chart, though, this year the trajectory has been largely downward.

.

At first glance this looks alarming, but of course it’s important to note that the vertical axis of the graph goes from minus £200 to plus £200, so in reality the losses aren’t as bad as that scary-looking precipice might suggest. Allowing for the fact that I received a £100 welcome bonus when I signed up with Bricklane, overall I am about £80 down on my £5,000 investment. Of course, that’s not what you would hope for, but this has been a particularly tough year for anyone investing in property. Among other things, rising unemployment, company failures, more people working from home, and rising defaults on loans and mortgages (along with mandatory payment holidays) have all affected demand and reduced rental returns and property values.

A recent email from Bricklane gave further insight into the problems they are facing. It turns out that the Regional Capitals fund (in which I am invested) includes a number of properties that may need extensive refurbishment in light of the Grenfell Tower tragedy. As I understand it, they have cladding which needs assessing by specialists and may have to be removed and replaced. This is a time-consuming and costly business. Of course, the owners (who include me as an investor) have no option but to undertake this, and inevitably this is having an impact on the value of the fund.

This does of course illustrate that any investment in a single asset class such as property carries additional sector-specific risks compared with broader-based investments, and you may see greater volatility as a result. On the plus side, when investing in property your money is secured by bricks and mortar, so it’s very unlikely you will lose your shirt.

I guess if I was braver and had a longer time horizon, I might look at Bricklane as a value-investing opportunity just now. As it is, I am leaving my money where it is but won’t be investing any more with them for the foreseeable future. I am not planning to sell up as I don’t currently need the money and that would only crystallize my losses.

Otherwise there is nothing dramatic to report on the financial front. My two Buy2LetCars investments are still delivering the promised monthly returns without any hassle. To recap, investors with Buy2LetCars put up the money to finance a car for a key worker such as a nurse or police officer. They then receive 36 monthly capital repayments followed by a final balancing payment of interest and capital. I heard from the company today that they are allowed to continue trading in England’s second lockdown and are already experiencing an upsurge of enquiries from key workers needing transport. So if you are looking for an income-producing investment with a substantial lump sum payment after three years, they are well worth checking out (and likewise if you’re a key worker looking for a lease car yourself). If you’d like to learn more, you can read my review of Buy2LetCars here and my more recent article about the company here. And here is a link to Wheels4Sure, their car-leasing website.

My Property Partner and Kuflink investments are still both ticking along satisfactorily. Unsurprisingly there have been delays in repaying some of my Kuflink loans, but I continue to receive monthly interest payments on them and am not unduly concerned. As regards The House Crowd, I assume that the sales of the two properties in which I hold £1,000 shares are progressing, but can understand that it is a slow process. As with Kuflink, rental payments are still accruing, which should help to defray some of the selling costs.

There has been no further word either regarding my investments with Crowdlords. As I said last month, I have two remaining investments with them, Kennington Road eco-houses and Trent House. I was told they hope to have exit options for these properties by the end of the year, but I’m not holding my breath. On the plus side, they are paying 6 percent interest on my Trent House investment, which is quite generous in these days of ultra-low interest rates.

Personal

Thankfully this month has been less eventful for me than the previous one. Touch wood my left eye is recovering well after the laser treatment (thank you to those who have asked and/or sent me good wishes about this). I am going back to Burton Hospital in a week’s time for what I hope will be a final check-up.

I still have floaters in both eyes – worse in the left – but that is not unusual for people of my age. It’s annoying but not dangerous in itself, and there isn’t really any treatment (I understand lasers can be used in extreme cases to ‘blast’ them, but it’s rare to do this as it risks causing other damage). I did read online about a Chinese study which found that eating pineapple can help reduce floaters, so I was happy to have an excuse to eat more of this delicious fruit!

As I write this, England is going into its second lockdown. I am dubious about the wisdom of this and worried for people whose physical and mental health is likely to suffer, especially as it appears the second wave has already peaked and new case numbers are starting to fall.

I am at least thankful that the schools have been exempted this time. I live quite near a secondary school, and it lifts my spirit when I see the young people bursting out of the school gates at the end of the day. chatting to their friends, larking around, and generally doing all the things young people do. And not a mask in sight!

Today I am off to see my accountant to discuss my annual accounts. He works from home and neither of us was sure what rules applied in this situation, so in the end we agreed to meet outside on his front drive. At least this will help to ensure that the meeting doesn’t go on a minute longer than it needs to 🙂

I had a winter flu jab last month (the first time I’ve qualified for a free one as I reach 65 later this year). It seemed a sensible thing to do, especially as it may give some protection from Covid too. I did have a reaction to it, though. I woke up at around 2 am shivering violently, and then I started to get nausea as well. By morning I was feeling a lot better, apart from having had almost no sleep. Apparently these are quite common side effects of the vaccine, though two friends (both older than me) didn’t get any effects at all.

I went for my last pre-lockdown swim on Tuesday. The centre was busier than usual, so I guess I wasn’t the only one who decided to take the opportunity while it was still available. I am very disappointed that pools have been made to close again as there is no evidence the virus is spreading this way and many people (me included) depend on swimming for our physical and mental health. I just hope they reopen at the start of December and the lockdown isn’t extended. Personally I expect the numbers of new cases to continue falling over the next few weeks, not due to the lockdown but simply because that is the trend now. If that is the case, there will be no excuse for prolonging the lockdown. But I guess by the time of my December update we will know one way or the other!

Finally I am still dutifully completing the UCL Virus Watch weekly questionnaire saying whether I have any possible Covid symptoms (none so far). And I am still waiting to hear when I will be able to take the blood test to see if I have any antibodies or other natural resistance to the virus. But I gather they wouldn’t be able to do that until a few weeks have elapsed after the flu jab anyhow, so it may be just as well I’ve heard nothing yet.

So that’s it for this month really. I hope you and your loved ones are staying safe and well. As always, if you have any comments or questions about this post, please do leave them below.

Disclosure: This post includes affiliate links. If you click through and make a purchase, I may receive a commission for introducing you. This will not affect the price you pay or the product or service you receive.

If you enjoyed this post, please link to it on your own blog or social media:

For many of us, our mortgage is our biggest monthly outgoing. So it’s important to keep a close eye on it and check regularly whether you could save money by switching to another provider.

That’s exactly what a new online service called Dashly aims to do. They evaluate your current mortgage deal against the whole market, taking into account your specific personal circumstances as well. If they find a better deal for you they let you know and – if you choose to proceed – assist you with the switching process.

How Does Dashly Work?

Dashly is available as a desktop site, with mobile apps for iOS and Android coming soon.

You start by registering and entering some details about your current mortgage and your personal circumstances. The latter is important, as things such as your income, employment type, credit score and age can all affect the deals you could be eligible for. This process takes 10-15 minutes. Dashly then compares your mortgage against an average of 10,000 products to find the best deal for you.

If they find a better deal than your present one, they send you a notification. You can then evaluate this and decide whether you want to switch. If you do, the team at Dashly will assist you with the switching process.

In addition, Dashly will continue monitoring your mortgage every month. If they find you could save money by switching again, they’ll let you know. It’s worth noting that the equity you have in your property changes on a monthly basis due to ever-changing house values and your decreasing mortgage balance. As your LTV (loan-to-value ratio) decreases, your mortgage may qualify for better, cheaper deals. Again, Dashly checks this on your behalf.

You receive a detailed personal report from Dashly about your mortgage every month. In addition, your dashboard will show you all the key facts at any time, from the changing value of your property to the amount of equity in it, any current deals that would save you money to your next payment date. It’s all there on one easy-to-read web page.

How Much Could You Save?

The savings can be substantial. Dashly say that on average their users save £2,620 (see footnote).

Of course, in practice savings will depend on a number of things, including the balance outstanding on your mortgage, the competitiveness of your current deal, the term left to run, and the effect of any early repayment penalties. Dashly takes all of these things into account in determining whether you could save money by switching to a new lender (and by how much).

Are There Any Costs?

Using Dashly is free. There are no hidden charges and Dashly say they will never hit you with advertisements or email campaigns to try to make money from you. They get paid out of mortgage provider fees, and are authorized and regulated by the Financial Conduct Authority.

Dashly are also founding members of Finance For Good, a charity run by social impact fintechs who put consumers first. They say that their security rivals that of the world’s leading banks.

In Conclusion

If you have a mortgage, in these uncertain times it’s more important than ever to ensure that you aren’t paying over the odds for it.

Dashly offers a free service that not only checks whether you are getting the best deal currently but also continues monitoring your situation month by month and recommends switching again if a new and better deal arises.

By using Dashly you could painlessly save hundreds or even thousands of pounds on the cost of your mortgage. There is never any obligation to switch or any fee to pay for the service. So you really have nothing to lose and everything to gain by registering for an account today.

Footnote: Your individual savings may vary and will depend on personal circumstances. £2,620 per year is the average amount based on research Dashly has conducted on the mortgage market. Find out more at www.dashly.com/reference-index.

Disclosure: This is a sponsored post on behalf of Dashly. If you sign up and make use of the service, I may receive a referral fee for introducing you. This will not affect in any way the service you receive or the deals you are offered.

If you enjoyed this post, please link to it on your own blog or social media:

Life insurance isn’t the most exciting of subjects, but in these uncertain times it’s something we all need to think about.

Not everyone requires life insurance. If you are single with no dependants and/or on a very low income, it may not be necessary or appropriate for you. But if you have a partner, children or other relatives who depend on your income, you probably should have life insurance to help provide for them in the event of your death.

What Is Life Insurance?

Life insurance is a type of insurance policy that protects your loved ones financially if you die. It can help minimize the financial impact that your death could have on your family and provide peace of mind for you and them.

Most life insurance policies are designed to pay a cash sum to your loved ones if you die while covered by the policy. This can help them cope with everyday money worries such as mortgage payments, household bills and childcare costs. It may also cover funeral costs. You can take out life insurance under joint or single names, and you can pay your premiums monthly or annually.

There are two main types of life insurance: term life insurance and whole of life insurance.

Term life insurance policies run for a fixed period such as 10, 20 or 25 years. These types of policy only pay out if you die during the term of the policy. A whole-of-life policy, on the other hand, pays out no matter when you die (as long as you keep up with your premium payments, of course).

There are three different types of term life insurance. With decreasing term insurance, the amount payable on death reduces over time. This type of policy is often taken out in conjunction with a mortgage as the payout reduces over time in line with the amount needed to clear the outstanding debt.

You can also get increasing term insurance, where the payout rises each year (typically to take account of inflation) and level term insurance, where it remains the same throughout. Not surprisingly, level term and (especially) increasing term policies are more expensive than decreasing term.

What Doesn’t It Cover?

Life insurance normally pays out only on death. If you become unable to work due to an accident or illness, you won’t generally be covered.

Some life insurance policies will pay out if you receive a terminal diagnosis. This is by no means always the case, though, so it’s important to check the wording of your policy carefully.

Most life insurance policies also have some exclusions, e.g. they might not pay out if you die from alcohol or drug abuse. In addition, if you take part in risky sports, you may have to pay a higher premium. If you have a serious health problem when you take out a policy, any cause of death related to that illness may be excluded.

For the above reasons, you may also want to consider taking out critical illness cover. This covers you if you get one of the medical conditions or injuries specified in the policy. Some examples of critical illnesses that might be covered include heart attack, stroke, cancer, and chronic, life-limiting conditions such as multiple sclerosis and MND. Most policies will also consider permanent disabilities as a result of injury or illness. These policies only pay out once and then the policy ends. Some policies will make a smaller payment for less severe conditions, or if one of your children contracts one of the specified conditions. Health conditions you knew you had before you took out the insurance won’t generally be covered.

What Does It Cost?

Life insurance can be surprisingly good value. Premiums start at just a few pounds a month. Prices vary a lot, however, so it’s important to shop around and take advice as appropriate.

A variety of factors may affect the price you are quoted. They include the following:

your age

your health

your weight

your occupation

your lifestyle

whether you smoke

your medical history

your family’s medical history

the length of the policy

the amount of money you want to cover

whether you want decreasing, level or increasing term cover

Other things being equal, the younger and healthier you are, the cheaper your policy is likely to be. But as the list above indicates, many other factors can affect the price you are quoted. In addition, women are typically charged a little less than men, as on average they live a few years longer.

The Bespoke Option

As you can see, while life insurance is a simple concept, in practice there are many variations. It is therefore important to establish what is the most appropriate option for you and your family, and shop around to get the best price for this.

A company that can help with both these things is Bespoke Financial. They are independent insurance and mortgage brokers, and will take the time to establish your exact requirements and design a ‘bespoke’ package to suit you and your family’s needs. Their trained advisers will visit you in your home (with all necessary Covid precautions) or you can speak on the phone to them. They can arrange all types of life insurance, critical illness cover, cover for long-term illness or disability, and so on.

To get an initial personalized quote, click through to the Life Insurance page of their website and answer six quick questions. You can then discuss this with an adviser to ensure you will be getting exactly the right type and level of cover for your needs.

And as an added bonus for readers of my blog, you can get a free will just by asking for a quotation. You can’t say fairer than that, now can you?

As always, if you have any comments or questions on this post, please do leave them below.

Disclosure: This is a sponsored post on behalf of Bespoke Financial. If you click through one of the links and end up making a purchase, i will receive a commission for introducing you. This will not affect in any way the product or service you receive.

If you enjoyed this post, please link to it on your own blog or social media:

2020 has been a year like no other. And while the first vaccine has just been approved, for many of us this winter still looks like being a long, hard and stressful one.

There is no doubt many people’s mental health has been impacted both by the threat of the virus and the measures taken by government to try to control it. Add to that, many people have seen their income reduced or lost their jobs altogether, causing financial hardship as well.

Clearly we all need to find methods for getting through this difficult time. So I asked some of my fellow bloggers to share any tips they might have, including things they are doing to help them (and their families) cope. I have listed their answers below, with my own reactions in italics afterwards where relevant. I will then say a bit about how I am planning to get through the Covid winter myself.

Bloggers’ Tips

Jo Jackson who blogs at Tea and Cake for the Soul says, ‘List your outgoing payments and see what can be got rid of or reduced. List all of your utility accounts, insurances and entertainment packages then look at comparison sites to see if you can get better deals elsewhere.’

Always a good idea and can save you a lot of money. Check out cashback websites as well, as they may offer cashback if you switch to a new supplier.

Sally Allsop of Life Loving says, ‘Buy yourself a big thermos or two and fill them with hot drinks and homemade soup. Then you can still go for days out without having to worry about mingling and queuing at eateries/cafes. You’ll also be able to keep yourself warm on theoretically safer outside winter activities.’

Hayley Muncey, who blogs as Miss Manypennies, says, ‘I’ve applied for the 30 hours’ free childcare funding for my 3-year-old. Normally I love taking her out and about to playgroups, the library and meeting to play with her little friends, but since everything is cancelled, closed and we’re not allowed to meet anyone (local lockdown), preschool is basically the only social activity she’ll have, so I’m going to up her hours. I think she’ll have more fun there than stuck at home! Plus it gives me more time to concentrate on working from home, so hopefully I can bring in a bit more money.’

I didn’t know anything about this scheme, but there are more details on this government website if you may be eligible. In England you need to have a child who is 3-4 years old. Other schemes apply in different parts of the UK.

Jennifer Graudenz of Monethalia says, ‘Sign up at your local library. Many libraries let you take out eBooks, so you will always have something to read, no matter how many lockdowns we have.’

Good idea. You can still borrow ordinary print books as well but special Covid precautions are likely to apply. Ask at your library for more info.

Ryan Maley who blogs at A SIngle Step says, ‘Try to keep some sort of routine, even if you are stuck in the house all day. If you’re working from home, make sure you stick to set hours with a lunch break, and have a separate space in which to work. Organise calls, video calls, quizzes and virtual catch-ups with friends and family. Try to get fresh air or exercise whilst following the rules. A run after work or exploring some local countryside can do wonders. Or even dancing along to a YouTube video in your bedroom. Most of all, if you are struggling, make sure you speak to friends or family. A problem shared really is a problem halved.’

Claire of Stapo’s Thrifty Life Hacks writes, ‘We are a family of three and a few weeks ago we invested in waterproofs for the whole family. We started walking a lot at the start of lockdown and as things ramp up again, we know that we will want to get out and explore where we can. As we now have all the right gear, we are hopeful that the rain and wind won’t put us off getting out there as autumn turns into winter.’

Fiona Hawkes who blogs at Savvy in Somerset says, ‘We’ve started planning at-home Christmas activities, as trips to visit Father Christmas and big family gatherings won’t be happening this year. I’m making my daughter an activity advent calendar for us to enjoy during December which includes things like Christmas story books, festive cake making, writing letters and cards to family we won’t see and making lovely decorations for our home.’

Human Carley, who blogs at the wonderfully named Unicorn Puffs and Rainbows, says, ‘Make your house as cosy as you can. Clear out anything you can now whist charity shops and recycling centres are open. Having as much usable space as possible will be important, as we will have much less time outside.’

You could sell anything you no longer need on eBay or similar sites to boost your income as well. There are some great tips about selling on eBay in this guest post by Lucy Olivia.

Anisa Alhilali who blogs at Two Traveling Texans says, ‘Feed your travel wanderlust. Even if you can’t travel there are ways to have “travel-like experiences” from home. You can take a virtual tour, have a travel-themed night, read a travel book, and more.’

Love this idea. You could start planning for future post-Covid adventures.

And Anisa also has a blog called Origami Expressions. She writes: ‘Take advantage of the time at home and learn origami. It is great for mindfulness and you will be amazed at all the things that you can make with just a sheet of paper!’

And it costs almost nothing as well. I may just try this myself!

Victoria Sully who blogs at Healthy Vix says, ‘Make sure you have ways to relax and chill at home to reduce the stress. This year I have just invested in a bath pillow, fluffy bath mat, candles and some soothing bath foam to indulge in some some luxurious baths this winter to take the stress away! Even something as simple as lighting candles in the evening can be calming and help to reduce stress.’

Anne Fraser who blogs at The Platinum Line says, ‘My lifesaver at the moment is our local leisure centre. Although a lot of classes have been cancelled they are still hosting an over 60s lane swim twice a week. I think it is important to find an indoor activity you enjoy and if it makes you healthier so much the better.’

Absolutely. I love swimming and was so relieved when my local leisure centre and pool reopened.

Vicky Smith of More Than A Mummy says, ‘For Christmas we will only buy gifts for the kids in the family. Will save valuable cash at a time when our business has been hit hard by the pandemic. We actually started doing this last year and it saved me hundreds as our family is huge!’

Jenny Tate of The Life Stuff says, ‘Check with your current suppliers to see if you can make any savings i.e. gas, electric, TV, internet providers. My internet bill was put up last week to £54/month so I called up the provider and got the exact same package for £26!’

Shelley Whitaker who blogs at Wander & Luxe says, ‘We are preparing at home by making sure we have plenty of things to entertain ourselves and our toddler. For example, crafts, puzzles, things to cook and DIY bits for around the house. We are also purposely not watching too many movies or TV shows so we have things we want to watch if needed. For now I am trying to get out each day and do normal things that I am able to (restrictions permitting), and basically just take each day as it comes.’

Sarah Bailey of Life in a Breakdown says, ‘Think about making some family time using a video calling service. Some of them cost after so long but some don’t, so shop around and don’t just use the one most spoken about. It will allow you to keep in touch with family during this time should the worst happen!’

Emma Reid who blogs at Emmareid.net says, ‘Just because it’s chilly doesn’t mean you can’t still go exploring and get outdoors. We are doing 1000 hours outside challenge and we still have a bit of a way to go to hit it so I am making the most of the days we have left to get outside whatever the weather. As long as you have the right gear, you can still have fun.’

Finally, Emily Jane of Emily Underworld says, ‘While winter means Christmas and the season of giving, don’t forget to practise self-care. This can be anything from rest to time alone for meditation. As my budget for Christmas this year is low, I’ll be supporting small UK businesses, as well as making some gifts myself. Getting creative is great for self-care, and it’s also great for my bank balance.’

Yes, as well as being kind to others we also need to be kind to ourselves at this difficult time. And I do agree as well with supporting local businesses, many of whom are having a very tough time of it.

My Own Thoughts

I have also been thinking a lot about how to stay sane and well over the coming months.

As you probably know, I’m semi-retired and live alone. Nowadays blogging is my main source of earned income. It doesn’t make me a fortune – far from it – but I’m lucky enough to have savings and investments and a small personal pension as well to keep my finances ticking over.

As well as being a source of income, working on the blog gives my days a bit of structure, which we all need at the moment. I typically spend a few hours each morning on it, then do other things (e.g. going for a swim or a walk) later. I feel as though once I have got my ‘work’ out of the way I have earned the right to do other things I enjoy. Though I do enjoy writing and blogging as well, of course!

I am planning other activities as well. Some friends told me recently that over the winter they intend to get on with some decorating projects. While that doesn’t appeal so much to me, there are a number of jobs around the house and garden that I really do need to tackle. I plan to make a list of them and see how many I can tick off before the spring!

I am also considering getting into video gaming – though as I spend a lot of time anyway at a computer or watching TV, I am not entirely sure I should be lining myself up for more hours staring into a screen.

I’m also thinking of teaching myself a musical instrument – possibly tenor ukulele, as I have heard they are among the easiest instruments to learn, although I am open to other suggestions 😀

I am also trying my best to keep some sort of social life going, even in the face of mounting restrictions. I don’t live in an area under lockdown (yet) so am hoping and planning to go on meeting friends for pub lunches. I am also keeping in touch with friends/relatives as much as possible using video calling and traditional phone calls. It has been particularly good to be in more regular touch with my sister Annie, who also lives alone. We speak on the phone most weekends now, and it’s been great to hear what’s been going on in her life and her job (she works as a librarian).

I agree with my fellow bloggers who pointed out the importance of staying active even in the cold winter months. I aim to go swimming at least once a week and really enjoy this, not least because it’s something normal I can still do at a time when our freedom of action is increasingly limited. I also try to go for a walk every day, though as the weather worsens I suspect I won’t be doing this quite as often.

Finally, although I did say I’m wary of spending any more time than I do already staring at a screen, I’m considering taking out a Britbox subscription for the long winter nights. They have a lot of classic BBC and ITV series that I would enjoy watching (or re-watching). And I must admit I wouldn’t mind giving the new Spitting Image a try as well!

I’d like to close this post by thanking my fellow bloggers for their varied and thought-provoking suggestions for surviving this Covid winter. I hope you may want to check out at least some of their blogs.

And, of course, if you have any comments or questions about this post, or any other suggestions for coping over the coming months, I’d love to hear them. Please leave a comment below as usual.

If you enjoyed this post, please link to it on your own blog or social media:

Regular readers will know that I have been posting about my personal experience of the coronavirus crisis since the original lockdown started (you can read my September update here if you like).

As previously I will discuss what has been happening with my finances and my life generally over the last few weeks, while trying to avoid being too repetitive!

As always, I will start with the money side of things.

Financial

As I’ve done before, I’ll begin with my Nutmeg stocks and shares ISA. This has gone up and down over the last few weeks, but currently stands at £16,578. That is over £500 up on last month, so I’m happy with that! Here is a screen capture covering the last three months…

My Property Partner and Kuflink investments are still both ticking along satisfactorily. Property Partner has resumed paying dividends on some properties, which is appreciated. The five-year sales process has also resumed. There is a backlog, though, so it will probably be longer than five years till the properties I hold shares in can be sold at the current, independently-assessed market price (or retained, of course).

There is nothing really to report about The House Crowd. I assume that the sales of the two properties in which I hold £1,000 shares are progressing, but can understand that it is a slow process at present. At least rental payments are still accruing, which should help to defray some of the selling costs.

There has been no further word either regarding my investments with Crowdlords. As I said last month, I have two remaining investments with them, Kennington Road eco-houses and Trent House. I was told they hope to have exit options for these properties by the end of the year, but I’m not holding my breath. On the plus side, they are paying 6 percent interest on my Trent House investment, which is quite generous in these days of ultra-low interest rates.

Personal

It’s been an eventful few weeks one way and the other.

As mentioned previously, I had booked a short break in Llandudno (see cover image) near the end of September. Thankfully I was able to go. If I had left it just a few days later I would have had to cancel, as the Welsh Assembly has decided to lock down the whole of the Llandudno and Conwy area due to rising infection rates. That means no-one can currently go in or out of the area without a compelling reason (and having a holiday booked there doesn’t count).

Anyway, I enjoyed my visit. I stayed in a self-catering apartment, which turned out to be a good choice in most respects. It was on two floors, with a lounge and well-equipped kitchen on the lower floor and a double bedroom and bathroom on the upper. The location was central but quiet, yet just five months’ walk from the sea. The only drawback was that parking was on the street and finding a spot was a bit of a lottery. I was lucky to get somewhere close when I arrived, but later in the holiday had to park on another road half a mile away, which was a bit of a pain. I paid £255 for my three-night stay via Booking.com, which I thought was reasonable. By comparison, the seafront hotels I checked out were charging over £600 for three nights’ bed and breakfast.

Not surprisingly Llandudno was quieter than usual for the time of year, but there were still plenty of visitors, and many of the small hotels and boarding houses had ‘No Vacancies’ signs in their windows. While some places and amenities were closed, many others were open, and I was pleased to find that the pier was fully operational (see photo below). Professor Codman’s famous Punch and Judy show on the promenade wasn’t running, though – a shame, as there were lots of young children who might have enjoyed it.

On my first day I left my car at the apartment and took a couple of bus tours. The first was the open-top bus that takes a circular route between Llandudno and Conwy and includes a running commentary. I have done this trip before and noticed that the recorded commentary hasn’t changed this year. Mind you, that may be just as well, as a post-Covid commentary would have had to include details about all the hotels and other places that have closed due to the virus, the seafront theatre that became a Covid field hospital, and so forth…

The other trip was on a vintage bus (see photo) around the Great Orme, one of the two promontories at either end of Llandudno’s seafront. This had a knowledgeable driver/guide, who provided an interesting – and up-to date – commentary. I must admit I particularly enjoyed seeing ‘Millionaire’s Row’ at the far side of the Orme. There are some amazing houses here, owned by people who like to preserve their privacy. Obviously the coach passes from a distance, but it was still a good opportunity to gawp at how the super-rich live. I particularly enjoyed hearing about the house that has its own private lift down to the beach!

On the second day of my visit I drove to the medieval walled town of Conwy, which is about three miles away. I booked a ticket online to see Plas Mawr, a restored Elizabethan town house (photo below). It was fascinating, and I was glad I took the option of borrowing one of the free electronic guides. You use these to scan a QR code in each room and it provides a commentary on the room itself and various interesting historical tidbits associated with it.

As with my visit to Dunster Castle near Minehead earlier in September, all the usual anti-virus measures were in place. I had to wear a face covering throughout, and staff ensured that there were no more than two households in a room at any one time. It worked pretty smoothly, although you had to follow a set route and there was no possibility of returning to a room once you had left it.

In case you’re wondering, the photo in my cover image shows the Haulfre Gardens Tearoom on the lower slopes of the Great Orme. It’s one of my favourite places in Llandudno, and I was pleased to find it was still open. I enjoyed afternoon tea in their lovely garden on both days of my visit. As you can see, I was pretty lucky with the weather!

As mentioned above, I was very glad to be able to make my trip before the current lockdown would have made it impossible. I feel very sorry for people who booked after me and were unable to go, especially as I have heard that some are now having problems getting their money back. But I am sorry also for the hotels and other businesses who have been left high and dry by the lockdown. I really hope for their sake it doesn’t go on too long 🙁

Moving on, I had an experience I would rather not have had in the last few weeks too. At a routine eye examination my optician saw something she didn’t like the look of in the retina of my left eye. So she packed me off to the eye clinic at Queens Hospital, Burton. The doctor there told me I had a perforation of the retina, and gave me laser treatment then and there. It wasn’t painful but it was obviously nerve-racking. The doctor did say it was a good thing my optician had spotted the problem, as it could have led to a detached retina if left untreated, which is clearly more serious. I have to go for a follow-up check this weekend, but touch wood the problem has been repaired. I guess if nothing else this does show why it’s so important to have your eyes checked regularly even if you don’t think there is anything wrong with them. That applies doubly to older people and those who (Iike me) are very short-sighted, as we are especially susceptible to this sort of thing.

On the Covid front, clearly most of the news hasn’t been good recently. Mind you, in most parts of the UK hospital admissions and deaths remain a lot lower than at the peak of the pandemic in the spring. I have seen the current situation described as a ‘casedemic’, which seems a pretty apt description. Clearly it’s important to protect the elderly and vulnerable at this time. Young people don’t typically suffer severe reactions to the virus, however, so I do wonder if some of the more extreme measures aimed at them are fair or necessary. Personally I am taking what I consider reasonable precautions but still trying to live my life as normally as possible. I volunteered for the UCL Virus Watch panel a few weeks ago and fill in a weekly questionnaire saying whether I have any possible Covid symptoms (none so far). They have also just asked me to take a blood test to see if I have any antibodies or other natural resistance to the virus. I’ll be interested to see the results of that!

As regards masks and such matters, I have been wearing a half-face shield in supermarkets (as a mask sceptic I’m not going to other shops till masks are voluntary again, though I might make an exception if the shop clearly states that they welcome non-mask-wearers). I find this better than the full face shield I was wearing before, as it doesn’t interfere with my vision. Shields are also much easier to breathe through than cloth masks, and I haven’t yet been challenged by any staff members or self-appointed mask police. In case you are interested, here’s an Amazon ad (affiliate) for some half-face shields similar to the type I am now using.

Well, I guess that’s enough for now. I do hope you and your loved ones are staying safe and well. As always, if you have any comments or questions about this post, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

In my previous article I talked about setting up as a consultant and how this can be a great way to capitalize on your work-related skills and experiences.

I discussed the range of opportunities for self-employed consultants and how to research the market and establish a strong personal brand. This time, I’ll be focusing specifically on how to market your consultancy business.

I’ll start with a time-honoured method…

Using a Mailshot

This is the traditional approach to marketing a service to businesses and still has many attractions. You will need to compile a list of potential clients you wish to target, perhaps using business directories and/or the internet. It is then a matter of putting together a package including a letter and maybe a brochure as well, along with any other enclosures you deem appropriate. A reply-paid envelope, for example, will often boost response rates.

The more modern approach is to use email. This has various advantages, the most important being that it is quicker and cheaper. Email marketing is typically used for establishing initial contact with a prospective client, to be followed up with written information and/or a phone call if any interest is expressed.

This method does have the drawback that you may not be able to find email addresses for all the businesses you want to target. In addition, many business people are inundated with emails, and other things being equal are less likely to read them than messages that arrive in the post (and if they have spam filters, they may not see your email at all). Nonetheless, when you are starting out, an email campaign has much to recommend it, and there is nothing to stop you following up with a mailshot and/or phone call later.

The Seminar Method

This can be a great way of making money as a trainer, and it can also help you land consultancy clients. Right now, due to anti-Covid measures, it is difficult to apply in the traditional way. Sooner or later, however, normal times will return and these measures will be relaxed. So I will set out the bare bones of the seminar method here.

The idea is that you arrange seminars or training sessions in your specialist subject, typically lasting a day or half-day. You book a room in a hotel or conference centre for this purpose and advertise your seminar through emails and/or mailshots sent to likely prospects.

A reasonable target for your first seminar would be 10 to 20 clients. You would need to pay the hotel a room hire fee of £50 to £100, and there would also be some publicity and promotional costs. An initial budget of around £400 would probably cover all of this.

If your clients pay £100 each, with the numbers mentioned you would be looking at a gross return of £1000 to £2000. Assuming – as mentioned above – you spent £400 on setting up and running the seminar, that would leave you £600 to £1600 clear profit.

That’s not a bad return in itself, but the big attraction is that if some clients are impressed by your expertise, there is every chance they will want to engage you for other services as well, from in-house training to mentoring and consultancy. If this becomes an ongoing arrangement you will have a source of regular income, and may be able to charge a monthly retainer for your services as well.

The seminar method is an under-used approach among trainers and consultants, yet it has huge money-making potential. While it would be difficult to apply at the present time, you could certainly adapt it to the online world (see below). For example, you could set up an online seminar using video-conferencing software such as Zoom or GoToMeeting. You could even create a web-based course in your specialist subject using a service such as Teachable.

Either way, in addition to whatever fees you charge, you would be building a pool of potential clients for your consultancy service as well.

Online Marketing

The internet is, of course, a massive boon for entrepreneurs. Used the right way, you can attract a never-ending stream of clients and potential clients by this means.

As I said last time, your website is an essential tool for this. If you take the time to create a good-looking site with quality content, in time you can expect to start attracting search-engine traffic. In other words, people looking for a consultant or trainer in your niche will see your site listed high in their search results and hopefully click through to find out more.

It will take a bit of time for your site to be listed in the search engines, and longer still for it to achieve a high ranking for your target keywords. You can, however, assist this process by using search engine optimization (SEO). This is a huge topic in itself, and I recommend looking online for more information. Search Engine Journal is a good place to start.

Here, though, are a few basic SEO tactics you can use to start boosting your rankings…

Share links to your site on social media such as Facebook, Twitter and Instagram.

Comment on blogs and websites relevant to your field of expertise, with links back to your site. You could offer guest posts to the owners of these sites as well.

Add a blog to your website, in which you talk about relevant issues and share helpful tips.

Join online forums and put a link to your site in your signature text (not all forums allow this, though, so check their guidelines first). Put a link in your email signature as well.

You could also consider self-publishing a short ebook on your specialism and give it away free from your site and/or sell it cheaply as an Amazon Kindle ebook. Again, link from your ebook back to your website. Not only will this assist with your search engine ranking, it may also bring you some clients directly.

SEO can work well over time, but if you want to get up and running faster you could consider paid advertising. One method that can bring results very quickly is Google Adwords. These are the small ‘Ads by Google’ that appear in search engine results and on related websites.

The method generally used to charge for these ads is ‘pay per click’ (PPC). In other words, you pay a set sum to Google every time someone clicks on one of your ads. You can choose the keywords that trigger your ads, and set a maximum you are willing to pay for them. The more you bid, the more prominently your ads will be displayed.

Google Adwords is a powerful tool for bringing targeted prospects to your website. For more information and to sign up, visit www.google.com/adwords.

Finally, there are websites where you can advertise your services and connect with potential clients. Job auction sites such as Guru and Upwork are one possibility, with many thousands of projects posted by would-be clients. You are unlikely to be able to earn top rates via these platforms, however. There is a lot of competition, and as they are international you will be up against people in low-wage economies whose overheads (and fee expectations) may be much lower than yours. If you are looking to gain experience and testimonials they may be worth trying, but they shouldn’t be your first port of call.

A better bet may be sites aimed specifically at connecting consultants with potential clients. One of the more established websites in this field is The Consultant Hub. Joining costs several hundred pounds (tax deductible, of course), but for that you get access to thousands of unadvertised consultancy opportunities, an individual profile page on the website, membership of a private online forum, and access to training and networking events.

More Top Tips

Finally, here are a few more tips for building your training and consultancy business…

Prepare a short pitch that answers the common question, ‘What Do You Do?’ Try to have a core message that can be summed up in one sentence, e.g. ‘I help small business professionals promote their products and services to people who need them.’

Keep up to date with your specialist subject. Join the relevant professional organization/s, read the latest books and journals, and subscribe to authoritative blogs and websites in your niche.

At the end of any training or consultancy session, ask for feedback. Not only will this give you valuable information on areas where you can improve, positive comments may be useful for testimonials (with the client’s permission, of course).

Listen carefully to what clients tell you about their businesses and any areas where they are having problems. This is priceless market research, and may suggest new services you can offer in future.

Build links with consultants and small businesses with expertise in areas related to yours. For example, if your specialism is copywriting, you might want to link up with a graphic design agency. As well as helping your clients by introducing them to other professionals with skills they need, you may be able to negotiate referral fees.

Keep in regular touch with clients, and let them know about any new services you may be offering. Typically 80% of your business will come from repeat clients, so be sure you stay on their radar for the next time they need someone with your particular expertise.

In Conclusion

Selling your skills and knowledge as a mentor, trainer or consultant can be both enjoyable and lucrative. You can work from home, and full-time or part-time as you prefer. This can also be an ideal opportunity for older people who may be looking to reduce their working hours while still earning a decent income.

The work is varied and interesting, and you will have the satisfaction of sharing your skills and experience with people and businesses who can benefit from them. And with many companies relying increasingly on freelancers to help keep overheads low, there has seldom been a better time to get into this field.

Good luck, and happy consulting!

Disclosure: this article includes some affiliate links. If you click through these and make a purchase, I will receive a commission for introducing you. This will not affect the service you receive or the price you pay.

If you enjoyed this post, please link to it on your own blog or social media:

In this two-part article I’ll be looking at a method almost anyone can use to make money, by selling their skills and knowledge as a mentor, trainer or consultant.

I say almost anyone, because clearly you need some skills and knowledge other people would be willing to pay you for. There is a huge range of possibilities, however, and if you have worked in any skilled, professional or managerial position, you almost certainly have knowledge and abilities you could sell – possibly after some polishing up first!

You can offer your services to private individuals (I’ll look at this in a moment) but by far the biggest and most lucrative potential market is businesses (including public sector organizations such as the NHS). They have budgets for training and consultancy, and generally pay well if you can deliver the services their managers and employees require.

To give you a flavour, here are just a few areas for which mentors, trainers and consultants are much in demand…

Health and Safety

Equal Opportunities

Marketing

Business Law

Salesmanship

Accounts and Financial Management

Planning

Copywriting

Computers

Leadership

Communication

Graphic Design

Social Media

One big advantage of working with businesses is that if all goes well, you are likely to be invited back in future, either to follow up your initial session or to train other staff. Also, one type of job can lead to another. For example, you might run a course for a client initially, and then be asked to provide ongoing mentoring or consultancy services.

Although businesses are your most likely clients, in some fields you could work with private individuals as well (or alternatively).

One example is computers. Many people struggle with mastering their home computers, and are willing to pay for help and instruction. If you can combine this with basic repairs and maintenance, you have the basis for a steady part-time or even full-time business. Admittedly it is unlikely to pay as well as working for business clients, but may suit some people better.

Business Basics

If you are going to offer any sort of training or consultancy service, even part-time, you will be regarded by the authorities as running a business. That means you will need to contact the tax authorities (HMRC in the UK) and let them know what you are doing.

You will also need to keep accurate financial records showing all money earned and any allowable expenses (stationery, advertising, phone bills, and so on). You or (more likely) your accountant will use these records in due course to produce annual accounts, which will determine how much tax you have to pay.

My personal advice would be to speak to an accountant early on and get his/her advice on how best to keep your books (financial records). This can save you a lot of hassle – and expense – later.

I don’t have space here to go into detail about the nuts and bolts of setting up in business, but there are many books on this subject available. You might also want to take a part-time college course if any are on offer in your area.

As always, the internet is a great source of information as well. Startups and the government’s business website are two very useful resources, but there are plenty of others. Just enter “Starting your own business” in any search engine to find more.

Marketing Yourself

Marketing is the key to making money in this field, so in the remainder of this post I will concentrate on this subject.

Contrary to what is sometimes believed, marketing isn’t the same as advertising. It is an approach or even a philosophy for doing business.

The marketing method involves finding out what potential clients need, and then setting out to meet those needs. This is important, as what you believe potential clients need may not always correspond with the reality.

Advertising (trying to persuade potential clients you can meet their needs) is therefore one aspect of marketing, but it’s far from the whole story. The first stage of marketing is market research, so let’s start there…

Market Research

If you’re planning to set up as a freelance trainer/consultant, it’s important to spend some time researching your chosen field to discover what exactly potential buyers might be looking for.

This will help ensure you pitch your offer correctly, and may also uncover additional niches you want to target. So it is well worth spending a bit of time on your preliminary research rather than jumping straight in.

There are various ways of doing market research, many of which can be performed from your desk or a library. One is researching what other people working in this field – your potential competitors, in other words – are offering.

This is easy to do on the internet. Put yourself in the position of a would-be client and do the sort of search query you might expect them to use: “leadership training”, for example. That should bring up a range of websites belonging to training and consultancy providers. Spend some time studying what these folk are offering and how they promote themselves. You might also want to make a note of how much they charge, if this information is given.

It’s also good to research what potential clients actually want. This isn’t quite so easy, but one way is to look on job auction sites such as People Per Hour and Guru. Businesses use these sites to post details of services they require, which freelancers then bid on. Look for companies advertising for help in your chosen niche, and see how they describe their requirements and the sort of assistance they are seeking.

It is also well worth contacting at least a few potential clients directly. If you have friends or former colleagues in business, for example, tell them what you are planning to do and ask for any advice they can offer. Most will be delighted to help, and you will also be alerting them to the fact that before long you will be available for work in this field.

Another method I have seen used successfully is to mailshot a range of potential clients with a market research questionnaire, and promise to make a donation to a specified charity for every one that is returned. This will obviously cost you a bit of money, but the information you get back will be valuable to you, and the contacts you make potentially even more so.

Through your market research you should be able to establish the type of client that may be the best fit for your skills, the services they need, and how best to present yourself to them as a potential provider.

Your Business Image

You are now almost ready to start promoting your services to potential clients, but one other thing you should give some thought to is your business image.

As a freelance mentor, trainer or consultant, it is vital that you present an impression of competence and professionalism. This applies even – or especially – if you are working from home.

Aside from obvious matters such as dress and appearance, you will need to ensure that this image precedes you in any advertising materials you produce. At the very least, you will need to have an attractive letterhead, and possibly a logo as well. If you want to keep your expenditure to a minimum, any printer will have someone who can do this sort of thing, but for the best possible results it’s best to engage a professional graphic designer.

The other thing necessary for anyone working in this field nowadays is a website. You can get a specialist website designer to create this for you, but if you have some computer skills it is quite possible to create a professional-looking site yourself, maybe using the popular WordPress platform. You could use the free WordPress.com service or (even better) set up your own self-hosted WordPress site using a service such as Bluehost (which I use – affiliate link). Either way, you’ll be able to choose from a wide range of themes and plugins to customize your site and ensure it presents your service in exactly the way you want.

When planning your website, you can take inspiration from sites created by other trainers and consultants, but there is nothing wrong with keeping it simple and straightforward at first. The main things you must have include information about yourself and your background, the services you offer, and any testimonials. Contact information is clearly essential, and if appropriate you might also include examples of your work (if your specialism is copywriting or graphic design, for example).

You could also put some information about pricing, although my advice would be to avoid giving chapter and verse about this. You don’t want to put people off if they think you are too expensive, or too cheap for that matter. In addition, it’s best to allow yourself some room for negotiation with individual clients.

With all this in place, you should be in a position to start contacting potential clients. I will discuss this in detail in my next post!

As ever, if you have any comments or questions about this post, please do leave them below..

If you enjoyed this post, please link to it on your own blog or social media:

I recently enjoyed a three-night break in the North Somerset coastal town of Minehead.

It was actually my first visit to Minehead. Early this year, before the pandemic struck, I booked breaks in a few places I hadn’t been to before. Minehead was the only one I didn’t have to cancel 🙁

After some online research, I had booked a room at the Channel House Hotel. This is on Minehead’s North Hill (see cover photo), on the opposite side of the bay from the Butlins holiday camp. Here’s a map by courtesy of Google.

The Channel House Hotel had excellent reviews and a great location near the harbour. It had its own car park as well, which is always a plus with seaside hotels!

Here’s some more information about my stay…

The Hotel

The Channel House Hotel is a small country-house hotel with eight bedrooms. They don’t accommodate dogs or children under the age of 15.

I had Room 7, on the top floor. I had been hoping for a sea view, but due to a line of trees I couldn’t really see it from my room. I could at least hear the waves, though! The hotel is in a quiet, peaceful location, and I slept very well on all three nights.

As you would expect in these strange times, various anti-virus precautions were in place. I had my temperature checked on arrival, and hand sanitizer was available by the front door and on all the tables in the dining room.

I opted for breakfast and an evening meal, although you can book bed and breakfast only. Other dining options near the hotel appear limited, though, especially in these times of Covid.

There was a good choice of breakfast options for a small hotel. As well as the full English (which you can customize as you wish) you could also have Eggs Benedict in three different variations or smoked haddock with poached egg. You could also have a plate of mixed fruit, cereal and/or yogurt, plus the usual toast and hot drinks. I’m not sure what the normal arrangements for breakfast are, but obviously at present they can’t have a self-service buffet, so most meal options are brought to your table.

There is a choice of starters and main meals in the evenings, with guests asked to say what they would like after breakfast. Fair enough in my view, as there is obviously no point in the hotel preparing meals nobody wants! That applies especially at the moment with visitor numbers so low – partly due to the virus and partly (I understand) as a deliberate policy to help preserve social distancing. During my stay, there were never any more than six guests including me.

Evening meals are served at 7.00 pm, with pre-meal drinks in the small bar from 6.30. Although the latter is obviously optional, I did find this an enjoyable way of meeting and getting to know my fellow guests. There was one couple and all the others were solo ladies around my age or older. We all got along well. I enjoyed hearing what they had been doing during the day, as most of them knew the area better than I did.

The evening meals were very good. They comprised five courses: starter, main, dessert, cheese and biscuits, and coffee. That may sound a lot, but the portions were sensibly sized, so I didn’t feel too guilty!

Fish seems to be a speciality and I particularly enjoyed the sole I had on the first night. One thing that surprised me, though, was that the menu never included any vegetarian main courses. They do cater for veggies and those with special diets, so I’m sure if I’d asked I could have had something. For three nights I was perfectly happy with what was on offer. But as I eat vegetarian quite often at home, it might have been nice to have that option on the menu as well, some nights at any rate!

My twin-bedded room was more than adequate for my needs. It had a small (by modern standards) wall-mounted TV, but that was fine for a short visit. The WiFi worked well once I sorted out a bit of confusion over the password, and I was able to use it in my room as well as the communal areas. The bathroom was a good size and had a bath with a modern electric shower over it. My bed was comfortable and there was plenty of storage space. I was well looked after and had an enjoyable and relaxing stay.

Financials

As Pounds and Sense is primarily a money blog, I should say a word about this.

I paid £360 for my three-night stay (including breakfasts and evening meals) at the Channel House Hotel, which I thought very reasonable. If I had chosen bed and breakfast only, the price would have been £285. As you may gather from this, the hotel charge a fixed price of £25 for their five-course evening meals.

You can check current prices and availability on the Hotels.com website. You can book this way (which I did) or directly with the hotel. The latter method may or may not work out cheaper.

Things to See and Do

Inevitably at the time of my visit a lot of places and attractions were either closed or not operating normally.

I was particularly disappointed that the West Somerset Railway – said to be the longest heritage railway in England – was not running. At the time of writing there is still no indication when it will reopen.

I was though able to visit Dunster Castle, which is owned by the National Trust. As a Trust member I was able to get free admission, but had to book a ticket in advance on the website. They are doing this to ensure that visitor numbers are controlled, to help maintain social distancing.

Dunster Castle goes back to at least Norman times, with an impressive medieval gatehouse and ruined tower providing a reminder of its long and sometimes turbulent history. The castle became a lavish country home during the 19th century for the Luttrell family, and the furnishings and decor are largely from that time. The castle is surrounded by a terraced garden displaying varieties of Mediterranean and subtropical plants. Below this is a riverside woodland garden leading to a historic working watermill (unfortunately closed at present).

Due to anti-virus measures, visitors have to follow a long and winding route through the gardens to get to the castle, so my top tip is to allow longer than you would expect to arrive at your allotted time. Bear in mind also that you will be expected to follow a similarly circuitous route afterwards to get back to the car park. This means there is a lot of walking before and after you see the castle itself. I was okay with that, but I suspect some older visitors might struggle.

Anyway I duly arrived at the castle entrance and, after giving a phone number for track-and-trace and using a hand sanitizer, was allowed to enter (wearing a face covering, of course). Only certain parts of the castle were open to visitors, not including the kitchens for some reason. On the plus side, though, with so few visitors there was plenty of room to see everything on view. Although entry is by timed ticket, once in you are allowed to stay for as long as you want (or at least for as long as you can stand wearing a face covering).

I spent around an hour in the castle, after which I was ready for some refreshments. I am not sure if the castle has a coffee shop normally but if so it was closed. They did though have a pop-up cafe in the gardens (you can just see this to the left of my photo above). I had a hot chocolate and a slice of coffee-and-walnut cake here, which I very much enjoyed even though it wasn’t exactly a healthy option!

Dunster Castle was the only formal visitor attraction I visited during my stay, and I do recommend it, so long as walking isn’t a problem for you.

In fact, I did a lot of walking throughout my break. That included along the seafront, from the harbour to the Butlins camp, and also up North Hill, which takes you to the edge of Exmoor. On the walk up North Hill, I stopped to admire the 16th century St Michael’s Church (also sadly closed).

Near the church is an area called Church Steps, where there are some beautiful thatched cottages.

I would like to show you the view across the bay from the top of North Hill, which I am told is quite spectacular. When I got to the viewing area, however, a closed and padlocked gate barred my way, with a forbidding warning notice about Covid-19. Having made the not-inconsiderable effort to walk up the hill (most people drive), this was pretty disappointing. I sat at the roadside for a few minutes collecting my thoughts before heading down again. That was probably the low point of the holiday!

On my last day in Minehead I took a short stroll to Blenheim Gardens, a well-tended and attractive public park. The cafe was closed as well, but I wandered down to the harbour and enjoyed a takeaway cream tea there 🙂

Closing Thoughts

Overall, I enjoyed my visit to Minehead, though obviously the fact that so many places were closed did spoil it a little. I had an enjoyable, relaxing time, with plenty of healthy fresh air and exercise (just as well in view of the cakes and five-course dinners!). I will hope to go back again when things are more normal.

As always, if you have any comments or questions about this post, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

A great number of people today need to transfer currencies, or receive transfers from abroad, for many different reasons. As globalization extends, this need has become more frequent as geographical borders become less relevant.

For example, our parents couldn’t even dream about services like eBay or Alibaba, where you can buy anything and have it delivered from a dozen countries away. And the whole thing might be cheaper than buying it in your local store!

But here is where the matter of foreign currency transfers becomes important. Paying for something abroad or getting money sent to you might not be cheap. That’s because not only do you have to pay bank fees for the transaction, you also lose money on currency exchange, which is often a mandatory step in cross-border transfers.

Luckily, today there are alternative money transfer services that allow you to cut these costs. You’ll need to look into them if you require regular foreign currency exchange (FX or forex) services.

Why You Might Need to Make Foreign Currency Transfers

One reason you might need to make a large money transfer abroad is real estate. Buying property is an important part of the retirement planning process and many Britons choose to retire abroad. For example, the latest data indicates that there are about 466,000 British pensioners living in the EU. There are even more among the 5.5 million Brits living worldwide.

Even if you don’t plan on moving or buying a vacation home on some tropical beach, you might consider investing. Investing in real estate is one of the less risky methods for growing your fortune. Of course, the coronavirus crisis has heavily affected this industry. But there are still some very promising prospects for the residential housing market.

Also, today you’ll need to make international payments when booking your holiday accommodation. So, if you plan to travel at all, you’ll need to look for cheap money transfer solutions.

Anyone involved in international business also needs to make and/or accept international payments. This also includes the simple process of buying goods through one of the many e-commerce platforms.

In addition to those reasons, if you are an expat or a traveller, you’ll need to exchange money regularly. The same goes for dealing with transfers like inheritance or even accepting dividend payments from your investments.

All in all, living in the modern world makes you exposed to foreign currency exchange and transfers in many ways. Therefore, the knowledge of how to save money on these transactions is sure to be useful.

How Much Do Foreign Currency Transfers Cost in a Bank?

The cost of an international bank wire transfer is a very complicated issue. First of all, you need to understand that banks will advertise, and sometimes even show you, only the transfer fee. In the UK those range from £8 to about £40. That doesn’t seem too bad, especially for large transfers, right?

However, the truth is that banks are deceiving customers most of the time. If they were fully transparent, you would understand that what truly matters is the FX rate margin. That’s the amount that the bank charges per currency conversion on top of the mid-market exchange rate.

Simply put, high FX margins are why you lose so much money on currency conversions. Different banks use different margins and that’s why they offer different exchange rates. But if you compare the options offered by top UK banks, you’ll see that they are all very close.

Therefore, you don’t have much of a choice.

Also, there might be additional fees involved in a cross-border money transfer. The recipient bank might charge its own fees. If there are any intermediary ‘stops’ along the way, more fees will come.