If you’ve been watching the news lately, you’ll probably have seen headlines about stock markets taking a tumble thanks to a wave of tariffs announced by Donald Trump. It’s enough to make any retiree feel uneasy – especially if your pension is tied to the markets.

But before you start panicking or making any big changes, take a deep breath. Here’s what you really need to know.

What’s Going On?

President Trump’s tariffs are stoking fears of a global trade war. Investors don’t like uncertainty, and the markets are reacting with volatility. There have been drops not just in the US but across the globe, including here in the UK.

For retirees, that can feel personal. If your pension pot or retirement income is invested in stocks and shares, you might be wondering: Am I going to be okay?

Short answer: Yes, if you stay calm and avoid knee-jerk reactions.

Why This Isn’t the Time to Panic

Markets have always had ups and downs. That’s not new. Whether it was the financial crisis of 2008, the Brexit vote, or the COVID crash (see below), every downturn has sooner or later been followed by recovery.

If you sell investments during a dip, you lock in those losses. But if you ride it out, your portfolio has every chance to bounce back, as has happened before. History is on your side.

Speaking of which…

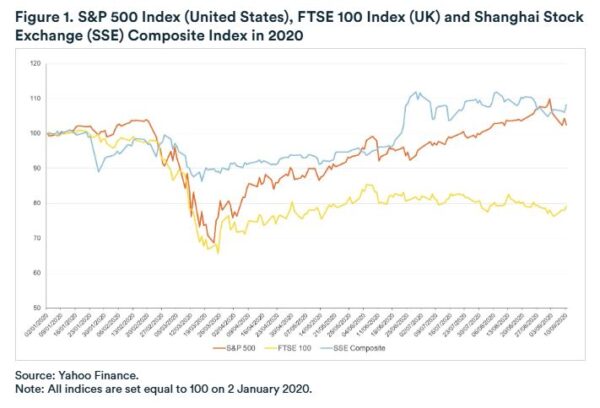

Consider The Covid Crash

In early 2020 it became clear that COVID was going to be a massive deal, and markets world-wide fell dramatically. And yet by mid-March, as the chart below from Yahoo Finance reveals, they were already recovering.

The recovery in stock market values continued through 2021. If you check out my in-depth review of the Nutmeg robo-adviser investment platform, you can see this for yourself. Overall, the period from March 2020 to December 2021 saw a big rise in the value of my Nutmeg investments. If I had panicked in early 2020 and withdrawn all my money then, I would certainly have been thousands of pounds worse off.

Your Pension Is Built to Withstand This

Most UK pensions – especially workplace and private pensions – are designed for long-term sustainability. They’re usually diversified across different types of assets like stocks, bonds and property. This helps soften the blow when markets get rocky.

If you have a defined benefit pension, you’re likely shielded from market fluctuations altogether. These pensions pay a fixed income and aren’t directly tied to the stock markets.

For those with defined contribution pensions – the majority of us these days – yes, the value can go up and down. But remember, pensions are managed by professionals who adjust strategies to navigate global changes like the current one.

What You Can Do (Instead of Worrying)

Check in with your adviser – They can help you understand how exposed your pension is to current events and whether any changes are needed. See also my article on Why Over-50s May Need an Independent Financial Adviser.

Keep a cash buffer – If possible have a few months’ worth of living expenses in cash or savings, so you’re not forced to sell your investments during market lows.

Stay diversified – A mixture of investments across regions and sectors helps spread risk.

Ignore the noise – Newspaper headlines are designed to grab attention. Focus on your long-term goals instead.

One other point is that, if you’re in the early days of retirement especially, dips can present an opportunity to buy while values are depressed, in the hope of gaining when (hopefully) they recover. This won’t be appropriate for everyone and it’s important to proceed cautiously. Timing the market is notoriously difficult, and if you get this wrong you can lose money rather than making it. But if you are careful (and not overly risk-averse) there are undoubtedly opportunities to be found at these times.

Bottom Line

Trump’s tariffs might be shaking the markets, but your retirement doesn’t have to be shaken with them. Your pension plan is more robust than you might think, and a temporary dip doesn’t mean disaster.

If you’re feeling anxious, that’s normal – but don’t let fear drive your financial decisions. Speak to a financial adviser if you need reassurance (I have one myself) and above all, keep your cool. Retirement is a long game, and a smart strategy will see you through.

As always, if you have any comments or questions about this article, please do leave them below.

DISCLOSURE: I am not a professional financial adviser and nothing in this article should be construed as personal financial advice. If you are uncertain how best to proceed, I strongly recommend speaking to a qualified financial adviser or planner. They will take the time to fully understand your particular circumstances and advise you how best to proceed. All investing carries a risk of loss.

If you enjoyed this post, please link to it on your own blog or social media:

Here is my latest monthly update about my investments (slightly earlier than usual due to other commitments). You can read my March 2025 Investments Update here if you like.

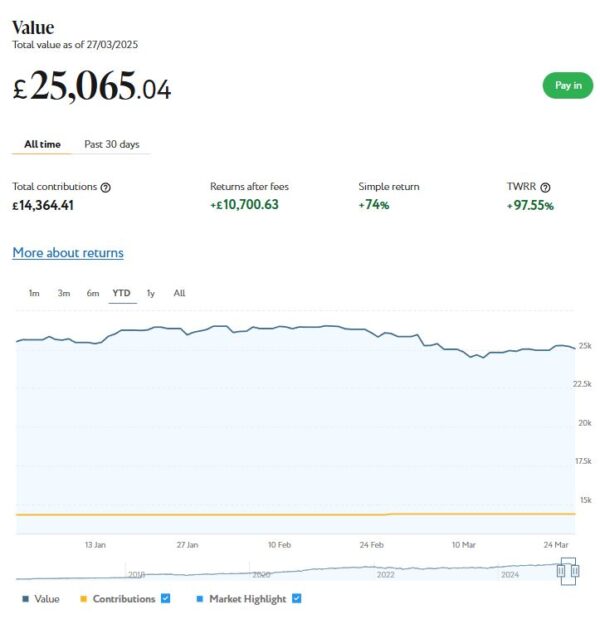

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

As the screenshot below for the year to date shows, my main Nutmeg portfolio is currently valued at £25,065. Last month it stood at £25,850, so that is a drop of £785.

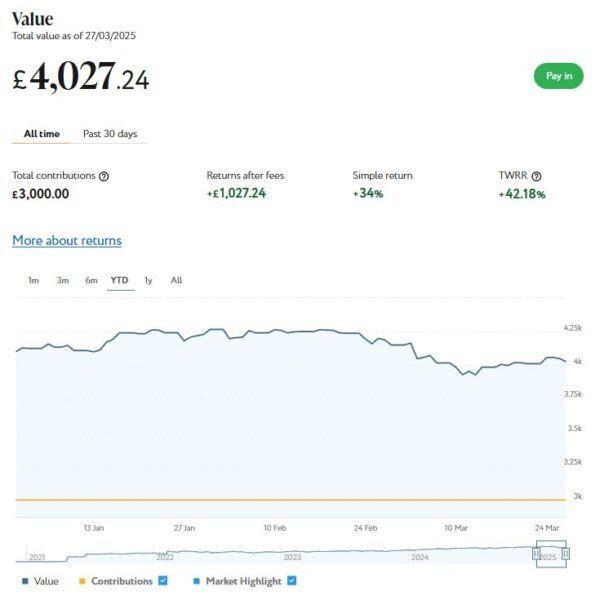

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £4,027 compared with £4,151 a month ago, a fall of £124. Here is a screen capture showing performance for the year to date.

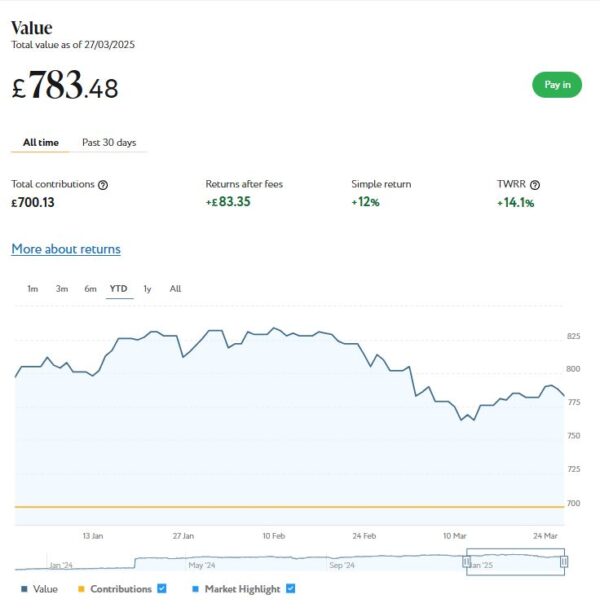

Finally, at the start of December 2023 I invested £500 in one of Nutmeg’s new thematic portfolios (Resource Transformation). In March I also invested a further £200 from referral bonuses. As you can see from the YTD screen capture below, this portfolio is now worth £783 compared with £803 last month, a fall of £20.

As you can see, March has been another disappointing month for my Nutmeg investments. Overall I am down by £929. This is mostly due to the continuing instability in world markets, caused by the the trade tariffs imposed by US President Donald Trump and other economic and social factors.

Nonetheless, the value of my Nutmeg investments is still up £1,477 in the last twelve months. And their value has increased by £3,559 or 13.52% since the start of January 2024. So the recent falls do need to be taken in context. Ups and downs are always to be expected with stock market investments, and over time they tend to even themselves out. In general the worst thing you can do is panic and sell up when downturns occur, as you are then crystallizing your losses. Indeed, I am considering topping up some of my investments now while values are depressed. That’s just how I’m thinking, of course, and doesn’t constitute investment advice!

You can read my full Nutmeg review here. If you are looking for a home for your annual ISA allowance, based on my overall experience over the last eight years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs), Lifetime ISAs and Junior ISAs as well.

Moving on, I also have investments with P2P property investment platform Assetz Exchange. As discussed in this recent post, the company recently rebranded as Housemartin.

My investments with Housemartin continue to generate steady returns. Housemartin focuses on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my HM portfolio has generated a respectable £238.70 in revenue from rental income. Capital growth has slowed, though, in line with UK property values generally.

At the time of writing, 15 of ‘my’ properties are showing gains, 2 are breaking even, and the remaining 19 are showing losses. My portfolio of 36 properties is currently showing a net decrease in value of £52.78, meaning that overall (rental income minus capital value decrease) I am up by £185.92. That’s still a decent return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Housemartin most projects are socially beneficial as well.

The overall fall in capital value of my Housemartin investments is obviously a little disappointing. But it’s important to remember that until/unless I choose to sell the investments in question, it is largely theoretical, based on the latest price at which shares in the property concerned have changed hands. The rental income, on the other hand, is real money (which in my case I’ve reinvested in other HM projects to further diversify my portfolio).

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of Housemartin as far as i am concerned. You can actually invest from as little as £1 per property if you really want to proceed cautiously.

As I noted in this blog post, Housemartin is particularly good if you want to compound your returns by reinvesting rental income. This effectively boosts the interest rate you are receiving. Personally, once I have accrued a minimum of £10 in rental payments, I reinvest this money in either a new HM project or one I have already invested in (thus increasing my holding). Over time, even if I don’t invest any more capital, this will ensure my investment with Housemartin grows at an accelerating rate and becomes more diversified as well.

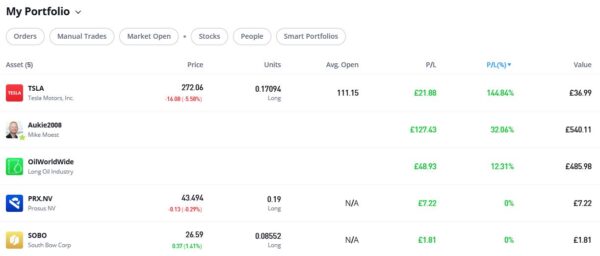

In 2022 I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios, Oil Worldwide. I also invested a small amount I had left over in Tesla shares.

As you can see from the screen captures below, my original investment (total value £888.36 in pounds sterling) is today worth £1,072.80, an overall increase of £184.44 or 20.76%.

Note: eToro now displays the value of investments in your native currency, although you can change this if you wish.

As you can see, my Oil WorldWide investment is currently showing a profit of 12.31%. That’s a welcome improvement since the portfolio was rebalanced by eToro. The investment team at eToro periodically rebalance all smart portfolios to ensure that the mix of investments remains aligned with the portfolio’s goals, and to take advantage of any new opportunities that may present themselves.

My copy trading investment with Aukie2008 has been doing better, with an overall 32.06% profit. To be fair, I have held the latter investment a bit longer.

My Tesla shares, which I bought as an afterthought with a bit of spare cash I had in my account, have done particularly well since I bought them, with an overall profit of 144.84%. If only I had put a bit more money into this!

You might also notice that I have small holdings in Prosus NV, a Dutch internet group, and South Bow, a Canadian energy infrastructure company. To be honest I don’t understand how I acquired these, but I assume they are some sort of bonus I was awarded. In any event, I am happy to have them in my portfolio!

eToro also offer the free eToro Money app. This allows you to deposit money to your eToro account without paying any currency conversion fees, saving you up to £5 for every £1,000 you deposit. You can also use the app to withdraw funds from your eToro account instantly to your bank account. I tried this myself and was impressed with how quickly and seamlessly it worked. You can read my blog post about eToro Money here. Note that it can also serve as a cryptocurrency wallet, allowing you to send and receive crypto from any other wallet address in the world.

If you would like more information about setting up an eToro account, please click on this no-obligation website link [affiliate]. Don’t forget that you also get a free $100,000 virtual portfolio, which you can use to experiment with trading and investing strategies. I have certainly earned a lot from mine.

Moving on, as I said last time, I am no longer writing for the Mouthy Money website, as they have decided to take their content creation in-house. From a personal perspective I am obviously disappointed about this, but I had a good run with them and wish them every success going forward. You can still read all the articles I contributed to Mouthy Money over the years by visiting my profile page on the website. How long they will keep this in place I really can’t say!

I also published several posts on Pounds and Sense in March. Some are no longer relevant, but I have listed the others below.

In Beat the Postage Stamp Price Rise!, I pointed out that stamp prices are rising again on 7th April 2025. This will actually be the the SIXTH rise in the price of first class stamps in just three years. See what prices are going up, along with my recommendations for mitigating the effects of the increases.

And in From Saving to Spending – The Retirement Mindset Shift I discussed a subject that has been on my mind recently as I enter my 70th year. This is how to negotiate the mindset shirt from saving to spending in retirement, and how (hopefully) to get the balance right.

The Pros and Cons of Investing for Dividends discusses a strategy that has been growing in popularity with older investors particularly. Dividend investing offers the potential for generating income combined with capital appreciation. In this post I examine the pros and cons of a dividend investing strategy and set out a few tips and guidelines for those new to this.

Finally, in Spotlight: The Mintos P2P European Investing Platform I take a closer look at Mintos, Europe’s largest P2P investment platform. As well as the ability to generate above-average returns by investing in loans to businesses world-wide, they have added new diversification options, including bonds, ETFs and real estate. And until the end of April they have a bonus offer for anyone investing €1,500 or above on the platform. In my blog post I look at the pros and cons of investing with Mintos and provide more details about their April bonus offer.

One other thing is that we’re currently just over a week away from the end of the 2024/25 financial year. If you still haven’t used all of your 2024/25 £20,000 tax-free ISA allowance, you have just a few days left before it’s gone. It is more important than ever to use all your tax-free allowances while you can, as the government looks set to reduce some of these allowances later in the year. See my recent blog post for more information.

I’ll close with a reminder that you can also follow Pounds and Sense on Facebook or Twitter (or X as we have to call it now). Twitter/X is my number one social media platform and I post regularly there. I share the latest news and information on financial matters, and other things that interest, amuse or concern me. So if you aren’t following my PAS account on Twitter/X, you are definitely missing out.

I am also on the BlueSky social media network under the username poundsandsense.bsky.social. For the time being anyway, Twitter/X will remain my primary social media platform, but I will also post details of my latest blog posts, third-party articles and other financial news and resources on BlueSky for those who prefer to follow me there.

As always, if you have any comments or questions, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts on PAS may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media:

Today I’m looking at investing for dividends. This is an increasingly popular strategy among investors seeking to generate passive income while potentially also growing their capital.

Dividend stocks can provide a steady income stream, but they also come with risks and considerations. So I’ll begin by looking at the pros and cons of this approach. I will set out some hints and tips for anyone who may be interested in getting started at dividend investing. I will also mention some established UK companies that have a reputation for paying regular dividends, and some online share-dealing platforms that may be suitable for anyone applying this strategy.

Let’s begin with some of the attractions of dividend investing, though…

Pros

Regular Income Stream

One of the biggest benefits of dividend investing is receiving regular cash payments, typically every quarter or six months, though occasionally monthly. This can be particularly appealing for retirees or anyone seeking passive income.

Potential for Long-Term Growth

Many well-established companies that pay dividends also experience share price growth. Reinvesting dividends through a dividend reinvestment plan (DRIP) can compound returns over time.

Stability in Market Downturns

Dividend-paying companies are often large, well-established firms that can weather economic downturns better than smaller, high-growth companies. Investors may find these stocks less volatile.

Tax Efficiency for UK Investors

UK investors benefit from the £500 dividend allowance (as of 2024/25) before dividend income is taxed. Additionally, holding dividend stocks in an ISA (Individual Savings Account) or SIPP (Self-Invested Personal Pension) shields the income from tax altogether.

Indication of a Strong Business

Companies that consistently pay and grow dividends often have strong financials, stable earnings, and a track record of profitability. This can be a sign of a well-managed company.

Cons

Slower Growth Compared to High-Growth Stocks

Dividend stocks are typically in mature industries, meaning they may not offer the rapid price appreciation seen in high-growth technology or small-cap stocks.

Dividends Are Not Guaranteed

A company can cut or suspend its dividend payments if it faces financial trouble, as seen during economic crises. This can lead to both income loss and share price declines.

Dividend Tax for Higher Earners

If your dividend income exceeds the £500 tax-free allowance, you will pay 8.75% tax (basic rate), 33.75% (higher rate), or 39.35% (additional rate) on the excess amount. This reduces overall returns compared to capital gains, which have different tax rates.

Sector Concentration Risk

Many high-dividend stocks are concentrated in certain industries, such as utilities, oil, and consumer goods. This can limit diversification and expose investors to sector-specific risks.

Tips for Beginners

If you’re new to dividend investing and want to try it, here are a few tips and guidelines to get you started…

Look for Dividend Growth, Not Just High Yields – A high yield can be a red flag if unsustainable. Instead, focus on established companies with low volatility and a history of gradually increasing dividends over time.

Diversify Your Portfolio – Don’t put all your money into one or two high-dividend stocks. Consider spreading investments across different sectors and countries.

Check the Dividend Cover Ratio – This metric (earnings per share divided by dividends per share) shows whether a company can afford its dividend. A ratio above 1.5 is generally considered safe.

Use Dividend Reinvestment – Reinvesting dividends can significantly increase long-term returns through compounding. Many brokers and online share-dealing platforms offer automatic reinvestment options.

Consider Dividend-Focused Funds – If picking individual stocks feels overwhelming, dividend ETFs or investment trusts like City of London Investment Trust (CTY) and Murray Income Trust (MUT) provide diversification and professional management. Popular dividend-focused ETFs include Vanguard High Dividend Yield Trust (VYM) and iShares Select Dividend ETF (DVY), which invests in high dividend yielding US stocks.

Examples of Strong Dividend-Paying UK Companies

Here are some UK companies known for consistent dividend payments in recent years.

Unilever (ULVR) – A consumer goods giant with a strong dividend history and steady growth.

Legal & General (LGEN) – A leading financial services company offering an attractive dividend yield.

National Grid (NG) – A stable utility company known for reliable dividend payouts.

BP (BP) – A major oil company that has historically paid strong dividends, though with some fluctuations.

Diageo (DGE) – A global leader in alcoholic beverages with a track record of dividend growth.

Online Share Dealing Platforms

Here are three UK share dealing platforms that are well-suited for dividend investors looking for relatively low costs.

Interactive Investor (ii)

Flat-fee pricing model, which can be cost-effective for those with larger portfolios.

Monthly plans start from £4.99, including a Stocks & Shares ISA.

Offers one free trade per month, with additional trades at £5.99.

Free regular investing option for cost-effective reinvestment of dividends.

Each of these platforms has strengths depending on your investing style. Trading 212 (a personal favourite of mine) is great for beginners and low-cost investors; Interactive Investor suits those with larger portfolios; and IWeb is a solid, no-frills option for long-term dividend investors.

Closing Thoughts

Dividend investing can be a great way to generate passive income, but it requires careful stock selection and risk management.

By focusing on financially strong companies with sustainable dividends and using tax-efficient accounts, investors can make the most of this strategy.

If you’re looking for a regular income from your investments combined with the potential for long-term growth, dividend investments have the potential to play a valuable role in your investing portfolio..

See also this guest post by my colleague Lewys Lew on his personal approach to dividend investing. Although it was published a while ago, there are still some useful tips to be gleaned from it.

PLEASE NOTE: I am not a qualified financial adviser and nothing in this article should be construed as personal financial advice. You should always do your own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

If you enjoyed this post, please link to it on your own blog or social media:

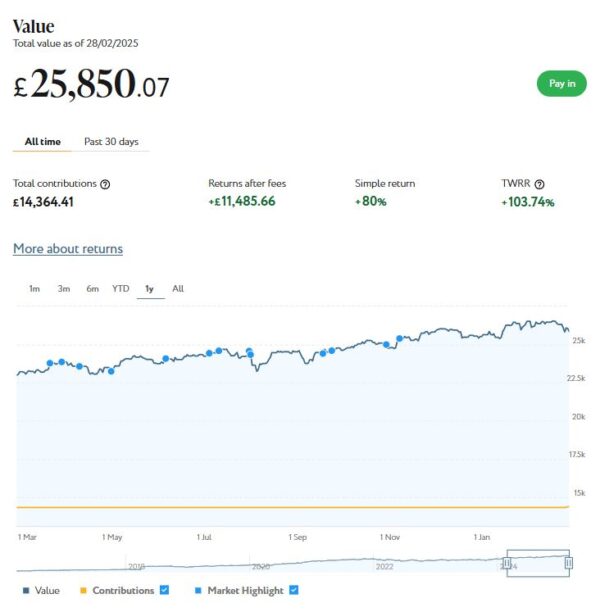

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

As the screenshot below for the last twelve months shows, my main Nutmeg portfolio is currently valued at £25,850. Last month it stood at £26,528, so that is a decrease of £678.

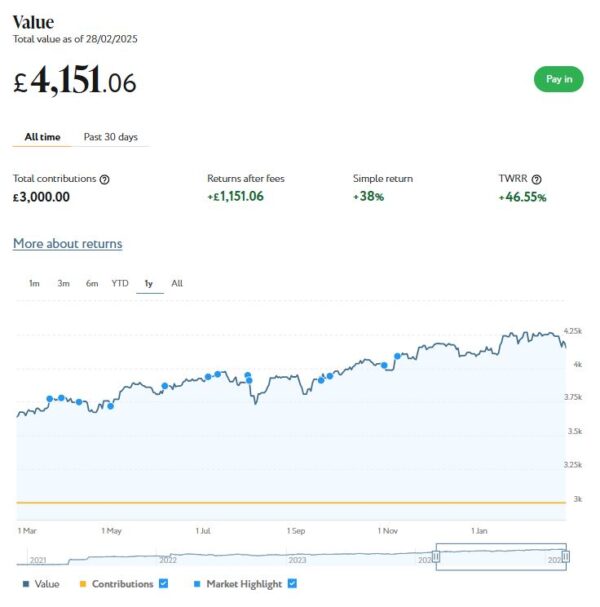

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £4,151 compared with £4,267 a month ago, a fall of £116. Here is a screen capture showing performance over the last twelve months.

Finally, at the start of December 2023 I invested £500 in one of Nutmeg’s new thematic portfolios (Resource Transformation). In March I also invested a further £200 from referral bonuses. As you can see from the screen capture below, this portfolio is now worth £803 (rounded up) compared with £832 last month, a fall of £29.

As you can see, February has been a disappointing month for my Nutmeg investments. Overall I am down by £823. This is mostly due to a general decrease in share values in the second half of the month.

Nonetheless, the value of my Nutmeg investments is still up £390 since the start of the year. And their value has increased by £3,441 or 12.67% in the twelve months since the end of February 2024.

You can read my full Nutmeg review here. If you are looking for a home for your annual ISA allowance, based on my overall experience over the last eight years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs), Lifetime ISAs and Junior ISAs as well.

Moving on, I also have investments with P2P property investment platform Assetz Exchange. As discussed in this recent post, the company recently rebranded as Housemartin.

My investments with Housemartin continue to generate steady returns. Housemartin focuses on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my HM portfolio has generated a respectable £235.31 in revenue from rental income. Capital growth has slowed, though, in line with UK property values generally.

At the time of writing, 17 of ‘my’ properties are showing gains, 1 is breaking even, and the remaining 19 are showing losses. My portfolio of 37 properties is currently showing a net decrease in value of £50.24, meaning that overall (rental income minus capital value decrease) I am up by £185.07. That’s still a decent return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Housemartin most projects are socially beneficial as well.

The overall fall in capital value of my Housemartin investments is obviously a little disappointing. But it’s important to remember that until/unless I choose to sell the investments in question, it is largely theoretical, based on the latest price at which shares in the property concerned have changed hands. The rental income, on the other hand, is real money (which in my case I’ve reinvested in other HM projects to further diversify my portfolio).

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of Housemartin as far as i am concerned. You can actually invest from as little as £1 per property if you really want to proceed cautiously.

As I noted in this blog post, Housemartin is particularly good if you want to compound your returns by reinvesting rental income. This effectively boosts the interest rate you are receiving. Personally, once I have accrued a minimum of £10 in rental payments, I reinvest this money in either a new HM project or one I have already invested in (thus increasing my holding). Over time, even if I don’t invest any more capital, this will ensure my investment with Housemartin grows at an accelerating rate and becomes more diversified as well.

My investment on Housemartin is in the form of an IFISA so there won’t be any tax to pay on profits, dividends or capital gains. I’ve been impressed by my experiences with Housemartin and the returns generated so far, and intend to continue investing with them. You can read my full review of Assetz Exchange/Housemartin here. You can also sign up for an account directly via this link [affiliate]. Bear in mind that, as from the current financial year (2024/25), you can open more than one IFISA per year.

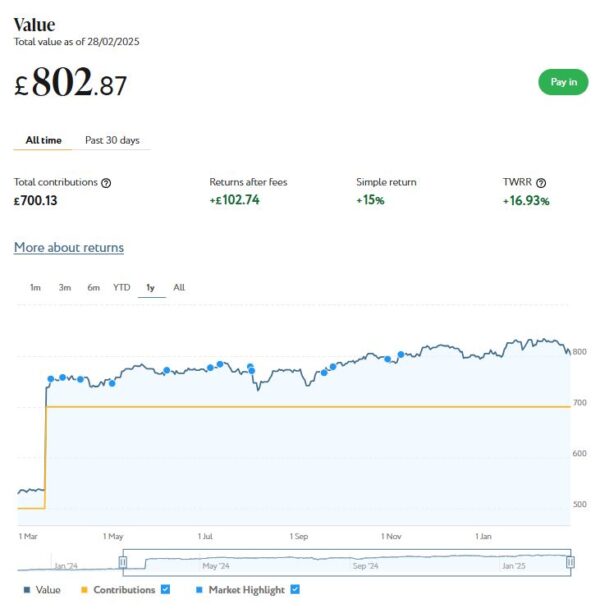

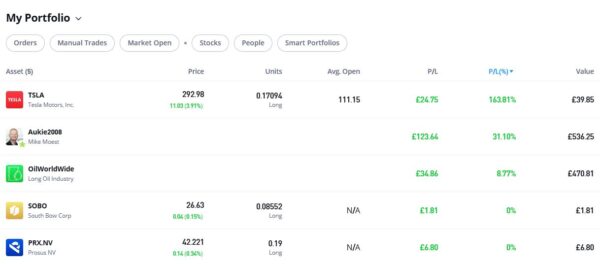

In 2022 I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios, Oil Worldwide. I also invested a small amount I had left over in Tesla shares.

As you can see from the screen captures below, my original investment (total value £888.36 in pounds sterling) is today worth £1,056.29, an overall increase of £167.93 or 18.90%.

Note: eToro now displays the value of investments in your native currency, although you can change this if you wish.

As you can see, my Oil WorldWide investment is showing a profit of 8.77%. That’s a small but nonetheless welcome improvement since the portfolio was rebalanced by eToro. The investment team at eToro periodically rebalance all smart portfolios to ensure that the mix of investments remains aligned with the portfolio’s goals, and to take advantage of any new opportunities that may present themselves.

My copy trading investment with Aukie2008 has been doing better, with an overall 31.18% profit. To be fair, I have held the latter investment a bit longer.

My Tesla shares, which I bought as an afterthought with a bit of spare cash I had in my account, have done particularly well since I bought them, with an overall profit of 163.81%. If only I had put a bit more money into this!

You might also notice that I have small holdings in Prosus NV, a Dutch internet group, and South Bow, a Canadian energy infrastructure company. To be honest I don’t understand how I acquired these, but I assume they are some sort of bonus I was awarded. In any event, I am happy to have them in my portfolio!

eToro also offer the free eToro Money app. This allows you to deposit money to your eToro account without paying any currency conversion fees, saving you up to £5 for every £1,000 you deposit. You can also use the app to withdraw funds from your eToro account instantly to your bank account. I tried this myself and was impressed with how quickly and seamlessly it worked. You can read my blog post about eToro Money here. Note that it can also serve as a cryptocurrency wallet, allowing you to send and receive crypto from any other wallet address in the world.

If you would like more information about setting up an eToro account, please click on this no-obligation website link [affiliate]. Don’t forget that you also get a free $100,000 virtual portfolio, which you can use to experiment with trading and investing strategies. I have certainly earned a lot from mine.

I had six more articles published in February on the excellent Mouthy Money website. The first is titled Travelling to Europe This Year? Here’s Why You Need a GHIC Card. If you’re unfamiliar with the GHIC or how it differs from the previous European Health Insurance Card (EHIC), this article reveals everything you need to know, from how to apply to why it’s so important for your travels.

Also in February Mouthy Money published How to Check Your Tax Code and Correct it if Necessary. Understanding your tax code and ensuring its accuracy can prevent you from overpaying (or underpaying) tax. In this article I explained everything you need in order to check and understand the code you have been allocated.

And in Make Extra Money Renting a Room I turned the spotlight on this traditional (but none the worse for that) method for making some extra money. If your circumstances allow it, letting a room in your home can be a great way of generating a sideline income. It will provide a regular, ongoing income stream, which could prove a lifeline in these financially challenging times. And you can choose between getting a full-time lodger or offering short-term lets. Better still, under the Rent a Room Scheme you can make up to £7,500 a year this way entirely tax free!

In What is the Trading Allowance and How Can You Profit From It? I discussed this valuable allowance for UK residents looking to earn extra income from trading or side hustles. Even if you have a full-time job already, under the Trading Allowance you can earn up to £1,000 a year without having to declare that income to the taxman or paying tax on it. Read my article for the full lowdown!

And in Could You Benefit From the Help to Save Scheme? I discussed this lesser-known government initiative which, if you’re eligible, can give your finances a valuable boost. The Help to Save scheme aims to help people on lower incomes build up their savings. Offering generous tax-free bonuses, Help to Save can provide significant benefits for qualifying individuals.

Finally, in Could a Smart Thermostat Save You Money?, I revealed how these clever devices can save you money on your energy bills. I recently had one fitted myself. In this article I reveal which I chose (and why) and share some tips based on my own experiences. My heating engineer Dave, who installed it for me, also gets an honourable mention!

As I’ve said before, Mouthy Money is a great resource for anyone interested in money-making and money-saving. From the range of articles published in February, I particularly enjoyed Where to Find the Best Money-Saving Resources in 2025 by regular MM contributor Shoestring Jane. Jane writes mainly about money saving and frugal living. You can see all of her articles for Mouthy Money via this web page.

The not-so-good news about Mouthy Money is that due to a change in their business strategy they will no longer be commissioning external content writers such as me and Jane. From a personal perspective I am obviously disappointed about this, but I have had a good run with them and wish them every success going forward. I will continue to follow Mouthy Money with interest and recommend PAS readers do the same. I am also available for other writing work in the personal finance sphere if anyone else should need me!

I also published several posts on Pounds and Sense in February. Some are no longer relevant, but I have listed the others below.

Debunking Common Myths About Over-50 Life Insurance is a guest post on behalf of my friends at British Seniors Insurance Services. It sets out seven common myths about life insurance for over-50s, including ‘I’m too old to get life insurance’ and ‘Life insurance for over-50s is too expensive’, and explains why these commonly-held beliefs are incorrect.

Marriage in Later Life – A Guide to the Financial and Legal Implications is another guest post, this time by my colleagues at HCR Law. In this eye-opening article, their family law specialist, Victoria Fellows, sets out some important considerations to take into account if you are thinking of marrying (or remarrying) in later life.

In How to Make Money From Stoozing, I discuss this method of making extra income by taking advantage of interest-free offer periods on credit cards. If you are well organized you can make hundreds of pounds by doing this, but there are certain pitfalls to avoid. My article sets out everything you need to know and shares some useful resources.

Don’t Miss Out! Use Your £20,000 ISA Allowance Before It’s Too Late is a reminder that the current tax year ends on 5 April 2025 – and if you don’t use your 2024/25 tax-free ISA allowance before that date, it will be gone forever. In my article I explain the main types of ISA and reveal the ones I invest in myself. I also reveal why using your ISA allowance may be especially important in the current tax year if certain rumours are to be believed.

Finally, in Get Your Will Written Free of Charge in March, I discuss Free Wills Month, which actually starts today (3rd March 2025). This event brings together a group of well-respected charities to offer members of the public aged 55 and over the chance to have their wills written (or updated) free using participating solicitors across the UK. If you don’t currently have a will, this no-obligation opportunity is well worth checking out.

I’ll close with a reminder that you can also follow Pounds and Sense on Facebook or Twitter (or X as we have to call it now). Twitter/X is my number one social media platform and I post regularly there. I share the latest news and information on financial matters, and other things that interest, amuse or concern me. So if you aren’t following my PAS account on Twitter/X, you are definitely missing out.

I am also on the BlueSky social media network under the username poundsandsense.bsky.social. For the time being anyway, Twitter/X will remain my primary social media platform, but I will also post details of my latest blog posts, third-party articles and other financial news and resources on BlueSky for those who prefer to follow me there.

As always, if you have any comments or questions, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts on PAS may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media:

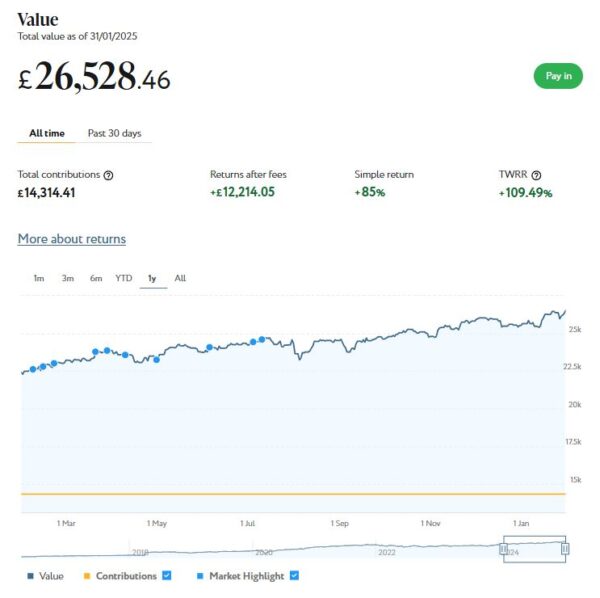

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

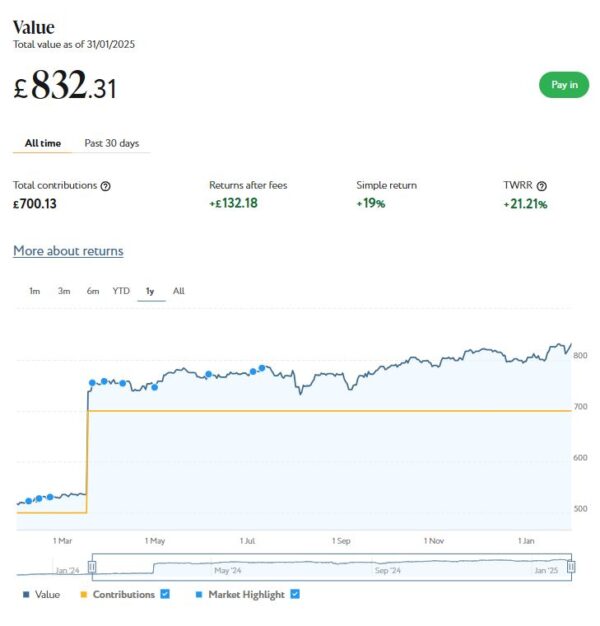

As the screenshot below for the last twelve months shows, my main Nutmeg portfolio is currently valued at £26,528. Last month it stood at £25,513, so that is an impressive rise of £1,015.

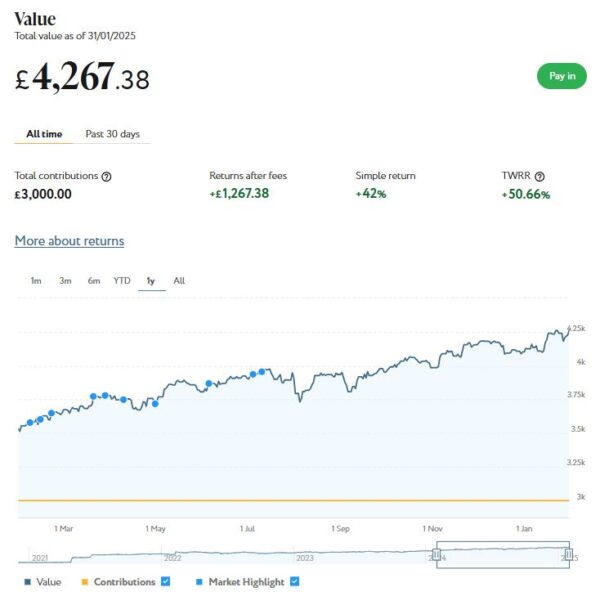

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £4,267 compared with £4,103 a month ago, a rise of £164. Here is a screen capture showing performance over the last twelve months.

Finally, at the start of December 2023 I invested £500 in one of Nutmeg’s new thematic portfolios (Resource Transformation). In March I also invested a further £200 from referral bonuses. As you can see from the screen capture below, this portfolio is now worth £832 compared with £798 last month, a rise of £34.

January has clearly been a good month for my Nutmeg investments. Their overall value has grown by £1,213 or 3.94% since the start of the year. And their value has increased by £5,193 or 19.65% in the twelve months since 31st January 2024.

You can read my full Nutmeg review here. If you are looking for a home for your annual ISA allowance, based on my overall experience over the last eight years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs), Lifetime ISAs and Junior ISAs as well.

Moving on, I also have investments with P2P property investment platform Assetz Exchange. As discussed in this recent post, the company has just rebranded as Housemartin.

My investments with Housemartin continue to generate steady returns. Housemartin focuses on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my HM portfolio has generated a respectable £229.98 in revenue from rental income. Capital growth has slowed, though, in line with UK property values generally.

At the time of writing, 15 of ‘my’ properties are showing gains, 2 are breaking even, and the remaining 18 are showing losses. My portfolio of 35 properties is currently showing a net decrease in value of £55.21, meaning that overall (rental income minus capital value decrease) I am up by £174.77. That’s still a decent return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Housemartin most projects are socially beneficial as well.

The overall fall in capital value of my Housemartin investments is obviously a little disappointing. But it’s important to remember that until/unless I choose to sell the investments in question, it is largely theoretical, based on the latest price at which shares in the property concerned have changed hands. The rental income, on the other hand, is real money (which in my case I’ve reinvested in other HM projects to further diversify my portfolio).

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of Housemartin as far as i am concerned. You can actually invest from as little as £1 per property if you really want to proceed cautiously.

As I noted in this blog post, Housemartin is particularly good if you want to compound your returns by reinvesting rental income. This effectively boosts the interest rate you are receiving. Personally, once I have accrued a minimum of £10 in rental payments, I reinvest this money in either a new HM project or one I have already invested in (thus increasing my holding). Over time, even if I don’t invest any more capital, this will ensure my investment with Housemartin grows at an accelerating rate and becomes more diversified as well.

My investment on Housemartin is in the form of an IFISA so there won’t be any tax to pay on profits, dividends or capital gains. I’ve been impressed by my experiences with Housemartin and the returns generated so far, and intend to continue investing with them. You can read my full review of Assetz Exchange/Housemartin here. You can also sign up for an account directly via this link [affiliate]. Bear in mind that, as from the current financial year (2024/25), you can open more than one IFISA per year.

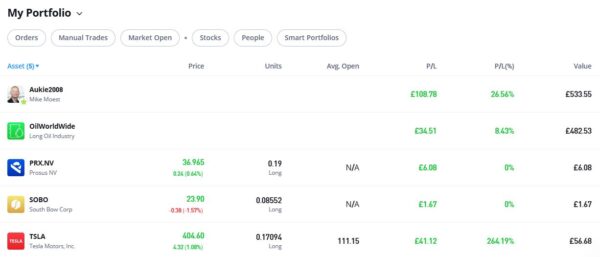

In 2022 I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios, Oil Worldwide. I also invested a small amount I had left over in Tesla shares.

As you can see from the screen captures below, my original investment (total value £888.36 in pounds sterling) is today worth £1,081.19, an overall increase of £192.16 or 21.71%.

Note: eToro now displays the value of investments in your native currency, although you can change this if you wish.

As you can see, my Oil WorldWide investment is showing a profit of 8.43%. That’s not overly exciting but the portfolio has just been rebalanced by eToro, so hopefully that will improve its performance going forward. The investment team at eToro periodically rebalance all smart portfolios to ensure that the mix of investments remains aligned with the portfolio’s goals, and to take advantage of any new opportunities that may present themselves.

My copy trading investment with Aukie2008 has been doing better, with an overall 26.56% profit. To be fair, I have held the latter investment a bit longer.

My Tesla shares, which I bought as an afterthought with a bit of spare cash I had in my account, have done particularly well in recent months. If only I had put a bit more money into this!

You might also notice that I have small holdings in Prosus NV, a Dutch internet group, and South Bow, a Canadian energy infrastructure company. To be honest I don’t understand how I acquired these, but I assume they are some sort of bonus I have been awarded. In any event, I am happy to have them in my portfolio!

eToro also offer the free eToro Money app. This allows you to deposit money to your eToro account without paying any currency conversion fees, saving you up to £5 for every £1,000 you deposit. You can also use the app to withdraw funds from your eToro account instantly to your bank account. I tried this myself and was impressed with how quickly and seamlessly it worked. You can read my blog post about eToro Money here. Note that it can also serve as a cryptocurrency wallet, allowing you to send and receive crypto from any other wallet address in the world.

If you would like more information about setting up an eToro account, please click on this no-obligation website link (affiliate).

I had another article published in January on the excellent Mouthy Money website. This is How to Make Money Through Bank Account Switching. In this article I discussed an easy method for generating handy lump sums by taking advantage of switching incentives offered by some UK banks. The banks are currently battling one another for your custom, and they are offering some enticing cash bonuses (and sometimes other freebies/benefits as well) to get you to sign up.

As I’ve said before, Mouthy Money is a great resource for anyone interested in money-making and money-saving. From the range of articles published in January, I particularly enjoyed 16 Ways to Be More Frugal and Save Money in 2025 by regular MM contributor Shoestring Jane. Jane writes mainly about money saving and frugal living. You can see all of her articles for Mouthy Money via this web page.

I also published several posts on Pounds and Sense in January. Some are no longer relevant, but I have listed the others below.

As mentioned earlier, I published a post titled P2P Property Investment Platform Assetz Exchange Rebrands as Housemartin. In this I discussed the recent rebrand of this P2P property investment platform, which I invest through myself. The post also discusses how the platform has changed since I first featured it here on Pounds and Sense.

In Here’s Why Most Over-50s Need More Protein in Their Diet I discussed a subject that will be relevant to many readers of this blog (which is of course aimed especially at over-50s). I must admit I hadn’t realised just how important this was until I saw the topic being discussed on GB News last month. I wanted to learn more and researched the subject with the aid of AI program ChatGPT. This blog post was the result.

In Take the Plum 52-Week Saving Challenge, I shared a method you can use to set aside a handy lump sum of up to £1,378 in a year. As you may gather, the method involves using the smart money app Plum [affiliate link]. This automates the whole process for you, making saving as easy and painless as possible. Read the article for full details!

Also in January I published a guest post on the subject Dos and Don’ts for Divorce in 2025. Written by an experienced divorce lawyer, this article sets out tips and guidelines to make the divorce process as pain-free as possible if, sadly, your marriage has run its course.

Finally, on a happier note, I published Planning a UK Holiday This Year? Here Are Some Ideas For You. In this article (which I update and republish annually) I set out a range of suggestions for short break (or longer) holidays in the UK, along with links to blog posts I have written about the destinations concerned.

Lastly, a reminder that you can also follow Pounds and Sense on Facebook or Twitter (or X as we have to call it now). Twitter/X is my number one social media platform and I post regularly there. I share the latest news and information on financial matters, and other things that interest, amuse or concern me. So if you aren’t following my PAS account on Twitter/X, you are definitely missing out.

I am also on the BlueSky social media network under the username poundsandsense.bsky.social. For the time being anyway, Twitter/X will remain my primary social media platform, but I will also post details of my latest blog posts, third-party articles and other financial news and resources on BlueSky for those who may prefer to follow me there.

That’s all for today. As always, if you have any comments or questions, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts on PAS may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media:

As regular readers of Pounds and Sense will know, I’m a fan of P2P property investment platform Assetz Exchange and have invested through them myself. AE have recently rebranded as Housemartin, so I thought I should write an update about this.

You can read my original detailed review of Assetz Exchange (as it was then) in this post. Much of this info still applies – so I won’t reproduce it all here – but certain things (as well as the name!) have changed.

Assetz Exchange began as a ‘traditional’ property crowdfunding platform, with investors coming together to buy a property. They then shared in the rental income received – and any profit if the property was subsequently sold – in proportion to the size of their investment. When I first wrote about Assetz Exchange they offered a variety of investment opportunities, including former show homes and development projects.

Nowadays, though, the company focuses on supported housing, working closely with charities and other organizations that assist people with physical and cognitive disabilities. These have generally proven the most reliable and hassle-free investments, so Housemartin have understandably chosen to concentrate on this.

Properties are generally let on long leases, with the charities taking responsibility for day-to-day management and maintenance. As mentioned, investors receive a share of the monthly rental received and any profits if/when the properties are sold (you can also potentially sell your holdings online at any time via the exchange, which serves as a secondary market). That puts these investments at the lower-risk end of the property investment spectrum (though there are, of course, still risks involved, and you should ensure you understand these and are comfortable with them before investing).

Assetz Exchange was originally part of the Assetz group of property investment companies that included Assetz Capital. In December 2023 Assetz announced it was withdrawing from the retail marketplace to work with institutional investors only. Partly as a consequence of this, the team behind Housemartin took the decision to part ways with the Assetz group and are no longer affiliated with them. Although they always operated separately from Assetz Capital, Housemartin is now an entirely independent P2P property investment platform. Regarding the name change, the company says:

“The name Housemartin reflects the company’s commitment to delivering robust, hassle-free, quality residential property investment opportunities that reward investors with monthly inflation-linked income. Just as the house martin bird is known for its sociability and adaptability, Housemartin aims to provide investors with an opportunity to pool funds with fellow investors to create much needed quality homes for people requiring support.”

Future Plans

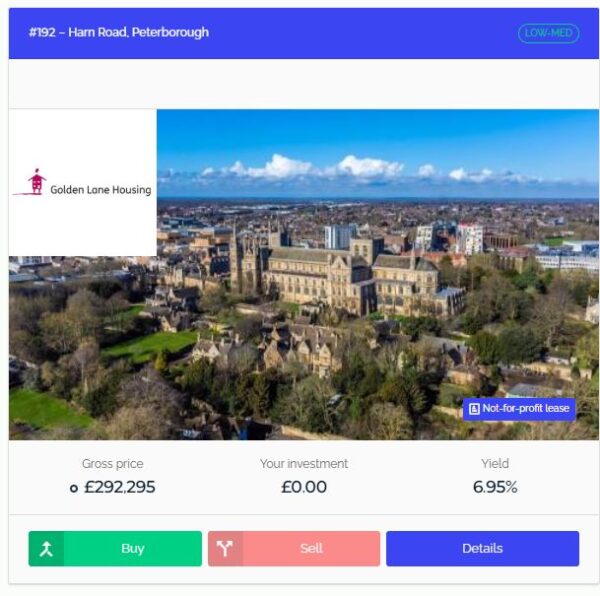

In its new guise as Housemartin, the company has big plans for 2025 and further into the future. They intend to stick to their strategy of working with partners in the supported housing sector, including (for example) Golden Lane Housing, Lets For Life and Halo Housing. A typical current opportunity from the website is shown below.

Peter Read, the MD of Housemartin, points out that with interest rates currently falling, this makes the returns of around 7% they can typically offer investors increasingly attractive (and of course there is the potential for capital growth as well). He also points out that rentals are raised every year in line with inflation.

Housemartin are currently launching a fundraising round on the investment platform Crowdcube. They are looking to raise additional capital which will be used to help the company expand and improve its offering. Anyone is welcome to invest via Crowdcube, though as this is a share offer it’s almost certainly riskier than investing via the platform itself, with no clearly defined exit route. Personally I do not plan to invest in Housemartin this way, but you can find out more if you wish by registering on the Crowdcube site.

My Own Experience

I put an initial £100 into the platform in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my portfolio has generated a respectable £227.35 in revenue from rental income. Capital growth has slowed, though, in line with UK property values generally.

At the time of writing, 12 of ‘my’ properties are showing gains, 3 are breaking even, and the remaining 20 are showing losses. My portfolio of 35 properties is currently showing a net decrease in value of £62.22, meaning that overall (rental income minus capital value decrease) I am up by £165.13. That’s still a decent return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Assetz Exchange the projects are socially beneficial as well.

The overall fall in capital value of my AE investments is obviously a bit disappointing. But it’s important to remember that until/unless I choose to sell the investments in question, it is theoretical, based on the latest price at which shares in the property concerned have changed hands. The rental income, on the other hand, is real money (which in my case I’ve reinvested in other HM projects to further diversify my portfolio).

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of HM as far as i am concerned. You can actually invest from as little as £1 per property if you really want to proceed cautiously.

As I noted in this blog post, Housemartin is particularly good if you want to compound your returns by reinvesting rental income. This effectively boosts the interest rate you are getting. Personally, once I have accrued a minimum of £10 in rental payments, I reinvest this money in either a new Housemartin project or one I have already invested in (thus increasing my holding). Over time, even if I don’t invest any more capital, this will ensure my investment with HM grows at an accelerating rate and becomes more diversified as well.

My investment on Housemartin is in the form of an IFISA so there won’t be any tax to pay on profits, dividends or capital gains. I’ve been impressed by my experiences with Housemartin and the returns generated so far, and intend to continue investing with them. If you wish you can also sign up for a no-obligation account on Housemartin directly via this link [affiliate]. Bear in mind that, as from this financial year (2024/25), you can open more than one IFISA per year so long as you don’t exceed your overall £20,000 ISA allowance.

Closing Thoughts

As I said earlier, I am a fan of Housemartin and have been investing with them for several years now. I have also spoken to their MD, Peter Read, on various occasions, and always found him open and honest.

My HM investments have performed well; and as far as I’m aware no investor has ever lost money through the platform. Obviously there are never any guarantees with investing – but if you like the idea of earning higher rates of interest than available from banks while helping vulnerable people secure a much-needed roof over their heads, Housemartin is certainly worth a look.

As always, if you have any queries about this blog post or Housemartin more generally, do leave a comment as usual.

Disclosure: As stated in this post, I am an investor with Housemartin and also an affiliate for them. If you click through my link and sign up, I may receive a commission for introducing you. This will not affect in any way the service you receive or the terms you are offered.

Please be aware also that I am not a professional financial adviser. You should always do your own ‘due diligence’ before investing and seek advice from a qualified adviser if in any doubt how best to proceed. All investing carries a risk of loss.

If you enjoyed this post, please link to it on your own blog or social media:

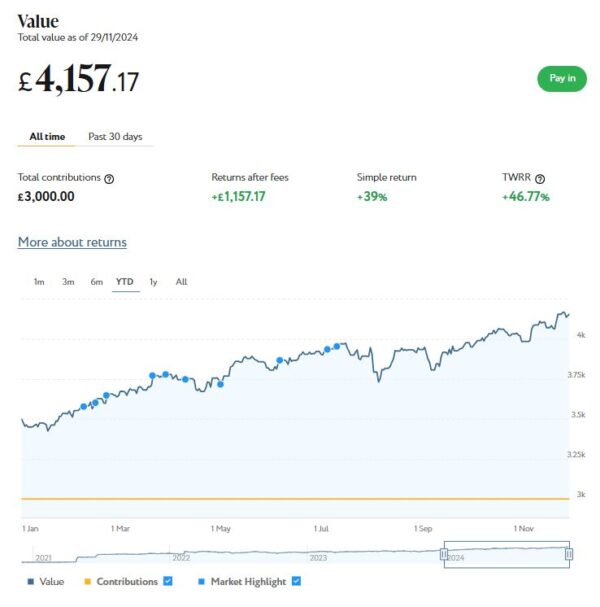

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

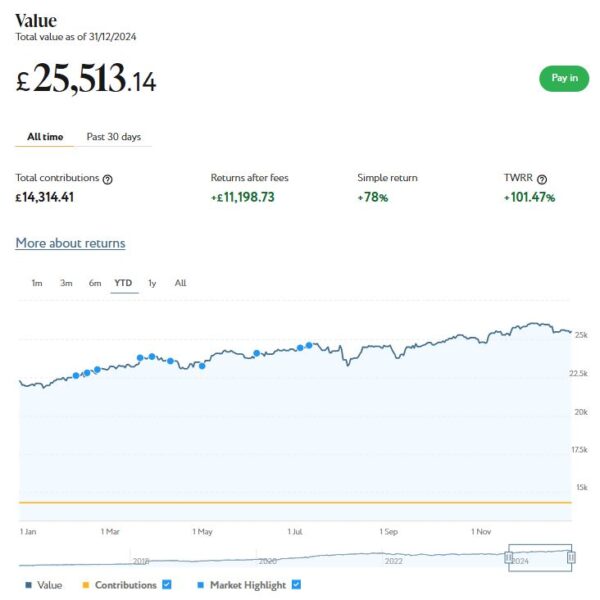

As the screenshot below for the year to date shows, my main Nutmeg portfolio is currently valued at £25,513. Last month it stood at £25,822, so that is a fall of £309.

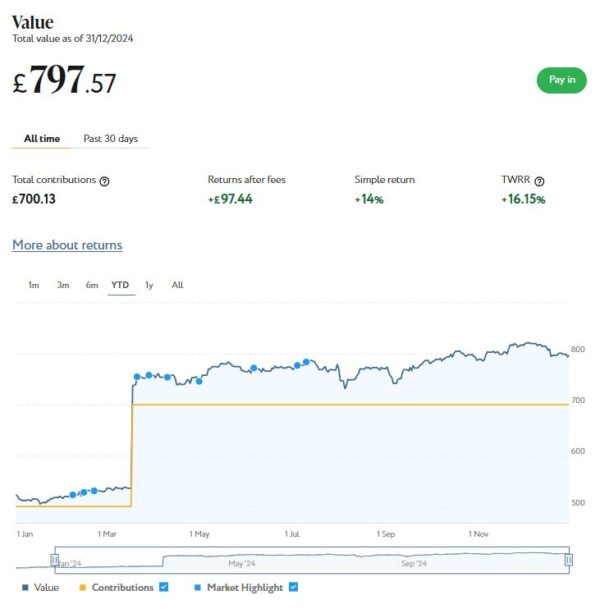

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £4,103 compared with £4,157 a month ago, a fall of £54. Here is a screen capture showing performance over the year to date.

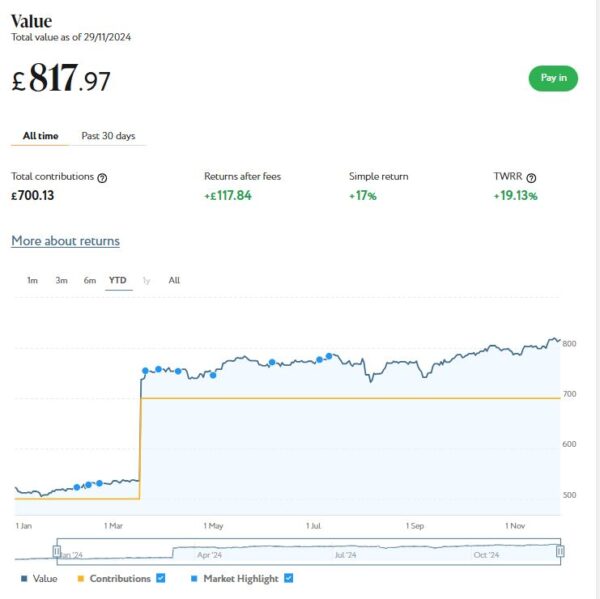

Finally, at the start of December 2023 I invested £500 in one of Nutmeg’s new thematic portfolios (Resource Transformation). In March I also invested a further £200 from referral bonuses. As you can see from the YTD screen capture below, this portfolio is now worth £798 (rounded up) compared with £818 last month, a fall of £20.

As you will note, following a very good month in November, December saw the value of my Nutmeg investments fall back somewhat. Their overall value dropped by £383 or 1.24% since the start of December. Sadly there was no sign of a Santa rally this year…

Overall, 2024 has still been a good year for my Nutmeg investments though. They are up in value by £4,098 or 15.57% since January 1st 2024.

You can read my full Nutmeg review here. If you are looking for a home for your annual ISA allowance, based on my overall experience over the last eight years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs), Lifetime ISAs and Junior ISAs as well.

Moving on, I also have investments with P2P property investment platform Assetz Exchange. This has now renamed itself as Housemartin. There have been a few other changes as well, so I shall be writing a separate blog post about this soon.

My investments with Housemartin continue to generate steady returns. Housemartin focuses on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my HM portfolio has generated a respectable £225.17 in revenue from rental income. Capital growth has slowed, though, in line with UK property values generally.

At the time of writing, 14 of ‘my’ properties are showing gains, 2 are breaking even, and the remaining 18 are showing losses. My portfolio of 34 properties is currently showing a net decrease in value of £48.60, meaning that overall (rental income minus capital value decrease) I am up by £176.57. That’s still a decent return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Housemartin most projects are socially beneficial as well.

The overall fall in capital value of my Housemartin investments is obviously a little disappointing. But it’s important to remember that until/unless I choose to sell the investments in question, it is largely theoretical, based on the latest price at which shares in the property concerned have changed hands. The rental income, on the other hand, is real money (which in my case I’ve reinvested in other HM projects to further diversify my portfolio).

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of Housemartin as far as i am concerned. You can actually invest from as little as 80p per property if you really want to proceed cautiously.

As I noted in this blog post, Housemartin is particularly good if you want to compound your returns by reinvesting rental income. This effectively boosts the interest rate you are receiving. Personally, once I have accrued a minimum of £10 in rental payments, I reinvest this money in either a new HM project or one I have already invested in (thus increasing my holding). Over time, even if I don’t invest any more capital, this will ensure my investment with Housemartin grows at an accelerating rate and becomes more diversified as well.

My investment on Housemartin is in the form of an IFISA so there won’t be any tax to pay on profits, dividends or capital gains. I’ve been impressed by my experiences with Housemartin and the returns generated so far, and intend to continue investing with them. You can read my full review of Assetz Exchange/Housemartin here. You can also sign up for an account directly via this link [affiliate]. Bear in mind that, as from this financial year (2024/25), you can open more than one IFISA per year.

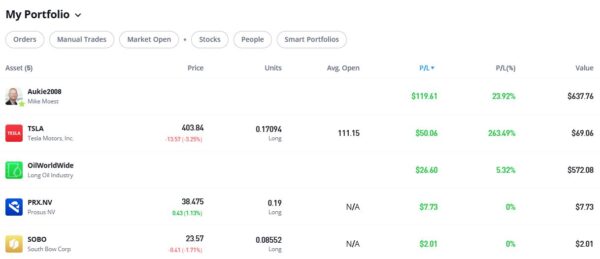

In 2022 I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios, Oil Worldwide. I also invested a small amount I had left over in Tesla shares.

As you can see from the screen captures below, my original investment totalling $1,022.26 is today worth $1,289.44, an overall increase of $266.98 or 26.14%.

As you can see, my Oil WorldWide investment is showing a modest profit of 5.32%. That’s a bit underwhelming but the portfolio has just been rebalanced by eToro, so hopefully that will improve its performance going forward. The investment team at eToro periodically rebalance all smart portfolios to ensure that the mix of investments remains aligned with the portfolio’s goals, and to take advantage of any new opportunities that may present themselves.

My copy trading investment with Aukie2008 has been doing better, with an overall 23.92% profit. To be fair, I have held the latter investment a bit longer.

My Tesla shares, which I bought as an afterthought with a bit of spare cash I had in my account, have done particularly well in recent weeks. If only I had put a bit more money into this!

You might also notice that I have small holdings in Prosus NV, a Dutch internet group, and South Bow, a Canadian energy infrastructure company. To be honest I don’t understand how I acquired these, but I assume they are some sort of bonus I have been awarded. In any event, I am happy to have them in my portfolio!

eToro also offer the free eToro Money app. This allows you to deposit money to your eToro account without paying any currency conversion fees, saving you up to £5 for every £1,000 you deposit. You can also use the app to withdraw funds from your eToro account instantly to your bank account. I tried this myself and was impressed with how quickly and seamlessly it worked. You can read my blog post about eToro Money here. Note that it can also serve as a cryptocurrency wallet, allowing you to send and receive crypto from any other wallet address in the world.

I had two more articles published in December on the excellent Mouthy Money website. The first is How to Save Money on Rail Fares With Split Ticketing. In this article I discussed a money-saving hack called ‘split ticketing’ that savvy travellers can use to reduce their fare costs, often by a substantial amount. Split ticketing involves breaking a journey into two or more smaller segments, purchasing separate tickets for each segment rather than one through-ticket. In my article I discussed how to apply this method and revealed my favourite split-ticketing app.

Also in December Mouthy Money published my article How to Check and Improve Your Credit Score. In this article I shone a spotlight on a vital aspect of our financial health. Your credit score affects everything from loan approvals to mortgage rates. It’s a measure of how reliably you handle credit and debt, and lenders use it to assess risk. My article reveals everything you need to understand, check and improve your credit score.

As I’ve said before, Mouthy Money is a great resource for anyone interested in money-making and money-saving. If you haven’t checked it out yet, why not get the new year off to a good start by visiting their website. Besides a wide range of interesting articles by me and other writers, currently you can enter a free competition to win one of five copies of How to Retire by Christine Benz.

I also published several posts on Pounds and Sense in December. Some are no longer relevant, but I have listed the others below.

With flu and other seasonal viruses (although not Covid) currently surging, in Stay Healthy This Winter: The Best Supplements for Cold and Flu Season I set out eight of the best supplements to support your immune system during the colder months. This post was researched and written with the assistance of AI (ChatGPT).

And in My Top Twenty Posts of 2024 I listed the top twenty posts on Pounds and Sense in 2024, based on comments, page-views and social media shares (excluding any posts that are no longer relevant). I hope you will enjoy revisiting these posts, or seeing them for the first time if you are new to PAS.

Lastly, a reminder that you can also follow Pounds and Sense on Facebook or Twitter (or X as we have to call it now). Twitter/X is my number one social media platform and I post regularly there. I share the latest news and information on financial matters, and other things that interest, amuse or concern me. So if you aren’t following my PAS account on Twitter/X, you are definitely missing out.

I have also just joined the new BlueSky social media network. My username there is poundsandsense.bsky.social. For the time being at least, Twitter/X will remain my main social media platform, but I will also post details of my latest blog posts, third-party articles and other financial news and resources on BlueSky for those who prefer to follow me there.

That’s all for today. Once again, I should like to wish you a very happy and prosperous new year. As always, if you have any comments or questions, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts on PAS may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media:

As is customary for bloggers at this time of year, here are the top twenty posts on Pounds and Sense in 2024, based on comments, page-views and social media shares. They are in no particular order. I have excluded any posts that are no longer relevant.

I hope you will enjoy revisiting these posts, or seeing them for the first time if you are new to PAS.

All posts in the list below should open in a new tab/window when you click on the link concerned.

Thank you for being a valued Pounds and Sense reader. Just a reminder that you can get notifications every time the blog is updated via the Subscribe box on the right (or scroll down on mobile devices). You can also follow PAS on X/Twitter and Facebook and now on BlueSky as well 🙂

If you have any comments or questions about this post, of course, feel free to leave them below as usual.

If you enjoyed this post, please link to it on your own blog or social media:

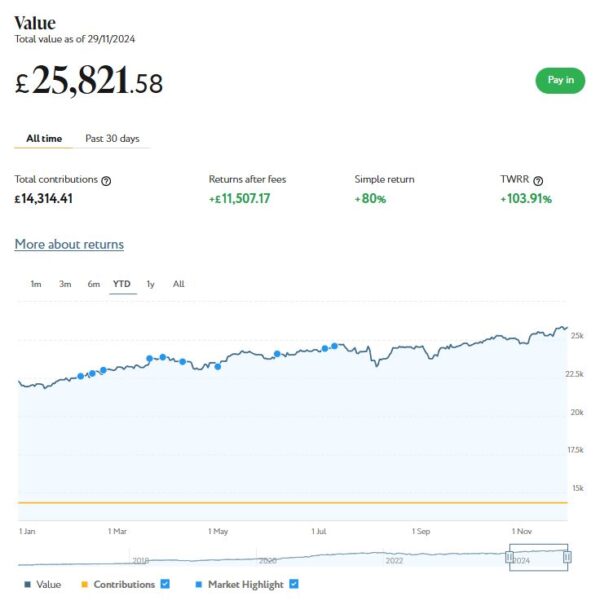

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

As the screenshot below for the year to date shows, my main Nutmeg portfolio is currently valued at £25,822 (rounded up). Last month it stood at £24,799, so that is an impressive increase of £1,023.

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £4,157 compared with £3,988 a month ago, a rise of £169. Here is a screen capture showing performance over the year to date.

Finally, at the start of December 2023 I invested £500 in one of Nutmeg’s new thematic portfolios (Resource Transformation). In March I also invested a further £200 from referral bonuses. As you can see from the YTD screen capture below, this portfolio is now worth £818 (rounded up) compared with £789 last month, a rise of £29.

As you can see, November was a good month for my Nutmeg investments. The overall value has risen by £1,221 or 4.13% since the start of November. They are also up by £4,482 or 17.03% since the start of the year.

You can read my full Nutmeg review here. If you are looking for a home for your annual ISA allowance, based on my overall experience over the last eight years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs), Lifetime ISAs and Junior ISAs as well.

Note that I am no longer an affiliate for Nutmeg. That means you won’t find any affiliate links in my review (or anywhere else on PAS). And you will no longer see the no-fees-for-six-months offer I used to promote as an affiliate. However, the better news is that you can still get six months free of any management fees by registering with Nutmeg via my Refer a Friend link. I will receive a gift voucher if you do this, which is duly appreciated

Don’t forget, also, that the current tax year began on 6 April 2024. Despite some predictions to the contrary, you still have a full £20,000 tax-free ISA allowance for 2024/25. As from this year, you can open any number of ISAs with different providers in the same tax year, as long as you don’t exceed your overall £20,000 allowance. So opening a stocks and shares ISA with Nutmeg won’t prevent you from also opening one with another S&S ISA provider (should you wish to) later in the financial year.

Moving on, I also have investments with P2P property investment platform Assetz Exchange. These continue to generate steady returns. Assetz Exchange focuses on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my AE portfolio has generated a respectable £220.04 in revenue from rental income. Capital growth has slowed, though, in line with UK property values generally.

At the time of writing, 12 of ‘my’ properties are showing gains, 4 are breaking even, and the remaining 18 are showing losses. My portfolio of 34 properties is currently showing a net decrease in value of £44.11, meaning that overall (rental income minus capital value decrease) I am up by £175.93. That’s still a decent return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Assetz Exchange most projects are socially beneficial as well.

The overall fall in capital value of my AE investments is obviously a little disappointing. But it’s important to remember that until/unless I choose to sell the investments in question, it is largely theoretical, based on the latest price at which shares in the property concerned have changed hands. The rental income, on the other hand, is real money (which in my case I’ve reinvested in other AE projects to further diversify my portfolio).

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of AE as far as i am concerned. You can actually invest from as little as 80p per property if you really want to proceed cautiously.

As I noted in this blog post, Assetz Exchange is particularly good if you want to compound your returns by reinvesting rental income. This effectively boosts the interest rate you are receiving. Personally, once I have accrued a minimum of £10 in rental payments, I reinvest this money in either a new AE project or one I have already invested in (thus increasing my holding). Over time, even if I don’t invest any more capital, this will ensure my investment with AE grows at an accelerating rate and becomes more diversified as well.

My investment on Assetz Exchange is in the form of an IFISA so there won’t be any tax to pay on profits, dividends or capital gains. I’ve been impressed by my experiences with Assetz Exchange and the returns generated so far, and intend to continue investing with them. You can read my full review of Assetz Exchange here. You can also sign up for an account on Assetz Exchange directly via this link [affiliate]. Bear in mind that, as from this financial year (2024/25), you can open more than one IFISA per year.

In 2022 I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios, Oil Worldwide. I also invested a small amount I had left over in Tesla shares.

As you can see from the screen captures below, my original investment totalling $1,022.26 is today worth $1,315.34, an overall increase of $293.08 or 28.67%.

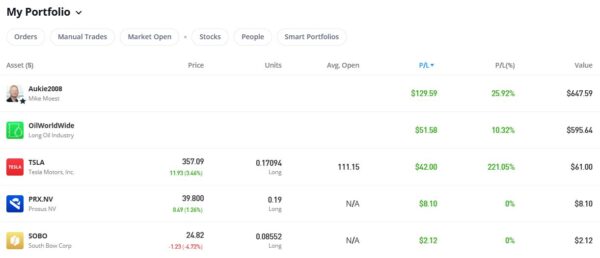

As you can see, my Oil WorldWide investment is showing a respectable if not outstanding profit of 10.32%. My copy trading investment with Aukie2008 has been doing better, with an overall 25.95% profit. To be fair, I have held the latter investment a bit longer.

You might also notice that I have small holdings in Prosus NV, a Dutch internet group, and South Bow, a Canadian energy infrastructure company. To be honest I don’t understand how I acquired these, but I assume they are some sort of bonus I have been awarded. In any event, I am happy to have them in my portfolio!

eToro also offer the free eToro Money app. This allows you to deposit money to your eToro account without paying any currency conversion fees, saving you up to £5 for every £1,000 you deposit. You can also use the app to withdraw funds from your eToro account instantly to your bank account. I tried this myself and was impressed with how quickly and seamlessly it worked. You can read my blog post about eToro Money here. Note that it can also serve as a cryptocurrency wallet, allowing you to send and receive crypto from any other wallet address in the world.

I had two more articles published in November on the excellent Mouthy Money website. The first is Ten Ways to Boost Your Bank Balance in the Run-up to Christmas. As Christmas approaches, many of us are feeling the pinch, with the cost of gifts, food and festivities adding up. And that’s before you even factor in the cost of living crisis, tax increases, benefit cuts, and so on. So in this article I set out a variety of ways you may be able to boost your income in the weeks leading up to the big day.

Also in November Mouthy Money published my article Get Fit, Make Money – How to Profit from Fitness Apps. In this article I revealed a variety of methods by which you may be able to get fit and boost your bank balance at the same time.

As I’ve said before, Mouthy Money is a great resource for anyone interested in money-making and money-saving. From the range of articles published in November, I particularly enjoyed this guide to saving money by selling stuff on eBay and other websites by regular MM contributor Shoestring Jane. Jane writes mainly about money saving and frugal living. You can see all of her articles for Mouthy Money via this web page.

I also published (or republished) several posts on Pounds and Sense in November. Some are no longer relevant, but I have listed the others below.

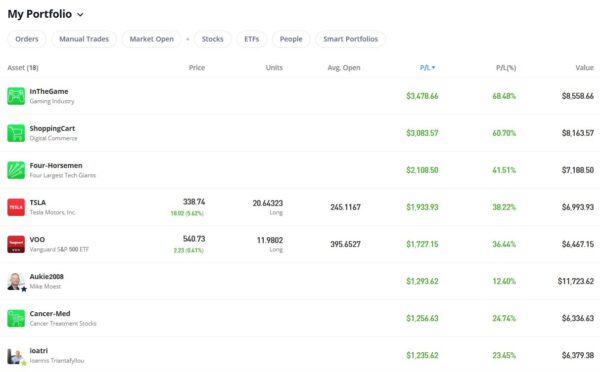

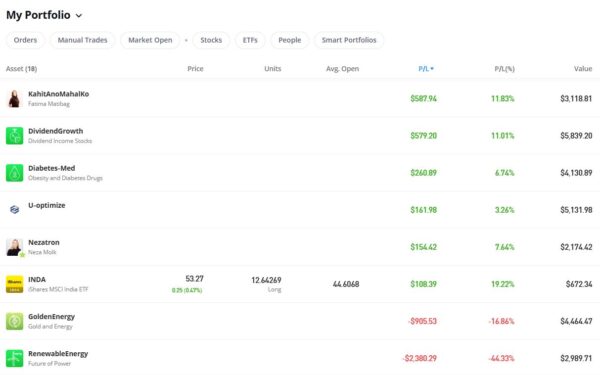

In Update on my eToro Virtual Portfolio, I brought readers up to date with how my eToro VP has been doing and discussed what lessons could be learned from it. As I say in the article, anyone joining the eToro trading and investing platform automatically gets a $100,000 virtual portfolio in which they can experiment with different investing styles and strategies. I found it very interesting to revisit my VP a year on. I was pleased to discover that since my previous VP update, and despite the fact I hadn’t really paid it much attention, performance had turned around and the port was showing a good profit (unfortunately virtual as well!). As ever there were winners and losers, and these will inform my real-money trading as well.

With Christmas fast approaching, last month I published What Are the Best Video Calling Tools for Older People? For older people (in particular) video calling can provide a great way of connecting with far-flung family and friends if – for whatever reason – they can’t meet in person. In this article I set out the main options available and shared a few hints and tips for making the most of them.

And in Twelve Great Christmas Gift Ideas for Older People (That Aren’t Socks) I set out 12 suggestions for presents for older friends and relatives that – based on my experience as an older person myself – should put a smile on their faces! If you’re struggling for ideas for gifts for older friends and relatives, check this out

Lastly, a reminder that you can also follow Pounds and Sense on Facebook or Twitter (or X as we have to call it now). Twitter/X is my number one social media platform and I post regularly there. I share the latest news and information on financial (and other) matters, and other things that interest, amuse or concern me. So if you aren’t following my PAS account on Twitter/X, you are definitely missing out.