Today I thought I would take a closer look at Index Funds. These are among the most straightforward and cost-effective ways to invest in the stock market – especially for long-term savers and beginners.

Instead of trying to pick individual shares, index funds track a market index such as the FTSE 100, giving you broad exposure to many companies at once. This helps spread risk and keeps costs low.

In this article, I’ll explain what index funds are, which market indices they track (with a focus on popular UK and global examples), the pros and cons of index investing, and how you can invest in these funds from the UK.

What Is an Index Fund?

An index fund is a type of pooled investment that aims to mirror the performance of a specific stock market index such as the FTSE 100 or the S&P 500, rather than trying to beat it via active stock picking.

Because these funds simply follow a set rule (i.e. “invest in all the companies in this index”), they tend to have much lower fees than actively managed funds.

Common Market Indices Tracked by Index Funds

UK Market Indices

FTSE 100 – Tracks the 100 largest companies on the London Stock Exchange, such as Shell and HSBC.

FTSE 250 – Covers mid-sized UK companies (not including those in the FTSE100), giving broader UK-specific economic exposure.

FTSE All-Share – Includes hundreds of UK companies across large, mid and small caps.

International Indices

S&P 500 (USA) – 500 of the largest US companies by market value.

FTSE All-World – Broad global coverage of thousands of companies across developed and emerging markets.

MSCI World – Tracks large and mid-cap companies in developed economies.

Popular UK Index Funds You Can Invest In

Here are some specific examples of index funds and ETFs available to UK investors:

UK-Focused Trackers

iShares Core FTSE 100 UCITS ETF (LSE: ISF) – Tracks the FTSE 100 index with a low ongoing charge (~0.07%).

Vanguard FTSE 100 UCITS ETF (VUKE) – Another FTSE 100 tracker, from Vanguard.

Vanguard FTSE 250 UCITS ETF – Provides exposure to mid-sized UK companies via the FTSE 250 index.

HSBC FTSE 250 Index Tracker – A low-cost option that tracks the FTSE 250.

Vanguard FTSE UK All-Share Index Fund – A broader UK fund tracking a wide range of UK shares.

Global and International Trackers

SPDR S&P 500 UCITS ETF – Tracks the S&P 500 for US market exposure.

FTSE All-World ETFs / Funds – Provide broad world-wide market exposure including developed and some emerging markets (often available via major brokers under names like FTSE All-World).

iShares MSCI World ETFs – Track global developed markets outside the UK.

💡 Most of these are available as ETFs you can buy and sell on the London Stock Exchange, and many can be held inside tax-efficient accounts like ISAs and SIPPs.

Pros of Investing in Index Funds

✅ Low Costs

Index funds usually have much lower fees than actively managed funds because there’s no expensive stock-picking involved.

✅ Diversification

A single index fund can give you exposure to hundreds or thousands of companies, spreading risk across many businesses.

✅ Simple and Transparent

The strategy and holdings are easy to understand – you know exactly which index you’re following.

✅ Competitive Long-Term Returns

Over long periods, passive index funds have often matched or beaten actively managed funds, especially after fees.

Cons of Investing in Index Funds

⚠️ You Can’t Beat the Market

Index funds aim to match the performance of their benchmark, not outperform it.

⚠️ No Protection in Downturns

When the market falls, your fund generally will too – there’s no active manager moving your investment into “safer” assets.

⚠️ Concentration Risk

Some indices (e.g. the S&P 500) are heavily weighted toward certain sectors (like tech), so your exposure might be concentrated.

Ways to Invest in Index Funds in the UK

🪙 Through a Stocks & Shares ISA

This is one of the most tax-efficient ways to hold index funds: you won’t pay UK taxes on gains or dividends each year.

🧓 Via a SIPP

Index funds can form the core of a low-cost SIPP (Self Invested Personal Pension) portfolio. Contributions may also receive tax relief.

📈 Through Investment Platforms

Platforms like Hargreaves Lansdown, AJ Bell, Interactive Investor and Trading 212 let you buy and manage index funds directly.

🤖 Robo-Advisers

Services like Nutmeg (recently renamed JP Morgan Personal Investing) or Moneybox automatically build diversified portfolios using index funds based on your risk profile.

Final Thoughts

Index funds are an excellent foundation for long-term investing – especially if you want a low-cost, diversified, hands-off approach. With options covering UK, US and global markets, you can build a portfolio that matches your goals and risk tolerance.

Disclaimer: I am not a qualified financial adviser and nothing in this article should be construed as personal financial advice. It’s important to do your own ‘due diligence’ before investing and speak to a professional financial adviser/planner if in any doubt how best to proceed. All investments carry a risk of loss.

If you enjoyed this post, please link to it on your own blog or social media:

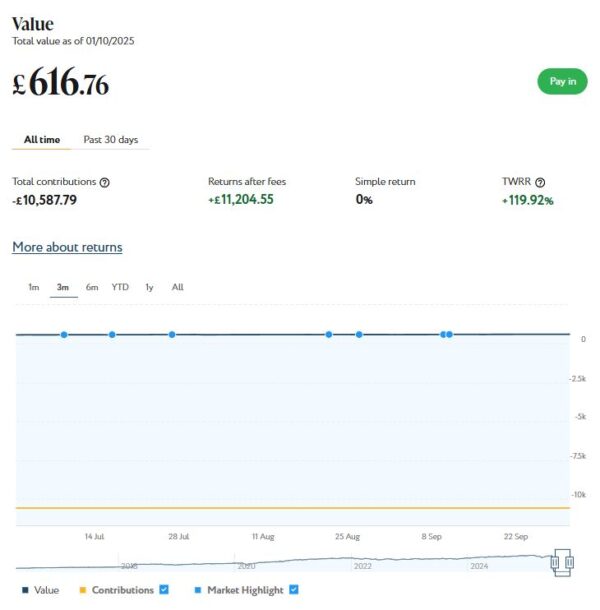

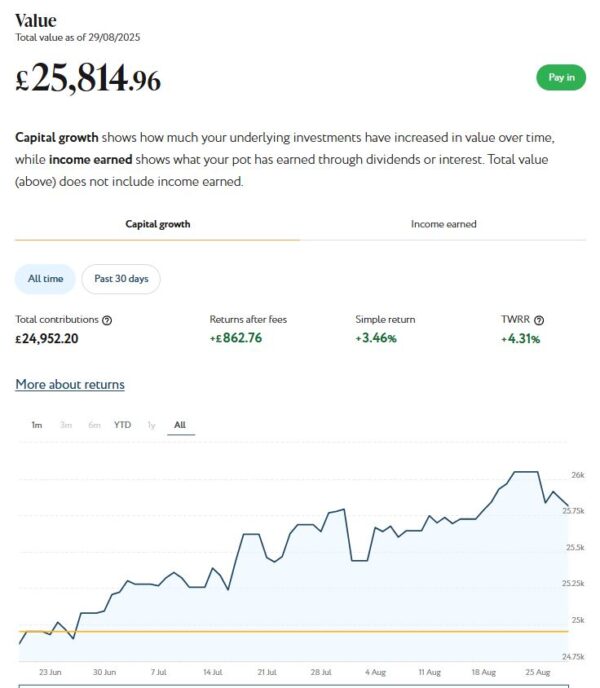

I’ll begin as usual with my JP Morgan Personal Investing (previously Nutmeg) Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

As regular readers will know, in June this year I transferred most of the money in my former Nutmeg Fully Managed portfolio (just under £25,000) to a new Nutmeg Income Portfolio. I discussed this in detail in this post, but basically money in this port is invested to generate an income from share dividends and other sources. This is then paid monthly. Capital appreciation is targeted as well, but these portfolios are aimed primarily at older people (and others) who want/need their investment to generate a regular cash income.

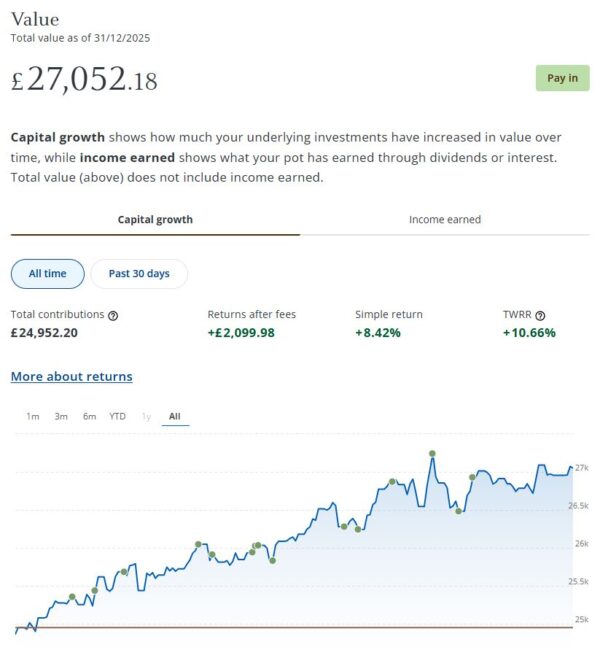

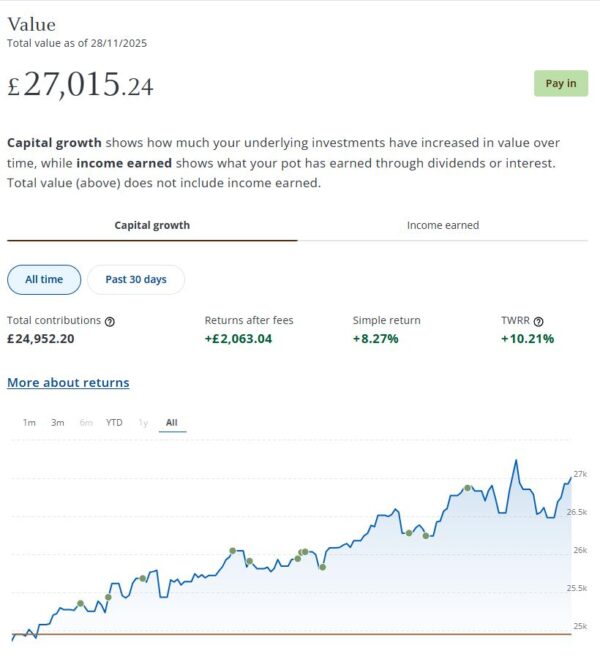

In December my JPM Investing income portfolio generated £75.04 of income, which was duly paid in to my bank account on 24 December 2025. That means I have now received a total (tax-free) income of £471.46 to date. That’s about what I would have hoped for based on JPM’s projected annual return of just under 5% for income ports at my chosen risk level (five).

My income portfolio grew in value again in December. It’s now worth £27,052 compared with £27,015 at the start of last month, a rise of £37. As the screen capture shows, the port has actually increased by £2,099.98 (8.42%) since I opened it in June this year. That’s clearly good going, though I don’t suppose it will carry on like this indefinitely. I should maybe also mention that performance may have been helped a bit by the no-fees introductory offer on Nutmeg/JPM income portfolios until the end of 2025. That has ended now, of course.

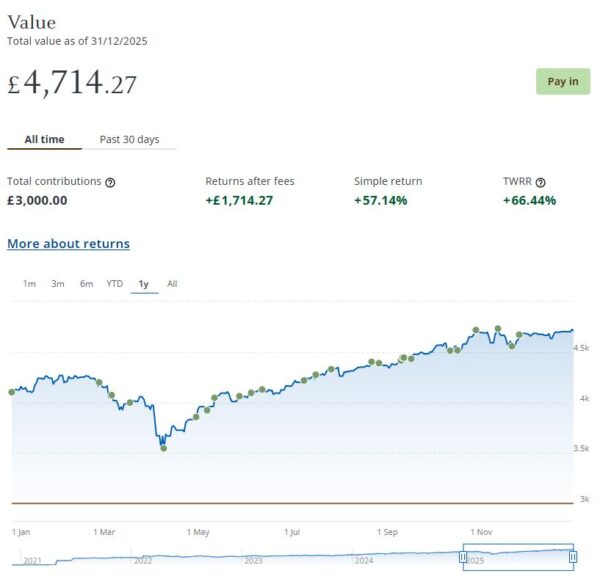

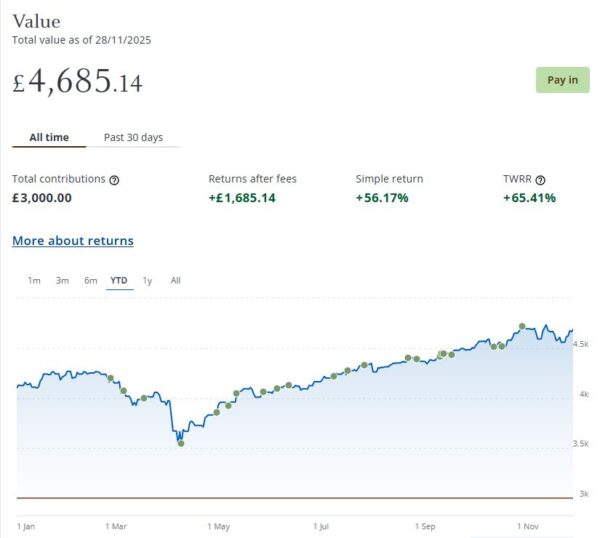

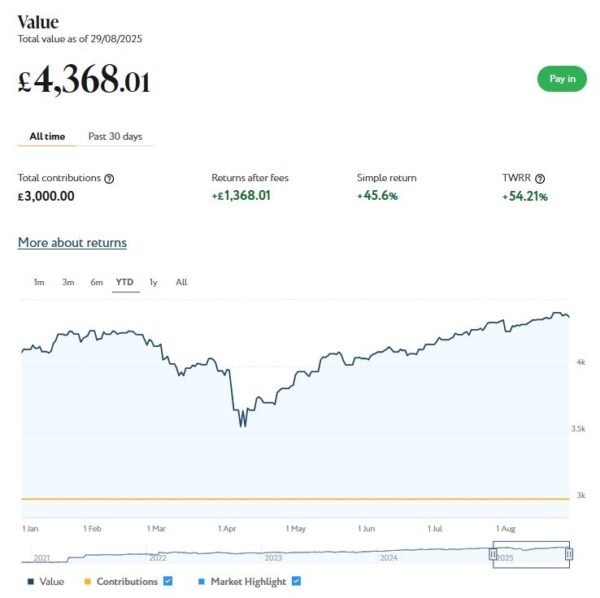

I still have a smaller, growth-oriented pot using JPM Investing’s Smart Alpha option. This is now worth £4,714 compared with £4,685 a month ago, an increase of £29. Here is a screen capture showing performance over the last year.

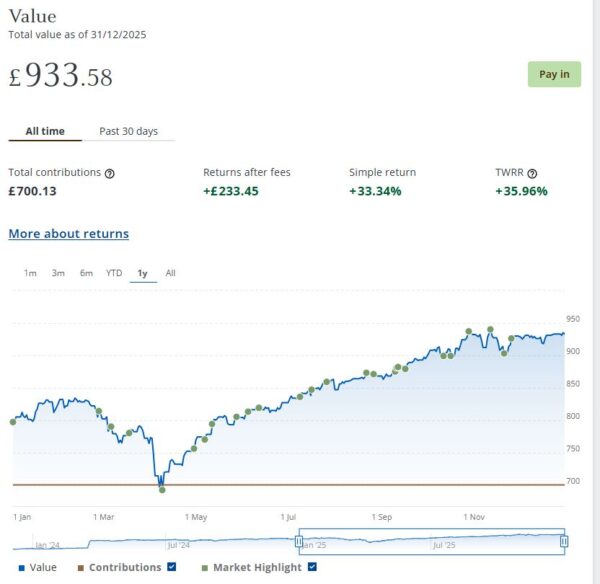

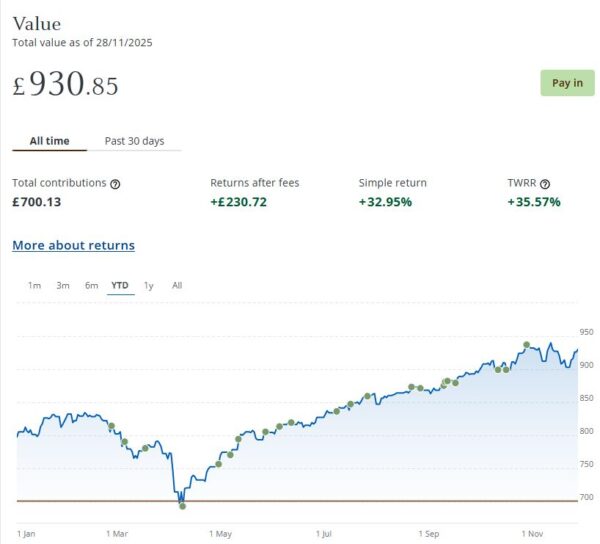

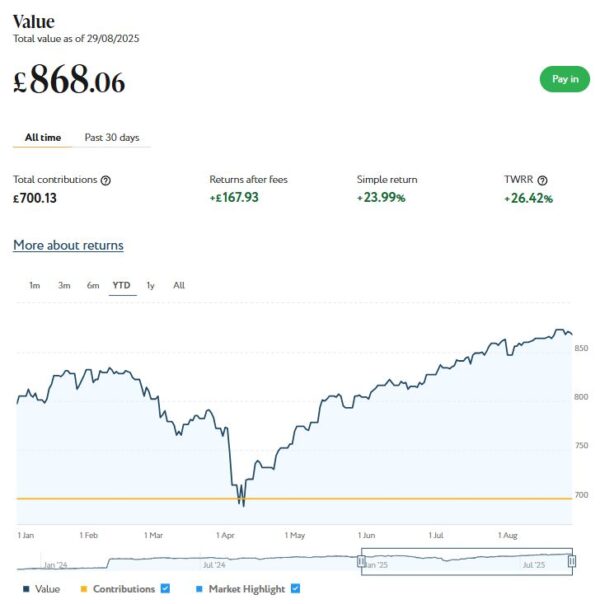

And at the start of December 2023 I invested £500 in one of Nutmeg/JPM’s thematic portfolios (Resource Transformation). In March 2024 I also invested a further £200 from referral bonuses (something I no longer receive for reasons I won’t bore you with). As you can see from the screen capture below, this portfolio is now worth £934 (rounded up) compared with £931 last month, a small increase of £3.

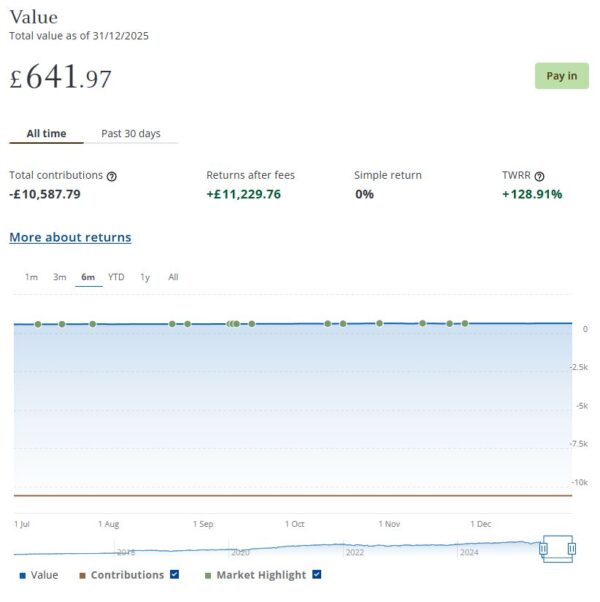

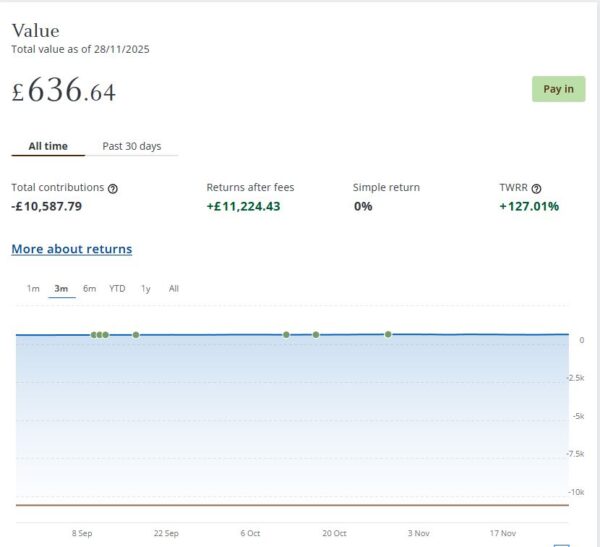

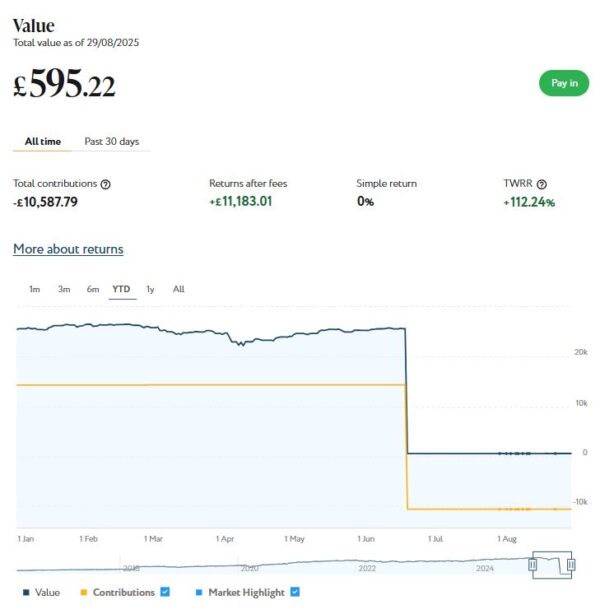

Finally, I still have a small amount left in my original Nutmeg/JPM Fully Managed portfolio. I have kept this largely for comparison purposes. This has also increased slightly in value from £637 at the start of December to £642 (rounded up) now, a rise of £5.

Overall in December I was up by £74 or 0.31%. In addition I did, of course, receive £75.04 in income from my income portfolio. Overall, then, I am in profit for the month by £149.04.

Excluding income generated, the overall value of my JPM investments is up by £2,914 or 9.58% since the start of 2025, so the April 2025 fall (caused largely by Trump’s tariffs) has now fully reversed. If you add to this figure the £471.46 of income generated so far, that gives a total profit for the last 12 months of £3,385.46 – not a bad return in these uncertain times.

As I always have to say, some volatility is to be expected with stock market investments, but over the longer term they tend to even themselves out (and generally perform better than bank savings accounts, although that is never guaranteed). In general the worst thing you can do is panic and sell up when downturns occur (as happened in April last year). You are then crystallizing your losses rather than giving the markets time to recover. This is something I had cause to discuss in this blog post.

You can read my full original Nutmeg/JPM review here. If you are looking for a home for your annual ISA allowance, based on my overall experience over the last nine years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs), Lifetime ISAs and Junior ISAs as well.

As mentioned above, Nutmeg have rebranded as J.P. Morgan Personal Investing and their website is now at www.personalinvesting.jpmorgan.com.

Moving on, I also have investments with P2P property investment platform Assetz Exchange. As discussed in this post, the company has rebranded as Housemartin.

My investments with Housemartin continue to generate steady returns. Housemartin focuses on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my HM portfolio has generated a respectable £291.50 in revenue from rental income. I have made a small net loss of £21.68 on property disposals. Capital growth generally has slowed, in line with UK property values generally.

At the time of writing, 13 of ‘my’ properties are showing gains, 5 are breaking even, and the remaining 24 are showing losses. My portfolio of 42 properties is currently showing a net decrease in value of £72.54. That means that overall (rental income minus capital value decrease and loss on disposal) I am up by £197.28. That’s still a respectable return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Housemartin most projects are socially beneficial as well.

The net fall in capital value of my Housemartin investments is obviously a little disappointing. But it’s important to remember that until/unless I choose to sell the investments in question, it is largely theoretical, based on the latest price at which shares in the property concerned have changed hands. The rental income, on the other hand, is real money (which in my case I’ve reinvested in other HM projects to further diversify my portfolio).

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of Housemartin as far as i am concerned. You can actually invest from as little as £1 per property if you really want to proceed cautiously.

As I noted in this blog post, Housemartin is particularly good if you want to compound your returns by reinvesting rental income. This effectively boosts the interest rate you are receiving. Personally, once I have accrued a minimum of £10 in rental payments, I usually reinvest this money in either a new HM project or one I have already invested in (thus increasing my holding). Over time, even if I don’t invest any more capital, this will ensure my investment with Housemartin grows at an accelerating rate and becomes more diversified as well.

In 2022 I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios, Oil Worldwide. I also invested a small amount I had left over in Tesla shares.

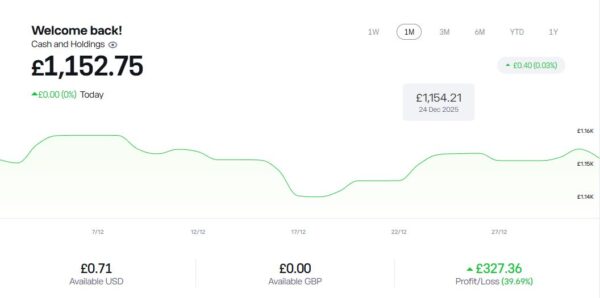

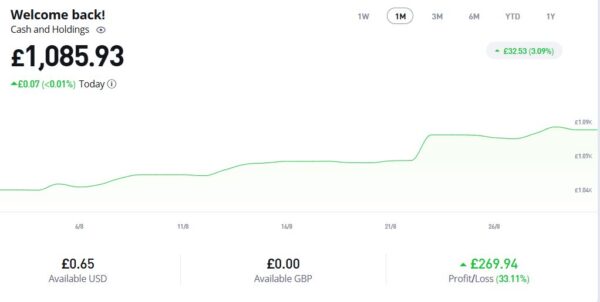

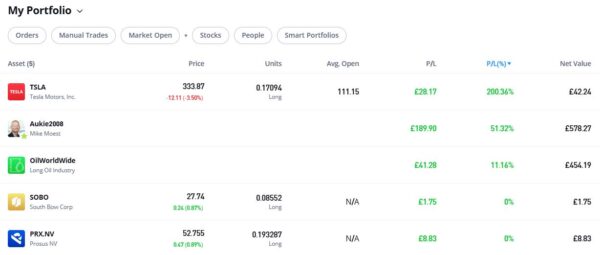

As you can see from the screen captures below, my original investment (total value £888.36 in pounds sterling) is today worth £1,152.75 an overall increase of £264.39 or 29.76%.

Note: eToro now displays the value of investments in your native currency, although you can change this if you wish.

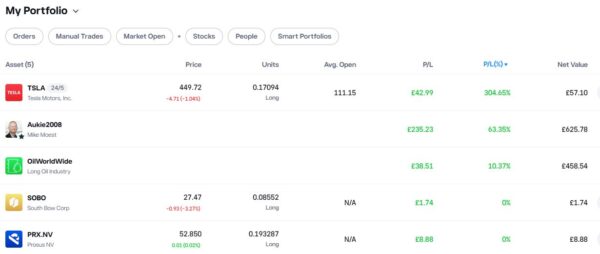

As you can see, my Oil WorldWide investment is in profit, though at 10.37% it is nothing to get excited about. My copy trading investment with Aukie2008 has been doing better, with an impressive overall profit of 63.35%. To be fair, I have held this investment a bit longer.

My Tesla shares, which I bought as an afterthought with some spare cash I had in my account, are up again this month. They are showing an overall profit of 304.65% since I bought them. If only I had put a bit more money into this!

You might also notice that I have small holdings in Prosus NV, a Dutch internet group, and South Bow, a Canadian energy infrastructure company. To be honest I don’t understand how I acquired these, but I assume they are some sort of bonus I was awarded. In any event, I am happy to have them in my portfolio.

If you would like more information about setting up an eToro account, please click on this no-obligation website link [affiliate]. Don’t forget that you also get a free $100,000 virtual portfolio, which you can use to experiment with trading and investing strategies. I have certainly earned a lot from mine.

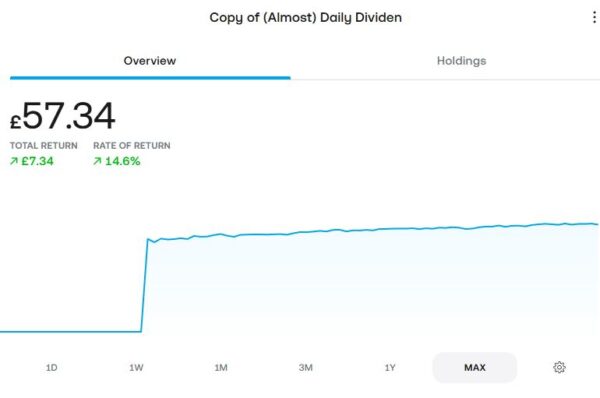

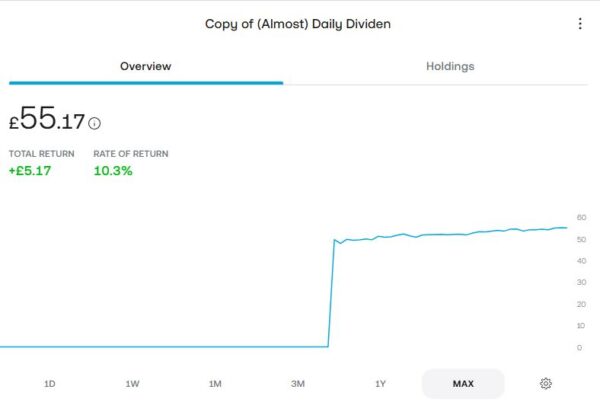

As an experiment, at the start of April this year I put £50 into an investment ISA with Trading 212. As mentioned in my recent blog post about dividend investing, I put it into the (Almost) Daily Dividends Portfolio, a ready-made portfolio or ‘pie’ on Trading 212. As you can see from the screen capture below, my portfolio is now worth £57.34, an increase of £7.34 or 14.60% over the nine-month period. It has even accrued a grand total of 77p in dividends!

I am quite impressed with how this investment has been faring, despite the small amount I put in (which means I may be missing out on some smaller dividends). If I increased my investment I would almost certainly become eligible for more dividends, and even more the longer I remain invested. If I had any spare money at the moment, I would consider doing this. Of course, I do now have an income-focused portfolio with JPM Investing as well (see above).

Moving on, I published various posts on Pounds and Sense in December. I have listed below those that are still relevant.

My Top 20 Posts of 2025 is pretty self-explanatory. In this post I listed the top twenty posts on Pounds and Sense in 2025, based on comments, page-views and social media shares, excluding any that were no longer relevant. I hope you might enjoy revisiting these posts, or seeing them for the first time if you are new to PAS.

In Why You Should Beware of Going ‘All-In’ on Electricity I focused on a topic that has become of increasing concern to me in recent months. Over the past decade, UK households have been encouraged to electrify almost everything. Cars are going electric. Gas boilers are being phased out in favour of electric heat pumps. Even cooking is increasingly moving from gas to electricity. Of course, on paper this all fits with the Government’s drive towards Net Zero. But in this post I addressed a growing issue that doesn’t get discussed nearly enough: What happens if the electricity supply isn’t always there when you need it?

Also in December I published New Trading 212 Offer – Get a Guaranteed £25 Cash. This is a rare opportunity to get a guaranteed £25 cash by opening a new Trading 212 Invest account (it’s different from their usual free share promotion, which is currently closed). My post explains what you have to do to claim this money. The offer ends on 20 January 2026.

I also published another syndicated guest post by Primrose Freestone, Senior Lecturer in Clinical Microbiology at Leicester University. This one is on the subject Can You Wear the Same Socks More Than Once? I published another article by Dr Freestone recently on how often you should wash your bedding, which generated a lot of interest. If you enjoyed that article, hopefully you will like this one as well. Again it contains a lot of eye-opening information, including some tips on when and how you should launder socks.

Finally, in What Are the Best Video Calling Tools for Older People? I discussed the benefits for older folk of using video-calling tools and apps to keep in touch with friends and family. I described a range of options, explaining how they work and whom they might be most suitable for. This article was published with Christmas in mind, but obviously it is relevant at other times of the year as well.

I’ll close with a reminder that you can also follow Pounds and Sense on Facebook or Twitter (or X as we have to call it now). Twitter/X is my number one social media platform and I post regularly there. I share the latest news and information on financial matters, and other things that interest, amuse or concern me. So if you aren’t following my PAS account on Twitter/X, you are definitely missing out!

I am also on the BlueSky social media network under the username poundsandsense.bsky.social. Twitter/X remains my primary social media platform, but I also post details of my latest blog posts, third-party articles and other financial news and resources on BlueSky for those who prefer to follow me there.

As always, if you have any comments or questions, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts on PAS may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media:

If you’ve been thinking about dipping your toes into investing – or you’re just after a quick cash boost at this expensive time of year – there’s a new Trading 212 offer on the table that’s worth checking out.

There is a £25 welcome reward for new UK customers who sign up and complete a few simple steps with Trading 212. Note that this is a limited-time offer that closes on 20 January 2026.

💰 What’s the Offer?

Trading 212 is currently running a limited-time promotion in the UK where new customers can earn a £25 cash reward by:

Signing up for a Trading 212 Invest account using a referral link (like mine below)

Verifying your identity

Depositing funds and ordering a free Trading 212 card

Using the card to make 3 transactions of £5 or more each within 10 days of opening your account

Once those conditions are met, you get £25 in cash credited to your account – and you can use that money however you like!

Here’s a breakdown of what you need to do if you want to take part in this offer:

📌 Step 1: Sign Up Click through my referral link and register for a new Trading 212 Invest account (UK residents only, new users only).

📌 Step 2: Verify Your Account Trading 212 requires standard ID checks (passport, driving licence, address details, etc.). This helps satisfy regulatory “Know Your Customer” requirements.

📌 Step 3: Deposit Funds Add at least £1 to your Trading 212 account – although you may want to deposit a bit more so you can do Step 4 straight away as well.

📌 Step 4: Order & Use Your Card Order the free Trading 212 card and make three transactions of £5 or more – these can be everyday purchases you’d make anyway.

📌 Step 5: Get Your £25 After you meet the criteria, your £25 reward should be credited within a few business days. (You will have to wait 30 days before you can withdraw it.)

💷 What Is the Trading 212 Card?

As part of this offer, you need to order and use the Trading 212 card. So what exactly is it?

The Trading 212 card is a free debit card (physical and virtual) linked directly to your Trading 212 Invest account. It allows you to spend money held in your account just like you would with a normal bank debit card. Here is a quick summary of how it works…

Linked to your Trading 212 balance Any uninvested cash in your Trading 212 account can be used for card payments.

Everyday spending You can use the card in shops, online, and via contactless payments, just like a standard debit card.

No need to invest You don’t have to buy shares or funds to use the card. You can simply deposit money and spend it.

Free to order There’s no charge to order the card, and it’s managed through the Trading 212 app.

UK and overseas use The card can be used abroad, making it handy for travel or online purchases from overseas retailers (although exchange rates and fees can vary, so always check the latest terms).

Even after the bonus is paid, some people choose to keep the card as a secondary spending card, while others simply withdraw their money and stop using it. There’s no obligation to keep spending with it long term.

As always, it’s worth keeping an eye on Trading 212’s terms and conditions, as card features and fees can change over time.

💡 Why This Is a Good Deal

This is a no-brainer for most people because:

You don’t need to invest in stocks and shares to earn the £25 – just make normal card purchases you were planning to do anyway.

The minimum effort required is low: three card payments within 10 days.

You can withdraw the bonus cash after a short delay and spend it or reinvest it however you choose.

🧠 Things to Know

Offers like this can end or change at any time – so if you are interested, it’s worth acting sooner rather than later.

This is different from Trading 212’s free share promotion, which exists separately and offers up to £100 in free shares for new users. I discussed this offer in a separate blog post. Note that the Trading 212 free share offer is not available at the time of writing and I don’t know when (or if) it will return.

You must use a referral link to qualify for the £25 bonus.

You must also open an Invest account to qualify. A Stocks ISA, Cash ISA or CFD account won’t work (though you can open any of these subsequently).

📌 Final Thoughts

If you’ve been on the fence about trying out a stock trading or investment app, this £25 welcome reward from Trading 212 is a genuinely easy way to benefit from signing up. It doesn’t require any complicated investing – you can simply earn the bonus and decide what comes next. Just be sure to follow the steps above carefully and meet all the qualifying requirements.

And don’t forget that this limited-time offer closes on 20 January 2026.

As always, if you have any comments or questions about this post, please do leave them below.

Disclosure: If you take up this offer via my referral link, I will also receive a cash bonus for introducing you. The £25 cash bonus is guaranteed if you follow the steps set out above. If you choose to reinvest this money, however, be aware that – as with all investing – there is a risk of loss if you put the money into equities (stocks and shares). You should always do your own “due diligence” before investing and seek advice from a qualified financial planner/adviser if in any doubt how best to proceed.

If you enjoyed this post, please link to it on your own blog or social media:

As is customary for bloggers at this time of year, here are the top twenty posts on Pounds and Sense in 2025, based on comments, page-views and social media shares. They are in no particular order. I have excluded any posts that are no longer relevant.

I hope you will enjoy revisiting these posts, or seeing them for the first time if you are new to PAS.

All posts in the list below should open in a new tab/window when you click on the link concerned.

I’ll be taking a break from blogging over the festive period (though I’ll still be around on X/Twitter and Facebook). I’ll therefore close by wishing you a Very Merry Christmas (strikes and cost-of-living crisis permitting) and for all of us a brighter, more prosperous new year

If you have any comments or questions, of course, feel free to leave them below as usual.

If you enjoyed this post, please link to it on your own blog or social media:

I’ll begin as usual with my JP Morgan Personal Investing (previously Nutmeg) Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

As regular readers will know, in June this year I transferred most of the money in my former Nutmeg Fully Managed portfolio (just under £25,000) to a new Nutmeg Income Portfolio. I discussed this in detail in this post, but basically money in this port is invested to generate an income from share dividends and other sources. This is then paid monthly. Capital appreciation is targeted as well, but these portfolios are aimed primarily at older people (and others) who want/need their investment to generate a regular cash income.

In November my JPM Investing income portfolio generated £119.59 of income, which was duly paid in to my bank account on 24 November 2025. That was around double the £63.96 I received in October and means I have now received a total (tax-free) income of £396.30 to date. That’s about what I would have hoped for based on JPM’s projected annual return of just under 5% for income ports at my chosen risk level (five).

My income portfolio grew in value again in November. It’s now worth £27,015 compared with £26,837 at the start of last month, a rise of £178. As the screen capture shows, the port has actually increased by £2,063.04 (8.27%) since I opened it in June this year. That’s clearly good going, though I don’t suppose it will carry on like this indefinitely. (I should maybe also mention that performance may have been helped a bit by the no-fees introductory offer on Nutmeg/JPM income portfolios until the end of 2025.)

I still have a smaller, growth-oriented pot using JPM Investing’s Smart Alpha option. This is now worth £4,685 compared with £4,694 a month ago, a small decrease of £9. Here is a screen capture showing performance for the year to date.

Smart Alpha portfolio Dec 2025

And at the start of December 2023 I invested £500 in one of Nutmeg/JPM’s thematic portfolios (Resource Transformation). In March 2024 I also invested a further £200 from referral bonuses (something I no longer receive for reasons I won’t bore you with). As you can see from the YTD screen capture below, this portfolio is now worth £931 (rounded up) compared with £932 last month, a small decrease of £1.

Finally, I still have a small amount left in my original Nutmeg/JPM Fully Managed portfolio. I have kept this largely for comparison purposes. This has also decreased slightly in value from £639 at the start of November to £637 (rounded up) now, a fall of £2.

Overall in November I was up by £166 or 0.49%. In addition I did, of course, receive £119.59 in income from my income portfolio. The latter was obviously my star performer in November and ensured that I made an overall profit for the month.

Excluding income generated, the overall value of my JPM investments is up by £2,839 or 9.33% since the start of 2025, so the April 2025 fall (caused largely by Trump’s tariffs) has now fully reversed. If you add to this figure the £396.30 of income generated so far this year, that gives a total profit of £3,235.30 – not a bad return in these uncertain times.

As I always have to say, some volatility is to be expected with stock market investments, but over the longer term they tend to even themselves out (and generally perform better than bank savings accounts, although that is never guaranteed). In general the worst thing you can do is panic and sell up when downturns occur (as happened in April this year). You are then crystallizing your losses rather than giving the markets time to recover. This is something I had cause to discuss in this blog post from earlier this year.

You can read my full original Nutmeg/JPM review here. If you are looking for a home for your annual ISA allowance, based on my overall experience over the last nine years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs), Lifetime ISAs and Junior ISAs as well.

As mentioned above, Nutmeg have rebranded as J.P. Morgan Personal Investing and their website is now at www.personalinvesting.jpmorgan.com.

Moving on, I also have investments with P2P property investment platform Assetz Exchange. As discussed in this post, the company has rebranded as Housemartin.

My investments with Housemartin continue to generate steady returns. Housemartin focuses on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my HM portfolio has generated a respectable £285.00 in revenue from rental income. I have made a small net loss of £21.68 on property disposals. Capital growth generally has slowed, in line with UK property values generally.

At the time of writing, 16 of ‘my’ properties are showing gains, 4 are breaking even, and the remaining 21 are showing losses. My portfolio of 41 properties is currently showing a net decrease in value of £54.99. That means that overall (rental income minus capital value decrease and loss on disposal) I am up by £208.33. That’s still a respectable return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Housemartin most projects are socially beneficial as well.

The net fall in capital value of my Housemartin investments is obviously a little disappointing. But it’s important to remember that until/unless I choose to sell the investments in question, it is largely theoretical, based on the latest price at which shares in the property concerned have changed hands. The rental income, on the other hand, is real money (which in my case I’ve reinvested in other HM projects to further diversify my portfolio).

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of Housemartin as far as i am concerned. You can actually invest from as little as £1 per property if you really want to proceed cautiously.

As I noted in this blog post, Housemartin is particularly good if you want to compound your returns by reinvesting rental income. This effectively boosts the interest rate you are receiving. Personally, once I have accrued a minimum of £10 in rental payments, I usually reinvest this money in either a new HM project or one I have already invested in (thus increasing my holding). Over time, even if I don’t invest any more capital, this will ensure my investment with Housemartin grows at an accelerating rate and becomes more diversified as well.

In 2022 I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios, Oil Worldwide. I also invested a small amount I had left over in Tesla shares.

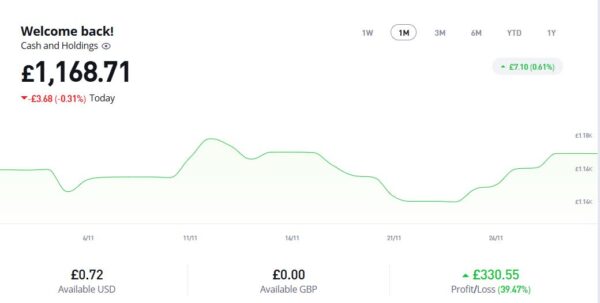

As you can see from the screen captures below, my original investment (total value £888.36 in pounds sterling) is today worth £1,168.71 an overall increase of £280.35 or 31.56%.

Note: eToro now displays the value of investments in your native currency, although you can change this if you wish.

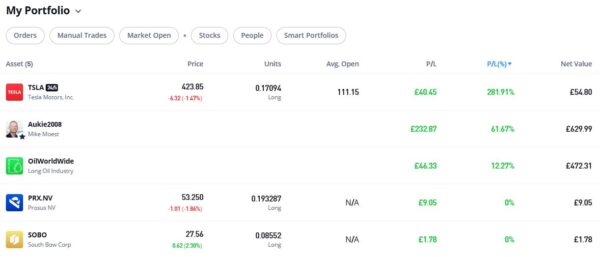

As you can see, my Oil WorldWide investment is in profit, though at 12.27% it is nothing to get too excited about. My copy trading investment with Aukie2008 has been doing better, with an impressive overall profit of 61.67%. To be fair, I have held this investment a bit longer.

My Tesla shares, which I bought as an afterthought with some spare cash I had in my account, are down a little this month but still showing an overall profit of 281.91% since I bought them. If only I had put a bit more money into this!

You might also notice that I have small holdings in Prosus NV, a Dutch internet group, and South Bow, a Canadian energy infrastructure company. To be honest I don’t understand how I acquired these, but I assume they are some sort of bonus I was awarded. In any event, I am happy to have them in my portfolio.

If you would like more information about setting up an eToro account, please click on this no-obligation website link [affiliate]. Don’t forget that you also get a free $100,000 virtual portfolio, which you can use to experiment with trading and investing strategies. I have certainly earned a lot from mine.

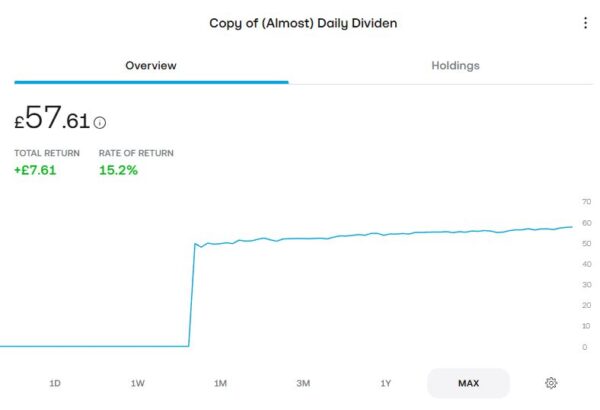

As an experiment, at the start of April this year I put £50 into an investment ISA with Trading 212. As mentioned in my recent blog post about dividend investing, I put it into the (Almost) Daily Dividends Portfolio, a ready-made portfolio or ‘pie’ on Trading 212. As you can see from the screen capture below, my portfolio is now worth £57.61, an increase of £7.61 or 15.20% over the eight-month period. It has even accrued a grand total of 67p in dividends!

I am quite impressed with how this investment has been faring, despite the small amount I put in (which means I may be missing out on some smaller dividends). If I increased my investment I would almost certainly become eligible for more dividends, and even more the longer I remain invested. If I had any spare money at the moment, I would consider doing this. Of course, I do now have an income-focused portfolio with JPM Investing as well (see above).

Moving on, I published various posts on Pounds and Sense in November. I have listed below those that are still relevant.

In What Are Money Market Funds and Who Should Invest in Them? I discussed what money market funds (MMFs) are and why they are seeing a surge in interest from UK investors at the moment. I examined their pros and cons and revealed how they may be a valuable addition to your investment portfolio, especially in light of Rachel Reeves’ recent Budget.

In Should You Take a Tax-Free Lump Sum From Your Pension Now? I addressed a question many people were asking in view of rumours that the Chancellor might be about to tighten the rules. As it happens no changes were made in the Budget regarding the tax-free lump sum. The article is still relevant, though, as it sets out the pros and cons of accessing this money early, and when doing so might (or might not) be a good idea.

The popular Trading 212 Free Share Offer reopened in November, so in Get a Free Share Worth Up to £100 With Trading 212 I explained how the offer works and how (If you haven’t done it before) you can take advantage of it. You will need to get your skates on with this, as the offer closes on Tuesday 3 December.

Why Growing Numbers of Over-50s are Buying Park Homes discusses the growing popularity of park homes among older people. The article explains the crucial differences between park homes and holiday homes, and sets out some reasons more and more older people are opting to go down this route. This article was written in association with my friends at Compass Insurance, who are leading specialist providers of park home insurance.

Finally, in Twelve Great Christmas Gift Ideas for Older People (That Aren’t Socks) I set out twelve varied ideas for Christmas presents for your older friends and relatives – based on my personal experience as an older person, of course! Older folk are traditionally harder to buy gifts for – so if you’re struggling with this, hopefully you may find some inspiration here 🙂

One other thing I wanted to mention this month is that currently EDF Energy are offering an enhanced switching bonus. Until 22 December 2025 you can get a hefty £75 (usually £50) credited to your energy account if you switch your supply to them via my link at https://edfenergy.com/quote/refer-a-friend/sunny-koala-9462. I will get a bonus too, so it really is win-win all round!

Additionally, if you’re already an EDF customer (or sign up now) you can enter a free prize draw to win a holiday in the UK with £700 prize money! Enter at https://www.edfenergy.com/edfstaycations. The closing date for this is 11 December 2025 – but if you switch to EDF Energy now, you still have time to enter.

I’ll close with a reminder that you can also follow Pounds and Sense on Facebook or Twitter (or X as we have to call it now). Twitter/X is my number one social media platform and I post regularly there. I share the latest news and information on financial matters, and other things that interest, amuse or concern me. So if you aren’t following my PAS account on Twitter/X, you are definitely missing out!

I am also on the BlueSky social media network under the username poundsandsense.bsky.social. Twitter/X remains my primary social media platform, but I also post details of my latest blog posts, third-party articles and other financial news and resources on BlueSky for those who prefer to follow me there.

As always, if you have any comments or questions, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts on PAS may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media:

According to various sources (here, for example) money market funds or MMFs are seeing a surge of interest from UK investors at the moment.

So today I thought I’d explain what MMFs are, their pros and cons, and who should (and perhaps shouldn’t) invest in them. I will also examine some likely reasons for the high level of interest in MMFs just now.

Let’s start with the most basic question, though…

What Are Money Market Funds?

A money market fund is a type of investment fund that invests in short-term, high-quality, liquid debt instruments — such as government treasury bills, bank certificates of deposit, commercial paper and other instruments with very short maturities. In the UK context, many asset managers describe them as a “park your cash” vehicle: not quite a deposit account, but relatively low risk compared to equities or longer-dated bonds.

Because the underlying assets mature quickly (many in weeks or a few months) the fund manager can reasonably anticipate the yield and maintain high liquidity.

In simple terms, you could think of a money market fund as somewhere between “keeping money in a bank account” and “investing for growth in the stock market” — it aims for capital preservation + modest income, rather than big capital gains.

Pros of money market funds

If you’re considering an MMF, here are some of the advantages that frequently show up in analyses:

Lower risk (relatively) Because the underlying holdings are short-dated and usually high credit quality, money market funds tend to carry lower risk than many other types of investment funds. For example, compared to longer-term bond funds or equities, there’s far less exposure to interest-rate/inflation risk and less time for issuers to go horribly wrong.

High liquidity Many funds allow you to redeem on a daily dealing basis (or very frequently) so you can access your money relatively quickly. This makes them useful as a “waiting place” for money or for short-term needs.

Potentially higher return than pure cash savings Especially in a higher interest-rate environment, the yields on money market funds can exceed those of some bank savings accounts or easy-access deposits — for investors willing to accept the (small) additional risk.

Diversification of cash holdings If you keep large sums of cash at one bank, you may be exposed to that institution; a money market fund spreads the credit risk across many issuers.

Use within tax-efficient wrappers In the UK, you can hold money market funds inside a Stocks and Shares ISA or SIPP, which may be advantageous rather than leaving all your money in a conventional cash account.

Cons of money market funds

As always, “lower-risk” doesn’t mean “no risk”, and there are some important drawbacks to bear in mind…

Capital is not guaranteed Unlike deposit accounts covered by the UK’s Financial Services Compensation Scheme (FSCS) (up to £85,000 per institution), investments in money market funds are subject to investment risk. You could get back less than you invested.

Return may not beat inflation Because the returns are modest (given the conservative nature of the underlying assets), there is a risk that inflation will erode the real value of your money over time. In other words: you may earn income, but your purchasing power may still decline.

Interest-rate/yield sensitivity The yield of a money market fund is influenced by short-term interest rates. If interest rates fall, the yield on the fund may drop. If the market is unsettled (or credit spreads widen) the value can move.

Liquidity risk in extreme scenarios While these funds are normally very liquid, in times of market stress there is still a risk of redemption delays, or assets becoming harder to value. Some regulators have highlighted this as a risk.

Limited capital growth potential These funds are designed for preservation and modest income, not high growth. If your goal is expanding your wealth significantly over many years, other assets (equities, long-term bonds, etc.) may suit you better.

Who Should Invest in MMFs?

Here are some scenarios where a money market fund may be a good fit:

If you have short-term needs (e.g. you expect to spend the money within the next 1 to 3 years) and want to avoid exposing it to the ups and downs of equities.

If you’re deciding what to do with funds (e.g. waiting for an investment opportunity) and need a place to park cash that offers a little bit more than a basic savings account, while keeping reasonable access.

If you hold a large sum of cash in an ISA or pension wrapper and you want it to “work a little harder” than a pure deposit, but without taking large risks.

If you have low risk-tolerance and want the bulk of your capital in safer, more liquid form — while still preserving flexibility.

Who Shouldn’t Invest In MMFs (or maybe think twice)?

On the flip side, money market funds may not be appropriate if:

Your investment horizon is long-term (say 5-10+ years) and you’re seeking substantial growth. The conservative nature of money market funds means they are unlikely to match the returns of equity or balanced portfolios over the long term.

You are relying on the investment to outpace inflation significantly. If inflation is high, the modest returns may mean your real-terms wealth declines.

You need instant access or expect frequent withdrawals. While liquidity is good relative to many investments, it is not always instant and sometimes there may be daily dealing only. Check the individual fund terms.

You misunderstand the risk: if you assume it’s the same as a deposit account (with full guarantee), you may be unpleasantly surprised. While risk is lower than many funds, it is not zero.

Examples of Popular UK MMFs

To illustrate what’s out there in the UK market, here are a few examples of well-known money market (or “cash/money-market”) funds. Note: this is for information only and not a product recommendation.

Royal London Short Term Money Market Fund — This fund is often cited as a top choice in the UK short-term money market fund category, with a low ongoing charge and yield of ~4–5% in recent years.

Vanguard Sterling Short‑Term Money Market Fund — Vanguard’s UK money market offering, described as “a low-risk place to park your money” by the provider.

abrdn Sterling Money Market Fund — Another UK-available fund in the segment, targeting short-term money market instruments and relatively modest returns.

When choosing a fund, you’ll want to consider: the fund’s objective, charges (ongoing management charge/OCF), dealing terms (how quickly you can withdraw), liquidity provisions, and whether the yield is appropriate for the risk.

Why Is Interest in MMFs High Right Now?

There are various reasons for this. A major one is a degree of caution among investors at present. Equities and long-duration bonds have had episodes of volatility, inflation remains a concern, and with rising rates the risk of capital losses in interest-sensitive assets is higher. In that context, MMFs — with their short-duration holdings and relatively low volatility — look like a safer option to hold cash or near-cash assets.

Also, with central banks (including the Bank of England) keeping base rates elevated, the returns available from short-term debt and cash-like instruments have increased. For example, one provider (Fidelity) notes that MMFs “made a comeback in 2023 and have remained popular ever since — thanks largely to interest rates remaining higher for longer than expected.”

Because MMFs can be held inside ISAs or pensions, they benefit from the same tax-efficient wrappers as other investment funds. For investors who already use their ISA or SIPP allowance, being able to park cash inside that wrapper via an MMF may be an attractive alternative to leaving it outside the wrapper in a separate (perhaps taxed) savings account.

And finally, many investors have cash allocations in their portfolios (for future investment or awaiting opportunity) or hold money inside tax-efficient wrappers as mentioned above, but may not want to leave it entirely in a low-interest bank account. MMFs provide a way to hold cash within an investment platform, maintain liquidity, and potentially earn slightly more than a basic savings account. For example, AJ Bell notes that one of the appeals is that an investor can hold the MMF inside their S&S ISA or pension without transferring it out to a separate cash savings account.

UPDATE: An additional attraction of MMFs has arisen due to the decision by Chancellor Rachel Reeves in her November 2025 Budget to reduce the annual Cash ISA allowance to £12,000 (with an exception for over-65s). If you would previously have put the full £20,000 into a Cash ISA, you could now put all that money into an MMF within a Stocks and Shares ISA instead. Alternatively you could put the maximum £12,000 into a Cash ISA and the remaining £8,000 into a MMF within a S&S ISA.

Key Takeaways

Money market funds can be a useful tool for parking money (relatively) safely, earning a bit more than a basic savings account, and maintaining liquidity.

They are not risk-free: capital is at risk, and returns may not keep pace with inflation.

They are most useful for short- to medium-term horizons, or as part of a diversified portfolio where some portion of assets is kept in safer, liquid form.

If you’re investing for the long term with a view to growth, you’ll likely need to supplement (or allocate differently) rather than relying solely on MMFs.

You can invest in MMFs directly or via a platform such as AJ Bell or Hargreaves Lansdown.

You can invest within a tax-free wrapper such as a SIPP or S&S ISA, or in a general investment account without tax-free status if you’ve used up your annual £20,000 ISA allowance.

Always read the fund’s Key Investor Information Document (KIID) or factsheet, check charges, underlying holdings and suitability for your goals and time horizon.

Comparison Chart: MMFs vs Bank Deposits vs Cash ISAs

Product type

Typical recent yield / rate*

Key features / caveats

Money Market Funds (UK)

Around ~3.9%-4.3% p.a. (e.g. Premier Miton UK Money Market Class B shows an underlying yield ~3.98%.

Variable yield; invested in short-dated instruments; not guaranteed like a deposit; liquidity good but subject to fund terms. May be held within a tax-free wrapper such as a SIPP or ISA.

UK bank deposits / savings accounts

For easy‐access/variable savings: up to ~4.20% or so.

Usually FSCS-protected up to £85,000; rates may change; access may be immediate or with notice depending on account.

Cash ISAs (UK)

Top easy‐access Cash ISAs: ~4.52% AER or thereabouts.

Tax-free interest; also FSCS-protected as with deposits; you must use your annual ISA allowance (£20,000 in 2025/26) for it to count as an ISA; yield may be variable or fixed term.

*Yields/interest shown are approximate at the time of writing and subject to change.

As the chart shows, if you’re looking for a place to “park” money in the UK, you’re getting broadly similar yields whether you go for a bank savings account, a cash ISA or a money market fund. The differences come down to tax treatment, level of guarantee/risk, which wrapper you use, and ease of access.

For example, a cash ISA is tax-free, which can boost your effective return if you’re a higher rate taxpayer. A bank deposit may offer the FSCS safety net. A money market fund may allow you to invest via your ISA or pension wrapper and keep your cash within your investment portfolio structure, but you must accept that capital preservation isn’t guaranteed.

If you value the FSCS protection and are comfortable with a savings account structure, a bank deposit or savings account/cash ISA might be your preference. If you already have your deposit needs covered and you’re simply looking for a place inside your investment wrapper to hold cash-like assets, a money market fund may fit the bill.

It’s also important to ascertain whether the quoted rate is fixed or variable, check any withdrawal penalties, and consider whether the returns will keep pace with inflation.

As always, if you have any comments or questions about this post, please do leave them below. Bear in mind that I am not a qualified financial adviser and nothing in this article should be construed as personal financial advice. You should always do your own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

If you enjoyed this post, please link to it on your own blog or social media:

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

As regular readers will know, in June this year I transferred most of the money in my Nutmeg Fully Managed portfolio (just under £25,000) to a new Nutmeg Income Portfolio. I discussed this in detail in this recent post, but basically money in this port is invested to generate an income from share dividends and other sources. This is then paid monthly. Capital appreciation is targeted as well, but these portfolios are aimed primarily at older people (and others) who want/need their investment to generate a regular cash income.

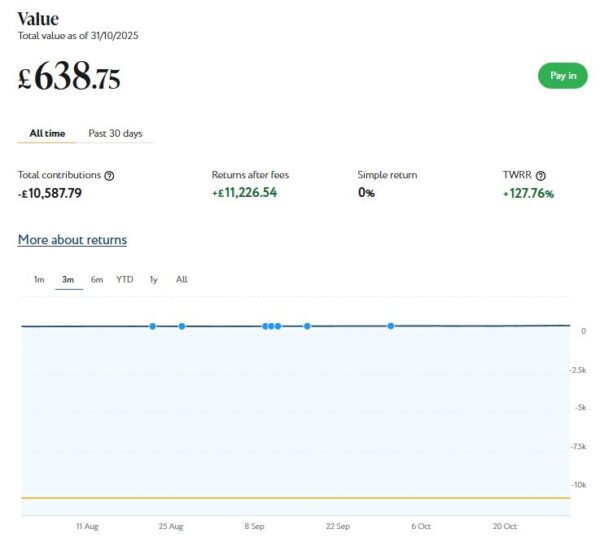

In October my Nutmeg income portfolio generated £64.60 of income, which was duly paid in to my bank account on 24 October 2025. That is down a bit on the £78.20 I received in September, but it means I have now received a total (tax-free) income of £276.83 to date. That’s a bit less than I would have hoped for based on Nutmeg’s projected annual return of just under 5% for income ports at my chosen risk level (five). It’s still too early to draw any significant conclusions from this, though.

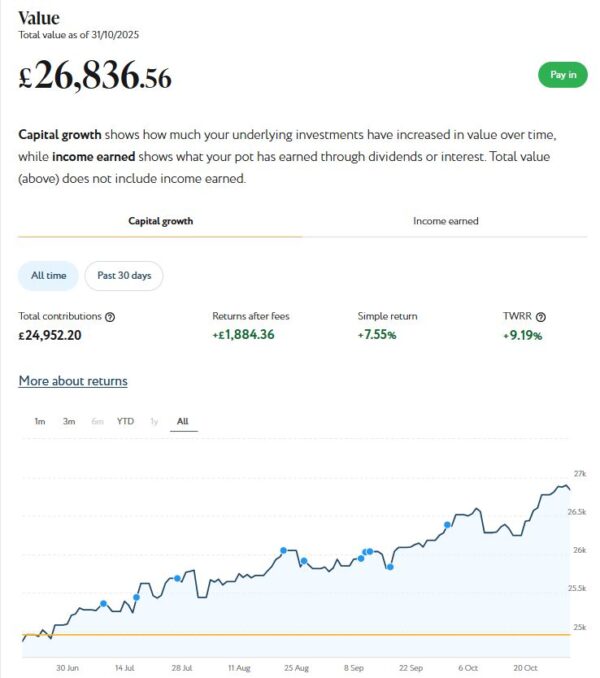

My income portfolio grew in value again in October. It’s now worth £26,837 (rounded up) compared with £26,383 at the start of last month, a rise of £454. As the screen capture shows, the port has actually increased by £1,844.36 (7.55%) since I opened it in June this year. That’s clearly good going, though I don’t suppose it will carry on like this indefinitely!

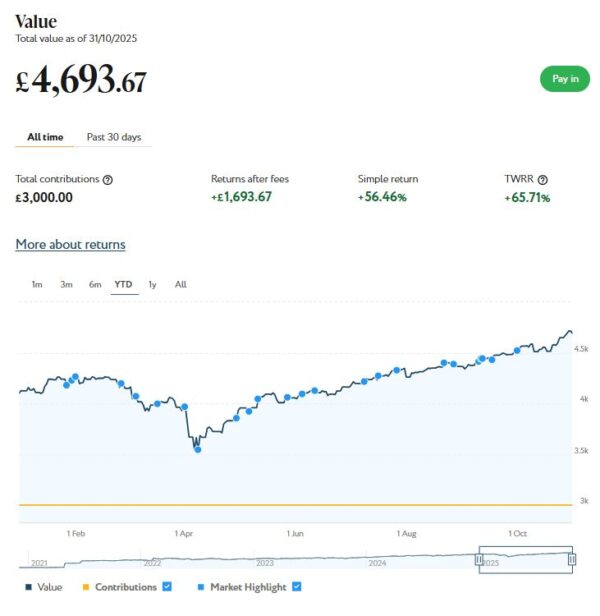

I still have a smaller, growth-oriented pot using Nutmeg’s Smart Alpha option. This is now worth £4,694 (rounded up) compared with £4,524 a month ago, a rise of £170. Here is a screen capture showing performance for the year to date.

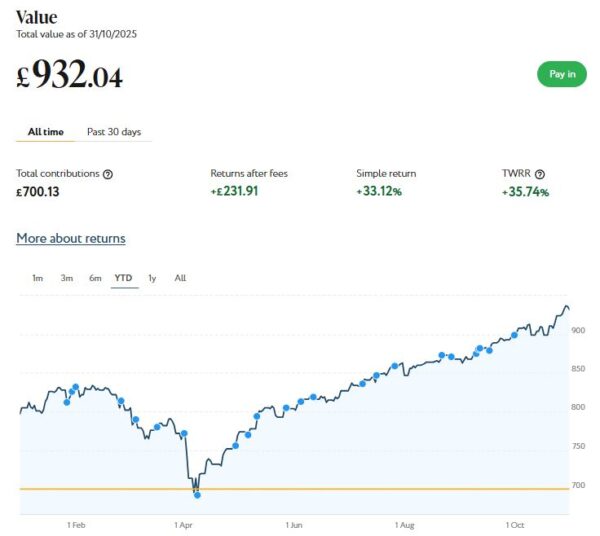

And at the start of December 2023 I invested £500 in one of Nutmeg’s thematic portfolios (Resource Transformation). In March 2024 I also invested a further £200 from referral bonuses (something I no longer receive for reasons I won’t bore you with). As you can see from the YTD screen capture below, this portfolio is now worth £932 compared with £900 last month, a rise of £32.

Finally, I still have a small amount left in my original Nutmeg Fully Managed portfolio. I have kept this largely for comparison purposes. This has increased in value from £617 at the start of October to £639 (rounded up) now, a rise of £22.

As you can see, October was another good month for my Nutmeg investments. Overall I was up by £678 or 2.46%. In addition I did, of course, receive £64.60 in income from my income portfolio.

Excluding income generated, the overall value of my Nutmeg investments is up by £2,673 since the start of 2025, so the April 2025 fall (caused largely by Trump’s tariffs) has now fully reversed. I am also up by £3,526 or 11.92% since the start of November last year, again excluding cash income received. All things considered, that’s not a bad result.

As I always have to say, some volatility is to be expected with stock market investments, but over the longer term they tend to even themselves out (and generally perform better than bank savings accounts, although that is never guaranteed). In general the worst thing you can do is panic and sell up when downturns occur (as happened in April this year). You are then crystallizing your losses rather than giving the markets time to recover. This is something I had cause to discuss in this blog post from earlier this year.

You can read my full Nutmeg review here. If you are looking for a home for your annual ISA allowance, based on my overall experience over the last nine years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs), Lifetime ISAs and Junior ISAs as well.

Note that Nutmeg are rebranding as J.P. Morgan Personal Investing and their website will be at www.personalinvesting.jpmorgan.com from this week onward.

Moving on, I also have investments with P2P property investment platform Assetz Exchange. As discussed in this post, the company has rebranded as Housemartin.

My investments with Housemartin continue to generate steady returns. Housemartin focuses on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my HM portfolio has generated a respectable £279.58 in revenue from rental income. I have made a small net loss of £19.02 on property disposals. Capital growth generally has slowed, in line with UK property values generally.

At the time of writing, 14 of ‘my’ properties are showing gains, 4 are breaking even, and the remaining 22 are showing losses. My portfolio of 40 properties is currently showing a net decrease in value of £54.00. That means that overall (rental income minus capital value decrease and loss on disposal) I am up by £206.56. That’s still a respectable return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Housemartin most projects are socially beneficial as well.

The net fall in capital value of my Housemartin investments is obviously a little disappointing. But it’s important to remember that until/unless I choose to sell the investments in question, it is largely theoretical, based on the latest price at which shares in the property concerned have changed hands. The rental income, on the other hand, is real money (which in my case I’ve reinvested in other HM projects to further diversify my portfolio).

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of Housemartin as far as i am concerned. You can actually invest from as little as £1 per property if you really want to proceed cautiously.

As I noted in this blog post, Housemartin is particularly good if you want to compound your returns by reinvesting rental income. This effectively boosts the interest rate you are receiving. Personally, once I have accrued a minimum of £10 in rental payments, I usually reinvest this money in either a new HM project or one I have already invested in (thus increasing my holding). Over time, even if I don’t invest any more capital, this will ensure my investment with Housemartin grows at an accelerating rate and becomes more diversified as well.

In 2022 I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios, Oil Worldwide. I also invested a small amount I had left over in Tesla shares.

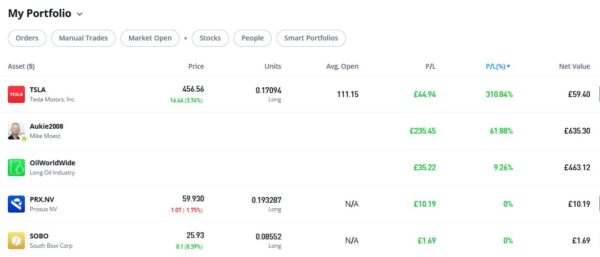

As you can see from the screen captures below, my original investment (total value £888.36 in pounds sterling) is today worth £1,170.40 an overall increase of £282.04 or 31.75%.

Note: eToro now displays the value of investments in your native currency, although you can change this if you wish.

As you can see, my Oil WorldWide investment is in profit, though at 9.26% it is nothing to write home about. My copy trading investment with Aukie2008 has been doing better, with an impressive overall profit of 61.88%. To be fair, I have held this investment a bit longer.

My Tesla shares, which I bought as an afterthought with some spare cash I had in my account, are up again this month. They are showing an overall profit of 310.84% since I bought them. If only I had put a bit more money into this!

You might also notice that I have small holdings in Prosus NV, a Dutch internet group, and South Bow, a Canadian energy infrastructure company. To be honest I don’t understand how I acquired these, but I assume they are some sort of bonus I was awarded. In any event, I am happy to have them in my portfolio.

eToro also offer the free eToro Money app. This allows you to deposit money to your eToro account without paying any currency conversion fees, saving you up to £5 for every £1,000 you deposit. You can also use the app to withdraw funds from your eToro account instantly to your bank account. I tried this myself and was impressed with how quickly and seamlessly it worked. You can read my blog post about eToro Money here. Note that it can also serve as a cryptocurrency wallet, allowing you to send and receive crypto from any other wallet address in the world.

If you would like more information about setting up an eToro account, please click on this no-obligation website link [affiliate]. Don’t forget that you also get a free $100,000 virtual portfolio, which you can use to experiment with trading and investing strategies. I have certainly earned a lot from mine.

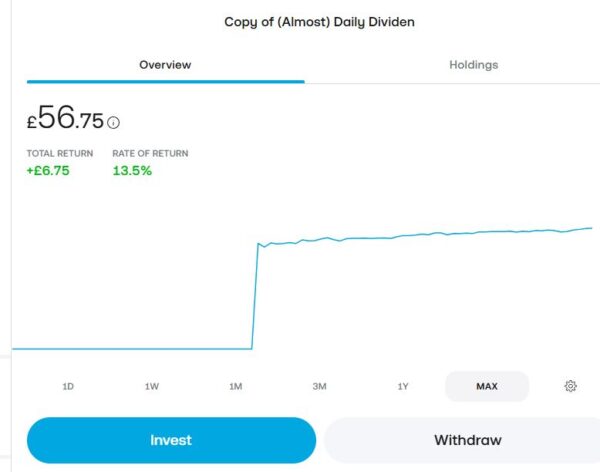

As an experiment, at the start of April this year I put £50 into an investment ISA with Trading 212. As mentioned in my recent blog post about dividend investing, I put it into the (Almost) Daily Dividends Portfolio, a ready-made portfolio or ‘pie’ on Trading 212. As you can see from the screen capture below, my portfolio is now worth £56.75, an increase of £6.75 or 13.5% over the seven-month period. It has even accrued a grand total of 59p in dividends!

I am quite impressed with how this investment has been faring, despite the small amount I put in (which means I may be missing out on some smaller dividends). If I increased my investment I would almost certainly become eligible for more dividends, and even more the longer I remain invested. If I had any spare money at the moment, I would consider doing this. Of course, I do now have an income-focused portfolio with Nutmeg as well (see above).

Moving on, I published various posts on Pounds and Sense in October. I have listed below those that are still relevant.

In Annuity or Drawdown? Weighing Up Your Pension Income Options After 50 I discussed an issue relevant to many PAS readers (and me personally). If – like most of us nowadays – you have a defined-contribution (aka money-purchase) pension, what is the best way to convert this into an income when the time comes? In this article I set out the pros and cons of the two main methods.

How to Save Money on Your Heating Bills This Winter covers a topic many of us are worried about right now. With energy bills soaring, what methods are available to us to save money on our heating and energy bills? Following these tips could save you hundreds of pounds in the months and years ahead.

In Winter Fuel Payment 2025/26 – What Pensioners Need to Know I explained how the rules regarding Winter Fuel Payment have changed this year. The good news is that WFP has been reinstated for most pensioners in 2025/26, but with one major caveat. Read the article for a full explanation of how things now stand and what – if anything – you need to do.

Finally, in How to Prepare for Winter Blackouts I revealed why power cuts are becoming increasingly probable in the UK and what steps you can take to prepare for them. While the prospect of winter blackouts may be daunting, thorough preparation should alleviate many of the challenges. By taking steps now, you can ensure the safety and comfort of your household, no matter what the winter months bring.

I’ll close with a reminder that you can also follow Pounds and Sense on Facebook or Twitter (or X as we have to call it now). Twitter/X is my number one social media platform and I post regularly there. I share the latest news and information on financial matters, and other things that interest, amuse or concern me. So if you aren’t following my PAS account on Twitter/X, you are definitely missing out!

I am also on the BlueSky social media network under the username poundsandsense.bsky.social. Twitter/X remains my primary social media platform, but I also post details of my latest blog posts, third-party articles and other financial news and resources on BlueSky for those who prefer to follow me there.

As always, if you have any comments or questions, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts on PAS may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media:

As you approach retirement, one of the biggest financial decisions you’ll face is how to turn your pension savings into a reliable income.

Two of the main options are buying an annuity or using a pension drawdown strategy. Both approaches have pros and cons, and which is right for you will depend on your circumstances, priorities and attitude to risk.

It’s also worth noting that annuity rates are currently more generous than they have been for many years, thanks largely to higher interest rates. That makes annuities a more attractive choice today than they might have seemed just a year or two ago.

What is an Annuity?

An annuity is a financial product you buy with some or all of your pension savings. In return, the provider guarantees to pay you an income for life (or for a fixed period). The amount depends on your age, health and the options you choose, e.g. whether payments continue to a spouse after your death.

You may also opt for payments to be fixed or rise in line with inflation. The latter will reduce the amount you receive initially but may be beneficial in the longer term.

For a ballpark estimate of how much income an annuity may generate for you, check out this free calculator. It will give you a rough figure based on your age and the size of your pension pot.

What is Drawdown?

With drawdown (also called flexi-access drawdown), your pension savings remain invested and you take money out as needed. You have control over how much you withdraw and when. This is the method I am using to generate an income currently from my Bestinvest SIPP.

Annuity vs Drawdown: Comparison Table

Here’s how the two main ways to turn your pension savings into income compare at a glance:

Feature

Annuity

Pension Drawdown

Income security

Guaranteed for life (or fixed term)

Depends on investment performance and withdrawals

Flexibility

Fixed once set up – limited changes allowed

Very flexible – you choose how much and when to withdraw

Potential for growth

None (income is fixed)

Pension pot remains invested and can grow

Risk level

Very low (no investment risk)

Higher (subject to market fluctuations)

Inheritance potential

Usually none unless special options chosen

Remaining funds can usually be passed to beneficiaries

Inflation protection

Optional – inflation-linked annuities start lower

Depends on investment returns and withdrawal strategy

Health impact

Poor health can mean higher income via “enhanced” rates

Health does not affect drawdown income directly

Ongoing management

None once purchased

Requires regular monitoring and possible financial advice

Best suited for

Those wanting guaranteed, worry-free income

Those comfortable with risk and wanting flexibility

Current appeal

Rates are now at their best for years due to higher interest rates

Still popular for flexibility, but requires careful planning

Which Option is Right for You?

If you value certainty and peace of mind, an annuity (especially with today’s higher rates) may be appealing.

If you want flexibility, growth potential, and the ability to leave an inheritance, drawdown could be the better fit.

Many people now choose a blend of the two – using part of their pot to buy an annuity for essential expenses, and keeping the rest in drawdown for flexibility and growth.

You Don’t Have to Decide All at Once

It’s important to remember that this isn’t necessarily an “either/or” decision. Many people begin their retirement with pension drawdown, giving them flexibility in the early years when spending needs can vary. Later on, when they want more security and less investment risk, they can choose to convert some or all of their remaining funds into an annuity. This phased approach offers the best of both worlds — flexibility when you’re active and security later in life.

And other things being equal, the older you are when you take out an annuity, the more generous the terms you are likely to get.

Final Thoughts

There’s no “one size fits all” answer. Your choice will depend on factors such as your health, whether you have other sources of income, your attitude to risk, and how important leaving an inheritance is to you.

With annuity rates at their most attractive in years, now could be a good time to revisit them as part of your retirement planning. But drawdown remains a strong option for those seeking control and flexibility and the potential for growth.

Before making any decisions, it’s wise to get independent financial advice to ensure you choose the strategy – or mix of strategies – that best fits your goals.

Disclosure: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. I highly recommend taking professional advice about your pension options before committing yourself to a particular course of action. This article lists a number of reputable advisory platforms and services for pension advice. Bear in mind that all investing carries a degree of risk.

If you enjoyed this post, please link to it on your own blog or social media:

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

As regular readers will know, in June I transferred most of the money in my Nutmeg Fully Managed portfolio (just under £25,000) to a new Nutmeg Income Portfolio. I discussed this in detail in this recent post, but basically money in this port is invested to generate an income from share dividends and other sources. This is then paid monthly. Capital appreciation is targeted as well, but these portfolios are aimed primarily at older people (and others) who want/need their investment to generate a regular cash income.

In September my Nutmeg income portfolio generated £78.72 of income, which was duly paid in to my bank account on 24 September 2025. That is down a bit on the £134.03 I received in August, but it means I have now received a total (tax-free) income of £212.75 to date. That is in line with Nutmeg’s projected annual return of just under 5% for income ports at my chosen risk level (five). Obviously it is too early to draw any significant conclusions from this, though.

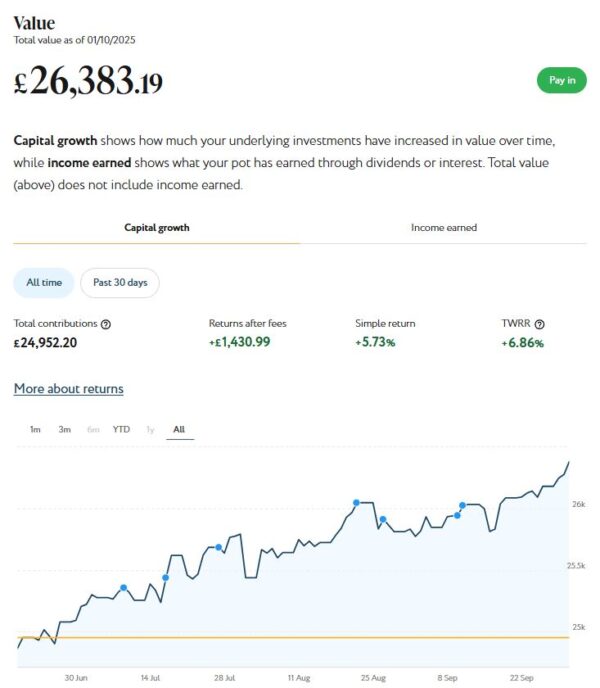

My income portfolio also grew in value in September. It’s now worth £26,383 compared with £25,815 at the start of last month, a rise of £568. As the screen capture shows, the port has actually increased by £1,430.99 (5.73%) since I opened it in June. That’s good going, though I don’t suppose it will carry on like this indefinitely!

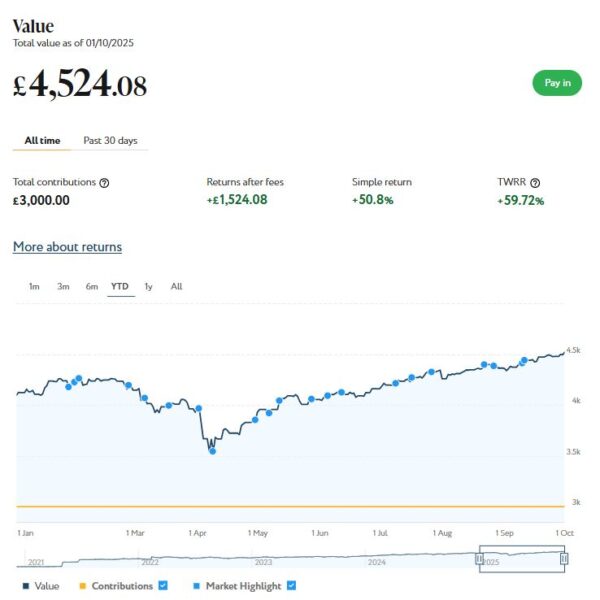

I still have a smaller, growth-oriented pot using Nutmeg’s Smart Alpha option. This is now worth £4,524 compared with £4,368 a month ago, a rise of £156. Here is a screen capture showing performance for the year to date.

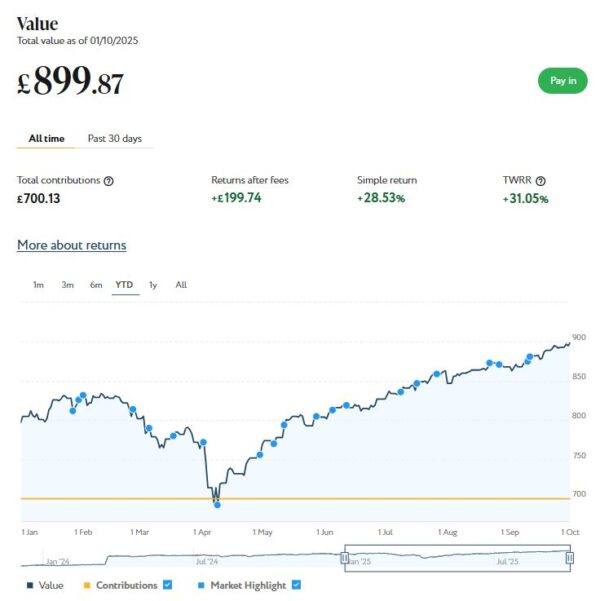

And at the start of December 2023 I invested £500 in one of Nutmeg’s thematic portfolios (Resource Transformation). In March 2024 I also invested a further £200 from referral bonuses (something I no longer receive for reasons I won’t bore you with). As you can see from the YTD screen capture below, this portfolio is now worth £900 (rounded up) compared with £868 last month, a rise of £32.

Finally, I still have a small amount left in my original Nutmeg Fully Managed portfolio. I have kept this largely for comparison purposes. This has increased in value from £595 at the start of September to £617 (rounded up) now, a rise of £22.

As you can see, September was a pretty good month for my Nutmeg investments. Overall I was up by £778 or 2.46%. In addition I did, of course, receive £78.72 in income from my income portfolio.

Excluding income generated, the overall value of my Nutmeg investments is up by £1,996 since the start of 2025, so the April 2025 fall (caused largely by Trump’s tariffs) has now fully reversed. I am also up by £3,069 or 10.45% since the start of October last year, again excluding cash income received. All things considered, that’s not a bad result.

As I always have to say, some volatility is to be expected with stock market investments, but over the longer term they tend to even themselves out (and generally perform better than bank savings accounts, although that is never guaranteed). In general the worst thing you can do is panic and sell up when downturns occur (as happened in April this year). You are then crystallizing your losses rather than giving the markets time to recover. This is something I had cause to discuss in this blog post from earlier this year.

You can read my full Nutmeg review here. If you are looking for a home for your annual ISA allowance, based on my overall experience over the last nine years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs), Lifetime ISAs and Junior ISAs as well.

Moving on, I also have investments with P2P property investment platform Assetz Exchange. As discussed in this post, the company has rebranded as Housemartin.

My investments with Housemartin continue to generate steady returns. Housemartin focuses on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my HM portfolio has generated a respectable £273.80 in revenue from rental income. I have made a small net loss of £19.02 on property disposals. Capital growth generally has slowed, in line with UK property values generally.

At the time of writing, 16 of ‘my’ properties are showing gains, 7 are breaking even, and the remaining 17 are showing losses. My portfolio of 40 properties is currently showing a net decrease in value of £43.52. That means that overall (rental income minus capital value decrease and loss on disposal) I am up by £211.26. That’s still a respectable return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Housemartin most projects are socially beneficial as well.

The net fall in capital value of my Housemartin investments is obviously a little disappointing. But it’s important to remember that until/unless I choose to sell the investments in question, it is largely theoretical, based on the latest price at which shares in the property concerned have changed hands. The rental income, on the other hand, is real money (which in my case I’ve reinvested in other HM projects to further diversify my portfolio).

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of Housemartin as far as i am concerned. You can actually invest from as little as £1 per property if you really want to proceed cautiously.

As I noted in this blog post, Housemartin is particularly good if you want to compound your returns by reinvesting rental income. This effectively boosts the interest rate you are receiving. Personally, once I have accrued a minimum of £10 in rental payments, I usually reinvest this money in either a new HM project or one I have already invested in (thus increasing my holding). Over time, even if I don’t invest any more capital, this will ensure my investment with Housemartin grows at an accelerating rate and becomes more diversified as well.

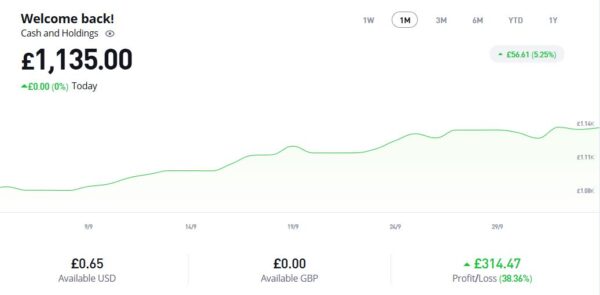

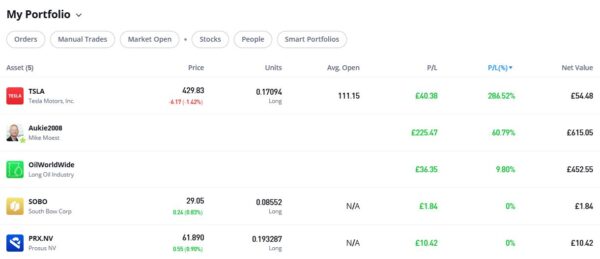

In 2022 I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios, Oil Worldwide. I also invested a small amount I had left over in Tesla shares.

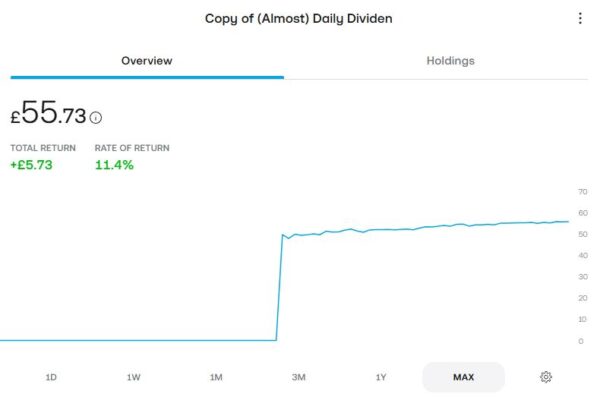

As you can see from the screen captures below, my original investment (total value £888.36 in pounds sterling) is today worth £1,135.00 an overall increase of £246.64 or 27.76%.

Note: eToro now displays the value of investments in your native currency, although you can change this if you wish.

As you can see, my Oil WorldWide investment is in profit, though at 9.80% it is nothing too exciting. My copy trading investment with Aukie2008 has been doing better, with an overall 60.79% profit. To be fair, I have held this investment a bit longer.

My Tesla shares, which I bought as an afterthought with some spare cash I had in my account, are up again this month. They are showing an impressive overall profit of 286.52% since I bought them. If only I had put a bit more money into this!

You might also notice that I have small holdings in Prosus NV, a Dutch internet group, and South Bow, a Canadian energy infrastructure company. To be honest I don’t understand how I acquired these, but I assume they are some sort of bonus I was awarded. In any event, I am happy to have them in my portfolio.

eToro also offer the free eToro Money app. This allows you to deposit money to your eToro account without paying any currency conversion fees, saving you up to £5 for every £1,000 you deposit. You can also use the app to withdraw funds from your eToro account instantly to your bank account. I tried this myself and was impressed with how quickly and seamlessly it worked. You can read my blog post about eToro Money here. Note that it can also serve as a cryptocurrency wallet, allowing you to send and receive crypto from any other wallet address in the world.

If you would like more information about setting up an eToro account, please click on this no-obligation website link [affiliate]. Don’t forget that you also get a free $100,000 virtual portfolio, which you can use to experiment with trading and investing strategies. I have certainly earned a lot from mine.