Today I have a guest post for you on a subject I don’t generally cover on Pounds and Sense.

Cryptocurrency investing/trading is risky and I appreciate that it may not appeal to many readers of this blog. On the other hand, I can’t deny there is a lot of interest in crypto, from younger people in particular. So today I am publishing a guest post for anyone who might be interested in finding out a bit more…

While some people prefer to invest in crypto as a side hustle, others want to take it a step further and become a full-time home-based crypto investor.

Investing time and money into crypto can be risky, so it’s important that you know what you are doing and you pay attention to how the markets change. In this article we will go over a few tips and tricks to help you get started.

Create a Working Space

One of the first things you will need to do is set up a working space for yourself. It is important that you have a designated area to work in, as this will help you stay concentrated and focused throughout the day. If you can, it would be a good idea to have your workspace away from anything else, as this will stop you from getting distracted. A spare room or even just a corner in one room of your house will work well.

Keep Updated with Crypto News

Keeping up to date with crypto news is a great way to start off as a crypto investor. The financial markets can be volatile, so you must stay current with all the latest changes so that you can make any necessary adjustments to your investments. There are plenty of ways to stay up to date, but it could be helpful to download a crypto app that will help you manage your investments and also learn about any changes to the market.

Research Ways to Earn Bitcoin

It would be beneficial for you as a home-based crypto investor to start researching ways that you can earn Bitcoin, one of the most popular types of cryptocurrency. Learning the different ways you can earn Bitcoin will help you become a successful investor. One way you can earn Bitcoin is by trading a gift card you don’t need for it. Paxful allows you to safely buy Bitcoin with a gift card, which makes earning Bitcoin super easy.

Join Crypto Communities

If you are new to the world of cryptocurrency, then a good way to get started is joining different crypto communities. There are plenty of discord servers or Reddit subs that are specifically for crypto investors, so these can be helpful to be a part of. Users share their different experiences with the crypto market and offer advice and suggestions about when and how you should invest. For someone starting out as a crypto investor this can be invaluable, as you will learn about crypto from people who have more knowledge and experience than you (though don’t take everything you read as gospel!). Having a supportive community behind you will allow you to learn and grow as a crypto investor.

Thank you to my friends at Paxful for an interesting article.

Just to emphasize what I said at the start, cryptocurrency trading is high risk and definitely not for everyone. Yes, you can make a lot of money, but you can also lose your shirt!

My personal advice if nonetheless you want to explore cryptocurrency trading/investment is to start small with money you can afford to lose in a worst-case scenario. I also like the idea mentioned in the article of earning cryptocurrency rather than buying it. Obviously if your crypto is something you have earned or otherwise acquired yourself (perhaps by exchanging a gift card), losing it isn’t likely to be as painful 😮

I would love to hear your reactions to this article, and whether you think I should cover cryptocurrency more often on Pounds and Sense. I’d also be interested to hear about your personal experiences with crypto (no spam, please). Please leave any comments or questions below as usual.

This is a collaborative post.

Disclaimer: Nothing in this article should be construed as personal financial advice. As stated in the article, cryptocurrency trading/investment can be very high risk and is not suitable for everyone. Proceed with care and take professional advice if in any doubt whether it is right for you. All investing carries a risk of loss and this is especially so with cryptocurrencies.

If you enjoyed this post, please link to it on your own blog or social media:

I’ve mentioned several times on PAS why I believe having an independent financial adviser makes sense, even if – like me – you consider yourself reasonably money-savvy.

So today I thought I would set out some reasons over-50s (in particular) may benefit from having an independent financial adviser (IFA) or at least speaking to one.

This post has been created in association with my colleagues at Unbiased.co.uk, a well-established financial services website that can put you in touch with suitable IFAs in your area.

Reasons for Having an IFA

1. Helping Your Children Through College or University

If you have children, you will naturally want to help them complete their education safely and with a reasonable degree of comfort. Sadly the days of student grants (which I was lucky enough to benefit from in the 1970s) are well behind us now. There are various options for helping finance your children’s college or university education and a financial adviser will be able to explore these with you. They will also explain the pros and cons of the student loans system.

2 – Pension Planning

If you are over 50 you will inevitably be thinking about pension options, including when you can retire and how much income you can expect. An IFA will go through your finances with you and look at ways you may be able to boost your pension pot. From 55 onwards you can normally start to draw your pension, but you shouldn’t do this unless a financial adviser has assured you it will last you through retirement.

3. Investing

Hopefully by your fifties you will be earning a decent salary and may also have paid off your mortgage. You may also receive an inheritance or other windfall. Either way, if you find yourself with some spare cash you will want to invest it to get the best possible returns from it. An IFA will have access to all the latest information about a vast range of investment opportunities. They will guide you towards investments that are suitable for you based on your financial goals, your investment timeframe and your appetite for risk.

4. Starting Your Own Business

Especially at this time of upheaval due to Covid, many people are looking to start their own businesses in mid-life. That may be in response to redundancy or unemployment, or simply in search of a better work/life balance. An IFA can help you with the financial aspects of doing this, including raising money for tools, premises, transport and so on, or perhaps buying a franchise.

5. Emigrating or Retiring Abroad

Another way to revitalize your life may be to start afresh somewhere else, with new challenges and opportunities (and perhaps a better climate as well!). Or you may be looking to move to a favourite vacation destination to enjoy your retirement. Either way, an IFA will be happy to discuss the pros and cons with you, point out all the things you will need to take into account, and assist you with the financial arrangements.

6. Divorce

Sadly middle age sees the largest number of divorces. Your first priority here will be appointing a good solicitor to act on your behalf and protect your interests. Beyond that, though, divorce can have major ramifications for your finances. An IFA can help you assess your situation objectively and plan for a financially secure and stable future.

7. Downsizing

As the children grow up and leave home you may want to move to a smaller property – to make life simpler, save time on housework and free up money for more exciting things. An IFA can help you explore the implications of doing this and make the necessary financial arrangements.

8. Equity Release

If you don’t want to move – and are over 55 – equity release is another option for releasing funds. In recent years it has grown a lot in popularity. There are various possibilities, including home reversion plans and flexible lifetime mortgages. Most now come with a no-negative-equity guarantee, ensuring you won’t end up passing on debts to your next of kin. An IFA can go over the options with you and point out the pros and cons before you contact any providers.

9. Estate Planning

This obviously includes writing your will, but depending on your circumstances it can cover a lot of other things as well. Nobody wants to see all their money and assets falling into the hands of the taxman rather than going to their nearest and dearest. Speaking to an IFA who specializes in estate planning can give peace of mind and ensure that your loved ones are well provided for when you are no longer here yourself.

10. Helping Elderly Relatives

If you have elderly parents (or other relatives) you may find they are increasingly reliant on you for help and support. It may be up to you to arrange care for them and/or set up power of attorney so you can manage their affairs if this becomes necessary. They may also need help with estate planning (see above). An IFA can assist with all these things as well.

Getting a Free Financial Check-Up

Independent financial advisers do of course charge for their services. They are by definition unaffiliated and do not receive commission, so any recommendations they make are based solely on their client’s best interests. As I have said before on PAS, I certainly don’t begrudge paying my own financial adviser, Mike, as he has undoubtedly saved (and made) me a lot more money than he has cost me over the years.

Nonetheless, most IFAs will be happy to see you for an initial financial healthcheck free of charge. This can focus on a particular area of concern, so you could request an investments review, a pension review or a mortgage review. Alternatively, if you’re not sure which aspect of your finances needs more attention – or indeed whether you need advice at all – you could simply request a broad financial healthcheck.

Here’s what. Adrian Kidd, a financial planner at Radcliffe & Newlands, says about his approach on the Unbiased website:

‘I’d generally offer one or possibly two free consultations, taking about an hour, and these can be as specific or as broad as required. When someone books a financial healthcheck with me, I ask them to bring along all their documents relating to their finances – savings, investments, mortgages, loans, insurance, pensions, the works – so I can build up a complete picture of their affairs. I then go through these in more detail after the consultation, and follow up with an email that gives a summary of their overall financial situation.’

In these free check-ups: advisers won’t generally talk to you about products at all. The process of choosing the right products comes later, after the adviser has built up an understanding of you as a person and your financial planning needs. Only then will they recommend products, if asked to do so.

If you follow my link to the Unbiased website, you can complete a short, step-by-step questionnaire designed to identify the best type of financial adviser for your needs. You will then be shown a selection of suitable advisers in your area with contact information. They will be happy to answer any queries you may have and arrange an initial meeting without obligation.

As ever, if you have any comments or questions about this post, please do leave them below.

Disclosure: This is a sponsored post on behalf of Unbiased.co.uk. If you click through my link and end up becoming a client of a financial adviser listed on the Unbiased site, I may receive a commission for introducing you. This will not affect the service you receive or any fees you are charged if you decide to proceed further.

This is a fully updated version of a post originally published in 2020.

If you enjoyed this post, please link to it on your own blog or social media:

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. As I only updated my full review of Nutmeg last week, however, I will keep it fairly brief today.

Nutmeg is the largest investment I hold other than my Bestinvest SIPP (personal pension). Withdrawals from the latter are still on hold to avert the risk of pound-cost ravaging.

My main Nutmeg portfolio, which I opened back in 2016, is currently valued at £19,733. Last month it stood at £19,292 so that is a rise of £441. My smaller Smart Alpha investment (opened in 2020) is currently valued at £2,987. Last month it stood at £2,921, so that is a rise of £66. My total Nutmeg investments have therefore increased by £507 month on month.

While the rise in October is of course welcome, my Nutmeg investments are still down by about 11% in value since the start of the year. As I said in my recent Nutmeg review, that’s clearly disappointing, but it’s still a lot less than the amount by which they went up in 2021 alone. And I am still over £5,400 in profit overall. I am therefore philosophical about this, recognising that all investments have their ups and downs and Nutmeg is hardly alone in seeing a drop in values this year. But I do understand why people who started investing with them in the last twelve months or so may be feeling disappointed. You might like to read this recent article on the Nutmeg blog where they discuss the performance of Nutmeg portfolios in 2022 and examine the outlook going forward.

There is actually an argument that now may be a good opportunity to invest while asset values are depressed. At some point we will see a recovery and people who invest at the present time will be well placed to benefit from this. Of course, nobody knows for sure when the recovery will happen or how much further asset values might fall first. Nonetheless, I am certainly considering adding further to my Nutmeg investments in the coming months.

Moving on, my Assetz Exchange investments continue to perform well. Regular readers will know that this is a P2P property investment platform focusing on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my AE portfolio has generated £81.40 in revenue from rental and £30.80 in capital growth, a total of £112.20. That’s a decent rate of return on my £1,000 investment and does illustrate the value of P2P property investment for diversifying your portfolio when equity markets are volatile.

I now have investments in 23 different projects and all are performing as expected, generating rental income and in most cases showing a profit on capital as well. So I am very happy with how this investment has been doing. And it doesn’t hurt that most projects are socially beneficial as well.

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of AE as far as i am concerned. You can actually invest from as little as 80p per property if you really want to proceed cautiously.

Another property platform I have investments with is Kuflink. They continue to do well, with new projects launching almost every day. I currently have around £2,600 invested with them in 17 different projects. To date I have never lost any money with Kuflink, though some loan terms have been extended once or twice. On the plus side, when this happens additional interest is paid for the period in question. At present most of my Kuflink loans are performing to schedule, though five have had their repayment dates put back.

My loans with Kuflink pay annual interest rates of 6 to 7.5 percent. These days I invest no more than £200 per loan (and often less). That is not because of any issues with Kuflink but more to do with losses of larger amounts on other P2P property platforms in the past. My days of putting four-figure sums into any single property investment are behind me now!

Nowadays I mainly opt to reinvest the monthly repayments I receive from Kuflink, which has the effect of boosting the percentage rate of return on the projects in question

Obviously a possible drawback with Kuflink and similar platforms is that your money is tied up in bricks and mortar, so not as easily accessible as cash savings or even (to some extent) shares. They do, however, have a secondary market on which you can offer any loan part for sale (as long as the loan in question is performing and not in arrears). Clearly that does depend on someone else wanting to buy it, but my experience has been that any loan parts offered are typically snapped up very quickly. So if an urgent need arises, withdrawing your money (or part of it) is unlikely to be an issue.

You can read my full Kuflink review here. They offer a variety of investment options, including a tax-free IFISA paying up to 7% interest per year with built-in automatic diversification. Alternatively you can now build your own IFISA, with most loans on the platform (including the one shown above) being IFISA-eligible.

My investment in European crowdlending platform Nibble continues to perform as advertised. My latest investment was in their Legal Strategy. These are loans that are in default and facing legal action. Nibble buy these loans at a heavily discounted rate and then seek to recover as much as possible of the money owed. The minimum investment is 10 euros and the minimum period is six months. I invested 100 euros for 12 months initially at a target annual interest rate of 12.5%.

The Legal Strategy comes with a deposit-back guarantee. This is a guarantee to return the full investment amount at the end of the investment period and a minimum yield of 9% per year. The actual yield depends on how successful recovery efforts prove, so in practice you may end up with a return of anywhere between 9% and 14.5%. All has gone to plan so far, but I will obviously continue to report on this in the months ahead.

Earlier this year I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie. Unsurprisingly my investment has been up and down in the last few months, but it is currently about $8 in profit. In these turbulent times I am quite happy with that.

In addition, since I started on eToro, the pound has weakened against the US dollar, so my investment has benefited from this. My $508 US is now worth around £440 in UK pounds, so I am effectively £28 up overall. I am not claiming this as a particular benefit of eToro, but it does demonstrate how exchange rate fluctuations can sometimes work in your favour!

In any event, I’m looking on this as a long-term investment so won’t be judging it yet. I am also considering a further investment with eToro, possibly in one of their themed portfolios. You can read my full in-depth review of eToro here. I am also planning to publish a more in-depth look at eToro copy trading on the blog soon.

Moving on, I had another article published on the always-excellent Mouthy Money website. This one is entitled How to Save Money on Petrol. I was actually commissioned to write this when petrol prices were peaking. Since then they have fallen back somewhat, but with no end in sight to the war in Ukraine prices could easily shoot back up again. In the article I discuss my favourite website for monitoring petrol prices locally and also set out my top tips for cutting your petrol (or diesel) consumption.

As a matter of interest, Mouthy Money recently asked if I could increase the number of articles I write for them (so I guess I must be doing something right!). From November they will be publishing two articles a month from me. While they don’t pay me a fortune, the extra cash will undoubtedly help a lot in the cold winter months ahead.

Obviously energy bills are a particular concern for many people at the moment, so I hope you are getting all the help you are entitled to. By now everyone should have received the first instalment (£66) of the £400 rebate all UK residents are due on their energy bills for the next six months. If not, chase it up with your energy supplier.

I am with EDF, and they are crediting the rebate payments to my bank account once my monthly direct debit has been taken. Other energy suppliers are doing it differently, e.g. deducting the rebate from monthly direct debits before they are taken. This article from the popular Moneysavingexpert website explains how different energy suppliers are applying the rebate.

I also received a letter last week confirming that, as I receive the state pension, I shall be getting an enhanced Winter Fuel Payment of £500 in November or December this year, which will be very welcome as well 🙏

In the last few years I also qualified for the Warm Home Discount, which this year is being increased from £140 to £150. The rules are changing, however, and I suspect I shall be one of the people who misses out. The full new rules still haven’t been announced, but I will update my blog post about WHD as soon as I know more.

As I’ve said previously, the government’s Help for Households website has a helpful summary of all the financial assistance currently available and is regularly updated.

Please do check out as well some of the other posts on Pounds and Sense for advice and resources, especially in the Making Money and Saving Money categories.

Don’t forget, also, that there are currently two opportunities to claim a free share available. One is with Wealthyhood and the other with Trading 212 (the links will take you to the relevant blog posts). The Trading 212 offer closes on 8 November 2022, so don’t delay if you want to take advantage of this one. As far as I know the Wealthyhood offer is open indefinitely, but that could always change, of course 🙂

That’s all for today. As always, if you have any comments or queries, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media:

Investing can be confusing, and it’s easy to lose track of where your money is going. Thankfully, Microsoft Excel has many tools that can help you effortlessly track your investments.

Excel offers many ways for users to easily track their investments, such as by tracking the value of their portfolio over time, analyzing past performance, and comparing how different asset classes performed in similar market conditions.

Excel can also help investors stay on top of balances and transaction activity across multiple accounts. It allows them to visualize how these transactions affect their total wealth over time. This information can help investors decide when to invest more or pull out some cash for other uses.

Excel can be beneficial for investment tracking, especially if you’re saving for retirement and want to see how much progress you’ve made over time.

You can either enrol in Excel training to learn a few tips or tricks to analyze your investment data (which will serve you well for life), or you can follow the guide below for a quick solution.

Create a Portfolio

A portfolio is a collection of individual investments held by an investor. A typical portfolio will include stocks, bonds, mutual funds, exchange-traded funds (ETFs), options, and other securities.

If you’re looking to create a portfolio in Excel, here’s how to do it:

1. Open up the spreadsheet application on your computer,

2. Click on ‘File’ and select ‘New’.

3. Select ‘Blank Workbook’ from the new screen’s drop-down menu. This will open up a new file for you to start creating your portfolio in Excel.

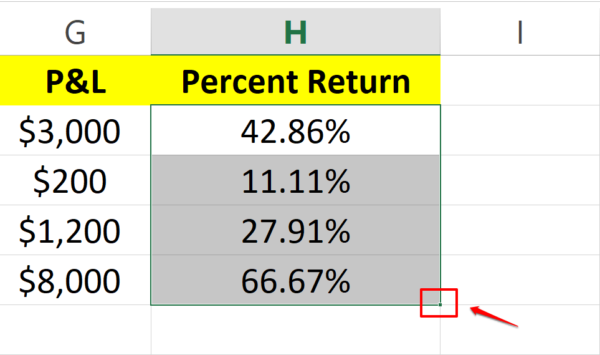

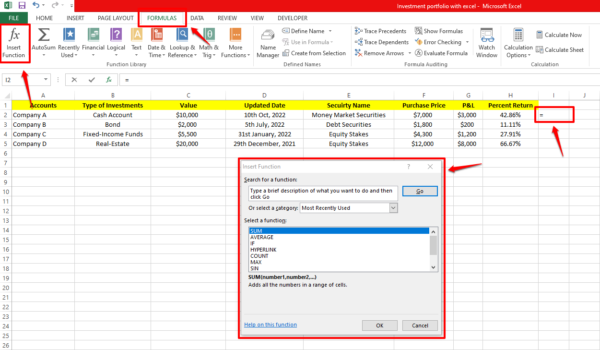

4. Type the heading ‘Accounts’ in one of the columns. The accounts should be listed from largest to smallest by value or assets under management (AUM). We recommend listing these accounts as rows instead of columns to make it easy to track.

5. Create columns for the type of investment you have in your portfolio against each account. These include cash accounts, bonds, fixed-income funds, stocks and equity funds, commodities, and other assets like real estate or intellectual property rights.

6. Now create another column with the heading ‘Shares/Investment’ and enter the data for each investment appropriately.

7. You can add columns related to Date, Security Name, Number of Shares or Units Owned, Purchase Price Per Share/Unit (or Cost Basis), and Current Market Value Per Share/Unit (or Current Value). In addition, add columns for Cost Basis (the original purchase price), Gain/Loss Per Unit, and Total Gain/Loss For All Units (for each security).

8. You may also want to include columns for Percent Gain/Loss.

9. Save the spreadsheet as an Excel file and then close it.

Use the ‘Difference Formulas’ in Excel

Excel’s most useful feature is its ability to calculate differences between two numbers. For example, if you have a list of investment values and you want to know how much money you have made since your purchase, you can try the following method:

1. Click the cell where you want to calculate the difference between your asset’s current price minus its original purchase value.

2. Type the equal sign ‘=’ and then select the cell containing the current value of your investment.

3. Type the minus sign ‘-‘ and then select the cell containing the original purchase price of the investment.

4. Press enter, and the difference will be calculated.

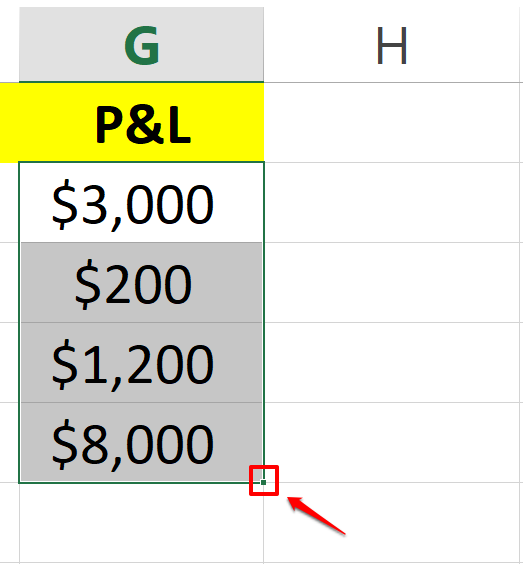

5. Now click and press the small square at the end of that cell (containing the difference), and drag it downwards to calculate the difference of each dataset automatically.

Use the ‘Percent Return Formulas’ in Excel

To track the return on investment over time, you can use Microsoft Excel’s percent return formulas. These formulas calculate the percentage increase or decrease in an investment’s value over time.

The formula for percent return is: (Current price – Purchase price) ÷ Purchase price

Here’s how you can apply the percent return formula in Excel:

1. Select the cell where you want the percent return formula to be calculated.

2. Type the equal sign ‘=’ and add an open parenthesis ‘(‘.

3. Select the cell containing the current value of your investment.

4. Type the minus sign ‘-‘ and select the cell containing the original purchase price of your investment and then close the parenthesis ‘)’.

5. Now, type the forward slash ‘/’ and select the cell containing the original purchase price.

6. Press enter, and the percent return will be calculated.

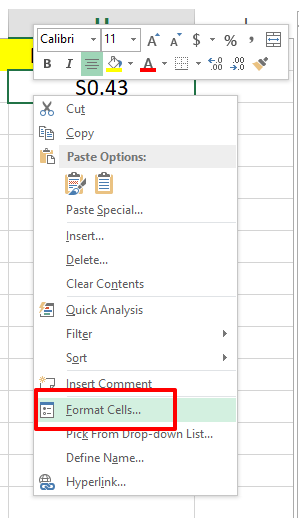

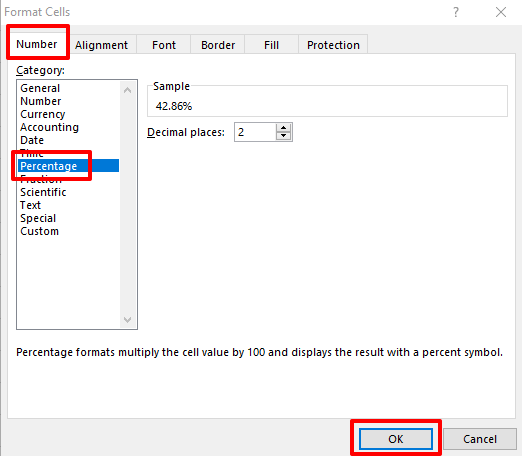

7. To make values appear as percentages, right-click on the cell, select the option of Format Cells, and select Percentage under the number tab.

8. Once done, click and drag the small square at the bottom right corner of your percent return cell and copy the formula for the rest of the dataset.

Use Advanced Excel Features to Customize your Sheet

Functions in Excel are a way for you to manipulate data in Excel programmatically. They can be used to perform calculations, transform data, and create new values.

You can find a list of all built-in functions in the Formula tab menu in Excel. To access it, click on any cell, navigate to the Formula tab and choose the ‘Insert Function’ option. The Insert Function dialogue box will appear, from where you can choose the function you are looking for by going through the list.

Here are the 10 most popular functions in Excel:

SUM function

IF function

LOOKUP function

VLOOKUP function

MATCH function

CHOOSE function

DATE function

DAYS function

INDEX function

FIND, FINDB functions

The best way to learn about each function is by using it. Try out different arguments and see what happens.

To Conclude

Excel is an excellent way to track investments because it saves and calculates dependable data. Also, you can use the program to graph your data and see how they change over time.

Thank you to my friends at Acuity Training for an informative guest article.

I use Excel spreadsheets for keeping track of my self-employed earnings and send them to my accountant once a year so that he can produce my annual accounts from them.

I do also use Excel for keeping track of my investments, but only in a very basic way. This article has inspired me to be a bit more ambitious with Excel and use formulas to automatically calculate the total and percentage returns from my investments, and so forth.

As always, if you have any comments or questions about this post, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

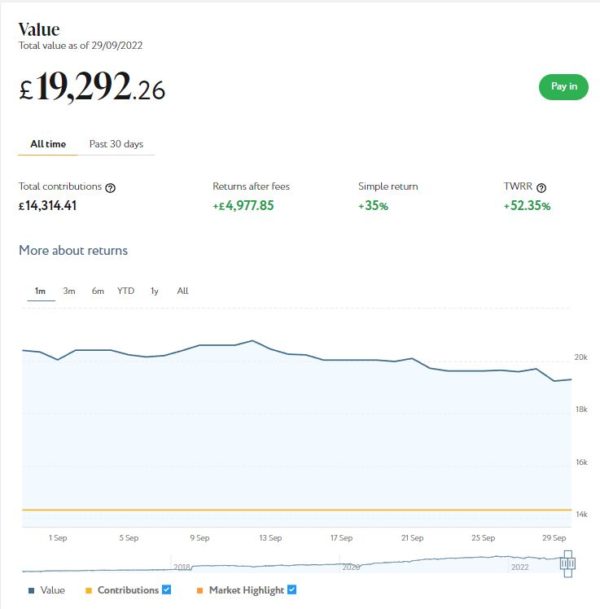

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension). Withdrawals from the latter are still on hold, incidentally, to avert the risk of pound-cost ravaging.

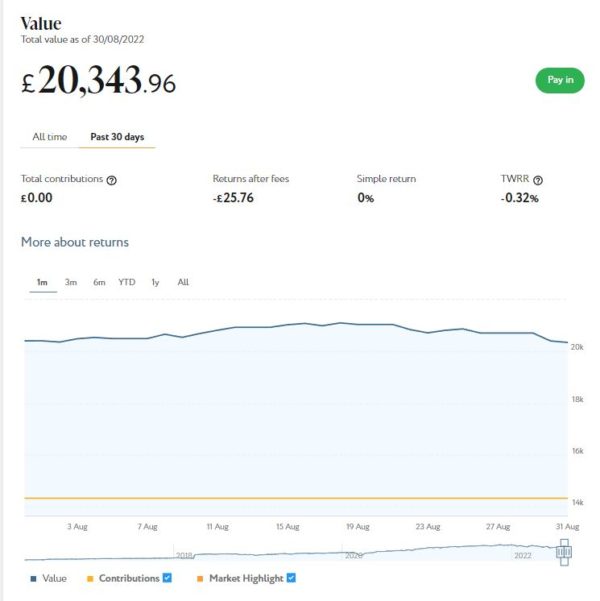

As the screenshot below of performance last month shows, my main portfolio is currently valued at £19,292. Last month it stood at £20,344 so that is a fall of £1,052.

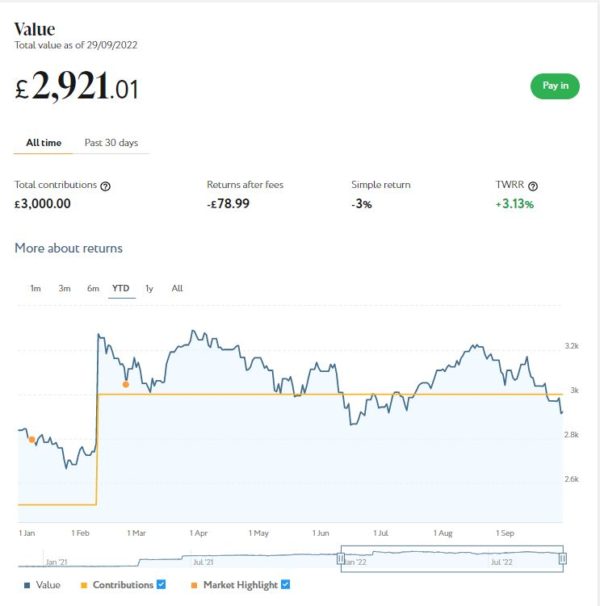

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £2,921 compared with £3,091 a month ago, another fall of £170.

Here is a screen capture showing performance since January 2022. As you can see, I topped up this account in February this year.

There is no denying that these falls are disappointing, especially with my Smart Alpha portfolio now worth less in total than I have contributed to it. As I’ve noted previously on PAS, however, you do have to expect ups and downs with equity-based investments. And this year there has been no lack of volatility, caused by rising inflation, the war in Ukraine and the aftermath of the pandemic (among other things).

About my only consolation is that things could have been even worse if – paradoxically – I’d opted for a lower-risk level with my investments. In their latest blog update, Nutmeg reveal that low and medium-risk portfolios actually performed worse overall last month than high-risk ones. I have copied below their explanation for this:

By design, Nutmeg’s low- and medium-risk portfolios have more exposure through ETFs to assets that are priced in sterling and with limited foreign currency exposure. As you will have seen in the headlines this week, the pound hit an all-time low against the dollar with markets initially placing little faith in the chancellor’s tax-cutting and pro-growth agenda.

This year it has been rewarding to hold foreign currency with sterling particularly weak versus the dollar. Some of our high-risk portfolios have benefited from currency moves, while low- and medium-risk portfolios have not. They haven’t lost money from having low foreign currency exposure, they just haven’t benefited from it.

Secondly, low- and medium-risk portfolios by design have more exposure – again through ETFs – to government bonds, which in ‘normal’ times are considered something of a safe haven and have much lower volatility than equities. After all, it is still highly unlikely that the UK government would default on its debts.

In a nutshell (no pun intended) low- and medium-risk Nutmeg portfolios hold a higher proportion of investments in pounds sterling and UK government bonds. These are normally regarded as lower risk, but last month both took a particular hammering. So in comparison nominally higher-risk portfolios like mine actually performed somewhat better.

This is one more reason I’m glad I opted for higher risk levels with my Nutmeg portfolios (9/10 for my main one and 5/5 for my Smart Alpha). If you haven’t yet seen it, you might also like to check out my blog post in which I looked at the performance over time of Nutmeg fully managed portfolios at every risk level from 1 to 10 . I was actually pretty amazed by the difference risk level makes, with higher-risk ports over almost any period of three or more years in the last ten generating significantly better overall returns. If you are investing for the long term (and you almost certainly should) opting for a hyper-cautious low-risk strategy may not be the smartest thing to do.

Since I started investing with Nutmeg in 2016 – and despite everything that has happened this year – I have still made a total net return on capital of £4,977 (35% or 52.35% time-weighted) on my main portfolio. So I can afford to be philosophical about the recent falls. Indeed, I am considering topping up my Nutmeg investments again now while asset values are depressed.

You can read my full Nutmeg review here (including a special offer at the end for PAS readers). If you are looking for a home for your annual ISA allowance, based on my experience over the last six years, they are certainly worth considering.

Moving on, my Assetz Exchange investments continue to perform well. Regular readers will know that this is a P2P property investment platform focusing on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my AE portfolio has generated £76.51 in revenue from rental and £63.58 in capital growth, a total of £140.09. That’s a decent rate of return on my £1,000 investment and does illustrate the value of P2P property investment for diversifying your portfolio when equity markets are volatile.

I now have investments in 23 different projects and all are performing as expected, generating rental income and in most cases showing a profit on capital as well. So I am very happy with how this investment has been doing. And it doesn’t hurt that most projects are socially beneficial as well.

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of AE as far as i am concerned. You can actually invest from as little as 80p per property if you really want to proceed cautiously.

Another property platform I have investments with is Kuflink. They continue to do well, with new projects launching almost every day. I currently have around £2,500 invested with them in 14 different projects. To date I have never lost any money with Kuflink, though some loan terms have been extended once or twice. On the plus side, when this happens additional interest is paid for the period in question. At present most of my Kuflink loans are performing to schedule, though two recently had their repayment dates put back by three months.

My loans with Kuflink pay annual interest rates of 6 to 7.5 percent. These days I invest no more than £200 per loan (and often less). That is not because of any issues with Kuflink but more to do with losses of larger amounts on other P2P property platforms in the past. My days of putting four-figure sums into any single property investment are behind me now!

Nowadays I mainly opt to reinvest the monthly repayments I receive from Kuflink, which has the effect of boosting the percentage rate of return on the projects in question

Obviously a possible drawback with Kuflink and similar platforms is that your money is tied up in bricks and mortar, so not as easily accessible as cash savings or even (to some extent) shares. They do, however, have a secondary market on which you can offer any loan part for sale (as long as the loan in question is performing and not in arrears). Clearly that does depend on someone else wanting to buy it, but my experience has been that any loan parts offered are typically snapped up very quickly. So if an urgent need arises, withdrawing your money (or part of it) is unlikely to be an issue.

You can read my full Kuflink review here. They offer a variety of investment options, including a tax-free IFISA paying up to 7% interest per year with built-in automatic diversification. Alternatively you can now build your own IFISA, with most loans on the platform (including the one shown above) being IFISA-eligible.

My investment in European crowdlending platform Nibble continues to perform as advertised. My latest investment was in their Legal Strategy. These are loans that are in default and facing legal action. Nibble buy these loans at a heavily discounted rate and then seek to recover as much as possible of the money owed. The minimum investment is 10 euros and the minimum period is six months. I invested 100 euros for 12 months initially at a target annual interest rate of 12.5%.

The Legal Strategy comes with a deposit-back guarantee. This is a guarantee to return the full investment amount at the end of the investment period and a minimum yield of 9% per year. The actual yield depends on how successful recovery efforts prove, so in practice you may end up with a return of anywhere between 9% and 14.5%. All has gone to plan so far, but I will obviously continue to report on this in the months ahead.

Moving on, I had another article published on the always-excellent Mouthy Money website. This one is entitled My Odd Smart Meter Story and Why Despite This I Still Recommend Them. In the article I discuss my rather strange experiences with a smart meter, which stopped working after I switched supplier and then rather mysteriously started again two years later! As per the article title, I do still recommend getting a smart meter, especially in these times of soaring energy bills.

Also in September I enjoyed a final (probably) short break of the year in Barmouth in Wales. I stayed at a Victorian Gothic hotel called Tyr Graig Castle. I was lucky with the weather, and enjoyed visiting nearby Harlech and Portmeirion (see cover image) as well as Barmouth itself.

I shall be publishing a full review of my short break in Barmouth soon. In the meantime, here is a photo of a rather splendid sunset taken from the hotel restaurant…

Finally, I know a lot of people are extremely anxious about the cost-of-living crisis. As I said last time, though, it’s important not to panic. I recommend a three pronged-approach of maximizing your income, minimizing your expenditure, and budgeting carefully (using your resources as effectively as possible, in other words).

Bear in mind, also, that a range of government support measures have been announced to mitigate the worst effects of the crisis. This government Help for Households website has a useful summary of all the help available and is regularly updated.

In the meantime, please do check out some of the other posts on Pounds and Sense for additional advice and resources, especially in the Making Money and Saving Money categories.

That’s all for today. As always, if you have any comments or queries, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media:

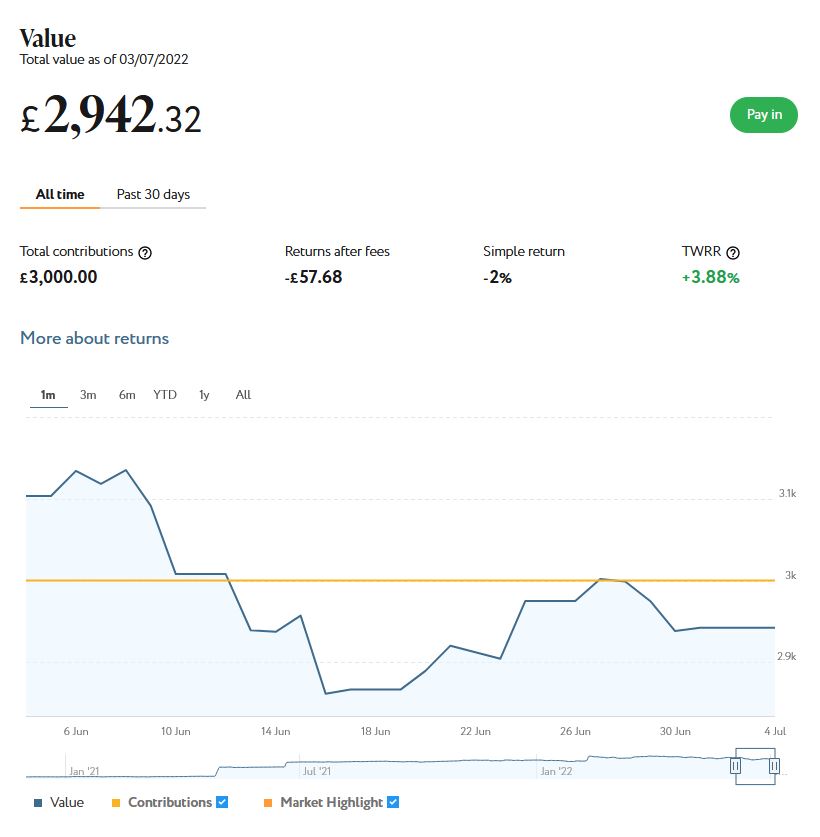

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

As the screenshot below of performance last month shows, my main portfolio is currently valued at £20,344. Last month it stood at £20,407 so that is a modest fall of £73.

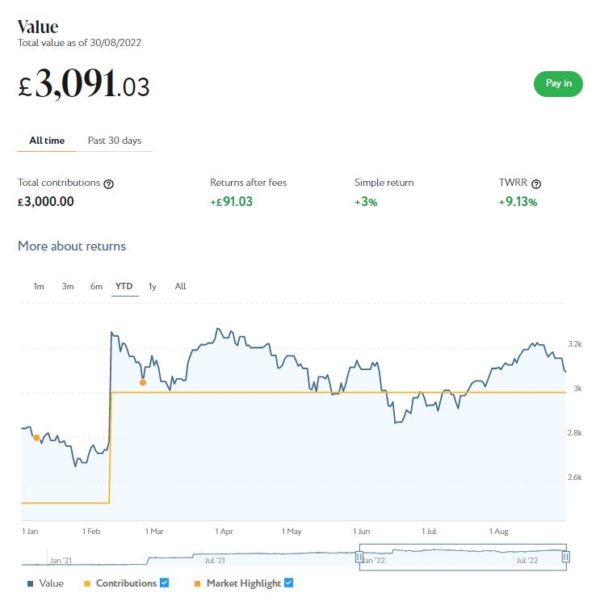

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £3,091 compared with £3,108 a month ago, another modest fall of £17.

Here is a screen capture showing performance since January 2022. As you can see, I have topped up this account several times this year.

The falls are obviously disappointing, though August was a roller-coaster month and until about a week ago both portfolios were showing a good profit since the end of July. As I’ve noted previously on PAS, you do have to expect ups and downs with equity-based investments. And this year there has been no lack of volatility in world markets, caused by rising inflation, the war in Ukraine and the aftermath of the pandemic (among other things).

Even so, since I started investing with Nutmeg in 2016 – and despite everything that has happened this year – I have still made a total net return on capital of 42.12% (or 60.65% time-weighted) on my main portfolio.

I should say as well that I selected quite a high risk level for both my Nutmeg accounts (9/10 for the main one and 5/5 for Smart Alpha). This has served me well generally, but I’m sure investors who selected lower risk levels will have seen fewer ups and downs over the last few months. If you also have a Nutmeg portfolio and plan to withdraw from it soon, there is certainly a case for switching to a lower risk level now.

You can read my full Nutmeg review here (including a special offer at the end for PAS readers). If you are looking for a home for your annual ISA allowance, based on my experience over the last six years, they are certainly worth considering.

My Assetz Exchange investments continue to perform well. Regular readers will know that this is a P2P property investment platform focusing on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my AE portfolio has generated £70.81 in revenue from rental and £85.35 in capital growth, a total of £156.16. That’s a decent rate of return on my £1,000 investment and does illustrate the value of P2P property investment for diversifying your portfolio when equity markets are volatile (as at the moment).

I now have investments in 23 different projects and all are performing as expected, generating rental income and in most cases showing a profit on capital as well. So I am very happy with how this investment has been doing. And it doesn’t hurt that most projects are socially beneficial as well.

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of AE as far as i am concerned. You can actually invest from as little as 80p per property if you really want to proceed cautiously.

Another property platform I have investments with is Kuflink. They continue to do well, with new projects launching almost every day. I currently have around £2,500 invested with them in 14 different projects. To date I have never lost any money with Kuflink, though some loan terms have been extended once or twice. On the plus side, when this happens additional interest is paid for the period in question. At present most of my Kuflink loans are performing to schedule, though two recently had their repayment dates put back by three months.

My loans with Kuflink pay annual interest rates of 6 to 7.5 percent. These days I invest no more than £200 per loan (and often less). That is not because of any issues with Kuflink but more to do with losses of larger amounts on other P2P property platforms in the past. My days of putting four-figure sums into any single property investment are behind me now!

Nowadays I mainly opt to reinvest the monthly repayments I receive from Kuflink, which has the effect of boosting the percentage rate of return on the projects in question

Obviously a possible drawback with Kuflink and similar platforms is that your money is tied up in bricks and mortar, so not as easily accessible as cash savings or even (to some extent) shares. They do, however, have a secondary market on which you can offer any loan part for sale (as long as the loan in question is performing and not in arrears). Clearly that does depend on someone else wanting to buy it, but my experience has been that any loan parts offered are typically snapped up very quickly. So if an urgent need arises, withdrawing your money (or part of it) is unlikely to be an issue.

You can read my full Kuflink review here. They offer a variety of investment options, including a tax-free IFISA paying up to 7% interest per year with built-in automatic diversification. Alternatively you can now build your own IFISA, with most loans on the platform (including the one shown above) being IFISA-eligible.

My investment in European crowdlending platform Nibble continues to perform as advertised. My latest investment was in their Legal Strategy. These are loans that are in default and facing legal action. Nibble buy these loans at a heavily discounted rate and then seek to recover as much as possible of the money owed. The minimum investment is 10 euros and the minimum period is six months. I invested 100 euros for 12 months initially at a target annual interest rate of 12.5%.

The Legal Strategy comes with a deposit-back guarantee. This is a guarantee to return the full investment amount at the end of the investment period and a minimum yield of 9% per year. The actual yield depends on how successful recovery efforts prove, so in practice you may end up with a return of anywhere between 9% and 14.5%. All has gone to plan so far, but I will obviously continue to report on this in the months ahead.

As mentioned last time, I recently set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (about £412) copying an experienced eToro trader called Aukie. My investment initially dipped, but I am now about $21 in profit. In these turbulent times I am quite happy with that. But in any event I’m looking on this as a long-term investment so won’t be judging it yet. I am also considering a further investment with eToro, possibly in one of their themed portfolios. You can read my full in-depth review of eToro here.

Moving on, I had another article published on the always-excellent Mouthy Money website. This one is titled Earn a Sideline Income From Online Surveys. In this article I set out my five favourite survey sites for generating a sideline income. Surveys represent an easy, stress-free way to give your income a bit of a boost, which clearly we could all do with just now.

I had quite a busy month in August (one reason I haven’t updated the blog for a while!). In particular, I agreed to present a session for The Joy Club (an online social group for retired and semi-retired people) on the subject of budgeting in the cost of living crisis. This involved rather more work than I anticipated, as I had to prepare a PowerPoint presentation, resources list and accompanying 7000 word script. But it seemed to go down well and I enjoyed the questions and discussion at the end. I know PAS has acquired some extra readers and subscribers as a result of this event, so a very warm welcome if that includes you!

Also in August I enjoyed a break in Lavenham in Suffolk, said to be England’s best-preserved medieval village. My original reason for going was to see Darkside, my favourite Pink Floyd tribute band (see photo below). But I thought I’d make a holiday of it as well, so I ended up staying four nights.

Lavenham is a charming, picturesque place, with various interesting historical buildings you can visit. These include the early 16th century Guildhall and Little Hall, a former wool merchant’s house. I plan to write a post about my Lavenham trip soon.

Finally, I know a lot of people are extremely anxious about the cost-of-living crisis. As I said in my Joy Club presentation last week, though, it’s important not to panic. I recommend a three pronged-approach of maximizing your income, minimizing your expenditure, and budgeting carefully (using your resources as effectively as possible, in other words). Bear in mind, also, that various government support measures have already been announced to try to mitigate the worst effects of the crisis. And once a new PM is (finally!) in place, more will certainly follow.

In the meantime, please do check out some of the other posts on Pounds and Sense for additional advice and resources, especially in the Making Money and Saving Money categories.

That’s all for today. As always, if you have any comments or queries, feel free to leave them below. I am always delighted to hear from PAS readers 🙂

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media:

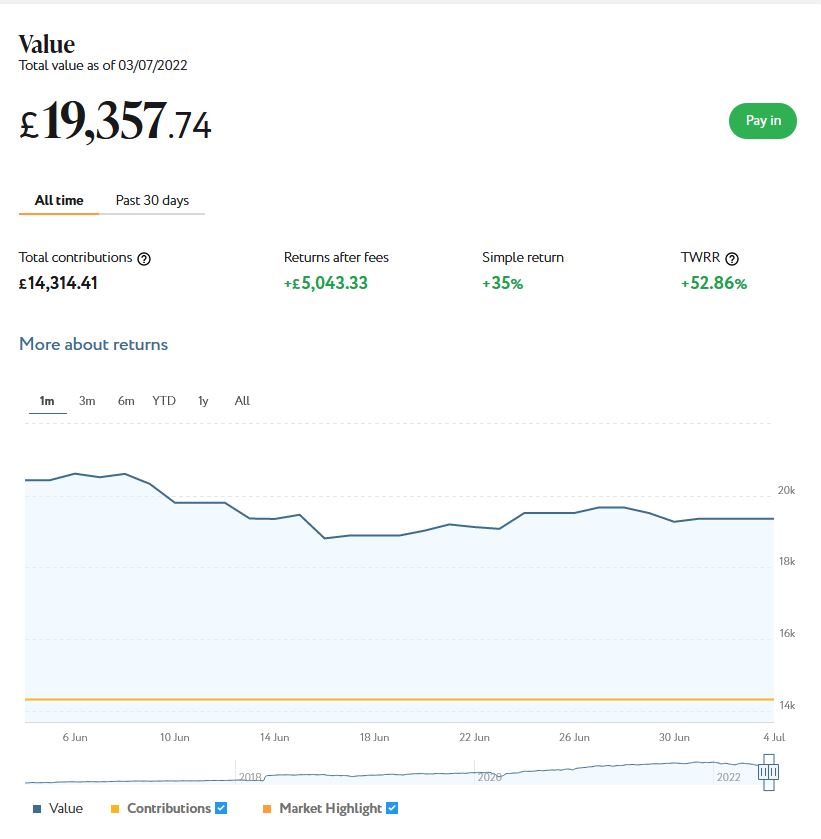

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

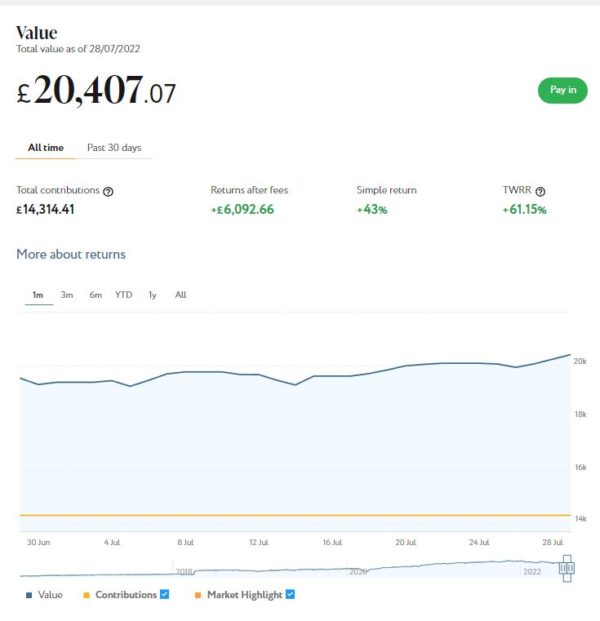

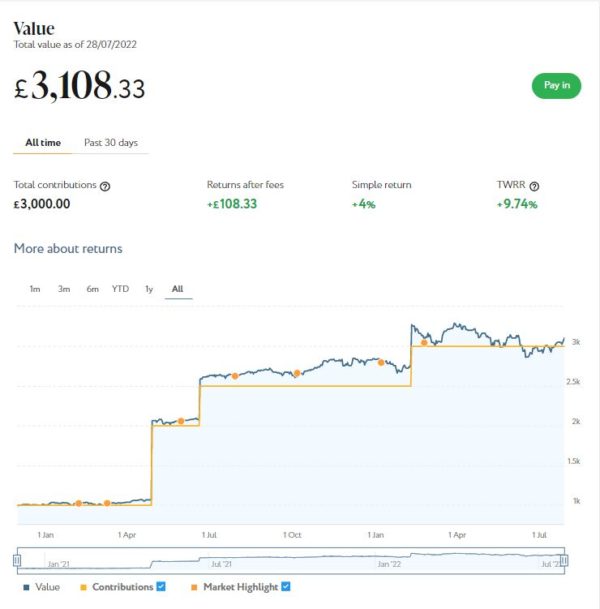

As the screenshot below of performance last month shows, my main portfolio is currently valued at £20,407. Last month it stood at £19,357 so that is a (very welcome) rise of £1,050.

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £3,108 compared with £2,942 a month ago, a rise of £166

Here is a screen capture showing performance since January 2022. As you may be able to see, I have topped up this account several times this year.

The rises in July are obviously encouraging. In particular, it is nice that my Smart Alpha portfolio (which I haven’t had as long) is worth more than I put into it once again!

Nonetheless, this month’s rises still don’t quite cancel out the falls of last month. And the total value of my Nutmeg portfoiio is still around 8% less than it was at the start of 2022.

As I’ve noted previously on PAS, you do have to expect ups and downs with equity-based investments. And this year there has been no lack of volatility in world markets, caused by rising inflation, the war in Ukraine and the aftermath of the pandemic (among other things).

Even so, since I started investing with Nutmeg in 2016 – and despite everything that has happened this year – I have still made a total net return on capital of 42.56% (or 61.15% time-weighted) on my main portfolio.

I should say as well that I selected quite a high risk level for both my Nutmeg accounts (9/10 for the main one and 5/5 for Smart Alpha). This has served me well generally, but I’m sure investors who selected lower risk levels will have seen smaller falls over the last few months. If you also have a Nutmeg portfolio and plan to withdraw from it soon, there may well be a case for switching to a lower risk level now.

You can read my full Nutmeg review here (including a special offer at the end for PAS readers). If you are looking for a home for your annual ISA allowance, based on my experience over the last six years, they are certainly worth considering.

Another property platform I have investments with is Kuflink. They continue to do well, with new projects launching almost every day. I currently have around £2,200 invested with them in 14 different projects. To date I have never lost any money with Kuflink, though some loan terms have been extended once or twice. On the plus side, when this happens additional interest is paid for the period in question. At present all my Kuflink loans are performing to schedule, though two are showing as ‘pending status update’, which may translate to a delay in repayment.

My loans with Kuflink pay annual interest rates of 6 to 7.5 percent. These days I invest no more than £200 per loan (and often less). That is not because of any issues with Kuflink but more to do with losses of larger amounts on other P2P property platforms in the past. My days of putting four-figure sums into any single property investment are behind me now!

Nowadays I mainly opt to reinvest the monthly repayments I receive from Kuflink, which has the effect of boosting the percentage rate of return on the projects in question

Obviously a possible drawback with Kuflink and similar platforms is that your money is tied up in bricks and mortar, so not as easily accessible as cash savings or even (to some extent) shares. They do, however, have a secondary market on which you can offer any loan part for sale (as long as the loan in question is performing and not in arrears). Clearly that does depend on someone else wanting to buy it, but my experience has been that any loan parts offered are typically snapped up very quickly. So if an urgent need arises, withdrawing your money (or part of it) is unlikely to be an issue.

You can read my full Kuflink review here. They offer a variety of investment options, including a tax-free IFISA paying up to 7% interest per year with built-in automatic diversification. Alternatively you can now build your own IFISA, with most loans on the platform (including the one shown above) being IFISA-eligible.

My investment in European crowdlending platform Nibble continues to perform as advertised. My latest investment was in their Legal Strategy. These are loans that are in default and facing legal action. Nibble buy these loans at a heavily discounted rate and then seek to recover as much as possible of the money owed. The minimum investment is 10 euros and the minimum period is six months. I invested 100 euros for 12 months initially at a target annual interest rate of 12.5%.

The Legal Strategy comes with a deposit-back guarantee. This is a guarantee to return the full investment amount at the end of the investment period and a minimum yield of 9% per year. The actual yield depends on how successful recovery efforts prove, so in practice you may end up with a return of anywhere between 9% and 14.5%. All has gone to plan so far, but I will obviously continue to report on this in the months ahead.

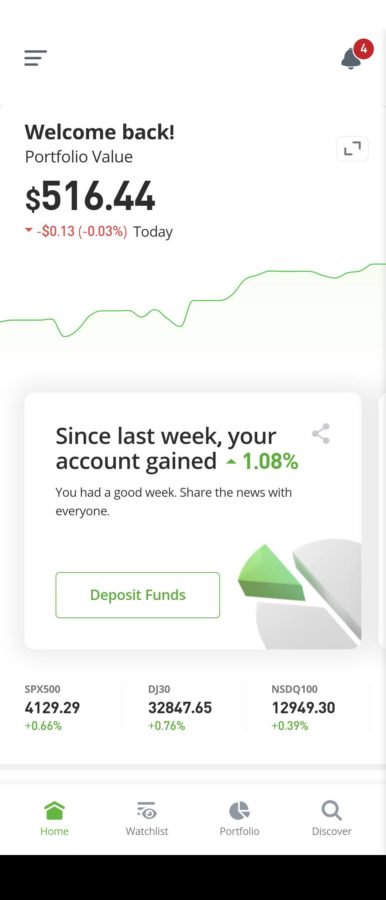

As mentioned last time, I recently set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (about £412) copying an experienced eToro trader called Aukie. My investment initially dipped, but as the screen capture below (of the app page on my mobile phone) shows, I am now about $16 in profit. That’s an increase of over 3% in just over a month. Obviously if it continues to do as well as this, I shall be delighted 🙂

In any event I am looking on this as a long-term investment so won’t be judging it yet. I am also considering a further investment with eToro, possibly in one of their themed portfolios. You can read my full in-depth review of eToro here if you like.

Moving on, I had another article published on the always-excellent Mouthy Money website. This one is titled Is Car Leasing Right For You? I found this very interesting to research and it gave me food for thought about what I may do when the time comes to bid goodbye to my current vehicle.

Turning to non-financial matters. I hope you are enjoying the (mostly) fine summer weather and making the most of our greater freedoms as we (hopefully) leave the pandemic behind. I recently enjoyed a day out with my friend Jeff at the National Trust’s Snowshill Manor and Gardens in Gloucestershire (pictured in the cover photo).

It was my first visit and I found it a fascinating place. The manor was owned by Charles Wade, an eccentric ex-Army officer. He used it to house his extensive collection of objects of all kinds, from musical instruments to children’s toys, bicycles to Samurai armour (see my photo below). I will try to find time to write a proper review of my trip to Snowshill soon.

And on the subject of summer, can I also remind you about the collaborative Summer Giveaway I am sponsoring in association with other UK bloggers. It’s free to enter, and the lucky winner will receive not only an MSpahot tub worth almost £1,000 but a range of other great prizes as well. The contest closes on 14 August 2022. Here’s a link to my blog post with details of how to enter.

That’s enough for today. As always, if you have any comments or queries, feel free to leave them below. I am always delighted to hear from PAS readers 🙂

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media:

More and more people are looking to invest ethically nowadays. As well as wanting decent returns from their money, they wish to ensure it is being used for purposes that will benefit the planet and local communities too.

So today I thought I would spotlight three ethical investment opportunities of which I have some experience and/or knowledge. There is nothing particularly scientific about this and I am certainly not saying these are the ‘best’ such opportunities. But based on my personal experience and feedback from colleagues and PAS readers, I am happy that they merit the ‘ethical’ description and are well-established and reputable.

Nutmeg Socially Responsible Portfolios

Regular readers of PAS will know that I am a fan of the robo-adviser platform Nutmeg and have a fairly substantial ISA investment with them.

As you probably know, an ISA is a tax-free wrapper that can be used for a range of investments. Every year you get an annual ISA allowance, which is currently £20,000. If you exceed your annual allowance (or invest it elsewhere) you can still invest in an ordinary Nutmeg account, which will be subject to taxation as usual.

Socially Responsible is an option you can choose for your Nutmeg portfolio (or one of them – you can have several). Your money is then invested in a managed, diversified fund which focuses on the environment, social values and good governance (ESG for short).

Nutmeg invest in exchange traded funds (or ETFs) that avoid companies engaged in controversial activities, while focusing on those that lead their peers on ESG. The screen capture below, taken from the Nutmeg site, shows the sort of things that are covered under ESG criteria.

As with all Nutmeg accounts, you can set your preferred risk level on a scale of 1-10 (you might like to check out this article in which I reveal why choosing a very low risk level when investing for the long term may not be the best idea).

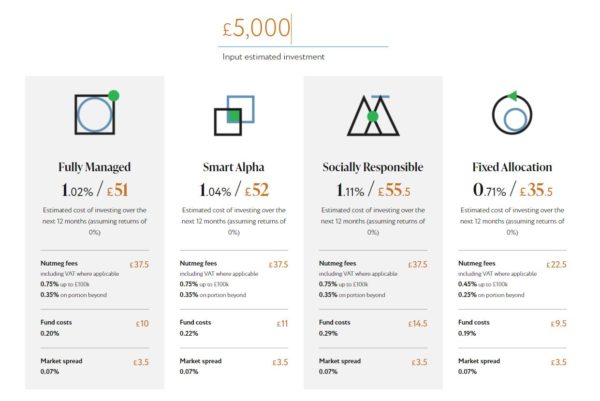

There are, of course, management and other fees to pay. For Socially Responsible portfolios these fees are slightly higher than the standard Fully Managed portfolios, but still moderate overall. Example costs for a £5,000 portfolio are shown below. On the Nutmeg website [affiliate link] you can enter any amount and see the likely fees you would be charged over a year.

You might wonder if choosing the Socially Responsible option means sacrificing performance, but Nutmeg say this is not the case. Since they started offering this option, performance has been roughly the same as their Fully Managed portfolios. Of course, the fact that charges are slightly higher means you may make a little less profit overall, but even so the difference should only be marginal.

For more information about Nutmeg, you may like to check out my in-depth review, which includes details of how my Fully Managed Nutmeg portfolio has performed since I opened it six years ago.

Assetz Exchange

Assetz Exchange is not an equities-based platform. Rather, it is a P2P property platform. I have been investing with Assetz Exchange since January last year and have gradually built up the amount I have with them (see below).

Assetz Exchange focuses on lower-risk properties, such as supported housing for people with learning difficulties or physical disabilities. Properties are bought jointly by investors under the usual crowdfunding/P2P model. Most are then leased to charities and housing associations. This means they are securely funded and there is a low risk of defaults.

Of course, defaults could still happen in certain circumstances – but as investors jointly own the property in question, ultimately you could still expect to get your capital (or most of it) back when the property is sold.

Although AE does also list some other types of property (e.g. show homes for new housing developments), you can of course choose which properties you wish to invest in. You could choose entirely charity/housing association projects – such as the one below – if you like.

I put an initial £100 into AE in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000. Since I opened my account, my AE portfolio has generated £65.52 in revenue from rental and £70.97 in net capital growth, a total of £136.49. That’s a decent rate of return on my £1,000 (staged) investment and does illustrate the value of P2P property investment for diversifying your portfolio when equity markets are volatile (as at the moment).

I now have investments in 23 different projects and all are performing as expected, generating rental income and – in all but two cases – showing a profit on capital. So I am very happy with how this investment has been doing, and the fact that projects are generally beneficial to society as well.

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of AE as far as I am concerned. You can actually invest from as little as 80p per property if you really want to proceed cautiously.

Abundance is a well-established investment platform (launched 2012) for green energy projects. Cards on the table, I haven’t invested directly through them myself, but I do have friends and colleagues who have done so with good results.

Abundance offers peer-to-peer lending for green infrastructure projects to help combat climate change. You can invest in projects operated by businesses and also projects run by local councils. Business projects tend to be riskier but offer higher potential returns.

When I checked just now, there were two council projects offering annual returns of around 2% and three business projects offering returns of up to 9%. An example of the latter is Carbon Plantations, a project to fund new sustainable hardwood trees that capture more carbon and help regenerate farmland. This project was offering a return of 8% a year over a ten-year period.

One thing which put me off Abundance in the past is that the investments are typically quite illiquid. You were locked into an investment of (typically) 5 to 10 years, with interest paid annually (or more often) but no way of getting your capital back until the end of the investment period. In common with other P2P platforms, however, they now have a secondary market where investments can be bought and sold by members. Of course, there is no guarantee that anyone else will want to buy your investment if you need to sell up early or what price you will get for it.

On the plus side, if you want your money to be used for green, ethical purposes, Abundance certainly ticks that box. I also like the fact that there is a low minimum investment of just £5. There are no hidden fees, and you can invest tax-free within an IFISA if you like. As with all investments, money is at risk, and I highly recommend diversifying across a range of platforms and projects.

In this article I have set out three different ethical investment opportunities for your consideration. While there are never any guarantees, if investing ethically is a priority for you, in my view they are all worth checking out.

As I always say, I am not a registered financial adviser and nothing in this post should be construed as personal financial advice. You should always do your own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

As always, if you have any comments or questions about this post, please do leave them below.

Note: Articles on Pounds and Sense may include affiliate links. If you click through these and make a purchase (or perform some other qualifying transaction) I may receive a fee for introducing you. This will not affect the price you pay or the terms you receive.

If you enjoyed this post, please link to it on your own blog or social media:

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

As the screenshot below of performance last month shows, my main portfolio is currently valued at £19,357. Last month it stood at £20,512 so, after another challenging month, that is a fall of £1,155.

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £2,942 compared with £3,119 last month, a fall of £177

Here is a screen capture showing performance over the last month.

There is no denying these are disappointing results. Though as I’ve noted previously on PAS, you do have to expect ups and downs with equity-based investments. And over the last few months there’s been no lack of volatility in world markets, caused by rising inflation, the war in Ukraine and the aftermath of the pandemic (among other things).

It is, however, worth noting that since I started investing with Nutmeg in 2016, and despite everything that has happened this year, I have still made a total net return on capital of 28.79% (or 52.94% time-weighted).

While performance this year has clearly been disappointing, I have no doubt there will be an uptick at some stage, and am considering topping up now while asset values are low. I definitely don’t plan to sell up, as that would only crystallize my losses this year and leave me unable to take advantage when – as I fully expect – things turn around again.

I should also mention that I selected quite a high risk level for both my Nutmeg accounts (9/10 for the main one and 5/5 for Smart Alpha). This has served me well generally, but I’m sure investors who selected lower risk levels will have seen smaller falls over the last few months. If you also have a Nutmeg portfolio and plan to withdraw from it soon, there is certainly a good case for switching to a lower risk level now.

You can read my full Nutmeg review here (including a special offer at the end for PAS readers). If you are looking for a home for your annual ISA allowance, based on my experience over the last six years, they are certainly worth considering.

I talked about the performance of my Kuflink and Assetz Exchange investments in my June update and also in this recent blog post. I don’t therefore plan to provide in-depth reports about them on this occasion. I will just say that both are continuing to provide steady returns for me, with a lot less ‘excitement’ than my equity-based investments!

As I said a few weeks ago, in these turbulent times I believe P2P/crowdlending platforms such as the two mentioned are well worth considering. Not only are the rates of return higher than those on offer from banks and building societies, they are relatively unaffected by ups and downs in the stock markets. P2P loans aren’t a way of hedging your equity-based investments directly, but they do help spread the risk.

To be clear, nobody should put all their spare cash into Kuflink, Assetz Exchange or any other P2P/crowdlending platform, but in my view (and experience) they are certainly worth considering as part of a diversified portfolio.

My investment in European crowdlending platform Nibble (as mentioned last time) continues to perform as advertised. My latest investment was in their Legal Strategy. These are loans that are in default and facing legal action. Nibble buy these loans at a heavily discounted rate and then seek to recover as much as possible of the money owed. The minimum investment is 10 euros and the minimum period is six months. I invested 100 euros for 12 months initially at a target annual interest rate of 12.5%.

The Legal Strategy comes with a deposit-back guarantee. This is a guarantee to return the full investment amount at the end of the investment period and a minimum yield of 9% per year. The actual yield depends on how successful recovery efforts prove, so in practice you may end up with a return of anywhere between 9% and 14.5%. All has gone to plan so far, but I will obviously continue to report on this in the months ahead.

Also as mentioned last time, I also recently set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (about £412) copying an experienced eToro trader called Aukie. As of today my investment has fallen to $473, which I guess in the current circumstances isn’t too bad. In any event I am looking on this as a long-term investment so obviously won’t be judging it yet. I am also considering a further investment with eToro, possibly in one of their themed portfolios.

Moving on, I had another article published on the always-excellent Mouthy Money website. This one is titled Starting Your Own Business With a Franchise. If you harbour an ambition to be your own boss, a franchise can be a great way of achieving this. My article sets out some hints and tips for choosing the right opportunity and making the most of it.

Finally, I enjoyed a short break in Criccieth, North Wales, at the end of June. I won’t go into detail about this here, as I plan to write a separate blog post about it soon [now published}. But I will say it was a very enjoyable, relaxing holiday, and I definitely hope to return there before too long. I stayed in a lovely sea-front apartment about five minutes’ walk from Criccieth Castle. Here is a photo taken from the castle showing the main beach…

That’s all for today. As always, if you have any comments or queries, feel free to leave them below. I am always delighted to hear from PAS readers 🙂

If you enjoyed this post, please link to it on your own blog or social media:

There isn’t much doubt this year has been a challenging one for stock market investors.

The war in Ukraine, rising inflation, and lingering fallout from the pandemic have all conspired to damage investor confidence. As a result, what we’re seeing now is a bear market, with share values falling across the board. How long this will continue I don’t know, though one thing I can say for certain is that there will be an upswing sooner or later.

I have witnessed this with my own equity investments and it hasn’t been pretty. My Nutmeg Stocks and Shares ISA has fallen by 11% in value since January 2022. My Bestinvest SIPP (personal pension) has fallen by a roughly similar amount (I’ve suspended withdrawals from it as a result, to avert the risk of pound-cost ravaging). I’m not panicking about this, as all equity investments have their ups and downs. And since I started both of these investments, I am still well up overall.

There is indeed an argument that now could be a good time to invest, while asset values are depressed. Nonetheless, I do of course understand why many people are wary of investing in stocks and shares at the moment, as markets may well have further to fall.

So today I thought I’d talk about an alternative approach that has fallen out of favour in the last year or two, but still has the potential to generate good returns for your money even when stock markets are in turmoil.

P2P/Crowdlending

I am, of course, talking about P2P/crowdlending. A few years ago these platforms were being touted as an exciting new alternative to banks, allowing individuals the opportunity to club together to buy property or lend to people/businesses. Investors could then benefit from interest paid, rentals received and/or capital gains made.

While initially everything went well, Covid in particular put a big spoke in the P2P sector’s wheel. More borrowers went into default, and platforms struggled to stay afloat as a result. Some (e.g. The House Crowd and Lendy) went bust. Others (e.g. Zopa and Ratesetter) decided to withdraw from P2P lending. Still others (e.g. Bricklane and Crowdlords) continue to operate but have closed to new investors and begun a process of winding down.

While that might sound depressingly negative, it’s not all doom and gloom. A number of P2P/crowdlending platforms are still running and indeed thriving. Three I have investments with myself are Kuflink, Assetz Exchange and Property Partner.

Interestingly, these are all property investment platforms. Kuflink offers secured loans to property developers, while the other two are more ‘conventional’ property crowdfunding platforms where investors jointly purchase a property and share pro rata in rental received and any capital gains on sales. P2P platforms that lend directly to individuals and businesses without the security of property are a lot scarcer nowadays than they used to be.

Regular PAS readers will know I have money in all three platforms mentioned above and am still actively investing in two of them (I am gradually winding down my Property Partner portfolio, though I do still recommend them). One big attraction of property platforms is that investment outcomes are not directly linked to the performance of stock markets. Yes, where the economy is rocky, this might ultimately impact on some commercial properties. Overall, though, these platforms are much less affected by market fluctuations than equity-based investments. That means they can offer an attractive alternative at times (like now) of high volatility.

In this article I’d like to highlight my two current favourite P2P/crowdlending platforms, Kuflink and Assetz Exchange. I will say a word about each and explain why I am still enthusiastic about them and continue to invest with them.

Kuflink

Kuflink offers opportunities to invest in loans secured against property. These loans are typically made to developers who require short- to medium-term bridging finance, e.g. to complete a major property renovation project, before refinancing with a commercial mortgage. They offer three types of investment, as follows:

Select-Invest (individual loans)

Auto-Invest

Tax-free IFISA (Innovative Finance ISA)

Auto Invest and IFISAs both automatically invest your money across a number of loans and pay a fixed interest rate, typically between 5 and 7%. You can choose a 1-year, 3-year or 5-year term, and interest is paid annually. The Auto-Invest product is basically the same as the IFISA, but without the tax-free wrapper. Self-Invest loans can also be put in an IFISA, with most (not all) loans on the platform being eligible.

I have been investing with Kuflink for nearly five years now. My experiences have been entirely positive and my investments have been generating the promised returns. I started cautiously with them, but have gradually built up the amount I have invested. Although – like all property P2P platforms – they were adversely affected by the pandemic, they appear to have come through it strongly, with new loans now being added almost daily.

There have been no defaults so far on any of my loans, and Kuflink say on their website that to date nobody has lost a penny on their platform. I have experienced short delays with loans being repaid, but in such cases you continue to earn interest, of course.

Although Kuflink don’t pay the highest rates in P2P lending, I think the returns on offer are realistic and sustainable. The steady expansion of the platform seems to testify to this, as does the fact that they have received several industry awards. .

Kuflink are also highly rated on the independent TrustPilot website, with an average 4.7 out of 5 (‘Excellent’). At the time of writing 80% of reviewers award them the maximum five-star rating, which is among the highest figures I have seen for a financial services platform.

As with all P2P lending, your money doesn’t enjoy the same level of protection as bank and building society accounts, which are covered (up to £85,000) by the Financial Services Compensation Scheme. Nonetheless, the rates of return on offer are significantly better than those from most financial institutions. And the fact that all loans are secured against bricks and mortar – and Kuflink themselves have cash invested in them – clearly offers some reassurance.

From my experience, Self-Select loans tend to fill up quickly. On the positive side, this shows investors have confidence in Kuflink and want to invest through the platform. On the minus side, it means there are typically no more than two or three new loans open for investment at any time.