Many of us today do most of our shopping in supermarkets. Although of course it’s important to support local/specialist shops, supermarkets typically offer a much wider range of products at prices small stores find hard to match.

But there are still lots of ways savvy shoppers can save money on their supermarket shopping. Here are ten top tips to shave a few pounds (or more) off your shopping bills…

Make the Most of Loyalty Cards

All the big name supermarkets have these, though some (e.g. Morrisons) are switching from plastic to app-based cards. The benefits on offer vary, but typically you get points which can be exchanged for discounts and gifts. I shop mainly at Morrisons and Waitrose, as they have branches closest to me.

With Morrisons, their (now virtual) More card gives you special offers based on things you normally buy anyway. I have had some great discounts on my groceries with these offers, but you do of course need to remember to ‘swipe’ the app barcode at the checkout.

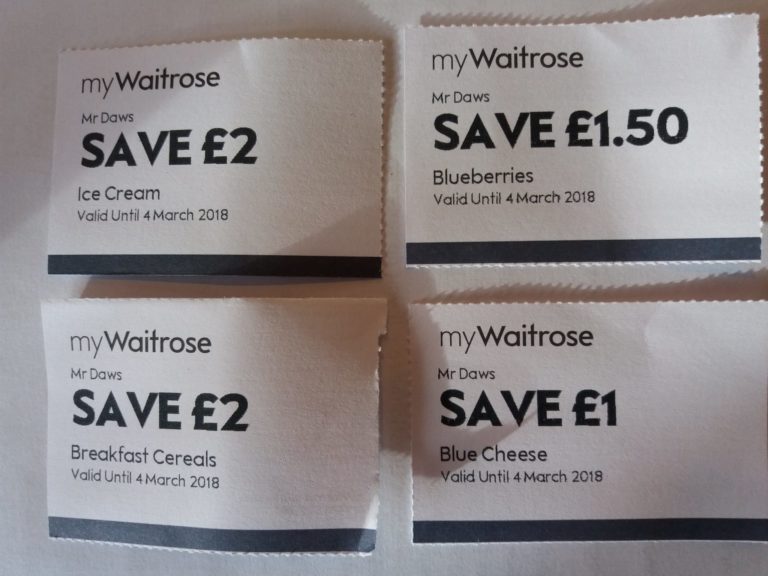

I also have a myWaitrose card. With this you can get a free newspaper with your shopping (subject to a £10 minimum spend). You can also get a free hot drink. You get vouchers sent in the post as well, such as the ones pictured below. It surprises me a bit when someone in the queue in front of me says they don’t have a myWaitrose card, but perhaps if they shop regularly at Waitrose they don’t have to worry too much about saving money 😉

Shop Late in the Day

Late in the day – ideally the hour before the store closes – is the best time to look for bargains. The shops will have stock they want to get rid of, probably because it is coming up to its ‘best before’ date. These items will often be marked down substantially, as the stores want to get at least some money for them rather than have to throw them away. Bear in mind that you can always freeze many foods if you can’t use them immediately – and in any event ‘best before’ dates aren’t set in stone.

Use Cashback Sites

I’ve talked about cashback sites like Quidco and Top Cashback on this blog before (e.g. in this post). If you shop online, you can get money back by clicking through to the retailer from the link on the cashback site. The most generous offers are generally reserved for new customers, e.g. on Top Cashback right now new Sainsbury’s online customers can get 16.5% cashback on Click and Collect orders of over £40. But even existing customers can get 5.5% cashback on Click and Collect orders of over £40 (all details correct at time of writing).

Plan Your Meals Ahead

We all lead busy lives these days. But it’s still good to devote some time to planning ahead where meals are concerned. Try to incorporate things you have in stock already, especially perishables which may not last more than a day or two. And rather than buying unusual/expensive ingredients for one dish only, see if you can find other recipes to use them up.

Batch cooking, where you make enough of a dish to last two days or more, is another great way to cut the cost of shopping. Of course, most dishes can be frozen if you can’t face having curry three days in a row!

Shop Online

Aside from the convenience of having goods delivered to your door, a big advantage of online shopping is that you will be less likely to succumb to impulse buys. Just make a list of what you need, visit the website, and add the items on your shopping list to your basket.

Admittedly you may have to pay a delivery fee, but many supermarkets now offer this free for new customers or for orders above a certain value. There are also in many cases ‘free delivery’ codes online if you search for them. And don’t forget to use cashback sites where possible as well (see above).

Search for Money Off Coupons and Vouchers

This is an old school method but it can still produce big savings. Look out for money-off vouchers in newspapers, magazines and the stores themselves. You can also search online if there are particular products you want to buy. This method can work particularly well with larger items such as dishwashers and tumble dryers [sponsored link], but it’s also worth searching for money-off vouchers for smaller/cheaper items, especially if they are things you buy regularly.

Try Own-Brand Products

All supermarkets have their own-brand products, and usually they cost less than heavily promoted consumer brands.

Many stores also have rock-bottom priced ‘Saver’ ranges. Sometimes these are not as good as more expensive branded or own-brand products. Other times, though, they are indistinguishable. For example, I now always buy Morrisons’ lowest-priced butter from their Savers range. I find it tastes just as good as the more expensive alternatives.

Use Discount Supermarkets and Stores

It’s easy to get in the habit of a weekly trip to Tesco or Sainsbury’s, but if you haven’t yet done so it’s well worth trying out discount supermarkets such as Iceland, Aldi and Lidl. They aren’t always the most attractive places to shop, but they make up for this with some amazingly low prices. Admittedly you won’t always recognize the brand names, but that doesn’t mean they aren’t high quality. Staples like bread, fruit and vegetables are often cheaper as well.

There are various apps and companies that will reward you for scanning and submitting your shopping receipts to them. One I’ve belonged to for some years now is ShopandScan. You can read more about this opportunity here.

ShopandScan pays in vouchers rather than cash, but the options include Amazon vouchers, which are of course nearly as good. I have received several thousand pounds worth of vouchers from ShopandScan since I started with them. As I say in my review, acceptance isn’t automatic, but if you apply there is every chance you will be sent an invitation within a few weeks.

Grow Your Own Food!

You can save significant sums of money by doing this. This summer I didn’t buy any tomatoes from July till mid-October, as I was eating ones I had grown myself. I highly recommend tomatoes, incidentally, not least as they are easy to grow in the garden, in a tub or hanging basket, or even on your window sill. They taste a lot better than most shop-bought varieties as well!

There are, of course, plenty of other things you can grow to save money, even if space is at a premium. Fresh herbs are one possibility, as are many types of berry (strawberries grow like weeds in my garden). I’ve also had some success with runner beans, courgettes and garlic, and salad vegetables such as chard, radishes and spring onions.

This year I also grew a pot of cut-and-come-again lettuce and was amazed by how much I got from this. It’s perfect for people who live alone like me, as you can just pick a few leaves when you want them, rather than buy a bag of salad leaves and have most of them go to waste.

I hope you’ve enjoyed this post and it has given you a few ideas for saving money on your supermarket shopping. If you have any other tips or comments, please do post them below!

If you enjoyed this post, please link to it on your own blog or social media:

Today I’m looking at a savings product that will be relevant mainly to the parents among you

A Junior ISA (sometimes abbreviated to JISA) is a savings product aimed at under-18s (and more specifically at their parents/guardians). These accounts allow money to be stashed away tax-free for a child until their 18th birthday. After this the money becomes the child’s to do with as they wish. The JISA account turns into an ordinary ISA at this time, thus retaining its tax-free status.

What Types of JISA are There?

There are two types of JISA: the Cash JISA and the Stocks and Shares JISA.

A Cash JISA is basically just a tax-free savings account. Interest is normally paid annually. According to the MoneySavingExpert website, the best-paying Cash JISA provider at the time of writing is Coventry Building Society, who are paying 4.95%. However, this is only available if you open an account in a branch or by post. If you want to open an account online, the best paying Cash JISA currently comes from Tesco Bank or NS&I, both paying 4%.

With a Stocks and Shares JISA, as the name indicates, the money is invested in the stock market. This offers the potential for greater returns, but with a higher degree of risk in the short term especially. I will say more about Stocks and Shares JISAs below.

As with adult ISAs, there is an annual limit to how much you can put into a Junior ISA. In the current (2024/25) tax year this is £9,000. You can put all of this into a Cash JISA or a Stocks and Shares JISA, or divide it between the two. You can switch providers as often as you like, but can only hold one of each type of JISA at any time.

Only a child’s parent or guardian can open a Junior ISA for them, but others including grandparents, friends, other relatives and the child him/herself can contribute. But it is important to be aware that (barring exceptional circumstances) all the money and interest in the account will be locked away until the child’s 18th birthday.

Which JISA is Best?

You won’t be surprised to hear that there is no simple answer to this.

If you want to avoid any risk of losing money, a Cash JISA is the way to go. Under the Financial Services Compensation Scheme (FSCS) the money will be completely safe so long as it’s invested with a UK-regulated provider and you have no more than £85,000 with that institution. Every year a known amount of interest will be added. The only risk you are taking is that the money won’t grow at the same rate as inflation.

On the other hand, if you are investing for at least a five-year period, there is certainly a case for putting at least some money into a Stocks and Shares JISA – and if it will be for ten years or more, the case becomes even more compelling. Over a five-year period stocks have outperformed cash in the great majority of such periods, and in almost all periods of ten years and over.

So if you are opening a JISA for a young child or infant, where the money may be invested for up to 18 years before it can be accessed, a Stocks and Shares ISA is very likely (though not guaranteed) to produce better returns than a Cash JISA. Of course, there is nothing to stop you hedging your bets and putting some money into one of each type.

What About Child Trust Funds?

Any child under the age of 18 born before January 2011 would have had a Child Trust Fund (CTF) opened for them by the government.

The government gave every child born between 1 September 2002 and 2 January 2011 a £250 voucher (£500 in the case of some low-income households). Parents could top up their child’s CTF themselves if they wished. The scheme ended in 2011 when CTFs were replaced by Junior ISAs. Unfortunately the government does not make a contribution towards these!

As with Junior ISAs, the money in a CTF could be placed in a Cash CTF or one where the money was invested in stocks and shares. Although new CTFs are no longer issued, there are many young people who still have one and will be able to access it on their 18th birthday. The first CTFs matured in September 2020, when the oldest account-holders turned 18. The last will mature in 2029. On maturity, a CTF can either be cashed in or transferred into an adult ISA.

Unfortunately the interest rates currently paid on Cash CTFs are generally very low indeed. So if your child has one, there may be a case for transferring it to a better-paying Junior ISA. Most JISA providers allow transfers from CTFs (or other JISAs), and it is certainly worth looking into this if your child has a low-interest-paying Cash CTF.

The Nutmeg Junior ISA

Regular readers of Pounds and Sense will know that I am a fan of of the Nutmeg investment platform and have a fairly large amount in an account with them. My money is invested in the form of a Stocks and Shares ISA. You can read more about this if you wish in my Nutmeg review or one of my regular investment updates such as this one.

Nutmeg do not offer a Cash JISA but they do offer a Stocks and Shares JISA. So if you are thinking of opening one of these for your child (maybe in addition to a Cash JISA) in my view they are well worth checking out.

With the Nutmeg Stocks and Shares JISA you have the same range of investment options as their adult ISA. These are discussed in detail in my Nutmeg review, but in brief they include Fully Managed, Smart Alpha, Socially Responsible and Fixed Allocation. My own investments are in the Fully Managed and Smart Alpha categories, and I am very happy with how both have been performing. But you should, of course, check the terms and conditions (and charges) carefully when deciding which is right for you.

Note that, unlike an adult ISA, in a Nutmeg JISA you cannot have different ‘pots’ within the same JISA wrapper. So you will need to pick your preferred option from one of the four mentioned, though you can change this any time later if you wish. You can also set a risk level between 1 and 10 and again you can change this at any time. You can read my recent blog post about Nutmeg risk levels here. My general advice, though, is that if you’re investing over a period of at least five years, it may pay not to be too cautious. In addition, if you choose to invest in a Nutmeg Junior ISA via my refer-a-friend link, you can get six months free of any charges.

Of course, Nutmeg are not the only providers of Junior ISAs. Some other possible options include Hargreaves Lansdown and BestInvest.

Closing Thoughts

If you are a parent or guardian, opening a Junior ISA is one of the best gifts you can give your child (or children).

The money will grow tax-free and can’t be touched until they are 18, when they can withdraw it or keep it as an ISA. It may provide a much-needed lump sum at a time when they are setting out in the world and really appreciate a financial leg-up. A JISA will also give them an early introduction to saving and investing, and form a valuable part of their financial education.

The main selling point of JISAs is, of course, their tax-free status. Admittedly this is not as big a deal with Cash JISAs as it used to be, as nowadays almost everyone has a tax-free Personal Savings Allowance of up to £1,000 and other tax-free allowances as well. As a result, interest on savings is usually paid without any deductions. So there may be no immediate tax advantage to investing in a Cash JISA if a non-JISA savings account pays better interest.

In the case of a Stocks and Shares JISA the tax-free status may be more significant, as it also gives exemption from dividend tax and capital gains tax (CGT) both of which have had their tax-free allowances slashed by the government.

Either way, though, money saved in a JISA will carry on growing tax-free forever (until it’s withdrawn) – so even if there is no immediate tax advantage, there may well be in years to come. This applies to an even greater extent if the young person stays invested on reaching maturity rather than immediately withdrawing all their money.

According to the This is Money website more parents open Cash JISAs than Stocks and Shares JISAs. As a money blogger, however, I would definitely think about opening a Stocks and Shares ISA for at least part of your child’s JISA allowance. That applies especially if it is more than ten years till their 18th birthday. As mentioned above, over almost any given ten-year period, stocks and shares have outperformed cash. And the longer timescale allows the inevitable ups and downs in the stock markets to even out. If you put all the money into a Cash JISA, by contrast, it is quite likely that the value of your child’s account will not keep up with inflation.

As always, if you have any comments or questions about this post, please do leave them below.

Disclaimer: I am not a registered financial adviser and nothing in this post should be construed as personal financial advice. Everyone’s circumstances are different and what is right for one person may not be appropriate for another. It is essential to do your own ‘due diligence’ before investing and seek help from a qualified financial services professional if in any doubt how best to proceed. All investing carries a risk of loss.

This post includes affiliate links. If you click through and make a purchase (or perform some other defined action) I may receive a fee for introducing you. This will not affect in any way the product or service you receive.

If you enjoyed this post, please link to it on your own blog or social media:

Today I am sharing some information about personal finance podcasts. This is not a subject I previously knew very much about, so I am grateful to my friends at All Finance Tax for supplying the excellent infographic and some of the other info below.

What is a Podcast?

A podcast is like a series of radio programmes on a particular theme or topic, from politics to cycling. You can subscribe for free using a suitable app on your smartphone (or other internet-enabled device). You can then listen whenever and wherever you like, via headphones, earphones, through speakers, in the car, on the train, and so on.

Podcasts are a booming medium and one of the major trends of the last five years. There are now podcast shows on nearly every topic you can think of. And with the rise of both independent and conglomerate podcast production studios, it seems likely this new medium will be in our lives for many years to come.

In the same way people were once passionate about certain radio shows, podcasts have the same dedicated followings, thanks to hosts who become familiar audio friends. Some even run live events. As a medium, podcasts are incredibly accessible, with few barriers beyond an internet connection and a smartphone or other device that can stream audio. No matter where you are or what you’re doing, podcasts offer content that educates, inspires and entertains. If you have never listened to a podcast before, the BBC Sounds podcasts page is one good place to start.

How to Listen to a Podcast

The easiest way to find and listen to podcasts is by using an app on your smartphone.

If you have an iPhone, it will have a built-in app called Apple Podcasts. This works very well and allows you to search for and subscribe to any of a huge range of podcasts. All you have to do then is open the app any time you want to listen and choose the episode you require.

Android owners can use the free Google Podcasts app. You can download this from the Google Play Store if you don’t have it already. It is not as user-friendly as the Apple app and doesn’t have as many features, but will certainly get you started. There are also other free or inexpensive apps you can download from Google Play such as the highly-rated Pocket Casts or Castbox.FM.

Finance Podcasts

One genre with a surprisingly large, dedicated listenership is finance. While to some that might sound a dry, unpromising subject, the podcast medium has enabled content to be reinvented with an unexpected, creative approach.

With hosts ranging from seasoned finance professionals to novice FIRE (financial independence) enthusiasts, podcasts allow people who would never previously have been interested in finance – or perhaps even have been intimidated by the topic – to access valuable information presented in an engaging, inclusive way.

All Finance Tax rounds up the top finance podcasts in the infographic guide below. Find out about the must-listen shows, including podcasts about:

Entrepreneurship

Billionaire case studies

Female-led finance

Personal and couples’ finance

Start-ups

And more!

With snapshots of real reviews plus the best episodes to start with, this resource will help you find the right show for your personal interests and needs regardless of your outlook on finance. Read on for the full list of finance podcasts to start your listening journey!

Many thanks again to my friends at All Finance Tax for their help with this article. I have listed below all the podcasts recommended in the infographic, with links to their homepages (or another website) where you can find out more. You can also listen to the podcasts on the web via these pages, though using an app on your smartphone (as discussed earlier) may be more convenient generally.

One more I would add is the Ask Martin Lewis podcast from BBC Radio Five Live. Martin is, of course, a well-known personal finance guru (and founder of the hugely popular MoneySavingExpert website). Although I can take or leave his TV shows, his podcasts are less gimmicky and include valuable, accessible advice on all aspects of personal finance (not including investing).

As always, if you have any comments or questions about this post, please do leave them below. I’d also love to hear about any personal finance podcasts not mentioned above which you enjoy and recommend!

If you enjoyed this post, please link to it on your own blog or social media:

Regular readers will know I’ve been posting ‘Coronavirus Crisis’ Updates since March 2020. These covered my investments and also more personal matters. You can read my August 2021 update here if you like

As I said in that update, since Freedom Day in England has now happened, with the scrapping of most restrictions, it no longer seems appropriate to go on publishing Coronavirus Crisis updates (though the virus hasn’t gone away, I know). So I shall now be publishing monthly investment-only updates, with more personal updates as and when seems appropriate.

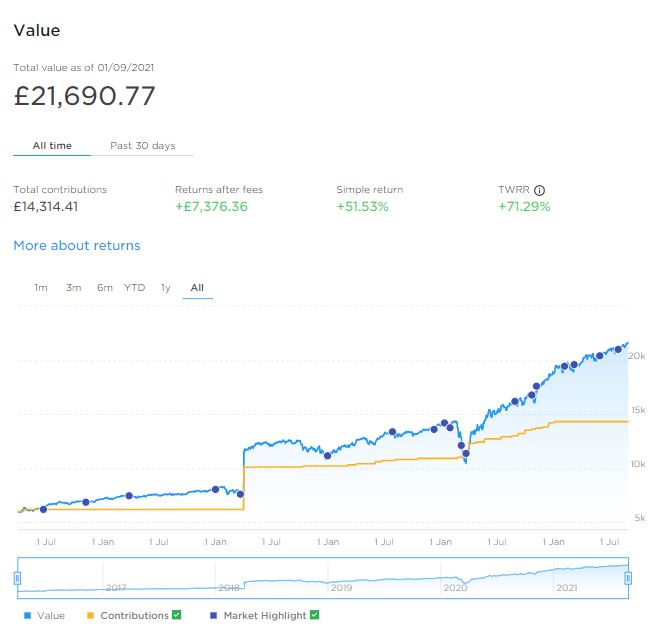

Let’s get straight on then. I’ll begin as usual with my Nutmeg stocks and shares ISA, as I know many of you like to hear what is happening with this.

As the screenshot below shows, my main portfolio performed well in August. It is currently valued at £21,690. Last month it stood at £21,015, so that is a rise of £675 (Nutmeg is now showing values including pence as well, but for simplicity I am not including this).

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s new Smart Alpha option. This pot also did well in August. It is now worth £2,710, compared with £2,625 last month. That’s an increase of £85 or just over 3%. Here is a screen capture showing performance in August 2021.

You can read my full Nutmeg review here (including a special offer at the end for PAS readers). If you are still looking for a home for your 2021/22 ISA allowance, based on my experience they are certainly worth considering. If you haven’t yet seen it, check out also my recent blog post in which I looked at the performance of Nutmeg fully managed portfolios at every risk level from 1 to 10 (my main port is level 9). I was actually amazed by the difference the risk level you choose makes.

You might also like to know that during September 2021 Nutmeg is running a special promotion on Junior ISAs (JISAS). If you open one of these for a child with Nutmeg (or transfer an existing Child Trust Fund) you will automatically be entered into a free prize draw to win £9,000 (this tax year’s full JISA allowance). For more information click on this link. I am also planning to write a blog post about this soon.

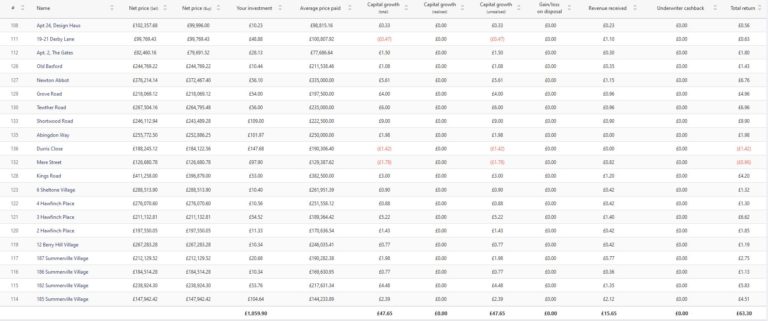

As regular readers will know, this year I am using Assetz Exchange for my IFISA. This is a P2P property investment platform that focuses on lower-risk properties (e.g. sheltered housing on long leases). I put £100 into this in mid-February and another £400 in April. Touch wood, everything has been going well, so in June I added another £500, bringing my total investment on the platform up to £1,000.

Since I opened my account, my portfolio has generated £15.65 in revenue from rental and £47.65 in capital growth, for a total return of £63.30. Here is my current statement:

To a degree Assetz Exchange has been a victim of its own success. They had a big influx of new members, meaning all available investments were quickly snapped up. At the same time, some of the new projects that were due to launch were delayed. In the last month, however, a small number of new projects went live on the platform, so I am pleased to say my £1,000 (and a bit more from dividends received) is now fully invested.

To control risk with all my property crowdfunding investments nowadays, I am investing relatively modest amounts in individual projects. I don’t therefore put more than around £100 into any one project. As you can see, I already have a well-diversified portfolio with Assetz Exchange comprising 21 different projects. This is a particular attraction of AE in my view. You can actually invest from as little as 80p per property if you really want to proceed cautiously.

Another property platform I have some investments with is Kuflink. They appear to have been doing well recently, with new projects launching almost every day on the platform.

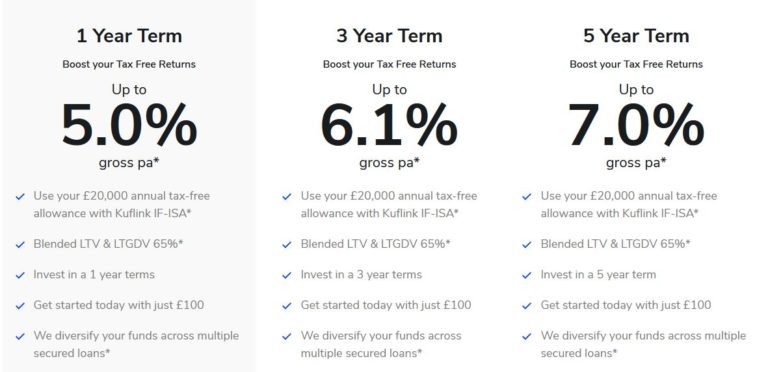

I have a well-diversified portfolio of loans with Kuflink paying annual interest rates of 6 to 7.5 percent. As mentioned above, these days I invest no more than around £100 per loan (and often less). That is not because of any issues with Kuflink but more to do with losses of larger amounts on other P2P property platforms (such as this one). My days of putting four-figure sums into any single property investment are definitely behind me now!

You can read my full Kuflink review here. They recently passed the milestone of £100 million loaned, and say that since their launch no investor has lost money with them. They offer a variety of investment options, including a tax-free IFISA paying up to 7% interest per year, with built-in automatic diversification. And I’d particularly draw your attention to their revised and more generous cashback offer for new investors. They are now paying cashback on new investments from as little as £500 (it used to be £1,000). And if you are looking to invest larger amounts, you can earn up to a maximum of £4,000 in cashback. That is one of the best cashback offers I have seen anywhere (though admittedly you will need to invest £100,000 or more to receive that!).

In August two more PAS readers signed up with the low-key sideline-earning opportunity mentioned in previous updates. They will have received their initial £100 reward payments about now. I still have a few more invitations available if anyone else would like to take advantage.

This opportunity is based on matched betting, a sideline I have been pursuing for several years myself. I was asked not to divulge too many details about it publicly, for good reasons I will explain privately to anyone who may be interested (and no, it’s not illegal!). It doesn’t require any financial outlay and is risk-free and entirely hands-off (once you have set up your account). No knowledge of betting is required and you don’t have to place any bets yourself (this is all done by the company’s clever software). You just have to set up a separate bank account for bets to go through, but running the account is entirely financed by the company.

The company has changed its terms somewhat for new members. You now get a larger £!00 initial reward payment once your account is up and running, and then £25 every month you remain a member. I think this is a good move personally, as setting up the account does involve a little work on your part (though it’s certainly not like going down the mines). So the £100 in effect compensates you for your time, and once it’s done you continue to get £25 a month for no effort at all. The company is constantly developing its offering, partly in response to feedback from PAS readers. They recently launched a new mobile-friendly website to make it even easier for new members to sign up (once you’re up and running you shouldn’t need to use the website at all). They also recently incorporated an Open Banking app so that members don’t have to provide their online banking info to the company, as some people were concerned about this.

Please note that this opportunity is only open to honest, trustworthy people who haven’t done matched betting before and have no more than two accounts already with online bookmakers. For more information (and to receive a no-obligation invitation) drop me a line including your email address via my Contact Me page. And yes, I will receive a reward for introducing you, but this will not affect the service or the rewards you receive.

In the interests of full transparency, I should say that if you do matched betting yourself, you may be able to make more money than what is being offered by the company. However, you will have to research the techniques in detail, place all bets yourself, and probably subscribe to a matched betting advisory service such as Profit Accumulator [affiliate link]. This opportunity is really for those who want an easy way to make some extra money without the hassle (or expense) of learning/applying matched-betting methods themselves.

Nobody would pretend life insurance is an exciting subject, but in these uncertain times it’s something we all need to think about at least. So in this post I thought I’d set out the basics regarding life insurance and why you might need it.

What Is Life Insurance?

Life insurance is a type of insurance policy that protects your loved ones financially if you die. It can help minimize the financial impact that your death could have on your family and provide peace of mind for you and them.

Most life insurance policies are designed to pay a cash sum to your loved ones if you die while covered by the policy. This can help them cope with everyday money worries such as mortgage payments, household bills and childcare costs. It may also cover funeral costs. You can take out life insurance under joint or single names, and you can pay your premiums monthly or annually.

There are two main types of life insurance: term life insurance and whole of life insurance.

Term life insurance policies run for a fixed period such as 10, 20 or 25 years. These types of policy only pay out if you die during the term of the policy. A whole-of-life insurance policy, on the other hand, pays out no matter when you die (as long as you keep up with your premium payments, of course).

There are three different types of term life insurance. With decreasing term insurance, the amount payable on death reduces over time. This type of policy is often taken out in conjunction with a mortgage as the payout reduces over time in line with the amount needed to clear the outstanding debt.

You can also get increasing term insurance, where the payout rises each year (typically to take account of inflation) and level term insurance, where it remains the same throughout. Not surprisingly, level term and (especially) increasing term policies are more expensive than decreasing term.

Over 50s Life Insurance

This type of whole-of-life insurance may be of particular interest to Pounds and Sense readers (PAS is particularly targeted at over 50s).

It allows you to leave a guaranteed fixed lump sum to your loved ones when you’re no longer around. To apply, you need to be aged 50 to 80 (85 in some cases) and a UK resident. No medical is normally required, and your monthly premium (which can be as low as £7) won’t change for as long as you live. In most cases cover for accidental death applies immediately, but for death from other causes there may be a waiting period (typically a year). This type of insurance is not normally index-linked, so over time the value of the lump sum payable may be eroded by inflation.

Who Needs Life Insurance?

Life insurance is intended to protect your dependants from getting into financial difficulties if you die. So if you’re single with no dependants and/or on a very low income, it may not be necessary or appropriate for you.

But if you have a partner, children or other relatives who depend on your income, you probably should have life insurance to help provide for them in the event of your death. Many people take out life insurance when they get married or start a family, or when taking on a major financial commitment such as a mortgage.

Most financial experts recommend you take out life insurance before you reach 35, as the sooner you get cover, the cheaper your premium.

What Doesn’t Life Insurance Cover?

Life insurance normally pays out only on death. If you become unable to work due to an accident or illness, you won’t generally be covered.

Some life insurance policies will pay out if you receive a terminal diagnosis. This is by no means always the case, though, so it’s important to check the wording of your policy carefully.

Most life insurance policies also have some exclusions, e.g. they might not pay out if you die from alcohol or drug abuse. In addition, if you take part in risky sports, you may have to pay a higher premium. If you have a serious health problem when you take out a policy, any cause of death related to that illness may be excluded.

For the above reasons, you may also want to consider taking out critical illness cover. This covers you if you get one of the medical conditions or injuries specified in the policy. Some examples of critical illnesses that might be covered include heart attack, stroke, cancer, and chronic, life-limiting conditions such as multiple sclerosis and MND. Most policies will also consider permanent disabilities as a result of injury or illness. These policies only pay out once and then the policy ends. Some policies will make a smaller payment for less severe conditions, or if one of your children contracts one of the specified conditions. Health conditions you knew you had before you took out the insurance won’t generally be covered.

What Does It Cost?

Life insurance can be surprisingly good value. Premiums start at just a few pounds a month. Prices vary a lot, however, so it’s important to shop around and take advice as appropriate.

A variety of factors may affect the price you are quoted. They include the following:

your age

your health

your weight

your occupation

your lifestyle

whether you smoke

your medical history

your family’s medical history

the length of the policy

the amount of money you want to cover

whether you want decreasing, level or increasing term cover

As mentioned above – and other things being equal – the younger you are, the cheaper your policy is likely to be. But as the list above indicates, many other factors can affect the price you are quoted. In addition, women are typically charged a little less than men, as on average they live a few years longer.

The Get Life Cover Option

As you can see, while life insurance is a simple concept, in practice there are many variations. It’s therefore important to establish what is the most appropriate choice for you and your family, and shop around to get the best price for this.

A company that can help with both these things is Get Life Cover. They will put you in touch with an independent financial adviser in your local area, not some anonymous call centre. The adviser will take the time to establish your exact requirements and recommend a bespoke policy tailored to your (and your family’s) needs. They will be able to arrange all types of life insurance, critical illness cover, cover for long-term illness or disability, and so on. Being independent they will also be able to select from the whole of the market. They are not tied to one insurance company, ensuring you get the best possible value for money.

If you wish, Get Life Cover’s independent advisers can also assist you with other financial matters, including investments, pensions, mortgages, tax, and so on.

To get an initial personalized quote, click through to the Get Life Cover website and provide a few basic details to get a quick quote in 30 seconds, without obligation. You can then discuss this with a local adviser to ensure you get exactly the right type and level of cover for your needs.

As always, if you have any comments or questions on this post, please do leave them below.

Disclosure: This is a sponsored post on behalf of Get Life Cover. If you click through one of the links and end up making a purchase, i will receive a commission for introducing you. This will not affect in any way the product or service you receive.

If you enjoyed this post, please link to it on your own blog or social media:

Today I have a (sponsored) guest post for you from my friends at Just Free Stuff.

They reveal some great ways you can get your hands on free and discounted baby products. Even though I know many PAS readers are beyond the age of having babies, many will have children (or grandchildren) who are now parents themselves. We all know having children is costly, so any help with saving money is always appreciated!

Over to Just Free Stuff then…

Looking for freebies is a growing trend in the UK and it’s easy to understand why.

Young mothers especially need help finding where and how to get the best baby free samples or other baby free stuff such as coupons, information, and so on. So, having been there ourselves, we decided to create this mini-guide, hoping you will enjoy it.

What Do We Mean by Free Baby Stuff?

Free baby stuff may include promo offers (e.g. get one and receive the second for free), money-off coupons, free samples or even information on where to go and buy baby products cheaply. The Internet is full of websites and blogs on this subject and it can become quite confusing. So we wrote this to give you a place to start.

Our Top Three Baby Freebie Sites

There are all sorts of freebie offers out there, some better than others, so we thought we should provide a short list of sites that include only the best. We will keep this updated when new offers arise, but right now you can check out our top three below.

Offer Oasis – This well-established website offers free samples and discount coupons. It also provides lots of valuable information on subjects related to the early months or years of a baby’s life, most-used products, etc. It also gives a helping hand through its online community of parents who discuss and advise or simply share their experiences, from which you can gain much free knowledge. Cherry on top: membership of this site is totally FREE.

Amazon Family – Amazon Prime members get access to this programme that offers a range of benefits to parents of babies and young children. They offer up to 20% discounts on most common baby products such as nappies and baby food, as well as up to 15% discounts on repeat deliveries. You do have to join Amazon Prime to get access to Amazon Family, but this brings many benefits in itself, including free, next-day delivery of many items.

Just Free Stuff – What could be the third option but our very own website? We post offers we find available in our BabyFree Samples category. You might want to come back and check out the newest additions to the list as they always appear on the top.

Why Do Companies Give Away Free Baby Stuff?

Free samples or promo offers for current or new products are a popular marketing strategy. Companies keep using them as they are known to be very effective. Why? Businesses need to create a loyal customer base. For this, they need customers to keep buying their products and not switch to competitors. So offering some products in special promos is a reward to customers for their loyalty and (hopefully) keeps them engaged with and enthusiastic about the company.

Also, new products are being developed every day and companies need customers to try them. So why not give away small quantities for free? A customer might think twice before spending money to try out a new product, as they may feel safer with products they have always used. But trying for free is something almost anyone would do. That is why there are always so many free samples and promo offers out there, and why there always will be. So do keep going back to check out the latest ones.

Many thanks to Free Stuff UK for sharing their tips and advice today. If you have any comments or questions – or other tips for saving money on baby products – please do share them below as usual.

Disclosure: this is a sponsored post for which I am receiving a fee.

If you enjoyed this post, please link to it on your own blog or social media:

Today I am pleased to bring you a guest post by Paul Green from Over50smoney. Paul is the founder and CEO of this popular website, which acts as a consumer champion for the over-50s.

Paul also has his own blog on Over50smoney, in which he mixes financial tips and guides with some personal pieces on subjects including sourdough bread making and growing his own fruit and vegetables!

In the article below (shared from his blog) Paul sets out some great tips for saving money that may particularly appeal to older people (though relevant to younger ones as well).

Over to Paul then…

My career has been spent helping people and businesses save money. With a business it makes sense to run operations efficiently as this enables investment to grow the business in the future. For individuals, saving money on everyday purchases is just the same. It enables you to save for the future. You can then spend the money you save however you like. This could be on holidays and enjoying life or maybe longer-term savings for your retirement. The choice is yours.

In this blog post I wanted to share five easy ways of saving money on everyday things that have worked for me. If you have other great tips that people over 50 could benefit from, please do share then below.

Don’t Take Out an Expensive Mobile Phone Contract

The smart phone has become a big part of most peoples lives. And this isn’t only the case for younger people. At Over50smoney about 80 percent of our website users visit the site with their mobile phones. However, those of us who wait in eager anticipation of upgrade time on our phone contracts are probably wasting hundreds of pounds. This used to include me until I realised how much money I was throwing away needlessly.

Let’s start by looking at why the standard type of pay monthly phone deal doesn’t make sense. The table below compares the latest Apple top of the range phone on a 24 month contact on the Vodaphone network against buying the phone upfront and getting the same data and minutes deal from Vodaphone on a SIM only deal. Taking out a phone contract is essentially the same as buying your mobile phone on Hire Purchase (HP). You have to pay for this. In the example below you are out of pocket to the tune of £250 over the course of a two-year deal.

You could also make buying your own phone and SIM even cheaper. If you shop around, you could get a significantly cheaper SIM deal depending on your needs. Keeping the same amount of data but giving up 5G capability can save money, but do you really use all your data anyway?

Comparison of a 24-month phone contract to buying your own phone

Phone contract

Get separately

Savings

Apple IPhone 12 Pro Max

£75 per month for 24 months = £1,800

Phone £1,099

Data £20 per month for 24 months = £480

Upfront payment

£29

£0

Total cost over 24 months

£1,829

£1,579

£250

*Data from Carphone Warehouse, Vodaphone and Apple, correct as at 31 May 2021

There are also cheaper SIM providers than the main networks so it’s worth considering providers like ID Mobile that uses the 3 network. The point is, if you buy your phone, you have more flexibility on the SIM deal you use.

Not everyone has a thousand pounds to buy a new top of the range phone outright. And in my opinion, this wouldn’t be the best option if you wanted to maximise savings on your smart phone anyway. Have a think about these ways of getting a good phone for less.

If you have a phone coming to the end of a contract why not keep it for another year? The build quality in modern phones is high, so unless you already have a problem with the phone, it’s likely to last for an additional year or two. It’s been a while since there were any real breakthroughs in phone design, so the extra benefits of upgrading are likely to be limited to things like a slightly more sophisticated camera. A friend of mine recently decided to keep his Samsung when he came to the end of his 24-month contract. He had been paying £65 per month during the contract term with O2. He wanted to stay with O2 so based on his usage he decided to move to an O2 SIM only deal and now pays £20 per month. As he stayed with the same provider, he didn’t even need to get a new SIM card. He now enjoys the same phone he really likes for £45 per month less than he was paying during the contract term.

If you want a new phone, it’s definitely worth looking at buying second hand. You can do this online or in many of the high street phone retailers. A quick Google search will show you several companies that specialise in selling high quality second-hand phones including WeSellTek [sponsored]. These will be wiped clean of previous owners’ data, refurbished and sanitized. You can get models that are currently being sold new for hundreds of pounds less. However, the biggest savings are usually on models that are just out of date. Given the pace at which the main manufacturers release new phones this probably means the phones are only a couple of years old and will have all the features and capabilities you want.

I’m not going to cover the pros and cons of moving to pay-as-you-go deals here. If you use your phone infrequently or usually have access to Wi-Fi this is something you could consider as additional cost savings are possible.

Double Savings With Amazon

Being someone who likes to shop local where I can, buying grocery items from Amazon initially went against the grain. However, financially it can make really good sense.

I first noticed this with a couple of items. We love coffee and a few years ago invested in a great, beans to cup, machine. This means we use a lot of coffee beans at home. Likewise, my wife makes amazing risotto. This is a staple on our menu once a week. Which means we also use a lot of arborio rice. Of course, we can pick up coffee beans and arborio rice from the supermarket, but they come in fairly small packets and we go through these pretty quickly. I discovered both coffee beans and arborio rice were available in big 1 kg sized packs from Amazon and that the price per KG is less buying these bigger packets than the smaller ones we used to get in store.

However, on top of the saving for buying bigger packets, if you use something regularly Amazon can give you additional savings. If you buy using Subscribe & Save you can control how often Amazon sends you a product. And, if you used less than normal it’s easy to delay an order so your cupboards don’t get too full. For most grocery items Subscribe and Save seems to offer a 10% price reduction initially that can increase to 15% with repeat orders over time. For some products the saving is lower, with a 5% initial reduction increasing to 10% over time.

So, I am now converted to getting some of my groceries from Amazon. The value is really good with both cheaper prices for bigger quantities and a Subscribe and Save discount on top of that. I also like the additional benefit of the products being delivered which means you don’t have to remember to put them on your shopping list and then carry them home!

Big Savings With Groupon

As the over-50s community is now well and truly online, I wanted to look at another couple of routes to savings when buying online. First up, Groupon.

Groupon has been around since 2008 and is based on the American love of coupons. The site works in the same way as cutting coupons out of a newspaper. You select an offer from the site, and read the small print so you understand things like the time period the offer is available for and how to claim it. Traditionally you had to print a voucher from Groupon, though nowadays that isn’t generally the case.

Groupon is easy to sign up for. You need an email address. It’s the most useful if you download the app to your phone or tablet as you can use the settings to get offer alerts close by when you are out. Groupon guarantees sellers a minimum number of customers. This means that they can create offers for the platform to drive sales when they need them. Groupon claim the typical discount on an offer on their site is the range of a 30-40% discount, although I have seen discounts stated as high as 90% and as low as 5%. Groupon earn a commission every time a customer takes an offer.

Groupon organises offers into different categories, making it easier to find what you want. The offers are updated all the time so if you can’t find what you want its worth coming back again. Different people I know use Groupon in different ways. For example, I have a friend who before the pandemic only bought toilet roll in bulk from Groupon (today, I have seen an offer of 120 rolls of Cusheen quilted luxury aloe vera toilet tissues for £17.50!). I’ve not typically used the site for “basics” but have found offers for services near where I live to be really useful. Again, before the pandemic when my wife and I went out with friends regularly, Groupon was a good source of mid-week deals on food in local pubs and restaurants.

So you understand why I like local deals on Groupon, these three are a selection from the recommendations near me as I write this post:

40% off a two-course meal for four people in a local fish restaurant. The price includes a glass of wine each and is reduced from £84 to £50. The offer is for Tuesdays, Wednesdays and Thursdays only, unless you book at least four weeks in advance when it also applies to Fridays;

60% off a spa day at a local hotel Mondays to Fridays or 56% off for Saturdays and Sundays. The offer for two people includes use of the spa facilities and hotel pool, Rasul mud treatment and lunch served with a glass of Prosecco. Mondays to Fridays the price is reduced from £201.90 to £79 or Saturdays and Sundays from £205.90 to £89. As it’s my wife’s birthday in couple of weeks this is an offer I may consider as it’s the type of experience she enjoys at a resort I know she likes;

The most interesting offer for me today is from a local chiropractor. Having hurt my back about a month ago lifting heavy pots in the garden I have put up with ongoing back ache. However, I will now book a visit for a chiropractic consultation and exam, which includes a report of findings and a treatment session. I haven’t been to this practice before, but it is offering a whopping 84% discount with the price reduced from £81 to £12.95. I wouldn’t have booked this at the full price but am happy to pay just under £13 to see if I can sort my ongoing backache out!

I think the two most important tips for using Groupon are to read the small print of the offers, especially availability in terms of dates or locations. Also, you do need to include the cost of postage when assessing an offer for goods. While the postage amount is specified on the site, for low value goods this can outweigh the savings from the offer.

Cashback Sites Offer Great Deals

I’ve written about cashback sites before and there is a range of content on the Over50smoney website about them. For example, they are mentioned on the short video here Revolutionise your finances – Part 2 (over50smoney.com).

You need to join a cashback site and because of the way they work this takes a little longer than signing up to Groupon. The two best cashback sites in the UK are TopCashback and Quidco. Both are well established, reputable businesses and free to join. Once you have signed up you can search the cashback offers available. If you select an offer, you will receive your goods or services and the appropriate cashback amount will be credited to your account. This can take a few weeks. Once the money is in your cashback account you will be able to transfer it into your bank account so long as you stay within the conditions of the site you are using. Transfers are usually straightforward. According to TopCashback members earn an average of £345 cashback a year. Retailers pay cashback sites a bonus based on volumes of sales. Cashback sites also earn revenue from sponsored adverts and promotions on their sites.

Cashback offers typically range from a few pounds for everyday products to hundreds of pounds for expensive items or ongoing services like energy or broadband deals. The important thing to remember with cashback sites is that while the offers can represent really good value for money you need to make sure you don’t get swayed just by the cashback amount. High cashback amounts can seem compelling but may be associated with high-cost products. You should be aware that many businesses use cashback sites to drive volumes when their prices may not be competitive. Always take a look online and see if the product or service you are thinking about is cheaper elsewhere when you include the cashback discount. If you have done your research and are confident that the cashback offer you have seen is a good overall deal, representing best value for money, it makes sense to purchase this way.

Both TopCashback and Quidco have a wide range of offers split into different categories including clothing, electricals, insurance, travel and so on. There are many offers in each category, so normally there will be a fair amount of choice if you want to make a purchase.

At the time of writing the following deals were available on TopCashback:

£210 off iPhone contracts with Tesco Mobile

£200 off energy with Scottish Power

Up to 8% discount on purchases from Marks & Spencer (different reductions depending on products purchased)

Up to 7% discount on purchases from ao.com (different reductions depending on products purchased)

3% discount on Lego

If you would buy online directly from a retailer it always makes sense to see if there is a discount available from a cashback site. For example, why send flowers from Marks & Spencer directly when you can save 8% buy buying through TopCashback?

Always Use the 30-Day Rule

As someone who used to be a spontaneous shopper, buying things I liked when I was out, the 30-Day Rule has been a godsend for me.

The 30-Day Rule goes like this:

If there is something you would like to buy, think about it for 30 days. If after that time you still want it, go and get it.

Putting this discipline in place stops you buying things you don’t really need or want. The ultimate waste of money is buying things you never use!

I think all of us have bought things on the spur of the moment because they seemed like a good idea, but ultimately, we didn’t really use them. Recently, I was talking to friends who were moving house. Their weakness was kitchen gadgets! They had cupboards full of things they were planning to give away before they moved. They had bought soup-makers, salad spinners, air fryers, rice cookers, etc, etc, that had seemed like a good idea but were ultimately only impulse buys. Bought, used once, and then forgotten about!

For me the 30-Day Rule has stopped this. Waiting 30 days gives me time to reflect on whether I really want something. I no longer waste money on things that I don’t use or enjoy.

Paul Green, 1 June 2021

Many thanks to Paul for an eye-opening guest post. I shall definitely be checking out Groupon more often in future! Do check out his blog on Over50smoney and the Over50smoney website itself.

I do strongly agree with Paul about the savings to be made through buying your mobile and SIM card separately. And there are some amazing deals out there right now. Personally I pay EE just £6 a month for a SIM-only deal with unlimited texts, unlimited voice calls and 5 GB a month of data. Okay, 5 GB might not be enough if you are out and about all day, but personally I’m nearly always within wifi range and don’t need that amount of data or anything like it.

Older people might also want to look into getting a big button mobile phone. These can be great for those whose eyesight isn’t what it once was and/or those with arthritis or similar who struggle to use the small buttons on modern mobiles. Click here for more information on big button mobile phones.

I am old enough to remember the days when mobile phone calls were so expensive you only made them when you really had to and kept calls as short as possible. How times have changed!

Release the Equity from Your Property

While 50 won’t cut it, the great news for homeowners over 55 is that you can use your property value while still retaining full ownership. So, if you’re not planning to move out any time soon and dream of retirement at home, then opting for a lifetime mortgage will provide you with up to 65% of your property value in tax-free cash.

You can receive your home equity as a lump sum, put it in a drawdown facility to release as you wish, or opt for a monthly salary lasting up to 25 years. What’s best is that the money can be used in any way you desire, and no repayments are necessary during your life.

Be warned that equity release can impact one’s access to means-tested benefits. Luckily, homeowners are required by Equity Release Council regulations to use a financial adviser to help with sound decision making throughout the process.

If you’re reading this post you will almost certainly know what an ISA is.

The term stands for Individual Savings Account. ISAs effectively serve as tax-free wrappers for various types of savings account. The two best-known types are the Cash ISA and the Stocks and Shares ISA.

You get an annual allowance for your ISA investments which currently stands at a generous £20,000 a year. Money saved in an ISA is permanently exempt from taxes such as income tax, dividends tax, capital gains tax, and so on.

So What Is An IFISA?

IFISAs are a lesser-known type of ISA that can be used for peer-to-peer (P2P) lending. They were launched in April 2016. After a slow start, the range available has grown steadily.

You can put any amount into an IFISA up to your annual ISA allowance. In the current 2021/22 tax year, as mentioned, this is £20,000. This can be divided however you choose between a cash ISA, a stocks and shares ISA, a Lifetime ISA (if eligible – you have to be under 40) and an IFISA. So, for example, you could invest £6,000 in a cash ISA, £10,000 in a stocks and shares ISA and £4,000 in an IFISA.

Note that under current rules you are only allowed to invest new money in one of each type of ISA in a tax year. It is though generally possible to transfer money from one type of ISA to another without it affecting your annual entitlement (although there may be platform fees to pay).

IFISAs vary considerably in the returns they offer. Annual rates range from from around 4% to 15%. Obviously, the higher rates reflect the higher levels of risk involved.

Although all IFISAs involve P2P lending, a number of different types are available. They may include lending for all the following purposes:

property development

business loans

personal loans

green energy projects

bonds and debentures

entertainment industry loans

infrastructure projects

What Are The Risks?

All UK IFISA providers have to be authorized by the Financial Conduct Authority (FCA) and HMRC. This doesn’t in itself protect lenders (or investors if you prefer) against the failure of a platform, however. While savers with UK banks and building societies are covered by the government’s Financial Services Compensation Scheme (FSCS), which guarantees to reimburse up to £85,000 of losses, this does not generally apply to IFISA platforms.

All IFISA providers do offer various safeguards, though. These vary, but include provision funds to cover potential losses, insurance policies, and so forth. In many cases loans are made against the security of property or other assets, which in the worst case could be sold to pay off any debts.

Even so, IFISA investors don’t enjoy the same level of protection in the UK as bank savers. This is, of course, a major reason why the returns on offer are significantly higher. It’s therefore important to be aware of the risks and ensure you are comfortable with them before investing this way. It’s also important to lend across a range of platforms and loans, and not make the mistake of putting all your savings eggs into one P2P lending basket.

What Are The Attractions?

So why might you want an IFISA? There are several reasons.

One is that they offer the potential of much higher rates of return that ordinary (bank) savings accounts. Even the best of these are currently paying interest rates of under 1 percent. IFISAs typically pay several times more than that (though obviously at somewhat greater risk).

Another big attraction of an IFISA is that it provides a way of gaining extra diversification for your portfolio. As mentioned earlier, the law currently only allows you to invest in one type of stocks and shares ISA per year. This rather perverse rule actually makes it harder to diversify your investments. But you can have an IFISA as well as a stocks and shares ISA, so long as you don’t exceed your total £20,000 allowance. So having an IFISA gives you a way of diversifying your investments while keeping them all protected within a tax-free ISA wrapper.

And finally, IFISA investments are typically not tied to the performance of stock markets in the way a stocks and shares ISA would be. This is a different type of investment, with different risks and rewards. While an IFISA won’t provide a way of hedging your equity investments directly, it is likely to be less directly affected by short-term fluctuations in the markets.

Two IFISA Examples

Two IFISAs of which I have direct experience are offered by Kuflink and Assetz Exchange. Both of these platforms offer tax-free IFISA options. They are both based around property investing.

Kuflink – which I reviewed in this post – offers an automatically diversified IFISA comprising loans on property. They quote interest rates from 5% to 7%, depending how long you invest for. Your money is automatically diversified across a range of secured loans. The screen capture below from the Kuflink website sets out the main features of their IFISA.

One point to be aware of is that there is no ‘self-select’ option with the Kuflink IFISA. So you have no choice about which projects your money is invested in. But, of course, it does make investing in a Kuflink IFISA very quick and simple.

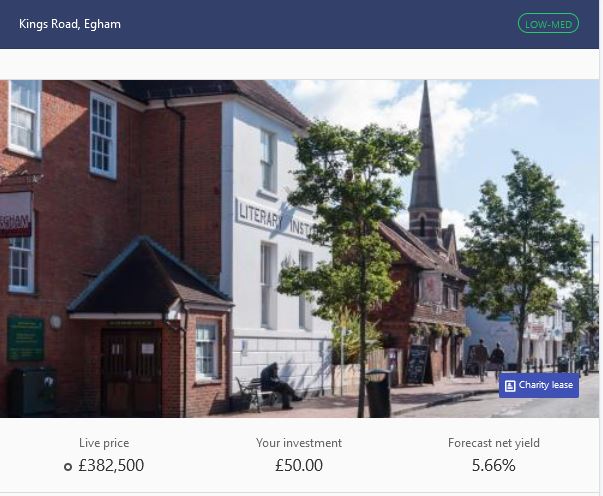

Assetz Exchange – which I reviewed in this post – has some similarities with Kuflink. But they concentrate on low-risk investments, typically with corporate clients (e.g. charities) on long leases. Here’s an example of the sort of investment I mean…

Assetz Exchange aims to offer net yields to investors of between 5.2 and 7.2% per year. One thing I especially like about them is that you can choose your own IFISA investments (indeed, they don’t currently offer an auto-select option). In addition, you can invest as little as 80 pence per project, making it easy to build a well-diversified portfolio even if you are only investing small amounts.

I am using Assetz Exchange for my 2021/22 IFISA, so here is a screen capture of my current portfolio for your interest. Note that while I have only invested £500 so far, I already have a well-diversified portfolio with 17 different investments!

Summing Up

If you are looking for a home for some of your savings that can offer better interest rates than banks and building societies and won’t incur any tax charges, an IFISA is certainly worth considering.

As well as the higher interest rates, they can add diversity to your investments, helping you ride out peaks and troughs in the financial markets.

Just be aware of the risks involved in P2P lending, diversify as widely as possible, and ensure you invest only as part of a well-balanced portfolio.

As always, if you have any comments or questions about this blog post, please do leave them below.

Disclaimer: I am not a registered financial adviser and nothing in this post should be construed as personal financial advice. You should always do your own ‘due diligence’ before investing, and speak to a professional financial adviser/planner if in any doubt before proceeding. All investments carry a risk of loss.

This post (and others on Pounds and Sense) includes my referral links. If you click through and make a qualifying transaction, I may receive a commission for introducing you. This will not affect the products or services you receive or any fees you may be charged.

If you enjoyed this post, please link to it on your own blog or social media:

Almost everyone loves getting something for free, and in this digital age it is easier than ever to get freebies. So why do so few people take advantage of the great opportunities on offer?

In some cases, people simply aren’t aware that such opportunities exist. However, the main reason for people not actively pursuing freebies is that they are suspicious of getting something for nothing – they believe that there is some sort of catch involved. Alternatively, they might assume that the freebies available are cheap, low quality or not worth the effort. Neither is necessarily true.

Whilst some freebies are undeniably low cost or in sample-size proportions, there are a lot of really great products and services available too. The trick is to identify what product niches you are specifically interested in, then target the offers accordingly. This can yield better results than scanning offer websites with no real intent, and is less labour-intensive if hunting for offers is not something you actively enjoy.

Where you should look for freebies will depend on what type of niche you are targeting. For example, if you are a parent looking for baby- or child-related items, simply signing up to a manufacturer’s website will sometimes result in freebies. Occasionally they may provide the items in exchange for consumer feedback or a product review. But often they will give away items for no other reason than to encourage brand loyalty.

Literature is another good niche to target if you love a free gift. Publishing companies are always looking for people, both adults and children, to review newly published books. You have complete control over which books are sent to you, and are only required to review those which truly interest you.

If your interests are broad and you are more motivated by the thrill of receiving something for nothing, there are many websites and forums where people will list opportunities for obtaining free goods and services. The most impressive freebies are normally offered in limited quantities or for a restricted time period, so you will need to check the listings regularly to get the best deals. Signing up for emails or downloading an app which will generate alerts can make the process easier.

Some of the best free products and experiences are available to those people who are willing to put in a little effort. In particular, mystery shopping can produce great results because the company is required to reimburse you for your time. Your assignment may involve a free experience, such as eating at a restaurant or visiting a local attraction, or visiting a specific store and getting financial recompense for shopping there.

However much free time you have, and whatever your interests, you will be able to find freebies which suit you. Companies frequently send out free samples in order to generate interest in their products, and often all you need to do is fill out your name and address. If you are willing to provide something in return such as a review or completing a short survey, the freebies you receive can be even more enticing.

Disclosure: This is a sponsored post on behalf of Free Stuff websites.

If you enjoyed this post, please link to it on your own blog or social media:

According to the Department for Business, Energy and Industrial Strategy (BEIS), there are now roughly a million homes in the UK with solar panels.

Mine is one of them. We had ours fitted in April 2011, just in time to benefit from the highest Feed-In Tariff (FIT) before the rate was slashed by over half.

I hadn’t really given the panels a lot of thought since then. I submitted meter readings every three months, and a few days later a handy, tax-free payment appeared in the bank account.

In March 2019, though, I had a couple of builders doing repairs to the woodwork around the eaves. This was an awkward job that involved having scaffolding put up. Anyway, one of the builders (a guy I have known for several years and trust) asked if I would like the panels cleaned while they were up there. “They’re filthy,” were his exact words.

He quoted me £60, which seemed a good price, and clearly it made sense to have the work done while they were there and the scaffolding was up. They gave the panels a thorough clean, using large sponges and buckets of warm water with washing-up liquid.

I was intrigued to see how much difference this would make to the amount of electricity the panels generated, so I downloaded a free program called Sunny Explorer that works with my solar PV system. It communicates with the inverter (the device that turns the electricity generated by the panels into usable power) via Bluetooth to show how much electricity your panels are producing. And, thankfully, it shows historical data going right back to when the panels were first installed.

Monitoring Solar Panel Performance

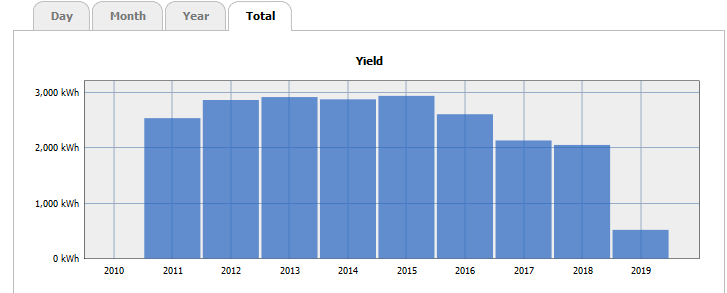

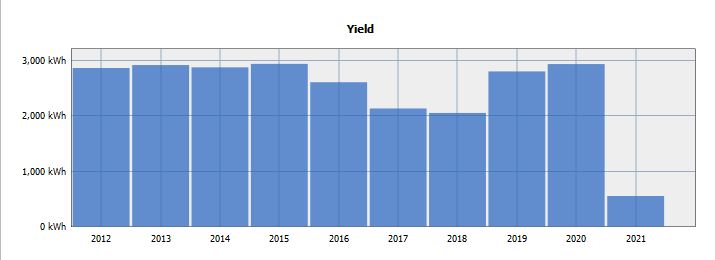

I found the data from Sunny Explorer genuinely eye-opening. First, take a look at this chart showing the total amount of electricity generated by my system year on year since the panels were installed.

As you can see (bearing in mind the panels weren’t installed till April 2011), for the first five years the total power output was pretty consistent. Then in 2016 and 2017 it dropped quite substantially, and again by a smaller amount in 2018, even though that summer was one of the hottest, driest on record. Obviously, if I was being scientific I would compare the total number of sunny days in each of those years, but I think it’s safe to assume that from 2016 onwards the build-up of dirt on the panels began reducing their efficiency.

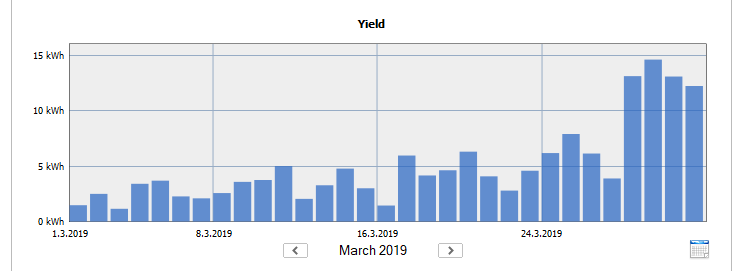

Now take a look at the monthly chart for March 2019. Can you guess what date the panels were cleaned?

Full marks if you said 27th March. The power generation was quite low that day as the panels weren’t cleaned until the afternoon, and obviously they had to be switched off while the cleaning was going on (the builders actually forgot to switch the system back on before they left, but I’ll forgive them that). Notice how much more power the panels generated in the last four days of the month, though.

2021 Update

Two years on, here is a chart showing how much electricity my panels have been producing year on year. Remember, they were cleaned in March 2019.

As you can see, in 2019 and 2020 my panels were back generating at the same level they had been prior to 2016. And neither of these years featured exceptional amounts of sunshine. Obviously as it’s only mid-April now the total figure for 2021 is lower, but from comparing the month-by-month figures from previous years it is clear that they are still working well.

If I hadn’t had the panels cleaned it’s likely that their electricity production would have continued at the 2018 level (and probably lower). As it was, in 2019 and 2020 they generated an extra 1,700 kwh compared to the 2018 level, worth about £850 to me in financial terms. So that £60 I paid to have them cleaned was a very good investment!

Overall, I think the lesson from this is that it’s well worth monitoring the performance of your panels, and having them cleaned if you notice it is declining. When our panels were installed we were told that they were ‘self cleaning’ due to the amount of rain we get in the UK, but that clearly wasn’t sufficient in my case anyway!

More Top Tips

I used the free Sunny Explorer software to monitor my system. This works with inverters made by SMA Solar Technology. If you have a different make of inverter it may not work for you, but there should be some other way to check your system’s performance. Ask your installer if in doubt.

If you have trees nearby (as I do) there will probably be more birds around, and over time their droppings are likely to build up on your panels and reduce their efficiency. While dust generally washes off with a good rain shower, bird droppings may not.

Before cleaning or inspecting solar PV panels, it is essential to switch them off via the main isolating switch (in my home it’s a bright red switch next to the solar power meter). Failing to do so could result in a severe electric shock.

If you cannot safely access your panels to clean them, hire a professional to do it. Don’t get up on the roof yourself unless you have the necessary training, expertise and equipment.

A good solution for cleaning solar panels that can avoid the need for going up on the roof is a water-fed pole with a soft brush, combined with a squeegee. Avoid using abrasive tools or products in case you scratch the glass.

Avoid cleaning your panels when the weather is hot, as spraying cold water on very hot panels could cause smearing or even damage them. Instead try to clean the panels in the morning or evening or on cooler days.

Based on my experience, it may not be necessary or cost-effective to clean your panels every year, but every three to five years could be a good strategy. In any event, monitoring the output of your panels will help you decide.

Good luck, and I hope your solar panels are soon working at peak efficiency again!

If you have any comments or questions about this post, as always, please feel free to post them below.

This is an update of my original 2019 post.

If you enjoyed this post, please link to it on your own blog or social media: