Sadly scams of all kinds are on the rise at the moment, with older people especially vulnerable to them. Read on for some top tips on how to spot attempted scams and keep your money safe.

Scams are a growing problem in the UK, with millions of people being taken advantage of each year.

From fake investment schemes to phishing e-mails, scammers are constantly finding new ways to trick unsuspecting individuals into giving away their money or personal information. The financial impact of scams can be devastating, leaving victims with empty bank accounts and a damaged credit rating.

Over 12% of UK consumers have fallen victim to payment fraud over the past four years, with an estimated £1.2 billion lost to scams in 2021 alone. With so many people having their savings impacted by fraud, it’s crucial to know how to protect yourself.

This article will set out four practical ways to prevent scams from reducing your savings.

Be cautious of unsolicited phone calls, e-mails and text messages

Scammers often use the promise of quick and easy money to lure people into their schemes. They do this through unsolicited phone calls, e-mails and text messages. Elderly people are particularly vulnerable to these monetary scams as they may not have the same level of technological literacy to spot one. However, anyone can easily fall into this trap as scamming methods grow increasingly sophisticated.

To protect your savings, you must not disclose your personal or financial information if you receive suspicious communication. You can also report dubious messages to the Information Commissioner’s Office, which has the power to take enforcement action against those involved in the scam.

Use strong passwords and security features

The government’s Cyber Aware campaign was launched in 2021 in response to growing scam and cybercrime incidents in the UK. One central piece of advice from the campaign is to use strong passwords and security features to prevent scammers from gaining access to your bank accounts.

For example, you can use a combination of letters, numbers and symbols on passwords to make them difficult to crack. Two-factor authentication provides another layer of protection by requiring a second form of verification in addition to your password. These two measures can significantly reduce your risk of falling victim to a scam that can empty your savings accounts.

Familiarise yourself with the technology used by merchants

As technology continues to evolve in the UK, so do the methods scammers use to steal your hard-earned savings. One way to protect yourself is to understand the methods used by merchants for their transactions.

Case in point, mobile card machines are commonly used by restaurants, cafés and pubs to process payments on the go. These devices are held to compliance standards like the Payment Card Industry Data Security Standard or PCI-DSS, which ensures that the machine follows protocols to protect cardholder data. Similarly, online merchants use virtual payment terminals to process payments online. Because shopping fraud schemes are on the rise in the UK, familiarising yourself with the technology merchants use can ensure you only interact with trusted businesses to keep your savings safe.

Choose banks with comprehensive fraud protection

In the UK, many banks offer fraud protection services as a standard feature. However, it’s still important to do your research and check that the bank holding your savings has the necessary fraud protection measures.

The Financial Ombudsman Service website offers resources regarding local banks’ anti-fraud policies. Additionally, you can check for your bank’s participation in the ‘Confirmation of Payee’ scheme. This initiative aims to protect customers from Authorised Push Payment scams, a type of fraud that tricks consumers into making a payment to a scammer. Banks participating in this scheme can check the recipient’s name against the account details provided by the customer and ensure the money is being sent to the correct person.

Scams can have a devastating impact on your savings—the fruit of your hard work. By taking the preventative measures outlined in this article, you can be vigilant and reduce your risk of being conned by one.

As always, if you have any comments or questions about this article, please do leave them below.

This is a collaborative post.

If you enjoyed this post, please link to it on your own blog or social media:

Regular readers will know that I joined the online trading and investment platform eToro earlier this year and have become a fan of it.

You can purchase a wide range of investment products on eToro, including individual company shares, ETFs, commodities, cryptocurrencies, thematic portfolios, and so on. You can also avail yourself of their popular copy trading facility, where you sign up to automatically copy the trades of an experienced (and hopefully successful!) eToro investor.

My own investments on eToro now comprise a thematic portfolio, a copy-trading portfolio, and a few shares in Tesla (basically because I had a spare $20 burning a hole in my account!). I will write more about thematic portfolios in a future post. Today, though, I want to talk about eToro Money.

What is eToro Money?

eToro Money is a recently-launched e-money account for eToro investors. It can be managed via a mobile phone app. It is free to set up and there are no ongoing charges.

The key attraction of eToro Money is that it allows you to deposit to your eToro investment account without paying the usual currency conversion fee. This can save you up to £5 per £1,000 compared with depositing directly to eToro using a bank debit card.

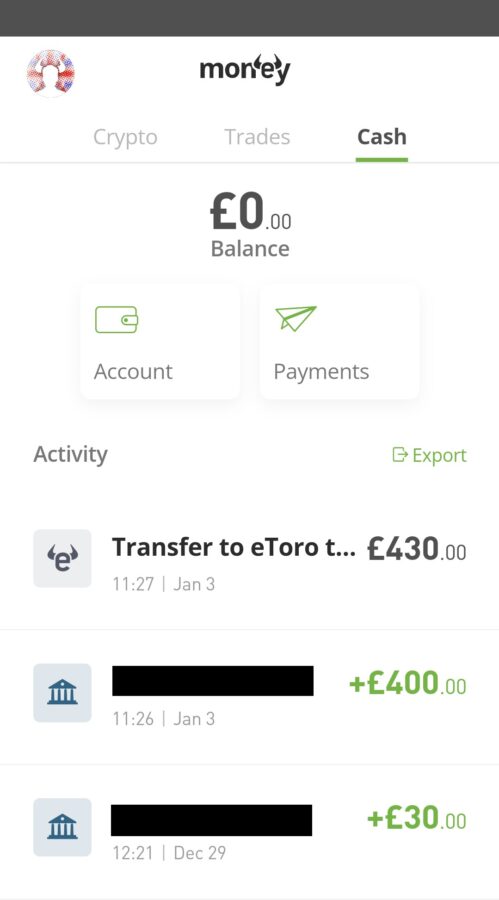

Essentially what happens is that you deposit to your eToro Money account with your bank debit card using the account details provided. This money then appears instantly in your eToro Money account and you can use it to invest on anything on eToro when you are ready.

When I tried this myself, I was impressed by how straightforward the process was, and in particular the speed with which the money showed up in my account (it really did seem to appear instantly). Using it to invest on the eToro platform was then straightforward. Of course, eToro operates in US Dollars, so I worked out in advance roughly how much I would need to deposit in GB pounds to get the $500 I was aiming to invest (I transferred £430 in total to be on the safe side). The money was then converted at a fair rate with no fees or charges. You can see these transactions listed in the screen capture of the app on my phone below. I have redacted my account name for security reasons.

You can also use eToro Money to withdraw funds from your eToro account. I haven’t tried this yet, but again eToro promise that the process is instant and I have no reason to doubt that. There are modest fees for withdrawing from eToro and you will still have to pay them, but having an eToro Money account keeps costs as low as possible. As I noted in my original review, eToro’s fees are very reasonable and they don’t generally impose any transaction charges.

Other Features

As well as managing your main (‘fiat’) currency in eToro Money, you can also securely store, send and receive most popular cryptocurrencies. eToro Money incorporates the functionality of the previous eToro Wallet app for cryptocurrencies, while offering additional features as well.

You can also use your eToro Money account to send money to and receive money from friends and family, set up direct debits, manage your household expenses, and so forth.

The eToro Money Debit Card

This is a further benefit of eToro Money some may wish to take advantage of. It is a debit card linked to your eToro Money account which you can use in the same way as a bank debit card to fund purchases, exchange currencies, and so on. They claim to offer market leading exchange rates across the globe.

To qualify for an eToro Money debit card, you must be a member of the eToro Club. Anyone with over $5,000 in realised equity on eToro is eligible for this. Realised equity in this context means the combined value of the available funds in your eToro account plus the original amount invested in all your holdings. So if you have $1,000 in cash in your account and have invested $4,000 in shares and other investments on the platform, you will have $5,000 in realised equity and qualify for a free eToro Money debit card if you want one.

Closing Thoughts

For most users the primary benefit of an eToro Money account will be to eliminate the currency conversion fee when depositing on eToro. It also speeds up the process of depositing to the platform and withdrawing from it.

While eToro Money is not a fully-fledged online banking service, you can also use it to send payments and/or set up direct debits. In that respect, it is a bit like PayPal. Though you will need to know the sort code and account number of the person or business you want to pay. An email address alone (as with PayPal) won’t cut it!

As mentioned above, if you have $5,000 or more in realised equity on eToro you are also entitled to an Etoro Money debit card if you wish. You can read more about this on the eToro Money website.

Overall, I think anyone who plans to invest via eToro should seriously consider opening an eToro Money account to reduce costs and speed up depositing and withdrawing. They will obviously then have the opportunity to take advantage of the other benefits too.

To set up an eToro Money account, the best option is to download the eToro Money app from Google Play (Android) or the App Store (Apple) and follow the instructions in the app. Obviously you should have an account on eToro already in order to use eToro Money.

If you have any questions or comments about this post, as always, please do leave them below.

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts on Pounds and Sense may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered.

If you enjoyed this post, please link to it on your own blog or social media:

As is customary for bloggers at this time of year, here are the top twenty posts on Pounds and Sense in 2022, based on comments, page-views and social media shares. They are in no particular order. I have excluded any posts that are no longer relevant.

I hope you will enjoy revisiting these posts, or seeing them for the first time if you are new to PAS.

All posts in the list below should open in a new tab/window when you click on the link concerned.

I’ll be taking a break from blogging over the festive period (though I’ll still be around on Twitter and Facebook). I’ll therefore close by wishing you a Very Merry Christmas (strikes and cost-of-living crisis permitting) and for all of us a much better new year 🍾

If you have any comments or questions, of course, feel free to leave them below as usual.

If you enjoyed this post, please link to it on your own blog or social media:

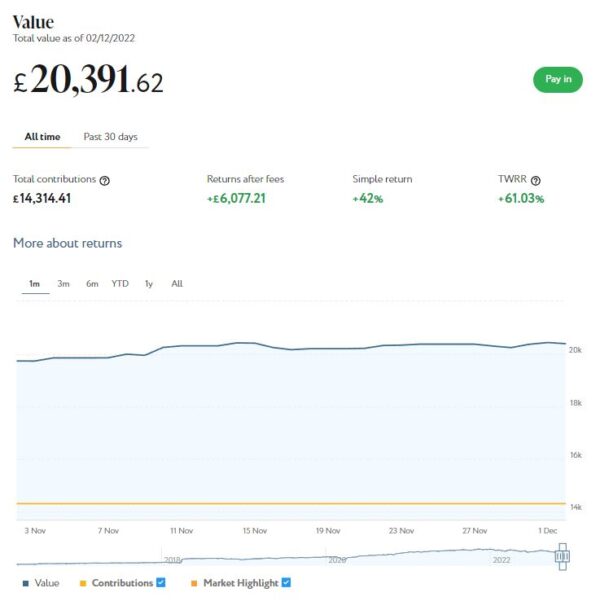

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension). I will discuss the latter a bit further down.

As the screenshot below of performance last month shows, my main Nutmeg portfolio is currently valued at £20,391. Last month it stood at £19,733 so that is a rise of £658.

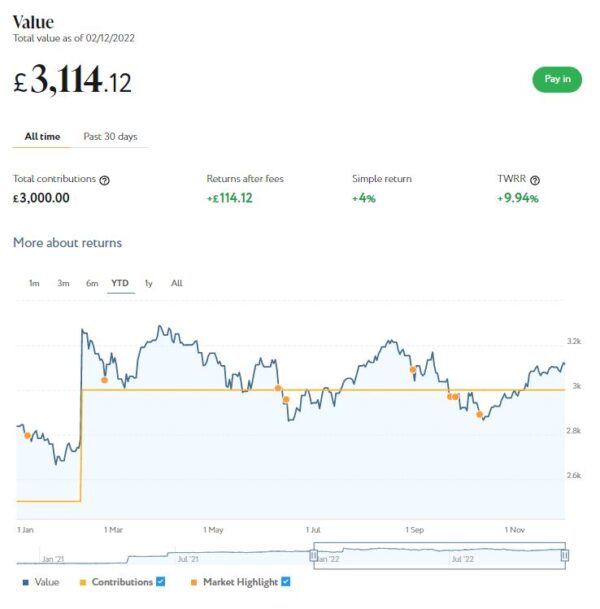

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £3,114 compared with £2,987 a month ago, an increase of £127.

Here is a screen capture showing performance since January 2022. As you can see, I topped up this account in February this year.

That is an overall month-on-month increase of £785. Furthermore since mid-October the total value of my Nutmeg investments has risen by £2,007 or around 8%. Anyone who was brave enough to invest in Nutmeg around the middle of October will therefore be looking at a substantial profit now. Of course, it’s always easy to spot an investment opportunity with 20/20 hindsight!

In my case, while the recent rises are very welcome, my Nutmeg investments are still down £1,607 or about 6.5% since the start of the year. To put this in context, though, in 2021 they rose by £3,552 (over 21%). And overall, I am still over £6,000 ahead since I started investing with Nutmeg in 2016. For my main portfolio that represents a return on capital of 42% or 51.03% time-weighted.

Of course, the real point of this is that investing is (or should be) a long-term endeavour. Over a period of years stock market investments such as those used by Nutmeg typically produce better returns than cash accounts, often by substantial margins. But there are never any guarantees, and in in the short to medium term at least, losses are always possible.

You can read my full Nutmeg review here (including a special offer at the end for PAS readers). If you are looking for a home for your annual ISA allowance, based on my experience over the last six years, they are certainly worth considering.

Moving on, my Assetz Exchange investments continue to perform well. Regular readers will know that this is a P2P property investment platform focusing on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my AE portfolio has generated £88.30 in revenue from rental and £17.59 in capital growth, a total of £105.89. That’s a decent rate of return on my £1,000 investment and does illustrate the value of P2P property investment for diversifying your portfolio when equity markets are volatile.

I now have investments in 23 different projects and all are performing as expected, generating rental income and in most cases showing a profit on capital as well. So I am very happy with how this investment has been doing. And it doesn’t hurt that most projects are socially beneficial as well.

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of AE as far as i am concerned. You can actually invest from as little as 80p per property if you really want to proceed cautiously.

Another property platform I have investments with is Kuflink. They continue to do well, with new projects launching almost every day. I currently have around £2,600 invested with them in 14 different projects. To date I have never lost any money with Kuflink, though some loan terms have been extended once or twice. On the plus side, when this happens additional interest is paid for the period in question. At present most of my Kuflink loans are performing to schedule, though two recently had their repayment dates put back by three months.

My loans with Kuflink pay annual interest rates of 6 to 7.5 percent. These days I invest no more than £200 per loan (and often less). That is not because of any issues with Kuflink but more to do with losses of larger amounts on other P2P property platforms in the past. My days of putting four-figure sums into any single property investment are behind me now!

Nowadays I mainly opt to reinvest the monthly repayments I receive from Kuflink, which has the effect of boosting the percentage rate of return on the projects in question

Obviously a possible drawback with Kuflink and similar platforms is that your money is tied up in bricks and mortar, so not as easily accessible as cash savings or even (to some extent) shares. They do, however, have a secondary market on which you can offer any loan part for sale (as long as the loan in question is performing and not in arrears). Clearly that does depend on someone else wanting to buy it, but my experience has been that any loan parts offered are typically snapped up very quickly. So if an urgent need arises, withdrawing your money (or part of it) is unlikely to be an issue.

You can read my full Kuflink review here. They offer a variety of investment options, including a tax-free IFISA paying up to 7% interest per year with built-in automatic diversification. Alternatively you can now build your own IFISA, with most loans on the platform (including the one shown above) being IFISA-eligible.

My investment in European crowdlending platform Nibble continues to perform as advertised. My latest investment was in their Legal Strategy. These are loans that are in default and facing legal action. Nibble buy these loans at a heavily discounted rate and then seek to recover as much as possible of the money owed. The minimum investment is 10 euros and the minimum period is six months. I invested 100 euros for 12 months initially at a target annual interest rate of 12.5%.

The Legal Strategy comes with a deposit-back guarantee. This is a guarantee to return the full investment amount at the end of the investment period and a minimum yield of 9% per year. The actual yield depends on how successful recovery efforts prove, so in practice you may end up with a return of anywhere between 9% and 14.5%. All has gone to plan so far, but I will obviously continue to report on this in the months ahead.

Earlier this year I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest). My investment has been up and down in the last few months, but it is currently $38 (about £31) in profit. In these turbulent times I am quite happy with that.

In any event, I’m looking on this as a long-term investment so won’t be judging it yet. I am also considering a further investment with eToro, possibly in one of their themed portfolios. You can read my full review of eToro here. You may also like to check out my recent more in-depth look at eToro copy trading.

Moving on, earlier I mentioned my Bestinvest SIPP (personal pension). This is now in drawdown, but regular readers will know that I suspended withdrawals from it in May this year to reduce the risk of pound-cost ravaging. I was able to do this because since December 2021 I have been receiving the state pension. And in association with my other income streams this has given me enough to live on (though by no means in luxury).

Anyway, with the cost of living crisis starting to bite, and energy bills shooting up at an alarming rate, I decided the time had come to resume taking payments from my SIPP. Plus, with the markets seemingly on an upward trajectory, the risk of pound-cost ravaging appeared to have receded.

I therefore asked Bestinvest to reinstate my payments from this month, though at a lower rate of £100 a month. One of the attractions of flexible drawdown pensions such as those from Bestinvest is that you can increase or decrease withdrawals at any time or even (as I did) suspend them completely. Obviously if you draw an excessive amount there is a risk of depleting your fund too quickly, so it runs out before you do. But Bestinvest sent me some reassuring projections that in any feasible scenario this was unlikely to happen in my case even if I live to the age of 99 (as I fully intend to 😀 ).

One other consideration I had with my SIPP is that withdrawals from it are taxable, whereas withdrawals from some of my other investments (e.g. Nutmeg ISA) are not. With the state pension also being taxable, this means withdrawing larger amounts from my SIPP would result in a portion of the money being grabbed by the taxman, which seems a waste. While I do of course accept that taxes have to be paid, I prefer to minimize my liability as much as possible (which we are all perfectly entitled to do).

I had two more articles published in November on the always-excellent Mouthy Money website. One of them was Win Fame and (Maybe) Fortune as a Quiz Show Contestant. This is something I have done myself in the past and enjoyed writing about again for MM. It can be a lot of fun, and any prizes you win are tax-free under UK law.

My other article was How to Cash in on Your Old Tech. Most of us have old technology we no longer use gathering dust in cupboards and drawers. This articles sets out ways you can make some much-needed cash out of this.

Obviously energy bills are a particular concern for many people at the moment, so I hope you are getting all the help you are entitled to. Everyone should be receiving a monthly rebate of £66 on their energy bill (going up to £67 in the new year). If you’re not, chase it up with your energy supplier.

I also recently updated my post about the Warm Home Discount, which this year is being increased from £140 to £150. The eligibility rules are changing somewhat, and I shall probably be one of the people who misses out, which is clearly disappointing. But on the plus side, most people won’t now have to apply for this benefit – if you are eligible, it should be applied automatically to your bill by your energy company.

The government’s Help for Households website has a helpful summary of all the financial assistance currently available and is regularly updated.

Please do check out as well some of the other posts on Pounds and Sense for advice and resources, especially in the Making Money and Saving Money categories.

Don’t forget, also, that there are currently two opportunities to claim a free share available. One is with Wealthyhood and the other with Trading 212 (the links will take you to the relevant blog posts). The current Trading 212 offer closes on 29 December 2022, so don’t delay if you want to take advantage of this one. As far as I know the Wealthyhood offer is open indefinitely, but that could always change, of course

That’s all for today. I hope you and your family are coping in these challenging times and wish you the happiest Christmas possible. I shall of course continue to update this blog over the coming weeks, and will return with a further update about my investments at the start of January.

As always, if you have any comments or queries, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media:

I’ve mentioned several times on PAS why I believe having an independent financial adviser makes sense, even if – like me – you consider yourself reasonably money-savvy.

So today I thought I would set out some reasons over-50s (in particular) may benefit from having an independent financial adviser (IFA) or at least speaking to one.

This post has been created in association with my colleagues at Unbiased.co.uk, a well-established financial services website that can put you in touch with suitable IFAs in your area.

Reasons for Having an IFA

1. Helping Your Children Through College or University

If you have children, you will naturally want to help them complete their education safely and with a reasonable degree of comfort. Sadly the days of student grants (which I was lucky enough to benefit from in the 1970s) are well behind us now. There are various options for helping finance your children’s college or university education and a financial adviser will be able to explore these with you. They will also explain the pros and cons of the student loans system.

2 – Pension Planning

If you are over 50 you will inevitably be thinking about pension options, including when you can retire and how much income you can expect. An IFA will go through your finances with you and look at ways you may be able to boost your pension pot. From 55 onwards you can normally start to draw your pension, but you shouldn’t do this unless a financial adviser has assured you it will last you through retirement.

3. Investing

Hopefully by your fifties you will be earning a decent salary and may also have paid off your mortgage. You may also receive an inheritance or other windfall. Either way, if you find yourself with some spare cash you will want to invest it to get the best possible returns from it. An IFA will have access to all the latest information about a vast range of investment opportunities. They will guide you towards investments that are suitable for you based on your financial goals, your investment timeframe and your appetite for risk.

4. Starting Your Own Business

Especially at this time of upheaval due to Covid, many people are looking to start their own businesses in mid-life. That may be in response to redundancy or unemployment, or simply in search of a better work/life balance. An IFA can help you with the financial aspects of doing this, including raising money for tools, premises, transport and so on, or perhaps buying a franchise.

5. Emigrating or Retiring Abroad

Another way to revitalize your life may be to start afresh somewhere else, with new challenges and opportunities (and perhaps a better climate as well!). Or you may be looking to move to a favourite vacation destination to enjoy your retirement. Either way, an IFA will be happy to discuss the pros and cons with you, point out all the things you will need to take into account, and assist you with the financial arrangements.

6. Divorce

Sadly middle age sees the largest number of divorces. Your first priority here will be appointing a good solicitor to act on your behalf and protect your interests. Beyond that, though, divorce can have major ramifications for your finances. An IFA can help you assess your situation objectively and plan for a financially secure and stable future.

7. Downsizing

As the children grow up and leave home you may want to move to a smaller property – to make life simpler, save time on housework and free up money for more exciting things. An IFA can help you explore the implications of doing this and make the necessary financial arrangements.

8. Equity Release

If you don’t want to move – and are over 55 – equity release is another option for releasing funds. In recent years it has grown a lot in popularity. There are various possibilities, including home reversion plans and flexible lifetime mortgages. Most now come with a no-negative-equity guarantee, ensuring you won’t end up passing on debts to your next of kin. An IFA can go over the options with you and point out the pros and cons before you contact any providers.

9. Estate Planning

This obviously includes writing your will, but depending on your circumstances it can cover a lot of other things as well. Nobody wants to see all their money and assets falling into the hands of the taxman rather than going to their nearest and dearest. Speaking to an IFA who specializes in estate planning can give peace of mind and ensure that your loved ones are well provided for when you are no longer here yourself.

10. Helping Elderly Relatives

If you have elderly parents (or other relatives) you may find they are increasingly reliant on you for help and support. It may be up to you to arrange care for them and/or set up power of attorney so you can manage their affairs if this becomes necessary. They may also need help with estate planning (see above). An IFA can assist with all these things as well.

Getting a Free Financial Check-Up

Independent financial advisers do of course charge for their services. They are by definition unaffiliated and do not receive commission, so any recommendations they make are based solely on their client’s best interests. As I have said before on PAS, I certainly don’t begrudge paying my own financial adviser, Mike, as he has undoubtedly saved (and made) me a lot more money than he has cost me over the years.

Nonetheless, most IFAs will be happy to see you for an initial financial healthcheck free of charge. This can focus on a particular area of concern, so you could request an investments review, a pension review or a mortgage review. Alternatively, if you’re not sure which aspect of your finances needs more attention – or indeed whether you need advice at all – you could simply request a broad financial healthcheck.

Here’s what. Adrian Kidd, a financial planner at Radcliffe & Newlands, says about his approach on the Unbiased website:

‘I’d generally offer one or possibly two free consultations, taking about an hour, and these can be as specific or as broad as required. When someone books a financial healthcheck with me, I ask them to bring along all their documents relating to their finances – savings, investments, mortgages, loans, insurance, pensions, the works – so I can build up a complete picture of their affairs. I then go through these in more detail after the consultation, and follow up with an email that gives a summary of their overall financial situation.’

In these free check-ups: advisers won’t generally talk to you about products at all. The process of choosing the right products comes later, after the adviser has built up an understanding of you as a person and your financial planning needs. Only then will they recommend products, if asked to do so.

If you follow my link to the Unbiased website, you can complete a short, step-by-step questionnaire designed to identify the best type of financial adviser for your needs. You will then be shown a selection of suitable advisers in your area with contact information. They will be happy to answer any queries you may have and arrange an initial meeting without obligation.

As ever, if you have any comments or questions about this post, please do leave them below.

Disclosure: This is a sponsored post on behalf of Unbiased.co.uk. If you click through my link and end up becoming a client of a financial adviser listed on the Unbiased site, I may receive a commission for introducing you. This will not affect the service you receive or any fees you are charged if you decide to proceed further.

This is a fully updated version of a post originally published in 2020.

If you enjoyed this post, please link to it on your own blog or social media:

Today I’m reviewing a new book called Extreme Frugality by my blogging colleague Jane Berry, also known as Shoestring Jane.

Jane runs a popular blog called Shoestring Cottage which follows her journey towards making a creative, happy and sustainable life on much less. She also runs a YouTube channel as Shoestring Jane, where she shares her thrifty life and money-saving ideas. And she is also a writer for the estimable Mouthy Money site, to which I am a regular contributor myself.

Extreme Frugality is divided into 13 main chapters, as follows:

Chapter 1: Frugal Foundations

Chapter 2: Stuff, Stuff and More Stuff

Chapter 3: Cooking and Eating Like Grandma

Chapter 4: Granny’s advice – ‘Make do & Mend’ and ‘Waste Not, Want Not’

Chapter 5: Buying Second-Hand and Getting Everything for Less

Chapter 6: Slashing Your Monthly Bills

Chapter 7: Making a Frugal Home

Chapter 8: The Frugal Cleaner

Chapter 9: The Frugal Garden

Chapter 10: Frugal Fashion: Dress for Less

Chapter 11: Frugal Fun and Travel

Chapter 12: A Frugal Christmas

Chapter 13: Health and Well-being on a Budget

There is also a section of references and resources at the end.

As you may gather, Extreme Frugality aims to show you how to develop thrifty habits (as our grandparents had to). The author says the purpose of doing this is to cushion you against hard times, be creative with what you have, buy just what you need, and eliminate waste from your home.

As a one-time professional writer and editor myself, I was impressed by the high standard to which Extreme Frugality has been produced. The style is clear and accessible, and the content neatly set out without any unnecessary typographical or design gimmicks.

Obviously in the current cost-of-living crisis we are all having to tighten our belts, so the advice in the book is very apposite at present. There are also plenty of suggestions for preventing waste, so the book should appeal to anyone concerned with their environmental impact as well.

It’s hard to pick out highlights as every chapter is packed with valuable tips and advice, but I especially enjoyed Chapter 6, which takes you through a wide range of methods for slashing monthly bills, including energy, water, Council Tax, broadband and so on. The advice in this chapter alone could easily save you thousands of pounds a year. But all the chapters contain useful advice, ideas and information. Even as a money blogger myself, I don’t mind admitting I learned a lot from it.

In summary, Extreme Frugality is a great guide for anyone looking to save money and reduce waste in these challenging times. It would also make an excellent gift for a friend or family member. I am happy to give it my highest recommendation.

As always, if you have any comments or questions about this post, please do leave them below.

Disclosure: I was sent a free copy of Extreme Frugality (in PDF form) to review. Please be aware also that this post (and others on PAS) includes affiliate links. If you click through one of these and make a purchase or perform some other defined action, I may receive a commission for introducing you. This will not affect in any way the price you pay or the product or service you receive.

If you enjoyed this post, please link to it on your own blog or social media:

Today I’m looking at Cardeo, a new, free credit card management app. It is designed to help save you money on your credit cards.

How Does Cardeo Work?

Cardeo brings together data from all your credit cards into a single app using open banking.

It then gives you insights into your borrowing and spending. Their payment plan works out how long it will take to pay off your cards. You can set a repayment target, decide how to get there, and repay all your cards through a single monthly payment (you can also use it with just a single credit card). Reminders make sure that you never miss a repayment.

You can change the payment plan as much as you like: edit the date, target or the monthly amount, make extra one-off payments, and pause/restart the plan as it suits you.

Cardeo works with most (though not yet all) UK credit cards. You can view the entire list here. All the most popular credit card providers appear to be covered, including Barclays, HSBC, Santander, MBNA, Virgin Money, and so on.

How Can Cardeo Save You Money?

First and foremost, payment reminders from Cardeo help you pay your cards on time each month. That way you avoid extra interest and late payment fees from your card provider. If – like me – you are prone to forget these payments on occasion, this is a valuable money-saving feature in its own right.

The Cardeo payment plan offers a choice of repayment strategies, including the so-called avalanche method. This repays the highest interest rate cards first (after minimum payments are covered). By this means you will minimise interest charges and pay off your cards in the shortest possible time.

Cardeo gives you insights into your credit card usage, helping you make smarter decisions about your spending and saving. Finally, Cardeo also offer deals from other parties which are designed to save you money.

How Does Cardeo Make Money?

As already mentioned, the Cardeo app is free to download and to use, with no in-app purchases or charges.

Cardeo say they make a small amount of money from deal providers each time a customer takes up a deal from the Cardeo app (e.g. a low-interest loan).

My Experience

I found downloading and installing the Cardeo app straightforward – I got mine from Google Play as I have an Android phone.

When you first open the app you have to put in certain details, including your full name and address, phone number (for log-in purposes), and so on. You may also be required to enter an email invitation code. All this took me maybe five minutes at most. I then saw the screen below…

After that, I clicked on ‘Add a Card’ and selected the name of my credit card provider, MBNA. I then had to follow a link to their website and log in with my usual online security credentials to authorize open banking.

Frustratingly, this took me a few attempts. MBNA required me to answer an automated call from them and enter a four-digit code on the telephone keypad to complete the process. Initially it told me I had got the code wrong, despite the fact that I had copied it from the MBNA site. I persevered, however, and eventually the card was linked to my Cardeo account 🙂

As a side note, I am probably not the ideal candidate for Cardeo, as these days I only have one credit card and use it just once or twice a year. The rest of the time, I use my bank debit card instead. I am in the fortunate position of having enough income/savings that I don’t need to borrow on my credit card. On the odd occasion I do use it, it is typically for larger purchases to take advantage of the extra legal protections you get with credit card purchases over £100.

Nevertheless, I am happy to confirm that everything in the Cardeo set-up process went smoothly for me, with the sole exception of the hiccup regarding authorizing open banking with MBNA. The latter wasn’t Cardeo’s fault, and has in fact happened to me before with MBNA. Hopefully you will be luckier!

My Thoughts

If you’re a regular credit card user, and especially if you pay interest on an outstanding balance (or balances), in my view Cardeo offers a great way to minimize the charges you pay and help reduce your debts as quickly as possible.

As I have noted before on Pounds and Sense, credit card borrowing can be very expensive, especially over a long period. So if you are in debt on your cards, it is important to take all possible steps to pay this off as quickly as possible, and Cardeo will certainly help you with this. It can also help build your credit score by ensuring you don’t miss any payments.

A further benefit is that Cardeo will save you administrative time and hassle. You simply make one monthly payment and this is automatically allocated by the app across all your credit cards.

I know some people are uneasy about open banking, and if this is a major concern then Cardeo may not be for you. Open banking is, however, now a well-established option allowing consumers to gain an overview of their financial products. If you’re trying to get (and keep) your finances under better control, this can only be beneficial. Cardeo require your permission to use open banking and you can remove this at any time. Your data is encrypted and your login details are kept hidden. You can read more about the security and privacy protections here if you wish.

As always if you have any comments or questions about this post, or Cardeo more generally, please do leave them below.

Disclosure: This post includes affiliate links. If you click through and download the Cardeo app or perform some other qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive in any way.

If you enjoyed this post, please link to it on your own blog or social media:

Amazon Prime Day is over now and the next big shopping event is Black Friday, which this year takes place on Friday 22nd November. But in this time of rising inflation, is it sensible to wait until then for any big-ticket items you need?

My colleagues at Offeroftheday have been crunching the numbers, and their figures indicate that in these inflationary times, waiting for Black Friday might not be the smartest thing to do.

How Are Prices Changing?

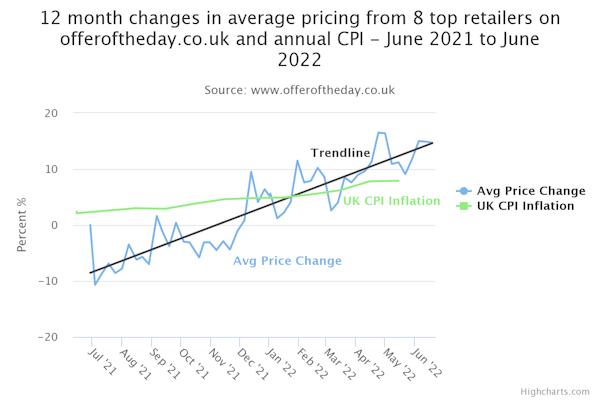

Figure 1 (below) shows how prices from eight popular retailers on the Offeroftheday website, including clothing, home & garden and electronic retailers, have changed over the last 12 months. It reveals that during this time average prices rose by over 15%. As the chart shows, this is a significantly higher rate than the UK’s CPI inflation rate.

While the chart does show a dip in prices around the Black Friday period in late November 2021, the data suggests that when prices are rising rapidly (as now) it may still be better to buy as early as possible rather than wait months for possible Black Friday discounts.

Why Are Prices Rising So Fast?

There are various reasons for the rapid rise this year in consumer prices. One is the record increase in energy bills. This has had a knock-on effect on retailers, who are now paying substantially higher running costs for their shops and factories.

A further factor is the big increase in fuel prices, adding to distribution costs. Inevitably, some of these increased costs get passed on to the consumer. The average pump price in June 2021 was 130.73p. Compare this to June 2022 where the average price was 190.93p, a jump of 46% in just twelve months.

Other factors causing prices to rise include logistical issues (e.g. HGV driver shortages), wage rises, shortages of goods and raw materials caused by trade barriers and the war in Ukraine, the effects of extreme weather (possibly caused by climate change), the ending of support schemes for businesses introduced during the pandemic, and so on.

So Is Black Friday Worth Waiting For?

In November 2021, Offeroftheday found the mean average discount of all products on the website was 5.6% compared with the previous month. Given the current trend in pricing shown in Figure 1, by Black Friday November 2022 this discount would need to be significantly higher than that to offset the new base prices.

So does this mean you should do your shopping now? Well, yes and no. Black Friday has a focus on high-ticket items. It is one of the few days when the Apple Store has discounts, and many retailers cut their prices by 50% and more on some electronics and white goods. Even allowing for rising inflation over the next few months, those are significant savings.

While in previous years prices on Black Friday fell far below any other time of the year, Figure 1 shows that Black Friday 2021 only briefly managed to offset price rises, effectively turning the clock back a few months at best. Not surprisingly, many sources reported a decrease in total spend on Black Friday 2021 compared to the previous two years. While some of this can be attributed to lockdown measures and furlough, the data shows that Black Friday discounts simply were not as impressive compared to previous years, especially compared to the prices being charged just a few months earlier.

Black Friday 2022 and Beyond

As mentioned above, Black Friday 2022 falls on Friday 25th November. However, If cost increases continue on their current trajectory, prices could rise as much as 7% between now and November. This means that a product averaging £500 today could cost upwards of £535 in five months time.

Some products will undoubtedly see big discounts on Black Friday 2022. But with inflation currently approaching 10%, we can expect average prices from retailers to continue rising overall. If you’re on the fence about a big purchase, it may therefore be worth buying now rather than hoping for big discounts later in the year. Once we pass August/September, it might be worth holding out for a month or two to reap the benefits of Black Friday discounts. But there is, of course, no guarantee that the particular product you want will be discounted for Black Friday, or whether any discount will be enough to offset price rises caused by inflation.

Black Friday is still the largest shopping day of the year for retailers, so expect to see some big discounts and eye-catching offers. But if it is anything like last year, average discounts may not be as impressive as in years gone by, and for many items you may actually get better prices if you buy now.

Although in this post I have focused on big ticket items, it should be said that Black Friday can also be good for buying cheaper items at a discount. I am thinking here of consumables such as ink cartridges, stationery, clothing, cosmetics, food and drink, and so on. Black Friday can present opportunities for stocking up on such items at bargain prices.

Thank you to my friends at Offeroftheday for sharing their data with me. Please do check out their website for great offers from a wide range of leading online retailers.

As always, if you have any comments or questions about this post, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

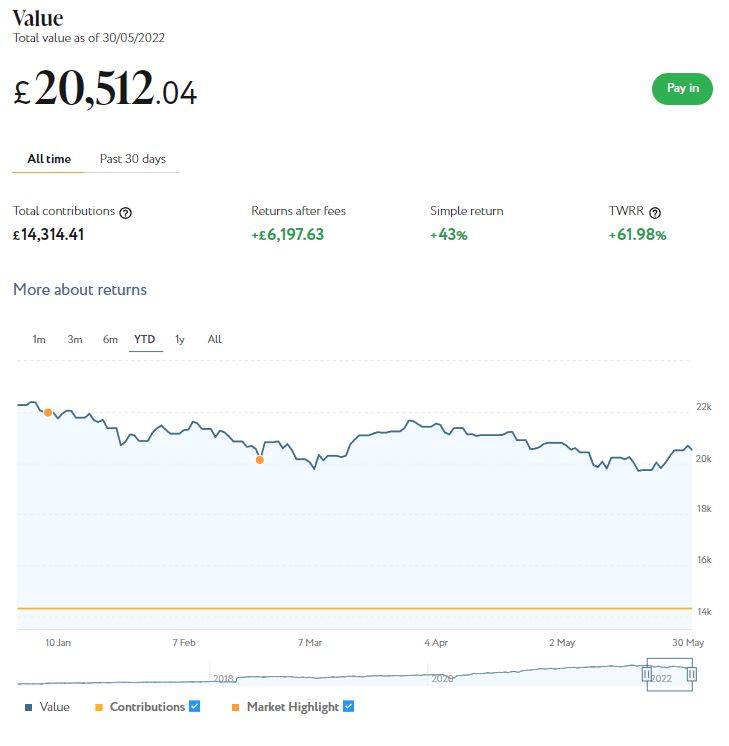

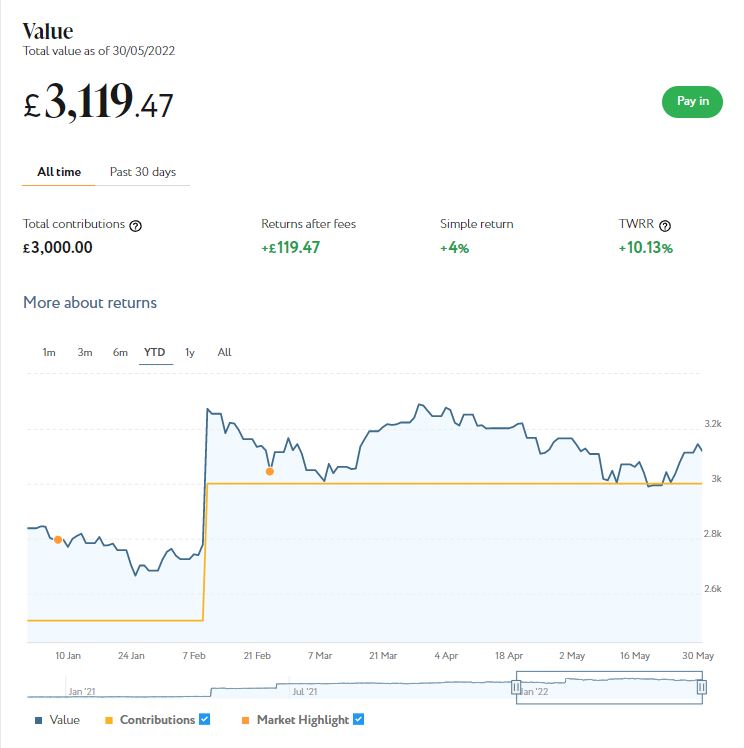

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

As the screenshot below of performance in the year to date shows, my main portfolio is currently valued at £20,512. Last month it stood at £20,799 so, after a roller-coaster month, that is a fall of £287.

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £3,119 compared with £3,166 last month, a fall of £47

Here is a screen capture showing performance this year.

Obviously the continuing falls are disappointing (though much smaller than last month). As I’ve noted previously on PAS, you do have to expect ups and downs with equity-based investments, and certainly over the last few months there has been no shortage of volatility in world markets. And it’s also worth noting that since I started investing with Nutmeg in 2016 I have still enjoyed a total return of 36.48% (or 62.07% time-weighted).

I should also mention that I selected quite a high risk level for both my Nutmeg accounts (9/10 for the main one and 5/5 for Smart Alpha). This has served me well generally, but I’m sure investors who selected lower risk levels will have seen smaller falls over the last two months.

If you also have a Nutmeg portfolio and plan to withdraw from it in the next few months, there is certainly a case for switching to a lower risk level right now.

You can read my full Nutmeg review here (including a special offer at the end for PAS readers). If you are looking for a home for your annual ISA allowance, based on my experience over the last six years, they are certainly worth considering.

Moving on, my Assetz Exchange investments continue to perform well. Regular readers will know that this is a P2P property investment platform focusing on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my AE portfolio has generated £57.24 in revenue from rental and £92.28 in capital growth, a total of £149.52. That’s a decent rate of return on my £1,000 investment and does illustrate the value of P2P property investment for diversifying your portfolio when equity markets are volatile (as at the moment).

I now have investments in 22 different projects and all are performing as expected, generating rental income and – in every case but one – showing a profit on capital. So I am very happy with how this investment has been doing. And it doesn’t hurt that most projects are socially beneficial as well.

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of AE as far as i am concerned. You can actually invest from as little as 80p per property if you really want to proceed cautiously.

Another property platform I have investments with is Kuflink. They have been doing well recently, with new projects launching almost every day. I currently have over £2,150 invested with them, quite a large proportion of which comes from reinvested profits. To date I have never lost any money with Kuflink, though some loan terms have been extended once or twice. On the plus side, when this happens additional interest is paid for the period in question. At present all my Kuflink loans are performing to schedule, though one is showing as ‘pending a status update’. I suspect this may translate to a delay in repayment. We shall see.

My loans with Kuflink pay annual interest rates of 6 to 7.5 percent. These days I invest no more than around £150 per loan (and often less). That is not because of any issues with Kuflink but more to do with losses of larger amounts on other P2P property platforms in the past. My days of putting four-figure sums into any single property investment are behind me now!

Nowadays I mainly opt to reinvest the monthly repayments I receive from Kuflink, which has the effect of boosting the percentage rate of return on the projects in question

Obviously a possible drawback with Kuflink and similar platforms is that your money is tied up in bricks and mortar, so not as easily accessible as cash savings or even (to some extent) shares. They do, however, have a secondary market on which you can offer any loan part for sale (as long as the loan in question is performing and not in arrears). Clearly that does depend on someone else wanting to buy it, but my experience has been that any loan parts offered are typically snapped up very quickly. So if an urgent need arises, withdrawing your money (or part of it) is unlikely to be an issue.

You can read my full Kuflink review here. They offer a variety of investment options, including a tax-free IFISA paying up to 7% interest per year with built-in automatic diversification. Alternatively you can now build your own IFISA, with most loans on the platform (including the one shown above) being IFISA-eligible.

I also recently published a blog post about another P2P property investment platform called BLEND. Like Kuflink, they offer the opportunity to invest in secured loans to experienced property developers. They offer (on average) somewhat higher rates of return than Kuflink, though arguably with a little more risk. As well as my blog post about BLEND, you can also check out what they have to offer on their website [affiliate link].

As mentioned last time, I invested some more money in European crowdlending platform Nibble last month. On this occasion I invested in their Legal Strategy. The loans in question are in default and facing legal action. Nibble buy these loans at a heavily discounted rate and then seek to recover as much as possible of the money owed. The minimum investment is 10 euro and the minimum period is six months.

The Legal Strategy comes with a deposit-back guarantee. This is a guarantee to return the full investment amount at the end of the investment period and a minimum yield of 9% per annum. The actual yield will depend on how successful recovery efforts prove, so in practice you may end up with a return of anywhere between 9% and 14.5%. All is going well so far, but I will obviously continue to report on this in the months ahead.

One other thing I wanted to mention is that I have just opened an account with online share trading/investment platform eToro. I’ve been planning to do this for a while, with a view to reviewing it on PAS. I’m finding it quite different from other online investment platforms I have used such as Bestinvest.

As well as commission-free share trading, eToro offer a popular copy-trading feature, where you can copy the trades of other successful investors automatically. You can also practise with a virtual portfolio of $100,000. I put some of this into Platinum on the eToro commodities market and initially its value soared. But then it went right down again. So I am not the investment genius I thought I was at first 😀 It’s all very interesting, though. If you’d like to check out eToro for yourself, here’s an invitation link [affiliate]. And keep an eye open for my full review in due course.

Incidentally, Mouthy Money currently have a vacancy for a graduate-level personal finance reporter. This is a one-year paid internship working partly from home and partly from MM’s London office. If you know anyone who might be interested in this opportunity, please do draw it to their attention.

Finally, there has been a lot of talk about the cost of living crisis this month. As you may know, Chancellor Rishi Sunak announced a raft of measures to try to mitigate the worst effects of this.

Whatever your political or economic views, I do think he has been quite generous to older people in particular. Not only will those of us receiving the state pension get £400 off our household energy bills, we will also receive an extra £300 on top of our usual Winter Fuel Allowance (that means I’ll get £500 this year).

Many pensioners will also qualify for the £150 bonus for those on non-means-tested disability benefits such as Attendance Allowance. And they may also get the £650 cost of living payment going to anyone receiving various means-tested benefits (everyone getting pension credit will qualify for this, for example). Some households will receive a total of £1,500 in additional benefits through these measures, which should certainly help in these challenging times. .

That’s enough for today, so I’ll close by wishing you a very happy Jubilee Holiday. Whatever you are doing in the next few days – going away or staying home with family and friends – I do hope you have a relaxing and enjoyable time. As ever, if you have any comments or queries, please feel free to leave them below. I always love hearing from my readers 🙂

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media:

Today I have a guest post for you from my colleague Richard Winstone (not pictured above). Richard has just launched a new, diary-style blog called Financially Fat about his quest to achieve ‘financial fitness’.

I thought Financially Fat could be of interest to many Pounds and Sense readers, so I invited Richard to create a guest post about it. He was happy to oblige, so here is his article.

Hi everyone. I’m Richard Winstone and I write a blog called Financially Fat.

I want to start this post by thanking Nick for allowing me to guest blog on Pounds and Sense. I appreciate the feedback he has given on my blog and am really proud to have this opportunity to showcase Financially Fat to the Pounds and Sense community.

What is Financially Fat?

“If financial fitness is the aim, then I am Financially Fat.” This is the tag-line of the Financially Fat blog.

Being financially fat isn’t supposed to paint the image of a fat, wealthy man. It’s meant to imply that my finances are out of shape, which they are.

I’ve decided to take a no-holds-barred approach to financial honesty in my blog: the good, the bad and the ugly. So, in the second post I wrote down my complete financial position. I left nothing to the imagination and fully revealed my “financial nakedness”. I did this because I wanted my readers to know that I’m not another rich guy giving quick tips to save a few quid (not that there’s anything wrong with that), but that I’m actually financially struggling and that I’m taking action to improve my financial fitness.

Financially Fit is written as a diary, in which every Friday I comment on how I did with the previous week’s targets and set new targets for the following week. There are also a couple of sections of me rambling about my thoughts from the previous week, which I hope are insightful but may just be the ramblings of a mad man 😉

The purpose of the blog is two-fold. First, I want to chronicle my journey from being financially fat to being financially fit. I think this is easier to do weekly while I’m on the journey rather than try to remember what I did after (I hope) I’ve become financially fit. And second, I’m hoping to provide a step-by-step guide for others to follow to help improve their financial fitness. I write and post my blog to the over50smoney.com website and email it out to our over50smoney community each week.

So, below is a quick summary of how my blogging journey has gone so far, now that I’m five weeks in…

This is another introductory post, but it goes into much more detail. I start by detailing what I hope to gain from Financially Fat and then move on to set out my starting financial position, including my salary, savings, debts, shares, assets and anything else I could think of. It’s a complete works of my financial position, which I’ve committed to reviewing monthly in a similar format so I can see how my financial position improves month-to-month (the next review is this Friday and I’m nervous!).

Right, Week 2 is when it starts getting more interesting and where the format of the blog really starts to become clear. I started this post by highlighting three things I did that were bad for my finances over the previous week, which were:

Moving home (kind of unavoidable)

Working from Costa far too often

Dining out

I then came up with the idea of setting targets for the following week to address things that I’ve done wrong in the previous week, with the hope that I’ll eventually move away from bad habits that cost me way too much money. This seems to be working to be honest, at the moment I’m down to working from Costa only once or twice a week and usually only for a couple of hours each time rather than full days.

Continuing the development of the blog format, Week 3 is where I started titling the blog posts a little more nicely, and where I started summing up my financial savings from following the targets on my previous week.

In this post, I point out how working from Costa only once a week instead of five times a week can save me around £50 per week, over £200 per month! I also discuss setting yourself targets as you follow the blog. Reading it is (I hope) interesting, but for the blog to be useful you need to follow the thought processes I go through and make sure you’re applying them to your own life. So, if you have a small, seemingly inexpensive habit that you do frequently, then I recommend reviewing how much that habit has actually cost you over a month and see how much you could save by cutting down.

In Week 4 I discussed the target of reviewing my standing orders and direct debits. After just one review, which took about 45 minutes, I was able to save just under £600 per year! Which is insane. I continued to review into the following week but was only able to save an additional £1 per month by changing my gym membership.

This is also the week I formalised my “Ramblings” as an introduction to the blog, I hope you enjoy reading them and please feel free to email me any time to comment, ask questions or provide suggestions (I’ve been getting some great tips from readers!).

By this point, I’ve started getting really into the money-saving game. I’m also discussing things like increasing income to ensure I’m not reliant only on my salary.

But, as the title indicates, I talk about tackling my biggest challenge yet, which is currently destroying my finances – smoking! I know, it’s a horrible habit and I’m obviously very aware of the negative health affects as well as the impact it’s having on my bank balance. So, I’ve set out a five-week plan to quit (which I can say I’m currently doing okay on, but it has only been four days).

Cutting out smoking could save me around £2,400 per year, which means from the Financially Fat blog I would have saved around £3,200 a year in disposable income just in the first five weeks, and there’s still so much more work to do!

Follow the Financially Fat Blog

That’s it for the summary of my first six blog posts. I hope you will click through and give them a read as there’s a lot more information in there and some interesting views, I like to think.

If you’re interested in following my blog, please head over to over50smoney.com and sign-up for our newsletters. Or, if you’d rather not receive emails, you could just follow us on Facebook. I write and post every Friday and put links on our Facebook page, so please consider liking and following this. Thank you 🙂

I want to thank Nick again for letting me write this short summary of Financially Fat. I really hope you find it as useful as I am. If you have any questions or comments, or just fancy a chat about finances, please feel free to reach out to me directly at richard@over50smoney.com. I sometimes take a few days to reply, but I promise I get back to every email I receive.

I’m Richard Winstone and I am Financially Fat.

Many thanks to Richard Winstone (pictured, right) for this article. I hope you will take a moment to check out Financially Fat.

I particularly admire the honesty with which Richard sets out his financial position. I try to be honest about my finances on PAS as well, but not in nearly as systematic a way as he is doing!

If you are also ‘financially fat’ (as Richard defines it) I hope you may find the info and advice on the new blog inspires you in your own quest to achieve financial fitness.

As always, if you have any comments or questions about this post (for me or for Richard), please do share them below.

If you enjoyed this post, please link to it on your own blog or social media:

tic a way as he is doing!

tic a way as he is doing!